UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21193

First American Minnesota Municipal Income Fund II, Inc.

(Exact name of registrant as specified in charter)

800 Nicollet Mall, Minneapolis, MN | | 55402 |

(Address of principal executive offices) | | (Zip code) |

Charles D. Gariboldi, Jr., 800 Nicollet Mall, Minneapolis, MN 55402

(Name and address of agent for service)

Registrant’s telephone number, including area code: 800-677-3863

Date of fiscal year end: | August 31 |

| |

Date of reporting period: | August 31, 2008 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

Item 1. Report to Shareholders

Annual Report

August 31, 2008

MXN

Minnesota Municipal

Income Fund II

Minnesota Municipal Income Fund II

Primary Investments

First American Minnesota Municipal Income Fund II (the "fund") invests primarily in a wide range of Minnesota municipal securities that, at the time of purchase, are rated investment-grade or are unrated and deemed to be of comparable quality by FAF Advisors, Inc. ("FAF Advisors"). The fund may invest up to 20% of its total assets in municipal securities that, at the time of purchase, are rated lower than investment-grade (securities commonly referred to as "high yield" securities or "junk bonds") or are unrated and deemed to be of comparable quality by FAF Advisors. The fund's investments may include municipal derivative securities, such as inverse floating-rate and inverse interest-only municipal securities, which may be more volatile than traditional municipal securities in certain market conditions. The fund's investments also may include repurchase agreements, futures contracts, options on futures contracts, options, and in terest-rate swaps, caps, and floors.

Fund Objective

The fund is a nondiversified, closed-end management investment company. The investment objective of the fund is to provide current income exempt from both regular federal income tax and regular Minnesota personal income tax. The fund's income may be subject to federal and/or Minnesota alternative minimum tax. Distributions of capital gains will be taxable to shareholders. Investors should consult their tax advisors. As with other investment companies, there can be no assurance the fund will achieve its objective.

Table of Contents

| | 1 | | | Explanation of Financial Statements | |

|

| | 2 | | | Fund Overview | |

|

| | 7 | | | Financial Statements | |

|

| | 10 | | | Notes to Financial Statements | |

|

| | 18 | | | Schedule of Investments | |

|

| | 21 | | | Report of Independent Registered Public Accounting Firm | |

|

| | 22 | | | Notice to Shareholders | |

|

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE

Explanation of FINANCIAL STATEMENTS

As a shareholder in the fund, you receive shareholder reports semiannually. We strive to present this financial information in an easy-to-understand format; however, for many investors, the information contained in this shareholder report may seem very technical. So, we would like to take this opportunity to explain several sections of the shareholder report.

The Statement of Assets and Liabilities lists the assets and liabilities of the fund on the last day of the reporting period and presents the fund's net asset value ("NAV") and market price per share. The NAV is calculated by dividing the fund's net assets (assets minus liabilities) by the number of shares outstanding. The market price is the closing price on the exchange on which the fund's shares trade. This price, which may be higher or lower than the fund's NAV, is the price an investor pays or receives when shares of the fund are purchased or sold. The investments, as presented in the Schedule of Investments, comprise substantially all of the fund's assets. Other assets include cash and receivables for items such as income earned by the fund but not yet received. Liabilities include payables for items such as fund expenses incurred but not yet pa id.

The Statement of Operations details the dividends and interest income earned from investments as well as the expenses incurred by the fund during the reporting period. Fund expenses may be reduced through fee waivers or reimbursements. This statement reflects total expenses before any waivers or reimbursements, the amount of waivers and reimbursements (if any), and the net expenses. This statement also shows the net realized and unrealized gains and losses from investments owned during the period. The Notes to Financial Statements provide additional details on investment income and expenses of the fund.

The Statement of Changes in Net Assets describes how the fund's net assets were affected by its operating results and distributions to shareholders during the reporting period. This statement is important to investors because it shows exactly what caused the fund's net asset size to change during the period.

The Statement of Cash Flows is required when a fund has a substantial amount of illiquid investments, a substantial amount of the fund's securities are internally valued, or the fund carries some amount of debt. When presented, this statement explains the change in cash during the reporting period. It reconciles net cash provided by and used for operating activities to the net increase or decrease in net assets from operations and classifies cash receipts and payments as resulting from operating, investing, and financing activities.

The Notes to Financial Statements disclose the organizational background of the fund, its significant accounting policies, federal tax information, fees and compensation paid to affiliates, and significant risks and contingencies. Included within the notes to financial statements is the Financial Highlights. This table provides a per-share breakdown of the components that affected the fund's NAV for the current and past reporting periods. It also shows total return, expense ratios, net investment income ratios, and portfolio turnover rates. The net investment income ratios summarize the income earned less expenses, divided by the average net assets. The expense ratios represent the percentage of average net assets that were used to cover operating expenses during the period. The portfolio turnover rate represents the percentage of the fund's holdings that have changed over the course of the period, and gives an idea of how long the fund holds onto a particular security. A 100% turnover rate implies that an amount equal to the value of the entire portfolio is turned over in a year through the purchase or sale of securities.

The Schedule of Investments details all of the securities held in the fund and their related dollar values on the last day of the reporting period. Securities are usually presented by type (bonds, common stock, etc.) and by industry classification (healthcare, education, etc.). This information is useful for analyzing how your fund's assets are invested and seeing where your portfolio manager believes the best opportunities exist to meet your objectives. Holdings are subject to change without notice and do not constitute a recommendation of any individual security. The Notes to Financial Statements provide additional details on how the securities are valued.

We hope this guide to your shareholder report will help you get the most out of this important resource.

Minnesota Municipal Income Fund II 2008 Annual Report

1

Fund OVERVIEW

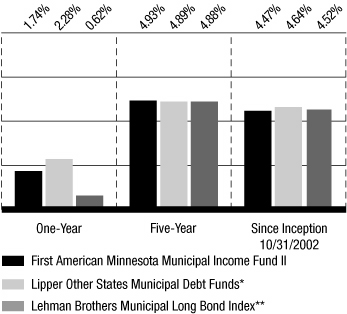

Average Annual Total Returns

Based on net asset value ("NAV") for the period ended August 31, 2008

*The Lipper Other States Municipal Debt Funds category median is calculated using the returns of all closed-end exchange traded funds in this category for each period disclosed. Lipper returns assume reinvestment of dividends. Previously, the fund had used the Lipper Minnesota Municipal Debt Funds category, which is no longer in existence.

**The Lehman Brothers Municipal Long Bond Index is comprised of municipal bonds with more than 22 years to maturity and an average credit quality of AA. The index is unmanaged and does not include any fees or expenses in its total return figures.

The average annual total returns for the fund are based on the change in its NAV and assume reinvestment of distributions at NAV. NAV-based performance is used to measure investment management results.

• Average annual total returns based on the change in market price for the one-year, five-year, and since-inception periods ended August 31, 2008, were 3.64%, 4.65%, and 2.79%, respectively.

• Market price returns assume that all distributions have been reinvested at actual prices pursuant to the fund's dividend reinvestment plan. Market price returns reflect any broker commissions or sales charges on dividends reinvested at market price.

• Please remember, you could lose money with this investment. Neither safety of principal nor stability of income is guaranteed. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that fund shares, when sold, may be worth more or less than their original cost. Closed-end funds, such as this fund, often trade at discounts to NAV. Therefore, you may be unable to realize the full NAV of your shares when you sell.

Minnesota Municipal Income Fund II 2008 Annual Report

2

Fund Management

Douglas J. White, CFA

is primarily responsible for the management of the fund. He has 25 years of financial experience.

Christopher L. Drahn

assists with the management of the fund. He has 28 years of financial experience.

First American Minnesota Municipal Income Fund II posted a total return of 1.74% based on NAV for the fiscal year ended August 31, 2008. The fund's market price return was 3.64% during the year. The fund's competitive group, the Lipper Other States Municipal Debt Funds, produced a median return of 2.28% during the year. The Lehman Brothers Municipal Long Bond Index, the benchmark comparison for the fund, which reflects no fees or expenses, returned 0.62%.

The municipal market endured one of its more tumultuous years ever as fallout from the housing debacle rocked market participants. Deterioration within their relatively new mortgage-backed book of business ultimately led to downgrades for several of the major monoline municipal bond insurers. The impaired credit quality and loss of confidence in many of the insurers affected much of the municipal market (use of insurance had become so pervasive that in recent years close to 50% of all new issuance came to market with an insurance wrap). The market was buffeted by irregular bouts of volatility and selling pressure as a number of accounts unwound positions. For example, tax-exempt money funds were forced to exit insured holdings en masse due to minimum ratings and liquidity requirements. To reduce debt, many municipal market investors were pressured to sell longer-maturity bonds when the floating-rate component of their borrowing programs was no longer money-fund eligible (the municipal market had in recent years developed its own form of "carry" trade, in which investors borrow in the short-term money markets and invest in longer maturities, trying to take advantage of the relative steepness of the municipal yield curve in comparison to other fixed-income markets).

Credit spreads (i.e., the differences in yield between higher- and lower-quality debt) were the first to widen as the market anticipated that lower-quality debt would struggle in a slowing economy. Ultimately, however, the insurer debacle cut an even wider swath through the market. Many insured bonds now trade solely based on the creditworthiness of underlying obligors with little or no value attributed to the insurance wrap. Not surprisingly, in this environment natural stand alone (i.e., without an insurance wrap) AAA and AA rated bonds were generally the best performers for the year.

Portfolio Allocation

As a percentage of total investments on August 31, 2008

| Healthcare Revenue | | | 24 | % | |

| Prerefunded Issues* | | | 16 | % | |

| Housing Revenue | | | 16 | % | |

| Lease Revenue | | | 12 | % | |

| General Obligations | | | 10 | % | |

| Utility Revenue | | | 5 | % | |

| Education Revenue | | | 5 | % | |

| Transportation Revenue | | | 5 | % | |

| Economic Development Revenue | | | 3 | % | |

| Authority Revenue | | | 2 | % | |

| Recreation Authority Revenue | | | 1 | % | |

| Tax Revenue | | | 1 | % | |

| | | | 100 | % | |

*Within the Schedule of Investments, prerefunded issues are classified under their applicable industries.

Minnesota Municipal Income Fund II 2008 Annual Report

3

Fund OVERVIEW

The municipal yield curve steepened over the past 12 months as yields on shorter maturities fell while longer maturity yields rose slightly. In terms of total return, intermediate maturities generally produced the best returns and longer-maturity bonds were the weakest-performing part of the curve. Although the overall municipal market started to regain its bearings near the end of the fiscal year, high-grade bonds still finished at yields of more than 90% (and in some cases more than 100%) of comparable-maturity Treasuries, which typically indicates that the high-grade bonds represent good value relative to Treasuries.

Better-quality bonds provided the best returns during the period. The fund's holdings of AAA- and A-rated bonds outperformed other positions as credit concerns emanating from the subprime loan market caused lower-rated and nonrated bonds to underperform higher-quality issues. While we do not believe the fundamental credit quality of most lower-rated holdings has been impaired, they nonetheless were a drag on performance.

The portfolio's short-intermediate holdings helped performance. As yields on these positions fell over the period, their prices rose more than the prices of shorter and longer maturities.

Prerefunded, lease-revenue, and general obligation sectors were the fund's better performing sectors. Senior care facilities, electric utility, and housing revenue positions lagged and had a negative impact on performance.

Bond Credit Quality Breakdown*

As a percentage of long-term investments on August 31, 2008

| AAA | | | 15 | % | |

| AA | | | 19 | % | |

| A | | | 26 | % | |

| BBB | | | 18 | % | |

| BB | | | 2 | % | |

| Nonrated | | | 20 | % | |

| | | | 100 | % | |

*Individual security ratings are based on information from Moody's Investors Service, Standard & Poor's, and/or Fitch. If there are multiple ratings for a security the lowest rating is used, unless ratings are provided by all three agencies, in which case the middle rating is used.

Minnesota Municipal Income Fund II 2008 Annual Report

4

The volatility in the municipal market during the period was in some respects historic, continuing the trend that began in late summer 2007. For example, municipal bonds continued their underperformance of comparable-maturity U.S. Treasuries to the point where, during the spring of 2008, municipal yields were the highest ever, relative to Treasuries. The volatility was primarily technical in nature, related to increased supply of municipals on the secondary market and the turbulence in the subprime market; it did not reflect broad credit quality deterioration in the municipal bond market. However, a slowing economy or recession resulting from the problems in the housing and financial markets could negatively impact the tax revenues of municipal issuers. A prolonged slowdown would in turn negatively impact some of these issuers' credit quality and poss ibly their ability to make timely interest and principal payments on their bonds. Our research staff is committed to monitoring the credit quality of the portfolio's holdings and we continue to actively manage the portfolio's risk.

We once again wish to express our appreciation for your ongoing investment in the fund. If you have any questions or need assistance with your investments, please call us at 800.677.FUND.

Sincerely,

Douglas J. White, CFA

Head of Tax Exempt Fixed Income

FAF Advisors, Inc.

Christopher L. Drahn

Senior Fixed-Income Portfolio Manager

FAF Advisors, Inc.

Minnesota Municipal Income Fund II 2008 Annual Report

5

Preferred Shares

The preferred shares issued by the fund pay dividends at a specified rate and have preference over common shares in the payments of dividends and the liquidation of assets. Rates paid on preferred shares are reset every seven days and are based on short-term tax-exempt interest rates. Preferred shareholders accept these short-term rates in exchange for low credit risk (preferred shares are rated AAA by Moody's and S&P) and high liquidity (preferred shares trade at par and are remarketed every seven days). The proceeds from the sale of preferred shares are invested at intermediate- and long-term tax-exempt rates. Because these intermediate- and long-term rates are normally higher than the short-term rates paid on preferred shares, common shareholders benefit by receiving higher dividends and/or an increase to the dividend reserve. However, the risk of having preferred shares is that if short-term rates rise higher than interm ediate- and long-term rates, creating an inverted yield curve, common shareholders may receive a lower rate of return than if their fund did not have any preferred shares outstanding. This type of economic environment is unusual and historically has been short term in nature. Investors should also be aware that the issuance of preferred shares results in the leveraging of common shares, which increases the volatility of both the NAV of the fund and the market value of common shares.

Normally, the dividend rates on the preferred shares are set at the market clearing rate determined through an auction process that brings together bidders who wish to buy preferred shares and holders of preferred shares who wish to sell. Since February 15, 2008, however, sell orders have exceeded bids and the regularly scheduled auctions for the fund's preferred shares have failed. When an auction fails, the fund is required to pay the maximum applicable rate on the preferred shares to holders of such shares for successive dividend periods until such time as the shares are successfully auctioned. The maximum applicable rate on the preferred shares is 110% of the higher of (1) the applicable AA Composite Commercial Paper Rate or (2) 90% of the Taxable Equivalent of the Short-Term Municipal Bond Rate.

During any dividend period, the maximum applicable rate could be higher than the dividend rate that would have been set had the auction been successful. In addition, as occurred for a period of time after the fund's fiscal year end, the maximum applicable rate could be higher than the fund's investment yield. Higher maximum applicable rates increase the fund's cost of leverage and reduce the fund's common share earnings.

Minnesota Municipal Income Fund II 2008 Annual Report

6

FINANCIAL STATEMENTS

Statement of Assets and Liabilities August 31, 2008

| Assets: | |

| Unaffiliated investments, at value (cost: $33,378,092) (note 2) | | $ | 32,865,525 | | |

| Receivable for accrued interest | | | 458,064 | | |

| Prepaid expenses and other assets | | | 9,681 | | |

| Total assets | | | 33,333,270 | | |

| Liabilities: | |

| Payable for preferred share distributions (note 3) | | | 6,620 | | |

| Payable for investment advisory fees (note 5) | | | 9,830 | | |

| Payable for administrative fees (note 5) | | | 5,617 | | |

| Payable for professional fees | | | 15,082 | | |

| Payable for transfer agent fees | | | 2,561 | | |

| Payable for other expenses | | | 2,574 | | |

| Total liabilities | | | 42,284 | | |

| Preferred shares, at liquidation value | | | 13,000,000 | | |

| Net assets applicable to outstanding common shares | | $ | 20,290,986 | | |

| Net assets applicable to outstanding common shares consist of: | |

| Common shares and additional paid-in capital | | $ | 20,798,974 | | |

| Undistributed net investment income | | | 87,440 | | |

| Accumulated net realized loss on investments and futures contracts | | | (82,861 | ) | |

| Net unrealized depreciation of investments | | | (512,567 | ) | |

| Net assets applicable to outstanding common shares | | $ | 20,290,986 | | |

| Net asset value and market price of common shares: | |

| Net assets applicable to outstanding common shares | | $ | 20,290,986 | | |

| Common shares outstanding (authorized 200 million shares of $0.01 par value) | | | 1,472,506 | | |

| Net asset value per share | | $ | 13.78 | | |

| Market price per share | | $ | 13.00 | | |

| Liquidation preference of preferred shares (note 3): | |

| Net assets applicable to preferred shares | | $ | 13,000,000 | | |

| Preferred shares outstanding (authorized one million shares) | | | 520 | | |

| Liquidation preference per share | | $ | 25,000 | | |

The accompanying notes are an integral part of the financial statements.

Minnesota Municipal Income Fund II 2008 Annual Report

7

FINANCIAL STATEMENTS

Statement of Operations For the Year Ended August 31, 2008

| Investment Income: | |

| Interest from unaffiliated investments | | $ | 1,729,715 | | |

| Dividends from unaffiliated money market fund | | | 7,355 | | |

| Total investment income | | | 1,737,070 | | |

| Expenses (note 5): | |

| Investment advisory fees | | | 135,363 | | |

| Administrative fees | | | 67,698 | | |

| Auction agent fees | | | 34,133 | | |

| Custodian fees | | | 1,735 | | |

| Professional fees | | | 49,185 | | |

| Postage and printing fees | | | 22,738 | | |

| Transfer agent fees | | | 19,022 | | |

| Listing fees | | | 4,599 | | |

| Directors' fees | | | 26,512 | | |

| Insurance fees | | | 11,965 | | |

| Pricing fees | | | 9,354 | | |

| Other expenses | | | 30,121 | | |

| Total expenses | | | 412,425 | | |

| Less: Wavier of advisory fees (note 5) | | | (16,891 | ) | |

| Less: Fee reimbursements (note 5) | | | (31 | ) | |

| Less: Indirect payments from custodian (note 5) | | | (3 | ) | |

| Total net expenses | | | 395,500 | | |

| Net investment income | | | 1,341,570 | | |

| Net realized and unrealized gains (losses) on investments and futures contracts (notes 2 and 4): | |

| Net realized gain (loss) on: | |

| Investments | | | 18,065 | | |

| Futures contracts | | | (11,099 | ) | |

| Net change in unrealized appreciation or depreciation of investments | | | (550,570 | ) | |

| Net loss on investments and futures contracts | | | (543,604 | ) | |

| Distributions to preferred shareholders (note 2): | |

| From net investment income | | | (366,396 | ) | |

| From net realized gain on investments | | | (72,361 | ) | |

| Total distributions | | | (438,757 | ) | |

| Net increase in net assets applicable to common shares resulting from operations | | $ | 359,209 | | |

The accompanying notes are an integral part of the financial statements.

Minnesota Municipal Income Fund II 2008 Annual Report

8

FINANCIAL STATEMENTS

Statements of Changes in Net Assets

| | | Year Ended

8/31/08 | | Year Ended

8/31/07 | |

| Operations: | |

| Net investment income | | $ | 1,341,570 | | | $ | 1,364,828 | | |

| Net realized gain (loss) on: | |

| Investments | | | 18,065 | | | | 110,393 | | |

| Futures contracts | | | (11,099 | ) | | | (36,867 | ) | |

| Net change in unrealized appreciation or depreciation of: | |

| Investments | | | (550,570 | ) | | | (1,277,844 | ) | |

| Futures contracts | | | — | | | | 44,459 | | |

| Distributions to preferred shareholders (note 2): | |

| From net investment income | | | (366,396 | ) | | | (444,604 | ) | |

| From net realized gain on investments | | | (72,361 | ) | | | (7,039 | ) | |

| Net increase (decrease) in net assets applicable to common shares resulting from operations | | | 359,209 | | | | (246,674 | ) | |

| Distributions to common shareholders (note 2): | |

| From net investment income | | | (949,766 | ) | | | (918,843 | ) | |

| From net realized gain on investments | | | (116,711 | ) | | | (16,463 | ) | |

| Total distributions | | | (1,066,477 | ) | | | (935,306 | ) | |

| Total decrease in net assets applicable to common shares | | | (707,268 | ) | | | (1,181,980 | ) | |

| Net assets applicable to common shares at beginning of year | | | 20,998,254 | | | | 22,180,234 | | |

| Net assets applicable to common shares at end of year | | $ | 20,290,986 | | | $ | 20,998,254 | | |

| Undistributed net investment income | | $ | 87,440 | | | $ | 66,794 | | |

Minnesota Municipal Income Fund II 2008 Annual Report

9

Notes to FINANCIAL STATEMENTS

(1) Organization

Minnesota Municipal Income Fund II, Inc. (the "fund") is registered under the Investment Company Act of 1940 (as amended) as a non-diversified, closed-end management investment company. The fund invests primarily in Minnesota municipal securities that, at the time of purchase, are rated investment grade or are unrated and deemed to be of comparable quality by FAF Advisors, Inc. ("FAF Advisors"). The fund may invest up to 20% of its total assets in municipal securities that, at the time of purchase, are rated lower than investment grade or are unrated and deemed to be of comparable quality by FAF Advisors. The fund's investments may include municipal derivative securities, such as inverse floating rate and inverse interest-only municipal securities, which may be more volatile than traditional municipal securities in certain market conditions. The fund's investments also may include repurchase agreements, futures contracts, options on futures contracts, options, and interest rate swaps, caps, and floors. Fund shares are listed on the American Stock Exchange under the symbol MXN.

The fund concentrates its investments in Minnesota and therefore, may have more credit risk related to the economic conditions of Minnesota than a portfolio with a broader geographical diversification.

(2) Summary of Significant Accounting Policies

Security Valuations

Debt obligations exceeding 60 days to maturity are valued by an independent pricing service that has been approved by the fund's board of directors. The pricing service may employ methodologies that utilize actual market transactions, broker-dealer supplied valuations, or other formula-driven valuation techniques. These techniques generally consider such factors as yields or prices of bonds of comparable quality, type of issue, coupon, maturity, ratings, and general market conditions. Securities for which prices are not available from an independent pricing service but where an active market exists are valued using market quotations obtained from one or more dealers that make markets in the securities or from a widely-used quotation system. Debt obligations with 60 days or less remaining until maturity may be valued at their amortized cost, which approximates market value. Investments in open-end mutual funds are valued at their respective net asset values on the valuation date.

The following investment vehicles, when held by the fund, are priced as follows: Exchange listed futures and options on futures are priced at their last sale price on the exchange on which they are principally traded, as determined by FAF Advisors, on the day the valuation is made. If there were no sales on that day, futures and options on futures will be valued at the last reported bid price. Options on securities, indices, and currencies traded on Nasdaq or listed on a stock exchange, whether domestic or foreign, are valued at the last sale price on Nasdaq or on any exchange on the day the valuation is made. If there were no sales on that day, the options will be valued at the last sale price on the previous valuation date. Last sale prices are obtained from an independent pricing service. Forward contracts (other than currency forward contracts), swaps, and over-the-counter options on securities, indices, and currencies are v alued at the quotations received from an independent pricing service, if available.

When market quotations are not readily available, securities are valued at fair value as determined in good faith by procedures established and approved by the fund's board of directors. Some of the factors which may be considered in determining fair value are fundamental analytical data relating to the investment; the nature and duration of any restrictions on disposition; trading in similar securities of the same issuer or comparable companies; information from broker-dealers; and an evaluation of the forces that influence the market in which the securities are purchased or sold. If events occur that materially affect the value of securities between the close of trading in those

Minnesota Municipal Income Fund II 2008 Annual Report

10

securities and the close of regular trading on the New York Stock Exchange, the securities will be valued at fair value.

As of August 31, 2008, the fund held no fair valued securities.

Security Transactions and Investment Income

For financial statement purposes, the fund records security transactions on the trade date of the security purchase or sale. Dividend income is recorded on the ex-dividend date. Interest income, including accretion of bond discounts and amortization of bond premiums, is recorded on an accrual basis. Security gains and losses are determined on the basis of identified cost, which is the same basis used for federal income tax purposes.

Inverse Floaters

As part of its investment strategy, the fund may invest in certain securities for which the potential income return is inversely related to changes in a floating interest rate ("inverse floaters"). In general, income on inverse floaters will decrease when short-term interest rates increase and increase when short-term interest rates decrease. Inverse floaters may be characterized as derivative securities and may subject the fund to the risks of reduced or eliminated interest payments and losses of invested principal. In addition, inverse floaters have the effect of providing investment leverage and, as a result, the market values of such securities will generally be more volatile than those of fixed-rate, tax-exempt securities. To the extent the fund invests in inverse floaters, the net asset value of the fund's shares may be more volat ile than if the fund did not invest in such securities. As of and for the year ended August 31, 2008, the fund had no outstanding investments in inverse floaters.

Repurchase Agreements

For repurchase agreements entered into with certain broker-dealers, the fund, along with other affiliated registered investment companies, may transfer uninvested cash balances into a joint trading account, the daily aggregate balance of which is invested in repurchase agreements secured by U.S. government or agency obligations. Securities pledged as collateral for all individual and joint repurchase agreements are held by the fund's custodian bank until maturity of the repurchase agreement. All agreements require that the daily market value of the collateral be in excess of the repurchase amount, including accrued interest, to protect the fund in the event of a default. As of August 31, 2008, the fund had no outstanding repurchase agreements.

Futures Transactions

In order to protect against changes in interest rates, the fund may buy and sell interest rate futures contracts. Upon entering into a futures contract, the fund is required to deposit cash or pledge U.S. government securities in an amount equal to 5% of the purchase price indicated in the futures contract (initial margin). Subsequent payments, which are dependent on the daily fluctuations in the value of the underlying security or securities, are made or received by the fund each day (daily variation margin) and recorded as unrealized gains (losses) until the contract is closed. When the contract is closed, the fund records a realized gain (loss) equal to the difference between the proceeds from (or cost of) the closing transaction and the fund's basis in the contract.

Risks of entering into futures contracts, in general, include the possibility that there will not be a perfect price correlation between the futures contracts and the underlying securities. Second, it is possible that a lack of liquidity for futures contracts could exist in the secondary market, resulting in an inability to close a futures position prior to its maturity date. Third, the purchase of a futures

Minnesota Municipal Income Fund II 2008 Annual Report

11

Notes to FINANCIAL STATEMENTS

contract involves the risk that the fund could lose more than the original margin deposit required to initiate a futures transaction. These contracts involve market risk in excess of the amount reflected in the fund's statement of assets and liabilities. Unrealized gains (losses) on outstanding positions in futures contracts held at the close of the period will be recognized as capital gains (losses) for federal income tax purposes. As of August 31, 2008, the fund had no outstanding futures contracts.

Securities Purchased on a When-Issued Basis

Delivery and payment for securities that have been purchased by the fund on a when-issued or forward-commitment basis can take place a month or more after the transaction date. Such securities do not earn interest, are subject to market fluctuation, and may increase or decrease in value prior to their delivery. The fund segregates assets with a market value equal to or greater than the amount of its purchase commitments. The purchase of securities on a when-issued or forward-commitment basis may increase the volatility of the fund's net asset value if the fund makes such purchases while remaining substantially fully invested. As of August 31, 2008, the fund had no outstanding when-issued or forward-commitment securities.

In connection with the ability to purchase securities on a when-issued basis, the fund may also enter into dollar rolls in which the fund sells securities purchased on a forward-commitment basis and simultaneously contracts with a counterparty to repurchase similar (same type, coupon, and maturity), but not identical securities on a specified future date. As an inducement for the fund to "rollover" its purchase commitments, the fund receives negotiated amounts in the form of reductions of the purchase price of the commitment. Dollar rolls are considered a form of leverage. As of and for the year ended August 31, 2008, the fund had no dollar roll transactions.

Taxes

Federal

The fund intends to continue to qualify as a regulated investment company as provided in Subchapter M of the Internal Revenue Code, as amended, and to distribute all taxable income, if any, to its shareholders. Accordingly, no provision for federal income taxes is required.

Financial Accounting Standards Board ("FASB") Interpretation No. 48, "Accounting for Uncertainty in Income Taxes" ("FIN 48") provides guidance for how uncertain tax positions should be recognized, measured, presented, and disclosed in the financial statements. FIN 48 requires the evaluation of tax positions taken or expected to be taken in the course of preparing the fund's tax returns to determine whether the tax positions are "more-likely-than-not" of being sustained by the applicable tax authority. Tax positions not deemed to meet a "more-likely-than-not" threshold would be recorded as a tax benefit or expense in the current year. As of August 31, 2008, the fund did not have any tax positions that did not meet the "more-likely-than-not" threshold of being sustained by the applicable taxing authority. Generally, tax authorities can examine all the tax returns filed for the last three years.

Net investment income and net realized gains and losses may differ for financial statement and tax purposes because of temporary or permanent book/tax differences. These differences are primarily due to deferred straddle losses. To the extent these differences are permanent, reclassifications are made to the appropriate capital accounts in the fiscal period that the differences arise.

| On the Statement of Assets and Liabilities, the following reclassifications were made: | |

|

Undistributed

Net Investment

Income | | Accumulated

Net Realized

Gain (Loss) | |

| $ | (4,762 | ) | | $ | 4,762 | | |

Minnesota Municipal Income Fund II 2008 Annual Report

12

The character of distributions made during the fiscal period from net investment income or net realized gains may differ from its ultimate characterization for federal income tax purposes. In addition, due to the timing of dividend distributions, the fiscal period in which amounts are distributed may differ from the fiscal period that the income or realized gains or losses were recorded by the fund.

The character of common and preferred share distributions paid during the fiscal years ended August 31, 2008 and August 31, 2007, were as follows:

| | | 8/31/08 | | 8/31/07 | |

| Distributions paid from: | |

| Tax exempt income | | $ | 1,311,021 | | | $ | 1,359,239 | | |

| Ordinary income | | | 15,062 | | | | 2,017 | | |

| Long-term capital gains | | | 179,566 | | | | 23,502 | | |

| | | $ | 1,505,649 | | | $ | 1,384,758 | | |

At August 31, 2008, the components of accumulated earnings (deficit) on a tax basis were as follows:

| Undistributed ordinary income | | $ | 2,962 | | |

| Undistributed tax-exempt income | | | 92,852 | | |

| Accumulated capital and post October loss | | | (73,952 | ) | |

| Unrealized appreciation (depreciation) | | | (521,476 | ) | |

| Accumulated earnings (deficit) | | $ | (499,614 | ) | |

The fund incurred losses of $73,952 for tax purposes for the period from November 1, 2007 to August 31, 2008. As permitted by tax regulations, the fund intends to elect to defer and treat the losses as arising in the fiscal year ending August 31, 2009.

State

Minnesota taxable net income is generally based on federal taxable income. The portion of tax-exempt dividends paid by the fund that is derived from interest on Minnesota municipal bonds will be excluded from Minnesota taxable net income of individuals, estates, and trusts, provided that the portion of the tax-exempt dividends paid from these obligations represents 95% or more of the exempt-interest dividends paid by the fund. The remaining portion of these dividends, and dividends that are not exempt-interest dividends or capital gains distributions, will be included in the Minnesota taxable net income of individuals, estates, and trusts, except for dividends directly attributable to interest on obligations of the U.S. government, its territories and possessions.

In 1995, Minnesota enacted a statement of intent that interest on obligations of Minnesota governmental units and Indian tribes be included in the net income of individuals, estates and trusts for Minnesota income tax purposes if a court determines that Minnesota's exemption of such interest and its taxation of interest on obligations of governmental issuers in other states unlawfully discriminates against interstate commerce. See Minn. Stat. § 289A.50, subd. 10. This provision applies to taxable years that begin during or after the calendar year in which any such determination becomes final.

Distributions to Shareholders

Distributions from net investment income are made monthly for common shareholders and weekly for preferred shareholders. Common share distributions are recorded as of the close of business on the ex-dividend date and preferred share dividends are accrued daily. Net realized gains distributions, if any, will be made at least annually. Distributions are payable in cash or, for

Minnesota Municipal Income Fund II 2008 Annual Report

13

Notes to FINANCIAL STATEMENTS

common shareholders pursuant to the fund's dividend reinvestment plan, reinvested in additional common shares of the fund. Under the dividend reinvestment plan, common shares will be purchased in the open market.

Deferred Compensation Plan

Under a Deferred Compensation Plan (the "Plan"), non-interested directors of the First American Family of Funds may participate and elect to defer receipt of part or all of their annual compensation. Deferred amounts are treated as though equivalent dollar amounts had been invested in shares of open-end First American Funds, preselected by each Director. All amounts in the Plan are 100% vested and accounts under the Plan are obligations of the fund. Deferred amounts remain in the fund until distributed in accordance with the Plan.

Use of Estimates in the Preparation of Financial Statements

The preparation of financial statements, in conformity with U.S. generally accepted accounting principles, requires management to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the results of operations during the reporting period. Actual results could differ from these estimates.

(3) Auction Preferred Shares

As of August 31, 2008, the fund had 520 auction preferred shares ("AP shares") with a liquidation preference of $25,000 per share. The dividend rate on the AP shares is adjusted every seven days (on Fridays), as determined through an auction process conducted by Bank of New York (the "Auction Agent").

Normally, the dividend rates on the AP shares are set at the market clearing rate determined through an auction process that brings together bidders who wish to buy AP shares and holders of AP shares who wish to sell. Since February 15, 2008, however, sell orders have exceeded bids and the regularly scheduled auctions for the fund's AP shares have failed. When an auction fails, the fund is required to pay the maximum applicable rate on the AP shares to holders of such shares for successive dividend periods until such time as the shares are successfully remarketed. The maximum applicable rate on the AP shares is 110% of the higher of (1) the applicable AA Composite Commercial Paper Rate or (2) 90% of the Taxable Equivalent of the Short-Term Municipal Bond Rate.

During any dividend period, the maximum applicable rate may be higher than the dividend rate that would have been set had the auction been successful. This would increase the fund's cost of leverage and reduce the fund's common share earnings. On August 31, 2008, the maximum applicable rate was 2.66%.

In the event of a failed auction, holders of AP shares will continue to receive dividends at the maximum applicable rate, but generally will not be able to sell their shares until the next successful auction. There is no way to predict when future auctions might succeed in attracting sufficient buyers for the shares offered.

(4) Investment Security Transactions

Cost of purchases and proceeds from sales of securities, other than temporary investments in short-term securities, for the year ended August 31, 2008, aggregated $7,416,018 and $7,593,108, respectively.

Minnesota Municipal Income Fund II 2008 Annual Report

14

(5) Expenses

Investment Advisory Fees

Pursuant to an investment advisory agreement (the "Agreement"), FAF Advisors, a subsidiary of U.S. Bank National Association ("U.S. Bank"), manages the fund's assets and furnishes related office facilities, equipment, research, and personnel. The Agreement as amended June 19, 2008 provides FAF Advisors with a monthly investment advisory fee in an amount equal to an annualized rate of 0.35% of the fund's average weekly net assets including preferred shares. For its fee, FAF Advisors provides investment advice and, in general, conducts the management and investment activities of the fund.

The fund may invest in related money market funds that are series of First American Funds, Inc., subject to certain limitations. In order to avoid the payment of duplicative investment advisory fees to FAF Advisors, which acts as the investment advisor to both the fund and the related money market funds, FAF Advisors will reimburse the fund an amount equal to the investment advisory fee received from the related money market funds that is attributable to the assets of the fund. These reimbursements, if any, are disclosed as "Fee reimbursements" in the Statement of Operations.

Administrative Fees

FAF Advisors serves as the fund's administrator pursuant to an administration agreement between FAF Advisors and the fund. Under this agreement, FAF Advisors receives a monthly administrative fee in an amount equal to an annualized rate of 0.20% of the fund's average weekly net assets including preferred shares. For its fee, FAF Advisors provides numerous services to the fund including, but not limited to, handling the general business affairs, financial and regulatory reporting, and various other services.

Auction Agent Fees

The fund has entered into an auction agency agreement with the Auction Agent. The auction agency agreement provides the Auction Agent with a monthly fee in an amount equal to an annual rate of 0.25% of the fund's average amount of preferred shares outstanding. For its fee, the Auction Agent will act as agent of the fund in conducting the auction of preferred shares at which the applicable dividend rate is determined for each seven-day dividend period.

Custodian Fees

U.S. Bank serves as the fund's custodian pursuant to a custodian agreement with the fund. The custodian fee charged to the fund is equal to an annual rate of 0.005% of average weekly net assets, including preferred shares. These fees are computed weekly and paid monthly.

Under this agreement, interest earned on uninvested cash balances is used to reduce a portion of the fund's custodian expenses. These credits, if any, are disclosed as "Indirect payments from custodian" in the Statement of Operations. Conversely, the custodian charges a fee for any cash overdrafts incurred, which will increase the fund's custodian expenses. For the year ended August 31, 2008, custodian fees were increased by $42 as a result of overdrafts and reduced by $3 as a result of interest earned.

Other Fees and Expenses

In addition to the investment advisory, administrative, auction agent, and custodian fees, the fund is responsible for paying most other operating expenses, including: legal, auditing, and accounting services, postage and printing of shareholder reports, transfer agent fees and expenses, listing fees, outside directors' fees and expenses, insurance, pricing, interest, taxes, and other miscellaneous expenses. For the year ended August 31, 2008, legal fees and expenses of $5,533 were paid to a law firm of which an Assistant Secretary of the fund is a partner.

Minnesota Municipal Income Fund II 2008 Annual Report

15

Notes to FINANCIAL STATEMENTS

Expenses that are directly related to the fund are charged directly to the fund. Other operating expenses of the First American Family of Funds are allocated to the fund on several bases, including evenly across all funds, allocated based on relative net assets of all funds within the First American Family of Funds, or a combination of both methods.

(6) Indemnifications

The fund enters into contracts that contain a variety of indemnifications. The fund's maximum exposure under these arrangements is unknown. However, the fund has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

(7) New Accounting Pronouncements

In September 2006, the FASB issued Statement of Financial Accounting Standards No. 157, "Fair Value Measurements" ("FAS 157"). FAS 157 clarifies the definition of fair value for financial reporting, establishes a framework for measuring fair value, and requires additional disclosure about the use of fair value measurements. FAS 157 is effective for financial statements issued for fiscal years beginning after November 15, 2007 and interim periods within those fiscal years. As of August 31, 2008, the fund does not believe the adoption of FAS 157 will materially impact the amounts reported in the financial statements; however, additional disclosures will be required about the inputs used to develop the measurements of fair value and the effect of certain measurements reported in the Statement of Operations for a fiscal period.

In March 2008, the FASB issued Statement of Financial Accounting Standards No. 161, Disclosures about Derivative Instruments and Hedging Activities ("FAS 161"). FAS 161 is effective for fiscal years and interim periods beginning after November 15, 2008. FAS 161 may require enhanced disclosures about the fund's derivative and hedging activities. Management is currently evaluating the impact the adoption of FAS 161 will have on the fund's financial statement disclosures.

Minnesota Municipal Income Fund II 2008 Annual Report

16

Notes to FINANCIAL STATEMENTS

(8) Financial Highlights

Per-share data for an outstanding common share throughout each period and selected information for each period are as follows:

| | | Year Ended August 31, | | Seven-Month

Fiscal

Period Ended | | Year Ended January 31, | |

| | | 2008 | | 2007 | | 2006 | | 8/31/05 | | 2005 | | 2004 | |

| Per-Share Data | |

| Net asset value, common shares, beginning of period | | $ | 14.26 | | | $ | 15.06 | | | $ | 15.41 | | | $ | 15.19 | | | $ | 14.70 | | | $ | 14.56 | | |

| Operations: | |

| Net investment income | | | 0.91 | | | | 0.93 | | | | 0.93 | | | | 0.53 | | | | 0.94 | | | | 0.82 | | |

Net realized and unrealized gains

(losses) on investments and futures contracts | | | (0.37 | ) | | | (0.79 | ) | | | (0.29 | ) | | | 0.25 | | | | 0.47 | | | | 0.39 | | |

| Distributions to preferred shareholders: | |

| From net investment income | | | (0.25 | ) | | | (0.30 | ) | | | (0.25 | ) | | | (0.10 | ) | | | (0.09 | ) | | | (0.07 | ) | |

| From net realized gain on investments | | | (0.05 | ) | | | (0.01 | ) | | | (0.01 | ) | | | — | | | | — | | | | — | | |

| Total from operations | | | 0.24 | | | | (0.17 | ) | | | 0.38 | | | | 0.68 | | | | 1.32 | | | | 1.14 | | |

| Distributions to common shareholders: | |

| From net investment income | | | (0.64 | ) | | | (0.62 | ) | | | (0.69 | ) | | | (0.46 | ) | | | (0.79 | ) | | | (0.80 | ) | |

| From net realized gain on investments | | | (0.08 | ) | | | (0.01 | ) | | | (0.04 | ) | | | — | | | | (0.04 | ) | | | (0.03 | ) | |

| Total distributions to common shareholders | | | (0.72 | ) | | | (0.63 | ) | | | (0.73 | ) | | | (0.46 | ) | | | (0.83 | ) | | | (0.83 | ) | |

Offering costs and underwriting discounts

associated with the issuance of preferred

shares and common shares | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | (0.17 | ) | |

| Net asset value, common shares, end of period | | $ | 13.78 | | | $ | 14.26 | | | $ | 15.06 | | | $ | 15.41 | | | $ | 15.19 | | | $ | 14.70 | | |

| Market value, common shares, end of period | | $ | 13.00 | | | $ | 13.25 | | | $ | 14.24 | | | $ | 15.06 | | | $ | 14.39 | | | $ | 14.60 | | |

| Selected Information | |

| Total return, common shares, net asset value (a) | | | 1.74 | % | | | (1.22 | )% | | | 2.65 | % | | | 4.57 | % (e) | | | 9.36 | % | | | 6.86 | % | |

| Total return, common shares, market value (b) | | | 3.64 | % | | | (2.73 | )% | | | (0.35 | )% | | | 8.00 | % (e) | | | 4.66 | % | | | 4.36 | % | |

Net assets applicable to common shares at end of

period (in millions) | | $ | 20 | | | $ | 21 | | | $ | 22 | | | $ | 23 | | | $ | 22 | | | $ | 22 | | |

Ratio of expenses to average weekly net assets

applicable to common shares before fee waivers (c) | | | 1.98 | % | | | 1.85 | % | | | 1.70 | % | | | 1.67 | % (f) | | | 1.61 | % | | | 1.99 | % | |

Ratio of expenses to average weekly net assets

applicable to common shares after fee waivers (c) | | | 1.90 | % | | | 1.77 | % | | | 1.62 | % | | | 1.59 | % (f) | | | 1.53 | % | | | 1.91 | % | |

Ratio of net investment income to average weekly net assets

applicable to common shares before fee waivers (c) | | | 6.46 | % | | | 6.12 | % | | | 6.13 | % | | | 5.95 | % (f) | | | 6.31 | % | | | 5.87 | % | |

Ratio of net investment income to average weekly net assets

applicable to common shares after fee waivers (c) | | | 6.54 | % | | | 6.20 | % | | | 6.21 | % | | | 6.03 | % (f) | | | 6.39 | % | | | 5.95 | % | |

| Portfolio turnover rate | | | 22 | % | | | 24 | % | | | 18 | % | | | 7 | % | | | 13 | % | | | 22 | % | |

Net assets applicable to preferred shares,

end of period (in millions) | | $ | 13 | | | $ | 13 | | | $ | 13 | | | $ | 13 | | | $ | 13 | | | $ | 13 | | |

| Asset coverage per preferred share (in thousands) (d) | | $ | 64 | | | $ | 65 | | | $ | 68 | | | $ | 69 | | | $ | 68 | | | $ | 67 | | |

Liquidation preference and market value per

preferred share (in thousands) | | $ | 25 | | | $ | 25 | | | $ | 25 | | | $ | 25 | | | $ | 25 | | | $ | 25 | | |

(a) Assumes reinvestment of distributions at net asset value.

(b) Assumes reinvestment of distributions at actual prices pursuant to the fund's dividend reinvestment plan.

(c) Ratios do not reflect the effect of dividend payments to preferred shareholders; income ratios reflect income earned on assets attributable to preferred shares, where applicable.

(d) Represents net assets applicable to common shares plus preferred shares at liquidation value divided by preferred shares outstanding.

(e) Total return has not been annualized.

(f) Annualized.

Minnesota Municipal Income Fund II 2008 Annual Report

17

Schedule of INVESTMENTS

Minnesota Municipal Income Fund II (MXN) August 31, 2008

| DESCRIPTION | | PAR | | VALUE I | |

| (Percentages of each investment category relate to total net assets applicable to outstanding common shares) | |

| Municipal Long-Term Investments — 161.2% | |

| Economic Development Revenue — 1.9% | |

| Agriculture and Economic Development Board, Small Business Program A — Lot 1 (AMT), 5.55%, 8/1/16 | | $ | 400,000 | | | $ | 392,804 | | |

| Education Revenue — 10.1% | |

| Higher Education Facilities, Augsburg College, Series 6, 5.00%, 5/1/28 | | | 200,000 | | | | 183,996 | | |

| Higher Education Facilities, College of Art & Design, 5.00%, 5/1/26 | | | 400,000 | | | | 372,412 | | |

| Higher Education Facilities, St. Catherine's College, 5.38%, 10/1/32 | | | 1,000,000 | | | | 955,130 | | |

| Higher Education Facilities, St. John's University, Series 5 (Prerefunded 10/1/11 @ 100), 5.25%, 10/1/26 A | | | 350,000 | | | | 379,085 | | |

| St. Paul Housing & Redevelopment Authority, Community Peace Academy Project, Series A, 5.00%, 12/1/36 | | | 200,000 | | | | 164,730 | | |

| | | | 2,055,353 | | |

| General Obligations — 16.4% | |

| City of Duluth, Series A, 5.00%, 2/1/34 | | | 700,000 | | | | 708,365 | | |

| Crow Wing County Jail, Series B (MBIA), 5.00%, 2/1/21 | | | 550,000 | | | | 573,799 | | |

| Duluth Independent School District Number 709, Series A (FSA) (MSDCEP), 4.25%, 2/1/23 | | | 500,000 | | | | 494,670 | | |

| Metropolitan Council Minneapolis-St Paul Metropolitan Area, Series C, 5.00%, 3/1/20 | | | 1,000,000 | | | | 1,068,480 | | |

| Puerto Rico Commonwealth, Series A, 5.00%, 7/1/28 | | | 500,000 | | | | 490,105 | | |

| | | | 3,335,419 | | |

| Healthcare Revenue — 54.4% | |

Agricultural and Development Board, Fairview Health Care System,

6.38%, 11/15/29 | | | 25,000 | | | | 25,771 | | |

| 6.38%, 11/15/29 (Prerefunded 11/15/10 @ 101) A | | | 675,000 | | | | 740,590 | | |

| Bemidji Health Care Facilities, North Country Health Services (RAAI), 5.00%, 9/1/31 | | | 1,000,000 | | | | 945,150 | | |

| Columbia Heights Multifamily & Health Care Facilities Revenue, Crest View Project, 5.70%, 7/1/42 | | | 350,000 | | | | 308,392 | | |

Cuyuna Range Hospital District,

5.00%, 6/1/29 | | | 350,000 | | | | 306,477 | | |

| 5.50%, 6/1/35 | | | 400,000 | | | | 364,096 | | |

Duluth Health Care Facility, Benedictine Health System-St. Mary's Hospital

(Prerefunded 2/15/14 @ 100), 5.25%, 2/15/33 A | | | 1,000,000 | | | | 1,107,660 | | |

Glencoe Health Care Facilities, Glencoe Regional Health Services

(Prerefunded 4/1/11 @ 101), 7.50%, 4/1/31 A | | | 400,000 | | | | 451,092 | | |

| Golden Valley Health Care Facilities, Covenant Retirement Communities, 5.50%, 12/1/25 | | | 600,000 | | | | 581,874 | | |

| Illinois Finance Authority Revenue, Franciscan Communities, 5.50%, 5/15/37 | | | 250,000 | | | | 206,748 | | |

| Inver Grove Heights Nursing, Presbyterian Homes, 5.50%, 10/1/33 | | | 250,000 | | | | 233,268 | | |

| Marshall Health Care Facility, Weiner Medical Center Project, 5.35%, 11/1/17 | | | 350,000 | | | | 356,741 | | |

| Minneapolis & St. Paul Housing & Redevelopment Authority, Healthpartners Project, 5.88%, 12/1/29 | | | 750,000 | | | | 743,452 | | |

Minneapolis Health Care Facilities System, Allina Health Systems

(Prerefunded 11/15/12 @ 100), 5.75%, 11/15/32 A | | | 300,000 | | | | 334,065 | | |

| Monticello, Big Lake Community Hospital District, Series C, 6.20%, 12/1/22 | | | 400,000 | | | | 395,928 | | |

| Moorhead Economic Development Authority, Housing Development Eventide Project, Series A, 5.15%, 6/1/29 | | | 300,000 | | | | 256,305 | | |

| New Hope Housing and Health Care Facility, Masonic Home North Ridge, 5.75%, 3/1/15 | | | 400,000 | | | | 394,992 | | |

| Shakopee Health Care Facility, St. Francis Regional Medical Center, 5.10%, 9/1/25 | | | 500,000 | | | | 470,560 | | |

St. Louis Park Health Care Facilities, Park Nicollet Health Systems, Series B (Prerefunded 7/1/14 @ 100),

5.50%, 7/1/25 A | | | 250,000 | | | | 281,382 | | |

| 5.25%, 7/1/30 A | | | 250,000 | | | | 278,073 | | |

| St. Paul Housing & Redevelopment Authority Hospital Revenue, HealthEast Project, 6.00%, 11/15/30 | | | 200,000 | | | | 196,846 | | |

| St. Paul Housing & Redevelopment Authority, Nursing Home Episcopal, 5.63%, 10/1/33 | | | 500,000 | | | | 428,195 | | |

St. Paul Housing & Redevelopment Authority, Regions Hospital

5.25%, 5/15/18 | | | 500,000 | | | | 498,830 | | |

| 5.30%, 5/15/28 | | | 170,000 | | | | 159,812 | | |

St. Paul Housing & Redevelopment Authority, Rossy and Richard Shaller, Sholom East Project,

Series A, 5.25%, 10/1/42 | | | 250,000 | | | | 202,445 | | |

| St. Paul Port Authority, HealthEast Midway Campus, 5.75%, 5/1/25 | | | 600,000 | | | | 573,624 | | |

| Winona Health Care Facilities, Winona Health Obligated Group, Series A, 6.00%, 7/1/34 | | | 200,000 | | | | 200,176 | | |

| | | | 11,042,544 | | |

The accompanying notes are an integral part of the financial statements.

Minnesota Municipal Income Fund II 2008 Annual Report

18

Minnesota Municipal Income Fund II (MXN)

| DESCRIPTION | | PAR | | VALUE I | |

| Housing Revenue — 27.8% | |

| Cottage Grove Senior Housing Revenue, Cottage Grove Project, 5.00%, 12/1/31 | | $ | 175,000 | | | $ | 147,406 | | |

| Eden Prairie Multifamily Housing, Preserve Place (GNMA), 5.60%, 7/20/28 | | | 500,000 | | | | 510,800 | | |

| Minneapolis Housing Revenue, Keeler Apartments Project, Series A, 5.00%, 10/1/37 | | | 300,000 | | | | 238,254 | | |

| Minneapolis Multifamily Housing, Seward Towers Project (GNMA), 5.00%, 5/20/36 | | | 1,190,000 | | | | 1,120,242 | | |

Minneapolis St. Paul Housing, Finance Board Single Family Mortgage Revenue,

Mortgage-Backed City Living (AMT) (FHLMC) (FNMA) (GNMA), 5.00%, 11/1/38 | | | 197,103 | | | | 167,949 | | |

| Minnesota State Housing Finance Agency, Residential Housing, Series D (AMT), 4.70%, 7/1/27 | | | 1,000,000 | | | | 871,750 | | |

| Moorhead Senior Housing Revenue, Sheyenne Crossing Project, 5.65%, 4/1/41 | | | 330,000 | | | | 284,685 | | |

| Prior Lake Senior Housing Revenue, Shepard's Path Senior Housing, Series B, 5.70%, 8/1/36 | | | 200,000 | | | | 184,066 | | |

Southeast State Multi-County Housing and Redevelopment Authority, Goodhue County Apartments

(Prerefunded 1/1/10 @ 100), 6.75%, 1/1/31 A | | | 320,000 | | | | 338,394 | | |

| St. Paul Multifamily Housing, Selby Grotto Housing Project (AMT) (FHA) (GNMA), 5.50%, 9/20/44 | | | 655,000 | | | | 654,974 | | |

| Washington County Housing and Redevelopment Authority, Woodland Park Apartments, 4.70%, 10/1/26 | | | 1,000,000 | | | | 949,210 | | |

| Worthington Housing Authority, Meadows Worthington Project, Series A, 5.38%, 5/1/37 | | | 200,000 | | | | 165,858 | | |

| | | | 5,633,588 | | |

| Industrial Development Revenue — 2.5% | |

| Duluth Seaway Port Authority, Cargill Project, 4.20%, 5/1/13 | | | 500,000 | | | | 509,755 | | |

| Leasing Revenue — 24.3% | |

Andover Economic Development Authority Public Facility Lease Revenue, Andover Community Center

(Crossover Refunded 2/1/14 @ 100)

5.13%, 2/1/24 ^ | | | 205,000 | | | | 222,265 | | |

| 5.13%, 2/1/24 ^ | | | 295,000 | | | | 319,845 | | |

Hopkins Housing and Redevelopment Authority, Public Facility Lease Revenue, Public Works and Fire Station,

Series A (MBIA) (Prerefunded 2/1/13 @ 100), 5.00%, 2/1/23 A | | | 1,000,000 | | | | 1,091,320 | | |

| Otter Tail County Housing and Redevelopment Authority, Building Lease Revenue, Series A, 5.00%, 2/1/19 | | | 525,000 | | | | 550,168 | | |

| Puerto Rico Public Buildings Authority, Series M (COMGTY), 6.25%, 7/1/31 | | | 200,000 | | | | 219,908 | | |

| Ramsey County Public Improvement, Series A, 4.75%, 1/1/24 | | | 1,000,000 | | | | 1,003,610 | | |

| St. Paul Housing & Redevelopment Authority, Jimmy Lee Recreation Center, 5.00%, 12/1/32 | | | 100,000 | | | | 99,714 | | |

| St. Paul Port Authority Office Building Facility, Robert Street, 5.25%, 12/1/27 | | | 1,000,000 | | | | 1,024,790 | | |

| Washington County Housing and Redevelopment Authority, Lower St. Croix Valley Fire Protection, 5.13%, 2/1/24 | | | 400,000 | | | | 400,376 | | |

| | | | 4,931,996 | | |

| Recreation Authority Revenue — 2.0% | |

| Moorhead Golf Course, Series B, 5.88%, 12/1/21 | | | 400,000 | | | | 400,012 | | |

| Tax Revenue — 4.0% | |

| Minneapolis Development Revenue, Limited Tax Supported Common Bond, Series 2-A (AMT), 5.13%, 6/1/22 | | | 500,000 | | | | 476,465 | | |

Minneapolis Tax Increment Revenue, St. Anthony Falls Project,

5.65%, 2/1/27 | | | 150,000 | | | | 137,769 | | |

| 5.75%, 2/1/27 | | | 200,000 | | | | 185,836 | | |

| | | | 800,070 | | |

| Transportation Revenue — 9.3% | |

Minneapolis & St Paul Metropolitan Airports Commission, Series A,

5.00%, 1/1/19 (AMBAC) | | | 750,000 | | | | 774,420 | | |

| 5.00%, 1/1/19 (MBIA) | | | 750,000 | | | | 784,815 | | |

| 5.25%, 1/1/32 (FGIC) (Prerefunded 1/1/11 @ 100) A | | | 300,000 | | | | 320,454 | | |

| | | | 1,879,689 | | |

| Utility Revenue — 8.5% | |

Chaska Electric, Series A

5.00%, 10/1/30 | | | 500,000 | | | | 493,395 | | |

| 6.10%, 10/1/30 | | | 10,000 | | | | 10,425 | | |

Minnesota Municipal Income Fund II 2008 Annual Report

19

Schedule of INVESTMENTS

Minnesota Municipal Income Fund II (MXN)

| DESCRIPTION | | PAR/

SHARES | | VALUE I | |

Northern Municipal Power Agency, Series A (AGTY),

5.00%, 1/1/18 | | $ | 400,000 | | | $ | 429,604 | | |

| 5.00%, 1/1/20 | | | 250,000 | | | | 262,937 | | |

| Puerto Rico Electric Power Authority, Series VV (MBIA), 5.25%, 7/1/29 | | | 500,000 | | | | 523,995 | | |

| | | | 1,720,356 | | |

Total Municipal Long-Term Investments

(Cost: $33,214,153) | | | 32,701,586 | | |

| Short-Term Investment — 0.8% | |

Federated Minnesota Municipal Cash Trust

(Cost: $163,939) | | | 163,939 | | | | 163,939 | | |

Total Investments p — 162.0%

(Cost: $33,378,092) | | | 32,865,525 | | |

| Preferred Shares at Liquidation Value — (64.1)% | | | (13,000,000 | ) | |

| Other Assets and Liabilities, Net — 2.1% | | | 425,461 | | |

| Total Net Assets — 100.0% | | $ | 20,290,986 | | |

Notes to Schedule of Investments:

I Securities are valued in accordance with procedures described in note 2 in Notes to Financial Statements

A Prerefunded issues are typically backed by U.S. government obligations, which secure the timely payment of principal and interest. These bonds mature at the call date and price indicated.

^ Crossover Refunded securities are typically backed by the credit of the refunding issuer, which secures the timely payment of principal and interest. These bonds mature at the call date and price indicated.

p On August 31, 2008, the cost of investments for federal income tax purposes was $33,387,001. The aggregate gross unrealized appreciation and depreciation of investments, based on this cost, were as follows:

| Gross unrealized appreciation | | $ | 669,429 | | |

| Gross unrealized depreciation | | | (1,190,905 | ) | |

| Net unrealized depreciation | | $ | (521,476 | ) | |

AGTY – Assured Guaranty

AMBAC – American Municipal Bond Assurance Corporation

AMT – Alternative Minimum Tax. As of August 31, 2008, the aggregate market value of securities subject to the Alternative Minimum Tax is $2,563,942 which represents 12.6% of total net assets applicable to common shares.

COMGTY – Commonwealth Guaranty

FGIC – Financial Guaranty Insurance Corporation

FHA – Federal Housing Administration

FHLMC – Federal Home Loan Mortgage Corporation

FNMA – Federal National Mortgage Association

FSA – Financial Security Assurance

GNMA – Government National Mortgage Association

MBIA – Municipal Bond Insurance Association

MSDCEP – Minnesota School District Credit Enhancement Program

RAAI – Radian Asset Assurance Inc.

The accompanying notes are an integral part of the financial statements.

Minnesota Municipal Income Fund II 2008 Annual Report

20

Report of Independent Registered PUBLIC ACCOUNTING FIRM

The Board of Directors and Shareholders

First American Minnesota Municipal Income Fund II, Inc.

We have audited the accompanying statement of assets and liabilities of First American Minnesota Municipal Income Fund II, Inc. (the "Fund"), including the schedule of investments, as of August 31, 2008, and the related statements of operations and changes in net assets and the financial highlights for the periods indicated therein. These financial statements and financial highlights are the responsibility of the Fund's management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Fund's internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund's internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and sig nificant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of August 31, 2008, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of First American Minnesota Municipal Income Fund II, Inc., at August 31, 2008, the results of its operations, the changes in its net assets, and the financial highlights for the periods indicated therein, in conformity with U.S. generally accepted accounting principles.

Minneapolis, Minnesota

October 23, 2008

Minnesota Municipal Income Fund II 2008 Annual Report

21

Notice to SHAREHOLDERS (unaudited)

TERMS AND CONDITIONS OF THE DIVIDEND REINVESTMENT PLAN

As a shareholder, you will be automatically enrolled in the fund's Dividend Reinvestment Plan (the plan). It's a convenient and economical way to buy additional shares of the fund by automatically reinvesting dividends and capital gains. The plan is administered by Computershare Trust Company, N.A. ("Computershare"), the plan administrator.

Shareholders may elect not to participate in the plan and to receive all dividends in cash by sending written instructions to Computershare at the address set forth below or by calling Computershare at 800.426.5523. Participation in the plan may be terminated or resumed at any time without penalty by contacting Computershare before the dividend record date; otherwise, the termination or resumption will be effective with respect to any subsequently declared dividend or other distribution.

Eligibility/Participation

In the event you opt out of the plan, you may resume participation in the plan at any time. Reinvestment of distributions will begin with the next distribution paid, provided your request is received before the record date for that distribution.

If your shares are in certificate form, you may re-join the plan directly and have your distributions reinvested in additional shares of the fund. To re-enroll in this plan, call Computershare at 800.426.5523. If your shares are registered in your brokerage firm's name or another name, ask the holder of your shares how you may resume participation.

If you are a beneficial owner and wish to join the plan, you must contact your bank, broker or other nominee to arrange participation in the plan on your behalf.

Alternatively, if you are a beneficial owner of our common stock, you may simply request that the number of shares of our common stock you wish to enroll in the plan be re-registered by the bank, broker or other nominee in your own name as record stockholder. You can then directly participate in the plan as described above. You should contact your bank, broker or nominee for information on how to re-register your shares.

Plan Administration

Whenever the fund declares a dividend or other capital gain distribution payable in cash, non-participants in the plan will receive cash and participants in the plan will receive the equivalent in common shares. Computershare will buy shares of the fund on the American Stock Exchange or elsewhere on the open market (open-market purchases), beginning on the payment date.

The fund will not issue any new shares in connection with the plan. All reinvestments will be at a weighted average price per share of all shares purchased in an open-market to fill the combined purchase order. Each participant will pay a pro rata share of brokerage commissions incurred in connection with the open-market purchases. The number of shares allocated to you is determined by dividing the amount of the dividend or distribution by the applicable price per share.

There is no direct charge for reinvestment of dividends and capital gains, since Computershare fees are paid for by the fund. However, each participant pays a pro rata portion of the brokerage commissions. Brokerage charges are expected to be lower than those for individual transactions because shares are purchased for all participants in blocks. As long as you continue to participate in the plan, distributions paid on the shares in your account will be reinvested.

Computershare maintains accounts for plan participants holding shares in certificate form and will furnish written confirmation of all transactions, including information you need for tax records.

Reinvested shares in your account will be held by Computershare in noncertificated form in your name.

Minnesota Municipal Income Fund II 2008 Annual Report

22

Tax Information

Distributions invested in additional shares of the fund are subject to income tax, to the same extent as if received in cash. Shareholders, as required by the Internal Revenue Service, will receive a Form 1099-DIV regarding the federal tax status of the prior year's distributions.

Plan Withdrawal

If you hold your shares in certificate form, you may terminate your participation in the plan at any time by giving written notice to Computershare or by calling Computershare at 800.426.5523. If your shares are registered in your brokerage firm's name, you may terminate your participation via verbal or written instructions to your investment professional. Written instructions should include your name and address as they appear on the certificate or account.

If notice is received before the record date, all future distributions will be paid directly to the shareholder of record.

If your shares are issued in certificate form and you discontinue your participation in the Plan, you (or your nominee) will receive an additional certificate for all full shares and a check for any fractional shares in your account.

Plan Amendment/Termination

The fund reserves the right to amend or terminate the plan. The fund will give you at least 30 days advance written notice if it makes a material amendment to or terminates the Plan.

Any questions about the Plan should be directed to your investment professional or to Computershare Trust Company, N.A., P.O. Box 43078, Providence, RI, 02940-3078, 800.426.5523.

TAX INFORMATION

The following per-share information describes the federal tax treatment of distributions made during the fiscal year. Exempt-interest dividends are exempt from federal income tax and should not be included in your gross income, but need to be reported on your income tax return for information purposes. Please consult a tax advisor on how to report these distributions at the state and local levels.

Common Share Income Distributions (the fund designates income from tax-exempt securities as 98.86%)

Minnesota Municipal Income Fund II 2008 Annual Report

23

Notice to SHAREHOLDERS (unaudited)

| Payable Date | | Amount | |

| September 26, 2007 | | $ | 0.05000 | | |

| October 24, 2007 | | | 0.05000 | | |

| November 28, 2007 | | | 0.05000 | | |

| December 26, 2007 | | | 0.05000 | | |

| January 10, 2008 | | | 0.05323 | | |

| February 20, 2008 | | | 0.05500 | | |

| March 26, 2008 | | | 0.05500 | | |

| April 23, 2008 | | | 0.05500 | | |

| May 21, 2008 | | | 0.05500 | | |

| June 25, 2008 | | | 0.05750 | | |

| July 23, 2008 | | | 0.05750 | | |

| August 27, 2008 | | | 0.06000 | | |

| Total | | $ | 0.64823 | | |

Common Share Long-Term Gain Distributions

(the fund designates the following amounts as long-term capital gains)

| Payable Date | | Amount | |

| January 10, 2008 | | $ | 0.07603 | | |

Preferred Share Income Distributions

(the fund designates income from tax-exempt securities, 98.86% qualifying as exempt-interest dividends)

| Payable Date | | Amount | |

| Total class "F" | | $ | 704.61 | | |

Preferred Share Long-Term Gain Distributions

(the fund designates the following amounts as long-term capital gains)

| Payable Date | | Amount | |

| December 26, 2007 | | $ | 139.16 | | |

Shareholder Notification of Federal Tax Status:

The fund designates 0.00% of the ordinary income distributions during the fiscal period ended August 31, 2008 as dividends qualifying for the dividends received deduction available to corporate shareholders.

In addition, the fund designates 0.00% of the ordinary income distributions from net investment income during the fiscal period ended August 31, 2008 as qualifying dividend income available to individual shareholders under the Jobs and Growth Tax Relief Reconciliation Act of 2003.

Additional Information Applicable to Foreign Shareholders Only:

The percentage of taxable ordinary income distributions that are designated as interest-related dividends under Internal Revenue Code Section 871(k)(1)(C) for the fund was 1.48%.