As filed with the Securities and Exchange Commission on January 5, 2023

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21168

NEUBERGER BERMAN MUNICIPAL FUND INC.

(Exact Name of Registrant as specified in charter)

c/o Neuberger Berman Investment Advisers LLC

1290 Avenue of the Americas

New York, New York 10104-0002

(Address of Principal Executive Offices – Zip Code)

Joseph V. Amato

Chief Executive Officer and President

Neuberger Berman Municipal Fund Inc.

c/o Neuberger Berman Investment Advisers LLC

1290 Avenue of the Americas

New York, New York 10104-0002

Lori L. Schneider, Esq.

K&L Gates LLP

1601 K Street, N.W.

Washington, D.C. 20006-1600

(Names and addresses of agents for service)

Registrant's telephone number, including area code: (212) 476-8800

Date of fiscal year end: October 31

Date of reporting period: October 31, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940, as amended (“Act”) (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-1090. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Report to Stockholders.

Following is a copy of the annual report transmitted to stockholders pursuant to Rule 30e-1 under the Act.

Neuberger Berman

Municipal Closed-End Funds

Neuberger Berman California

Municipal Fund Inc. |

|

Neuberger Berman Municipal

Fund Inc. |

|

Neuberger Berman New York

Municipal Fund Inc. |

Annual Report

October 31, 2022

The "Neuberger Berman" name and logo and "Neuberger Berman Investment Advisers LLC" name are registered service marks of Neuberger Berman Group LLC. The individual Fund names in this piece are either service marks or registered service marks of Neuberger Berman Investment Advisers LLC. ©2022 Neuberger Berman Investment Advisers LLC. All rights reserved.

President’s Letter

Dear Stockholder,

I am pleased to present this annual report for Neuberger Berman California Municipal Fund Inc. (NBW), Neuberger Berman Municipal Fund Inc. (NBH) and Neuberger Berman New York Municipal Fund Inc. (NBO and, together with NBW and NBH, the Funds) for the 12 months ended October 31, 2022 (the reporting period). The report includes for each Fund a portfolio commentary, a listing of the Fund’s investments and its audited financial statements for the reporting period.

Each Fund’s investment objective is to provide a high level of current income exempt from federal income tax and, for the state-specific Funds, NBW seeks to provide income that is also exempt from California personal income taxes and NBO seeks to provide income that is also exempt from New York State and New York City personal income taxes. The Funds may invest in securities the interest on which is subject to the federal alternative minimum tax.

We maintain a conservative investment philosophy and disciplined investment process in an effort to provide you with tax-exempt current income over the long term with less volatility and risk.

As previously communicated, in December 2021, each Fund extended the term of its existing Variable Rate Municipal Term Preferred Shares (VMTP Shares) to December 15, 2024. Each Fund’s VMTP Shares previously had a term redemption date of March 31, 2022. In both August 2022 and November 2022, each Fund redeemed a portion of its outstanding VMTP Shares. For each partial redemption, the redemption price for the VMTP Shares was the $100,000 liquidation preference per share plus the final accumulated distribution amounts owed. Overall, as a result of the transactions, NBH redeemed 247 VMTP Shares and has 1,457 VMTP Shares outstanding; NBW redeemed 93 VMTP Shares and has 457 VMTP Shares outstanding; and NBO redeemed 98 VMTP Shares and has 365 VMTP Shares outstanding.

In April 2022, NBH announced a decrease in its monthly distribution rate to $0.05025 per share of common stock from the prior monthly distribution rate of $0.06244 per share. The decrease in the Fund’s distribution rate was the result of numerous factors, including the expected level of yields available in the municipal market and the corresponding impact on the Fund’s level of earnings, expected increased costs of leverage associated with forecasted interest-rate hikes and the amount of available undistributed net investment income.

Thank you for your confidence in the Funds. We will continue to do our best to retain your trust in the years to come.

Sincerely,

Joseph V. Amato

President and CEO

Neuberger Berman California Municipal Fund Inc.

Neuberger Berman Municipal Fund Inc.

Neuberger Berman New York Municipal Fund Inc.

Neuberger Berman Municipal Closed-End Funds

Portfolio Commentary (Unaudited)

For the 12 months ended October 31, 2022 (the reporting period), on a net asset value (NAV) basis, all three of the Neuberger Berman Municipal Closed-End Funds underperformed their benchmark, the Bloomberg 10-Year Municipal Bond Index (the Index). Neuberger Berman California Municipal Fund Inc. (NBW), Neuberger Berman Municipal Fund Inc. (NBH) and Neuberger Berman New York Municipal Fund Inc. (NBO and, together with NBW and NBH, the Funds) posted -20.22%, -21.57% and -22.61% total returns, respectively, whereas the Index generated a -10.23% total return for the same period. (Fund performance on a market price basis is provided in the tables immediately following this commentary.) The use of leverage (typically a performance enhancer in up markets and a detractor during market retreats) was a meaningful detractor from performance given the negative price return for the municipal market during the reporting period.

The investment-grade municipal bond market generated weak results but outperformed the taxable bond market during the reporting period. All told, the Bloomberg Municipal Bond Index returned -11.98% for the reporting period, whereas the overall taxable investment-grade bond market, as measured by the Bloomberg U.S. Aggregate Bond Index, returned -15.68%. While the U.S. Federal Reserve Board (Fed) initially characterized rising inflation as being "transitory," this was not the case. Robust consumer spending, supply chain bottlenecks, repercussions from the war in Ukraine, and other factors combined to push U.S. inflation to a 40-year high. Against this backdrop, the Fed began an aggressive rate hike campaign in March 2022, which we expect to continue until inflation is under control, even if it potentially leads to a recession. Rising yields dragged down fixed income market performance, as yields and bond prices moved in the opposite direction.

Looking at the Funds’ performance, an overweight to lower coupon, lower-quality, and longer-term bonds versus the Index detracted from results as interest rates moved sharply higher. Overweight to BB and underweight to AA rated bonds also detracted from overall returns. Overall, security selection of revenue bonds was not rewarded. On the upside, an overweight to pre-refunded securities was additive for returns as they outperformed the Index. For NBW, an overweight to California versus the Index was beneficial. For NBO, an overweight to New York versus the Index was positive for performance.

There were no meaningful changes to the Funds’ portfolios during the reporting period as a whole.

Looking ahead, we anticipate market volatility to remain elevated until there is more clarity on the economic outlook. From a supply/demand perspective, mutual fund outflows have reached record highs as the Fed raises rates in an attempt to rein in inflation. Meanwhile, municipal bonds’ supply remains lower than in 2021 and new issuance tends to be lighter as we near the end of the year. While municipal bonds’ credit fundaments have generally peaked, in our opinion, most issuers are cushioned with solid balance sheets. In addition, we believe that stronger cash positions should provide a cushion as economic growth moderates. We continue to be cautious in terms of our duration positioning but believe higher yields and volatility create a favorable backdrop to deploy cash and capitalize on attractively valued securities.

Sincerely,

James L. Iselin and S. Blake Miller

Portfolio Co-Managers

The portfolio composition, industries and holdings of each Fund are subject to change without notice.

The opinions expressed are those of the Funds' portfolio managers. The opinions are as of the date of this report and are subject to change without notice.

The value of securities owned by a Fund, as well as the market value of shares of the Fund’s common stock, may decline in response to certain events, including those directly involving the issuers whose securities are owned by the Fund; conditions affecting the general economy; overall market changes; local, regional, national or global political, social or economic instability; regulatory or legislative developments; price and interest rate fluctuations, including those resulting from changes in central bank policies; and changes in investor sentiment.

The bond rating(s) noted above represent segments of the Bloomberg 10-Year Municipal Bond Index, which are determined based on the average ratings issued by S&P Global, Moody’s and Fitch.

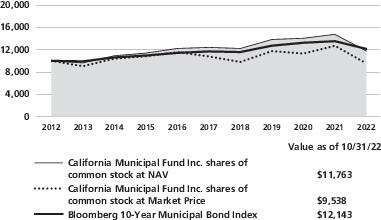

California Municipal Fund Inc. (Unaudited)

|

California Municipal Fund Inc. | |

PORTFOLIO BY STATE AND TERRITORY |

(as a % of Total Investments*) |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Does not include the impact of the Fund’s open positions in derivatives, if any. |

|

| | Average Annual Total Return

Ended 10/31/2022 |

| | | | |

| | | | | |

California Municipal Fund Inc. | | | | | |

| | | | | |

California Municipal Fund Inc. | | | | | |

| | | | | |

Bloomberg 10-Year Municipal | | | | | |

Listed closed-end funds, unlike open-end funds, are not continually offered. Generally, there is an initial public offering and, once issued, shares of common stock of closed-end funds are sold in the secondary market on a stock exchange.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For current performance data, please visit www.nb.com/cef-performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a stockholder would pay on Fund distributions or on the sale of shares of the Fund's common stock.

The investment return and market price will fluctuate and shares of the Fund’s common stock may trade at prices above or below NAV. Shares of the Fund’s common stock, when sold, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not waived a portion of its investment management fees during certain of the periods shown. The waived fees are from prior years that are no longer disclosed in the Financial Highlights.

California Municipal Fund Inc. (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The graph is based on the Fund’s shares of common stock both at net asset value (NAV) and at market price. The Fund’s common stock may trade at market prices above or below NAV per share (see Performance Highlights chart). The result is compared with a broad-based market index. The market index has not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any, at prices obtained under the Fund’s Distribution Reinvestment Plan. The results do not reflect the effect of taxes a stockholder would pay on Fund distributions or on the sale of Fund shares. Results represent past performance and do not indicate future results.

Impact of the Fund’s Distribution Policy

The Fund has a practice of seeking to maintain a relatively stable level of distributions to common stockholders. In general, this practice does not affect the Fund’s investment strategy and may reduce the Fund’s NAV. Management believes the practice helps maintain the Fund’s competitiveness and may benefit the Fund’s market price and its premium/discount to the Fund’s NAV per share. During the 12-month period ended October 31, 2022, the Fund made distributions to common stockholders totaling $0.54 per share, of which $0.00 will be treated as a return of capital for tax purposes.

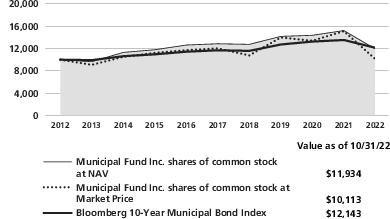

Municipal Fund Inc. (Unaudited)

PORTFOLIO BY STATE AND TERRITORY |

(as a % of Total Investments*) |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Does not include the impact of the Fund’s open positions in derivatives, if any. |

|

| | Average Annual Total Return

Ended 10/31/2022 |

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

Bloomberg 10-Year

Municipal | | | | | |

Listed closed-end funds, unlike open-end funds, are not continually offered. Generally, there is an initial public offering and, once issued, shares of common stock of closed-end funds are sold in the secondary market on a stock exchange.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For current performance data, please visit www.nb.com/cef-performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a stockholder would pay on Fund distributions or on the sale of shares of the Fund's common stock.

The investment return and market price will fluctuate and shares of the Fund’s common stock may trade at prices above or below NAV. Shares of the Fund’s common stock, when sold, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not waived a portion of its investment management fees during certain of the periods shown. The waived fees are from prior years that are no longer disclosed in the Financial Highlights.

Municipal Fund Inc. (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The graph is based on the Fund’s shares of common stock both at net asset value (NAV) and at market price. The Fund’s common stock may trade at market prices above or below NAV per share (see Performance Highlights chart). The result is compared with a broad-based market index. The market index has not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any, at prices obtained under the Fund’s Distribution Reinvestment Plan. The results do not reflect the effect of taxes a stockholder would pay on Fund distributions or on the sale of Fund shares. Results represent past performance and do not indicate future results.

Impact of the Fund’s Distribution Policy

The Fund has a practice of seeking to maintain a relatively stable level of distributions to common stockholders. In general, this practice does not affect the Fund’s investment strategy and may reduce the Fund’s NAV. Management believes the practice helps maintain the Fund’s competitiveness and may benefit the Fund’s market price and its premium/discount to the Fund’s NAV per share. During the 12-month period ended October 31, 2022, the Fund made distributions to common stockholders totaling $0.66 per share, of which $0.00 will be treated as a return of capital for tax purposes.

New York Municipal Fund Inc. (Unaudited)

|

New York Municipal Fund Inc. | |

PORTFOLIO BY STATE AND TERRITORY |

(as a % of Total Investments*) |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Does not include the impact of the Fund’s open positions in derivatives, if any. |

|

| | Average Annual Total Return

Ended 10/31/2022 |

| | | | |

| | | | | |

New York Municipal Fund Inc. | | | | | |

| | | | | |

New York Municipal Fund Inc. | | | | | |

| | | | | |

Bloomberg 10-Year

Municipal | | | | | |

Listed closed-end funds, unlike open-end funds, are not continually offered. Generally, there is an initial public offering and, once issued, shares of common stock of closed-end funds are sold in the secondary market on a stock exchange.

The performance data quoted represent past performance and do not indicate future results. Current performance may be lower or higher than the performance data quoted. For current performance data, please visit www.nb.com/cef-performance.

The results shown in the table reflect the reinvestment of income dividends and other distributions, if any. The results do not reflect the effect of taxes a stockholder would pay on Fund distributions or on the sale of shares of the Fund's common stock.

The investment return and market price will fluctuate and shares of the Fund’s common stock may trade at prices above or below NAV. Shares of the Fund’s common stock, when sold, may be worth more or less than their original cost.

Returns would have been lower if Neuberger Berman Investment Advisers LLC ("NBIA") had not waived a portion of its investment management fees during certain of the periods shown. The waived fees are from prior years that are no longer disclosed in the Financial Highlights.

New York Municipal Fund Inc. (Unaudited)

COMPARISON OF A $10,000 INVESTMENT

This graph shows the change in value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal years. The graph is based on the Fund’s shares of common stock both at net asset value (NAV) and at market price. The Fund’s common stock may trade at market prices above or below NAV per share (see Performance Highlights chart). The result is compared with a broad-based market index. The market index has not been reduced to reflect any of the fees and costs of investing. The results shown in the graph reflect the reinvestment of income dividends and other distributions, if any, at prices obtained under the Fund’s Distribution Reinvestment Plan. The results do not reflect the effect of taxes a stockholder would pay on Fund distributions or on the sale of Fund shares. Results represent past performance and do not indicate future results.

Impact of the Fund’s Distribution Policy

The Fund has a practice of seeking to maintain a relatively stable level of distributions to common stockholders. In general, this practice does not affect the Fund’s investment strategy and may reduce the Fund’s NAV. Management believes the practice helps maintain the Fund’s competitiveness and may benefit the Fund’s market price and its premium/discount to the Fund’s NAV per share. During the 12-month period ended October 31, 2022, the Fund made distributions to common stockholders totaling $0.47 per share, of which $0.00 will be treated as a return of capital for tax purposes.

| A portion of each Fund’s income may be a tax preference item for purposes of the federal alternative minimum tax for certain stockholders. |

| Returns based on the NAV of each Fund. |

| Returns based on the market price of shares of each Fund’s common stock on the NYSE American. |

| Please see "Description of Index" on page 10 for a description of the index. |

For more complete information on any of the Neuberger Berman Municipal Closed-End Funds, call Neuberger Berman Investment Advisers LLC at (877) 461-1899, or visit our website at www.nb.com.

Description of Index (Unaudited)

Bloomberg 10-Year Municipal Bond Index: | The index is the 10-year (8-12 years to maturity) component of the Bloomberg Municipal Bond Index. The Bloomberg Municipal Bond Index measures the investment grade, U.S. dollar-denominated, long-term, tax-exempt bond market and has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. |

Please note that the index does not take into account any fees and expenses or any tax consequences of investing in the individual securities that it tracks and that individuals cannot invest directly in any index. Data about the performance of this index are prepared or obtained by NBIA and include reinvestment of all income dividends and other distributions, if any. Each Fund may invest in securities not included in the above described index and generally does not invest in all securities included in the index.

Legend October 31, 2022 (Unaudited)

Neuberger Berman Municipal Closed-End Funds

|

| = Neuberger Berman Investment Advisers LLC |

Schedule of Investments California Municipal Fund Inc.^

October 31, 2022

| |

|

|

| American Samoa Econ. Dev. Au. Gen. Rev. Ref., Ser. 2015-A, 6.25%, due 9/1/2029 | |

|

| Bay Area Toll Au. Toll Bridge Rev., Ser. 2013-S-4, 5.00%, due 4/1/2027 Pre-Refunded 4/1/2023 | |

| California Comm. Choice Fin. Clean Energy Proj. Au. Rev. Green Bond, Ser. 2021 B-1, (LOC: Morgan Stanley), 4.00%, due 2/1/2052 Putable 8/1/2031 | |

| California Ed. Facs. Au. Ref. Rev. (Univ. of Redlands) | |

| Ser. 2016-A, 5.00%, due 10/1/2028 | |

| Ser. 2016-A, 3.00%, due 10/1/2029 | |

| Ser. 2016-A, 3.00%, due 10/1/2030 | |

| California Ed. Facs. Au. Rev. (Green Bond- Loyola Marymount Univ.), Ser. 2018-B, 5.00%, due 10/1/2048 | |

| California HFA Muni. Cert. | |

| Class A, Ser. 2019-2, Class A, 4.00%, due 3/20/2033 | |

| Class A, Ser. 2021-1-A, 3.50%, due 11/20/2035 | |

| California Hlth. Facs. Fin. Au. Rev. (Children's Hosp. Los Angeles), Ser. 2012-A, 5.00%, due 11/15/2026 Pre-Refunded 11/15/2022 | |

| California Infrastructure & Econ. Dev. Bank Rev. (Wonderful Foundations Charter Sch. Portfolio Proj.), Ser. 2020-A-1, 5.00%, due 1/1/2055 | |

| California Infrastructure & Econ. Dev. Bank St. Sch. Fund Rev. (King City Joint Union High Sch.), Ser. 2010, 5.13%, due 8/15/2024 | |

| California Muni. Fin. Au. Charter Sch. Lease Rev. (Sycamore Academy Proj.), Ser. 2014, 5.63%, due 7/1/2044 | |

| California Muni. Fin. Au. Charter Sch. Lease Rev. (Vista Charter Middle Sch. Proj.), Ser. 2014, 5.13%, due 7/1/2029 | |

| California Muni. Fin. Au. Charter Sch. Rev. (John Adams Academics Proj.) | |

| Ser. 2015-A, 4.50%, due 10/1/2025 | |

| Ser. 2019-A, 5.00%, due 10/1/2049 | |

| California Muni. Fin. Au. Charter Sch. Rev. (Palmdale Aerospace Academy Proj.), Ser. 2016, 5.00%, due 7/1/2031 | |

| California Muni. Fin. Au. Rev. (Baptist Univ.), Ser. 2015-A, 5.00%, due 11/1/2030 | |

| California Muni. Fin. Au. Rev. (Biola Univ.) | |

| Ser. 2013, 4.00%, due 10/1/2025 | |

| Ser. 2013, 4.00%, due 10/1/2026 | |

| Ser. 2013, 4.00%, due 10/1/2027 | |

| California Muni. Fin. Au. Rev. (Touro College & Univ. Sys. Obligated Group) | |

| Ser. 2014-A, 4.00%, due 1/1/2027 | |

| Ser. 2014-A, 4.00%, due 1/1/2028 | |

| Ser. 2014-A, 4.00%, due 1/1/2029 | |

| California Muni. Fin. Au. Std. Hsg. Rev. (CHF-Davis I, LLC-West Village Std. Hsg. Proj.), Ser. 2018, (BAM Insured), 4.00%, due 5/15/2048 | |

| California Pub. Fin. Au. Ref. (Henry Mayo Newhall Hosp.) | |

| Ser. 2021-A, 4.00%, due 10/15/2027 | |

| Ser. 2021-A, 4.00%, due 10/15/2028 | |

| California Sch. Fac. Fin. Au. Rev. (Alliance College - Ready Pub. Sch. Proj.), Ser. 2015-A, 5.00%, due 7/1/2030 | |

| California Sch. Fac. Fin. Au. Rev. (Green Dot Pub. Sch. Proj.), Ser. 2018-A, 5.00%, due 8/1/2048 | |

See Notes to Financial Statements

Schedule of Investments California Municipal Fund Inc.^ (cont’d)

| |

|

| California Sch. Fac. Fin. Au. Rev. (KIPP LA Proj.) | |

| Ser. 2014-A, 4.13%, due 7/1/2024 | |

| Ser. 2017-A, 4.00%, due 7/1/2023 | |

| Ser. 2017-A, 5.00%, due 7/1/2025 | |

| Ser. 2017-A, 5.00%, due 7/1/2027 | |

| California St. Dept. of Veterans Affairs Home Purchase Ref. Rev., Ser. 2016-A, 3.00%, due 6/1/2029 | |

| | |

| Ser. 2020, 3.00%, due 11/1/2050 | |

| Ser. 2022, 3.00%, due 4/1/2052 | |

| Ser. 2022, 5.00%, due 9/1/2052 | |

| California St. Infrastructure & Econ. Dev. Bank Rev. (California Academy of Sciences), Ser. 2018-D, (SIFMA), 2.59%, due 8/1/2047 Putable 8/1/2024 | |

| California St. Poll. Ctrl. Fin. Au. Rev. (San Jose Wtr. Co. Proj.), Ser. 2016, 4.75%, due 11/1/2046 | |

| California St. Poll. Ctrl. Fin. Au. Solid Waste Disp. Rev. (Aemerage Redak Svcs. So. California LLC Proj.), Ser. 2016, 7.00%, due 12/1/2027 | |

| California St. Poll. Ctrl. Fin. Au. Solid Waste Disp. Rev. (Calplant I Green Bond Proj.), Ser. 2019, 7.50%, due 12/1/2039 | |

| California St. Poll. Ctrl. Fin. Au. Solid Waste Disp. Rev. (Green Bond-Rialto Bioenergy Fac. LLC, Proj.), Ser. 2019, 7.50%, due 12/1/2040 | |

| California St. Poll. Ctrl. Fin. Au. Wtr. Furnishing Rev., Ser. 2012, 5.00%, due 7/1/2027 | |

| California St. Sch. Fin. Au. Charter Sch. Rev. (Downtown College Prep-Oblig. Group), Ser. 2016, 4.50%, due 6/1/2031 | |

| California St. Sch. Fin. Au. Charter Sch. Rev. (Rocketship Ed.), Ser. 2016-A, 5.00%, due 6/1/2031 | |

| California St. Sch. Fin. Au. Ed. Facs. Rev. (New Designs Charter Sch. Administration Campus Proj.), Ser. 2019-A, 5.00%, due 6/1/2050 | |

| California St. Sch. Fin. Au. Ed. Facs. Rev. (Partnerships Uplifts Comm. Valley Proj.), Ser. 2014-A, 5.35%, due 8/1/2024 | |

| California Statewide CDA College Hsg. Rev. (NCCD-Hooper Street LLC-College of the Arts Proj.), Ser. 2019, 5.25%, due 7/1/2052 | |

| California Statewide CDA Hosp. Rev. (Methodist Hosp. of Southern Proj.), Ser. 2018, 4.25%, due 1/1/2043 | |

| California Statewide CDA Rev. (Henry Mayo Newhall Mem. Hosp.), Ser. 2014-A, (AGM Insured), 5.00%, due 10/1/2026 Pre-Refunded 10/1/2024 | |

| California Statewide CDA Rev. (Loma Linda Univ. Med. Ctr.), Ser. 2018-A, 5.50%, due 12/1/2058 | |

| California Statewide CDA Rev. (Redwoods Proj.), Ser. 2013, 5.00%, due 11/15/2028 Pre-Refunded 15/11/2023 | |

| California Statewide CDA Rev. Ref. (Lancer Ed. Std. Hsg. Proj.), Ser. 2016-A, 5.00%, due 6/1/2036 | |

| California Statewide CDA Rev. Ref. (Loma Linda Univ. Med. Ctr.), Ser. 2014-A, 5.25%, due 12/1/2029 | |

| California Statewide CDA Rev. Ref. (Redlands Comm. Hosp.), Ser. 2016, 4.00%, due 10/1/2041 | |

| California Statewide CDA Spec. Tax Rev. Ref. (Comm. Facs. Dist. Number 2007-01 Orinda Wilder Proj.), Ser. 2015, 4.50%, due 9/1/2025 | |

| California Statewide CDA Std. Hsg. Rev. (Univ. of Irvin Campus Apts. Phase IV), Ser. 2017-A, 5.00%, due 5/15/2032 | |

| California Statewide CDA Std. Hsg. Rev. Ref. (Baptist University), Ser. 2017-A, 5.00%, due 11/1/2032 | |

| Contra Costa Co. Redev. Agcy. Successor Agcy. Tax Allocation Ref., Ser. 2017-A, (BAM Insured), 5.00%, due 8/1/2031 | |

| Corona Norco Unified Sch. Dist. Pub. Fin. Au. Sr. Lien Rev. | |

| Ser. 2013-A, 5.00%, due 9/1/2026 Pre-Refunded 9/1/2023 | |

| Ser. 2013-A, 5.00%, due 9/1/2027 Pre-Refunded 9/1/2023 | |

| Davis Joint Unified Sch. Dist. Cert. of Participation (Yolo Co.), Ser. 2014, (BAM Insured), 4.00%, due 8/1/2024 | |

| Deutsche Bank Spears/Lifers Trust Rev., Ser. 2020, (LOC: Deutsche Bank AG), 2.64%, due 12/1/2052 | |

See Notes to Financial Statements

Schedule of Investments California Municipal Fund Inc.^ (cont’d)

| |

|

| Emeryville Redev. Agcy. Successor Agcy. Tax Allocation Ref. Rev., Ser. 2014-A, (AGM Insured), 5.00%, due 9/1/2025 | |

| Foothill-Eastern Trans. Corridor Agcy. Toll Road Rev. Ref., Subser. 2014-B2, 3.50%, due 1/15/2053 | |

| Golden St. Tobacco Securitization Corp. Tobacco Settlement Rev. Ref., Ser. 2021-B-2, 0.00%, due 6/1/2066 | |

| Imperial Comm. College Dist. G.O. Cap. Appreciation (Election 2010), Ser. 2011-A, (AGM Insured), 6.75%, due 8/1/2040 Pre-Refunded 8/1/2025 | |

| Inglewood Unified Sch. Dist. Facs. Fin. Au. Rev., Ser. 2007, (AGM Insured), 5.25%, due 10/15/2026 | |

| Irvine Spec. Tax (Comm. Facs. Dist. Number 2005-2) | |

| Ser. 2013, 4.00%, due 9/1/2023 | |

| Ser. 2013, 4.00%, due 9/1/2024 | |

| Ser. 2013, 4.00%, due 9/1/2025 | |

| Ser. 2013, 3.50%, due 9/1/2026 | |

| Ser. 2013, 3.63%, due 9/1/2027 | |

| Jurupa Pub. Fin. Auth. Spec. Tax Rev., Ser. 2014-A, 5.00%, due 9/1/2024 | |

| Los Angeles City Dept. of Arpts. Arpt. Rev., Ser. 2020-C, 4.00%, due 5/15/2050 | |

| Los Angeles Co., Ser. 2022, 4.00%, due 6/30/2023 | |

| Los Angeles Co. Metro. Trans. Au. Rev. (Green Bond), Ser. 2020-A, 5.00%, due 6/1/2031 | |

| North Orange Co. Comm. College Dist. G.O., Ser. 2022-C, 4.00%, due 8/1/2047 | |

| Ohlone Comm. College Dist. G.O. (Election 2010), Ser. 2014-B, 0.00%, due 8/1/2029 Pre-Refunded 8/1/2024 | |

| Oxnard Harbor Dist. Rev., Ser. 2011-B, 4.50%, due 8/1/2024 | |

| Palomar Hlth. Ref. Rev., Ser. 2016, 4.00%, due 11/1/2039 | |

| Rancho Cucamonga Redev. Agcy. Successor Agcy. Tax Allocation Rev. (Rancho Redev. Proj.), Ser. 2014, (AGM Insured), 5.00%, due 9/1/2027 | |

| Riverside Co. Comm. Facs. Dist. Spec. Tax Rev. (Scott Road), Ser. 2013, 5.00%, due 9/1/2025 | |

| Riverside Co. Trans. Commission Toll Rev. Ref. Sr. Lien (RCTC Number 91 Express Lanes), Ser. 2021-B-1, 4.00%, due 6/1/2046 | |

| Riverside Co. Trans. Commission Toll Rev. Sr. Lien (Cap. Appreciation), Ser. 2013-B, 0.00%, due 6/1/2023 | |

| Romoland Sch. Dist. Spec. Tax Ref. (Comm. Facs. Dist. Number 2006-1) | |

| Ser. 2017, 4.00%, due 9/1/2029 | |

| Ser. 2017, 4.00%, due 9/1/2030 | |

| Ser. 2017, 3.25%, due 9/1/2031 | |

| Sacramento Area Flood Ctrl. Agcy. Ref. (Consol Cap. Assessment Dist. Number 2), Ser. 2016-A, 5.00%, due 10/1/2047 | |

| Sacramento City Fin. Au. Ref. Rev. (Master Lease Prog. Facs.) | |

| Ser. 2006-E, (AMBAC Insured), 5.25%, due 12/1/2024 | |

| Ser. 2006-E, (AMBAC Insured), 5.25%, due 12/1/2026 | |

| Sacramento Co. Arpt. Sys. Rev. Ref., Ser. 2018-C, 5.00%, due 7/1/2033 | |

| Sacramento Spec. Tax (Natomas Meadows Comm. Facs. Dist. Number 2007-01), Ser. 2017, 5.00%, due 9/1/2047 | |

| San Jose Multi-Family Hsg. Rev. (Fallen Leaves Apts. Proj.), Ser. 2002-J1, (AMBAC Insured), 4.95%, due 12/1/2022 | |

| San Mateo Foster City Sch. Dist. G.O. (Election 2015), Ser. 2016-A, 4.00%, due 8/1/2029 Pre-Refunded 8/1/2025 | |

| Santa Maria Bonita Sch. Dist. Cert. of Participation (New Sch. Construction Proj.) | |

| Ser. 2013, (BAM Insured), 3.25%, due 6/1/2025 | |

| Ser. 2013, (BAM Insured), 3.50%, due 6/1/2026 | |

| Ser. 2013, (BAM Insured), 3.50%, due 6/1/2027 | |

| Ser. 2013, (BAM Insured), 3.50%, due 6/1/2028 | |

See Notes to Financial Statements

Schedule of Investments California Municipal Fund Inc.^ (cont’d)

| |

|

| Santa Monica-Malibu Unified Sch. Dist. Ref. G.O., Ser. 2013, 3.00%, due 8/1/2027 Pre-Refunded 8/1/2023 | |

| Sulphur Springs Union Sch. Dist. Cert. of Participation Conv. Cap. Appreciation Bonds | |

| Ser. 2010, (AGM Insured), 6.50%, due 12/1/2037 | |

| Ser. 2010, (AGM Insured), 6.50%, due 12/1/2037 Pre-Refunded 12/1/2025 | |

| Ser. 2010, (AGM Insured), 6.50%, due 12/1/2037 | |

| Sweetwater Union High Sch. Dist. Pub. Fin. Au. Rev., Ser. 2013, (BAM Insured), 5.00%, due 9/1/2025 | |

| Tobacco Securitization Au. Southern California Tobacco Settlement Rev. Ref. (San Diego Co. Asset Securitization Corp.), Ser. 2019-A, Class 1, 5.00%, due 6/1/2048 | |

| Univ. of California Ref. Rev., Ser. 2013-AL-4, 1.20%, due 5/15/2048 | |

| Victor Valley Comm. College Dist. G.O. Cap. Appreciation (Election 2008), Ser. 2009-C, 6.88%, due 8/1/2037 | |

| William S. Hart Union High Sch. Dist. G.O. Cap. Appreciation (Election 2001), Ser. 2005-B, (AGM Insured), 0.00%, due 9/1/2026 | |

| Wiseburn Sch. Dist. G.O. Cap. Appreciation (Election 2010), Ser. 2011-B, (AGM Insured), 0.00%, due 8/1/2036 | |

| | |

|

| Antonio B. Won Pat Int'l Arpt. Au. Rev. Ref., Ser. 2023-A, 5.38%, due 10/1/2040 | |

| Guam Gov't Bus. Privilege Tax Rev. Ref., Ser. 2021-F, 4.00%, due 1/1/2036 | |

| Guam Gov't Hotel Occupancy Tax Rev. Ref., Ser. 2021-A, 5.00%, due 11/1/2040 | |

| Guam Pwr. Au. Rev., Ser. 2022-A, 5.00%, due 10/1/2037 | |

| | |

|

| Chicago G.O. Ref., Ser. 2003-B, 5.00%, due 1/1/2023 | |

|

| Goddard Kansas Sales Tax Spec. Oblig. Rev. (Olympic Park Star Bond Proj.) | |

| Ser. 2019, 3.60%, due 6/1/2030 | |

| Ser. 2021, 3.50%, due 6/1/2034 | |

| | |

|

| Louisiana St. Pub. Facs. Au. Rev. (Southwest Louisiana Charter Academy Foundation Proj.), Ser. 2013-A, 7.63%, due 12/15/2028 | |

|

| New Jersey St. Econ. Dev. Au. Rev. (Continental Airlines, Inc., Proj.), Ser. 1999, 5.13%, due 9/15/2023 | |

|

| Build NYC Res. Corp. Rev., Ser. 2014, 5.25%, due 11/1/2034 | |

|

| Buckeye Tobacco Settlement Fin. Au. Asset-Backed Sr. Ref. Rev., Ser. 2020-B-2, 5.00%, due 6/1/2055 | |

| So. Ohio Port Exempt Fac. Au. Rev., (PureCycle Proj.), Ser. 2020-A, 7.00%, due 12/1/2042 | |

| | |

|

| Puerto Rico Commonwealth G.O. (Restructured), Ser. 2021-A-1, 4.00%, due 7/1/2046 | |

| Puerto Rico Ind. Tourist Ed. Med. & Env. Ctrl. Fac. Rev. (Hosp. Auxilio Mutuo Oblig. Group Proj.), Ser. 2021, 5.00%, due 7/1/2027 | |

| Puerto Rico Sales Tax Fin. Corp. Sales Tax Rev., Ser. 2018-A-1, 5.00%, due 7/1/2058 | |

| | |

See Notes to Financial Statements

Schedule of Investments California Municipal Fund Inc.^ (cont’d)

| |

|

| South Carolina Jobs Econ. Dev. Au. Econ. Dev. Rev. (River Park Sr. Living Proj.), Ser. 2017-A, 7.75%, due 10/1/2057 | |

| South Carolina St. Jobs Econ. Dev. Au. Solid Waste Disp. Rev. (AMT-Green Bond-Last Step Recycling LLC Proj.), Ser. 2021-A, 6.50%, due 6/1/2051 | |

| | |

|

| Mission Econ. Dev. Corp. Wtr. Supply Rev. (Green Bond-Env. Wtr. Minerals Proj.), Ser. 2015, 7.75%, due 1/1/2045 | |

| New Hope Cultural Ed. Facs. Fin. Corp. Sr. Living Rev. (Bridgemoor Plano Proj.), Ser. 2018-A, 7.25%, due 12/1/2053 | |

| | |

|

| Matching Fund Spec. Purp. Securitization Corp. Ref., Ser. 2022-A, 5.00%, due 10/1/2039 | |

|

| Pub. Fin. Au. Retirement Fac. Rev. Ref. (Friends Homes), Ser. 2019, 5.00%, due 9/1/2054 | |

Total Investments 177.7% (Cost $124,974,124) | |

Other Assets Less Liabilities 1.1% | |

Liquidation Preference of Variable Rate Municipal Term Preferred Shares (78.8%) | |

Net Assets Applicable to Common Stockholders 100.0% | |

| Securities were purchased under Rule 144A of the Securities Act of 1933, as amended, or are otherwise restricted and, unless registered under the Securities Act of 1933 or exempted from registration, may only be sold to qualified institutional investors or may have other restrictions on resale. At October 31, 2022, these securities amounted to $15,572,994, which represents 24.0% of net assets applicable to common stockholders of the Fund. |

| |

| Variable rate demand obligation where the stated interest rate is not based on a published reference rate and spread. Rather, the interest rate generally resets daily or weekly and is determined by the remarketing agent. The rate shown represents the rate in effect at October 31, 2022. |

| Currently a zero coupon security; will convert to 7.30% on August 1, 2026. |

| When-issued security. Total value of all such securities at October 31, 2022 amounted to $465,426, which represents 0.7% of net assets applicable to common stockholders of the Fund. |

The following is a summary, categorized by Level (see Note A of the Notes to Financial Statements), of inputs used to value the Fund’s investments as of October 31, 2022:

| The Schedule of Investments provides information on the state/territory categorization. |

^

A balance indicated with a "—", reflects either a zero balance or an amount that rounds to less than 1.

See Notes to Financial Statements

Schedule of Investments Municipal Fund Inc.^

October 31, 2022

| |

|

|

| Columbia IDB PCR Ref. (Alabama Pwr. Co. Proj.), Ser. 2014-A, 1.72%, due 12/1/2037 | |

| Sumter Co. Ind. Dev. Au.(Green Bond-Enviva, Inc.), Ser. 2022, 6.00%, due 7/15/2052 Putable 7/15/2032 | |

| | |

|

| American Samoa Econ. Dev. Au. Gen. Rev. Ref., Ser. 2015-A, 6.25%, due 9/1/2029 | |

|

| Maricopa Co. Ind. Dev. Au. Ed. Ref. Rev. (Paradise Sch. Proj. Paragon Management, Inc.), Ser. 2016, 5.00%, due 7/1/2036 | |

| Navajo Nation Ref. Rev., Ser. 2015-A, 5.00%, due 12/1/2025 | |

| Phoenix Ind. Dev. Au. Ed. Rev. (Great Hearts Academies Proj.), Ser. 2014, 3.75%, due 7/1/2024 | |

| Phoenix-Mesa Gateway Arpt. Au. Spec. Fac. Rev. (Mesa Proj.), Ser. 2012, 5.00%, due 7/1/2024 | |

| | |

|

| California Hlth. Facs. Fin. Au. Rev. (Children's Hosp. Los Angeles), Ser. 2012-A, 5.00%, due 11/15/2026 Pre-Refunded 11/15/2022 | |

| California Infrastructure & Econ. Dev. Bank St. Sch. Fund Rev. (King City Joint Union High Sch.), Ser. 2010, 5.13%, due 8/15/2024 | |

| California Muni. Fin. Au. Charter Sch. Lease Rev. (Sycamore Academy Proj.) | |

| Ser. 2014, 5.00%, due 7/1/2024 | |

| Ser. 2014, 5.13%, due 7/1/2029 | |

| California Muni. Fin. Au. Charter Sch. Lease Rev. (Vista Charter Middle Sch. Proj.) | |

| Ser. 2014, 5.00%, due 7/1/2024 | |

| Ser. 2014, 5.13%, due 7/1/2029 | |

| California Muni. Fin. Au. Charter Sch. Rev. (Palmdale Aerospace Academy Proj.), Ser. 2016, 5.00%, due 7/1/2031 | |

| California Muni. Fin. Au. Rev. (Baptist Univ.), Ser. 2015-A, 5.00%, due 11/1/2030 | |

| California Muni. Fin. Au. Rev. (Touro College & Univ. Sys. Obligated Group), Ser. 2014-A, 4.00%, due 1/1/2026 Pre-Refunded 7/1/2024 | |

| California Muni. Fin. Au. Std. Hsg. Rev. (CHF-Davis I, LLC-West Village Std. Hsg. Proj.), Ser. 2018, 5.00%, due 5/15/2051 | |

| California Muni. Fin. Au. Std. Hsg. Rev. (CHF-Davis II, LLC, Green Bond-Orchard Park Std. Hsg. Proj.), Ser. 2021, (BAM Insured), 3.00%, due 5/15/2054 | |

| California Sch. Fac. Fin. Au. Rev. (Alliance College - Ready Pub. Sch. Proj.), Ser. 2015-A, 5.00%, due 7/1/2030 | |

| California St. Dept. of Veterans Affairs Home Purchase Ref. Rev. | |

| Ser. 2016-A, 2.90%, due 6/1/2028 | |

| Ser. 2016-A, 2.95%, due 12/1/2028 | |

| California St. G.O., Ser. 2022, 3.00%, due 4/1/2052 | |

| California St. Poll. Ctrl. Fin. Au. Solid Waste Disp. Rev. (Aemerage Redak Svcs. So. California LLC Proj.), Ser. 2016, 7.00%, due 12/1/2027 | |

| California St. Poll. Ctrl. Fin. Au. Solid Waste Disp. Rev. (Calplant I Green Bond Proj.), Ser. 2019, 7.50%, due 12/1/2039 | |

| California St. Poll. Ctrl. Fin. Au. Solid Waste Disp. Rev. (Green Bond-Rialto Bioenergy Fac. LLC, Proj.), Ser. 2019, 7.50%, due 12/1/2040 | |

| California St. Poll. Ctrl. Fin. Au. Wtr. Furnishing Rev., Ser. 2012, 5.00%, due 7/1/2027 | |

| Deutsche Bank Spears/Lifers Trust Rev., Ser. 2020, (LOC: Deutsche Bank AG), 2.64%, due 12/1/2052 | |

| Golden St. Tobacco Securitization Corp. Tobacco Settlement Rev. Ref., Ser. 2021-B-2, 0.00%, due 6/1/2066 | |

See Notes to Financial Statements

Schedule of Investments Municipal Fund Inc.^ (cont’d)

| |

|

| Imperial Comm. College Dist. G.O. Cap. Appreciation (Election 2010), Ser. 2011-A, (AGM Insured), 6.75%, due 8/1/2040 Pre-Refunded 8/1/2025 | |

| North Orange Co. Comm. College Dist. G.O., Ser. 2022-C, 4.00%, due 8/1/2047 | |

| Norwalk-La Mirada Unified Sch. Dist. G.O. Cap. Appreciation, Ser. 2005-B, (AGM Insured), 0.00%, due 8/1/2024 | |

| Norwalk-La Mirada Unified Sch. Dist. G.O. Cap. Appreciation (Election 2002), Ser. 2009-E, (Assured Guaranty Insured), 5.50%, due 8/1/2029 | |

| Redondo Beach Unified Sch. Dist. G.O., Ser. 2009, 6.38%, due 8/1/2034 Pre-Refunded 8/1/2026 | |

| Sacramento City Fin. Au. Ref. Rev. (Master Lease Prog. Facs.), Ser. 2006-E, (AMBAC Insured), 5.25%, due 12/1/2026 | |

| San Bernardino Comm. College Dist. G.O. Cap. Appreciation (Election), Ser. 2009-B, 6.38%, due 8/1/2034 Pre-Refunded 8/1/2024 | |

| San Mateo Foster City Sch. Dist. G.O. Cap. Appreciation (Election 2008), Ser. 2010-A, 0.00%, due 8/1/2032 | |

| Sweetwater Union High Sch. Dist. Pub. Fin. Au. Rev., Ser. 2013, (BAM Insured), 5.00%, due 9/1/2025 | |

| Victor Valley Comm. College Dist. G.O. Cap. Appreciation (Election 2008), Ser. 2009-C, 6.88%, due 8/1/2037 | |

| Victor Valley Joint Union High Sch. Dist. G.O. Cap. Appreciation Bonds, Ser. 2009, (Assured Guaranty Insured), 0.00%, due 8/1/2026 | |

| Wiseburn Sch. Dist. G.O. Cap. Appreciation (Election 2010), Ser. 2011-B, (AGM Insured), 0.00%, due 8/1/2036 | |

| | |

|

| Colorado Ed. & Cultural Facs. Au. Rev. (Charter Sch.- Atlas Preparatory Sch. Proj.) | |

| Ser. 2015, 4.50%, due 4/1/2025 | |

| Ser. 2015, 5.13%, due 4/1/2035 Pre-Refunded 4/1/2025 | |

| Ser. 2015, 5.25%, due 4/1/2045 Pre-Refunded 4/1/2025 | |

| Colorado Ed. & Cultural Facs. Au. Rev. Ref., Ser. 2014, 4.50%, due 11/1/2029 | |

| Plaza Metro. Dist. Number 1 Tax Allocation Rev., Ser. 2013, 4.00%, due 12/1/2023 | |

| Villages at Castle Rock Co. Metro. Dist. Number 6 (Cabs - Cobblestone Ranch Proj.), Ser. 2007-2, 0.00%, due 12/1/2037 | |

| | |

|

| Hamden G.O., Ser. 2013, (AGM Insured), 3.13%, due 8/15/2025 | |

District of Columbia 0.3% |

| Dist. of Columbia Std. Dorm. Rev. (Provident Group-Howard Prop.), Ser. 2013, 5.00%, due 10/1/2045 | |

|

| Cap. Trust Agcy. Sr. Living Rev. (H-Bay Ministries, Inc. Superior Residences-Third Tier), Ser. 2018-C, 7.50%, due 7/1/2053 | |

| Cap. Trust Agcy. Sr. Living Rev. (Wonderful Foundations Sch. Proj.), Ser. 2020-A-1, 5.00%, due 1/1/2055 | |

| CityPlace Comm. Dev. Dist. Spec. Assessment Ref. Rev., Ser. 2012, 5.00%, due 5/1/2026 | |

| Florida Dev. Fin. Corp. Ed. Facs. Rev. (Renaissance Charter Sch., Inc.) | |

| Ser. 2013-A, 6.75%, due 12/15/2027 Pre-Refunded 6/15/2023 | |

| Ser. 2014-A, 5.75%, due 6/15/2029 | |

| Florida Dev. Fin. Corp. Ed. Facs. Rev. Ref. (Pepin Academies, Inc.), Ser. 2016-A, 5.00%, due 7/1/2036 | |

| Hillsborough Co. Ind. Dev. Au. Hosp. Rev. (Tampa General Hosp. Proj.), Ser. 2020-A, 3.50%, due 8/1/2055 | |

| Village Comm. Dev. Dist. Number 11 Spec. Assessment Rev., Ser. 2014, 4.13%, due 5/1/2029 | |

See Notes to Financial Statements

Schedule of Investments Municipal Fund Inc.^ (cont’d)

| |

|

| Village Comm. Dev. Dist. Number 13 Spec. Assessment Rev., Ser. 2019, 3.70%, due 5/1/2050 | |

| | |

|

| DeKalb Co. Hsg. Au. Sr. Living Rev. Ref. (Baptist Retirement Comm. of Georgia Proj.), Ser. 2019-A, 5.13%, due 1/1/2049 | |

|

| A.B. Won Pat Int'l Arpt. Au. Rev. Ref., Ser. 2023-A, 5.38%, due 10/1/2043 | |

| Guam Pwr. Au. Rev., Ser. 2022-A, 5.00%, due 10/1/2035 | |

| | |

|

| Hawaii St. Dept. of Budget & Fin. Spec. Purp. Rev. (Hawaiian Elec. Co., Inc. - Subsidiary), Ser. 2019, 3.50%, due 10/1/2049 | |

|

| Berwyn G.O., Ser. 2013-A, 5.00%, due 12/1/2027 | |

| | |

| Ser. 2002-2002B, 5.13%, due 1/1/2027 | |

| Ser. 2002-B, 5.00%, due 1/1/2025 | |

| Ser. 2019-A, 5.00%, due 1/1/2044 | |

| | |

| Ser. 2005-D, 5.50%, due 1/1/2040 | |

| Ser. 2014-A, 5.00%, due 1/1/2027 | |

| Ser. 2017-A, 6.00%, due 1/1/2038 | |

| Cook Co. Sch. Dist. Number 83 G.O. (Mannheim) | |

| Ser. 2013-C, 5.45%, due 12/1/2030 | |

| Ser. 2013-C, 5.50%, due 12/1/2031 | |

| Illinois Fin. Au. Ref. Rev. (Presence Hlth. Network Obligated Group), Ser. 2016-C, 5.00%, due 2/15/2031 | |

| Illinois Fin. Au. Rev. Ref. (Northwestern Mem. Hlth. Care Obligated Group), Ser. 2017-A, 4.00%, due 7/15/2047 | |

| Illinois Sports Facs. Au. Cap. Appreciation Rev. (St. Tax Supported), Ser. 2001, (AMBAC Insured), 0.00%, due 6/15/2026 | |

| | |

| Ser. 2012, 4.00%, due 8/1/2025 | |

| Ser. 2013, 5.00%, due 7/1/2023 | |

| Ser. 2017-D, 5.00%, due 11/1/2028 | |

| Ser. 2021-A, 4.00%, due 3/1/2039 | |

| Ser. 2021-A, 4.00%, due 3/1/2040 | |

| Ser. 2021-A, 5.00%, due 3/1/2046 | |

| Illinois St. G.O. Ref., Ser. 2016, 5.00%, due 2/1/2024 | |

| So. Illinois Univ. Cert. of Participation (Cap. Imp. Proj.) | |

| Ser. 2014-A-1, (BAM Insured), 5.00%, due 2/15/2027 | |

| Ser. 2014-A-1, (BAM Insured), 5.00%, due 2/15/2028 | |

| Ser. 2014-A-1, (BAM Insured), 5.00%, due 2/15/2029 | |

| Univ. of Illinois (Hlth. Svc. Facs. Sys.) | |

| Ser. 2013, 5.00%, due 10/1/2027 | |

| Ser. 2013, 5.75%, due 10/1/2028 | |

| Upper Illinois River Valley Dev. Au. Rev. Ref. (Cambridge Lakes Learning Ctr.), Ser. 2017-A, 5.25%, due 12/1/2047 | |

| | |

See Notes to Financial Statements

Schedule of Investments Municipal Fund Inc.^ (cont’d)

| |

|

| Valparaiso Exempt Facs. Rev. (Pratt Paper LLC Proj.), Ser. 2013, 5.88%, due 1/1/2024 | |

|

| Iowa St. Higher Ed. Loan Au. Rev. (Des Moines Univ. Proj.), Ser. 2020, 5.00%, due 10/1/2028 | |

|

| Wyandotte Co. & Kansas City Kanuni Gov't. G.O. Temporary Notes, Ser. 2022-I, 1.25%, due 4/1/2023 | |

|

| Ashland City, Kentucky Med. Ctr. Ref. Rev. (Ashland Hosp. Corp. DBA Kings Daughter Med. Ctr.), Ser. 2019, (AGM Insured), 3.00%, due 2/1/2040 | |

|

| Louisiana Local Gov't Env. Facs. & Comm. Dev. Au. Rev. Ref. (Westside Habilitation Ctr. Proj.), Ser. 2017-A, 5.75%, due 2/1/2032 | |

| Louisiana St. Local Gov’t Env. Facs. & Comm. Dev. Au. Rev. (Lafourche Parish Gomesa Proj.), Ser. 2019, 3.95%, due 11/1/2043 | |

| Louisiana St. Pub. Facs. Au. Rev. (Southwest Louisiana Charter Academy Foundation Proj.), Ser. 2013-A, 7.63%, due 12/15/2028 | |

| St. John the Baptist Parish LA Rev. Ref. (Marathon Oil Corp. Proj.), Subser. 2017-A-1, 2.00%, due 6/1/2037 Putable 4/1/2023 | |

| | |

|

| Maine St. Fin. Au. (Green Bond-Go Lab Madison, LLC Proj.), Ser. 2021, 8.00%, due 12/1/2051 | |

|

| Baltimore Spec. Oblig. Ref. Rev. Sr. Lien (Harbor Point Proj.), Ser. 2022, 5.00%, due 6/1/2051 | |

|

| Massachusetts St. Dev. Fin. Agcy. Rev. (Milford Reg. Med. Ctr.) | |

| Ser. 2014-F, 5.00%, due 7/15/2024 | |

| Ser. 2014-F, 5.00%, due 7/15/2025 | |

| Ser. 2014-F, 5.00%, due 7/15/2026 | |

| Ser. 2014-F, 5.00%, due 7/15/2027 | |

| Ser. 2014-F, 5.00%, due 7/15/2028 | |

| Massachusetts St. Ed. Fin. Au. Rev., Ser. 2012-J, 4.70%, due 7/1/2026 | |

| | |

|

| | |

| Ser. 2021-A, 5.00%, due 4/1/2046 | |

| Ser. 2021-A, 5.00%, due 4/1/2050 | |

| Detroit Downtown Dev. Au. Tax Increment Rev. Ref. (Catalyst Dev. Proj.), Ser. 2018-A, (AGM Insured), 5.00%, due 7/1/2048 | |

| Michigan St. Bldg. Au. Rev. (Facilities Prog.), Ser. 2022-I, 5.00%, due 10/15/2047 | |

| Michigan St. Strategic Fund Ltd. Oblig. Rev. (Green Bond-Recycled Board Machine Proj.), Ser. 2021, 4.00%, due 10/1/2061 Putable 10/1/2026 | |

| Michigan St. Strategic Fund Ltd. Oblig. Rev. (Improvement Proj.), Ser. 2018, 5.00%, due 6/30/2048 | |

| Summit Academy Pub. Sch. Academy Ref. Rev., Ser. 2005, 6.38%, due 11/1/2035 | |

| | |

|

| St. Paul Hsg. & Redev. Au. Charter Sch. Lease Rev. (Metro Deaf Sch. Proj.), Ser. 2018-A, 5.00%, due 6/15/2038 | |

See Notes to Financial Statements

Schedule of Investments Municipal Fund Inc.^ (cont’d)

| |

|

| Mississippi Dev. Bank Spec. Oblig. (Jackson Co. Gomesa Proj.), Ser. 2021, 3.63%, due 11/1/2036 | |

|

| Director of the St. of Nevada Dept. of Bus. & Ind. Rev. (Somerset Academy) | |

| Ser. 2015-A, 4.00%, due 12/15/2025 | |

| Ser. 2015-A, 5.13%, due 12/15/2045 | |

| | |

|

| National Fin. Au. Rev. (Green Bond), Ser. 2020-B, 3.75%, due 7/1/2045 Putable 7/2/2040 | |

|

| New Jersey Econ. Dev. Au. Rev. (Sch. Facs. Construction), Ser. 2019-LLL, 5.00%, due 6/15/2028 | |

| New Jersey Econ. Dev. Au. Rev. (The Goethals Bridge Replacement Proj.) | |

| Ser. 2013, 5.25%, due 1/1/2025 | |

| Ser. 2013, 5.50%, due 1/1/2026 | |

| New Jersey Econ. Dev. Au. Rev. (United Methodist Homes of New Jersey Obligated Group) | |

| Ser. 2013, 3.50%, due 7/1/2024 Pre-Refunded 7/1/2023 | |

| Ser. 2013, 3.63%, due 7/1/2025 Pre-Refunded 7/1/2023 | |

| Ser. 2013, 3.75%, due 7/1/2026 Pre-Refunded 7/1/2023 | |

| Ser. 2013, 4.00%, due 7/1/2027 Pre-Refunded 7/1/2023 | |

| New Jersey Higher Ed. Assist. Au. Rev. (Std. Loan Rev.), Ser. 2012-1A, 4.38%, due 12/1/2026 | |

| New Jersey St. Econ. Dev. Au. Rev. (Continental Airlines, Inc., Proj.), Ser. 1999, 5.13%, due 9/15/2023 | |

| New Jersey St. Econ. Dev. Au. Sch. Rev. (Beloved Comm. Charter, Sch., Inc. Proj.) | |

| Ser. 2019-A, 5.00%, due 6/15/2049 | |

| Ser. 2019-A, 5.00%, due 6/15/2054 | |

| New Jersey St. Trans. Trust Fund Au., Ser. 2019-BB, 4.00%, due 6/15/2050 | |

| New Jersey St. Trans. Trust Fund Au. Trans. Sys. Rev. Ref. | |

| Ser. 2018-A, 5.00%, due 12/15/2036 | |

| Ser. 2018-A, 4.25%, due 12/15/2038 | |

| Ser. 2018-A, (BAM Insured), 4.00%, due 12/15/2037 | |

| | |

|

| Winrock Town Ctr. Tax Increment Dev. Dist. Number 1 (Sr. Lien), Ser. 2022, 4.25%, due 5/1/2040 | |

|

| Buffalo & Erie Co. Ind. Land Dev. Corp. Rev. Ref. (Charter Sch. for Applied Technologies Proj.), Ser. 2017-A, 5.00%, due 6/1/2035 | |

| Buffalo & Erie Co. Ind. Land Dev. Corp. Rev. Ref. (Orchard Park), Ser. 2015, 5.00%, due 11/15/2029 | |

| Build NYC Res. Corp. Ref. Rev. (New York Law Sch. Proj.), Ser. 2016, 4.00%, due 7/1/2045 | |

| Build NYC Res. Corp. Rev. | |

| Ser. 2014, 5.00%, due 11/1/2024 | |

| Ser. 2014, 5.25%, due 11/1/2029 | |

| Ser. 2014, 5.50%, due 11/1/2044 | |

| Build NYC Res. Corp. Rev. (Metro. Lighthouse Charter Sch. Proj.), Ser. 2017-A, 5.00%, due 6/1/2047 | |

| Build NYC Res. Corp. Rev. (New Dawn Charter Sch. Proj.), Ser. 2019, 5.75%, due 2/1/2049 | |

| Build NYC Res. Corp. Rev. (South Bronx Charter Sch. for Int'l Cultures and the Arts) | |

| Ser. 2013-A, 3.88%, due 4/15/2023 | |

| Ser. 2013-A, 5.00%, due 4/15/2043 | |

| Build NYC Res. Corp. Solid Waste Disp. Ref. Rev. (Pratt Paper, Inc. Proj.), Ser. 2014, 4.50%, due 1/1/2025 | |

See Notes to Financial Statements

Schedule of Investments Municipal Fund Inc.^ (cont’d)

| |

|

| Hempstead Town Local Dev. Corp. Rev. (Molloy College Proj.) | |

| Ser. 2014, 5.00%, due 7/1/2023 | |

| Ser. 2014, 5.00%, due 7/1/2024 | |

| Ser. 2018, 5.00%, due 7/1/2030 | |

| Jefferson Co. IDA Solid Waste Disp. Rev. (Green Bond-Reenergy Black River LLC Proj.), Ser. 2014, 5.25%, due 1/1/2024 | |

| Metro. Trans. Au. Rev. (Green Bond) | |

| Ser. 2020-D-3, 4.00%, due 11/15/2049 | |

| Ser. 2020-D-3, 4.00%, due 11/15/2050 | |

| New York City IDA Rev. (Yankee Stadium Proj.), Ser. 2020, 3.00%, due 3/1/2049 | |

| New York Liberty Dev. Corp. Ref. Rev. (3 World Trade Ctr. Proj.), Ser. 2014-2, 5.38%, due 11/15/2040 | |

| New York St. Dorm. Au. Rev. Non St. Supported Debt (Univ. Facs.), Ser. 2013-A, 5.00%, due 7/1/2028 Pre-Refunded 7/1/2023 | |

| New York St. Dorm. Au. Rev. Ref. Non St. Supported Debt (Montefiore Oblig. Group), Ser. 2018-A, 5.00%, due 8/1/2035 | |

| New York St. Dorm. Au. Rev. St. Supported Debt (New Sch.), Ser. 2022-A, 4.00%, due 7/1/2052 | |

| New York St. Mtge. Agcy. Homeowner Mtge. Ref. Rev., Ser. 2014-189, 3.45%, due 4/1/2027 | |

| New York St. Trans. Dev. Corp. Fac. Rev. (Empire St. Thruway Svc. Areas Proj.), Ser. 2021, 4.00%, due 4/30/2053 | |

| New York St. Trans. Dev. Corp. Spec. Fac. Rev. (Delta Airlines, Inc.-LaGuardia Arpt. Term. C&D Redev.), Ser. 2018, 5.00%, due 1/1/2033 | |

| New York St. Trans. Dev. Corp. Spec. Fac. Rev. Ref. (JFK Int'l Arpt. Term. 4 Proj.), Ser. 2022, 5.00%, due 12/1/2039 | |

| Suffolk Co. Judicial Facs. Agcy. Lease Rev. (H. Lee Dennison Bldg.), Ser. 2013, 4.25%, due 11/1/2026 | |

| Utility Debt Securitization Au. Rev., Ser. 2013-TE, 5.00%, due 12/15/2028 | |

| Westchester Co. Local Dev. Corp. Rev. (Purchase Sr. Learning Comm., Inc. Proj.), Ser. 2021-A, 5.00%, due 7/1/2056 | |

| Westchester Co. Local Dev. Corp. Rev. Ref. (Wartburg Sr. Hsg. Proj.), Ser. 2015-A, 5.00%, due 6/1/2030 | |

| | |

|

| North Carolina HFA Homeownership Ref. Rev., Ser. 2020-45, (GNMA/FNMA/FHLMC Insured), 2.20%, due 7/1/2040 | |

| North Carolina Med. Care Commission Retirement Facs. Rev. | |

| Ser. 2013, 5.13%, due 7/1/2023 | |

| Ser. 2020-A, 4.00%, due 9/1/2050 | |

| North Carolina Med. Care Commission Retirement Facs. Rev. (Twin Lakes Comm.), Ser. 2019-A, 5.00%, due 1/1/2049 | |

| | |

|

| Buckeye Tobacco Settlement Fin. Au. Asset-Backed Sr. Ref. Rev., Ser. 2020-B-2, 5.00%, due 6/1/2055 | |

| Jefferson Co. Port Econ. Dev. Au. Rev. (JSW Steel USA, Ohio, Inc. Proj.), Ser. 2021, 3.50%, due 12/1/2051 | |

| Ohio St. Air Quality Dev. Au. Exempt Facs. Rev. (AMG Vanadium LLC), Ser. 2019-D, 5.00%, due 7/1/2049 | |

| Ohio St. Air Quality Dev. Au. Rev. (Ohio Valley Elec. Corp. Proj.), Ser. 2014-B, 2.60%, due 6/1/2041 Putable 10/1/2029 | |

| Port Au. of Greater Cincinnati Dev. Rev. (Convention Ctr. Hotel Acquisition and Demolition Proj.), Ser. 2020-A, 3.00%, due 5/1/2023 | |

| | |

See Notes to Financial Statements

Schedule of Investments Municipal Fund Inc.^ (cont’d)

| |

|

| Oklahoma St. Dev. Fin. Au. Hlth. Sys. Rev. (OU Medicine Proj.), Ser. 2018-B, 5.00%, due 8/15/2033 | |

| Tulsa Arpt. Imp. Trust Ref. Rev. | |

| Ser. 2015-A, (BAM Insured), 5.00%, due 6/1/2024 | |

| Ser. 2015-A, (BAM Insured), 5.00%, due 6/1/2025 Pre-Refunded 6/1/2024 | |

| | |

|

| Oregon St. Hsg. & Comm. Svc. Dept. Multi-Family Rev., Ser. 2012-B, (FHA/GNMA/FNMA/FHLMC Insured), 3.50%, due 7/1/2027 | |

|

| Lancaster Co. Hosp. Au. Ref. Rev. (Hlth. Centre-Landis Homes Retirement Comm. Proj.), Ser. 2015-A, 4.25%, due 7/1/2030 | |

| Lancaster Ind. Dev. Au. Rev. (Garden Spot Village Proj.), Ser. 2013, 5.38%, due 5/1/2028 Pre-Refunded 5/1/2023 | |

| Leigh Co. Ind. Dev. Au. Poll. Ctrl. Rev. Ref., Ser. 2016-A, 3.00%, due 9/1/2029 | |

| Pennsylvania Econ. Dev. Fin. Au. Exempt Facs. Rev. Ref. (Amtrak Proj.), Ser. 2012-A, 5.00%, due 11/1/2024 | |

| Pennsylvania Econ. Dev. Fin. Au. Rev. Ref. (Tapestry Moon Sr. Hsg. Proj.), Ser. 2018-A, 6.75%, due 12/1/2053 | |

| | |

|

| Puerto Rico Commonwealth G.O. (Restructured), Ser. 2021-A-1, 4.00%, due 7/1/2046 | |

| Puerto Rico Sales Tax Fin. Corp. Sales Tax Rev., Ser. 2018-A-1, 5.00%, due 7/1/2058 | |

| | |

|

| Rhode Island St. Hsg. & Mtge. Fin. Corp. Rev. (Homeownership Opportunity), Ser. 2020-73-A, 2.30%, due 10/1/2040 | |

|

| South Carolina Jobs Econ. Dev. Au. Econ. Dev. Rev. (River Park Sr. Living Proj.), Ser. 2017-A, 7.75%, due 10/1/2057 | |

| South Carolina Jobs Econ. Dev. Au. Solid Waste Disp. Rev. (Green Bond-Jasper Pellets LLC, Proj.), Ser. 2018-A, 7.00%, due 11/1/2038 | |

| South Carolina Jobs Econ. Dev. Au. Solid Waste Disp. Rev. (RePower South Berkeley LLC Proj.), Ser. 2017, 6.25%, due 2/1/2045 | |

| | |

|

| Tennessee St. Energy Acquisition Corp. Gas Rev. (Goldman Sachs Group, Inc.), Ser. 2006-A, 5.25%, due 9/1/2023 | |

|

| Anson Ed. Facs. Corp. Ed. Rev. (Arlington Classics Academy), Ser. 2016-A, 5.00%, due 8/15/2045 | |

| Arlington Higher Ed. Fin. Corp. Rev. (Universal Academy) | |

| Ser. 2014-A, 5.88%, due 3/1/2024 | |

| Ser. 2014-A, 6.63%, due 3/1/2029 | |

| Austin Comm. College Dist. Pub. Fac. Corp. Lease Rev., Ser. 2018-C, 4.00%, due 8/1/2042 | |

| Clifton Higher Ed. Fin. Corp. Rev. (Uplift Ed.), Ser. 2013-A, 3.10%, due 12/1/2022 | |

| Dallas Co. Flood Ctrl. Dist. Number 1 Ref. G.O., Ser. 2015, 5.00%, due 4/1/2028 | |

| Fort Bend Co. Ind. Dev. Corp. Rev. (NRG Energy, Inc.), Ser. 2012-B, 4.75%, due 11/1/2042 | |

See Notes to Financial Statements

Schedule of Investments Municipal Fund Inc.^ (cont’d)

| |

|

| Hale Ctr. Ed. Fac. Corp. Rev. Ref. (Wayland Baptist Univ. Proj.) | |

| Ser. 2022, 5.00%, due 3/1/2033 | |

| Ser. 2022, 5.00%, due 3/1/2034 | |

| Ser. 2022, 4.00%, due 3/1/2035 | |

| Harris Co. Cultural Ed. Facs. Fin. Corp. Rev. (Brazos Presbyterian Homes, Inc. Proj.), Ser. 2013-B, 5.75%, due 1/1/2028 | |

| New Hope Cultural Ed. Facs. Fin. Corp. Rev. (Beta Academy) | |

| Ser. 2019, 5.00%, due 8/15/2039 | |

| Ser. 2019, 5.00%, due 8/15/2049 | |

| New Hope Cultural Ed. Facs. Fin. Corp. Sr. Living Rev. (Bridgemoor Plano Proj.), Ser. 2018-A, 7.25%, due 12/1/2053 | |

| New Hope Cultural Ed. Facs. Fin. Corp. Sr. Living Rev. (Cardinal Bay, Inc. Village On The Park Carriage), Ser. 2016-C, 5.50%, due 7/1/2046 | |

| Parkway Utils. Dist. Wtr. & Swr. Sys. Rev. | |

| Ser. 2022, (AGM Insured), 3.00%, due 3/1/2033 | |

| Ser. 2022, (AGM Insured), 3.00%, due 3/1/2034 | |

| Ser. 2022, (AGM Insured), 3.00%, due 3/1/2035 | |

| Texas Private Activity Bond Surface Trans. Corp. Sr. Lien Rev. Ref. (North Tarrant Express Managed Lanes Proj.), Ser. 2019-A, 4.00%, due 12/31/2039 | |

| Texas St. Private Activity Bond Surface Trans. Corp. Rev. (Segment 3C Proj.), Ser. 2019, 5.00%, due 6/30/2058 | |

| | |

|

| Salt Lake City Arpt. Rev. | |

| Ser. 2017-A, 5.00%, due 7/1/2042 | |

| Ser. 2017-A, 5.00%, due 7/1/2047 | |

| Ser. 2018-A, 5.00%, due 7/1/2043 | |

| Salt Lake Co. Hosp. Rev. (IHC Hlth. Svc., Inc.), Ser. 2001, (AMBAC Insured), 5.40%, due 2/15/2028 | |

| | |

|

| Vermont Econ. Dev. Au. Solid Waste Disp. Rev. (Casella Waste Sys., Inc.), Ser. 2022-A-1, 5.00%, due 6/1/2052 Putable 6/1/2027 | |

| Vermont Std. Assist. Corp. Ed. Loan Rev. | |

| Ser. 2014-A, 5.00%, due 6/15/2024 | |

| Ser. 2015-A, 4.13%, due 6/15/2027 | |

| | |

|

| Matching Fund Spec. Purp. Securitization Corp. Ref., Ser. 2022-A, 5.00%, due 10/1/2039 | |

|

| Fairfax Co. Econ. Dev. Au. Residential Care Fac. Rev. (Vinson Hall LLC), Ser. 2013-A, 4.00%, due 12/1/2022 | |

| Virginia St. Small Bus. Fin. Au. Rev. Ref. (Sr. Lien I-495, Hot Lanes Proj.), Ser. 2022, 5.00%, due 12/31/2047 | |

| | |

|

| Vancouver Downtown Redev. Au. Rev. (Conference Ctr. Proj.), Ser. 2013, 4.00%, due 1/1/2028 | |

| Washington St. Econ. Dev. Fin. Au. Env. Facs. Rev. (Green Bond), Ser. 2020-A, 5.63%, due 12/1/2040 | |

| Washington St. Hlth. Care Fac. Au. Rev. Ref. (Virginia Mason Med. Ctr.), Ser. 2017, 5.00%, due 8/15/2026 | |

See Notes to Financial Statements

Schedule of Investments Municipal Fund Inc.^ (cont’d)

| |

|

| Washington St. Hsg. Fin. Commission, Ser. 2021-A-1, 3.50%, due 12/20/2035 | |

| | |

|

| Pub. Fin. Au. Arpt. Fac. Rev. Ref. (Trips Oblig. Group), Ser. 2012-B, 5.00%, due 7/1/2042 | |

| Pub. Fin. Au. Ed. Rev. (Pine Lake Preparatory, Inc.), Ser. 2015, 4.95%, due 3/1/2030 | |

| Pub. Fin. Au. Ed. Rev. (Resh Triangle High Sch. Proj.), Ser. 2015-A, 5.38%, due 7/1/2035 | |

| Pub. Fin. Au. Rev. Ref. (Roseman Univ. Hlth. Sciences Proj.), Ser. 2015, 5.00%, due 4/1/2025 | |

| | |

|

| JPMorgan Chase Putters/Drivers Trust Var. Sts. Rev. (Putters), (LOC: JP Morgan Chase Bank N.A.), Ser. 2019, 2.42%, due 3/20/2024 | |

Total Investments 174.8% (Cost $395,855,341) | |

Other Assets Less Liabilities 4.8% | |

Liquidation Preference of Variable Rate Municipal Term Preferred Shares (79.6%) | |

Net Assets Applicable to Common Stockholders 100.0% | |

| Variable rate demand obligation where the stated interest rate is not based on a published reference rate and spread. Rather, the interest rate generally resets daily or weekly and is determined by the remarketing agent. The rate shown represents the rate in effect at October 31, 2022. |

| Securities were purchased under Rule 144A of the Securities Act of 1933, as amended, or are otherwise restricted and, unless registered under the Securities Act of 1933 or exempted from registration, may only be sold to qualified institutional investors or may have other restrictions on resale. At October 31, 2022, these securities amounted to $53,861,694, which represents 25.9% of net assets applicable to common stockholders of the Fund. |

| |

| Currently a zero coupon security; will convert to 6.13% on August 1, 2023. |

| Currently a zero coupon security; will convert to 7.30% on August 1, 2026. |

| When-issued security. Total value of all such securities at October 31, 2022 amounted to $218,238, which represents 0.1% of net assets applicable to common stockholders of the Fund. |

| Value determined using significant unobservable inputs. |

| Security fair valued as of October 31, 2022 in accordance with procedures approved by the valuation designee. Total value of all such securities at October 31, 2022 amounted to $140,000, which represents 0.1% of net assets applicable to common stockholders of the Fund. |

| Represents less than 0.05% of net assets applicable to common stockholders of the Fund. |

See Notes to Financial Statements

Schedule of Investments Municipal Fund Inc.^ (cont’d)

The following is a summary, categorized by Level (see Note A of the Notes to Financial Statements), of inputs used to value the Fund’s investments as of October 31, 2022:

| The Schedule of Investments provides a categorization by state/territory. |

| The following is a reconciliation between the beginning and ending balances of investments in which unobservable inputs (Level 3) were used in determining value: |

| Beginning

balance as

of 11/1/2021 | Accrued

discounts/

(premiums) | | Change

in unrealized

appreciation/

(depreciation) | | | | | | Net change in

unrealized

appreciation/

(depreciation)

from

investments

still held as of

10/31/2022 |

Investments in

Securities: | | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

(1) Quantitative Information about Level 3 Fair Value Measurements: |

| | | | | | Impact to

valuation

from

increase

in input(b) |

| | | | | | |

(a) The weighted averages disclosed in the table above were weighted by relative fair value. |

(b) Represents the expected directional change in the fair value of the Level 3 investments that would result from an increase or decrease in the corresponding input. Significant changes in these inputs could result in significantly higher or lower fair value measurements. |

^

A balance indicated with a "—", reflects either a zero balance or an amount that rounds to less than 1.

See Notes to Financial Statements

Schedule of Investments New York Municipal Fund Inc.^

October 31, 2022

| |

|

|

| American Samoa Econ. Dev. Au. Gen. Rev. Ref., Ser. 2015-A, 6.25%, due 9/1/2029 | |

|

| California St. Poll. Ctrl. Fin. Au. Solid Waste Disp. Rev. (Aemerage Redak Svcs. So. California LLC Proj.), Ser. 2016, 7.00%, due 12/1/2027 | |

| California St. Poll. Ctrl. Fin. Au. Solid Waste Disp. Rev. (Green Bond-Rialto Bioenergy Fac. LLC, Proj.), Ser. 2019, 7.50%, due 12/1/2040 | |

| Corona-Norca Unified Sch. Dist. G.O. Cap. Appreciation (Election 2006), Ser. 2009-C, (AGM Insured), 0.00%, due 8/1/2024 | |

| | |

|

| A.B. Won Pat Int'l Arpt. Au. Rev. Ref., Ser. 2023-A, 5.38%, due 10/1/2043 | |

| Guam Gov't Bus. Privilege Tax Rev. Ref., Ser. 2021-F, 4.00%, due 1/1/2036 | |

| Guam Gov't Hotel Occupancy Tax Rev., Ser. 2021-A, 5.00%, due 11/1/2035 | |

| Guam Pwr. Au. Rev., Ser. 2022-A, 5.00%, due 10/1/2036 | |

| | |

|

| Chicago G.O. Ref., Ser. 2003-B, 5.00%, due 1/1/2023 | |

|

| Goddard Kansas Sales Tax Spec. Oblig. Rev. (Olympic Park Star Bond Proj.) | |

| Ser. 2019, 3.60%, due 6/1/2030 | |

| Ser. 2021, 3.50%, due 6/1/2034 | |

| | |

|

| Louisiana St. Pub. Facs. Au. Rev. (Southwest Louisiana Charter Academy Foundation Proj.), Ser. 2013-A, 7.63%, due 12/15/2028 | |

|

| Albany Cap. Res. Corp. Ref. Rev. (Albany College of Pharmacy & Hlth. Sciences) | |

| Ser. 2014-A, 5.00%, due 12/1/2027 | |

| Ser. 2014-A, 5.00%, due 12/1/2028 | |

| Ser. 2014-A, 5.00%, due 12/1/2029 | |

| Broome Co. Local Dev. Corp. Rev. (Good Shepherd Village at Endwell, Inc. Proj.), Ser. 2021, 4.00%, due 1/1/2047 | |

| Buffalo & Erie Co. Ind. Land Dev. Corp. Rev. (Tapestry Charter Sch. Proj.), Ser. 2017-A, 5.00%, due 8/1/2047 | |

| Buffalo & Erie Co. Ind. Land Dev. Corp. Rev. Ref. (Charter Sch. for Applied Technologies Proj.), Ser. 2017-A, 5.00%, due 6/1/2035 | |

| Buffalo & Erie Co. Ind. Land Dev. Corp. Rev. Ref. (Orchard Park) | |

| Ser. 2015, 5.00%, due 11/15/2027 | |

| Ser. 2015, 5.00%, due 11/15/2028 | |

| Build NYC Res. Corp. Ref. Rev. (City Univ. - Queens College) | |

| Ser. 2014-A, 5.00%, due 6/1/2026 | |

| Ser. 2014-A, 5.00%, due 6/1/2029 | |

| Build NYC Res. Corp. Ref. Rev. (Methodist Hosp. Proj.), Ser. 2014, 5.00%, due 7/1/2029 Pre-Refunded 7/1/2024 | |

| Build NYC Res. Corp. Ref. Rev. (New York Law Sch. Proj.), Ser. 2016, 4.00%, due 7/1/2045 | |

See Notes to Financial Statements

Schedule of Investments New York Municipal Fund Inc.^ (cont’d)

| |

|

| Build NYC Res. Corp. Ref. Rev. (Packer Collegiate Institute Proj.) | |

| Ser. 2015, 5.00%, due 6/1/2026 | |

| Ser. 2015, 5.00%, due 6/1/2027 | |

| Ser. 2015, 5.00%, due 6/1/2028 | |

| Ser. 2015, 5.00%, due 6/1/2029 | |

| Ser. 2015, 5.00%, due 6/1/2030 | |

| Build NYC Res. Corp. Rev., Ser. 2014, 5.00%, due 11/1/2024 | |

| Build NYC Res. Corp. Rev. (Metro. Lighthouse Charter Sch. Proj.), Ser. 2017-A, 5.00%, due 6/1/2047 | |

| Build NYC Res. Corp. Rev. (New Dawn Charter Sch. Proj.), Ser. 2019, 5.75%, due 2/1/2049 | |

| Build NYC Res. Corp. Rev. (New World Preparatory Charter Sch. Proj.), Ser. 2021-A, 4.00%, due 6/15/2056 | |

| Build NYC Res. Corp. Rev. (Shefa Sch. Proj.), Ser. 2021-A, 5.00%, due 6/15/2051 | |

| Build NYC Res. Corp. Rev. (South Bronx Charter Sch. for Int'l Cultures and the Arts), Ser. 2013-A, 3.88%, due 4/15/2023 | |

| Build NYC Res. Corp. Solid Waste Disp. Ref. Rev. (Pratt Paper, Inc. Proj.), Ser. 2014, 4.50%, due 1/1/2025 | |

| Dutchess Co. Local Dev. Corp. Rev. (Culinary Institute of America Proj.) | |

| Ser. 2016-A-1, 5.00%, due 7/1/2041 | |

| Ser. 2016-A-1, 5.00%, due 7/1/2046 | |

| Hempstead Town Local Dev. Corp. Rev. (Molloy College Proj.) | |

| Ser. 2018, 5.00%, due 7/1/2031 | |

| Ser. 2018, 5.00%, due 7/1/2032 | |

| Ser. 2018, 5.00%, due 7/1/2033 | |

| Metro. Trans. Au. Rev. (Green Bond) | |

| Ser. 2020-C-1, 5.00%, due 11/15/2050 | |

| Ser. 2020-D-3, 4.00%, due 11/15/2049 | |

| Monroe Co. Ind. Dev. Corp. Rev. (Monroe Comm. College), Ser. 2014, (AGM Insured), 5.00%, due 1/15/2029 | |

| Monroe Co. Ind. Dev. Corp. Rev. (Nazareth College of Rochester Proj.) | |

| Ser. 2013-A, 5.00%, due 10/1/2024 | |

| Ser. 2013-A, 5.00%, due 10/1/2025 | |

| Ser. 2013-A, 4.00%, due 10/1/2026 | |

| Monroe Co. Ind. Dev. Corp. Rev. (St. John Fisher College) | |

| Ser. 2012-A, 5.00%, due 6/1/2023 | |

| Ser. 2012-A, 5.00%, due 6/1/2025 | |

| Nassau Co. G.O. (Gen. Imp. Bonds), Ser. 2013-B, 5.00%, due 4/1/2028 Pre-Refunded 4/1/2023 | |

| Nassau Co. Local Econ. Assist. Corp. Rev. (Catholic Hlth. Svcs. of Long Island Obligated Group Proj.) | |

| Ser. 2014, 5.00%, due 7/1/2023 | |

| Ser. 2014, 5.00%, due 7/1/2027 | |

| Nassau Co. Tobacco Settlement Corp. Asset Backed, Ser. 2006-A-3, 5.13%, due 6/1/2046 | |

| New York City IDA Rev. (Queens Ballpark Co. LLC), Ser. 2021-A, (AGM Insured), 3.00%, due 1/1/2046 | |

| New York City IDA Rev. (Yankee Stadium Proj.), Ser. 2020, (AGM Insured), 3.00%, due 3/1/2049 | |

| New York City Muni. Wtr. Fin. Au. Wtr. & Swr. Sys. Rev. (Second Gen. Resolution Rev. Bonds), Ser. 2013-AA-2, 1.59%, due 6/15/2050 | |

| New York City Trust for Cultural Res. Ref. Rev. (Lincoln Ctr. for the Performing Arts, Inc.), Ser. 2020-A, 4.00%, due 12/1/2035 | |

| New York Liberty Dev. Corp. Ref. Rev. (3 World Trade Ctr. Proj.), Ser. 2014-2, 5.38%, due 11/15/2040 | |

| New York Liberty Dev. Corp. Rev. (Goldman Sachs Headquarters), Ser. 2005, 5.25%, due 10/1/2035 | |

| New York Liberty Dev. Corp. Rev. Ref. (Bank of America Tower at One Bryant Park Proj.), Ser. 2019, Class 3, 2.80%, due 9/15/2069 | |

See Notes to Financial Statements

Schedule of Investments New York Municipal Fund Inc.^ (cont’d)

| |

|

| New York St. Dorm. Au. Rev. | |

| Ser. 2018-A, 5.00%, due 7/1/2048 Pre-Refunded 7/1/2028 | |

| Ser. 2018-A, 5.00%, due 7/1/2048 | |

| New York St. Dorm. Au. Rev. Non St. Supported Debt (Culinary Institute of America), Ser. 2013, 4.63%, due 7/1/2025 | |

| New York St. Dorm. Au. Rev. Non St. Supported Debt (Touro College & Univ. Sys. Obligated Group) | |

| Ser. 2014-A, 4.00%, due 1/1/2026 | |

| Ser. 2014-A, 4.00%, due 1/1/2027 | |

| Ser. 2014-A, 4.00%, due 1/1/2028 | |

| Ser. 2014-A, 4.13%, due 1/1/2029 | |

| New York St. Dorm. Au. Rev. Non St. Supported Debt (Univ. Facs.), Ser. 2013-A, 5.00%, due 7/1/2028 Pre-Refunded 7/1/2023 | |

| New York St. Dorm. Au. Rev. Non St. Supported Debt (Vaughn College of Aeronautics & Technology), Ser. 2016, 5.00%, due 12/1/2026 | |

| New York St. Dorm. Au. Rev. Ref. Non St. Supported Debt (Garnet Hlth. Med. Ctr.), Ser. 2017, 5.00%, due 12/1/2035 | |

| New York St. Dorm. Au. Rev. Ref. Non St. Supported Debt (Montefiore Oblig. Group), Ser. 2018-A, 5.00%, due 8/1/2035 | |

| New York St. Dorm. Au. Rev. Ref. Non St. Supported Debt (Orange Reg. Med. Ctr.) | |

| Ser. 2017, 5.00%, due 12/1/2036 | |

| Ser. 2017, 5.00%, due 12/1/2037 | |

| New York St. Dorm. Au. Rev. St. Personal Income Tax Rev., Ser. 2012-A, 5.00%, due 12/15/2026 | |

| New York St. Env. Facs. Corp. Solid Waste Disp. Rev. (Casella Waste Sys. Inc. Proj.) | |

| Ser. 2014, 2.88%, due 12/1/2044 Putable 12/3/2029 | |

| Ser. 2020-R-1, 2.75%, due 9/1/2050 Putable 9/2/2025 | |

| New York St. HFA Rev. (Affordable Hsg.), Ser. 2012-F, (SONYMA Insured), 3.05%, due 11/1/2027 | |

| New York St. HFA Rev. Ref. (Affordable Hsg.), Ser. 2020-H, 2.45%, due 11/1/2044 | |

| New York St. Mtge. Agcy. Homeowner Mtge. Ref. Rev., Ser. 2014-189, 3.45%, due 4/1/2027 | |

| New York St. Trans. Dev. Corp. Fac. Rev. (Empire St. Thruway Svc. Areas Proj.), Ser. 2021, 4.00%, due 4/30/2053 | |

| New York St. Trans. Dev. Corp. Spec. Fac. Ref. Rev. (American Airlines, Inc.-John F Kennedy Int'l Arpt. Proj.), Ser. 2016, 5.00%, due 8/1/2031 | |

| New York St. Trans. Dev. Corp. Spec. Fac. Rev. (Delta Airlines, Inc.-LaGuardia Arpt. Term. C&D Redev.), Ser. 2018, 5.00%, due 1/1/2033 | |

| New York St. Trans. Dev. Corp. Spec. Fac. Rev. (LaGuardia Arpt. Term. B Redev. Proj.), Ser. 2016-A, 4.00%, due 7/1/2041 | |

| New York St. Trans. Dev. Corp. Spec. Fac. Rev. Ref. (JFK Int'l Arpt. Term. 4 Proj.) | |

| Ser. 2020-A, 4.00%, due 12/1/2042 | |

| Ser. 2020-C, 4.00%, due 12/1/2042 | |

| Niagara Area Dev. Corp. Solid Waste Disp. Fac. Rev. Ref. (Covanta Proj.), Ser. 2018-A, 4.75%, due 11/1/2042 | |

| Niagara Frontier Trans. Au. Rev. Ref. (Buffalo Niagara Int'l Arpt.) | |

| Ser. 2019-A, 5.00%, due 4/1/2037 | |

| Ser. 2019-A, 5.00%, due 4/1/2038 | |

| Ser. 2019-A, 5.00%, due 4/1/2039 | |

| Oneida Co. Local Dev. Corp. Rev. Ref. (Mohawk Valley Hlth. Sys. Proj.) | |

| Ser. 2019-A, (AGM Insured), 3.00%, due 12/1/2044 | |

| Ser. 2019-A, (AGM Insured), 4.00%, due 12/1/2049 | |

| Port Au. New York & New Jersey Cons. Bonds Rev. Ref. (Two Hundred), Ser. 2017, 5.00%, due 4/15/2057 | |

| St. Lawrence Co. IDA Civic Dev. Corp. Rev. (St. Lawrence Univ. Proj.), Ser. 2012, 5.00%, due 7/1/2028 | |

| Suffolk Co. Judicial Facs. Agcy. Lease Rev. (H. Lee Dennison Bldg.), Ser. 2013, 5.00%, due 11/1/2025 | |

See Notes to Financial Statements

Schedule of Investments New York Municipal Fund Inc.^ (cont’d)

| |

|

| Suffolk Tobacco Asset Securitization Corp. Ref. (Tobacco Settle Asset Backed Sub. Bonds), Ser. 2021-B-1, 4.00%, due 6/1/2050 | |

| Triborough Bridge & Tunnel Au. Spec. Oblig., Ser. 1998-A, (National Public Finance Guarantee Corp. Insured), 4.75%, due 1/1/2024 | |

| | |

| Ser. 2017-A, 5.00%, due 6/1/2028 | |

| Ser. 2017-A, 5.00%, due 6/1/2041 | |

| Utility Debt Securitization Au. Rev., Ser. 2013-TE, 5.00%, due 12/15/2028 | |

| Westchester Co. Local Dev. Corp. Ref. Rev. (Westchester Med. Ctr.) | |

| Ser. 2016, 5.00%, due 11/1/2030 | |

| Ser. 2016, 3.75%, due 11/1/2037 | |

| Westchester Co. Local Dev. Corp. Rev. (Purchase Sr. Learning Comm., Inc. Proj.), Ser. 2021-A, 5.00%, due 7/1/2056 | |

| Westchester Co. Local Dev. Corp. Rev. Ref. (Kendal on Hudson Proj.), Ser. 2022-B, 5.00%, due 1/1/2051 | |

| Westchester Co. Local Dev. Corp. Rev. Ref. (Wartburg Sr. Hsg. Proj.), Ser. 2015-A, 5.00%, due 6/1/2030 | |

| Yonkers Econ. Dev. Corp. Ed. Rev. (Charter Sch. of Ed. Excellence Proj.), Ser. 2019-A, 5.00%, due 10/15/2049 | |

| | |

|

| So. Ohio Port Exempt Fac. Au. Rev., (PureCycle Proj.), Ser. 2020-A, 7.00%, due 12/1/2042 | |

|

| Puerto Rico Commonwealth G.O. (Restructured), Ser. 2021-A-1, 4.00%, due 7/1/2046 | |

| Puerto Rico Sales Tax Fin. Corp. Sales Tax Rev., Ser. 2018-A-1, 5.00%, due 7/1/2058 | |

| | |

|

| South Carolina St. Jobs Econ. Dev. Au. Solid Waste Disp. Rev. (AMT-Green Bond-Last Step Recycling LLC Proj.), Ser. 2021-A, 6.50%, due 6/1/2051 | |

|

| Mission Econ. Dev. Corp. Wtr. Supply Rev. (Green Bond-Env. Wtr. Minerals Proj.), Ser. 2015, 7.75%, due 1/1/2045 | |

| New Hope Cultural Ed. Facs. Fin. Corp. Sr. Living Rev. (Bridgemoor Plano Proj.), Ser. 2018-A, 7.25%, due 12/1/2053 | |

| | |

|

| Matching Fund Spec. Purp. Securitization Corp. Ref., Ser. 2022-A, 5.00%, due 10/1/2039 | |

|

| Pub. Fin. Au. Retirement Fac. Rev. Ref. (Friends Homes), Ser. 2019, 5.00%, due 9/1/2054 | |

| St. Croix Chippewa Indians of Wisconsin Ref., Ser. 2021, 5.00%, due 9/30/2041 | |

| | |

Total Investments 170.9% (Cost $100,964,363) | |

Other Assets Less Liabilities 9.3% | |

Liquidation Preference of Variable Rate Municipal Term Preferred Shares (80.2%) | |

Net Assets Applicable to Common Stockholders 100.0% | |

See Notes to Financial Statements

Schedule of Investments New York Municipal Fund Inc.^ (cont’d)

| Securities were purchased under Rule 144A of the Securities Act of 1933, as amended, or are otherwise restricted and, unless registered under the Securities Act of 1933 or exempted from registration, may only be sold to qualified institutional investors or may have other restrictions on resale. At October 31, 2022, these securities amounted to $8,524,457, which represents 16.3% of net assets applicable to common stockholders of the Fund. |

| |

| When-issued security. Total value of all such securities at October 31, 2022 amounted to $436,476, which represents 0.8% of net assets applicable to common stockholders of the Fund. |

| Variable rate demand obligation where the stated interest rate is not based on a published reference rate and spread. Rather, the interest rate generally resets daily or weekly and is determined by the remarketing agent. The rate shown represents the rate in effect at October 31, 2022. |