Exhibit 99.1

Investor Day 2013 December 6, 2013

1

Dr. Luis A. Clavell-Rodríguez Chairman of the Board Triple-S Management Corporation Welcome

2

Presenters Ramón Ruiz-Comas President and CEO Amilcar Jordán Chief Financial Officer Carlos Carrero Managed Care - Medicare Pablo Almodóvar Managed Care – Commercial and Medicaid Frank Astor Chief Medical Officer Scott Serota CEO, Blue Cross Blue Shield Association

3

Agenda 1:10 – 2:30 GTS Overview Ramón Ruiz-Comas Financial Overview Amilcar L. Jordán Medicare Carlos Carrero Commercial and Medicaid Pablo Almodóvar Member Care Frank Astor Blue Cross Blue Shield Scott Serota 2:30 – 3:00 Q & A

4

Safe Harbor This presentation and the accompanying oral remarks (collectively, this “presentation”) may contain forward-looking statements within the meaning of the U.S. federal securities laws. Forward-looking statements are statements that include information about possible or assumed future sales, results of operations, developments, regulatory approvals or other circumstances. Statements that use the terms “believe,” “expect,” “plan,” intend,” “estimate,” “anticipate,” “project,” “may,” “will,” “shall,” “should” and similar expressions, whether in the positive or negative, are intended to identify forward-looking statements. These statements involve estimates and predictions of our future financial condition, performance, plans and strategies, and are thus dependent on a number of factors including, without limitation, assumptions and data that may be imprecise or incorrect. Specific factors that may impact performance or other predictions of future actions have, in many but not all cases, been identified in connection with specific forward-looking statements. Forward-looking statements are subject to risks and uncertainties, and as a result, actual future results may differ significantly from those expressed or implied herein. Such risks and uncertainties are described under headings such as “Risk Factors” in the preliminary prospectus supplement relating to this presentation, in our Annual Report or Form 10-K and in our Quarterly Reports on Form 10-Q. We caution you not to place undue reliance on these forward-looking statements that speak only as of the date they were made. In view of these uncertainties, we do not intend to update or revise any of these forward-looking statements to reflect events or circumstances after the date of this presentation or to reflect the occurrence of unanticipated events.

5

Ramón Ruiz-Comas GTS Overview

6

Triple-S Key Facts Leading Managed Care Organization in Puerto Rico with 2.2 million members Only MCO in Medicare, Medicaid, Group and Individual Over 50 Years in the Market Exclusive Blue Cross Blue Shield licensee for Puerto Rico and the U.S. Virgin Islands Largest physician network on the island Strong contracting with high retention Diversified and complementary business base Life and Property & Casualty Businesses Largest full-line insurance company on the island

7

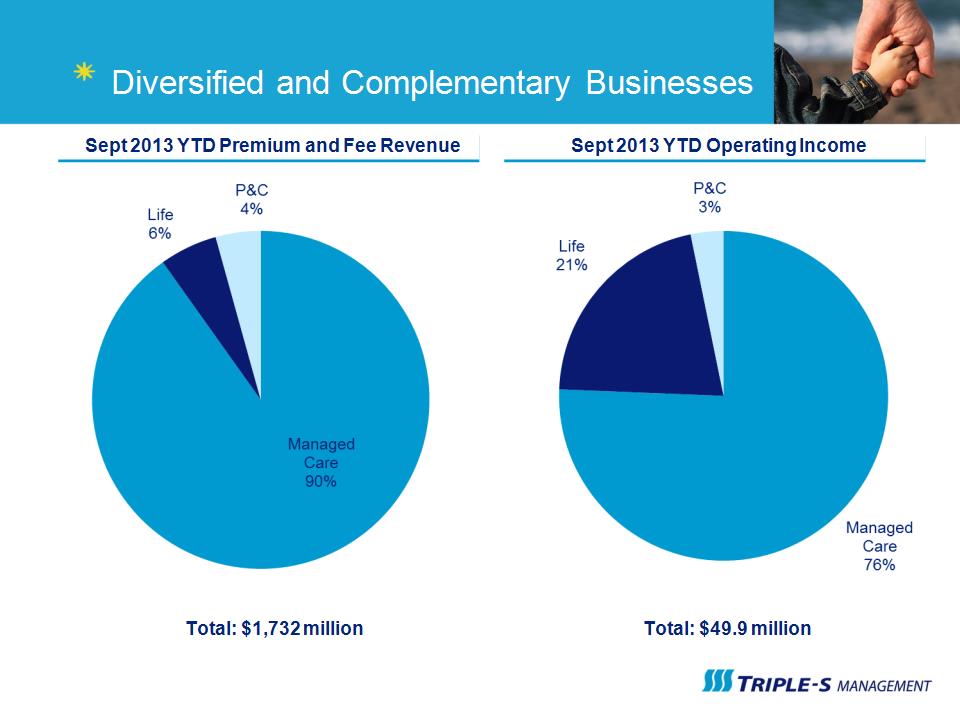

Diversified and Complementary Businesses Sept 2013 YTD Premium and Fee Revenue Sept 2013 YTD Operating Income Total: $1,732 million Total: $49.9 million

8

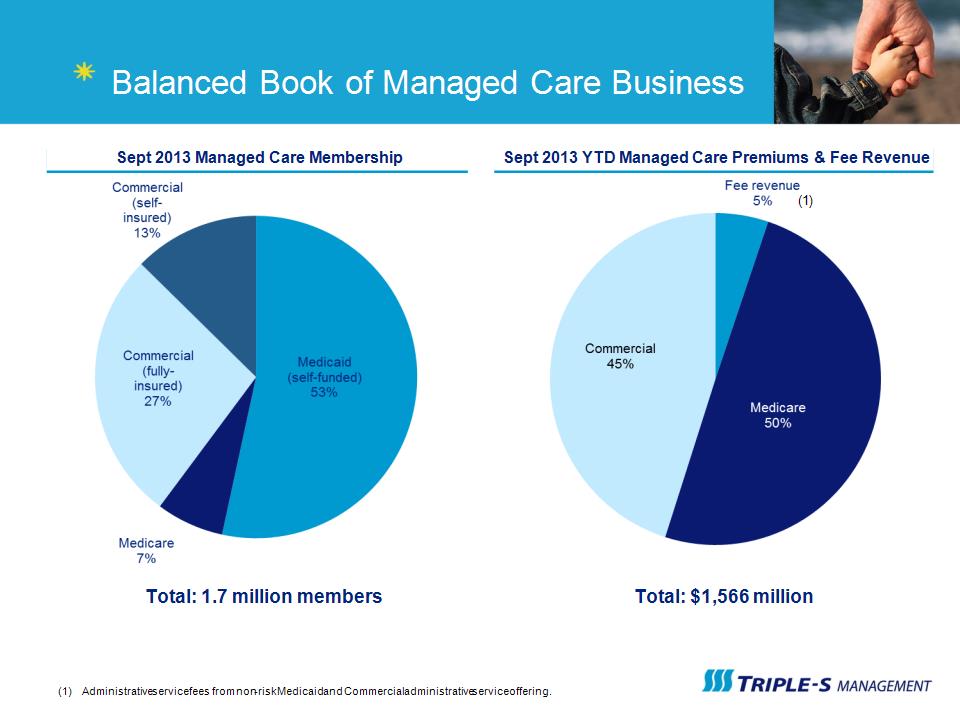

Balanced Book of Managed Care Business Sept 2013 Managed Care Membership Sept 2013 YTD Managed Care Premiums & Fee Revenue Total: 1.7 million members Total: $1,566 million (1) Administrative service fees from non-risk Medicaid and Commercial administrative service offering. (1)

9

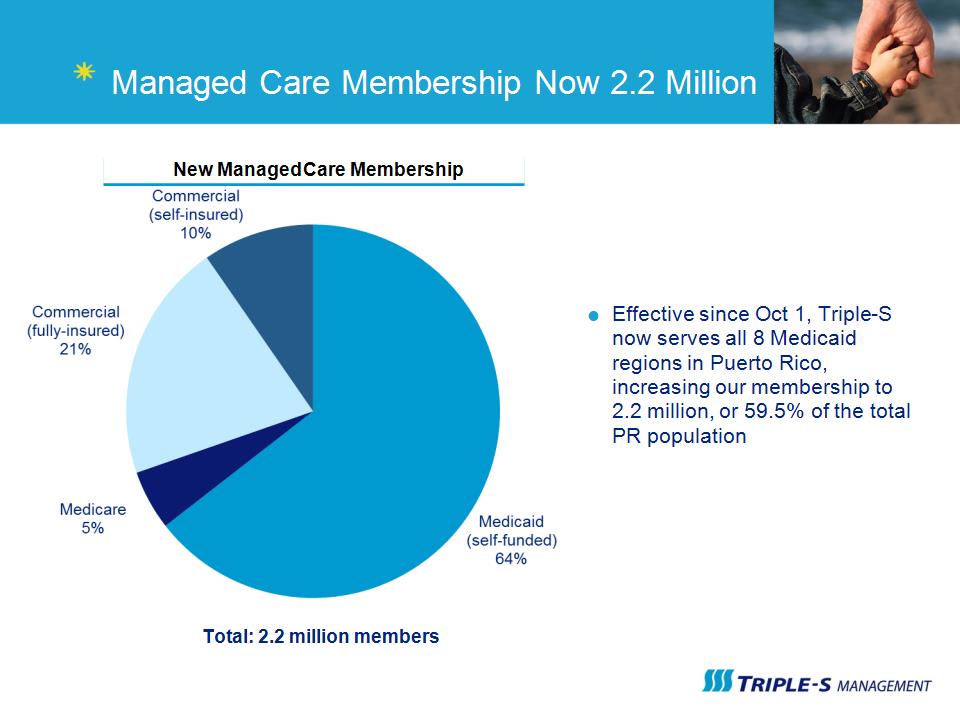

Managed Care Membership Now 2.2 Million Effective since Oct 1, Triple-S now serves all 8 Medicaid regions in Puerto Rico, increasing our membership to 2.2 million, or 59.5% of the total PR population New Managed Care Membership Total: 2.2 million members

10

2013 Highlights Medicare Advantage Turnaround New PBM New Provider Compensation Model Renewal and Expansion of MiSalud (Medicaid) Serve 1.4 million members Class A Stock Conversion Purchase of ASICO – Formal entry into Latin America Costa Rica, British Virgin Islands and Anguilla

11

Puerto Rico Health Insurance Market

12

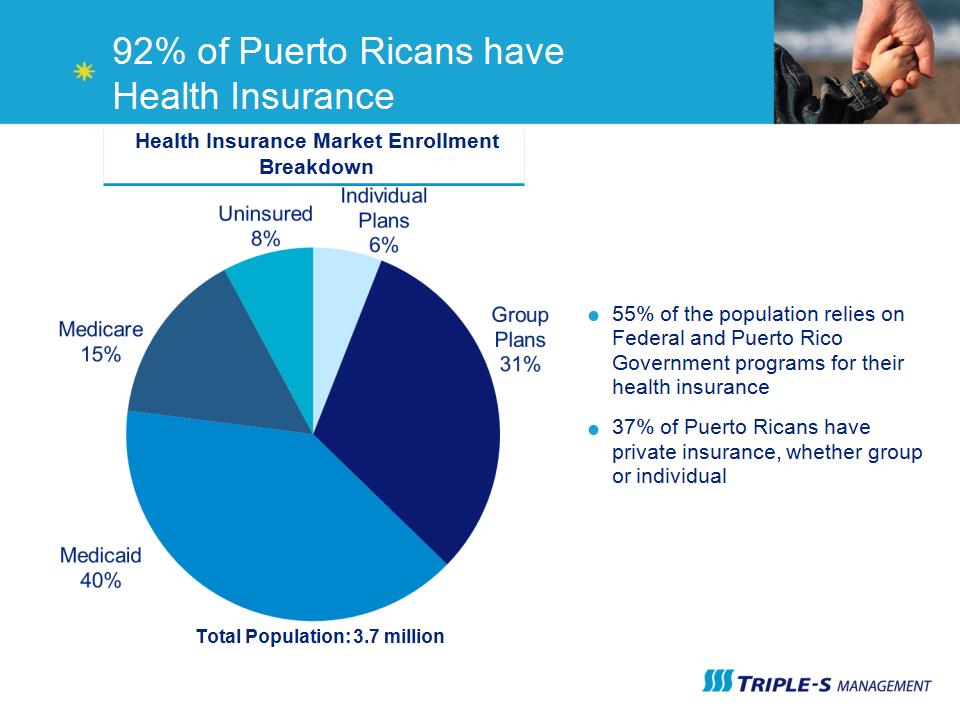

55% of the population relies on Federal and Puerto Rico Government programs for their health insurance 37% of Puerto Ricans have private insurance, whether group or individual Health Insurance Market Enrollment Breakdown Total Population: 3.7 million 92% of Puerto Ricans have Health Insurance

13

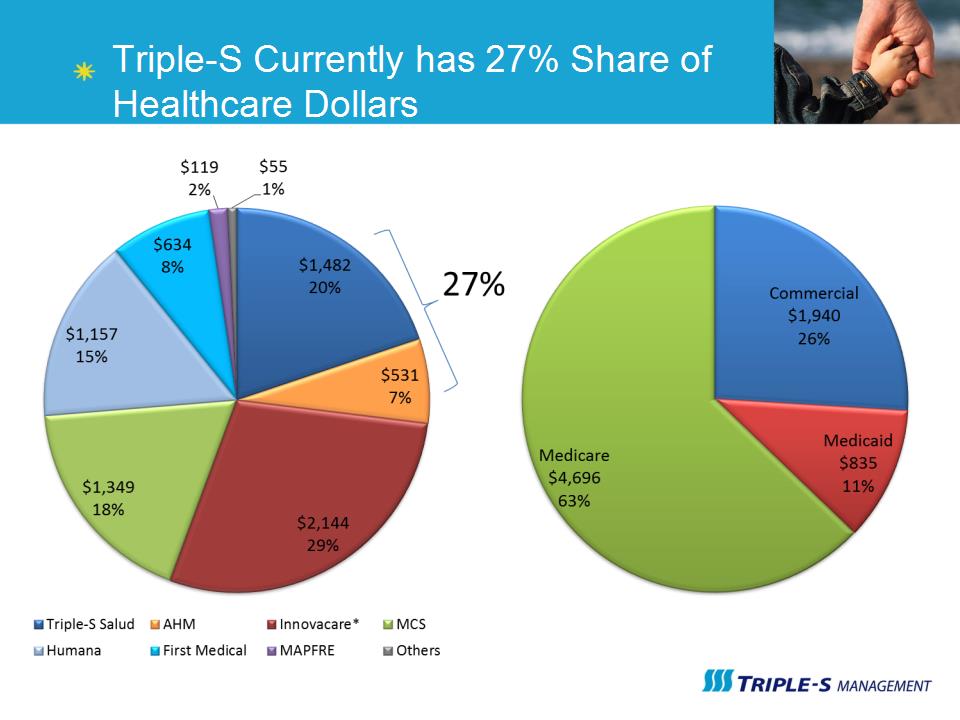

Triple-S Currently has 27% Share of Healthcare Dollars

14

Medicare Advantage is an Opportunity for Triple-S

15

Triple-S Strategy

16

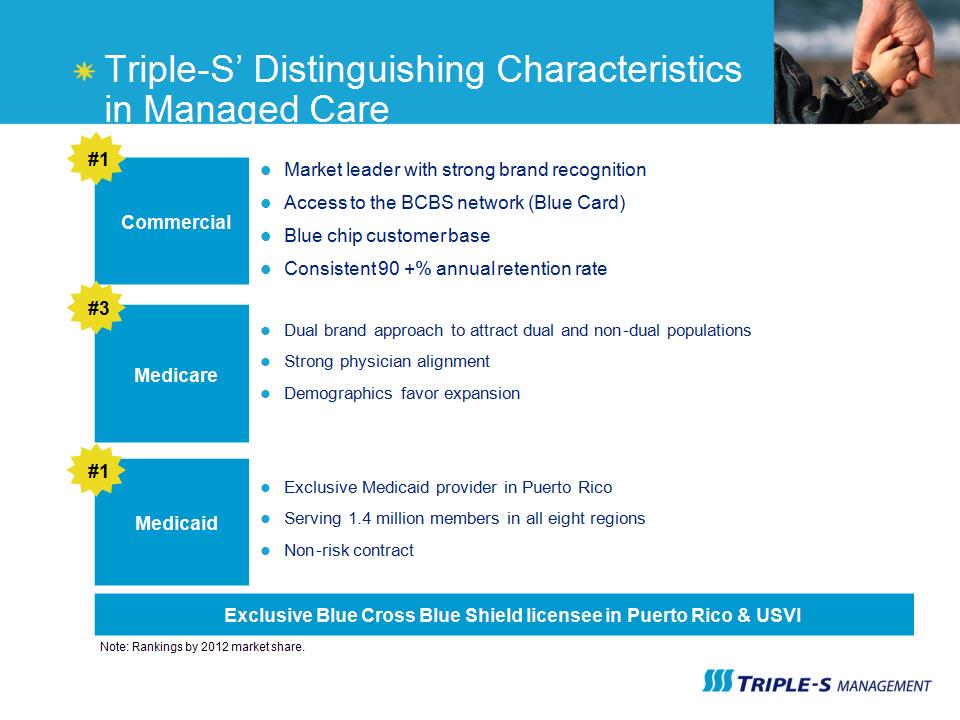

Triple-S’ Distinguishing Characteristics in Managed Care Market leader with strong brand recognition Access to the BCBS network (Blue Card) Blue chip customer base Consistent 90 +% annual retention rate Commercial Exclusive Blue Cross Blue Shield licensee in Puerto Rico & USVI Medicaid Exclusive Medicaid provider in Puerto Rico Serving 1.4 million members in all eight regions Non-risk contract #1 #1 Medicare Dual brand approach to attract dual and non-dual populations Strong physician alignment Demographics favor expansion #3 Note: Rankings by 2012 market share.

17

Our Strategy Commercial: Expand product offering while improving pricing, thereby maintaining a profitable business as ACA rolls out on the island Enhance clinical outcomes and utilization and improve quality of care while reducing hospital admissions Medicare Advantage: Market both Triple-S and AHM brands to the rapidly aging population to grow market share profitably Utilize advanced data analytics to improve patient care Medicaid: Leverage existing infrastructure and streamline the regional office network Work with PR Government to deliver quality care at a lower cost Invest in Health and Life Insurance Businesses in Latin America Partner with BCBS in Latin America Deploy Capital with Double-Digit IRR

��

18

Amilcar Jordán Chief Financial Officer Triple-S Management Financial Update

19

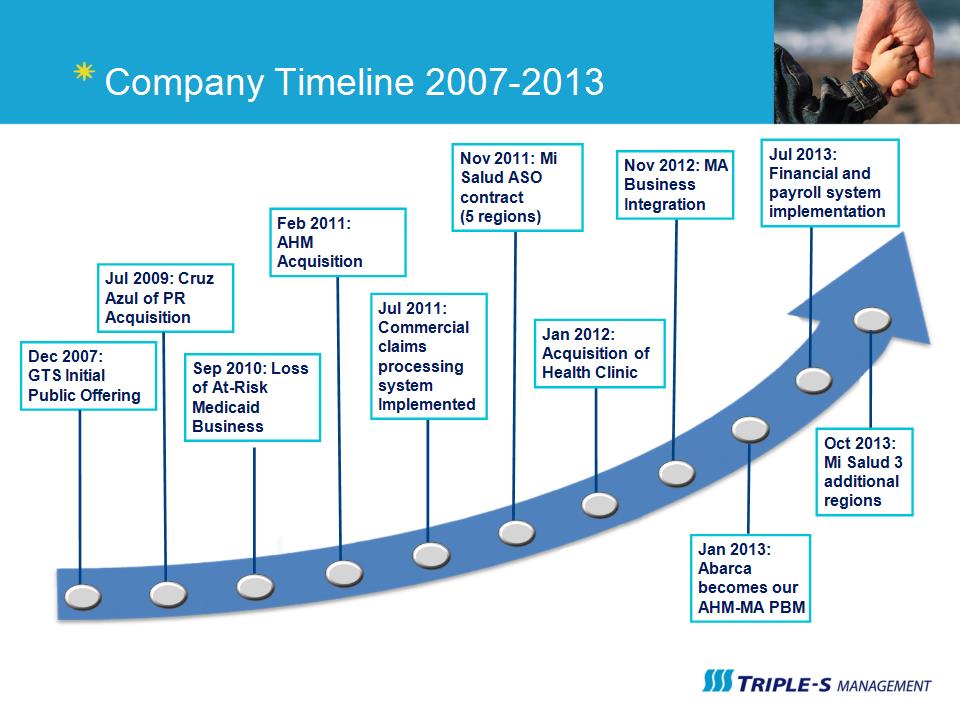

Company Timeline 2007-2013 Dec 2007: GTS Initial Public Offering Jul 2009: Cruz Azul of PR Acquisition Sep 2010: Loss of At-Risk Medicaid Business Feb 2011: AHM Acquisition Jul 2011: Commercial claims processing system Implemented Nov 2011: Mi Salud ASO contract (5 regions) Jan 2012: Acquisition of Health Clinic Nov 2012: MA Business Integration Jan 2013: Abarca becomes our AHM-MA PBM Jul 2013: Financial and payroll system implementation Oct 2013: Mi Salud 3 additional regions

20

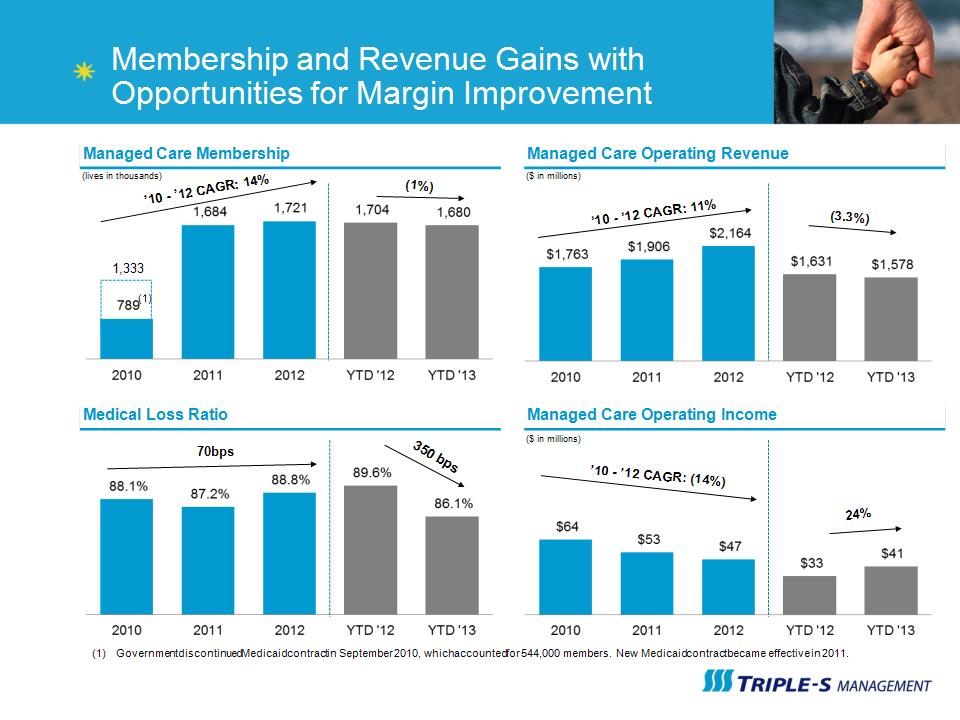

Membership and Revenue Gains with Opportunities for Margin Improvement Managed Care Membership (lives in thousands) ’10 – ’12 CAGR: 14% (1) Managed Care Operating Revenue Medical Loss Ratio ($ in millions) Managed Care Operating Income ($ in millions) 1,333 ’10 – ’12 CAGR: 11% (1) Government discontinued Medicaid contract in September 2010, which accounted for 544,000 members. New Medicaid contract became effective in 2011. (3.3%) 24% (1%) 350 bps 70bps ’10 – ’12 CAGR: (14%)

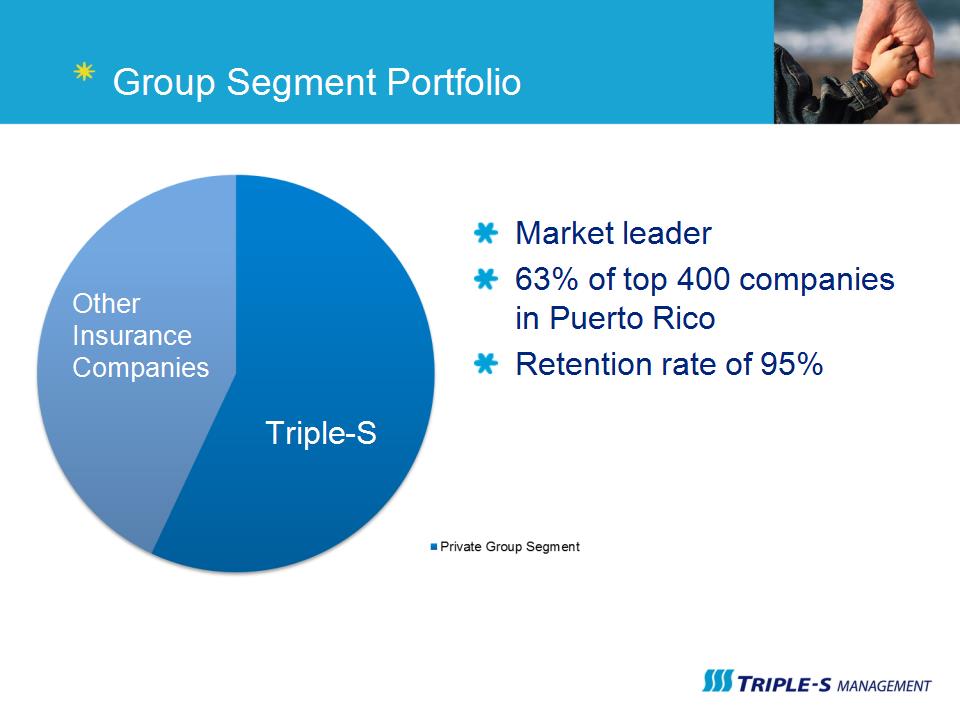

21

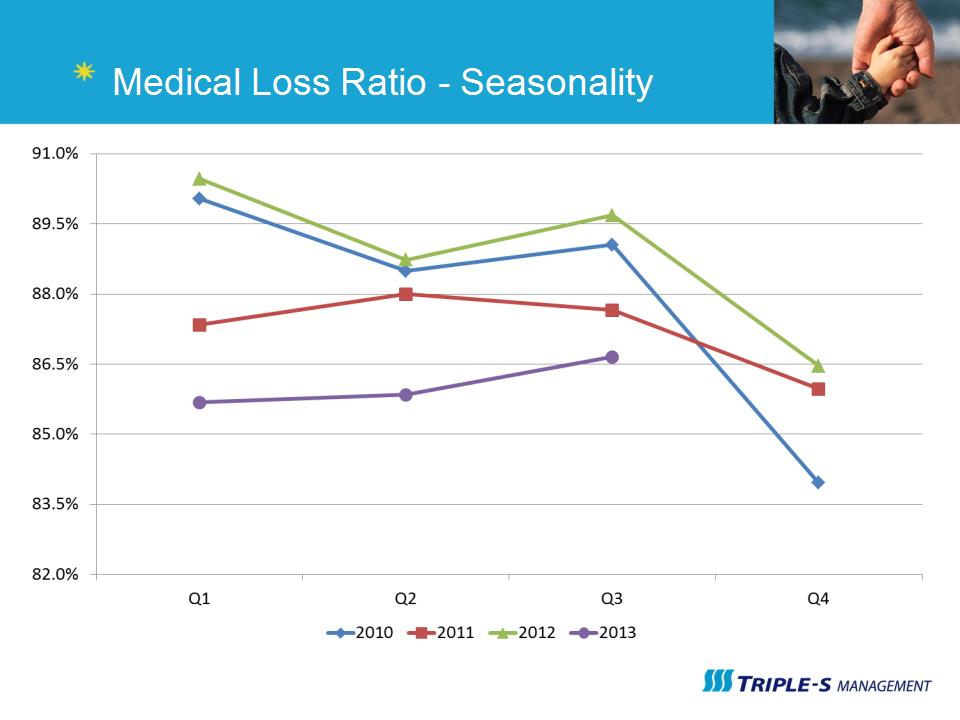

Medical Loss Ratio - Seasonality

22

MLR Initiatives Commercial Implementation of specialty pharmacy network Increase generic fill rate Oncology disease management program Enhancement of discharge planning program Wellness and prevention centers Medicare Alignment of provider compensation arrangements Consolidation of PBMs

23

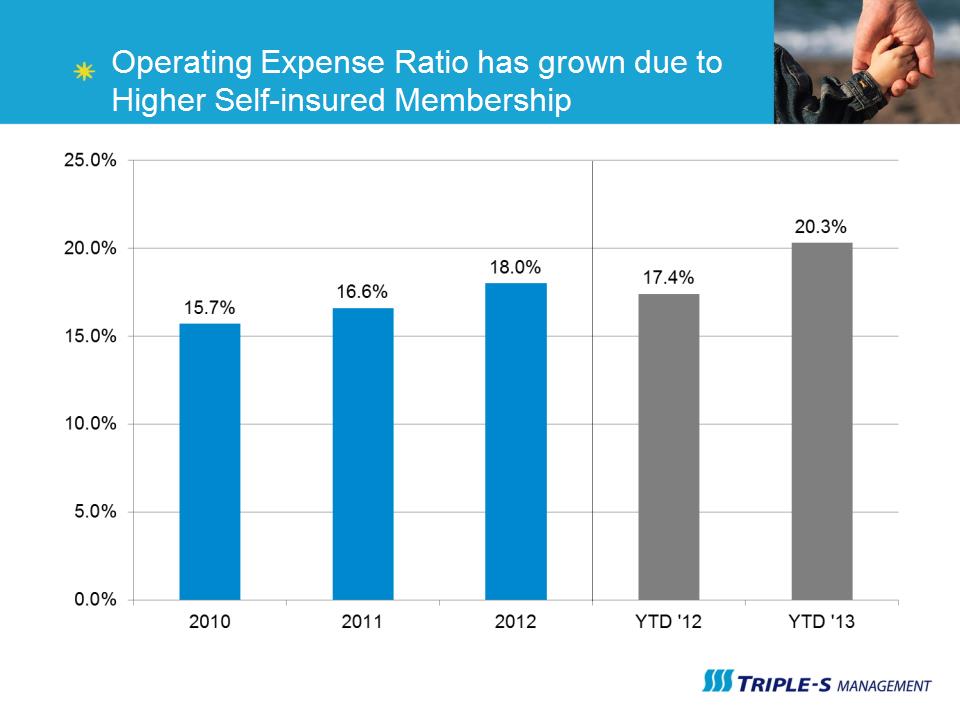

Operating Expense Ratio has grown due to Higher Self-insured Membership

24

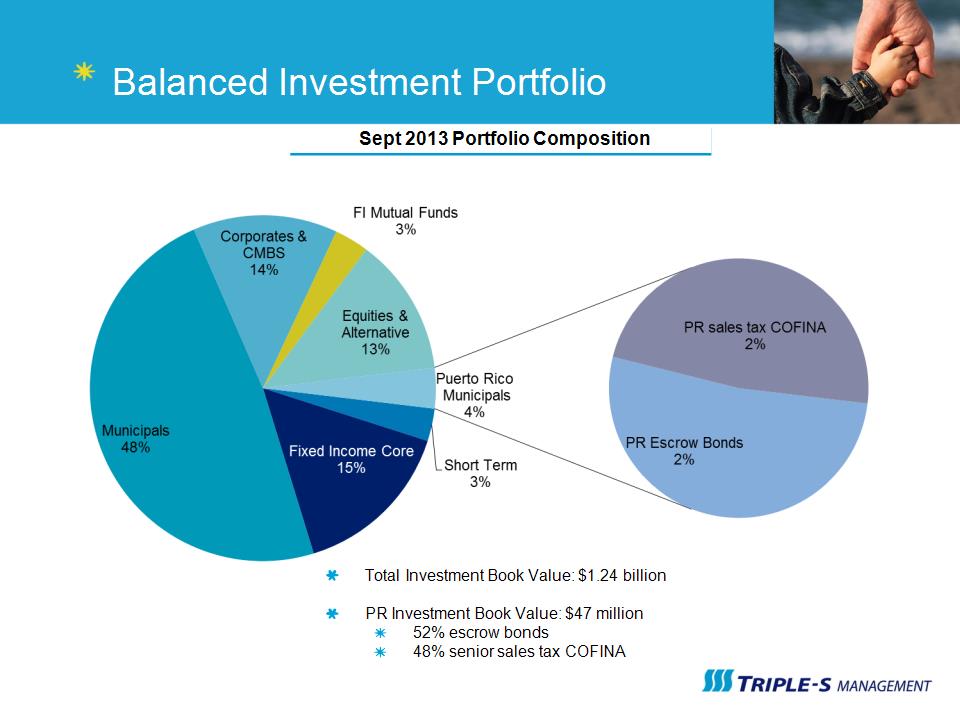

Balanced Investment Portfolio Total Investment Book Value: $1.24 billion PR Investment Book Value: $47 million 52% escrow bonds 48% senior sales tax COFINA Sept 2013 Portfolio Composition

25

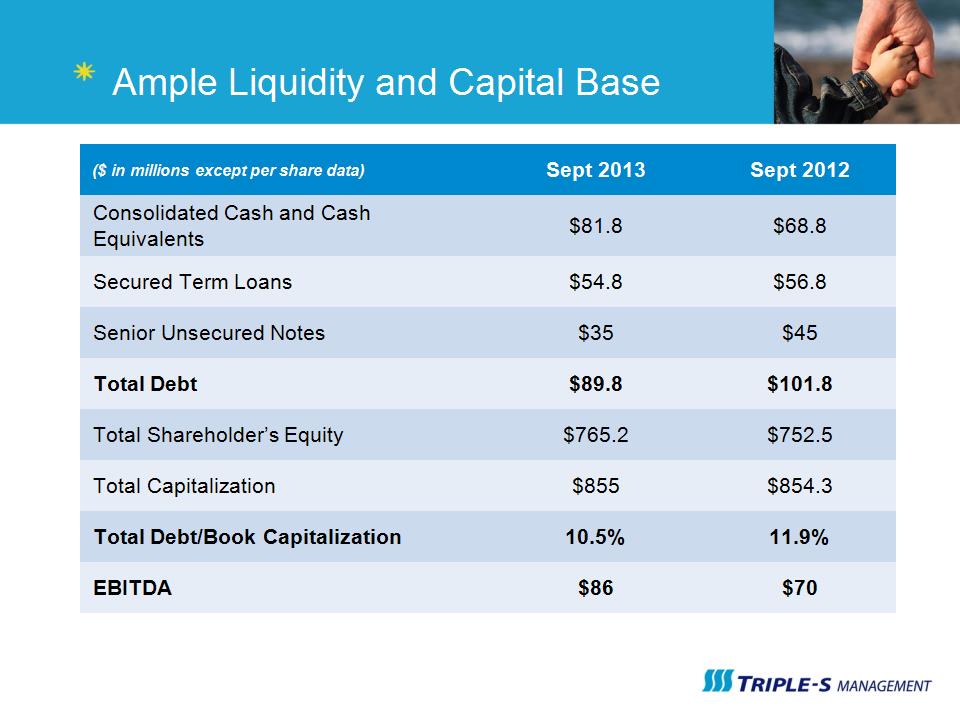

Ample Liquidity and Capital Base ($ in millions except per share data) Sept 2013 Sept 2012 Consolidated Cash and Cash Equivalents $81.8 $68.8 Secured Term Loans $54.8 $56.8 Senior Unsecured Notes $35 $45 Total Debt $89.8 $101.8 Total Shareholder’s Equity $765.2 $752.5 Total Capitalization $855 $854.3 Total Debt/Book Capitalization 10.5% 11.9% EBITDA $86 $70

26

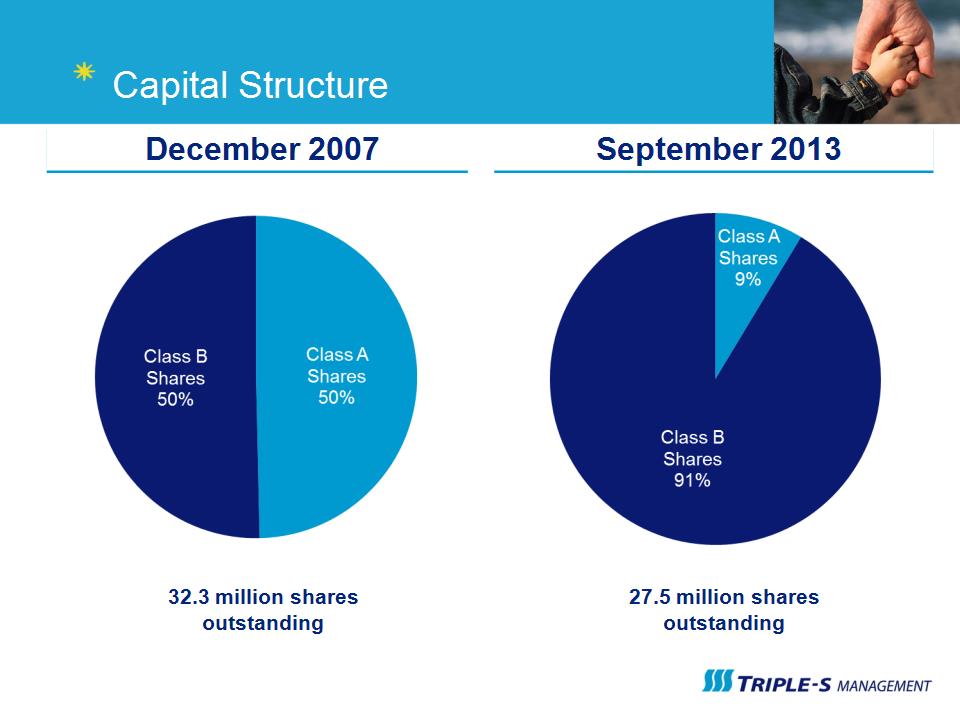

Capital Structure December 2007 September 2013 32.3 million shares outstanding 27.5 million shares outstanding

27

Medicare: Building for the Future Carlos Carrero Chief Executive Officer Socios Mayores en Salud

28

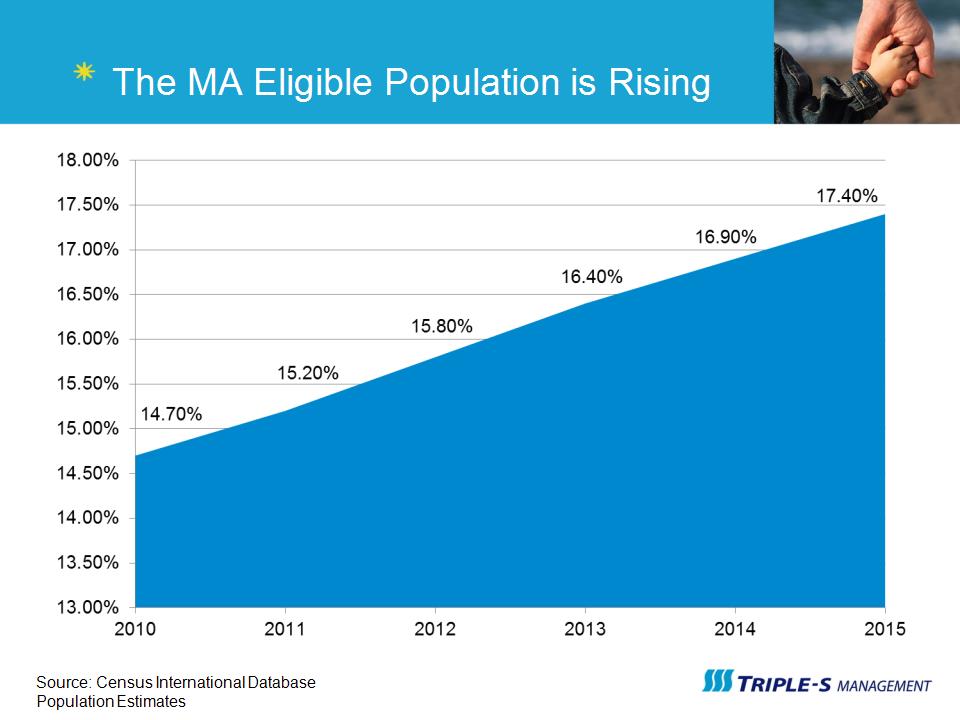

The MA Eligible Population is Rising Source: Census International Database Population Estimates

29

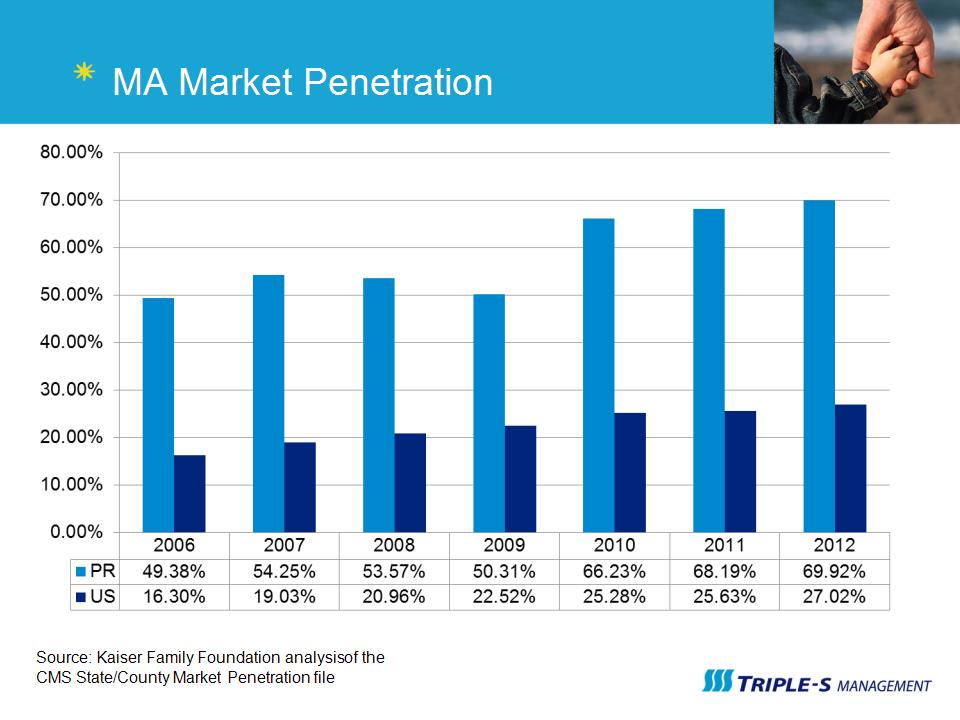

MA Market Penetration Source: Kaiser Family Foundation analysis of the CMS State/County Market Penetration file

30

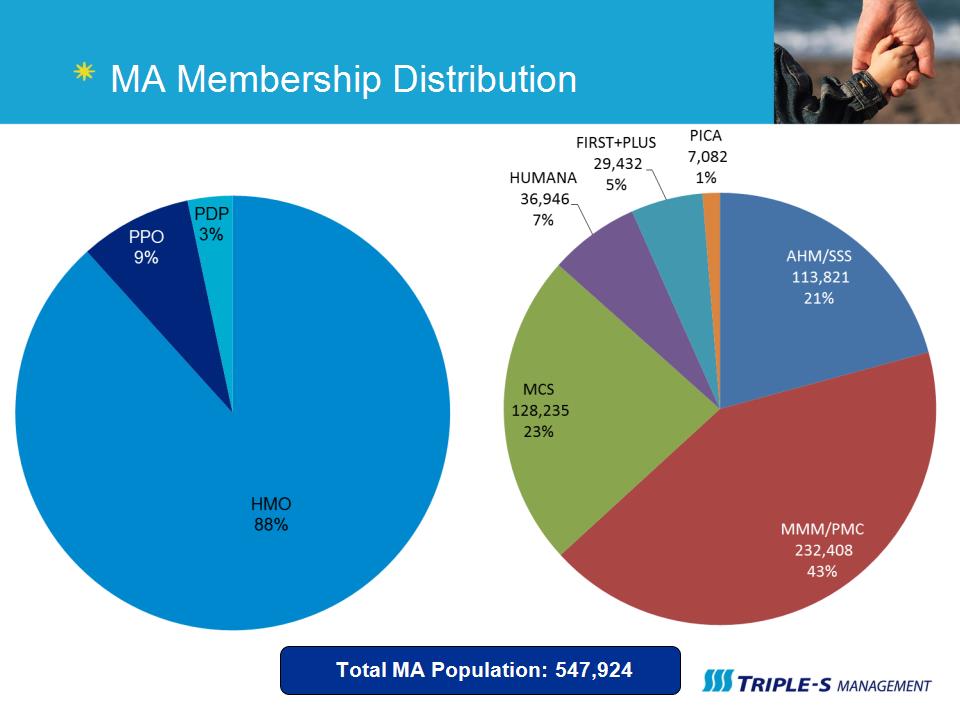

MA Membership Distribution Total MA Population: 547,924

31

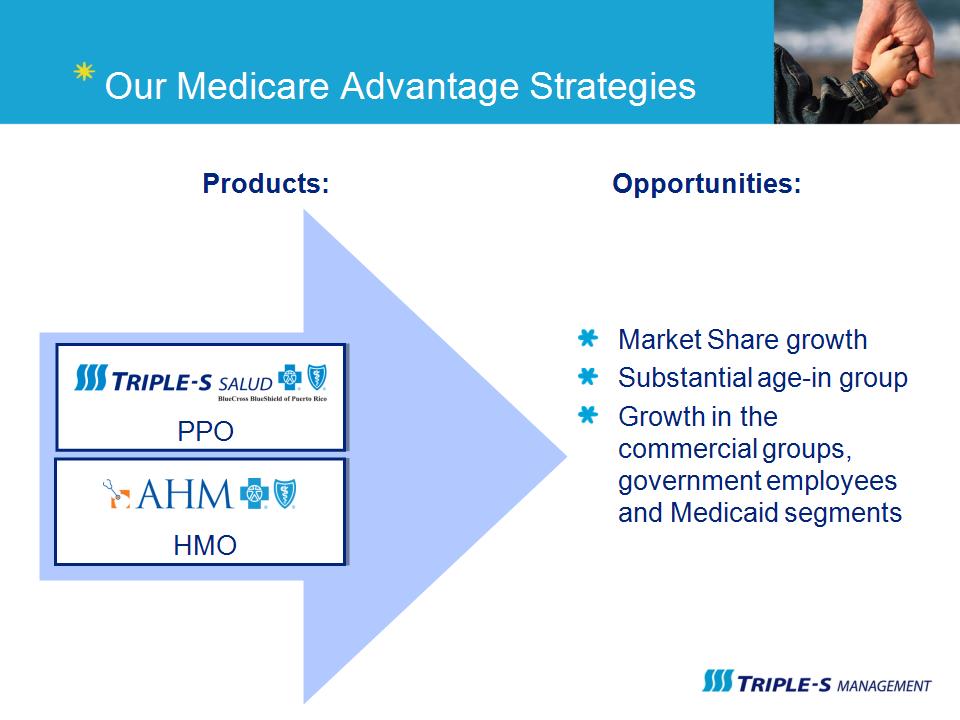

Our Medicare Advantage Strategies Products: Opportunities: Market Share growth Substantial age-in group Growth in the commercial groups, government employees and Medicaid segments PPO HMO

32

Our Medicare Advantage Strategies Main Focus: Efficiency and Cost-Saving Measures Medical Loss Ratio Unique Product Design Quality Initiatives Attrition

33

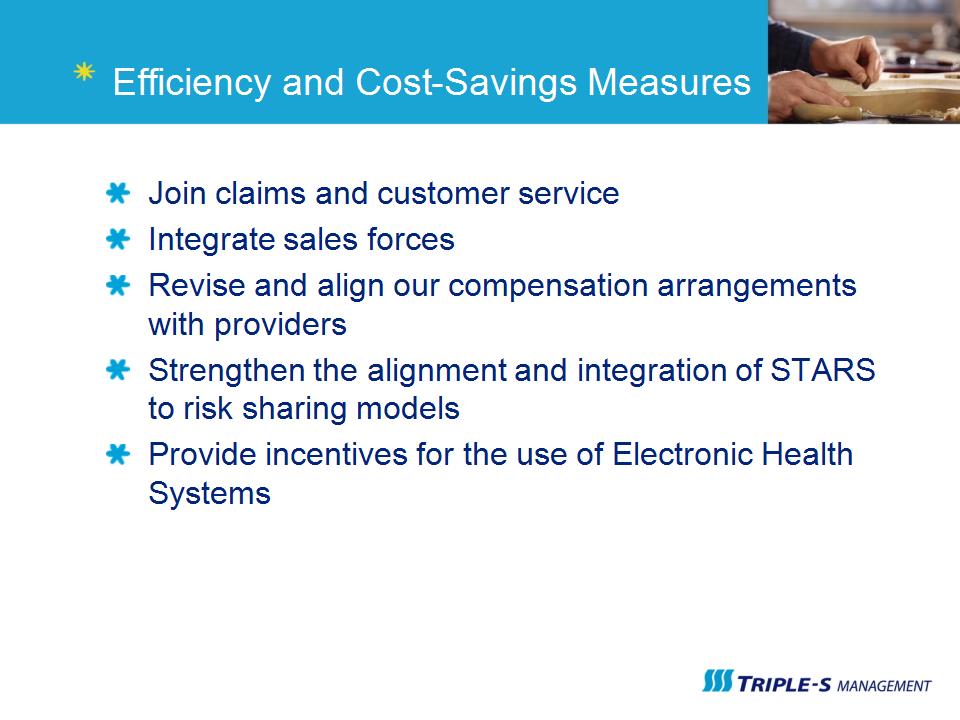

Efficiency and Cost-Savings Measures Join claims and customer service Integrate sales forces Revise and align our compensation arrangements with providers Strengthen the alignment and integration of STARS to risk sharing models Provide incentives for the use of Electronic Health Systems

34

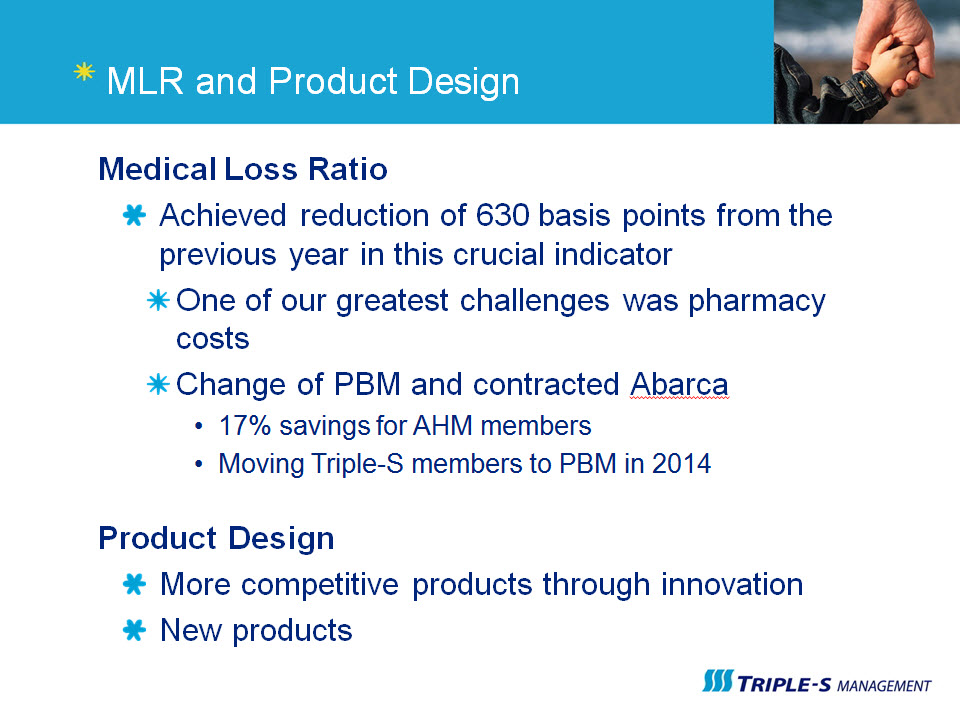

MLR and Product Design Medical Loss Ratio Achieved reduction of 630 basis points from the previous year in this crucial indicator One of our greatest challenges was pharmacy costs Change of PBM and contracted Abarca 17% savings for AHM members Moving Triple-S members to PBM in 2014 Product Design More competitive products through innovation New products

35

Quality Initiatives STARS 82% of our membership is in a plan with an overall 3.0 STAR rating In Puerto Rico, currently no company has an overall STAR score of over 3.0 We aligned our compensation, incentives and risk pools with STARS Contracted with Inovalon

36

A Winning Strategy

37

Managed Care – Commercial and Medicaid Pablo Almodóvar Chief Executive Officer Triple-S Salud

38

Three Main Aspects Medicaid segment Commercial business scenario Affordable Care Act

39

Mi Salud (Medicaid) Segment Transferred 750,000 members in 2011 Contracted approximately 6,500 providers Three regions added Now serving 1.4 million lives Transitioned in October Previous experience of strong performance was determining factor for extension

40

MI Salud (Medicaid) Segment With patients’ support the Mi Salud plan (Medicaid) 62% of people surveyed consider MI Salud (Medicaid) the most successful government initiative Source: Survey by El Nuevo Día

41

Mi Salud (Medicaid) Segment Our strategy: Long-term commitment to social responsibility New initiatives to improve service quality and health outcomes Reduce delivery costs Contracts with Primary Medical Groups (PMGs) Hospital reimbursements Pharmacy benefits strategies

42

Commercial Segment Only health plan that serves all market niches Groups Individual Supplemental Medicare Local and federal government employees Medicaid

43

Group Segment Portfolio Market leader 63% of top 400 companies in Puerto Rico Retention rate of 95% Triple-S Other Insurance Companies

44

Strategies for Commercial Increase local government employee market share Improve our MLR Seek to maintain our 90%+ retention rate Reduce Administrative Expenses Professional services fees Temporary services Administrative efficiencies

45

Federal Employees 95% of federal employees Three consecutive years as one of the top ten plans

46

Affordable Care Act Key difference in territories versus US: Guaranteed issue applies Individual/employer mandate does not apply

47

Affordable Care Act

48

Local Government Decision Local government announced it will expand the MI Salud program Raise the income ceiling so that more people can qualify for the program Provide assistance to lower income individuals who do not qualify for Medicaid so that they can buy coverage through MI Salud Estimates that around 75,000 individuals will qualify to buy coverage through MI Salud

49

Other Initiatives Specialty Pharmacy New Protocols for cancer Provider compensation/incentives tied to compliance

50

The Key for the Future Our structure Our work force Our commitment

51

Quality of Care for Our Members Frank Astor, MD Chief Medical Officer Triple-S Salud

52

Challenges and Opportunities Prevention Holistic/Integrated Address social issues Drive down prevalent conditions

53

Prevalent Conditions in Puerto Rico Diabetes 13% Almost double national average Obese and overweight 70% Hypertension 33% In line with US Hispanics

54

New Approach to Healthcare Solutions Local, grassroots health initiatives Focused on regional, ethnic differences Supportive of emotional, social, environmental issues

55

Improving Healthcare Delivery Efficiency Patient-centered medical models Selective, highly efficient provider networks

56

New Approach to Healthcare Solutions Twelve medical homes Multi-specialty provider groups Cost-efficient quality care targeted to conditions and age

57

New Approach to Healthcare Solutions Premier ambulatory healthcare facility Member Mayo Clinic Care Network Expertise close to home Open to vertical strategies for Triple-S Salud and AHM

58

New Approach to Healthcare Solutions Integrated Wellness and Prevention Centers Eight throughout the Island One-stop shop for preventive services Detailed report to share with primary healthcare provider

59

New Approach to Healthcare Solutions Provider compensation based on outcomes Population management and outcome-based guidelines New compensation model based on compliance with HEDIS measures Incentive structure for contracting hospitals Oncology program

60

New Approach to Healthcare Solutions Innovations for Medicaid (Mi Salud) Incentives for EHR Insulin-Dependent Management Program to improve adherence High-Utilizers Initiative

61

Leveraging Technology The move to ICD-10 Encouraged providers Collaboration with professional associations On-going program of workshops and on-line education

62

Leveraging Technology State of the art clinical platform Upgraded coordinated care management system Better wellness and disease management Integrated browser-based health care tool Hospital data sharing and integration New strategy to address high-intensity/severity conditions

63

Managing Pharmacy Costs Percentage of pharmacy expenditure higher in PR than US mainland PR included in US pricing structure Consolidation of distribution channels results in spiraling cost of generics 9.1% increase during 2012 35% of each premium dollar goes to cover drug costs

64

Managing Pharmacy Costs Specialty Pharmacy Strategy Chronic diseases (immune, genetic, cancer and inflammatory conditions) Monitor adherence, follow-up and interactions Outcome-based incentives

65

Our Goals Better outcomes Quality and cost efficiency Face new challenges in healthcare Partner with providers, members and health organizations

66

Investor Day 2013 December 6, 2013

67