UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 30, 2016

or

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ______________ to ________________ |

Commission File Number: 001-15274

| J. C. PENNEY COMPANY, INC. | ||||||

| (Exact name of registrant as specified in its charter) | ||||||

| Delaware | 26-0037077 | |||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||

| 6501 Legacy Drive, Plano, Texas 75024-3698 | ||||||

| (Address of principal executive offices) | ||||||

| (Zip Code) | ||||||

| (972) 431-1000 | ||||||

| (Registrant's telephone number, including area code) | ||||||

| Securities registered pursuant to Section 12(b) of the Act: | ||||||

| Title of each class | Name of each exchange on which registered | |||||

| Common Stock of 50 cents par value | New York Stock Exchange | |||||

| Preferred Stock Purchase Rights | New York Stock Exchange | |||||

| Securities registered pursuant to Section 12(g) of the Act: | ||||||

| None | ||||||

| (Title of class) | ||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

| (Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter (August 1, 2015). $2,512,275,429

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date.

306,624,828 shares of Common Stock of 50 cents par value, as of March 11, 2016.

| DOCUMENTS INCORPORATED BY REFERENCE | ||

| Documents from which portions are incorporated by reference | Parts of the Form 10-K into which incorporated | |

| J. C. Penney Company, Inc. 2016 Proxy Statement | Part III | |

INDEX

| Page | ||

2

PART I

Item 1. Business

Business Overview

J. C. Penney Company, Inc. is a holding company whose principal operating subsidiary is J. C. Penney Corporation, Inc. (JCP). JCP was incorporated in Delaware in 1924, and J. C. Penney Company, Inc. was incorporated in Delaware in 2002, when the holding company structure was implemented. The new holding company assumed the name J. C. Penney Company, Inc. (Company). The holding company has no independent assets or operations, and no direct subsidiaries other than JCP. Common stock of the Company is publicly traded under the symbol “JCP” on the New York Stock Exchange. The Company is a co-obligor (or guarantor, as appropriate) regarding the payment of principal and interest on JCP’s outstanding debt securities. The guarantee by the Company of certain of JCP’s outstanding debt securities is full and unconditional. The holding company and its consolidated subsidiaries, including JCP, are collectively referred to in this Annual Report on Form 10-K as “we,” “us,” “our,” “ourselves,” “Company” or “JCPenney.”

Since our founding by James Cash Penney in 1902, we have grown to be a major retailer, operating 1,021 department stores in 49 states and Puerto Rico as of January 30, 2016. Our fiscal year ends on the Saturday closest to January 31. Unless otherwise stated, references to years in this report relate to fiscal years, rather than to calendar years. Fiscal year 2015 ended on January 30, 2016; fiscal year 2014 ended on January 31, 2015; and fiscal year 2013 ended on February 1, 2014. Each consisted of 52 weeks.

Our business consists of selling merchandise and services to consumers through our department stores and our website at jcpenney.com, which utilizes fully optimized applications for desktop, mobile and tablet devices. Our department stores and website generally serve the same type of customers, our website offers virtually the same mix of merchandise as our in store assortment along with other extended categories that are not offered in store, and our department stores generally accept returns from sales made in stores and via our website. We fulfill online customer purchases by direct shipment to the customer from our distribution facilities and stores or from our suppliers' warehouses and by in store customer pick up. We sell family apparel and footwear, accessories, fine and fashion jewelry, beauty products through Sephora inside JCPenney and home furnishings. In addition, our department stores provide our customers with services such as styling salon, optical, portrait photography and custom decorating.

Based on how we categorized our divisions in 2015, our merchandise mix of total net sales over the last three years was as follows:

| 2015 | 2014 | 2013 | |||||||

| Women’s apparel | 25 | % | 26 | % | 26 | % | |||

| Men’s apparel and accessories | 22 | % | 22 | % | 22 | % | |||

| Home | 12 | % | 12 | % | 11 | % | |||

| Women’s accessories, including Sephora | 12 | % | 11 | % | 10 | % | |||

| Children’s apparel | 10 | % | 10 | % | 11 | % | |||

| Footwear and handbags | 8 | % | 8 | % | 9 | % | |||

| Jewelry | 6 | % | 6 | % | 6 | % | |||

| Services and other | 5 | % | 5 | % | 5 | % | |||

| 100 | % | 100 | % | 100 | % | ||||

Operating Strategy

We have developed our strategic framework to focus on the following three pillars:

•private brands;

•omnichannel; and

•revenue per customer.

We believe these three pillars provide the foundation to increase loyalty with our customers and enable the organization to simplify its focus by ensuring that resources and capital investments are effectively allocated to drive these priorities.

3

Our first priority is private brands. We plan to leverage our sourcing and private brand infrastructure to increase our production of private brands with style, quality and value. With an established global network of sourcing offices, along with a team of in-house designers, we plan to grow private brand penetration and increase our profitability.

Our second priority is to become a world-class omnichannel retailer. We have a rich heritage of being a catalog retailer and have much of our omnichannel infrastructure already in place. We have three large, strategically located dot-com distribution centers with approximately five million square feet of space with plans to effectively digitize these centers. Our objective is to create a seamless connection between our digital and brick-and-mortar operations through initiatives such as buy-online-pick-up-in-store same day (BOPIS).

Our final strategic priority is increasing revenue per customer. We have approximately the same number of active customers as we did in 2011; however, there is an increased opportunity to grow shopping frequency and the amount these customers spend on every transaction. We plan to address this opportunity by enhancing our cross-merchandising appeal with initiatives to upgrade each store’s center core, which is the area of the store that includes fashion and fine jewelry, handbags, footwear, sunglasses, and accessories, along with accelerating the growth of our Sephora inside JCPenney locations.

Competition and Seasonality

The business of selling merchandise and services is highly competitive. We are one of the largest department store and e-commerce retailers in the United States, and we have numerous competitors, as further described in Item 1A, Risk Factors. Many factors enter into the competition for the consumer’s patronage, including price, quality, style, service, product mix, convenience, loyalty programs and credit availability. Our annual earnings depend to a great extent on the results of operations for the last quarter of the fiscal year, which includes the holiday season, when a significant portion of our sales and profits are recorded.

Trademarks

The JCPenney®, JCP®, Liz Claiborne®, Claiborne®, Okie Dokie®, Worthington®, a.n.a®, St. John’s Bay®, The Original Arizona Jean Company®, Ambrielle®, Decree®, Stafford®, J. Ferrar®, Xersion®, Belle + Sky™, Total Girl®, monet®, JCPenney Home®, Studio JCP Home™, Home Collection by JCPenney™, Made for Life™, The Boutique Plus™, Stylus®, Sleep Chic®, Home Expressions® and Cooks JCPenney Home™ trademarks, as well as certain other trademarks, have been registered, or are the subject of pending trademark applications with the United States Patent and Trademark Office and with the registries of many foreign countries and/or are protected by common law. We consider our marks and the accompanying name recognition to be valuable to our business.

Website Availability

We maintain an Internet website at www.jcpenney.com and make available free of charge through this website our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all related amendments to those reports, as soon as reasonably practicable after the materials are electronically filed with or furnished to the Securities and Exchange Commission. In addition, our website provides press releases, access to webcasts of management presentations and other materials useful in evaluating our Company.

Suppliers

We have a diversified supplier base, both domestic and foreign, and are not dependent to any significant degree on any single supplier. We purchase our merchandise from approximately 2,300 domestic and foreign suppliers, many of which have done business with us for many years. In addition to our Plano, Texas home office, we, through our purchasing subsidiary, maintained buying and quality assurance offices in 10 foreign countries as of January 30, 2016.

Employment

The Company and its consolidated subsidiaries employed approximately 105,000 full-time and part-time employees as of January 30, 2016.

4

Environmental Matters

Environmental protection requirements did not have a material effect upon our operations during 2015. It is possible that compliance with such requirements (including any new requirements) would lengthen lead time in expansion or renovation plans and increase construction costs, and therefore operating costs, due in part to the expense and time required to conduct environmental and ecological studies and any required remediation.

As of January 30, 2016, we estimated our total potential environmental liabilities to range from $20 million to $25 million and recorded our best estimate of $23 million in Other accounts payable and accrued expenses and Other liabilities in the Consolidated Balance Sheet as of that date. This estimate covered potential liabilities primarily related to underground storage tanks, remediation of environmental conditions involving our former drugstore locations and asbestos removal in connection with approved plans to renovate or dispose of our facilities. We continue to assess required remediation and the adequacy of environmental reserves as new information becomes available and known conditions are further delineated. If we were to incur losses at the upper end of the estimated range, we do not believe that such losses would have a material effect on our financial condition, results of operations or liquidity.

5

Executive Officers of the Registrant

The following is a list, as of March 11, 2016, of the names and ages of the executive officers of J. C. Penney Company, Inc. and of the offices and other positions held by each such person with the Company. These officers hold identical positions with JCP. There is no family relationship between any of the named persons.

| Name | Offices and Other Positions Held With the Company | Age | ||

| Myron E. Ullman, III | Chairman of the Board | 69 | ||

| Marvin R. Ellison | Chief Executive Officer | 51 | ||

| Edward J. Record | Executive Vice President and Chief Financial Officer | 47 | ||

| Brynn L. Evanson | Executive Vice President, Human Resources | 46 | ||

| Janet M. Link | Executive Vice President, General Counsel | 46 | ||

| Therace M. Risch | Executive Vice President, Chief Information Officer | 43 | ||

| Andrew S. Drexler | Senior Vice President, Chief Accounting Officer and Controller | 45 | ||

Mr. Ullman has served as Chairman of the Board of Directors since August 2015, and as a director of the Company and a director of JCP since 2013. He previously served as Chief Executive Officer of the Company from 2004 to 2011 and from 2013 to 2015 and as Chairman of the Board of Directors of the Company from 2004 to 2012. He was Directeur General, Group Managing Director, LVMH Moët Hennessy Louis Vuitton (luxury goods manufacturer/retailer) from 1999 to 2002. He was President of LVMH Selective Retail Group from 1998 to 1999. From 1995 to 1998, he was Chairman of the Board and Chief Executive Officer of DFS Group Ltd. (luxury retailer). From 1992 to 1995, he was Chairman of the Board and Chief Executive Officer of R. H. Macy & Company, Inc.

Mr. Ellison has served as Chief Executive Officer since August 2015, and as a director of the Company and a director of JCP since 2014. He previously served as President of the Company from 2014 to 2015. Prior to joining the Company, he served as Executive Vice President - U.S. Stores of The Home Depot, Inc. from 2008 to 2014. His prior roles with The Home Depot, Inc. included President - Northern Division from 2006 to 2008, Senior Vice President - Logistics from 2005 to 2006, Vice President - Logistics from 2004 to 2005, and Vice President - Loss Prevention from 2002 to 2004. Mr. Ellison began his career with Target Corporation where he served in a variety of operational roles.

Mr. Record has served as Executive Vice President and Chief Financial Officer of the Company and as a director of JCP since 2014. Prior to joining the Company, he served in positions of increasing responsibility with Stage Stores, Inc. (apparel retailer), including Executive Vice President and Chief Operating Officer from 2010 to 2014, Chief Financial Officer from September 2007 to 2010 and Executive Vice President and Chief Administrative Officer from May 2007 to September 2007. Mr. Record also served as Senior Vice President of Finance of Kohl’s Corporation from 2005 to 2007. Prior to that, he served with Belk, Inc. as Senior Vice President of Finance and Controller from April 2005 to October 2005 and Senior Vice President and Controller from 2002 to April 2005.

Ms. Evanson has served as Executive Vice President, Human Resources since 2013. Prior to that she served as Vice President, Compensation, Benefits and Talent Operations from 2010 to 2013 and Director of Compensation from 2009 to 2010. Prior to joining the Company, she worked at the Dayton Hudson Corporation from 1991 to 2009 (renamed Target Corporation in 2000). Ms. Evanson began her career with Marshall Field’s where she advanced through positions in stores, finance, human resources and merchandising and moved to the Target stores division in 2000, ultimately serving as Director of Executive Compensation and Retirement Plans.

Ms. Link has served as Executive Vice President, General Counsel since May 2015. Prior to that, she served as interim General Counsel from March 2015 to May 2015 and as Vice President, Deputy General Counsel from September 2014 to March 2015. Prior to joining the Company, she served as Vice President, Deputy General Counsel of CC Media Holdings, Inc. (now known as iHeart Media Holdings, Inc.) and Clear Channel Outdoor Holdings, Inc. from 2013 to 2014 and as Vice President, Associate General Counsel - Litigation from 2010 to 2013. She also served as Interim General Counsel of Clear Channel Outdoor - Americas from 2010 to 2011. Ms. Link was a partner with Latham & Watkins LLP from 2005 to 2010 where she was the Vice-Chair of the Global Litigation Department.

Ms. Risch has served as Executive Vice President and Chief Information Officer since December 2015. Prior to joining the Company, she served as Executive Vice President and Chief Information Officer of Country Financial (insurance and investment services) from 2014 to 2015. Prior to that, Ms. Risch spent 10 years at Target Corporation in a variety of technology roles of increasing responsibility, including Vice President of Technology Delivery Services from 2012 to 2014 and Vice President, Business Technology Team from 2009 to 2012.

6

Mr. Drexler has served as Senior Vice President, Chief Accounting Officer and Controller since June 2015. Prior to joining the Company, he served as Senior Vice President and Chief Financial Officer of Giant Eagle, Inc. (grocery retailer) from 2014 to 2015. He also served as Senior Vice President, Finance, and Corporate Controller for GNC Holdings, Inc. from 2011 to 2014. Prior to that, Mr. Drexler spent 11 years at Wal-Mart Stores, Inc. in roles of increasing responsibility, including Vice President of Finance for the information systems division from 2010 to 2011. Earlier in his career, he held a variety of roles with PricewaterhouseCoopers, LLP. Mr. Drexler is a certified public accountant.

Item 1A. Risk Factors

The following risk factors should be read carefully in connection with evaluating our business and the forward-looking information contained in this Annual Report on Form 10-K. Any of the following risks could materially adversely affect our business, operating results, financial condition and the actual outcome of matters as to which forward-looking statements are made in this Annual Report on Form 10-K.

Our ability to return to profitable growth is subject to both the risks affecting our business generally and the inherent difficulties associated with implementing our strategic plan.

As we position the Company for long-term growth, it may take longer than expected to achieve our objectives, and actual results may be materially less than planned. Our ability to improve our operating results depends upon a significant number of factors, some of which are beyond our control, including:

| • | customer response to our marketing and merchandise strategies; |

| • | our ability to achieve profitable sales and to make adjustments in response to changing conditions; |

| • | our ability to respond to competitive pressures in our industry; |

| • | our ability to effectively manage inventory; |

| • | the success of our omnichannel strategy; |

| • | our ability to benefit from capital improvements made to our store environment; |

| • | our ability to respond to any unanticipated changes in expected cash flows, liquidity and cash needs, including our ability to obtain any additional financing or other liquidity enhancing transactions, if and when needed; |

| • | our ability to achieve positive cash flow; |

| • | our ability to access an adequate and uninterrupted supply of merchandise from suppliers at expected levels and on acceptable terms; |

| • | changes to the regulatory environment in which our business operates; and |

| • | general economic conditions. |

There is no assurance that our marketing, merchandising and omnichannel strategies, or any future adjustments to our strategies, will improve our operating results.

We operate in a highly competitive industry, which could adversely impact our sales and profitability.

The retail industry is highly competitive, with few barriers to entry. We compete with many other local, regional and national retailers for customers, employees, locations, merchandise, services and other important aspects of our business. Those competitors include other department stores, discounters, home furnishing stores, specialty retailers, wholesale clubs, direct-to-consumer businesses, including those on the Internet, and other forms of retail commerce. Some competitors are larger than JCPenney, and/or have greater financial resources available to them, and, as a result, may be able to devote greater resources to sourcing, promoting, selling their products, updating their store environment and updating their technology. Competition is

7

characterized by many factors, including merchandise assortment, advertising, price, quality, service, location, reputation, credit availability and customer loyalty. We have experienced, and anticipate that we will continue to experience for at least the foreseeable future, significant competition from our competitors. The performance of competitors as well as changes in their pricing and promotional policies, marketing activities, customer loyalty programs, new store openings, store renovations, launches of Internet websites or mobile platforms, brand launches and other merchandise and operational strategies could cause us to have lower sales, lower gross margin and/or higher operating expenses such as marketing costs and other selling, general and administrative expenses, which in turn could have an adverse impact on our profitability.

Our sales and operating results depend on our ability to develop merchandise offerings that resonate with our existing customers and help to attract new customers.

Our sales and operating results depend in part on our ability to predict and respond to changes in fashion trends and customer preferences in a timely manner by consistently offering stylish, quality merchandise assortments at competitive prices. We continuously assess emerging styles and trends and focus on developing a merchandise assortment to meet customer preferences. There is no assurance that these efforts will be successful or that we will be able to satisfy constantly changing customer demands. To the extent our decisions regarding our merchandise differ from our customers’ preferences, we may be faced with reduced sales and excess inventories for some products and/or missed opportunities for others. Any sustained failure to identify and respond to emerging trends in lifestyle and customer preferences and buying trends could have an adverse impact on our business. In addition, merchandise misjudgments may adversely impact the perception or reputation of our Company, which could result in declines in customer loyalty and vendor relationship issues, and ultimately have a material adverse effect on our business, financial condition and results of operations.

We may also seek to expand into new lines of business from time to time, such as offering large appliances for sale in our stores and online. There is no assurance that these efforts will be successful. Further, if we devote time and resources to new lines of business and those businesses are not as successful as we planned, then we risk damaging our overall business results. We also may not be able to develop new lines of business in a manner that improves our overall business and operating results and may therefore be forced to close the new lines of business, which may damage our reputation and negatively impact our operating results.

Our results may be negatively impacted if customers do not maintain their favorable perception of our Company and our private brand merchandise.

Maintaining and continually enhancing the value of our Company and our private brand merchandise is important to the success of our business. The value of our private brands is based in large part on the degree to which customers perceive and react to them. The value of our private brands could diminish significantly due to a number of factors, including customer perception that we have acted in an irresponsible manner in sourcing our private brand merchandise, adverse publicity about our private brand merchandise, our failure to maintain the quality of our private brand products, or the failure of our private brand merchandise to deliver consistently good value to the customer. The growing use of social and digital media by customers, us, and third parties increases the speed and extent that information or misinformation and opinions can be shared. Negative posts or comments about us, our private brands, or any of our merchandise on social or digital media could seriously damage our reputation. If we do not maintain the favorable perception of our Company and our private brand merchandise, our business results could be negatively impacted.

Our ability to increase sales and store productivity is largely dependent upon our ability to increase customer traffic and conversion.

Customer traffic depends upon our ability to successfully market compelling merchandise assortments as well as present an appealing shopping environment and experience to customers. Our strategies focus on increasing customer traffic and improving conversion in our stores and online; however, there can be no assurance that our efforts will be successful or will result in increased sales. In addition, external events outside of our control, including pandemics, terrorist threats, domestic conflicts and civil unrest, may influence customers' decisions to visit malls or might otherwise cause customers to avoid public places. There is no assurance that we will be able to reverse any decline in traffic or that increases in Internet sales will offset any decline in store traffic. We may need to respond to any declines in customer traffic or conversion rates by increasing markdowns or promotions to attract customers, which could adversely impact our gross margins, operating results and cash flows from operating activities.

8

If we are unable to manage our inventory effectively, our gross margins could be adversely affected.

Our profitability depends upon our ability to manage appropriate inventory levels and respond quickly to shifts in consumer demand patterns. We must properly execute our inventory management strategies by appropriately allocating merchandise among our stores and online, timely and efficiently distributing inventory to stores, maintaining an appropriate mix and level of inventory in stores and online, adjusting our merchandise mix between our private and exclusive brands and national brands, appropriately changing the allocation of floor space of stores among product categories to respond to customer demand and effectively managing pricing and markdowns. If we overestimate customer demand for our merchandise, we will likely need to record inventory markdowns and sell the excess inventory at clearance prices which would negatively impact our gross margins and operating results. If we underestimate customer demand for our merchandise, we may experience inventory shortages which may result in missed sales opportunities and have a negative impact on customer loyalty.

We must protect against security breaches or other unauthorized disclosures of confidential data about our customers as well as about our employees and other third parties.

As part of our normal operations, we and third-party service providers with whom we contract receive and maintain information about our customers (including credit/debit card information), our employees and other third parties. Confidential data must at all times be protected against security breaches or other unauthorized disclosure. We have, and require our third-party service providers to have, administrative, physical and technical safeguards and procedures in place to protect the security, confidentiality and integrity of such information and to protect such information against unauthorized access, disclosure or acquisition. Despite our safeguards and security processes and procedures, there is no assurance that all of our systems and processes, or those of our third-party service providers, are free from vulnerability to security breaches or inadvertent data disclosure or acquisition by third parties or us. Further, because the methods used to obtain unauthorized access change frequently and may not be immediately detected, we may be unable to anticipate these methods or promptly implement safeguards. Any failure to protect confidential data about our business or our customers, employees or other third parties could materially damage our brand and reputation as well as result in significant expenses and disruptions to our operations, and loss of customer confidence, any of which could have a material adverse impact on our business and results of operations. We could also be subject to government enforcement actions and private litigation as a result of any such failure.

The failure to retain, attract and motivate our employees, including employees in key positions, could have an adverse impact on our results of operations.

Our results depend on the contributions of our employees, including our senior management team and other key employees. This depends to a great extent on our ability to retain, attract and motivate talented employees throughout the organization, many of whom, particularly in the stores, are in entry level or part-time positions, which have historically had high rates of turnover. We currently operate with significantly fewer individuals than we have in the past who have assumed additional duties and responsibilities, which could have an adverse impact on our operating performance and efficiency. Negative media reports regarding the Company or the retail industry in general could also have an adverse impact on our ability to attract, retain and motivate our employees. If we are unable to retain, attract and motivate talented employees with the appropriate skill sets, we may not achieve our objectives and our results of operations could be adversely impacted. Our ability to meet our changing labor needs while controlling our costs is also subject to external factors such as unemployment levels, competing wages, potential union organizing efforts and increased government regulation. An inability to provide wages and/or benefits that are competitive within the markets in which we operate could adversely affect our ability to retain and attract employees. In addition, the loss of one or more of our key personnel or the inability to effectively identify a suitable successor to a key role in our senior management could have a material adverse effect on our business.

If we are unable to successfully develop and maintain a relevant and reliable omnichannel experience for our customers, our sales, results of operations and reputation could be adversely affected.

One of the pillars of our strategic framework is to deliver a superior omnichannel shopping experience for our customers through the integration of our store and digital shopping channels. Omnichannel retailing is rapidly evolving and we must anticipate and meet changing customer expectations. Our omnichannel initiatives include our ship-from-store and pickup-in-store programs and expansion of our SKU count online. In addition, we continue to explore ways to enhance our customers’ omnichannel shopping experience. These initiatives involve significant investments in IT systems and significant operational changes. In addition, our competitors are also investing in omnichannel initiatives, some of which may be more successful than our initiatives. If the implementation of our omnichannel initiatives is not successful or does not meet customer expectations, or we do not realize a return on our omnichannel investments, our reputation and operating results may be adversely affected.

9

Disruptions in our Internet website or mobile applications, or our inability to successfully execute our online strategies, could have an adverse impact on our sales and results of operations.

We sell merchandise over the Internet through our website, www.jcpenney.com, and through mobile applications for smart phones and tablets. Our Internet operations are subject to numerous risks, including rapid technological change and the implementation of new systems and platforms; liability for online and mobile content; violations of state or federal laws, including those relating to online and mobile privacy and intellectual property rights; credit card fraud; problems associated with the operation and security of our website, mobile applications and related support systems; computer viruses; telecommunications failures; electronic break-ins and similar disruptions; and the allocation of inventory between our online operations and department stores. The failure of our website or mobile applications to perform as expected could result in disruptions and costs to our operations and make it more difficult for customers to purchase merchandise online. In addition, our inability to successfully develop and maintain the necessary technological interfaces for our customers to purchase merchandise through our website and mobile applications, including user friendly software applications for smart phones and tablets, could result in the loss of Internet sales and have an adverse impact on our results of operations.

Our operations are dependent on information technology systems; disruptions in those systems or increased costs relating to their implementation could have an adverse impact on our results of operations.

Our operations are dependent upon the integrity, security and consistent operation of various systems and data centers, including the point-of-sale systems in the stores, our Internet website and mobile applications, data centers that process transactions, communication systems and various software applications used throughout our Company to track inventory flow, process transactions, generate performance and financial reports and administer payroll and benefit plans.

We have implemented several products from third party vendors to simplify our processes and reduce our use of customized existing legacy systems and expect to place additional applications into operation in the future. Implementing new systems carries substantial risk, including implementation delays, cost overruns, disruption of operations, potential loss of data or information, lower customer satisfaction resulting in lost customers or sales, inability to deliver merchandise to our stores or our customers, the potential inability to meet reporting requirements and unintentional security vulnerabilities. There can be no assurances that we will successfully launch the new systems as planned, that the new systems will perform as expected or that the new systems will be implemented without disruptions to our operations, any of which may cause critical information upon which we rely to be delayed, unreliable, corrupted, insufficient or inaccessible.

We also outsource various information technology functions to third party service providers and may outsource other functions in the future. We rely on those third party service providers to provide services on a timely and effective basis and their failure to perform as expected or as required by contract could result in disruptions and costs to our operations.

Our vendors are also highly dependent on the use of information technology systems. Major disruptions in their information technology systems could result in their inability to communicate with us or otherwise to process our transactions or information, their inability to perform required functions, or in the loss or corruption of our information, any and all of which could result in disruptions to our operations. Our vendors are responsible for having safeguards and procedures in place to protect the confidentiality, integrity and security of our information, and to protect our information and systems against unauthorized access, disclosure or acquisition. Any failure in their systems to operate or in their ability to protect our information or systems could have a material adverse impact on our business and results of operations.

We are in the process of insourcing certain business functions from third party vendors and may seek to relocate certain business functions to international locations in an attempt to achieve additional efficiencies, both of which subject us to risks, including disruptions in our business.

We are in the process of insourcing certain business functions and may also need to continue to insource other aspects of our business in the future in order to effectively manage our costs and stay competitive. We may also seek from time to time to relocate certain business functions to countries other than the United States to access highly skilled labor markets and further control costs. There is no assurance that these efforts will be successful. Further, these actions may cause disruptions that negatively impact our business. If we are ultimately unable to perform insourced functions better than, or at least as well as, our current third party providers, our operating results could be adversely impacted.

10

Changes in our credit ratings may limit our access to capital markets and adversely affect our liquidity.

The credit rating agencies periodically review our capital structure and the quality and stability of our earnings. Any future downgrades to our long-term credit ratings could result in reduced access to the credit and capital markets and higher interest costs on future financings. The future availability of financing will depend on a variety of factors such as economic and market conditions, the availability of credit and our credit ratings, as well as the possibility that lenders could develop a negative perception of us. There is no assurance that we will be able to obtain additional financing on favorable terms or at all.

Our profitability depends on our ability to source merchandise and deliver it to our customers in a timely and cost-effective manner.

Our merchandise is sourced from a wide variety of suppliers, and our business depends on being able to find qualified suppliers and access products in a timely and efficient manner. Inflationary pressures on commodity prices and other input costs could increase our cost of goods, and an inability to pass such cost increases on to our customers or a change in our merchandise mix as a result of such cost increases could have an adverse impact on our profitability. Additionally, the impact of economic conditions on our suppliers cannot be predicted and our suppliers may be unable to access financing or become insolvent and thus become unable to supply us with products.

Our arrangements with our suppliers and vendors may be impacted by our financial results or financial position.

Substantially all of our merchandise suppliers and vendors sell to us on open account purchase terms. There is a risk that our key suppliers and vendors could respond to any actual or apparent decrease in or any concern with our financial results or liquidity by requiring or conditioning their sale of merchandise to us on more stringent or more costly payment terms, such as by requiring standby letters of credit, earlier or advance payment of invoices, payment upon delivery or other assurances or credit support or by choosing not to sell merchandise to us on a timely basis or at all. Our arrangements with our suppliers and vendors may also be impacted by media reports regarding our financial position. Our need for additional liquidity could significantly increase and our supply of merchandise could be materially disrupted if a significant portion of our key suppliers and vendors took one or more of the actions described above, which could have a material adverse effect on our sales, customer satisfaction, cash flows, liquidity and financial position.

Our senior secured real estate term loan credit facility is secured by certain of our real property and substantially all of our personal property, and such property may be subject to foreclosure or other remedies in the event of our default. In addition, the real estate term loan credit facility contains provisions that could restrict our operations and our ability to obtain additional financing.

We are party to a $2.25 billion senior secured term loan credit facility that is secured by mortgages on certain real property of the Company, in addition to liens on substantially all personal property of the Company, subject to certain exclusions set forth in the credit and security agreement governing the term loan credit facility and related security documents. The real property subject to mortgages under the term loan credit facility includes our headquarters, distribution centers and certain of our stores.

The credit and guaranty agreement governing the term loan credit facility contains operating restrictions which may impact our future alternatives by limiting, without lender consent, our ability to borrow additional funds, execute certain equity financings or enter into dispositions or other liquidity enhancing or strategic transactions regarding certain of our assets, including our real property. Our ability to obtain additional or other financing or to dispose of certain assets could also be negatively impacted because a substantial portion of our owned assets have been pledged as collateral for repayment of our indebtedness under the term loan credit facility.

If an event of default occurs and is continuing, our outstanding obligations under the term loan credit facility could be declared immediately due and payable or the lenders could foreclose on or exercise other remedies with respect to the assets securing the term loan credit facility, including our headquarters, distribution centers and certain of our stores. If an event of default occurs, there is no assurance that we would have the cash resources available to repay such accelerated obligations or refinance such indebtedness on commercially reasonable terms, or at all. The occurrence of any one of these events could have a material adverse effect on our business, financial condition, results of operations and liquidity.

11

Our senior secured asset-based revolving credit facility limits our borrowing capacity to the value of certain of our assets. In addition, our senior secured asset-based revolving credit facility is secured by certain of our personal property, and lenders may exercise remedies against the collateral in the event of our default.

We are party to a $2.35 billion senior secured asset-based revolving credit facility. Our borrowing capacity under our revolving credit facility varies according to the Company’s inventory levels, accounts receivable and credit card receivables, net of certain reserves. In the event of any material decrease in the amount of or appraised value of these assets, our borrowing capacity would similarly decrease, which could adversely impact our business and liquidity.

Our revolving credit facility contains customary affirmative and negative covenants and certain restrictions on operations become applicable if our availability falls below certain thresholds. These covenants could impose significant operating and financial limitations and restrictions on us, including restrictions on our ability to enter into particular transactions and to engage in other actions that we may believe are advisable or necessary for our business.

Our obligations under the revolving credit facility are secured by liens with respect to inventory, accounts receivable, deposit accounts and certain related collateral. In the event of a default that is not cured or waived within any applicable cure periods, the lenders’ commitment to extend further credit under our revolving credit facility could be terminated, our outstanding obligations could become immediately due and payable, outstanding letters of credit may be required to be cash collateralized and remedies may be exercised against the collateral, which generally consists of the Company’s inventory, accounts receivable and deposit accounts and cash credited thereto. If we are unable to borrow under our revolving credit facility, we may not have the necessary cash resources for our operations and, if any event of default occurs, there is no assurance that we would have the cash resources available to repay such accelerated obligations, refinance such indebtedness on commercially reasonable terms, or at all, or cash collateralize our letters of credit, which would have a material adverse effect on our business, financial condition, results of operations and liquidity.

Our level of indebtedness may adversely affect our business and results of operations and may require the use of our available cash resources to meet repayment obligations, which could reduce the cash available for other purposes.

As of January 30, 2016, we have $4.805 billion in total indebtedness and we are highly leveraged. Our level of indebtedness may limit our ability to obtain additional financing, if needed, to fund additional projects, working capital requirements, capital expenditures, debt service, and other general corporate or other obligations, as well as increase the risks to our business associated with general adverse economic and industry conditions. Our level of indebtedness may also place us at a competitive disadvantage to our competitors that are not as highly leveraged.

We are required to make quarterly repayments in a principal amount equal to $5.625 million during the five-year term of the real estate term loan credit facility, subject to certain reductions for mandatory and optional prepayments. In addition, we are required to make prepayments of the real estate term loan credit facility with the proceeds of certain asset sales, insurance proceeds and excess cash flow, which will reduce the cash available for other purposes, including capital expenditures for store improvements, and could impact our ability to reinvest in other areas of our business.

There is no assurance that our internal and external sources of liquidity will at all times be sufficient for our cash requirements.

We must have sufficient sources of liquidity to fund our working capital requirements, capital improvement plans, service our outstanding indebtedness and finance investment opportunities. The principal sources of our liquidity are funds generated from operating activities, available cash and cash equivalents, borrowings under our credit facilities, other debt financings, equity financings and sales of non-operating assets. We expect our ability to generate cash through the sale of non-operating assets to diminish as our portfolio of non-operating assets decreases. In addition, our recent operating losses have limited our capital resources. Our ability to achieve our business and cash flow plans is based on a number of assumptions which involve significant judgments and estimates of future performance, borrowing capacity and credit availability, which cannot at all times be assured. Accordingly, there is no assurance that cash flows from operations and other internal and external sources of liquidity will at all times be sufficient for our cash requirements. If necessary, we may need to consider actions and steps to improve our cash position and mitigate any potential liquidity shortfall, such as modifying our business plan, pursuing additional financing to the extent available, reducing capital expenditures, pursuing and evaluating other alternatives and opportunities to obtain additional sources of liquidity and other potential actions to reduce costs. There can be no assurance that any of these actions would be successful, sufficient or available on favorable terms. Any inability to generate or obtain sufficient levels of liquidity to meet our cash requirements at the level and times needed could have a material adverse impact on our business and financial position.

12

Our ability to obtain any additional financing or any refinancing of our debt, if needed at any time, depends upon many factors, including our existing level of indebtedness and restrictions in our debt facilities, historical business performance, financial projections, prospects and creditworthiness and external economic conditions and general liquidity in the credit and capital markets. Any additional debt, equity or equity-linked financing may require modification of our existing debt agreements, which there is no assurance would be obtainable. Any additional financing or refinancing could also be extended only at higher costs and require us to satisfy more restrictive covenants, which could further limit or restrict our business and results of operations, or be dilutive to our stockholders.

Our use of interest rate hedging transactions could expose us to risks and financial losses that may adversely affect our financial condition, liquidity and results of operations.

To reduce our exposure to interest rate fluctuations, we have entered into, and in the future may enter into, interest rate swaps with various financial counterparties. The interest rate swap agreements effectively convert a portion of our variable rate interest payments to a fixed price. There can be no assurances, however, that our hedging activity will be effective in insulating us from the risks associated with changes in interest rates. In addition, our hedging transactions may expose us to certain risks and financial losses, including, among other things:

| • | counterparty credit risk; |

| • | the risk that the duration or amount of the hedge may not match the duration or amount of the related liability; |

| • | the hedging transactions may be adjusted from time to time in accordance with accounting rules to reflect changes in fair values, downward adjustments or “mark-to-market losses,” which would affect our stockholders’ equity; and |

| • | the risk that we may not be able to meet the terms and conditions of the hedging instruments, in which case we may be required to settle the instruments prior to maturity with cash payments that could significantly affect our liquidity. |

Further, we have designated the swaps as cash flow hedges in accordance with Accounting Standards Codification Topic 815, Derivatives and Hedging. However, in the future, we may fail to qualify for hedge accounting treatment under these standards for a number of reasons, including if we fail to satisfy hedge documentation and hedge effectiveness assessment requirements or if the swaps are not highly effective. If we fail to qualify for hedge accounting treatment, losses on the swaps caused by the change in their fair value will be recognized as part of net income, rather than being recognized as part of other comprehensive income.

Operating results and cash flows may cause us to incur asset impairment charges.

Long-lived assets, primarily property and equipment, are reviewed at the store level at least annually for impairment, or whenever changes in circumstances indicate that a full recovery of net asset values through future cash flows is in question. We also assess the recoverability of indefinite-lived intangible assets at least annually or whenever events or changes in circumstances indicate that the carrying amount may not be fully recoverable. Our impairment review requires us to make estimates and projections regarding, but not limited to, sales, operating profit and future cash flows. If our operating performance reflects a sustained decline, we may be exposed to significant asset impairment charges in future periods, which could be material to our results of operations.

Reductions in income and cash flow from our marketing and servicing arrangement related to our private label and co-branded credit cards could adversely affect our operating results and cash flows.

Synchrony Financial (“Synchrony”) owns and services our private label credit card and co-branded MasterCard® programs. Our agreement with Synchrony provides for certain payments to be made by Synchrony to the Company, including a share of revenues from the performance of the credit card portfolios. The income and cash flow that the Company receives from Synchrony is dependent upon a number of factors including the level of sales on private label and co-branded accounts, the percentage of sales on private label and co-branded accounts relative to the Company’s total sales, the level of balances carried on the accounts, payment rates on the accounts, finance charge rates and other fees on the accounts, the level of credit losses for the accounts, Synchrony’s ability to extend credit to our customers as well as the cost of customer rewards programs. All of these factors can vary based on changes in federal and state credit card, banking and consumer protection laws, which could also materially limit the availability of credit to consumers or increase the cost of credit to our cardholders. The factors affecting the income and cash flow that the Company receives from Synchrony can also vary based on a variety of economic,

13

legal, social and other factors that we cannot control. If the income or cash flow that the Company receives from our consumer credit card program agreement with Synchrony decreases, our operating results and cash flows could be adversely affected.

We are subject to customer payment-related risks that could increase operating costs, expose us to fraud or theft, subject us to potential liability and potentially disrupt our business.

We accept payments using a variety of methods, including cash, checks, credit and debit cards (including private label credit cards) and gift cards. Acceptance of these payment options subjects us to rules, regulations, contractual obligations and compliance requirements, including payment network rules and operating guidelines, data security standards and certification requirements, and rules governing electronic funds transfers. These requirements may change over time or be reinterpreted, making compliance more difficult or costly. The payment card industry set October 1, 2015 as the date on which liability shifted for certain debit and credit card transactions to retailers who are not able to accept EMV chip technology transactions. Implementation of the EMV chip technology and receipt of final certification is subject to the time availability of third-party service providers. As a result, we bear the chargeback risk for fraudulent transactions generated through EMV chip enabled cards before our implementation and certification of the EMV chip technology. Further, we may experience a decrease in transaction volume if we cannot process transactions for cardholders whose issuer has migrated entirely from magnetic strip to EMV chip enabled cards. Any prolonged inability to accept EMV chip technology transactions may subject us to increased risk of liability for fraudulent transactions and may adversely affect our business and operating results.

We are subject to risks associated with importing merchandise from foreign countries.

A substantial portion of our merchandise is sourced by our vendors and by us outside of the United States. All of our vendors must comply with our supplier legal compliance program and applicable laws, including consumer and product safety laws. Although we diversify our sourcing and production by country and supplier, the failure of a supplier to produce and deliver our goods on time, to meet our quality standards and adhere to our product safety requirements or to meet the requirements of our supplier compliance program or applicable laws, or our inability to flow merchandise to our stores or through the Internet channel in the right quantities at the right time, could adversely affect our profitability and could result in damage to our reputation.

Although we have implemented policies and procedures designed to facilitate compliance with laws and regulations relating to doing business in foreign markets and importing merchandise from abroad, there can be no assurance that suppliers and other third parties with whom we do business will not violate such laws and regulations or our policies, which could subject us to liability and could adversely affect our results of operations.

We are subject to the various risks of importing merchandise from abroad and purchasing product made in foreign countries, such as:

| • | potential disruptions in manufacturing, logistics and supply; |

| • | changes in duties, tariffs, quotas and voluntary export restrictions on imported merchandise; |

| • | strikes and other events affecting delivery; |

| • | consumer perceptions of the safety of imported merchandise; |

| • | product compliance with laws and regulations of the destination country; |

| • | product liability claims from customers or penalties from government agencies relating to products that are recalled, defective or otherwise noncompliant or alleged to be harmful; |

| • | concerns about human rights, working conditions and other labor rights and conditions and environmental impact in foreign countries where merchandise is produced and raw materials or components are sourced, and changing labor, environmental and other laws in these countries; |

| • | local business practice and political issues that may result in adverse publicity or threatened or actual adverse consumer actions, including boycotts; |

14

| • | compliance with laws and regulations concerning ethical business practices, such as the U.S. Foreign Corrupt Practices Act; and |

| • | economic, political or other problems in countries from or through which merchandise is imported. |

Political or financial instability, trade restrictions, tariffs, currency exchange rates, labor conditions, congestion and labor issues at major ports, transport capacity and costs, systems issues, problems in third party distribution and warehousing and other interruptions of the supply chain, compliance with U.S. and foreign laws and regulations and other factors relating to international trade and imported merchandise beyond our control could affect the availability and the price of our inventory. These risks and other factors relating to foreign trade could subject us to liability or hinder our ability to access suitable merchandise on acceptable terms, which could adversely impact our results of operations.

Disruptions and congestion at ports through which we import merchandise may increase our costs and/or delay the receipt of goods in our stores, which could adversely impact our profitability, financial position and cash flows.

We ship the majority of our private brand merchandise by ocean to ports in the United States. Our national brand suppliers also

ship merchandise by ocean. Disruptions in the operations of ports through which we import our merchandise, including but not

limited to labor disputes involving work slowdowns, lockouts or strikes, could require us and/or our vendors to ship merchandise by air freight or to alternative ports in the United States. Shipping by air is significantly more expensive than shipping by ocean which could adversely affect our profitability. Similarly, shipping to alternative ports in the United States could result in increased lead times and transportation costs. Disruptions at ports through which we import our goods could also result in unanticipated inventory shortages, which could adversely impact our reputation and our results of operations.

Our Company’s growth and profitability depend on the levels of consumer confidence and spending.

Our results of operations are sensitive to changes in overall economic and political conditions that impact consumer spending, including discretionary spending. Many economic factors outside of our control, including the housing market, interest rates, recession, inflation and deflation, energy costs and availability, consumer credit availability and terms, consumer debt levels, tax rates and policy, and unemployment trends influence consumer confidence and spending. The domestic and international political situation and actions also affect consumer confidence and spending. Additional events that could impact our performance include pandemics, terrorist threats and activities, worldwide military and domestic disturbances and conflicts, political instability and civil unrest. Declines in the level of consumer spending could adversely affect our growth and profitability.

Our business is seasonal, which impacts our results of operations.

Our annual earnings and cash flows depend to a great extent on the results of operations for the last quarter of our fiscal year, which includes the holiday season. Our fiscal fourth-quarter results may fluctuate significantly, based on many factors, including holiday spending patterns and weather conditions. This seasonality causes our operating results to vary considerably from quarter to quarter.

Our profitability may be impacted by weather conditions.

Our merchandise assortments reflect assumptions regarding expected weather patterns and our profitability depends on our ability to timely deliver seasonally appropriate inventory. Unseasonable or unexpected weather conditions such as warm temperatures during the winter season or prolonged or extreme periods of warm or cold temperatures could render a portion of our inventory incompatible with consumer needs. Extreme weather or natural disasters could also severely hinder our ability to timely deliver seasonally appropriate merchandise, preclude customers from traveling to our stores, delay capital improvements or cause us to close stores. A reduction in the demand for or supply of our seasonal merchandise could have an adverse effect on our inventory levels, gross margins and results of operations.

Changes in federal, state or local laws and regulations could increase our expenses and adversely affect our results of operations.

Our business is subject to a wide array of laws and regulations. Government intervention and activism and/or regulatory reform may result in substantial new regulations and disclosure obligations and/or changes in the interpretation of existing laws and regulations, which may lead to additional compliance costs as well as the diversion of our management’s time and attention from strategic initiatives. If we fail to comply with applicable laws and regulations we could be subject to legal risk, including

15

government enforcement action and class action civil litigation that could disrupt our operations and increase our costs of doing business. Changes in the regulatory environment regarding topics such as privacy and information security, product safety, environmental protection, including regulations in response to concerns regarding climate change, collective bargaining activities, minimum wage, wage and hour, and health care mandates, among others, as well as changes to applicable accounting rules and regulations, such as changes to lease accounting standards, could also cause our compliance costs to increase and adversely affect our business, financial condition and results of operations.

Legal and regulatory proceedings could have an adverse impact on our results of operations.

Our Company is subject to various legal and regulatory proceedings relating to our business, certain of which may involve jurisdictions with reputations for aggressive application of laws and procedures against corporate defendants. We are impacted by trends in litigation, including class action litigation brought under various consumer protection, employment, and privacy and information security laws. In addition, litigation risks related to claims that technologies we use infringe intellectual property rights of third parties have been amplified by the increase in third parties whose primary business is to assert such claims. Reserves are established based on our best estimates of our potential liability. However, we cannot accurately predict the ultimate outcome of any such proceedings due to the inherent uncertainties of litigation. Regardless of the outcome or whether the claims are meritorious, legal and regulatory proceedings may require that we devote substantial time and expense to defend our Company. Unfavorable rulings could result in a material adverse impact on our business, financial condition or results of operations.

Significant changes in discount rates, actual investment return on pension assets, and other factors could affect our earnings, equity, and pension contributions in future periods.

Our earnings may be positively or negatively impacted by the amount of income or expense recorded for our qualified pension plan. Generally accepted accounting principles in the United States of America (GAAP) require that income or expense for the plan be calculated at the annual measurement date using actuarial assumptions and calculations. The most significant assumptions relate to the capital markets, interest rates and other economic conditions. Changes in key economic indicators can change the assumptions. Two critical assumptions used to estimate pension income or expense for the year are the expected long-term rate of return on plan assets and the discount rate. In addition, at the measurement date, we must also reflect the funded status of the plan (assets and liabilities) on the balance sheet, which may result in a significant change to equity through a reduction or increase to other comprehensive income. We may also experience volatility in the amount of the annual actuarial gains or losses recognized as income or expense because we have elected to recognize pension expense using mark-to-market accounting. Although GAAP expense and pension contributions are not directly related, the key economic factors that affect GAAP expense would also likely affect the amount of cash we could be required to contribute to the pension plan. Potential pension contributions include both mandatory amounts required under federal law and discretionary contributions to improve a plan’s funded status.

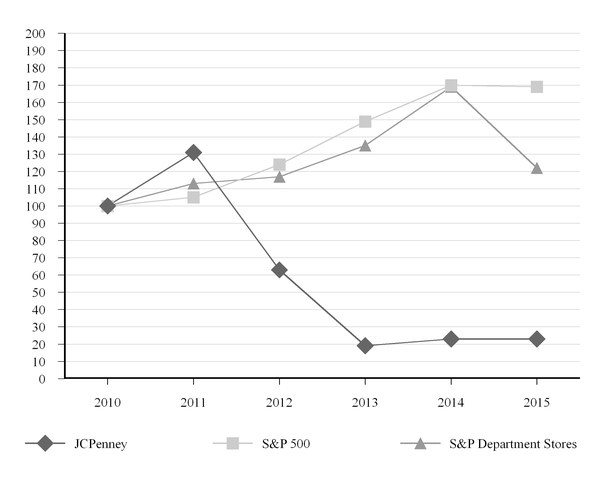

Our stock price has been and may continue to be volatile.

The market price of our common stock has fluctuated substantially and may continue to fluctuate significantly. Future announcements or disclosures concerning us or any of our competitors, our strategic initiatives, our sales and profitability, our financial condition, any quarterly variations in actual or anticipated operating results or comparable sales, any failure to meet analysts’ expectations and sales of large blocks of our common stock, among other factors, could cause the market price of our common stock to fluctuate substantially. In addition, the stock market has experienced price and volume fluctuations that have affected the market price of many retail and other stocks that have often been unrelated or disproportionate to the operating performance of these companies. This volatility could affect the price at which you could sell shares of our common stock.

Securities class action litigation has often been instituted against companies following periods of volatility in the overall market and in the market price of a company’s securities. The Company and certain of our current and former members of the Board of Directors and executives are defendants in a consolidated class action lawsuit and two related stockholder derivative actions that were filed following our announcement of an issuance of common stock on September 26, 2013. Such litigation could result in substantial costs, divert our management’s attention and resources and have an adverse effect on our business, results of operations and financial condition.

16

The Company’s ability to use net operating loss carryforwards to offset future taxable income for U.S. federal income tax purposes may be limited.

The Company has a federal net operating loss (NOL) of $2.6 billion as of January 30, 2016. These NOL carryforwards (expiring in 2032 through 2035) are available to offset future taxable income. The Company may recognize additional NOLs in the future.

Section 382 of the Internal Revenue Code of 1986, as amended (the Code) imposes an annual limitation on the amount of taxable income that may be offset by a corporation's NOLs if the corporation experiences an “ownership change” as defined in Section 382 of the Code. An ownership change occurs when the Company’s “five-percent shareholders” (as defined in Section 382 of the Code) collectively increase their ownership in the Company by more than 50 percentage points (by value) over a rolling three-year period. Additionally, various states have similar limitations on the use of state NOLs following an ownership change.

If an ownership change occurs, the amount of the taxable income for any post-change year that may be offset by a pre-change loss is subject to an annual limitation that is cumulative to the extent it is not all utilized in a year. This limitation is derived by multiplying the fair market value of the Company stock as of the ownership change by the applicable federal long-term tax-exempt rate, which was 2.65% at January 30, 2016. To the extent that a company has a net unrealized built-in gain at the time of an ownership change, which is realized or deemed recognized during the five-year period following the ownership change, there is an increase in the annual limitation for each of the first five-years that is cumulative to the extent it is not all utilized in a year.

The Company has an ongoing study of the rolling three-year testing periods. Based upon the elections the Company has made and the information that has been filed with the Securities and Exchange Commission through January 30, 2016, the Company has not had a Section 382 ownership change through January 30, 2016.

If an ownership change should occur in the future, the Company’s ability to use the NOL to offset future taxable income will be subject to an annual limitation and will depend on the amount of taxable income generated by the Company in future periods. There is no assurance that the Company will be able to fully utilize the NOL and the Company could be required to record an additional valuation allowance related to the amount of the NOL that may not be realized, which could impact the Company’s result of operations.

We believe that these NOL carryforwards are a valuable asset for us. Consequently, we have a stockholder rights plan in place, which was approved by the Company’s stockholders, to protect our NOLs during the effective period of the rights plan. Although the rights plan is intended to reduce the likelihood of an “ownership change” that could adversely affect us, there is no assurance that the restrictions on transferability in the rights plan will prevent all transfers that could result in such an “ownership change”.

The rights plan could make it more difficult for a third party to acquire, or could discourage a third party from acquiring, our Company or a large block of our common stock. A third party that acquires 4.9% or more of our common stock could suffer substantial dilution of its ownership interest under the terms of the rights plan through the issuance of common stock or common stock equivalents to all stockholders other than the acquiring person.

The foregoing provisions may adversely affect the marketability of our common stock by discouraging potential investors from acquiring our stock. In addition, these provisions could delay or frustrate the removal of incumbent directors and could make more difficult a merger, tender offer or proxy contest involving us, or impede an attempt to acquire a significant or controlling interest in us, even if such events might be beneficial to us and our stockholders.

Item 1B. Unresolved Staff Comments

None.

17

Item 2. Properties

At January 30, 2016, we operated 1,021 department stores throughout the continental United States, Alaska and Puerto Rico, of which 418 were owned, including 118 stores located on ground leases. The following table lists the number of stores operating by state as of January 30, 2016:

| Alabama | 20 | Maine | 6 | Oklahoma | 19 | |||||

| Alaska | 1 | Maryland | 18 | Oregon | 13 | |||||

| Arizona | 22 | Massachusetts | 10 | Pennsylvania | 35 | |||||

| Arkansas | 16 | Michigan | 41 | Rhode Island | 2 | |||||

| California | 80 | Minnesota | 25 | South Carolina | 16 | |||||

| Colorado | 21 | Mississippi | 15 | South Dakota | 7 | |||||

| Connecticut | 8 | Missouri | 26 | Tennessee | 25 | |||||

| Delaware | 3 | Montana | 7 | Texas | 91 | |||||

| Florida | 55 | Nebraska | 11 | Utah | 9 | |||||

| Georgia | 27 | Nevada | 7 | Vermont | 4 | |||||

| Idaho | 9 | New Hampshire | 9 | Virginia | 24 | |||||

| Illinois | 37 | New Jersey | 14 | Washington | 22 | |||||

| Indiana | 27 | New Mexico | 10 | West Virginia | 9 | |||||

| Iowa | 15 | New York | 42 | Wisconsin | 14 | |||||

| Kansas | 19 | North Carolina | 29 | Wyoming | 5 | |||||

| Kentucky | 22 | North Dakota | 8 | Puerto Rico | 7 | |||||

| Louisiana | 16 | Ohio | 43 | |||||||

| Total square feet | 104.7 million | |||||||||

In May 2013, we entered into a $2.25 billion five-year senior secured term loan that is secured by mortgages on certain real property of the Company, in addition to liens on substantially all personal property of the Company, subject to certain exclusions set forth in the credit and security agreement governing the term loan credit facility and related security documents. The real property subject to mortgages under the term loan credit facility includes our headquarters, distribution centers and certain of our stores.

18

At January 30, 2016, our supply chain network operated 13 facilities with multiple types of distribution activities, including store merchandise distribution centers (stores), regional warehouses (regional), jcpenney.com fulfillment centers (direct to customers) and furniture distribution centers (furniture) as indicated in the following table:

| Square Footage | |||||||

| Location | Leased/Owned | Primary Function(s) | (in thousands) | ||||

| Manchester, Connecticut | Owned | stores, furniture | 2,120 | ||||

| Lenexa, Kansas | Owned | stores, direct to customers | 1,944 | ||||

| Columbus, Ohio | Owned | stores, direct to customers | 1,902 | ||||

| Milwaukee, Wisconsin | Owned | stores, furniture | 1,869 | ||||

| Atlanta, Georgia | Owned | stores, regional, furniture | 1,764 | ||||

| Reno, Nevada | Owned | regional, direct to customers | 1,660 | ||||

| Buena Park, California | Owned | stores, regional, furniture | 1,082 | ||||

| Alliance, Texas | Owned | regional | 1,071 | ||||

| Statesville, North Carolina | Owned | stores, regional | 595 | ||||

| Lathrop, California | Leased | regional | 436 | ||||

| Cedar Hill, Texas | Leased | stores | 420 | ||||

| Spanish Fork, Utah | Leased | stores | 400 | ||||

| Lakeland, Florida | Leased | stores | 360 | ||||

| Total supply chain network | 15,623 | ||||||

19

Item 3. Legal Proceedings

The matters under the caption "Litigation" in Note 21 of the Notes to Consolidated Financial Statements attached to this Form 10-K are incorporated herein by reference.

Item 4. Mine Safety Disclosures

Not applicable.

20

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market for Registrant’s Common Equity

Our common stock is traded principally on the New York Stock Exchange (NYSE) under the symbol “JCP.” The number of stockholders of record at March 11, 2016, was 24,791. In addition to common stock, we have authorized 25 million shares of preferred stock, of which no shares were issued and outstanding at January 30, 2016.

The table below sets forth the quoted high and low intraday sale prices of our common stock on the NYSE for each quarterly period indicated and the quarter-end closing market price of our common stock:

| Fiscal Year 2015 | First Quarter | Second Quarter | Third Quarter | Fourth Quarter | ||||||||||||

| Market price: | ||||||||||||||||

| High | $ | 9.50 | $ | 9.39 | $ | 10.09 | $ | 9.34 | ||||||||

| Low | $ | 7.01 | $ | 8.02 | $ | 7.21 | $ | 6.00 | ||||||||

| Close | $ | 8.43 | $ | 8.24 | $ | 9.17 | $ | 7.26 | ||||||||

| Fiscal Year 2014 | First Quarter | Second Quarter | Third Quarter | Fourth Quarter | ||||||||||||

| Market price: | ||||||||||||||||

| High | $ | 9.28 | $ | 9.93 | $ | 11.30 | $ | 8.30 | ||||||||

| Low | $ | 4.90 | $ | 8.03 | $ | 6.73 | $ | 5.90 | ||||||||

| Close | $ | 8.58 | $ | 9.63 | $ | 7.61 | $ | 7.27 | ||||||||

Since May 2012, the Company has not paid a dividend. Under our 2013 senior secured term loan and 2014 senior secured asset-based credit facility, we are subject to restrictive covenants regarding our ability to pay cash dividends.