UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-21200 |

|

The Denali Fund Inc. |

(Exact name of registrant as specified in charter) |

|

Fund Administrative Services 2344 Spruce Street, Suite A Boulder, CO | | 80302 |

(Address of principal executive offices) | | (Zip code) |

|

Fund Administrative Services 2344 Spruce Street, Suite A Boulder, CO 80302 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (303) 444-5483 | |

|

Date of fiscal year end: | October 31, 2009 | |

|

Date of reporting period: | October 31, 2009 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

The Report to Stockholders is attached herewith.

Table of Contents

LETTER FROM THE ADVISER

Dear Shareholder:

Over the past year, the stock markets in the U.S. (and abroad) and The Denali Fund have experienced some wild swings. Pleasantly, the most recent swing has been to the upside. The Denali Fund had a total return on net asset value (NAV) of 2.0% for the fiscal year ended October 31, 2009. It may not sound like much, but it’s a nice comeback from being down as much as 30% earlier in the year. The Denali Fund underperformed the S&P 500 Index which was up 9.8% over the same period. Part of the reason for the underperformance was the relatively high cash position in Denali.

Here’s the Fund’s performance for the trailing quarter, six months and one year:

TOTAL RETURNS

| | 3 Months | | 6 Months | | One Year | |

Cumulative Returns | | Ended 10/31/09 | | Ended 10/31/09 | | Ended 10/31/09 | |

Denali Fund NAV | | 7.9 | % | 25.5 | % | 2.0 | % |

S&P 500 Index | | 5.5 | % | 20.0 | % | 9.8 | % |

Dow Jones Industrial Average | | 6.6 | % | 20.7 | % | 7.7 | % |

NASDAQ Composite | | 3.6 | % | 19.6 | % | 20.1 | % |

To give you some perspective on just how “wild” and volatile the markets have been, we’ve reproduced the table above reflecting what the trailing total returns were just 3 months earlier, for the period ending July 31, 2009.

| | 3 Months | | 6 Months | | One Year | |

Cumulative Returns | | Ended 7/31/09 | | Ended 7/31/09 | | Ended 7/31/09 | |

Denali Fund NAV | | 16.4 | % | 18.9 | % | -18.3 | % |

S&P 500 Index | | 13.8 | % | 21.1 | % | -20.0 | % |

Dow Jones Industrial Average | | 13.2 | % | 16.6 | % | -16.6 | % |

NASDAQ Composite | | 15.5 | % | 34.7 | % | -14.0 | % |

Look closely and compare the trailing one year returns. In a 3 month period, The Denali Fund went from being down 18.3% for the trailing year ending 7/31/09 to being up 2.0% for the trailing year ending 10/31/09. Based on the fact that DNY was up 7.9% for the most recent trailing quarter, it tells you that the performance that was “lopped off” from a year ago must have been terrible. It was. The Fund was down - -13.6% for the quarter ending 10/31/08, which was much better than the S&P for the same period, which was down a whopping 23.1%! So the markets have gone from being down double digits to being up double digits in a very short time-span. Part, if not most, of the answer lies in uncertainty. If there’s one thing investors hate, it’s uncertainty and there was probably more uncertainty surrounding the market, the banking

Annual Report | October 31, 2009

1

Table of Contents

system and the economy a year ago than at any time since the Great Depression. As this uncertainty has dissipated, the markets have rebounded. But beware, we may not be out of the woods yet.

We told you in the semi-annual report, but as a reminder, your Denali Fund received two 2008 Performance Achievement Certificates from Lipper Analytical Services in its closed-end classification of Real Estate Funds:

· The Denali Fund ranked #1 in the Lipper Closed-End Equity Fund Performance Analysis for Real Estate Funds for the 1-year ended December 31, 2008

· The Denali Fund ranked #1 in the Lipper Closed-End Equity Fund Performance Analysis for Real Estate Funds for the 5-years ended December 31, 2008

Though Denali is no longer a real estate fund, we believe the changes we instituted were directly responsible for getting these awards. For a short discussion on these awards, please read the shareholder letter contained in the Fund’s 4/30/09 Semi-Annual Report.

Berkshire Hathaway, the Fund’s largest position, making up nearly one-quarter of the Fund’s total assets, was down 14.3% for the 12 months ending 10/31/09. While this was certainly a drag on performance for the period, there was progress and positive news that came out of Berkshire. Berkshire made their biggest acquisition ever, buying Burlington Northern Sante Fe Railroad at an all-in price of $44 billion. Investing on that size and scale is both a tricky endeavor and a long-term benefit to Berkshire. It’s tricky because the price paid per share has to be reasonable. Pay too much, and it could take years, even decades to make up the difference. It’s a long-term benefit because it allows Berkshire to put the bulk of their idle cash into solid earning assets that can grow over time. A compound return at 10% annually requires only 7.2 years to double one’s money. Burlington’s returns for Berkshire should be near that level. There are not too many places you can invest $44 billion and expect to double your money in less than 10 years.

The Fund made a significant purchase of Johnson & Johnson (approximately 5% of the Fund’s assets). It also continued buying stock in closed-end funds trading at big discounts. So far, we’ve been getting “double-dip” returns on these closed-ends. Not only have the underlying assets in these funds increased, but the discounts have also been shrinking, meaning the market price has been appreciating faster than the NAV’s. We also made some foreign security purchases for Denali including Kiwi Income Property, a New Zealand REIT, and Unilever.

We’ve sold off the last of the REIT preferreds that we inherited two years ago, though we still own two REIT common stocks, Ventas and LTC Properties, from when we took over as advisers. Ventas is the bigger of the two positions, at over 8.5% of the Fund’s assets. Of REIT securities, we think healthcare REITs should do well in the years to come while other sectors in the REIT market may have some tough roads ahead. The

www.thedenalifund.com

2

Table of Contents

Ithan Creek Partners L.P. which we bought back in June ‘08 has performed quite well the past year.

The markets have had quite a ride upward over the past 6 to 7 months. Stocks seem to be more fully valued based on earnings, but the economy is not out of the woods quite yet. Unemployment could remain high for quite some time. A high foreclosure rate in the housing market will also temper potential rebounds. We’ve tried to make investments that will perform reasonably well even in a topsy-turvy economy. In any case, among our top investment rules are: 1) Don’t lose what we already have, 2) Invest in companies we understand with good margins, good management, and a reasonable use of debt and 3) Invest more money in our best ideas. The Horejsi affiliates own about 75% of the common stock of this Fund, so you could say without hesitation that management eats its own cooking.

The Fund has a website at www.thedenalifund.com. One of the features on the website is the ability to sign up for electronic delivery of shareholder information. Through electronic delivery, you can enjoy the convenience and timeliness of receiving and viewing stockholder communications (such as annual reports, press releases, proxy statements, etc.) online in addition to, but more quickly than, the hard copies you currently receive. To enroll, simply go to www.thedenalifund.com and click on “Sign up for email updates”. We hope you find the site useful.

Sincerely,

Carl D. Johns

Boulder Investment Advisers, LLC

Boulder, Colorado

3

Table of Contents

FINANCIAL DATA Unaudited

| | Per Share of Common Stock | |

| | Net Asset Value | | NYSE Closing Price | | Dividend Paid | |

10/31/2008 | | 15.36 | | 11.27 | | 0.195 | |

11/30/2008 | | 13.00 | | 9.84 | | 0.000 | |

12/31/2008 | | 13.88 | | 10.49 | | 0.000 | |

1/31/2009 | | 12.21 | | 10.27 | | 0.000 | |

2/28/2009 | | 10.13 | | 7.80 | | 0.000 | |

3/31/2009 | | 10.90 | | 8.22 | | 0.000 | |

4/30/2009 | | 12.48 | | 9.49 | | 0.000 | |

5/31/2009 | | 12.89 | | 10.11 | | 0.000 | |

6/30/2009 | | 13.08 | | 10.02 | | 0.000 | |

7/31/2009 | | 14.52 | | 11.91 | | 0.000 | |

8/31/2009 | | 15.35 | | 12.54 | | 0.000 | |

9/30/2009 | | 15.80 | | 13.05 | | 0.000 | |

10/31/2009 | | 15.66 | | 13.25 | | 0.000 | |

| | |

The Denali Fund Inc.: | |

· Ranked #1 in the Lipper Closed-End Equity Fund Performance Analysis for Real Estate Funds for the 1-Year Ended December 31, 2008

· Ranked #1 in the Lipper Closed-End Equity Fund Performance Analysis for Real Estate Funds for the 5-Years Ended December 31, 2008*

LIPPER and LIPPER Corporate Marks are propriety trademarks of Lipper, a Reuters Company. Used by permission.

* BIA and SIA assumed management of The Denali Fund in October 2007.

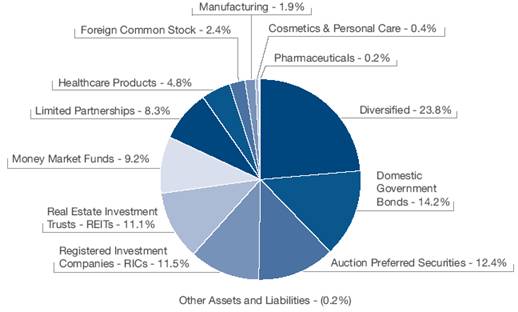

INVESTMENTS AS A % OF NET ASSETS AVAILABLE TO COMMON STOCK AND PREFERRED SHARES

4

Table of Contents

PORTFOLIO OF INVESTMENTS

October 31, 2009

Shares or | | | | | |

Principal Amount | | Description | | Value (Note 1) | |

LONG TERM INVESTMENTS 76.8% | | | |

DOMESTIC COMMON STOCKS 53.7% | | | |

Cosmetics & Personal Care 0.4% | | | |

8,000 | | The Procter & Gamble Co. | | $ | 464,000 | |

Diversified 23.8% | | | |

254 | | Berkshire Hathaway, Inc., Class A* | | 25,146,000 | |

| | | | | |

Healthcare-Products 4.8% | | | |

86,000 | | Johnson & Johnson | | 5,078,300 | |

| | | | | |

Manufacturing 1.9% | | | |

18,000 | | 3M Co. | | 1,324,260 | |

50,000 | | General Electric Co. | | 713,000 | |

| | | | 2,037,260 | |

Pharmaceuticals 0.2% | | | |

9,700 | | Pfizer, Inc. | | 165,191 | |

| | | | | |

Real Estate Investment Trusts (REITs) 11.1% | | | |

112,000 | | LTC Properties, Inc. | | 2,660,000 | |

226,200 | | Ventas, Inc. | | 9,077,406 | |

| | | | 11,737,406 | |

Registered Investment Companies (RICs) 11.5% | | | |

30,000 | | Clough Global Opportunities Fund | | 360,000 | |

220,825 | | Cohen & Steers Advantage Income Realty Fund, Inc. | | 1,157,123 | |

127,839 | | Cohen & Steers Premium Income Realty Fund, Inc. | | 609,792 | |

487,392 | | Cohen & Steers REIT and Utility Income Fund, Inc. | | 4,352,411 | |

110,700 | | Cohen & Steers Select Utility Fund, Inc. | | 1,465,668 | |

111,600 | | Cohen & Steers Worldwide Realty Income Fund, Inc. | | 650,628 | |

210,716 | | Flaherty & Crumrine/Claymore Total Return Fund, Inc. | | 2,686,629 | |

143,664 | | ING Clarion Global Real Estate Income Fund | | 833,251 | |

| | | | 12,115,502 | |

TOTAL DOMESTIC COMMON STOCKS

(Cost $48,477,757) | | 56,743,659 | |

| | | | | |

FOREIGN COMMON STOCKS 2.4% | | | |

Hong Kong 0.0%(1) | | | |

5,000 | | Guoco Group, Ltd. | | 56,289 | |

| | | | | | |

See accompanying notes to financial statements.

5

Table of Contents

Shares or | | | | | |

Principal Amount | | Description | | Value (Note 1) | |

Netherlands 1.3% | | | |

45,000 | | Unilever NV | | $ | 1,391,039 | |

| | | | | |

New Zealand 0.3% | | | |

390,199 | | Kiwi Income Property Trust | | 305,186 | |

| | | | | |

United Kingdom 0.8% | | | |

20,000 | | GlaxoSmithKline PLC-ADR | | 823,200 | |

| | | | | |

TOTAL FOREIGN COMMON STOCKS

(Cost $1,807,039) | | 2,575,714 | |

| | | | | |

AUCTION PREFERRED SECURITIES 12.4% | | | |

160 | | Advent Claymore Global Convertible Securities & Income Fund, Series W7(2) | | 3,920,000 | |

65 | | Blackrock Preferred and Equity Advantage Trust, Series F7(2) | | 1,592,500 | |

68 | | Gabelli Dividend & Income Trust, Series C(2) | | 1,666,000 | |

13 | | Neuberger Berman Real Estate Securities Income Fund, Inc., Series A(2) | | 318,500 | |

69 | | PIMCO Corporate Opportunity Fund, Series W(2) | | 1,690,500 | |

81 | | TS&W/Claymore Tax-Advantaged Balanced Fund(2) | | 1,984,500 | |

80 | | Western Asset Premier Bond Fund, Series M(2) | | 1,960,000 | |

| | | | | |

TOTAL AUCTION PREFERRED SECURITIES

(Cost $13,368,736) | | 13,132,000 | |

| | | |

LIMITED PARTNERSHIPS 8.3% | | | |

7 | | Ithan Creek Partners, L.P.*(2) | | 8,816,723 | |

| | | |

TOTAL LIMITED PARTNERSHIPS

(Cost $7,000,000) | | 8,816,723 | |

| | | | | |

TOTAL LONG TERM INVESTMENTS

(Cost $70,653,532) | | 81,268,096 | |

| | | |

SHORT TERM INVESTMENTS 23.4% | | | |

Domestic Government Bonds 14.2% | | | |

$ | 15,000,000 | | United States Treasury Bills, Discount Notes, 0.025% due 11/5/2009 | | 14,999,958 | |

| | | | | | | |

See accompanying notes to financial statements.

6

Table of Contents

Shares or | | | | | |

Principal Amount | | Description | | Value (Note 1) | |

Total Domestic Government Bonds

(Cost $14,999,958) | | $ | 14,999,958 | |

| | | |

Money Market Funds 9.2% | | | |

9,771,846 | | Dreyfus Treasury Cash Management Money Market Fund, Institutional Class, 7 Day Yield - 0.000% | | 9,771,846 | |

| | | | | |

Total Money Market Funds

(Cost $9,771,846) | | 9,771,846 | |

| | | |

TOTAL SHORT TERM INVESTMENTS

(Cost $24,771,804) | | 24,771,804 | |

| | | |

TOTAL INVESTMENTS 100.2%

(Cost $95,425,336) | | 106,039,900 | |

| | | |

OTHER ASSETS AND LIABILITIES (0.2%) | | (251,480 | ) |

| | | |

TOTAL NET ASSETS AVAILABLE TO COMMON STOCK AND PREFERRED SHARES 100.0% | | 105,788,420 | |

| | | |

AUCTION PREFERRED SHARES (APS) REDEMPTION VALUE | | (40,700,000 | ) |

| | | |

TOTAL NET ASSETS AVAILABLE TO COMMON STOCK | | $ | 65,088,420 | |

* Non-income producing security.

(1) Less than 0.1% but greater than 0.05% of total net assets available to common stock and preferred shares.

(2) Fair valued security under procedures established by the Fund’s Board of Directors. Total market of fair valued securities as of October 31, 2009 is $21,948,723, or 20.7% of total net assets available to common stock and preferred shares.

For Fund compliance purposes, the Fund’s industry and/or geography classifications refer to any one of the industry/geography sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund Management. This definition may not apply for purposes of this report, which may combine industry/geography sub-classifications for reporting ease. Industries/ geographies are shown as a percentage of net assets available to common stock and preferred shares. These industry/geography classifications are unaudited.

See accompanying notes to financial statements.

7

Table of Contents

| | stAtement of Assets And liAbilities |

| | October 31, 2009 |

ASSETS: | | | |

Investments, at value (Cost $95,425,336) (Note 1) | | $ | 106,039,900 | |

Dividends and interest receivable | | 6,428 | |

Prepaid expenses and other assets | | 8,591 | |

Total Assets | | 106,054,919 | |

| | | |

LIABILITIES: | | | |

Investment co-advisory fees payable (Note 2) | | 113,826 | |

Legal and audit fees payable | | 50,280 | |

Printing fees payable | | 28,313 | |

Administration and co-administration fees payable (Note 2) | | 24,209 | |

Directors’ fees and expenses payable | | 21,752 | |

Accumulated dividends on Auction Preferred Shares (Note 5) | | 551 | |

Accrued expenses and other payables | | 27,568 | |

Total Liabilities | | 266,499 | |

FUND TOTAL NET ASSETS | | $ | 105,788,420 | |

| | | |

AUCTION PREFERRED ShARES: | | | |

$0.0001 par value, 2,000 shares authorized, 1,628 shares outstanding, liquidation preference of $25,000 per share (Note 5) | | 40,700,000 | |

TOTAL NET ASSETS (APPLICABLE TO COMMON STOCKhOLDERS) | | $ | 65,088,420 | |

| | | |

TOTAL NET ASSETS (APPLICABLE TO COMMON STOCKhOLDERS) CONSISTS OF: | | | |

Par value of common stock (Note 4) | | $ | 416 | |

Paid-in capital in excess of par value of common stock | | 53,873,399 | |

Undistributed net investment income | | 131,550 | |

Accumulated net realized gain on investments sold and foreign currency related transactions | | 468,491 | |

Net unrealized appreciation on investments | | 10,614,564 | |

TOTAL NET ASSETS (APPLICABLE TO COMMON STOCKhOLDERS) | | $ | 65,088,420 | |

| | | | |

Net Asset Value, $65,088,420/4,157,117 common stock outstanding | | $ | 15.66 | |

See accompanying notes to financial statements.

8

Table of Contents

stAtement of opeRAtions

For the Year Ended October 31, 2009

INVESTMENT INCOME: | | | |

Dividends (Net of foreign withholding taxes of $4,644) | | $ | 2,070,366 | |

Interest | | 24,165 | |

Total Investment Income | | 2,094,531 | |

| | | |

Expenses: | | | |

Investment co-advisory fee (Note 2) | | 1,205,303 | |

Administration and co-administration fees (Note 2) | | 263,350 | |

Legal and audit fees | | 107,090 | |

Directors’ fees and expenses (Note 2) | | 76,700 | |

Preferred shares broker commissions and auction agent fees | | 55,072 | |

Transfer agency fees | | 20,601 | |

Insurance expense | | 13,191 | |

Custody fees | | 10,185 | |

Other | | 64,077 | |

Total Expenses | | 1,815,569 | |

Net Investment Income | | 278,962 | |

| | | |

REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | | | |

Net realized gain/(loss) on: | | | |

Investment securities | | 508,911 | |

Foreign currency related transactions | | (6,107 | ) |

| | 502,804 | |

| | | |

Net change in unrealized appreciation/(depreciation) of: | | | |

Investment securities | | 299,172 | |

Foreign currency related transactions | | 177,586 | |

| | 476,758 | |

| | | |

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS: | | 979,562 | |

PREFERRED ShARES TRANSACTIONS: | | | |

Distributions from net investment income | | (154,223 | ) |

Discount on redemption of Auction Preferred Shares (Note 5) | | 130,000 | |

Total Preferred Shares Transactions | | (24,223 | ) |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 1,234,301 | |

See accompanying notes to financial statements.

9

Table of Contents

| | stAtements of chAnges in net Assets |

| | Year Ended

October 31, 2009 | | Year Ended

October 31, 2008 | |

OPERATIONS: | | | | | |

Net investment income | | $ | 278,962 | | $ | 2,441,788 | |

Net realized gain on investments | | 502,804 | | 5,591,867 | |

Net change in unrealized appreciation/(depreciation) of investments | | 476,758 | | (32,729,088 | ) |

Net Increase/(Decrease) in Net Assets Resulting from Operations | | 1,258,524 | | (24,695,433 | ) |

| | | | | |

PREFERRED ShARES TRANSACTIONS: | | | | | |

Distributions from net investment income | | (154,223 | ) | (466,354 | ) |

Distributions from net realized capital gains | | — | | (1,186,226 | ) |

Discount on redemption of Auction Preferred Shares | | 130,000 | | — | |

Total Preferred Shares Transactions | | (24,223 | ) | (1,652,580 | ) |

Net Increase/(Decrease) in Net Assets Resulting from Operations Applicable to Common Stockholders | | 1,234,301 | | (26,348,013 | ) |

| | | | | |

DISTRIBUTIONS: COMMON STOCK | | | | | |

From net investment income | | — | | (1,668,999 | ) |

From net realized capital gains | | — | | (11,863,775 | ) |

From tax return of capital | | — | | (1,557,574 | ) |

Total Distributions: Common Stock | | — | | (15,090,348 | ) |

Net Increase/(Decrease) in Net Assets | | 1,234,301 | | (41,438,361 | ) |

| | | | | |

REDEMPTION OF AUCTION PREFERRED ShARES (par value) | | (1,300,000 | ) | — | |

| | | | | |

NET ASSETS: | | | | | |

Beginning of year | | 105,854,119 | | 147,292,480 | |

End of period (including un/(over) distributed net investment income of $131,550 and $(27,502), respectively) | | 105,788,420 | | 105,854,119 | |

Auction Preferred Shares (APS) Redemption Value | | (40,700,000 | ) | (42,000,000 | ) |

Net Assets Applicable to Common Stockholders | | $ | 65,088,420 | | $ | 63,854,119 | |

See accompanying notes to financial statements.

10

Table of Contents

Contained below is selected data for a share of common stock outstanding, total investment return, ratios to average net assets and other supplemental data for the period indicated. This information has been determined based upon information provided in the financial statements and market price data for the Fund’s shares.

OPERATING PERFORMANCE |

Net Asset Value - Beginning of Year |

|

Income from Investment Operations: |

Net investment income (a) |

Net realized and unrealized gain/(loss) on investments |

Total from Investment Operations |

|

Preferred Shares Transactions |

Dividends paid from net investment income (a) |

Distributions paid from net realized capital gains (a) |

Discount on redemption of Auction Preferred Shares |

Total APS* Transactions |

|

Net Increase/(Decrease) from Operations Applicable to Common Stock |

|

Distributions: Common Stock |

Dividends paid from net investment income |

Distributions paid from net realized capital gains |

Distributions paid from tax return of capital |

Total Dividends Paid to Common Stockholders |

|

Common Stock Net Asset Value - End of Year |

Common Stock Market Value - End of Year |

|

Total Return, Common Stock Net Asset Value (b) |

Total Return, Common Stock Market Value (b) |

|

RATIOS TO AVERAGE NET ASSETS AVAILABLE TO COMMON STOCKHOLDERS:(c) |

|

Gross Operating Expenses (d) |

Net Operating Expenses (e) |

Net Investment Income |

|

SUPPLEMENTAL DATA: |

Portfolio Turnover Rate |

Net Assets Applicable to Common Stockholders, End of Year (000s) |

* | Auction Preferred Shares (“APS”). |

(a) | Calculated based on the average number of shares outstanding during each fiscal period. |

Footnotes continued on page 14.

12

Table of Contents

FINANCIAL HIGHLIGHTS

For a Common Share Outstanding Throughout Each Period.

Years Ended October 31, | |

2009 | | 2008 | | 2007 | | 2006 | | 2005 | |

| | | | | | | | | |

$ | 15.36 | | $ | 25.33 | | $ | 32.22 | | $ | 24.71 | | $ | 23.00 | |

| | | | | | | | | |

0.07 | | 0.59 | | 1.26 | | 1.10 | | 0.36 | |

0.24 | | (6.53 | ) | (4.03 | ) | 8.70 | | 3.42 | |

0.31 | | (5.94 | ) | (2.77 | ) | 9.80 | | 3.78 | |

| | | | | | | | | |

(0.04 | ) | (0.11 | ) | (0.19 | ) | (0.27 | ) | (0.08 | ) |

— | | (0.29 | ) | (0.36 | ) | (0.20 | ) | (0.22 | ) |

0.03 | | — | | — | | — | | — | |

(0.01 | ) | (0.40 | ) | (0.55 | ) | (0.47 | ) | (0.30 | ) |

| | | | | | | | | |

0.30 | | (6.34 | ) | (3.32 | ) | 9.33 | | 3.48 | |

| | | | | | | | | |

— | | (0.40 | ) | (1.24 | ) | (1.03 | ) | (0.45 | ) |

— | | (2.86 | ) | (2.33 | ) | (0.79 | ) | (1.31 | ) |

— | | (0.37 | ) | — | | — | | (0.01 | ) |

— | | (3.63 | ) | (3.57 | ) | (1.82 | ) | (1.77 | ) |

| | | | | | | | | |

$ | 15.66 | | $ | 15.36 | | $ | 25.33 | | $ | 32.22 | | $ | 24.71 | |

$ | 13.25 | | $ | 11.27 | | $ | 22.08 | | $ | 28.06 | | $ | 21.36 | |

| | | | | | | | | |

1.95 | % | (25.3 | )% | (10.7 | )% | 40.5 | % | 16.9 | % |

17.57 | % | (37.1 | )% | (10.6 | )% | 41.5 | % | 16.2 | % |

| | | | | | | | | |

3.30 | % | 1.77 | % | 0.72 | % | 0.87 | % | 3.02 | % |

3.30 | % | 1.77 | % | 0.71 | % | 0.86 | % | 3.01 | % |

0.51 | % | 1.98 | % | 4.34 | % | 4.00 | % | 1.52 | % |

| | | | | | | | | |

25 | % | 91 | % | 17 | % | 15 | % | 8 | % |

$ | 65,088 | | $ | 63,854 | | $ | 105,292 | | $ | 133,933 | | $ | 102,721 | |

See accompanying notes to financial statements.

13

Table of Contents

(b) | Total return based on per share net asset value reflects the effects of changes in net asset value on the performance of the Fund during each fiscal period. Total return based on common stock market value assumes the purchase of common stock at the market price on the first day and sales of common stock at the market price on the last day of the period indicated. Dividends and distributions, if any, are assumed to be reinvested at prices obtained under the Fund’s distribution reinvestment plan. Results represent past performance and do not guarantee future results. Current returns may be lower or higher than the performance data quoted. Investment returns may fluctuate and shares when sold may be worth more or less than original cost. Total return would have been lower if Prior Management had not waived a portion of the investment administration fees. The calculation does not reflect brokerage commissions. |

(c) | Expense ratios do not include the effect of transactions with preferred shareholders. Income ratios include income earned on assets attributable to Preferred Shares outstanding. |

(d) | The Fund is required to calculate an expense ratio without taking into consideration any expense reductions related to offset arrangements. |

(e) | After waiver of, depending on the period, all or a portion of the management and/or administration fees by Prior Management. Had Prior Management not undertaken such actions, the annualized ratios of net expenses to average daily net assets applicable to common stockholders would have been: |

Years Ended October 31, | |

2009 | | 2008 | | 2007 | | 2006 | | 2005 | |

— | | — | | 1.83 | % | 2.03 | % | 4.22 | % |

The table below sets out information with respect to Auction Preferred Shares currently outstanding. (1)

| | | | | | | | Involuntary | | Average | |

| | | | | | Asset | | Liquidating | | Market | |

| | Liquidation | | Total Shares | | Coverage | | Preference | | Value | |

| | Value (000) | | Outstanding (000) | | Per Share(2) | | Per Share(3) | | Per Share(3) | |

10/31/09 | | $ | 40,700 | | 1.63 | | $ | 64,980 | | $ | 25,000 | | $ | 25,000 | |

10/31/08 | | 42,000 | | 1.68 | | 62,992 | | 25,000 | | 25,000 | |

10/31/07 | | 42,000 | | 1.68 | | 87,698 | | 25,000 | | 25,000 | |

10/31/06 | | 42,000 | | 1.68 | | 104,743 | | 25,000 | | 25,000 | |

10/31/05 | | 42,000 | | 1.68 | | 86,156 | | 25,000 | | 25,000 | |

| | | | | | | | | | | | | | | |

(1) | See Note 5. |

(2) | Calculated by subtracting the Fund’s total liabilities (excluding accumulated unpaid distributions on Preferred Shares) from the Fund’s total assets and dividing by the number of Preferred Shares outstanding. |

(3) | Excludes accumulated undeclared dividends. |

See accompanying notes to financial statements.

14

Table of Contents

NOTES TO FINANCIAL STATEMENTS

October 31, 2009

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES

The Denali Fund Inc. (the “Fund”) (formerly known as the Neuberger Berman Real Estate Income Fund Inc.) was incorporated in Maryland on September 11, 2002 as a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Board of Directors of the Fund (the “Board”) may classify or re-classify any unissued shares of capital shares into one or more classes of preferred shares without the approval of stockholders.

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. The preparation of financial statements is in accordance with generally accepted accounting principles in the United States of America, which requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

Portfolio Valuation: Investments in equity securities by the Fund are valued at the latest sale price where that price is readily available; securities for which no sales were reported, unless otherwise noted, are valued at the last available bid price. Securities traded primarily on the NASDAQ Stock Market are normally valued by the Fund at the NASDAQ Official Closing Price (“NOCP”) provided by NASDAQ each business day. Because of delays in reporting trades, the NOCP may not be based on the price of the last trade to occur before the market closes. In the absence of sales of listed securities and with respect to securities for which the most recent sale prices are not deemed to represent fair market value, and unlisted securities (other than money market instruments), securities are valued at the mean between the closing bid and asked prices, or based on a matrix system which utilizes information (such as credit ratings, yields and maturities) from independent sources. Redeemable securities issued by open-end registered investment companies are valued at the investment company’s applicable net asset value. Investments for which market quotations are not readily available or do not otherwise accurately reflect the fair value of the investment are valued at fair value as determined in good faith by or under the direction of the Board of Directors of the Fund, including reference to valuations of other securities which are considered comparable in quality, maturity and type. Short-term debt securities with less than 60 days until maturity may be valued at cost which, when combined with interest earned, approximates market value.

The Fund has adopted the Financial Accounting Standards Board (“FASB”) Accounting Standards CodificationTM (“ASC”), issued in June 2009. The Fund follows the provisions of ASC 820, “Fair Value Measurements and Disclosures” (“ASC 820”). In accordance with ASC 820, fair value is defined as the price that the Fund would receive upon selling an investment in a timely transaction to an independent buyer in the principal or most advantageous market of the investment. ASC 820 established a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a

15

Table of Contents

particular valuation technique used to measure fair value including such a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below.

| · | Level 1— quoted prices in active markets for identical investments |

| · | Level 2— significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) |

| · | Level 3— significant unobservable inputs (including the Fund’s own assumption in determining the fair value of investments) |

The valuation techniques used by the Fund to measure fair value during the year ended October 31, 2009 maximized the use of observable inputs and minimized the use of unobservable inputs. The Fund utilized the following fair value techniques: discounted future cash flow models, weighted average of last available trade prices and multi-dimensional relational pricing model.

The following is a summary of the inputs used as of October 31, 2009 in valuing the Fund’s investments carried at value:

Investments in

Securities at Value | | Level 1

Quoted Prices | | Level 2

Significant

Observable Inputs | | Level 3

Significant

Unobservable Inputs | | Total | |

Domestic Common Stocks | | $ | 56,743,659 | | $ | — | | $ | — | | $ | 56,743,659 | |

Foreign Common Stocks | | 2,575,714 | | — | | — | | 2,575,714 | |

Auction Preferred Securities | | — | | 13,132,000 | | — | | 13,132,000 | |

Hedge Funds | | — | | — | | 8,816,723 | | 8,816,723 | |

Short Term Investments | | 24,771,804 | | — | | — | | 24,771,804 | |

Total | | $ | 84,091,177 | | $ | 13,132,000 | | $ | 8,816,723 | | $ | 106,039,900 | |

16

Table of Contents

NOTES TO FINANCIAL STATEMENTS

October 31, 2009

The following is a reconciliation of assets in which significant unobservable inputs (Level 3) were used in determining fair value:

Investments | | Balance | | | | Change in | | | | Transfer in | | Balance | |

in Securities | | as of | | Realized | | unrealized | | Net | | and/or out | | as of | |

at Value | | 11/1/2008 | | gain/(loss) | | appreciation | | purchases/ (sales) | | of Level 3 | | 10/31/2009 | |

| | | | | | | | | | | | | |

Domestic Preferred Stocks | | $ | 1,500,000 | | $ | (750,000 | ) | $ | — | | $ | (750,000 | ) | $ | — | | $ | — | |

Hedge Funds | | 7,068,741 | | — | | 1,747,982 | | — | | — | | 8,816,723 | |

Total | | $ | 8,568,741 | | $ | (750,000 | ) | $ | 1,747,982 | | $ | (750,000 | ) | $ | — | | $ | 8,816,723 | |

Realized gains/(losses) and net unrealized appreciation/(deprecation), shown on the reconciliation of Level 3 securities, are included in the Statement of Operations in Net realized gain/(loss) on investments and in Net change in unrealized appreciation/(depreciation) on investments, respectively. Additionally, the Net change in unrealized appreciation for all Level 3 investments still held as of October 31, 2009, is included on the Statement of Operations in Net change in unrealized appreciation/(depreciation) on investments.

Securities Transactions and Investment Income: Securities transactions are recorded on trade date for financial reporting purposes. Dividend income is recorded on the ex-dividend date. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Interest income, including accretion of original issue discount, where applicable, and accretion of discount on short-term investments, if any, is recorded on the accrual basis. Realized gains and losses from securities transactions and foreign currency transactions, if any, are recorded on the basis of identified cost and stated separately in the Statement of Operations.

Foreign Currency Translation: The Fund may invest a portion of its assets in foreign securities. Foreign securities may carry more risk than U.S. securities, such as political, market and currency risks. The books and records of the Fund are maintained in U.S. dollars. Foreign currencies, investments and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars at the exchange rate prevailing at the end of the period, and purchases and sales of investment securities, income and expenses transacted in foreign currencies are translated at the exchange rate on the dates of such transactions. Foreign currency gains and losses result from fluctuations in exchange rates between trade date and settlement date on securities transactions, foreign currency transactions and the difference between the amounts of interest and dividends recorded on the books of the Fund and the amounts actually received. Foreign realized and unrealized gains and losses related to fluctuation in exchange rates are included in the Statement of Operations under Foreign currency related transactions.

Distributions to Stockholders: Prior to November 10, 2008, it was the policy of the Fund to declare quarterly and pay monthly distributions to common stockholders (the “Policy”). In an effort to maintain a stable distribution amount, the Fund could have paid distributions

17

Table of Contents

consisting of net investment income, realized gains and return of paid-in capital. Return of paid-in capital should not be considered yield by investors in the Fund. To the extent stockholders receive a return of paid-in capital they will be required to adjust their cost basis by the same amount upon the sale of their Fund shares. The composition of the Fund’s distributions, if any, for the calendar year 2009 will be reported to Fund stockholders on IRS Form 1099-DIV. The Fund may pay distributions in excess of those required to avoid excise tax or to satisfy the requirements of Subchapter M of the Internal Revenue Code. Distributions to common stockholders are recorded on the ex-date.

The Fund’s Policy was suspended, as approved by the Board, at the regular meeting held November 10, 2008.

In November 2008 the SEC issued an order approving exemptive relief for the Fund from Section 19(b) and Rule 19b-1 under the Securities Act of 1940 (the “Order”). In accordance with the Order, the Fund implemented a managed distribution plan for the fiscal year ended October 31, 2008.

Historically, the Fund had a significant portion of its assets invested in securities issued by real estate companies, including real estate investment trusts (“REITs”). The distributions the Fund receives from REITs are generally comprised of income, capital gains, and return of capital, but the REITs do not report this information to the Fund until the following calendar year. At October 31, 2009, the Fund estimated these amounts within the financial statements since the information is not available from the REITs until after the Fund’s fiscal year-end. For the year ended October 31, 2008, the character of distributions paid to stockholders is disclosed within the Statement of Changes and is also based on these estimates. All estimates are based upon REIT information sources available to the Fund together with actual IRS Forms 1099-DIV received to date. After calendar year-end, when the Fund learns the nature of the distributions paid by REITs during that year, distributions previously identified as income are often recharacterized as return of capital and/or capital gain. After all applicable REITs have informed the Fund of the actual breakdown of distributions paid to the Fund during its fiscal year, estimates previously recorded are adjusted on the books of the Fund to reflect actual results. As a result, the composition of the Fund’s distributions as reported herein may differ from the final composition determined after calendar year-end and reported to Fund stockholders on IRS Form 1099-DIV.

Interest Rate Swaps: The Fund may enter into interest rate swap transactions, with institutions that Management has determined are creditworthy, to reduce the risk that an increase in short-term interest rates could reduce common share net earnings as a result of leverage. Under the terms of the interest rate swap contracts, the Fund agrees to pay the swap counter party a fixed-rate payment in exchange for the counter party’s paying the Fund a variable-rate payment that is intended to approximate all or a portion of the Fund’s variable-rate payment obligation on the Fund’s Preferred Shares. The fixed-rate and variable-rate payment flows are netted against each other, with the difference being paid by one party to the other on a monthly basis. The Fund segregates cash or liquid securities having a value at least equal to the Fund’s net payment obligations under any swap transaction, marked to market periodically.

18

Table of Contents

NOTES TO FINANCIAL STATEMENTS

October 31, 2009

Risks may arise if the counterparty to a swap contract fails to comply with the terms of its contract. The loss incurred by the failure of a counter party is generally limited to the net interest payment to be received by the Fund and/or the termination value at the end of the contract. Additionally, risks may arise from movements in interest rates unanticipated by Management. At October 31, 2009, the Fund had no outstanding interest rate swap contracts.

Repurchase Agreements: The Fund may enter into repurchase agreements with institutions that Management has determined are creditworthy. Each repurchase agreement is recorded at cost. The Fund requires that the securities purchased in a repurchase agreement be transferred to the custodian in a manner sufficient to enable the Fund to assert a perfected security interest in those securities in the event of a default under the repurchase agreement. The Fund monitors, on a daily basis, the value of the securities transferred to ensure that their value, including accrued interest, is greater than amounts owed to the Fund under each such repurchase agreement. The Fund had no outstanding repurchase agreements as of October 31, 2009.

Concentration of Risk: The Fund operates as a “non-diversified” investment company, as defined in the 1940 Act. As a result of being “non-diversified”, with respect to 50% of the Fund’s portfolio, the Fund must limit to 5% the portion of its assets invested in the securities of a single issuer. There are no such limitations with respect to the balance of the Fund’s portfolio, although no single investment can exceed 25% of the Fund’s total assets at the time of purchase. A more concentrated portfolio may cause the Fund’s net asset value to be more volatile than it has been historically and thus may subject stockholders to more risk. The Fund may hold a substantial position (up to 25% of its assets) in the common stock of a single issuer. As of October 31, 2009, the Fund held close to 25% of its assets in Berkshire Hathaway, Inc. Thus, the volatility of the Fund’s common stock, and the Fund’s net asset value and its performance in general, depends disproportionately more on the performance of this single issuer than that of a more diversified fund.

In March 2008, the Fund changed its investment objective and eliminated its concentration policy in the real estate industry.

Indemnifications: Like many other companies, the Fund’s organizational documents provide that its officers and directors are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, both in some of its principal service contracts and in the normal course of its business, the Fund enters into contracts that provide indemnifications to other parties for certain types of losses or liabilities. The Fund’s maximum exposure under these arrangements is unknown as this could involve future claims against the Fund.

Federal Income Tax: It is the policy of the Fund to continue to qualify as a regulated investment company by complying with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies and to distribute substantially all of its earnings to its stockholders. Therefore, no federal income or excise tax provision is required.

19

Table of Contents

Income distributions and capital gain distributions are determined in accordance with income tax regulations, which may differ from U.S. generally accepted accounting principles. These differences are primarily due to differing treatments of income and gains on various investment securities held by the Fund, timing differences and differing characterization of distributions made by the Fund as a whole.

The Fund follows ASC 740 “Income Taxes” (“ASC 740”), which requires that the financial statement effects of a tax position taken or expected to be taken in a tax return be recognized in the financial statements when it is more likely than not, based on the technical merits, that the position will be sustained upon examination. Management has concluded that the Fund has taken no uncertain tax positions that require adjustment to the financial statements to comply with the provisions of ASC 740. The Fund files income tax returns in the U.S. federal jurisdiction and Colorado. The statue of limitations on the Fund’s federal and state tax filings remains open for the fiscal years ended October 31, 2006 through October 31, 2009.

NOTE 2. MANAGEMENT FEES, ADMINISTRATION FEES, AND OTHER TRANSACTIONS WITH AFFILIATES

Boulder Investment Advisers, L.L.C. (“BIA”) and Stewart Investment Advisers (“SIA”) (together, the “Advisers”) serve as co-advisers to the Fund. The Fund pays the Advisers a monthly fee at an annual rate of 1.25% of the value of the Fund’s average monthly net assets plus the principal amount of leverage, if any (“Net Assets”). The equity owners of BIA are Evergreen Atlantic, LLC, a Colorado limited liability company (“EALLC”), and the Lola Brown Trust No. 1B (the “Lola Trust”), each of which is considered to be an “affiliated person” of the Fund as that term is defined in the 1940 Act. Stewart West Indies Trading Company, Ltd. is a Barbados international business company doing business as Stewart Investment Advisers. SIA receives a fee equal to 75% of the fees earned by the Advisers and BIA receives 25% of the fees earned by the Advisers. The equity owner of SIA is the Stewart West Indies Trust, considered to be an “affiliated person” of the Fund as that term is defined in the 1940 Act.

Fund Administrative Services, LLC (“FAS”) serves as the Fund’s co-administrator. Under the Administration Agreement, FAS provides certain administrative and executive management services to the Fund. The Fund pays FAS a monthly fee calculated at an annual rate of 0.20% of the Fund’s Net Assets. The equity owners of FAS are EALLC and the Lola Trust, each of which is considered to be an “affiliated person” of the Fund as that term is defined in the 1940 Act.

The Fund pays each Director who is not a director, officer, employee, or affiliate of the Advisers or FAS, a fee of $8,000 per annum, plus $3,000 for each in-person meeting of the Board of Directors and $500 for each telephone meeting. In addition, the Chairman of the Board and the Chairman of the Audit Committee each receive $1,000 per meeting and each member of the Audit Committee receives $500 per meeting. The Fund will also reimburse independent Directors for travel and out-of-pocket expenses incurred in connection with such meetings.

20

Table of Contents

NOTES TO FINANCIAL STATEMENTS

October 31, 2009

ALPS Fund Services, Inc. (“ALPS”) serves as the Fund’s co-administrator. As compensation for its services, ALPS receives certain out-of-pocket expenses and asset-based fees, which are accrued daily and paid monthly. Fees paid to ALPS are calculated based on combined assets of the Fund, the Boulder Total Return Fund, Inc., the Boulder Growth & Income Fund, Inc., and First Opportunity Fund, Inc. (the “Fund Group”). ALPS receives the greater of the following, based on combined assets of the Fund Group: an annual minimum of $460,000, or an annualized fee of 0.045% on assets up to $1 billion, an annualized fee of 0.03% on assets between $1 and $3 billion, and an annualized fee of 0.02% on assets above $3 billion.

Bank of New York Mellon (“BNY Mellon”) serves as the Fund’s custodian and Common Stock servicing agent (“Transfer Agent”), dividend-paying agent and registrar, and as compensation for BNY Mellon’s services as such, the Fund pays BNY Mellon a monthly fee plus certain out-of-pocket expenses.

NOTE 3. SECURITIES TRANSACTIONS

During the year ended October 31, 2009, there were purchase and sale transactions (excluding short term securities and interest rate swap contracts) of $20,345,563 and $37,903,784, respectively.

On October 31, 2009, based on cost of $95,545,173 for federal income tax purposes, aggregate gross unrealized appreciation for all securities in which there is an excess of value over tax cost was $15,305,072 and aggregate gross unrealized depreciation for all securities in which there is an excess of tax cost over value was $4,810,345, resulting in net unrealized appreciation of $10,494,727.

NOTE 4. CAPITAL

The Fund has authorized a total of 999,998,000, $0.0001 par value Common Shares, which may be converted into Preferred Shares. At October 30, 2009, 4,157,117 Common Shares were outstanding.

Transactions in common stock were as follows:

| | Year Ended | | Year Ended | |

| | October 31, 2009 | | October 31, 2008 | |

Common Stock outstanding — beginning of year | | 4,157,117 | | 4,157,117 | |

Common Stock issued as reinvestment of dividends | | — | | — | |

Common Stock outstanding — end of year | | 4,157,117 | | 4,157,117 | |

21

Table of Contents

NOTE 5. PREFERRED SHARES

On December 12, 2002, the Fund re-classified 1,500 unissued capital shares as Series A Auction Preferred Shares (“Preferred Shares”). On February 7, 2003, the Fund issued 1,260 Preferred Shares. On September 10, 2003, the Fund re-classified an additional 500 unissued shares of capital shares as Preferred Shares. On October 24, 2003, the Fund issued an additional 420 Preferred Shares. All Preferred Shares have a liquidation preference of $25,000 per share plus any accumulated unpaid distributions, whether or not earned or declared by the Fund, but excluding interest thereon (“Liquidation Value”). On October 23, 2009, the Fund retired 52 Preferred Shares, with a total par value of $1,300,000. Those shares were purchased at a discount, at $22,500 per share, resulting in a realized discount of $130,000.

Except when the Fund has declared a special rate period, distributions to preferred stockholders, which are cumulative, are accrued daily and paid every 7 days. Distribution rates are reset every 7 days based on the results of an auction, except during special rate periods. In February 2008, the Preferred Shares market across all closed-end funds became illiquid, resulting in failed auctions for the Preferred Shares. A failed auction is not an event of default for the Fund but it has a negative impact on the liquidity of the Preferred Shares. A failed auction occurs when there are more sellers of a fund’s auction rate preferred shares than buyers. It is impossible to predict how long this imbalance will last. A successful auction for the Preferred Shares may not occur for some time, if ever, and even if liquidity does resume, holders of Preferred Shares may not have the ability to sell the Preferred Shares at its liquidation preference. As such, the Fund continues to pay dividends on the Preferred Shares at the maximum rate (set forth in the Fund’s governing document for the Preferred Shares), set at the current “AA” Financial Composite Commercial Paper rate times 150%.

For the year ended October 31, 2009, distribution rates ranged from 0.11% to 1.32%. The Fund declared distributions to preferred stockholders for the period November 1, 2008 to October 31, 2009 of $154,223.

The Fund may redeem Preferred Shares, in whole or in part, on the second business day preceding any distribution payment date at Liquidation Value. The Fund is also subject to certain restrictions relating to the Preferred Shares. Specifically, the Fund is required under the 1940 Act to maintain an asset coverage with respect to the Preferred Shares of 200% or greater. The Fund is also required to maintain certain coverage amounts for Fitch and Moody’s (“rating agencies”). Failure to comply with these restrictions could preclude the Fund from declaring any distributions to common stockholders or repurchasing common shares and/or could trigger the mandatory redemption of Preferred Shares at Liquidation Value. The holders of Preferred Shares are entitled to one vote per share and will vote with holders of common stock as a single class, except that the Preferred Shares will vote separately as a class on certain matters, as required by law or the Fund’s charter. The holders of the Preferred Shares, voting as a separate class, are entitled at all times to elect two Directors of the Fund, and to elect a majority of the Directors of the Fund if the Fund fails to pay distributions on Preferred Shares for two consecutive years.

22

Table of Contents

NOTES TO FINANCIAL STATEMENTS

October 31, 2009

In connection with the settlement of each Preferred Share auction, the Fund pays, through the auction agent, a service fee to each participating broker-dealer based upon the aggregate liquidation preference of the Preferred Shares held by the broker-dealer’s customers. Prior to February 19, 2009 the Fund paid at an annual rate 0.25% and upon this date the annual rate was reduced to 0.05%, until further notice from the Fund. These fees are paid for failed auctions as well.

In order to satisfy rating agencies’ requirements, the Fund is required to provide each rating agency a report on a monthly basis verifying that the Fund is maintaining eligible assets having a discounted value equal to or greater than the Preferred Shares Basic Maintenance Amount, which is a minimum level set by each rating agency as one of the conditions to maintain the AAA/Aaa rating on the Preferred Shares. “Discounted value” refers to the fact that the rating agencies require the Fund, in performing this calculation, to discount portfolio securities below their market value, at rates determined by the rating agencies. The Fund was in compliance with these requirements as of October 31, 2009.

NOTE 6. SIGNIFICANT SHAREHOLDERS

On October 31, 2009, the Lola Trust owned 3,082,592 Common Shares of the Fund, representing approximately 74.15% of the total Fund shares. The Lola Trust is an affiliated person of the Fund, as that term is defined in the 1940 Act. Also see Note 2 — Management fees, Administration fees, and Other Transactions with Affiliates.

NOTE 7. SHARE REPURCHASE PROGRAM

In accordance with Section 23(c) of the 1940 Act, the Fund may from time to time, effect redemptions and/or repurchases of its Preferred Shares and/or its Common Stock, in the open market or through private transactions; at the option of the Board of Directors and upon such terms as the Directors shall determine.

For the year ended October 31, 2009, the Fund purchased 52 Preferred Shares at a discount and retired them at par value. The Fund did not repurchase any common stock for the year ended October 31, 2009.

NOTE 8. TAX BASIS DISTRIBUTIONS

As determined on October 31, 2009, permanent differences resulting primarily from different book and tax accounting for distributions in excess of earnings were reclassified at fiscal year-end. These reclassifications had no effect on the net increase in net assets resulting from operations, net asset value applicable to common stockholders or net asset value per common share of the Fund. Permanent book and tax basis differences of $34,313, $(164,313), and $130,000 were reclassified at October 31, 2009 among undistributed net investment income, accumulated net realized gains on investments, and paid in capital, respectively, for the Fund.

23

Table of Contents

| NOTES TO FINANCIAL STATEMENTS |

The tax character of distributions paid during the years ended October 31, 2009 and October 31, 2008 was as follows:

| | Year Ended | | Year Ended | |

| | October 31, 2009 | | October 31, 2008 | |

Distributions paid from: | | | | | |

Ordinary Income | | $ | 154,223 | | $ | 2,135,353 | |

Long-Term Capital Gain | | — | | 13,050,001 | |

Tax Return of Capital | | — | | 1,557,574 | |

| | $ | 154,223 | | $ | 16,742,928 | |

As of October 31, 2009, the components of distributable earnings on a U.S. federal income tax basis were as follows:

Undistributed Ordinary Income | | $ | 719,878 | |

Net Unrealized Appreciation | | 10,494,727 | |

| | $ | 11,214,605 | |

The difference between book and tax basis distributable earnings is attributable primarily to temporary differences related to mark to market of passive foreign investment companies and partnership book and tax differences.

NOTE 9. RECENTLY ISSUED ACCOUNTING PRONOUNCEMENTS

In June 2009, the FASB issued ASC 105 (formerly FASB Statement 168), Generally Accepted Accounting Principles, establishing the FASB Accounting Standards CodificationTM (ASC) as the source of authoritative generally accepted accounting principles (GAAP) to be applied by nongovernmental entities. FASB ASC 105 is effective for annual and interim periods ending after September 15, 2009, and the Fund has updated its references to GAAP in this report in accordance with the provisions of this pronouncement. The implementation of FASB ASC 105 did not have a material effect on its financial position or results of operation.

In April 2009, the FASB issued FASB ASC 820-10-65 (formerly FASB Staff Position No. FAS 157-4), Determining Fair Value When the Volume and Level of Activity for the Asset or Liability Have Significantly Decreased and Identifying Transactions That Are Not Orderly. This standard applies to all assets and liabilities within the scope of accounting pronouncements that require or permit fair value measurements, with certain defined exceptions, and provides additional guidance for estimating fair value when the volume and level of activity for the asset or liability have significantly decreased. ASC 820-10-65 is effective for interim reporting periods ending after June 15, 2009. The implementation of ASC 820-10-65 did not have a material effect on the Fund’s financial position or results of operation.

NOTE 10. SUBSEQUENT EVENTS

Management has performed a review for subsequent events through December 23, 2009, the date this report was issued. There were no reportable events for the Fund as a result of their review.

24

Table of Contents

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

October 31, 2009

To the Stockholders and Board of Directors of The Denali Fund Inc.:

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of The Denali Fund Inc. (the “Fund”), as of October 31, 2009, the related statement of operations for the year then ended and the statements of changes in net assets and its financial highlights for each of the two years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. The financial highlights for each of the three years in the period ended October 31, 2007 were audited by other auditors whose reports, dated December 28, 2007 and December 8, 2006, expressed an unqualified opinion on such financial highlights.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of October 31, 2009, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of The Denali Fund Inc. as of October 31, 2009, the results of its operations for the year then ended, and the changes in its net assets and its financial highlights for each of the two years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

December 23, 2009

Denver, CO

25

Table of Contents

The Bank of New York Mellon (“Plan Agent”) will act as Plan Agent for stockholders who have not elected in writing to receive dividends and distributions in cash (each a “Participant”), will open an account for each Participant under the Distribution Reinvestment Plan (“Plan”) in the same name as their then current Shares are registered, and will put the Plan into effect for each Participant as of the first record date for a dividend or capital gains distribution.

Whenever the Fund declares a dividend or distribution with respect to the common shares of the Fund (“Shares”), each Participant will receive such dividends and distributions in additional Shares, including fractional Shares acquired by the Plan Agent and credited to each Participant’s account. If on the payment date for a cash dividend or distribution, the net asset value is equal to or less than the market price per Share plus estimated brokerage commissions, the Plan Agent shall automatically receive such Shares, including fractions, for each Participant’s account. Except in the circumstances described in the next paragraph, the number of additional Shares to be credited to each Participant’s account shall be determined by dividing the dollar amount of the dividend or distribution payable on their Shares by the greater of the net asset value per Share determined as of the date of purchase or 95% of the then current market price per Share on the payment date.

Should the net asset value per Share exceed the market price per Share plus estimated brokerage commissions on the payment date for a cash dividend or distribution, the Plan Agent or a broker-dealer selected by the Plan Agent shall endeavor, for a purchase period lasting until the last business day before the next date on which the Shares trade on an “ex-dividend” basis, but in no event, except as provided below, more than 30 days after the payment date, to apply the amount of such dividend or distribution on each Participant’s Shares (less their pro rata share of brokerage commissions incurred with respect to the Plan Agent’s open-market purchases in connection with the reinvestment of such dividend or distribution) to purchase Shares on the open market for each Participant’s account. No such purchases may be made more than 30 days after the payment date for such dividend or distribution except where temporary curtailment or suspension of purchase is necessary to comply with applicable provisions of federal securities laws. If, at the close of business on any day during the purchase period the net asset value per Share equals or is less than the market price per Share plus estimated brokerage commissions, the Plan Agent will not make any further open-market purchases in connection with the reinvestment of such dividend or distribution. If the Plan Agent is unable to invest the full dividend or distribution amount through open-market purchases during the purchase period, the Plan Agent shall request that, with respect to the uninvested portion of such dividend or distribution amount, the Fund issue new Shares at the close of business on the earlier of the last day of the purchase period or the first day during the purchase period on which the net asset value per Share equals or is less than the market price per Share, plus estimated brokerage commissions, such Shares to be issued in accordance with the terms specified in the third paragraph hereof. These newly issued Shares will be valued at the then-current market price per Share at the time such Shares are to be issued.

26

Table of Contents

DISTRIBUTION REINVESTMENT PLAN Unaudited

October 31, 2009

For purposes of making the reinvestment purchase comparison under the Plan, (a) the market price of the Shares on a particular date shall be the last sales price on the New York Stock Exchange (or if the Shares are not listed on the New York Stock Exchange, such other exchange on which the Shares are principally traded) on that date, or, if there is no sale on such Exchange (or if not so listed, in the over-the-counter market) on that date, then the mean between the closing bid and asked quotations for such Shares on such Exchange on such date and (b) the net asset value per Share on a particular date shall be the net asset value per Share most recently calculated by or on behalf of the Fund. All dividends, distributions and other payments (whether made in cash or Shares) shall be made net of any applicable withholding tax. Open-market purchases provided for above may be made on any securities exchange where the Fund’s Shares are traded, in the over-the-counter market or in negotiated transactions and may be on such terms as to price, delivery and otherwise as the Plan Agent shall determine. Each Participant’s uninvested funds held by the Plan Agent will not bear interest, and it is understood that, in any event, the Plan Agent shall have no liability in connection with any inability to purchase Shares within 30 days after the initial date of such purchase as herein provided, or with the timing of any purchases effected. The Plan Agent shall have no responsibility as to the value of the Shares acquired for each Participant’s account. For the purpose of cash investments, the Plan Agent may commingle each Participant’s funds with those of other shareholders of the Fund for whom the Plan Agent similarly acts as agent, and the average price (including brokerage commissions) of all Shares purchased by the Plan Agent as Plan Agent shall be the price per Share allocable to each Participant in connection therewith.

The Plan Agent may hold each Participant’s Shares acquired pursuant to the Plan together with the Shares of other stockholders of the Fund acquired pursuant to the Plan in noncertificated form in the Plan Agent’s name or that of the Plan Agent’s nominee. The Plan Agent will forward to each Participant any proxy solicitation material and will vote any Shares so held for each Participant only in accordance with the instructions set forth on proxies returned by the Participant to the Fund.

The Plan Agent will confirm to each Participant each acquisition made for their account as soon as practicable but not later than 60 days after the date thereof. Although each Participant may from time to time have an undivided fractional interest (computed to three decimal places) in a Share, no certificates for a fractional Share will be issued. However, dividends and distributions on fractional Shares will be credited to each Participant’s account. In the event of termination of a Participant’s account under the Plan, the Plan Agent will adjust for any such undivided fractional interest in cash at the market value of the Shares at the time of termination, less the pro rata expense of any sale required to make such an adjustment.

Any Share dividends or split Shares distributed by the Fund on Shares held by the Plan Agent for Participants will be credited to their accounts. In the event that the Fund makes available to its shareholders rights to purchase additional Shares or other securities, the Shares held for each Participant under the Plan will be added to other Shares held by the Participant in calculating the number of rights to be issued to each Participant.

27

Table of Contents

DISTRIBUTION REINVESTMENT PLAN

October 31, 2009 (Unaudited)

The Plan Agent’s service fee for handling capital gains distributions or income dividends will be paid by the Fund. Participants will be charged their pro rata share of brokerage commissions on all open-market purchases.

Each Participant may terminate their account under the Plan by notifying the Plan Agent in writing. Such termination will be effective immediately if the Participant’s notice is received by the Plan Agent not less than ten days prior to any dividend or distribution record date, otherwise such termination will be effective the first trading day after the payment date for such dividend or distribution with respect to any subsequent dividend or distribution. The Plan may be terminated by the Plan Agent or the Fund upon notice in writing mailed to each Participant at least 30 days prior to any record date for the payment of any dividend or distribution by the Fund.

These terms and conditions may be amended or supplemented by the Plan Agent or the Fund at any time or times but, except when necessary or appropriate to comply with applicable law or the rules or policies of the Securities and Exchange Commission or any other regulatory authority, only by mailing to each Participant appropriate written notice at least 30 days prior to the effective date thereof. The amendment or supplement shall be deemed to be accepted by each Participant unless, prior to the effective date thereof, the Plan Agent receives written notice of the termination of their account under the Plan. Any such amendment may include an appointment by the Plan Agent in its place and stead of a successor Plan Agent under these terms and conditions, with full power and authority to perform all or any of the acts to be performed by the Plan Agent under these terms and conditions. Upon any such appointment of any Plan Agent for the purpose of receiving dividends and distributions, the Fund will be authorized to pay to such successor Plan Agent, for each Participant’s account, all dividends and distributions payable on Shares held in their name or under the Plan for retention or application by such successor Plan Agent as provided in these terms and conditions.

The Plan Agent shall at all times act in good faith and agrees to use its best efforts within reasonable limits to ensure the accuracy of all services performed under this Agreement and to comply with applicable law, but assumes no responsibility and shall not be liable for loss or damage due to errors unless such error is caused by the Plan Agent’s negligence, bad faith, or willful misconduct or that of its employees.

These terms and conditions shall be governed by the laws of the State of Maryland.

28

Table of Contents

DIRECTORS AND OFFICERS Unaudited

October 31, 2009

Set forth in the following table is information about the Directors of the Fund, together with their address, age, position with the Fund, length of time served and principal occupation during the last five years.

INDEPENDENT DIRECTORS

Name,

Address*, Age | | Position and

Length of

Term Served | | Principal Occupation(s) and

Other Directorships held During

the Past Five Years | | Number

of Funds

in Fund

Complex†

Overseen by

Director |

Joel W.Looney Chairman Age: 47 | | Class I Director of the Fund and Chairman of the Board since 2007. | | Partner (since 1999), Financial Management Group, LLC (investment adviser); Director (since 2002) and Chairman (since 2003), Boulder Growth & Income Fund, Inc.; Director (since 2001), Boulder Total Return Fund, Inc.; Director and Chairman (since 2003), First Opportunity Fund, Inc. | | 4 |

| | | | | | |

Dr. Dean L. Jacobson Age: 70 | | Class III Director of the Fund since 2007. | | Founder and President (since 1989), Forensic Engineering, Inc. (engineering investigations); Professor Emeritus (since 1997), Arizona State University; Director (since 2006), Boulder Growth & Income Fund, Inc.; Director (since 2004) Boulder Total Return Fund, Inc.; Director (since 2003), First Opportunity Fund, Inc. | | 4 |

| | | | | | |

Richard I. Barr Age: 71 | | Class II Director of the Fund since 2007. | | Retired (since 2001). Manager (1963-2001), Advantage Sales and Marketing, Inc. (food brokerage); Director (since 2002), Boulder Growth & Income Fund, Inc.; Director (since 1999) and Chairman (since 2003), Boulder Total Return Fund, Inc.; Director (since 2001), First Opportunity Fund, Inc. | | 4 |

29

Table of Contents

INTERESTED DIRECTORS**

| | | | | | Number |

| | | | | | of Funds |

| | | | | | in Fund |

| | Position and | | Principal Occupation(s) and | | Complex† |

Name, | | Length of | | Other Directorships held During | | Overseen by |

Address*, Age | | Term Served | | the Past Five Years | | Director |

Susan L. Ciciora Age: 44 | | Class III Director of the Fund since 2007. | | Trustee (since 1994), Lola Brown Trust No. 1B and the Ernest Horejsi Trust No. 1B (since 1992); Director (since 1997), Horejsi Charitable Foundation, Inc. (private charitable foundation); Director (since 2006), Boulder Growth & Income Fund, Inc.; Director (since 2001), Boulder Total Return Fund, Inc.; Director (since 2003), First Opportunity Fund, Inc. | | 4 |

| | | | | | |

John S. Horejsi Age: 41 | | Class II Director of the Fund since 2007. | | Director (since 1997), Horejsi Charitable Foundation (private charitable foundation); Director (since 2004), Boulder Growth & Income Fund, Inc.; Director (since 2006), Boulder Total Return Fund, Inc.; Director (since 2006), First Opportunity Fund, Inc. | | 4 |

* | Unless otherwise specified, the Directors’ respective addresses are c/o The Denali Fund Inc., 2344 Spruce Street, Suite A, Boulder, Colorado 80302. |

† | Includes the Fund, Boulder Growth & Income Fund, Inc., Boulder Total Return Fund, Inc., and First Opportunity Fund, Inc. |

** | Ms. Ciciora and Mr. Horejsi each are an “interested person” as a result of the extent of their beneficial ownership of Fund shares and by virtue of their indirect beneficial ownership of BIA and FAS. |

30

Table of Contents

The names of the executive officers of the Fund are listed in the table below. Each officer was elected to office by the Board at a meeting held on February 9, 2009. This table shows certain additional information. Officers are elected annually and will hold such office until a successor has been elected by the Board.

Name,

Address*, Age | | Position, Length

of Term Served,

and Term of Office | | Principal Occupation(s) and Other Directorships

held During the Past Five Years |

Stephen C. Miller Age: 57 | | President of the Fund since 2007. Appointed annually. | | President and General Counsel (since 1999), Boulder Investment Advisers LLC; Manager (since 1999), Fund Administrative Services L.L.C.; Vice President (since 1998), Stewart Investment Advisers; President (since 2002) and Director (2002-2004), Boulder Growth & Income Fund, Inc.; President (since 1999) and Director (1999-2004), Boulder Total Return Fund, Inc.; President (since 2003) and Director and Chairman (2003), First Opportunity Fund, Inc.; officer of various other entities affiliated with the Horejsi family; Of Counsel (since 1991), Krassa & Miller, LLC. |

| | | | |

Carl D. Johns Age: 46 | | Chief Financial Officer, Chief Accounting Officer, Vice President and Treasurer of the Fund since 2007. Appointed annually. | | Vice President and Treasurer (since 1999), Boulder Investment Advisers LLC; Assistant Manager (since 1999), Fund Administrative Services L.L.C.; Chief Financial Officer, Chief Accounting Officer, Vice President and Treasurer (since 2002), Boulder Growth & Income Fund, Inc.; Vice President, Chief Financial Officer and Chief Accounting Officer (since 1999), Boulder Total Return Fund, Inc.; Vice President, Chief Financial Officer and Chief Accounting Officer (since 2003), First Opportunity Fund, Inc. |

| | | | |

Joel L. Terwilliger

Age: 41 | | Chief Compliance Officer of the Fund since 2007. Appointed annually. | | Associate General Counsel (since 2006) and Chief Compliance Officer (since 2007), Boulder Investment Advisers LLC, Stewart Investment Advisers, Fund Administrative Services L.L.C., Boulder Growth & Income Fund, Inc., Boulder Total Return Fund, Inc., and First Opportunity Fund, Inc.; Senior Associate/Managing Counsel (2002-2006), Great-West Life & Annuity Insurance Company. |

31

Table of Contents

Name,

Address*, Age | | Position, Length

of Term Served,

and Term of Office | | Principal Occupation(s) and Other Directorships

held During the Past Five Years |

Stephanie J. Kelley

Age: 53 | | Secretary since 2007. Appointed annually. | | Secretary (since 2002), Boulder Growth & Income Fund, Inc.; Secretary (since 2000), Boulder Total Return Fund, Inc., Secretary (since 2003), First Opportunity Fund, Inc.; Assistant Secretary and Assistant Treasurer of various other entities affiliated with the Horejsi family. |

| | | | |

Nicole L. Murphey

Age: 32 | | Vice President (since 2008) and Assistant Secretary since 2007. Appointed Annually. | | Vice President (since 2008) and Assistant Secretary (since 2002), Boulder Growth & Income Fund, Inc.; Vice President (since 2008) and Assistant Secretary (since 2000), Boulder Total Return Fund, Inc.; Vice President (since 2008) and Assistant Secretary (since 2003) First Opportunity Fund, Inc. |

* | Unless otherwise specified, the Officers’ respective addresses are c/o The Denali Fund Inc., 2344 Spruce Street, Suite A, Boulder, Colorado 80302. |

32

Table of Contents

ADDITIONAL INFORMATION Unaudited

October 31, 2009

Significant Events