Exhibit 13

On Demand is in.

Broadband is booming.

Voice is growing stronger.

Convergence is real.

Comcast is on.

[comcast logo] 2005 Annual Report

The digital world isn’t just the future.

It’s here now.

And as it accelerates, so do

Comcast’s opportunities for growth.

2 Opportunities for Growth Comcast 2005 Annual Report

1

We’re expanding our reach and relationships.

> | | We added 1.5 million new high-speed Internet, 1.1 million new digital cable and 202,000 Comcast Digital Voice customers in 2005, driving our average monthly revenue per customer from $77 to $84. |

> | | We now exceed 22.4 million customer relationships, and new products continue to expand our growth potential among the 41.6 million homes in our markets. |

Comcast 2005 Annual Report Opportunities for Growth 3

2

Our products deliver a superior experience.

> | | Our growing ON DEMAND library attracted more than 1.4 billion views in 2005, nearly a 150 percent jump over the previous year. |

> | | We keep raising the bar for Internet performance — increasing speeds to 6 and 8 megabits per second and adding features that deliver a better broadband experience. |

4 Opportunities for Growth Comcast 2005 Annual Report

3

We have the bandwidth to grow.

> Our fiber-rich network delivers what customers want today — including more ON DEMAND, more HD programming and faster Internet speeds — and it has the capacity to meet future demand without rebuilding.

> | | We’re working on technology to deliver broadband speeds of 200 megabits per second and beyond — surpassing today’s top speed by 25 times or more — over our existing network. |

Comcast 2005 Annual Report Opportunities for Growth 5

4

We’re positioned to lead a converging world.

> | | With Sprint Nextel, we are developing new wireless products that will provide integrated entertainment and communications services to customers, at home and wherever they go. |

> | | We’re working with industry leaders — including Microsoft, Motorola, Panasonic, Pace, Samsung and TiVo — to develop next-generation digital |

devices | | that will expand our offerings and our competitive advantage. |

6 Opportunities for Growth Comcast 2005 Annual Report

5

We are funded for the future.

> | | We generated $2.6 billion in free cash flow in reinvesting these funds in initiatives to extend our leadership position and return value to shareholders through stock buybacks. |

> | | Since, we have invested $1.9 billion in our business and $5 billion in our stock, while maintaining a strong investment grade rating. |

Comcast is on.

Comcast 2005 Annual Report Letter to Shareholders 9

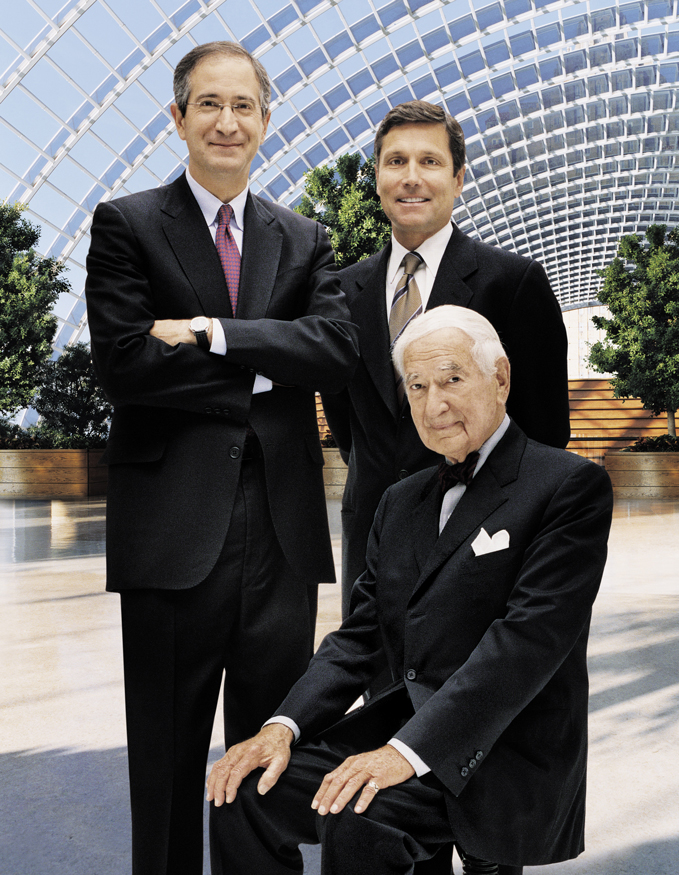

< Brian L. Roberts (left)

Chairman and Chief Executive Officer

Ralph J. Roberts (seated)

Chairman, Executive and Finance Committee

Stephen B. Burke (right)

Executive Vice President and Chief Operating Officer; President, Comcast Cable

Dear Comcast Shareholders, Employees and Friends:

The digital world—once a distant dream—is finally here. Televisions, computers, telephones and other electronic devices are all converging at an accelerating rate. This transformation is already changing the way we live, giving consumers greater convenience, choice and control than ever before. It’s also creating significant new growth opportunities for companies like ours.

Comcast is at the center of this transformation, delivering the products consumers want today and investing in the exciting innovations that will shape tomorrow. Over the past decade, we’ve grown from a single-product regional cable provider to the nation’s largest integrated video, broadband and communications company with 22.4 million customers and a network that passes 41.6 million homes—or about one in every 3.5 homes in the country.

By continuously enhancing our products—and staying at the forefront of rapidly changing consumer trends and technologies—we have been able to deliver superior operating and financial performance and position ourselves for future growth.

10 Letter to Shareholders Comcast 2005 Annual Report

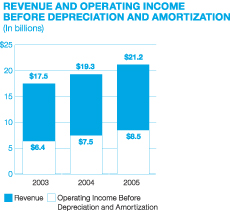

In 2005, consolidated revenues increased 9.6 percent to $22.3 billion. Operating cash flow(1) rose 12.8 percent to $8.5 billion, our fifth straight year of double-digit growth.

During the year, we sold more than 2.6 million new products—or revenue generating units (RGUs), as they are known in the industry—and increased our average monthly revenue per customer from $77 to nearly $84. To build on this momentum, we strengthened our fiber-rich cable infrastructure — creating a truly “converged” network —to facilitate the deployment of new services, including Comcast Digital Voice. We also partnered with technology and consumer electronics leaders to drive innovation and expand our services across all platforms.

At the same time, we expanded our ON DEMAND library with hundreds of movies from Sony and Starz/Encore, premiered PBS KIDS Sprout, and launched partnerships with the National Hockey League and, most recently, the PGA TOUR. These investments not only increase the value of our cable networks, they also enable us to provide unique content to Comcast customers and to differentiate our products in the marketplace.

Where Others See Uncertainty, We See Opportunity

Despite our strong results in 2005, the value of Comcast common stock declined 22 percent, compared to a 3 percent increase in the S&P 500 during the year. Why the disconnect? The most likely explanation is that unprecedented changes are taking place in the way communications services and content are delivered to consumers. Comcast has been at the leading edge of this transition. But with so many new contenders and approaches in the marketplace, there is a fog of uncertainty about who the winners and losers will be.

While no one can predict the future, I believe tomorrow’s leaders will be those companies that master change and provide customers with exciting new products and services that make their

(1) See definitions on page 16.

140 million ON DEMAND programs were viewed in December, including 15 million free movies, 18 million kids’ shows and 30 million music programs.

89 of all ON DEMAND users say it enhances the digital experience, 72 percent say it has improved the value of our service.

Comcast 2005 Annual Report Letter to Shareholders 11

lives easier, more efficient—and a whole lot more fun. At Comcast, that is exactly our game plan. We are building a superior communications and entertainment experience that will enable us to sustain our growth and deliver long-term value to shareholders.

Transforming the Television Experience

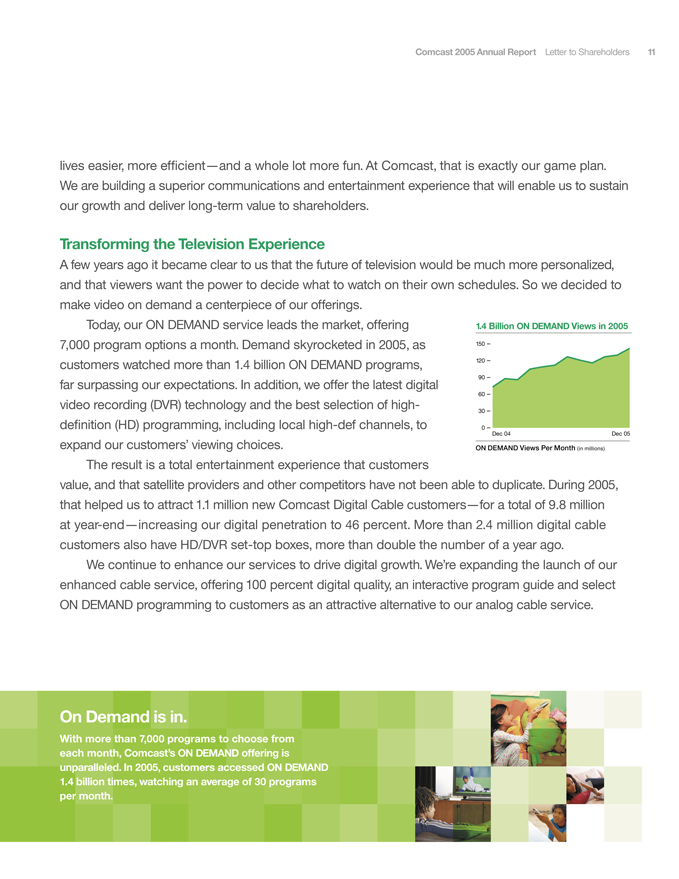

A few years ago it became clear to us that the future of television would be much more personalized, and that viewers want the power to decide what to watch on their own schedules. So we decided to make video on demand a centerpiece of our offerings.

[ILLUSTRATED GRAPH]

Today, our ON DEMAND service leads the market, offering 7,000 program options a month. Demand skyrocketed in 2005, as customers watched more than 1.4 billion ON DEMAND programs, far surpassing our expectations. In addition, we offer the latest digital video recording (DVR) technology and the best selection of high-definition (HD) programming, including local high-def channels, to expand our customers’ viewing choices.

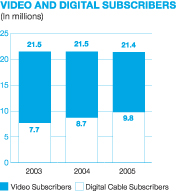

The result is a total entertainment experience that customers value, and that satellite providers and other competitors have not been able to duplicate. During 2005, that helped us to attract 1.1 million new Comcast Digital Cable customers—for a total of 9.8 million at year-end —increasing our digital penetration to 46 percent. More than 2.4 million digital cable customers also have HD/DVR set-top boxes, more than double the number of a year ago.

We continue to enhance our services to drive digital growth. We’re expanding the launch of our enhanced cable service, offering 100 percent digital quality, an interactive program guide and select ON DEMAND programming to customers as an attractive alternative to our analog cable service.

On Demand is in.

With more than 7,000 programs to choose from each month, Comcast’s ON DEMAND offering is unparalleled. In 2005, customers

accessed ON DEMAND 1.4 billion times, watching an average of 30 programs per month.

12 Letter to Shareholders Comcast 2005 Annual Report

Taking High-Speed Internet to a Higher Level

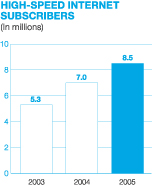

As the country’s No. 1 high-speed Internet provider, Comcast is in an excellent position to capitalize on the explosive growth of broadband services. During 2005, we increased revenues from our high-speed Internet business by almost 28 percent and added 1.5 million customers, bringing our total to more than 8.5 million.

[ILLUSTRATED GRAPH]

While some companies have chosen to compete almost solely on price, we focus on delivering greater value, better service and enhanced features. This strategy continues to be successful as we maintained our average monthly revenue per customer above $42.

Speed is essential to the equation. During 2005, we made Comcast High-Speed Internet a faster and richer experience for our customers, increasing our broadband speeds to 6 and 8 megabits per second. We’ll continue to increase these speeds over time to maintain our competitive advantage.

In addition, we plan to keep adding innovative features like Video Mail, PhotoShow, Comcast Rhapsody Radio PLUS and The Fan™—a fast and easy way to search, save and view video on the Internet. In 2005, our customers downloaded more than 400 million video clips through The Fan. There is no question that video will become increasingly important on every device, including the computer. As the leader in both cable and broadband, we believe Comcast has an advantage in this emerging market.

Delivering a Superior Communications Service

During 2005, we launched Comcast Digital Voice to more than 16 million homes in 25 markets, and achieved our year-end target by adding 202,000 new customers. Early reviews have been outstanding:

8.5 million households now have Comcast High-Speed Internet service, making us the No. 1 broadband service provider in the country.

84% of consumers interested in broadband say that a faster connection is among their key decision-making criteria.

Comcast 2005 Annual Report Letter to Shareholders 13

Business Week called Comcast Digital Voice a “standout” among Internet-based phone products, and 92 percent of our customers rated our service good to excellent.

Building on this success, we’ll continue to enhance Comcast Digital Voice and expand its rollout across all of our markets. Our goal is to add at least 1 million new customers in 2006, and to grow to 8 million customers within five years, representing roughly 20 percent penetration of the homes in our markets.

To expand our capabilities, we have formed a joint venture with Sprint Nextel and leading cable companies to offer our customers a combination of wireless, video, high-speed Internet and digital voice services. Through this joint venture, we will launch a new generation of products that will provide customers with a wide range of new anywhere/anytime services—from “video over phone” and remote TV programming, to fast and easy access to e-mail, voice mail and video mail across a variety of devices.

Unlocking the Power of the Bundle

Convergence is clearly the next wave of growth. With our technology platform in place—and our three services available across most of our markets this year—Comcast is ready to capture the opportunity. Among our initiatives: marketing packages (or “bundles”) of services to many more of the 41.6 million homes in our markets.

We have already tested several of these bundled product offerings in select markets with great success. Not only are these bundles helping us to deepen our existing customer relationships, but they are also enabling us to build new relationships with the nearly 20 million homes in our markets that haven’t yet purchased one of our products.

Broadband is booming. With speeds of 6 to 8 megabits per second and dozens of new enhancements, including advanced security features, Comcast High-Speed Internet keeps getting better. Our goal: to deliver the best speed, reliability and broadband content

available of the Internet—all in a way that’s fast, easy and unbelievably fun.

14 Letter to Shareholders Comcast 2005 Annual Report

During 2005, we reorganized our management team to focus the talent of our people company-wide, creating one operations team, one marketing and product development team, and one engineering team to serve all of our products—video, voice, data and wireless. As convergence continues to take hold, this new structure will improve our ability to develop better and more integrated services that are also easier for customers to purchase and use.

[ILLUSTRATED GRAPH]

We Are Positioned to Compete—and Determined to Win

We finished 2005 with one of the strongest balance sheets in our history. All three major rating agencies upgraded our debt ratings during the year, and we are now solidly investment grade.

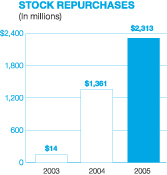

Free cash flow(1) for the year reached $2.6 billion, helping us to invest $786 million in new content and technologies to drive future growth and to reinvest $2.3 billion in our stock. Over the past two years, we have invested $5 billion in our stock and related securities, representing approximately 7.5 percent of our shares outstanding. Our Board recently authorized an additional stock buyback of up to $5 billion.

We will apply a similar game plan in 2006, investing to differentiate our products and launching new services while buying back stock at what we think are attractive levels, given our opportunities for growth. We’ll expand our programming and seek new opportunities to increase the value of our content portfolio. We’re committed to creating new offerings that clearly distinguish Comcast products in the marketplace.

At the same time, we’ll continue to invest in the development of our people, and I believe this will prove to be one of our greatest competitive advantages. Steve Burke’s vision and energy—coupled with the core values that my father, Ralph, cemented here long ago—have

(1)

See definitions on page 16.

Comcast 2005 Annual Report Letter to Shareholders 15

helped us build an organization that is not only a leader of the cable industry, but also of the evolving digital world. We cannot thank each of our 80,000 employees enough for their outstanding efforts in 2005. Their hard work and unflinching determination have enabled us to build a powerful new engine for growth that will drive our business to higher and higher levels of performance.

For all of these reasons, I remain firmly confident in our approach, our business strategy and our team. My confidence only grew as I walked the floor of the Consumer Electronics Show earlier this year. As I talked to business leaders there—from device manufacturers and technology giants to leading content companies—I kept hearing the same sentiments voiced over and over again, including “make it simple,” “give consumers more choices” and “put the customer in control.”

The experience was energizing, because these watchwords have guided every decision we’ve made at Comcast for the past decade. We’ll continue to maintain this focus in everything we do, as we seek to expand our leadership as America’s preferred broadband communications service provider.

It’s a great privilege to help manage this amazing company.

Sincerely,

[SIGNATURE]

Brian L. Roberts

Chairman and Chief Executive Officer Comcast Corporation February 21, 2006

Voice is growing stronger.

We made Comcast Digital Voice easy to use and set up, including professional installation. The service features unlimited local and domestic long-distance calling, Web access to voice mail, Enhanced 911 service, and a dozen other popular calling features, all for one

low monthly price.

16 Financial Highlights Comcast 2005 Annual Report

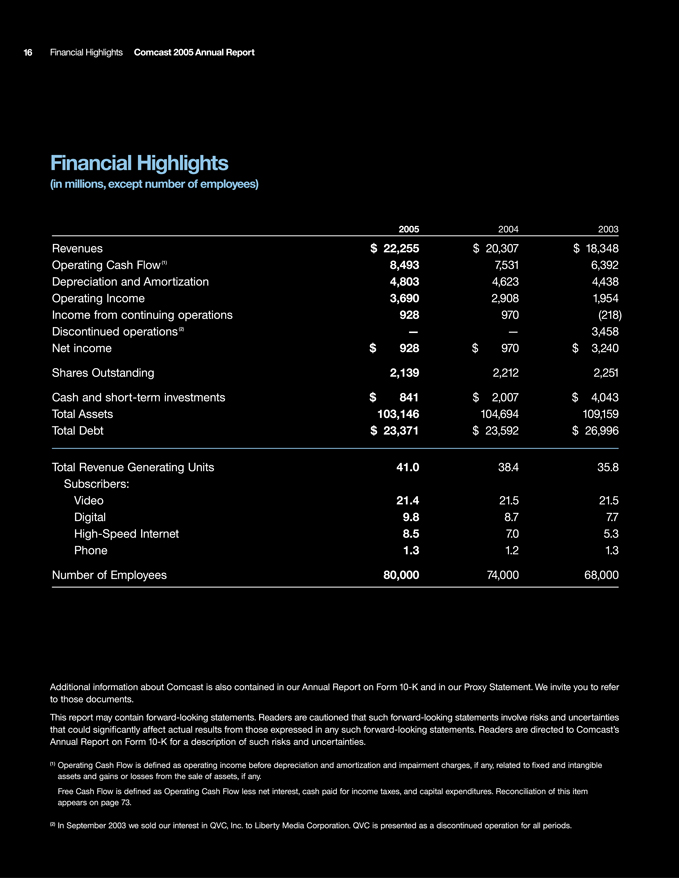

Financial Highlights

(in millions, except number of employees)

2005 2004 2003

Revenues $22,255 $20,307 $18,348

Operating Cash Flow(1) 8,493 7,531 6,392

Depreciation and Amortization 4,803 4,623 4,438

Operating Income 3,690 2,908 1,954

Income from continuing operations 928 970 (218)

Discontinued operations(2) — — 3,458

Net income $928 $970 $3,240

Shares Outstanding 2,139 2,212 2,251

Cash and short-term Investments $841 $2,007 $4,043

Total Assets 103,146 104,694 109,159

Total Debt $23,371 $23,592 $26,996

Total Revenue Generating Units 41.0 38.4 35.8

Subscribers:

Video 214.4 21.5 21.5

Digital 9.8 8.7 7.7

High-Speed Internet 8.5 7.0 5.3

Phone 1.3 1.2 1.3

Number of Employees 80,000 74,000 68,000

Additional information about Comcast is also contained in our Annual Report on Form 10-K and in our Proxy Statement. We invite you to refer to those documents.

This report may contain forward-looking statements. Readers are cautioned that such forward-looking statements involve risks and uncertainties that could significantly affect actual results from those expressed in any such forward-looking statements. Readers are directed to Comcast’s Annual Report on Form 10-K for a description of such risks and uncertainties.

(1) Operating Cash Flow is defined as operating income before depreciation and amortization and impairment charges, if any, related to fixed and intangible assets and gains or losses from the sale of assets, if any.

Free Cash Flow is defined as Operating Cash Flow less net interest, cash paid for income taxes, and capital expenditures. Reconciliation of this item appears on page 73.

(2) In September 2003 we sold our interest in QVC, Inc. to Liberty Media Corporation. QVC is presented as a discontinued operation for all periods.

| | | | | | |

| | | Comcast 2005 Annual Report | | Financial Report | | 17 |

Financial Report

| | | | |

| 18 | | MD&A | | Comcast 2005 Annual Report |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Introduction and Overview

We are the nation’s largest broadband cable provider and offer a wide variety of consumer entertainment and communication products and services, serving more than 21 million video subscribers, 8 million high-speed Internet subscribers and 1 million phone subscribers. Our broadband cable systems pass over 41 million homes in 35 states and the District of Columbia, including a presence in 22 of the nation’s major television markets, commonly known as DMAs. We also have a controlling interest in six national cable networks and other sports and entertainment related businesses. During 2005, our operations generated consolidated revenues of more than $22 billion.

We classify our operations in two reportable segments: Cable and Content. Our Cable segment develops, manages and operates our broadband cable systems, including video, high-speed Internet and phone services (“cable services”).

The majority of our Cable segment revenue is earned from monthly subscriptions for these cable services. Other revenue sources include advertising sales and the operation of our regional sports and news networks. In 2002, our Cable segment more than doubled in size with the acquisition of AT&T Corporation’s broadband cable business, which we refer to as “Broadband.” The Broadband cable systems at that time included 12.8 million subscribers and other cable-related investments. The Cable segment generates approximately 95% of our consolidated revenues.

Our Content segment consists of our six national cable networks: E! Entertainment Television; Style Network; The Golf Channel;

OLN; G4; and AZN Television. Revenue from our Content segment is earned primarily from advertising sales and from monthly per subscriber license fees paid by cable system operators and satellite television companies.

Our other business interests include Comcast Spectacor, which owns the Philadelphia Flyers, the Philadelphia 76ers and two large multipurpose arenas in Philadelphia, and manages other facilities for sporting events, concerts and other events. Comcast Spectacor and all other businesses not included in our Cable or Content segments are included in “Corporate and Other” activities.

In 2003, we completed the sale to Liberty Media Corporation of our approximate 57% interest in QVC, Inc. (an electronic retailer) for a total value of approximately $7.7 billion. We present financial information about QVC, Inc. as a discontinued operation in our consolidated financial statements.

Highlights for 2005 include the following:

| > | Consolidated revenue growth of approximately 9.6% and operating income growth of 26.9%, driven primarily by subscriber growth in our digital cable and high-speed Internet services and price increases in our video service offerings. |

| > | The launch of Comcast Digital Voice, our Internet-Protocol (“IP”)-enabled phone service, in 25 markets. |

| > | The repurchase of approximately $2.3 billion of our Class A Special common stock under our Board-authorized share repurchase program. |

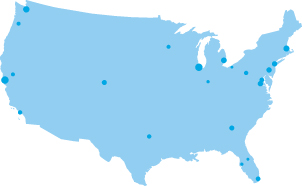

The map below shows the 22 major television markets where we operate and the approximate number of total video subscribers we serve in each of those markets as of December 31, 2005. Approximately 70% of our total video subscribers are in these markets.

(Subscribers in millions)

| | | | |

| | |

| 0.7 Atlanta | | 0.2 Indianapolis | | 0.4 Portland |

| | |

| 0.6 Baltimore | | 0.5 Los Angeles | | 0.4 Sacramento |

| | |

| 1.0 Boston | | 0.6 Miami | | 1.4 San Francisco |

| | |

| 1.6 Chicago | | 0.8 New York | | 1.1 Seattle |

| | |

| 0.1 Cleveland | | 0.1 Orlando | | 0.4 St. Paul/Minneapolis |

| | |

| 0.5 Dallas | | 1.8 Philadelphia | | 0.2 Tampa/Sarasota |

| | |

| 0.7 Denver | | 0.5 Pittsburgh | | 0.8 Washington, D.C. |

| | |

| 0.9 Detroit | | | | |

| | | | |

| Comcast 2005 Annual Report | | MD&A | | 19 |

| > | Investments in our Content segment to provide more programming options, the most significant of which are: |

| | • | | In April 2005, we completed a transaction with a group of investors to acquire Metro-Goldwyn-Mayer Inc. (“MGM”). We acquired our 20% interest for approximately $250 million in cash. This transaction contemplates the inclusion of Sony Pictures and MGM programming in our Video on Demand (“VOD”) service. |

| | • | | In August 2005, we acquired the rights to broadcast National Hockey League games on OLN for the next two years, with options to televise additional seasons. OLN’s coverage of NHL games began in October 2005, with some hockey programming also available on VOD and our high-speed Internet service. |

| | • | | In September 2005, we, together with a group of investors, launched PBS KIDS Sprout, a new 24/7 cable network designed for preschoolers. Some of Sprout’s programming is also available on VOD and our high-speed Internet service. |

| > | A joint venture with Sprint Nextel Corporation (“Sprint”), Time Warner Cable, Cox Communications and Advance/Newhouse Communications to develop communication and entertainment products for consumers that combine our cable products and interactive features with wireless technology. |

| > | The continued investment in technologies that allow us greater control over the development, delivery and quality of our advanced digital cable services. |

| > | Agreements for the following transactions, which we expect to close in 2006, that will allow us to continue to grow the number of subscribers in new and existing markets: |

| | • | | In April 2005 we entered into agreements with Time Warner to: (i) jointly acquire substantially all the assets of Adelphia Communications Corporation; (ii) redeem our interest in Time Warner Cable and its subsidiary, Time Warner Entertainment; and (iii) exchange certain cable systems with Time Warner Cable. As a result of these transactions, on a net basis, our cash investment is expected to be $1.5 billion and we expect to gain approximately 1.7 million video subscribers in complementary geographic areas (including South Florida, New England, MidAtlantic and Minnesota). The cable systems we expect to transfer to Time Warner in the exchange are located in Los Angeles, Cleveland and Dallas. |

| | • | | In October 2005, we entered into an agreement with Susquehanna Communications, an organization in which we own an approximate 30% interest, to acquire Susquehanna’s cable systems for $775 million. As a result of this transaction, we expect to add approximately 225,000 video subscribers. |

Refer toNote 5to our consolidated financial statements for information about acquisitions and other significant events.

Consolidated Operating Results

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | % Change | | | % Change | |

| Year Ended December 31 (Dollars in millions) | | 2005 | | | | | 2004 | | | 2003 | | | 2004 to 2005 | | | 2003 to 2004 | |

Revenues | | $ | 22,255 | | | | | $ | 20,307 | | | $ | 18,348 | | | 9.6 | % | | 10.7 | % |

Costs and Expenses | | | | | | | | | | | | | | | | | | | | |

Operating, selling, general and administrative (excluding depreciation) | | | 13,762 | | | | | | 12,776 | | | | 11,956 | | | 7.7 | | | 6.9 | |

Depreciation | | | 3,630 | | | | | | 3,420 | | | | 3,166 | | | 6.1 | | | 8.0 | |

Amortization | | | 1,173 | | | | | | 1,203 | | | | 1,272 | | | (2.5 | ) | | (5.4 | ) |

Operating Income | | | 3,690 | | | | | | 2,908 | | | | 1,954 | | | 26.9 | | | 48.8 | |

Other Income (Expense) Items, Net | | | (1,810 | ) | | | | | (1,098 | ) | | | (2,091 | ) | | 64.8 | | | (47.5 | ) |

Income (Loss) from Continuing Operations before Income Taxes and Minority Interest | | | 1,880 | | | | | | 1,810 | | | | (137 | ) | | 3.9 | | | n/m | |

Income Tax (Expense) Benefit | | | (933 | ) | | | | | (826 | ) | | | 16 | | | 13.0 | | | n/m | |

Income (Loss) from Continuing Operations before Minority Interest | | | 947 | | | | | | 984 | | | | (121 | ) | | (3.8 | ) | | n/m | |

Minority Interest | | | (19 | ) | | | | | (14 | ) | | | (97 | ) | | 35.7 | | | (85.6 | ) |

Income (Loss) from Continuing Operations | | $ | 928 | | | | | $ | 970 | | | $ | (218 | ) | | (4.3 | )% | | n/m | % |

All percentages are calculated based on actual amounts. Minor differences may exist due to rounding.

| | | | |

| 20 | | MD&A | | Comcast 2005 Annual Report |

Consolidated Revenues

Our Cable segment accounted for 94.5% and 93.2% of the increases in consolidated revenues for 2005 and 2004, respectively. Our Content segment accounted for 6.8% and 8.1% of the increases in consolidated revenues for 2005 and 2004, respectively. Cable segment and Content segment revenues are discussed separately below inSegment Operating Results. These increases were partially offset by the revenue decrease in our other business activities, primarily Comcast Spectacor, whose revenues were adversely affected by the NHL lockout.

Consolidated Operating, Selling, General and

Administrative Expenses

Our Cable segment accounted for 86.6% and 86.1% of the increases in consolidated operating, selling, general and administrative expenses for 2005 and 2004, respectively. Our Content segment accounted for 11.5% and 13.2% of the increases in consolidated operating, selling, general and administrative expenses for 2005 and 2004, respectively. Cable segment and Content segment operating, selling, general and administrative expenses are discussed separately below inSegment Operating Results. The remaining changes relate to our other business activities, primarily Comcast Spectacor.

Consolidated Depreciation and Amortization

The increases in depreciation expense are primarily attributable to the effects of capital expenditures in our Cable segment.

The decreases in amortization expense for 2005 and 2004 are primarily attributable to our Cable segment and are primarily attributable to decreases in the amortization of our franchise-related customer relationship intangible assets. These decreases were partially offset by increased amortization expense related to intangibles acquired in various transactions, including Motorola (March 2005) and Gemstar (March 2004), and amortization expense related to intangibles acquired in the TechTV (May 2004) and Liberty exchange (July 2004) transactions. (SeeNote 5to our consolidated financial statements for further discussion about these transactions.)

Segment Operating Results

To measure the performance of our operating segments, we use operating income before depreciation and amortization, excluding impairment charges related to fixed and intangible assets, and gains or losses from the sale of assets, if any. This measure eliminates the significant level of non-cash depreciation and amortization expense that results from the capital-intensive nature of our businesses and from intangible assets recognized in business combinations. It is also unaffected by our capital structure or investment activities. We use this measure to evaluate our consolidated operating performance, the operating performance of our operating segments, and to allocate resources and capital to our operating segments. It is also a significant component of our annual incentive compensation programs. We believe that this measure is useful to investors because it is one of the bases for comparing our operating performance with other companies in our industries, although our measure may not be directly comparable to similar measures used by other companies. Because we use this metric to measure our segment profit or loss, we reconcile it to operating income, the most directly comparable financial measure calculated and presented in accordance with Generally Accepted Accounting Principles (“GAAP”) in the business segment footnote to our consolidated financial statements. You should not consider this measure a substitute for operating income (loss), net income (loss), net cash provided by operating activities, or other measures of performance or liquidity we have reported in accordance with GAAP.

Cable Segment Overview

Our Cable segment offers cable services through our broadband cable systems, which offer full two-way capability and can simultaneously provide video, high-speed Internet and phone services to our subscribers. The majority of our Cable segment revenue is earned from subscriptions to these cable services. Subscribers typically pay us monthly, based on their chosen level of service, number of services and the type of equipment they use, and generally may discontinue services at any time. The following is a summary of our Cable segment results of operations.

| | | | |

| Comcast 2005 Annual Report | | MD&A | | 21 |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | % Change | | | % Change | |

| Cable Segment(Dollars in millions) | | 2005 | | | | 2004 | | 2003 | | 2004 to 2005 | | | 2003 to 2004 | |

Video | | $ | 13,635 | | | | $ | 12,892 | | $ | 12,096 | | 5.8 | % | | 6.6 | % |

High-speed Internet | | | 3,986 | | | | | 3,124 | | | 2,255 | | 27.6 | | | 38.5 | |

Phone | | | 687 | | | | | 701 | | | 801 | | (2.0 | ) | | (12.5 | ) |

Advertising sales | | | 1,359 | | | | | 1,287 | | | 1,112 | | 5.6 | | | 15.7 | |

Other | | | 811 | | | | | 666 | | | 620 | | 21.8 | | | 7.4 | |

Franchise fees | | | 680 | | | | | 646 | | | 608 | | 5.3 | | | 6.3 | |

Revenues | | | 21,158 | | | | | 19,316 | | | 17,492 | | 9.5 | | | 10.4 | |

Operating expenses | | | 7,514 | | | | | 7,170 | | | 6,762 | | 4.8 | | | 6.0 | |

Selling, general and administrative expenses | | | 5,186 | | | | | 4,675 | | | 4,380 | | 10.9 | | | 6.7 | |

Operating income before depreciation and amortization | | $ | 8,458 | | | | $ | 7,471 | | $ | 6,350 | | 13.2 | % | | 17.6 | % |

Cable Segment Revenues

As a result of the growth in the demand for our products and services, discussed further below, we have been able to increase our operating income before depreciation and amortization.

Video

We offer a full range of video services ranging from our limited basic service, which provides subscribers access to between 10 and 20 channels, to our full digital cable service, which provides subscribers access to over 250 channels, including premium and pay-per-view channels; VOD (which allows subscribers to access a library of movies, sports and news, and to start their selection whenever they choose, as well as pause, rewind and fast-forward selections); music channels; and an interactive, on-screen program guide (which allows subscribers to navigate the channel lineup and VOD library). Digital cable subscribers may also subscribe to additional advanced services including DVR, which allows subscribers to record programs digitally, and to pause and rewind live television, and HDTV, which provides multiple channels in high definition.

As of December 31, 2005, approximately 46% of our 21.4 million video subscribers subscribed to at least one of our digital services, compared to approximately 40% and approximately 36% as of December 31, 2004 and 2003, respectively.

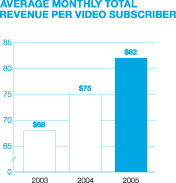

Our video revenues continue to grow from price increases and growth in our digital cable services, including the sale of advanced services. As a result of these factors, our average monthly video revenue per video subscriber, measured on an annual basis, increased from $47 in 2003 to $53 in 2005, even while our video subscriber base of 21.4 million has been stable.

High-Speed Internet

We offer high-speed Internet service with downstream speeds generally from 6Mbps to 8Mbps depending on the service selected. Our high-speed Internet service also includes our interactive portal, Comcast.net, which provides multiple e-mail addresses, online storage and a variety of value-added features and enhancements designed to take advantage of the speed of the service we provide.

As of December 31, 2005, 20.7% of our estimated available homes subscribed to our high-speed Internet service, compared to 17.5% and 15.2% as of December 31, 2004 and 2003, respectively. The increases in high-speed Internet revenue are due to the addition of approximately 1.5 million high-speed Internet subscribers in 2005

| | | | |

| 22 | | MD&A | | Comcast 2005 Annual Report |

and 1.7 million subscribers in 2004. This growth reflects consumer demand for the faster and more reliable Internet service provided over our broadband cable systems. Average monthly revenue per high-speed Internet subscriber has remained relatively stable between $42 and $43, from 2003 through 2005. We expect that the rate of subscriber and revenue growth will slow as the market matures and competition increases.

Phone

We offer Comcast Digital Voice, our IP-enabled phone service that provides unlimited local and domestic long-distance calling, including such features as Voice Mail, Caller ID, and Call Waiting. Comcast Digital Voice service was available to 16 million homes in 25 markets at December 31, 2005. We expect that by the end of 2006 approximately 27 million homes will have access to Comcast Digital Voice.

In some areas, we offer our circuit-switched local phone service. Substantially all of this business was obtained in the Broadband acquisition. Subscribers to this service have access to a full array of associated calling features and third-party long-distance services.

The decreases in phone revenue in 2005 and 2004 from the previous year are primarily a result of a reduction in the number of circuit-switched subscribers as we continued to market Comcast Digital Voice. Our circuit-switched subscribers generate higher revenue per subscriber than Comcast Digital Voice subscribers. In 2005, our phone subscribers increased slightly to approximately 1.3 million compared to 1.2 million in 2004 as a result of the increase in Comcast Digital Voice subscribers in the second half of 2005. We expect the number of phone subscribers will grow as we expand Comcast Digital Voice to new markets in 2006.

Advertising Sales

As part of our license agreements with cable networks, we often receive an allocation of scheduled advertising time, which we may sell to local, regional and national advertisers. We also coordinate the advertising sales efforts of other cable operators in some markets; and we have formed and operate advertising interconnects, which establish a physical, direct link between multiple cable systems and provide for the sale of regional and

national advertising across larger geographic areas than could be provided by a single cable operator.

The increases in advertising sales revenue for 2005 and 2004 from the previous year are primarily due to the effects of the growth in regional and national advertising as a result of the continued success of our regional interconnects, continued growth in local advertising, and in 2004, an increase in political advertising.

Franchise Fees

Our franchise fee revenues represent the pass-through to our subscribers of the fees required to be paid to state and local franchising authorities. Under the terms of our franchise agreements, we are generally required to pay up to 5% of our gross revenues to the local franchising authority. The increases in franchise fees collected from our cable subscribers are primarily attributable to the increases in our revenues upon which the fees apply.

Other

We also generate revenues from our regional sports and news networks, installation services, commissions from third-party electronic retailing, and fees for other services, such as providing businesses with Internet connectivity and networked business applications. Our regional sports and news networks include Comcast SportsNet (Philadelphia), Comcast SportsNet Mid-Atlantic (Baltimore/ Washington), Cable Sports Southeast, CN8–The Comcast Network, Comcast SportsNet Chicago and Comcast SportsNet West (Sacramento). These networks earn revenue through the sale of advertising time and receive license fees paid by cable system operators and satellite television companies. The increase in other revenue for 2005 from the previous year is primarily due to the launch of Comcast SportsNet Chicago and Comcast SportsNet West in the fourth quarter of 2004.

As a result of the growth in our products and services, we have been able to increase our average monthly revenue per video subscriber (including all revenue sources), measured on an annual basis.

| | | | |

| Comcast 2005 Annual Report | | MD&A | | 23 |

Cable Segment Expenses

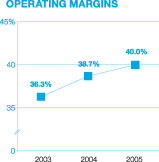

We continue to focus on controlling the growth of expenses which has resulted in steady growth in our operating margins (operating income before depreciation and amortization as a percentage of revenue) over the last three years.

Operating Expenses

Cable programming expenses, our largest expense, are the fees we pay to cable networks to license the programming we distribute, package and offer to our video subscribers. These expenses are affected by changes in the rates charged by cable networks, the number of subscribers, and the programming options we offer to subscribers. Cable programming expenses

increased $222 million to $4.371 billion in 2005 and $240 million to $4.149 billion in 2004. We anticipate our cable programming expenses will increase in the future, as the fees charged by cable networks increase and as we provide additional channels and VOD programming options to our subscribers. We anticipate that these increases may be mitigated to some extent by volume discounts.

Other operating expenses increased $122 million to $3.143 billion in 2005 and $168 million to $3.021 billion in 2004. The increase in 2005 primarily relates to increases in our technical services group due to the launch of Comcast Digital Voice, the deployment of digital simulcasting and the implementation of a new provisioning system and, to a lesser degree, repairing our cable systems as a result of weather-related damage. The increase in 2004 primarily related to increased technical services costs associated with our growth of our digital cable and high-speed Internet services.

Selling, General and Administrative Expenses

Selling, general and administrative expenses increased $511 million to $5.186 billion in 2005 and $295 million to $4.675 billion in 2004. The increase in 2005 is primarily due to the launch of Comcast Digital Voice, the deployment of digital simulcasting and the implementation of a new provisioning system. The increase in 2004 primarily related to increased customer service and marketing expenses associated with the growth of our digital cable and high-speed Internet services.

Content Segment

Our Content segment consists of our national cable networks:

| | | | | | | |

| Network | | Economic

Ownership % | | | Approximate

U.S. Subscribers (In millions) | | Description |

E! Entertainment Television | | 60.5 | % | | 79.3 | | Pop culture entertainment-related programming |

Style Network | | 60.5 | | | 35.2 | | Lifestyle-related programming |

The Golf Channel | | 99.9 | | | 57.0 | | Golf-related programming |

OLN | | 100.0 | | | 54.9 | | Sports and leisure programming |

G4 | | 83.5 | | | 50.6 | | Gamer lifestyle programming |

AZN Television | | 100.0 | | | 13.7 | | Asian American programming |

In addition to the national cable networks above, which we consolidate in our financial statements, we also own non-controlling interests in programming entities including PBS KIDS Sprout (40%), TV One (32.8%) and MGM (20%).

| | | | |

| 24 | | MD&A | | Comcast 2005 Annual Report |

Content Segment Revenues

Revenue from our Content segment is earned primarily from advertising sales and from monthly per subscriber license fees paid by cable system operators and satellite television companies. Content revenues for 2005 increased 16.7% to $919 million and 25.3% to $787 million in 2004 due to increases in subscriber rates, the number of subscribers and advertising revenue across all of our cable networks. The full-year impact of our acquisition of Tech TV (May 2004) and AZN Television (July 2004) also contributed to a growth in revenues. For 2005, 2004 and 2003, approximately 11% of our Content segment revenues were generated from our Cable segment and are eliminated in our consolidated financial statements, but are included in the amounts presented above.

Content Segment Operating, Selling, General and Administrative Expenses

Operating, selling, general and administrative expenses consist mainly of the cost of producing television programs and live events, the purchase of programming rights, marketing and promoting our cable networks, and administrative costs. Content operating, selling, general and administrative expenses for 2005 and 2004 increased $114 million or 21.7% to $636 million and $108 million or 26.0% to $522 million, respectively, primarily due to an increase in the production and programming rights costs for new and live event programming for our cable networks, including the NHL on OLN, and a corresponding increase in marketing expenses for this programming. The full-year impact of our 2004 acquisitions of Tech TV and AZN also contributed to the growth in 2005 expenses. We have and expect to continue to invest in new and live event programming, such as our recent rights agreement with the NHL, which will cause our Content segment expenses to increase in the future.

Consolidated Other Income (Expense) Items

| | | | | | | | | | | | | | |

| December 31 (Dollars in millions) | | 2005 | | | | | 2004 | | | 2003 | |

Interest expense | | $ | (1,796 | ) | | | | $ | (1,876 | ) | | $ | (2,018 | ) |

Investment income (loss), net | | | 89 | | | | | | 472 | | | | (84 | ) |

Equity in net losses of affiliates | | | (47 | ) | | | | | (88 | ) | | | (60 | ) |

Other income (expense) | | | (56 | ) | | | | | 394 | | | | 71 | |

Total | | $ | (1,810 | ) | | | | $ | (1,098 | ) | | $ | (2,091 | ) |

Interest Expense

The decrease in interest expense for 2005 from the previous year is primarily a result of the effects of $57 million of gains recognized in 2005 and $69 million of losses recognized in 2004, in connection with the early extinguishment of some of our debt

facilities, partially offset by the effects of higher interest rates on variable rate debt in 2005.

The decrease in interest expense for 2004 from the previous year is primarily a result of the effects of our net debt repayments and the effects of our interest rate risk management program, partially offset by $69 million of losses recognized in 2004 in connection with the early extinguishment of some of our debt facilities. The decrease for 2004 was also partially offset by the effects of our adoption of Statement of Financial Accounting Standards (“SFAS”) No. 150, “Accounting for Certain Financial Instruments with Characteristics of Both Liabilities and Equity” (“SFAS No. 150”), on July 1, 2003. As a result of adopting SFAS No. 150, we included as interest expense for the years 2004 and 2003 $100 million and $53 million, respectively, of dividends on a subsidiary’s preferred stock. Before the adoption of SFAS No.150, we classified these dividends as a minority interest.

Investment Income (Loss), Net

The components of investment income (loss), net for 2005, 2004 and 2003 are presented in a table inNote 6to our consolidated financial statements.

We have entered into derivative financial instruments that we account for at fair value and which economically hedge the market price fluctuations in the common stock of all of our investments accounted for as trading securities (as of December 31, 2005). The differences between the unrealized gains or losses on trading securities and hedged items and the mark to market adjustments on derivatives related to trading securities and hedged items, as presented in the table inNote 6,result from one or more of the following:

| > | We did not maintain an economic hedge for our entire investment in the security during some or all of the period. |

| > | There were changes in the derivative valuation assumptions such as interest rates, volatility and dividend policy. |

| > | The magnitude of the difference between the market price of the underlying security to which the derivative relates and the strike price of the derivative. |

| > | The change in the time value component of the derivative value during the period. |

| > | The security to which the derivative relates changed due to a corporate reorganization of the issuing company to a security with a different volatility rate. |

| | | | | | |

| Comcast 2005 Annual Report | | MD&A | | | | 25 |

Mark to market adjustments on derivatives, as presented in the table inNote 6, consist principally of the fair value adjustments for the derivative component of the notes exchangeable into Comcast stock. We were exposed to changes in the fair value of this derivative since the underlying shares of Comcast Class A Special common stock that we hold in treasury are carried at our historical cost and not adjusted for changes in fair value. During 2005, we settled for cash the remaining outstanding obligations related to notes exchangeable into Comcast stock.

Equity in Net Losses of Affiliates

The decrease in equity in net losses of affiliates for 2005 from the previous year results principally from the effects of changes in the net income or loss of our equity investees, offset by the effects of equity in net losses in 2005 related to our investment in MGM. The increase in equity in net losses of affiliates for 2004 from the previous year results principally from the effects of our additional investments, and from changes in the net income or loss of our equity method investees.

Other Income (Expense)

Other expense for 2005 consists principally of a $170 million payment representing our share of the settlement amount related to certain of AT&T’s litigation with At Home, partially offset by a $24 million gain on the exchange of one of our equity method investments and $62 million of gains recognized on the sale or restructuring of investment assets in 2005. Other income for 2004 consists principally of the $250 million reduction in the estimated fair value liability associated with certain AT&T securities litigation recorded as part of the Broadband acquisition and the $94 million gain recognized on the sale of one of our equity method investments. Other income for 2003 consists principally of lease rental income.

Income Tax (Expense) Benefit

Our effective income tax rate was (49.6)%, (45.6)% and 11.7% for 2005, 2004 and 2003, respectively. Tax expense in 2005 and 2004 reflects an effective income tax rate higher than the federal statutory rate primarily due to state income taxes, adjustments to prior year accruals and related interest, and in 2005, taxes associated with other investments. The tax benefit in 2003 reflects an effective income tax rate significantly lower than the federal statutory rate due to the impact of adjustments to prior year accruals and related interest and the relatively low pre-tax loss. We expect our recent effective tax rates to be more reflective of our anticipated future effective tax rates. However, our tax provision is, in part, based on estimates, and consequently fluctuations may occur (seeCritical Accounting Judgments and Estimates – Income Taxes).

Minority Interest

The increase in minority interest for 2005 from the previous year is attributable to increases in the net income of our less than wholly-owned consolidated subsidiaries. The decrease in minority interest for 2004 from the previous year is attributable to the effects of our adoption of SFAS No. 150 on July 1, 2003, under which we now record our subsidiary preferred dividends, previously classified in minority interest, to interest expense and, to a lesser extent, to increases in the net losses of some of our less than wholly-owned consolidated subsidiaries.

Discontinued Operations

In 2003, we completed the sale to Liberty Media Corporation of our approximate 57% interest in QVC, Inc. (an electronic retailer) for a total value of approximately $7.7 billion. We present financial information about QVC, Inc. as a discontinued operation in our financial statements.

Liquidity and Capital Resources

As we describe further below, our businesses generate significant cash flow from operating activities. The proceeds from monetizing our non-strategic investments have also provided us with a significant source of cash flow. We believe that we will be able to meet our current and long term liquidity and capital requirements, including fixed charges, through our cash flows from operating activities, existing cash, cash equivalents and investments; through available borrowings under our existing credit facilities; and through our ability to obtain future external financing. We anticipate continuing to use a substantial portion of our cash flow to fund our capital expenditures, repurchase our stock and to invest in business opportunities.

Operating Activities

Net cash provided by operating activities from continuing operations amounted to $4.922 billion for 2005, due principally to our operating income before depreciation and amortization, the effects of interest and income tax payments, payments representing our share of the settlement amounts related to certain of AT&T’s litigation with At Home ($170 million) and certain of AT&T’s securities litigation ($50 million), and changes in operating assets and liabilities.

During 2005, we made cash payments for interest totaling $1.809 billion. We anticipate that our cash paid for interest will increase modestly in 2006 as average debt balances increase as a result of the pending Adelphia and Time Warner and Susquehanna transactions. During 2005, we made cash payments for income taxes totaling

| | | | |

| 26 | | MD&A | | Comcast 2005 Annual Report |

$1.137 billion, which included a payment of $557 million related to unsettled federal tax contingencies from the Broadband acquisition. We anticipate that our income tax payments will continue to be significant in future years.

During 2005, the net decrease in other operating assets and liabilities was $860 million. The reduction in other operating assets and liabilities is attributable to payments associated with liabilities recorded as part of the Broadband acquisition, including the $557 million federal tax contingency mentioned above, a $46 million pension funding and the $50 million payment representing our share of the settlement related to certain of AT&T’s securities litigation.

Financing Activities

Net cash used in financing activities from continuing operations was $933 million for 2005, and consists principally of our net repayments of debt of $2.706 billion and repurchases of common stock of $2.313 billion, offset by our borrowings of $3.978 billion. During 2005, our debt repayments and borrowings consisted of the following:

Repayments

$2.341 billion under senior and medium term notes,

$253 million of Comcast exchangeable debt, and

$112 million under capital leases and other debt instruments.

Borrowings

$3.742 billion of senior notes,

$230 million, net under our commercial paper program, and

$6 million of other debt instruments.

We have made, and may from time to time in the future make, optional repayments on our debt obligations, which may include open market repurchases of our outstanding public notes and debentures, depending on various factors, such as market conditions.

Available Borrowings Under Credit Facilities

We traditionally maintain significant availability under lines of credit to meet our short-term liquidity requirements. Our Commercial Paper Program and Revolving Bank Credit Facilities are described inNote 8to our consolidated financial statements.

Debt Covenants

We and our cable subsidiaries that have provided guarantees (seeNote 8to our consolidated financial statements for information about our Guarantee Structures) are subject to the covenants and restrictions set forth in the indentures governing our public debt securities and in the credit agreement governing our bank credit facilities. We and the guarantors are in compliance with the covenants, and we believe that neither the covenants nor the restrictions in our indentures or loan documents will limit our ability to operate our business or raise additional capital. Our covenants are tested on an ongoing basis. Our new credit facility contains a financial covenant relating only to leverage (ratio of debt to operating income before depreciation and amortization), which we met at December 31, 2005, by a significant margin. Our ability to comply with the financial covenant in the future does not depend on further debt reduction or on improved operating results.

Stock Repurchases

During 2005, under our Board-authorized share repurchase program, we repurchased 79.8 million shares of our Class A Special common stock for $2.3 billion. In January 2006, our Board authorized the repurchase of an additional $5 billion of Class A or Class A Special common stock under our share repurchase program. We expect such repurchases to continue from time to time in the open market or in private transactions, subject to market conditions.

SeeNote 8andNote 10to our consolidated financial statements for further discussion of our financing activities.

| | | | |

| Comcast 2005 Annual Report | | MD&A | | 27 |

Investing Activities

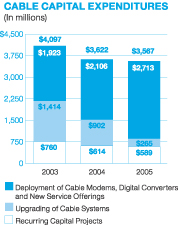

Net cash used in investing activities from continuing operations was $3.748 billion for 2005, and consists primarily of capital expenditures of $3.621 billion, cash paid for intangible assets of $281 million, various cable system and technology-related acquisitions which aggregated $199 million and capital contributions to and purchases of investments of $306 million. These cash outflows were partially offset by proceeds from sales, settlements and restructuring of investments of $861 million.

Capital Expenditures.Our most significant recurring investing activity has been for capital expenditures and we expect that this will continue in the future. The following chart illustrates the capital expenditures we incurred in our Cable segment from 2003 to 2005:

Capital expenditures in our Content segment and our other business activities have been relatively stable from 2003 through 2005.

The amount of our capital expenditures for 2006 and for subsequent years will depend on numerous factors, including acquisitions, competition, changes in technology and the timing and rate of deployment of new services.

Intangible Assets.Cash paid for intangible assets primarily relates to software-related intangibles of approximately $154 million, access agreements with multiple dwelling units (such as apartment buildings and condominium complexes) of approximately $68 million, and other licenses and intangibles of approximately $59 million.

Investments.Proceeds from sales, settlements, and restructurings of investments totaled $861 million during 2005, related to the sales of our non-strategic investments, including Time Warner common stock.

Capital contributions to and purchases of investments primarily relate to our approximate $250 million investment in MGM.

We do not have any significant contractual funding commitments under any of our investments.

Refer toNote 6andNote 7to our consolidated financial statements for a discussion of our investments and our intangible assets, respectively.

Interest Rate Risk Management

We maintain a mix of fixed and variable rate debt. Over 97% of our total debt of $23.371 billion is at fixed rates with the remaining at variable rates. We are exposed to the market risk of adverse changes in interest rates. In order to manage the cost and volatility relating to our interest cost of our outstanding debt, we enter into various interest rate risk management derivative transactions pursuant to our policies.

We monitor our interest rate risk exposures using techniques that include market value and sensitivity analyses. We do not hold or issue any derivative financial instruments for speculative purposes and we are not a party to leveraged derivative instruments.

We manage the credit risks associated with our derivative financial instruments through the evaluation and monitoring of the credit-worthiness of the counterparties. Although we may be exposed to losses in the event of nonperformance by the counterparties, we do not expect such losses, if any, to be significant.

Our interest-rate derivative financial instruments, which can include swaps, rate locks, caps and collars, represent an integral part of our interest rate risk management program. Through this program, we decreased our interest expense by approximately $16 million in 2005 and by $66 million in 2004. Our derivative financial instruments did not have a significant effect on our interest expense in 2003. Interest rate risk management instruments may have a significant effect on our interest expense in the future.

| | | | |

| 28 | | MD&A | | Comcast 2005 Annual Report |

The table set forth below summarizes the fair values and contract terms of financial instruments subject to interest rate risk maintained by us as of December 31, 2005:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in millions) | | 2006 | | | 2007 | | | 2008 | | | 2009 | | | 2010 | | | Thereafter | | | Total | | | Fair

Value

12/31/05 | |

Debt | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Fixed Rate | | $ | 1,666 | | | $ | 725 | | | $ | 1,469 | | | $ | 992 | | | $ | 1,127 | | | $ | 16,725 | | | $ | 22,704 | | | $ | 24,638 | |

Average Interest Rate | | | 7.5 | % | | | 8.2 | % | | | 7.3 | % | | | 7.5 | % | | | 5.7 | % | | | 7.5 | % | | | 7.4 | % | | | | |

Variable Rate | | $ | 23 | | | $ | 54 | | | $ | 7 | | | $ | 10 | | | $ | 573 | | | $ | – | | | $ | 667 | | | $ | 667 | |

Average Interest Rate | | | 5.8 | % | | | 5.2 | % | | | 5.5 | % | | | 5.6 | % | | | 4.9 | % | | | – | | | | 5.0 | % | | | | |

Interest Rate Instruments(1) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Fixed to Variable Swaps | | $ | 400 | | | $ | – | | | $ | 600 | | | $ | 750 | | | $ | 200 | | | $ | 1,650 | | | $ | 3,600 | | | $ | (97 | ) |

Average Pay Rate | | | 8.3 | % | | | – | | | | 8.0 | % | | | 7.7 | % | | | 5.9 | % | | | 5.8 | % | | | 6.8 | % | | | | |

Average Receive Rate | | | 6.4 | % | | | – | | | | 6.2 | % | | | 6.9 | % | | | 5.9 | % | | | 5.4 | % | | | 6.0 | % | | | | |

| (1) | Wedo not have any variable to fixed swaps at December 31, 2005. |

We use the notional amounts on the instruments to calculate the interest to be paid or received. They do not represent the amount of our exposure to credit loss. The estimated fair value approximates the payments necessary to settle the outstanding contracts. We estimate interest rates on variable debt using the average implied forward LIBOR rates for the year of maturity based on the yield curve in effect at December 31, 2005, plus the applicable borrowing margin in effect for the new credit facility at December 31, 2005. We estimate the floating rates on our swaps using the average implied forward LIBOR rates for the year of maturity based on the yield curve in effect at December 31, 2005.

As a matter of practice, we typically do not structure our financial contracts to include credit ratings-based triggers that could affect our liquidity. In the ordinary course of business, some of our swaps could be subject to termination provisions if we do not maintain investment grade credit ratings. As of December 31, 2005, the estimated fair value of those swaps was a liability of $69 million and was an immaterial amount at December 31, 2004. The amount to be paid or received upon termination, if any, would be based upon the fair value of those outstanding contracts at that time.

Equity Price Risk Management

We are exposed to the market risk of changes in the equity prices of our investments in marketable securities. We enter into various derivative transactions pursuant to our policies to manage the volatility relating to these exposures.

Through market value and sensitivity analyses, we monitor our equity price risk exposures to ensure that the instruments are matched with the underlying assets or liabilities, reduce our risks relating to equity prices and maintain a high correlation to the risk inherent in the hedged item.

We use the following equity derivative financial instruments, which we account for at fair value, to limit our exposure to and benefits from price fluctuations in the common stock of some of our investments:

| > | Equity collar agreements; |

| > | Prepaid forward sales agreements; |

| > | Indexed or exchangeable debt instruments. |

Except as described inInvestment Income (Loss), Neton page 24, the changes in the fair value of our investments that we accounted for as trading securities were substantially offset by the changes in the fair values of the equity derivative financial instruments.

Refer toNote 2to our consolidated financial statements for a discussion of our accounting policies for derivative financial instruments and toNote 6andNote 8to our consolidated financial statements for discussions of our derivative financial instruments.

| | | | |

| Comcast 2005 Annual Report | | MD&A | | 29 |

Stock Option Accounting

In December 2004, the Financial Accounting Standards Board (“FASB”) issued SFAS No. 123 (revised 2004), “Share-Based Payment” (“SFAS No. 123R”), which replaces SFAS No. 123, “Accounting for Stock-Based Compensation” (“SFAS No. 123”) and supersedes Accounting Principles Board (“APB”) Opinion No. 25, “Accounting for Stock Issued to Employees” (“APB No. 25”). In March 2005, the SEC issued Staff Accounting Bulletin No. 107 (“SAB 107”) regarding the SEC’s interpretation of SFAS No. 123R and the valuation of share-based payments for public companies. SFAS No. 123R requires all share-based payments to

employees, including grants of employee stock options, to be recognized in the financial statements based on their fair values at grant date or later modification. In addition, SFAS No. 123R will cause unrecognized expense (based on the amounts in our pro forma footnote disclosure) related to options vesting after the date of initial adoption to be recognized as a charge to results of operations over the remaining requisite service period. We have elected to adopt SFAS No. 123R on January 1, 2006, using the modified prospective approach. Refer toNote 3to our consolidated financial statements for further discussion of SFAS No. 123R.

Contractual Obligations

Our unconditional contractual obligations as of December 31, 2005, which consist primarily of our debt obligations and the effect such obligations are expected to have on our liquidity and cash flow in future periods, are summarized in the following table:

| | | | | | | | | | | | | | | |

| | | Payments Due by Period |

| Contractual Obligations(Dollars in millions) | | Total | | Year 1 | | Years

2–3 | | Years

4–5 | | More

than 5

years |

Debt Obligations, excluding Exchangeable Notes(1) | | $ | 23,305 | | $ | 1,669 | | $ | 2,227 | | $ | 2,699 | | $ | 16,710 |

Capital lease obligations | | | 66 | | | 20 | | | 27 | | | 4 | | | 15 |

Operating lease obligations | | | 1,405 | | | 202 | | | 329 | | | 249 | | | 625 |

Purchase Obligations(2) | | | 9,540 | | | 2,778 | | | 3,142 | | | 1,287 | | | 2,333 |

Other long term liabilities reflected on the balance sheet: | | | | | | | | | | | | | | | |

Acquisition related obligations(3) | | | 289 | | | 143 | | | 103 | | | 29 | | | 14 |

Other long term obligations(4) | | | 3,891 | | | 187 | | | 445 | | | 153 | | | 3,106 |

Total | | $ | 38,496 | | $ | 4,999 | | $ | 6,273 | | $ | 4,421 | | $ | 22,803 |

Refer toNote 8(long term debt) andNote 13(commitments)to our consolidated financial statements.

| (1) | Excludesinterest payments. |

| (2) | Purchaseobligations consist of agreements to purchase goods and services that are enforceable and legally binding on us and that specify all significant terms, including fixed or minimum quantities to be purchased, price provisions and timing of the transaction. Our purchase obligations principally relate to our Cable segment, including contracts with programming networks, customer premise equipment manufacturers, communication vendors, other cable operators for which we provide advertising sales representation, and other contracts entered into in the normal course of business. We also have purchase obligations through Comcast Spectacor for the players and coaches of our professional sports teams. We did not include contracts with immaterial future commitments. |

| (3) | Acquisition-relatedobligations consist primarily of costs related to terminating employees, costs relating to exiting contractual obligations, and other assumed contractual obligations of the acquired entity. |

| (4) | Other longterm obligations consist principally of our prepaid forward sales transactions of equity securities we hold, subsidiary preferred shares, deferred compensation obligations, pension, post-retirement and post-employment benefit obligations, and program rights payable under license agreements. |

| | | | |

| 30 | | MD&A | | Comcast 2005 Annual Report |

Off-Balance Sheet Arrangements

We do not have any significant off-balance sheet arrangements that are reasonably likely to have a current or future effect on our financial condition, results of operations, liquidity, capital expenditures or capital resources.

Critical Accounting Judgments and Estimates

The preparation of our financial statements requires us to make estimates that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and contingent liabilities. We base our judgments on historical experience and on various other assumptions that we believe are reasonable under the circumstances, the results of which form the basis for making estimates about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions.

We believe our judgments and related estimates associated with the valuation and impairment testing of our cable franchise rights and the accounting for income taxes and legal contingencies are critical in the preparation of our financial statements. Management has discussed the development and selection of these critical accounting judgments and estimates with the Audit Committee of our Board of Directors, and the Audit Committee has reviewed our disclosures relating to them presented below.

Refer toNote 2to our consolidated financial statements for a discussion of our accounting policies with respect to these and other items.

Valuation and Impairment Testing of Cable Franchise Rights

Our largest asset, our cable franchise rights, results from agreements we have with state and local governments which allow us to construct and operate a cable business within a specified geographic area. The value of a franchise is derived from the economic benefits we receive from the right to solicit new subscribers and to market new services such as advanced digital services, high-speed Internet, and phone services in our service areas. The amounts we record for cable franchise rights are

primarily the result of cable system acquisitions. Often these cable system acquisitions include multiple franchise territories. Typically when we acquire a cable system, the most significant asset we record is the value of the franchise intangible. We currently serve approximately 4,500 franchise areas in the United States.

We have concluded that our cable franchise rights have an indefinite useful life since there are no legal, regulatory, contractual, competitive, economic or other factors which limit the period over which these rights will contribute to our cash flows. Accordingly, we do not amortize our cable franchise rights but assess them periodically for any impairment in our carrying value according to SFAS No. 142, “Goodwill and Other Intangible Assets.”

We assess the carrying value of our cable franchise rights annually, or more frequently whenever events or changes in circumstances indicate that the carrying amount may exceed its fair value (the “impairment test”).

Our 2005 impairment tests did not result in an impairment charge. For the purpose of our impairment testing we have aggregated the recorded values of our franchise rights into geographic regions based on the guidance prescribed in Emerging Issues Task Force issue No. 02-7, “Unit of Accounting for Testing of Impairment of Indefinite-Lived Assets.” We estimate the fair value of our cable franchise rights primarily based on a discounted cash flow analysis which involves significant judgment in developing individual assumptions for each of the geographic regions, including long term growth rate and discount rate assumptions.

If we determined the value of our cable franchise rights is less than the carrying amount, we would recognize an impairment charge for the difference between the estimated fair value and the carrying value of the assets.

We could record an impairment charge in the future if there are changes in market conditions, operating results in or changes in the groupings of the geographic regions in which we test for impairment, or in federal and state regulations that prevent us from recovering the carrying value of these franchise rights. At our last

| | | | |

| Comcast 2005 Annual Report | | MD&A | | 31 |

impairment test date, the amounts that the estimated fair value of our franchise rights exceeded the carrying value for our 22 geographic regions ranged from approximately $46 million to in excess of $3.0 billion. A 10% decline in the estimated fair value of the franchise rights for each of these regions would result in an impairment at four of these regions and an impairment charge of approximately $750 million.

Income Taxes

Our provision for income taxes is based on our current period income, changes in deferred income tax assets and liabilities, income tax rates and tax planning opportunities available in the jurisdictions in which we operate. From time to time, we engage in transactions in which the tax consequences may be subject to uncertainty. Examples of such transactions include business acquisitions and disposals, including like-kind exchanges of cable systems, issues related to consideration paid or received in connection with acquisitions, and certain financing transactions. Significant judgment is required in assessing and estimating the tax consequences of these transactions. We prepare and file tax returns based on our interpretation of tax laws and regulations, and we record estimates based on these judgments and interpretations.

In the normal course of business, our tax returns are subject to examination by various taxing authorities. Such examinations may result in future tax and interest assessments by these taxing authorities and we record a liability when we believe that it is probable that we will be assessed. We adjust our estimates periodically because of ongoing examinations by and settlements with the various taxing authorities, as well as changes in tax laws, regulations and precedent. The effects on our financial statements

of income tax uncertainties that arise in connection with business combinations and those associated with entities acquired in business combinations are discussed inNote 2to our consolidated financial statements. The consolidated tax provision of any given year includes adjustments to prior year income tax accruals that are considered appropriate and any related estimated interest. We believe that adequate accruals have been made for income taxes. Differences between the estimated and actual amounts determined upon ultimate resolution, individually or in the aggregate, are not expected to have a material adverse effect on our consolidated financial position but could possibly be material to our consolidated results of operations or cash flow of any one period.

Legal Contingencies

We are subject to legal, regulatory and other proceedings and claims that arise in the ordinary course of our business and, in certain cases, those that we assume from an acquired entity in a business combination. We record an estimated liability for those proceedings and claims arising in the ordinary course of business based upon the probable and reasonably estimable criteria contained in SFAS No. 5, “Accounting for Contingencies.” For those litigation contingencies assumed in a business combination subsequent to the adoption of SFAS No.141, we record a liability based on estimated fair value when we can determine such fair value. We review outstanding claims with internal as well as external counsel to assess the probability and the estimates of loss. We reassess the risk of loss as new information becomes available, and we adjust liabilities as appropriate. The actual cost of resolving a claim may be substantially different from the amount of the liability recorded.

| | | | |

| 32 | | Report of Management | | Comcast 2005 Annual Report |

REPORT OF MANAGEMENT

Management’s Report on Financial Statements

Our management is responsible for the preparation, integrity and fair presentation of information in our consolidated financial statements, including estimates and judgments. The consolidated financial statements presented in this report have been prepared in accordance with accounting principles generally accepted in the United States of America. Our management believes the consolidated financial statements and other financial information included in this report fairly present, in all material respects, our financial condition, results of operations and cash flows as of and for the periods presented in this report. The consolidated financial statements have been audited by Deloitte & Touche LLP, an independent registered public accounting firm, as stated in their report, which is included herein.

Management’s Report on Internal Control Over Financial Reporting

Our management is responsible for establishing and maintaining an adequate system of internal control over financial reporting. Our system of internal control over financial reporting is designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with accounting principles generally accepted in the United States of America.

Our internal control over financial reporting includes those policies and procedures that:

| > | Pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect our transactions and dispositions of our assets. |

| > | Provide reasonable assurance that our transactions are recorded as necessary to permit preparation of our financial statements in accordance with accounting principles generally accepted in the United States of America, and that our receipts and expenditures are being made only in accordance with authorizations of our management and our directors. |

| > | Provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of our assets that could have a material effect on the financial statements. |