As filed with the Securities and Exchange Commission on June 30, 2011

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

____________

FORM 20-F

(Mark One) | |

| o | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2010 |

| OR | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| o | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 001-34983

PROMOTORA DE INFORMACIONES, S.A.

(Exact Name of Registrant as Specified in Its Charter)

PROMOTER OF INFORMATION, S.A.

(Translation of Registrant’s name into English)

KINGDOM OF SPAIN

(Jurisdiction of incorporation or organization)

Gran Vía, 32

28013 Madrid, Spain

(Address of principal executive offices)

Iñigo Dago Elorza

General Counsel

Gran Vía, 32

28013 Madrid, Spain

Tel: +34 (91) 330 10 00

Fax: +34 (91) 330 10 70

(Name, Telephone, E-Mail and/or Facsimile number and Address of Company Contact Person)

_____________

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

| American Depositary Shares, each representing four (4) Class A ordinary shares | New York Stock Exchange |

Class A ordinary shares, nominal value €0.10 per share* | |

| American Depositary Shares, each representing four (4) Class B convertible non-voting shares | New York Stock Exchange |

Class B convertible non-voting shares, nominal value €0.10 per share* | |

| * Listed not for trading or quotation purposes, but only in connection with the registration of the American Depositary Shares (“ADSs”) pursuant to the requirements of the Securities and Exchange Commission. | |

Securities for which there is a reporting obligation pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Class A Ordinary Shares: 443,991,020 Class B convertible non-voting shares: 402,987,000

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No ý

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o Non-accelerated filer ý

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

US GAAP o International Financial Reporting Standards as Issued by the International Accounting Standards Board ý Other o

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 o Item 18 ý

If this is an annual report indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No ý

Page

| PART I | ||

| Item 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISORS | 1 |

| A. | 1 | |

| B. | 1 | |

| C. | 1 | |

| Item 2. | 1 | |

| Item 3. | 1 | |

| A. | 1 | |

| B. | 3 | |

| C. | 3 | |

| D. | 3 | |

| — | 3 | |

| — | 4 | |

| — | 7 | |

| Item 4. | 8 | |

| A. | 8 | |

| B. | 10 | |

| C. | 27 | |

| D. | 27 | |

| Item 4A. | 28 | |

| Item 5. | 28 | |

| A. | 28 | |

| B. | 42 | |

| C. | 46 | |

| D. | 47 | |

| E. | 49 | |

| F. | 49 | |

| Item 6. | 50 | |

| A. | 50 | |

| B. | 56 | |

| C. | 59 | |

| D. | 63 | |

| E. | 63 | |

| Item 7. | 65 | |

| A. | 65 | |

| B. | 68 | |

| C. | 69 | |

| Item 8. | 69 | |

| A. | 69 | |

| B. | 73 | |

| Item 9. | 73 | |

| A. | 73 | |

| B. | 75 | |

| C. | 75 | |

| D. | 75 | |

| E. | 75 | |

| F. | 75 | |

| Item 10. | 75 | |

| A. | 75 | |

| B. | 75 | |

| C. | 83 | |

| D. | 83 | |

| E. | 83 | |

| F. | 86 | |

| G. | 86 | |

| H. | 86 | |

| I. | 87 | |

| Item 11. | 88 | |

| Item 12. | 91 | |

| A. | 91 | |

| B. | 91 | |

| C. | 91 | |

| D. | 91 | |

i

| Item 13. | 93 | |

| Item 14. | 93 | |

| Item 15. | 93 | |

| Item 16. | 93 | |

| Item 16A. | 93 | |

| Item 16B. | 94 | |

| Item 16C. | 94 | |

| Item 16D. | 95 | |

| Item 16E. | 95 | |

| Item 16F. | 95 | |

| Item 16G. | 95 | |

| PART III | ||

| Item 17. | 96 | |

| Item 18. | 96 | |

| Item 19. | 96 | |

CURRENCIES

In this annual report, unless otherwise specified or the context otherwise requires:

| · | ‘‘$,” “US$” and “U.S. dollar” each refer to the United States dollar; and |

| · | ‘‘€,” “EUR” and “euro” each refer to the euro, the single currency established for members of the European Economic and Monetary Union since January 1, 1999. |

IMPORTANT INFORMATION ABOUT GAAP AND NON-GAAP FINANCIAL MEASURES

Our audited financial statements are prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board and referred to in this annual report as “IFRS.”

Adjusted EBITDA, as presented in this annual report, is a supplemental measure of performance that is not required by, or presented in accordance with, IFRS. It is not a measurement of financial performance under IFRS and should not be considered as (i) an alternative to operating or net income or cash flows from operating activities, in each case determined in accordance with IFRS, (ii) an indicator of cash flow or (iii) a measure of liquidity.

We define “Adjusted EBITDA” as profit from operations, as shown on our financial statements, plus asset depreciation expense, plus changes in operating allowances, plus impairment of assets and plus goodwill deterioration. We use Adjusted EBITDA as a financial measure to assess the performance of our businesses. We present Adjusted EBITDA because we believe Adjusted EBITDA is frequently used by securities analysts, investors and other interested parties in evaluating similar issuers, a significant number of which present Adjusted EBITDA (or a similar measure) when reporting their results.

Although we use Adjusted EBITDA as a financial measure to assess the performance of our businesses, the use of Adjusted EBITDA has important limitations, including that Adjusted EBITDA:

● does not represent funds available for dividends, reinvestment or other discretionary uses; |

● does not reflect cash outlays for capital expenditures or contractual commitments; |

● does not reflect changes in, or cash requirements for, working capital; |

● does not reflect the interest expense or the cash requirements necessary to service interest or principal payments on indebtedness; |

● does not reflect income tax expense or the cash necessary to pay income taxes; |

● excludes depreciation and amortization and, although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future; |

● does not reflect cash requirements for such replacements; and |

● may be calculated differently by other companies, including other companies in our industry, limiting its usefulness as a comparative measure. |

Because of these limitations, Adjusted EBITDA should not be considered as a measure of discretionary cash available to us to invest in the growth of our businesses. We compensate for these limitations by relying primarily on IFRS results and using Adjusted EBITDA measures only supplementally. See “Operating and Financial Review and Prospects” and the consolidated financial statements contained elsewhere in this annual report.

We also occasionally uses “EBIT” as another name for the IFRS measure profit from operations, as shown in our audited financial statements and accompanying notes.

INDUSTRY AND MARKET DATA

In this annual report, we rely on and refer to information and statistics regarding market shares in the sectors in which we compete and other industry data. We obtained this information and statistics from third-party sources, such as independent industry publications, government publications or reports by market research firms, such as Zenith Optimedia, TNS Sofres and Marktest. We have supplemented this information where necessary with information from various other third-party sources, discussions with our customers and our own internal estimates taking into account publicly available information about other industry participants and our management’s best view as to information that is not publicly available. We believe that these third-party sources are reliable, but we have not independently verified the information and statistics obtained from them.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains statements that constitute forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. The forward-looking statements in this annual report can be identified, in some instances, by the use of words such as “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions, but the absence of these words does not mean that a statement is not forward-looking. These statements appear in a number of places in this annual report including, without limitation, certain statements made in “Item 3. Key Information—Risk Factors,” “Item 4. Information about Prisa,” “Item 5. Operating and Financial Review and Prospects” and “Item 11. Quantitative and Qualitative Disclosures About Market Risk” and include statements regarding our intent, belief or current expectations with respect to, among other things:

● the effect on our results of operations of competition in the markets in which we operate; |

● trends affecting our financial condition or results of operations; |

● acquisitions or investments that we may make in the future; |

● our capital expenditures plan; |

● our ability to repay debt with estimated future cash flows; |

● supervision and regulation of the sectors where we have significant operations; |

● our strategic partnerships; and |

● the potential for growth and competition in current and anticipated areas of our business. |

Such forward-looking statements are not guarantees of future performance and involve numerous risks and uncertainties, and actual results may differ materially from those anticipated in the forward-looking statements as a result of various factors. The risks and uncertainties involved in our business that could affect the matters referred to in such forward-looking statements include but are not limited to:

● changes in general economic, business or political conditions in the domestic or international markets (particularly in Latin America) in which we operate or have material investments that may affect demand for our services; |

● changes in currency exchange rates, interest rates or in credit risk in our treasury investments or in some of our financial transactions; |

● general economic conditions in the countries in which we operate; |

● existing or worsening conditions in the international financial markets; |

● the actions of existing and potential competitors in each of our markets; |

● the impact of current, pending or future legislation and regulation in countries in which we operate; |

● failure to renew or obtain the necessary licenses, authorizations and concessions to carry out our operations; and |

● the outcome of pending litigation. |

| A. | Directors and Senior Management |

Not applicable.

| B. |

Not applicable.

| C. |

Not applicable.

Not applicable.

Item 3. KEY INFORMATION

| A. | Selected Financial Data |

The following table presents financial data as of and for the years ended December 31, 2010, 2009, 2008, 2007 and 2006. You should read this information in conjunction with our historical consolidated financial statements, including the related notes. Our financial data as of and for the years ended December 31, 2010, 2009 and 2008 are derived from our audited consolidated financial statements for those years included elsewhere in this annual report. Our financial data as of and for the years ended December 31, 2007 and 2006 are derived from our audited financial statements for those years that are not included in this annual report. The historical results below and elsewhere in this annual report may not be indicative of our future performance.

Our consolidated financial statements are presented in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB, and as approved by the European Union, and the year-end financial statements have been audited. The IFRS approved by the European Union differ in some aspects to IFRS published by the IASB; however, these differences do not have a relevant impact on our consolidated financial statements for the years presented. Accordingly, they present fairly our consolidated equity and financial position at December 31, 2010. For additional information see our financial statements and the accompanying notes in this annual report.

In comparing the information for 2007 and 2006 the following change in the scope of consolidation should be taken into account:

Media Capital: In 2005, we purchased all the shares of Vertix, SPGS, S.A., or Vertix, which held 33% of Media Capital and which we accounted for using the equity method. Media Capital ceased to be accounted for by the equity method and started to be fully consolidated from February 2007 onwards as we increased our stake in the company to reach 94.7%, as a consequence of the results of the voluntary and mandatory takeover bids launched for 100% of the company. This change in the scope of consolidation explains the main differences in the results for the year ended December 31, 2007 as compared to the previous year.

Spanish free-to-air TV “Cuatro”: In 2010, due to the restructuring process (spin-off) of the Spanish free-to-air TV business, and after the sale of Sociedad General de Televisión Cuatro, S.A. on December 28, 2010, we decided to present the results of Spanish free-to-air TV in “Loss after tax from discontinued operations”on the consolidated income statement. According to IFRS 5, and for comparison effects, the consolidated income statements and the selected financial data for the years ended December 31, 2009 and 2008 have been restated to present the results of operations of Cuatro as discontinued operations.

In the selected financial data for the years ended December 31, 2007 and December 31, 2006, Cuatro´s figures are classified as continued operations, because of the unreasonable effort and expense involved to supply this information on a restated basis.

| For the Year Ended December 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| (thousands of euros, except per share data) | ||||||||||||||||||||

| Consolidated Statements of Operations Data: | ||||||||||||||||||||

| Operating Income | 2,822,731 | 2,975,120 | 3,694,738 | 3,696,028 | 2,811,758 | |||||||||||||||

| Operating Expenses | (2,486,579 | ) | (2,594,656 | ) | (2,946,031 | ) | (3,176,097 | ) | (2,525,810 | ) | ||||||||||

| Profit from Operations | 336,152 | 380,464 | 748,707 | 519,931 | 285,948 | |||||||||||||||

| Financial Loss | (159,211 | ) | (214,269 | ) | (397,068 | ) | (195,263 | ) | (110,795 | ) | ||||||||||

| Result of companies accounted for using the equity method | (99,553 | ) | (20,158 | ) | (7,592 | ) | (32,056 | ) | (6,025 | ) | ||||||||||

| Loss from other investments | (4,302 | ) | (4,256 | ) | (1,350 | ) | (3,612 | ) | (2,709 | ) | ||||||||||

| Profit before tax from continuing operations | 73,086 | 141,781 | 342,697 | 289,000 | 166,419 | |||||||||||||||

| Income tax | (73,024 | ) | (67,068 | ) | (105,590 | ) | (26,919 | ) | 64,357 | |||||||||||

| Profit from continuing operations | 62 | 74,713 | 237,107 | 262,081 | 230,776 | |||||||||||||||

| Loss after tax from discontinued operations | (35,011 | ) | (9,888 | ) | (110,707 | ) | — | (449 | ) | |||||||||||

| Consolidated profit for the year | (34,949 | ) | 64,825 | 126,400 | 262,081 | 230,327 | ||||||||||||||

| Profit attributable to non-controlling interests | (37,921 | ) | (14,346 | ) | (43,404 | ) | (70,108 | ) | (1,418 | ) | ||||||||||

| Profit attributable to the parent | (72,870 | ) | 50,479 | 82,996 | 191,973 | 228,909 | ||||||||||||||

| Earning (loss) per share from continuing operations | (€0.16 | ) | €0.28 | €0.86 | €0.92 | €1.10 | ||||||||||||||

| Basic earnings per share | (€0.28 | ) | €0.23 | €0.38 | €0.92 | €1.10 | ||||||||||||||

| Cash dividend per share | — | — | — | €0.18 | €0.16 | |||||||||||||||

As of December 31, | ||||||||||||||||||||

2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| (thousands of euros, except per share data) | ||||||||||||||||||||

| Consolidated Balance Sheet Data: | ||||||||||||||||||||

| ASSETS | ||||||||||||||||||||

| Non-Current Assets | 6,293,489 | 6,420,766 | 6,512,270 | 4,832,055 | 4,174,445 | |||||||||||||||

| Property, Plant and Equipment | 295,560 | 345,754 | 397,932 | 423,163 | 475,885 | |||||||||||||||

| Investment Property | 430 | 1 | 28 | 85 | 12,331 | |||||||||||||||

| Goodwill | 3,903,514 | 4,319,603 | 4,302,739 | 2,420,078 | 1,547,561 | |||||||||||||||

| Intangible assets | 360,512 | 365,670 | 400,084 | 444,337 | 400,723 | |||||||||||||||

| Non-current financial assets | 70,611 | 57,218 | 93,344 | 157,166 | 86,837 | |||||||||||||||

| Investments accounted for using the equity method | 613,542 | 13,644 | 12,936 | 13,248 | 280,744 | |||||||||||||||

| Deferred tax assets | 1,046,030 | 1,313,820 | 1,298,475 | 1,364,975 | 1,359,081 | |||||||||||||||

| Other non-current assets | 3,290 | 5,056 | 6,732 | 9,003 | 11,283 | |||||||||||||||

| Current Assets | 1,854,312 | 1,514,898 | 1,594,297 | 1,621,418 | 1,756,105 | |||||||||||||||

| Inventories | 203,152 | 218,066 | 306,079 | 325,160 | 270,322 | |||||||||||||||

| Trade and other receivables | 1,245,687 | 1,207,204 | 1,237,723 | 1,215,684 | 945,858 | |||||||||||||||

| Current financial assets | 160,260 | 6,593 | 838 | 7,456 | 5,162 | |||||||||||||||

| Cash and cash equivalents | 244,988 | 82,810 | 49,432 | 72,827 | 534,538 | |||||||||||||||

| Other current assets | 225 | 225 | 225 | 291 | 225 | |||||||||||||||

| Assets Held For Sale | 3,653 | 257,388 | 519 | 72,887 | 93,971 | |||||||||||||||

| Total Assets | 8,151,454 | 8,193,052 | 8,107,086 | 6,526,360 | 6,024,521 | |||||||||||||||

| EQUITY AND LIABILITIES | ||||||||||||||||||||

| Equity | 2,650,185 | 1,373,019 | 1,258,236 | 1,353,547 | 1,157,234 | |||||||||||||||

| Share Capital | 84,698 | 21,914 | 21,914 | 22,036 | 21,881 | |||||||||||||||

| Other Reserves | 1,120,539 | 833,697 | 779,225 | 721,503 | 610,997 | |||||||||||||||

| Accumulated Profit | 798,876 | 403,478 | 398,975 | 440,972 | 400,282 | |||||||||||||||

| From prior years | 871,746 | 352,999 | 315,979 | 248,999 | 171,373 | |||||||||||||||

| For the year: Profit attributable to the Parent | (72,870 | ) | 50,479 | 82,996 | 191,973 | 228,909 | ||||||||||||||

| Treasury Shares | (4,804 | ) | (3,044 | ) | (24,726 | ) | (39,101 | ) | (38,881 | ) | ||||||||||

| Exchange Differences | 20,213 | (1,561 | ) | (18,422 | ) | (3,475 | ) | 1,497 | ||||||||||||

| Non-controlling interests | 630,663 | 118,535 | 101,270 | 211,612 | 161,458 | |||||||||||||||

| Non-Current Liabilities | 3,526,496 | 2,351,466 | 2,751,369 | 3,124,842 | 2,803,180 | |||||||||||||||

| Exchangeable Bond in Issue | — | — | — | 158,408 | 154,674 | |||||||||||||||

| Non-Current Bank Borrowings | 2,931,190 | 1,917,963 | 2,348,078 | 2,558,372 | 2,252,004 | |||||||||||||||

| Non-Current Financial Liabilities | 362,754 | 249,538 | 232,565 | 202,378 | 202,875 | |||||||||||||||

| Deferred Tax Liabilities | 28,555 | 72,799 | 79,278 | 112,931 | 116,204 | |||||||||||||||

| Long-Term Provisions | 185,592 | 90,150 | 74,807 | 67,346 | 50,906 | |||||||||||||||

| Other Non-Current Liabilities | 18,405 | 21,016 | 16,641 | 25,407 | 26,517 | |||||||||||||||

| Current Liabilities | 1,974,773 | 4,263,133 | 4,097,481 | 2,047,971 | 1,996,942 | |||||||||||||||

| Trade Payables | 1,234,846 | 1,181,437 | 1,257,945 | 1,233,136 | 970,309 | |||||||||||||||

| Payable to Associates | 16,361 | 10,955 | 27,296 | 25,913 | 12,377 | |||||||||||||||

| Other Non-Trade Payables | 99,583 | 107,693 | 142,568 | 137,863 | 96,905 | |||||||||||||||

| Current Bank Borrowings | 411,109 | 2,796,362 | 2,532,091 | 536,046 | 843,410 | |||||||||||||||

| Current Financial Liabilities | 17,788 | 3,295 | 21,676 | — | — | |||||||||||||||

| Payable to Public Authorities | 154,879 | 124,288 | 79,972 | 73,245 | 43,106 | |||||||||||||||

| Provisions for Returns | 9,804 | 9,417 | 9,369 | 8,457 | 5,127 | |||||||||||||||

| Other Current Liabilities | 30,403 | 29,686 | 26,564 | 33,311 | 25,708 | |||||||||||||||

| Liabilities Held For Sale | — | 205,434 | — | — | 67,165 | |||||||||||||||

| Total Equity and Liabilities | 8,151,454 | 8,193,052 | 8,107,086 | 6,526,360 | 6,024,521 | |||||||||||||||

| Book value per share | €7.30 | €5.74 | €5.39 | €5.36 | €4.73 | |||||||||||||||

Exchange Rate Information

The following table provides, for the periods and dates indicated, information concerning the exchange rate between the U.S dollar and the euro. These rates may differ from the rates we use in the presentation of our financial statements or other financial information appearing in this annual report.

The data provided in the following tables are expressed in U.S dollars per euro and are based on the closing spot rates as published by Bloomberg at 5:00 p.m. (New York time) (the “Closing Rate”) on each business day during the period. The Closing Rate on June 29, 2011 was $1.4421 = €1.00.

High | Low | Average (1) | Period End | |||||||||||||

| Annual Data (Year Ended December, 31) | (U.S. dollars per euro) | |||||||||||||||

| 2006……………………………………..……………………………………..………...………...……….. | 1.334 | 1.182 | 1.257 | 1.319 | ||||||||||||

| 2007……………………………………..……………………………………..………...………...……….. | 1.487 | 1.289 | 1.371 | 1.459 | ||||||||||||

| 2008……………………………………..……………………………………..………...………...……….. | 1.599 | 1.245 | 1.471 | 1.397 | ||||||||||||

| 2009……………………………………..……………………………………..………...………...……….. | 1.513 | 1.253 | 1.395 | 1.433 | ||||||||||||

| 2010……………………………………..……………………………………..………...………...……….. | 1.458 | 1.188 | 1.327 | 1.326 | ||||||||||||

| (1) | The average rates for the annual periods were calculated by taking the simple average of the exchange rates on the last business day of each month during relevant period. |

High | Low | ||||||||

| Recent Monthly Data | (U.S. dollars per euro) | ||||||||

| December 2010………………………………..…………………………… | 1.350 | 1.297 | |||||||

| January 2011………………………………..…………………………….... | 1.376 | 1.287 | |||||||

| February 2011………………………………..…………………………….. | 1.386 | 1.343 | |||||||

| March 2011………………………………..……………………………...... | 1.425 | 1.374 | |||||||

| April 2011………………………………..……………………………........ | 1.488 | 1.406 | |||||||

| May 2011………………………………..……………………………......... | 1.494 | 1.397 | |||||||

| June 2011 (through June 29)……………………………….……………..... | 1.468 | 1.416 | |||||||

Not applicable.

Not applicable.

| D. |

In addition to the other information contained in this annual report, prospective investors should carefully consider the risks described below before making any investment decision. The risks described below are not the only ones that we face. Additional risks not currently known to us or that we currently deem immaterial may also impair our business and results of operations. Our business, financial condition, results of operations and cash flow could be materially adversely affected by any of these risks, and investors could lose all or part of their investment.

We have a significant amount of indebtedness, which may adversely affect our cash flow and our ability to operate our businesses, remain in compliance with debt covenants and make payments on our indebtedness.

We have significant financial obligations, as summarized in “Operating and Financial Review and Prospects—Liquidity and Capital Resources.” As of December 31, 2010, our bank borrowings amounted to €3,342 million (December 31, 2009: €4,714 million). Our borrowing levels pose significant risks, including:

| · | increasing our vulnerability to general economic downturns and adverse industry conditions; |

| · | requiring a substantial portion of cash flow from operations to be dedicated to the payment of principal and interest on the indebtedness, therefore reducing our ability to use our cash flow to fund operations, capital expenditures and future business operations; |

| · | exposing us to the risk of increased interest rates, as most of the borrowings are at variable rates of interest; and |

| · | limiting our ability to adjust to changing market conditions and placing us at a disadvantage compared to competitors who have less debt. |

Further, if our operating cash flow and capital resources are insufficient to service our debt obligations, we may be forced to sell assets, seek additional equity or debt capital or further restructure our debt. However, these measures might be unsuccessful or inadequate in permitting us to meet scheduled debt service obligations.

Restrictive covenants in our agreements governing our indebtedness could adversely affect our businesses and operating results by limiting flexibility.

The agreements governing the terms of our indebtedness contain restrictive covenants and requirements to comply with certain leverage and other financial maintenance tests. Many of these agreements also include cross default provisions applicable to other agreements, meaning that a default under any one of these agreements could result in a default under our other debt agreements. These covenants and requirements limit our ability to take various actions, including incurring additional debt, guaranteeing indebtedness and engaging in various types of transactions, including mergers, acquisitions and sales of assets. These covenants could place us at a disadvantage compared to competitors, who may have fewer restrictive covenants and may not be required to operate under these restrictions. Further, these covenants could adversely impact our businesses by limiting our ability to take advantage of financing, mergers and acquisitions or other opportunities.

Our loans are subject to fluctuations in interest rates which may not be adequately protected, or protected at all, by our hedging strategies.

The terms of our bank debt provide exclusively for variable interest rates, and therefore we are exposed to fluctuations in interest rates (see “Operating and Financial Review and Prospects—Liquidity and Capital Resources”). Consequently, we arrange interest rate hedges through contracts providing for interest rate caps (interest rate swap agreements and combination of options). There can be no certainty that our hedging activities will be successful or fully protect us from interest rate exposure. If our hedging strategy is inadequate or the counterparties to the hedging agreements become insolvent, we may not be capable of fully or partially neutralizing the risks associated with changes in interest rates, which would adversely impact our results of operations and financial condition.

Fluctuations in foreign exchange rates could have an adverse effect on our results of operations.

We are exposed to fluctuations in the exchange rates of the various countries in which we operate. our foreign currency risk relates mainly to operating income (revenues) generated outside of the European market, resulting from operations carried on in non-euro zone countries which are tied to the performance of their respective currencies, and financial investments made to acquire ownership interests in foreign companies. Our principal foreign currencies are the U.S. dollar, Brazilian real, Mexican peso, Argentine peso, Chilean peso and Colombian peso. In order to mitigate this risk, we arrange hedges to cover the risk of changes in exchange rates (mainly foreign currency hedges, forwards and options) on the basis of our projections and budgets. If our hedging strategy is inadequate or the counterparties in the hedging arrangements become insolvent, we may not be capable of fully or partially neutralizing the risks associated with the changes in the exchange rate, which would adversely impact our results of operations and financial condition.

Fluctuations in the price of paper could have an adverse effect on our results of operations and financial condition.

We are exposed to the possibility of fluctuations in our results due to changes in the price of paper, an essential raw material for certain of our production processes. Paper is the main raw material of our printed media. In 2010 and in 2009, paper purchase expenses represented 3.6% and 4.1%, respectively, of our total consolidated operating expenses in those years (without considering charges for depreciation and amortization or impairment losses). We have established a program for strategically monitoring changes in paper prices, the aim of which, bearing in mind the cyclical nature of changes in paper prices, is to hedge the price of a percentage of the volume of paper that we expect to consume in the medium term. However, an increase in those prices or an interruption of supply could adversely affect our press and book publishing businesses and, therefore, adversely impact our businesses, results of operations and financial position.

We have significant tax credits that we may not be able to use if the subsidiary at which the loss arose does not generate sufficient income.

As of December 31, 2010, we have recognized tax assets amounting to €1,046 million in our consolidated financial statements. Of this amount, €769 million relates to tax assets recorded at a 30% rate arising from tax loss carryforwards as a result mainly of prior years’ losses (totaling €2,547 million) of the Prisa Televisión (formerly Sogecable) companies. The deadline for recovering these tax assets by offsetting them against future profits is 15 years from the tax year in which they were generated (or of the year in which the company concerned first earns a profit, which is the case with DTS). Since these assets were earned mainly by companies outside the scope of the Prisa consolidated tax group, they will have to be recovered outside of this scope, i.e., they will have to be offset against the individual profits of each company at which they arose.

Of the remainder, €244 million relates mainly to investment tax credits which are deducted from the income tax charge. These credits correspond mainly to tax credits for export activities carried out by Prisa, various Santillana companies and SER. Tax credits for export activities consist of earning a tax credit amounting to 25% of the investments of Prisa in foreign entities that promote the export of goods and/or services and which meet certain requirements. The deadline for taking these credits against future profits, in accordance with the Corporation Tax Law, is ten years from the date on which they were earned. In addition to this deadline, restrictions apply as to the amount that may be used each year, to the extent that, of the balances available for use, credits corresponding to only 35% of the gross tax payable (resulting, in turn, from 30% of the taxable profit less double taxation tax credits) in that year may be used. Certain of these unused tax credits were earned outside the scope of the Prisa consolidated tax group and, therefore, they will have to be recovered outside of this scope; i.e., they will have to be taken against the individual profits of each company at which they arose.

Should our businesses fail to produce sufficient profits in the future against which these tax assets (tax loss carryforwards and tax credits) may be used within the time horizon indicated above, such credits would be lost, which could significantly impact our results of operations and financial condition. The deferred tax assets and liabilities recognized are reassessed at the end of each reporting period in order to ascertain whether they still exist, and the appropriate adjustments are made on the basis of the findings of the analyses performed and the tax rate then in force.

A significant portion of the tax credits for export activities generated by us in the past, totaling €253 million, has been questioned in various tax audits, since the tax authorities considered that the requirements for use of this tax benefit had not been met and, therefore, the tax credits were disallowed by the tax inspectors. We do not concur with the position of the tax authorities and have appealed. Some of our appeals have reached the Supreme Court of Spain and others are still at the administrative stage. The outcome of the current court proceedings and other proceedings that may arise from the tax credits reported could adversely affect our results of operations and financial condition.

We have recorded a provision of €11 million to cover, inter alia, any payments that we may be required to make in connection with these appeals.

We have guaranteed certain significant obligations of Dédalo Grupo Gráfico, S.L., and our financial position and results of operations could be significantly affected if these guarantees were to be called.

We account for our investment in Dédalo, the head of a group of companies engaged in the printing and copying of texts and mechanical binding, using the equity method. In recent years, Dédalo’s subsidiaries, which are engaged in the printing of books and in the printing of magazines and sales brochures using offsetting and photogravure, have incurred ongoing losses, primarily as a result of increased competition in the printing markets in which they operate and restructuring costs that they incurred in relation to these activities to adjust to the demand in those markets.

In 2008, Dédalo and its subsidiaries entered into a syndicated loan and credit agreement for €130 million, principally to cover restructuring costs and operating losses of the photogravure and offsetting businesses. We have guaranteed the full amount outstanding under the agreement and the related hedges since November 2009. As of December 31, 2010, the total amount outstanding under the loan agreement was €130 million.

If any of the Dédalo companies were to fail to comply with their financial obligations or to successfully restructure the printing business, this could adversely impact our businesses, results of operations and financial position.

Economic conditions may adversely affect our businesses and customers, which could adversely affect our results of operations and financial condition.

Spain and other countries in which we operate have experienced slowdowns and volatility in their economies. This downturn has led to and could lead to further lower spending on our products and services by customers, including advertisers, subscribers, licensees, retailers and other consumers of our content offerings and services. In addition, in unfavorable economic environments, our business customers may have difficulties obtaining capital to finance their ongoing businesses and operations and may face insolvency, all of which could impair their ability to make timely payments and continue operations. We cannot predict the duration and severity of weakened economic conditions and such conditions and resultant effects could adversely impact our businesses, results of operations and financial condition.

A decline in advertising expenditures could cause our revenue and operating results to decline significantly in any given period or in specific markets.

A significant portion of our operating income (revenues) depends on the revenues generated from the advertising market through our Press, Radio and Audiovisual businesses, together with the digital business activities that we operate across all business areas. Expenditures by advertisers tend to be cyclical, reflecting overall economic conditions, as well as budgeting and buying patterns. A decline in the economic prospects of advertisers or the economy in general could alter current or prospective advertisers’ spending priorities. Demand for our products is also a factor in determining advertising rates. For example, ratings points for our radio stations, television audience levels and circulation levels for our newspapers are factors that are weighed when determining advertising rates. A drop in advertising revenue could adversely impact our businesses, results of operations and financial condition.

The use of alternative means of delivery for newspapers and magazines may adversely affect our businesses.

Revenue in the newspaper and magazine publishing industry is dependent primarily upon advertising revenue, subscription fees and sale of copies. The use of alternative means of delivery, such as free Internet sites, for news and other content has increased significantly in recent years. Should significant numbers of customers choose to receive content using these alternative delivery sources rather than through our product offerings, we may face a long-term decline in circulation, which may adversely impact our results of operations and financial condition.

The industries in which we operate are highly competitive and we may not successfully react to competitors’ actions.

The press, radio, education, audiovisual, digital, media distribution, advertising and publishing industries in which we operate are highly competitive. To compete effectively in these industries we must successfully market our products and react appropriately to our competitors’ actions, both by launching new products or services and by adjusting our pricing strategies. Such rigorous competition poses an ongoing challenge to our ability to increase audience share, increase sales, retain our present customers, attract new customers and improve our profit margins.

Furthermore, the regulatory policies of many countries in which we conduct business tend, where possible, to enable increased competition in most of the industries in which we operate. These counties have in the past granted, and can be expected to continue to grant, new licenses enabling the entry of new competitors into the marketplace. Such entries have the potential to reduce our revenues or make our operations less profitable.

We may not be capable of competing successfully with current or future industry participants, and the entry of new competitors into the industries in which we currently operate may reduce our revenue, market share or profitability. Any of these events could have an adverse impact on our businesses, results of operations and financial condition.

We may fail to adequately evolve our business strategy as the industry segments in which we compete further mature.

Our principal lines of business, specifically press, radio, education, audiovisual, digital, media distribution, advertising and publishing, are conducted in mature industry segments typified by moderate growth rates (or, in some cases, declining demand), standardized product offerings, a significant number of competitors and difficulties in developing and offering new products and services to consumers.

Advertising revenues represent a significant portion of our revenue (24% of our 2010 operating income). According to December 2010 Zenith Optimedia estimates, advertising expenditure in Spain is expected to grow by 3.0%, 5.0% and 6.0% in 2011, 2012 and 2013, respectively, which represents a 5.5% compound annual rate for 2011-2013. This same source estimates that advertising expenditure in television in Portugal will grow by 2.7%, 5.5% and 9.1% in 2011, 2012 and 2013 respectively and advertising expenditure in radio in Latin America will grow by 5.4%, 5.4% and 5.3% in 2011, 2012 and 2013 respectively.

According to the PricewaterhouseCoopers Global Entertainment and Media Outlook 2009-2013 Report, the digital component of newspaper advertising revenue in Spain is estimated to grow at a 12.5% compound annual rate. However, daily newspaper unit paid circulation in Spain is expected to decline at a 0.4% compound annual rate.

Sales of books and training represented 22% of our operating income for the year ended December 31, 2010. Regarding the total spending in the print educational book market, the report shows that Spain is the only country in Western Europe expected to grow in the period 2009-2013 (+1.3%). In Latin America, the report expects a 0.8% compound annual rate over the same period.

Revenue from subscribers represented 32% of our operating income for the year ended December 31, 2010. In relation to the pay television subscription market, the report states that the strong competition in the sector has cut into subscription TV household growth during the past three years in the EMEA (Europe, Middle East and Africa) region. Also, the deteriorating economic environment is expected to further cut into subscription household growth, with a slower take-up rate for new subscriptions and cutbacks in premium services, pay-per-view and video-on-demand. In 2010, the growth in subscription TV households in the EMEA region is expected to reach 1.9%. As economic conditions improve, the report expects a 4.2% increase in 2011 and a more than 5% increase during 2012-2013 in this region.

We must adopt new strategies to adequately address the challenges posed by this competitive climate. These new strategies may include capturing the benefits of economies of scale, cost reduction, better use of production capacity, increased employee productivity and achieving product and service differentiation through innovative marketing, product design, customer service and organization, among others, to provide us with a competitive edge over other industry participants and enhance the effectiveness of our response to customer demands.

Our failure to adapt strategically to the continuing maturity of the industries in which we operate or to adopt appropriate business strategies in the future could result in the loss of our current market share and, consequently, could adversely impact our businesses, results of operations and financial condition.

We are exposed to liability stemming from the contents of our publications and programming.

Although we attempt to verify the lawfulness of the contents of its publications, programs and broadcasts, we cannot guarantee that third parties will not bring claims against us in connection with its public dissemination of publications and the broadcasting of programs. We could be required to publish corrections to any such broadcasts or publications.

We could be ordered to pay damages, retract statements or restrict the content of our publications or programs if we are found to have infringed third party rights, any of which could adversely impact our businesses, results of operations and financial condition.

We operate in highly regulated industries and are therefore exposed to legislative, administrative and regulatory risks that could adversely impact our businesses.

Our businesses are subject to comprehensive regulations including the requirement to maintain concessions and licenses for our operations in our Audiovisual and Radio segments. Changes in applicable laws or regulations, or in their interpretation, may occur and may substantially impact our business operations, including by requiring changes to our business methods, increasing our costs of doing business or by forcing us to cease conducting business in those segments. There can be no assurance that the regulatory environment in which we operate will not change significantly and adversely in the future.

Television & Radio

Our radio and television operations in both Europe and Latin America are subject to government regulation and are conducted under revocable administrative concessions or licenses. Applicable radio and television regulations cover, among other matters, minimum coverage, necessary technical specifications, program content and permissible advertising. The regulations also cover the ownership and transfer of equity interests in companies engaged in the regulated activities.

We provide a considerable portion of our services under licenses or concessions granted by the governments and administrative bodies of the countries in which we operate. These licenses and concessions require us to comply with the imposed terms and conditions, including with specified investment commitments and established geographic coverage requirements, and to meet established service quality standards. The performance of such obligations is frequently secured by guarantees. In the event of any failure to comply with applicable law or the terms and conditions of a license or a concession, supervising authorities may review or revoke the license or concession or impose penalties on us. The continuity and the terms of the licenses and concessions may be subject to review by the relevant regulatory bodies and the regulators may also construe, amend or terminate a license or a concession. In the event of termination of a concession or license, we may not have access to any meaningful means of redress and termination could significantly adversely affect our business, results of its operations and financial condition.

Our business and our ability to meet the targets established by our strategic plan would be adversely affected in the event that any new legislation or regulations impose more restrictive provisions or more burdensome compliance requirements than those presently in effect or otherwise significantly quantitatively or qualitatively impact any of our licenses or concessions, or if such licenses or concessions were not to be renewed or are revoked, thereby negatively impacting our businesses, results of operations and financial condition.

Publishing

Our book publishing operations are subject to both general legislation applicable to book publishing as well as legislation regulating the publication of educational materials specifically applicable to textbooks. In addition, in Spain, Autonomous Community legislation (legislation by principal governmental bodies responsible for primary and secondary education, universities and higher education and other state-funded education) imposes various obligations on publishers of educational material and textbooks, and the legislation enacted in support of these functions is extensive. Should we breach any of our statutory obligations with respect to the publication of educational materials and textbooks, penalties could be imposed on us and our textbooks and other educational material could be declared unsuitable. Moreover, the increased adoption of book lending in schools by the Spanish Autonomous Communities is likely to entail a reduction in sales. Any of these developments could adversely impact our businesses, results of operations and financial condition.

Our operations outside of Spain subject us to risks typical to investments in countries with emerging economies.

For the year ended December 31, 2010 approximately 20% of our operating revenues was derived from operations in Latin America.

Various risks typical to investments in countries with emerging economies could adversely affect our operations and investments in Latin America, the most significant of which include:

| · | the possible devaluation of foreign currencies or introduction of exchange restrictions, or other restrictions imposed on the free flow of capital across borders; |

| · | the potential effects of inflation and/or the possible devaluation of local currencies, which could lead to equity deficits at our subsidiaries operating in these countries and require us either to recapitalize the affected subsidiaries or wind up the operations of any such affected subsidiary; |

| · | the potential for foreign government expropriation or nationalization of our foreign assets; |

| · | the potential for substantial changes in applicable foreign tax levels or the introduction of new foreign taxes or levies; |

| · | the possibility of changes in policies and/or regulations affecting the economic climate or business conditions of the foreign markets in which we operate; and |

| · | the possibility of economic crises, economic instability or public unrest, which could have an adverse effect on our operations in those countries. |

Any of the above circumstances could adversely impact both our ability to grow our operations in the affected countries and our results of operations and financial position.

If we do not successfully respond to the rapid technological changes that characterize our businesses, our competitive position may be adversely impacted.

In order to maintain and grow our business, we must adapt to technological advances, for which research and development are key factors. Technological changes could give rise to new competitors in our various businesses and provide new opportunities for existing competitors to increase market share at our expense. Consequently, should we fail to keep sufficiently abreast of the current and future technological developments in the industry, this could adversely impact our businesses, results of operations and financial condition, as well as our capacity to achieve our business, strategic and financial objectives.

Losses in excess of insurance, or losses resulting in increases to insurance premiums or failure to renew, could have an adverse effect on our business, financial condition or results of operations.

Although all of our companies maintain insurance policies with scope and coverage which we believe to be consistent with industry practices, our business, financial condition or results of operations could be significantly adversely affected by any exposure to a significant uninsured risk, any incurrence of losses significantly exceeding our insurance coverage, or any considerable increase in our insurance premiums due to claims in any given year significantly exceeding the historical level of claims.

Furthermore, as our insurance policies are subject to annual renewal, we may not be able to renew our existing policies on similar or favorable terms and conditions, if at all.

We are subject to material litigation that, if unfavorably determined, could adversely impact our results of operations or financial condition.

As of the date of this annual report, we are a party to various lawsuits. Since these proceedings are in progress, we cannot reliably anticipate the outcome thereof, nor can we fully assess the consequences of potential judgments. A judgment adverse to our interests could adversely impact our businesses, results of operations and financial condition. Moreover, even if claims brought against us are unsuccessful or without merit, we are required to defend ourselves against such claims. The defense of any such actions may be time-consuming and costly and may distract our management’s attention from executing our business plan.

We depend significantly on our pay television business and negative developments in this market could have an adverse effect on our results of operations.

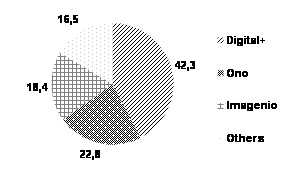

In 2010, revenue from the Spanish pay television market through Digital+ accounted for 40.2% of our operating income. Our share of the total pay television market in Spain in terms of revenues is 66.4%, according to the Spanish Telecommunication Market Commission (CMT) 3Q report 2010. The growth and profitability of the Digital+ business are dependent on developments in the pay television industry as a whole, as well as on changes in the film production and distribution industry. Industry developments impact:

| · | our ability to stimulate pay television consumption, win new subscribers and increase the rate of penetration of pay television among homes with televisions; and |

| · | our ability to ensure the future continuity of the supply of television programming produced by third parties. |

6

Should the market for pay television suffer a downturn or a significant reduction in subscribers, this would adversely impact our results of operations and financial condition.

Our business depends on a number of third-party infrastructures and technological systems for the provision of services to subscribers and any breakdown thereof could interrupt those services.

Currently, Prisa Televisión has contracts for the supply of satellite transmission services with the operators Hispasat, S.A. and Société Europeene des Satellites, S.A., or SES ASTRA. The provision by Prisa Televisión of satellite television services through Digital+ depends on these supply contracts remaining in force. The revocation, termination or failure to renew these contracts could prevent Prisa Televisión from providing its subscribers with satellite television services and could lead to an interruption in these services and adversely impact our businesses, results of operations and financial condition.

The failure of our controlling shareholder group to continue to hold, directly or indirectly, at least 30% of our share capital may trigger change of control provisions contained in a material shareholders agreement among shareholders of DTS.

If holders of a sufficient number of Prisa Class B convertible non-voting shares convert their shares into Prisa Class A ordinary shares and our existing controlling shareholder group does not exercise a sufficient number of its warrants to maintain ownership of, directly or indirectly, at least 30% of Prisa’s Class A ordinary shares, then the change of control provision contained in a material agreement may be triggered pursuant to the definition of “change of control” as defined in such agreement.

The terms of the shareholders agreement among the shareholders of DTS (Prisa Televisión, Telefónica and Telecinco) provide that, within 15 days of learning of a change of control of Prisa, each of Telefónica and/or Telecinco may require Prisa Televisión to sell all of its shares in DTS to Telefónica and/or Telecinco, pro rata, at a purchase price to be determined by internationally recognized investment banks chosen by each party. In the event of a change of control, through Prisa Televisión, we could lose our stake in our pay television business.

A change of control of Prisa is defined in the shareholders agreement as (i) the Prisa controlling shareholder group ceasing to own at least 30% of Prisa’s share capital or (ii) the existence of an individual Prisa shareholder or a group of Prisa shareholders (acting jointly through one or more voting agreements) holding an ownership interest in Prisa greater than the ownership interest held by the Prisa controlling shareholder group.

The loss of our stake in our pay television business would adversely impact our results of operations and financial condition.

Supermajority and other voting provisions in our bylaws, along with the existence of a controlling shareholder group, may have the effect of discouraging potentially interested parties from seeking to acquire us or otherwise influence the outcome of significant matters affecting our shareholders.

Our bylaws require a 75% supermajority shareholder vote to approve bylaw amendments, increases or reductions in our share capital, mergers and similar extraordinary transactions and, in some cases, the election of directors not nominated by our board of directors. Our controlling shareholder group currently controls over 30% of our total voting power. As a result, these bylaw provisions may have the effect of rendering more difficult or discouraging an acquisition of Prisa not supported by the controlling shareholder group or otherwise precluding corporate actions that the controlling shareholder group opposes, even if supported by a majority of our voting shares.

Because Prisa is a holding company and its assets are held primarily by its subsidiaries, we may not be able to pay dividends on our Class B convertible non-voting shares, even if we have sufficient distributable profits on a consolidated basis to make such payments.

The Prisa Class B convertible non-voting shares issued in connection with the business combination are entitled to receive a minimum annual dividend of €0.175, but only to the extent that Prisa has sufficient “distributable profits” for the applicable year, as that term is defined by the Spanish Companies Law, or sufficient premium reserve created by the issuance of the Prisa Class B convertible non-voting shares. If Prisa has no distributable profits in a given year or insufficient premium reserve created by the issuance of the Prisa Class B convertible non-voting shares, then no dividend will be payable for such year, and if Prisa has distributable profits in a given year or premium reserve created by the issuance of the Prisa Class B convertible non-voting shares which are insufficient to pay the annual dividend in full, then a partial dividend will be paid for such year, up to the amount of such distributable profits and premium reserve created by the issuance of the Prisa Class B convertible non-voting shares (so long as there is no legal restriction against such payment). Any unpaid dividends will accumulate from year to year.

Under the Spanish Companies Law, the determination of whether Prisa has distributable profits does not take into account the assets or profits of any of Prisa’s subsidiaries. Prisa is a holding company with no significant operating assets other than through its ownership of shares of, or other interests in, its subsidiaries. Prisa receives substantially all of its operating income from its subsidiaries. Prisa’s subsidiaries are separate and distinct legal entities and they will have no obligation, contingent or otherwise, to pay dividends or distribute any amounts to Prisa, or to otherwise make any funds available to Prisa, to allow Prisa to pay dividends on the Prisa Class B convertible non-voting shares. In addition, the ability of Prisa’s subsidiaries to pay dividends or make distributions to Prisa may be subject to, among other things, applicable laws and/or restrictions contained in agreements or debt instruments to which such subsidiaries are bound. In addition, third parties own substantial interests in certain of Prisa’s subsidiaries and, accordingly, Prisa must share with minority shareholders any dividends paid by these subsidiaries. Prisa had, on a non-consolidated basis, a distributable profit of approximately €9.3 million in 2010, a loss in 2009, and a distributable profit of approximately €37.2 million in 2008.

Although Prisa has agreed to propose to its shareholders a resolution requiring Prisa to exercise its voting rights to cause its subsidiaries to deliver distributable profits to Prisa, there can be no assurance that the subsidiaries will be able to distribute such profits to Prisa, or that the amount of the distributable profits will be enough to allow Prisa to pay the minimum annual dividend on the Prisa Class B convertible non-voting shares. As a result, Prisa may not be able to pay all or a portion of the dividend payable on the Prisa Class B convertible non-voting shares, even if Prisa and its subsidiaries, on a consolidated basis, have profits in an amount greater than that needed to pay the minimum annual dividend.

The amount of the premium reserve created by the issuance of the Prisa Class B convertible non-voting shares was fixed prior to closing of the business combination as the difference between the issuance price of the Prisa Class B convertible non-voting shares and the nominal amount of such shares (€0.10). The premium reserve created by the issuance of the Prisa Class B convertible non-voting shares may be reduced as a result of losses in Prisa.

In addition any remaining accumulated dividends at the time of conversion (whether voluntary or automatic at the 42-month anniversary of issuance) will be paid on or before the date on which Prisa Class A ordinary shares are delivered in exchange for the converted Prisa Class B convertible non-voting shares to the extent there are distributable profits for the year of conversion or the previous year (if the minimum dividend for such year has not been declared) that are permitted by applicable law to be paid out. At that time, Prisa will determine and pay both the amount of the annual dividend payable for the portion of the year of conversion during which the shares subject to conversion remained outstanding and the amount of dividend that remained accrued at the time of conversion. Any such dividends (whether for the portion of the year of, or accrued at the time of, conversion) that do not become payable at that time due to the lack of sufficient distributable profits for that year or lack of available premium reserve will not thereafter become payable or be paid. Based on the number of Prisa Class B convertible non-voting shares issued in the business combination (approximately 403 million shares), an aggregate annual minimum dividend of €70.5 million would have been payable on the Prisa Class B convertible non-voting shares for each of 2008, 2009 and 2010. For 2008, Prisa would have been obligated to pay €37.2 million of this amount from available distributable profits and the remaining €33.3 million out of a charge against the premium reserve that would have been created at the time of issuance; for 2009, since Prisa did not have distributable profits for the year, Prisa would have been obligated to pay the entire €70.5 million out of a charge against the premium reserve. For 2010, Prisa is obligated to pay €0.014583 per Class B convertible non-voting share.

We have not previously operated as a foreign private issuer in the United States and fulfilling our obligations as a foreign private issuer after the business combination may be expensive and time consuming.

We have not previously been required to prepare or file periodic and other reports with the SEC or to comply with the other requirements of U.S. federal securities laws applicable to public companies, such as Section 404 of the Sarbanes-Oxley Act of 2002. Although we currently maintain separate legal and compliance and internal audit functions, and although Prisa is a public company in Spain with its shares listed on the Spanish Continuous Market Exchange and thus has to comply with the securities laws and regulations that apply to Prisa in Spain (including rules with respect to corporate governance practices, reporting requirements and accounting rules), we have not previously been required to establish and maintain disclosure controls and procedures and internal controls over financial reporting as will be required with respect to a public company with substantial operations and shares registered in the United States.

Under the Sarbanes-Oxley Act of 2002 and the related rules and regulations of the SEC, as well as the rules of the New York Stock Exchange, we are required to implement additional corporate governance practices and adhere to a variety of reporting requirements and accounting rules. However, as a “foreign private issuer,” we are exempt from some corporate governance practices, reporting requirements and accounting rules under the rules of the New York Stock Exchange and under the Sarbanes-Oxley Act of 2002. For example, we are permitted to follow Spanish corporate governance practices in lieu of the New York Stock Exchange rules with some exceptions so long as we disclose the ways in which our corporate governance practices differ from those followed by U.S. issuers under New York Stock Exchange listing standards. As an additional example, the Sarbanes-Oxley Act of 2002 gives foreign private issuers certain exemptions from the requirement that each member of the foreign private issuer’s audit committee be “independent.”

Compliance with obligations from which foreign private issuers are not exempt may require members of our management and our finance and accounting staff to divert time and resources from other responsibilities to ensuring these additional regulatory requirements are fulfilled and may increase our legal, insurance and financial compliance costs.

You may have to pay taxes on constructive distributions without receiving a corresponding distribution of cash or property.

If the conversion ratio of the Prisa Class B convertible non-voting shares into Prisa Class A common shares is increased, as provided in the terms of the Prisa Class B convertible non-voting shares, holders of Prisa ADS-NVs may be treated as having received a constructive distribution if such increase in the conversion ratio has the effect of increasing the proportionate interest of such holders in Prisa’s earnings and profits or assets. In such a case, holders may be required to include an amount in income for U.S. federal income tax purposes, notwithstanding that they do not receive such distributions.

Item 4. INFORMATION ABOUT PRISA

Overview

Promotora de Informaciones, S.A., which operates under the commercial name “Prisa,” was incorporated in the city of Madrid on January 18, 1972. We are the leading multimedia group in Spain and Portugal and we believe we are one of the leading multimedia groups in the Spanish-speaking world. We operate in more than 20 countries, including Brazil, Mexico and Argentina as well as many other Latin American countries and the United States.

History

The following are certain significant events in the development of Prisa:

1972

| · | Prisa founded, but does not begin operations. |

1976

| · | El País first issue. |

1980s

| · | We acquire Cadena SER. |

| · | We acquire Cinco Días. |

1990

| · | Sogecable, 25.0% owned by Prisa, is awarded a television license to operate Canal+, first experience of pay TV in the country. |

1996

| · | We acquire a controlling equity interest in AS and launches websites for El País, Digital+, AS and Cadena SER. |

1997

| · | Sogecable launches Canal Satélite Digital, Spain’s leading multi-channel digital direct-to-home platform. |

1999

| · | We expand our activities into the music market by founding Gran Vía Musical. |

| · | We acquire our equity interest in Caracol, S.A., or “Radio Caracol”—the largest radio group in Colombia—and create Participaciones de Radio Latinoamericana S.L., or “PRL,” through which we carry out our radio operations in Chile, Costa Rica, Panama, the United States and France. |

2000

| · | We launch our initial public offering and our shares begin trading through the Spanish stock market interconnection system. |

| · | We expand our activities to media advertising sales through the acquisition of GDM. |

| · | We expand our activities to book publishing and printing through Santillana and Dédalo, respectively. |

2001

| · | We establish audiovisual producer Plural Entertainment, to develop and produce audiovisual content. |

| · | We enter the radio market in Mexico through an agreement with Grupo Televisa A.B., or Televisa, to develop the radio market in Mexico, which involved the acquisition of a 50.0% equity interest in Sistema Radiópolis, S.A. de C.V., which is referred to as “Radiópolis.” Management is run by Prisa. |

| · | We acquire Editora Moderna Ltda., or “Editora Moderna,” in Brazil. |

2002

| · | We organize Grupo Latino de Radio S.A., or “GLR,” as a holding company to restructure our radio businesses in Latin America, and our equity interests in PRL, Radiópolis and Grupo Caracol are transferred to GLR. |

2005

| · | We enter the Portuguese media market through the acquisition of 100.0% of the equity of Vertix, which owns 33.0% of the equity of Media Capital. |

2006

| · | We increase our ownership interest in Sogecable to 42.9%. |

| · | We combine our ratio activities in Latin America and Spain into Unión Radio. |

2007

| · | We acquire all of the shares of Iberoamericana Radio Chile, S.A. through GLR Chile, Ltda. |

| · | We increase our ownership interest in Media Capital to 94.7% |

2008

| · | We acquire the remaining outstanding share capital of Sogecable, increasing our ownership interest to 100%. |

8

The following significant events occurred in 2010:

| · | We carried out a capital increase and obtained €650 million in cash. After this transaction, the investors of Liberty Acquisition Holdings Corp became Prisa shareholders. At the same time, Prisa shareholders before the 23rd of November were granted Prisa warrants. In connection with this transaction, we listed our shares, in the form of American Depositary Shares on the New York Stock Exchange. Our new shares started trading on the NYSE and on the Spanish stock exchanges in December. Our warrants are also traded on the Spanish stock exchanges. |

| · | We refinanced our debt, extending its maturity to 2013. |

| · | Within the process of the entrance of strategic partners in the group, during 2010 the following agreements were closed: |

| - | We sold a 25% stake in Santillana to DLJ South American Partners LP. |

| - | Through Prisa Televisión (formerly Sogecable), we sold a 44% stake in Digital+ to Telefónica (22%) and Telecinco (22%) for €976 million in cash, which was mainly used for debt amortization. |

| - | On December 28, 2010, Prisa Televisión sold 100% of Sociedad General de Televisión Cuatro, S.A. and subsidiaries to Gestevisión Telecinco, S.A. This sale was carried out through the subscription by Prisa Televisión of a 17.336% stake in Gestevisión Telecinco, S.A. in non-cash capital increase approved by the shareholders of Gestevisión Telecinco, S.A. in their general meeting held on December 24, 2010. The market value of this investment on subscription was €590 million. As a result of this transaction, we consolidate Gestevisión Telecinco, S.A. Group and subsidiaries using the equity method. |

| · | We announced a restructuring plan, which will reduce our workforce by 18% through outsourcing and voluntary redundancy. |

Business areas

Our principal business operations are:

| · | Audiovisual, which includes pay television, free-to-air television and television and film production; |

| · | Education, which includes the publishing and sale of general books, educational material and training materials; |

| · | Radio, which includes the sale of advertising on our networks; and |

| · | Press, which includes the publishing of newspapers and magazines and the sale of advertising in such publications. |

We operate a digital platform that provides services and support to each of these principal business operations. We also sell media advertising and promote and produce musical events. We are the leader in Spain, and we believe we are one of the leaders in the Spanish-speaking world, in daily newspapers through El País, in radio through Cadena SER, and in education and publishing through Santillana. Through Prisa Televisión and its digital platform, Digital+, we are also the leader in pay television in Spain. In specialized press, we are ranked second in sports press through AS and are ranked second in financial press through Cinco Días.

Media Capital, our subsidiary, operates TVI, the leading free-to-air television network in Portugal. Media Capital also operates an audiovisual production business as well as a radio network, produces music recordings and distributes films and video/DVDs.

Prisa is domiciled in Spain, its legal form is a public limited liability company and its activity is subject to Spanish legislation and particularly to the Spanish Companies Law. It has been in continuous operation since its public deed of incorporation was executed, and now has perpetual existence. Our registered office is located at Gran Vía 32, 28013 Madrid, Spain. Our telephone number is +34 (91) 330 10 00.

Capital expenditures and disposals

Our principal capital expenditures during the three years ended December 31, 2010 consisted of additions to property, plant and equipment and additions to intangible assets. In 2010, 2009 and 2008, we made capital expenditures of €206 million, €128 million and €191 million, respectively.

Year ended December 31, 2010

Our capital expenditure increased by 61.0% to €206 million in 2010 compared to €128 million in 2009, mainly as a result of acquisition of digital set-top boxes and cards by the change in the marketing model iPlus from a sales model to a transfer with licensing fees.

The most significant disposals in 2010 were the result of the sale of Prisa Televisión’s headquarters in Tres Cantos and the sale of data processing equipment at its carrying amount to CSI Renting de Tecnología, S.A.U. within the framework of an outsourcing agreement signed with Indra Sistemas, S.A. on December 23, 2009. The agreement provides for the outsourcing of our IT technology management systems and R&D projects for a seven-year period.

Year ended December 31, 2009

Our capital expenditure decreased by 32.8% from 2008 to 2009. This reduction was largely due to a decrease in Digital + capital expenditures related to the decline in the number of suscribers, a cost saving plan and a capital expenditures reduction policy.

Year ended December 31, 2008

On July 29, 2008, we entered into an agreement for the sale and leaseback of three of our buildings in Madrid (Gran Vía, 32 and Miguel Yuste, 40) and Barcelona (Caspe, 6-20) with Longshore, S.L., or Longshore, for €300 million, which gave rise to a gain of €227 million.

Financial Investments

Our principal financial investment in 2010 was the acquisition of an additional stake in V-me Media Inc, the fourth largest TV operator in the US Hispanic market.

In 2008 we launched a mandatory takeover bid for the remaining outstanding shares of Prisa Televisión (52.91%) resulting in an investment in financial assets of €2,057 million.

Recent Developments

At the beginning of 2011, we began implementation of a restructuring plan which will affect 18% of our workforce globally (2,500 people), including 2,000 people in Spain and 500 people in Portugal and Latin America. This restructuring will be extended until the first quarter of 2012 and will include various measures (outsourcing, voluntary redundancy, early retirement, etc.). This plan is based on a thorough analysis of each of our companies with the aim of resizing teams to appropriate levels and achieving the rationalization of resources, as well as the standardization and centralization of global processes. As of the date of this annual report, we were evaluating the economic impact of these measures, which will be definitive once negotiation with labor representatives has terminated.

During 2011, we reached an agreement with PortQuay West I B.V., a company which is controlled by Miguel Pais do Amaral, to sell 10% of Grupo Media Capital SGPS, S.A.’s share capital for approximately EUR 35 million. This agreement will allow the buyer the option to purchase up to an additional 19.69%.

| B. |

Our activities are organized into the following segments: Audiovisual, Education, Radio and Press. This structure is supported by the Digital area, which provides services and support to all business segments. Additionally, we do business in other areas not part of any business segment including distribution, an advertising agency, Prisa Innova, real estate and printing (known as Dédalo).

The following table describes our organizational structure by segment.

| Audiovisual | Education | Radio | Press |

● Prisa Televisión (formerly Sogecable) | ● Education ● General Publishing | ● Radio in Spain ● International Radio | ● El Pais ● AS |

● Media Capital | ● Training | ● Gran Via Musical | ● Cinco Dias |

● Audiovisual Production | ● Magazines |

The following table shows our revenues, by business segment, for the previous three fiscal years (in thousands of euros, except for margins).