UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21128

Legg Mason Partners Variable Equity Trust

(Exact name of registrant as specified in charter)

620 Eighth Avenue, 49th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-877-721-1926

Date of fiscal year end: December 31

Date of reporting period: June 30, 2020

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Semi-Annual Report to Stockholders is filed herewith.

| | |

| Semi-Annual Report | | June 30, 2020 |

Legg Mason/QS

Model Portfolio Funds

Legg Mason/QS Aggressive Model Portfolio

Legg Mason/QS Moderately Aggressive Model Portfolio

Legg Mason/QS Moderate Model Portfolio

Legg Mason/QS Moderately Conservative Model Portfolio

Legg Mason/QS Conservative Model Portfolio

Beginning in January 2021, as permitted by regulations adopted by the Securities and Exchange Commission, your insurance company may no longer send you paper copies of the Fund’s shareholder reports like this one by mail, unless you specifically request paper copies of the reports from the insurance company or your financial intermediary. Instead, the shareholder reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report. Instructions for requesting paper copies will be provided by your insurance company.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. If your insurance company offers electronic delivery, you may elect to receive shareholder reports and other communications from them electronically by following the instructions provided by the insurance company.

You may elect to receive all future reports in paper free of charge. You can inform the insurance company that you wish to continue receiving paper copies of shareholder reports by following the instructions provided by them. Your election will apply to all Funds available under your contract with the insurance company.

|

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

Legg Mason/QS Model Portfolio Funds

Legg Mason/QS Model Portfolio Funds (“Model Portfolio Funds”) consists of separate investment Portfolios, each with its own investment objective and policies. Each Portfolio is a “fund of funds,” investing in insurance-dedicated mutual funds, and is managed as an asset allocation program.

The Portfolios are separate investment series of Legg Mason Partners Variable Equity Trust, a Maryland statutory trust.

Letter from the president

Dear Shareholder,

We are pleased to provide the semi-annual report of Legg Mason/QS Model Portfolio Funds for the six-month reporting period ended June 30, 2020.

Special shareholder notice

On July 31, 2020, Franklin Resources, Inc. (“Franklin Resources”) acquired Legg Mason, Inc. (“Legg Mason”) in an all-cash transaction. As a result of the transaction, Legg Mason Partners Fund Advisor, LLC (“LMPFA”) and the subadviser(s) became indirect, wholly-owned subsidiaries of Franklin Resources. Under the Investment Company Act of 1940, as amended, consummation of the transaction automatically terminated the management and subadvisory agreements that were in place for the Portfolios prior to the transaction. The Portfolios’ manager and subadviser(s) continue to provide uninterrupted services with respect to the Portfolios pursuant to new management and subadvisory agreements that were approved by each Portfolio’s shareholders.

Franklin Resources, whose principal executive offices are at One Franklin Parkway, San Mateo, California 94403, is a global investment management organization operating, together with its subsidiaries, as Franklin Templeton. As of June 30, 2020, after giving effect to the transaction described above, Franklin Templeton’s asset management operations had aggregate assets under management of approximately $1.4 trillion.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our website, www.leggmason.com. Here you can gain immediate access to market and investment information, including:

| • | | Market insights and commentaries from our portfolio managers and |

| • | | A host of educational resources. |

We look forward to helping you meet your financial goals.

Sincerely,

Jane Trust, CFA

President and Chief Executive Officer

July 31, 2020

| | |

| II | | Legg Mason/QS Model Portfolio Funds |

Portfolio overview

Each of the five Legg Mason/QS Model Portfolio Funds is managed as an asset allocation program and allocates its assets among insurance-dedicated mutual funds that have been selected by New York Life Insurance and Annuity Corporation (“NYLIAC”) as investment options for use with their variable annuity and variable universal life insurance policies (the “underlying funds”). The underlying funds include funds managed by investment advisers that are not affiliated with Legg Mason and funds managed by Legg Mason affiliated investment advisers. When selecting investments to fulfill a desired asset class exposure, the portfolio managers expect to allocate primarily to underlying funds managed by unaffiliated investment advisers, but may also allocate to Legg Mason-affiliated underlying funds. The underlying funds may change from time to time without prior notice to shareholders.

Legg Mason/QS Aggressive Model Portfolio

Legg Mason/QS Aggressive Model Portfolio seeks capital appreciation. The Portfolio organizes its investments in underlying funds into two main asset classes: the equity class (equity securities of all types) and the fixed income class (fixed income securities of all types). The portfolio managers may invest across all asset classes and strategies. Under ordinary circumstances, the portfolio managers expect to allocate between 80% to 100% of the Portfolio’s assets among underlying funds that invest in equity and equity-like strategies and between 0% to 20% of the Portfolio’s assets among underlying funds that invest in fixed income strategies. The Portfolio’s allocation to each class will be measured at the time of purchase and may vary thereafter as a result of market movement. The Portfolio compares its performance to a composite benchmark, consisting of 75% Russell 3000 Indexi, 15% MSCI World Ex U.S.A. Indexii, and 10% Bloomberg Barclays U.S. Aggregate Indexiii. The portfolio managers will seek to maintain a level of risk in the Portfolio similar to that of this composite benchmark.

Legg Mason/QS Moderately Aggressive Model Portfolio

Legg Mason/QS Moderately Aggressive Model Portfolio seeks capital appreciation. The Portfolio organizes its investments in underlying funds into two main asset classes: the equity class (equity securities of all types) and the fixed income class (fixed income securities of all types). The portfolio managers may invest across all asset classes and strategies. Under ordinary circumstances, the portfolio managers expect to allocate between 60% to 70% of the Portfolio’s assets among underlying funds that invest in equity and equity-like strategies and between 30% to 40% of the Portfolio’s assets among underlying funds that invest in fixed income strategies. The Portfolio’s allocation to each class will be measured at the time of purchase and may vary thereafter as a result of market movement. The Portfolio compares its performance to a composite benchmark, consisting of 60% Russell 3000 Index, 10% MSCI World Ex U.S.A. Index, and 30% Bloomberg Barclays U.S. Aggregate Index. The portfolio managers will seek to maintain a level of risk in the Portfolio similar to that of this composite benchmark.

Legg Mason/QS Moderate Model Portfolio

Legg Mason/QS Moderate Model Portfolio seeks capital appreciation. The Portfolio organizes its investments in underlying funds into two main asset classes: the equity class (equity securities of all types) and the fixed income class (fixed income securities of all types). The portfolio managers may invest across all asset classes and strategies. Under ordinary circumstances, the portfolio managers expect to allocate between 45% to 65% of the Portfolio’s assets among underlying funds that invest in equity and equity-like strategies and between 35% to 55% of the Portfolio’s assets among underlying funds that invest in fixed income strategies. The Portfolio’s allocation to each class will be measured at the time of purchase and may vary thereafter as a result of market movement. The Portfolio compares its performance to a composite benchmark, consisting of 45% Russell 3000 Index, 10% MSCI World Ex U.S.A. Index, and 45% Bloomberg Barclays U.S. Aggregate Index. The portfolio managers will seek to maintain a level of risk in the Portfolio similar to that of this composite benchmark.

Legg Mason/QS Moderately Conservative Model Portfolio

Legg Mason/QS Moderately Conservative Model Portfolio seeks a balance of capital appreciation and income. The Portfolio organizes its investments in underlying funds into two main asset classes: the equity class (equity securities of all types) and the fixed income class (fixed income securities of all types). The portfolio managers may invest across all asset classes and strategies. Under ordinary circumstances, the portfolio managers expect to allocate between 30% to 50% of the Portfolio’s assets among underlying funds that invest in equity and equity-like strategies and between 50% to 70% of the Portfolio’s assets among underlying funds that invest in fixed income strategies. The Portfolio’s allocation to each class will be measured at the time of purchase and may vary thereafter as a result of market movement. The Portfolio compares its performance to a composite benchmark, consisting of 35% Russell 3000 Index,

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | III |

Portfolio overview (cont’d)

5% MSCI World Ex U.S.A. Index, and 60% Bloomberg Barclays U.S. Aggregate Index. The portfolio managers will seek to maintain a level of risk in the Portfolio similar to that of this composite benchmark.

Legg Mason/QS Conservative Model Portfolio

Legg Mason/QS Conservative Model Portfolio seeks a balance between capital appreciation and income. The Portfolio organizes its investments in underlying funds into two main asset classes: the equity class (equity securities of all types) and the fixed income class (fixed income securities of all types). The portfolio managers may invest across all asset classes and strategies. Under ordinary circumstances, the portfolio managers expect to allocate between 10% to 30% of the Portfolio’s assets among underlying funds that invest in equity and equity-like strategies and between 70% to 90% of the Portfolio’s assets among underlying funds that invest in fixed income strategies. The Portfolio’s allocation to each class will be measured at the time of purchase and may vary thereafter as a result of market movement. The Portfolio compares its performance to a composite benchmark, consisting of 20% Russell 3000 Index and 80% Bloomberg Barclays U.S. Aggregate Index. The portfolio managers will seek to maintain a level of risk in the Portfolio similar to that of this composite benchmark.

As always, thank you for your confidence in our stewardship of your assets.

Sincerely,

Jane Trust, CFA

President and Chief Executive Officer

July 31, 2020

RISKS: Each Portfolio is newly organized, with a limited history of operations. Equity securities are subject to price fluctuation and possible loss of principal. Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks. International investments are subject to special risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Emerging market countries tend to have economic, political, and legal systems that are less developed and are less stable than those of more developed countries. Fixed-income securities involve interest rate, credit, inflation, and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed-income securities falls. High yield bonds are subject to greater price volatility, illiquidity, and possibility of default.

Each Portfolio is a fund of funds and is subject to the risks of the underlying funds in which it invests. In addition to the Portfolios’ operating expenses, you will indirectly bear the operating expenses of the underlying funds. The investment strategies employed by the underlying funds and the securities in which they invest may change without the knowledge of the Portfolios’ portfolio managers. The portfolio managers may invest each Portfolio’s assets in underlying funds that have a limited performance history. Each underlying fund may engage in active and frequent trading, resulting in higher portfolio turnover and transaction costs. As a non-diversified Portfolio, each Portfolio may invest a larger percentage of its assets in a smaller number of underlying funds than a diversified Portfolio, which may magnify the Portfolios’ losses from events affecting an underlying fund. The underlying funds in which each Portfolio invests may be either diversified or non-diversified. Certain of the underlying funds may engage in short selling, which is a speculative strategy that involves special risks. Unlike the possible loss on a security that is purchased, there is no limit on the amount of loss on an appreciating security that is sold short.

The model used to manage each Portfolio’s assets provides no assurance that the recommended allocation will either maximize returns or minimize risks. There is no assurance that a recommended allocation will prove the ideal allocation in all circumstances. Derivatives, such as options and futures, can be illiquid, may disproportionately increase losses, and have a potentially large impact on each Portfolio’s performance. Please see the Portfolios’ prospectus for a more complete discussion of these and other risks and each Portfolio’s investment strategies.

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. All index performance reflects no deduction for fees, expenses, or taxes. Please note that an investor cannot invest directly in an index.

IMPORTANT INFORMATION: These Portfolios are available as investment options under a variable annuity or variable life contract. Shares of the Portfolios are offered only to insurance company separate accounts established by New York Life Insurance and Annuity Corporation that fund certain variable annuity or variable life insurance contracts. These Portfolios may not be available in all states and may only be offered in certain variable products. Please refer to the prospectuses. Variable annuities are long-term, tax-deferred investment vehicles designed for retirement purposes. Gains from tax-deferred investments are taxable as ordinary income upon withdrawal. Withdrawals made prior to age 59 1/2 are subject to a 10% IRS penalty charge and/or surrender charges. Investments in a variable annuity are subject to market risks, including loss of principal. Guarantees are based on the claims-paying ability of the insurer.

| | |

| IV | | Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report |

| i | The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the U.S. equity market. |

| ii | MSCI World Ex U.S.A. Index captures large, mid and small cap representation across 22 of 23 Developed Markets (DM) countries — excluding the United States. The MSCI World Ex U.S.A. Index calculates performance utilizing local currencies taking out the effect of converting to the U.S. dollar. |

| iii | The Bloomberg Barclays U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | V |

(This page intentionally left blank.)

Portfolios at a glance (unaudited)

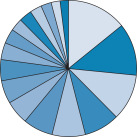

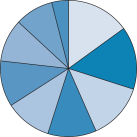

Legg Mason/QS Aggressive Model Portfolio Breakdown† as of — June 30, 2020

As a Percent of Total Long-Term Investments

| | | | |

| % of Total Long-Term Investments | | Top 5 Sectors |

| | 14.2 MainStay VP Funds Trust — MainStay VP MacKay S&P 500 Index Portfolio, Initial Class | | Software Technology Hardware, Storage & Peripherals IT Services Interactive Media & Services Internet & Direct Marketing Retail |

| | 12.4 Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | Health Care Financials Information Technology Industrials Consumer Discretionary |

| | 11.0 MainStay VP Funds Trust — MainStay VP MacKay Common Stock Portfolio, Initial Class | | Software Technology Hardware, Storage & Peripherals Internet & Direct Marketing Retail Interactive Media & Services IT Services |

| | 8.4 MainStay VP Funds Trust — MainStay VP Fidelity Institutional AM Utilities Portfolio, Initial Class | | Electric Utilities Multi-Utilities Independent Power & Renewable Electricity Producers Short-Term Investments Gas Utilities |

| | 7.9 MainStay VP Funds Trust — MainStay VP Indexed Bond Portfolio, Initial Class | | U.S. Government & Federal Agencies Corporate Bonds Short-Term Investments Exchange-Traded Funds Foreign Government Bonds |

| | 7.1 American Funds Insurance Series — Growth Fund, Class 1A | | Information Technology Communication Services Consumer Discretionary Health Care Financials |

| | 5.6 MainStay VP Funds Trust — MainStay VP Winslow Large Cap Growth Portfolio, Initial Class | | Software IT Services Interactive Media & Services Internet & Direct Marketing Retail Technology Hardware, Storage & Peripherals |

| | 5.5 American Funds Insurance Series — New World Fund, Class 1A | | Information Technology Consumer Discretionary Health Care Financials Communication Services |

| | 5.0 MainStay VP Funds Trust — MainStay Epoch U.S. Equity Yield Portfolio, Initial Shares | | Electric Utilities Pharmaceuticals Semiconductors & Semiconductor Equipment Insurance Banks |

| | 4.0 Variable Insurance Products Fund II — VIP Contrafund® Portfolio, Initial Class(a) | | Information Technology Health Care Communication Services Consumer Discretionary Financials |

| | 3.5 BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | Semiconductors & Semiconductor Equipment Software Internet & Direct Marketing Retail Interactive Media & Services IT Services |

| | 3.0 Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | Healthcare Information Technology Financials Communication Services Consumer Staples |

| | 3.0 Janus Aspen Series — Janus Henderson VIT Global Research Portfolio, Institutional Shares | | Financials Technology Consumer Industrials & Materials Health Care |

| | 2.8 Variable Insurance Products Fund II — VIP International Index Portfolio, Initial Class | | Financials Industrials Consumer Discretionary Information Technology Health Care |

| | 2.5 MainStay VP Funds Trust — MainStay VP CBRE Global Infrastructure Portfolio, Initial Class | | Utilities Transportation Communications Midstream/Pipelines Diversified Property Holding |

| | 2.1 American Funds Insurance Series — Blue Chip Income and Growth Fund, Class 1A | | Health Care Information Technology Industrials Energy Consumer Staples |

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 1 |

Portfolios at a glance (unaudited) (cont’d)

| | | | |

| % of Total Long-Term Investments | | Top 5 Sectors |

| | 2.0 Variable Insurance Products Fund III — VIP Growth Opportunities Portfolio, Initial Class | | Information Technology Consumer Discretionary Communication Services Health Care Industrials |

| † | Subject to change at any time. |

| (a) | Contrafund is a registered service mark of FMR LLC. |

| | |

| 2 | | Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report |

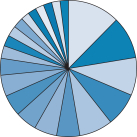

Legg Mason/QS Moderately Aggressive Model Portfolio Breakdown† as of — June 30, 2020

As a Percent of Total Long-Term Investments

| | | | |

| % of Total Long-Term Investments | | Top 5 Sectors |

| | 12.4 MainStay VP Funds Trust — MainStay VP MacKay S&P 500 Index Portfolio, Initial Class | | Software Technology Hardware, Storage & Peripherals IT Services Interactive Media & Services Internet & Direct Marketing Retail |

| | 10.0 MainStay VP Funds Trust — MainStay VP Indexed Bond Portfolio, Initial Class | | U.S. Government & Federal Agencies Corporate Bonds Short-Term Investments Exchange-Traded Funds Foreign Government Bonds |

| | 9.0 MainStay VP Funds Trust — MainStay VP MacKay Common Stock Portfolio, Initial Class | | Software Technology Hardware, Storage & Peripherals Internet & Direct Marketing Retail Interactive Media & Services IT Services |

| | 8.0 MainStay VP Funds Trust — MainStay VP Bond Portfolio, Initial Class | | Corporate Bonds U.S. Government & Federal Agencies Asset-Backed Securities Mortgage-Backed Securities Short-Term Investments |

| | 7.9 Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | Health Care Financials Information Technology Industrials Consumer Discretionary |

| | 5.5 MainStay VP Funds Trust — MainStay Epoch U.S. Equity Yield Portfolio, Initial Shares | | Electric Utilities Pharmaceuticals Semiconductors & Semiconductor Equipment Insurance Banks |

| | 5.4 MainStay VP Funds Trust — MainStay VP Fidelity Institutional AM Utilities Portfolio, Initial Class | | Electric Utilities Multi-Utilities Independent Power & Renewable Electricity Producers Short-Term Investments Gas Utilities |

| | 5.1 American Funds Insurance Series — Growth Fund, Class 1A | | Information Technology Communication Services Consumer Discretionary Health Care Financials |

| | 5.1 Columbia Funds Variable Series Trust II — Columbia Variable Portfolio — Emerging Markets Bond Fund, Class I | | Sovereign External Quasi Sovereign Investment Grade Corporates High Yield Corporates Cash and Cash Equivalents |

| | 5.0 PIMCO Variable Insurance Trust — PIMCO International Bond Portfolio (U.S. Dollar-Hedged), Institutional Class | | Government Related Securitized Emerging Market Local Investment Grade Credit Covered Bonds and Pfandbriefe |

| | 4.0 MainStay VP Funds Trust — MainStay VP Winslow Large Cap Growth Portfolio, Initial Class | | Software IT Services Interactive Media & Services Internet & Direct Marketing Retail Technology Hardware, Storage & Peripherals |

| | 3.0 Variable Insurance Products Fund II — VIP Contrafund® Portfolio, Initial Class(a) | | Information Technology Health Care Communication Services Consumer Discretionary Financials |

| | 2.6 Variable Insurance Products Fund II — VIP International Index Portfolio, Initial Class | | Financials Industrials Consumer Discretionary Information Technology Health Care |

| | 2.5 American Funds Insurance Series — New World Fund, Class 1A | | Information Technology Consumer Discretionary Health Care Financials Communication Services |

| | 2.5 MainStay VP Funds Trust — MainStay VP CBRE Global Infrastructure Portfolio, Initial Class | | Utilities Transportation Communications Midstream/Pipelines Diversified Property Holding |

| | 2.0 American Funds Insurance Series — Blue Chip Income and Growth Fund, Class 1A | | Health Care Information Technology Industrials Energy Consumer Staples |

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 3 |

Portfolios at a glance (unaudited) (cont’d)

| | | | |

| % of Total Long-Term Investments | | Top 5 Sectors |

| | 2.0 BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | Semiconductors & Semiconductor Equipment Software Internet & Direct Marketing Retail Interactive Media & Services IT Services |

| | 2.0 MainStay VP Funds Trust — MainStay VP MacKay Government Portfolio, Initial Class | | U.S. Government & Federal Agencies Mortgage-Backed Securities Short-Term Investments Corporate Bonds Asset-Backed Securities |

| | 2.0 Janus Aspen Series — Janus Henderson VIT Global Research Portfolio, Institutional Shares | | Financials Technology Consumer Industrials & Materials Health Care |

| | 2.0 Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | Healthcare Information Technology Financials Communication Services Consumer Staples |

| | 2.0 Variable Insurance Products Fund III — VIP Growth Opportunities Portfolio, Initial Class | | Information Technology Consumer Discretionary Communication Services Health Care Industrials |

| † | Subject to change at any time. |

| (a) | Contrafund is a registered service mark of FMR LLC. |

| | |

| 4 | | Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report |

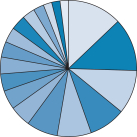

Legg Mason/QS Moderate Model Portfolio Breakdown† as of — June 30, 2020

As a Percent of Total Long-Term Investments

| | | | |

| % of Total Long-Term Investments | | Top 5 Sectors |

| | 12.9 MainStay VP Funds Trust — MainStay VP Bond Portfolio, Initial Class | | Corporate Bonds U.S. Government & Federal Agencies Asset-Backed Securities Mortgage-Backed Securities Short-Term Investments |

| | 12.6 MainStay VP Funds Trust — MainStay VP MacKay S&P 500 Index Portfolio, Initial Class | | Software Technology Hardware, Storage & Peripherals IT Services Interactive Media & Services Internet & Direct Marketing Retail |

| | 10.4 PIMCO Variable Insurance Trust — PIMCO International Bond Portfolio (U.S. Dollar-Hedged), Institutional Class | | Government Related Securitized Emerging Market Local Investment Grade Credit Covered Bonds and Pfandbriefe |

| | 8.7 MainStay VP Funds Trust — MainStay VP Indexed Bond Portfolio, Initial Class | | U.S. Government & Federal Agencies Corporate Bonds Short-Term Investments Exchange-Traded Funds Foreign Government Bonds |

| | 8.1 MainStay VP Funds Trust — MainStay VP MacKay Common Stock Portfolio, Initial Class | | Software Technology Hardware, Storage & Peripherals Internet & Direct Marketing Retail Interactive Media & Services IT Services |

| | 7.4 MainStay VP Funds Trust — MainStay VP MacKay Government Portfolio, Initial Class | | U.S. Government & Federal Agencies Mortgage-Backed Securities Short-Term Investments Corporate Bonds Asset-Backed Securities |

| | 5.0 MainStay VP Funds Trust — MainStay VP Fidelity Institutional AM Utilities Portfolio, Initial Class | | Electric Utilities Multi-Utilities Independent Power & Renewable Electricity Producers Short-Term Investments Gas Utilities |

| | 4.5 MainStay VP Funds Trust — MainStay Epoch U.S. Equity Yield Portfolio, Initial Shares | | Electric Utilities Pharmaceuticals Semiconductors & Semiconductor Equipment Insurance Banks |

| | 4.1 MainStay VP Funds Trust — MainStay VP Winslow Large Cap Growth Portfolio, Initial Class | | Software IT Services Interactive Media & Services Internet & Direct Marketing Retail Technology Hardware, Storage & Peripherals |

| | 4.0 Columbia Funds Variable Series Trust II — Columbia Variable Portfolio — Emerging Markets Bond Fund, Class I | | Sovereign External Quasi Sovereign Investment Grade Corporates High Yield Corporates Cash and Cash Equivalents |

| | 3.7 Variable Insurance Products Fund II — VIP International Index Portfolio, Initial Class | | Financials Industrials Consumer Discretionary Information Technology Health Care |

| | 3.6 American Funds Insurance Series — Growth Fund, Class 1A | | Information Technology Communication Services Consumer Discretionary Health Care Financials |

| | 3.5 Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | Health Care Financials Information Technology Industrials Consumer Discretionary |

| | 3.0 MainStay VP Funds Trust — MainStay VP CBRE Global Infrastructure Portfolio, Initial Class | | Utilities Transportation Communications Midstream/Pipelines Diversified Property Holding |

| | 2.5 Variable Insurance Products Fund II — VIP Contrafund® Portfolio, Initial Class(a) | | Information Technology Health Care Communication Services Consumer Discretionary Financials |

| | 2.0 American Funds Insurance Series — Blue Chip Income and Growth Fund, Class 1A | | Health Care Information Technology Industrials Energy Consumer Staples |

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 5 |

Portfolios at a glance (unaudited) (cont’d)

| | | | |

| % of Total Long-Term Investments | | Top 5 Sectors |

| | 2.0 BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | Semiconductors & Semiconductor Equipment Software Internet & Direct Marketing Retail Interactive Media & Services IT Services |

| | 2.0 Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | Healthcare Information Technology Financials Communication Services Consumer Staples |

| † | Subject to change at any time. |

| (a) | Contrafund is a registered service mark of FMR LLC. |

| | |

| 6 | | Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report |

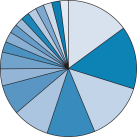

Legg Mason/QS Moderately Conservative Model Portfolio Breakdown† as of — June 30, 2020

As a Percent of Total Long-Term Investments

| | | | |

| % of Total Long-Term Investments | | Top 5 Sectors |

| | 14.9 PIMCO Variable Insurance Trust — PIMCO International Bond Portfolio (U.S. Dollar-Hedged), Institutional Class | | Government Related Securitized Emerging Market Local Investment Grade Credit Covered Bonds and Pfandbriefe |

| | 14.9 MainStay VP Funds Trust — MainStay VP Bond Portfolio, Initial Class | | Corporate Bonds U.S. Government & Federal Agencies Asset-Backed Securities Mortgage-Backed Securities Short-Term Investments |

| | 13.9 MainStay VP Funds Trust — MainStay VP MacKay Government Portfolio, Initial Class | | U.S. Government & Federal Agencies Mortgage-Backed Securities Short-Term Investments Corporate Bonds Asset-Backed Securities |

| | 11.4 MainStay VP Funds Trust — MainStay VP MacKay S&P 500 Index Portfolio, Initial Class | | Software Technology Hardware, Storage & Peripherals IT Services Interactive Media & Services Internet & Direct Marketing Retail |

| | 8.7 MainStay VP Funds Trust — MainStay VP Indexed Bond Portfolio, Initial Class | | U.S. Government & Federal Agencies Corporate Bonds Short-Term Investments Exchange-Traded Funds Foreign Government Bonds |

| | 7.1 MainStay VP Funds Trust — MainStay VP MacKay Common Stock Portfolio, Initial Class | | Software Technology Hardware, Storage & Peripherals Internet & Direct Marketing Retail Interactive Media & Services IT Services |

| | 4.0 MainStay VP Funds Trust — MainStay VP Fidelity Institutional AM Utilities Portfolio, Initial Class | | Electric Utilities Multi-Utilities Independent Power & Renewable Electricity Producers Short-Term Investments Gas Utilities |

| | 4.0 Variable Insurance Products Fund II — VIP International Index Portfolio, Initial Class | | Financials Industrials Consumer Discretionary Information Technology Health Care |

| | 2.5 MainStay VP Funds Trust — MainStay VP CBRE Global Infrastructure Portfolio, Initial Class | | Utilities Transportation Communications Midstream/Pipelines Diversified Property Holding |

| | 2.5 Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | Health Care Financials Information Technology Industrials Consumer Discretionary |

| | 2.1 American Funds Insurance Series — Growth Fund, Class 1A | | Information Technology Communication Services Consumer Discretionary Health Care Financials |

| | 2.0 Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | Healthcare Information Technology Financials Communication Services Consumer Staples |

| | 2.0 BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | Semiconductors & Semiconductor Equipment Software Internet & Direct Marketing Retail Interactive Media & Services IT Services |

| | 2.0 MainStay VP Funds Trust — MainStay VP Winslow Large Cap Growth Portfolio, Initial Class | | Software IT Services Interactive Media & Services Internet & Direct Marketing Retail Technology Hardware, Storage & Peripherals |

| | 2.0 BlackRock Variable Series Funds II, Inc. — BlackRock High Yield V.I. Fund, Class I | | Corporate Bond Bank Loan Cash & Equivalents Convertible Future/Forward |

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 7 |

Portfolios at a glance (unaudited) (cont’d)

| | | | |

| % of Total Long-Term Investments | | Top 5 Sectors |

| | 2.0 Columbia Funds Variable Series Trust II — Columbia Variable Portfolio — Emerging Markets Bond Fund, Class I | | Sovereign External Quasi Sovereign Investment Grade Corporates High Yield Corporates Cash and Cash Equivalents |

| | 2.0 MainStay VP Funds Trust — MainStay VP MacKay High Yield Corporate Bond Portfolio, Initial Class | | Corporate Bonds Short-Term Investment Loan Assignments Common Stocks Convertible Bonds |

| | 2.0 Variable Insurance Products Fund II — VIP Contrafund® Portfolio, Initial Class(a) | | Information Technology Health Care Communication Services Consumer Discretionary Financials |

| † | Subject to change at any time. |

| (a) | Contrafund is a registered service mark of FMR LLC. |

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 8 |

Legg Mason/QS Conservative Model Portfolio Breakdown† as of — June 30, 2020

As a Percent of Total Long-Term Investments

| | | | |

| % of Total Long-Term Investments | | Top 5 Sectors |

| | 15.0 MainStay VP Funds Trust — MainStay VP MacKay Government Portfolio, Initial Class | | U.S. Government & Federal Agencies Mortgage-Backed Securities Short-Term Investments Corporate Bonds Asset-Backed Securities |

| | 14.9 MainStay VP Funds Trust — MainStay VP Bond Portfolio, Initial Class | | Corporate Bonds U.S. Government & Federal Agencies Asset-Backed Securities Mortgage-Backed Securities Short-Term Investments |

| | 13.5 PIMCO Variable Insurance Trust — PIMCO International Bond Portfolio (U.S. Dollar-Hedged), Institutional Class | | Government Related Securitized Emerging Market Local Investment Grade Credit Covered Bonds and Pfandbriefe |

| | 11.5 PIMCO Variable Insurance Trust — PIMCO Total Return Portfolio, Institutional Class | | US Government — Treasury Securitized Investment Grade Credit Emerging markets High Yield Credit |

| | 11.0 MainStay VP Funds Trust — MainStay VP MacKay S&P 500 Index Portfolio, Initial Class | | Software Technology Hardware, Storage & Peripherals IT Services Interactive Media & Services Internet & Direct Marketing Retail |

| | 10.9 MainStay VP Funds Trust — MainStay VP MacKay High Yield Corporate Bond Portfolio, Initial Class | | Corporate Bonds Short-Term Investment Loan Assignments Common Stocks Convertible Bonds |

| | 10.1 MainStay VP Funds Trust — MainStay VP MacKay Common Stock Portfolio, Initial Class | | Software Technology Hardware, Storage & Peripherals Internet & Direct Marketing Retail Interactive Media & Services IT Services |

| | 9.1 MainStay VP Funds Trust — MainStay VP Indexed Bond Portfolio, Initial Class | | U.S. Government & Federal Agencies Corporate Bonds Short-Term Investments Exchange-Traded Funds Foreign Government Bonds |

| | 4.0 BlackRock Variable Series Funds II, Inc. — BlackRock High Yield V.I. Fund, Class I | | Corporate Bond Bank Loan Cash & Equivalents Convertible Future/Forward |

| † | Subject to change at any time. |

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 9 |

Portfolios expenses (unaudited)

Example

As a shareholder of the Portfolio, you may incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other funds.

This example is based on an investment of $1,000 invested on January 1, 2020 and held for the six months ended June 30, 2020, unless otherwise noted.

Actual expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| Based on actual total return1 | | | | | | | | | Based on hypothetical total return5 | |

Legg Mason/QS

Aggressive

Model Portfolio | | Actual

Total

Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | | | | | | Legg Mason/QS

Aggressive

Model Portfolio | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period6 | |

| Class I | | | 9.00 | % | | $ | 1,000.00 | | | $ | 1,090.00 | | | | 0.23 | % | | $ | 0.50 | | | | | | | Class I | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,023.72 | | | | 0.23 | % | | $ | 1.16 | |

| Class II | | | 8.90 | | | | 1,000.00 | | | | 1,089.00 | | | | 0.48 | | | | 1.04 | | | | | | | Class II | | | 5.00 | | | | 1,000.00 | | | | 1,022.48 | | | | 0.48 | | | | 2.41 | |

| 1 | For the period April 15, 2020 (inception date) to June 30, 2020. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Does not include fees and expenses of the Underlying Funds in which the Portfolio invests. |

| 4 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal period (76), then divided by 366. |

| 5 | For the six months ended June 30, 2020. |

| 6 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (182), then divided by 366. |

| | |

| 10 | | Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report |

Example

As a shareholder of the Portfolio, you may incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other funds.

This example is based on an investment of $1,000 invested on January 1, 2020 and held for the six months ended June 30, 2020, unless otherwise noted.

Actual expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| Based on actual total return1 | | | | | | | | | Based on hypothetical total return5 | |

Legg Mason/QS

Moderately

Aggressive

Model Portfolio | | Actual

Total

Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | | | | | | Legg Mason/QS

Moderately

Aggressive

Model Portfolio | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period6 | |

| Class I | | | 8.10 | % | | $ | 1,000.00 | | | $ | 1,081.00 | | | | 0.21 | % | | $ | 0.45 | | | | | | | Class I | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,023.82 | | | | 0.21 | % | | $ | 1.06 | |

| Class II | | | 8.00 | | | | 1,000.00 | | | | 1,080.00 | | | | 0.46 | | | | 0.99 | | | | | | | Class II | | | 5.00 | | | | 1,000.00 | | | | 1,022.58 | | | | 0.46 | | | | 2.31 | |

| 1 | For the period April 15, 2020 (inception date) to June 30, 2020. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Does not include fees and expenses of the Underlying Funds in which the Portfolio invests. |

| 4 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal period (76), then divided by 366. |

| 5 | For the six months ended June 30, 2020. |

| 6 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (182), then divided by 366. |

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 11 |

Portfolios expenses (unaudited) (cont’d)

Example

As a shareholder of the Portfolio, you may incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other funds.

This example is based on an investment of $1,000 invested on January 1, 2020 and held for the six months ended June 30, 2020, unless otherwise noted.

Actual expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| Based on actual total return1 | | | | | | | | | Based on hypothetical total return5 | |

Legg Mason/QS

Moderate

Model Portfolio | | Actual

Total

Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | | | | | | Legg Mason/QS

Moderate Model

Portfolio | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period6 | |

| Class I | | | 6.10 | % | | $ | 1,000.00 | | | $ | 1,061.00 | | | | 0.21 | % | | $ | 0.45 | | | | | | | Class I | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,023.82 | | | | 0.21 | % | | $ | 1.06 | |

| Class II | | | 6.00 | | | | 1,000.00 | | | | 1,060.00 | | | | 0.46 | | | | 0.98 | | | | | | | Class II | | | 5.00 | | | | 1,000.00 | | | | 1,022.58 | | | | 0.46 | | | | 2.31 | |

| 1 | For the period April 15, 2020 (inception date) to June 30, 2020. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Does not include fees and expenses of the Underlying Funds in which the Portfolio invests. |

| 4 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal period (76), then divided by 366. |

| 5 | For the six months ended June 30, 2020. |

| 6 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (182), then divided by 366. |

| | |

| 12 | | Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report |

Example

As a shareholder of the Portfolio, you may incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other funds.

This example is based on an investment of $1,000 invested on January 1, 2020 and held for the six months ended June 30, 2020, unless otherwise noted.

Actual expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| Based on actual total return1 | | | | | | | | | Based on hypothetical total return5 | |

Legg Mason/QS

Moderately

Conservative

Model Portfolio | | Actual

Total

Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | | | | | | Legg Mason/QS

Moderately

Conservative

Model Portfolio | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period6 | |

| Class I | | | 5.40 | % | | $ | 1,000.00 | | | $ | 1,054.00 | | | | 0.23 | % | | $ | 0.49 | | | | | | | Class I | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,023.72 | | | | 0.23 | % | | $ | 1.16 | |

| Class II | | | 5.30 | | | | 1,000.00 | | | | 1,053.00 | | | | 0.48 | | | | 1.02 | | | | | | | Class II | | | 5.00 | | | | 1,000.00 | | | | 1,022.48 | | | | 0.48 | | | | 2.41 | |

| 1 | For the period April 15, 2020 (inception date) to June 30, 2020. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Does not include fees and expenses of the Underlying Funds in which the Portfolio invests. |

| 4 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal period (76), then divided by 366. |

| 5 | For the six months ended June 30, 2020. |

| 6 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (182), then divided by 366. |

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 13 |

Portfolios expenses (unaudited) (cont’d)

Example

As a shareholder of the Portfolio, you may incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other funds.

This example is based on an investment of $1,000 invested on January 1, 2020 and held for the six months ended June 30, 2020, unless otherwise noted.

Actual expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| Based on actual total return1 | | | | | | | | | Based on hypothetical total return5 | |

Legg Mason/QS

Conservative

Model Portfolio | | Actual

Total

Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | | | | | | Legg Mason/QS

Conservative

Model Portfolio | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period6 | |

| Class I | | | 3.80 | % | | $ | 1,000.00 | | | $ | 1,038.00 | | | | 0.23 | % | | $ | 0.49 | | | | | | | Class I | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,023.72 | | | | 0.23 | % | | $ | 1.16 | |

| Class II | | | 3.70 | | | | 1,000.00 | | | | 1,037.00 | | | | 0.48 | | | | 1.02 | | | | | | | Class II | | | 5.00 | | | | 1,000.00 | | | | 1,022.48 | | | | 0.48 | | | | 2.41 | |

| 1 | For the period April 15, 2020 (inception date) to June 30, 2020. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Does not include fees and expenses of the Underlying Funds in which the Portfolio invests. |

| 4 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal period (76), then divided by 366. |

| 5 | For the six months ended June 30, 2020. |

| 6 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (182), then divided by 366. |

| | |

| 14 | | Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report |

Schedules of investments (unaudited)

June 30, 2020

Legg Mason/QS Aggressive Model Portfolio

| | | | | | | | | | | | |

| Description | | | | | Shares | | | Value | |

| Investments in Underlying Funds — 97.9% | | | | | | | | | | | | |

American Funds Insurance Series: | | | | | | | | | | | | |

Blue Chip Income and Growth Fund, Class 1A | | | | | | | 26,256 | | | $ | 319,795 | |

Growth Fund, Class 1A | | | | | | | 12,639 | | | | 1,114,344 | |

New World Fund, Class 1A | | | | | | | 35,229 | | | | 858,522 | |

BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | | | | | | 20,570 | | | | 552,722 | |

Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | | | | | | 18,432 | | | | 475,359 | |

Janus Aspen Series — Janus Henderson VIT Global Research Portfolio, Institutional Shares | | | | | | | 9,158 | | | | 468,823 | |

MainStay VP Funds Trust: | | | | | | | | | | | | |

MainStay Epoch U.S. Equity Yield Portfolio, Initial Shares | | | | | | | 56,804 | | | | 782,583 | |

MainStay VP CBRE Global Infrastructure Portfolio, Initial Class | | | | | | | 62,051 | | | | 391,049 | |

MainStay VP Fidelity Institutional AM Utilities Portfolio, Initial Class | | | | | | | 113,286 | | | | 1,315,200 | |

MainStay VP Indexed Bond Portfolio, Initial Class | | | | | | | 109,470 | | | | 1,237,495 | * |

MainStay VP MacKay Common Stock Portfolio, Initial Class | | | | | | | 67,029 | | | | 1,723,933 | |

MainStay VP MacKay S&P 500 Index Portfolio, Initial Class | | | | | | | 37,089 | | | | 2,216,722 | |

MainStay VP Winslow Large Cap Growth Portfolio, Initial Class | | | | | | | 30,330 | | | | 867,293 | |

Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | | | | | | 96,886 | | | | 1,928,028 | |

Variable Insurance Products Fund II: | | | | | | | | | | | | |

VIP Contrafund® Portfolio, Initial Class | | | | | | | 15,273 | | | | 616,888 | (a) |

VIP International Index Portfolio, Initial Class | | | | | | | 48,963 | | | | 439,200 | |

Variable Insurance Products Fund III — VIP Growth Opportunities Portfolio, Initial Class | | | | | | | 5,481 | | | | 309,884 | |

Total Investments in Underlying Funds before Short-Term Investments (Cost — $15,336,682) | | | | | | | | | | | 15,617,840 | |

| | | |

| | | Rate | | | | | | | |

| Short-Term Investments — 2.2% | | | | | | | | | | | | |

Blackrock Liquidity Funds — Treasury Trust Fund, Institutional Shares

(Cost — $355,048) | | | 0.065 | % | | | 355,048 | | | | 355,048 | |

Total Investments — 100.1% (Cost — $15,691,730) | | | | | | | | | | | 15,972,888 | |

Liabilities in Excess of Other Assets — (0.1)% | | | | | | | | | | | (23,690 | ) |

Total Net Assets — 100.0% | | | | | | | | | | $ | 15,949,198 | |

| * | Non-income producing security. |

| (a) | Contrafund is a registered service mark of FMR LLC. |

See Notes to Financial Statements.

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 15 |

Schedules of investments (unaudited) (cont’d)

June 30, 2020

Legg Mason/QS Moderately Aggressive Model Portfolio

| | | | | | | | | | | | |

| Description | | | | | Shares | | | Value | |

| Investments in Underlying Funds — 97.2% | | | | | | | | | | | | |

American Funds Insurance Series: | | | | | | | | | | | | |

Blue Chip Income and Growth Fund, Class 1A | | | | | | | 82,234 | | | $ | 1,001,612 | |

Growth Fund, Class 1A | | | | | | | 28,476 | | | | 2,510,698 | |

New World Fund, Class 1A | | | | | | | 50,391 | | | | 1,228,022 | |

BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | | | | | | 36,971 | | | | 993,406 | |

Columbia Funds Variable Series Trust II — Columbia Variable Portfolio — Emerging Markets Bond Fund, Class I | | | | | | | 271,134 | | | | 2,491,724 | |

Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | | | | | | 38,204 | | | | 985,273 | |

Janus Aspen Series — Janus Henderson VIT Global Research Portfolio, Institutional Shares | | | | | | | 19,254 | | | | 985,602 | |

MainStay VP Funds Trust: | | | | | | | | | | | | |

MainStay Epoch U.S. Equity Yield Portfolio, Initial Shares | | | | | | | 196,611 | | | | 2,708,712 | |

MainStay VP Bond Portfolio, Initial Class | | | | | | | 257,122 | | | | 3,951,728 | |

MainStay VP CBRE Global Infrastructure Portfolio, Initial Class | | | | | | | 194,688 | | | | 1,226,945 | |

MainStay VP Fidelity Institutional AM Utilities Portfolio, Initial Class | | | | | | | 231,256 | | | | 2,684,772 | |

MainStay VP Indexed Bond Portfolio, Initial Class | | | | | | | 437,313 | | | | 4,943,563 | * |

MainStay VP MacKay Common Stock Portfolio, Initial Class | | | | | | | 172,837 | | | | 4,445,230 | |

MainStay VP MacKay Government Portfolio, Initial Class | | | | | | | 87,425 | | | | 987,907 | |

MainStay VP MacKay S&P 500 Index Portfolio, Initial Class | | | | | | | 102,231 | | | | 6,110,083 | |

MainStay VP Winslow Large Cap Growth Portfolio, Initial Class | | | | | | | 69,459 | | | | 1,986,213 | |

PIMCO Variable Insurance Trust — PIMCO International Bond Portfolio (U.S. Dollar-Hedged), Institutional Class | | | | | | | 228,279 | | | | 2,472,267 | |

Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | | | | | | 195,797 | | | | 3,896,358 | |

Variable Insurance Products Fund II: | | | | | | | | | | | | |

VIP Contrafund® Portfolio, Initial Class | | | | | | | 36,104 | | | | 1,458,232 | (a) |

VIP International Index Portfolio, Initial Class | | | | | | | 142,757 | | | | 1,280,526 | |

Variable Insurance Products Fund III — VIP Growth Opportunities Portfolio, Initial Class | | | | | | | 17,223 | | | | 973,811 | |

Total Investments in Underlying Funds before Short-Term Investments (Cost — $48,370,087) | | | | | | | | | | | 49,322,684 | |

| | | |

| | | Rate | | | | | | | |

| Short-Term Investments — 6.0% | | | | | | | | | | | | |

Blackrock Liquidity Funds — Treasury Trust Fund, Institutional Shares

(Cost — $3,026,151) | | | 0.065 | % | | | 3,026,151 | | | | 3,026,151 | |

Total Investments — 103.2% (Cost — $51,396,238) | | | | | | | | | | | 52,348,835 | |

Liabilities in Excess of Other Assets — (3.2)% | | | | | | | | | | | (1,627,704 | ) |

Total Net Assets — 100.0% | | | | | | | | | | $ | 50,721,131 | |

| * | Non-income producing security. |

| (a) | Contrafund is a registered service mark of FMR LLC. |

See Notes to Financial Statements.

| | |

| 16 | | Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report |

Legg Mason/QS Moderate Model Portfolio

| | | | | | | | | | | | |

| Description | | | | | Shares | | | Value | |

| Investments in Underlying Funds — 97.1% | | | | | | | | | | | | |

American Funds Insurance Series: | | | | | | | | | | | | |

Blue Chip Income and Growth Fund, Class 1A | | | | | | | 75,083 | | | $ | 914,507 | |

Growth Fund, Class 1A | | | | | | | 18,170 | | | | 1,602,037 | |

BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | | | | | | 33,891 | | | | 910,663 | |

Columbia Funds Variable Series Trust II — Columbia Variable Portfolio — Emerging Markets Bond Fund, Class I | | | | | | | 195,101 | | | | 1,792,973 | |

Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | | | | | | 35,205 | | | | 907,943 | |

MainStay VP Funds Trust: | | | | | | | | | | | | |

MainStay Epoch U.S. Equity Yield Portfolio, Initial Shares | | | | | | | 146,688 | | | | 2,020,914 | |

MainStay VP Bond Portfolio, Initial Class | | | | | | | 375,557 | | | | 5,771,968 | |

MainStay VP CBRE Global Infrastructure Portfolio, Initial Class | | | | | | | 213,724 | | | | 1,346,912 | |

MainStay VP Fidelity Institutional AM Utilities Portfolio, Initial Class | | | | | | | 191,600 | | | | 2,224,376 | |

MainStay VP Indexed Bond Portfolio, Initial Class | | | | | | | 346,114 | | | | 3,912,606 | * |

MainStay VP MacKay Common Stock Portfolio, Initial Class | | | | | | | 140,155 | | | | 3,604,684 | |

MainStay VP MacKay Government Portfolio, Initial Class | | | | | | | 294,944 | | | | 3,332,901 | |

MainStay VP MacKay S&P 500 Index Portfolio, Initial Class | | | | | | | 94,135 | | | | 5,626,197 | |

MainStay VP Winslow Large Cap Growth Portfolio, Initial Class | | | | | | | 63,400 | | | | 1,812,951 | |

PIMCO Variable Insurance Trust — PIMCO International Bond Portfolio (U.S. Dollar-Hedged), Institutional Class | | | | | | | 430,599 | | | | 4,663,388 | |

Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | | | | | | 78,234 | | | | 1,556,864 | |

Variable Insurance Products Fund II: | | | | | | | | | | | | |

VIP Contrafund® Portfolio, Initial Class | | | | | | | 27,464 | | | | 1,109,279 | (a) |

VIP International Index Portfolio, Initial Class | | | | | | | 183,678 | | | | 1,647,590 | |

Total Investments in Underlying Funds before Short-Term Investments (Cost — $44,161,696) | | | | | | | | | | | 44,758,753 | |

| | | |

| | | Rate | | | | | | | |

| Short-Term Investments — 3.2% | | | | | | | | | | | | |

Blackrock Liquidity Funds — Treasury Trust Fund, Institutional Shares

(Cost — $1,498,790) | | | 0.065 | % | | | 1,498,790 | | | | 1,498,790 | |

Total Investments — 100.3% (Cost — $45,660,486) | | | | | | | | | | | 46,257,543 | |

Liabilities in Excess of Other Assets — (0.3)% | | | | | | | | | | | (145,792 | ) |

Total Net Assets — 100.0% | | | | | | | | | | $ | 46,111,751 | |

| * | Non-income producing security. |

| (a) | Contrafund is a registered service mark of FMR LLC. |

See Notes to Financial Statements.

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 17 |

Schedules of investments (unaudited) (cont’d)

June 30, 2020

Legg Mason/QS Moderately Conservative Model Portfolio

| | | | | | | | | | | | |

| Description | | | | | Shares | | | Value | |

| Investments in Underlying Funds — 88.9% | | | | | | | | | | | | |

American Funds Insurance Series — Growth Fund, Class 1A | | | | | | | 5,218 | | | $ | 460,099 | |

BlackRock Variable Series Funds II, Inc. — BlackRock High Yield V.I. Fund, Class I | | | | | | | 64,116 | | | | 447,527 | |

BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | | | | | | 16,892 | | | | 453,876 | |

Columbia Funds Variable Series Trust II — Columbia Variable Portfolio — Emerging Markets Bond Fund, Class I | | | | | | | 48,690 | | | | 447,463 | |

Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | | | | | | 17,604 | | | | 454,013 | |

MainStay VP Funds Trust: | | | | | | | | | | | | |

MainStay VP Bond Portfolio, Initial Class | | | | | | | 217,178 | | | | 3,337,825 | |

MainStay VP CBRE Global Infrastructure Portfolio, Initial Class | | | | | | | 88,768 | | | | 559,428 | |

MainStay VP Fidelity Institutional AM Utilities Portfolio, Initial Class | | | | | | | 76,981 | | | | 893,713 | |

MainStay VP Indexed Bond Portfolio, Initial Class | | | | | | | 171,004 | | | | 1,933,100 | * |

MainStay VP MacKay Common Stock Portfolio, Initial Class | | | | | | | 61,565 | | | | 1,583,391 | |

MainStay VP MacKay Government Portfolio, Initial Class | | | | | | | 275,554 | | | | 3,113,785 | |

MainStay VP MacKay High Yield Corporate Bond Portfolio, Initial Class | | | | | | | 46,582 | | | | 444,764 | |

MainStay VP MacKay S&P 500 Index Portfolio, Initial Class | | | | | | | 42,821 | | | | 2,559,313 | |

MainStay VP Winslow Large Cap Growth Portfolio, Initial Class | | | | | | | 15,805 | | | | 451,937 | |

PIMCO Variable Insurance Trust — PIMCO International Bond Portfolio (U.S. Dollar-Hedged), Institutional Class | | | | | | | 308,367 | | | | 3,339,615 | |

Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | | | | | | 27,899 | | | | 555,193 | |

Variable Insurance Products Fund II: | | | | | | | | | | | | |

VIP Contrafund® Portfolio, Initial Class | | | | | | | 10,973 | | | | 443,202 | (a) |

VIP International Index Portfolio, Initial Class | | | | | | | 99,173 | | | | 889,578 | |

Total Investments in Underlying Funds before Short-Term Investments (Cost — $22,306,462) | | | | | | | | | | | 22,367,822 | |

| | | |

| | | Rate | | | | | | | |

| Short-Term Investments — 2.7% | | | | | | | | | | | | |

Blackrock Liquidity Funds — Treasury Trust Fund, Institutional Shares

(Cost — $683,849) | | | 0.065 | % | | | 683,849 | | | | 683,849 | |

Total Investments — 91.6% (Cost — $22,990,311) | | | | | | | | | | | 23,051,671 | |

Other Assets in Excess of Liabilities — 8.4% | | | | | | | | | | | 2,127,636 | |

Total Net Assets — 100.0% | | | | | | | | | | $ | 25,179,307 | |

| * | Non-income producing security. |

| (a) | Contrafund is a registered service mark of FMR LLC. |

See Notes to Financial Statements.

| | |

| 18 | | Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report |

Legg Mason/QS Conservative Model Portfolio

| | | | | | | | | | | | |

| Description | | | | | Shares | | | Value | |

| Investments in Underlying Funds — 98.6% | | | | | | | | | | | | |

BlackRock Variable Series Funds II, Inc. — BlackRock High Yield V.I. Fund, Class I | | | | | | | 59,907 | | | $ | 418,148 | |

MainStay VP Funds Trust: | | | | | | | | | | | | |

MainStay VP Bond Portfolio, Initial Class | | | | | | | 101,387 | | | | 1,558,226 | |

MainStay VP Indexed Bond Portfolio, Initial Class | | | | | | | 83,604 | | | | 945,094 | * |

MainStay VP MacKay Common Stock Portfolio, Initial Class | | | | | | | 40,902 | | | | 1,051,977 | |

MainStay VP MacKay Government Portfolio, Initial Class | | | | | | | 137,940 | | | | 1,558,740 | |

MainStay VP MacKay High Yield Corporate Bond Portfolio, Initial Class | | | | | | | 119,480 | | | | 1,140,796 | |

MainStay VP MacKay S&P 500 Index Portfolio, Initial Class | | | | | | | 19,173 | | | | 1,145,908 | |

PIMCO Variable Insurance Trust: | | | | | | | | | | | | |

PIMCO International Bond Portfolio (U.S. Dollar-Hedged), Institutional Class | | | | | | | 129,693 | | | | 1,404,573 | |

PIMCO Total Return Portfolio, Institutional Class | | | | | | | 104,643 | | | | 1,196,068 | |

Total Investments in Underlying Funds before Short-Term Investments (Cost — $10,345,269) | | | | | | | | | | | 10,419,530 | |

| | | |

| | | Rate | | | | | | | |

| Short-Term Investments — 10.3% | | | | | | | | | | | | |

Blackrock Liquidity Funds — Treasury Trust Fund, Institutional Shares

(Cost — $1,094,143) | | | 0.065 | % | | | 1,094,143 | | | | 1,094,143 | |

Total Investments — 108.9% (Cost — $11,439,412) | | | | | | | | | | | 11,513,673 | |

Liabilities in Excess of Other Assets — (8.9)% | | | | | | | | | | | (943,285 | ) |

Total Net Assets — 100.0% | | | | | | | | | | $ | 10,570,388 | |

| * | Non-income producing security. |

See Notes to Financial Statements.

| | |

| Legg Mason/QS Model Portfolio Funds 2020 Semi-Annual Report | | 19 |

Statements of assets and liabilities (unaudited)

June 30, 2020

| | | | | | | | | | | | |

| | | Legg Mason/

QS Aggressive

Model Portfolio | | | Legg Mason/QS

Moderately

Aggressive

Model Portfolio | | | Legg Mason/QS

Moderate

Model Portfolio | |

| | | |

| Assets: | | | | | | | | | | | | |

Investments in Underlying Funds, at cost | | $ | 15,691,730 | | | $ | 51,396,238 | | | $ | 45,660,486 | |

Investments in Underlying Funds, at value | | | 15,972,888 | | | | 52,348,835 | | | | 46,257,543 | |

Receivable for Portfolio shares sold | | | 206,456 | | | | 929,543 | | | | 931,080 | |

Deferred offering costs | | | 28,029 | | | | 28,029 | | | | 28,029 | |