UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21128

Legg Mason Partners Variable Equity Trust

(Exact name of registrant as specified in charter)

620 Eighth Avenue, 49th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-877-721-1926

Date of fiscal year end: December 31

Date of reporting period: December 31, 2016

| ITEM | 1. REPORT TO STOCKHOLDERS. |

The Annual Report to Stockholders is filed herewith.

| | |

| Annual Report | | December 31, 2016 |

ENTRUSTPERMAL

ALTERNATIVE SELECT VIT PORTFOLIO

|

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

Portfolio objective

The Portfolio seeks to provide investors with long term capital appreciation.

Portfolio name change

Prior to July 22, 2016, the Portfolio was known as Permal Alternative Select VIT Portfolio. There was no change in the Portfolio’s investment objective, policies and strategy as a result of the name change.

Letter from the president

Dear Shareholder,

We are pleased to provide the annual report of EnTrustPermal Alternative Select VIT Portfolio for the twelve-month reporting period ended December 31, 2016. Please read on for a detailed look at prevailing economic and market conditions during the Portfolio’s reporting period and to learn how those conditions have affected Portfolio performance.

Special shareholder notice

The Portfolio’s Board of Trustees has determined that it is in the best interests of the Portfolio and its shareholders to terminate the Portfolio. The Portfolio is expected to cease operations on or about June 2, 2017. Before the termination is effected, and at the discretion of portfolio management, the assets of the Portfolio will be liquidated and the Portfolio will cease to pursue its investment objective.

Shares of the Portfolio will be closed to purchases and incoming exchanges as of April 28, 2017, except for the reinvestment of dividends and distributions, if any. Shareholders of the Portfolio who elect to redeem their shares prior to the completion of the liquidation will be redeemed in the ordinary course at the Portfolio’s net asset value per share. Each shareholder who remains in the Portfolio until termination will receive a liquidating distribution equal to the aggregate net asset value of the shares of the Portfolio that such shareholder then holds. Please contact your insurance company or retirement plan provider to consider options that may be available for the re-allocation of your assets.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our website, www.leggmason.com. Here you can gain immediate access to market and investment information, including:

| • | | Market insights and commentaries from our portfolio managers and |

| • | | A host of educational resources. |

| | |

| II | | EnTrustPermal Alternative Select VIT Portfolio |

We look forward to helping you meet your financial goals.

Sincerely,

Jane Trust, CFA

President and Chief Executive Officer

January 31, 2017

| | |

| EnTrustPermal Alternative Select VIT Portfolio | | III |

Investment commentary

Economic review

The pace of U.S. economic activity fluctuated during the twelve months ended December 31, 2016 (the “reporting period”). Looking back, the U.S. Department of Commerce reported that first and second quarter 2016 U.S. gross domestic product (“GDP”)i growth was 0.8% and 1.4%, respectively. GDP growth for the third quarter of 2016 was 3.5%, the strongest reading in two years. The U.S. Department of Commerce’s initial reading for fourth quarter 2016 GDP growth — released after the reporting period ended — was 1.9%. The deceleration in growth reflected a downturn in exports, an acceleration in imports, a deceleration in personal consumption expenditures and a downturn in federal government spending.

While there was a pocket of weakness in May 2016, job growth in the U.S. was solid overall and a tailwind for the economy during the reporting period. When the reporting period ended on December 31, 2016, the unemployment rate was 4.7%, as reported by the U.S. Department of Labor. The percentage of longer-term unemployed also declined over the period. In December 2016, 24.2% of Americans looking for a job had been out of work for more than six months, versus 26.9% when the period began.

Turning to the global economy, in its January 2017 World Economic Outlook Update, released after the reporting period ended, the International Monetary Fund (“IMF”)ii said, “After a lackluster outturn in 2016, economic activity is projected to pick up pace in 2017 and 2018, especially in emerging market and developing economies. However, there is a wide dispersion of possible outcomes around the projections, given uncertainty surrounding the policy

stance of the incoming U.S. administration and its global ramifications.” From a regional perspective, the IMF estimates 2017 growth in the Eurozone will be 1.6%, versus 1.7% in 2016. Japan’s economy is expected to expand 0.8% in 2017, compared to 0.9% in 2016. Elsewhere, the IMF projects that overall growth in emerging market countries will accelerate to 4.5% in 2017, versus 4.1% in 2016.

After an extended period of maintaining the federal funds rateiii at a historically low range between zero and 0.25%, the Federal Reserve Board (the “Fed”)iv increased the rate at its meeting on December 16, 2015. This marked the first rate hike since 2006. In particular, the U.S. central bank raised the federal funds rate to a range between 0.25% and 0.50%. The Fed then kept rates on hold at each meeting prior to its meeting in mid-December 2016. On December 14, 2016, the Fed raised rates to a range between 0.50% and 0.75%. In the Fed’s statement after the December meeting it said, “The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.”

Given the economic challenges in the Eurozone, the European Central Bank (“ECB”)v took a number of actions to stimulate growth and ward off deflation. In January 2015, before the reporting period began, the ECB announced that, beginning in March 2015, it would start a €60 billion-per-month bond buying program that was expected to run until September 2016. In December

| | |

| IV | | EnTrustPermal Alternative Select VIT Portfolio |

2015, the ECB extended its monthly bond buying program until at least March 2017. In March 2016, the ECB announced that it would increase its bond purchasing program to €80 billion-per-month. It also lowered its deposit rate to -0.4% and its main interest rate to 0%. Finally, in December 2016 — the ECB again extended its bond buying program until December 2017. From April 2017 through December 2017, the ECB will purchase €60 billion-per-month of bonds. Looking at other developed countries, in the aftermath of the June 2016 U.K. referendum to leave the European Union (“Brexit”), the Bank of England (“BoE”)vi lowered rates in October 2016 from 0.50% to 0.25% — an all-time low. After holding rates steady at 0.10% for more than five years, in January 2016, the Bank of Japanvii announced that it lowered the rate on current accounts that commercial banks hold with it to -0.10%. Elsewhere, the People’s Bank of Chinaviii kept rates steady at 4.35%.

As always, thank you for your confidence in our stewardship of your assets.

Sincerely,

Jane Trust, CFA

President and Chief Executive Officer

January 31, 2017

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. Forecasts and predictions are inherently limited and should not be relied upon as an indication of actual or future performance.

| i | Gross domestic product (“GDP”) is the market value of all final goods and services produced within a country in a given period of time. |

| ii | The International Monetary Fund (“IMF”) is an organization of 189 countries, working to foster global monetary cooperation, secure financial stability, facilitate international trade, promote high employment and sustainable economic growth, and reduce poverty around the world. |

| iii | The federal funds rate is the rate charged by one depository institution on an overnight sale of immediately available funds (balances at the Federal Reserve) to another depository institution; the rate may vary from depository institution to depository institution and from day to day. |

| iv | The Federal Reserve Board (the “Fed”) is responsible for the formulation of U.S. policies designed to promote economic growth, full employment, stable prices and a sustainable pattern of international trade and payments. |

| v | The European Central Bank (“ECB”) is responsible for the monetary system of the European Union and the euro currency. |

| vi | The Bank of England (“BoE”), formally the Governor and Company of the BoE, is the central bank of the United Kingdom. The BoE’s purpose is to maintain monetary and financial stability. |

| vii | The Bank of Japan is the central bank of Japan. The bank is responsible for issuing and handling currency and treasury securities, implementing monetary policy, maintaining the stability of the Japanese financial system and the yen currency. |

| viii | The People’s Bank of China (“PBoC”) is the central bank of the People’s Republic of China with the power to carry out monetary policy and regulate financial institutions in mainland China. |

| | |

| EnTrustPermal Alternative Select VIT Portfolio | | V |

Portfolio overview

Q. What is the Portfolio’s investment strategy?

A. The Portfolio seeks to provide investors with long-term capital appreciation. This multi-manager, multi-strategy Portfolio seeks to achieve long-term capital appreciation while generating attractive risk- adjusted returns. The Portfolio will attempt to produce positive returns over a full market cycle, allocating assets to strategies that historically have had a low correlation to each other and may include Equity Hedge, Event Driven, Global Macro and Relative Value strategies. The Portfolio will also attempt to limit declines during equity market corrections with lower overall Portfolio volatility.

In seeking to meet its investment goal, the Portfolio implements a tactical asset allocation program of alternative strategies overseen by the Portfolio’s manager, EnTrustPermal Management LLC (“EnTrustPermal” or the “manager”), through which the Portfolio will allocate its assets among a number of alternative investment strategies implemented by multiple unaffiliated and affiliated investment subadvisers and trading advisors. EnTrustPermal may also manage Portfolio assets directly to seek return, or to implement various market hedges.

Allocations to each of the investment strategies are expected to range from 0% to 50% of the Portfolio’s net assets. Multiple subadvisers may be utilized to gain access to different investment approaches within each category and EnTrustPermal may manage Portfolio assets directly within each category. Ongoing decisions by EnTrustPermal to allocate Portfolio assets among strategies will be based on a continuous evaluation of market conditions. Due to its assessment of prevailing market conditions, the manager may emphasize certain strategies and investment themes that the manager believes are more likely to produce positive returns.

The manager and the subadvisers implement the various alternative investment strategies by investing in a wide variety of securities of companies of any market capitalization and other financial instruments available in both U.S. and non-U.S. markets, including emerging markets. The financial instruments in which the manager and the subadvisers may invest include, but are not limited to: common stock; preferred stock; rights and warrants to purchase common stock and depositary receipts; convertible debt; loans (including collateralized loan obligations (“CLOs”); mortgage-backed securities, including collateralized mortgage obligations (“CMOs”); loan participations; trade claims; convertible securities; debt securities of governments (including the U.S. government) as well as their agencies and/or instrumentalities; debt securities of corporations throughout the world (including U.S. corporations); debt securities of any credit quality and maturity, including debt securities below investment grade; collateralized debt obligations (“CDOs”); collateralized bond obligations (“CBOs”); exchange-traded notes (“ETNs”); investment companies, including exchange-traded funds (“ETFs”); partnership interests, including master limited partnerships (“MLPs”); royalty trusts; mortgage-backed and asset-backed securities; other pooled investment vehicles, including real estate investment trusts (“REITs”)i; foreign currencies; and repurchase agreements. The Portfolio may invest in private placements. The Portfolio may also invest in various types of

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 1 |

Portfolio overview (cont’d)

derivatives, including swaps, such as credit default swaps, total return swaps, interest rate swaps, swaps on credit indices and variance swaps, futures, options, forward contracts on currencies and commodities and indexed and inverse securities. Any of these derivatives may be used in an effort to gain economic exposure to one or more alternative investment strategies, to enhance returns, or to hedge the Portfolio’s positions by managing or adjusting the risk profile of the Portfolio or its individual positions.

The Portfolio may obtain synthetic exposure to investment strategies through the use of one or more total return swaps through which the Portfolio makes payments to a counterparty (at either a fixed or variable rate) in exchange for receiving from the counterparty payments that reflect the return of a “basket” of securities, derivatives or commodity interests representing a particular index sponsored by a third-party investment manager identified by the manager.

Q. What were the overall market conditions during the Portfolio’s reporting period?

A. The first quarter of 2016 began with a continuation of last year’s market turmoil, as concerns of a U.S. recession dominated headlines. Additionally, fears surrounding decelerating worldwide growth – in China, in particular – and the impact on demand for energy and other commodities drove prices lower across most global risk assets. Equity markets and commodity prices continued to display a high degree of positive correlation. Within the first six weeks of the quarter, the MSCI World Indexii plunged almost 12% and West Texas Intermediate (“WTI”) crude oil prices bottomed at $26.21 per barrel, with government bonds and gold benefiting from the risk-off environment. During the second half of the quarter, the tone reversed sharply amid additional stimulus from the European Central Bank (“ECB”)iii as well as the Federal Reserve Board (the “Fed”)iv lowering its median projected expectation for the pace of further rate increases. U.S. interest rates moved lower across most maturities, with the ten-year Treasury yield ending the quarter down 49 basis pointsv at 1.78% after reaching a low of 1.64% in February 2016. The Fed’s more cautious stance, as well as crude oil finding a price floor, provided upward support to a highly volatile U.S equity market, which ended the quarter in positive territory. The outlook for oil prices improved as major producers were said to be in talks regarding capping production, and with U.S. economic data assuaging concerns regarding a near-term downturn. Similarly, U.S. high yield bond and leveraged loan indices more than recovered the losses suffered in the first two months of the year. The fundamental outlook for the U.S. economy remained relatively solid, with the February 2016 non-farm payrolls report exceeding consensus expectations as well as an upward revision of second quarter 2016 gross domestic product (“GDP”)vi growth to 1.4% from the previous 0.7% estimate earlier in the quarter.

During the second quarter of 2016, the global economy showed signs of stabilization, providing a foundation for equity markets to register modest gains despite heightened volatility around the U.K referendum to leave the European Unio (“Brexit”) vote in late-June 2016. The Brexit referendum resulted in 52% of British voters expressing a desire to leave the 28-nation bloc while 48% voted to stay. Subsequently, British Prime Minister David Cameron

| | |

| 2 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

announced his resignation and global equity markets suffered a sharp drawdown due to uncertainty over future economic implications. U.K. bank shares plummeted amid broad recession fears and the British pound plunged 7% against the U.S. dollar to 30-year lows. While market volatility spiked immediately after the referendum, a strong bounce-back rally erased the majority of losses. Despite the somewhat defensive market tone, most risk assets posted gains during the quarter. Beaten-down commodities staged a strong recovery, with WTI crude oil gaining 26% over the second quarter 2016, ending June 2016 above $48 a barrel. Gold ended up almost 7% for the quarter, benefiting from anticipation of continued easing by global central banks and functioning as a safe haven asset amid continued geopolitical uncertainty. Within U.S. equities, investors favored high dividend-paying sectors — such as Utilities and Consumer Staples — which posted strong gains in a low rate environment, with cyclicals lagging the broader market.

Early in the third quarter of 2016, risk assets extended the rally that began after the Brexit referendum vote, boosted by strong economic data, better-than-expected corporate earnings results, and expectations that global central banks would continue to provide monetary stimulus. In the aftermath of the Brexit referendum, focus shifted to a busy quarter for central banks and continuing speculation about politics. September 2016 was marked by a series of central bank meetings, starting with the ECB, and continuing with the Bank of Japan (“BOJ”)vii and the Fed. After the ECB held steady on rates and quantitative easing, the BOJ made some technical changes that amounted to very little. In an apparent attempt to shift the burden of action onto the fiscal authorities, the BOJ announced a “cap” on ten-year Japanese Government Bond rates at 0%. Finally, after weeks of speculation and conflicting statements from various governors and regional presidents, the Fed, too, held steady, deferring any rate hike to December 2016 or beyond. At the end of the third quarter of 2016, the total market value of negative-yielding global debt fell to $10.7 trillion, and longer-term bond yields rose modestly, cooling off the recent rally in bond-proxy assets such as the REITs, Utilities, and Consumer Staples sectors. U.S. yields remained higher than most of their developed market peers, with the yield on the benchmark ten-year Treasury note rising from 1.47% to 1.59%, though yields peaked at 1.72% in mid-September 2016. Due to the modest yield increase, the Bloomberg Barclays U.S. Aggregate Indexviii produced a muted gain of 0.46% for the quarter. Global corporate bonds performed strongly over the quarter as the Bloomberg Barclays U.S. Corporate Bond Indexix rose by 1.43%, while the BofA Merrill Lynch U.S. High Yield Indexx generated 5.49%, benefiting from spreads tightening beyond historical average levels. Global equity markets recovered from the Brexit sell-off during the third quarter of 2016, which was marked by significantly lower volatility compared to the first half of the year. U.K. equities meaningfully rebounded against a more stable political backdrop, as Theresa May was confirmed as Prime Minister, with weakness in the sterling pound also serving as a tailwind. U.S. equities benefited from the “risk on” environment and posted strong gains over the quarter with the S&P 500 Indexxi and Russell 2000 Indexxii advancing 3.85% and 9.04%, respectively. At the end of the

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 3 |

Portfolio overview (cont’d)

period, U.S. second quarter of 2016 GDP growth was revised up to a 1.40% gain.

In the last quarter of the year, markets were shaped by speculation and the result of the long-awaited outcome of the U.S. presidential election. Markets responded dramatically to Donald Trump’s win, with a rotation from growth to value and defensives to cyclicals. Another of the resulting consequences was a rising U.S. dollar — especially against developed market currencies such as the yen and the euro. The foreign exchange markets also saw the sterling pound continue to fall on renewed concerns surrounding the U.K.’s exit from the European Union. Meanwhile, China continued to allow the yuan to slip lower, with the currencies of neighboring countries such as Singapore and Korea dropping in sympathy. The December 2016 U.S. rate hike, which was widely expected following the results of the U.S. presidential election, had little effect on markets. In general, the environment was positive for equities. Credit markets also held firm and spreads generally narrowed with riskier, higher-yielding names outperforming. Government bond yields rose, however, especially in longer-dated issues, as central banks in developed markets made their desire for steeper yield curvesxiii clear.

Q. How did we respond to these changing market conditions?

A. The Portfolio began the period with five different subadvisers across three different strategies. As of January 1, 2016, the Portfolio was overweight Global Macro almost entirely at the expense of Relative Value, while being just above market weight Equity Hedge, and just below market weight Event Driven relative to the HFRX Global Hedge Fund Index weights. Global Macro was 41.2% of Portfolio’s net assets, Equity Hedge was 30.9% and Event Driven was 26.0%.

Several changes were made in the period. In February 2016, Apex Capital LLC communicated their intent to restructure into a family office and return outside capital at month-end. In March 2016, First Quadrant L.P., a new sub-advisor focused on Systematic Macro, was funded. In April 2016, Electron Capital Partners, LLC, a new sub-advisor focused on Global Long/Short Equity in the Utilities Sector was funded. In June 2016, River Canyon Fund Management LLC, and TT International were fully redeemed. The decision to redeem from the Event Driven strategy (previously subadvised by River Canyon) was due to concerns around liquidity in the credit markets. The decision to redeem from the Global Macro strategy (previously subadvised by TT International) was based on a negative outlook for the trading opportunities in the currency and fixed income markets in that sleeve going forward.

All of these changes resulted in a portfolio with four different subadvisers across two different strategies at the end of the period. The Portfolio was materially overweight Global Macro and Equity Hedge at the expense of zero allocations to Event Driven and Relative Value. Global Macro was 44.9% of Portfolio net assets and Equity Hedge was 45.4%.

The Portfolio uses derivatives for a variety of reasons. During the reporting period, the Portfolio traded options, futures, swaps and forward currency contracts. The net result of the Portfolio’s derivative trading activity, both in terms of realized and unrealized gains/losses, was a positive impact on Portfolio performance.

| | |

| 4 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

Performance review

For the twelve months ended December 31, 2016, Class II shares of EnTrustPermal Alternative Select VIT Portfolio1 returned -2.62%. The Portfolio’s unmanaged benchmarks, the HFRX Global Hedge Fund Index, and the Citigroup 3-Month U.S. Treasury Bill Indexxiv returned 2.50% and 0.27% respectively, for the same period. The Lipper Variable Alternative Other Funds Category Average2 returned 6.29% for the same period.

| | | | | | | | |

Performance Snapshot as of December 31, 2016

(unaudited) | |

| | | 6 months | | | 12 months | |

EnTrustPermal Alternative Select VIT Portfolio1: | | | | | | | | |

Class II | | | 1.78 | % | | | -2.62 | % |

| HFRX Global Hedge Fund Index | | | 3.36 | % | | | 2.50 | % |

Citigroup 3-Month U.S. Treasury Bill Index | | | 0.15 | % | | | 0.27 | % |

| Lipper Variable Alternative Other Funds Category Average2 | | | 3.01 | % | | | 6.29 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value, investment returns and yields will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost.

Portfolio return assumes the reinvestment of all distributions at net asset value and the deduction of all Portfolio expenses. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

Portfolio performance figures reflect fee waivers and/or expense reimbursements, without which the performance would have been lower.

|

| Total Annual Operating Expenses (unaudited) |

As of the Portfolio’s current prospectus dated May 1, 2016, the gross total annual fund operating expense ratio for Class II shares was 4.77%.

Actual expenses may be higher. For example, expenses may be higher than those shown if average net assets decrease. Net assets are more likely to decrease and Portfolio expense ratios are more likely to increase when markets are volatile.

As a result of an expense limitation arrangement, the ratio of total annual fund operating expenses (other than taxes; interest; extraordinary expenses; brokerage commissions and expenses; fees, costs and expenses associated with any prime brokerage arrangement (including the costs of any securities borrowing arrangement); acquired fund fees and expenses; and dividend and interest expenses on securities sold short) to average net assets will not exceed 2.70% for Class II shares. This expense limitation arrangement cannot be terminated prior to December 31, 2018 without the Board of Trustees’ consent.

The manager is permitted to recapture amounts waived and/or reimbursed to the class during the same fiscal year if the class’ total annual operating expenses have fallen to a level below the expense

| 1 | The Portfolio is an underlying investment option of various variable annuity and variable life insurance products. The Portfolio’s performance returns do not reflect the deduction of expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the performance of the Portfolio. Past performance is no guarantee of future results. |

| 2 | Lipper, Inc., a wholly-owned subsidiary of Reuters, provides independent insight on global collective investments. Returns are based on the period ended December 31, 2016, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 98 funds for the six-month period and among the 97 funds for the twelve-month period in the Portfolio’s Lipper category. |

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 5 |

Portfolio overview (cont’d)

limitation (“expense cap”) in effect at the time the fees were earned or the expenses incurred. In no case will the manager recapture any amount that would result, on any particular business day of the Portfolio, in the class’ total annual operating expenses exceeding the expense cap or any other lower limit then in effect.

Q. What were the leading contributors to performance?

A. Three subadvisers contributed positively to performance relative to their HFRX Global Hedge Fund Index sub-indices, BH-DG Systematic Trading LLC (Systematic Macro), First Quadrant L.P. (Systematic Macro) and Atlantic Investment Management, Inc. (Equity Hedge). More specifically, tactical currency trading, particularly in the Japanese yen, proved profitable for the Systematic Macro managers while long exposure in the Industrials sector drove gains for the Equity Hedge managers.

Q. What were the leading detractors from performance?

A. Relative to the HFRX Global Hedge Fund Index, the Portfolio’s strategy allocation decisions detracted from performance during the reporting period. From a manager selection perspective, the aggregate effect also detracted from excess returns above the HRFX Global Hedge Fund Index. On the subadviser level, four of the seven managers used to manage the Portfolio during the reporting period lagged their respective HFRX Global Hedge Fund Index sub-index. The decision by Apex Capital LLC to return capital to investors in mid-February 2016 at the bottom of the market correction also led to underperformance, as there was a cash drag during the market recovery at the portfolio level until proceeds could be redeployed in an efficient manner to other subadvisers.

Thank you for your investment in EnTrustPermal Alternative Select VIT Portfolio. As always, we appreciate that you have chosen us to manage your assets.

Sincerely,

Robert Kaplan

Co-Portfolio Manager

EnTrustPermal Management LLC

Christopher Zuehlsdorff, CFA

Co-Portfolio Manager

EnTrustPermal Management LLC

January 21, 2017

RISKS: The Portfolio’s investment strategies and portfolio investments differ from those of many other mutual funds. The manager and the subadvisers may devote significant portions of the Portfolio’s assets to pursuing investment opportunities or strategies, including through the use of derivatives, that may create a form of investment leverage in the Portfolio. This approach to investing may make the Portfolio a more volatile investment option than other mutual funds and cause the Portfolio to perform less favorably than other mutual funds under similar market or other conditions.

The Portfolio utilizes alternative hedge strategies, which involve highly speculative investments that employ aggressive investment strategies and carry substantial risk. The Portfolio, and the subadvised

| | |

| 6 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

strategies, may employ leverage, which increases the volatility of investment returns and subjects the Portfolio to magnified losses if the Portfolio’s investments decline in value. The Portfolio and the subadvisers may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Portfolio performance. The Portfolio and some of the subadvisers may employ short selling which is a speculative strategy. Unlike the possible loss on a security that is purchased, there is no limit on the amount of loss on an appreciating security that is sold short. The Portfolio and each subadviser may engage in active and frequent trading, resulting in higher portfolio turnover and transaction costs. There is no assurance strategies used by the Portfolio or subadvised funds will be successful. Equity securities are subject to market and price fluctuations. International investments are subject to special risks including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks. Fixed income securities involve interest rate, credit, inflation, and reinvestment risks. As interest rates rise, the value of fixed income securities falls. High-yield (“junk”) bonds possess greater price volatility, illiquidity, and possibility of default than higher-grade bonds. The Portfolio is classified as “non-diversified,” which means it may invest a larger percentage of its assets in a smaller number of issuers than a diversified fund. Please see the prospectus for a more complete discussion of these and other risks and the Portfolio’s investment strategies.

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 7 |

Portfolio overview (cont’d)

| i | Real estate investment trusts (“REITs”) invest in real estate or loans secured by real estate and issue shares in such investments, which can be illiquid. |

| ii | The MSCI World Index is an unmanaged index considered representative of growth stocks of developed countries. Index performance is calculated with net dividends. |

| iii | The European Central Bank (“ECB”) is responsible for the monetary system of the European Union and the euro currency. |

| iv | The Federal Reserve Board (the “Fed”) is responsible for the formulation of U.S. policies designed to promote economic growth, full employment, stable prices and a sustainable pattern of international trade and payments. |

| v | A basis point is one-hundredth (1/100 or 0.01) of one percent. |

| vi | Gross domestic product (“GDP”) is the market value of all final goods and services produced within a country in a given period of time. |

| vii | The Bank of Japan is the central bank of Japan. The bank is responsible for issuing and handling currency and treasury securities, implementing monetary policy, maintaining the stability of the Japanese financial system and the yen currency. |

| viii | The Bloomberg Barclays U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| ix | The Bloomberg Barclays U.S. Corporate Index measures the investment grade, fixed rate, taxable corporate bond, market. It includes USD-Denominated securities publicly issued by U.S. and non-U.S. industrial and financial issuers. |

| x | The BofA Merrill Lynch U.S. High Yield Index tracks the performance of US dollar denominated below investment grade corporate debt publicly issued in the U.S. domestic market. |

| xi | The S&P 500 Index is an unmanaged index of 500 stocks and is generally representative of the performance of larger companies in the U.S. |

| xii | The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 is a subset of the Russell 3000 Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the U.S. equity market. |

| xiii | The yield curve is the graphical depiction of the relationship between the yield on bonds of the same credit quality but different maturities. |

| xiv | The Citigroup 3-Month U.S. Treasury Bill Index is an unmanaged index generally representative of the average yield of 3-month U.S. Treasury bills. |

| | |

| VIII | | EnTrustPermal Alternative Select VIT Portfolio |

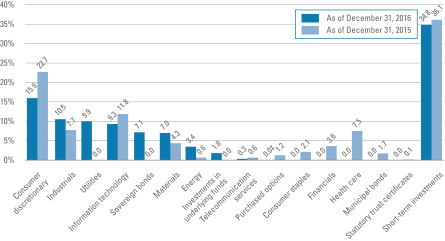

Portfolio at a glance (unaudited)

Investment breakdown† (%) as a percent of total investments

| † | The bar graph above represents the composition of the Portfolio’s investments as of December 31, 2016 and December 31, 2015 and does not include derivatives such as written options, futures contracts, swap contracts and forward foreign currency contracts. The Portfolio is actively managed. As a result, the composition of the Portfolio’s investments is subject to change at any time. |

| ‡ | Represents less than 0.1%. |

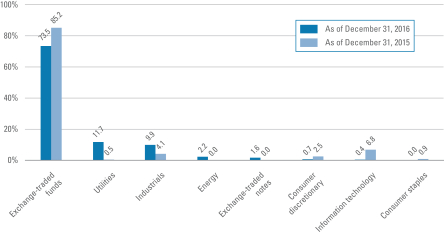

Securities sold short breakdown* (%) as a percent of total securities sold short

| * | The bar graph above represents the composition of the Portfolio’s securities sold short as of December 31, 2016 and December 31, 2015 and does not include derivatives. The Portfolio is actively managed. As a result, the composition of the Portfolio’s securities sold short is subject to change at any time. |

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 9 |

Portfolio expenses (unaudited)

Example

As a shareholder of the Portfolio, you may incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on July 1, 2016 and held for the six months ended December 31, 2016.

Actual expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period“.

Hypothetical example for comparison purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other funds. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Based on actual total return1 | | | | | | Based on hypothetical total return1 | |

| | | Actual

Total Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio | | | Expenses

Paid

During

the

Period3 | | | | | | | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio | | | Expenses

Paid

During

the

Period3 | |

| Class II | | | 1.78 | % | | $ | 1,000.00 | | | $ | 1,017.80 | | | | 3.30 | % | | $ | 16.74 | | | | | | | Class II | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,008.55 | | | | 3.30 | % | | $ | 16.66 | |

| 1 | For the six months ended December 31, 2016. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total return does not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total return. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to the class’ annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 366. |

| | |

| 10 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

Portfolio performance (unaudited)

| | | | |

| Average annual total returns1 | | | |

| | | Class II | |

| Twelve Months Ended 12/31/16 | | | -2.62 | % |

| Inception* through 12/31/16 | | | -2.95 | |

| | | | |

| Cumulative total returns1 | | | |

| Class II (Inception date of 10/6/14 through 12/31/16) | | | -6.47 | % |

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower.

| 1 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. |

| * | Inception date for Class II is October 6, 2014. |

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 11 |

Portfolio performance (unaudited) (cont’d)

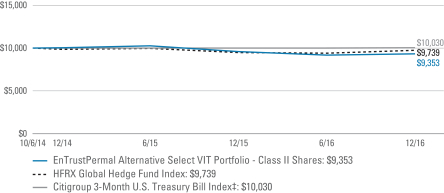

Historical performance

Value of $10,000 invested in

Class II Shares of EnTrustPermal Alternative Select VIT Portfolio vs. HFRX Global Hedge Fund Index and Citigroup 3-Month U.S. Treasury Bill Index† — October 6, 2014 - December 2016

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower.

| † | Hypothetical illustration of $10,000 invested in Class II shares of EnTrustPermal Alternative Select VIT Portfolio at inception on October 6, 2014, assuming the reinvestment of all distributions, including returns of capital, if any, at net asset value through December 31, 2016. The hypothetical illustration also assumes a $10,000 investment, as applicable, in the HFRX Global Hedge Fund Index and Citigroup 3-Month U.S. Treasury Bill Index. The HFRX Global Hedge Fund Index is designed to be representative of the overall composition of the hedge fund universe. It is comprised of all eligible hedge fund strategies; including but not limited to convertible arbitrage, distressed securities, equity hedge, equity market neutral, event-driven, macro, merger arbitrage, and relative value arbitrage. The strategies are asset weighted based on the distribution of assets in the hedge fund industry. The Citigroup 3-Month U.S. Treasury Bill Index is an unmanaged index generally representative of the average yield of 3-Month U.S. Treasury Bills. The Indices are unmanaged and are not subject to the same management and trading expenses as a mutual fund. Please note that an investor cannot invest directly in an index. |

| ‡ | Citigroup 3-Month U.S. Treasury Bill Index is as of month end September 30, 2014. |

| | |

| 12 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

Consolidated schedule of investments

December 31, 2016

EnTrustPermal Alternative Select VIT Portfolio

| | | | | | | | | | | | | | | | |

| Security | | | | | | | | Shares | | | Value | |

| Common Stocks — 37.4% | | | | | | | | | | | | | | | | |

| Consumer Discretionary — 9.7% | | | | | | | | | | | | | | | | |

Auto Components — 5.9% | | | | | | | | | | | | | | | | |

GKN PLC | | | | | | | | | | | 147,784 | | | $ | 602,026 | (a) |

Goodyear Tire & Rubber Co. | | | | | | | | | | | 14,868 | | | | 458,975 | (b) |

Koito Manufacturing Co., Ltd. | | | | | | | | | | | 5,100 | | | | 269,306 | (a) |

Magna International Inc. | | | | | | | | | | | 5,776 | | | | 250,678 | |

NGK Spark Plug Co., Ltd. | | | | | | | | | | | 25,600 | | | | 566,692 | (a) |

Total Auto Components | | | | | | | | | | | | | | | 2,147,677 | |

Household Durables — 2.3% | | | | | | | | | | | | | | | | |

Harman International Industries Inc. | | | | | | | | | | | 7,574 | | | | 841,926 | (b) |

Specialty Retail — 1.5% | | | | | | | | | | | | | | | | |

Asbury Automotive Group Inc. | | | | | | | | | | | 4,584 | | | | 282,833 | * |

Office Depot Inc. | | | | | | | | | | | 56,491 | | | | 255,339 | |

Total Specialty Retail | | | | | | | | | | | | | | | 538,172 | |

Total Consumer Discretionary | | | | | | | | | | | | | | | 3,527,775 | |

| Energy — 2.3% | | | | | | | | | | | | | | | | |

Energy Equipment & Services — 0.6% | | | | | | | | | | | | | | | | |

Baker Hughes Inc. | | | | | | | | | | | 830 | | | | 53,925 | |

Halliburton Co. | | | | | | | | | | | 1,002 | | | | 54,198 | |

Schlumberger Ltd. | | | | | | | | | | | 646 | | | | 54,232 | |

Tenaris SA, ADR | | | | | | | | | | | 1,605 | | | | 57,315 | |

Total Energy Equipment & Services | | | | | | | | | | | | | | | 219,670 | |

Oil, Gas & Consumable Fuels — 1.7% | | | | | | | | | | | | | | | | |

Cheniere Energy Inc. | | | | | | | | | | | 4,069 | | | | 168,579 | * |

China Suntien Green Energy Corp., Ltd., Class H Shares | | | | | | | | | | | 257,000 | | | | 32,912 | (a) |

Cosan Ltd., Class A Shares | | | | | | | | | | | 7,083 | | | | 53,193 | |

GasLog Ltd. | | | | | | | | | | | 1,442 | | | | 23,216 | |

Golar LNG Ltd. | | | | | | | | | | | 2,784 | | | | 63,865 | |

Hoegh LNG Holdings Ltd. | | | | | | | | | | | 4,902 | | | | 54,744 | (a) |

PetroChina Co., Ltd., Class H Shares | | | | | | | | | | | 294,548 | | | | 217,348 | (a) |

Total Oil, Gas & Consumable Fuels | | | | | | | | | | | | | | | 613,857 | |

Total Energy | | | | | | | | | | | | | | | 833,527 | |

| Industrials — 7.2% | | | | | | | | | | | | | | | | |

Aerospace & Defense — 1.4% | | | | | | | | | | | | | | | | |

Triumph Group Inc. | | | | | | | | | | | 18,841 | | | | 499,286 | (b) |

Building Products — 0.3% | | | | | | | | | | | | | | | | |

Daikin Industries Ltd. | | | | | | | | | | | 1,202 | | | | 110,079 | (a) |

See Notes to Consolidated Financial Statements.

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 13 |

Consolidated schedule of investments (cont’d)

December 31, 2016

EnTrustPermal Alternative Select VIT Portfolio

| | | | | | | | | | | | | | | | |

| Security | | | | | | | | Shares | | | Value | |

Commercial Services & Supplies — 0.9% | | | | | | | | | | | | | | | | |

Advanced Disposal Services Inc. | | | | | | | | | | | 8,637 | | | $ | 191,914 | * |

China Everbright International Ltd. | | | | | | | | | | | 136,574 | | | | 154,088 | (a) |

Total Commercial Services & Supplies | | | | | | | | | | | | | | | 346,002 | |

Construction & Engineering — 0.5% | | | | | | | | | | | | | | | | |

Beijing Urban Construction Design & Development Group Co., Ltd., Class H Shares | | | | | | | | | | | 179,664 | | | | 110,874 | (a)(c) |

Dycom Industries Inc. | | | | | | | | | | | 914 | | | | 73,385 | * |

Total Construction & Engineering | | | | | | | | | | | | | | | 184,259 | |

Electrical Equipment — 0.6% | | | | | | | | | | | | | | | | |

ABB Ltd., Registered Shares | | | | | | | | | | | 10,242 | | | | 215,608 | (a) |

Philips Lighting NV | | | | | | | | | | | 550 | | | | 13,543 | *(a)(c) |

Total Electrical Equipment | | | | | | | | | | | | | | | 229,151 | |

Machinery — 1.6% | | | | | | | | | | | | | | | | |

Kurita Water Industries Ltd. | | | | | | | | | | | 13,800 | | | | 303,147 | (a) |

Mueller Water Products Inc., Class A Shares | | | | | | | | | | | 9,216 | | | | 122,665 | |

SMC Corp. | | | | | | | | | | | 431 | | | | 102,566 | (a) |

Xylem Inc. | | | | | | | | | | | 1,198 | | | | 59,325 | |

Total Machinery | | | | | | | | | | | | | | | 587,703 | |

Professional Services — 0.5% | | | | | | | | | | | | | | | | |

Randstad Holding NV | | | | | | | | | | | 3,047 | | | | 165,033 | (a) |

Road & Rail — 0.6% | | | | | | | | | | | | | | | | |

Union Pacific Corp. | | | | | | | | | | | 1,988 | | | | 206,116 | |

Trading Companies & Distributors — 0.3% | | | | | | | | | | | | | | | | |

Mitsubishi Corp. | | | | | | | | | | | 5,260 | | | | 111,771 | (a) |

Transportation Infrastructure — 0.5% | | | | | | | | | | | | | | | | |

OHL Mexico SAB de CV | | | | | | | | | | | 169,247 | | | | 166,474 | |

Total Industrials | | | | | | | | | | | | | | | 2,605,874 | |

| Information Technology — 6.4% | | | | | | | | | | | | | | | | |

Communications Equipment — 1.5% | | | | | | | | | | | | | | | | |

ARRIS International PLC | | | | | | | | | | | 6,193 | | | | 186,595 | * |

CommScope Holding Co. Inc. | | | | | | | | | | | 9,114 | | | | 339,041 | * |

Total Communications Equipment | | | | | | | | | | | | | | | 525,636 | |

Electronic Equipment, Instruments & Components — 1.4% | | | | | | | | | | | | | | | | |

Hitachi Ltd. | | | | | | | | | | | 21,409 | | | | 115,353 | (a) |

Murata Manufacturing Co., Ltd. | | | | | | | | | | | 795 | | | | 105,868 | (a) |

Osaki Electric Co., Ltd. | | | | | | | | | | | 5,536 | | | | 57,565 | (a) |

Universal Display Corp. | | | | | | | | | | | 594 | | | | 33,442 | * |

VeriFone Systems Inc. | | | | | | | | | | | 10,789 | | | | 191,289 | * |

Total Electronic Equipment, Instruments & Components | | | | | | | | | | | | | | | 503,517 | |

See Notes to Consolidated Financial Statements.

| | |

| 14 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

EnTrustPermal Alternative Select VIT Portfolio

| | | | | | | | | | | | | | | | |

| Security | | | | | | | | Shares | | | Value | |

Internet Software & Services — 0.2% | | | | | | | | | | | | | | | | |

NetEase Inc., ADR | | | | | | | | | | | 302 | | | $ | 65,033 | |

IT Services — 2.3% | | | | | | | | | | | | | | | | |

Atos SE | | | | | | | | | | | 4,929 | | | | 519,973 | (a) |

ITOCHU Techno-Solutions Corp. | | | | | | | | | | | 12,600 | | | | 327,257 | (a) |

Total IT Services | | | | | | | | | | | | | | | 847,230 | |

Software — 0.2% | | | | | | | | | | | | | | | | |

Silver Spring Networks Inc. | | | | | | | | | | | 5,240 | | | | 69,744 | * |

Technology Hardware, Storage & Peripherals — 0.8% | | | | | | | | | | | | | | | | |

Diebold Nixdorf Inc. | | | | | | | | | | | 11,410 | | | | 286,961 | |

Total Information Technology | | | | | | | | | | | | | | | 2,298,121 | |

| Materials — 4.8% | | | | | | | | | | | | | | | | |

Chemicals — 2.4% | | | | | | | | | | | | | | | | |

Albemarle Corp. | | | | | | | | | | | 860 | | | | 74,029 | |

Eastman Chemical Co. | | | | | | | | | | | 9,281 | | | | 698,024 | (b) |

Shin-Etsu Chemical Co., Ltd. | | | | | | | | | | | 1,468 | | | | 113,139 | (a) |

Total Chemicals | | | | | | | | | | | | | | | 885,192 | |

Construction Materials — 0.2% | | | | | | | | | | | | | | | | |

Cemex SAB de CV, Participation Certificates, ADR | | | | | | | | | | | 3,592 | | | | 28,844 | * |

Forterra Inc. | | | | | | | | | | | 1,189 | | | | 25,753 | * |

Total Construction Materials | | | | | | | | | | | | | | | 54,597 | |

Containers & Packaging — 2.1% | | | | | | | | | | | | | | | | |

Owens-Illinois Inc. | | | | | | | | | | | 44,175 | | | | 769,087 | *(b) |

Metals & Mining — 0.1% | | | | | | | | | | | | | | | | |

China Molybdenum Co., Ltd., Class H Shares | | | | | | | | | | | 156,057 | | | | 37,935 | (a) |

Total Materials | | | | | | | | | | | | | | | 1,746,811 | |

| Telecommunication Services — 0.2% | | | | | | | | | | | | | | | | |

Diversified Telecommunication Services — 0.2% | | | | | | | | | | | | | | | | |

China Unicom (Hong Kong) Ltd. | | | | | | | | | | | 60,000 | | | | 69,701 | (a) |

| Utilities — 6.8% | | | | | | | | | | | | | | | | |

Electric Utilities — 4.2% | | | | | | | | | | | | | | | | |

Avangrid Inc. | | | | | | | | | | | 5,845 | | | | 221,409 | |

Companhia Energetica de Minas Gerais, ADR | | | | | | | | | | | 44,301 | | | | 101,006 | |

Enel SpA | | | | | | | | | | | 65,723 | | | | 289,222 | (a) |

Eversource Energy | | | | | | | | | | | 2,718 | | | | 150,115 | |

Exelon Corp. | | | | | | | | | | | 10,512 | | | | 373,071 | |

NextEra Energy Inc. | | | | | | | | | | | 702 | | | | 83,861 | |

Pampa Energia SA, ADR | | | | | | | | | | | 4,195 | | | | 146,028 | * |

Power Assets Holdings Ltd. | | | | | | | | | | | 17,903 | | | | 157,725 | (a) |

Total Electric Utilities | | | | | | | | | | | | | | | 1,522,437 | |

See Notes to Consolidated Financial Statements.

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 15 |

Consolidated schedule of investments (cont’d)

December 31, 2016

EnTrustPermal Alternative Select VIT Portfolio

| | | | | | | | | | | | | | | | |

| Security | | | | | | | | Shares | | | Value | |

Gas Utilities — 0.4% | | | | | | | | | | | | | | | | |

Italgas SpA | | | | | | | | | | | 41,026 | | | $ | 161,429 | * |

Independent Power and Renewable Electricity Producers — 0.2% | |

Huadian Power International Corp. Ltd., Class H Shares | | | | | | | | | | | 43,540 | | | | 19,667 | (a) |

Huaneng Power International Inc., Class H Shares | | | | | | | | | | | 58,817 | | | | 38,869 | (a) |

Total Independent Power and Renewable Electricity Producers | | | | | | | | | | | | 58,536 | |

Multi-Utilities — 1.5% | | | | | | | | | | | | | | | | |

Dominion Resources Inc. | | | | | | | | | | | 2,762 | | | | 211,542 | |

E.ON SE | | | | | | | | | | | 10,946 | | | | 76,346 | (a) |

Hera SpA | | | | | | | | | | | 76,505 | | | | 176,315 | (a) |

Innogy SE | | | | | | | | | | | 2,277 | | | | 79,169 | *(a)(c) |

Total Multi-Utilities | | | | | | | | | | | | | | | 543,372 | |

Water Utilities — 0.5% | | | | | | | | | | | | | | | | |

Beijing Enterprises Water Group Ltd. | | | | | | | | | | | 153,025 | | | | 100,909 | (a) |

Guangdong Investment Ltd. | | | | | | | | | | | 52,560 | | | | 68,983 | (a) |

Total Water Utilities | | | | | | | | | | | | | | | 169,892 | |

Total Utilities | | | | | | | | | | | | | | | 2,455,666 | |

Total Common Stocks (Cost — $12,503,651) | | | | | | | | | | | | | | | 13,537,475 | |

| Investments in Underlying Funds — 1.3% | | | | | | | | | | | | | | | | |

Global X MSCI Colombia ETF | | | | | | | | | | | 2,264 | | | | 20,648 | |

iShares Trust — iShares Russell 2000 ETF | | | | | | | | | | | 1,452 | | | | 195,802 | |

Nomura TOPIX ETF | | | | | | | | | | | 7,452 | | | | 98,979 | (a) |

SPDR Dow Jones Industrial Average ETF Trust | | | | | | | | | | | 707 | | | | 139,639 | |

Total Investments in Underlying Funds (Cost — $438,117) | | | | 455,068 | |

| | | | |

| | | Rate | | | | | | | | | | |

| Preferred Stocks — 1.1% | | | | | | | | | | | | | | | | |

| Consumer Discretionary — 1.1% | | | | | | | | | | | | | | | | |

Auto Components — 1.1% | | | | | | | | | | | | | | | | |

Schaeffler AG (Cost — $397,050) | | | 1.625 | % | | | | | | | 27,286 | | | | 402,719 | (a) |

| | | | |

| | | | | | Maturity

Date | | | Face

Amount† | | | | |

| Sovereign Bonds — 4.8% | | | | | | | | | | | | | | | | |

Canada — 2.0% | | | | | | | | | | | | | | | | |

Canada Treasury Bills | | | 0.438 | % | | | 2/23/17 | | | | 980,000 | CAD | | | 729,462 | (d) |

Germany — 1.1% | | | | | | | | | | | | | | | | |

German Treasury Bills | | | -1.573 | % | | | 1/25/17 | | | | 386,000 | EUR | | | 406,575 | (d)(e) |

United Kingdom — 1.7% | | | | | | | | | | | | | | | | |

United Kingdom Treasury Gilt, Bonds | | | 0.220 | % | | | 5/15/17 | | | | 500,000 | GBP | | | 615,595 | (d) |

Total Sovereign Bonds (Cost — $1,821,238) | | | | | | | | | | | | | | | 1,751,632 | |

See Notes to Consolidated Financial Statements.

| | |

| 16 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

EnTrustPermal Alternative Select VIT Portfolio

| | | | | | | | | | | | | | | | |

| Security | | | | | Expiration

Date | | | Contracts | | | Value | |

| Purchased Options — 0.0% | | | | | | | | | | | | | | | | |

Tesla Motors Inc., Put @ $160.00 | | | | | | | 1/20/17 | | | | 6 | | | $ | 138 | |

Tesla Motors Inc., Put @ $160.00 | | | | | | | 3/17/17 | | | | 5 | | | | 1,200 | |

Tesla Motors Inc., Put @ $180.00 | | | | | | | 1/20/17 | | | | 4 | | | | 292 | |

Total Purchased Options (Cost — $12,230) | | | | | | | | | | | | | | | 1,630 | |

Total Investments before Short-Term Investments (Cost — $15,172,286) | | | | 16,148,524 | |

| | | | |

| | | Rate | | | Maturity

Date | | | Face

Amount † | | | | |

| Short-Term Investments — 23.8% | | | | | | | | | | | | | | | | |

| U.S. Treasury Bills — 4.5% | | | | | | | | | | | | | | | | |

U.S. Treasury Bills | | | 0.470 | % | | | 2/23/17 | | | | 250,000 | | | | 249,834 | (d) |

U.S. Treasury Bills | | | 0.512 | % | | | 3/23/17 | | | | 250,000 | | | | 249,731 | (d) |

U.S. Treasury Bills | | | 0.356 | % | | | 1/26/17 | | | | 430,000 | | | | 429,902 | (d) |

U.S. Treasury Bills | | | 0.376 | % | | | 2/16/17 | | | | 300,000 | | | | 299,863 | (d) |

U.S. Treasury Bills | | | 0.501 | % | | | 4/20/17 | | | | 400,000 | | | | 399,337 | (d) |

Total U.S. Treasury Bills (Cost — $1,628,724) | | | | | | | | | | | | | | | 1,628,667 | |

| | | | |

| | | | | | | | | Shares | | | | |

| Money Market Funds — 19.3% | | | | | | | | | | | | | | | | |

State Street Institutional Treasury Plus Money Market Fund, Premier Class | | | 0.394 | % | | | | | | | 3,306,864 | | | | 3,306,864 | |

State Street Institutional U.S. Government Money Market Fund, Premier Class | | | 0.411 | % | | | | | | | 3,675,410 | | | | 3,675,410 | |

Total Money Market Funds (Cost — $6,982,274) | | | | | | | | | | | | | | | 6,982,274 | |

Total Short-Term Investments (Cost — $8,610,998) | | | | | | | | | | | | | | | 8,610,941 | |

Total Investments — 68.4% (Cost — $23,783,284#) | | | | | | | | | | | | | | | 24,759,465 | |

Other Assets in Excess of Liabilities — 31.6% | | | | | | | | | | | | | | | 11,462,193 | |

Total Net Assets — 100.0% | | | | | | | | | | | | | | $ | 36,221,658 | |

| * | Non-income producing security. |

| † | Face amount denominated in U.S. dollars, unless otherwise noted. |

| (a) | Security is valued in good faith in accordance with procedures approved by the Board of Trustees (See Note 1). |

| (b) | All or a portion of this security is held at the broker as collateral for open securities sold short. |

| (c) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Trustees, unless otherwise noted. |

| (d) | Rate shown represents yield-to-maturity. |

| (e) | Security is exempt from registration under Regulation S of the Securities Act of 1933. Regulation S applies to securities offerings that are made outside of the United States and do not involve direct selling efforts in the United States. This security has been deemed liquid pursuant to guidelines approved by the Board of Trustees, unless otherwise noted. |

| # | Aggregate cost for federal income tax purposes is $24,234,725. |

See Notes to Consolidated Financial Statements.

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 17 |

Consolidated schedule of investments (cont’d)

December 31, 2016

EnTrustPermal Alternative Select VIT Portfolio

| | |

Abbreviations used in this schedule: |

| ADR | | — American Depositary Receipts |

| CAD | | — Canadian Dollar |

| ETF | | — Exchange-Traded Fund |

| EUR | | — Euro |

| GBP | | — British Pound |

| SPDR | | — Standard & Poor’s Depositary Receipts |

| | | | | | | | | | | | | | | | |

| Security | | | | | | | | Shares | | | Value | |

| Securities Sold Short‡ | | | | | | | | | | | | | | | | |

| Common Stocks — (16.7)% | | | | | | | | | | | | | | | | |

| Consumer Discretionary — (0.1)% | | | | | | | | | | | | | | | | |

Automobiles — (0.1)% | | | | | | | | | | | | | | | | |

Tesla Motors Inc. | | | | | | | | | | | (190 | ) | | $ | (40,601 | ) * |

| Energy — (0.4)% | | | | | | | | | | | | | | | | |

Oil, Gas & Consumable Fuels — (0.4)% | | | | | | | | | | | | | | | | |

Spectra Energy Corp. | | | | | | | | | | | (3,270 | ) | | | (134,364 | ) |

| Exchange-Traded Funds — (12.4)% | | | | | | | | | | | | | | | | |

Alerian MLP ETF | | | | | | | | | | | (7,619 | ) | | | (95,999 | ) |

iShares China Large-Cap ETF | | | | | | | | | | | (2,336 | ) | | | (81,082 | ) |

iShares, Inc. — iShares MSCI Brazil Capped ETF | | | | | | | | | | | (1,242 | ) | | | (41,408 | ) |

iShares, Inc. — iShares MSCI Mexico Capped ETF | | | | | | | | | | | (1,575 | ) | | | (69,253 | ) |

Nomura TOPIX ETF | | | | | | | | | | | (37,300 | ) | | | (495,426 | ) (a) |

SPDR S&P 500 ETF Trust | | | | | | | | | | | (5,444 | ) | | | (1,216,897 | ) |

SPDR S&P Midcap 400 ETF Trust | | | | | | | | | | | (3,159 | ) | | | (953,165 | ) |

The Select Sector SPDR Trust — The Energy Select Sector SPDR Fund | | | | | | | | | | | (9,418 | ) | | | (709,364 | ) |

VanEck Vectors Russia ETF | | | | | | | | | | | (1,882 | ) | | | (39,936 | ) |

Vanguard FTSE Europe ETF | | | | | | | | | | | (16,906 | ) | | | (810,474 | ) |

Total Exchange-Traded Funds | | | | | | | | | | | | | | | (4,513,004 | ) |

| Industrials — (1.7)% | | | | | | | | | | | | | | | | |

Construction & Engineering — (0.1)% | | | | | | | | | | | | | | | | |

Chicago Bridge & Iron Co. NV | | | | | | | | | | | (484 | ) | | | (15,367 | ) |

MasTec Inc. | | | | | | | | | | | (252 | ) | | | (9,639 | ) * |

Total Construction & Engineering | | | | | | | | | | | | | | | (25,006 | ) |

Electrical Equipment — (0.4)% | | | | | | | | | | | | | | | | |

Generac Holdings Inc. | | | | | | | | | | | (3,604 | ) | | | (146,827 | ) * |

Machinery — (0.9)% | | | | | | | | | | | | | | | | |

Mitsubishi Heavy Industries Ltd. | | | | | | | | | | | (42,747 | ) | | | (194,190 | ) (a) |

SKF AB, Class B Shares | | | | | | | | | | | (6,548 | ) | | | (120,192 | ) (a) |

Total Machinery | | | | | | | | | | | | | | | (314,382 | ) |

See Notes to Consolidated Financial Statements.

| | |

| 18 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

EnTrustPermal Alternative Select VIT Portfolio

| | | | | | | | | | | | | | | | |

| Security | | | | | | | | Shares | | | Value | |

Road & Rail — (0.3)% | | | | | | | | | | | | | | | | |

CSX Corp. | | | | | | | | | | | (1,702 | ) | | $ | (61,153 | ) |

Norfolk Southern Corp. | | | | | | | | | | | (571 | ) | | | (61,708 | ) |

Total Road & Rail | | | | | | | | | | | | | | | (122,861 | ) |

Total Industrials | | | | | | | | | | | | | | | (609,076 | ) |

| Information Technology — (0.1)% | | | | | | | | | | | | | | | | |

Semiconductors & Semiconductor Equipment — (0.1)% | | | | | | | | | | | | | | | | |

SolarEdge Technologies Inc. | | | | | | | | | | | (1,908 | ) | | | (23,659 | ) * |

| Utilities — (2.0)% | | | | | | | | | | | | | | | | |

Electric Utilities — (0.8)% | | | | | | | | | | | | | | | | |

Alliant Energy Corp. | | | | | | | | | | | (662 | ) | | | (25,083 | ) |

CEZ AS | | | | | | | | | | | (1,882 | ) | | | (31,487 | ) (a) |

Duke Energy Corp. | | | | | | | | | | | (252 | ) | | | (19,595 | ) |

El Paso Electric Co. | | | | | | | | | | | (252 | ) | | | (11,718 | ) |

Fortum OYJ | | | | | | | | | | | (1,378 | ) | | | (21,091 | ) (a) |

IDACORP Inc. | | | | | | | | | | | (306 | ) | | | (24,648 | ) |

PNM Resources Inc. | | | | | | | | | | | (745 | ) | | | (25,554 | ) |

Portland General Electric Co. | | | | | | | | | | | (573 | ) | | | (24,828 | ) |

Southern Co. | | | | | | | | | | | (444 | ) | | | (21,873 | ) |

Terna-Rete Elettrica Nazionale SpA | | | | | | | | | | | (7,779 | ) | | | (35,586 | ) (a) |

Xcel Energy Inc. | | | | | | | | | | | (1,112 | ) | | | (45,259 | ) |

Total Electric Utilities | | | | | | | | | | | | | | | (286,722 | ) |

Gas Utilities — (0.1)% | | | | | | | | | | | | | | | | |

Tokyo Gas Co., Ltd. | | | | | | | | | | | (10,890 | ) | | | (49,160 | ) (a) |

Independent Power and Renewable Electricity Producers — (0.6)% | | | | | | | | | | | | | | | | |

Calpine Corp. | | | | | | | | | | | (17,274 | ) | | | (197,442 | ) * |

Multi-Utilities — (0.3)% | | | | | | | | | | | | | | | | |

Avista Corp. | | | | | | | | | | | (282 | ) | | | (11,277 | ) |

Consolidated Edison Inc. | | | | | | | | | | | (722 | ) | | | (53,197 | ) |

WEC Energy Group Inc. | | | | | | | | | | | (648 | ) | | | (38,005 | ) |

Total Multi-Utilities | | | | | | | | | | | | | | | (102,479 | ) |

Water Utilities — (0.2)% | | | | | | | | | | | | | | | | |

American Water Works Co. Inc. | | | | | | | | | | | (744 | ) | | | (53,836 | ) |

Aqua America Inc. | | | | | | | | | | | (941 | ) | | | (28,268 | ) |

Total Water Utilities | | | | | | | | | | | | | | | (82,104 | ) |

Total Utilities | | | | | | | | | | | | | | | (717,907 | ) |

Total Common Stocks (Proceeds — $(5,768,121)) | | | | | | | | | | | | | | | (6,038,611 | ) |

| Exchange-Traded Note — (0.3)% | | | | | | | | | | | | | | | | |

JPMorgan Alerian MLP Index ETN (Proceeds — $(93,625)) | | | | | | | | | | | (3,102 | ) | | | (98,054 | ) |

Total Securities Sold Short (Proceeds — $(5,861,746)) | | | | | | | | | | | | | | $ | (6,136,665 | ) |

See Notes to Consolidated Financial Statements.

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 19 |

Consolidated schedule of investments (cont’d)

December 31, 2016

EnTrustPermal Alternative Select VIT Portfolio

| * | Non-income producing security. |

| ‡ | Percentages indicated are based on net assets. |

| (a) | Security is valued in good faith in accordance with procedures approved by the Board of Trustees (See Note 1). |

| | |

Abbreviations used in this schedule: |

| ETF | | — Exchange-Traded Fund |

| ETN | | — Exchange-Traded Note |

| SPDR | | — Standard & Poor’s Depositary Receipts |

See Notes to Consolidated Financial Statements.

| | |

| 20 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

Consolidated statement of assets and liabilities

December 31, 2016

| | | | |

|

| Assets: | |

Investments, at value (Cost — $23,783,284) | | $ | 24,759,465 | |

Foreign currency, at value (Cost — $331,553) | | | 326,943 | |

Cash | | | 8,299,885 | |

Deposits with brokers for securities sold short | | | 4,032,770 | |

Deposits with brokers for OTC swap contracts | | | 2,185,000 | |

Foreign cash collateral held at broker for securities sold short (Cost — $1,171,517) | | | 1,120,059 | |

Deposits with brokers for forward foreign currency contracts | | | 917,000 | |

Receivable for securities sold | | | 643,916 | |

Unrealized appreciation on forward foreign currency contracts | | | 627,724 | |

Deposits with brokers for open futures contracts | | | 311,980 | |

OTC swaps, at value | | | 105,202 | |

Foreign currency collateral for open futures contracts, at value (Cost — $66,837) | | | 68,806 | |

Receivable from broker — variation margin on open futures contracts | | | 60,298 | |

Receivable from investment manager | | | 21,779 | |

Dividends and interest receivable | | | 18,733 | |

Receivable for open OTC swap contracts | | | 3,421 | |

Prepaid expenses | | | 3,577 | |

Total Assets | | | 43,506,558 | |

|

| Liabilities: | |

Investments sold short, at value (proceeds received — $5,861,746) | | | 6,136,665 | |

Unrealized depreciation on forward foreign currency contracts | | | 680,566 | |

OTC swaps, at value | | | 85,698 | |

Payable for securities purchased | | | 50,392 | |

Foreign currency collateral due to brokers for securities sold short, at value (Cost — $37,171) | | | 37,178 | |

Foreign currency collateral due to brokers for open futures contracts, at value (Cost — $24,267) | | | 22,871 | |

Dividends payable on securities sold short | | | 11,485 | |

Service and/or distribution fees payable | | | 7,653 | |

Payable for Portfolio shares repurchased | | | 991 | |

Payable for open OTC swap contracts | | | 390 | |

Trustees’ fees payable | | | 369 | |

Accrued expenses | | | 250,642 | |

Total Liabilities | | | 7,284,900 | |

| Total Net Assets | | $ | 36,221,658 | |

See Notes to Consolidated Financial Statements.

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 21 |

Consolidated statement of assets and liabilities (cont’d)

December 31, 2016

| | | | |

|

| Net Assets: | |

Par value (Note 5) | | $ | 40 | |

Paid-in capital in excess of par value | | | 38,701,247 | |

Overdistributed net investment income | | | (25,695) | |

Accumulated net realized loss on investments, futures contracts, written options, short sales,

swap contracts and foreign currency transactions | | | (3,129,326) | |

Net unrealized appreciation on investments, futures contracts, short sales, swap contracts

and foreign currencies | | | 675,392 | |

| Total Net Assets | | $ | 36,221,658 | |

|

| Shares Outstanding: | |

Class II | | | 3,963,326 | |

|

| Net Asset Value: | |

Class II | | | $9.14 | |

See Notes to Consolidated Financial Statements.

| | |

| 22 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

Consolidated statement of operations

For the Year Ended December 31, 2016

| | | | |

|

| Investment Income: | |

Dividends | | $ | 230,307 | |

Interest | | | 154,181 | |

Less: Foreign taxes withheld | | | (8,327) | |

Total Investment Income | | | 376,161 | |

|

| Expenses: | |

Investment management fee (Note 2) | | | 663,642 | |

Custody fees | | | 316,856 | |

Legal fees | | | 150,566 | |

Dividend expense on securities sold short | | | 143,008 | |

Service and/or distribution fees (Note 2) | | | 87,321 | |

Audit and tax fees | | | 68,505 | |

Compliance fees | | | 62,500 | |

Shareholder reports | | | 46,701 | |

Interest expense on securities sold short | | | 38,954 | |

Commodity pool reports | | | 32,594 | |

Administration fees (Note 2) | | | 31,436 | |

Fund accounting fees | | | 25,361 | |

Insurance | | | 2,533 | |

Trustees’ fees | | | 2,527 | |

Transfer agent fees | | | 1,675 | |

Miscellaneous expenses | | | 4,115 | |

Total Expenses | | | 1,678,294 | |

Less: Fee waivers and/or expense reimbursements (Note 2) | | | (553,259) | |

Net Expenses | | | 1,125,035 | |

| Net Investment Loss | | | (748,874) | |

|

Realized and Unrealized Gain (Loss) on Investments, Futures Contracts,

Written Options, Short Sales, Swap Contracts and Foreign Currency Transactions (Notes 1, 3 and 4): | |

Net Realized Gain (Loss) From: | |

Investment transactions | | | (2,256,460) | |

Futures contracts | | | 60,861 | |

Written options | | | (104,029) | |

Securities sold short | | | (112,526) | |

Swap contracts | | | 209,695 | |

Foreign currency transactions | | | 626,272 | |

Net Realized Loss | | | (1,576,187) | |

See Notes to Consolidated Financial Statements.

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 23 |

Consolidated statement of operations (cont’d)

December 31, 2016

| | | | |

Change in Net Unrealized Appreciation (Depreciation) From: | |

Investments | | | 1,866,701 | |

Futures contracts | | | 77,319 | |

Written options | | | 40,825 | |

Securities sold short | | | (309,928) | |

Swap contracts | | | (85,557) | |

Foreign currencies | | | (117,849) | |

Change in Net Unrealized Appreciation (Depreciation) | | | 1,471,511 | |

| Net Loss on Investments, Futures Contracts, Written Options, Short Sales, Swap Contracts and Foreign Currency Transactions | | | (104,676) | |

| Decrease in Net Assets From Operations | | $ | (853,550) | |

See Notes to Consolidated Financial Statements.

| | |

| 24 | | EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report |

Consolidated statements of changes in net assets

| | | | | | | | |

| For the Years Ended December 31, | | 2016 | | | 2015 | |

| | |

| Operations: | | | | | | | | |

Net investment loss | | $ | (748,874) | | | $ | (458,143) | |

Net realized loss | | | (1,576,187) | | | | (558,065) | |

Change in net unrealized appreciation (depreciation) | | | 1,471,511 | | | | (694,771) | |

Decrease in Net Assets From Operations | | | (853,550) | | | | (1,710,979) | |

| | |

| Distributions to Shareholders From (Note 1): | | | | | | | | |

Net investment income | | | (15,000) | | | | (311,103) | |

Net realized gains | | | — | | | | (329,804) | |

Decrease in Net Assets From Distributions to Shareholders | | | (15,000) | | | | (640,907) | |

| | |

| Portfolio Share Transactions (Note 5): | | | | | | | | |

Net proceeds from sale of shares | | | 4,666,397 | | | | 12,147,741 | |

Reinvestment of distributions | | | 15,000 | | | | 640,907 | |

Cost of shares repurchased | | | (1,268,587) | | | | (55,232) | |

Increase in Net Assets From Portfolio Share Transactions | | | 3,412,810 | | | | 12,733,416 | |

Increase in Net Assets | | | 2,544,260 | | | | 10,381,530 | |

| | |

| Net Assets: | | | | | | | | |

Beginning of year | | | 33,677,398 | | | | 23,295,868 | |

End of year* | | $ | 36,221,658 | | | $ | 33,677,398 | |

*Includes overdistributed net investment income of: | | | $(25,695) | | | | $(415,342) | |

See Notes to Consolidated Financial Statements.

| | |

| EnTrustPermal Alternative Select VIT Portfolio 2016 Annual Report | | 25 |

Consolidated financial highlights

| | | | | | | | | | | | |

For a share of beneficial interest outstanding throughout each year ended December 31,

unless otherwise noted: | |

| Class II Shares1 | | 2016 | | | 2015 | | | 20142 | |

| | | |

| Net asset value, beginning of year | | | $9.39 | | | | $10.03 | | | | $10.00 | |

|

| Income (loss) from operations: | |

Net investment loss | | | (0.19) | | | | (0.16) | | | | (0.03) | |

Net realized and unrealized gain (loss) | | | (0.06) | | | | (0.28) | | | | 0.08 | |

Total income (loss) from operations | | | (0.25) | | | | (0.44) | | | | 0.05 | |

|

| Less distributions from: | |

Net investment income | | | (0.00) | 3 | | | (0.10) | | | | (0.02) | |

Net realized gains | | | — | | | | (0.10) | | | | — | |

Total distributions | | | (0.00) | 3 | | | (0.20) | | | | (0.02) | |

| | | |

| Net asset value, end of year | | | $9.14 | | | | $9.39 | | | | $10.03 | |

Total return4 | | | (2.62) | % | | | (4.37) | % | | | 0.44 | % |

| | | |