UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________

Form 6-K

______________

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

June 28, 2022

Commission File Number 001-15244

CREDIT SUISSE GROUP AG

(Translation of registrant’s name into English)

Paradeplatz 8, 8001 Zurich, Switzerland

(Address of principal executive office)

______________

Commission File Number 001-33434

CREDIT SUISSE AG

(Translation of registrant’s name into English)

Paradeplatz 8, 8001 Zurich, Switzerland

(Address of principal executive office)

______________

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

| Form 20-F ☒ | Form 40-F ☐ |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

This report includes the media release and the slides for the presentation to investors in connection with the Investor Deep Dive 2022 held on June 28, 2022.

Media release |

Credit Suisse holds Investor Deep Dive sessions on Risk Management, Compliance and Technology & Operations as well as on Wealth Management

Zurich, June 28, 2022 – Credit Suisse Group AG (Credit Suisse) is today holding an Investor Deep Dive to inform investors about its key priorities and achievements across the Risk, Compliance and Technology & Operations functions as well as in the Wealth Management business.

Today’s event will be hosted by Credit Suisse Group CEO Thomas Gottstein. After his introduction, the following Credit Suisse executives will provide a detailed insight into the four core themes of the Investor Deep Dive:

▪ David Wildermuth, Chief Risk Officer, will set out the actions that Credit Suisse is taking to elevate its risk culture and capabilities and explain the advances made in strengthening its risk management framework.

▪ Rafael Lopez Lorenzo, Chief Compliance Officer, will highlight the initiatives being taken to strengthen the bank through effective and efficient compliance risk management.

▪ Joanne Hannaford, Chief Technology & Operations Officer, will give an insight into how Credit Suisse is simplifying and strengthening its Technology & Operations platforms and engineering its digital future.

▪ Francesco De Ferrari, CEO Wealth Management, will provide an update on the execution of the strategic priorities to drive sustainable growth and deliver value for clients.

Thomas Gottstein, Chief Executive Officer of Credit Suisse Group AG, commented: “At today’s Investor Deep Dive, we are providing an in-depth view on the delivery of our strategy in four key areas of the bank, namely in Risk Management, Compliance, Technology & Operations and in Wealth Management. Despite the challenging market environment, we remain firmly focused on the execution of our strategic plan during the transition year 2022 and on reinforcing our risk culture – crucially, while staying close to our clients. At the same time, we are continuing to drive the bank’s digital transformation, which is key to building a robust, scalable and agile organization that is fit for the future.”

Investor Deep Dive webcast and documents

The event will be broadcast via webcast beginning at 09:00 CEST / 08.00 BST / 03.00 EST and can be accessed at: 2022 Investor Deep Dive – Credit Suisse (credit-suisse.com)

The Investor Deep Dive presentations will be available to download from 07.00 CEST / 06.00 BST / 01.00 EST today at: 2022 Investor Deep Dive – Credit Suisse (credit-suisse.com)

Page 1 | June 28, 2022 |

Media release |

Contact details Kinner Lakhani, Investor Relations, Credit Suisse Tel: +41 44 333 71 49 Email: investor.relations@credit-suisse.com Dominik von Arx, Corporate Communications, Credit Suisse Tel: +41 844 33 88 44 Email: media.relations@credit-suisse.com |

Credit Suisse

Credit Suisse is one of the world's leading financial services providers. Our strategy builds on Credit Suisse's core strengths: its position as a leading wealth manager, its specialist investment banking capabilities and its strong presence in our home market of Switzerland. We seek to follow a balanced approach to wealth management, aiming to capitalize on both the large pool of wealth within mature markets as well as the significant growth in wealth in Asia Pacific and other emerging markets, while also serving key developed markets with an emphasis on Switzerland. Credit Suisse employs approximately 51,030 people. The registered shares (CSGN) of Credit Suisse Group AG, are listed in Switzerland and, in the form of American Depositary Shares (CS), in New York. Further information about Credit Suisse can be found at www.credit-suisse.com.

Cautionary statement regarding forward-looking information

This document contains statements that constitute forward-looking statements. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to the following:

▪ our plans,

▪ targets or goals;

▪ our future economic performance or prospects;

▪ the potential effect on our future performance of certain contingencies;and

▪ assumptions underlying any such statements.

Words such as “believes,” “anticipates,” “expects,” “intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, targets, goals, expectations, estimates and intentions expressed in such forward-looking statements and that the ongoing COVID-19 pandemic creates significantly greater uncertainty about forward-looking statements in addition to the factors that generally affect our business. These factors include:

▪ the ability to maintain sufficient liquidity and access capital markets;

▪ market volatility, increases in inflation and interest rate fluctuations or developments affecting interest rate levels;

▪ the ongoing significant negative consequences of the Archegos and supply chain finance funds matters and our ability to successfully resolve these matters;

▪ our ability to improve our risk management procedures and policies and hedging strategies;

▪ the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations, in particular the risk of negative impacts of COVID-19 on the global economy and financial markets and the risk of continued slow economic recovery or downturn in the EU, the US or other developed countries or in emerging markets in 2022 and beyond;

▪ the emergence of widespread health emergencies, infectious diseases or pandemics, such as COVID-19, and the actions that may be taken by governmental authorities to contain the outbreak or to counter its impact;

▪ potential risks and uncertainties relating to the severity of impacts from COVID-19 and the duration of the pandemic, including potential material adverse effects on our business, financial condition and results of operations;

▪ the direct and indirect impacts of deterioration or slow recovery in residential and commercial real estate markets;

▪ adverse rating actions by credit rating agencies in respect of us, sovereign issuers, structured credit products or other credit-related exposures;

▪ the ability to achieve our strategic goals, including those related to our targets, ambitions and financial goals;

▪ the ability of counterparties to meet their obligations to us and the adequacy of our allowance for credit losses;

▪ the effects of, and changes in, fiscal, monetary, exchange rate, trade and tax policies;

▪ the effects of currency fluctuations, including the related impact on our business, financial condition and results of operations due to moves in foreign exchange rates;

▪ geopolitical and diplomatic tensions, instabilities and conflicts, including war, civil unrest, terrorist activity, sanctions or other geopolitical events or escalations of hostilities;

Page 2 | June 28, 2022 |

Media release |

▪ political, social and environmental developments, including climate change;

▪ the ability to appropriately address social, environmental and sustainability concerns that may arise from our business activities;

▪ the effects of, and the uncertainty arising from, the UK’s withdrawal from the EU;

▪ the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations;

▪ operational factors such as systems failure, human error, or the failure to implement procedures properly;

▪ the risk of cyber attacks, information or security breaches or technology failures on our reputation, business or operations, the risk of which is increased while large portions of our employees work remotely;

▪ the adverse resolution of litigation, regulatory proceedings and other contingencies;

▪ actions taken by regulators with respect to our business and practices and possible resulting changes to our business organization, practices and policies in countries in which we conduct our operations;

▪ the effects of changes in laws, regulations or accounting or tax standards, policies or practices in countries in which we conduct our operations;

▪ the discontinuation of LIBOR and other interbank offered rates and the transition to alternative reference rates;

▪ the potential effects of changes in our legal entity structure;

▪ competition or changes in our competitive position in geographic and business areas in which we conduct our operations;

▪ the ability to retain and recruit qualified personnel;

▪ the ability to protect our reputation and promote our brand;

▪ the ability to increase market share and control expenses;

▪ technological changes instituted by us, our counterparties or competitors;

▪ the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users;

▪ acquisitions, including the ability to integrate acquired businesses successfully, and divestitures, including the ability to sell non-core assets; and

▪ other unforeseen or unexpected events and our success at managing these and the risks involved in the foregoing.

We caution you that the foregoing list of important factors is not exclusive. When evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, including the information set forth in “Risk factors” in I – Information on the company in our Annual Report 2021.

Disclaimer

This document was produced by and the opinions expressed are those of Credit Suisse as of the date of writing and are subject to change. It has been prepared solely for information purposes and for the use of the recipient. It does not constitute an offer or an invitation by or on behalf of Credit Suisse to any person to buy or sell any security. Any reference to past performance is not necessarily a guide to the future. The information and analysis contained in this publication have been compiled or arrived at from sources believed to be reliable but Credit Suisse does not make any representation as to their accuracy or completeness and does not accept liability for any loss arising from the use hereof.

The English language version of this document is the controlling version.

Copyright © 2022 Credit Suisse Group AG and/or its affiliates. All rights reserved.

Page 3 | June 28, 2022 |

Investor Deep Dive 2022 June 28, 2022

Disclaimer (1/2) 2 This material does not purport to contain all of the information that you may wish to consider. This material is not to be relied upon as such or used in substitution for the exercise of independent judgment.Cautionary statement regarding forward-looking statements This document contains forward-looking statements that involve inherent risks and uncertainties, and we might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements. A number of important factors could cause results to differ materially from the plans, targets, goals, expectations, estimates and intentions we express in these forward-looking statements, including those we identify in “Risk factors” in our Annual Report on Form 20-F for the fiscal year ended December 31, 2021 and in the “Cautionary statement regarding forward-looking information” in our media release relating to the 2022 Investor Deep Dive published on June 28, 2022 and submitted to the US Securities and Exchange Commission, and in other public filings and press releases. We do not intend to update these forward-looking statements.In particular, the terms “Estimate”, “Illustrative”, “Ambition”, “Objective”, “Outlook”, “Goal”, “Commitment” and “Aspiration” are not intended to be viewed as targets or projections, nor are they considered to be Key Performance Indicators. All such estimates, illustrations, ambitions, objectives, outlooks, goals, commitments and aspirations are subject to a large number of inherent risks, assumptions and uncertainties, many of which are completely outside of our control. These risks, assumptions and uncertainties include, but are not limited to, general market conditions, market volatility, increased inflation, interest rate volatility and levels, global and regional economic conditions, challenges and uncertainties resulting from Russia’s invasion of Ukraine, political uncertainty, changes in tax policies, scientific or technological developments, evolving sustainability strategies, changes in the nature or scope of our operations, changes in carbon markets, regulatory changes, changes in levels of client activity as a result of any of the foregoing and other factors. Accordingly, these statements, which speak only as of the date made, are not guarantees of future performance and should not be relied on for any purpose. We do not intend to update these estimates, illustrations, ambitions, objectives, outlooks, goals, commitments, aspirations or any other forward-looking statements. For these reasons, we caution you not to place undue reliance upon any forward-looking statements. We may not achieve the benefits of our strategic initiativesWe may not achieve all of the expected benefits of our strategic initiatives. Factors beyond our control, including but not limited to the market and economic conditions including macroeconomic and other challenges and uncertainties, for example, resulting from Russia’s invasion of Ukraine, changes in laws, rules or regulations and other challenges discussed in our public filings, could limit our ability to achieve some or all of the expected benefits of these initiatives.Estimates and assumptionsIn preparing this document, management has made estimates and assumptions that affect the numbers presented. Actual results may differ. Annualized numbers do not take into account variations in operating results, seasonality and other factors and may not be indicative of actual, full-year results. Figures throughout this document may also be subject to rounding adjustments. All opinions and views constitute good faith judgments as of the date of writing without regard to the date on which the reader may receive or access the information. This information is subject to change at any time without notice and we do not intend to update this information.

Disclaimer (2/2) 3 Statement regarding non-GAAP financial measuresThis document contains non-GAAP financial measures, including results excluding certain items included in our reported results as well as return on regulatory capital. Further details and information needed to reconcile such non-GAAP financial measures to the most directly comparable measures under US GAAP can be found in the Appendix, which is available on our website at www.credit-suisse.com.Our estimates, ambitions, objectives, aspirations and targets often include metrics that are non-GAAP financial measures and are unaudited. A reconciliation of the estimates, ambitions, objectives, aspirations and targets to the nearest GAAP measures is unavailable without unreasonable efforts. Results excluding certain items included in our reported results do not include items such as goodwill impairment, major litigation provisions, real estate gains, impacts from foreign exchange and other revenue and expense items included in our reported results, all of which are unavailable on a prospective basis. Return on tangible equity is based on tangible shareholders’ equity, a non-GAAP financial measure also known as tangible book value, which is calculated by deducting goodwill and other intangible assets from total shareholders' equity as presented in our balance sheet, both of which are unavailable on a prospective basis. Return on regulatory capital (a non-GAAP financial measure) is calculated using income/(loss) after tax and assumes a tax rate of 25% and capital allocated based on the average of 13.5% of risk-weighted assets and 4.25% of leverage exposure; the essential components of this calculation are unavailable on a prospective basis. Such estimates, ambitions, objectives and targets are calculated in a manner that is consistent with the accounting policies applied by us in preparing our financial statements.Statement regarding capital, liquidity and leverageCredit Suisse is subject to the Basel framework, as implemented in Switzerland, as well as Swiss legislation and regulations for systemically important banks, which include capital, liquidity, leverage and large exposure requirements and rules for emergency plans designed to maintain systemically relevant functions in the event of threatened insolvency. Credit Suisse has adopted the Bank for International Settlements (BIS) leverage ratio framework, as issued by the Basel Committee on Banking Supervision (BCBS) and implemented in Switzerland by the Swiss Financial Market Supervisory Authority FINMA.Unless otherwise noted, leverage exposure is based on the BIS leverage ratio framework and consists of period-end balance sheet assets and prescribed regulatory adjustments. The tier 1 leverage ratio and CET1 leverage ratio are calculated as BIS tier 1 capital and CET1 capital, respectively, divided by period-end leverage exposure. SourcesCertain material in this document has been prepared by Credit Suisse on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. Credit Suisse has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to accuracy, completeness, reasonableness or reliability of such information.

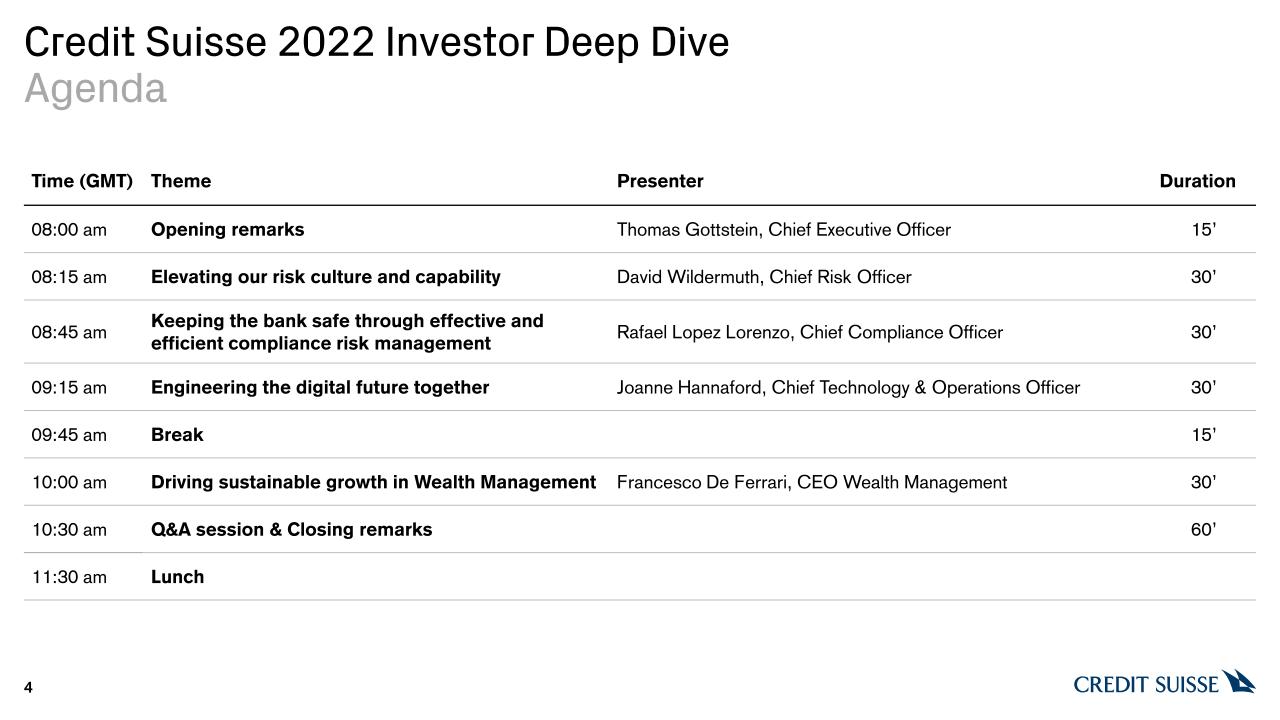

Credit Suisse 2022 Investor Deep DiveAgenda 4 Time (GMT) Theme Presenter Duration 08:00 am Opening remarks Thomas Gottstein, Chief Executive Officer 15’ 08:15 am Elevating our risk culture and capability David Wildermuth, Chief Risk Officer 30’ 08:45 am Keeping the bank safe through effective and efficient compliance risk management Rafael Lopez Lorenzo, Chief Compliance Officer 30’ 09:15 am Engineering the digital future together Joanne Hannaford, Chief Technology & Operations Officer 30’ 09:45 am Break 15’ 10:00 am Driving sustainable growth in Wealth Management Francesco De Ferrari, CEO Wealth Management 30’ 10:30 am Q&A session & Closing remarks 60’ 11:30 am Lunch

Risk Elevating our risk culture and capability David Wildermuth, Chief Risk OfficerJune 28, 2022

Invest for growth Simplify the operating model The past 12 months have been a period of significant change for the Risk organization 6 Aligned on priorities for Risk going forward, investing in our people, processes and infrastructure Strengthen the core business Credit Suisse has set new strategic goals… …and Risk has evolved to match Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Reset our risk appetite and managed our risk profile to position ourselves with the Group strategy Reinforced the Risk organization, established expectations for first line of defense ownership, and developed path forward for risk culture

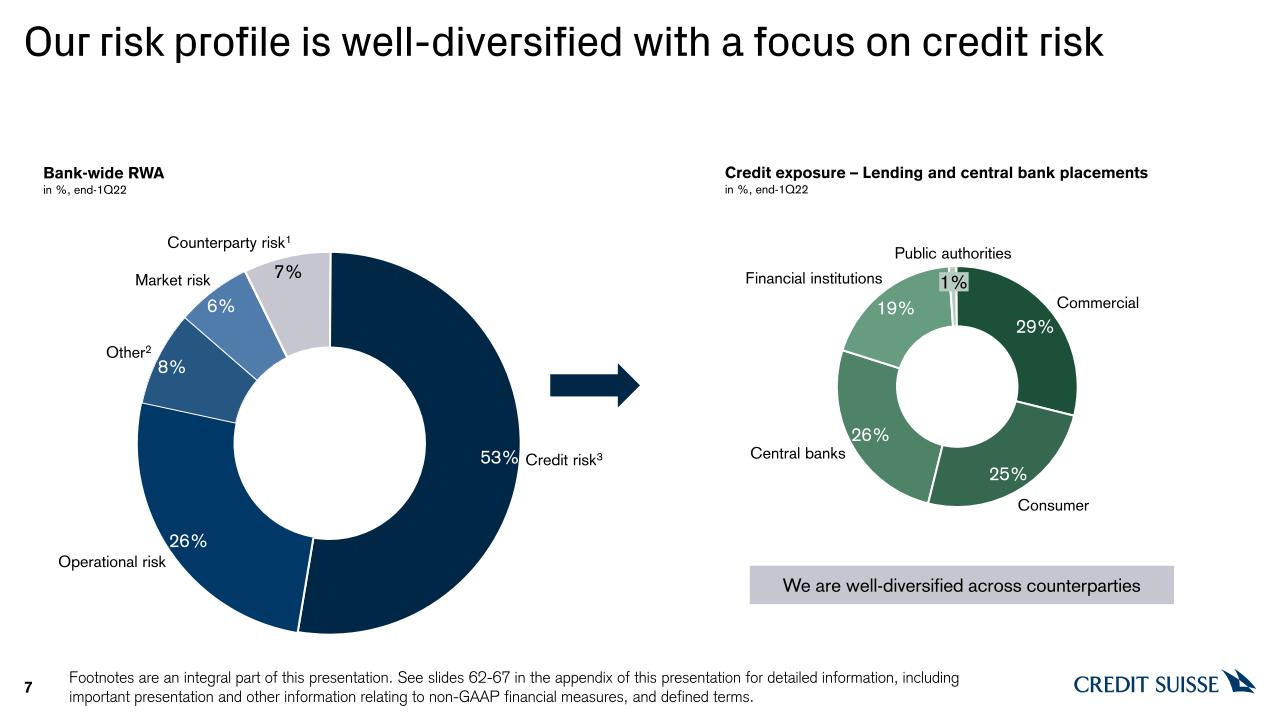

Our risk profile is well-diversified with a focus on credit risk 7 Bank-wide RWAin %, end-1Q22 185(68%) 70(26%) Credit risk Operational Risk Market risk Credit exposure – Lending and central bank placementsin %, end-1Q22 Market risk Other2 Counterparty risk1 Credit risk3 Operational risk 1% Central banks Financial institutions Public authorities Commercial Consumer We are well-diversified across counterparties Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

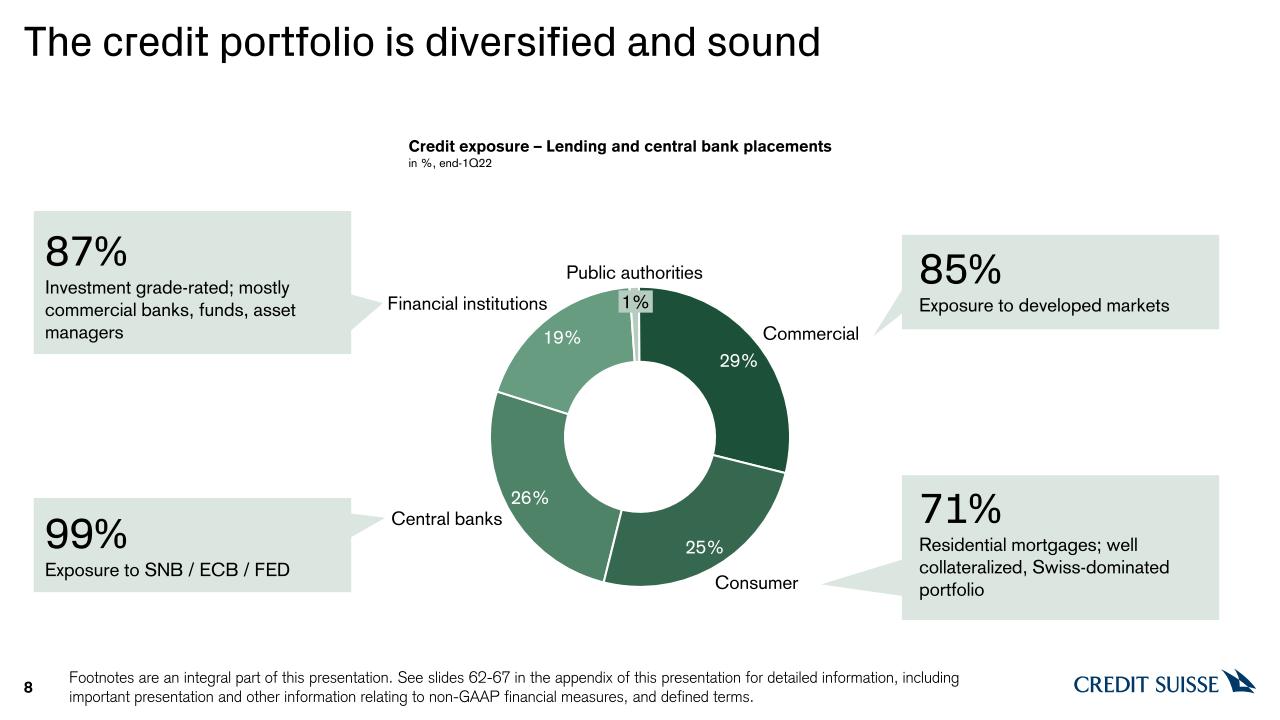

The credit portfolio is diversified and sound 8 Credit exposure – Lending and central bank placements in %, end-1Q22 Central banks Consumer Financial institutions 1% Public authorities Commercial Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. 87%Investment grade-rated; mostly commercial banks, funds, asset managers 99%Exposure to SNB / ECB / FED 85%Exposure to developed markets 71%Residential mortgages; well collateralized, Swiss-dominated portfolio

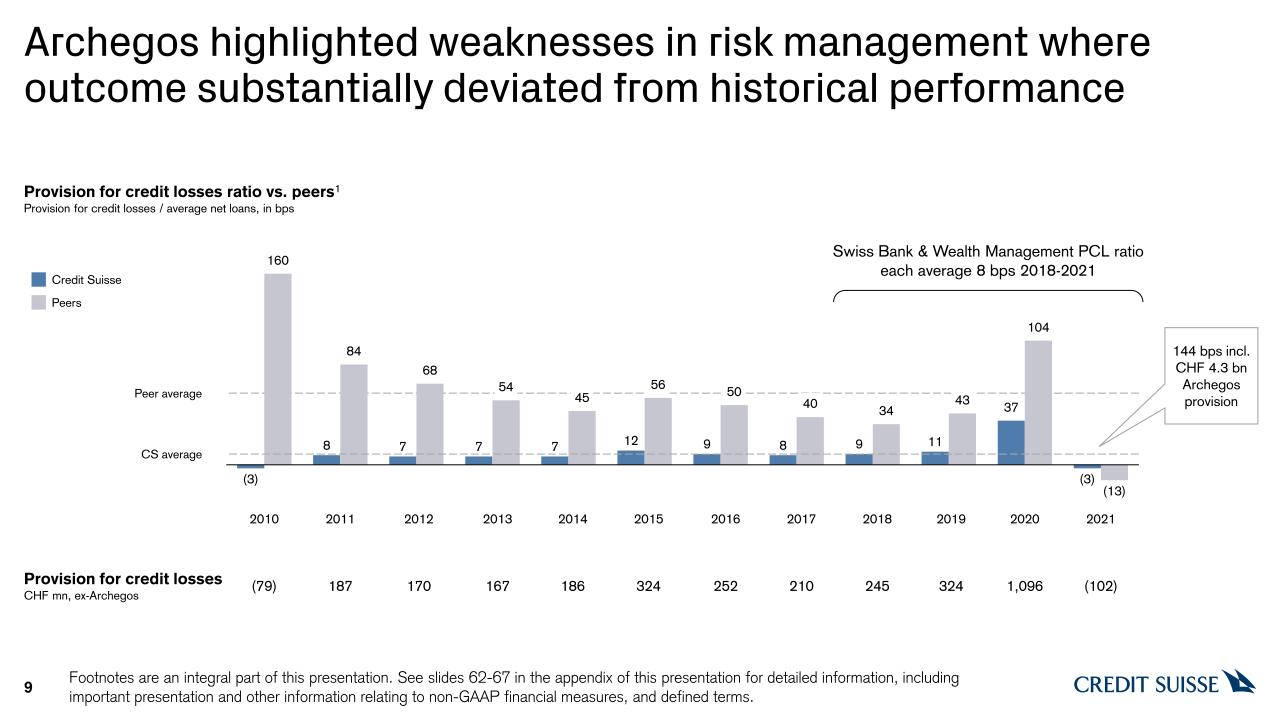

Archegos highlighted weaknesses in risk management where outcome substantially deviated from historical performance 9 Provision for credit losses ratio vs. peers1Provision for credit losses / average net loans, in bps Provision for credit lossesCHF mn, ex-Archegos Peer average CS average Credit Suisse Peers 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 (79) 187 170 167 186 324 252 210 245 324 1,096 (102) 144 bps incl. CHF 4.3 bn Archegos provision Swiss Bank & Wealth Management PCL ratio each average 8 bps 2018-2021 Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

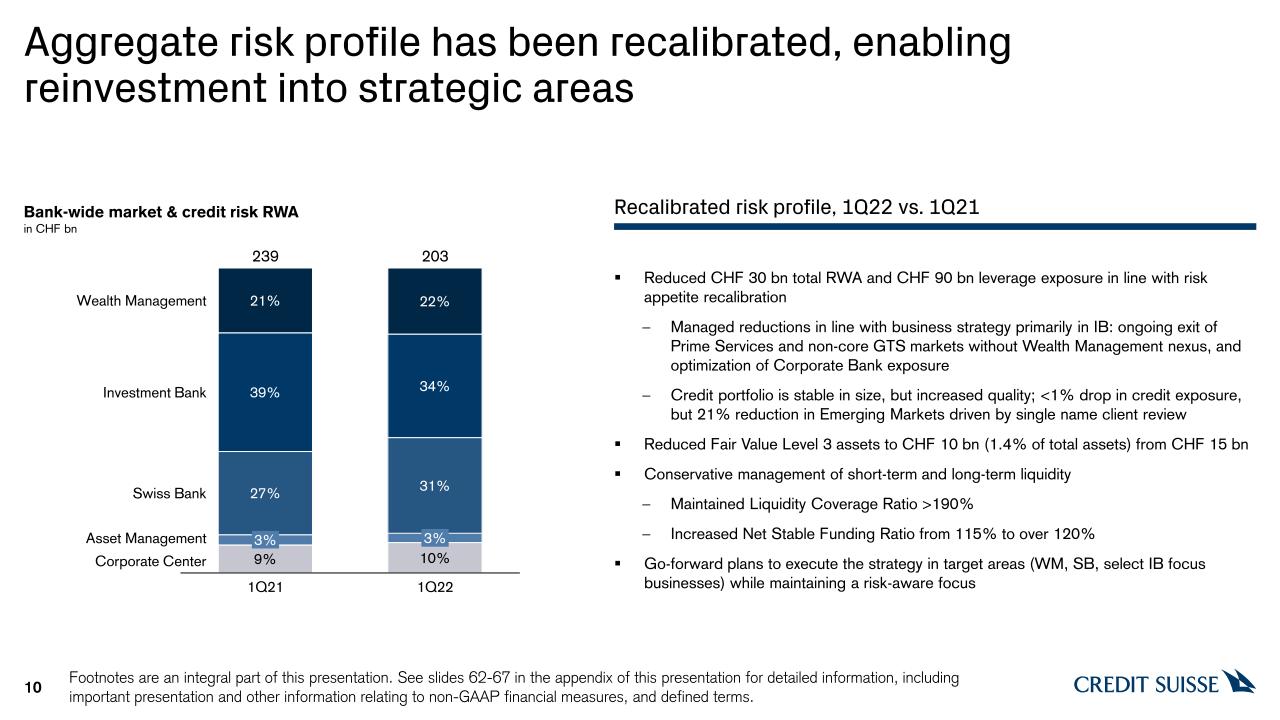

Aggregate risk profile has been recalibrated, enabling reinvestment into strategic areas 10 Bank-wide market & credit risk RWAin CHF bn Reduced CHF 30 bn total RWA and CHF 90 bn leverage exposure in line with risk appetite recalibrationManaged reductions in line with business strategy primarily in IB: ongoing exit of Prime Services and non-core GTS markets without Wealth Management nexus, and optimization of Corporate Bank exposureCredit portfolio is stable in size, but increased quality; <1% drop in credit exposure, but 21% reduction in Emerging Markets driven by single name client reviewReduced Fair Value Level 3 assets to CHF 10 bn (1.4% of total assets) from CHF 15 bnConservative management of short-term and long-term liquidityMaintained Liquidity Coverage Ratio >190%Increased Net Stable Funding Ratio from 115% to over 120%Go-forward plans to execute the strategy in target areas (WM, SB, select IB focus businesses) while maintaining a risk-aware focus Wealth Management 1Q21 3% 1Q22 3% Investment Bank Swiss Bank Asset Management Corporate Center 239 203 Recalibrated risk profile, 1Q22 vs. 1Q21 Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

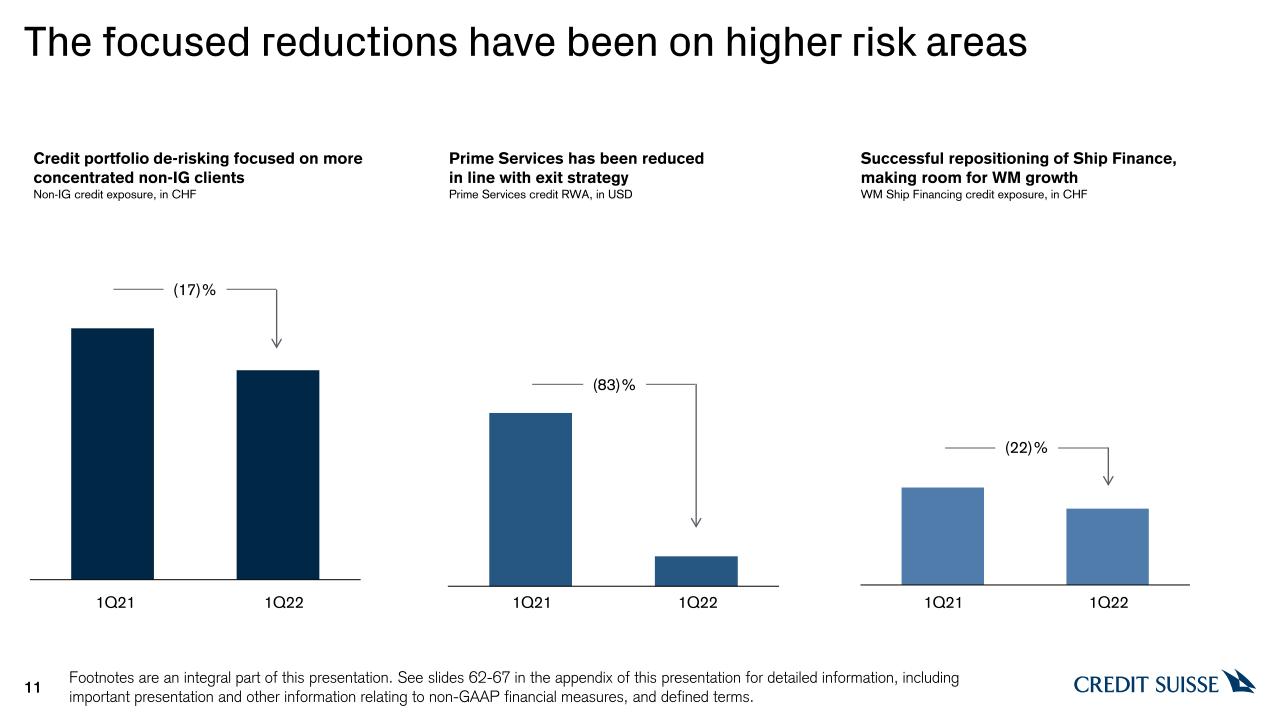

The focused reductions have been on higher risk areas Credit portfolio de-risking focused on more concentrated non-IG clientsNon-IG credit exposure, in CHF Prime Services has been reduced in line with exit strategyPrime Services credit RWA, in USD Successful repositioning of Ship Finance, making room for WM growthWM Ship Financing credit exposure, in CHF 1Q21 1Q22 1Q22 1Q21 1Q21 1Q22 (17)% (83)% (22)% Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. 11

Deep dive on selected portfolios 12 Forward looking risk management measures 1Q22 portfolio Swiss Bank portfolio (CHF 163 bn) of high quality; 93%1 investment grade rated73% relates to real estate lending (~45% average LTV)Commodity Trade Finance (CTF) portfolio concentrated on large/mid-size players – focus on energy (43%) and metals (45%) Conservative lending standards aligned to Swiss Banking AssociationResilient to interest rate changesCTF with 75% of exposures transactionally secured with maturities under 180 days Swiss Bank 75% investment grade rated – focused on liquid listed collateralDiversified portfolio of transactions with core UHNW clientsGlobal book; largest region APAC, supporting Entrepreneur strategy De-risked portfolio; with de-risking focus on concentration risksEmphasis on conservative LTV terms, collateral support and structural mitigants Remains a core product for WM client growth Share-Backed Lending 1Q22 NIG underwriting exposure of USD 7.4 bn, ~25% lower vs. 1Q21Underwriting exposure further reduced as deals syndicate2Q22 shift toward higher quality and defensive names with de-risking underway Track record of managing and distributing risk in adverse marketsMaintain robust and improved underwriting terms New commitments well structured and reflect current investor appetiteDisciplined approval of higher quality new underwriting IB Leveraged Finance Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

Strengthened risk pillarsEnabled greater consistency across all risk types; new risk types elevated (Cyber & Tech, Sustainability) Reinforced leadership team4 new CRO direct reports hired since April 2021 Increased industry expertiseCRO direct reports average ~25 years experience Greater top-of-house transparency6 CRO direct reports no longer dual-hatted since April 2021 More CS tenure and institutional insightsCRO direct reports average ~11 years at Credit Suisse Heightened investmentRisk budget increase of >15% for 2022 vs. 2020 Investing in our people and our organizational design is critical to strengthening our Risk management 13 Clearer lines of control Depth of experience Improved stability Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

We continue to invest in embedding Climate risk into our risk management framework building on strong progress to-date 14 Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. We are engaging with peers & the broader community as climate risk management continues to evolve UN Environment Programme – Finance Initiative Sustainable Markets Initiative – Financial Services Taskforce Task Force on Climate-Related Financial Disclosures Taskforce on Nature-related Financial Disclosures Carbon Disclosure Project Net Zero Asset Managers Initiative Climate Bonds Initiative Climate Action 100+ Science-Based Targets Initiative Poseidon Principles Select examples:

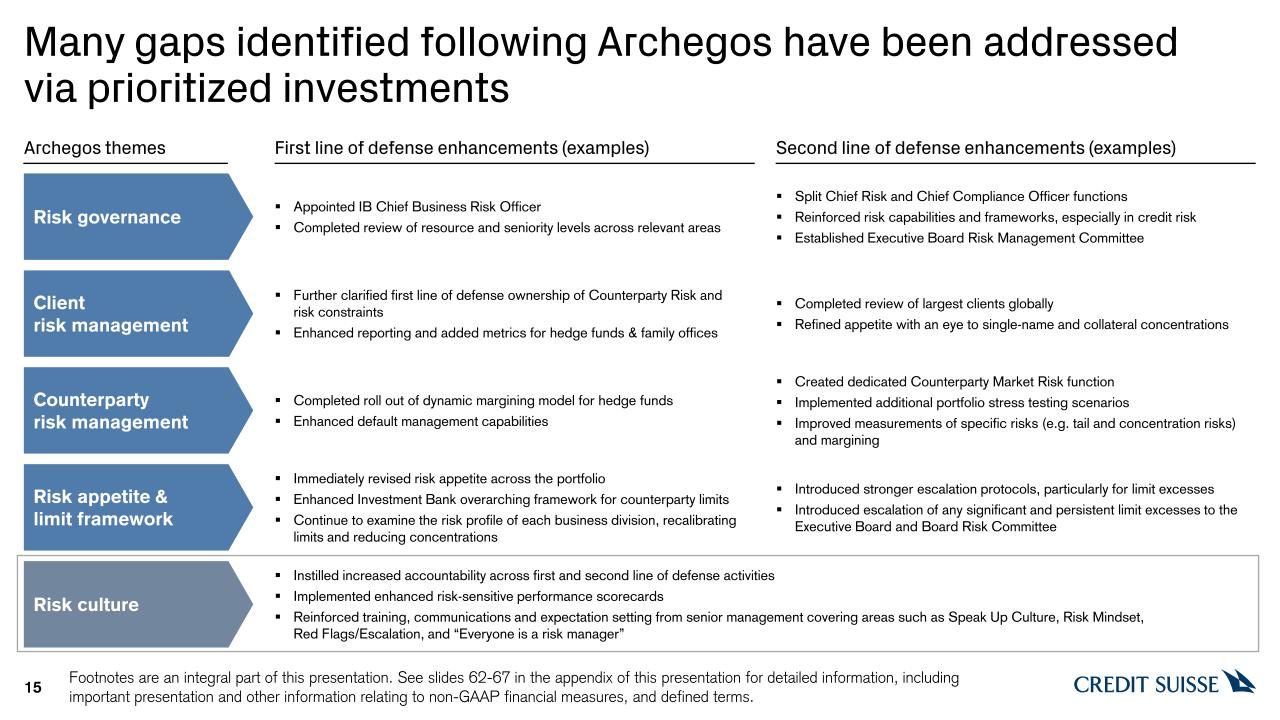

Risk culture Risk appetite & limit framework Client risk management Risk governance Counterparty risk management Many gaps identified following Archegos have been addressed via prioritized investments 15 Archegos themes First line of defense enhancements (examples) Second line of defense enhancements (examples) Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Appointed IB Chief Business Risk OfficerCompleted review of resource and seniority levels across relevant areas Further clarified first line of defense ownership of Counterparty Risk and risk constraintsEnhanced reporting and added metrics for hedge funds & family offices Completed roll out of dynamic margining model for hedge fundsEnhanced default management capabilities Immediately revised risk appetite across the portfolioEnhanced Investment Bank overarching framework for counterparty limitsContinue to examine the risk profile of each business division, recalibrating limits and reducing concentrations Instilled increased accountability across first and second line of defense activitiesImplemented enhanced risk-sensitive performance scorecardsReinforced training, communications and expectation setting from senior management covering areas such as Speak Up Culture, Risk Mindset, Red Flags/Escalation, and “Everyone is a risk manager” Split Chief Risk and Chief Compliance Officer functionsReinforced risk capabilities and frameworks, especially in credit riskEstablished Executive Board Risk Management Committee Completed review of largest clients globallyRefined appetite with an eye to single-name and collateral concentrations Created dedicated Counterparty Market Risk functionImplemented additional portfolio stress testing scenariosImproved measurements of specific risks (e.g. tail and concentration risks) and margining Introduced stronger escalation protocols, particularly for limit excessesIntroduced escalation of any significant and persistent limit excesses to the Executive Board and Board Risk Committee

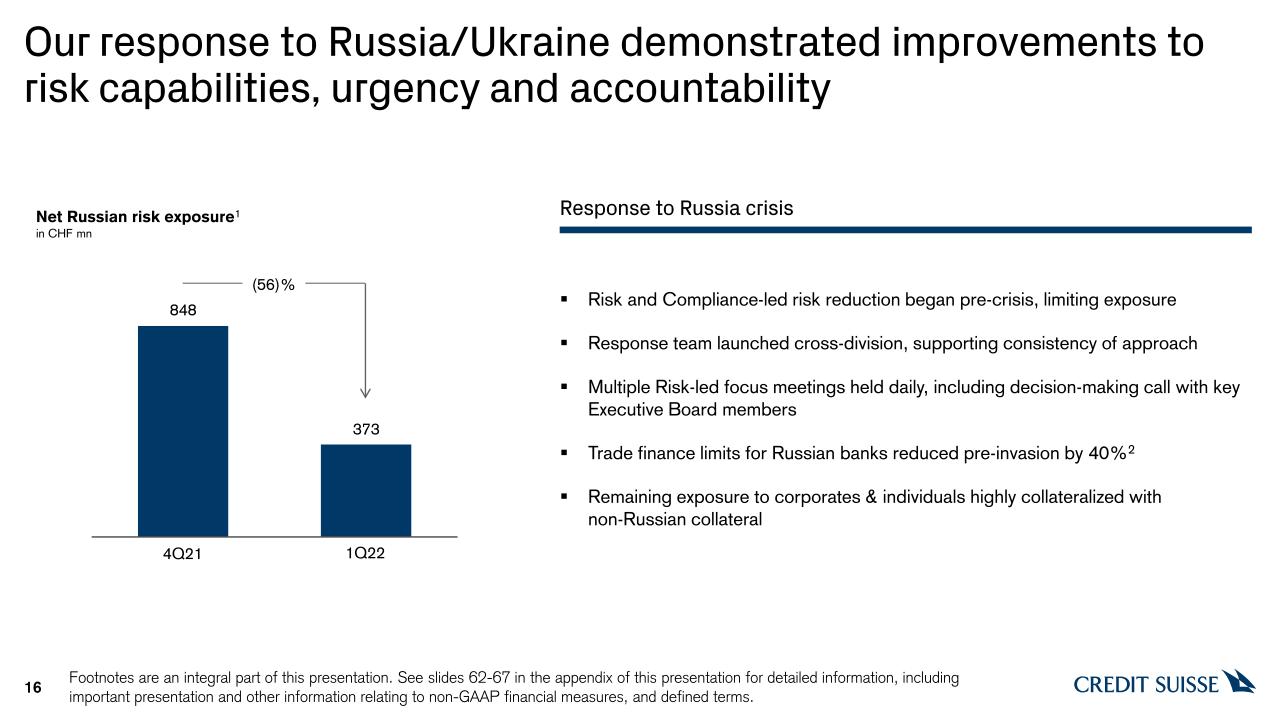

Our response to Russia/Ukraine demonstrated improvements to risk capabilities, urgency and accountability 16 Risk and Compliance-led risk reduction began pre-crisis, limiting exposureResponse team launched cross-division, supporting consistency of approachMultiple Risk-led focus meetings held daily, including decision-making call with key Executive Board membersTrade finance limits for Russian banks reduced pre-invasion by 40%2Remaining exposure to corporates & individuals highly collateralized with non-Russian collateral Net Russian risk exposure1in CHF mn 1Q22 4Q21 Response to Russia crisis (56)% Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

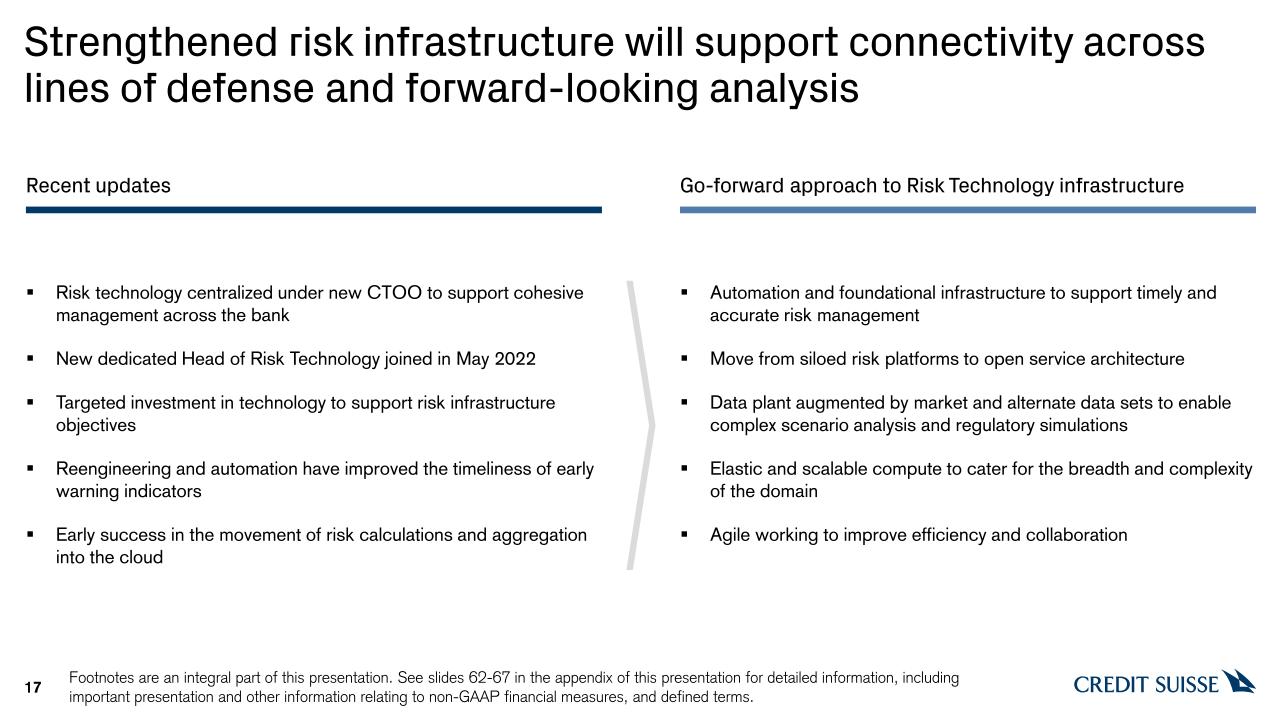

Strengthened risk infrastructure will support connectivity across lines of defense and forward-looking analysis 17 Go-forward approach to Risk Technology infrastructure Automation and foundational infrastructure to support timely and accurate risk managementMove from siloed risk platforms to open service architectureData plant augmented by market and alternate data sets to enable complex scenario analysis and regulatory simulationsElastic and scalable compute to cater for the breadth and complexity of the domainAgile working to improve efficiency and collaboration Recent updates Risk technology centralized under new CTOO to support cohesive management across the bankNew dedicated Head of Risk Technology joined in May 2022Targeted investment in technology to support risk infrastructure objectivesReengineering and automation have improved the timeliness of early warning indicatorsEarly success in the movement of risk calculations and aggregation into the cloud Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

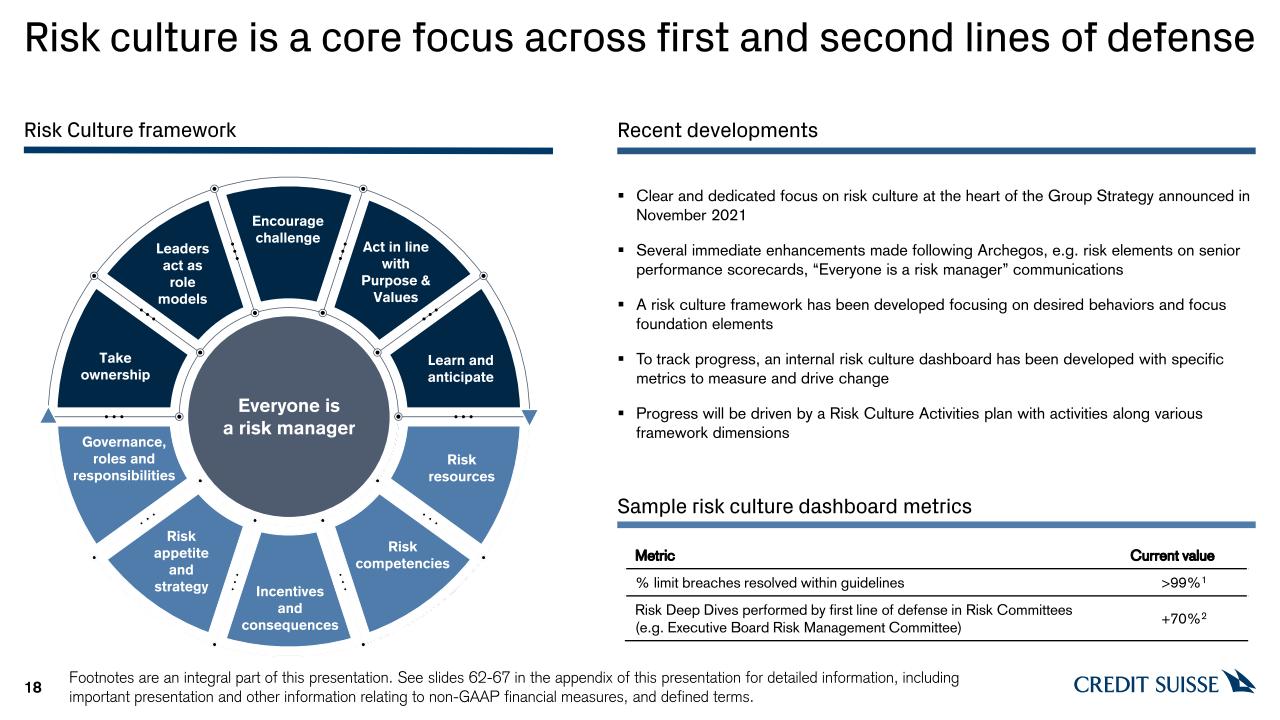

Risk culture is a core focus across first and second lines of defense Metric Current value % limit breaches resolved within guidelines >99%1 Risk Deep Dives performed by first line of defense in Risk Committees (e.g. Executive Board Risk Management Committee) +70%2 Clear and dedicated focus on risk culture at the heart of the Group Strategy announced in November 2021Several immediate enhancements made following Archegos, e.g. risk elements on senior performance scorecards, “Everyone is a risk manager” communicationsA risk culture framework has been developed focusing on desired behaviors and focus foundation elementsTo track progress, an internal risk culture dashboard has been developed with specific metrics to measure and drive changeProgress will be driven by a Risk Culture Activities plan with activities along various framework dimensions Sample risk culture dashboard metrics Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Learn and anticipate Take ownership Encourage challenge Leaders act as role models Act in line with Purpose & Values Governance, roles and responsibilities Risk appetite and strategy Incentives andconsequences Risk competencies Risk resources Everyone is a risk manager Risk Culture framework Recent developments 18

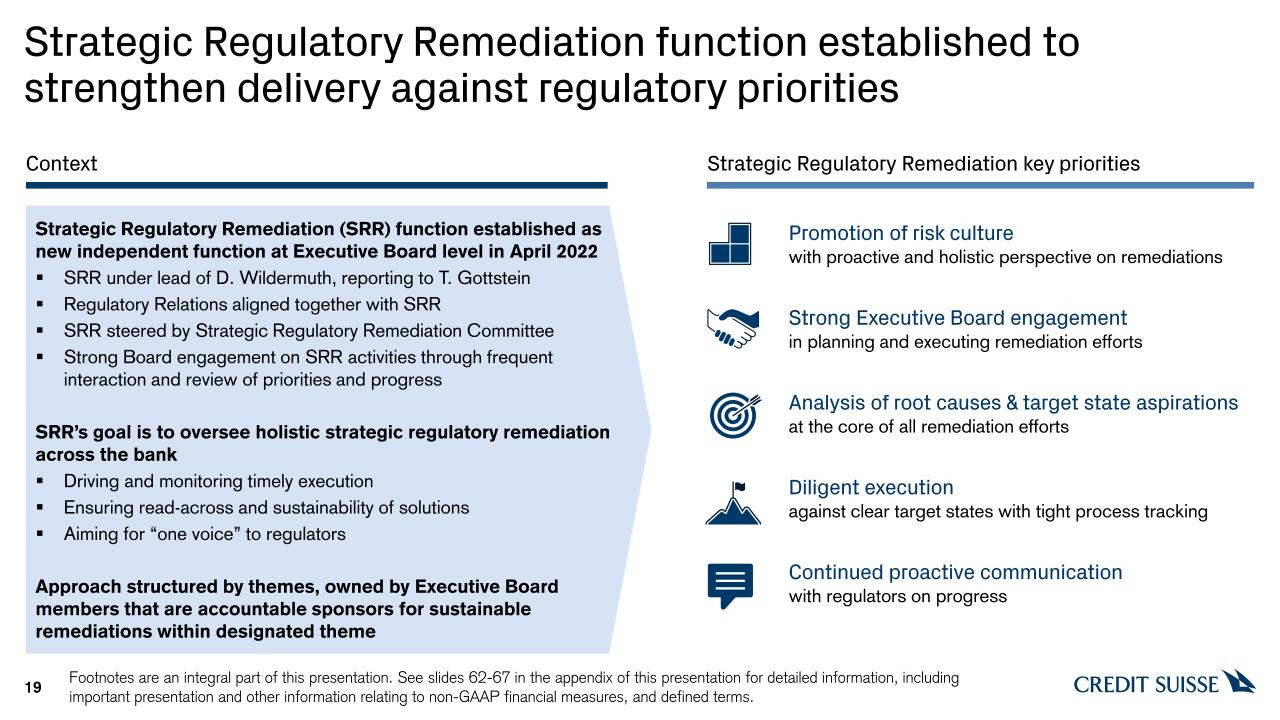

Strategic Regulatory Remediation function established to strengthen delivery against regulatory priorities 19 Strategic Regulatory Remediation (SRR) function established as new independent function at Executive Board level in April 2022SRR under lead of D. Wildermuth, reporting to T. GottsteinRegulatory Relations aligned together with SRR SRR steered by Strategic Regulatory Remediation Committee Strong Board engagement on SRR activities through frequent interaction and review of priorities and progressSRR’s goal is to oversee holistic strategic regulatory remediation across the bankDriving and monitoring timely executionEnsuring read-across and sustainability of solutions Aiming for “one voice” to regulatorsApproach structured by themes, owned by Executive Board members that are accountable sponsors for sustainable remediations within designated theme Promotion of risk culturewith proactive and holistic perspective on remediations Strong Executive Board engagementin planning and executing remediation efforts Analysis of root causes & target state aspirationsat the core of all remediation efforts Diligent executionagainst clear target states with tight process tracking Continued proactive communicationwith regulators on progress Strategic Regulatory Remediation key priorities Context Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

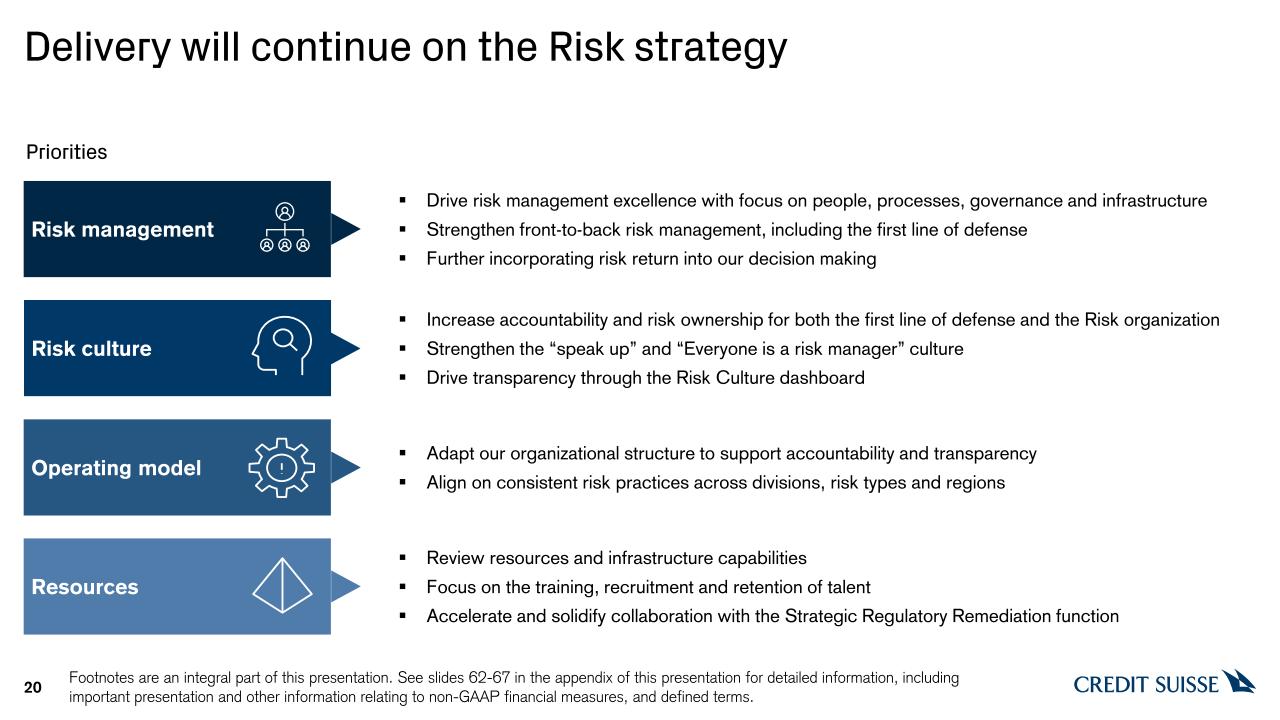

20 Risk culture Increase accountability and risk ownership for both the first line of defense and the Risk organizationStrengthen the “speak up” and “Everyone is a risk manager” cultureDrive transparency through the Risk Culture dashboard Operating model Adapt our organizational structure to support accountability and transparencyAlign on consistent risk practices across divisions, risk types and regions Resources Review resources and infrastructure capabilitiesFocus on the training, recruitment and retention of talentAccelerate and solidify collaboration with the Strategic Regulatory Remediation function Risk management Drive risk management excellence with focus on people, processes, governance and infrastructureStrengthen front-to-back risk management, including the first line of defenseFurther incorporating risk return into our decision making Delivery will continue on the Risk strategy Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Priorities

Compliance Keeping the bank safe through effective and efficient compliance risk management Rafael Lopez Lorenzo, Chief Compliance OfficerJune 28, 2022

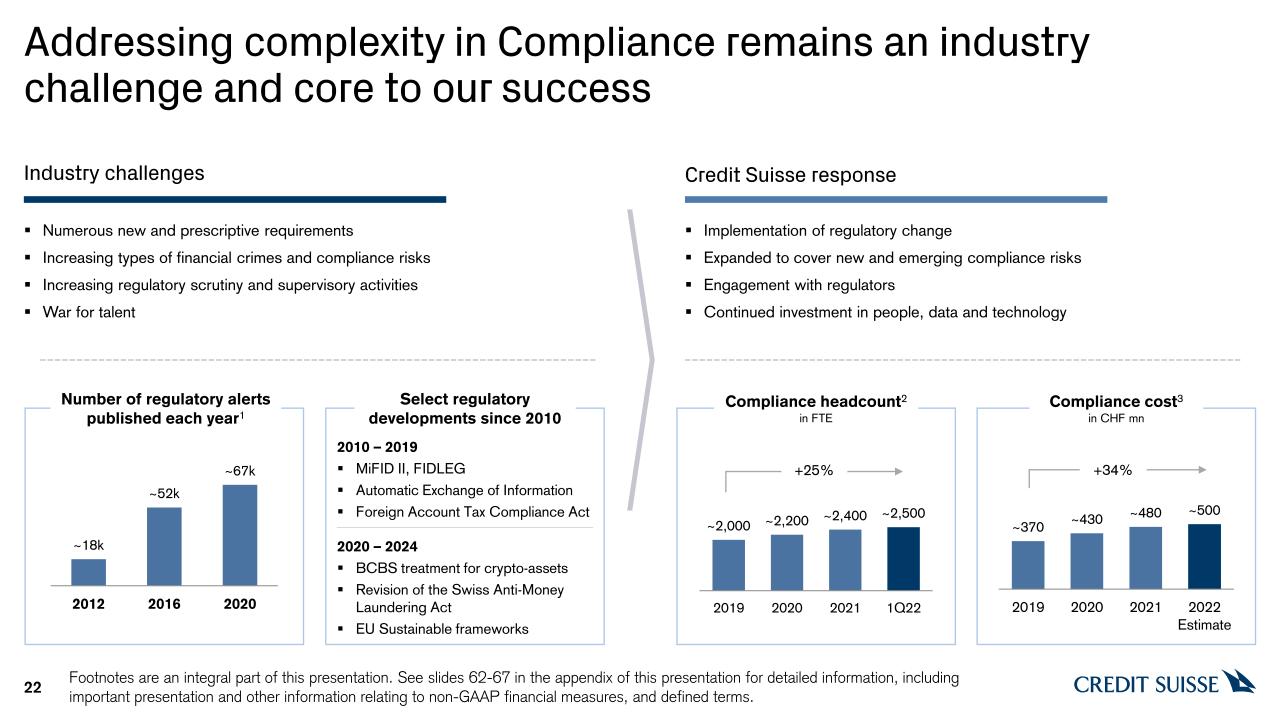

Addressing complexity in Compliance remains an industry challenge and core to our success +34% Number of regulatory alerts published each year1 Numerous new and prescriptive requirementsIncreasing types of financial crimes and compliance risksIncreasing regulatory scrutiny and supervisory activitiesWar for talent Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. 22 Implementation of regulatory changeExpanded to cover new and emerging compliance risksEngagement with regulatorsContinued investment in people, data and technology Industry challenges Credit Suisse response Compliance headcount2in FTE Compliance cost3in CHF mn 2010 – 2019MiFID II, FIDLEGAutomatic Exchange of InformationForeign Account Tax Compliance Act 2020 – 2024BCBS treatment for crypto-assets Revision of the Swiss Anti-Money Laundering ActEU Sustainable frameworks Select regulatory developments since 2010 +25%

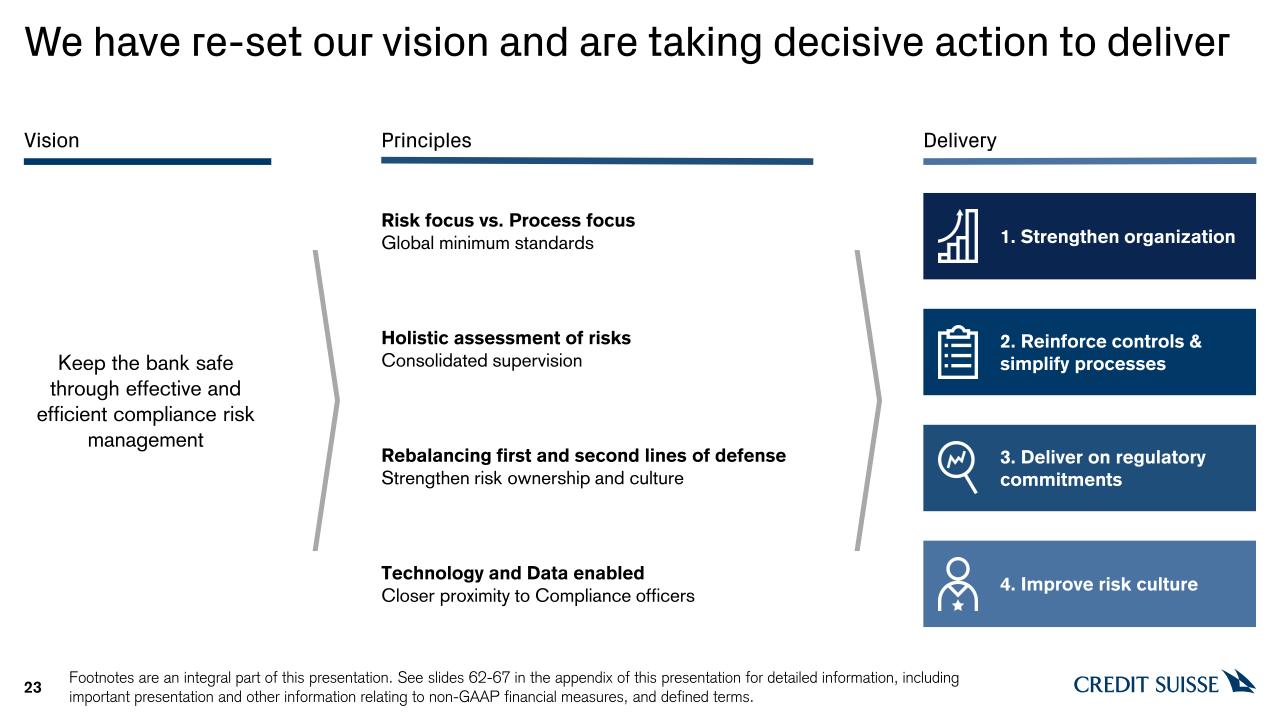

We have re-set our vision and are taking decisive action to deliver Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. 23 1. Strengthen organization 2. Reinforce controls & simplify processes 3. Deliver on regulatory commitments 4. Improve risk culture Delivery Keep the bank safe through effective and efficient compliance risk management Risk focus vs. Process focusGlobal minimum standards Holistic assessment of risksConsolidated supervision Rebalancing first and second lines of defenseStrengthen risk ownership and culture Technology and Data enabledCloser proximity to Compliance officers Vision Principles

Refreshed leadership and simplification have strengthened the CCO organization Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. 24 Strengthening seniority 14% MDs/Directors in Compliance function 22 new MDs/Directors hired YTD1 A refreshed and diverse teamAverage professional experience of 21 years 55% female employees in Compliance function Increased leadership bandwidthSenior leadership team increased from 8 to 132Reduced dual hatting to increase risk oversight Rafael Lopez LorenzoChief Compliance OfficerMember of the Executive Board Thomas GottsteinChief Executive OfficerCredit Suisse Group AG Centralized teams Divisional & Regional teams Risk-aligned teams Risk-aligned teams setting Global Minimum Standards and overseeing these as thematic risk ownersDivisional / Regional teamschallenging compliance risk and seeking to ensure execution against Global Minimum StandardsCentralized teams simplify and accelerate priorities of change, data, technology and regulatory deliverables …with very clear benefits… Responsibilities and ownership… …and a focus on strong leadership and talent

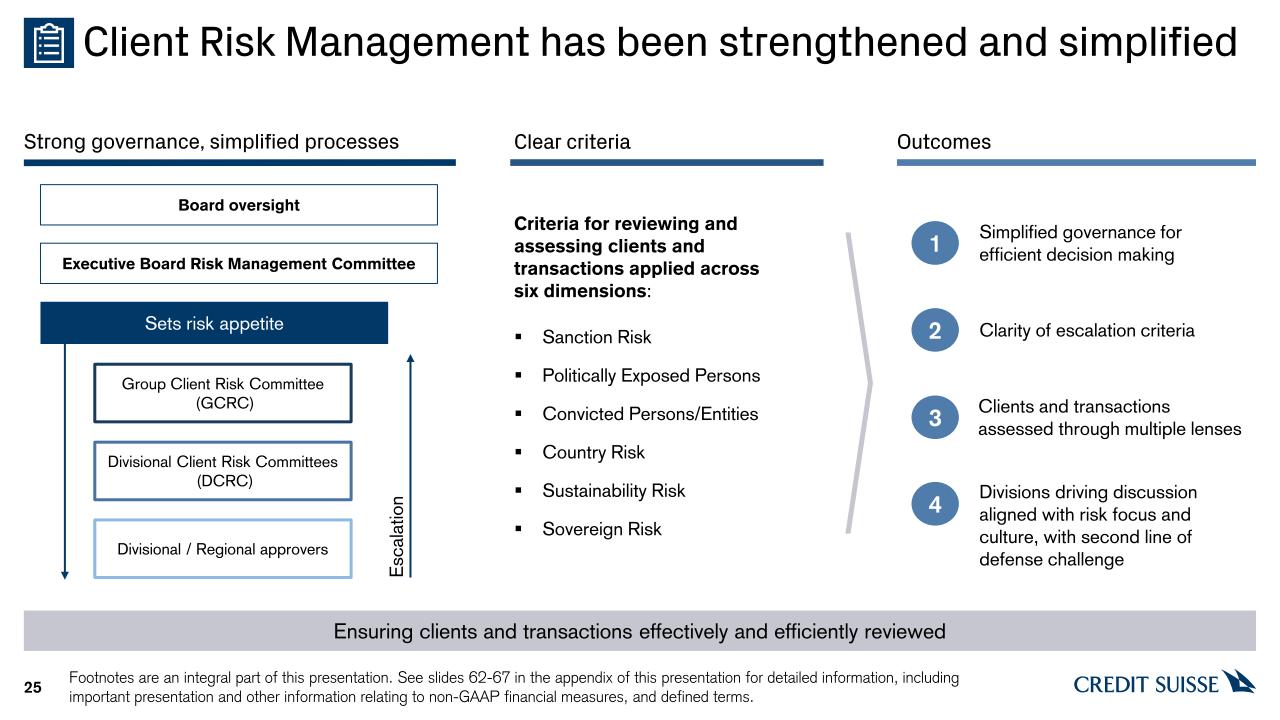

Client Risk Management has been strengthened and simplified Ensuring clients and transactions effectively and efficiently reviewed Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Clear criteria Strong governance, simplified processes Outcomes Criteria for reviewing and assessing clients and transactions applied across six dimensions:Sanction RiskPolitically Exposed PersonsConvicted Persons/EntitiesCountry RiskSustainability RiskSovereign Risk 1 2 Clarity of escalation criteria 3 Clients and transactions assessed through multiple lenses Simplified governance for efficient decision making 4 Divisions driving discussion aligned with risk focus and culture, with second line of defense challenge Divisional / Regional approvers Divisional Client Risk Committees (DCRC) Group Client Risk Committee (GCRC) Executive Board Risk Management Committee Sets risk appetite Escalation Board oversight 25

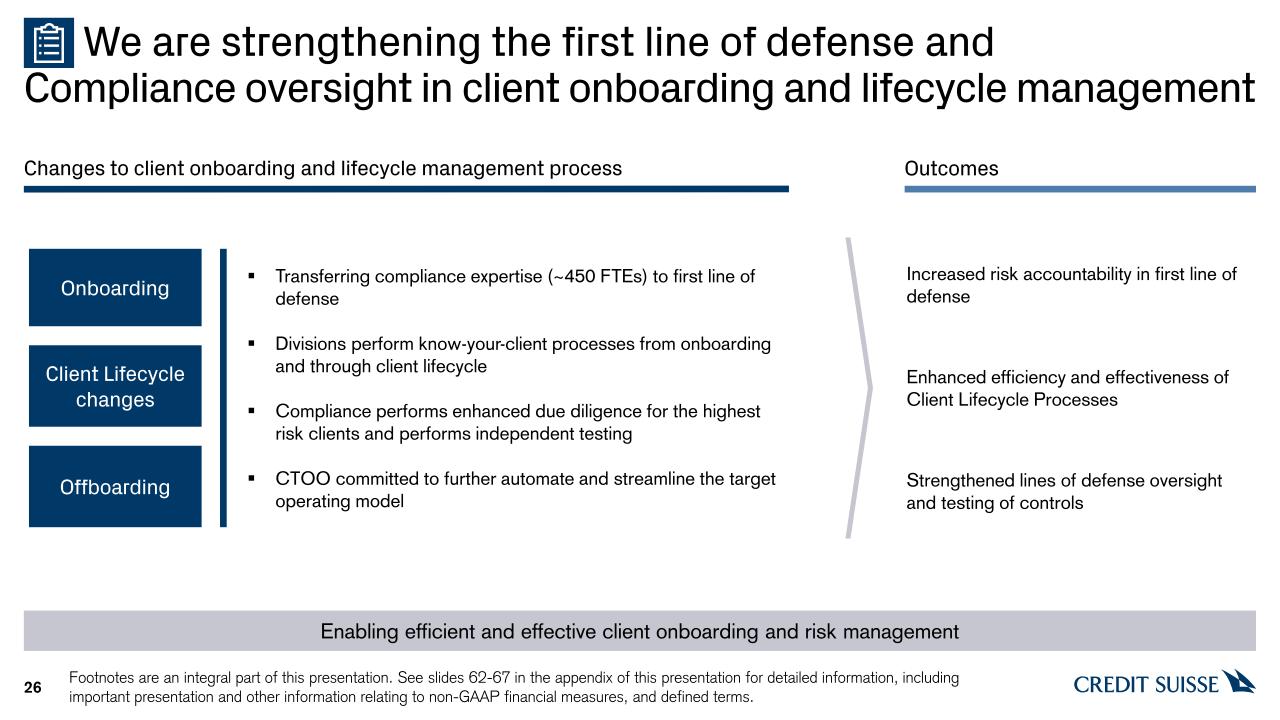

We are strengthening the first line of defense and Compliance oversight in client onboarding and lifecycle management 26 Onboarding Client Lifecycle changes Offboarding Transferring compliance expertise (~450 FTEs) to first line of defenseDivisions perform know-your-client processes from onboarding and through client lifecycleCompliance performs enhanced due diligence for the highest risk clients and performs independent testingCTOO committed to further automate and streamline the target operating model Enabling efficient and effective client onboarding and risk management Outcomes Changes to client onboarding and lifecycle management process Enhanced efficiency and effectiveness of Client Lifecycle Processes Strengthened lines of defense oversight and testing of controls Increased risk accountability in first line of defense Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

Our approach to sanctions demonstrates the effectiveness of our controls to manage evolving market developments 27 Global Sanctions team well connected with sanction authoritiesScenario planning – pre-sanction client exposure assessmentBank-wide client screening to identify impacted relationships as sanctions evolveFirst line of defense driving engagement on exposure assessment and mitigationExecutive Board oversight with dedicated governance and escalation Mitigating the risk of clients circumventing sanctions regimes We apply global sanctions timely and effectively across all impacted clients and businesses Our sanctions approach Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

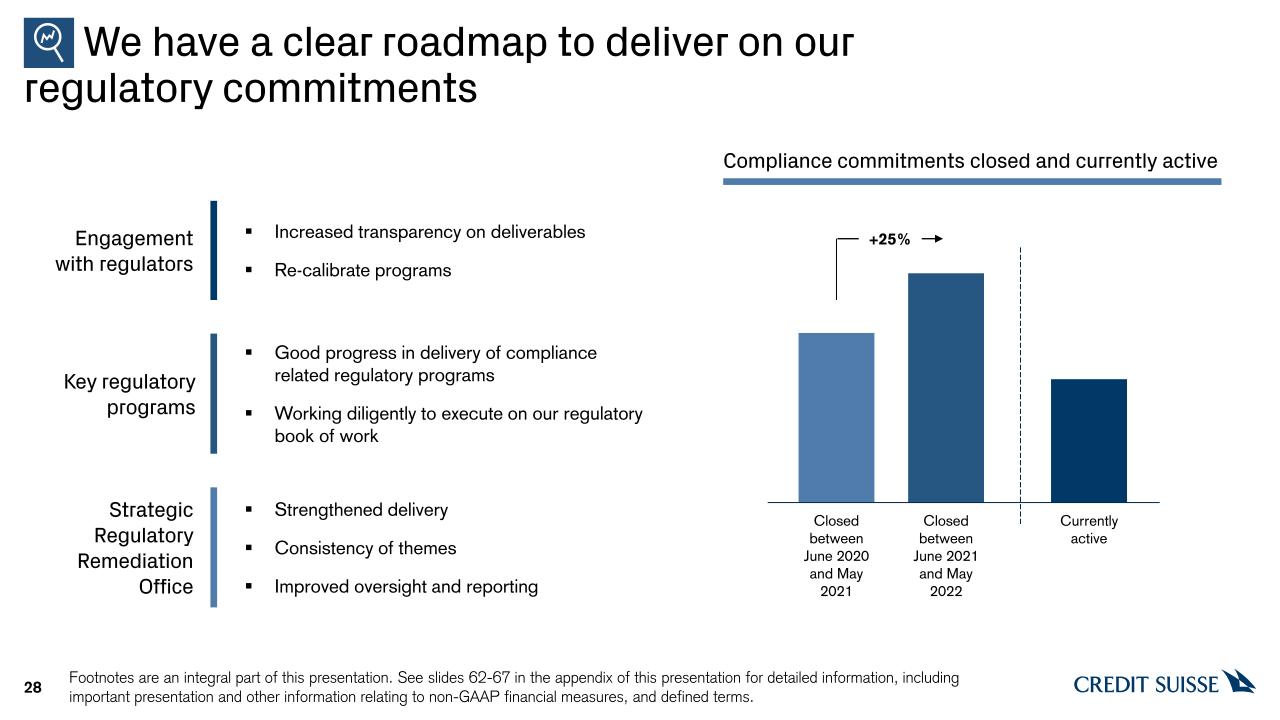

We have a clear roadmap to deliver on our regulatory commitments 28 Increased transparency on deliverablesRe-calibrate programs Engagement with regulators Strengthened delivery Consistency of themesImproved oversight and reporting Strategic Regulatory Remediation Office Good progress in delivery of compliance related regulatory programsWorking diligently to execute on our regulatory book of work Key regulatory programs Closed between June 2020 and May 2021 Closed between June 2021 and May 2022 Currently active Compliance commitments closed and currently active Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. +25%

We are making fundamental changes to the Compliance risk culture 29 1 Co-ownership of key regulatory programs 4 Active challenge from the second to the first line of defense Divisions and Regions leading discussions on compliance risk through bank governance 2 Clear accountability of client risk appetite 3 Lead mindset where “Everyone is a risk manager” 5 Changes in Risk Culture observed by Compliance Risk Culture framework Learn and anticipate Take ownership Encourage challenge Leaders act as role models Act in line with Purpose & Values Governance, roles and responsibilities Risk appetite and strategy Incentives andconsequences Risk competencies Risk resources Everyone is a risk manager Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

Delivery to continue… 30 3. Deliver on regulatory commitments 2. Reinforce controls & simplify processes 4. Improve risk culture 1. Strengthen organization Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

Technology & Operations Engineering the digital future together Joanne Hannaford, Chief Technology & Operations Officer June 28, 2022

Technology and Operations (CTOO) supports our business today 32 Wealth Management 15booking centers >800 bnAuM in CHF1 >100kvirtual & physical servers 37krelational databases 3kapplications ~90kworkstations 13data centers Rationalization opportunities for foundational infrastructure Investment Bank 250multi-asset execution venues 4.5kclients actively trading on IB platform daily >160 mndaily client orders on electronic trading platform Swiss Bank ~240 mnannual payment transactions2 ~430ATMs 7 mndigital online banking sessions per month Asset Management >440investment funds >460 bnAuM in CHF ~70%institutional clients ~140countries covered Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. ~180 Petabytestotal data stored

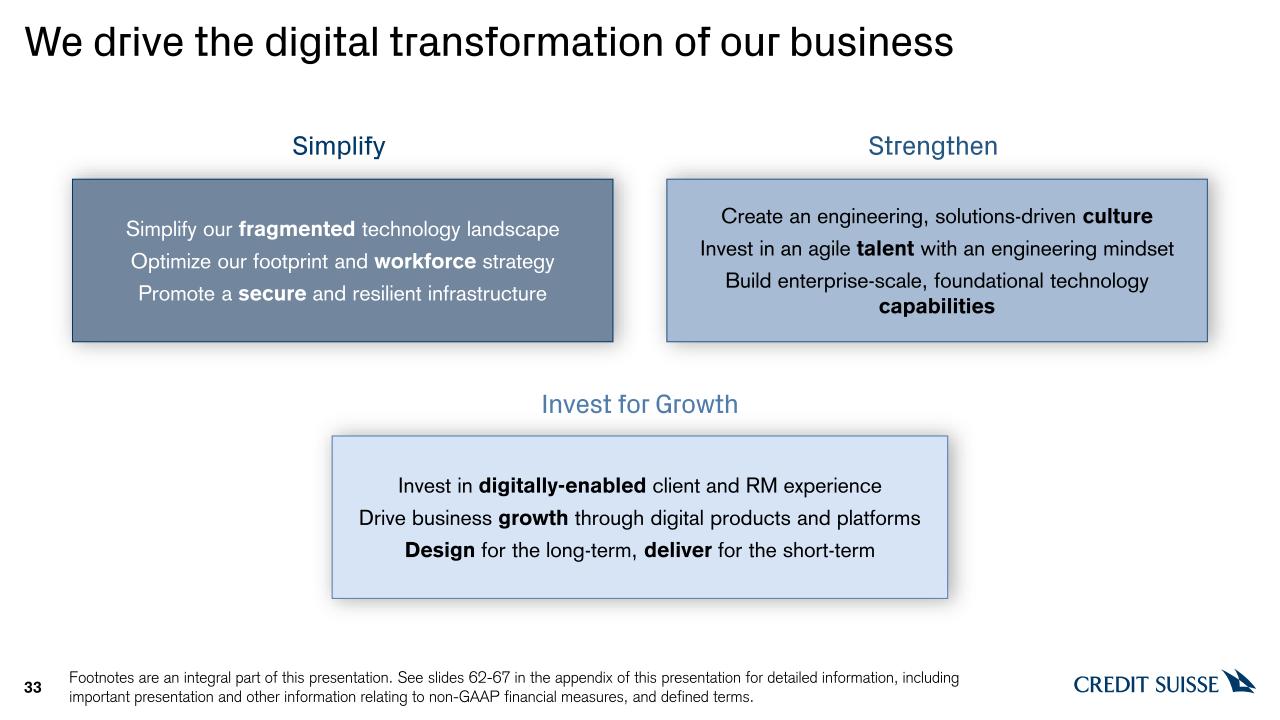

We drive the digital transformation of our business 33 Simplify our fragmented technology landscapeOptimize our footprint and workforce strategyPromote a secure and resilient infrastructure Simplify Create an engineering, solutions-driven cultureInvest in an agile talent with an engineering mindsetBuild enterprise-scale, foundational technology capabilities Strengthen Invest in digitally-enabled client and RM experienceDrive business growth through digital products and platformsDesign for the long-term, deliver for the short-term Invest for Growth Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

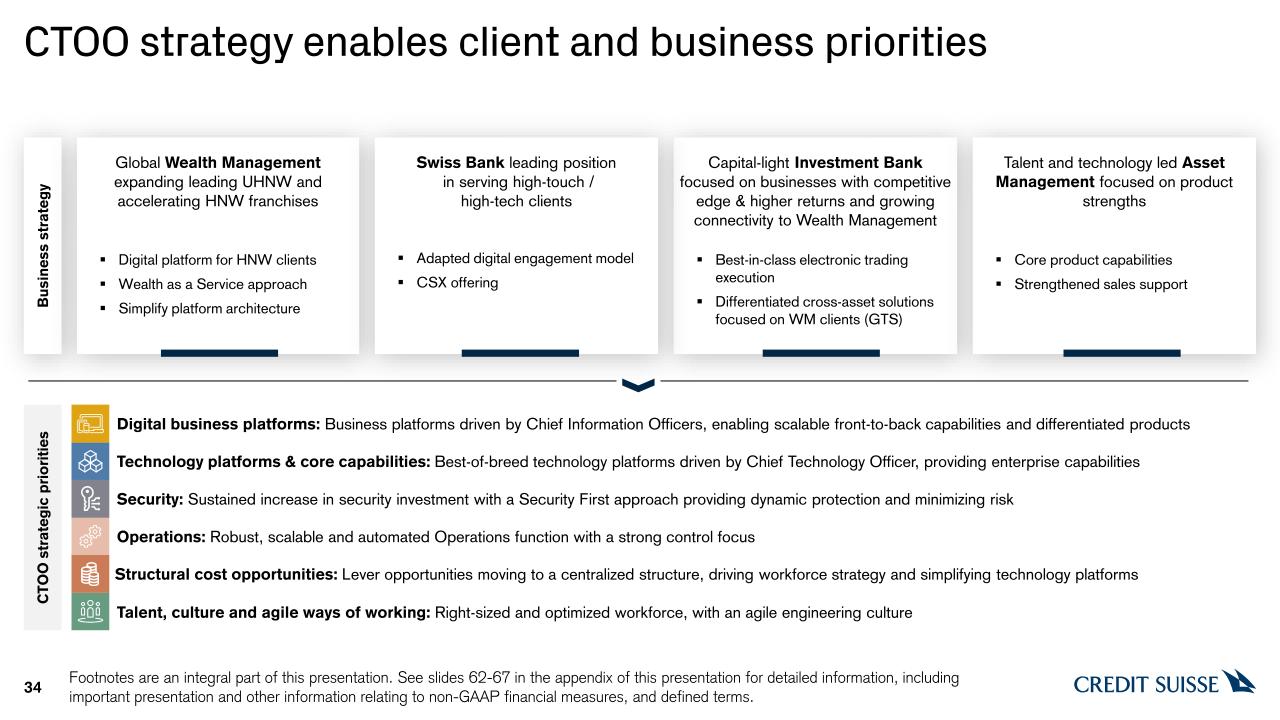

CTOO strategy enables client and business priorities 34 CTOO strategic priorities 2 Business strategy Technology platforms & core capabilities: Best-of-breed technology platforms driven by Chief Technology Officer, providing enterprise capabilities Digital business platforms: Business platforms driven by Chief Information Officers, enabling scalable front-to-back capabilities and differentiated products Talent, culture and agile ways of working: Right-sized and optimized workforce, with an agile engineering culture Operations: Robust, scalable and automated Operations function with a strong control focus Security: Sustained increase in security investment with a Security First approach providing dynamic protection and minimizing risk Global Wealth Management expanding leading UHNW and accelerating HNW franchisesDigital platform for HNW clientsWealth as a Service approachSimplify platform architecture Capital-light Investment Bank focused on businesses with competitive edge & higher returns and growing connectivity to Wealth ManagementBest-in-class electronic trading executionDifferentiated cross-asset solutions focused on WM clients (GTS) Talent and technology led Asset Management focused on product strengthsCore product capabilitiesStrengthened sales support Swiss Bank leading position in serving high-touch / high-tech clientsAdapted digital engagement modelCSX offering Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Structural cost opportunities: Lever opportunities moving to a centralized structure, driving workforce strategy and simplifying technology platforms

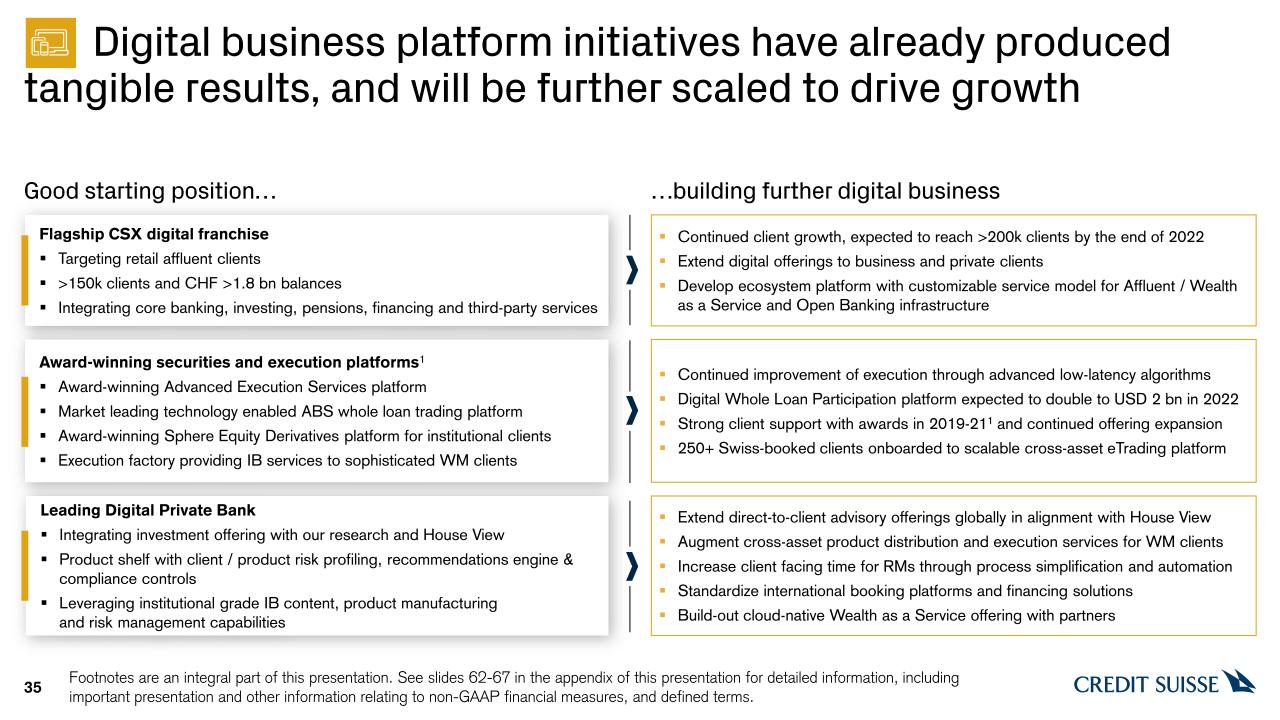

2 2 2 Digital business platform initiatives have already produced tangible results, and will be further scaled to drive growth 35 Good starting position… …building further digital business Flagship CSX digital franchise Targeting retail affluent clients >150k clients and CHF >1.8 bn balancesIntegrating core banking, investing, pensions, financing and third-party services Continued client growth, expected to reach >200k clients by the end of 2022Extend digital offerings to business and private clients Develop ecosystem platform with customizable service model for Affluent / Wealth as a Service and Open Banking infrastructure Award-winning securities and execution platforms1Award-winning Advanced Execution Services platformMarket leading technology enabled ABS whole loan trading platformAward-winning Sphere Equity Derivatives platform for institutional clientsExecution factory providing IB services to sophisticated WM clients Continued improvement of execution through advanced low-latency algorithmsDigital Whole Loan Participation platform expected to double to USD 2 bn in 2022Strong client support with awards in 2019-211 and continued offering expansion250+ Swiss-booked clients onboarded to scalable cross-asset eTrading platform Leading Digital Private Bank Integrating investment offering with our research and House ViewProduct shelf with client / product risk profiling, recommendations engine & compliance controlsLeveraging institutional grade IB content, product manufacturing and risk management capabilities Extend direct-to-client advisory offerings globally in alignment with House ViewAugment cross-asset product distribution and execution services for WM clientsIncrease client facing time for RMs through process simplification and automationStandardize international booking platforms and financing solutionsBuild-out cloud-native Wealth as a Service offering with partners Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

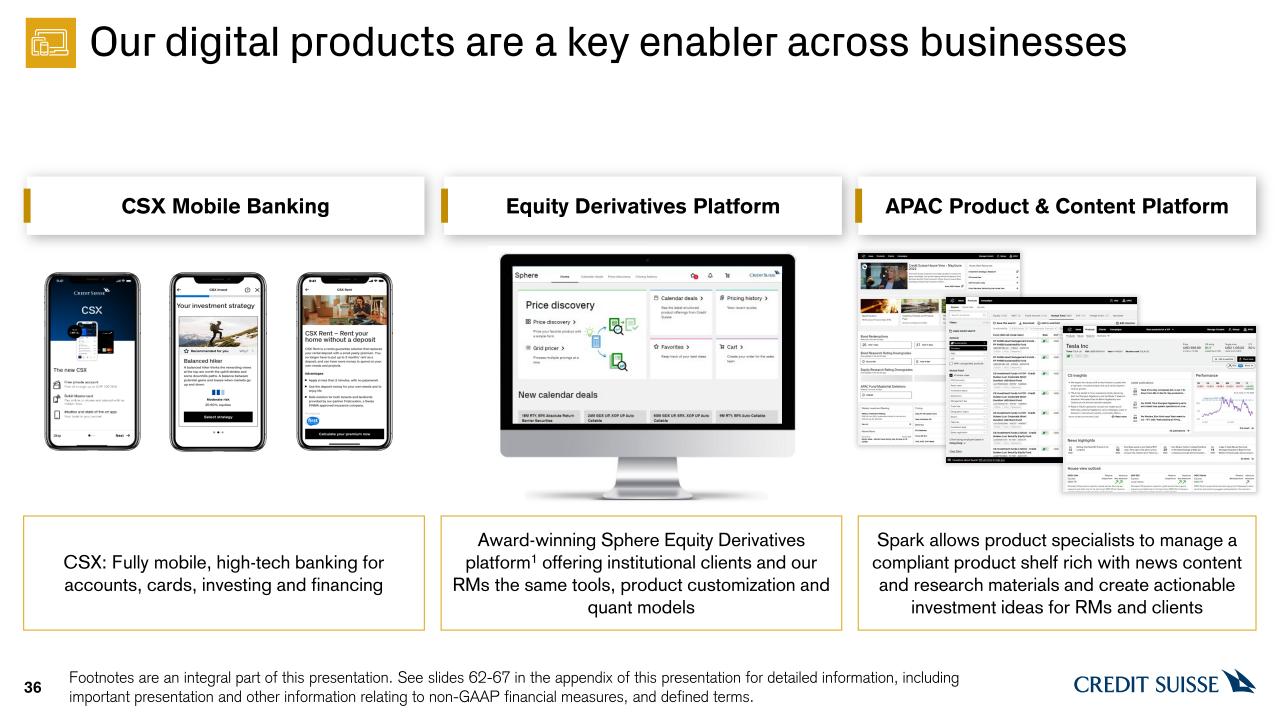

Our digital products are a key enabler across businesses 36 CSX: Fully mobile, high-tech banking for accounts, cards, investing and financing CSX Mobile Banking Award-winning Sphere Equity Derivatives platform1 offering institutional clients and our RMs the same tools, product customization and quant models Equity Derivatives Platform Spark allows product specialists to manage a compliant product shelf rich with news content and research materials and create actionable investment ideas for RMs and clients APAC Product & Content Platform Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

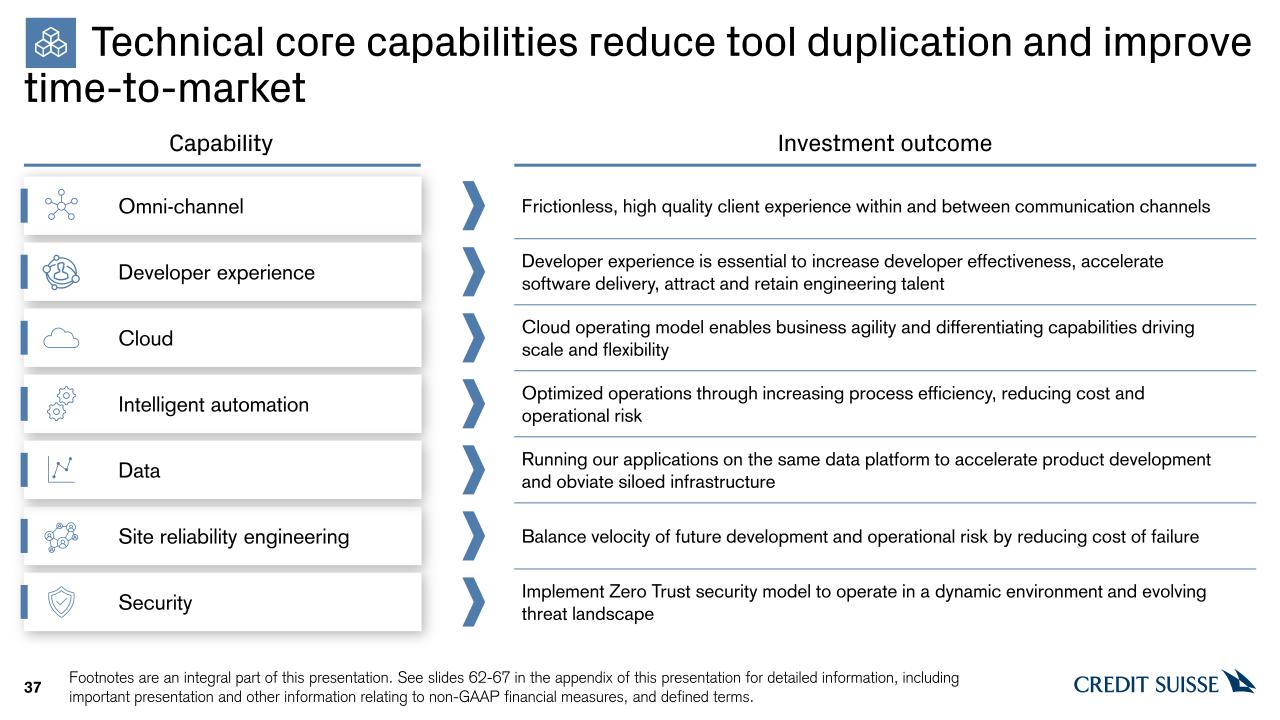

Technical core capabilities reduce tool duplication and improve time-to-market 37 Omni-channel Frictionless, high quality client experience within and between communication channels Developer experience is essential to increase developer effectiveness, accelerate software delivery, attract and retain engineering talent Cloud operating model enables business agility and differentiating capabilities driving scale and flexibility Optimized operations through increasing process efficiency, reducing cost and operational risk Balance velocity of future development and operational risk by reducing cost of failure Running our applications on the same data platform to accelerate product development and obviate siloed infrastructure Implement Zero Trust security model to operate in a dynamic environment and evolving threat landscape Developer experience Cloud Intelligent automation Site reliability engineering Data Security Capability Investment outcome Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

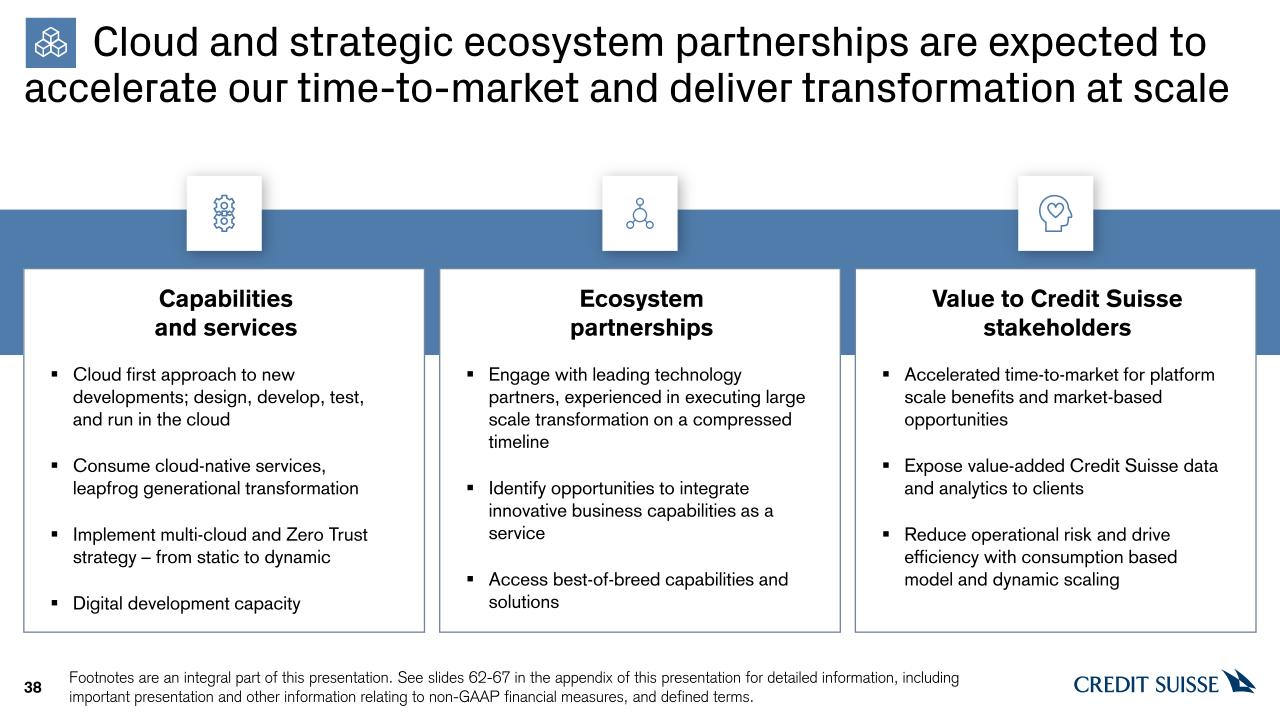

Cloud and strategic ecosystem partnerships are expected to accelerate our time-to-market and deliver transformation at scale 38 Ecosystem partnerships Capabilities and services Value to Credit Suisse stakeholders Cloud first approach to new developments; design, develop, test, and run in the cloudConsume cloud-native services, leapfrog generational transformationImplement multi-cloud and Zero Trust strategy – from static to dynamicDigital development capacity Engage with leading technology partners, experienced in executing large scale transformation on a compressed timelineIdentify opportunities to integrate innovative business capabilities as a serviceAccess best-of-breed capabilities and solutions Accelerated time-to-market for platform scale benefits and market-based opportunitiesExpose value-added Credit Suisse data and analytics to clientsReduce operational risk and drive efficiency with consumption based model and dynamic scaling Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

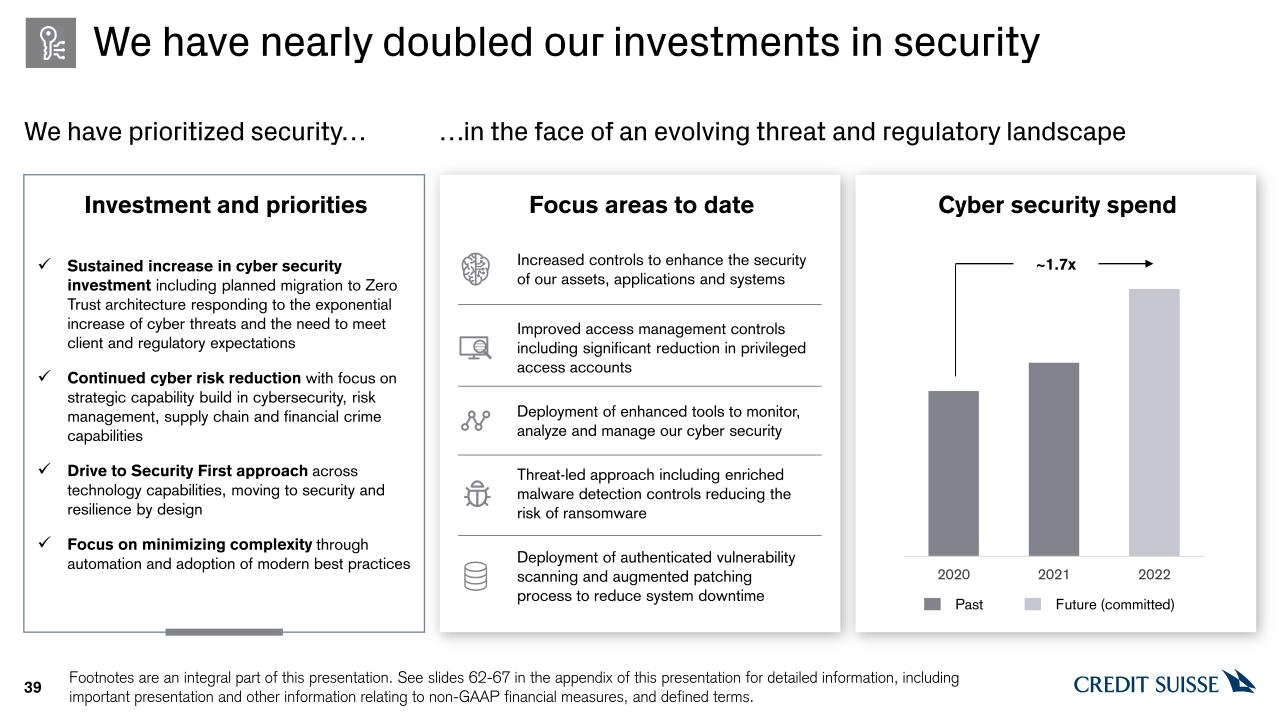

Investment and priorities We have nearly doubled our investments in security 39 We have prioritized security… …in the face of an evolving threat and regulatory landscape Sustained increase in cyber security investment including planned migration to Zero Trust architecture responding to the exponential increase of cyber threats and the need to meet client and regulatory expectationsContinued cyber risk reduction with focus on strategic capability build in cybersecurity, risk management, supply chain and financial crime capabilitiesDrive to Security First approach across technology capabilities, moving to security and resilience by designFocus on minimizing complexity through automation and adoption of modern best practices Focus areas to date Cyber security spend Deployment of authenticated vulnerability scanning and augmented patching process to reduce system downtime Threat-led approach including enriched malware detection controls reducing the risk of ransomware Improved access management controls including significant reduction in privileged access accounts Increased controls to enhance the security of our assets, applications and systems Deployment of enhanced tools to monitor, analyze and manage our cyber security Past Future (committed) Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. ~1.7x

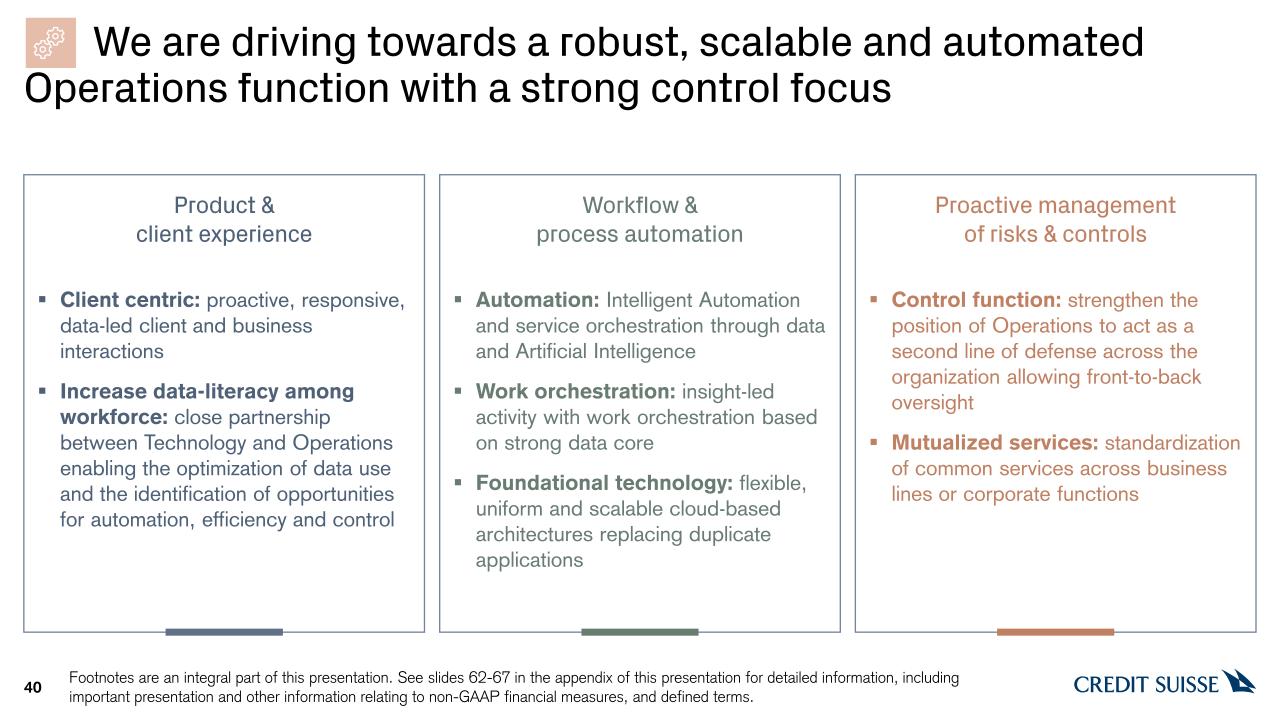

We are driving towards a robust, scalable and automated Operations function with a strong control focus 40 Product & client experienceClient centric: proactive, responsive, data-led client and business interactionsIncrease data-literacy among workforce: close partnership between Technology and Operations enabling the optimization of data use and the identification of opportunities for automation, efficiency and control Workflow & process automationAutomation: Intelligent Automation and service orchestration through data and Artificial IntelligenceWork orchestration: insight-led activity with work orchestration based on strong data coreFoundational technology: flexible, uniform and scalable cloud-based architectures replacing duplicate applications Proactive management of risks & controlsControl function: strengthen the position of Operations to act as a second line of defense across the organization allowing front-to-back oversight Mutualized services: standardization of common services across business lines or corporate functions Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

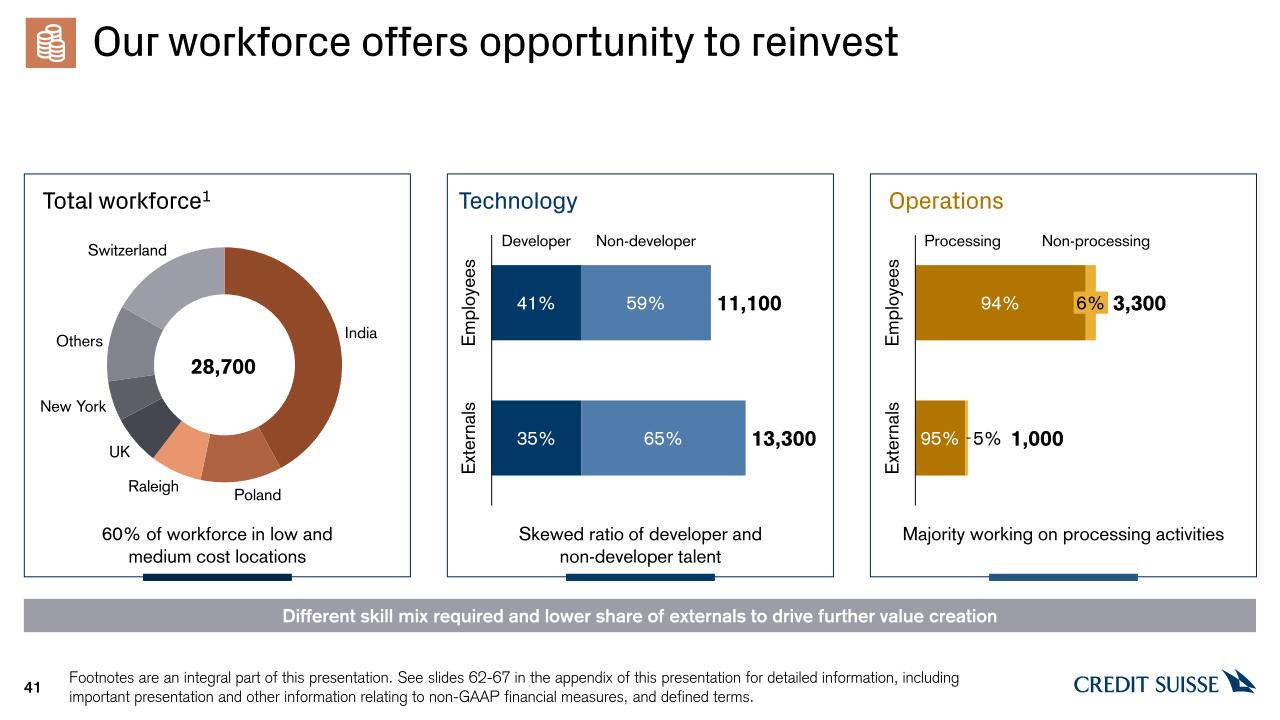

41 India Poland Others Raleigh Switzerland UK New York 28,700 60% of workforce in low and medium cost locations Employees 35% 59% 65% 41% 11,100 Externals Developer Non-developer 13,300 Processing 6% Externals 94% Employees 5% Non-processing 1,000 95% 3,300 Skewed ratio of developer and non-developer talent Majority working on processing activities Different skill mix required and lower share of externals to drive further value creation Total workforce1 Technology Operations Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Our workforce offers opportunity to reinvest

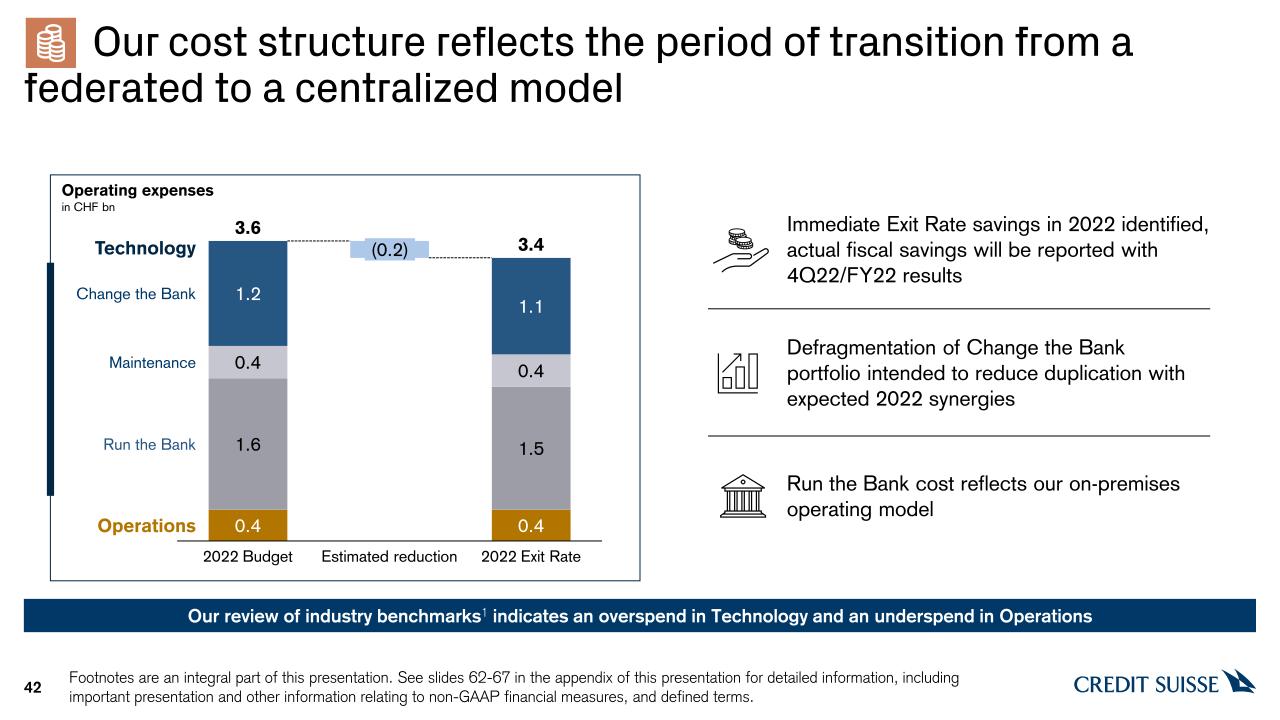

42 Our review of industry benchmarks1 indicates an overspend in Technology and an underspend in Operations Run the Bank Estimated reduction 1.2 0.4 1.1 2022 Budget 0.4 1.6 Maintenance (0.2) 0.4 0.4 1.5 2022 Exit Rate Change the Bank Operations 3.6 3.4 Technology Operating expenses in CHF bn Run the Bank cost reflects our on-premises operating model Immediate Exit Rate savings in 2022 identified, actual fiscal savings will be reported with 4Q22/FY22 results Defragmentation of Change the Bank portfolio intended to reduce duplication with expected 2022 synergies Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Our cost structure reflects the period of transition from a federated to a centralized model

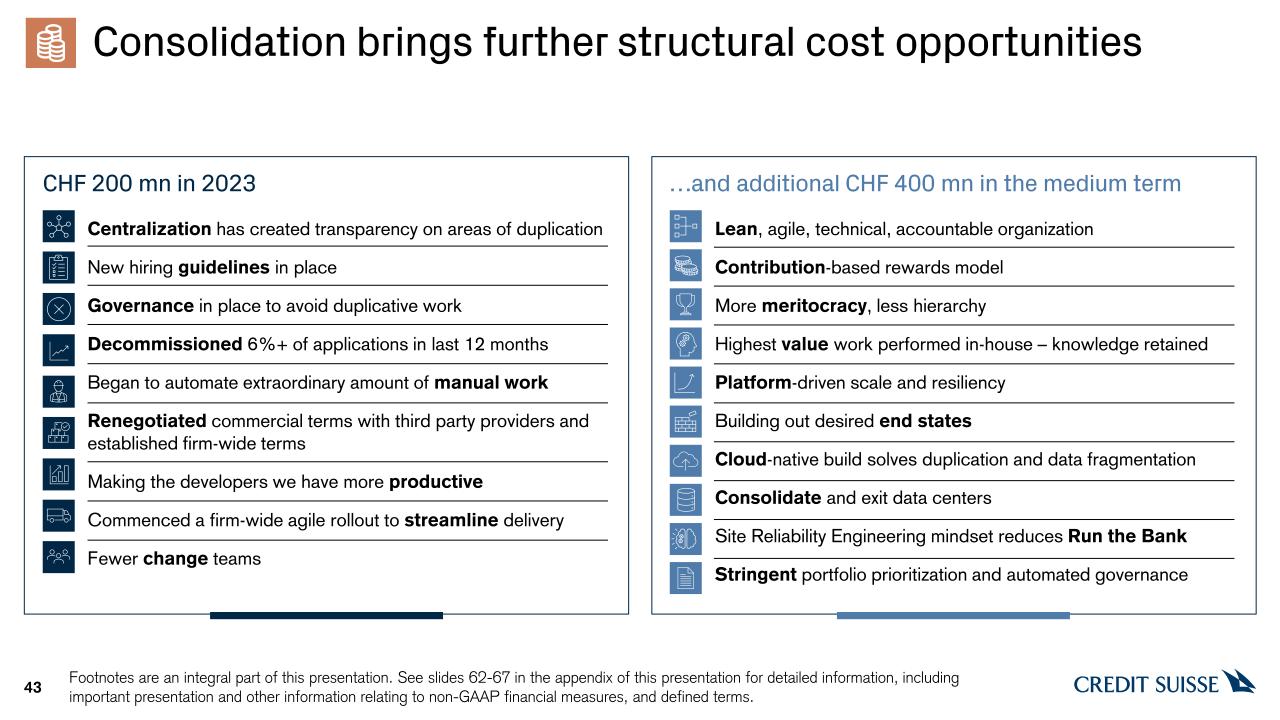

Centralization has created transparency on areas of duplicationNew hiring guidelines in placeGovernance in place to avoid duplicative workDecommissioned 6%+ of applications in last 12 monthsBegan to automate extraordinary amount of manual workRenegotiated commercial terms with third party providers and established firm-wide termsMaking the developers we have more productiveCommenced a firm-wide agile rollout to streamline delivery Fewer change teams 43 CHF 200 mn in 2023 Lean, agile, technical, accountable organizationContribution-based rewards model More meritocracy, less hierarchyHighest value work performed in-house – knowledge retainedPlatform-driven scale and resiliencyBuilding out desired end statesCloud-native build solves duplication and data fragmentationConsolidate and exit data centersSite Reliability Engineering mindset reduces Run the BankStringent portfolio prioritization and automated governance …and additional CHF 400 mn in the medium term Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Consolidation brings further structural cost opportunities

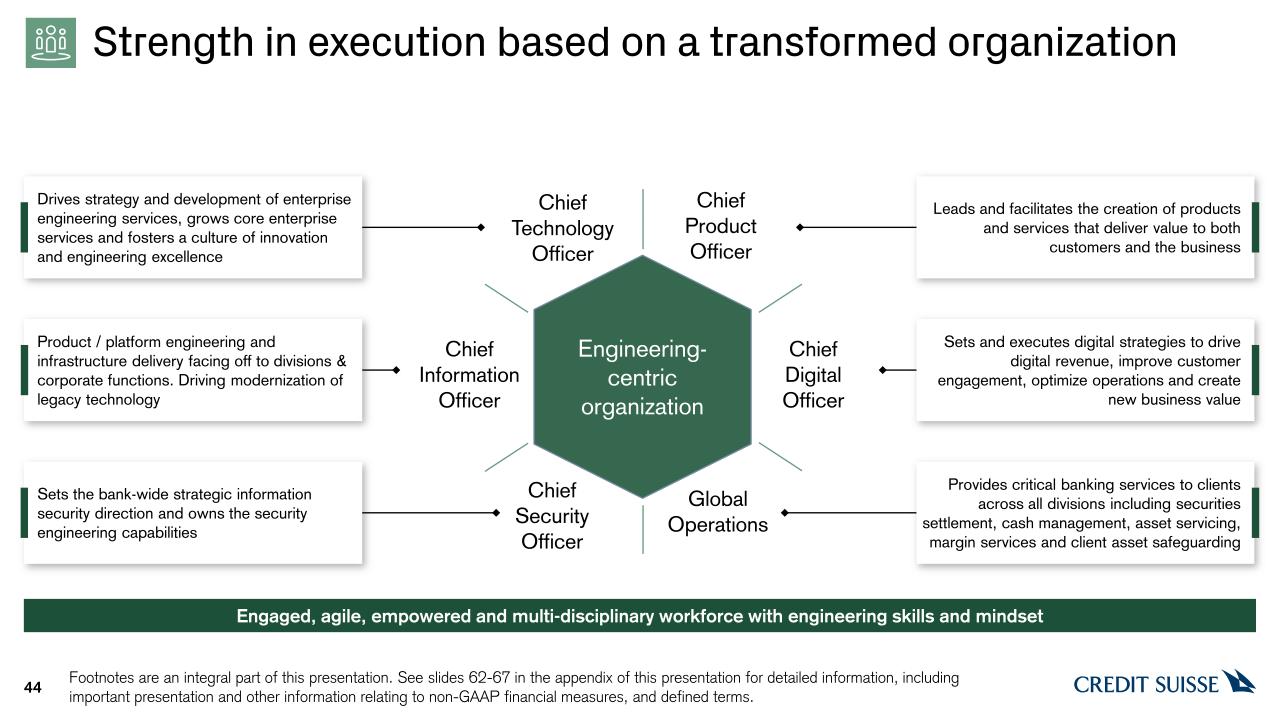

Strength in execution based on a transformed organization 44 Engineering- centric organization Chief Technology Officer Chief Product Officer Chief Digital Officer Chief Information Officer Chief Security Officer Global Operations Drives strategy and development of enterprise engineering services, grows core enterprise services and fosters a culture of innovation and engineering excellence Product / platform engineering and infrastructure delivery facing off to divisions & corporate functions. Driving modernization of legacy technology Sets the bank-wide strategic information security direction and owns the security engineering capabilities Engaged, agile, empowered and multi-disciplinary workforce with engineering skills and mindset Leads and facilitates the creation of products and services that deliver value to both customers and the business Sets and executes digital strategies to drive digital revenue, improve customer engagement, optimize operations and create new business value Provides critical banking services to clients across all divisions including securities settlement, cash management, asset servicing, margin services and client asset safeguarding Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

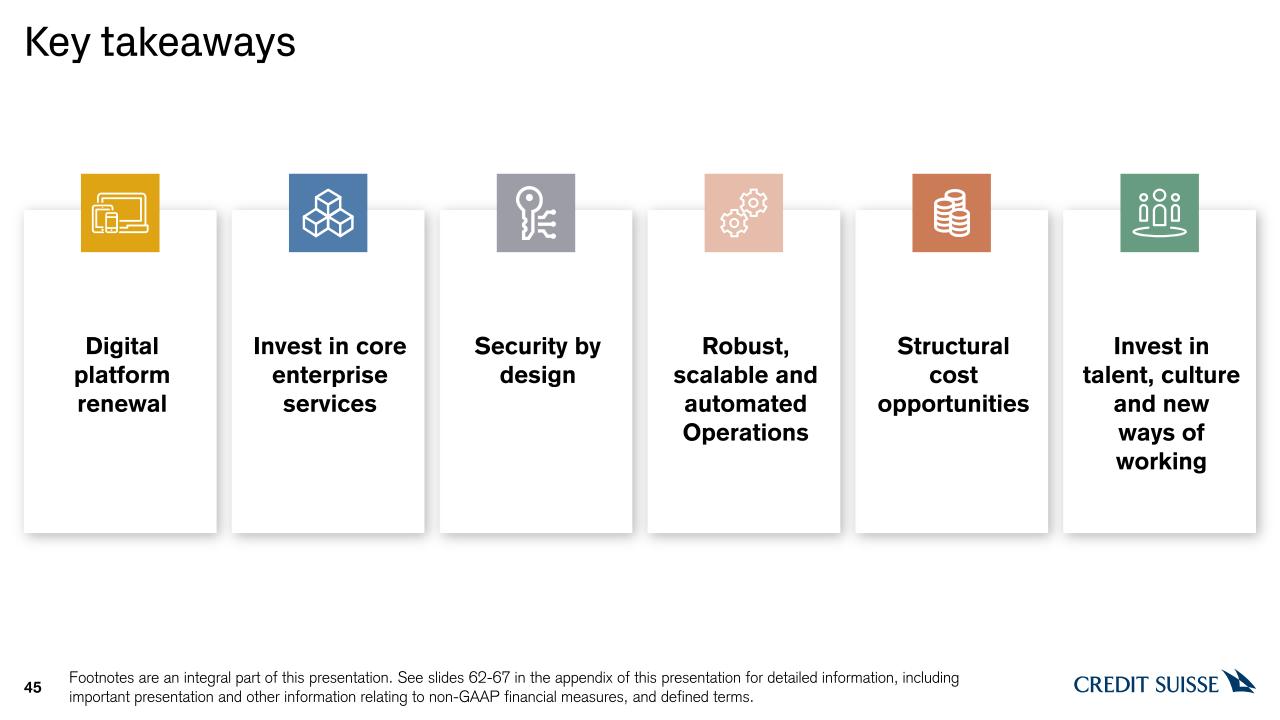

Key takeaways 45 Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Structural cost opportunities Invest in talent, culture and new ways of working Security by design Robust, scalable and automated Operations Digital platform renewal Invest in core enterprise services

Wealth Management Driving sustainable growth Francesco De Ferrari, CEO Wealth ManagementJune 28, 2022

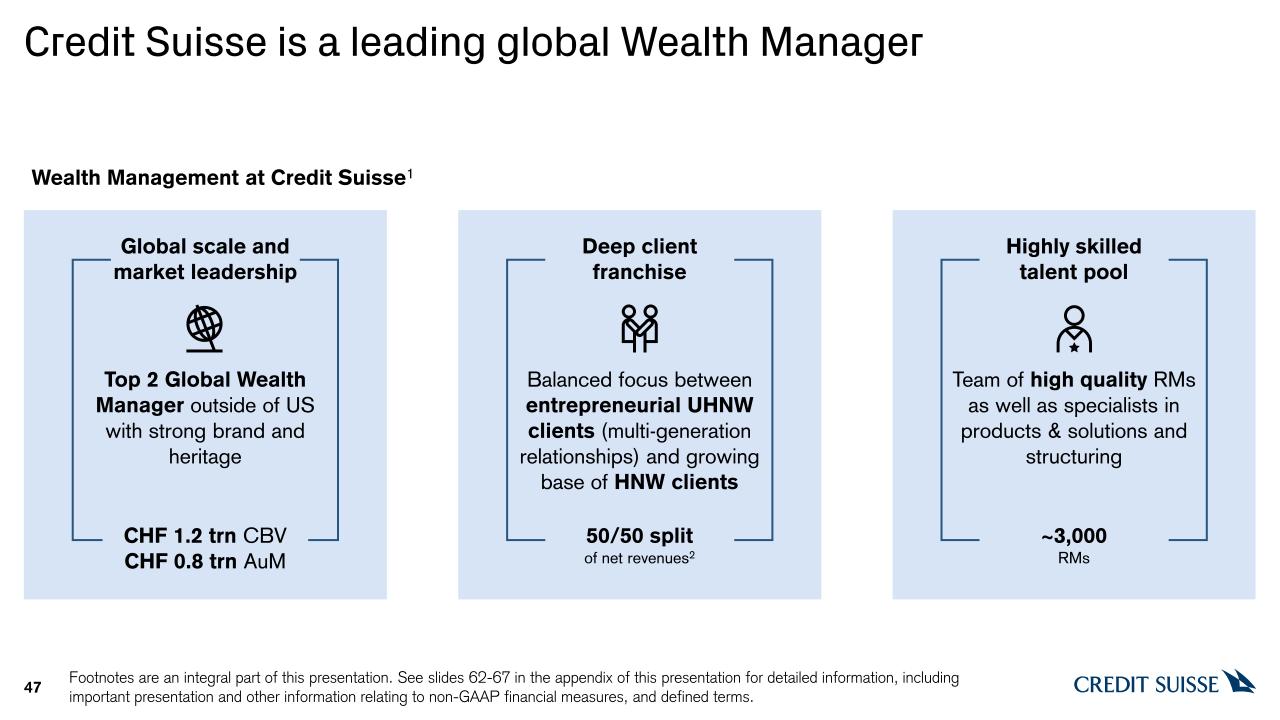

47 Credit Suisse is a leading global Wealth Manager Top 2 Global Wealth Manager outside of US with strong brand and heritage Global scale and market leadership CHF 1.2 trn CBVCHF 0.8 trn AuM Balanced focus betweenentrepreneurial UHNW clients (multi-generation relationships) and growing base of HNW clients Deep client franchise 50/50 split of net revenues2 Team of high quality RMs as well as specialists in products & solutions and structuring Highly skilled talent pool ~3,000 RMs Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Wealth Management at Credit Suisse1

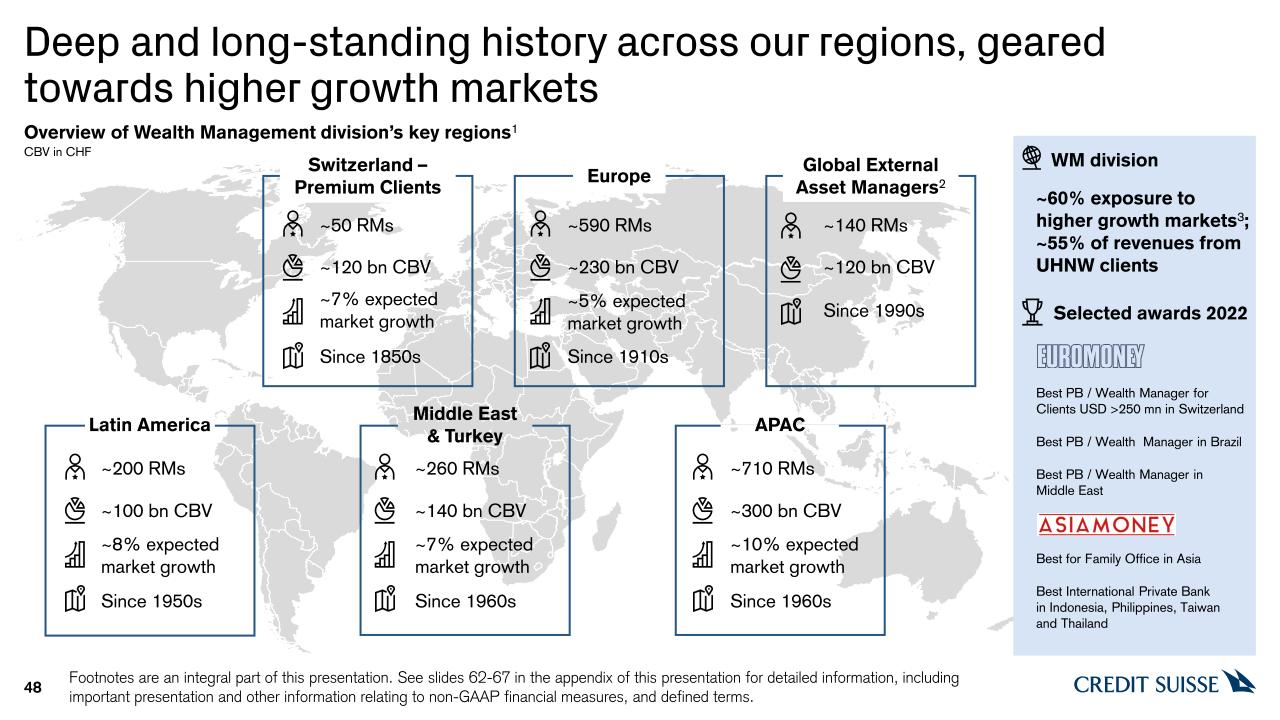

48 Deep and long-standing history across our regions, geared towards higher growth markets Switzerland – Premium Clients Europe Latin America Middle East & Turkey APAC ~140 RMs ~120 bn CBV Since 1990s Global External Asset Managers2 Best PB / Wealth Manager in Brazil Best for Family Office in Asia Best PB / Wealth Manager in Middle East Best International Private Bank in Indonesia, Philippines, Taiwan and Thailand Best PB / Wealth Manager for Clients USD >250 mn in Switzerland ~60% exposure to higher growth markets3; ~55% of revenues from UHNW clients Selected awards 2022 WM division Overview of Wealth Management division’s key regions1CBV in CHF ~710 RMs ~300 bn CBV Since 1960s ~200 RMs ~100 bn CBV Since 1950s ~260 RMs ~140 bn CBV Since 1960s ~50 RMs ~120 bn CBV Since 1850s ~590 RMs ~230 bn CBV Since 1910s ~7% expected market growth ~8% expectedmarket growth ~7% expectedmarket growth ~10% expectedmarket growth ~5% expected market growth Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

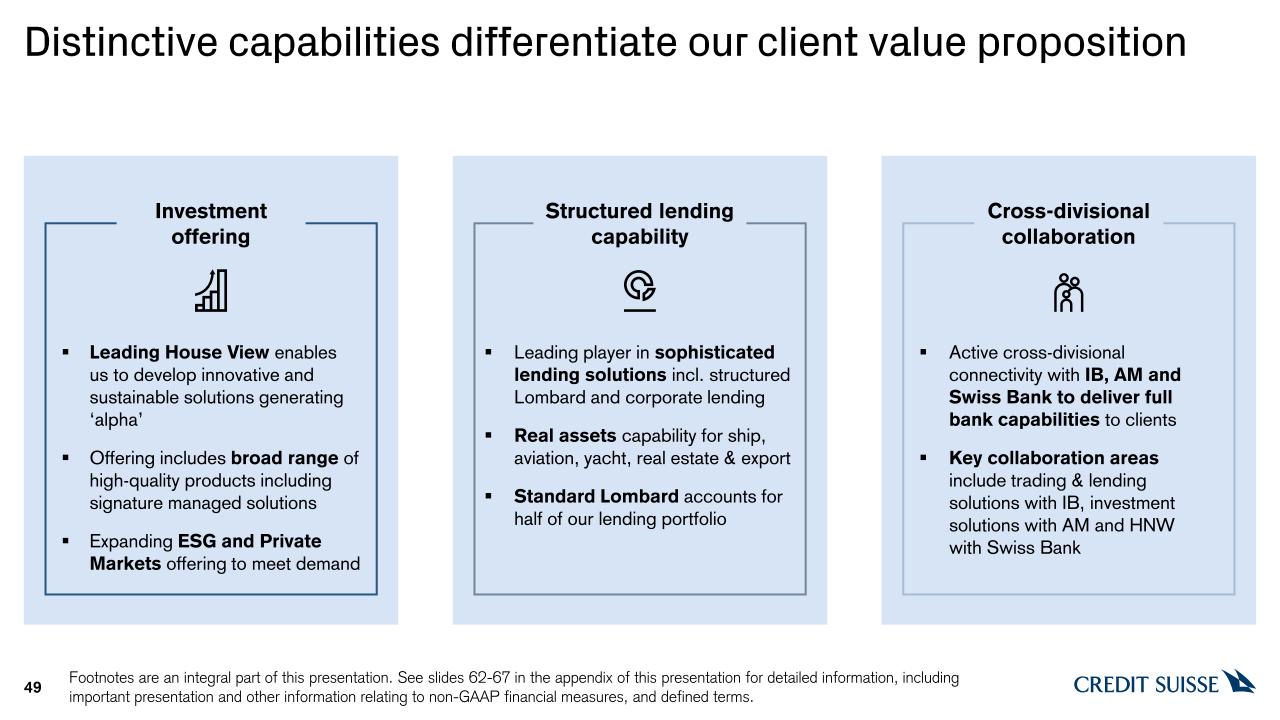

Distinctive capabilities differentiate our client value proposition 49 Leading House View enables us to develop innovative and sustainable solutions generating ‘alpha’Offering includes broad range of high-quality products including signature managed solutions Expanding ESG and Private Markets offering to meet demand Investment offering Structured lending capability Cross-divisional collaboration Leading player in sophisticated lending solutions incl. structured Lombard and corporate lendingReal assets capability for ship, aviation, yacht, real estate & exportStandard Lombard accounts for half of our lending portfolio Active cross-divisional connectivity with IB, AM and Swiss Bank to deliver full bank capabilities to clientsKey collaboration areas include trading & lending solutions with IB, investment solutions with AM and HNW with Swiss Bank Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

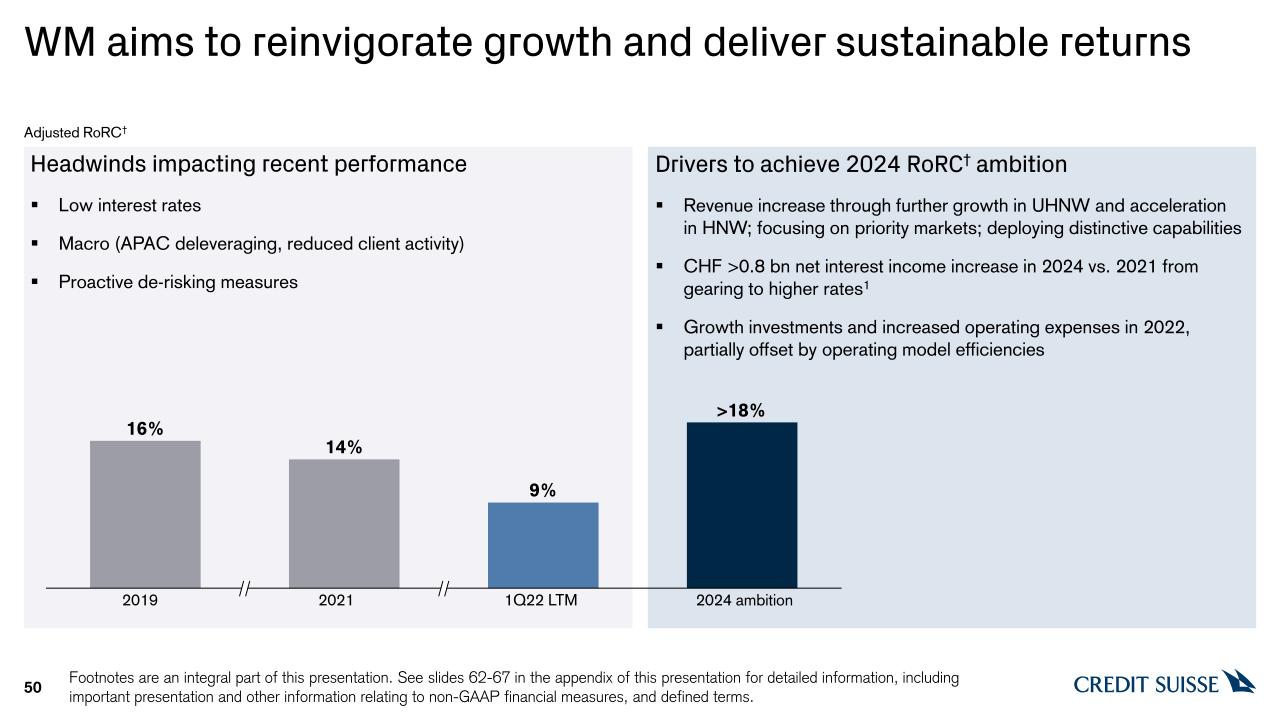

WM aims to reinvigorate growth and deliver sustainable returns 50 Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Drivers to achieve 2024 RoRC† ambitionRevenue increase through further growth in UHNW and acceleration in HNW; focusing on priority markets; deploying distinctive capabilitiesCHF >0.8 bn net interest income increase in 2024 vs. 2021 from gearing to higher rates1Growth investments and increased operating expenses in 2022, partially offset by operating model efficiencies Adjusted RoRC† >18% 2019 2021 1Q22 LTM 2024 ambition Headwinds impacting recent performance Low interest ratesMacro (APAC deleveraging, reduced client activity)Proactive de-risking measures

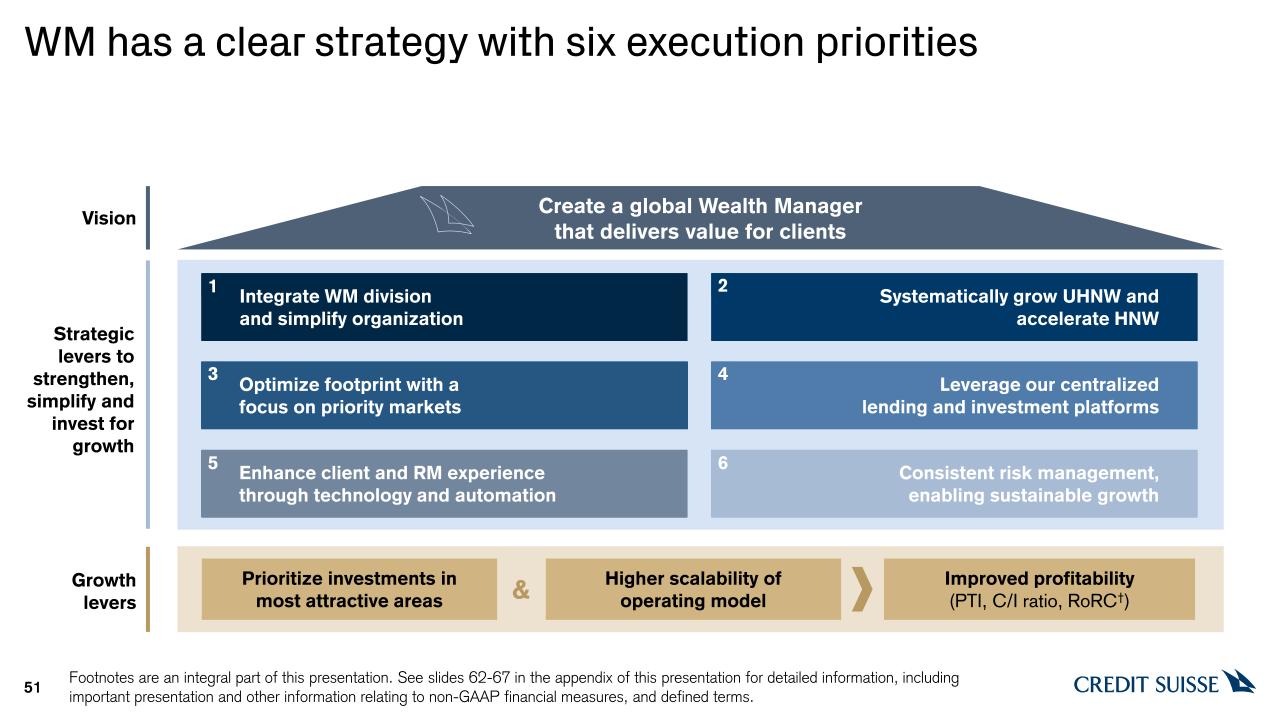

Enhance client and RM experiencethrough technology and automation WM has a clear strategy with six execution priorities 51 Higher scalability of operating model Improved profitability(PTI, C/I ratio, RoRC†) & Growthlevers Prioritize investments in most attractive areas Integrate WM division and simplify organization Systematically grow UHNW andaccelerate HNW Leverage our centralizedlending and investment platforms Optimize footprint with afocus on priority markets Consistent risk management,enabling sustainable growth Strategic levers to strengthen, simplify and invest for growth Create a global Wealth Manager that delivers value for clients Vision 1 2 5 6 3 4 Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

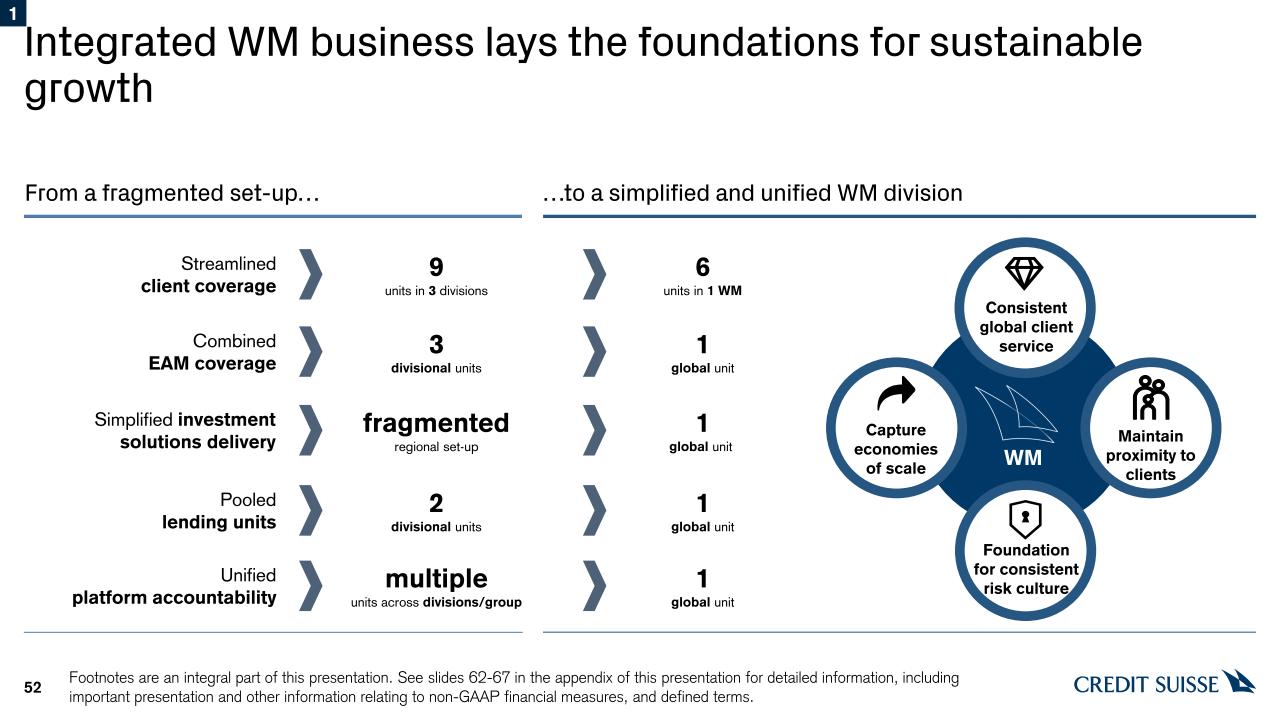

9units in 3 divisions Streamlinedclient coverage 6units in 1 WM Integrated WM business lays the foundations for sustainable growth 52 From a fragmented set-up… Capture economiesof scale Maintain proximity to clients WM …to a simplified and unified WM division CombinedEAM coverage 3divisional units 1global unit Simplified investmentsolutions delivery 1global unit fragmentedregional set-up Pooled lending units 1global unit 2divisional units Unifiedplatform accountability 1global unit multipleunits across divisions/group Consistent global client service Foundation for consistent risk culture 1 Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

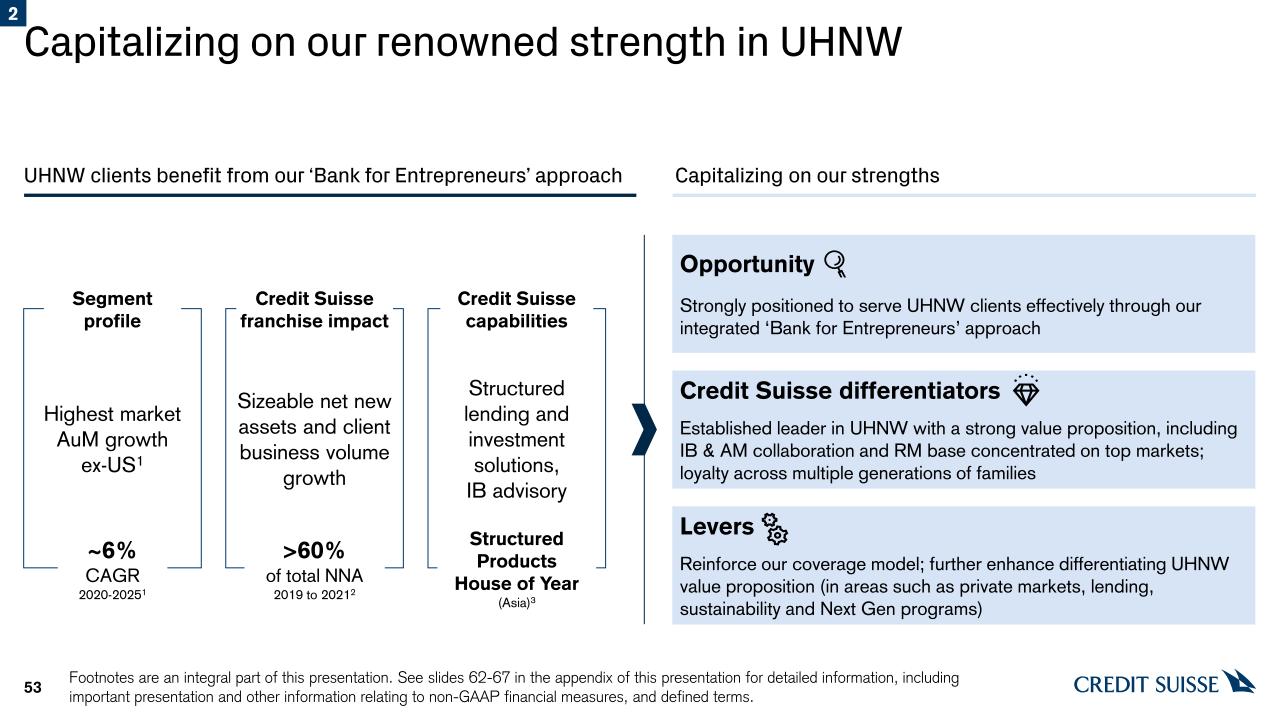

Capitalizing on our renowned strength in UHNW 53 UHNW clients benefit from our ‘Bank for Entrepreneurs’ approach Capitalizing on our strengths Highest market AuM growth ex-US1 Sizeable net new assets and client business volume growth Structured lending and investment solutions,IB advisory Opportunity Strongly positioned to serve UHNW clients effectively through our integrated ‘Bank for Entrepreneurs’ approach Credit Suisse differentiatorsEstablished leader in UHNW with a strong value proposition, including IB & AM collaboration and RM base concentrated on top markets; loyalty across multiple generations of families LeversReinforce our coverage model; further enhance differentiating UHNW value proposition (in areas such as private markets, lending, sustainability and Next Gen programs) Segment profile Credit Suisse franchise impact Credit Suissecapabilities ~6% CAGR2020-20251 >60%of total NNA2019 to 20212 Structured Products House of Year (Asia)3 2 Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

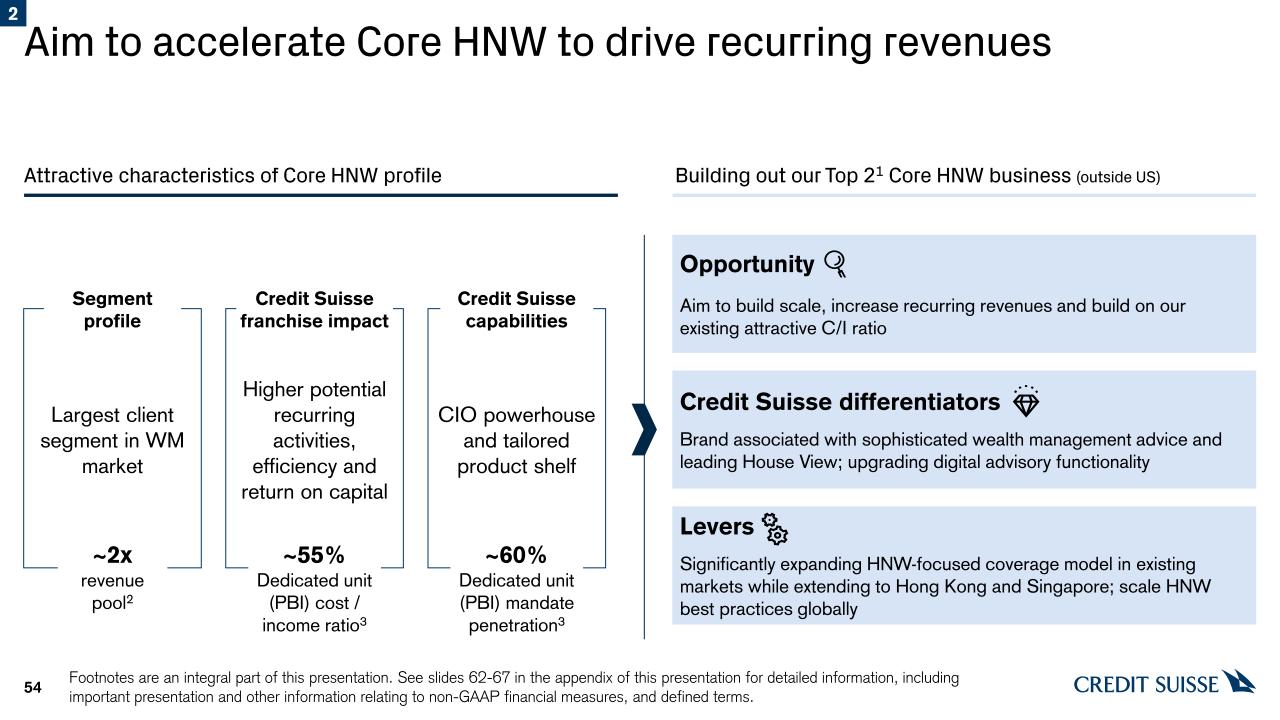

Aim to accelerate Core HNW to drive recurring revenues 54 Opportunity Aim to build scale, increase recurring revenues and build on our existing attractive C/I ratio Credit Suisse differentiatorsBrand associated with sophisticated wealth management advice and leading House View; upgrading digital advisory functionality LeversSignificantly expanding HNW-focused coverage model in existing markets while extending to Hong Kong and Singapore; scale HNW best practices globally 2 Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms. Largest client segment in WM market Higher potential recurring activities, efficiency and return on capital CIO powerhouse and tailored product shelf ~2x revenue pool2 ~55%Dedicated unit (PBI) cost / income ratio3 ~60%Dedicated unit (PBI) mandate penetration3 Segment profile Credit Suisse franchise impact Credit Suissecapabilities Attractive characteristics of Core HNW profile Building out our Top 21 Core HNW business (outside US)

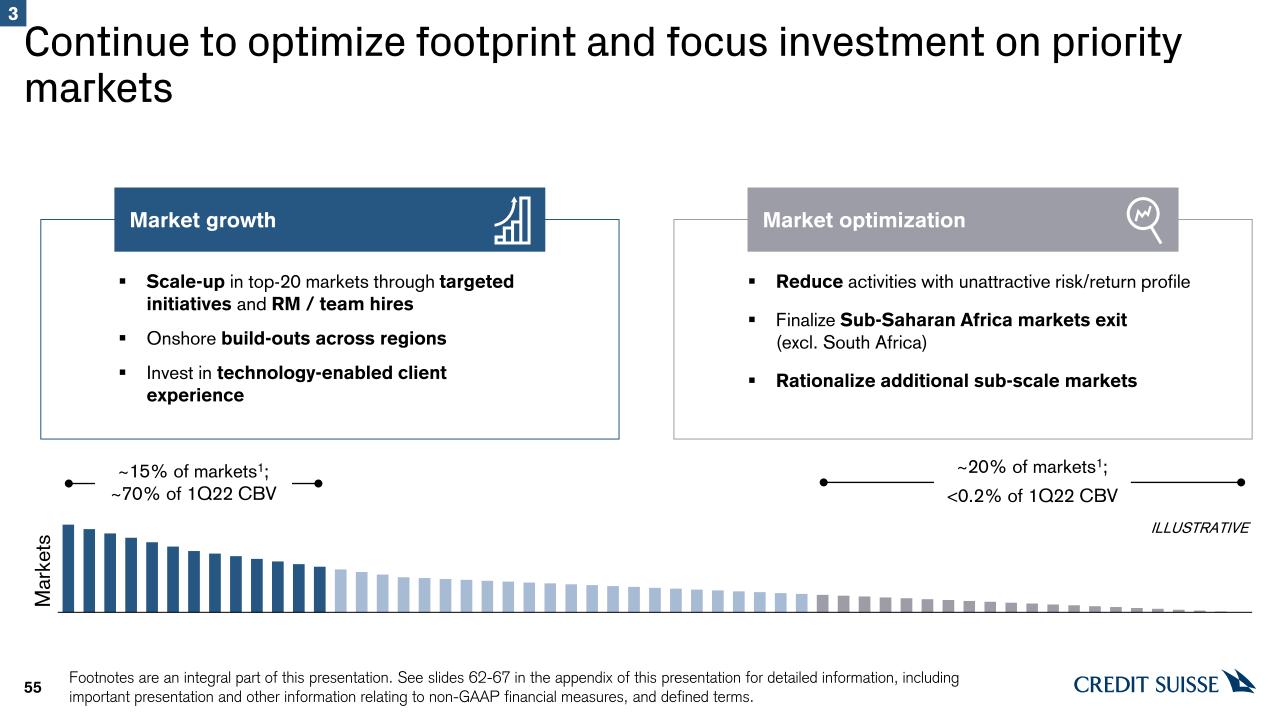

55 Continue to optimize footprint and focus investment on priority markets Reduce activities with unattractive risk/return profileFinalize Sub-Saharan Africa markets exit(excl. South Africa)Rationalize additional sub-scale markets Scale-up in top-20 markets through targeted initiatives and RM / team hires Onshore build-outs across regionsInvest in technology-enabled client experience Markets ~15% of markets1;~70% of 1Q22 CBV ~20% of markets1;<0.2% of 1Q22 CBV Market growth Market optimization 3 ILLUSTRATIVE Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

Aim to leverage our centralized lending and investment platforms and drive recurring revenue growth 56 Solutions Systematically deploying our House View to cater for client needs Further integrating ESG into client advisory and investment processAccelerating Private Markets sales through our single center of competence Key recurring revenue growth levers 2024 ambitions Leveraging our centralized capability while maintaining focus on managing credit portfolio and operational riskDeploying consistent product offering across regions Investments Lending Mandate penetration1 >35% Private Markets2 Double AuM 4 Sustainable investing Fully embed in advisory process Credit Volume growth Mid- to high-single digit Sustainable Finance Support CS Group in growing sustainable finance Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

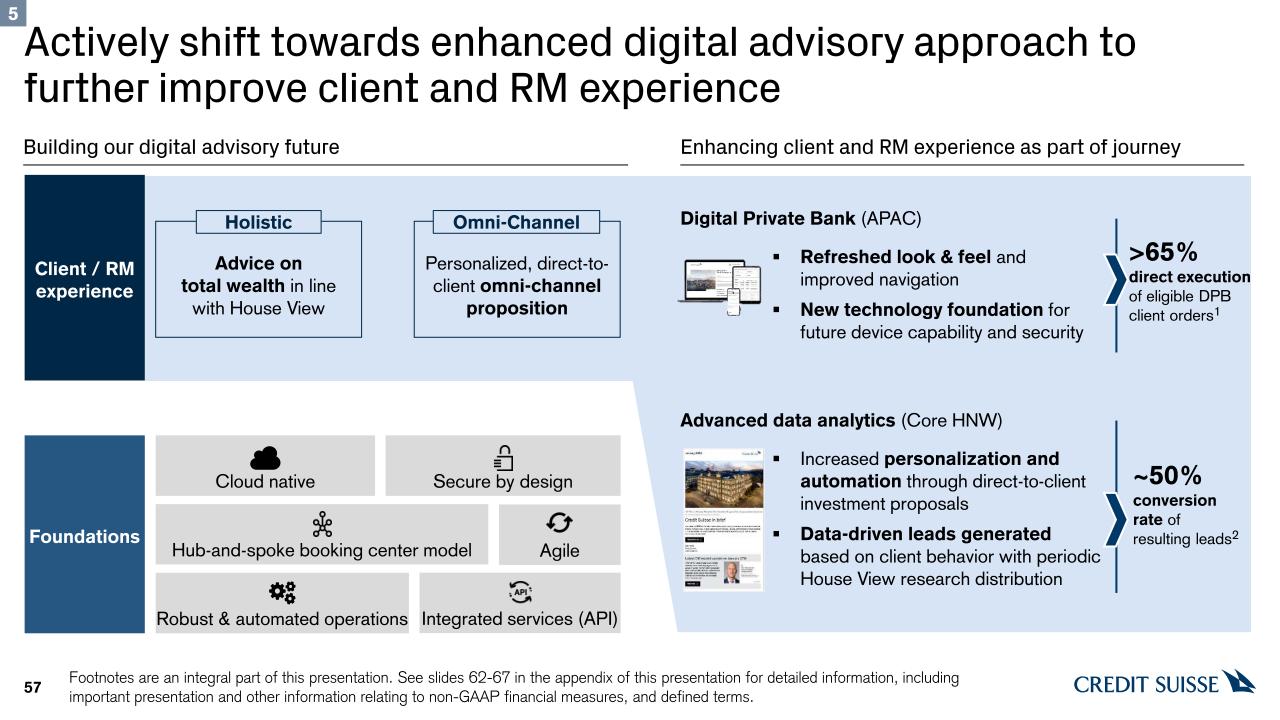

~50% conversion rate of resulting leads2 Agile Actively shift towards enhanced digital advisory approach to further improve client and RM experience 57 Foundations Cloud native Hub-and-spoke booking center model Robust & automated operations Building our digital advisory future Enhancing client and RM experience as part of journey Secure by design Integrated services (API) Personalized, direct-to-client omni-channel proposition Omni-Channel Advice on total wealth in line with House View Holistic Digital Private Bank (APAC)Refreshed look & feel and improved navigation New technology foundation for future device capability and security >65% direct execution of eligible DPB client orders1 Advanced data analytics (Core HNW)Increased personalization and automation through direct-to-client investment proposalsData-driven leads generated based on client behavior with periodic House View research distribution Client / RM experience 5 Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

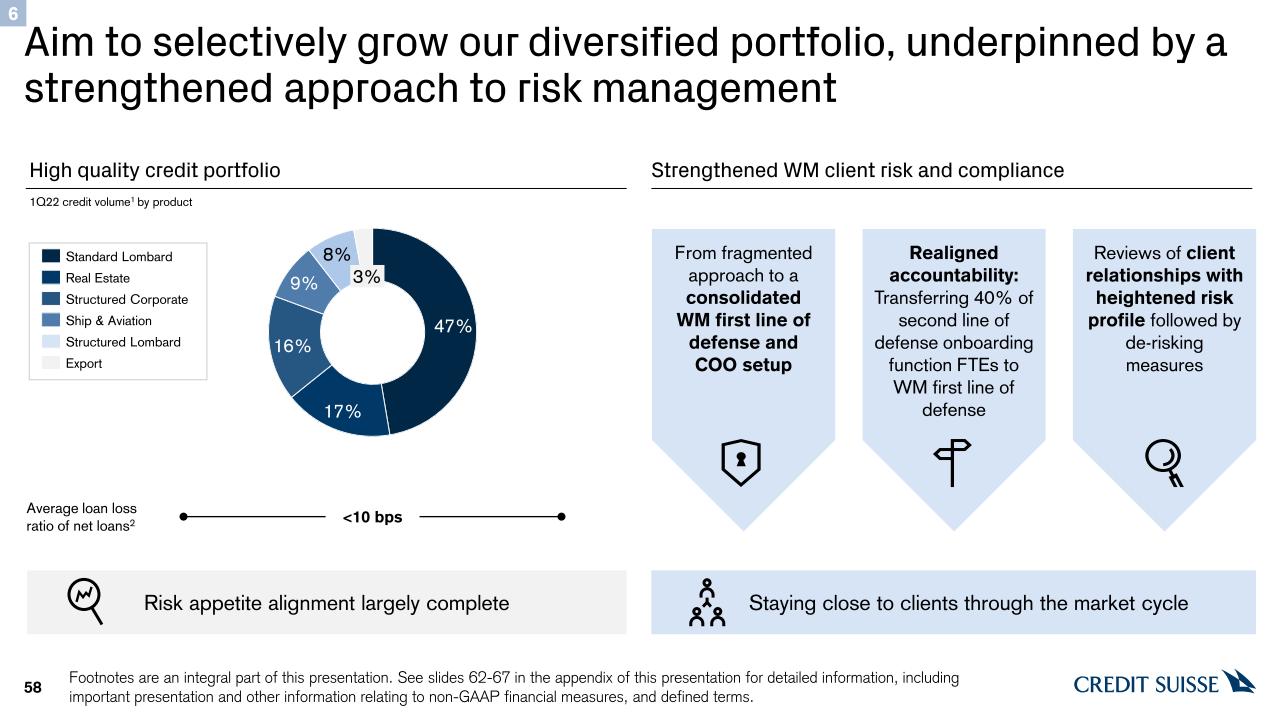

Aim to selectively grow our diversified portfolio, underpinned by a strengthened approach to risk management 58 Average loan loss ratio of net loans2 1Q22 credit volume1 by product <10 bps High quality credit portfolio 3% Standard Lombard Real Estate Structured Corporate Ship & Aviation Structured Lombard Export Strengthened WM client risk and compliance Staying close to clients through the market cycle From fragmented approach to a consolidated WM first line of defense and COO setup Realigned accountability: Transferring 40% of second line of defense onboarding function FTEs to WM first line of defense Reviews of client relationships with heightened risk profile followed by de-risking measures 6 Risk appetite alignment largely complete Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

Wealth Management is focused on driving sustainable growth 59 We have a leading and distinctive franchise We have set the foundations of our global business and have a strong team in place We have a clear strategy and execution plan Footnotes are an integral part of this presentation. See slides 62-67 in the appendix of this presentation for detailed information, including important presentation and other information relating to non-GAAP financial measures, and defined terms.

Appendix

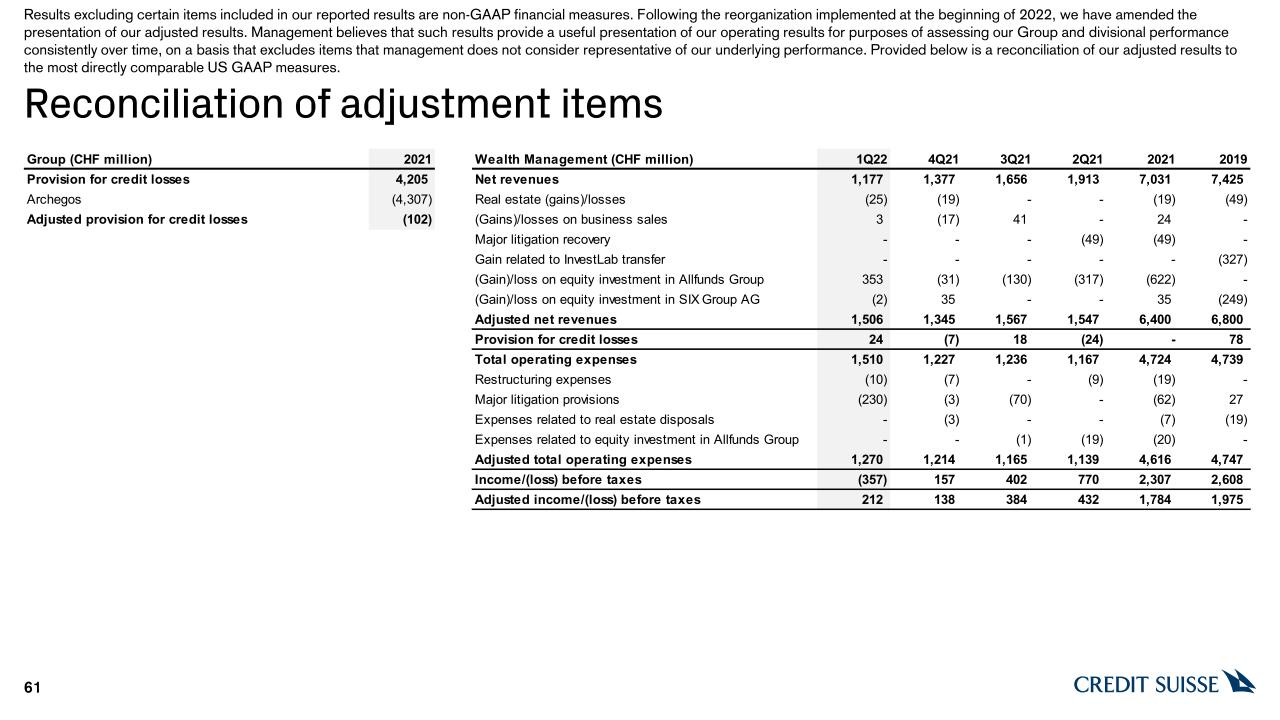

61 Results excluding certain items included in our reported results are non-GAAP financial measures. Following the reorganization implemented at the beginning of 2022, we have amended the presentation of our adjusted results. Management believes that such results provide a useful presentation of our operating results for purposes of assessing our Group and divisional performance consistently over time, on a basis that excludes items that management does not consider representative of our underlying performance. Provided below is a reconciliation of our adjusted results to the most directly comparable US GAAP measures. Reconciliation of adjustment items