UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-21120 |

| Conestoga Funds |

| (Exact name of registrant as specified in charter) |

| 550 E. Swedesford Road, Suite 120 Wayne, PA | 19087 |

| (Address of principal executive offices) | (Zip code) |

| Conestoga Capital Advisors 550 E. Swedesford Road, Suite 120 Wayne, PA 19087 |

| (Name and address of agent for service) |

| With Copy To: |

| Josh Deringer, Esq. |

| Faegre Drinker Biddle & Reath LLP |

| One Logan Square, Suite 2000 |

| Philadelphia, PA 19103 |

| Registrant’s telephone number, including area code: | (800) 320-7790 |

| Date of fiscal year end: | September 30 | |

| Date of reporting period: | September 30, 2023 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles. A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public.

A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| (a) |

Conestoga Funds

SMALL CAP FUND

SMID CAP FUND

MID CAP FUND

DISCOVERY FUND

M a n a g e d B y

ANNUAL REPORT

September 30, 2023

The Securities and Exchange Commission (the “SEC”) has adopted new regulations that will result in changes to the design and delivery of annual and semi-annual shareholder reports. Beginning in July 2024, the Funds will be required by the SEC to send shareholders a paper copy of a new tailored shareholder report in place of the full shareholder report that you are now receiving. If you would like to receive shareholder reports and other communications from the Funds electronically instead of by mail, you may make that request at any time by contacting your financial intermediary or at 1-800-494-2755.

CONESTOGA FUNDS | November 28, 2023 |

Dear Fellow Shareholders,

I am pleased to provide you with our Conestoga Funds 2023 Annual Report. Equity markets mostly rebounded over the Funds’ fiscal year ended September 30, 2023 after declining significantly in the Funds’ prior fiscal year. The rally by U.S. equity markets has been led by larger capitalization stocks, and as our Portfolio Managers describe in their letter to shareholders, there has been a linear relationship between capitalization and performance.

We are excited to announce that Ted Chang has been promoted to Partner. Ted joined Conestoga Capital Advisors, LLC (“Conestoga”) in June 2020 and serves as Co-Portfolio Manager for the firm’s Mid Cap Growth strategy and the Conestoga Mid Cap Fund, as well as a Research Analyst across all of the firm’s investment strategies. With the addition of Ted, as well as Christina Kowalski as Partners earlier this year, Conestoga’s ownership now includes 14 of our 16 employees. Ted and Christina’s purchases from our retired partner Bill Martindale’s family trust effectively complete the ownership transition from Bill.

As of September 30, 2023, Conestoga’s total assets were approximately $6.9 billion. Net assets within each of the Funds were as follows:

Small Cap Fund: | $3.5 billion | SMid Cap Fund: | $383 million |

Discovery Fund: | $2 million | Mid Cap Fund: | $2 million |

Flows to the Funds have been generally positive over the fiscal year. The Small Cap Fund has experienced modest net inflows of just over $50 million and remains in soft close. The Small Cap Fund is only available to shareholders and advisors with current investments in the Small Cap Fund. The SMid Cap Fund received net inflows of $14 million over the fiscal year. Our newest Funds, the Discovery Fund and Mid Cap Fund, experienced small inflows over the fiscal year.

We thank you for your investment in the Conestoga Funds, it is greatly appreciated.

Sincerely,

Robert M. Mitchell.

Robert M. Mitchell

Chairman and Chief Executive Officer

1

CONESTOGA FUNDS | November 28, 2023 |

Dear Fellow Shareholders,

The optimism that pushed equity markets higher in the fourth quarter of 2022 and first two quarters of 2023 faded through the summer. Major equity indices moved lower during the third quarter of 2023 as investors’ sanguine outlook for an economic soft landing and a “goldilocks” stock market was cooled by concerns that interest rates would stay higher for longer. After raising the Federal Funds rate eleven times and over 5% since 2021, the Federal Reserve elected to keep rates unchanged in their September 2023 meeting, while also communicating they expect to raise rates once more before the end of the year. Meanwhile, inflation pressures eased modestly, but are still well above the central bank’s target of 2%. Gross domestic product was reported at 2.1% for the second quarter of 2023 and unemployment remained under 4%. More forecasters have increased their expectations for a recession in 2024 as higher borrowing costs take a toll on interest rate sensitive industries and consumers.

Large capitalization stocks have outperformed small capitalization stocks for four consecutive quarters. We note here that our 2022 letter highlighted our expectations for a new cycle of small cap outperformance after twelve years of underperformance relative to large caps – clearly that forecast has proven early at this point. That said, we observe that virtually all of the relative outperformance of the S&P 500 Index relative to the Russell 2000 Index is due to the outsized contribution of the mega capitalization technology stocks known as the “Magnificent Seven”. These stocks – Alphabet Inc. (GOOG), Amazon.com Inc. (AMZN), Apple Inc. (AAPL), Meta Platforms Inc. (META), Microsoft Inc. (MSFT), Nvidia Corp. (NVDA), and Tesla Inc. (TSLA) – have surged an average of over 50% in 2023 while the remaining 493 stocks in the S&P 500 Index have underperformed the Russell 2000 Index year-to-date. The valuation of small caps relative to large caps has become more appealing in our opinion, and we stand by our expectations for a new small cap cycle in the years to come.

SMALL CAP FUND PERFORMANCE REVIEW

For the twelve months ended September 30, 2023, the Conestoga Small Cap Fund (the “Small Cap Fund”) (Investors Class Shares) outperformed the Russell 2000 Growth Index. The Small Cap Fund returned 16.33% versus the Russell 2000 Growth Index return of 9.59%. A combination of positive stock selection and sector allocation effects were the primary drivers of excess return.

Stock selection was most positive in the Health Care, Industrials and Consumer Discretionary sectors. Within Health Care, our positions in Stevanato Group S.p.A. (STVN) and Vericel Corp. (VCEL), each added to relative return. Performance in the sector was also aided by the large underweight to the underperforming biotechnology and pharmaceuticals industries. The Industrials sector was another area with strong stock selection with our high conviction positions in Simpson Manufacturing, Inc. (SSD), Axon Enterprise, Inc. (AXON), and AAON, Inc. (AAON) leading the way.

2

In the Consumer Discretionary sector, SiteOne Landscape Supply Inc. (SITE) and Fox Factory Holding Corp. (FOXF) both contributed to positive stock selection effects. Each name saw their revenues and earnings grow during the pandemic as consumers spent more on home improvement (landscaping, which boosted SITE) and outdoor leisure activities (biking, which benefited FOXF). Each stock moved lower as the economy exited the pandemic era in 2022, but both stocks have recovered as their earnings growth has exhibited more durability than expected.

Stock selection was weakest in the Technology sector, led by a decline in Model N, Inc. (MODN). The company has given back some of its 2022 gains during the first half of 2023. MODN reported robust financial results, but the stock sold off. We believe the sell-off was related to profit taking and/or future guidance not being raised more aggressively.

SMID CAP FUND PERFORMANCE REVIEW

The Conestoga SMid Cap Fund (the “SMid Cap Fund”) (Investors Class Shares) returned 16.59% over the twelve months ended September 30, 2023. This outperformed the Russell 2500 Growth Index return of 10.61%. Stock selection and sector allocation were both additive to relative returns. Stock selection was especially strong in the Health Care and Industrials sectors, while the Technology sector was the biggest laggard.

Stock selection was most positive in the Health Care sector with our positions in West Pharmaceutical Services, Inc. (WST), and Stevanato Group S.p.A. (STVN), adding the most value. Performance in the sector was also aided by the large underweight to the underperforming biotechnology and pharmaceuticals industries.

The Industrials sector was another bright spot for the portfolio with our positions in Fair Isaac Corp. (FICO), Axon Enterprise, Inc. (AXON), Watsco, Inc. (WSO), and Simpson Manufacturing Co. (SSD) all contributing more than 100 bps to return.

An underweight to Financials generated positive sector allocation effects, particularly the SMid Cap Fund’s lack of exposure to the banking industry, which suffered severe losses over the twelve months ended September 30, 2023. Our sole position in this sector, Clearwater Analytics Holdings Inc. Class A (CWAN), added positive stock selection effects as well.

Stock selection was weakest in the Technology sector. Our holdings in Definitive Healthcare Corp. (DH), Paycor HCM (PYCR), and Five9, Inc. (FIVN) were the largest drags on relative performance. The portfolio’s lack of exposure to the Consumer Staples sector (the best performing sector in the index over the last twelve months) was also a headwind.

MID CAP FUND PERFORMANCE REVIEW

The Conestoga Mid Cap Fund (the “Mid Cap Fund”) (Investors Class Shares) advanced 16.24% over the twelve months ended September 30, 2023. This trailed the Russell Midcap Growth Index return of 17.47%. Stock selection effects were mixed with strong results in the Health Care sector, being offset by subpar returns in the Industrials sector. Sector allocation effects were modestly negative.

Stock selection was most positive in the Health Care sector with positions in West Pharmaceutical Services, Inc. (WST), Align Technology, Inc. (ALGN), and IDEXX Laboratories, Inc. (IDXX) providing the most benefit. WST was up over 50% during the

3

twelve months ended September 30, 2023 and has put to rest fears that COVID revenue declines would hamper financial results. Management has talked about strength in the core business offsetting COVID declines and this was exhibited with strong revenue growth. Long-time holding ALGN bounced back from a drop in demand for their elective/non-essential offerings during the pandemic and rewarded investors with a 47% return for the fiscal year ended September 30, 2023. IDXX continues to gain share value and has seen labor trends as well as overall veterinary capacity return to pre-pandemic levels.

The Mid Cap Fund’s lack of exposure to the Energy sector also provided a boost to relative returns. We are typically underweight in this area of the market given its slower growth and dependence on underlying commodity prices. After rising more than 40% and being the best performing sector in fiscal year 2022, the sector was one of only three that had negative returns in 2023. In addition, the Basic Materials sector was the worst performing sector in the Russell Midcap Growth Index and our continued underweight to these companies benefited performance.

Losses in the Industrials sector were broad-based with eight of our twelve positions detracting from relative results. Jack Henry & Associates, Inc. (JKHY), Mettler-Toledo International, Inc. (MTD), and Generac Holdings, Inc. (GNRC) were the biggest laggards. JKHY shares declined after lowering its full year revenue guidance to reflect slowing consumer spending and concerns that financial technology companies would be negatively impacted by the collapse of Silicon Valley Bank and others. MTD was pressured by continued de-stocking of pipette tips in the Biotech and Pharmaceutical end markets. GNRC has been negatively impacted by the lack of installers for its residential home standby generators and a large bankruptcy from a reseller in its solar division.

Our large underweight to the stronger performing Financials sector proved a headwind for relative performance during the fiscal year ended September 30, 2023, as did our overweight to the weaker performing Utilities sector. The Mid Cap Fund holds one position in each of these sectors: FactSet Research Systems Inc. (FDS) within Financials, and Waste Connections Inc. (WCN) within Utilities.

DISCOVERY FUND PERFORMANCE REVIEW

The Conestoga Discovery Fund (the “Discovery Fund”) (Investors Class Shares) underperformed the Russell Microcap Growth Index over the Fund’s fiscal year ended September 30, 2023. The Discovery Fund declined -10.35% versus the Russell Microcap Growth Index decline of -3.10%. Most of the underperformance can be attributed to negative stock selection while positive sector allocation effects proved slightly additive to the portfolio. Stock selection was most positive in the Technology and Telecommunications sectors but was not enough to overcome negative returns in the Health Care, Financials, and Industrials sectors.

The Technology sector provided significant positive stock selection effects, led by the Discovery Fund’s positions in UserTesting, Inc. (USER), and PROS Holdings, Inc. (PRO). After being one of the Discovery Fund’s biggest laggards in fiscal year 2022, USER was acquired by a private equity consortium led by Thoma Bravo and was the largest contributor to relative returns in 2023. The acquisition price represented a 90% premium

4

to the unaffected share price. PRO shares traded higher after outlining its three-year targets for revenue growth and free cash flow margins, both of which were well received by investors.

The Discovery Fund was also a beneficiary of its lack of exposure to the poorly performing Consumer Staples sector which was down over 30% during the twelve months ended September 30, 2023. These types of companies typically lack the type of growth profile and competitive advantages we seek when constructing the portfolio.

Stock selection within Health Care proved to be most challenging during the fiscal year ended September 30, 2023. Losses were broad-based with eight of eleven positions detracting from relative performance. Nanostring Technologies Inc., (NTSG) traded lower after a German court issued an injunction on sales of their CosMx product line from a suit filed by competitor 10X Genomics. This introduced uneasiness that a U.S. filed petition could lead to a similar outcome. BioLife Solutions, Inc., (BLFS), fell due to a lower-than-expected contribution from its Freezer and Thaw Systems platform. The miss reflected supply-chain issues that delayed shipment of several cryogenic freezer orders. OrthoPediatrics Corp. (KIDS) and Semler Scientific, Inc. (SMLR) were two other names in the Health Care space that were a significant drag on results.

Financials is an area where the portfolio is typically underweight due to its lack of consistent growth and differentiation. However, the Discovery Fund’s lone position in the sector, Palomar Holdings, Inc. (PLMR) was one of the Discovery Fund’s biggest laggards during the twelve months ended September 30, 2023. The company experienced higher attritional losses due to the magnitude of damage caused by Hurricane Ian in Florida. Shares were also pressured by comments by the California Earthquake Authority (CEA) that reinsurance coverage was both more expensive and more difficult to find.

Industrials was another difficult sector for the Discovery Fund throughout the fiscal year ended September 30, 2023 with our positions in SoundThinking, Inc. (SSTI) and CryoPort, Inc. (CYRX) leading the way lower.

OUR OUTLOOK

The market rally since its lows in the second half of 2022 has largely been driven by the largest Technology stocks. Large capitalization stocks have outperformed small capitalization stocks, with the S&P 500 Index outperforming the Russell 2000 Index in eight of the last nine quarters. Volatility levels have declined to historically low levels and the market has generally shrugged off the yoke of higher interest rates, inflation, banking sector turmoil, and geopolitics. Expectations of a recession have been deferred to 2024 and some forecasters now believe the economy may actually achieve a soft landing. We believe the market may be due for a pause or retrenchment given its recent strength, narrowness, and low volatility expectations. We still believe small capitalization stocks are attractively valued relative to large capitalization stocks, and we remain optimistic that a new small cap cycle is imminent.

5

On behalf of all the members of Conestoga Capital Advisors, LLC, we thank you for your investment in the Funds.

Sincerely,

Robert M. Mitchell | Joseph F. Monahan |

Managing Partner – Co-Portfolio Manager | Managing Partner – Co-Portfolio Manager |

Small Cap and SMid Cap Funds | Small Cap, SMid Cap and Discovery Funds |

Derek S. Johnston | David R. Neiderer |

Partner – Co-Portfolio Manager | Partner – Co-Portfolio Manager |

SMid Cap and Mid Cap Funds | Discovery Fund |

Ted Chang | |

Co-Portfolio Manager | |

Mid Cap Fund |

6

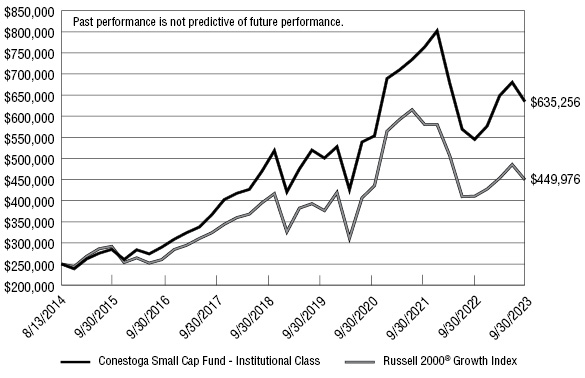

CONESTOGA SMALL CAP FUND - INSTITUTIONAL CLASS |

Comparison of the Change in Value of a $250,000 Investment in

Conestoga Small Cap Fund – Institutional Class (since inception on 08/13/2014)

versus the Russell 2000® Growth Index

Average Annual Total Returns for the Periods Ended September 30, 2023 | |||||

1 Year | 3 Years | 5 Years | Since | ||

Conestoga Small Cap Fund - Institutional Class | 16.54% | 4.70% | 4.15% | 10.75% | |

Russell 2000® Growth Index | 9.59% | 1.09% | 1.55% | 6.65% | |

The Fund’s past performance does not predict its future performance. The graph and table shown above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares but do reflect the reinvestment of all dividends and distributions. The Fund’s benchmark, the Russell 2000® Growth Index, measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000® companies with higher price-to-value ratios and higher forecasted growth values. The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000® Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities in the Russell 3000® Index based on a combination of their market capitalization and current index membership.

7

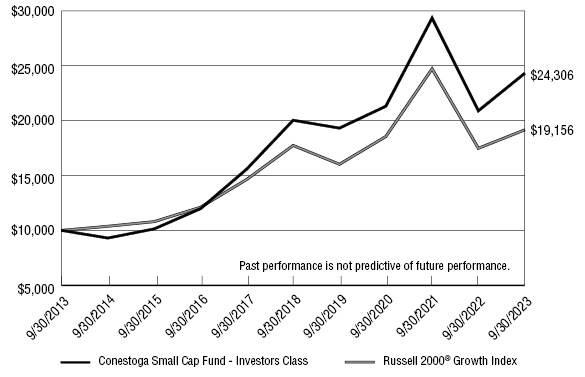

CONESTOGA SMALL CAP FUND - INVESTORS CLASS |

10 Year Comparison of the Change in Value of a $10,000

Investment in Conestoga Small Cap Fund – Investors Class

versus the Russell 2000® Growth Index

Average Annual Total Returns for the Periods Ended September 30, 2023 | |||||||

1 Year | 3 Years | 5 Years | 10 Years | 15 Years | Since | ||

Conestoga Small Cap Fund - Investors Class | 16.33% | 4.49% | 3.94% | 9.29% | 10.97% | 11.00% | |

Russell 2000® Growth Index | 9.59% | 1.09% | 1.55% | 6.72% | 8.82% | 9.60% | |

The Fund’s past performance does not predict its future performance. The graph and table shown above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares but do reflect the reinvestment of all dividends and distributions. The Fund’s benchmark, the Russell 2000® Growth Index, measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000® companies with higher price-to-value ratios and higher forecasted growth values. The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000® Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities in the Russell 3000® Index based on a combination of their market capitalization and current index membership.

8

CONESTOGA SMID CAP FUND - INSTITUTIONAL CLASS |

Comparison of the Change in Value of a $250,000 Investment in

Conestoga SMid Cap Fund – Institutional Class (since inception on 12/15/2014)

versus the Russell 2500® Growth Index

Average Annual Total Returns for the Periods Ended September 30, 2023 | |||||

1 Year | 3 Years | 5 Years | Since | ||

Conestoga SMid Cap Fund - Institutional Class | 16.82% | 2.84% | 4.71% | 10.54% | |

Russell 2500® Growth Index | 10.61% | 1.01% | 4.05% | 8.33% | |

The Fund’s past performance does not predict its future performance. The graph and table shown above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares but do reflect the reinvestment of all dividends and distributions. The Fund’s benchmark, the Russell 2500® Growth Index, measures the performance of the small- to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500® companies with higher growth earnings potential as defined by Russell’s leading style methodology. The Russell 2500® Index measures the performance of the small- to mid-cap segment of the U.S. equity universe, commonly referred to as “smid” cap. The Russell 2500® Index is a subset of the Russell 3000® Index. It includes approximately 2500 of the smallest securities in the Russell 3000® Index based on a combination of their market capitalization and current index membership.

9

CONESTOGA SMID CAP FUND - INVESTORS CLASS |

Comparison of the Change in Value of a $10,000 Investment in

Conestoga SMid Cap Fund – Investors Class (since inception on 01/21/2014)

versus the Russell 2500® Growth Index

Average Annual Total Returns for the Periods Ended September 30, 2023 | |||||

1 Year | 3 Years | 5 Years | Since | ||

Conestoga SMid Cap Fund - Investors Class | 16.59% | 2.58% | 4.46% | 7.99% | |

Russell 2500® Growth Index | 10.61% | 1.01% | 4.05% | 7.60% | |

The Fund’s past performance does not predict its future performance. The graph and table shown above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares but do reflect the reinvestment of all dividends and distributions. The Fund’s benchmark, the Russell 2500® Growth Index, measures the performance of the small- to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500® companies with higher growth earnings potential as defined by Russell’s leading style methodology. The Russell 2500® Index measures the performance of the small- to mid-cap segment of the U.S. equity universe, commonly referred to as “smid” cap. The Russell 2500® Index is a subset of the Russell 3000® Index. It includes approximately 2500 of the smallest securities in the Russell 3000® Index based on a combination of their market capitalization and current index membership.

10

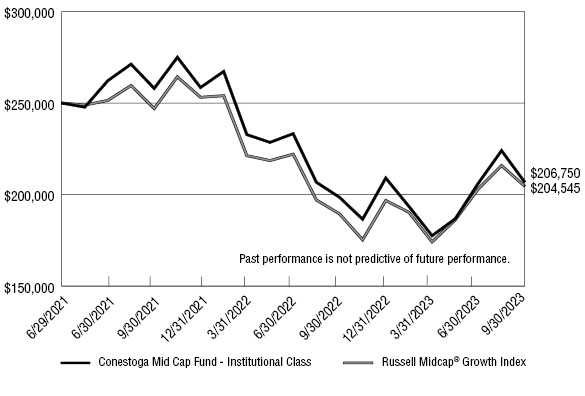

CONESTOGA MID CAP FUND - INSTITUTIONAL CLASS |

Comparison of the Change in Value of a $250,000 Investment in

Conestoga Mid Cap Fund – Institutional Class (since inception on 6/29/2021)

versus the Russell Midcap® Growth Index

Average Annual Total Returns for the Periods Ended September 30, 2023 | |||||

1 Year | Since | ||||

Conestoga Mid Cap Fund - Institutional Class | 16.48% | -8.08% | |||

Russell Midcap® Growth Index | 17.47% | -8.52% | |||

The Fund’s past performance does not predict its future performance. The graph and table shown above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares but do reflect the reinvestment of all dividends and distributions. The Fund’s benchmark, the Russell Midcap® Growth Index, measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell Midcap® Growth Index is constructed to provide a comprehensive and unbiased barometer of the mid-cap growth market. The index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap growth market.

11

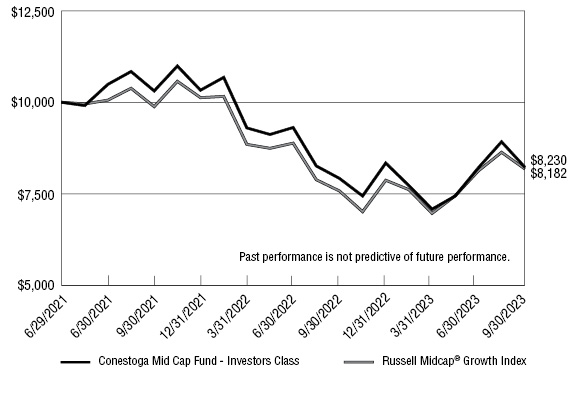

CONESTOGA MID CAP FUND - INVESTORS CLASS |

Comparison of the Change in Value of a $10,000 Investment in

Conestoga Mid Cap Fund – Investors Class (since inception on 6/29/2021)

versus the Russell Midcap® Growth Index

Average Annual Total Returns for the Periods Ended September 30, 2023 | |||||

1 Year | Since | ||||

Conestoga Mid Cap Fund - Investors Class | 16.24% | -8.28% | |||

Russell Midcap® Growth Index | 17.47% | -8.52% | |||

The Fund’s past performance does not predict its future performance. The graph and table shown above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares but do reflect the reinvestment of all dividends and distributions. The Fund’s benchmark, the Russell Midcap® Growth Index, measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell Midcap® Growth Index is constructed to provide a comprehensive and unbiased barometer of the mid-cap growth market. The index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap growth market.

12

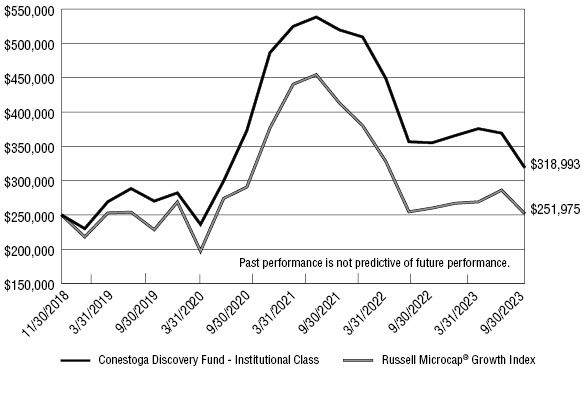

CONESTOGA DISCOVERY FUND - INSTITUTIONAL CLASS |

Comparison of the Change in Value of a $250,000 Investment in

Conestoga Discovery Fund – Institutional Class (since inception on 11/30/2018)

versus the Russell Microcap® Growth Index

Average Annual Total Returns for the Periods Ended September 30, 2023 | ||||

1 Year | 3 Years | Since | ||

Conestoga Discovery Fund - Institutional Class | -10.18% | -5.07% | 5.17% | |

Russell Microcap® Growth Index | -3.10% | -4.65% | 0.16% | |

The Fund commenced operations as a series of Conestoga Funds on December 20, 2021, when all of the assets of Conestoga Micro Cap Fund, LP (the “Predecessor Fund”) transferred to Institutional Class and Investors Class shares of the Fund. The Fund’s investment objectives, policies, guidelines and restrictions are in all material respects equivalent to those of the Predecessor Fund, and the investment adviser and portfolio managers for the Fund are the same as those of the Predecessor Fund. Accordingly, the performance information shown for periods prior to December 20, 2021 is that of the Predecessor Fund. The Predecessor Fund was not registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and thus was not subject to certain investment and operational restrictions that are imposed by the 1940 Act. If the Predecessor Fund had been registered under the 1940 Act, its performance may have been adversely affected. Accordingly, future Fund performance may be different than the Predecessor Fund’s restated past performance. The graph and table shown above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares but do reflect the reinvestment of all dividends and distributions. The Fund’s benchmark, the Russell Microcap® Growth Index, measures the performance of those Russell Microcap® companies with higher price-to-book ratios and higher forecasted growth values.

13

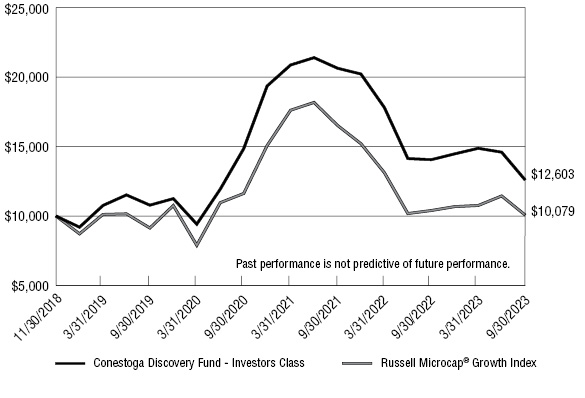

CONESTOGA DISCOVERY FUND - INVESTORS CLASS |

Comparison of the Change in Value of a $10,000 Investment in

Conestoga Discovery Fund – Investors Class (since inception on 11/30/2018)

versus the Russell Microcap® Growth Index

Average Annual Total Returns for the Periods Ended September 30, 2023 | ||||

1 Year | 3 Years | Since | ||

Conestoga Discovery Fund - Investors Class | -10.35% | -5.32% | 4.90% | |

Russell Microcap® Growth Index | -3.10% | -4.65% | 0.16% | |

The Fund commenced operations as a series of Conestoga Funds on December 20, 2021, when all of the assets of Conestoga Micro Cap Fund, LP (the “Predecessor Fund”) transferred to Institutional Class and Investors Class shares of the Fund. The Fund’s investment objectives, policies, guidelines and restrictions are in all material respects equivalent to those of the Predecessor Fund, and the investment adviser and portfolio managers for the Fund are the same as those of the Predecessor Fund. Accordingly, the performance information shown for periods prior to December 20, 2021 is that of the Predecessor Fund. The Predecessor Fund was not registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and thus was not subject to certain investment and operational restrictions that are imposed by the 1940 Act. If the Predecessor Fund had been registered under the 1940 Act, its performance may have been adversely affected. Accordingly, future Fund performance may be different than the Predecessor Fund’s restated past performance. The graph and table shown above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares but do reflect the reinvestment of all dividends and distributions. The Fund’s benchmark, the Russell Microcap® Growth Index, measures the performance of those Russell Microcap® companies with higher price-to-book ratios and higher forecasted growth values.

14

CONESTOGA SMALL CAP FUND |

Diversification*

(% of Net Assets)

Top Ten Equity Holdings

Security Description | % of Net Assets | |

SPS Commerce, Inc. | 4.6% | |

Casella Waste Systems, Inc. - Class A | 3.9% | |

Descartes Systems Group, Inc. (The) | 3.8% | |

AAON, Inc. | 3.8% | |

Simpson Manufacturing Company, Inc. | 3.7% | |

Exponent, Inc. | 3.6% | |

FirstService Corporation | 3.2% | |

Novanta, Inc. | 3.2% | |

SiteOne Landscape Supply, Inc. | 3.2% | |

Altair Engineering, Inc. - Class A | 2.7% |

* | Industry categories represent the industry assigned at the time of purchase. See Note 7 of the Notes to Financial Statements. |

15

CONESTOGA SMALL CAP FUND | ||||||||

COMMON STOCKS — 94.9% | Shares | Value | ||||||

Basic Materials — 5.6% | ||||||||

Metal Fabricating — 3.2% | ||||||||

Omega Flex, Inc. | 226,754 | $ | 17,852,342 | |||||

RBC Bearings, Inc. (a) | 407,675 | 95,448,948 | ||||||

| 113,301,290 | ||||||||

Specialty Chemicals — 2.4% | ||||||||

Balchem Corporation | 670,560 | 83,176,262 | ||||||

Consumer Discretionary — 5.4% | ||||||||

Home Improvement Retailers — 3.2% | ||||||||

SiteOne Landscape Supply, Inc. (a) | 674,330 | 110,219,239 | ||||||

Recreational Products — 2.2% | ||||||||

Fox Factory Holding Corporation (a) | 790,888 | 78,361,183 | ||||||

Consumer Staples — 1.3% | ||||||||

Nondurable Household Products — 1.3% | ||||||||

WD-40 Company | 222,351 | 45,190,617 | ||||||

Financials — 2.1% | ||||||||

Financial Data Providers — 2.1% | ||||||||

Clearwater Analytics Holdings, Inc. - Class A (a) | 3,837,363 | 74,214,600 | ||||||

Health Care — 12.9% | ||||||||

Biotechnology — 1.4% | ||||||||

Vericel Corporation (a) | 1,474,900 | 49,438,648 | ||||||

Health Care Management Services — 0.7% | ||||||||

National Research Corporation | 553,399 | 24,554,314 | ||||||

Medical Equipment — 6.4% | ||||||||

LeMaitre Vascular, Inc. (b) | 1,350,696 | 73,585,918 | ||||||

Merit Medical Systems, Inc. (a) | 1,265,295 | 87,330,661 | ||||||

Repligen Corporation (a) | 390,810 | 62,142,698 | ||||||

| 223,059,277 | ||||||||

Medical Supplies — 4.4% | ||||||||

Neogen Corporation (a) | 3,922,816 | 72,729,009 | ||||||

Stevanato Group S.p.A. (b) | 2,767,677 | 82,255,360 | ||||||

| 154,984,369 | ||||||||

16

CONESTOGA SMALL CAP FUND | ||||||||

COMMON STOCKS — 94.9% (Continued) | Shares | Value | ||||||

Industrials — 31.2% | ||||||||

Building Materials: Other — 5.5% | ||||||||

Simpson Manufacturing Company, Inc. | 856,790 | $ | 128,355,710 | |||||

Trex Company, Inc. (a) | 1,053,485 | 64,926,281 | ||||||

| 193,281,991 | ||||||||

Building: Climate Control — 3.8% | ||||||||

AAON, Inc. | 2,325,237 | 132,236,228 | ||||||

Commercial Vehicles and Parts — 1.6% | ||||||||

Federal Signal Corporation | 934,350 | 55,808,725 | ||||||

Construction — 2.7% | ||||||||

Construction Partners, Inc. - Class A (a)(b) | 2,616,607 | 95,663,152 | ||||||

Defense — 3.0% | ||||||||

Axon Enterprise, Inc. (a) | 306,240 | 60,938,698 | ||||||

Mercury Systems, Inc. (a) | 1,132,183 | 41,992,667 | ||||||

| 102,931,365 | ||||||||

Diversified Industrials — 2.8% | ||||||||

CSW Industrials, Inc. | 130,715 | 22,906,497 | ||||||

ESCO Technologies, Inc. | 716,430 | 74,823,949 | ||||||

| 97,730,446 | ||||||||

Electronic Equipment: Control & Filter — 2.1% | ||||||||

Helios Technologies, Inc. | 1,320,632 | 73,268,663 | ||||||

Electronic Equipment: Gauges & Meters — 2.5% | ||||||||

Mesa Laboratories, Inc. (b) | 350,206 | 36,796,144 | ||||||

Transcat, Inc. (a)(b) | 525,824 | 51,514,977 | ||||||

| 88,311,121 | ||||||||

Engineering & Contracting Services — 3.6% | ||||||||

Exponent, Inc. | 1,468,105 | 125,669,788 | ||||||

Industrial Suppliers — 1.0% | ||||||||

Hillman Solutions Corporation (a) | 4,020,387 | 33,168,193 | ||||||

Machinery: Construction & Handling — 1.0% | ||||||||

Douglas Dynamics, Inc. (b) | 1,172,834 | 35,396,130 | ||||||

Machinery: Industrial — 1.6% | ||||||||

John Bean Technologies Corporation | 536,430 | 56,400,250 | ||||||

17

CONESTOGA SMALL CAP FUND | ||||||||

COMMON STOCKS — 94.9% (Continued) | Shares | Value | ||||||

Real Estate — 3.2% | ||||||||

Real Estate Services — 3.2% | ||||||||

FirstService Corporation | 777,235 | $ | 113,118,782 | |||||

Technology — 27.7% | ||||||||

Computer Services — 1.6% | ||||||||

Workiva, Inc. (a) | 568,085 | 57,569,734 | ||||||

Consumer Digital Services — 0.6% | ||||||||

Definitive Healthcare Corporation - Class A (a) | 2,445,323 | 19,538,131 | ||||||

Production Technology Equipment — 4.2% | ||||||||

Azenta, Inc. (a) | 733,425 | 36,810,601 | ||||||

Novanta, Inc. (a) | 768,865 | 110,285,996 | ||||||

| 147,096,597 | ||||||||

Software — 21.3% | ||||||||

Altair Engineering, Inc. - Class A (a) | 1,531,230 | 95,793,749 | ||||||

BlackLine, Inc. (a) | 944,815 | 52,408,888 | ||||||

Descartes Systems Group, Inc. (The) (a) | 1,834,196 | 134,593,302 | ||||||

Model N, Inc. (a)(b) | 2,122,832 | 51,818,329 | ||||||

Paycor HCM, Inc. (a) | 2,258,230 | 51,555,391 | ||||||

PROS Holdings, Inc. (a) | 2,219,665 | 76,844,802 | ||||||

Q2 Holdings, Inc. (a) | 1,003,236 | 32,374,426 | ||||||

Simulations Plus, Inc. (b) | 1,307,375 | 54,517,538 | ||||||

SPS Commerce, Inc. (a) | 949,180 | 161,939,600 | ||||||

Vertex, Inc. - Class A (a) | 1,477,677 | 34,134,339 | ||||||

| 745,980,364 | ||||||||

Telecommunications — 1.6% | ||||||||

Telecommunications Equipment — 1.6% | ||||||||

Digi International, Inc. (a)(b) | 2,118,000 | 57,186,000 | ||||||

Utilities — 3.9% | ||||||||

Waste & Disposal Services — 3.9% | ||||||||

Casella Waste Systems, Inc. - Class A (a) | 1,775,035 | 135,435,171 | ||||||

Total Common Stocks (Cost $2,227,192,127) | $ | 3,322,290,630 | ||||||

18

CONESTOGA SMALL CAP FUND | ||||||||

MONEY MARKET FUNDS — 1.8% | Shares | Value | ||||||

Fidelity Investments Money Market Treasury Portfolio - Class I, 5.22% (c) (Cost $61,399,054) | 61,399,054 | $ | 61,399,054 | |||||

Total Investments at Value — 96.7% (Cost $2,288,591,181) | $ | 3,383,689,684 | ||||||

Other Assets in Excess of Liabilities — 3.3% | 115,207,520 | |||||||

Net Assets — 100.0% | $ | 3,498,897,204 | ||||||

(a) | Non-income producing security. |

(b) | The Fund owned 5% or more of the company’s outstanding voting shares thereby making the company an affiliate of the Fund as that term is defined in the Investment Company Act of 1940 (Note 5). |

(c) | The rate shown is the 7-day effective yield as of September 30, 2023. |

Schedule of Investments uses the Russell ICB Industry and Sector classification. | |

See accompanying notes to financial statements. | |

19

CONESTOGA SMID CAP FUND |

Diversification*

(% of Net Assets)

Top Ten Equity Holdings

Security Description | % of Net Assets | |

Fair Isaac Corporation | 4.5% | |

Casella Waste Systems, Inc. - Class A | 4.0% | |

FirstService Corporation | 3.8% | |

SPS Commerce, Inc. | 3.3% | |

Exponent, Inc. | 3.1% | |

Rollins, Inc. | 3.0% | |

Watsco, Inc. | 3.0% | |

Descartes Systems Group, Inc. (The) | 3.0% | |

Pool Corporation | 2.8% | |

Construction Partners, Inc. - Class A | 2.8% |

* | Industry categories represent the industry assigned at the time of purchase. See Note 7 of the Notes to Financial Statements. |

20

CONESTOGA SMID CAP FUND | ||||||||

COMMON STOCKS — 97.7% | Shares | Value | ||||||

Basic Materials — 4.3% | ||||||||

Metal Fabricating — 2.7% | ||||||||

RBC Bearings, Inc. (a) | 43,875 | $ | 10,272,454 | |||||

Specialty Chemicals — 1.6% | ||||||||

Balchem Corporation | 48,985 | 6,076,099 | ||||||

Consumer Discretionary — 12.8% | ||||||||

Consumer Services: Miscellaneous — 3.0% | ||||||||

Rollins, Inc. | 309,000 | 11,534,970 | ||||||

Education Services — 1.5% | ||||||||

Bright Horizons Family Solutions, Inc. (a) | 73,345 | 5,974,684 | ||||||

Home Improvement Retailers — 2.4% | ||||||||

SiteOne Landscape Supply, Inc. (a) | 55,695 | 9,103,348 | ||||||

Hotels & Motels — 1.8% | ||||||||

Vail Resorts, Inc. | 30,720 | 6,816,461 | ||||||

Recreational Products — 2.8% | ||||||||

Pool Corporation | 30,045 | 10,699,025 | ||||||

Recreational Vehicles & Boats — 1.3% | ||||||||

LCI Industries | 42,200 | 4,955,124 | ||||||

Financials — 1.9% | ||||||||

Financial Data Providers — 1.9% | ||||||||

Clearwater Analytics Holdings, Inc. - Class A (a) | 372,000 | 7,194,480 | ||||||

Health Care — 12.9% | ||||||||

Medical Equipment — 4.9% | ||||||||

Merit Medical Systems, Inc. (a) | 136,258 | 9,404,527 | ||||||

Repligen Corporation (a) | 60,540 | 9,626,465 | ||||||

| 19,030,992 | ||||||||

Medical Supplies — 8.0% | ||||||||

Bio-Techne Corporation | 94,125 | 6,407,089 | ||||||

Neogen Corporation (a) | 300,111 | 5,564,058 | ||||||

Stevanato Group S.p.A. | 223,577 | 6,644,708 | ||||||

21

CONESTOGA SMID CAP FUND | ||||||||

COMMON STOCKS — 97.7% (Continued) | Shares | Value | ||||||

Health Care — 12.9% (Continued) | ||||||||

Medical Supplies — 8.0% (Continued) | ||||||||

Teleflex, Inc. | 22,975 | $ | 4,512,520 | |||||

West Pharmaceutical Services, Inc. | 20,000 | 7,504,200 | ||||||

| 30,632,575 | ||||||||

Industrials — 35.9% | ||||||||

Aerospace — 2.3% | ||||||||

HEICO Corporation - Class A | 67,350 | 8,702,967 | ||||||

Building Materials: Other — 4.6% | ||||||||

Simpson Manufacturing Company, Inc. | 54,050 | 8,097,231 | ||||||

Trex Company, Inc. (a) | 155,105 | 9,559,121 | ||||||

| 17,656,352 | ||||||||

Building: Climate Control — 3.0% | ||||||||

Watsco, Inc. | 30,080 | 11,361,818 | ||||||

Construction — 2.8% | ||||||||

Construction Partners, Inc. - Class A (a) | 289,450 | 10,582,292 | ||||||

Defense — 3.5% | ||||||||

Axon Enterprise, Inc. (a) | 38,155 | 7,592,463 | ||||||

Mercury Systems, Inc. (a) | 155,700 | 5,774,913 | ||||||

| 13,367,376 | ||||||||

Diversified Industrials — 0.6% | ||||||||

CSW Industrials, Inc. | 11,950 | 2,094,118 | ||||||

Electronic Equipment: Gauges & Meters — 1.2% | ||||||||

Cognex Corporation | 107,000 | 4,541,080 | ||||||

Engineering & Contracting Services — 3.1% | ||||||||

Exponent, Inc. | 139,605 | 11,950,188 | ||||||

Industrial Suppliers — 1.4% | ||||||||

Hillman Solutions Corporation (a) | 671,805 | 5,542,391 | ||||||

Machinery: Engines — 0.9% | ||||||||

Generac Holdings, Inc. (a) | 31,660 | 3,449,674 | ||||||

Machinery: Industrial — 3.2% | ||||||||

EVI Industries, Inc. (a) | 289,692 | 7,190,155 | ||||||

John Bean Technologies Corporation | 48,605 | 5,110,330 | ||||||

| 12,300,485 | ||||||||

22

CONESTOGA SMID CAP FUND | ||||||||

COMMON STOCKS — 97.7% (Continued) | Shares | Value | ||||||

Industrials — 35.9% (Continued) | ||||||||

Machinery: Specialty — 2.5% | ||||||||

Graco, Inc. | 133,055 | $ | 9,697,048 | |||||

Professional Business Support Services — 4.5% | ||||||||

Fair Isaac Corporation (a) | 20,000 | 17,370,600 | ||||||

Transaction Processing Services — 2.3% | ||||||||

Jack Henry & Associates, Inc. | 58,970 | 8,912,726 | ||||||

Real Estate — 3.8% | ||||||||

Real Estate Services — 3.8% | ||||||||

FirstService Corporation | 100,625 | 14,644,962 | ||||||

Technology — 22.1% | ||||||||

Computer Services — 3.0% | ||||||||

Gartner, Inc. (a) | 17,000 | 5,841,370 | ||||||

Workiva, Inc. (a) | 55,833 | 5,658,116 | ||||||

| 11,499,486 | ||||||||

Consumer Digital Services — 0.9% | ||||||||

Definitive Healthcare Corporation - Class A (a) | 422,760 | 3,377,852 | ||||||

Production Technology Equipment — 2.7% | ||||||||

Novanta, Inc. (a) | 73,645 | 10,563,639 | ||||||

Software — 15.5% | ||||||||

Altair Engineering, Inc. - Class A (a) | 90,145 | 5,639,471 | ||||||

Descartes Systems Group, Inc. (The) (a) | 154,475 | 11,335,375 | ||||||

Five9, Inc. (a) | 54,300 | 3,491,490 | ||||||

Guidewire Software, Inc. (a) | 74,620 | 6,715,800 | ||||||

Paycor HCM, Inc. (a) | 209,030 | 4,772,155 | ||||||

Q2 Holdings, Inc. (a) | 139,030 | 4,486,498 | ||||||

SPS Commerce, Inc. (a) | 73,434 | 12,528,575 | ||||||

Tyler Technologies, Inc. (a) | 27,000 | 10,425,780 | ||||||

| 59,395,144 | ||||||||

23

CONESTOGA SMID CAP FUND | ||||||||

COMMON STOCKS — 97.7% (Continued) | Shares | Value | ||||||

Utilities — 4.0% | ||||||||

Waste & Disposal Services — 4.0% | ||||||||

Casella Waste Systems, Inc. - Class A (a) | 200,200 | $ | 15,275,260 | |||||

Total Investments at Value — 97.7% (Cost $295,338,723) | $ | 374,575,670 | ||||||

Other Assets in Excess of Liabilities — 2.3% | 8,997,338 | |||||||

Net Assets — 100.0% | $ | 383,573,008 | ||||||

(a) | Non-income producing security. |

Schedule of Investments uses the Russell ICB Industry and Sector classification. | |

See accompanying notes to financial statements. | |

24

CONESTOGA MID CAP FUND |

Diversification*

(% of Net Assets)

Top Ten Equity Holdings

Security Description | % of Net Assets | |

Copart, Inc. | 5.5% | |

Rollins, Inc. | 4.5% | |

West Pharmaceutical Services, Inc. | 4.3% | |

Verisk Analytics, Inc. | 4.3% | |

CoStar Group, Inc. | 4.0% | |

HEICO Corporation - Class A | 3.9% | |

Roper Technologies, Inc. | 3.8% | |

Pool Corporation | 3.8% | |

IDEXX Laboratories, Inc. | 3.6% | |

Tyler Technologies, Inc. | 3.6% |

* | Industry categories represent the industry assigned at the time of purchase. See Note 7 of the Notes to Financial Statements. |

25

CONESTOGA MID CAP FUND | ||||||||

COMMON STOCKS — 96.3% | Shares | Value | ||||||

Consumer Discretionary — 18.8% | ||||||||

Consumer Services: Miscellaneous — 10.0% | ||||||||

Copart, Inc. (a) | 2,960 | $ | 127,546 | |||||

Rollins, Inc. | 2,825 | 105,457 | ||||||

| 233,003 | ||||||||

Education Services — 1.7% | ||||||||

Bright Horizons Family Solutions, Inc. (a) | 495 | 40,323 | ||||||

Hotels & Motels — 1.8% | ||||||||

Vail Resorts, Inc. | 185 | 41,050 | ||||||

Recreational Products — 3.8% | ||||||||

Pool Corporation | 250 | 89,025 | ||||||

Specialty Retail — 1.5% | ||||||||

Tractor Supply Company | 175 | 35,534 | ||||||

Financials — 2.2% | ||||||||

Financial Data Providers — 2.2% | ||||||||

FactSet Research Systems, Inc. | 115 | 50,285 | ||||||

Health Care — 21.3% | ||||||||

Health Care Services — 3.3% | ||||||||

Veeva Systems, Inc. - Class A (a) | 375 | 76,294 | ||||||

Medical Equipment — 8.3% | ||||||||

IDEXX Laboratories, Inc. (a) | 195 | 85,268 | ||||||

Repligen Corporation (a) | 340 | 54,063 | ||||||

STERIS plc | 250 | 54,855 | ||||||

| 194,186 | ||||||||

Medical Supplies — 9.7% | ||||||||

Align Technology, Inc. (a) | 125 | 38,165 | ||||||

Bio-Techne Corporation | 870 | 59,221 | ||||||

Teleflex, Inc. | 145 | 28,479 | ||||||

West Pharmaceutical Services, Inc. | 270 | 101,307 | ||||||

| 227,172 | ||||||||

26

CONESTOGA MID CAP FUND | ||||||||

COMMON STOCKS — 96.3% (Continued) | Shares | Value | ||||||

Industrials — 24.2% | ||||||||

Aerospace — 3.9% | ||||||||

HEICO Corporation - Class A | 710 | $ | 91,746 | |||||

Building: Climate Control — 2.7% | ||||||||

Watsco, Inc. | 165 | 62,324 | ||||||

Electronic Equipment: Gauges & Meters — 2.7% | ||||||||

Cognex Corporation | 575 | 24,403 | ||||||

Mettler-Toledo International, Inc. (a) | 35 | 38,782 | ||||||

| 63,185 | ||||||||

Electronic Equipment: Pollution Control — 1.3% | ||||||||

Xylem, Inc. | 335 | 30,495 | ||||||

Engineering & Contracting Services — 2.0% | ||||||||

Exponent, Inc. | 560 | 47,936 | ||||||

Machinery: Engines — 1.4% | ||||||||

Generac Holdings, Inc. (a) | 290 | 31,598 | ||||||

Machinery: Specialty — 3.0% | ||||||||

Graco, Inc. | 975 | 71,058 | ||||||

Professional Business Support Services — 4.3% | ||||||||

Verisk Analytics, Inc. | 425 | 100,402 | ||||||

Transaction Processing Services — 2.9% | ||||||||

Jack Henry & Associates, Inc. | 450 | 68,013 | ||||||

Real Estate — 4.0% | ||||||||

Real Estate Services — 4.0% | ||||||||

CoStar Group, Inc. (a) | 1,210 | 93,037 | ||||||

Technology — 22.2% | ||||||||

Computer Services — 3.2% | ||||||||

Gartner, Inc. (a) | 220 | 75,594 | ||||||

27

CONESTOGA MID CAP FUND | ||||||||

COMMON STOCKS — 96.3% (Continued) | Shares | Value | ||||||

Technology — 22.2% (Continued) | ||||||||

Software — 19.0% | ||||||||

ANSYS, Inc. (a) | 270 | $ | 80,339 | |||||

Bentley Systems, Inc. | 520 | 26,083 | ||||||

Five9, Inc. (a) | 290 | 18,647 | ||||||

Fortinet, Inc. (a) | 1,130 | 66,308 | ||||||

Guidewire Software, Inc. (a) | 420 | 37,800 | ||||||

Lightspeed Commerce, Inc. (a) | 1,145 | 16,064 | ||||||

Procore Technologies, Inc. (a) | 365 | 23,842 | ||||||

Roper Technologies, Inc. | 185 | 89,592 | ||||||

Tyler Technologies, Inc. (a) | 220 | 84,951 | ||||||

| 443,626 | ||||||||

Utilities — 3.6% | ||||||||

Waste & Disposal Services — 3.6% | ||||||||

Waste Connections, Inc. | 630 | 84,609 | ||||||

Total Investments at Value — 96.3% (Cost $2,468,482) | $ | 2,250,495 | ||||||

Other Assets in Excess of Liabilities — 3.7% | 86,777 | |||||||

Net Assets — 100.0% | $ | 2,337,272 | ||||||

(a) | Non-income producing security. |

Schedule of Investments uses the Russell ICB Industry and Sector classification. | |

See accompanying notes to financial statements. | |

28

CONESTOGA DISCOVERY FUND |

Diversification*

(% of Net Assets)

Top Ten Equity Holdings

Security Description | % of Net Assets | |

Transcat, Inc. | 5.1% | |

Construction Partners, Inc. - Class A | 5.0% | |

PROS Holdings, Inc. | 4.6% | |

Vericel Corporation | 4.5% | |

NV5 Global, Inc. | 4.2% | |

I3 Verticals, Inc. - Class A | 4.1% | |

Hillman Solutions Corporation | 4.0% | |

Simulations Plus, Inc. | 3.9% | |

Palomar Holdings, Inc. | 3.8% | |

U.S. Physical Therapy, Inc. | 3.8% |

* | Industry categories represent the industry assigned at the time of purchase. See Note 7 of the Notes to Financial Statements. |

29

CONESTOGA DISCOVERY FUND | ||||||||

COMMON STOCKS — 97.3% | Shares | Value | ||||||

Consumer Discretionary — 2.6% | ||||||||

Entertainment — 2.6% | ||||||||

Thunderbird Entertainment Group, Inc. (a) | 33,801 | $ | 52,054 | |||||

Financials — 3.8% | ||||||||

Property & Casualty Insurance — 3.8% | ||||||||

Palomar Holdings, Inc. (a) | 1,511 | 76,683 | ||||||

Health Care — 21.6% | ||||||||

Biotechnology — 6.4% | ||||||||

Alpha Teknova, Inc. (a) | 13,811 | 38,533 | ||||||

Vericel Corporation (a) | 2,709 | 90,806 | ||||||

| 129,339 | ||||||||

Health Care Facilities — 3.8% | ||||||||

U.S. Physical Therapy, Inc. | 829 | 76,044 | ||||||

Health Care Services — 3.4% | ||||||||

Phreesia, Inc. (a) | 3,610 | 67,435 | ||||||

Medical Equipment — 8.0% | ||||||||

BioLife Solutions, Inc. (a) | 3,599 | 49,702 | ||||||

OrthoPediatrics Corporation (a) | 2,134 | 68,288 | ||||||

Semler Scientific, Inc. (a) | 1,681 | 42,647 | ||||||

| 160,637 | ||||||||

Industrials — 39.3% | ||||||||

Construction — 5.0% | ||||||||

Construction Partners, Inc. - Class A (a) | 2,748 | 100,467 | ||||||

Electronic Equipment: Gauges & Meters — 7.4% | ||||||||

Mesa Laboratories, Inc. | 441 | 46,336 | ||||||

Transcat, Inc. (a) | 1,045 | 102,379 | ||||||

| 148,715 | ||||||||

Engineering & Contracting Services — 3.1% | ||||||||

Willdan Group, Inc. (a) | 3,061 | 62,536 | ||||||

Industrial Suppliers — 6.7% | ||||||||

CryoPort, Inc. (a) | 3,922 | 53,771 | ||||||

Hillman Solutions Corporation (a) | 9,800 | 80,850 | ||||||

| 134,621 | ||||||||

30

CONESTOGA DISCOVERY FUND | ||||||||

COMMON STOCKS — 97.3% (Continued) | Shares | Value | ||||||

Industrials — 39.3% (Continued) | ||||||||

Machinery: Construction & Handling — 3.1% | ||||||||

Douglas Dynamics, Inc. | 2,047 | $ | 61,778 | |||||

Professional Business Support Services — 7.0% | ||||||||

Montrose Environmental Group, Inc. (a) | 1,940 | 56,764 | ||||||

NV5 Global, Inc. (a) | 869 | 83,624 | ||||||

| 140,388 | ||||||||

Security Services — 2.9% | ||||||||

SoundThinking, Inc. (a) | 3,185 | 57,012 | ||||||

Transaction Processing Services — 4.1% | ||||||||

I3 Verticals, Inc. - Class A (a) | 3,852 | 81,431 | ||||||

Technology — 26.6% | ||||||||

Consumer Digital Services — 2.0% | ||||||||

Definitive Healthcare Corporation - Class A (a) | 4,925 | 39,351 | ||||||

Software — 24.6% | ||||||||

Model N, Inc. (a) | 2,852 | 69,617 | ||||||

Olo, Inc. - Class A (a) | 12,050 | 73,023 | ||||||

Planet Labs PBC - Class A (a) | 19,350 | 50,310 | ||||||

PROS Holdings, Inc. (a) | 2,673 | 92,539 | ||||||

Q2 Holdings, Inc. (a) | 1,800 | 58,086 | ||||||

Simulations Plus, Inc. | 1,893 | 78,938 | ||||||

TECSYS, Inc. | 3,525 | 70,500 | ||||||

| 493,013 | ||||||||

Telecommunications — 3.4% | ||||||||

Telecommunications Equipment — 3.4% | ||||||||

Digi International, Inc. (a) | 2,540 | 68,580 | ||||||

Total Investments at Value — 97.3% (Cost $2,252,862) | $ | 1,950,084 | ||||||

Other Assets in Excess of Liabilities — 2.7% | 54,306 | |||||||

Net Assets — 100.0% | $ | 2,004,390 | ||||||

(a) | Non-income producing security. |

Schedule of Investments uses the Russell ICB Industry and Sector classification. | |

See accompanying notes to financial statements. | |

31

CONESTOGA FUNDS | ||||||||

| Conestoga | Conestoga | ||||||

ASSETS | ||||||||

Investments in unaffiliated securities, at cost | $ | 1,819,132,997 | $ | 295,338,723 | ||||

Investments in affiliated securities, at cost | 469,458,184 | — | ||||||

Total investments, at cost | $ | 2,288,591,181 | $ | 295,338,723 | ||||

Investments in unaffiliated securities, at value (Note 2) | $ | 2,844,956,136 | $ | 374,575,670 | ||||

Investments in affiliated securities, at value (Notes 2 & 5) | 538,733,548 | — | ||||||

Total investments, at value | 3,383,689,684 | 374,575,670 | ||||||

Cash (Note 2) | 110,530,286 | 9,218,161 | ||||||

Receivable for capital shares sold | 11,258,584 | 239,603 | ||||||

Dividends and interest receivable | 1,214,771 | 58,832 | ||||||

Other assets | 78,242 | 22,109 | ||||||

Total assets | 3,506,771,567 | 384,114,375 | ||||||

LIABILITIES | ||||||||

Payable for capital shares redeemed | 1,431,480 | 211,965 | ||||||

Payable for investment securities purchased | 3,564,563 | — | ||||||

Payable to Adviser (Note 4) | 2,527,317 | 209,628 | ||||||

Accrued distribution fees (Note 4) | 173,219 | 20,828 | ||||||

Accrued Trustees’ fees (Note 4) | 53,190 | 53,190 | ||||||

Payable to administrator (Note 4) | 49,435 | 9,951 | ||||||

Accrued legal fees | 13,500 | 13,500 | ||||||

Accrued audit fees | 16,000 | 14,500 | ||||||

Other accrued expenses | 45,659 | 7,805 | ||||||

Total liabilities | 7,874,363 | 541,367 | ||||||

CONTINGENCIES AND COMMITMENTS (NOTES 4 & 8) | — | — | ||||||

NET ASSETS | $ | 3,498,897,204 | $ | 383,573,008 | ||||

NET ASSETS CONSIST OF: | ||||||||

Paid-in capital | $ | 2,387,673,692 | $ | 324,727,577 | ||||

Distributable earnings | 1,111,223,512 | 58,845,431 | ||||||

NET ASSETS | $ | 3,498,897,204 | $ | 383,573,008 | ||||

NET ASSET VALUE PER SHARE: | ||||||||

INSTITUTIONAL CLASS | ||||||||

Net assets applicable to Institutional Class | $ | 2,795,501,718 | $ | 340,635,716 | ||||

Institutional Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 42,181,567 | 16,235,688 | ||||||

Net asset value, offering price and redemption price per share (Note 2) | $ | 66.27 | $ | 20.98 | ||||

INVESTORS CLASS | ||||||||

Net assets applicable to Investors Class | $ | 703,395,486 | $ | 42,937,292 | ||||

Investors Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 10,841,511 | 2,092,888 | ||||||

Net asset value, offering price and redemption price per share (Note 2) | $ | 64.88 | $ | 20.52 | ||||

See accompanying notes to financial statements. |

32

CONESTOGA FUNDS | ||||||||

| Conestoga | Conestoga | ||||||

ASSETS | ||||||||

Investments in unaffiliated securities, at cost | $ | 2,468,482 | $ | 2,252,862 | ||||

Investments in unaffiliated securities, at value (Note 2) | $ | 2,250,495 | $ | 1,950,084 | ||||

Cash (Note 2) | 102,272 | 71,418 | ||||||

Receivable due from Adviser (Note 4) | 9,939 | 13,864 | ||||||

Receivable for capital shares sold | 200 | — | ||||||

Dividends and interest receivable | 479 | 537 | ||||||

Other assets | 13,530 | 7,687 | ||||||

Total assets | 2,376,915 | 2,043,590 | ||||||

LIABILITIES | ||||||||

Accrued distribution fees (Note 4) | 4,050 | 3,745 | ||||||

Accrued Trustees’ fees (Note 4) | 600 | 522 | ||||||

Payable to administrator (Note 4) | 5,140 | 5,140 | ||||||

Accrued legal fees | 13,500 | 13,500 | ||||||

Accrued audit fees | 14,500 | 14,500 | ||||||

Other accrued expenses | 1,853 | 1,793 | ||||||

Total liabilities | 39,643 | 39,200 | ||||||

CONTINGENCIES AND COMMITMENTS (NOTES 4 & 8) | — | — | ||||||

NET ASSETS | $ | 2,337,272 | $ | 2,004,390 | ||||

NET ASSETS CONSIST OF: | ||||||||

Paid-in capital | $ | 2,671,356 | $ | 2,465,144 | ||||

Accumulated deficit | (334,084 | ) | (460,754 | ) | ||||

NET ASSETS | $ | 2,337,272 | $ | 2,004,390 | ||||

NET ASSET VALUE PER SHARE: | ||||||||

INSTITUTIONAL CLASS | ||||||||

Net assets applicable to Institutional Class | $ | 1,893,383 | $ | 1,864,173 | ||||

Institutional Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 228,825 | 293,611 | ||||||

Net asset value, offering price and redemption price per share (Note 2) | $ | 8.27 | $ | 6.35 | ||||

INVESTORS CLASS | ||||||||

Net assets applicable to Investors Class | $ | 443,889 | $ | 140,217 | ||||

Investors Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 53,960 | 22,181 | ||||||

Net asset value, offering price and redemption price per share (Note 2) | $ | 8.23 | $ | 6.32 | ||||

See accompanying notes to financial statements. |

33

CONESTOGA FUNDS | ||||||||

| Conestoga | Conestoga | ||||||

INVESTMENT INCOME | ||||||||

Dividend income from unaffiliated investments | $ | 9,154,133 | $ | 1,810,835 | ||||

Dividend income from affiliated investments (Note 5) | 3,069,864 | — | ||||||

Foreign withholding taxes on dividends | (131,744 | ) | (16,294 | ) | ||||

Interest | 3,630,252 | 258,727 | ||||||

Total investment income | 15,722,505 | 2,053,268 | ||||||

EXPENSES | ||||||||

Management fees (Note 4) | 30,597,346 | 3,128,924 | ||||||

Distribution fees - Investors Class (Note 4) | 1,770,395 | 119,450 | ||||||

Shareholder Servicing Fees (Note 4) | ||||||||

Institutional Class | 1,270,812 | 224,229 | ||||||

Investors Class | 354,089 | 23,891 | ||||||

Trustees’ fees and expenses (Note 4) | 212,567 | 212,567 | ||||||

Transfer agent fees (Note 4) | ||||||||

Institutional Class | 108,568 | 12,524 | ||||||

Investors Class | 222,991 | 20,868 | ||||||

Fund accounting fees (Note 4) | 248,048 | 89,850 | ||||||

Custody and bank service fees | 169,190 | 27,840 | ||||||

Legal fees | 93,124 | 93,124 | ||||||

Registration and filing fees | 115,227 | 68,706 | ||||||

Postage and supplies | 106,940 | 13,764 | ||||||

Audit and tax services fees | 16,826 | 15,326 | ||||||

Insurance expense | 9,828 | 9,828 | ||||||

Shareholder reporting expenses | 10,626 | 8,238 | ||||||

Administration fees (Note 4) | 3,000 | 3,000 | ||||||

Borrowing expenses | 3,101 | 1,760 | ||||||

Other expenses | 20,838 | 16,546 | ||||||

Total expenses | 35,333,516 | 4,090,435 | ||||||

Fee reductions and expense reimbursements by the Adviser (Note 4) | (3,320,403 | ) | (842,060 | ) | ||||

Net expenses | 32,013,113 | 3,248,375 | ||||||

NET INVESTMENT LOSS | (16,290,608 | ) | (1,195,107 | ) | ||||

REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS | ||||||||

Net realized gains (losses) from unaffiliated investments | 46,896,618 | (11,227,870 | ) | |||||

Net realized losses from affiliated investments (Note 5) | (7,307,986 | ) | — | |||||

Net change in unrealized appreciation (depreciation) on unaffiliated investments | 435,926,747 | 65,117,817 | ||||||

Net change in unrealized appreciation (depreciation) on affiliated investments (Note 5) | 20,789,542 | — | ||||||

NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS | 496,304,921 | 53,889,947 | ||||||

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 480,014,313 | $ | 52,694,840 | ||||

See accompanying notes to financial statements. |

34

CONESTOGA FUNDS | ||||||||

| Conestoga | Conestoga | ||||||

INVESTMENT INCOME | ||||||||

Dividend income from unaffiliated investments | $ | 11,804 | $ | 5,746 | ||||

Foreign withholding taxes on dividends | (91 | ) | — | |||||

Interest | 2,674 | 2,929 | ||||||

Total investment income | 14,387 | 8,675 | ||||||

EXPENSES | ||||||||

Legal fees | 102,624 | 102,624 | ||||||

Fund accounting fees (Note 4) | 43,707 | 41,856 | ||||||

Registration and filing fees | 41,089 | 40,940 | ||||||

Management fees (Note 4) | 16,890 | 23,415 | ||||||

Audit and tax services fees | 15,326 | 15,326 | ||||||

Transfer agent fees (Note 4) | ||||||||

Institutional Class | 4,868 | 7,002 | ||||||

Investors Class | 10,382 | 7,233 | ||||||

Insurance expense | 9,851 | 9,848 | ||||||

Shareholder reporting expenses | 6,181 | 6,732 | ||||||

Postage and supplies | 3,522 | 3,330 | ||||||

Administration fees (Note 4) | 3,000 | 3,000 | ||||||

Trustees’ fees and expenses (Note 4) | 2,423 | 2,577 | ||||||

Shareholder Servicing Fees (Note 4) | ||||||||

Institutional Class | 1,674 | 2,154 | ||||||

Investors Class | 219 | 94 | ||||||

Custody and bank service fees | 663 | 977 | ||||||

Distribution fees - Investors Class (Note 4) | 1,094 | 469 | ||||||

Borrowing expenses | 3 | — | ||||||

Other expenses | 15,064 | 20,596 | ||||||

Total expenses | 278,580 | 288,173 | ||||||

Fee reductions and expense reimbursements by the Adviser (Note 4) | (260,597 | ) | (258,435 | ) | ||||

Net expenses | 17,983 | 29,738 | ||||||

NET INVESTMENT LOSS | (3,596 | ) | (21,063 | ) | ||||

REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS | ||||||||

Net realized losses from unaffiliated investments | (78,501 | ) | (106,006 | ) | ||||

Net change in unrealized appreciation (depreciation) on unaffiliated investments | 366,579 | (99,707 | ) | |||||

NET REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS | 288,078 | (205,713 | ) | |||||

NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS | $ | 284,482 | $ | (226,776 | ) | |||

See accompanying notes to financial statements. |

35

CONESTOGA SMALL CAP FUND | ||||||||

| Year Ended | Year Ended | ||||||

FROM OPERATIONS | ||||||||

Net investment loss | $ | (16,290,608 | ) | $ | (25,158,766 | ) | ||

Net realized gains from investments | 39,588,632 | 140,269,117 | ||||||

Net change in unrealized appreciation (depreciation) on investments | 456,716,289 | (1,353,094,139 | ) | |||||

Net increase (decrease) in net assets resulting from operations | 480,014,313 | (1,237,983,788 | ) | |||||

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | ||||||||

Institutional Class | (95,526,570 | ) | (174,426,787 | ) | ||||

Investors Class | (26,143,886 | ) | (51,042,164 | ) | ||||

Decrease in net assets from distributions to shareholders | (121,670,456 | ) | (225,468,951 | ) | ||||

CAPITAL SHARE TRANSACTIONS (Note 6) | ||||||||

Institutional Class | ||||||||

Proceeds from shares sold | 636,483,743 | 685,880,670 | ||||||

Reinvestment of distributions to shareholders | 66,677,631 | 115,710,799 | ||||||

Payments for shares redeemed | (547,835,383 | ) | (683,555,542 | ) | ||||

Net increase in Institutional Class net assets from capital share transactions | 155,325,991 | 118,035,927 | ||||||

Investors Class | ||||||||

Proceeds from shares sold | 109,107,169 | 125,440,330 | ||||||

Reinvestment of distributions to shareholders | 22,531,924 | 45,633,567 | ||||||

Payments for shares redeemed | (146,791,000 | ) | (179,700,944 | ) | ||||

Net decrease in Investors Class net assets from capital share transactions | (15,151,907 | ) | (8,627,047 | ) | ||||

TOTAL INCREASE (DECREASE) IN NET ASSETS | 498,517,941 | (1,354,043,859 | ) | |||||

| ||||||||

NET ASSETS | ||||||||

Beginning of year | 3,000,379,263 | 4,354,423,122 | ||||||

End of year | $ | 3,498,897,204 | $ | 3,000,379,263 | ||||

See accompanying notes to financial statements. |

36

CONESTOGA SMID CAP FUND | ||||||||

| Year Ended | Year Ended | ||||||

FROM OPERATIONS | ||||||||

Net investment loss | $ | (1,195,107 | ) | $ | (1,721,644 | ) | ||

Net realized losses from investments | (11,227,870 | ) | (5,628,511 | ) | ||||

Net change in unrealized appreciation (depreciation) on investments | 65,117,817 | (133,534,114 | ) | |||||

Net increase (decrease) in net assets resulting from operations | 52,694,840 | (140,884,269 | ) | |||||

CAPITAL SHARE TRANSACTIONS (Note 6) | ||||||||

Institutional Class | ||||||||

Proceeds from shares sold | 91,800,730 | 111,657,408 | ||||||

Payments for shares redeemed | (68,915,724 | ) | (76,820,766 | ) | ||||

Net increase in Institutional Class net assets from capital share transactions | 22,885,006 | 34,836,642 | ||||||

Investors Class | ||||||||

Proceeds from shares sold | 12,570,141 | 31,237,466 | ||||||

Payments for shares redeemed | (21,382,886 | ) | (30,051,109 | ) | ||||

Net increase (decrease) in Investors Class net assets from capital share transactions | (8,812,745 | ) | 1,186,357 | |||||

TOTAL INCREASE (DECREASE) IN NET ASSETS | 66,767,101 | (104,861,270 | ) | |||||

NET ASSETS | ||||||||

Beginning of year | 316,805,907 | 421,667,177 | ||||||

End of year | $ | 383,573,008 | $ | 316,805,907 | ||||

See accompanying notes to financial statements. |

37

CONESTOGA MID CAP FUND | ||||||||

| Year Ended | Year Ended | ||||||

FROM OPERATIONS | ||||||||

Net investment loss | $ | (3,596 | ) | $ | (7,855 | ) | ||

Net realized losses from investments | (78,501 | ) | (34,733 | ) | ||||

Net change in unrealized appreciation (depreciation) on investments | 366,579 | (621,587 | ) | |||||

Net increase (decrease) in net assets resulting from operations | 284,482 | (664,175 | ) | |||||

CAPITAL SHARE TRANSACTIONS (Note 6) | ||||||||

Institutional Class | ||||||||

Proceeds from shares sold | 351,158 | 727,504 | ||||||

Payments for shares redeemed | (86,211 | ) | (1,249 | ) | ||||

Net increase in Institutional Class net assets from capital share transactions | 264,947 | 726,255 | ||||||

Investors Class | ||||||||

Proceeds from shares sold | 2,000 | 49,000 | ||||||

Payments for shares redeemed | (15,628 | ) | (44,626 | ) | ||||

Net increase (decrease) in Investors Class net assets from capital share transactions | (13,628 | ) | 4,374 | |||||

TOTAL INCREASE IN NET ASSETS | 535,801 | 66,454 | ||||||

NET ASSETS | ||||||||

Beginning of year | 1,801,471 | 1,735,017 | ||||||

End of year | $ | 2,337,272 | $ | 1,801,471 | ||||

See accompanying notes to financial statements. |

38

CONESTOGA DISCOVERY FUND | ||||||||

| Year Ended | Period Ended | ||||||

FROM OPERATIONS | ||||||||

Net investment loss | $ | (21,063 | ) | $ | (18,146 | ) | ||

Net realized losses from investments | (106,006 | ) | (36,215 | ) | ||||

Net change in unrealized appreciation (depreciation) on investments | (99,707 | ) | (854,041 | ) | ||||

Net decrease in net assets resulting from operations | (226,776 | ) | (908,402 | ) | ||||

CAPITAL SHARE TRANSACTIONS (Note 6) | ||||||||

Institutional Class | ||||||||

Proceeds from shares sold | — | 148,375 | ||||||

Payments for shares redeemed | — | (15 | ) | |||||

Shares issued in connection with Fund Reorganization (Note 1) | — | 2,777,245 | ||||||

Net increase in Institutional Class net assets from capital share transactions | — | 2,925,605 | ||||||

Investors Class | ||||||||

Proceeds from shares sold | 5,944 | 97,357 | ||||||

Payments for shares redeemed | (33,040 | ) | (14,117 | ) | ||||

Shares issued in connection with Fund Reorganization (Note 1) | — | 157,819 | ||||||

Net increase (decrease) in Investors Class net assets from capital share transactions | (27,096 | ) | 241,059 | |||||

TOTAL INCREASE (DECREASE) IN NET ASSETS | (253,872 | ) | 2,258,262 | |||||

NET ASSETS | ||||||||

Beginning of period | 2,258,262 | — | ||||||

End of period | $ | 2,004,390 | $ | 2,258,262 | ||||

(a) | Represents the period from commencement of operations (December 20, 2021) through September 30, 2022. |

See accompanying notes to financial statements. | |

39

CONESTOGA SMALL CAP FUND | ||||||||||||||||||||

Per Share Data for a Share Outstanding Throughout Each Year: | ||||||||||||||||||||

| Year | Year | Year | Year | Year | |||||||||||||||

Net asset value at beginning of year | $ | 59.06 | $ | 87.18 | $ | 63.19 | $ | 58.40 | $ | 61.27 | ||||||||||

Income (loss) from investment operations: | ||||||||||||||||||||

Net investment loss (a) | (0.29 | ) | (0.45 | ) | (0.56 | ) | (0.33 | ) | (0.23 | ) | ||||||||||

Net realized and unrealized gains (losses) on investments | 9.93 | (23.17 | ) | 24.55 | 6.39 | (1.93 | ) | |||||||||||||

Total from investment operations | 9.64 | (23.62 | ) | 23.99 | 6.06 | (2.16 | ) | |||||||||||||

Less distributions from net realized gains | (2.43 | ) | (4.50 | ) | — | (1.27 | ) | (0.71 | ) | |||||||||||

Net asset value at end of year | $ | 66.27 | $ | 59.06 | $ | 87.18 | $ | 63.19 | $ | 58.40 | ||||||||||

Total return (b) | 16.54 | % | (28.62 | %) | 37.96 | % | 10.53 | % | (3.39 | %) | ||||||||||

Net assets at end of year (000,000’s) | $ | 2,796 | $ | 2,359 | $ | 3,386 | $ | 2,204 | $ | 1,752 | ||||||||||

Ratios/supplementary data: | ||||||||||||||||||||

Ratio of total expenses to average net assets | 0.98 | % | 0.98 | % | 0.98 | % | 1.00 | % | 0.99 | % | ||||||||||

Ratio of net expenses to average net assets (c) | 0.90 | % | 0.90 | % | 0.90 | % | 0.90 | % | 0.90 | % | ||||||||||

Ratio of net investment loss to average net assets (c) | (0.44 | %) | (0.62 | %) | (0.69 | %) | (0.56 | %) | (0.41 | %) | ||||||||||

Portfolio turnover rate | 13 | % | 24 | % | 19 | % | 22 | % | 26 | % | ||||||||||

(a) | Per share net investment loss has been determined on the basis of average number of shares outstanding during the year. |

(b) | Total return is a measure of the change in value of an investment in the Fund over the years covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced management fees and/or reimbursed expenses (Note 4). |

(c) | Ratio was determined after management fee reductions and/or expense reimbursements (Note 4). |

See accompanying notes to financial statements. | |

40

CONESTOGA SMALL CAP FUND | ||||||||||||||||||||

Per Share Data for a Share Outstanding Throughout Each Year: | ||||||||||||||||||||

| Year | Year | Year | Year | Year | |||||||||||||||

Net asset value at beginning of year | $ | 57.97 | $ | 85.83 | $ | 62.33 | $ | 57.74 | $ | 60.70 | ||||||||||

Income (loss) from investment operations: | ||||||||||||||||||||

Net investment loss (a) | (0.41 | ) | (0.59 | ) | (0.70 | ) | (0.44 | ) | (0.33 | ) | ||||||||||

Net realized and unrealized gains (losses) on investments | 9.75 | (22.77 | ) | 24.20 | 6.30 | (1.92 | ) | |||||||||||||

Total from investment operations | 9.34 | (23.36 | ) | 23.50 | 5.86 | (2.25 | ) | |||||||||||||

Less distributions from net realized gains | (2.43 | ) | (4.50 | ) | — | (1.27 | ) | (0.71 | ) | |||||||||||

Net asset value at end of year | $ | 64.88 | $ | 57.97 | $ | 85.83 | $ | 62.33 | $ | 57.74 | ||||||||||

Total return (b) | 16.33 | % | (28.78 | %) | 37.70 | % | 10.30 | % | (3.57 | %) | ||||||||||

Net assets at end of year (000,000’s) | $ | 703 | $ | 642 | $ | 968 | $ | 805 | $ | 858 | ||||||||||

Ratios/supplementary data: | ||||||||||||||||||||

Ratio of total expenses to average net assets | 1.26 | % | 1.26 | % | 1.25 | % | 1.28 | % | 1.27 | % | ||||||||||

Ratio of net expenses to average net assets (c) | 1.10 | % | 1.10 | % | 1.10 | % | 1.10 | % | 1.10 | % | ||||||||||

Ratio of net investment loss to average net assets (c) | (0.64 | %) | (0.82 | %) | (0.89 | %) | (0.75 | %) | (0.60 | %) | ||||||||||

Portfolio turnover rate | 13 | % | 24 | % | 19 | % | 22 | % | 26 | % | ||||||||||

(a) | Per share net investment loss has been determined on the basis of average number of shares outstanding during the year. |

(b) | Total return is a measure of the change in value of an investment in the Fund over the years covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced management fees and/or reimbursed expenses (Note 4). |

(c) | Ratio was determined after management fee reductions and/or expense reimbursements (Note 4). |

See accompanying notes to financial statements. | |

41

CONESTOGA SMID CAP FUND | ||||||||||||||||||||

Per Share Data for a Share Outstanding Throughout Each Year: | ||||||||||||||||||||

| Year | Year | Year | Year | Year | |||||||||||||||

Net asset value at beginning of year | $ | 17.96 | $ | 26.13 | $ | 19.29 | $ | 17.18 | $ | 17.05 | ||||||||||

Income (loss) from investment operations: | ||||||||||||||||||||

Net investment loss (a) | (0.06 | ) | (0.09 | ) | (0.11 | ) | (0.06 | ) | (0.03 | ) | ||||||||||

Net realized and unrealized gains (losses) on investments | 3.08 | (8.08 | ) | 6.95 | 2.40 | 0.30 | ||||||||||||||

Total from investment operations | 3.02 | (8.17 | ) | 6.84 | 2.34 | 0.27 | ||||||||||||||

Less distributions from net realized gains | — | — | — | (0.23 | ) | (0.14 | ) | |||||||||||||

Net asset value at end of year | $ | 20.98 | $ | 17.96 | $ | 26.13 | $ | 19.29 | $ | 17.18 | ||||||||||

Total return (b) | 16.82 | % | (31.27 | %) | 35.46 | % | 13.76 | % | 1.72 | % | ||||||||||

Net assets at end of year (000’s) | $ | 340,636 | $ | 272,623 | $ | 357,479 | $ | 188,836 | $ | 80,814 | ||||||||||

Ratios/supplementary data: | ||||||||||||||||||||

Ratio of total expenses to average net assets | 1.07 | % | 1.07 | % | 1.10 | % | 1.26 | % | 1.39 | % | ||||||||||

Ratio of net expenses to average net assets (c) | 0.85 | % | 0.85 | % | 0.85 | % | 0.85 | % | 0.85 | % | ||||||||||

Ratio of net investment loss to average net assets (c) | (0.29 | %) | (0.41 | %) | (0.47 | %) | (0.34 | %) | (0.20 | %) | ||||||||||

Portfolio turnover rate | 9 | % | 15 | % | 17 | % | 11 | % | 37 | % | ||||||||||

(a) | Per share net investment loss has been determined on the basis of average number of shares outstanding during the year. |

(b) | Total return is a measure of the change in value of an investment in the Fund over the years covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced management fees and/or reimbursed expenses (Note 4). |

(c) | Ratio was determined after management fee reductions and/or expense reimbursements (Note 4). |

See accompanying notes to financial statements. | |

42

CONESTOGA SMID CAP FUND | ||||||||||||||||||||

Per Share Data for a Share Outstanding Throughout Each Year: | ||||||||||||||||||||

| Year | Year | Year | Year | Year | |||||||||||||||

Net asset value at beginning of year | $ | 17.60 | $ | 25.68 | $ | 19.01 | $ | 16.97 | $ | 16.88 | ||||||||||

Income (loss) from investment operations: | ||||||||||||||||||||

Net investment loss (a) | (0.11 | ) | (0.15 | ) | (0.17 | ) | (0.10 | ) | (0.07 | ) | ||||||||||

Net realized and unrealized gains (losses) on investments | 3.03 | (7.93 | ) | 6.84 | 2.37 | 0.30 | ||||||||||||||

Total from investment operations | 2.92 | (8.08 | ) | 6.67 | 2.27 | 0.23 | ||||||||||||||

Less distributions from net realized gains | — | — | — | (0.23 | ) | (0.14 | ) | |||||||||||||

Net asset value at end of year | $ | 20.52 | $ | 17.60 | $ | 25.68 | $ | 19.01 | $ | 16.97 | ||||||||||

Total return (b) | 16.59 | % | (31.46 | %) | 35.09 | % | 13.52 | % | 1.50 | % | ||||||||||

Net assets at end of year (000’s) | $ | 42,937 | $ | 44,183 | $ | 64,189 | $ | 50,577 | $ | 43,422 | ||||||||||

Ratios/supplementary data: | ||||||||||||||||||||

Ratio of total expenses to average net assets | 1.38 | % | 1.36 | % | 1.36 | % | 1.51 | % | 1.64 | % | ||||||||||

Ratio of net expenses to average net assets (c) | 1.10 | % | 1.10 | % | 1.10 | % | 1.10 | % | 1.10 | % | ||||||||||

Ratio of net investment loss to average net assets (c) | (0.54 | %) | (0.66 | %) | (0.71 | %) | (0.57 | %) | (0.45 | %) | ||||||||||

Portfolio turnover rate | 9 | % | 15 | % | 17 | % | 11 | % | 37 | % | ||||||||||

(a) | Per share net investment loss has been determined on the basis of average number of shares outstanding during the year. |