UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

INVESTMENT COMPANY ACT FILE NUMBER: 811-21080

Calamos Convertible Opportunities and Income Fund

(EXACT NAME OF REGISTRANT AS SPECIFIED IN CHARTER)

2020 Calamos Court, Naperville,

Illinois 60563-2787

(ADDRESS OF PRINCIPAL EXECUTIVE OFFICES)

John P. Calamos, Sr., President,

Calamos Advisors LLC

2020 Calamos Court

Naperville, Illinois

60563-2787

(NAME AND ADDRESS OF AGENT FOR SERVICE)

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE: (630) 245-7200

DATE OF FISCAL YEAR END: October 31, 2014

DATE OF REPORTING PERIOD: November 1, 2013 through April 30, 2014

Item 1. Report to Shareholders

Experience and Foresight

About Calamos Investments

For over 35 years, we have helped investors like you manage and build wealth to meet their long-term individual objectives by working to capitalize on the opportunities of the evolving global marketplace. We launched our first mutual fund in 1985 and our first closed-end fund in 2002. Today, we manage five closed-end funds. Two are income-oriented total return offerings, which seek current income, with increased emphasis on capital gains potential. Three are enhanced fixed income offerings, which pursue high current income from income and capital gains. Calamos Convertible Opportunities and Income Fund (CHI) falls into this category. Please see page 5 for a more detailed overview of our closed-end offerings.

We are dedicated to helping our clients build and protect wealth. We understand when you entrust us with your assets, you also entrust us with your achievements, goals and aspirations. We believe we best honor this trust by making investment decisions guided by integrity, by discipline, and by our conscientious research.

We believe an active, risk-conscious approach is essential for wealth creation. In the 1970s, we pioneered strategies that seek to participate in equity market upside and mitigate some of the potential risks of equity market volatility. Our investment process seeks to manage risk at multiple levels and draws upon our experience investing through multiple market cycles.

We have a global perspective. We believe globalization offers tremendous opportunities for countries and companies all over the world. In our view, this creates significant opportunities for investors. In our U.S., global and international portfolios, we are seeking to capitalize on the potential growth of the global economy.

We believe there are opportunities in all markets. Our history traces back to the 1970s, a period of significant volatility and economic concerns. We have invested through multiple market cycles, each with its own challenges. Out of this experience comes our belief that the flipside of volatility is opportunity.

Letter to Shareholders

JOHN P. CALAMOS, SR.

CEO and Global Co-CIO

Dear Fellow Shareholder:

Welcome to your semiannual report for the six-month period ended April 30, 2014. This report includes commentary from our investment team, as well as a listing of portfolio holdings, financial statements and highlights, and detailed information about the performance and allocation of your Fund. I invite you to read it carefully.

As our investment teams look to the future, we are excited about the breadth of possible investment opportunities we see as the U.S. and global economy continues on its recovery track. Still, we believe the climate during the reporting period highlights the importance of taking a long-term and active approach, guided by global perspective.

Calamos Convertible Opportunities and Income Fund (CHI) is an enhanced fixed income fund. We utilize dynamic asset allocation to pursue high current income with a less rate-sensitive approach, while also maintaining a focus on capital gains. We believe the flexibility to invest in high yield corporate bonds and convertible securities is an important differentiator, especially given the reduction in the Federal Reserve’s quantitative easing activities and the impact that would have on the fixed income markets.

Steady and Competitive Distributions

During the period, CHI provided steady monthly distributions. We believe the Fund’s distribution rate, which was 8.29%* on a market price basis as of April 30, 2014, was very competitive, given the low interest rates in many segments of the bond market. In our view, the Fund’s distributions illustrate the benefits of a multi-asset class approach and flexible allocation strategy.

We understand that many closed-end fund investors seek steady, predictable distributions instead of distributions that fluctuate. Therefore, this Fund has a level rate distribution policy. As part of this policy, we aim to keep distributions consistent from month to month, and at a level that we believe can be sustained over the long term. In

| * | Current Annualized Distribution Rate is the Fund’s most recent distribution, expressed as an annualized percentage of the Fund’s current market price per share. The Fund’s 4/15/14 distribution was $0.0950 per share. Based on our current estimates, we anticipate that approximately $0.0692 is paid from ordinary income and that approximately $0.0258 represents a return of capital. Estimates are calculated on a tax basis rather than on a generally accepted accounting principles (GAAP) basis, but should not be used for tax reporting purposes. Distributions are subject to re-characterization for tax purposes after the end of the fiscal year. This information is not legal or tax advice. Consult a professional regarding your specific legal or tax matters. Under the Fund’s level rate distribution policy, distributions paid to common shareholders may include net investment income, net realized short-term capital gains and return of capital. When the net investment income and net realized short-term capital gains are not sufficient, a portion of the level rate distribution will be a return of capital. In addition, a limited number of distributions per calendar year may include net realized long-term capital gains. Distribution rate may vary. |

| | | | | | |

| | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | | 1 | |

Letter to Shareholders

setting the Fund’s distribution rate, the investment management team and the Fund’s Board of Trustees consider the interest rate, market and economic environment. We also factor in our assessment of individual securities and asset classes. (For additional information on our level rate distribution policy, please see “The Calamos Closed-End Funds: An Overview” on page 5 and “Level Rate Distribution Policy” on page 34.)

Market Environment

Equities advanced at a good clip during the six-month period. The U.S. equity market rose 8.36%, as represented by the S&P 500 Index, and convertible securities benefited from their equity participation, as reflected in a gain of 8.23% for the BofA Merrill Lynch All U.S. Convertibles Index.

There’s a popular adage that “every bull market must climb a wall of worry.” This saying rang true during the reporting period, as returns were earned in an environment of increasing volatility and changing market leadership. In the first months of the reporting period, investors generally favored equities with growth characteristics—such as technology and biotechnology. However, in mid-March, market participants became concerned that U.S. interest rates might rise more rapidly than had been generally expected. This led to a sell-off in the stocks of growth companies where the majority of earnings and cash flows may not be realized for many years, including many of the growth stocks that had led in the previous months. Questions about the future prospects for the U.S. economic recovery intensified and investors rewarded stocks in sectors thought of as more defensive—such as utilities and consumer staples.

Meanwhile, mounting anxiety about interest rates hindered the corporate and government bond markets, and the Barclays Capital U.S. Aggregate Bond Index earned just 1.74%. High yield bonds benefited from their historically reduced interest rate sensitivity as well as from investors’ search for yield, with the Credit Suisse High Yield Index gaining 4.78%.

We See Opportunity in the Markets

We believe the economy is positioned for continued expansion, albeit at a modest overall pace, and that inflation appears to be generally well contained. We are identifying many compelling growth prospects in cyclical growth and secular growth companies. Cyclical growth companies are those that are tied to the general business cycle, such as financial companies that could benefit from higher interest rates. Secular growth companies are those that are positioned to capitalize on secular trends, such as the rise of the emerging market middle class or the global hunger for access to information and entertainment.

| | | | |

| 2 | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | |

Letter to Shareholders

By many of our favored measures, equities are attractively priced, especially the stocks of growth companies. As economic recovery continues, we believe that market participants will come to more fully appreciate the merits of growth companies. We are also optimistic about trends in the convertible market, and see opportunities for active approaches. In addition to providing the opportunity to participate in equity market advances with potentially less downside, convertibles have been less sensitive to rising interest rates. In contrast, we are more concerned about the prospects for investment grade and government bonds. Although rates stayed low, our view is that interest rates will likely rise, first in the U.S., but eventually in the euro zone as recovery continues.

Our Use of Leverage**

We have the flexibility to utilize leverage in this Fund. Over the long term, we believe that the judicious use of leverage provides us with opportunities to enhance total return and support the Fund’s distribution rate. Leverage strategies typically entail borrowing at short-term interest rates and investing the proceeds at higher rates of return. During the reporting period, we believed the prudent use of leverage would be advantageous given the economic environment, specifically the low borrowing costs we were able to secure. Overall, use of leverage contributed favorably to the returns of the Fund, as the performance of the Fund’s holdings exceeded the costs of borrowing.

Consistent with our focus on risk management, we have employed techniques to hedge against a rise in interest rates. We have used interest rate swaps to manage the borrowing costs associated with the Fund’s use of leverage. Interest rate swaps allow us to “lock down” an interest rate we believe to be attractive. Although rates are at historically low levels across much of the fixed income market, history has taught us that rates can rise quickly, in some cases, in a matter of months. We believe the Fund’s use of interest rate swaps is beneficial because it provides a degree of protection should a rise in rates occur. However, we will continue to assess the costs versus benefits of employing swaps on an ongoing basis as part of our leverage strategy.

Asset Allocation Strategies in an Evolving Environment

I often speak with investors who ask about how they should be responding to the near-term changes in the economic environment. My advice typically focuses on looking through the short-term ups and downs and staying focused on longer-term growth trends and the broad economic landscape. Investors who time the markets are likely to get whipsawed—missing the upside and capturing the downside.

| ** | Leverage creates risks that may adversely affect return, including the likelihood of greater volatility of net asset value and market price of common shares, and fluctuations in the variable rates of the leverage financing. |

| | | | | | |

| | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | | 3 | |

Letter to Shareholders

In closing, I believe that this is an environment where active management and rigorous research will drive investment results. Our team is committed to serving your interests by identifying the most compelling investments in the global economy. If you have any questions or would like additional information, please visit us at www.calamos.com or contact us at 800.582.6959.

We are honored to serve you.

Sincerely,

John P. Calamos, Sr.

CEO and Global Co-CIO,

Calamos Advisors LLC

Before investing, carefully consider a fund’s investment objectives, risks, charges and expenses. Please see the prospectus containing this and other information or call 800.582.6959. Please read the prospectus carefully. Performance data represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted.

The S&P 500 Index is an unmanaged index generally considered representative of the U.S. stock market. The BofA Merrill Lynch All U.S. Convertibles Index represents the U.S. convertible securities market. The Barclays Capital U.S. Aggregate Bond Index is considered generally representative of the investment-grade bond market. The Credit Suisse High Yield Index is an unmanaged index of approximately 1,600 issues with an average maturity range of seven to 10 years with a minimum capitalization of $75 million. The Index is considered generally representative of the U.S. market for high yield bonds. Sources: Mellon Analytical Solutions and Lipper.

Unmanaged index returns assume reinvestment of any and all distributions and, unlike fund returns, do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index. Investments in overseas markets pose special risks, including currency fluctuation and political risks. These risks are generally intensified for investments in emerging markets. Countries, regions, and sectors mentioned are presented to illustrate countries, regions, and sectors in which a fund may invest. Fund holdings are subject to change daily. The Funds are actively managed. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the securities mentioned. The information contained herein, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable. There are certain risks involved with investing in convertible securities in addition to market risk, such as call risk, dividend risk, liquidity risk and default risk, that should be carefully considered prior to investing. This information is being provided for informational purposes only and should not be considered investment advice or an offer to buy or sell any security in the portfolio.

This report is intended for informational purposes only and should not be considered investment advice.

| | | | |

| 4 | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | |

The Calamos Closed-End Funds: An Overview

In our closed-end funds, we draw upon decades of investment experience, including a long history of opportunistically blending asset classes in an attempt to capture upside potential while managing downside risk. We launched our first closed-end fund in 2002.

Closed-end funds are long-term investments. Most focus on providing monthly distributions, but there are important differences among individual closed-end funds. Calamos closed-end funds can be grouped into multiple categories that seek to produce income while offering exposure to various asset classes and sectors.

| | |

| Portfolios Positioned to Pursue High Current Income from Income and Capital Gains | | Portfolios Positioned to Seek Current Income, with Increased Emphasis on Capital Gains Potential |

| |

| OBJECTIVE: U.S. ENHANCED FIXED INCOME | | OBJECTIVE: GLOBAL TOTAL RETURN |

Calamos Convertible Opportunities and Income Fund (Ticker: CHI) Invests in high yield and convertible securities, primarily in U.S. markets | | Calamos Global Total Return Fund (Ticker: CGO) Invests in equities and higher-yielding convertible securities and corporate bonds, in both U.S. and non-U.S. markets |

| |

| | | OBJECTIVE: U.S. TOTAL RETURN |

Calamos Convertible and High Income Fund (Ticker CHY) Invests in high yield and convertible securities, primarily in U.S. markets | | Calamos Strategic Total Return Fund (Ticker: CSQ) Invests in equities and higher-yielding convertible securities and corporate bonds, primarily in U.S. markets |

| |

| OBJECTIVE: GLOBAL ENHANCED FIXED INCOME | | |

Calamos Global Dynamic Income Fund (Ticker: CHW) Invests in global fixed income securities, alternative investments and equities | | |

Our Level Rate Distribution Policy

Closed-end fund investors often look for a steady stream of income. Recognizing this, Calamos closed-end funds have a level rate distribution policy in which we aim to keep monthly income consistent through the disbursement of net investment income, net realized short-term capital gains and, if necessary, return of capital. We set distributions at levels that we believe are sustainable for the long term. Our team is focused on delivering an attractive monthly distribution, while maintaining a long-term focus on risk management. The level of the funds’ distributions can be greatly influenced by market conditions, including the interest rate environment. The funds’ distributions will depend on the individual performance of positions the funds hold, our view of the benefits of retaining leverage, fund tax considerations, and maintaining regulatory requirements.

For more information about any of these funds, we encourage you to contact your financial advisor or Calamos Investments at 800.582.6959 (Monday through Friday from 8:00 a.m. to 6:00 p.m., Central Time). You can also visit us at www.calamos.com.

For more information on our level rate distribution policy, please see page 34.

| | | | | | |

| | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | | 5 | |

Investment Team Discussion

| | | | | | | | | | | | |

| TOTAL RETURN* AS OF 4/30/14 | |

Common Shares – Inception 6/26/02 | |

| | | 6 Months | | | 1 Year | | | Since

Inception** | |

On Market Price | | | 9.63% | | | | 17.40% | | | | 10.49% | |

On NAV | | | 6.97% | | | | 13.91% | | | | 10.77% | |

*Total return measures net investment income and net realized gain or loss from Fund investments, and change in net unrealized appreciation or depreciation, assuming reinvestment of income and net realized gains distributions. **Annualized since inception. | |

| | | | |

SECTOR WEIGHTINGS***

AS OF 4/30/14 | |

Consumer Discretionary | | | 18.0 | % |

Information Technology | | | 16.5 | |

Health Care | | | 14.0 | |

Industrials | | | 13.2 | |

Energy | | | 12.5 | |

Financials | | | 11.0 | |

Materials | | | 5.2 | |

Consumer Staples | | | 2.6 | |

Telecommunication Services | | | 2.6 | |

Utilities | | | 2.1 | |

***Sector Weightings are based on managed assets and may vary over time. Sector Weightings exclude any government/sovereign bonds or options on broad market indexes the Fund may hold.

CONVERTIBLE OPPORTUNITIES AND

INCOME FUND (CHI)

INVESTMENT TEAM DISCUSSION

Please discuss the Fund’s strategy and role within an asset allocation.

Calamos Convertible Opportunities and Income Fund (CHI) is an enhanced fixed income investment product, seeking total return through a combination of capital appreciation and current income. It provides an alternative to funds investing exclusively in investment grade fixed income instruments, and seeks to be less sensitive to interest rates. Like all five Calamos closed-end funds, the Fund seeks to provide a steady stream of distributions paid on a monthly basis and invests in multiple asset classes.

Within this Fund, we invest in a diversified portfolio of convertible securities and high yield securities. The allocation to each asset class is dynamic, and reflects our view of the economic landscape, as well as the potential of individual securities. By combining these asset classes, we believe the Fund is well positioned to generate capital gains as well as income. We believe the broader range of security types in which the Fund invests also provides us with increased opportunities for managing the risk and reward characteristics of the portfolio over full market cycles.

We seek companies with respectable balance sheets, reliable debt servicing and good prospects for sustainable growth. While we invest primarily in securities of U.S. issuers, we favor those companies that are actively participating in globalization with geographically diversified revenue streams and global business strategies.

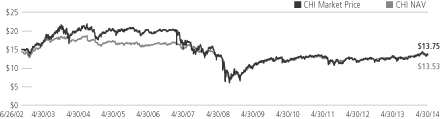

How did the Fund perform over the reporting period?

The Fund gained 6.97% on a net asset value (NAV) basis and 9.63% on a market price basis for the six-month period ended April 30, 2014, versus the 4.78% return for the Credit Suisse High Yield Index and a 8.23% gain for the BofA Merrill Lynch All U.S. Convertibles Index for the same period.

At the end of the reporting period, the Fund’s shares traded at a 1.63% premium to net asset value.

SINCE INCEPTION MARKET PRICE AND NAV HISTORY THROUGH 4/30/14

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value of an investment will fluctuate so that your shares, when sold, may be worth more or less than their original cost. Returns at NAV reflect the deduction of the Fund’s management fee, debt leverage costs and all other applicable fees and expenses. You can obtain performance data current to the most recent month end by visiting www.calamos.com.

| | | | |

| 6 | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | |

Investment Team Discussion

How do NAV and market price return differ?

Closed-end funds trade on exchanges, where the price of shares may be driven by factors other than the value of the underlying securities. The price of a share in the market is called market value. Market price may be influenced by factors unrelated to the performance of the fund’s holdings, such as general market sentiment or future expectation. A fund’s NAV return measures the actual return of the individual securities in the portfolio, less fund expenses. It also measures how a manager was able to capitalize on market opportunities. Because we believe closed-end funds are best utilized as long-term holdings within asset allocations, we believe NAV return is the better measure of a fund’s performance. However, when managing the Fund, we strongly consider actions and policies that we believe will optimize its overall price performance and returns based on market value.

Please discuss the Fund’s distributions during the period.

We employ a level rate distribution policy within this Fund with the goal of providing shareholders with a consistent distribution stream. The Fund maintained its monthly distribution at $0.095 through the period. The Fund’s annual distribution rate was 8.29% of market price as of April 30, 2014.

We believe that both the Fund’s distribution rate and level remained attractive and competitive, as low interest rates limited yield opportunities in much of the marketplace. For example, as of April 30, 2014, the dividend yield of S&P 500 Index stocks averaged 1.95%. Yields also remained low within the U.S. government bond market, with 10-year U.S. Treasurys and 30-year U.S. Treasurys yielding 2.65% and 3.46%, respectively.

What factors influenced performance over the reporting period?

The Fund’s convertible securities and high yield corporate credits both contributed to the positive performance for the period. Within the convertible market, the convertibles that performed the best during the reporting period had either the most equity sensitivity or the most credit sensitivity. These securities benefited from strong equity market performance during the period. As our Fund has been historically managed towards total return convertibles—convertibles that display asymmetric upside and downside relative to the underlying common stock—we had lighter allocations to these outperforming areas during the reporting period and this held back returns. About half of the Fund consists of convertibles, which allowed for participation convertible-market rally.

From an economic sector perspective, the Fund’s overweight toward industrials, specifically the construction machinery and heavy trucks industry, and health care, in particular holdings in pharmaceuticals, boosted performance. Conversely, an underweight toward materials, namely holdings in diversified metals and mining, and consumer discretionary, such as homebuilding names, were detrimental to performance.

How is the Fund positioned?

The Fund is allocated heaviest to convertibles displaying, in our view, attractive risk-reward attributes relative to their underlying common stocks. While the Fund invests across the entire credit quality spectrum, it currently has a much lighter allocation to the most speculatively rated (CCC) issuers. We have witnessed in the past that these most speculatively rated holdings do not provide the necessary downside protection

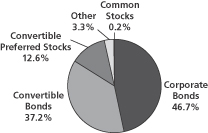

ASSET ALLOCATION AS OF 4/30/14

Fund asset allocations are based on total investments and may vary over time.

| | | | | | |

| | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | | 7 | |

Investment Team Discussion

when the underlying equity declines. In the current environment, we have also been selective in regard to our most speculative issues, reflecting our concerns that these credits may not presently provide adequate compensation for the associated risk.

Accordingly, we continue to maintain a higher average credit quality than the Credit Suisse High Yield Index. We continue to hold the majority of our fixed income securities in the BB credit tier as we believe this offers optimal risk/reward dynamics.

We increased our convertible exposure during the period. We believe that this increase allows us to meaningfully participate in further improvement in the equity markets through convertibles. The increase has come largely by reducing our holdings in high yield fixed income securities. We believe that convertible securities offer an attractive risk managed way to gain or maintain access to the equity markets in the current environment.

We have slightly increased our exposures in consumer discretionary, health care and energy. We believe given the current macroeconomic dynamics, these areas are in the best position to perform well. We have slightly reduced our holdings in industrials and telecommunication services.

The Fund is currently employing leverage at approximately 27%, borrowing through floating rate bank debt. Given the low borrowing costs at the present rate, we believe this has been, and continues to be, beneficial to our shareholders. In addition, 27% of our floating rate debt is hedged through interest rate swaps, a defensive strategy that mitigates the Fund’s exposure to a sudden rise in short-term interest rates.

Do you have any closing thoughts for Fund shareholders?

We believe that investing in convertibles is about participating in a portion of the equity market upside while also providing a measured degree of downside protection. In this respect, we believe returns are best viewed over a full market cycle. During the period, the convertible market captured nearly all of the equity market’s upside. As we maintain a cautiously optimistic view of the U.S. economy, we believe heavier exposure to equity-sensitive convertibles will allow the Fund to optimize total return. Our dynamic allocation mandate allows us to deploy assets over different asset classes to benefit our shareholders. Accordingly, we believe that active management in the convertible and high yield space is essential to providing desirable risk-managed results over time.

As investors have increasingly sought out convertibles and deltas have risen, we believe that opportunities are significant, but the need for disciplined active management remains paramount. We maintain a focus on convertibles that are neither extremely equity nor credit sensitive as we remain committed to balancing upside equity participation with potential downside protection. Through dynamic asset allocation we are able to optimize the total return of the Fund as we adjust our exposure to take advantage of market opportunities within various sectors and asset classes. We believe our exposure to fixed income securities allows us to maintain a competitive distribution. However, given the asset classes represented in the Fund and the overall low associated duration of the Fund, we believe that we are well defended against rising interest rates.

| | | | |

| 8 | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | |

Schedule of Investments April 30, 2014 (Unaudited)

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | CORPORATE BONDS (50.1%) | |

| | | | | | Consumer Discretionary (10.3%) | |

| | 1,098,000 | | | | | Altice, SA*

7.750%, 05/15/22 | | $ | 1,146,038 | |

| | 1,627,000 | | | | | Bon-Ton Department Stores, Inc.^m

8.000%, 06/15/21 | | | 1,562,937 | |

| | 275,000 | | | | | Brunswick Corp.*m

4.625%, 05/15/21 | | | 272,422 | |

| | 290,000 | | | | | Century Communities*

6.875%, 05/15/22 | | | 287,793 | |

| | 1,569,000 | | | | | Chrysler Group, LLC*

8.000%, 06/15/19 | | | 1,717,074 | |

| | 847,000 | | | | | Cogeco Cable, Inc.*m

4.875%, 05/01/20 | | | 853,882 | |

| | 4,793,000 | | | | | Cooper Tire & Rubber Company^m

8.000%, 12/15/19 | | | 5,392,125 | |

| | 3,550,000 | | | | | Dana Holding Corp.m

6.750%, 02/15/21 | | | 3,849,531 | |

| | | | | | DISH DBS Corp.m | | | | |

| | 5,302,000 | | | | | 5.125%, 05/01/20 | | | 5,580,355 | |

| | 4,282,000 | | | | | 7.875%, 09/01/19^ | | | 5,084,875 | |

| | 3,137,000 | | | | | Dufry Finance, SCA*m

5.500%, 10/15/20 | | | 3,264,441 | |

| | 2,223,000 | | | | | Golden Nugget Escrow, Inc.*^m

8.500%, 12/01/21 | | | 2,293,858 | |

| | 1,039,000 | | | | | Goodyear Tire & Rubber Companym

8.250%, 08/15/20 | | | 1,151,991 | |

| | 1,995,000 | | | | | Greektown Holdings, LLC*^

8.875%, 03/15/19 | | | 2,061,084 | |

| | 1,859,000 | | | | | Hasbro, Inc.^m

6.600%, 07/15/28 | | | 2,097,491 | |

| | | | | | Icahn Enterprises, LP* | | | | |

| | 3,027,000 | | | | | 5.875%, 02/01/22 | | | 3,079,973 | |

| | 1,851,000 | | | | | 6.000%, 08/01/20m | | | 1,959,746 | |

| | 427,000 | | | | | 4.875%, 03/15/19m | | | 433,138 | |

| | 3,921,000 | | | | | Jaguar Land Rover Automotive, PLC*m 8.125%, 05/15/21 | | | 4,445,434 | |

| | | | | | L Brands, Inc.m | | | | |

| | 2,353,000 | | | | | 7.600%, 07/15/37 | | | 2,523,593 | |

| | 533,000 | | | | | 6.950%, 03/01/33 | | | 550,323 | |

| | 1,105,000 | | | | | Liberty Interactive, LLC^m

8.250%, 02/01/30 | | | 1,211,356 | |

| | | | | | Meritage Homes Corp.m | | | | |

| | 2,667,000 | | | | | 7.150%, 04/15/20 | | | 2,968,705 | |

| | 1,496,000 | | | | | 7.000%, 04/01/22 | | | 1,644,665 | |

| | 1,467,000 | | | | | NCL Corp., Ltd. - Class Cm

5.000%, 02/15/18 | | | 1,521,096 | |

| | | | | | Neiman Marcus Group LTD, LLC* | | | | |

| | 482,000 | | | | | 8.750%, 10/15/21 | | | 533,815 | |

| | 384,000 | | | | | 8.000%, 10/15/21m | | | 422,160 | |

| | 2,216,000 | | | | | Netflix, Inc.m

5.375%, 02/01/21 | | | 2,314,335 | |

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | | | | | Numericable Group, SA* | | | | |

| | 2,196,000 | | | | | 6.000%, 05/15/22 | | $ | 2,250,900 | |

| | 157,000 | | | | | 6.250%, 05/15/24 | | | 160,729 | |

| | 4,471,000 | | | | | Outerwall, Inc.m 6.000%, 03/15/19 | | | 4,644,251 | |

| | 839,000 | | | | | Quiksilver, Inc. / QS Wholesale, Inc.*m

7.875%, 08/01/18 | | | 910,839 | |

| | 3,031,000 | | | | | Royal Caribbean Cruises, Ltd.^

7.500%, 10/15/27 | | | 3,419,347 | |

| | | | | | Ryland Group, Inc.m | | | | |

| | 4,314,000 | | | | | 6.625%, 05/01/20^ | | | 4,691,475 | |

| | 1,169,000 | | | | | 5.375%, 10/01/22 | | | 1,162,424 | |

| | | | | | Sally Holdings, LLC / Sally Capital, Inc.m | | | | |

| | 1,467,000 | | | | | 5.750%, 06/01/22^ | | | 1,560,521 | |

| | 753,000 | | | | | 5.500%, 11/01/23 | | | 769,001 | |

| | 2,745,000 | | | | | Service Corp. International^m

7.500%, 04/01/27 | | | 2,949,159 | |

| | 2,290,000 | | | | | Six Flags Entertainment Corp.*m

5.250%, 01/15/21 | | | 2,322,919 | |

| | 2,351,000 | | | | | Taylor Morrison Communities, Inc.*m

5.250%, 04/15/21 | | | 2,381,857 | |

| | 1,157,000 | | | | | Time, Inc.*^

5.750%, 04/15/22 | | | 1,153,384 | |

| | | | | | Toll Brothers Finance Corp. | | | | |

| | 2,588,000 | | | | | 5.625%, 01/15/24^ | | | 2,691,520 | |

| | 902,000 | | | | | 4.000%, 12/31/18m | | | 925,678 | |

| | 2,980,000 | | | | | Viking Cruises, Ltd.*m

8.500%, 10/15/22 | | | 3,382,300 | |

| | | | | | | | | | |

| | | | | | | | | 95,600,540 | |

| | | | | | | | | | |

| | | | | | Consumer Staples (2.4%) | |

| | 761,000 | | | | | Alphabet Holding Company, Inc.m

7.750%, 11/01/17 | | | 788,586 | |

| | 2,863,000 | | | | | Fidelity & Guaranty Life Holdings, Inc.*m

6.375%, 04/01/21 | | | 3,063,410 | |

| | 3,896,000 | | | | | JBS USA, LLC*m

7.250%, 06/01/21 | | | 4,207,680 | |

| | 4,235,000 | | | | | Land O’Lakes, Inc.*^m

6.000%, 11/15/22 | | | 4,475,866 | |

| | | | | | Post Holdings, Inc.m | | | | |

| | 5,925,000 | | | | | 7.375%, 02/15/22 | | | 6,380,484 | |

| | 337,000 | | | | | 7.375%, 02/15/22* | | | 359,326 | |

| | 2,471,000 | | | | | Smithfield Foods, Inc.m

6.625%, 08/15/22 | | | 2,696,479 | |

| | | | | | | | | | |

| | | | | | | | | 21,971,831 | |

| | | | | | | | | | |

| | | | | | Energy (10.4%) | |

| | 2,620,000 | | | | | Atwood Oceanics, Inc.m

6.500%, 02/01/20 | | | 2,808,312 | |

| | 1,961,000 | | | | | Berry Petroleum Company

6.375%, 09/15/22 | | | 2,024,733 | |

| | 1,961,000 | | | | | Bonanza Creek Energy, Inc.m

6.750%, 04/15/21 | | | 2,098,270 | |

| | 1,765,000 | | | | | Calfrac Holdings, LP*m

7.500%, 12/01/20 | | | 1,878,622 | |

| | | | | | |

| See accompanying Notes to Schedule of Investments | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | | 9 | |

Schedule of Investments April 30, 2014 (Unaudited)

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | | | | | Calumet Specialty Products Partners, LP | | | | |

| | 1,804,000 | | | | | 7.625%, 01/15/22m | | $ | 1,899,838 | |

| | 1,497,000 | | | | | 6.500%, 04/15/21*^ | | | 1,500,743 | |

| | 1,176,000 | | | | | 9.625%, 08/01/20m | | | 1,359,015 | |

| | | | | | Carrizo Oil & Gas, Inc.m | | | | |

| | 3,467,000 | | | | | 7.500%, 09/15/20 | | | 3,813,700 | |

| | 2,561,000 | | | | | 8.625%, 10/15/18 | | | 2,745,072 | |

| | 1,302,000 | | | | | Chesapeake Oilfield Operating, LLCm 6.625%, 11/15/19 | | | 1,361,404 | |

| | 4,706,000 | | | | | Cimarex Energy Company^m

5.875%, 05/01/22 | | | 5,132,481 | |

| | 5,490,000 | | | | | Drill Rigs Holdings, Inc.*m

6.500%, 10/01/17 | | | 5,671,856 | |

| | 2,274,000 | | | | | Energy Transfer Equity, LPm

5.875%, 01/15/24 | | | 2,325,165 | |

| | 1,647,000 | | | | | EPL Oil & Gas, Inc.

8.250%, 02/15/18 | | | 1,778,760 | |

| | 459,000 | | | | | Forum Energy Technologies, Inc.*m

6.250%, 10/01/21 | | | 486,827 | |

| | 4,314,000 | | | | | Gulfmark Offshore, Inc.m

6.375%, 03/15/22 | | | 4,489,256 | |

| | 5,004,000 | | | | | Gulfport Energy Corp.m

7.750%, 11/01/20 | | | 5,482,507 | |

| | 4,314,000 | | | | | Laredo Petroleum, Inc.m

7.375%, 05/01/22 | | | 4,777,755 | |

| | | | | | Linn Energy, LLCm | | | | |

| | 3,921,000 | | | | | 8.625%, 04/15/20 | | | 4,239,581 | |

| | 1,569,000 | | | | | 7.250%, 11/01/19*‡ | | | 1,625,876 | |

| | 1,176,000 | | | | | 7.750%, 02/01/21 | | | 1,258,320 | |

| | 784,000 | | | | | 6.500%, 05/15/19 | | | 815,850 | |

| | | | | | Oasis Petroleum, Inc.m | | | | |

| | 3,286,000 | | | | | 6.500%, 11/01/21 | | | 3,526,289 | |

| | 980,000 | | | | | 6.875%, 01/15/23 | | | 1,063,913 | |

| | 1,780,000 | | | | | Pacific Drilling, SA*m

5.375%, 06/01/20 | | | 1,737,725 | |

| | 2,156,000 | | | | | Petroleum Geo-Services, ASA*m

7.375%, 12/15/18 | | | 2,315,005 | |

| | 1,344,000 | | | | | Pioneer Energy Services Corp.*m

6.125%, 03/15/22 | | | 1,381,800 | |

| | 2,583,000 | | | | | Rice Energy, Inc.*^

6.250%, 05/01/22 | | | 2,584,614 | |

| | 3,921,000 | | | | | SEACOR Holdings, Inc.m

7.375%, 10/01/19 | | | 4,420,927 | |

| | 1,961,000 | | | | | SESI, LLCm

7.125%, 12/15/21 | | | 2,211,027 | |

| | 1,412,000 | | | | | SM Energy Companym

6.500%, 11/15/21 | | | 1,523,195 | |

| | 2,667,000 | | | | | Swift Energy Companym

8.875%, 01/15/20 | | | 2,817,019 | |

| | 2,823,000 | | | | | Trinidad Drilling, Ltd.*^

7.875%, 01/15/19 | | | 3,020,610 | |

| | 7,294,000 | | | | | W&T Offshore, Inc.^

8.500%, 06/15/19 | | | 7,918,549 | |

| | 2,180,000 | | | | | Western Refining, Inc.m

6.250%, 04/01/21 | | | 2,267,200 | |

| | | | | | | | | | |

| | | | | | | | | 96,361,816 | |

| | | | | | | | | | |

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | Financials (2.6%) | | | | |

| | 1,883,000 | | | | | AON Corp.m

8.205%, 01/01/27 | | $ | 2,379,227 | |

| | 4,463,000 | | | | | Black Knight InfoServ, LLCm

5.750%, 04/15/23 | | | 4,794,177 | |

| | 1,020,000 | | | | | DuPont Fabros Technology, LP

5.875%, 09/15/21 | | | 1,066,538 | |

| | 847,000 | | | | | First Cash Financial Services, Inc.*

6.750%, 04/01/21 | | | 878,233 | |

| | 1,553,000 | | | | | iStar Financial, Inc.m

4.875%, 07/01/18 | | | 1,589,884 | |

| | | | | | Jefferies Finance, LLC*m | | | | |

| | 3,333,000 | | | | | 7.375%, 04/01/20 | | | 3,510,066 | |

| | 943,000 | | | | | 6.875%, 04/15/22 | | | 947,715 | |

| | 1,796,000 | | | | | Nationstar Mortgage, LLC /

Nationstar Capital Corp.m

6.500%, 07/01/21 | | | 1,720,792 | |

| | 4,314,000 | | | | | Neuberger Berman Group, LLC*m

5.875%, 03/15/22 | | | 4,626,765 | |

| | 2,314,000 | | | | | Nuveen Investments, Inc.*^

9.125%, 10/15/17 | | | 2,536,722 | |

| | | | | | | | | | |

| | | | | | | | | 24,050,119 | |

| | | | | | | | | | |

| | | | | | Health Care (5.6%) | | | | |

| | 2,529,000 | | | | | Alere, Inc.m

6.500%, 06/15/20 | | | 2,658,611 | |

| | 6,823,000 | | | | | Community Health Systems, Inc.m

7.125%, 07/15/20 | | | 7,330,461 | |

| | 998,000 | | | | | ConvaTec Finance International, SA*m 8.250%, 01/15/19 | | | 1,027,316 | |

| | | | | | Endo Health Solutions, Inc. | | | | |

| | 5,882,000 | | | | | 7.000%, 12/15/20 | | | 6,326,826 | |

| | 784,000 | | | | | 7.000%, 07/15/19 | | | 845,740 | |

| | | | | | HCA Holdings, Inc.m | | | | |

| | 6,274,000 | | | | | 5.875%, 05/01/23 | | | 6,399,480 | |

| | 1,522,000 | | | | | 6.250%, 02/15/21 | | | 1,615,223 | |

| | 2,353,000 | | | | | HCA, Inc.m

7.750%, 05/15/21 | | | 2,588,300 | |

| | 4,514,000 | | | | | Hologic, Inc.m

6.250%, 08/01/20 | | | 4,784,840 | |

| | 1,208,000 | | | | | Salix Pharmaceuticals, Ltd.*m

6.000%, 01/15/21 | | | 1,297,845 | |

| | 4,314,000 | | | | | Teleflex, Inc.^m

6.875%, 06/01/19 | | | 4,610,588 | |

| | 4,823,000 | | | | | Tenet Healthcare Corp.m

6.750%, 02/01/20 | | | 5,088,265 | |

| | | | | | Valeant Pharmaceuticals

International, Inc.*m | | | | |

| | 4,863,000 | | | | | 7.000%, 10/01/20 | | | 5,227,725 | |

| | 753,000 | | | | | 7.500%, 07/15/21 | | | 840,536 | |

| | 745,000 | | | | | VPII Escrow Corp.*

6.750%, 08/15/18 | | | 809,256 | |

| | | | | | | | | | |

| | | | | | | | | 51,451,012 | |

| | | | | | | | | | |

| | | | |

| 10 | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | See accompanying Notes to Schedule of Investments |

Schedule of Investments April 30, 2014 (Unaudited)

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | Industrials (6.9%) | | | | |

| | 3,686,000 | | | | | ACCO Brands Corp.m

6.750%, 04/30/20 | | $ | 3,824,225 | |

| | 2,020,000 | | | | | Clean Harbors, Inc.m

5.125%, 06/01/21 | | | 2,051,562 | |

| | 4,863,000 | | | | | Deluxe Corp.m

6.000%, 11/15/20 | | | 5,103,111 | |

| | 2,259,000 | | | | | Digitalglobe, Inc.m

5.250%, 02/01/21 | | | 2,229,351 | |

| | 4,286,000 | | | | | Dycom Investments, Inc.m

7.125%, 01/15/21 | | | 4,644,952 | |

| | 2,141,000 | | | | | Edgen Murray Corp.*m

8.750%, 11/01/20 | | | 2,476,869 | |

| | 1,729,000 | | | | | Garda World Security Corp.*m

7.250%, 11/15/21 | | | 1,812,208 | |

| | 2,216,000 | | | | | GrafTech International, Ltd.^

6.375%, 11/15/20 | | | 2,274,170 | |

| | 3,572,000 | | | | | H&E Equipment Services, Inc.m

7.000%, 09/01/22 | | | 3,935,897 | |

| | 2,745,000 | | | | | Manitowoc Company, Inc.m

8.500%, 11/01/20 | | | 3,086,409 | |

| | 1,122,000 | | | | | Meritor, Inc.^

6.750%, 06/15/21 | | | 1,187,918 | |

| | 1,161,000 | | | | | Michael Baker Holdings, LLC /

Michael Baker Finance Corp.*m

8.875%, 04/15/19 | | | 1,175,513 | |

| | 2,274,000 | | | | | Michael Baker International, LLC /

CDL Acquisition Company, Inc.*m

8.250%, 10/15/18 | | | 2,421,810 | |

| | 2,353,000 | | | | | Navistar International Corp.^

8.250%, 11/01/21 | | | 2,407,413 | |

| | 1,415,000 | | | | | Nortek, Inc.m

8.500%, 04/15/21 | | | 1,561,806 | |

| | 5,137,000 | | | | | Rexel, SA*^m

6.125%, 12/15/19 | | | 5,480,537 | |

| | 3,812,000 | | | | | Terex Corp.m

6.000%, 05/15/21 | | | 4,083,605 | |

| | 1,588,000 | | | | | Titan International, Inc.*m

6.875%, 10/01/20 | | | 1,675,340 | |

| | | | | | TransDigm, Inc. | | | | |

| | 1,843,000 | | | | | 5.500%, 10/15/20 | | | 1,864,886 | |

| | 1,094,000 | | | | | 7.750%, 12/15/18m | | | 1,164,426 | |

| | 1,569,000 | | | | | Triumph Group, Inc.m

4.875%, 04/01/21 | | | 1,557,233 | |

| | 1,804,000 | | | | | United Continental Holdings, Inc.^

6.375%, 06/01/18 | | | 1,949,448 | |

| | | | | | United Rentals North America, Inc.m | | | | |

| | 4,314,000 | | | | | 7.625%, 04/15/22 | | | 4,869,427 | |

| | 1,098,000 | | | | | 6.125%, 06/15/23 | | | 1,183,095 | |

| | | | | | | | | | |

| | | | | | | | | 64,021,211 | |

| | | | | | | | | | |

| | | | | | Information Technology (5.2%) | | | | |

| | 761,000 | | | | | ACI Worldwide, Inc.*m

6.375%, 08/15/20 | | | 807,611 | |

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | 2,510,000 | | | | | Activision Blizzard, Inc.*m

5.625%, 09/15/21 | | $ | 2,680,994 | |

| | | | | | Amkor Technology, Inc.m | | | | |

| | 2,580,000 | | | | | 6.375%, 10/01/22^ | | | 2,705,775 | |

| | 736,000 | | | | | 6.625%, 06/01/21 | | | 787,520 | |

| | 6,274,000 | | | | | Belden, Inc.*^m

5.500%, 09/01/22 | | | 6,344,583 | |

| | 1,569,000 | | | | | Equinix, Inc.m

5.375%, 04/01/23 | | | 1,603,322 | |

| | 5,098,000 | | | | | Hughes Satellite Systems Corp.m

7.625%, 06/15/21 | | | 5,757,554 | |

| | 3,137,000 | | | | | J2 Global, Inc.m

8.000%, 08/01/20 | | | 3,413,448 | |

| | 2,353,000 | | | | | Magnachip Semiconductor, Inc.^

6.625%, 07/15/21 | | | 2,341,235 | |

| | 6,596,000 | | | | | Nuance Communications, Inc.*^m

5.375%, 08/15/20 | | | 6,666,082 | |

| | | | | | NXP Semiconductors, NV*m | | | | |

| | 1,569,000 | | | | | 5.750%, 02/15/21 | | | 1,662,159 | |

| | 627,000 | | | | | 5.750%, 03/15/23 | | | 660,701 | |

| | 3,533,000 | | | | | Sungard Data Systems, Inc.m

6.625%, 11/01/19 | | | 3,709,650 | |

| | 2,667,000 | | | | | ViaSat, Inc.m

6.875%, 06/15/20 | | | 2,862,024 | |

| | 4,314,000 | | | | | Viasystems, Inc.*m

7.875%, 05/01/19 | | | 4,621,373 | |

| | 1,412,000 | | | | | WEX, Inc.*m

4.750%, 02/01/23 | | | 1,326,398 | |

| | | | | | | | | | |

| | | | | | | | | 47,950,429 | |

| | | | | | | | | | |

| | | | | | Materials (3.5%) | | | | |

| | 1,125,000 | | | | | Chemtura Corp.m

5.750%, 07/15/21 | | | 1,169,297 | |

| | | | | | First Quantum Minerals, Ltd.* | | | | |

| | 1,194,000 | | | | | 7.000%, 02/15/21 | | | 1,210,418 | |

| | 1,194,000 | | | | | 6.750%, 02/15/20 | | | 1,208,925 | |

| | 5,882,000 | | | | | FMG Resources*^

8.250%, 11/01/19 | | | 6,492,257 | |

| | 3,459,000 | | | | | Greif, Inc.m

7.750%, 08/01/19 | | | 3,958,393 | |

| | | | | | INEOS Group Holdings, SA*^ | | | | |

| | 1,725,000 | | | | | 6.125%, 08/15/18 | | | 1,791,844 | |

| | 941,000 | | | | | 5.875%, 02/15/19 | | | 960,996 | |

| | | | | | New Gold, Inc.*m | | | | |

| | 3,137,000 | | | | | 7.000%, 04/15/20 | | | 3,315,417 | |

| | 863,000 | | | | | 6.250%, 11/15/22 | | | 886,733 | |

| | 1,843,000 | | | | | PH Glatfelter Companym

5.375%, 10/15/20 | | | 1,921,327 | |

| | | | | | Sealed Air Corp.*m | | | | |

| | 1,612,000 | | | | | 6.500%, 12/01/20 | | | 1,786,298 | |

| | 886,000 | | | | | 5.250%, 04/01/23 | | | 899,290 | |

| | 4,471,000 | | | | | Trinseo Materials Operating, SCAm

8.750%, 02/01/19 | | | 4,786,764 | |

| | 2,196,000 | | | | | United States Steel Corp.^m

6.875%, 04/01/21 | | | 2,345,602 | |

| | | | | | | | | | |

| | | | | | | | | 32,733,561 | |

| | | | | | | | | | |

| | | | | | |

| See accompanying Notes to Schedule of Investments | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | | 11 | |

Schedule of Investments April 30, 2014 (Unaudited)

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | Telecommunication Services (2.1%) | | | | |

| | 1,597,000 | | | | | CenturyLink, Inc.m

6.750%, 12/01/23 | | $ | 1,717,645 | |

| | 2,182,000 | | | | | Frontier Communications Corp.m 7.625%, 04/15/24 | | | 2,266,553 | |

| | | | | | Intelsat, SA | | | | |

| | 4,392,000 | | | | | 7.750%, 06/01/21^ | | | 4,584,150 | |

| | 314,000 | | | | | 8.125%, 06/01/23 | | | 330,681 | |

| | 1,843,000 | | | | | SBA Communications Corp.m

5.625%, 10/01/19 | | | 1,939,758 | |

| | | | | | Sprint Corp.*m | | | | |

| | 2,525,000 | | | | | 7.875%, 09/15/23 | | | 2,783,812 | |

| | 1,161,000 | | | | | 7.125%, 06/15/24 | | | 1,216,873 | |

| | 812,000 | | | | | 7.250%, 09/15/21 | | | 885,080 | |

| | 3,686,000 | | | | | T-Mobile USA, Inc.^

6.625%, 04/01/23 | | | 3,953,235 | |

| | | | | | | | | | |

| | | | | | | | | 19,677,787 | |

| | | | | | | | | | |

| | | | | | Utilities (1.1%) | | | | |

| | 2,353,000 | | | | | AES Corp.m

7.375%, 07/01/21 | | | 2,695,655 | |

| | 3,890,000 | | | | | AmeriGas Finance Corp.^m

7.000%, 05/20/22 | | | 4,288,725 | |

| | | | | | Calpine Corp.* | | | | |

| | 2,353,000 | | | | | 7.875%, 07/31/20m | | | 2,585,359 | |

| | 339,000 | | | | | 7.500%, 02/15/21^ | | | 371,629 | |

| | | | | | | | | | |

| | | | | | | | | 9,941,368 | |

| | | | | | | | | | |

| | | | | | TOTAL CORPORATE BONDS

(Cost $440,224,617) | | | 463,759,674 | |

| | | | | | | | | | |

| | CONVERTIBLE BONDS (50.9%) | |

| | | | | | Consumer Discretionary (11.4%) | | | | |

| | 6,400,000 | | | | | HomeAway, Inc.*

0.125%, 04/01/19 | | | 6,183,680 | |

| | | | | | Iconix Brand Group, Inc.m | | | | |

| | 5,600,000 | | | | | 1.500%, 03/15/18 | | | 8,180,704 | |

| | 2,000,000 | | | | | 2.500%, 06/01/16 | | | 2,891,680 | |

| | | | | | Jarden Corp.*^ | | | | |

| | 8,015,000 | | | | | 1.125%, 03/15/34 | | | 7,992,839 | |

| | 6,000,000 | | | | | 1.500%, 06/15/19m | | | 7,096,020 | |

| | 2,350,000 | | | | | KB Home^

1.375%, 02/01/19 | | | 2,322,341 | |

| | 16,850,000 | | | | | Liberty Interactive, LLC

(Time Warner Cable, Inc.,

Time Warner, Inc.)§

0.750%, 03/30/43 | | | 21,965,997 | |

| | 5,050,000 | | | | | Liberty Media Corp.*^

1.375%, 10/15/23 | | | 4,918,902 | |

| | 10,500,000 | | | | | MGM Resorts International^m

4.250%, 04/15/15 | | | 14,952,367 | |

| | 6,027,000 | | | | | Priceline Group, Inc.^m

1.000%, 03/15/18 | | | 8,429,151 | |

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | 4,800,000 | | | | | Standard Pacific Corp.^m

1.250%, 08/01/32 | | $ | 5,819,832 | |

| | | | | | Tesla Motors, Inc. | |

| | 12,150,000 | | | | | 1.250%, 03/01/21 | | | 11,071,019 | |

| | 4,000,000 | | | | | 0.250%, 03/01/19^ | | | 3,713,060 | |

| | | | | | | | | | |

| | | | | | | | | 105,537,592 | |

| | | | | | | | | | |

| | | | | | Energy (1.2%) | | | | |

| | 8,500,000 | | | | | Chesapeake Energy Corp.^m

2.250%, 12/15/38 | | | 8,097,950 | |

| | 3,300,000 | | | | | Energy XXI Bermuda, Ltd.*m

3.000%, 12/15/18 | | | 3,260,153 | |

| | | | | | | | | | |

| | | | | | | | | 11,358,103 | |

| | | | | | | | | | |

| | | | | | Financials (5.7%) | | | | |

| | | | | | Ares Capital Corp.m | | | | |

| | 7,300,000 | | | | | 4.750%, 01/15/18 | | | 7,849,872 | |

| | 4,027,000 | | | | | 5.750%, 02/01/16 | | | 4,373,866 | |

| | 1,600,000 | | | EUR | | Azimut Holding S.p.A.

2.125%, 11/25/20 | | | 2,537,678 | |

| | 2,850,000 | | | | | Health Care REIT, Inc.m

3.000%, 12/01/29 | | | 3,519,964 | |

| | 3,500,000 | | | | | IAS Operating Partnership, LP*m

5.000%, 03/15/18 | | | 3,413,568 | |

| | 1,215,000 | | | | | Jefferies Group, Inc.m

3.875%, 11/01/29 | | | 1,291,648 | |

| | | | | | MGIC Investment Corp.m | | | | |

| | 5,400,000 | | | | | 5.000%, 05/01/17^ | | | 6,215,319 | |

| | 4,400,000 | | | | | 2.000%, 04/01/20 | | | 6,294,552 | |

| | 5,000,000 | | | | | National Health Investors, Inc.

3.250%, 04/01/21 | | | 5,008,800 | |

| | 3,047,000 | | | | | Portfolio Recovery Associates, Inc.*m

3.000%, 08/01/20 | | | 3,579,844 | |

| | 4,800,000 | | | | | Prologis, Inc.^

3.250%, 03/15/15 | | | 5,487,216 | |

| | 2,900,000 | | | | | Starwood Property Trust, Inc.^

4.550%, 03/01/18 | | | 3,357,693 | |

| | | | | | | | | | |

| | | | | | | | | 52,930,020 | |

| | | | | | | | | | |

| | | | | | Health Care (11.3%) | | | | |

| | | | | | BioMarin Pharmaceutical, Inc.^ | | | | |

| | 5,742,000 | | | | | 0.750%, 10/15/18 | | | 5,886,785 | |

| | 5,711,000 | | | | | 1.500%, 10/15/20m | | | 5,872,450 | |

| | 5,900,000 | | | | | Cepheid, Inc.*^

1.250%, 02/01/21 | | | 5,953,041 | |

| | 12,250,000 | | | | | Cubist Pharmaceuticals, Inc.*^m

1.875%, 09/01/20 | | | 14,264,757 | |

| | 3,050,000 | | | | | Emergent Biosolutions, Inc.*^

2.875%, 01/15/21 | | | 3,417,174 | |

| | 3,175,000 | | | | | Fluidigm Corp.m

2.750%, 02/01/34 | | | 3,385,391 | |

| | 4,100,000 | | | | | Gilead Sciences, Inc.

1.625%, 05/01/16 | | | 14,145,205 | |

| | 2,800,000 | | | | | Hologic, Inc.‡

2.000%, 12/15/37 | | | 3,148,376 | |

| | | | |

| 12 | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | See accompanying Notes to Schedule of Investments |

Schedule of Investments April 30, 2014 (Unaudited)

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | 2,644,000 | | | | | Illumina, Inc.*m

0.250%, 03/15/16 | | $ | 4,491,244 | |

| | 1,435,000 | | | | | Incyte Corp, Ltd.*m

1.250%, 11/15/20 | | | 1,760,652 | |

| | 1,304,000 | | | | | Medicines Company

1.375%, 06/01/17 | | | 1,541,452 | |

| | 5,689,000 | | | | | Medidata Solutions, Inc.*^

1.000%, 08/01/18 | | | 5,741,879 | |

| | 5,745,000 | | | | | Molina Healthcare, Inc.^

1.125%, 01/15/20 | | | 6,485,473 | |

| | 5,450,000 | | | | | Salix Pharmaceuticals, Ltd.^m

1.500%, 03/15/19 | | | 9,771,796 | |

| | 12,700,000 | | | | | WellPoint, Inc.m

2.750%, 10/15/42 | | | 18,560,923 | |

| | | | | | | | | | |

| | | | | | | | | 104,426,598 | |

| | | | | | | | | | |

| | | | | | Industrials (3.4%) | | | | |

| | 3,397,000 | | | | | Air Lease Corp.^

3.875%, 12/01/18 | | | 4,911,518 | |

| | 3,650,000 | | | | | Alliant Techsystems, Inc.m

3.000%, 08/15/24 | | | 6,872,950 | |

| | 1,550,000 | | | | | Greenbrier Companies, Inc.m

3.500%, 04/01/18 | | | 2,402,353 | |

| | 10,500,000 | | | | | Trinity Industries, Inc.^m

3.875%, 06/01/36 | | | 17,407,635 | |

| | | | | | | | | | |

| | | | | | | | | 31,594,456 | |

| | | | | | | | | | |

| | | | | | Information Technology (15.3%) | | | | |

| | 3,300,000 | | | | | Cardtronics, Inc.*

1.000%, 12/01/20 | | | 3,072,861 | |

| | 3,300,000 | | | | | Citrix Systems, Inc.*

0.500%, 04/15/19 | | | 3,300,000 | |

| | 6,400,000 | | | | | Concur Technologies, Inc.*^m

0.500%, 06/15/18 | | | 6,869,408 | |

| | 3,450,000 | | | | | Cornerstone OnDemand, Inc.*

1.500%, 07/01/18 | | | 3,589,121 | |

| | 759,000 | | | | | Electronic Arts, Inc.^

0.750%, 07/15/16 | | | 866,672 | |

| | 4,400,000 | | | | | Finisar Corp.*^

0.500%, 12/15/33 | | | 5,057,580 | |

| | 6,200,000 | | | | | InvenSense, Inc.*^m

1.750%, 11/01/18 | | | 7,449,672 | |

| | 11,944,000 | | | | | Linear Technology Corp.

3.000%, 05/01/27 | | | 13,986,723 | |

| | 14,250,000 | | | | | Mentor Graphics Corp.^

4.000%, 04/01/31 | | | 17,284,751 | |

| | 4,165,000 | | | | | Netsuite, Inc.*^

0.250%, 06/01/18 | | | 4,283,702 | |

| | 1,814,000 | | | | | Novellus Systems, Inc.^

2.625%, 05/15/41 | | | 3,213,664 | |

| | 3,300,000 | | | | | NVIDIA Corp.*^m

1.000%, 12/01/18 | | | 3,709,613 | |

| | 5,757,000 | | | | | ON Semiconductor Corp.^

2.625%, 12/15/26 | | | 7,028,606 | |

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | 3,600,000 | | | | | Salesforce.com, Inc.^m

0.250%, 04/01/18 | | $ | 3,967,866 | |

| | 25,000,000 | | | | | SanDisk Corp.*^m

0.500%, 10/15/20 | | | 28,450,500 | |

| | 11,550,000 | | | | | ServiceNow, Inc.*^

0.000%, 11/01/18 | | | 11,685,366 | |

| | 1,531,000 | | | | | SunEdison, Inc.*

2.000%, 10/01/18 | | | 2,284,099 | |

| | 6,700,000 | | | | | Take-Two Interactive Software, Inc.^m

1.000%, 07/01/18 | | | 7,849,452 | |

| | | | | | Workday, Inc.*m | | | | |

| | 3,450,000 | | | | | 1.500%, 07/15/20 | | | 4,044,107 | |

| | 3,450,000 | | | | | 0.750%, 07/15/18 | | | 3,986,268 | |

| | | | | | | | | | |

| | | | | | | | | 141,980,031 | |

| | | | | | | | | | |

| | | | | | Materials (2.6%) | | | | |

| | 6,950,000 | | | | | Cemex, SAB de CV

3.250%, 03/15/16 | | | 9,896,904 | |

| | 5,200,000 | | | | | Glencore Finance Europe, SAm

5.000%, 12/31/14 | | | 5,704,820 | |

| | | | | | RTI International Metals, Inc. | | | | |

| | 2,800,000 | | | | | 1.625%, 10/15/19^ | | | 2,823,002 | |

| | 2,600,000 | | | | | 3.000%, 12/01/15 | | | 2,776,228 | |

| | 2,600,000 | | | | | Steel Dynamics, Inc.m

5.125%, 06/15/14 | | | 2,821,208 | |

| | | | | | | | | | |

| | | | | | | | | 24,022,162 | |

| | | | | | | | | | |

| | | | | | TOTAL CONVERTIBLE BONDS

(Cost $419,536,787) | | | 471,848,962 | |

| | | | | | | | | | |

| | | | | | | | | | |

| | U.S. GOVERNMENT AND AGENCY SECURITY (0.1%) | |

| | 1,137,000 | | | | | United States Treasury Note~

0.125%, 12/31/14

(Cost $1,137,000) | | | 1,137,489 | |

| | | | | | | | | | |

| | | | | | | | | | |

| | SYNTHETIC CONVERTIBLE SECURITIES (16.2%) ¤ | |

| | Corporate Bonds (13.8%) | | | | |

| | | | | | Consumer Discretionary (2.8%) | | | | |

| | 302,000 | | | | | Altice, SA*

7.750%, 05/15/22 | | | 315,213 | |

| | 448,000 | | | | | Bon-Ton Department Stores, Inc.^m

8.000%, 06/15/21 | | | 430,360 | |

| | 75,000 | | | | | Brunswick Corp.*m

4.625%, 05/15/21 | | | 74,297 | |

| | 80,000 | | | | | Century Communities*

6.875%, 05/15/22 | | | 79,391 | |

| | 431,000 | | | | | Chrysler Group, LLC*

8.000%, 06/15/19 | | | 471,676 | |

| | 233,000 | | | | | Cogeco Cable, Inc.*m

4.875%, 05/01/20 | | | 234,893 | |

| | 1,318,000 | | | | | Cooper Tire & Rubber Company^m

8.000%, 12/15/19 | | | 1,482,750 | |

| | 976,000 | | | | | Dana Holding Corp.m

6.750%, 02/15/21 | | | 1,058,350 | |

| | | | | | |

| See accompanying Notes to Schedule of Investments | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | | 13 | |

Schedule of Investments April 30, 2014 (Unaudited)

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | | | | | DISH DBS Corp.m | |

| | 1,458,000 | | | | | 5.125%, 05/01/20 | | $ | 1,534,545 | |

| | 1,178,000 | | | | | 7.875%, 09/01/19^ | | | 1,398,875 | |

| | 863,000 | | | | | Dufry Finance, SCA*m

5.500%, 10/15/20 | | | 898,059 | |

| | 611,000 | | | | | Golden Nugget Escrow, Inc.*^m

8.500%, 12/01/21 | | | 630,476 | |

| | 286,000 | | | | | Goodyear Tire & Rubber Companym

8.250%, 08/15/20 | | | 317,103 | |

| | 549,000 | | | | | Greektown Holdings, LLC*^

8.875%, 03/15/19 | | | 567,186 | |

| | 511,000 | | | | | Hasbro, Inc.^m

6.600%, 07/15/28 | | | 576,556 | |

| | | | | | Icahn Enterprises, LP* | | | | |

| | 833,000 | | | | | 5.875%, 02/01/22 | | | 847,577 | |

| | 509,000 | | | | | 6.000%, 08/01/20m | | | 538,904 | |

| | 118,000 | | | | | 4.875%, 03/15/19m | | | 119,696 | |

| | 1,079,000 | | | | | Jaguar Land Rover Automotive, PLC*m

8.125%, 05/15/21 | | | 1,223,316 | |

| | | | | | L Brands, Inc.m | | | | |

| | 647,000 | | | | | 7.600%, 07/15/37 | | | 693,907 | |

| | 147,000 | | | | | 6.950%, 03/01/33 | | | 151,778 | |

| | 304,000 | | | | | Liberty Interactive, LLC^m

8.250%, 02/01/30 | | | 333,260 | |

| | | | | | Meritage Homes Corp.m | | | | |

| | 733,000 | | | | | 7.150%, 04/15/20 | | | 815,921 | |

| | 412,000 | | | | | 7.000%, 04/01/22 | | | 452,942 | |

| | 403,000 | | | | | NCL Corp., Ltd. - Class Cm

5.000%, 02/15/18 | | | 417,861 | |

| | | | | | Neiman Marcus Group LTD, LLC* | | | | |

| | 133,000 | | | | | 8.750%, 10/15/21 | | | 147,298 | |

| | 106,000 | | | | | 8.000%, 10/15/21m | | | 116,534 | |

| | 609,000 | | | | | Netflix, Inc.m

5.375%, 02/01/21 | | | 636,024 | |

| | | | | | Numericable Group, SA* | | | | |

| | 604,000 | | | | | 6.000%, 05/15/22 | | | 619,100 | |

| | 43,000 | | | | | 6.250%, 05/15/24 | | | 44,021 | |

| | 1,229,000 | | | | | Outerwall, Inc.m

6.000%, 03/15/19 | | | 1,276,624 | |

| | 231,000 | | | | | Quiksilver, Inc. / QS Wholesale, Inc.*m

7.875%, 08/01/18 | | | 250,779 | |

| | 834,000 | | | | | Royal Caribbean Cruises, Ltd.^

7.500%, 10/15/27 | | | 940,856 | |

| | | | | | Ryland Group, Inc.m | | | | |

| | 1,186,000 | | | | | 6.625%, 05/01/20^ | | | 1,289,775 | |

| | 321,000 | | | | | 5.375%, 10/01/22 | | | 319,194 | |

| | | | | | Sally Holdings, LLC / Sally Capital, Inc.m | | | | |

| | 403,000 | | | | | 5.750%, 06/01/22^ | | | 428,691 | |

| | 207,000 | | | | | 5.500%, 11/01/23 | | | 211,399 | |

| | 755,000 | | | | | Service Corp. International^m

7.500%, 04/01/27 | | | 811,153 | |

| | 630,000 | | | | | Six Flags Entertainment Corp.*m

5.250%, 01/15/21 | | | 639,056 | |

| | 647,000 | | | | | Taylor Morrison Communities, Inc.*m

5.250%, 04/15/21 | | | 655,492 | |

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | 318,000 | | | | | Time, Inc.*^

5.750%, 04/15/22 | | $ | 317,006 | |

| | | | | | Toll Brothers Finance Corp. | |

| | 712,000 | | | | | 5.625%, 01/15/24^ | | | 740,480 | |

| | 248,000 | | | | | 4.000%, 12/31/18m | | | 254,510 | |

| | 820,000 | | | | | Viking Cruises, Ltd.*m

8.500%, 10/15/22 | | | 930,700 | |

| | | | | | | | | | |

| | | | | | | | | 26,293,584 | |

| | | | | | | | | | |

| | | | | | Consumer Staples (0.7%) | | | | |

| | 209,000 | | | | | Alphabet Holding Company, Inc.m

7.750%, 11/01/17 | | | 216,576 | |

| | 787,000 | | | | | Fidelity & Guaranty Life Holdings, Inc.*m

6.375%, 04/01/21 | | | 842,090 | |

| | 1,072,000 | | | | | JBS USA, LLC*m

7.250%, 06/01/21 | | | 1,157,760 | |

| | 1,165,000 | | | | | Land O’Lakes, Inc.*^m

6.000%, 11/15/22 | | | 1,231,260 | |

| | | | | | Post Holdings, Inc.m | | | | |

| | 1,630,000 | | | | | 7.375%, 02/15/22 | | | 1,755,306 | |

| | 93,000 | | | | | 7.375%, 02/15/22* | | | 99,161 | |

| | 679,000 | | | | | Smithfield Foods, Inc.m

6.625%, 08/15/22 | | | 740,959 | |

| | | | | | | | | | |

| | | | | | | | | 6,043,112 | |

| | | | | | | | | | |

| | | | | | Energy (2.9%) | | | | |

| | 721,000 | | | | | Atwood Oceanics, Inc.m

6.500%, 02/01/20 | | | 772,822 | |

| | 539,000 | | | | | Berry Petroleum Company

6.375%, 09/15/22 | | | 556,517 | |

| | 539,000 | | | | | Bonanza Creek Energy, Inc.m

6.750%, 04/15/21 | | | 576,730 | |

| | 485,000 | | | | | Calfrac Holdings, LP*m

7.500%, 12/01/20 | | | 516,222 | |

| | | | | | Calumet Specialty Products Partners, LP | | | | |

| | 496,000 | | | | | 7.625%, 01/15/22m | | | 522,350 | |

| | 412,000 | | | | | 6.500%, 04/15/21*^ | | | 413,030 | |

| | 324,000 | | | | | 9.625%, 08/01/20m | | | 374,423 | |

| | | | | | Carrizo Oil & Gas, Inc.m | | | | |

| | 953,000 | | | | | 7.500%, 09/15/20 | | | 1,048,300 | |

| | 704,000 | | | | | 8.625%, 10/15/18 | | | 754,600 | |

| | 358,000 | | | | | Chesapeake Oilfield Operating, LLCm

6.625%, 11/15/19 | | | 374,334 | |

| | 1,294,000 | | | | | Cimarex Energy Company^m

5.875%, 05/01/22 | | | 1,411,269 | |

| | 1,510,000 | | | | | Drill Rigs Holdings, Inc.*m

6.500%, 10/01/17 | | | 1,560,019 | |

| | 626,000 | | | | | Energy Transfer Equity, LPm

5.875%, 01/15/24 | | | 640,085 | |

| | 453,000 | | | | | EPL OIl & Gas, Inc.

8.250%, 02/15/18 | | | 489,240 | |

| | 126,000 | | | | | Forum Energy Technologies, Inc.*m

6.250%, 10/01/21 | | | 133,639 | |

| | 1,186,000 | | | | | Gulfmark Offshore, Inc.m

6.375%, 03/15/22 | | | 1,234,181 | |

| | | | |

| 14 | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | See accompanying Notes to Schedule of Investments |

Schedule of Investments April 30, 2014 (Unaudited)

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | 1,376,000 | | | | | Gulfport Energy Corp.m

7.750%, 11/01/20 | | $ | 1,507,580 | |

| | 1,186,000 | | | | | Laredo Petroleum, Inc.m

7.375%, 05/01/22 | | | 1,313,495 | |

| | | | | | Linn Energy, LLCm | | | | |

| | 1,079,000 | | | | | 8.625%, 04/15/20 | | | 1,166,669 | |

| | 431,000 | | | | | 7.250%, 11/01/19*‡ | | | 446,624 | |

| | 324,000 | | | | | 7.750%, 02/01/21 | | | 346,680 | |

| | 216,000 | | | | | 6.500%, 05/15/19 | | | 224,775 | |

| | | | | | Oasis Petroleum, Inc.m | | | | |

| | 904,000 | | | | | 6.500%, 11/01/21 | | | 970,105 | |

| | 270,000 | | | | | 6.875%, 01/15/23 | | | 293,119 | |

| | 490,000 | | | | | Pacific Drilling, SA*m

5.375%, 06/01/20 | | | 478,362 | |

| | 593,000 | | | | | Petroleum Geo-Services, ASA*m

7.375%, 12/15/18 | | | 636,734 | |

| | 370,000 | | | | | Pioneer Energy Services Corp.*m

6.125%, 03/15/22 | | | 380,406 | |

| | 710,000 | | | | | Rice Energy, Inc.*^

6.250%, 05/01/22 | | | 710,444 | |

| | 1,079,000 | | | | | SEACOR Holdings, Inc.m

7.375%, 10/01/19 | | | 1,216,572 | |

| | 539,000 | | | | | SESI, LLCm

7.125%, 12/15/21 | | | 607,722 | |

| | 388,000 | | | | | SM Energy Companym

6.500%, 11/15/21 | | | 418,555 | |

| | 733,000 | | | | | Swift Energy Companym

8.875%, 01/15/20 | | | 774,231 | |

| | 777,000 | | | | | Trinidad Drilling, Ltd.*^

7.875%, 01/15/19 | | | 831,390 | |

| | 2,006,000 | | | | | W&T Offshore, Inc.^

8.500%, 06/15/19 | | | 2,177,764 | |

| | 600,000 | | | | | Western Refining, Inc.m

6.250%, 04/01/21 | | | 624,000 | |

| | | | | | | | | | |

| | | | | | | | | 26,502,988 | |

| | | | | | | | | | |

| | | | | | Financials (0.7%) | | | | |

| | 518,000 | | | | | AON Corp.m

8.205%, 01/01/27 | | | 654,509 | |

| | 1,227,000 | | | | | Black Knight InfoServ, LLCm

5.750%, 04/15/23 | | | 1,318,049 | |

| | 280,000 | | | | | DuPont Fabros Technology, LP

5.875%, 09/15/21 | | | 292,775 | |

| | 233,000 | | | | | First Cash Financial Services, Inc.*

6.750%, 04/01/21 | | | 241,592 | |

| | 427,000 | | | | | iStar Financial, Inc.m

4.875%, 07/01/18 | | | 437,141 | |

| | | | | | Jefferies Finance, LLC*m | |

| | 917,000 | | | | | 7.375%, 04/01/20 | | | 965,716 | |

| | 259,000 | | | | | 6.875%, 04/15/22 | | | 260,295 | |

| | 494,000 | | | | | Nationstar Mortgage, LLC /

Nationstar Capital Corp.m

6.500%, 07/01/21 | | | 473,314 | |

| | 1,186,000 | | | | | Neuberger Berman Group, LLC*m

5.875%, 03/15/22 | | | 1,271,985 | |

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | 636,000 | | | | | Nuveen Investments, Inc.*^

9.125%, 10/15/17 | | $ | 697,215 | |

| | | | | | | | | | |

| | | | | | | | | 6,612,591 | |

| | | | | | | | | | |

| | | | | | Health Care (1.5%) | | | | |

| | 696,000 | | | | | Alere, Inc.m

6.500%, 06/15/20 | | | 731,670 | |

| | 1,877,000 | | | | | Community Health Systems, Inc.m

7.125%, 07/15/20 | | | 2,016,602 | |

| | 274,000 | | | | | ConvaTec Finance International, SA*m

8.250%, 01/15/19 | | | 282,049 | |

| | | | | | Endo Health Solutions, Inc. | |

| | 1,618,000 | | | | | 7.000%, 12/15/20 | | | 1,740,361 | |

| | 216,000 | | | | | 7.000%, 07/15/19 | | | 233,010 | |

| | | | | | HCA Holdings, Inc.m | |

| | 1,726,000 | | | | | 5.875%, 05/01/23 | | | 1,760,520 | |

| | 418,000 | | | | | 6.250%, 02/15/21 | | | 443,602 | |

| | 647,000 | | | | | HCA, Inc.m

7.750%, 05/15/21 | | | 711,700 | |

| | 1,241,000 | | | | | Hologic, Inc.m

6.250%, 08/01/20 | | | 1,315,460 | |

| | 332,000 | | | | | Salix Pharmaceuticals, Ltd.*m

6.000%, 01/15/21 | | | 356,693 | |

| | 1,186,000 | | | | | Teleflex, Inc.^m

6.875%, 06/01/19 | | | 1,267,537 | |

| | 1,327,000 | | | | | Tenet Healthcare Corp.m

6.750%, 02/01/20 | | | 1,399,985 | |

| | | | | | Valeant Pharmaceuticals

International, Inc.*m | |

| | 1,337,000 | | | | | 7.000%, 10/01/20 | | | 1,437,275 | |

| | 207,000 | | | | | 7.500%, 07/15/21 | | | 231,064 | |

| | 205,000 | | | | | VPII Escrow Corp.*

6.750%, 08/15/18 | | | 222,681 | |

| | | | | | | | | | |

| | | | | | | | | 14,150,209 | |

| | | | | | | | | | |

| | | | | | Industrials (1.9%) | | | | |

| | 1,014,000 | | | | | ACCO Brands Corp.m

6.750%, 04/30/20 | | | 1,052,025 | |

| | 555,000 | | | | | Clean Harbors, Inc.m

5.125%, 06/01/21 | | | 563,672 | |

| | 1,337,000 | | | | | Deluxe Corp.m

6.000%, 11/15/20 | | | 1,403,014 | |

| | 621,000 | | | | | Digitalglobe, Inc.m

5.250%, 02/01/21 | | | 612,849 | |

| | 1,179,000 | | | | | Dycom Investments, Inc.m

7.125%, 01/15/21 | | | 1,277,741 | |

| | 589,000 | | | | | Edgen Murray Corp.*m

8.750%, 11/01/20 | | | 681,399 | |

| | 476,000 | | | | | Garda World Security Corp.*m

7.250%, 11/15/21 | | | 498,908 | |

| | 609,000 | | | | | GrafTech International, Ltd.^

6.375%, 11/15/20 | | | 624,986 | |

| | 983,000 | | | | | H&E Equipment Services, Inc.m

7.000%, 09/01/22 | | | 1,083,143 | |

| | 755,000 | | | | | Manitowoc Company, Inc.m

8.500%, 11/01/20 | | | 848,903 | |

| | | | | | |

| See accompanying Notes to Schedule of Investments | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | | 15 | |

Schedule of Investments April 30, 2014 (Unaudited)

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | 308,000 | | | | | Meritor, Inc.^

6.750%, 06/15/21 | | $ | 326,095 | |

| | 319,000 | | | | | Michael Baker Holdings, LLC /

Michael Baker Finance Corp.*m

8.875%, 04/15/19 | | | 322,988 | |

| | 626,000 | | | | | Michael Baker International, LLC /

CDL Acquisition Company, Inc.*m

8.250%, 10/15/18 | | | 666,690 | |

| | 647,000 | | | | | Navistar International Corp.^

8.250%, 11/01/21 | | | 661,962 | |

| | 389,000 | | | | | Nortek, Inc.m

8.500%, 04/15/21 | | | 429,359 | |

| | 1,413,000 | | | | | Rexel, SA*^m

6.125%, 12/15/19 | | | 1,507,494 | |

| | 1,048,000 | | | | | Terex Corp.m

6.000%, 05/15/21 | | | 1,122,670 | |

| | 437,000 | | | | | Titan International, Inc.*m

6.875%, 10/01/20 | | | 461,035 | |

| | | | | | TransDigm, Inc. | |

| | 507,000 | | | | | 5.500%, 10/15/20 | | | 513,021 | |

| | 301,000 | | | | | 7.750%, 12/15/18µ | | | 320,377 | |

| | 431,000 | | | | | Triumph Group, Inc.m

4.875%, 04/01/21 | | | 427,768 | |

| | 496,000 | | | | | United Continental Holdings, Inc.^

6.375%, 06/01/18 | | | 535,990 | |

| | | | | | United Rentals North America, Inc.m | |

| | 1,186,000 | | | | | 7.625%, 04/15/22 | | | 1,338,697 | |

| | 302,000 | | | | | 6.125%, 06/15/23 | | | 325,405 | |

| | | | | | | | | | |

| | | | | | | | | 17,606,191 | |

| | | | | | | | | | |

| | | | | | Information Technology (1.4%) | |

| | 209,000 | | | | | ACI Worldwide, Inc.*m

6.375%, 08/15/20 | | | 221,801 | |

| | 690,000 | | | | | Activision Blizzard, Inc.*m

5.625%, 09/15/21 | | | 737,006 | |

| | | | | | Amkor Technology, Inc.m | |

| | 710,000 | | | | | 6.375%, 10/01/22^ | | | 744,612 | |

| | 203,000 | | | | | 6.625%, 06/01/21 | | | 217,210 | |

| | 1,726,000 | | | | | Belden, Inc.*^m

5.500%, 09/01/22 | | | 1,745,417 | |

| | 431,000 | | | | | Equinix, Inc.m

5.375%, 04/01/23 | | | 440,428 | |

| | 1,402,000 | | | | | Hughes Satellite Systems Corp.m

7.625%, 06/15/21 | | | 1,583,384 | |

| | 863,000 | | | | | J2 Global, Inc.m

8.000%, 08/01/20 | | | 939,052 | |

| | 647,000 | | | | | Magnachip Semiconductor, Inc.^

6.625%, 07/15/21 | | | 643,765 | |

| | 1,814,000 | | | | | Nuance Communications, Inc.*^m

5.375%, 08/15/20 | | | 1,833,274 | |

| | | | | | NXP Semiconductors, NV*m | |

| | 431,000 | | | | | 5.750%, 02/15/21 | | | 456,591 | |

| | 173,000 | | | | | 5.750%, 03/15/23 | | | 182,299 | |

| | 972,000 | | | | | Sungard Data Systems, Inc.m

6.625%, 11/01/19 | | | 1,020,600 | |

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | 733,000 | | | | | ViaSat, Inc.µ

6.875%, 06/15/20 | | $ | 786,601 | |

| | 1,186,000 | | | | | Viasystems, Inc.*µ

7.875%, 05/01/19 | | | 1,270,502 | |

| | 388,000 | | | | | WEX, Inc.*µ

4.750%, 02/01/23 | | | 364,478 | |

| | | | | | | | | | |

| | | | | | | | | 13,187,020 | |

| | | | | | | | | | |

| | | | | | Materials (1.0%) | | | | |

| | 310,000 | | | | | Chemtura Corp.m

5.750%, 07/15/21 | | | 322,206 | |

| | | | | | First Quantum Minerals, Ltd.* | |

| | 329,000 | | | | | 7.000%, 02/15/21 | | | 333,524 | |

| | 329,000 | | | | | 6.750%, 02/15/20 | | | 333,113 | |

| | 1,618,000 | | | | | FMG Resources*^

8.250%, 11/01/19 | | | 1,785,867 | |

| | 951,000 | | | | | Greif, Inc.m

7.750%, 08/01/19 | | | 1,088,301 | |

| | | | | | INEOS Group Holdings, SA*^ | |

| | 475,000 | | | | | 6.125%, 08/15/18 | | | 493,406 | |

| | 259,000 | | | | | 5.875%, 02/15/19 | | | 264,504 | |

| | | | | | New Gold, Inc.*m | |

| | 863,000 | | | | | 7.000%, 04/15/20 | | | 912,083 | |

| | 237,000 | | | | | 6.250%, 11/15/22 | | | 243,518 | |

| | 507,000 | | | | | PH Glatfelter Companym

5.375%, 10/15/20 | | | 528,548 | |

| | | | | | Sealed Air Corp.*m | |

| | 443,000 | | | | | 6.500%, 12/01/20 | | | 490,899 | |

| | 244,000 | | | | | 5.250%, 04/01/23 | | | 247,660 | |

| | 1,229,000 | | | | | Trinseo Materials Operating, SCAm

8.750%, 02/01/19 | | | 1,315,798 | |

| | 604,000 | | | | | United States Steel Corp.^m

6.875%, 04/01/21 | | | 645,147 | |

| | | | | | | | | | |

| | | | | | | | | 9,004,574 | |

| | | | | | | | | | |

| | | | | | Telecommunication Services (0.6%) | | | | |

| | 439,000 | | | | | CenturyLink, Inc.m

6.750%, 12/01/23 | | | 472,164 | |

| | 600,000 | | | | | Frontier Communications Corp.m

7.625%, 04/15/24 | | | 623,250 | |

| | | | | | Intelsat, SA | |

| | 1,208,000 | | | | | 7.750%, 06/01/21^ | | | 1,260,850 | |

| | 86,000 | | | | | 8.125%, 06/01/23 | | | 90,569 | |

| | 507,000 | | | | | SBA Communications Corp.m

5.625%, 10/01/19 | | | 533,618 | |

| | | | | | Sprint Corp.*m | |

| | 695,000 | | | | | 7.875%, 09/15/23 | | | 766,237 | |

| | 319,000 | | | | | 7.125%, 06/15/24 | | | 334,352 | |

| | 223,000 | | | | | 7.250%, 09/15/21 | | | 243,070 | |

| | 1,014,000 | | | | | T-Mobile USA, Inc.^

6.625%, 04/01/23 | | | 1,087,515 | |

| | | | | | | | | | |

| | | | | | | | | 5,411,625 | |

| | | | | | | | | | |

| | | | | | Utilities (0.3%) | | | | |

| | 647,000 | | | | | AES Corp.m

7.375%, 07/01/21 | | | 741,219 | |

| | | | |

| 16 | | CALAMOS CONVERTIBLE OPPORTUNITIES AND INCOME FUND SEMIANNUAL REPORT | | See accompanying Notes to Schedule of Investments |

Schedule of Investments April 30, 2014 (Unaudited)

| | | | | | | | | | |

PRINCIPAL

AMOUNT | | | | | | | VALUE | |

| | | | | | | | | | |

| | 1,070,000 | | | | | AmeriGas Finance Corp.^m

7.000%, 05/20/22 | | $ | 1,179,675 | |

| | | | | | Calpine Corp.* | |

| | 647,000 | | | | | 7.875%, 07/31/20m | | | 710,891 | |

| | 93,000 | | | | | 7.500%, 02/15/21^ | | | 101,951 | |

| | | | | | | | | | |

| | | | | | | | | 2,733,736 | |

| | | | | | | | | | |

| | | | | | TOTAL CORPORATE BONDS | | | 127,545,630 | |

| | | | | | | | | | |

| | | | | | | | | | |

| | U.S. Government and Agency Security (0.0%) | |

| | 313,000 | | | | | United States Treasury Note~

0.125%, 12/31/14 | | | 313,134 | |

| | | | | | | | | | |

NUMBER OF

CONTRACTS | | | | | | | VALUE | |

| | Purchased Options (2.4%) # | |

| | | | | | Consumer Discretionary (0.3%) | |

| | 8,100 | | | | | D.R. Horton, Inc.

Call, 08/16/14, Strike $24.00 | | | 664,200 | |

| | 1,775 | | | | | Lennar Corp.

Call, 01/17/15, Strike $37.00 | | | 825,375 | |

| | 515 | | | | | Michael Kors Holdings, Ltd.

Call, 01/17/15, Strike $82.50 | | | 785,375 | |

| | 4,900 | | | | | Toll Brothers, Inc.

Call, 09/20/14, Strike $37.00 | | | 673,750 | |

| | | | | | | | | | |

| | | | | | | | | 2,948,700 | |

| | | | | | | | | | |

| | | | | | Energy (0.3%) | | | | |

| | 736 | | | | | Continental Resources, Inc.

Call, 01/17/15, Strike $105.00 | | | 2,675,360 | |

| | | | | | | | | | |

| | | | | | Health Care (1.0%) | | | | |

| | 3,825 | | | | | Gilead Sciences, Inc.

Call, 01/17/15, Strike $72.50 | | | 4,570,875 | |

| | 3,760 | | | | | Mylan, Inc.

Call, 01/17/15, Strike $45.00 | | | 3,308,800 | |

| | 190 | | | | | Regeneron Pharmaceuticals, Inc.