UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21108

Pioneer Series Trust X

(Exact name of registrant as specified in charter)

60 State Street, Boston, MA 02109

(Address of principal executive offices) (ZIP code)

Christopher J. Kelley, Amundi Asset Management, Inc.,

60 State Street, Boston, MA 02109

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 742-7825

Date of fiscal year end: August 31, 2023

Date of reporting period: September 1, 2022 through February 28, 2023

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Pioneer Corporate

High Yield Fund

Semiannual Report | February 28, 2023

visit us: www.amundi.com/us

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/231

President’s Letter

Dear Shareholders,

On February 13, 2023, Amundi US celebrated the 95th anniversary of Pioneer Fund, the second-oldest mutual fund in the United States. We recognized the anniversary with ringing of the closing bell at the New York Stock Exchange, which seemed fitting for this special milestone.

Pioneer Fund was launched on February 13, 1928 by Phil Carret, the father of value investing and a leading innovator in the asset management industry. Mr. Carret began investing in the 1920s and founded Pioneer Investments (now Amundi US) in 1928, and was one of the first investors to realize he could uncover value through rigorous, innovative, fundamental research techniques.

Consistent with Mr. Carret’s investment approach and employing many of the same techniques utilized in the 1920s, Amundi US's portfolio managers have adapted Mr. Carret’s philosophy to a new age of “Active” investing.

The last few years have seen investors face some unprecedented challenges, from a global pandemic that shuttered much of the world’s economy for months, to geopolitical strife, to rising inflation that has reached levels not seen in decades. Now, more than ever, Amundi US believes active management – that is, making active investment decisions across all of our portfolios – can help mitigate the risks during periods of market volatility.

At Amundi US, active management begins with our own fundamental, bottom-up research process. Our team of dedicated research analysts and portfolio managers analyzes each security under consideration, communicating frequently with the management teams of the companies and other entities issuing the securities, and working together to identify those securities that we believe best meet our investment criteria for our family of funds. Our risk management approach begins with each security under consideration, as we strive to develop a deep understanding of the potential opportunity, while considering any potential risk factors.

Today, as shareholders, we have many options. It is our view that active management can serve shareholders well, not only when markets are thriving, but also during periods of market stress. As you consider your long-term investment goals, we encourage you to work with your financial professional to develop an investment plan that paves the way for you to pursue both your short-term and long-term goals.

2Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

We greatly appreciate the trust you have placed in us and look forward to continuing to serve you in the future.

Lisa M. Jones

Head of the Americas, President and CEO of US

Amundi Asset Management US, Inc.

April 2023

Any information in this shareowner report regarding market or economic trends or the factors influencing the Fund’s historical or future performance are statements of opinion as of the date of this report. Past performance is no guarantee of future results.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/233

Portfolio Management Discussion | 2/28/23

In the following interview, portfolio managers Matthew Shulkin, Andrew Feltus, and Ken Monaghan discuss the factors that influenced the performance of Pioneer Corporate High Yield Fund during the six-month period ended February 28, 2023. Mr. Shulkin, a senior vice president and a portfolio manager at Amundi Asset Management US, Inc. (Amundi US), Mr. Feltus, CFA, Managing Director, Co-Director of High Yield, and a portfolio manager at Amundi US, and Mr. Monaghan, Managing Director, Co-Director of High Yield, and a portfolio manager at Amundi US, are responsible for the day-to-day management of the Fund.

| Q | How did the Fund perform during the six-month period ended February 28, 2023? |

| A | Pioneer Corporate High Yield Fund’s Class A shares returned 1.18% at net asset value during the six-month period ended February 28, 2023, while the Fund’s benchmark, the ICE Bank of America US High Yield Index (the ICE BofA Index), returned 2.36%. During the same period, the average return of the 700 mutual funds in Morningstar’s High Yield Bond Funds category was 2.29%. |

| Q | Could you please describe the investment environment for high-yield corporate bonds during the six-month period ended February 28, 2023? |

| A | With inflation showing signs of modest easing entering the period, investors began to anticipate a pivot by the US Federal Reserve (Fed) to a more dovish stance on monetary policy after months of interest-rate increases. The speculation led to strong returns in the bond market during October and November 2022, despite the Fed’s making another 75-basis point (bps) increase to the target range for the federal funds rate in early November. (A basis point is equal to 1/100th of percentage point.) However, the market soon turned its attention to the potential recessionary effects of the higher-interest-rate regime already put in place by the Fed earlier in 2022, which led riskier assets, such as corporate bonds, to retrace some of their fourth-quarter gains as December progressed. The Fed implemented a more modest increase of 50 bps to the federal funds rate target range at its December meeting, leaving the target range at 4.25% ‒ 4.50% at the end of 2022, its highest level since the fall of 2007. |

| | Entering 2023, riskier assets rallied once again, due to growing optimism among investors that the Fed and other major central |

4Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

| | banks were poised to stop raising interest rates altogether. January saw Treasury yields ease off their recent highs on the outlook for easier monetary policies, which boosted performance for bonds in general. In addition, the reopening of China’s economy as the government unwound its “Zero-COVID” policy eased concerns about slowing global economic growth. Against that backdrop, areas of the market that had lagged during the 2022 sell-off, such as growth stocks and corporate credit, outperformed. On February 1, 2023, the Fed increased the federal funds target range by another 25 bps, to 4.50% ‒ 4.75%. |

| | However, as the six-month period came to a close, the market was anticipating further, significant increases in the federal funds rate target range, based on hawkish rhetoric from Fed Chair Jerome Powell. As of February 28, 2023, the yield on the 10-year Treasury stood at 3.92%, an increase of 77 bps over the 3.15% yield at the beginning of the period six months earlier. |

| Q | Can you review your principal strategies in managing the Fund during the six-month period ended February 28, 2023, and the degree to which the portfolio’s positioning affected benchmark-relative returns? |

| A | We have based our investment process for the Fund on security and sector selection. We believe that diligent, detailed, fundamental research could uncover mispriced securities, and that actively managing the portfolio to capture those opportunities may produce competitive returns over the longer term. |

| | During the six-month period, our use of index-based credit-default swap contracts, as part of our efforts to reduce portfolio-level credit risk, was the largest detractor from the Fund’s benchmark-relative performance. Overall security selection results also detracted from the Fund’s relative returns, most notably among the portfolio’s holdings within the transportation, and technology and electronics sectors. |

| | On the positive side, security selection results within the basic industry sector proved additive for the Fund’s relative returns, and overall sector allocation results likewise contributed positively to relative performance. With regard to sector allocation, the portfolio’s underweight to the media sector and |

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/235

| | overweight to the transportation sector made the biggest positive contributions to the Fund’s relative results. |

| | With regard to individual holdings, the Fund’s relative performance for the period benefited from exposures to the debt of gold-miner Iamgold, aircraft-leasing firms Aviation Capital and Global Aircraft Leasing, and TimkenSteel, a steel provider. On the downside, detractors from the Fund’s relative returns for the period included positions in air-cargo company WGA, cable-services provider CSC Holdings, remote-work software company LogMeIn, and specialty-retailer Party City. |

| Q | Can you discuss the factors that affected the Fund’s income-generation (or distributions* to shareholders), either positively or negatively, during the six-month period ended February 28, 2023? |

| A | The Fund’s monthly distribution rate slightly increased during the six-month period, the result of rising interest rates as well as below-investment-grade corporate bond yields over the period. |

| Q | Did the Fund have any exposure to derivatives during the six-month period ended February 28, 2023? If so, did the derivatives have a material effect on the Fund’s performance? |

| A | We utilize derivatives in the portfolio from time to time, in order to maintain the desired level of exposure to the high-yield market, while also seeking to maintain sufficient liquidity to make opportunistic purchases and help meet any unanticipated shareholder redemptions. As noted earlier, our use of index-based credit-default-swap contracts detracted from the Fund’s relative performance for the six-month period. |

| Q | What is your assessment of the current climate for high-yield investing? |

| A | The US macroeconomic situation remains highly unusual, in our view, due to the lingering effects of COVID-19-related changes in consumption, production, and supply chains. Even as consumption has continued to shift away from goods to services and as supply chains have continued to normalize, backlogs still remain for many products. At the same time, the domestic job market has remained overheated, with job openings far in excess |

| * | Distributions are not guaranteed. |

6Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

| | of available workers. Inflation has remained well above the Fed’s longer-run goal of 2%, and wage growth has been above levels consistent with that inflation target. The Fed has continued to focus on cooling the labor market to bring wage inflation down, and likely hopes that it can do so without tipping the economy into recession. However, we believe the path to such a “soft landing” for the economy remains narrow. |

| | We believe clarity on when the Fed will eventually pause its rate-hiking cycle could boost investor demand for riskier assets in general, and provide a tailwind for fixed-income market returns, based on both credit-spread tightening and declining interest rates. (Credit spreads are commonly defined as the differences in yield between Treasuries and other types of fixed-income securities with similar maturities.) That said, we see elevated risk for persistent, high inflation, especially with respect to core services, where the Fed’s policy tightening has, so far, had little impact. Together with a robust employment backdrop, we believe this suggests that the terminal (ending) target range for the federal funds rate could be higher than previously expected. |

| | While we believe having a strong focus on credit selection remains critical, on balance, we feel that a steep recession featuring elevated levels of high-yield defaults is unlikely, and so we have been seeking to maintain the portfolio’s risk profile at close to neutral versus that of the benchmark, while being prepared to decrease or increase portfolio risk as credit spreads narrow or widen. We believe current high-yield spreads are priced in anticipation of a mild recession. While our analysts have been uncovering some signs of economic slowing, they also have reported that most issuers appear to be in relatively good condition. |

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/237

Please refer to the Schedule of Investments on pages 17–28 for a full listing of Fund securities.

All investments are subject to risk, including the possible loss of principal. In the past several years, financial markets have experienced increased volatility and heightened uncertainty. The market prices of securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict including Russia's military invasion of Ukraine, sanctions against

Russia, other nations or individuals or companies and possible countermeasures, market disruptions caused by tariffs, trade disputes or other government actions, or adverse investor sentiment. These conditions may continue, recur, worsen or spread.

Investments in high-yield or lower rated securities are subject to greater-than-average price volatility, illiquidity and possibility of default.

The Fund’s investments, payment obligations and financing terms may be based on floating rates, such as LIBOR (London Interbank Offered Rate), or SOFR (Secured Overnight Financing Rate). Plans are underway to phase out the use of LIBOR. There remains uncertainty regarding the nature of any replacement rate and the impact of the transition from LIBOR on the Fund, issuers of instruments in which the Fund invests, and financial markets generally.

The market price of securities may fluctuate when interest rates change. When interest rates rise, the prices of fixed income securities in the Fund will generally fall. Conversely, when interest rates fall, the prices of fixed income securities in the Fund will generally rise.

Investments in the Fund are subject to possible loss due to the financial failure of issuers of underlying securities and their inability to meet their debt obligations.

Prepayment risk is the chance that an issuer may exercise its right to prepay its security, if falling interest rates prompt the issuer to do so. Forced to reinvest the unanticipated proceeds at lower interest rates, the Fund would experience a decline in income and lose the opportunity for additional price appreciation.

The portfolio may invest in mortgage-backed securities, which during times of fluctuating interest rates may increase or decrease more than other fixed-income securities. Mortgage-backed securities are also subject to pre-payments.

8Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

The Fund may use derivatives, such as options, futures, inverse floating rate obligations, swaps, and others, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance. Derivatives may have a leveraging effect on the Fund.

For more information on this or any Pioneer fund, please visit amundi.com/usinvestors or call 1-800-622-9876. This material must be preceded or accompanied by the Fund's current prospectus or summary prospectus. Before investing, consider the product's investment objectives, risks, charges, and expenses. Read it carefully.

Any information in this shareholder report regarding market or economic trends or the factors influencing the Fund’s historical or future performance are statements of opinion as of the date of this report. Past performance is not a guarantee of future results.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/239

Portfolio Summary | 2/28/23

Portfolio Diversification

(As a percentage of total investments)*

+ Amount rounds to less than 0.1%.

10 Largest Holdings

| (As a percentage of total investments)* |

| 1. | FAGE International SA/FAGE USA Dairy Industry, Inc., 5.625%, 8/15/26 (144A) | 1.66% |

| 2. | Uniti Group LP/Uniti Fiber Holdings, Inc./CSL Capital LLC, 7.875%, 2/15/25 (144A) | 1.57 |

| 3. | Garda World Security Corp., 4.625%, 2/15/27 (144A) | 1.55 |

| 4. | Mativ Holdings, Inc., 6.875%, 10/1/26 (144A) | 1.51 |

| 5. | Koppers, Inc., 6.00%, 2/15/25 (144A) | 1.49 |

| 6. | Altice France Holding SA, 6.00%, 2/15/28 (144A) | 1.49 |

| 7. | Western Global Airlines LLC, 10.375%, 8/15/25 (144A) | 1.30 |

| 8. | NCR Corp., 5.00%, 10/1/28 (144A) | 1.17 |

| 9. | iStar, Inc., 4.75%, 10/1/24 | 1.14 |

| 10. | Dealer Tire LLC/DT Issuer LLC, 8.00%, 2/1/28 (144A) | 1.09 |

| | |

| * | Excludes short-term investments and all derivative contracts except for options purchased. The Fund is actively managed, and current holdings may be different. The holdings listed should not be considered recommendations to buy or sell any securities. |

10Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

Prices and Distributions | 2/28/23

Net Asset Value per Share

| Class | 2/28/23 | 8/31/22 |

| A | $7.84 | $7.97 |

| C | $7.78 | $7.92 |

| Y | $7.88 | $8.01 |

| | | |

Distributions per Share: 9/1/22 - 2/28/23

| Class | Net

Investment

Income | Short-Term

Capital Gains | Long-Term

Capital Gains |

| A | $0.2200 | $— | $— |

| C | $0.1893 | $— | $— |

| Y | $0.2329 | $— | $— |

Index Definitions

The ICE BofA US High Yield Index is an unmanaged, commonly accepted measure of the performance of high-yield securities. Indices are unmanaged and their returns assume reinvestment of dividends and do not reflect any fees or expenses. It is not possible to invest directly in an index.

The index defined here pertains to the “Value of $10,000 Investment” and “Value of $5 Million Investment” charts on pages 12 - 14.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2311

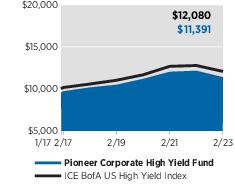

| Performance Update | 2/28/23 | Class A Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $10,000 investment made in Class A shares of Pioneer Corporate High Yield Fund at public offering price during the periods shown, compared to that of the ICE BofA US High Yield Index.

Average Annual Total Returns

(As of February 28, 2023) |

| Period | Net

Asset

Value

(NAV) | Public

Offering

Price

(POP) | ICE

BofA US

High Yield

Index |

Life of Class

(1/3/17) | 2.91% | 2.14% | 3.30% |

| 5 Years | 2.30 | 1.37 | 2.70 |

| 1 Year | -6.34 | -10.60 | -5.52 |

Expense Ratio

(Per prospectus dated December 28, 2022) |

| Gross | Net |

| 1.30% | 0.90% |

Value of $10,000 Investment

Performance of Class A shares shown in the graph above is from the inception of Class A shares on 1/3/17 through 2/28/23. Index information shown in the graph above is from 1/31/17 through 2/28/23.

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

The Fund acquired the assets and liabilities of Pioneer Corporate High Yield Fund (the “Predecessor Fund”) on September 25, 2020 (the “Reorganization”). As a result of the Reorganization, the Predecessor Fund’s performance and financial history became the performance and financial history of the Fund. The performance of Class A shares of the Fund is the performance of Class A shares of the Predecessor Fund for periods prior to the Reorganization, and has not been restated to reflect any differences in expenses.

NAV results represent the percent change in net asset value per share. NAV returns would have been lower had sales charges been reflected. POP returns reflect deduction of maximum 4.50% sales charge. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The net expense ratio reflects the contractual expense limitation in effect through January 1, 2024 for Class A shares. There can be no assurance that Amundi US will extend the expense limitation beyond such time. Please see the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for more current expense ratios.

12Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

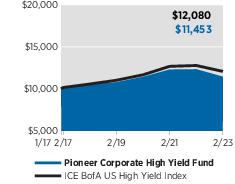

| Performance Update | 2/28/23 | Class C Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $10,000 investment made in Class C shares of Pioneer Corporate High Yield Fund during the periods shown, compared to that of the ICE BofA US High Yield Index.

Average Annual Total Returns

(As of February 28, 2023) |

| Period | If

Held | If

Redeemed | ICE

BofA US

High Yield

Index |

Life of Class

(1/3/17) | 2.23% | 2.23% | 3.30% |

| 5 Years | 1.65 | 1.65 | 2.70 |

| 1 Year | -7.23 | -8.12 | -5.52 |

Expense Ratio

(Per prospectus dated December 28, 2022) |

| Gross | Net |

| 2.06% | 1.65% |

Value of $10,000 Investment

Performance of Class C shares shown in the graph above is from the inception of Class C shares on 1/3/17 through 2/28/23. Index information shown in the graph above is from 1/31/17 through 2/28/23.

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

The Fund acquired the assets and liabilities of Pioneer Corporate High Yield Fund (the “Predecessor Fund”) on September 25, 2020 (the “Reorganization”). As a result of the Reorganization, the Predecessor Fund’s performance and financial history became the performance and financial history of the Fund. The performance of Class C shares of the Fund is the performance of Class C shares of the Predecessor Fund for periods prior to the Reorganization, and has not been restated to reflect any differences in expenses.

Class C shares held for less than one year are subject to a 1% contingent deferred sales charge (CDSC). “If Held” results represent the percent change in net asset value per share. “If Redeemed” returns reflect deduction of the CDSC for the one-year period, assuming a complete redemption of shares at the last price calculated on the last business day of the period, and no CDSC for the five-year and Life-of-Class periods. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The net expense ratio reflects the contractual expense limitation in effect through January 1, 2024 for Class C shares. There can be no assurance that Amundi US will extend the expense limitation beyond such time. Please see the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for more current expense ratios.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2313

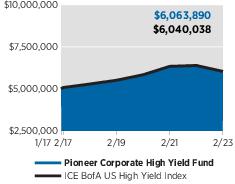

| Performance Update | 2/28/23 | Class Y Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $5 million investment made in Class Y shares of Pioneer Corporate High Yield Fund during the periods shown, compared to that of the ICE BofA US High Yield Index.

Average Annual Total Returns

(As of February 28, 2023) |

| Period | Net

Asset

Value

(NAV) | ICE

BofA US

High Yield

Index |

Life of Class

(1/3/17) | 3.18% | 3.30% |

| 5 Years | 2.58 | 2.70 |

| 1 Year | -6.11 | -5.52 |

Expense Ratio

(Per prospectus dated December 28, 2022) |

| Gross | Net |

| 1.11% | 0.60% |

Value of $5 Million Investment

Performance of Class Y shares shown in the graph above is from the inception of Class Y shares on 1/3/17 through 2/28/23. Index information shown in the graph above is from 1/31/17 through 2/28/23.

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

The Fund acquired the assets and liabilities of Pioneer Corporate High Yield Fund (the “Predecessor Fund”) on September 25, 2020 (the “Reorganization”). As a result of the Reorganization, the Predecessor Fund’s performance and financial history became the performance and financial history of the Fund. The performance of Class Y shares of the Fund is the performance of Class Y shares of the Predecessor Fund for periods prior to the Reorganization, and has not been restated to reflect any differences in expenses.

Class Y shares are not subject to sales charges and are available for limited groups of eligible investors, including institutional investors. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The net expense ratio reflects the contractual expense limitation in effect through January 1, 2024 for Class Y shares. There can be no assurance that Amundi US will extend the expense limitation beyond such time. Please see the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for more current expense ratios.

14Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

Comparing Ongoing Fund Expenses

As a shareowner in the Fund, you incur two types of costs:

| (1) | ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses; and |

| (2) | transaction costs, including sales charges (loads) on purchase payments. |

This example is intended to help you understand your ongoing expenses (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 at the beginning of the Fund’s latest six-month period and held throughout the six months.

Using the Tables

Actual Expenses

The first table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period as follows:

| (1) | Divide your account value by $1,000

Example: an $8,600 account value ÷ $1,000 = 8.6 |

| (2) | Multiply the result in (1) above by the corresponding share class’s number in the third row under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. |

Expenses Paid on a $1,000 Investment in Pioneer Corporate High Yield Fund

Based on actual returns from September 1, 2022 through February 28, 2023.

| Share Class | A | C | Y |

Beginning Account

Value on 9/1/22 | $1,000.00 | $1,000.00 | $1,000.00 |

Ending Account Value

(after expenses) on 2/28/23 | $1,011.80 | $1,006.60 | $1,013.40 |

Expenses Paid

During Period* | $4.49 | $8.21 | $3.00 |

| | |

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.90%, 1.65%, and 0.60% for Class A, Class C, and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the partial year period). |

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2315

Comparing Ongoing Fund Expenses (continued)

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) that are charged at the time of the transaction. Therefore, the table below is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Expenses Paid on a $1,000 Investment in Pioneer Corporate High Yield Fund

Based on a hypothetical 5% return per year before expenses, reflecting the period from September 1, 2022 through February 28, 2023.

| Share Class | A | C | Y |

Beginning Account

Value on 9/1/22 | $1,000.00 | $1,000.00 | $1,000.00 |

Ending Account Value

(after expenses) on 2/28/23 | $1,020.33 | $1,016.61 | $1,021.82 |

Expenses Paid

During Period* | $4.51 | $8.25 | $3.01 |

| | |

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.90%, 1.65%, and 0.60% for Class A, Class C, and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the partial year period). |

16Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

Schedule of Investments | 2/28/23

(unaudited)

Principal

Amount

USD ($) | | | | | | Value |

| | UNAFFILIATED ISSUERS — 99.2% | |

| | Corporate Bonds — 94.7% of Net Assets | |

| | Advertising — 3.4% | |

| 275,000 | Clear Channel Outdoor Holdings, Inc., 7.50%, 6/1/29 (144A) | $ 222,750 |

| 170,000 | Clear Channel Outdoor Holdings, Inc., 7.75%, 4/15/28 (144A) | 141,078 |

| 100,000 | Outfront Media Capital LLC/Outfront Media Capital Corp., 4.25%, 1/15/29 (144A) | 82,250 |

| 380,000 | Outfront Media Capital LLC/Outfront Media Capital Corp., 6.25%, 6/15/25 (144A) | 376,822 |

| 378,000 | Stagwell Global LLC, 5.625%, 8/15/29 (144A) | 325,084 |

| 301,000 | Summer BC Bidco B LLC, 5.50%, 10/31/26 (144A) | 257,912 |

| | Total Advertising | $1,405,896 |

|

|

| | Aerospace & Defense — 1.1% | |

| 253,000 | Bombardier, Inc., 7.875%, 4/15/27 (144A) | $ 251,434 |

| 110,000 | Spirit AeroSystems, Inc., 9.375%, 11/30/29 (144A) | 116,187 |

| 90,000 | Triumph Group, Inc., 9.00%, 3/15/28 (144A) | 90,000 |

| | Total Aerospace & Defense | $457,621 |

|

|

| | Airlines — 0.9% | |

| 66,850 | American Airlines 2021-1 Class B Pass Through Trust, 3.95%, 7/11/30 | $ 58,468 |

| 125,000 | American Airlines, Inc./AAdvantage Loyalty IP, Ltd., 5.50%, 4/20/26 (144A) | 121,656 |

| 205,000 | Spirit Loyalty Cayman, Ltd./Spirit IP Cayman, Ltd., 8.00%, 9/20/25 (144A) | 205,769 |

| | Total Airlines | $385,893 |

|

|

| | Apparel — 0.3% | |

| 115,000 | Hanesbrands, Inc., 9.00%, 2/15/31 (144A) | $ 116,282 |

| | Total Apparel | $116,282 |

|

|

| | Auto Manufacturers — 1.6% | |

| 100,000 | Ford Motor Co., 6.10%, 8/19/32 | $ 93,077 |

| 200,000 | Ford Motor Credit Co. LLC, 3.625%, 6/17/31 | 158,446 |

| 230,000 | Ford Motor Credit Co. LLC, 4.125%, 8/17/27 | 204,921 |

| 206,000 | JB Poindexter & Co., Inc., 7.125%, 4/15/26 (144A) | 198,530 |

| | Total Auto Manufacturers | $654,974 |

|

|

| | Auto Parts & Equipment — 1.5% | |

| 70,000 | Adient Global Holdings, Ltd., 7.00%, 4/15/28 | $ 70,000 |

The accompanying notes are an integral part of these financial statements.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2317

Schedule of Investments | 2/28/23

(unaudited) (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Auto Parts & Equipment — (continued) | |

| 135,000 | Adient Global Holdings, Ltd., 8.25%, 4/15/31 | $ 135,000 |

| 475,000 | Dealer Tire LLC/DT Issuer LLC, 8.00%, 2/1/28 (144A) | 431,281 |

| | Total Auto Parts & Equipment | $636,281 |

|

|

| | Banks — 1.3% | |

| 317,000 | Freedom Mortgage Corp., 8.25%, 4/15/25 (144A) | $ 300,298 |

| 250,000(a)(b) | HSBC Holdings Plc, 8.00% (1 Year CMT Index + 386 bps) | 250,000 |

| | Total Banks | $550,298 |

|

|

| | Building Materials — 3.0% | |

| 260,000 | Builders FirstSource, Inc., 4.25%, 2/1/32 (144A) | $ 218,276 |

| 145,000 | Builders FirstSource, Inc., 6.375%, 6/15/32 (144A) | 139,255 |

| 450,000 | Cornerstone Building Brands, Inc., 6.125%, 1/15/29 (144A) | 326,265 |

| 613,000 | Koppers, Inc., 6.00%, 2/15/25 (144A) | 592,630 |

| | Total Building Materials | $1,276,426 |

|

|

| | Chemicals — 3.2% | |

| 650,000 | Mativ Holdings, Inc., 6.875%, 10/1/26 (144A) | $ 598,994 |

| 111,000 | Olin Corp., 5.00%, 2/1/30 | 101,005 |

| 200,000 | SCIL IV LLC/SCIL USA Holdings LLC, 5.375%, 11/1/26 (144A) | 179,748 |

| 370,000 | Trinseo Materials Operating SCA/Trinseo Materials Finance, Inc., 5.125%, 4/1/29 (144A) | 246,395 |

| 251,000 | Tronox, Inc., 4.625%, 3/15/29 (144A) | 204,565 |

| | Total Chemicals | $1,330,707 |

|

|

| | Commercial Services — 5.4% | |

| 20,000 | Allied Universal Holdco LLC/Allied Universal Finance Corp., 6.625%, 7/15/26 (144A) | $ 18,995 |

| 275,000 | Allied Universal Holdco LLC/Allied Universal Finance Corp., 9.75%, 7/15/27 (144A) | 252,323 |

| 80,000 | Brink's Co., 5.50%, 7/15/25 (144A) | 77,881 |

| 692,000 | Garda World Security Corp., 4.625%, 2/15/27 (144A) | 612,881 |

| 215,000 | Neptune Bidco US, Inc., 9.29%, 4/15/29 (144A) | 203,261 |

| 190,000 | NESCO Holdings II, Inc., 5.50%, 4/15/29 (144A) | 169,338 |

| 295,000 | PECF USS Intermediate Holding III Corp., 8.00%, 11/15/29 (144A) | 207,366 |

| 35,000 | Prime Security Services Borrower LLC/Prime Finance, Inc., 5.25%, 4/15/24 (144A) | 34,475 |

The accompanying notes are an integral part of these financial statements.

18Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

Principal

Amount

USD ($) | | | | | | Value |

| | Commercial Services — (continued) | |

| 420,000 | Prime Security Services Borrower LLC/Prime Finance, Inc., 6.25%, 1/15/28 (144A) | $ 389,592 |

| 300,000 | Sotheby's, 7.375%, 10/15/27 (144A) | 283,014 |

| | Total Commercial Services | $2,249,126 |

|

|

| | Computers — 2.6% | |

| 287,000 | Diebold Nixdorf, Inc., 9.375%, 7/15/25 (144A) | $ 200,900 |

| 329,000 | KBR, Inc., 4.75%, 9/30/28 (144A) | 296,100 |

| 540,000 | NCR Corp., 5.00%, 10/1/28 (144A) | 464,969 |

| 150,000 | NCR Corp., 5.25%, 10/1/30 (144A) | 124,015 |

| | Total Computers | $1,085,984 |

|

|

| | Diversified Financial Services — 5.4% | |

| 442,347(c) | Avation Capital SA, 8.25% (9.00% PIK or 8.25% Cash), 10/31/26 (144A) | $ 379,043 |

| 65,000 | Bread Financial Holdings, Inc., 4.75%, 12/15/24 (144A) | 60,254 |

| 250,000 | Bread Financial Holdings, Inc., 7.00%, 1/15/26 (144A) | 234,044 |

| 444,722(c) | Global Aircraft Leasing Co., Ltd., 6.50% (7.25% PIK or 6.50% Cash), 9/15/24 (144A) | 402,033 |

| 240,000 | Nationstar Mortgage Holdings, Inc., 6.00%, 1/15/27 (144A) | 220,800 |

| 242,000 | Provident Funding Associates LP/PFG Finance Corp., 6.375%, 6/15/25 (144A) | 217,800 |

| 201,000 | United Wholesale Mortgage LLC, 5.50%, 4/15/29 (144A) | 166,368 |

| 305,000 | United Wholesale Mortgage LLC, 5.75%, 6/15/27 (144A) | 268,473 |

| 357,000 | VistaJet Malta Finance Plc/XO Management Holding, Inc., 6.375%, 2/1/30 (144A) | 312,470 |

| | Total Diversified Financial Services | $2,261,285 |

|

|

| | Electric — 2.5% | |

| 215,000 | Clearway Energy Operating LLC, 3.75%, 2/15/31 (144A) | $ 174,956 |

| 85,000 | Clearway Energy Operating LLC, 3.75%, 1/15/32 (144A) | 67,362 |

| 153,000 | Leeward Renewable Energy Operations LLC, 4.25%, 7/1/29 (144A) | 130,185 |

| 135,000 | NRG Energy, Inc., 3.375%, 2/15/29 (144A) | 109,615 |

| 290,000 | NRG Energy, Inc., 3.875%, 2/15/32 (144A) | 224,907 |

| 46,236 | NSG Holdings LLC/NSG Holdings, Inc., 7.75%, 12/15/25 (144A) | 45,311 |

| 55,000 | Vistra Operations Co. LLC, 4.375%, 5/1/29 (144A) | 47,514 |

| 257,000 | Vistra Operations Co. LLC, 5.625%, 2/15/27 (144A) | 243,538 |

| | Total Electric | $1,043,388 |

|

|

| | Electrical Components & Equipments — 1.3% | |

| 253,000 | Energizer Holdings, Inc., 4.75%, 6/15/28 (144A) | $ 220,793 |

The accompanying notes are an integral part of these financial statements.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2319

Schedule of Investments | 2/28/23

(unaudited) (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Electrical Components & Equipments — (continued) | |

| 30,000 | Energizer Holdings, Inc., 6.50%, 12/31/27 (144A) | $ 28,800 |

| 310,000 | WESCO Distribution, Inc., 7.125%, 6/15/25 (144A) | 312,811 |

| | Total Electrical Components & Equipments | $562,404 |

|

|

| | Engineering & Construction — 1.6% | |

| 396,995 | Artera Services LLC, 9.033%, 12/4/25 (144A) | $ 341,416 |

| 225,000 | Promontoria Holding 264 BV, 7.875%, 3/1/27 (144A) | 216,289 |

| 160,000 | TopBuild Corp., 4.125%, 2/15/32 (144A) | 131,379 |

| | Total Engineering & Construction | $689,084 |

|

|

| | Entertainment — 1.6% | |

| 77,000 | Penn Entertainment, Inc., 4.125%, 7/1/29 (144A) | $ 62,490 |

| 110,000 | Scientific Games Holdings LP/Scientific Games US FinCo, Inc., 6.625%, 3/1/30 (144A) | 96,738 |

| 214,000 | Scientific Games International, Inc., 7.25%, 11/15/29 (144A) | 210,255 |

| 350,000 | SeaWorld Parks & Entertainment, Inc., 5.25%, 8/15/29 (144A) | 313,250 |

| | Total Entertainment | $682,733 |

|

|

| | Environmental Control — 1.3% | |

| 130,000 | GFL Environmental, Inc., 4.00%, 8/1/28 (144A) | $ 113,127 |

| 270,000 | GFL Environmental, Inc., 4.375%, 8/15/29 (144A) | 233,734 |

| 201,000 | Tervita Corp., 11.00%, 12/1/25 (144A) | 216,075 |

| | Total Environmental Control | $562,936 |

|

|

| | Food — 3.0% | |

| 280,000 | Albertsons Cos. Inc/Safeway, Inc./New Albertsons LP/Albertsons LLC, 6.50%, 2/15/28 (144A) | $ 278,418 |

| 701,000 | FAGE International SA/FAGE USA Dairy Industry, Inc., 5.625%, 8/15/26 (144A) | 659,885 |

| 280,000 | Lamb Weston Holdings, Inc., 4.125%, 1/31/30 (144A) | 245,726 |

| 95,000 | US Foods, Inc., 4.625%, 6/1/30 (144A) | 82,977 |

| | Total Food | $1,267,006 |

|

|

| | Forest Products & Paper — 0.7% | |

| 334,000 | Mercer International, Inc., 5.125%, 2/1/29 | $ 273,864 |

| | Total Forest Products & Paper | $273,864 |

|

|

| | Healthcare-Products — 0.5% | |

| 255,000 | Medline Borrower LP, 3.875%, 4/1/29 (144A) | $ 212,536 |

| | Total Healthcare-Products | $212,536 |

|

|

| | Healthcare-Services — 2.9% | |

| 229,000 | LifePoint Health, Inc., 5.375%, 1/15/29 (144A) | $ 150,299 |

The accompanying notes are an integral part of these financial statements.

20Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

Principal

Amount

USD ($) | | | | | | Value |

| | Healthcare-Services — (continued) | |

| 318,000 | Prime Healthcare Services, Inc., 7.25%, 11/1/25 (144A) | $ 287,790 |

| 54,000 | RegionalCare Hospital Partners Holdings, Inc./LifePoint Health, Inc., 9.75%, 12/1/26 (144A) | 45,967 |

| 36,000 | Surgery Center Holdings, Inc., 6.75%, 7/1/25 (144A) | 35,532 |

| 247,000 | Surgery Center Holdings, Inc., 10.00%, 4/15/27 (144A) | 251,326 |

| 110,000 | Tenet Healthcare Corp., 6.125%, 6/15/30 (144A) | 104,774 |

| 260,000 | US Acute Care Solutions LLC, 6.375%, 3/1/26 (144A) | 230,542 |

| 353,000 | US Renal Care, Inc., 10.625%, 7/15/27 (144A) | 112,262 |

| | Total Healthcare-Services | $1,218,492 |

|

|

| | Home Builders — 0.7% | |

| 157,000 | KB Home, 4.00%, 6/15/31 | $ 128,226 |

| 205,000 | M/I Homes, Inc., 3.95%, 2/15/30 | 166,240 |

| | Total Home Builders | $294,466 |

|

|

| | Internet — 0.7% | |

| 285,000 | Cogent Communications Group, Inc., 7.00%, 6/15/27 (144A) | $ 275,738 |

| | Total Internet | $275,738 |

|

|

| | Iron & Steel — 1.5% | |

| 290,000 | Carpenter Technology Corp., 7.625%, 3/15/30 | $ 289,147 |

| 39,000 | Mineral Resources, Ltd., 8.00%, 11/1/27 (144A) | 38,805 |

| 360,000 | TMS International Corp., 6.25%, 4/15/29 (144A) | 281,645 |

| | Total Iron & Steel | $609,597 |

|

|

| | Leisure Time — 2.4% | |

| 55,000 | Carnival Holdings Bermuda, Ltd., 10.375%, 5/1/28 (144A) | $ 58,850 |

| 290,000 | NCL Corp., Ltd., 5.875%, 3/15/26 (144A) | 250,850 |

| 55,000 | NCL Corp., Ltd., 7.75%, 2/15/29 (144A) | 47,878 |

| 75,000 | NCL Finance, Ltd., 6.125%, 3/15/28 (144A) | 62,437 |

| 120,000 | Royal Caribbean Cruises, Ltd., 5.50%, 4/1/28 (144A) | 104,592 |

| 20,000 | Royal Caribbean Cruises, Ltd., 7.25%, 1/15/30 (144A) | 20,050 |

| 200,000 | Royal Caribbean Cruises, Ltd., 11.625%, 8/15/27 (144A) | 213,008 |

| 290,000 | Viking Ocean Cruises Ship VII, Ltd., 5.625%, 2/15/29 (144A) | 248,953 |

| | Total Leisure Time | $1,006,618 |

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2321

Schedule of Investments | 2/28/23

(unaudited) (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Lodging — 1.0% | |

| 232,000 | Hilton Grand Vacations Borrower Escrow LLC/Hilton Grand Vacations Borrower Esc, 5.00%, 6/1/29 (144A) | $ 203,613 |

| 202,000 | Travel + Leisure Co., 6.625%, 7/31/26 (144A) | 198,010 |

| | Total Lodging | $401,623 |

|

|

| | Media — 3.2% | |

| 355,000 | CCO Holdings LLC/CCO Holdings Capital Corp., 4.50%, 6/1/33 (144A) | $ 276,191 |

| 121,000 | CCO Holdings LLC/CCO Holdings Capital Corp., 4.75%, 3/1/30 (144A) | 101,757 |

| 160,000 | CCO Holdings LLC/CCO Holdings Capital Corp., 4.75%, 2/1/32 (144A) | 129,600 |

| 55,000 | CCO Holdings LLC/CCO Holdings Capital Corp., 7.375%, 3/1/31 (144A) | 53,356 |

| 800,000 | CSC Holdings LLC, 4.625%, 12/1/30 (144A) | 430,700 |

| 362,000 | McGraw-Hill Education, Inc., 8.00%, 8/1/29 (144A) | 309,402 |

| 25,000 | VZ Secured Financing BV, 5.00%, 1/15/32 (144A) | 20,563 |

| | Total Media | $1,321,569 |

|

|

| | Metal Fabricate/Hardware — 0.2% | |

| 130,000 | Park-Ohio Industries, Inc., 6.625%, 4/15/27 | $ 98,788 |

| | Total Metal Fabricate/Hardware | $98,788 |

|

|

| | Mining — 2.6% | |

| 191,000 | Coeur Mining, Inc., 5.125%, 2/15/29 (144A) | $ 144,549 |

| 250,000 | Constellium SE, 3.75%, 4/15/29 (144A) | 207,630 |

| 235,000 | Eldorado Gold Corp., 6.25%, 9/1/29 (144A) | 207,853 |

| 265,000 | First Quantum Minerals, Ltd., 7.50%, 4/1/25 (144A) | 257,051 |

| 339,000 | IAMGOLD Corp., 5.75%, 10/15/28 (144A) | 252,528 |

| | Total Mining | $1,069,611 |

|

|

| | Oil & Gas — 10.3% | |

| 302,000 | Aethon United BR LP/Aethon United Finance Corp., 8.25%, 2/15/26 (144A) | $ 290,473 |

| 309,000 | Baytex Energy Corp., 8.75%, 4/1/27 (144A) | 314,407 |

| 302,000 | Energean Plc, 6.50%, 4/30/27 (144A) | 277,742 |

| 365,000 | Harbour Energy Plc, 5.50%, 10/15/26 (144A) | 337,625 |

| 90,000 | Hilcorp Energy I LP/Hilcorp Finance Co., 6.00%, 4/15/30 (144A) | 81,647 |

| 90,000 | Hilcorp Energy I LP/Hilcorp Finance Co., 6.25%, 4/15/32 (144A) | 81,611 |

| 262,000 | International Petroleum Corp., 7.25%, 2/1/27 (144A) | 249,555 |

| 200,000 | Kosmos Energy, Ltd., 7.75%, 5/1/27 (144A) | 175,448 |

| 50,000 | Nabors Industries, Inc., 7.375%, 5/15/27 (144A) | 48,189 |

The accompanying notes are an integral part of these financial statements.

22Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

Principal

Amount

USD ($) | | | | | | Value |

| | Oil & Gas — (continued) | |

| 182,000 | Nabors Industries, Ltd., 7.50%, 1/15/28 (144A) | $ 168,000 |

| 300,000 | Neptune Energy Bondco Plc, 6.625%, 5/15/25 (144A) | 291,655 |

| 420,000 | Parkland Corp., 4.625%, 5/1/30 (144A) | 349,650 |

| 66,000 | Precision Drilling Corp., 6.875%, 1/15/29 (144A) | 59,506 |

| 210,000 | Shelf Drilling Holdings, Ltd., 8.875%, 11/15/24 (144A) | 212,100 |

| 324,000 | Southwestern Energy Co., 5.375%, 3/15/30 | 295,968 |

| 304,000 | Strathcona Resources, Ltd., 6.875%, 8/1/26 (144A) | 249,205 |

| 360,000 | Tap Rock Resources LLC, 7.00%, 10/1/26 (144A) | 329,400 |

| 115,000 | Transocean, Inc., 8.75%, 2/15/30 (144A) | 117,013 |

| 40,000 | Transocean Titan Financing, Ltd., 8.375%, 2/1/28 (144A) | 40,828 |

| 260,000 | Tullow Oil Plc, 10.25%, 5/15/26 (144A) | 210,860 |

| 126,000 | Vermilion Energy, Inc., 6.875%, 5/1/30 (144A) | 111,173 |

| | Total Oil & Gas | $4,292,055 |

|

|

| | Oil & Gas Services — 0.5% | |

| 215,000 | Enerflex, Ltd., 9.00%, 10/15/27 (144A) | $ 212,192 |

| | Total Oil & Gas Services | $212,192 |

|

|

| | Packaging & Containers — 2.2% | |

| 344,000 | Clearwater Paper Corp., 4.75%, 8/15/28 (144A) | $ 300,811 |

| 125,000 | Crown Cork & Seal Co., Inc., 7.375%, 12/15/26 | 128,954 |

| 189,000 | OI European Group BV, 4.75%, 2/15/30 (144A) | 168,417 |

| 195,000 | Sealed Air Corp., 5.00%, 4/15/29 (144A) | 178,070 |

| 164,000 | TriMas Corp., 4.125%, 4/15/29 (144A) | 142,680 |

| | Total Packaging & Containers | $918,932 |

|

|

| | Pharmaceuticals — 2.6% | |

| 155,000 | AdaptHealth LLC, 5.125%, 3/1/30 (144A) | $ 134,075 |

| 350,000 | Owens & Minor, Inc., 6.625%, 4/1/30 (144A) | 287,875 |

| 395,000 | P&L Development LLC/PLD Finance Corp., 7.75%, 11/15/25 (144A) | 316,064 |

| 185,000 | Par Pharmaceutical, Inc., 7.50%, 4/1/27 (144A) | 139,244 |

| 260,000 | Teva Pharmaceutical Finance Netherlands III BV, 5.125%, 5/9/29 | 230,142 |

| | Total Pharmaceuticals | $1,107,400 |

|

|

| | Pipelines — 4.7% | |

| 202,000 | CQP Holdco LP/BIP-V Chinook Holdco LLC, 5.50%, 6/15/31 (144A) | $ 177,255 |

| 190,000 | Crestwood Midstream Partners LP/Crestwood Midstream Finance Corp., 7.375%, 2/1/31 (144A) | 185,083 |

| 330,000 | Delek Logistics Partners LP/Delek Logistics Finance Corp., 7.125%, 6/1/28 (144A) | 290,400 |

| 405,000(a)(b) | Energy Transfer LP, 7.125% (5 Year CMT Index + 531 bps) | 360,045 |

The accompanying notes are an integral part of these financial statements.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2323

Schedule of Investments | 2/28/23

(unaudited) (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Pipelines — (continued) | |

| 6,000 | EnLink Midstream LLC, 5.375%, 6/1/29 | $ 5,571 |

| 135,000 | EnLink Midstream LLC, 6.50%, 9/1/30 (144A) | 132,965 |

| 357,000 | EnLink Midstream Partners LP, 5.60%, 4/1/44 | 290,955 |

| 185,000 | Genesis Energy LP/Genesis Energy Finance Corp., 8.00%, 1/15/27 | 180,932 |

| 369,000 | Harvest Midstream I LP, 7.50%, 9/1/28 (144A) | 355,849 |

| | Total Pipelines | $1,979,055 |

|

|

| | Real Estate — 0.5% | |

| 270,000 | Kennedy-Wilson, Inc., 4.75%, 2/1/30 | $ 207,504 |

| | Total Real Estate | $207,504 |

|

|

| | REITs — 4.3% | |

| 310,000 | HAT Holdings I LLC/HAT Holdings II LLC , 3.375%, 6/15/26 (144A) | $ 268,925 |

| 50,000 | iStar, Inc., 4.25%, 8/1/25 | 49,748 |

| 452,000 | iStar, Inc., 4.75%, 10/1/24 | 451,155 |

| 300,000 | MPT Operating Partnership LP/MPT Finance Corp., 3.50%, 3/15/31 | 205,638 |

| 610,000 | Uniti Group LP/Uniti Fiber Holdings, Inc./CSL Capital LLC, 7.875%, 2/15/25 (144A) | 621,850 |

| 215,000 | Uniti Group LP/Uniti Group Finance, Inc./CSL Capital LLC, 10.50%, 2/15/28 (144A) | 215,043 |

| | Total REITs | $1,812,359 |

|

|

| | Retail — 3.7% | |

| 181,000 | Asbury Automotive Group, Inc., 4.625%, 11/15/29 (144A) | $ 157,392 |

| 190,000 | Bath & Body Works, Inc., 6.625%, 10/1/30 (144A) | 179,974 |

| 220,000 | Beacon Roofing Supply, Inc., 4.125%, 5/15/29 (144A) | 188,375 |

| 90,000 | Gap, Inc., 3.625%, 10/1/29 (144A) | 66,000 |

| 50,000 | Gap, Inc., 3.875%, 10/1/31 (144A) | 35,873 |

| 213,000 | Ken Garff Automotive LLC, 4.875%, 9/15/28 (144A) | 183,475 |

| 435,000 | LCM Investments Holdings II LLC, 4.875%, 5/1/29 (144A) | 353,565 |

| 235,000 | Murphy Oil USA, Inc., 3.75%, 2/15/31 (144A) | 190,141 |

| 206,000 | Staples, Inc., 7.50%, 4/15/26 (144A) | 183,340 |

| | Total Retail | $1,538,135 |

|

|

| | Software — 0.7% | |

| 199,000 | AthenaHealth Group, Inc., 6.50%, 2/15/30 (144A) | $ 157,398 |

| 340,000 | Rackspace Technology Global, Inc., 5.375%, 12/1/28 (144A) | 133,566 |

| | Total Software | $290,964 |

|

|

The accompanying notes are an integral part of these financial statements.

24Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

Principal

Amount

USD ($) | | | | | | Value |

| | Telecommunications — 4.0% | |

| 850,000 | Altice France Holding SA, 6.00%, 2/15/28 (144A) | $ 591,345 |

| 185,000 | CommScope, Inc., 4.75%, 9/1/29 (144A) | 150,775 |

| 359,000 | CommScope, Inc., 8.25%, 3/1/27 (144A) | 305,150 |

| 445,000 | Lumen Technologies, Inc., 4.50%, 1/15/29 (144A) | 235,183 |

| 500,000 | Windstream Escrow LLC/Windstream Escrow Finance Corp., 7.75%, 8/15/28 (144A) | 408,600 |

| | Total Telecommunications | $1,691,053 |

|

|

| | Transportation — 3.8% | |

| 450,000 | Carriage Purchaser, Inc., 7.875%, 10/15/29 (144A) | $ 336,559 |

| 219,000 | Danaos Corp., 8.50%, 3/1/28 (144A) | 213,508 |

| 160,000 | Rand Parent LLC, 8.50%, 2/15/30 (144A) | 153,617 |

| 110,000 | Seaspan Corp., 5.50%, 8/1/29 (144A) | 82,800 |

| 300,000 | Seaspan Corp., 6.50%, 4/29/26 (144A) | 298,320 |

| 858,000 | Western Global Airlines LLC, 10.375%, 8/15/25 (144A) | 515,332 |

| | Total Transportation | $1,600,136 |

|

|

| | Total Corporate Bonds

(Cost $45,465,574) | $39,651,011 |

|

|

| Shares | | | | | | |

| | Right/Warrant — 0.0%† of Net Assets | |

| | Aerospace & Defense — 0.0%† | |

| GBP 7,525(d) | Avation Plc, 1/1/59 | $ 3,530 |

| | Total Aerospace & Defense | $3,530 |

|

|

| | Total Right/Warrant

(Cost $—) | $3,530 |

|

|

Face

Amount

USD ($) | | | | | | |

| | Insurance-Linked Securities — 0.0%† of Net

Assets# | |

| | Collateralized Reinsurance — 0.0%† | |

| | Multiperil – Worldwide — 0.0%† | |

| 250,000(d)(e) + | Cypress Re 2017, 1/31/24 | $ 25 |

| 250,000(d)(e) + | Resilience Re, 5/1/23 | — |

| | | | | | | $ 25 |

|

|

| | Total Collateralized Reinsurance | $25 |

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2325

Schedule of Investments | 2/28/23

(unaudited) (continued)

Face

Amount

USD ($) | | | | | | Value |

|

| | Reinsurance Sidecars — 0.0%† | |

| | Multiperil – U.S. — 0.0%† | |

| 1,500,000(d)(f) + | Harambee Re 2018, 12/31/24 | $ — |

| | Multiperil – Worldwide — 0.0%† | |

| 41,791(d)(e) + | Berwick Re 2018-1, 12/31/24 | $ 3,230 |

| 29,857(d)(e) + | Berwick Re 2019-1, 12/31/24 | 4,762 |

| 1,500,000(d)(e) + | Versutus Re 2018, 12/31/24 | 2,400 |

| 250,000(d)(f) + | Viribus Re 2018, 12/31/24 | — |

| 106,153(d)(f) + | Viribus Re 2019, 12/31/24 | 754 |

| | | | | | | $ 11,146 |

|

|

| | Total Reinsurance Sidecars | $11,146 |

|

|

| | Total Insurance-Linked Securities

(Cost $47,759) | $11,171 |

|

|

| Shares | | | | | | |

| | SHORT TERM INVESTMENTS — 4.5% of Net Assets | |

| | Open-End Fund — 4.5% | |

| 1,880,005(g) | Dreyfus Government Cash Management,

Institutional Shares, 4.47% | $ 1,880,005 |

| | | | | | | $ 1,880,005 |

|

|

| | TOTAL SHORT TERM INVESTMENTS

(Cost $1,880,005) | $1,880,005 |

|

|

| | TOTAL INVESTMENTS IN UNAFFILIATED ISSUERS — 99.2%

(Cost $47,393,338) | $41,545,717 |

| | OTHER ASSETS AND LIABILITIES — 0.8% | $ 335,229 |

| | net assets — 100.0% | $ 41,880,946 |

| | | | | | | |

| bps | Basis Points. |

| CMT | Constant Maturity Treasury Index. |

| REIT | Real Estate Investment Trust. |

The accompanying notes are an integral part of these financial statements.

26Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

| (144A) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. Such securities may be resold normally to qualified institutional buyers in a transaction exempt from registration. At February 28, 2023, the value of these securities amounted to $35,287,217, or 84.3% of net assets. |

| (a) | Security is perpetual in nature and has no stated maturity date. |

| (b) | The interest rate is subject to change periodically. The interest rate and/or reference index and spread shown at February 28, 2023. |

| (c) | Payment-in-kind (PIK) security which may pay interest in the form of additional principal amount. |

| (d) | Non-income producing security. |

| (e) | Issued as participation notes. |

| (f) | Issued as preference shares. |

| (g) | Rate periodically changes. Rate disclosed is the 7-day yield at February 28, 2023. |

| † | Amount rounds to less than 0.1%. |

| + | Security is valued using significant unobservable inputs (Level 3). |

| # | Securities are restricted as to resale. |

| Restricted Securities | Acquisition date | Cost | Value |

| Berwick Re 2018-1 | 1/29/2018 | $ 6,104 | $ 3,230 |

| Berwick Re 2019-1 | 12/31/2018 | 3,568 | 4,762 |

| Cypress Re 2017 | 1/24/2017 | 840 | 25 |

| Harambee Re 2018 | 12/19/2017 | 31,843 | — |

| Resilience Re | 2/8/2017 | 124 | — |

| Versutus Re 2018 | 12/20/2017 | — | 2,400 |

| Viribus Re 2018 | 12/22/2017 | 5,280 | — |

| Viribus Re 2019 | 3/25/2019 | — | 754 |

| Total Restricted Securities | | | $11,171 |

| % of Net assets | | | 0.0% |

The accompanying notes are an integral part of these financial statements.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2327

Schedule of Investments | 2/28/23

(unaudited) (continued)

SWAP CONTRACTS

CENTRALLY CLEARED CREDIT DEFAULT SWAP CONTRACTS – BUY PROTECTION

Notional

Amount ($)(1) | Reference

Obligation/Index | Pay/

Receive(2) | Annual

Fixed Rate | Expiration

Date | Premiums

Paid | Unrealized

(Depreciation) | Market

Value |

| 6,850,000 | Markit CDX North America High Yield Index Series 39 | Pay | 5.00% | 12/20/27 | $198,356 | $(362,469) | $(164,113) |

TOTAL CENTRALLY CLEARED CREDIT DEFAULT

SWAP CONTRACTS – BUY PROTECTION | $ 198,356 | $ (362,469) | $ (164,113) |

| TOTAL SWAP CONTRACTS | | $ 198,356 | $ (362,469) | $ (164,113) |

| | |

| (1) | The notional amount is the maximum amount that a seller of credit protection would be obligated to pay upon occurrence of a credit event. |

| (2) | Pays quarterly. |

Principal amounts are denominated in U.S. dollars (“USD”) unless otherwise noted.

Purchases and sales of securities (excluding short-term investments) for the six months ended February 28, 2023, aggregated $4,128,009 and $11,127,019, respectively.

At February 28, 2023, the net unrealized depreciation on investments based on cost for federal tax purposes of $47,389,007 was as follows:

| Aggregate gross unrealized appreciation for all investments in which there is an excess of value over tax cost | $ 277,661 |

| Aggregate gross unrealized depreciation for all investments in which there is an excess of tax cost over value | (6,285,064) |

| Net unrealized depreciation | $(6,007,403) |

The accompanying notes are an integral part of these financial statements.

28Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in the three broad levels below.

| Level 1 | – | unadjusted quoted prices in active markets for identical securities. |

| Level 2 | – | other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risks, etc.). See Notes to Financial Statements — Note 1A. |

| Level 3 | – | significant unobservable inputs (including the Adviser's own assumptions in determining fair value of investments). See Notes to Financial Statements — Note 1A. |

The following is a summary of the inputs used as of February 28, 2023, in valuing the Fund's investments:

| | Level 1 | Level 2 | Level 3 | Total |

| Corporate Bonds | $ — | $39,651,011 | $ — | $39,651,011 |

| Right/Warrant | 3,530 | — | — | 3,530 |

| Insurance-Linked Securities | | | | |

| Collateralized Reinsurance | | | | |

| Multiperil – Worldwide | — | — | 25 | 25 |

| Reinsurance Sidecars | | | | |

| Multiperil – U.S. | — | — | —* | —* |

| Multiperil – Worldwide | — | — | 11,146 | 11,146 |

| Open-End Fund | 1,880,005 | — | — | 1,880,005 |

| Total Investments in Securities | $ 1,883,535 | $ 39,651,011 | $ 11,171 | $ 41,545,717 |

| Other Financial Instruments | | | | |

| Swap contracts, at value | $ — | $ (164,113) | $ — | $ (164,113) |

| Total Other Financial Instruments | $ — | $ (164,113) | $ — | $ (164,113) |

| * | Securities valued at $0. |

During the period ended February 28, 2023, there were no significant transfers in or out of Level 3.

The accompanying notes are an integral part of these financial statements.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2329

Statement of Assets and Liabilities | 2/28/23 (unaudited)

| ASSETS: | |

| Investments in unaffiliated issuers, at value (cost $47,393,338) | $ 41,545,717 |

| Swaps collateral | 561,723 |

| Variation margin for centrally cleared swap contracts | 11,784 |

| Receivables — | |

| Fund shares sold | 42,513 |

| Interest | 679,020 |

| Due from the Adviser | 7,041 |

| Other assets | 25,390 |

| Total assets | $ 42,873,188 |

| LIABILITIES: | |

| Overdraft due to custodian | $ 11,784 |

| Payables — | |

| Investment securities purchased | 545,000 |

| Fund shares repurchased | 170,357 |

| Distributions | 7,927 |

| Trustees' fees | 1,352 |

| Professional fees | 63,439 |

| Swap contracts, at value (net premiums paid $198,356) | 164,113 |

| Management fees | 2,861 |

| Administrative expenses | 4,032 |

| Distribution fees | 863 |

| Accrued expenses | 20,514 |

| Total liabilities | $ 992,242 |

| NET ASSETS: | |

| Paid-in capital | $113,742,099 |

| Distributable earnings (loss) | (71,861,153) |

| Net assets | $ 41,880,946 |

| NET ASSET VALUE PER SHARE: | |

| No par value (unlimited number of shares authorized) | |

| Class A (based on $16,624,275/2,120,729 shares) | $ 7.84 |

| Class C (based on $2,164,903/278,220 shares) | $ 7.78 |

| Class Y (based on $23,091,768/2,930,665 shares) | $ 7.88 |

| MAXIMUM OFFERING PRICE PER SHARE: | |

| Class A (based on $7.84 net asset value per share/100%-4.50% maximum sales charge) | $ 8.21 |

The accompanying notes are an integral part of these financial statements.

30Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

Statement of Operations (unaudited)

FOR THE SIX MONTHS ENDED 2/28/23

| INVESTMENT INCOME: | | |

| Interest from unaffiliated issuers | $ 1,603,301 | |

| Dividends from unaffiliated issuers | 28,352 | |

| Total Investment Income | | $ 1,631,653 |

| EXPENSES: | | |

| Management fees | $ 113,951 | |

| Administrative expenses | 12,929 | |

| Transfer agent fees | | |

| Class A | 4,781 | |

| Class C | 586 | |

| Class Y | 10,450 | |

| Distribution fees | | |

| Class A | 21,882 | |

| Class C | 12,106 | |

| Shareowner communications expense | 4,155 | |

| Consulting fees | 12,167 | |

| Custodian fees | 93 | |

| Registration fees | 17,457 | |

| Professional fees | 70,700 | |

| Printing expense | 16,893 | |

| Officers' and Trustees' fees | 4,190 | |

| Miscellaneous | 12,263 | |

| Total expenses | | $ 314,603 |

| Less fees waived and expenses reimbursed by the Adviser | | (138,897) |

| Net expenses | | $ 175,706 |

| Net investment income | | $ 1,455,947 |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | | |

| Net realized gain (loss) on: | | |

| Investments in unaffiliated issuers | $(1,188,543) | |

| Swap contracts | 6,697 | |

| Other assets and liabilities denominated in foreign currencies | (6,637) | $(1,188,483) |

| Change in net unrealized appreciation (depreciation) on: | | |

| Investments in unaffiliated issuers | $ 603,682 | |

| Swap contracts | (415,529) | |

| Other assets and liabilities denominated in foreign currencies | 4,804 | $ 192,957 |

| Net realized and unrealized gain (loss) on investments | | $ (995,526) |

| Net increase in net assets resulting from operations | | $ 460,421 |

The accompanying notes are an integral part of these financial statements.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2331

Statements of Changes in Net Assets

| | Six Months

Ended

2/28/23

(unaudited) | Year

Ended

8/31/22 |

| FROM OPERATIONS: | | |

| Net investment income (loss) | $ 1,455,947 | $ 3,170,042 |

| Net realized gain (loss) on investments | (1,188,483) | (954,202) |

| Change in net unrealized appreciation (depreciation) on investments | 192,957 | (7,935,454) |

| Net increase (decrease) in net assets resulting from operations | $ 460,421 | $ (5,719,614) |

| DISTRIBUTIONS TO SHAREOWNERS: | | |

| Class A ($0.22 and $0.39 per share, respectively) | $ (496,257) | $ (943,019) |

| Class C ($0.19 and $0.32 per share, respectively) | (59,422) | (181,668) |

| Class Y ($0.23 and $0.42 per share, respectively) | (765,877) | (1,626,083) |

| Total distributions to shareowners | $ (1,321,556) | $ (2,750,770) |

| FROM FUND SHARE TRANSACTIONS: | | |

| Net proceeds from sales of shares | $ 1,787,839 | $ 6,870,247 |

| Reinvestment of distributions | 1,267,847 | 2,631,093 |

| Cost of shares repurchased | (10,283,319) | (21,481,429) |

| Net decrease in net assets resulting from Fund share transactions | $ (7,227,633) | $(11,980,089) |

| Net decrease in net assets | $ (8,088,768) | $ (20,450,473) |

| NET ASSETS: | | |

| Beginning of period | $ 49,969,714 | $ 70,420,187 |

| End of period | $ 41,880,946 | $ 49,969,714 |

The accompanying notes are an integral part of these financial statements.

32Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

| | Six Months

Ended

2/28/23

Shares

(unaudited) | Six Months

Ended

2/28/23

Amount

(unaudited) | Year

Ended

8/31/22

Shares | Year

Ended

8/31/22

Amount |

| Class A | | | | |

| Shares sold | 158,736 | $ 1,240,647 | 457,441 | $ 3,975,150 |

| Reinvestment of distributions | 59,800 | 465,456 | 102,547 | 879,915 |

| Less shares repurchased | (451,942) | (3,544,092) | (739,675) | (6,423,136) |

| Net decrease | (233,406) | $(1,837,989) | (179,687) | $ (1,568,071) |

| Class C | | | | |

| Shares sold | 4,054 | $ 31,871 | 15,041 | $ 134,079 |

| Reinvestment of distributions | 6,496 | 50,141 | 18,863 | 162,521 |

| Less shares repurchased | (119,035) | (923,897) | (404,270) | (3,491,003) |

| Net decrease | (108,485) | $ (841,885) | (370,366) | $ (3,194,403) |

| Class Y | | | | |

| Shares sold | 65,419 | $ 515,321 | 313,756 | $ 2,761,018 |

| Reinvestment of distributions | 96,174 | 752,250 | 183,733 | 1,588,657 |

| Less shares repurchased | (742,258) | (5,815,330) | (1,313,540) | (11,567,290) |

| Net decrease | (580,665) | $(4,547,759) | (816,051) | $ (7,217,615) |

The accompanying notes are an integral part of these financial statements.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2333

| | Six Months

Ended

2/28/23

(unaudited) | Year

Ended

8/31/22 | Year

Ended

8/31/21* | Year

Ended

8/31/20* | Year

Ended

8/31/19* | Year

Ended

8/31/18* |

| Class A | | | | | | |

| Net asset value, beginning of period | $ 7.97 | $ 9.22 | $ 8.78 | $ 9.06 | $ 8.90 | $ 9.13 |

| Increase (decrease) from investment operations: | | | | | | |

| Net investment income (loss) (a) | $ 0.24 | $ 0.45 | $ 0.46 | $ 0.46 | $ 0.45 | $ 0.42 |

| Net realized and unrealized gain (loss) on investments | (0.15) | (1.31) | 0.44 | (0.27) | 0.16 | (0.20) |

| Net increase (decrease) from investment operations | $ 0.09 | $ (0.86) | $ 0.90 | $ 0.19 | $ 0.61 | $ 0.22 |

| Distributions to shareowners: | | | | | | |

| Net investment income | $ (0.22) | $ (0.39) | $ (0.30) | $ (0.47) | $ (0.45) | $ (0.41) |

| Net realized gain | — | — | — | — | — | (0.04) |

| Tax return of capital | — | — | (0.16) | — | — | — |

| Total distributions | $ (0.22) | $ (0.39) | $ (0.46) | $ (0.47) | $ (0.45) | $ (0.45) |

| Net increase (decrease) in net asset value | $ (0.13) | $ (1.25) | $ 0.44 | $ (0.28) | $ 0.16 | $ (0.23) |

| Net asset value, end of period | $ 7.84 | $ 7.97 | $ 9.22 | $ 8.78 | $ 9.06 | $ 8.90 |

| Total return (b) | 1.18%(c) | (9.54)% | 10.45% | 2.25% | 7.13% | 2.60% |

| Ratio of net expenses to average net assets | 0.90%(d) | 0.90% | 0.90% | 0.93% | 1.00% | 1.01% |

| Ratio of net investment income (loss) to average net assets | 6.26%(d) | 5.20% | 5.05% | 5.27% | 5.10% | 4.68% |

| Portfolio turnover rate | 10%(c) | 33% | 83% | 92% | 60% | 114% |

| Net assets, end of period (in thousands) | $16,624 | $18,769 | $23,369 | $9,052 | $8,374 | $8,009 |

| Ratios with no waiver of fees and assumption of expenses by the Adviser and no reduction for fees paid indirectly: | | | | | | |

| Total expenses to average net assets | 1.47%(d) | 1.30% | 1.40% | 2.03% | 2.12% | 1.91% |

| Net investment income (loss) to average net assets | 5.69%(d) | 4.80% | 4.55% | 4.17% | 3.98% | 3.78% |

| * | The Fund acquired the assets and liabilities of Pioneer Corporate High Yield Fund (the “Predecessor Fund”) on September 25, 2020 (the “Reorganization”). As a result of the Reorganization, the Predecessor Fund’s performance and financial history became the performance and financial history of the Fund. Historical per-share amounts prior to September 25, 2020 have been adjusted to reflect the exchange ratio used to align the net asset values of the Predecessor Fund with those of the Fund. See Notes to Financial Statements — Note 8. |

| (a) | The per-share data presented above is based on the average shares outstanding for the period presented. |

| (b) | Assumes initial investment at net asset value at the beginning of each period, reinvestment of all distributions, the complete redemption of the investment at net asset value at the end of each period and no sales charges. Total return would be reduced if sales charges were taken into account. |

| (c) | Not annualized. |

| (d) | Annualized. |

The accompanying notes are an integral part of these financial statements.

34Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/23

| | Six Months

Ended

2/28/23

(unaudited) | Year

Ended

8/31/22 | Year

Ended

8/31/21* | Year

Ended

8/31/20* | Year

Ended

8/31/19* | Year

Ended

8/31/18* |

| Class C | | | | | | |

| Net asset value, beginning of period | $ 7.92 | $ 9.17 | $ 8.73 | $ 8.94 | $ 8.79 | $ 9.01 |

| Increase (decrease) from investment operations: | | | | | | |

| Net investment income (loss) (a) | $ 0.21 | $ 0.37 | $ 0.39 | $ 0.41 | $ 0.38 | $ 0.35 |

| Net realized and unrealized gain (loss) on investments | (0.16) | (1.30) | 0.44 | (0.21) | 0.15 | (0.19) |

| Net increase (decrease) from investment operations | $ 0.05 | $ (0.93) | $ 0.83 | $ 0.20 | $ 0.53 | $ 0.16 |

| Distributions to shareowners: | | | | | | |

| Net investment income | $ (0.19) | $ (0.32) | $ (0.24) | $ (0.41) | $ (0.38) | $ (0.34) |

| Net realized gain | — | — | — | — | — | (0.04) |

| Tax return of capital | — | — | (0.15) | — | — | — |

| Total distributions | $ (0.19) | $ (0.32) | $ (0.39) | $(0.41) | $ (0.38) | $ (0.38) |

| Net increase (decrease) in net asset value | $ (0.14) | $ (1.25) | $ 0.44 | $(0.21) | $ 0.15 | $ (0.22) |

| Net asset value, end of period | $ 7.78 | $ 7.92 | $ 9.17 | $ 8.73 | $ 8.94 | $ 8.79 |

| Total return (b) | 0.66%(c) | (10.30)% | 9.64% | 2.30% | 6.34% | 1.84% |

| Ratio of net expenses to average net assets | 1.65%(d) | 1.65% | 1.65% | 1.50% | 1.75% | 1.75% |

| Ratio of net investment income (loss) to average net assets | 5.50%(d) | 4.29% | 4.35% | 4.67% | 4.35% | 3.94% |

| Portfolio turnover rate | 10%(c) | 33% | 83% | 92% | 60% | 114% |

| Net assets, end of period (in thousands) | $2,165 | $ 3,061 | $6,940 | $ 853 | $4,089 | $3,983 |

| Ratios with no waiver of fees and assumption of expenses by the Adviser and no reduction for fees paid indirectly: | | | | | | |

| Total expenses to average net assets | 2.22%(d) | 2.06% | 2.14% | 2.58% | 2.87% | 2.65% |

| Net investment income (loss) to average net assets | 4.93%(d) | 3.88% | 3.86% | 3.59% | 3.23% | 3.04% |

| * | The Fund acquired the assets and liabilities of Pioneer Corporate High Yield Fund (the “Predecessor Fund”) on September 25, 2020 (the “Reorganization”). As a result of the Reorganization, the Predecessor Fund’s performance and financial history became the performance and financial history of the Fund. Historical per-share amounts prior to September 25, 2020 have been adjusted to reflect the exchange ratio used to align the net asset values of the Predecessor Fund with those of the Fund. See Notes to Financial Statements — Note 8. |

| (a) | The per-share data presented above is based on the average shares outstanding for the period presented. |

| (b) | Assumes initial investment at net asset value at the beginning of each period, reinvestment of all distributions, the complete redemption of the investment at net asset value at the end of each period and no sales charges. Total return would be reduced if sales charges were taken into account. |

| (c) | Not annualized. |

| (d) | Annualized. |

The accompanying notes are an integral part of these financial statements.

Pioneer Corporate High Yield Fund | Semiannual Report | 2/28/2335

Financial Highlights (continued)

| | Six Months

Ended

2/28/23

(unaudited) | Year

Ended

8/31/22 | Year

Ended

8/31/21* | Year

Ended

8/31/20* | Year

Ended

8/31/19* | Year

Ended

8/31/18* |

| Class Y | | | | | | |

| Net asset value, beginning of period | $ 8.01 | $ 9.27 | $ 8.82 | $ 9.11 | $ 8.95 | $ 9.17 |

| Increase (decrease) from investment operations: | | | | | | |

| Net investment income (loss) (a) | $ 0.26 | $ 0.48 | $ 0.49 | $ 0.48 | $ 0.48 | $ 0.45 |

| Net realized and unrealized gain (loss) on investments | (0.16) | (1.32) | 0.45 | (0.27) | 0.16 | (0.20) |

| Net increase (decrease) from investment operations | $ 0.10 | $ (0.84) | $ 0.94 | $ 0.21 | $ 0.64 | $ 0.25 |

| Distributions to shareowners: | | | | | | |

| Net investment income | $ (0.23) | $ (0.42) | $ (0.33) | $ (0.50) | $ (0.48) | $ (0.43) |

| Net realized gain | — | — | — | — | — | (0.04) |

| Tax return of capital | — | — | (0.16) | — | — | — |

| Total distributions | $ (0.23) | $ (0.42) | $ (0.49) | $ (0.50) | $ (0.48) | $ (0.47) |

| Net increase (decrease) in net asset value | $ (0.13) | $ (1.26) | $ 0.45 | $ (0.29) | $ 0.16 | $ (0.22) |

| Net asset value, end of period | $ 7.88 | $ 8.01 | $ 9.27 | $ 8.82 | $ 9.11 | $ 8.95 |

| Total return (b) | 1.34%(c) | (9.31)% | 10.80% | 2.53% | 7.41% | 2.86% |

| Ratio of net expenses to average net assets | 0.60%(d) | 0.60% | 0.60% | 0.63% | 0.75% | 0.75% |

| Ratio of net investment income (loss) to average net assets | 6.56%(d) | 5.47% | 5.40% | 5.58% | 5.35% | 4.94% |

| Portfolio turnover rate | 10%(c) | 33% | 83% | 92% | 60% | 114% |

| Net assets, end of period (in thousands) | $23,092 | $28,139 | $40,111 | $12,934 | $8,163 | $8,021 |