Exhibit 99.1

ALGONQUIN POWER & UTILITIES CORP.

ANNUAL INFORMATION FORM

March 31, 2011

TABLE OF CONTENTS

| | | | | | | | | | |

| | | | | Page | |

| | |

| 1. | | CORPORATE STRUCTURE | | | 1 | |

| | | |

| | 1.1 | | Name, Address and Incorporation | | | 1 | |

| | 1.2 | | Intercorporate Relationships | | | 1 | |

| | | | (a) | | Subsidiaries | | | 1 | |

| | | | (b) | | Other Interests in Energy Related Developments | | | 6 | |

| | |

| 2. | | GENERAL DEVELOPMENT OF THE BUSINESS | | | 7 | |

| | | |

| | 2.1 | | General | | | 7 | |

| | | | (a) | | The Unit Exchange | | | 7 | |

| | | | (b) | | Business Strategy | | | 7 | |

| | 2.2 | | Three Year History | | | 9 | |

| | | | (a) | | Fiscal 2008 | | | 9 | |

| | | | (b) | | Fiscal 2009 | | | 10 | |

| | | | (c) | | Fiscal 2010 | | | 10 | |

| | 2.3 | | Recent Developments | | | 11 | |

| | | | (a) | | Power Generation - New Wind Projects Under Development | | | 11 | |

| | | | (b) | | Power Generation: Development | | | 11 | |

| | | | (c) | | Power Generation | | | 12 | |

| | | | (d) | | Senior Credit Facility | | | 12 | |

| | | | (e) | | Liberty Water | | | 13 | |

| | | | (f) | | Liberty Energy | | | 13 | |

| | 2.4 | | Significant Acquisitions | | | 13 | |

| | | | (a) | | Power Generation | | | 13 | |

| | | | (b) | | Energy Utilities | | | 14 | |

| | |

| 3. | | DESCRIPTION OF THE BUSINESS | | | 15 | |

| | | |

| | 3.1 | | General Description of the Regulatory Regimes in which the Business Operates | | | 15 | |

| | | | (a) | | Power Generation Regulatory Regimes | | | 15 | |

| | | | (b) | | Water Utility Services Regulatory Regimes | | | 17 | |

| | | | (c) | | Electrical Utility Services Regulatory Regimes | | | 17 | |

| | 3.2 | | Production Method, Principal Markets, Distribution Methods and Material Facilities | | | 18 | |

| | | | (a) | | Power Generation: Renewable - Hydroelectric | | | 18 | |

| | | | (b) | | Power Generation: Renewable - Wind Power | | | 23 | |

| | | | (c) | | Power Generation: Thermal - Energy From Waste | | | 26 | |

| | | | (d) | | Power Generation: Thermal - Cogeneration | | | 27 | |

| | | | (e) | | Power Generation: Energy Services Business | | | 31 | |

| | | | (f) | | Power Generation: Development | | | 32 | |

| | | | (g) | | Utilities: Water and Wastewater | | | 36 | |

| | | | (h) | | Utilities: Electrical Distribution | | | 41 | |

| | 3.3 | | Revenues for 2010 and 2009 | | | 43 | |

| | 3.4 | | Specialized Skill and Knowledge | | | 43 | |

| | 3.5 | | Competitive Conditions | | | 44 | |

| | 3.6 | | Environmental Protection | | | 45 | |

| | 3.7 | | Employees | | | 46 | |

| | 3.8 | | Foreign Operations | | | 46 | |

| | 3.9 | | Intangible Properties | | | 46 | |

| | 3.10 | | Cycles and Seasonality | | | 47 | |

| | | | (a) | | Power Generation - Hydrology | | | 47 | |

| | | | (b) | | Power Generation - Wind | | | 47 | |

- i -

| | | | | | | | | | |

| | | | (c) | | Water Utilities | | | 47 | |

| | | | (d) | | Electric Utilities | | | 47 | |

| | 3.11 | | Customers | | | 48 | |

| | 3.12 | | Economic Dependence | | | 48 | |

| | 3.13 | | Social or Environmental Policies | | | 48 | |

| | |

4. | | RISK FACTORS | | | 48 | |

| | | |

| | 4.1 | | Treasury Risk Management | | | 48 | |

| | | | (a) | | Foreign currency risk | | | 49 | |

| | | | (b) | | Market price risk | | | 49 | |

| | | | (c) | | Credit/Counterparty risk | | | 49 | |

| | | | (d) | | Interest rate risk | | | 50 | |

| | | | (e) | | Liquidity risk | | | 51 | |

| | | | (f) | | Commodity price risk | | | 52 | |

| | | | (g) | | Risk of Default under Senior Credit Facility | | | 53 | |

| | 4.2 | | Operational Risk Management | | | 53 | |

| | | | (a) | | Mechanical and Operational Risks | | | 53 | |

| | | | (b) | | Asset Retirement Obligations | | | 54 | |

| | | | (c) | | Environmental Risks | | | 55 | |

| | | | (d) | | Litigation risks and other contingencies | | | 59 | |

| | | | (e) | | Tax Related Risks | | | 60 | |

| | | | (f) | | Tax risks Associated with the Unit Exchange | | | 60 | |

| | | | (g) | | Obligations to Serve | | | 60 | |

| | 4.3 | | Regulatory Climate and Permitting Risks | | | 60 | |

| | | | (a) | | Power Generation | | | 60 | |

| | | | (b) | | Water Utilities | | | 61 | |

| | | | (c) | | Electrical Utilities | | | 61 | |

| | 4.4 | | Dependence upon APUC Businesses | | | 61 | |

| | | | (a) | | Power Generation | | | 61 | |

| | | | (b) | | Water Utilities | | | 62 | |

| | | | (c) | | Electrical Utilities | | | 62 | |

| | 4.5 | | Safety Considerations | | | 62 | |

| | 4.6 | | Labour Relations | | | 62 | |

| | | | (a) | | Power Generation | | | 62 | |

| | | | (b) | | Liberty Water | | | 63 | |

| | | | (c) | | Liberty Energy | | | 63 | |

| | 4.7 | | Dependence Upon Key Customers | | | 63 | |

| | 4.8 | | Potential Conflicts of Interest | | | 63 | |

| | 4.9 | | Construction / Development Risk | | | 63 | |

| | 4.10 | | Acquisitions and Divestitures | | | 63 | |

| | |

5. | | DIVIDENDS/DISTRIBUTIONS | | | 63 | |

| | |

6. | | DESCRIPTION OF CAPITAL STRUCTURE | | | 64 | |

| | | |

| | 6.1 | | Common Shares | | | 64 | |

| | 6.2 | | Preferred Shares | | | 64 | |

| | 6.3 | | Convertible Debentures | | | 64 | |

| | | | (a) | | Series 1A Debentures | | | 65 | |

| | | | (b) | | Series 2A Debentures | | | 65 | |

| | | | (c) | | Series 3 Debentures | | | 65 | |

| | 6.4 | | Shareholders’ Rights Plan | | | 71 | |

- ii -

| | | | | | | | | | |

| | |

| 7. | | MARKET FOR SECURITIES | | | 71 | |

| | | |

| | 7.1 | | Trading Price and Volume | | | 71 | |

| | | | (a) | | Common Shares | | | 71 | |

| | | | (b) | | Series 1A Debentures | | | 72 | |

| | | | (c) | | Series 2A Debentures | | | 72 | |

| | | | (d) | | Series 3 Debentures | | | 73 | |

| | 7.2 | | Prior Sales | | | 73 | |

| | |

| 8. | | DIRECTORS AND OFFICERS | | | 73 | |

| | | |

| | 8.1 | | Name, Occupation and Security Holdings | | | 73 | |

| | 8.2 | | Audit Committee | | | 76 | |

| | | | (a) | | Audit Committee Charter | | | 76 | |

| | | | (b) | | Relevant Education and Experience | | | 76 | |

| | | | (c) | | Pre-Approval Policies and Procedures | | | 77 | |

| | 8.3 | | Corporate Governance and Compensation Committees | | | 77 | |

| | 8.4 | | Bankruptcies | | | 77 | |

| | 8.5 | | Potential Material Conflicts of Interest | | | 78 | |

| | |

| 9. | | LEGAL PROCEEDINGS AND REGULATORY ACTIONS | | | 78 | |

| | | |

| | 9.1 | | Legal Proceedings | | | 78 | |

| | | | (a) | | Trafalgar | | | 78 | |

| | | | (b) | | Côte Ste-Catherine Water Lease Dues | | | 78 | |

| | 9.2 | | Regulatory Actions | | | 79 | |

| | |

| 10. | | INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | | | 79 | |

| | |

| 11. | | TRANSFER AGENTS AND REGISTRARS | | | 79 | |

| | |

| 12. | | MATERIAL CONTRACTS | | | 79 | |

| | |

| 13. | | INTERESTS OF EXPERTS | | | 81 | |

| | |

| 14. | | ADDITIONAL INFORMATION | | | 81 | |

| | |

| | SCHEDULE A | | | A1 | |

| | SCHEDULE B | | | B1 | |

| | SCHEDULE C | | | C1 | |

| | SCHEDULE D | | | D1 | |

| | SCHEDULE E | | | E1 | |

| | SCHEDULE F | | | F1 | |

All information contained in this Annual Information Form (“AIF”) is presented as at March 31, 2011, unless otherwise specified. In this AIF, all dollar figures are in Canadian dollars, unless otherwise indicated.

- iii -

| 1.1 | Name, Address and Incorporation |

Algonquin Power & Utilities Corp. (“APUC” or the “Corporation”) was originally incorporated under theCanada Business Corporations Act (“CBCA”) on August 1, 1988 as Traduction Militech Translation Inc. Pursuant to articles of amendment dated August 20, 1990 and January 24, 2007, the corporation amended its articles to change its name to Societe Hydrogenique Incorporée – Hydrogenics Corporation and Hydrogenics Corporation – Corporation Hydrogenique, respectively. Pursuant to a certificate and articles of arrangement dated October 27, 2009, the corporation, among other things, created a new class of common shares (the “Common Shares”) and changed its name to Algonquin Power & Utilities Corp. The head and principal office of APUC is located at 2845 Bristol Circle, Oakville, Ontario, L6H 7H7.

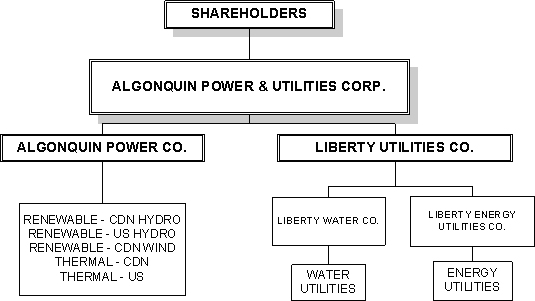

APUC is continuing the business of Algonquin Power Income Fund (“Algonquin” or the “Fund”). APUC’s principal holdings are its trust units (“Trust Units”) of Algonquin Power Co. (“APCo”), shares of Liberty Water Co. (“Liberty Water”) and shares of Liberty Energy Utilities Co. (“Liberty Energy”).

Unless the context indicates otherwise, references in this AIF to “APUC” include, for reporting purposes only, the direct or indirect subsidiaries of APUC and partnership interests held by APUC and its subsidiaries. Such use of “APUC” to refer to these other legal entities and partnership interests does not constitute a waiver by APUC or such entities or partnerships of their separate legal status, for any purpose.

| 1.2 | Intercorporate Relationships |

The subsidiaries of APUC are grouped into the independent power generation and the utilities businesses. The principle holding for APUC’s independent power generation business is an investment in 100% of the issued and outstanding Trust Units of APCo. The principle holding for APUC’s utilities business is an investment in 100% of the issued and outstanding common shares of Liberty Utilities (Canada) Corp., a federal corporation, which in turn owns all of the issued and outstanding common shares of Liberty Utilities, a Delaware corporation, which in turn owns both Liberty Water and Liberty Energy. Each of APCo, Liberty Water and Liberty Energy have their own subsidiaries and ownership chains.

The subsidiaries of APCo include the ownership chains of Algonquin Power Trust (“APT”), Algonquin Power Operating Trust (“APOT”), Algonquin Power Fund (Canada) Inc. (“APFC”) and Algonquin Power Fund (America) Inc. (“APFA”). The Liberty Energy chain is currently structured to hold the electric utility assets located in California and acquired January 1, 2011, and the Liberty Water chain is structured to hold the water and wastewater assets located in the United States. These major chains are defined and shown in the chart below, and a detailed description of the legal entities that comprise these chains and the Facilities they own is then provided. Additional information on the Facilities is described in Schedules A, B, C and D.

APCo is the sole beneficiary of APT, which owns all the Trust Units of APOT. APT is an unincorporated open ended trust created by a declaration of trust dated June 30, 2000 in accordance with the laws of the Province of Ontario. APT controls the entities that own some of the Canadian hydroelectric facilities, and the energy-from-waste facility (the “EFW Facility”) located in the Regional Municipality of Peel, Ontario (“Peel”). APOT is an unincorporated open ended trust created by an amended and restated trust indenture effective January 2, 1997, in accordance with the laws of the Province of Alberta. APOT controls the entities that own the Canadian cogeneration facility located at Brampton, Ontario (the “BCI Facility”), the wind facility located at St. Leon, Manitoba (the “St. Leon Facility”), one hydroelectric facility in Alberta (the “Dickson Dam Facility”) and APCo’s 50% interest in the Alberta biomass facility (the “Valley Power Facility”). APCo also owns Algonquin Holdco Inc., an Ontario corporation, which owns APFC. APFC was incorporated in Nova Scotia and it controls the entities that own the majority of the hydroelectric facilities in Canada. APFC also owns APFA, a Delaware corporation, which is the top APCo entity in the United States. APFA owns and controls the U.S. hydroelectric entities, and also controls the entities that own the U.S. thermal cogeneration facilities known as the Sanger Facility and the Windsor Locks. Facility

APT forms part of the APCo business unit and indirectly owns the EFW Facility in the city of Brampton located in Peel by virtue of owning all the Trust Units in KMS Power Income Fund, an unincorporated open ended trust created by a declaration of trust dated February 18, 1997 in accordance with the laws of the Province of Alberta. This trust owns Algonquin Power Energy From Waste Inc. (“APEFW”), an Ontario corporation that owns the EFW Facility.

APT also holds interests in certain of APCo’s Canadian hydroelectric Facilities. It directly owns the hydroelectric Hydraska Facility and the Arthurville Facility , and owns both the general partnership and the limited partnership interests in Algonquin Power (Campbellford) Limited Partnership

2

(“Campbellford LP”), an Ontario limited partnership which operates a 4 megawatt (“MW”) hydroelectric generation station on the Trent River near Campbellford, Ontario (the “Campbellford Facility”). It also holds a 42% limited partnership interest in the Algonquin Power (Mont-Laurier) Limited Partnership (the “Mont-Laurier Partnership”), a Québec limited partnership, which owns the Mont-Laurier and the Côte Ste.-Catherine Facilities. APEFW owns the remaining 58% partnership interests, comprised of a 46.5% limited partnership interest and an 11.5% general partnership interest.

APT owns Corporation D’Investissements Éoliennes Algonquin Power (“Éoliennes”), a Canadian corporation. Éoliennes indirectly owns St. Ulric Wind Energy Investments L.P. (“St. Ulrich LP”), a Québec limited partnership, through its ownership of the limited partnership of St. Ulrich LP, (Société en Commandite Algonquin (Éoliennes), a Québec limited partnership, and its direct ownership of the general partner of St. Ulrich LP, named Corporation D’Investissements Éolienes St-Laurent Inc. (“Corporation St-Laurent”), a Québec corporation. Corporation St-Laurent Inc. is the 50% owner of Saint-Damase Wind Energy Fleur de Lis General Partner Corporation, a federal corporation, which is the general partner of the partnership known as Saint-Damase Wind Energy Fleur de Lis Limited Partnership (“Fleur de Lis LP”). Fleur de Lis LP has an interest in the Saint - Damase wind energy project and described below in “Power Generation - New Wind Projects Under Development”. St. Ulrich LP owns a 49.995% equity interest in the Fleur de Lis LP, the general partner owns a .02% equity interest, and a non-Algonquin, Saint-Damase party owns the remaining 49.995% equity interest. APT also has an interest in Société Éoliennes Belle- Rivière, société en commandite (“Belle Rivière”), a Quebec partnership and the owner of the Val- Éo wind energy project, also described below in “Power Generation - New Wind Projects Under Development”. It owns a 25% equity interest in the general partner, 9231-5498 Québec Inc. and it also holds a 24.9975% limited partner interest.

The APOT entities that own the BCI Facility are Brampton Cogeneration Limited Partnership, an Ontario partnership, the partners of which are Brampton Cogeneration Inc. (“BCI”), which is the general partner and holds one general partnership unit, and APOT, which owns 100% of the Class A Units (entitled to vote on all matters) and 50% of the Class B Units (vote on only specific matters) in the limited partnership. BCI is an Ontario corporation and is owned by APOT.

The APOT entity that owns the St. Leon Facility is St. Leon Wind Energy LP, an Ontario partnership (“St. Leon LP”). It is owned 26.43% by the general partner, St. Leon Wind Energy GP Inc. (“St. Leon GP”), 73.16% by St. Leon Wind Energy Trust, a Manitoba trust (“St. Leon Trust”) and 0.42% by AirSource Power Fund I LP, a Manitoba limited partnership (“AirSource”). St. Leon LP has issued 100 Class B limited partnership units. Two executives of APUC, Ian Robertson and Christopher Jarratt (the “Senior Officers”) indirectly each own 18 of the 100 Class B units. St. Leon Trust is owned 100% by AirSource, the limited partner of which is Algonquin (AirSource) Power LP (“AAP LP”) which holds a 99.99% interest in the limited partnership, and which in turn is owned 99.99% by APOT as limited partner. AirSource is also the 100% owner of St. Leon GP. St. Leon GP is a Canadian corporation and St. Leon Trust is a trust created by a declaration of trust dated June 28, 2005 in accordance with the laws of the Province of Manitoba. The AirSource and AAP LP limited partnerships were formed in Manitoba and Ontario, respectively. APOT is also the sole limited partner in St. Leon II Wind Energy LP, a Manitoba partnership, the general partner of which is St. Leon II Wind Energy GP Inc. which is also owned by APOT.

APOT also owns Loyalist Wind Project GP Inc., an Ontario corporation, which is the general partner of Loyalist Wind Project LP (“Loyalist LP”), an Ontario limited partnership. APUC is the majority limited partner of Loyalist LP, holding a 87.49125% interest. The remaining limited partner of Loyalist LP is an unrelated third party, holding a 12.49875% interest.

3

APOT has two ownership interests in Alberta. First, it is the beneficial owner of the Dickson Dam Facility. Second, it owns 50% of Valley Power Corp., an Ontario corporation, which holds a 0.0001% limited partnership interest partner in Valley Power LP, an Alberta limited partnership which owns the Valley Power Facility. APOT directly holds a further 49.9995% limited partnership interest in Valley Power LP.

In Ontario, APFC directly owns the Burgess and Hurdman Facilities, and has an agreement in place to buy ownership interests in the parties to the joint venture that owns the interests in the Long Sault Rapids Facility. In Québec, APFC directly owns the facilities known as Rawdon, Hydro Snemo, St. Raphael, Belleterre and St. Brigette Facilities. APFC also holds a direct interest in Société Hydro-Donnacona, S.E.N.C. (the “S.E.N.C.”), the owner of the Donnacona Facility. The S.E.N.C. is a Québec general partnership, and is owned as to 99.99% by APFC and 0.01% by Donnacona Holdings Inc., an Ontario corporation 100% owned by APFC. In Newfoundland, APFC holds a 45% partnership interest in the Algonquin Power (Rattle Brook) Partnership, a Newfoundland partnership that owns the Rattlebrook Facility. APFC also 100% owns Algonquin Power Services Canada Inc., a Canadian corporation that provides purchasing services to Canadian APCo entities.

APFA owns Algonquin Power Sanger LLC (“Sanger LLC”), a California limited liability company, and Algonquin Power Windsor Locks LLC, a Connecticut limited liability company. These entities own the U.S. cogeneration Sanger and Windsor Locks Facilities. Sanger LLC directly owns 100% of Dyna Fibers Inc., a California corporation that operates a hydro-mulch business at the Sanger Facility site. APFA also owns KMS Crossroads, LLC, a Delaware limited liability corporation.

APFA indirectly owns numerous hydroelectric facilities through majority interests ranging from 99.7 to 99.99% in the subsidiaries described in this paragraph, with Algonquin Power Fund (America) Holdco Inc. (“Algonquin Holdco”), a Delaware corporation owned by APFA, holding the remaining interests. The New York general partnerships Burt Dam Power Company and Hollow Dam Power Company own the Burt Dam and Hollow Dam Facilities, respectively. The Vermont partnership Moretown Hydro Energy Company owns the Moretown Facility. The New Hampshire limited partnerships Gregg Falls Hydroelectric Associates Limited Partnership, Pembroke Hydro Associates Limited Partnership and Mine Falls Hydroelectric Limited Partnership own the Gregg Falls, Pembroke and Mine Falls Facilities, respectively.

APFA owns the New Hampshire limited liability company Clement Dam Hydroelectric, LLC which owns the Clement Dam Facility. The Franklin, Beaver Falls, Lakeport and Milton Facilities are owned by, respectively, Franklin Power, LLC, a New Hampshire company, Algonquin Power (Beaver Falls) LLC, a Delaware corporation, Lakeport Hydroelectric Corp., a New Hampshire corporation, and SFR Hydro Corporation, a New Hampshire company. The Otter Creek and Kings Falls Facilities are owned by Tug Hill Energy, Inc. a New York corporation, which is owned by Court Street Investments, Inc. (“Court Street”), a Massachusetts corporation, which in turn is owned 100% by APFA. Court Street also owns CSI Oswego Corp., a Delaware corporation, which is a partner in Oswego Hydro Partners L.P., the Delaware partnership that owns the Phoenix Facility. The other partner in this partnership is Oswego Energy Corp., a Delaware corporation, which is 100% owned by Oswego Power Company, Inc., a Massachusetts corporation, which in turn is 100% owned by APFA. The remaining hydroelectric facilities in the United States are the Great Falls and Lochmere Facilities. The Great Falls Facility is owned by the Great Falls Hydroelectric Company Limited Partnership, a Maryland limited partnership in which APFA holds a 98% limited partner interest. Great Falls Energy, LLC holds the remaining 2%

4

general partner interest. Great Falls Energy, LLC is a Maryland limited liability company wholly owned by APFA. The Lochmere Facility is owned by the Indiana general partnership HDI Associates I, which is held 1% by Algonquin Holdco and 99% by APFA.

APFA, in January 2010, 100% acquired two entities, now known as Algonquin Tinker Gen Co. (“Tinker Gen Co.”) and Algonquin Northern Maine Gen Co. (“Northern Maine Gen Co.”), both Wisconsin companies. Tinker Gen Co. is also registered in New Brunswick, and Northern Maine Gen Co. is also registered in Maine. Tinker Gen Co. leases the 36.8MW of electrical generating assets in New Brunswick (the “Tinker Assets”) from APT, and Northern Maine Gen Co. is the owner of the Caribou, Squa Pan and Flos Inn hydro, diesel and steam Facilities. APFA also 100% owns Algonquin Energy Services Inc., a Delaware corporation (“AES”) that is also registered in Connecticut, District of Columbia, Maine, Maryland, New Brunswick and Ohio. AES’s business primarily involves providing the electrical energy requirements for commercial and industrial customers in northern Maine. On February 4, 2010, AES acquired a number of load supply and energy procurement contracts in northern Maine and the Independent System Operator New England (“ISO-NE”) market (the “Energy Services Business”). See “Significant Acquisitions” in “General Development of the Business”and “Energy Services Business” in “Description of the Business”.

In addition, APFA owns 100% of Algonquin Power Acquisition Inc., a Delaware corporation that was incorporated as an acquisition vehicle for proposed acquisitions by APCo in the United States. It currently has no assets. APFC also 100% owns Algonquin Power Services America LLC, a Delaware corporation that provides purchasing services to U.S. APCo entities.

On December 22, 2010, APCo completed a corporate reorganization involving Liberty Water wherein 100% of the issued and outstanding common shares of Liberty Water were transferred to APUC at their estimated fair market value which approximated the book value of the shares. Liberty Water was originally formed under the laws of the state of Delaware as Algonquin Water Resources of America, Inc. The name was changed on April 28, 2009 to Liberty Water Co. Liberty Water Co. forms the top of the Liberty Water Group and indirectly owns the water and wastewater businesses located in Arizona, Texas, Missouri and Illinois, in each case through a 100% wholly-owned subsidiary, with the exception of the Entrada Del Oro Sewer Company, Inc. (“Entrada”) in which it currently operates and holds a beneficial interest in the shares of the company pending regulatory approval of its acquisition by Liberty Water. All of these 100% wholly-owned subsidiaries (except Northwest Sewer, Inc.) are currently conducting business as “Liberty Water”; however the actual legal names of the relevant entities are set out below.

In Arizona, the following Arizona corporations own the following facilities: Bella Vista Water Co., Inc. owns the Bella Vista Facility; Black Mountain Sewer Corporation owns the Black Mountain Facility; Gold Canyon Sewer Company owns the Gold Canyon Facility; Litchfield Park Service Company owns the Litchfield Facility; Northern Sunrise Water Company, Inc. owns the Northern Sunrise Facility; Rio Rico Utilities, Inc. owns the Rio Rico Facility; and Southern Sunrise Water Company, Inc. owns the Southern Sunrise Facility. Northwest Sewer, Inc., an Arizona corporation, has undertaken to a group of developers and homeowner’s associations located to the west of Phoenix to apply for a Certificate of Convenience and Necessity and, if successful, operate a wastewater treatment utility in those areas. Entrada, discussed above, is an Arizona corporation, and it owns the beneficial interest in the Entrada Del Oro Facility. In Texas, the following Texas corporations own the following facilities: Tall Timbers Utility Company, Inc. owns the Tall Timbers Facility; Woodmark Utilities, Inc. owns the Woodmark Facility; and Algonquin Water Resources of Texas, LLC, a Texas limited liability company, owns water and water treatment assets at the resorts of Galveston, Holly Lake Ranch, Hill County, Piney Shores and The Villages (also known as “Big Eddy”). In Missouri, Algonquin Water Resources of Missouri, LLC, a

5

Missouri limited liability company, owns assets associated with the Holiday Hills, Ozark Mountain and Timber Creek resorts. In Illinois, Algonquin Water Resources of Illinois, LLC, an Illinois limited liability company, owns assets for the Fox River resort. All water and wastewater utilities are operated under the Liberty Water brand.

In addition, Algonquin Water Services LLC (“Water Services”) is a company established to manage and operate water distribution and wastewater treatment facilities in Arizona and Texas. It is an Arizona limited liability company owned 99% by New Spring Acquisition Partnership, an Ontario partnership, which in turn is owned 50% by APCo. Algonquin Environmental Services LLC, a Delaware limited liability company owned 100% by Liberty Water, was also established to service various entities.

| | (vii) | Liberty Energy Group |

Liberty Energy is a Delaware corporation. It owns 50.001% of California Pacific Utilities Ventures, LLC, a California limited liability company (“CPUV”), which in turn owns California Pacific Electric Company, LLC, a California limited liability company (“Calpeco”). Effective January 1, 2011, Calpeco acquired the California-based electricity distribution and related generation assets of NV Energy, Inc. (“NV Energy”). See “Significant Acquisitions”. Liberty Energy also owns Liberty Energy Utilities (New Hampshire) Corp. (“Liberty Energy NH”), a Delaware corporation registered in New Hampshire. Liberty Energy NH is the named purchaser of the shares of Granite State Electric Company (“Granite State”) and EnergyNorth Natural Gas Inc. (“EnergyNorth”) currently owned by for the assets of National Grid USA (“National Grid”).

Outside of the APCo, Liberty Water and Liberty Energy chains described above, APUC beneficially owns, directly or indirectly 100% of the following: 3793257 Canada Inc. (“3793257”), a corporation incorporated under the CBCA; and Windlectric Inc. (“Windlectric”), a federal corporation that is developing the Amherst Island wind project, described below in “Power Generation - New Wind Projects Under Development”.

| (b) | Other Interests in Energy Related Developments |

The Corporation also has notes receivable and equity in companies owning generating facilities as described below. APT owns 25% of the Class B non-voting shares issued by Cochrane Power Corporation, the owner of a combined cycle cogeneration facility located in Cochrane, Ontario. APT also owns 32.4% of the Class B non-voting shares in Kirkland Lake Power Corporation, an entity which burns natural gas and wood waste to generate electricity. APT also owns a 12.1% interest in Tranche A and Tranche B term loan interests issued by Chapais Energie, Société en Commandité (“Chapais”) which owns a wood waste facility in Chapais, Québec. It also owns a 33.9% interest in the Class B non-voting preferred shares of Chapais. The loans bear interest at the rate of 10.789% and 4.91%, respectively.

In addition, APUC is entitled to a royalty in the form of cash flows generated by the Long Sault Rapids Facility (the “LSR Royalty Interest”). It is also the owner of a 14.14% secured, subordinated note (the “LSR Subordinate Note”) in the principal amount of $2,000,000 issued jointly and severally by Algonquin Power (Long Sault) Corporation Inc., Energy Acquisition (Long Sault) Ltd., Nicholls Holdings Inc. and Radtke Holdings Inc. The LSR Subordinate Note was acquired by the Fund on April 17, 1998.

6

| 2. | GENERAL DEVELOPMENT OF THE BUSINESS |

On October 27, 2009, Algonquin completed a transaction (the “Unit Exchange”) in which Algonquin’s unitholders exchanged their trust units of Algonquin, on a one-for-one basis, for Common Shares of an existing corporation. As a result of the Unit Exchange, the Fund itself became a wholly-owned subsidiary of the Corporation and all of the unitholders of the Fund became shareholders of the Corporation. The Unit Exchange did not result in any change to the underlying business operations of the Fund and accordingly, for accounting purposes, the Corporation is considered a continuation of the Fund. The Fund has since changed its name to Algonquin Power Co.

APUC’s business strategy is to maximize long term shareholder value as a dividend paying, growth-oriented corporation in the power and utilities business sectors. APUC is committed to delivering a total shareholder return comprised of dividends augmented by capital appreciation arising through growth in dividends supported by increasing cash flows and earnings. Through an emphasis on sustainable, long-view renewable power and utility investments, over a medium-term planning horizon APUC strives to deliver annualized per share earnings growth of 5% and to grow its dividend supported by growth in cash flows, earnings and investment prospects.

APUC understands the importance of the dividend to its shareholders. In the fiscal year ended December 31, 2010, APUC paid quarterly cash dividends to shareholders of $0.06 per share or $0.24 per share per annum. On March 3, 2011, the board of directors of APUC (the “Board”) approved an annual dividend increase of $0.02 per common share for a total annual dividend of $0.26, paid quarterly at a rate of $0.065 per common share. The Board also declared a dividend of $0.065 per share payable on April 15, 2011 to the shareholders of record on March 31, 2011.

APUC believes this level of dividends will continue to allow for both an immediate return on investment for shareholders and retention of sufficient cash within APUC to fund growth opportunities, reduce short term debt obligations and mitigate the impact of fluctuations in foreign exchange rates. Any increases in the level of dividends paid by APUC will be at the discretion of the Board and dividend levels shall be reviewed periodically by the Board in the context of cash available for distribution and earnings together with an assessment of the growth prospects available to the Corporation. APUC strives to achieve its results within a moderate risk profile consistent with top-quartile North American power and utility operations.

APUC produces stable earnings through a diversified portfolio of renewable power and utility businesses owned and operated by its subsidiary entities. APUC conducts its operations primarily through two businesses: independent power generation and utilities (water, gas and electric). These businesses of APUC are herein referred to as the “APUC Businesses”.

Independent Power Generation:APCo develops, owns and operates a diversified portfolio of electrical energy generation facilities. Within this business there are three distinct divisions: Renewable Energy, Thermal Energy and Development. The Renewable Energy division operates APCo’s hydroelectric and wind power facilities. The Thermal Energy division operates co-generation, energy-from-waste, and steam production facilities. The Development division seeks to deliver continuing growth to APCo through development of APCo’s greenfield power generation projects, accretive acquisitions of electrical

7

energy generation facilities as well as development of organic growth opportunities within APCo’s existing portfolio of renewable energy and thermal energy facilities.

The renewable power and thermal energy generation business of APCo is managed with an emphasis on growth through the development of green-field projects and opportunities within APCo’s existing portfolio. This involves building on APCo’s expertise in the origination of greenfield renewable energy projects, expanding APCo’s existing portfolio of assets for further growth, and capitalizing on new opportunities as they arise.

APCo’s Renewable Energy division generates and sells electrical energy through a diverse portfolio of clean, renewable power generation and thermal power generation facilities across North America. As at March 15, 2011, APCo owns or has interests in 44 hydroelectric facilities operating in Ontario (4), Québec (12), Newfoundland (1), New Brunswick (1) Alberta (1), New York State (13), New Hampshire (8), Vermont (1), Maine (2) and New Jersey (1) with a combined generating capacity of approximately 165 MW. APCo also owns a 104 MW wind powered generating station in Manitoba and holds debt securities in a 26 MW wind powered generating station recently completed in Saskatchewan. Approximately 75% of the installed capacity of APCo’s renewable energy facilities sell their electrical output pursuant to long term power purchase agreements (“PPAs”) with major utilities and have a weighted average remaining contract life of 16 years.

APCo’s Thermal Energy division holds equity interests in one energy-from-waste facility in Ontario with an installed generating capacity of 10 MW, 4 diesel generating facilities in Maine and New Brunswick with total installed generating capacity of 34 MW and 3 natural gas-fired cogeneration facilities in each of California, Connecticut, and Ontario with an installed capacity of approximately 112 MW. In addition, APCo’s Thermal Energy division owns partnership, share and debt interests in two biomass-fired generating facilities with combined installed capacity of approximately 43 MW located in Alberta and Québec. APCo’s Thermal Energy division holds minority investments in two natural gas/wood waste-fired generating facilities with joint installed capacity of approximately 170 MW located in northern Ontario. APCo’s ownership interest in the combined installed generating capacity represents approximately 210 MW. APCo’s thermal energy facilities operate under long term PPAs with major utilities and have an average remaining contract life of 6 years. Detailed information on the facilities owned and operated by APCo is set out in Schedules A and B.

Utilities:Liberty Utilities Co. (“Liberty Utilities”) owns and operates utilities through its two wholly-owned subsidiaries, Liberty Energy and Liberty Water. Liberty Energy is in the electricity distribution, transmission and generation sector as well as natural gas distribution. Liberty Water is in the water distribution and wastewater treatment sector. These utilities share certain common infrastructure to generate economies of scale to support best-in-class customer care for its utility ratepayers. The underlying business strategy is to be a leading provider of safe, high quality and reliable utility services while providing stable and predictable earnings from utility operations. In addition to encouraging and supporting organic growth within its service territories, Liberty Utilities is focused on delivering continued growth in earnings by identifying acquisition opportunities which provides accretive expansion of its business portfolio.

Liberty Utilities’ water utility division operates under the name of Liberty Water. Liberty Water provides water and wastewater utility services to approximately 74,000 customers through 19 water distribution and wastewater collection and treatment utility systems located in four U.S. States (Arizona (8), Illinois (1), Missouri (3) and Texas (7)). These utilities generally operate under rate regulation, overseen by the public utility commissions of the States in which they operate. Detailed information on the water distribution and wastewater utility systems owned and operated by Liberty Water is set out in Schedule C.

8

In 2009, APUC branded all of its water and wastewater utilities under the Liberty Water brand. Liberty Water is committed to being a leading utility provider of safe, high quality and reliable water and wastewater services while providing stable and predictable earnings from its utility operations. Liberty Water delivers long term value by profitably owning and operating water and wastewater utilities while providing safe, reliable transportation and delivery of water and wastewater treatment in its service areas. It is also focused on delivering continued growth in earnings by identifying opportunities which accretively expand its business portfolio.

Liberty Utilities’ energy utility division operates under the name of Liberty Energy. Liberty Energy provides local electrical and natural gas utility services. On January 1, 2011, Liberty Energy acquired a 50.001% interest in a California-based electricity distribution utility and related generation assets, and now provides electric distribution service to customers in the Lake Tahoe region (the “California Utility”). Liberty Energy has entered into agreements to acquire two additional utilities which currently provide electric and natural gas distribution services to customers in New Hampshire. Detailed information on the electrical utilities systems owned and operated by Liberty Energy is set out in Schedule D.

The following is a description of the general development of the business of the Corporation over the last three fiscal years.

On January 16, 2008, the Fund renewed its combined $175.0 million senior secured revolving operating and acquisition credit facility (the “Senior Credit Facility”) with a syndicate of Canadian banks. Under terms of the renewal, the Senior Credit Facility was extended for a three year term with a maturity date of January 14, 2011. The renewal included improved pricing and other terms as well as an accordion feature that, subject to certain conditions, allowed the Senior Credit Facility to increase to $225.0 million to accommodate future growth and acquisitions. The Fund subsequently exercised a portion of the accordion feature, resulting in total committed and available Senior Credit Facility of $192.8 million.

In June 2008, the BCI Facility was commissioned and became operational. The project involved diverting the existing steam produced by the EFW Facility to a nearby recycled paper board manufacturing mill that requires approximately 90,000 pounds of steam per hour in its manufacturing activities. BCI was established to supply steam produced through normal operations at the EFW Facility to this mill.

On June 27, 2008, the Fund entered into a business combination agreement (the “Business Combination Agreement”) with Highground Capital Corporation (“Highground”) and CJIG Management Inc. (“CJIG”), the manager of Highground and a related party of the Fund controlled by the shareholders of Algonquin Power Management Inc. (“APMI”). APMI was the manager of APCo up to December 22, 2009 and two executives of APUC, the Senior Executives, are principals of APMI. Pursuant to the Business Combination Agreement, CJIG acquired all of the issued and outstanding common shares of Highground, and the Fund issued approximately 3.5 million Trust Units at an ascribed value of approximately $7.69 per Trust Unit. The trading price of the Trust Units at the time of issue was $7.41. Of these Trust Units, approximately 3.1 million Trust Units were received by shareholders of Highground as part of the Business Combination Agreement, with the remaining Trust Units being retained by CJIG. The Fund recorded the Trust Units issued at the estimated fair value of the assets to be liquidated by Highground which, net of transaction costs of $0.8 million, resulted in proceeds of the Trust Units being recorded at a value of $26.2 million. In connection with this transaction, the Fund received: (a) net cash

9

in an amount of $20.6 million; (b) the return of notes, having an aggregate face value of approximately $4.8 million, that were issued by the Fund affiliates related to its St. Leon and BCI Facilities; and (c) a note receivable of $0.8 million related to a hydroelectric facility in Ontario.

The final consideration for the Trust Units is dependent on the proceeds realized from the liquidation of certain Highground investments. APUC’s final consideration will be equal to the lesser of (a) $27.0 million plus 50% of the amount, if any, of the value of the assets formerly owned by Highground after payment of the transaction costs that exceeds $27.0 million and (b) the value of all of the assets formerly owned by Highground after payment of the transaction costs. The value of any non-cash securities received by APUC will be determined through negotiation between the Board and CJIG. The remaining investments, formerly held by Highground, consist primarily of non-liquid debt assets having a book value of approximately $3.2 million. APUC is entitled to 50% of the ultimate proceeds from these investments, after certain adjustments for transaction costs.

On October 27, 2009, the Fund and the Corporation completed the Unit Exchange. See “The Unit Exchange”. As part of the Unit Exchange, on October 27, 2009, the trustees of the Fund also became directors of APUC.

Also on October 27, 2009, in connection with the Unit Exchange, the debentureholders of the Fund exchanged their convertible debentures for convertible debentures of the Corporation or Common Shares. As a result, the debentureholders of the Fund became debentureholders and shareholders of the Corporation. See “Capital Structure - Convertible Debentures”.

On December 2, 2009, APUC completed a public offering of 5,980,000 Common Shares at a price of $3.35 per Common Share for gross proceeds of approximately $20 million and approximately $55 million principal amount of 7% convertible unsecured subordinated debentures due June 30, 2017 (the “Series 3 Debentures”). The underwriters of the offering also exercised in full an over-allotment option to purchase an additional 897,000 Common Shares and approximately $8.2 million principal amount of Series 3 Debentures resulting in aggregate gross proceeds of approximately $86.2 million. See “Capital Structure - Convertible Debentures”.

On December 21, 2009, the board of directions of the Corporation (the “Board”) reached agreement with the shareholders of APMI to internalize all management functions of the Fund which were provided by APMI. APUC acquired the interest previously held by APMI in the management services agreement, with consideration paid in the form of issuance of 1,158,748 Common Shares.

At the annual general meeting on June 23, 2010 (the “Meeting”), APUC adopted a Shareholders’ Rights Plan (the “Rights Plan”). See “Capital Structure - Shareholders’ Rights Plan”.

Liberty Water had ongoing rate cases at a number of its utilities which were processed throughout 2010. See “Utilities: Water and Wastewater - Rate Cases” for further discussion of the status of these rate cases. During the year ended December 31, 2010, Liberty Water completed rate case proceedings at nine utilities in Arizona and Texas which on an annualized basis were expected to contribute an additional U.S. $10.2 million in revenue in Liberty Water. As these rate cases were settled at various times throughout the year ended December 31, 2010, approximately U.S. $2.3 million of the overall annualized revenue increase from rate cases completed in Arizona and Texas was achieved in the year. One

10

additional rate case requesting U.S. $1.1 million in annual revenue requirement is expected to be concluded by the first quarter of 2011.

On December 22, 2010, Liberty Water completed a private placement financing of senior unsecured 5.6% notes for gross proceeds of approximately U.S. $50 million. The notes have a 10 year term bear interest until June 2016 when annual principal repayments of U.S. $5.0 million annually commence. The funds were used to reduce outstanding indebtedness under the Senior Credit Facility.

| (a) | Power Generation - New Wind Projects Under Development |

75 MW Wind - Amherst Island:On February 25, 2011, APUC announced that the Ontario Power Authority (“OPA”) awarded a contract to the wholly-owned 75 MW Amherst Island Wind Project. The Amherst Island Wind Project is located on Amherst Island in the village of Stella, approximately 25 kilometres southwest of Kingston, Ontario. The contract was awarded as part of the second round of the OPA’s Feed-in Tariff (“FIT”) program. Construction is expected to commence shortly following the approval of the application and is expected to take 12 months.

| (b) | Power Generation: Development |

25MW Wind - Saint-Damase: The Saint-Damase Wind Project is located in the local municipality of Saint-Damase which is within the regional municipality of la Matapédia. The project proponents include the Municipality of Saint-Damase and APUC. The first 24 MW phase of the project currently has a targeted commercial operations date in late 2013.

25 MW Wind - Val-Éo: The Val-Éo Wind Project is located in the local municipality of Saint-Gédéon de Grandmont, which is within the regional municipality of Lac-Saint-Jean-Est. The project proponents include the Val-Éo wind cooperative formed by community based landowners and APUC. The first 24 MW phase of the project currently has a targeted commercial operations date of late 2015.

Preliminary permitting began for both projects in early 2011, with all major authorizations targeted for completion by the end of 2012.

20 MW Wind - Morse: On March 21, 2011, APUC announced it has executed an asset purchase agreement with Kineticor Renewables Inc. (“Kineticor”), to acquire all of the assets related to two proposed adjacent 10 MW wind energy development projects near Morse, Saskatchewan (the “Morse Projects”). The Morse Projects are approximately 180 km west of Regina and 400 km west of the 26.4 MW wind generation facility in southeastern Saskatchewan (“Red Lily I”).

The Morse Projects were selected by SaskPower for award of PPAs in accordance with the SaskPower Green Options Partners Program in May 2010. Upon SaskPower’s approval and execution of the PPAs, Kineticor will assign the PPAs to APCo. The Morse Projects are expected to be completed in late 2013.

The Morse Projects are approximately 180 km west of Regina and 400 km west of the 26.4 MW wind generation facility in southeastern Saskatchewan (“Red Lily I”). It is contemplated that the Morse Projects will be situated on 1,120 acres of private lands, with additional land under lease or option in order to facilitate future expansion of the Morse Projects.

11

For a more detailed description of the current projects under development, see “Current Development Projects” and “Quebec Community Wind Projects” in the section entitled “Power Generation: Development” below.

On February 28, 2011, APUC announced that Red Lily I commenced commercial operation under the SaskPower PPA. The PPA with SaskPower is for 25 years and includes a 2% annual increase throughout the term of the agreement. APUC’s commitment in Red Lily I is structured in the form of senior and subordinated debt investment of approximately $19.6 million bearing a blended interest rate of 8.43%.

Project construction costs at Red Lily I are expected to total $71.2 million. In addition to interest payments on its portion of the debt financing, APUC is entitled to certain supervisory fees, estimated at $1.3 million in the first full year of operation. Total interest and fee payments to APUC in 2011 are estimated to be approximately $2.4 million, representing approximately 75% of the expected net cash flows from Red Lily I. APUC has the option to formally exchange its debt investment and fee interest in the project for a 75% equity interest in Red Lily I, exercisable in February 2016.

For a more detailed description of the options and expected impact see “Red Lily Facility” under “Material Facilities” in the section entitled “Power Generation: Renewable – Wind Power” below.

Subsequent to December 31, 2010, the Energy Services Business entered into a three year contract with Maine Public Service Company, a regulated electric transmission and distribution utility serving approximately 36,000 electricity customer accounts in Northern Maine starting March 1, 2011 to provide standard offer service to multiple commercial and industrial customers in Northern Maine. The anticipated customer load associated with the standard offer service is approximately 135,000 MW-hrs.

The capital upgrade at the EFW Facility, completed in July 2010, is expected to result in higher throughput and lower operating costs at the Facility in the first quarter of 2011 as compared to the same period in 2010 when the Facility was temporarily shut down as a result of an unplanned outage experienced in January 2010.

The Windsor Locks Facility will continue to sell a portion of its electricity capacity and all of its steam capacity to the industrial host with the balance of the electrical capacity available to be sold either into the ISO-NE day-ahead market or to retail customers through the Energy Services Business. The Facility did not commit any portion of its electrical capacity to the forward reserve market for the winter of 2011 due to unacceptably low auction prices. It is anticipated that performance during the first quarter of 2011 will be strong, resulting from moderate natural gas prices and a cold winter in the north-east U.S. that has resulted in high electricity prices. APCo has completed preliminary engineering for a repowering project at the Windsor Locks Facility and is in negotiations with Ahlstrom Windsor Locks, LLC (“Ahlstrom”) regarding this project. For a more detailed description of the options and expected impact see “Windsor Locks” under “Material Facilities” in the section entitled “Cogeneration” below.

| (d) | Senior Credit Facility |

On January 14, 2011, APUC announced that it has received commitments from a syndicate of Canadian banks for a new $142 million Senior Credit Facility with a three year term. Under the terms of the new banking agreement, as at December 31, 2010, APCo had $44.4 million of committed and available bank facilities remaining and $5.1 million of cash resulting in $49.5 million of total liquidity and capital reserves. The APCo Senior Credit Facility now matures on February 14, 2014.

12

As at March 25, 2011, APCo had used the Senior Credit Facility to post (i) a letter of credit in the approximate amount of U.S. $19.5 million in respect of the Sanger Facility; (ii) a $1.0 million letter of credit in respect of the Dickson Dam Facility; (iii) letters of credit for the EFW Facility totalling $5.4 million; (iv) letters of credit pursuant to the BCI Facility totalling $2.3 million; (v) letters of credit in connection with the St. Leon Facility totalling $1.8 million; (vi) letters of credit in connection with the Long Sault Rapids Facility totalling $1.2 million; (vii) letters of credit in connection with the Amherst Island Wind Project totalling $1.5 million; and (viii) various other letters of credit required by APCo entities totalling $1.1 million.

On December 11, 2010, the Arizona Corporate Commission (“ACC”) approved an order authorizing a rate increase of U.S. $0.9 million for the Rio Rico Facility, effective February 1, 2011. It is anticipated that the regulatory review of the proposed rates and tariffs for the Bella Vista, Northern Sunrise, and Southern Sunrise Facilities will be completed in Q1 2011. Total revenue increases from rate cases completed in Arizona and Texas represent an additional U.S. $10.2 million in annualized revenue. As these rate cases were settled at various times throughout the year ended December 31, 2010, approximately U.S. $2.3 million of the overall annualized revenue increase from rate cases completed in Arizona and Texas was achieved in the year.

In 2009, APUC announced plans to acquire the California Utility assets in partnership with Emera Inc. (“Emera”). The acquisition was approved by both the California Public Utilities Commission (“CPUC”) and the Public Utilities Commission of Nevada in the fourth quarter of 2010. The transaction was completed on January 1, 2011 for a purchase price of approximately U.S. $131.8 million, subject to certain working capital and other closing adjustments. The acquisition was funded in part with the proceeds of a U.S. $70 million senior unsecured private debt placement at the utility. Liberty Energy’s ownership share of the cost of acquisition of the California Utility was primarily funded through the proceeds of subscription receipts held by Emera for 8.532 million APUC Common Shares at a price of $3.25 per share.

On December 9, 2010 APUC announced that Liberty Energy had entered into agreements to acquire all issued and outstanding shares of Granite State, a regulated electric distribution utility, and EnergyNorth, a regulated natural gas distribution utility for total consideration of U.S. $285.0 million. See “Significant Acquisitions - Energy Utilities”.

Liberty Energy is pursuing additional investments in electric and gas distribution utilities and electric transmission assets, sharing certain common infrastructure between utilities to support best in-class-customer care for its subsidiary utility ratepayers.

| 2.4 | Significant Acquisitions |

On January 12, 2010, APCo completed the acquisition of three hydroelectric generating stations, the 34.5MW Tinker Hydro Facility, a hydroelectric generating facility with sufficient reservoir storage capability to move significant amounts of energy from off-peak to on-peak generation located on the Aroostook River near the Town of Perth-Andover, New Brunswick, Caribou Hydro Facility, a 0.9MW run-of-river hydroelectric generating facility located in Northern Maine and Squa Pan Hydro Facility, a 1.4MW run-of-river hydroelectric generating facility located in Northern Maine.

13

APCo also acquired five thermal generating facilities with a rated capacity of 40MW in Northern Maine and New Brunswick utilized for installed reserve capacity, not continuous generation, and New Brunswick Public Utilities Board regulated transmission lines and interconnections which allow direct and indirect access to multiple electricity markets (Northern Maine ISA, New Brunswick ISO, ISO-NE).

In connection with the acquisition of the Tinker Assets, on February 4, 2010, APCo acquired the Energy Services Business which markets the energy generated from the Tinker Assets. It is anticipated that the majority of the energy sold by the Energy Services Business will be supplied through generation from the Tinker Assets, based on historical long term average levels of hydroelectric energy generation of these facilities. The Energy Services Business primarily involves standard offer contracts for the supply of energy to commercial and industrial customers in northern Maine, as well as energy purchase obligations with the ISO-NE required to supplement self-generated energy.

The Energy Services Business consists of a series of short-term energy supply agreements. These include energy sales to a town in New Brunswick, standard offer service contracts with three local electric utilities in northern Maine, and a series of direct energy contracts with commercial buyers also in northern Maine.

On April 23, 2009, APUC announced plans to co-acquire an electrical generation and regulated distribution utility in partnership with Emera. APUC and Emera would own 50.001% and 49.999%, respectively, of CPUV, which owns 100% of Calpeco. Calpeco was formed to acquire the California-based electricity distribution and related generation assets of NV Energy for the purchase price of approximately US $132 million, subject to certain working capital and other closing adjustments, as outlined in the asset purchase agreement by and between Sierra Pacific Power Company d/b/a NV Energy and Calpeco dated April 22, 2009 (the “Purchase Agreement”).

In October 2009, an application was filed with the CPUC requesting approval of the transaction in which NV Energy had agreed to sell its California electric distribution and generation assets to Calpeco. The transaction was subject to State and Federal regulatory approval. On January 1, 2011, following receipt of all U.S. State and Federal regulatory approvals, Calpeco acquired the assets comprising the California Utility. The California Utility provides electric distribution service to approximately 48,000 customers in the Lake Tahoe region.

As an element of the California Utility partnership, pursuant to a subscription and unitholder agreement dated April 22, 2009 (the “Subscription Agreement”), Emera agreed to a conditional treasury subscription of approximately 8.5 million Trust Units of the Fund at a price of $3.25 per unit. Subsequent to the completion of the Unit Exchange, the Subscription Agreement was amended to reflect a subscription of Common Shares rather than Trust Units of Algonquin. Upon closing, Emera exchanged these subscription receipts into 8.532 million Common Shares at a purchase price of $3.25 per Common Share. The proceeds of the subscription receipts were utilized to fund Liberty Energy’s ownership share of the cost of acquisition of the California Utility.

The acquisition was also funded in part with the proceeds of a U.S. $70 million senior unsecured private debt placement at the utility entered into on December 29, 2010. The private placement is a senior unsecured private placement with U.S. institutional investors, backed solely by the California Utility assets. The notes are fixed rate and split into two tranches, U.S. $45 million of ten year 5.19% notes and U.S. $25 million of 5.59% fifteen year notes.

14

On December 9, 2010, APUC announced that Liberty Energy had entered into agreements to acquire all issued and outstanding shares of Granite State, a regulated electric distribution utility, and EnergyNorth, a regulated natural gas distribution utility from National Grid for total consideration of U.S. $285.0 million, subject to certain working capital and other closing adjustments, as outlined in the share purchase agreements by and between National Grid and Liberty Energy entered into on December 8, 2010 and amended and restated on January 11, 2011 (the “Purchase Agreements”).

Granite State provides electric service to over 43,000 customers in 21 communities in New Hampshire. EnergyNorth provides natural gas services to over 83,000 customers in five counties and 30 communities in New Hampshire. Granite State and EnergyNorth are anticipated to have regulatory assets at closing of approximately U.S. $72.0 million and U.S. $178.8 million.

Closings of the transactions are subject to certain conditions including state and federal regulatory approval, and are expected to occur in the fall of 2011. Financing of the acquisitions is expected to occur simultaneously with the closing of the transactions. Liberty Energy is targeting a capital structure with not more than 50% debt to total capital, consistent with investment grade utilities.

As an element of the EnergyNorth and Granite State acquisitions and pursuant to a subscription agreement dated December 9, 2010 (the “2010 Subscription Agreement”), Emera has agreed to a conditional treasury subscription of 12.0 million trust units of APUC at a price of $5.00 per Common Share representing an approximate 5% premium to APUC’s closing share price on December 8, 2010. Delivery of the shares under the subscription receipts is conditional on and is planned to occur simultaneously with the closing of the acquisition of Granite State and EnergyNorth.

For complete details on the Purchase Agreement(s) and the Subscription Agreement, reference should be made to the documents as filed on SEDAR at www.sedar.com.

| 3. | DESCRIPTION OF THE BUSINESS |

| 3.1 | General Description of the Regulatory Regimes in which the Business Operates. |

| (a) | Power Generation Regulatory Regimes |

In Canada, the provinces have legislative authority over the supply of energy. The majority of the electrical supply within the Canadian provinces is provided by large Crown corporations such as Ontario Power Generation Inc. and Hydro-Québec or smaller, investor-owned utilities. These large utilities have been primarily responsible for the generation, transmission and distribution of electricity.

“Green Power” is considered electricity generated from renewable energy sources that do not contribute to greenhouse gas emissions. Green Power includes technologies such as small hydroelectric (generally defined as facilities of less than 20 MW in capacity), bioenergy, landfill gas, wind and photovoltaic technologies. Since 1997, both the federal and provincial governments in Canada have provided various incentives to stimulate the production of Green Power in Canada. The incentives have varied from direct subsidies, to tax credits to higher than market rates for electricity generated from renewable energy sources.

Most recently in 2007, the Federal government established a new Renewable Power Production Incentive program (“RPPI”) called “ecoEnergy for Renewable Power” that was created to stimulate up to 14.3 terawatt hours of other new renewable energy. The RPPI provides for an incentive of $10 per MW-Hr of

15

production for the first ten years of operations for eligible projects commissioned after April 1, 2007 and before March 31, 2011. Eligible technologies include waterpower, advanced, innovative and highly efficient biomass, combustion technologies using biogas and other renewable technologies. The ecoEnergy program is scheduled to be completed by the end of March 2011.

The power generation industry in the United States is regulated by the United States Federal Energy Regulatory Commission (“FERC”) under the U.S. Public Utilities Regulatory Policies Act (“PURPA”). FERC, pursuant to the PURPA legislation, mandates the development of policies by state utility commissions and utilities themselves that enable private producers to build power facilities. The key policy issue was the development of long term PPAs with fixed, long-term power purchase rates. The long-term rates were based on projections of the utilities’ Avoided Costs. “Avoided Costs” means costs a utility does not incur to add new generating capacity to the system by purchasing electricity from an independent or parallel generator. Today, due to market forces and economic changes, many of these long-term agreements are priced far above current market rates. While these higher costs are burdensome to the utilities, most have recognized these as costs incurred prior to deregulation that can no longer be paid by the rate base due to changes to various factors.

On February 2, 2006, PURPA issued revised rules,Revised Regulations Governing Small Power Production and Cogeneration Facilities, Order No. 671, 114 FERC 61,102 (2006). Further regulations were also issued to clarify the regulations and became effective on April 20, 2006. In order to comply with the new regulations, in June of 2006, APUC filed with FERC a notification of holding company status for each direct and indirect subsidiary company of APUC. Based on an initial review of the regulations, APFC may be impacted by the revised rules. APUC is currently investigating the option of filing an exemption or waiver with FERC for APFC.

The key regulations that impact APUC are:

| | (1) | Any type of Qualifying Facility that exists but has never filed a self-certification (or obtained an order certifying it as a Qualifying Facility) must file a self-certification (or petition for an order) within 60 days of Order No. 671. Self-certification documents were filed for all affected APUC Facilities in compliance this regulation. |

| | (2) | Any cogeneration Qualifying Facility, any small power production Qualifying Facility less than 30 MW, and any geothermal small power production Qualifying Facility, is now subject to rate regulation under Section 205 and 206 of theFederal Power Act. However, sales of energy or capacity made by Qualifying Facilities 20 MW or smaller, or made pursuant to a contract executed on or before March 4, 2006, or made pursuant to a state regulatory authority’s implementation of PURPA are exempt from scrutiny under sections 205 and 206. If this exception does not apply, then these Qualifying Facilities must make a rate filing under section 205 of the Federal Power Act in order to be eligible to sell electricity. Rate filings were required to be made on or before the effective date of Order 671, which was March 4, 2006. All relevant APUC facilities had PPAs in place predating this section of the new FERC regulations and as such have not been impacted. |

The Obama-BidenNew Energy for America Plan supports 10% of electricity in the United Sates being generated from renewable sources by 2012 and 25% by 2025. The demand for additional renewable power is also expected to increase from the desire by various government entities to increase infrastructure spending.

16

| (b) | Water Utility Services Regulatory Regimes |

| | (i) | United States Water Services Industry |

Investor-owned utilities are subject to regulation by the public utility commissions of the states in which they operate. The respective public utility commissions typically have jurisdiction over rates, service, accounting procedures, issuance of securities, acquisitions and other matters. The utilities generally operate under cost-of-service regulation as administered by these state authorities, using a test year in the establishment of rates for the utility and pursuant to this method the determination of the rate of return on approved rate base and deemed capital structure, together with all reasonable and prudent costs, establishes the revenue requirement upon which each utility’s customer rates are determined. Rates charged by these utilities are determined such that rates are set so as to provide the utilities with sufficient revenues to generate after-tax equity returns of approximately 8% to 12%.

Generally, water and wastewater providers in the United States operate as geographic monopolies within the areas in which they serve. A water or wastewater company is provided a service territory defined by a Certificate of Convenience and Necessity which imposes an exclusive right and duty to serve in the service territory. A Certificate of Convenience and Necessity is typically granted by a State agency, which also serves as an economic and service quality regulator for these water or wastewater service providers. Such agencies are charged with ensuring that water and wastewater services are provided at reasonable rates and quality to the company’s customers. The agency must balance the interests of the rate payers as well as companies and their shareholders. Rates are approved by the agency to provide the water or wastewater company the opportunity, but not the guarantee, to earn a reasonable return on its investment after recovering its prudently incurred operating expenses.

| (c) | Electrical Utility Services Regulatory Regimes |

| | (i) | United States Electric Services Industry |

Investor-owned electricity utilities are subject to regulation by the public utility commissions of the States in which they operate. The respective public utility commissions typically have jurisdiction over rates, service, accounting procedures, issuance of securities, acquisitions and other matters. The utilities generally operate under cost-of-service regulation as administered by these state authorities, using a test year in the establishment of rates for the utility and pursuant to this method the determination of the rate of return on approved rate base and deemed capital structure, together with all reasonable and prudent costs, establishes the revenue requirement upon which each utility’s customer rates are determined. Rates charged by these utilities are determined such that rates are set so as to provide the utilities with sufficient revenues to generate after-tax equity returns of approximately 8% to 12%.

Generally, electricity providers in the United States operate as geographic monopolies within the areas in which they serve. An electricity distribution company is provided a service territory which imposes an exclusive right and duty to serve in the service territory. The approval to serve is typically granted by a State agency, which also serves as an economic and service quality regulator for these electric service providers. Such agencies are charged with ensuring that electric services are provided at reasonable rates and quality to the company’s customers. The agency must balance the interests of the rate payers as well as companies and their shareholders. Rates are approved by the agency to provide the electric services company the opportunity, but not the guarantee, to earn a reasonable return on its investment after recovering its prudently incurred operating expenses.

The electricity industry remains perhaps the most highly regulated in the United States. The industry is regulated under strict standards at multiple levels - federal, state and sometimes local. Under the Federal

17

Power Act, FERC regulates interstate transmission, wholesale sales of electricity, corporate acquisitions and dispositions, securities and debt issuances, debt acquisitions, and reliability. State utility commissions perform a similar role, regulating sales of electricity to end-use customers, as well as financial stability and reliability. This oversight also includes cost-of-service regulation to establish rates for the utility and pursuant to this method the determination of the rate of return on approved rate base and deemed capital structure, together with all reasonable and prudent costs in order to determine the revenue requirement upon which each utility’s customer rates are set. Rates charged by these utilities are determined such that rates are set so as to provide the utilities with sufficient revenues to generate after-tax equity returns of approximately 8% to 12%. This oversight and other rules set by the state utility commissions are intended to ensure reliable service and adequate supplies of electricity together with financial security, transparency in the rate setting process and reasonable prices.

| 3.2 | Production Method, Principal Markets, Distribution Methods and Material Facilities |

| (a) | Power Generation: Renewable - Hydroelectric |

A hydroelectric generating facility consists of a number of components, including a dam, headrace canal or penstock, intake structure, electromechanical equipment consisting of a turbine(s), a generator(s), draft tube and tailrace canal. In addition, there are electrical switchgear and controls equipment which are necessary to interconnect the facility with the receiving electrical grid system.

A dam structure is required to create or increase the natural elevation difference between the upstream reservoir and the downstream tailrace (referred to as “head”), as well as to provide sufficient depth within the reservoir for an intake. Dam structures are also used to create an upstream reservoir which allows water to be stored within a headpond.

Water flows are conveyed from the upstream reservoir to the generating equipment via a penstock or headrace canal. A penstock is a pipeline capable of operating under pressure, and is normally constructed of steel or other suitable materials. A headrace canal is a channel which conveys water from the reservoir to the intake in a hydraulically efficient manner. The intake structure is a water intake located at the entrance to a penstock or at the end of a headrace canal. The purpose of the intake structure is to collect water from the upstream reservoir. Turbine(s) and generator(s) transform the hydraulic energy into electrical energy.

The water which has flowed through the hydraulic turbine(s) is discharged back to the natural watercourse. A transmission line is often required to interconnect a facility with the grid. The majority of hydroelectric generating facilities are also equipped with remote monitoring equipment, which allows the facility to be monitored and operated from a remote location.

| | (ii) | Principal Markets and Distribution Methods |

The principal markets of in Canada are Alberta, Ontario, New Brunswick and Québec. In the US, the principal markets are Maine, New York State and New Hampshire. The majority of generated hydroelectricity is conveyed from the relevant APCo facility to the purchasers under the terms of long term PPAs. The electricity is generally transferred by transmission line from the generating facility to the delivery point for the purchaser, and it is distributed through the grid to end user customers of the purchaser. A summary of the PPAs for APCo’s Renewable Energy division is set out in Schedule A.

18

Electrical power generators in Alberta are regulated by theElectric Utilities Act (Alberta) and theIndependent Power and Small Power Regulation.

The Ontario government develops the regulatory framework for wholesale and retail competition through the Ontario Energy Board (the “OEB”). While transitional issues such as pricing and metering continue to be considered by the OEB, full competition in the wholesale and retail electricity market commenced on May 1, 2002.

The Ontario Electricity Financial Corporation (“OEFC”) holds all rights, obligations and liabilities under such PPAs. This Ontario government agency purchases the energy generated by the Ontario facilities in which APCo has an interest pursuant to the existing contracts. APCo has also received a licence to generate from the OEB as required by theEnergy Act (Ontario).

| | (3) | New Brunswick and Northern Maine |

In 2003 the New Brunswick government amended the provincialElectricity Act (New Brunswick) (the “Electricity Act”) which resulted in the start of competition in the generation business.

As a result of the Electricity Act, which took effect in October of 2004, New Brunswick Power Corporation (“NB Power”) was divided into separate businesses with the aim of selling off the various components. The distribution and customer service division of NB Power now functions as a regulated monopoly and serves all the residential and industrial power consumers in the province, with the exception of those in Saint John, Edmundston and Perth-Andover which are served by Saint John Energy, City of Edmundston Electric and the Perth-Andover Electric Light Commission, respectively.

One of the separate entities created by the Electricity Act is the New Brunswick System Operator (“NBSO”), an independent not-for-profit statutory corporation. NBSO is responsible for the adequacy and reliability of the integrated electricity system, and for facilitating the development and operation of the New Brunswick electricity market. These responsibilities take the form of operation of the NBSO-controlled grid and administration of the Open Access Transmission Tariff and the New Brunswick Electricity Market Rules.

The NBSO is the Balancing Authority for New Brunswick, Prince Edward Island, and Northern Maine, and the Transmission Provider for New Brunswick. NBSO provides load following and regulation service to the system in order to supply customer load in the province while maintaining scheduled flows on interconnections within established limits. NBSO is the authority responsible for the operation of the Bulk Power System in New Brunswick, Nova Scotia, Prince Edward Island, and a portion of northeastern Maine.

Similar to Ontario, the Québec government develops the regulatory framework for wholesale and retail competition. Since 1991 Hydro-Québec has procured some of its power requirements from private producers. The province continues to introduce various programs to stimulate renewable power from hydroelectric and wind powered facilities as well as cogeneration plants fuelled by biomass and natural gas.

19

In April 2002, the Québec government adopted theDam Safety Act (Quebec) and corresponding regulations. TheDam Safety Act (Quebec) imposes a series of safety measures governing the construction, alteration and operation of high-capacity dams. It requires dam owners to maintain their facilities in good repair and monitor their hydraulic works. As a result of this legislation, APCo’s Renewable Energy division was required to undertake technical assessments of eleven of the twelve hydroelectric facility dams owned or leased by APCo within the Province of Québec.

As a result of the assessments and preliminary evaluation of the associated remedial work, APCo currently estimates it will incur capital expenditures of approximately $17.1 million related to compliance with the legislation. APCo anticipates that these expenditures will be required to be invested over the next five years as follows:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Total | | | 2011 | | | 2012 | | | 2013 | | | 2014 | | | 2015 | |

Estimated Capital Expenditures | | $ | 17,100 | | | | 800 | | | | 5,000 | | | | 5,500 | | | | 3,000 | | | | 2,800 | |

The majority of these capital costs are associated with the Donnacona, St. Alban, Belleterre and Mont-Laurier Facilities. APCo does not anticipate any significant impact on power generation or associated revenue while the dam safety work is ongoing. APCo is also exploring several alternatives to mitigate the capital costs of modifications, including cost sharing with other stakeholders and revenue enhancements which can be achieved through the modifications.

| | (1) | Long Sault Rapids Facility |