| UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 |

| FORM N-CSR |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES |

| Investment Company Act file number 811-21233 |

| PARADIGM FUNDS (Exact name of registrant as specified in charter) |

| Nine Elk Street, Albany, NY 12207-1002 (Address of principal executive offices) (Zip code) |

| Robert A. Benton Nine Elk Street, Albany, NY 12207-1002 (Name and address of agent for service) |

Registrant's telephone number, including area code: (518) 431-3500

Date of fiscal year end: December 31

Date of reporting period: December 31, 2008

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e -1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Paradigm Funds

| Paradigm Value Fund Paradigm Select Fund Paradigm Opportunity Fund Paradigm Intrinsic Value Fund For Investors Seeking Long-Term Capital Appreciation |

| ANNUAL REPORT December 31, 2008 |

Table of Contents

| PARADIGM FUNDS | ||

| Letter to Shareholders | 2 | |

| Sector Allocation | 6 | |

| Performance Information | 8 | |

| Schedules of Investments | 12 | |

| Statements of Assets and Liabilities | 22 | |

| Statements of Operations | 22 | |

| Statements of Changes in Net Assets | 24 | |

| Financial Highlights | 26 | |

| NOTES TO FINANCIAL STATEMENTS | 28 | |

| DISCLOSURE OF EXPENSES | 33 | |

| ADDITIONAL INFORMATION | 35 | |

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | 36 | |

| TRUSTEES & OFFICERS | 38 | |

2008 Annual Report 1

Letter to Shareholders January 26, 2009 |

The final two quarters of 2008 saw one of the worst routs in the stock market in the past thirty years, as the failure of Lehman Brothers in September, and fears surrounding Lehman's derivatives book, led to a run on the country's remaining bulge bracket investment banks. The panic that ensued was greatly exacerbated by the lack of direction from Treasury, and by the intense bickering in Congress during the vote on Treasury's TARP proposal. Panic flourishes in a leadership vacuum.

Although the Lehman failure was the most proximate cause, how the financial system got to this point obviously goes well beyond the specific circumstances of one company. The question is: how could so many investment banks and major financial institutions (Lehman Brothers, Bear Stearns, Merrill Lynch, Freddie Mac, Fannie Mae, AIG, etc.) all have brought themselves to the brink of ruin so heedlessly? Most of the investment banks failed because money had been easy for a long time, and they had leveraged themselves up and thrown themselves into the housing bubble, through subprime mortgage securitizations and derivatives. The Basel II accords and US financial deregulation allowed investment banks to greatly increase their leverage as a function of common equity, and investment banks that used to have 10x - 12x leverage ratios had ratios as high as 30x - 40x by the end of 2007. Fannie Mae and Freddie Mac were allowed to leveraged themselves in a similar fashion by their regul ators. The two companies used their federal charter and implicit government guarantees to corner the market in prime mortgage securitizations, and then used the funds generated by their increased leverage to hold giant investment portfolios of mortgage-backed securities that they themselves guaranteed (that is, doubling their exposure on an already levered capital base.)

The investment banks ignored the tremendous risks of subprime mortgages because the profits were so big; because management got paid out with large bonuses on an annual basis, and thus didn't have to worry about the long-term consequences of their actions; because the ratings agencies blessed subprime securitizations with AAA ratings, because they themselves were making a lot of money and were compensated on a short-term basis; because the investment banks were given a free ride by the regulators, who were clearly asleep at the wheel; because the nation itself was in the thralls of the housing bubble, and was not worried about risk; and, well, because the last time the financial markets got into trouble, the Fed bailed them out.

This inferred bailout of the financial markets used to be called the "Greenspan Put." As the government finalizes its latest bailout of the financial industry, it's worth keeping in mind how many times the Treasury and Fed-how many times the Greenspan Put-had come to the rescue of the financial markets over the last twenty years, with each crisis worse than the last, and with each successful rescue serving paradoxically to increase the level of leverage and risk-taking by the financial community and the investing public, precisely because the rescue had been handled so masterfully. The Greenspan Put was a classic example of moral hazard; and moral hazard is what created the housing bubble out of the collapse of the tech bubble, and what took down the investment banking industry last fall.

Now the world is in a process of deleveraging and economic contraction. The process has been painful for investors, and will be painful for most Americans as the recession runs its course. But, the leverage we held was unsustainable, and for all of its pain, deleveraging will end up having positive effects for our country in the future. The derivatives market should have been regulated after Long Term Capital Management; we have paid the price, but it will be so going forward. Off-balance sheet financing and "shadow" banking should have been cut off at the knees after Enron. It was not; but banking regulation and leverage requirements will change as well. The cost of bailing

2008 Annual Report 2

out the financial system and stimulating the economy will be high, in the trillions. The US can handle that. One should assume, though, that the current low levels of long-term interest rates will come to an end as the Treasury continues to issue new debt.

As for the investing climate, the market (as measured by the S&P 500) is down by more than 40% since its highs in October of 2007. In every sell-off of similar magnitude in the post-war period, the market has rallied substantially in the one or two-year period afterwards. In 1973-1974, the market sold off 42% from its peak in the beginning of '73 to the end of '74. It rallied 54% in the following two years. In the crash of '87, the market fell 33% peak to trough in the fourth quarter; only to rally 60% over the next two years. In each of these cases, the markets rallied not because the world had suddenly become a better place (1975 marked the fall of Saigon; 1988 was the peak of the savings and loan crisis), but simply because markets overreact during panics. This is something we are seeing clearly in our bottom-up research of individual stocks in the small cap marketplace: valuations have fallen so low that stocks should be able to achieve above-average returns even assuming mediocre economic conditions over the next few years.

2008 was a frustrating year. But we are value investors, and we are taking advantage of the market's downturn to buy some great businesses at very cheap valuations. We do not know how long this recession will last. We firmly believe, however, that disciplined value investing in this kind of environment will ultimately lead to exceptional results well into the future.

2008 Annual Report 3

Paradigm Value Fund Portfolio Performance |

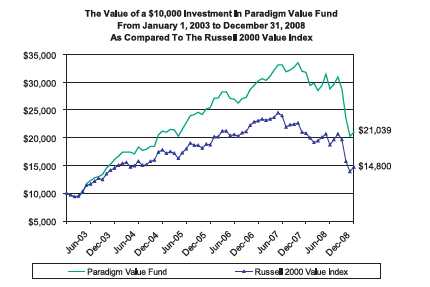

The Paradigm Value Fund declined 33.88% during 2008, compared to a 28.92% drop for its benchmark, the Russell 2000 Value Index. Over the past three years on an annualized basis, the Fund has declined 6.10% vs. a 7.49% drop for the benchmark. Since inception (1/1/03) on an annualized basis, the Fund has generated a return of 13.18% compared to 6.75% for the Russell 2000 Value Index.

Relative to the benchmark, the Fund experienced a challenging 2008 in the Industrials and Energy sectors. These two sectors were significant drivers of Fund outperformance over the last market cycle. We reduced our exposure to both sectors as the year progressed. However, the speed and depth of the economic slowdown had a negative impact on portfolio performance.

The Fund's Consumer Staples and Health Care stocks did relatively well in 2008. Flowers Foods, a southeastern U.S. bakery, expertly navigated the volatile commodity environment and generated 26% earnings growth. The stock appreciated 6% for the year. Two of our pharmaceutical holdings also generated strong returns. Alpharma, a specialty pharmaceutical company focused on pain management, was acquired by King Pharmaceutical for a significant premium, and returned 78%. Later in the year, we took advantage of the market sell-off to acquire shares of Endo Pharmaceutical, another specialty player focused on pain management. Endo continued to generate revenue and earnings growth above expectations, and appreciated 23%.

| Paradigm Select Fund Portfolio Performance |

The Paradigm Select Fund declined 33.61% during 2008 compared to a 36.79% drop for its benchmark, the Russell 2500 Index. Over the past three years on an annualized basis, the Fund has declined 5.16% vs. a 9.37% drop for the benchmark. Since inception (1/1/05) on an annualized basis, the Fund has declined 1.13% compared to decline of 5.29% for the Russell 2500 Index.

Relative to the benchmark, the Fund experienced a strong year in the Consumer Staples, Energy, and Financials sectors, driven by both stock and sector allocation decisions. In the traditionally defensive Consumer Staples sector, both Flowers Foods, a southeastern U.S. baking company, and Church & Dwight, a marketer of household products, posted strong earnings growth in 2008 of 26% and 16%, respectively. In the Energy sector, our profit-taking in the middle of the year left us with an underweight position relative to our benchmark when oil prices collapsed in the fall. Finally, our decision to underweight banks and stick with conservative balance sheets in the Financial sector was a major contributor to relative performance in the year.

The Fund experienced a challenging year in the Consumer Discretionary sector. In particular, our exposure to two auto-related names negatively impacted performance. While the two companies, Goodyear Tire and Penske Auto, are high quality businesses, neither was able dodge the tsunami that hit the industry this fall. Several retail names were also significant detractors to Fund performance this year.

2008 Annual Report 4

Paradigm Opportunity Fund Portfolio Performance |

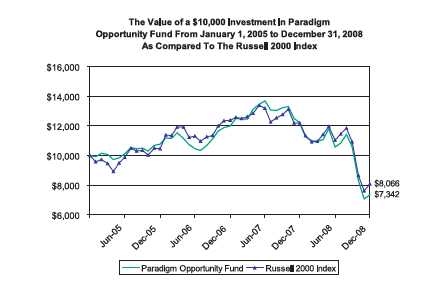

The Paradigm Opportunity Fund declined 39.89% during 2008 compared to a 33.79% drop for its benchmark, the Russell 2000 Index. Over the past three years on an annualized basis, the Fund has declined 11.97% vs. an 8.28% drop for the benchmark. Since inception (1/1/05) on an annualized basis, the Fund has declined 7.43% compared to 5.23% for the Russell 2000 Index.

Relative to the benchmark, the Fund experienced a challenging year in cyclical Consumer Discretionary, Industrials, and Technology sectors. The Fund was overweight Technology and Consumer Discretionary, two of the three worst performing sectors in the index. Poor stock selection in Industrials also hurt relative performance.

The Fund benefited from positive stock selection in the Energy, Materials and Financials sectors. In addition, our overweight allocation to the defensive Health Care sector also helped returns. The Fund's two top performing stocks came from the Health Care sector, Endo Pharmaceutical and Cantel Medical. Endo Pharmaceutical specializes in pain management, and was purchased during the market sell-off in the fall. Cantel Medical, a niche medical device company, posted improvements in revenue, earnings and cash flows throughout the year, resulting in a 30% return for the Fund in the stock. Lastly, within the Financials sector, EZ Corp, an operator of pawn shops, returned 21%, as the recession and credit crisis led to increased demand for the company's services.

| Paradigm Intrinsic Value Fund Portfolio Performance |

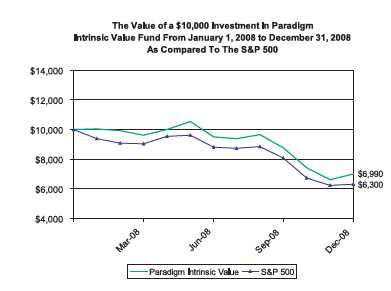

The Paradigm Intrinsic Value Fund declined 30.10% during 2008 (also the since inception period) compared to a 37.00% drop for its benchmark, the S&P 500 Index. The Fund's relative outperformance during 2008 was due to both stock selection and sector allocation, with investments in the Financial and Industrial sectors having the greatest impact on performance. Quanta Capital, a micro-cap special situation in the Financial sector, was the Fund's top performer, with a 60.3% positive return. Pacer International, in the Industrial sector, contributed a 33.67% return. Investments in gold and health-care also helped Fund performance this year.

The Consumer Discretionary sector was the largest relative detractor to Fund performance. Holdings like Coach and Phillips-Van Heusen were hit hard by the collapse in consumer spending this fall. Two investments in the Materials sector, RTI International and Innospec, also hurt performance, as the collapse in commodity prices and industrial production took its toll on these smaller capitalization, niche players.

2008 Annual Report 5

Paradigm Funds (Unaudited)

| PARADIGM VALUE FUND Sector Allocation (Unaudited) (As a Percentage of Equity Securities Held) |

| PARADIGM SELECT FUND Sector Allocation (Unaudited) (As a Percentage of Equity Securities Held) |

2008 Annual Report 6

Paradigm Funds (Unaudited)

PARADIGM OPPORTUNITY FUND

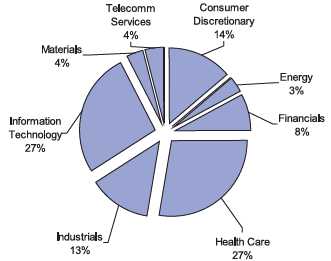

Sector Allocation (Unaudited)

(As a Percentage of Equity Securities Held)

PARADIGM INTRINSIC VALUE FUND

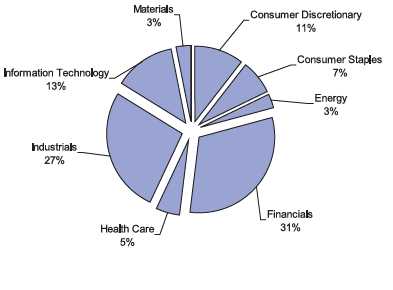

Sector Allocation (Unaudited)

(As a Percentage of Equity Securities Held)

2008 Annual Report 7

Paradigm Value Fund (Unaudited)

PERFORMANCE INFORMATION

Average Annual Rate of Return (%) for The Periods Ended December 31, 2008

December 31, 2008 NAV $32.51

| Since | ||||||||

| 1 Year(A) | 3 Years(A) | 5 Years(A) | Inception(A) | |||||

| Paradigm Value Fund | (33.88)% | (6.10)% | 5.51% | 13.18% | ||||

| Russell 2000 Value Index(B) | (28.92)% | (7.49)% | 0.27% | 6.75% |

(A)1 Year, 3 Years, 5 Years and Since Inception returns include change in share prices and in each case includes reinvestment of any dividends and capital gain distributions. The inception date of the Paradigm Value Fund was January 1, 2003.

(B)The Russell 2000® Value Index (whose composition is different from the Fund) is an unmanaged index of small-capitalization stocks with lower price-to-book ratios and lower forecasted growth values than the total population of small-capitalization stocks.

For purposes of the graph and the accompanying table, it is assumed that all dividends and distributions were reinvested.

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS. INVESTMENT RETURN AND PRINCIPAL VALUE WILL FLUCTUATE SO THAT SHARES, WHEN REDEEMED, MAY BE WORTH MORE OR LESS THAN THEIR ORIGINAL COST. RETURNS DO NOT REFLECT THE DEDUCTION OF TAXES THAT A SHAREHOLDER WOULD PAY ON FUND DISTRIBUTIONS OR THE REDEMPTION OF FUND SHARES. CURRENT PERFORMANCE MAY BE LOWER OR HIGHER THAT THE PERFORMANCE DATA QUOTED. TO OBTAIN PERFORMANCE DATA CURRENT TO THE MOST RECENT MONTH END, PLEASE CALL 1-800-239-0732 OR VISIT OUR WEBSITE AT www.paradigm-funds.com.

2008 Annual Report 8

Paradigm Select Fund (Unaudited)

PERFORMANCE INFORMATION

Average Annual Rate of Return (%) for The Periods Ended December 31, 2008

December 31, 2008 NAV $18.53

| Since | ||||||

| 1 Year(A) | 3 Year(A) | Inception(A) | ||||

| Paradigm Select Fund | (33.61)% | (5.16)% | (1.13)% | |||

| Russell 2500 Index(B) | (36.79)% | (9.37)% | (5.29)% |

(A)1 Year, 3 Year and Since Inception returns include change in share prices and in each case includes reinvestment of any dividends and capital gain distributions. The inception date of the Paradigm Select Fund was January 1, 2005.

(B)The Russell 2500® Index (whose composition is different from the Fund) measures the performance of the small to mid-cap segment of the U.S. equity universe, commonly referred to as "mid" cap. The Russell 2500 Index is a subset of the Russell 3000® Index. It includes approximately 2,500 of the smallest securities based on a combination of their market cap and current index membership.

For purposes of the graph and the accompanying table, it is assumed that all dividends and distributions were reinvested.

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS. INVESTMENT RETURN AND PRINCIPAL VALUE WILL FLUCTUATE SO THAT SHARES, WHEN REDEEMED, MAY BE WORTH MORE OR LESS THAN THEIR ORIGINAL COST. RETURNS DO NOT REFLECT THE DEDUCTION OF TAXES THAT A SHAREHOLDER WOULD PAY ON FUND DISTRIBUTIONS OR THE REDEMPTION OF FUND SHARES. CURRENT PERFORMANCE MAY BE LOWER OR HIGHER THAT THE PERFORMANCE DATA QUOTED. TO OBTAIN PERFORMANCE DATA CURRENT TO THE MOST RECENT MONTH END, PLEASE CALL 1-800-239-0732 OR VISIT OUR WEBSITE AT www.paradigm-funds.com.

2008 Annual Report 9

Paradigm Opportunity Fund (Unaudited)

PERFORMANCE INFORMATION

Average Annual Rate of Return (%) for The Periods Ended December 31, 2008

December 31, 2008 NAV $13.79

| Since | ||||||

| 1 Year(A) | 3 Year(A) | Inception(A) | ||||

| Paradigm Opportunity Fund | (39.89)% | (11.97)% | (7.43)% | |||

| Russell 2000 Index(B) | (33.79)% | (8.28)% | (5.23)% |

(A)1 Year, 3 Year and Since Inception returns include change in share prices and in each case includes reinvestment of any dividends and capital gain distributions. The inception date of the Paradigm Opportunity Fund was January 1, 2005.

(b)The Russell 2000® Index (whose composition is different from the Fund) consists of the smallest 2,000 companies in the Russell 3000 Index (which represents approximately 98% of the investable U.S. equity market). The Index is an unmanaged index generally considered as the premier of small capitalization stocks.

For purposes of the graph and the accompanying table, it is assumed that all dividends and distributions were reinvested.

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS. INVESTMENT RETURN AND PRINCIPAL VALUE WILL FLUCTUATE SO THAT SHARES, WHEN REDEEMED, MAY BE WORTH MORE OR LESS THAN THEIR ORIGINAL COST. RETURNS DO NOT REFLECT THE DEDUCTION OF TAXES THAT A SHAREHOLDER WOULD PAY ON FUND DISTRIBUTIONS OR THE REDEMPTION OF FUND SHARES. CURRENT PERFORMANCE MAY BE LOWER OR HIGHER THAT THE PERFORMANCE DATA QUOTED. TO OBTAIN PERFORMANCE DATA CURRENT TO THE MOST RECENT MONTH END, PLEASE CALL 1-800-239-0732 OR VISIT OUR WEBSITE AT www.paradigm-funds.com.

2008 Annual Report 10

Paradigm Intrinsic Value Fund (Unaudited)

PERFORMANCE INFORMATION

Average Annual Rate of Return (%) for The Period Ended December 31, 2008

December 31, 2008 NAV $13.98

| Since | ||

| Inception(A) | ||

| Paradigm Intrinsic Value Fund | (30.10)% | |

| S&P 500 Index(B) | (37.00)% |

(A)Since Inception returns include change in share prices and in each case includes reinvestment of any dividends and capital gain distributions. The inception date of the Paradigm Intrinsic Value Fund was January 1, 2008.

(B)The S&P 500® Index (whose composition is different from the Fund) is a managed index which measures the performance of 500 companies chosen by Standard & Poor’s to represent the large cap U.S. equity market.

For purposes of the graph and the accompanying table, it is assumed that all dividends and distributions were reinvested.

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS. INVESTMENT RETURN AND PRINCIPAL VALUE WILL FLUCTUATE SO THAT SHARES, WHEN REDEEMED, MAY BE WORTH MORE OR LESS THAN THEIR ORIGINAL COST. RETURNS DO NOT REFLECT THE DEDUCTION OF TAXES THAT A SHAREHOLDER WOULD PAY ON FUND DISTRIBUTIONS OR THE REDEMPTION OF FUND SHARES. CURRENT PERFORMANCE MAY BE LOWER OR HIGHER THAT THE PERFORMANCE DATA QUOTED. TO OBTAIN PERFORMANCE DATA CURRENT TO THE MOST RECENT MONTH END, PLEASE CALL 1-800-239-0732 OR VISIT OUR WEBSITE AT www.paradigm-funds.com.

2008 Annual Report 11

| Paradigm Value Fund | ||||||

| Schedule of Investments | ||||||

| December 31, 2008 | ||||||

| Shares/Principal Amount | Market Value | % of Net Assets | ||||

| COMMON STOCKS | ||||||

| Aircraft Part & Auxiliary Equipment | ||||||

| 98,000 | LMI Aerospace Inc. * | $ 1,114,260 | 1.31% | |||

| Apparel & Other Finished Products of Fabrics & Similar Materials | ||||||

| 136,200 | Volcom Inc. * | 1,484,580 | 1.75% | |||

| Canned, Frozen & Preserved Fruit, Vegetables & Food Specialties | ||||||

| 48,500 | Corn Products International Inc. | 1,399,225 | 1.65% | |||

| Carpets & Rugs | ||||||

| 170,300 | Interface Inc. Class A | 790,192 | 0.93% | |||

| Chemical & Allied Products | ||||||

| 45,600 | Arch Chemicals Inc. | 1,188,792 | ||||

| 108,500 | Innospec Inc. | 639,065 | ||||

| 1,827,857 | 2.15% | |||||

| Computer Services Software & Services | ||||||

| 142,350 | Aspen Technology Inc. * | 1,056,237 | 1.24% | |||

| Construction Machinery & Equipment | ||||||

| 64,600 | Columbus McKinnon Corp. * | 881,790 | 1.04% | |||

| Crude Petroleum & Natural Gas | ||||||

| 60,300 | St. Mary Land & Exploration Co. | 1,224,693 | ||||

| 23,400 | Swift Energy Co. * | 393,354 | ||||

| 32,800 | Whiting Petroleum Corp. * | 1,097,488 | ||||

| 2,715,535 | 3.19% | |||||

| Deep Sea Foreign Transportation of Freight | ||||||

| 17,400 | Seacor Holdings Inc. * | 1,159,710 | 1.36% | |||

| Drilling Oil & Gas Wells | ||||||

| 49,800 | Atwood Oceanics Inc. * | 760,944 | 0.90% | |||

| Electric Services | ||||||

| 67,600 | Portland General Electric Co. | 1,316,172 | 1.55% | |||

| Electrical Industrial Apparatus | ||||||

| 43,600 | Woodward Governor Co. | 1,003,672 | 1.18% | |||

| Electronic Components, NEC | ||||||

| 340,350 | Spectrum Control Inc. * | 2,089,749 | 2.46% | |||

| Fire, Marine & Casualty Insurance | ||||||

| 67,000 | American Financial Group Inc. | 1,532,960 | ||||

| 56,200 | Harleysville Group Inc. | 1,951,826 | ||||

| 3,484,786 | 4.10% | |||||

| Food and Kindred Products | ||||||

| 66,650 | Flowers Foods Inc. | 1,623,594 | 1.91% | |||

| Games, Toys & Children's Vehicles (No Dolls & Bicycles) | ||||||

| 53,500 | JAKKS Pacific Inc. * | 1,103,705 | 1.30% | |||

| Hospital & Medical Service Plans | ||||||

| 77,600 | Molina Healthcare Inc. * | 1,366,536 | 1.61% | |||

| In Vitro & In Vivo Diagnostic Substances | ||||||

| 177,000 | Trinity Biotech plc * ** | 283,200 | 0.33% | |||

| Industrial Instruments For Measurement, Display and Control | ||||||

| 8,730 | K-Tron International Inc. * | 697,527 | 0.82% | |||

| Industrial Organic Chemicals | ||||||

| 65,600 | Sensient Technologies Corp. | 1,566,528 | 1.84% | |||

| Laboratory Analytical Instruments | ||||||

| 49,800 | PerkinElmer Inc. | 692,718 | 0.81% | |||

| Life Insurance | ||||||

| 8,100 | National Western Life Insurance Co. | 1,370,277 | 1.61% | |||

| *Non-Income Producing Securities. **ADR - American Depository Receipt. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 12

Paradigm Value Fund | ||||||

| Schedule of Investments | ||||||

| December 31, 2008 | ||||||

| Shares/Principal Amount | Market Value | % of Net Assets | ||||

| COMMON STOCKS | ||||||

| Men's & Boy's Furnishings, Work Clothing & Allied Garments | ||||||

| 48,000 | Phillips-Van Heusen Corp. | $ 966,240 | 1.14% | |||

| Metal Cans | ||||||

| 45,400 | Silgan Holdings Inc. | 2,170,574 | 2.55% | |||

| Miscellaneous Industrial & Commercial Machinery & Equipment | ||||||

| 48,200 | Curtiss-Wright Corp. | 1,609,398 | 1.89% | |||

| Miscellaneous Chemical Products | ||||||

| 49,800 | WD-40 Co. | 1,408,842 | 1.66% | |||

| Motor Vehicle Parts & Accessories | ||||||

| 60,800 | Superior Industries International Inc. | 639,616 | 0.75% | |||

| Orthopedic, Prosthetic & Surgical Appliances & Supplies | ||||||

| 56,800 | Steris Corp. | 1,356,952 | 1.60% | |||

| Pharmaceutical Preparations | ||||||

| 119,400 | Endo Pharmaceuticals Holdings Inc. * | 3,090,072 | 3.63% | |||

| Railroads, Line-Haul Operating | ||||||

| 58,100 | Kansas City Southern * | 1,106,805 | 1.30% | |||

| Retail - Miscellaneous Retail | ||||||

| 108,100 | EZCORP Inc. * | 1,644,201 | 1.93% | |||

| Retail - Shoe Stores | ||||||

| 59,700 | Genesco Inc. * | 1,010,124 | 1.19% | |||

| Rolling, Drawing & Extruding of Nonferrous Metals | ||||||

| 66,600 | RTI International Metals Inc. * | 953,046 | 1.12% | |||

| Savings Institution, Federally Chartered | ||||||

| 105,600 | United Financial Bancorp | 1,598,784 | ||||

| 182,700 | Westfield Financial Inc. | 1,885,464 | ||||

| 3,484,248 | 4.10% | |||||

| Security Brokers, Dealers & Flotation Companies | ||||||

| 101,600 | Jefferies Group Inc. | 1,428,496 | ||||

| 43,900 | Piper Jaffray Companies * | 1,745,464 | ||||

| 3,173,960 | 3.73% | |||||

| Semiconductors & Related Devices | ||||||

| 33,300 | Cabot Microelectronics Corp. * | 868,131 | ||||

| 69,300 | Verigy, Ltd. * | 666,666 | ||||

| 1,534,797 | 1.81% | |||||

| Services - Business Services | ||||||

| 63,200 | Fair Isaac Corp. | 1,065,552 | ||||

| 174,100 | Premiere Global Services, Inc. * | 1,499,001 | ||||

| 2,564,553 | 3.02% | |||||

| Services - Computer Programming Services | ||||||

| 248,100 | Ness Technologies Inc. * ** | 1,061,868 | 1.25% | |||

| Services - Hospitals | ||||||

| 67,700 | Magellan Health Services Inc. * | 2,651,132 | ||||

| 88,400 | Rehabcare Group Inc. * | 1,340,144 | ||||

| 3,991,276 | 4.69% | |||||

| Services - Motion Picture Theaters | ||||||

| 165,500 | Regal Entertainment Group | 1,689,755 | 1.99% | |||

| Services - Prepackaged Software | ||||||

| 47,100 | ACI Worldwide, Inc. * | 748,890 | ||||

| 244,600 | Compuware Corp. * | 1,651,050 | ||||

| 69,800 | Sybase, Inc. * | 1,728,946 | ||||

| 4,128,886 | 4.86% | |||||

| *Non-Income Producing Securities. **ADR - American Depository Receipt. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 13

Paradigm Value Fund | ||||||

| Schedule of Investments | ||||||

| December 31, 2008 | ||||||

| Shares/Principal Amount | Market Value | % of Net Assets | ||||

| COMMON STOCKS | ||||||

| Sporting & Athletic Goods, NEC | ||||||

| 154,100 | Callaway Golf Co. | $ 1,431,589 | ||||

| 444,100 | Cybex International Inc. * | 817,144 | ||||

| 2,248,733 | 2.65% | |||||

| Surgical & Medical Instruments & Apparatus | ||||||

| 77,900 | Cantel Medical Corp. * | 1,142,793 | 1.34% | |||

| Telephone Communications | ||||||

| 84,000 | iBasis Inc. * | 118,440 | 0.14% | |||

| Water, Sewer, Pipeline, Comm & Power Line Construction | ||||||

| 16,936 | Preformed Line Products Co. | 779,734 | 0.92% | |||

| Wholesale - Machinery, Equipment & Supplies | ||||||

| 101,000 | Kaman Corp. | 1,831,130 | 2.14% | |||

| Total for Common Stock (Cost $93,489,185) | $ 73,494,837 | 86.44% | ||||

| REAL ESTATE INVESTMENT TRUSTS | ||||||

| 245,200 | Anworth Mortgage Asset Corp. | 1,576,636 | ||||

| 274,400 | MFA Mortgage Investments Inc. | 1,616,216 | ||||

| Total for Real Estate Investment Trusts (Cost $4,341,221) | 3,192,852 | 3.76% | ||||

| CORPORATE BONDS | ||||||

| 2,000,000 | Ciena Corp. (0.25% expires 5/1/2013) | 1,066,644 | ||||

| Total for Corporate Bonds (Cost $1,110,910) | 1,066,644 | 1.25% | ||||

| CASH EQUIVALENTS | ||||||

| 7,683,785 | SEI Daily Income Treasury Government CL B 1.41% *** | 7,683,785 | 9.04% | |||

| Total for Cash Equivalents (Cost $7,683,785) | ||||||

| Total Investment Securities | 85,438,118 | 100.49% | ||||

| (Cost $106,625,101) | ||||||

| Liabilities In Excess of Other Assets | (420,025) | -0.49% | ||||

| Net Assets | $ 85,018,093 | 100.00% | ||||

| *Non-Income Producing Securities. ***Variable Rate Security; the rate shown was the rate at December 31, 2008. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 14

Paradigm Select Fund | ||||||

| Schedule of Investments | ||||||

| December 31, 2008 | ||||||

| Shares/Principal Amount | Market Value | % of Net Assets | ||||

| COMMON STOCKS | ||||||

| Aircraft Part & Auxiliary Equipment, NEC | ||||||

| 400 | Rockwell Collins Inc. | $ 15,636 | 0.77% | |||

| Biological Products, (No Diagnostic Substances) | ||||||

| 1,700 | Life Technologies Corporation * | 39,627 | 1.95% | |||

| Canned, Fruits, Vegetables, Preserves, Jams & Jellies | ||||||

| 900 | The J. M. Smucker Company | 39,024 | 1.92% | |||

| Carpets & Rugs | ||||||

| 3,400 | Interface Inc. Class A | 15,776 | 0.78% | |||

| Chemical & Allied Products | ||||||

| 1,800 | Innospec Inc. | 10,602 | 0.52% | |||

| Computer Services Software & Services | ||||||

| 3,200 | Aspen Technology Inc. * | 23,744 | 1.17% | |||

| Crude Petroleum & Natural Gas | ||||||

| 900 | Denbury Resources Inc. * | 9,828 | ||||

| 1,100 | Plains Exploration & Production Company * | 25,564 | ||||

| 1,300 | St. Mary Land & Exploration Co. | 26,403 | ||||

| 800 | Whiting Petroleum Corp. * | 26,768 | ||||

| 88,563 | 4.36% | |||||

| Electric & Other Services Combined | ||||||

| 2,600 | CMS Energy Corp. | 26,286 | 1.29% | |||

| Electric Services | ||||||

| 3,500 | Dynegy Inc. * | 7,000 | ||||

| 1,900 | Portland General Electric Co. | 36,993 | ||||

| 43,993 | 2.17% | |||||

| Electrical Industrial Apparatus | ||||||

| 1,000 | Woodward Governor Co. | 23,020 | 1.13% | |||

| Fabricated Rubber Products | ||||||

| 1,000 | West Pharmaceutical Services, Inc. | 37,770 | 1.86% | |||

| Fire, Marine & Casualty Insurance | ||||||

| 261 | Alleghany Inc. * | 73,602 | ||||

| 2,000 | American Financial Group Inc. | 45,760 | ||||

| 400 | Everest Re Group Ltd. ** | 30,456 | ||||

| 1,700 | Harleysville Group Inc. | 59,041 | ||||

| 150 | Markel Corp. * | 44,850 | ||||

| 253,709 | 12.49% | |||||

| Food & Kindred Products | ||||||

| 1,575 | Flowers Foods Inc. | 38,367 | 1.89% | |||

| Guided Missiles & Space Vehicles & Parts | ||||||

| 500 | Alliant Techsystems Inc. * | 42,880 | 2.11% | |||

| Insurance Agents, Brokers & Service | ||||||

| 1,700 | Arthur J Gallagher & Co. | 44,047 | 2.17% | |||

| Iron & Steel Foundries | ||||||

| 300 | Precision Castparts Corp. | 17,844 | 0.88% | |||

| Laboratory Analytical Instruments | ||||||

| 2,348 | PerkinElmer Inc. | 32,661 | 1.61% | |||

| Life Insurance | ||||||

| 148 | National Western Life Insurance Co. | 25,037 | 1.23% | |||

| Meat Packing Plants | ||||||

| 1,100 | Hormel Foods Corp. | 34,188 | 1.68% | |||

| Men's & Boy's Furnishings, Work Clothing & Allied Garments | ||||||

| 1,580 | Phillips-Van Heusen Corp. | 31,805 | 1.57% | |||

| Metal Cans | ||||||

| 1,600 | Crown Holdings Inc. * | 30,720 | 1.51% | |||

| *Non-Income Producing Securities. **ADR - American Depository Receipt. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 15

| Paradigm Select Fund | ||||||

| Schedule of Investments | ||||||

| December 31, 2008 | ||||||

| Shares/Principal Amount | Market Value | % of Net Assets | ||||

| COMMON STOCKS | ||||||

| Miscellaneous Industrial & Commercial Machinery & Equipment | ||||||

| 1,100 | Curtiss-Wright Corp. | $ 36,729 | 1.81% | |||

| Orthopedic, Prosthetic & Surgical Appliances & Supplies | ||||||

| 1,300 | Steris Corp. | 31,057 | 1.53% | |||

| Pharmaceutical Preparations | ||||||

| 2,600 | Endo Pharmaceuticals Holdings Inc. * | 67,288 | 3.31% | |||

| Plastics Products | ||||||

| 1,100 | AptarGroup Inc. | 38,764 | 1.91% | |||

| Pumps & Pumping Equipment | ||||||

| 900 | Robbins & Myers Inc. | 14,553 | 0.72% | |||

| Radiotelephone Communications | ||||||

| 1,100 | Telephone & Data Systems Inc. | 30,910 | 1.52% | |||

| Railroad, Line-Haul Operating | ||||||

| 1,348 | Kansas City Southern * | 25,679 | 1.26% | |||

| Retail - Retail Stores | ||||||

| 1,300 | Petsmart Inc. | 23,985 | 1.18% | |||

| Secondary Selting & Refining of Nonferrous Metals | ||||||

| 1,600 | Titanium Metals Corp. | 14,096 | 0.70% | |||

| Security & Commodity Brokers, Dealers, Exchanges & Services | ||||||

| 2,000 | Interactive Data Corporation | 49,320 | 2.43% | |||

| Security Brokers, Dealers & Flotation Companies | ||||||

| 2,300 | Jefferies Group Inc. | 32,338 | ||||

| 1,100 | Piper Jaffray Companies * | 43,736 | ||||

| 76,074 | 3.75% | |||||

| Semiconductors & Related Devices | ||||||

| 1,000 | Cabot Microelectronics Corp. * | 26,070 | ||||

| 1,600 | Verigy, Ltd. * ** | 15,392 | ||||

| 41,462 | 2.04% | |||||

| Services - Business Services | ||||||

| 1,500 | Fair Isaac Corp. | 25,290 | ||||

| 3,800 | Premiere Global Services Inc. * | 32,718 | ||||

| 58,008 | 2.86% | |||||

| Services - Computer Integrated Systems Design | ||||||

| 2,800 | Convergys Corp. * | 17,948 | 0.88% | |||

| Services - Hospitals | ||||||

| 1,300 | Magellan Health Services Inc. * | 50,908 | 2.51% | |||

| Services - Miscellaneous Health & Allied Services, NEC | ||||||

| 1,200 | Lincare Holdings Inc. * | 32,316 | 1.59% | |||

| Services - Motion Picture Theaters | ||||||

| 3,000 | Regal Entertainment Group | 30,630 | 1.51% | |||

| Services - Prepackaged Software | ||||||

| 5,300 | Compuware Corp. * | 35,775 | ||||

| 1,700 | Sybase, Inc. * | 42,109 | ||||

| 77,884 | 3.83% | |||||

| Soap, Detergents, Cleaning Preparations, Perfumes, Cosmetics | ||||||

| 700 | Church & Dwight Co., Inc. | 39,284 | 1.93% | |||

| Special Industry Machinery (No Metalworking Machinery) | ||||||

| 800 | Pentair Inc. | 18,936 | 0.93% | |||

| Sporting & Athletic Goods, NEC | ||||||

| 3,400 | Callaway Golf Co. | 31,586 | 1.56% | |||

| State Commercial Banks | ||||||

| 800 | Wilmington Trust Corporation | 17,792 | 0.88% | |||

| *Non-Income Producing Securities. **ADR - American Depository Receipt. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 16

Paradigm Select Fund | ||||||

| Schedule of Investments | ||||||

| December 31, 2008 | ||||||

| Shares/Principal Amount | Market Value | % of Net Assets | ||||

| COMMON STOCKS | ||||||

| Water Transportation | ||||||

| 1,000 | Alexander & Baldwin Inc. | $ 25,060 | 1.23% | |||

| Wholesale - Electronic Parts & Equipment | ||||||

| 2,200 | Avnet Inc. * | 40,062 | 1.97% | |||

| Total for Common Stock (Cost $2,056,351) | $ 1,805,630 | 88.90% | ||||

| REAL ESTATE INVESTMENT TRUSTS | ||||||

| 7,700 | Anworth Mortgage Asset Corp. | 49,511 | ||||

| 6,600 | MFA Mortgage Investments Inc. | 38,874 | ||||

| Total for Real Estate Investment Trusts (Cost $98,976) | 88,385 | 4.36% | ||||

| CASH EQUIVALENTS | ||||||

| 327,459 | SEI Daily Income Treasury Government CL B 1.41% *** | 327,459 | 16.12% | |||

| Total for Cash Equivalents (Cost $327,459) | ||||||

| Total Investment Securities | 2,221,474 | 109.38% | ||||

(Cost $2,482,786) | ||||||

| Liabilities In Excess of Other Assets | (190,441) | -9.38% | ||||

| Net Assets�� | $ 2,031,033 | 100.00% | ||||

| *Non-Income Producing Securities. ***Variable Rate Security; the rate shown was the rate at December 31, 2008. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 17

Paradigm Opportunity Fund | ||||||

| Schedule of Investments | ||||||

| December 31, 2008 | ||||||

| Shares/Principal Amount | Market Value | % of Net Assets | ||||

| COMMON STOCKS | ||||||

| Aircraft Parts & Auxiliary Equipment | ||||||

| 7,400 | LMI Aerospace Inc. * | $ 84,138 | 3.47% | |||

| Apparel & Other Finished Products of Fabrics & Similar Materials | ||||||

| 7,600 | Volcom Inc. * | 82,840 | 3.42% | |||

| Biological Products, (No Diagnostic Substances) | ||||||

| 3,200 | Life Technologies Corporation * | 74,592 | 3.08% | |||

| Carpets & Rugs | ||||||

| 14,800 | Interface Inc. Class A | 68,672 | 2.83% | |||

| Computer Services Software | ||||||

| 12,300 | Aspen Technology Inc. * | 91,266 | 3.76% | |||

| Construction Machinery & Equipment | ||||||

| 6,300 | Columbus Mckinnon Corp. * | 85,995 | 3.55% | |||

| Crude Petroleum & Natural Gas | ||||||

| 3,800 | St. Mary Land & Exploration Co. | 77,178 | 3.18% | |||

| Electronic Components, NEC | ||||||

| 19,900 | Spectrum Control Inc. * | 122,186 | 5.04% | |||

| Hospital & Medical Service Plans | ||||||

| 4,100 | Molina Healthcare Inc. * | 72,201 | 2.98% | |||

| In Vitro & In Vivo Diagnostic Substances | ||||||

| 17,200 | Trinity Biotech plc * ** | 27,520 | 1.13% | |||

| Laboratory Analytical Instruments | ||||||

| 5,300 | PerkinElmer Inc. | 73,723 | 3.04% | |||

| Metal Cans | ||||||

| 4,500 | Crown Holdings Inc. * | 86,400 | 3.56% | |||

| Orthopedic, Prosthetic & Surgical Appliances & Supplies | ||||||

| 3,100 | Steris Corp. | 74,059 | 3.05% | |||

| Pharmaceutical Preparations | ||||||

| 5,900 | Endo Pharmaceuticals Holdings Inc. * | 152,692 | 6.30% | |||

| Retail - Miscellaneous Retail | ||||||

| 6,300 | EZCORP Inc. * | 95,823 | 3.95% | |||

| Services - Business Services | ||||||

| 10,200 | Premiere Global Services Inc. * | 87,822 | 3.62% | |||

| Services - Computer Programming Services | ||||||

| 16,500 | Ness Technologies Inc. * ** | 70,620 | 2.91% | |||

| Services - Hospitals | ||||||

| 2,300 | Magellan Health Services Inc. * | 90,068 | 3.71% | |||

| Services - Motion Picture Theaters | ||||||

| 8,200 | Regal Entertainment Group | 83,722 | 3.45% | |||

| Service - Prepackaged Software | ||||||

| 5,200 | ACI Worldwide, Inc. * | 82,680 | ||||

| 12,400 | Compuware Corp. * | 83,700 | ||||

| 6,600 | Parametric Technology Corp. * | 83,490 | ||||

| 3,600 | Sybase, Inc. * | 89,172 | ||||

| 339,042 | 13.98% | |||||

| Sporting & Athletic Goods, NEC | ||||||

| 8,100 | Callaway Golf Co. | 75,249 | ||||

| 44,100 | Cybex International Inc. * | 81,144 | ||||

| 156,393 | 6.45% | |||||

| Surgical & Medical Instruments & Apparatus | ||||||

| 5,100 | Cantel Medical Corp. * | 74,817 | 3.09% | |||

| *Non-Income Producing Securities. **ADR - American Depository Receipt. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 18

Paradigm Opportunity Fund | ||||

| Schedule of Investments | ||||

| December 31, 2008 | ||||

| Shares/Principal Amount | Market Value | % of Net Assets | ||

| COMMON STOCKS | ||||

| Wholesale - Machinery, Equipment & Supplies | ||||

| 4,000 Kaman Corp. | $ 72,520 | 2.99% | ||

| Total for Common Stock (Cost $3,044,315) | $ 2,244,289 | 92.54% | ||

| REAL ESTATE INVESTMENT TRUSTS | ||||

| 14,400 MFA Mortgage Investments Inc. | 84,816 | 3.50% | ||

| Total for Real Estate Investment Trusts (Cost $80,826) | ||||

| CASH EQUIVALENTS | ||||

| 162,579 SEI Daily Income Treasury Government CL B 1.41% *** | 162,579 | 6.71% | ||

| Total for Cash Equivalents (Cost $162,579) | ||||

| Total Investment Securities | 2,491,684 | 102.75% | ||

| (Cost $3,287,720) | ||||

| Liabilities In Excess of Other Assets | (66,592) | -2.75% | ||

| Net Assets | $ 2,425,092 | 100.00% | ||

| ***Variable Rate Security; the rate shown was the rate at December 31, 2008. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 19

| Paradigm Intrinsic Value Fund | ||||||

| Schedule of Investments | ||||||

| December 31, 2008 | ||||||

| Shares/Principal Amount | Market Value | % of Net Assets | ||||

| COMMON STOCKS | ||||||

| Apparel & Other Finished Products of Fabrics & Similar Materials | ||||||

| 2,780 | Volcom Inc. * | $ 30,302 | 1.87% | |||

| Beverages | ||||||

| 725 | Dr Pepper Snapple Group, Inc. * | 11,781 | ||||

| 655 | Pepsico, Inc. | 35,874 | ||||

| 47,655 | 2.94% | |||||

| Chemicals & Allied Products | ||||||

| 5,845 | Innospec Inc. | 34,427 | 2.13% | |||

| Crude Petroleum & Natural Gas | ||||||

| 245 | EnCana Corp. | 11,388 | ||||

| 570 | Plains Exploration & Production Company * | 13,247 | ||||

| 420 | Whiting Petroleum Corp. * | 14,053 | ||||

| 38,688 | 2.39% | |||||

| Engines & Turbines | ||||||

| 890 | Cummins Inc. | 23,790 | 1.47% | |||

| Fire, Marine & Casualty Insurance | ||||||

| 3,950 | American Financial Group Inc. | 90,376 | ||||

| 11 | Berkshire Hathaway Inc. Class B * | 35,354 | ||||

| 125,730 | 7.76% | |||||

| Food and Kindred Products | ||||||

| 1,547 | Nestle SA ** | 61,416 | 3.79% | |||

| Guided Missiles & Space Vehicles & Parts | ||||||

| 435 | Alliant Techsystems Inc. * | 37,306 | 2.30% | |||

| Insurance Agents, Brokers & Service | ||||||

| 2,640 | Marsh & McLennan Companies, Inc. | 64,073 | 3.96% | |||

| Iron & Steel Foundries | ||||||

| 550 | Precision Castparts Corp. | 32,714 | 2.02% | |||

| Leather & Leather Products | ||||||

| 2,655 | Coach Inc. * | 55,144 | 3.40% | |||

| Men's & Boys' Furnishings, Work Clothing, and Allied Garments | ||||||

| 1,915 | Phillips-Van Heusen Corp. | 38,549 | 2.38% | |||

| Misccellaneous Industrial & Commercial Machinery & Equipment | ||||||

| 1,295 | Curtiss-Wright Corp. | 43,240 | 2.67% | |||

| Miscellaneous Fabricated Metal Products | ||||||

| 2,010 | Crane Co. | 34,652 | ||||

| 1,525 | Parker Hannifin Corporation | 64,874 | ||||

| 99,526 | 6.14% | |||||

| National Commercial Banks | ||||||

| 1,510 | Bank of America Corporation | 21,261 | 1.31% | |||

| Newspapers: Publishing or Publishing & Printing | ||||||

| 3,660 | News Corp. | 33,269 | 2.05% | |||

| Petroleum Refining | ||||||

| 195 | ConocoPhillips | 10,101 | 0.62% | |||

| Pharmaceutical Preparations | ||||||

| 1,100 | Endo Pharmaceuticals Holdings Inc. * | 28,468 | 1.76% | |||

| Railroads, Line-Haul Operating | ||||||

| 910 | Canadian National Railway Company | 33,452 | 2.07% | |||

| Rolling Drawing & Extruding of Nonferrous Metals | ||||||

| 820 | RTI International Metals Inc. * | 11,734 | 0.72% | |||

| Security Brokers, Dealers & Flotation Companies | ||||||

| 415 | Goldman Sachs Group Inc. | 35,022 | ||||

| 2,250 | Jefferies Group Inc. | 31,635 | ||||

| 840 | Morgan Stanley | 13,474 | ||||

| 80,131 | 4.95% | |||||

| *Non-Income Producing Securities. **ADR - American Depository Receipt. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 20

Paradigm Intrinsic Value Fund | ||||||

| Schedule of Investments | ||||||

| December 31, 2008 | ||||||

| Shares/Principal Amount | Market Value | % of Net Assets | ||||

| COMMON STOCKS | ||||||

| Semiconductors & Related Devices | ||||||

| 1,955 | Applied Materials Inc. | $ 19,804 | 1.22% | |||

| Services - Business Services | ||||||

| 990 | Fair Isaac Corp. | 16,691 | 1.03% | |||

| Services - Hospitals | ||||||

| 1,135 | Magellan Health Services Inc. * | 44,447 | 2.75% | |||

| Service - Prepackaged Software | ||||||

| 5,995 | Compuware Corp. * | 40,466 | 2.50% | |||

| Ship & Boat Building & Repairing | ||||||

| 1,055 | General Dynamics Corp. | 60,758 | 3.75% | |||

| Special Industry Machinery, NEC | ||||||

| 870 | Cymer Inc. * | 19,062 | ||||

| 1,220 | Varian Semiconductor Equipment Associates Inc. * | 22,106 | ||||

| 41,168 | 2.54% | |||||

| State Commercial Banks | ||||||

| 1,480 | The Bank of New York Mellon Corporation | 41,928 | 2.59% | |||

| Wholesale - Electronic Parts & Equipment, NEC | ||||||

| 4,240 | Avnet Inc. * | 77,210 | 4.77% | |||

| Total for Common Stock (Cost $1,766,092) | $ 1,293,448 | 79.85% | ||||

| REAL ESTATE INVESTMENT TRUSTS | ||||||

| 10,650 | Anworth Mortgage Asset Corp. | 68,480 | ||||

| 10,725 | MFA Mortgage Investments Inc. | 63,170 | ||||

| Total for Real Estate Investment Trusts (Cost - $144,963) | 131,650 | 8.13% | ||||

| EXCHANGE TRADED FUNDS | ||||||

| 870 | iShares COMEX Gold Trust * | 75,394 | ||||

| Total for Exchange Traded Funds (Cost - $71,558) | 75,394 | 4.65% | ||||

| CASH EQUIVALENTS | ||||||

| 117,673 | SEI Daily Income Treasury Government CL B 1.41% *** | 117,673 | 7.26% | |||

| Total for Cash Equivalents (Cost $117,673) | ||||||

| Total Investment Securities | 1,618,165 | 99.89% | ||||

(Cost $2,100,286) | ||||||

| Other Assets In Excess of Liabilities | 1,712 | 0.11% | ||||

| Net Assets | $ 1,619,877 | 100.00% | ||||

| *Non-Income Producing Securities. ***Variable Rate Security; the rate shown was the rate at December 31, 2008. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 21

Paradigm Funds | ||||

| Statements of Assets and Liabilities | Value | Select | ||

| December 31, 2008 | Fund | Fund | ||

| Assets: | ||||

| Investment Securities at Market Value* | $ 85,438,118 | $ 2,221,474 | ||

| Receivable for Securities Sold | 119,883 | 708,943 | ||

| Receivable for Fund Shares Sold | 236,322 | - | ||

| Dividend Receivable | 107,632 | 4,342 | ||

| Interest Receivable | 8,420 | 301 | ||

| Total Assets | 85,910,375 | 2,935,060 | ||

| Liabilities: | ||||

| Payable for Securities Purchased | 188,532 | - | ||

| Payable for Fund Shares Redeemed | 551,770 | 900,198 | ||

| Payable to Advisor | 151,980 | 3,829 | ||

| Total Liabilities | 892,282 | 904,027 | ||

| Net Assets | $ 85,018,093 | $ 2,031,033 | ||

| Net Assets Consist of: | ||||

| Paid In Capital | $ 120,477,310 | $ 2,702,048 | ||

| Accumulated Undistributed Net Investment Income | - | 7,832 | ||

| Accumulated Undistributed Realized Gain (Loss) on Investments - Net | (14,272,234) | (417,535) | ||

| Unrealized Appreciation (Depreciation) in Value of Investments Securities - Net | (21,186,983) | (261,312) | ||

| Net Assets | $ 85,018,093 | $ 2,031,033 | ||

| Net Asset Value and Offering Price (Note 2) | $ 32.51 | $ 18.53 | ||

| * Investments at Identified Cost | $ 106,625,101 | $ 2,482,786 | ||

| Shares Outstanding (Unlimited number of shares | 2,615,172 | 109,606 | ||

| authorized without par value) | ||||

| Statements of Operations | ||||

| For year ended December 31, 2008 | ||||

| Investment Income: | ||||

| Dividends | $ 1,378,222 | $ 93,157 | ||

| Interest | 244,257 | 6,404 | ||

| Total Investment Income | 1,622,479 | 99,561 | ||

| Expenses: | ||||

| Investment Advisor Fees | 2,201,843 | 91,729 | ||

| Interest Expense | 2,352 | - | ||

| Total Expenses | 2,204,195 | 91,729 | ||

| Net Expenses | 2,204,195 | 91,729 | ||

| Net Investment Income (Loss) | (581,716) | 7,832 | ||

| Realized and Unrealized Gain (Loss) on Investments: | ||||

| Net Realized Gain (Loss) on Investments | (14,224,732) | (410,099) | ||

| Net Change in Unrealized Appreciation (Depreciation) on Investments | (30,472,841) | (1,584,796) | ||

| Net Realized and Unrealized Gain (Loss) on Investments | (44,697,573) | (1,994,895) | ||

| Net Increase (Decrease) in Net Assets from Operations | $ (45,279,289) | $ (1,987,063) | ||

| The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 22

Paradigm Funds | ||||

| Statements of Assets and Liabilities | Opportunity | Intrinsic Value | ||

| December 31, 2008 | Fund | Fund | ||

| Assets: | ||||

| Investment Securities at Market Value* | $ 2,491,684 | $ 1,618,165 | ||

| Dividend Receivable | 560 | 3,309 | ||

| Interest Receivable | 93 | 125 | ||

| Total Assets | 2,492,337 | 1,621,599 | ||

| Liabilities: | ||||

| Payable for Securities Purchased | 64,093 | - | ||

| Payable to Advisor | 3,152 | 1,722 | ||

| Total Liabilities | 67,245 | 1,722 | ||

| Net Assets | $ 2,425,092 | $ 1,619,877 | ||

| Net Assets Consist of: | ||||

| Paid In Capital | $ 3,951,256 | $ 2,319,949 | ||

| Accumulated Undistributed Net Investment Income | - | 15,123 | ||

| Accumulated Undistributed Realized Gain (Loss) on Investments - Net | (730,128) | (233,074) | ||

| Unrealized Appreciation (Depreciation) in Value of Investments Securities - Net | (796,036) | (482,121) | ||

| Net Assets | $ 2,425,092 | $ 1,619,877 | ||

| Net Asset Value and Offering Price (Note 2) | $ 13.79 | $ 13.98 | ||

| * Investments at Identified Cost | $ 3,287,720 | $ 2,100,286 | ||

| Shares Outstanding (Unlimited number of shares | 175,818 | 115,861 | ||

| authorized without par value) | ||||

| Statements of Operations | ||||

| For year ended December 31, 2008 | ||||

| Investment Income: | ||||

| Dividends (Net of foreign withholding tax and fees of $0 and $303, respectively) | $ 27,918 | $ 26,258 | ||

| Interest | 4,209 | 10,722 | ||

| Total Investment Income | 32,127 | 36,980 | ||

| Expenses: | ||||

| Investment Advisor Fees | 76,853 | 21,857 | ||

| Total Expenses | 76,853 | 21,857 | ||

| Less: Expenses Waived | (19,213) | - | ||

| Net Expenses | 57,640 | 21,857 | ||

| Net Investment Income (Loss) | (25,513) | 15,123 | ||

| Realized and Unrealized Gain (Loss) on Investments: | ||||

| Net Realized Gain (Loss) on Investments | (728,182) | (233,074) | ||

| Net Change in Unrealized Appreciation (Depreciation) on Investments | (1,000,597) | (482,121) | ||

| Net Realized and Unrealized Gain (Loss) on Investments | (1,728,779) | (715,195) | ||

| Net Decrease in Net Assets from Operations | $ (1,754,292) | $ (700,072) | ||

| The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 23

Paradigm Funds | ||||||||

| Statements of Changes in Net Assets | Value Fund | Select Fund | ||||||

| 1/1/2008 | 1/1/2007 | 1/1/2008 | 1/1/2007 | |||||

| to | to | to | to | |||||

| 12/31/2008 | 12/31/2007 | 12/31/2008 | 12/31/2007 | |||||

| From Operations: | ||||||||

| Net Investment Income (Loss) | $ (581,716) | $ (785,187) | $ 7,832 | $ (25,547) | ||||

| Net Realized Gain (Loss) on Investments and Short Positions | (14,224,732) | 4,153,214 | (410,099) | 17,379 | ||||

| Change in Net Unrealized Appreciation (Depreciation) | (30,472,841) | (459,174) | (1,584,796) | 565,965 | ||||

| Increase (Decrease) in Net Assets from Operations | (45,279,289) | 2,908,853 | (1,987,063) | 557,797 | ||||

| From Distributions to Shareholders: | ||||||||

| Net Investment Income | - | - | - | - | ||||

| Net Realized Gain from Security Transactions | (174,123) | (3,925,744) | - | (17,970) | ||||

| Total Distributions to Shareholders | (174,123) | (3,925,744) | - | (17,970) | ||||

| From Capital Share Transactions: | ||||||||

| Proceeds From Sale of Shares | 64,736,515 | 100,524,715 | 237,464 | 5,370,689 | ||||

| Proceeds from Redemption Fees (Note 2) | 118,899 | 27,242 | - | - | ||||

| Shares Issued on Reinvestment of Dividends | 171,705 | 3,867,545 | - | 17,970 | ||||

| Cost of Shares Redeemed | (50,802,151) | (43,898,992) | (7,328,411) | (1,493,447) | ||||

| Net Increase (Decrease) from Shareholder Activity | 14,224,968 | 60,520,510 | (7,090,947) | 3,895,212 | ||||

| Net Increase (Decrease) in Net Assets | (31,228,444) | 59,503,619 | (9,078,010) | 4,435,039 | ||||

| Net Assets at Beginning of Period | 116,246,537 | 56,742,918 | 11,109,043 | 6,674,004 | ||||

| Net Assets at End of Period | $ 85,018,093 | $ 116,246,537 | $ 2,031,033 | $ 11,109,043 | ||||

| Accumulated Undistributed Net Investment Income | $ - | $ - | $ 7,832 | $ - | ||||

| Share Transactions: | ||||||||

| Issued | 1,523,593 | 1,967,239 | 9,419 | 199,502 | ||||

| Reinvested | 5,425 | 78,195 | - | 638 | ||||

| Redeemed | (1,273,065) | (854,854) | (297,807) | (54,151) | ||||

| Net Increase (Decrease) in Shares | 255,953 | 1,190,580 | (288,388) | 145,989 | ||||

| Shares Outstanding Beginning of Period | 2,359,219 | 1,168,639 | 397,994 | 252,005 | ||||

| Shares Outstanding End of Period | 2,615,172 | 2,359,219 | 109,606 | 397,994 | ||||

| The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 24

| Paradigm Funds | ||||||

| Statements of Changes in Net Assets | Opportunity Fund | Intrinsic Value | ||||

| 1/1/2008 | 1/1/2007 | 1/1/2008* | ||||

| to | to | to | ||||

| 12/31/2008 | 12/31/2007 | 12/31/2008 | ||||

| From Operations: | ||||||

| Net Investment Income (Loss) | $ (25,513) | $ (9,582) | $ 15,123 | |||

| Net Realized Gain (Loss) on Investments | (728,182) | 167,757 | (233,074) | |||

| Change in Net Unrealized Appreciation (Depreciation) | (1,000,597) | (204,857) | (482,121) | |||

| Increase (Decrease) in Net Assets from Operations | (1,754,292) | (46,682) | (700,072) | |||

| From Distributions to Shareholders: | ||||||

| Net Investment Income | - | - | - | |||

| Net Realized Gain from Security Transactions | - | (166,837) | - | |||

| Total Distributions to Shareholders | - | (166,837) | - | |||

| From Capital Share Transactions: | ||||||

| Proceeds From Sale of Shares | 48,186 | 2,073,387 | 2,336,408 | |||

| Proceeds from Redemption Fees (Note 2) | 385 | - | - | |||

| Shares Issued on Reinvestment of Dividends | - | 166,837 | - | |||

| Cost of Shares Redeemed | (1,481,767) | (132,952) | (16,459) | |||

| Net Increase (Decrease) from Shareholder Activity | (1,433,196) | 2,107,272 | 2,319,949 | |||

| Net Increase (Decrease) in Net Assets | (3,187,488) | 1,893,753 | 1,619,877 | |||

| Net Assets at Beginning of Period | 5,612,580 | 3,718,827 | - | |||

| Net Assets at End of Period | $ 2,425,092 | $ 5,612,580 | $ 1,619,877 | |||

| Accumulated Undistributed Net Investment Income | $ - | $ - | $ 15,123 | |||

| Share Transactions: | ||||||

| Issued | 2,364 | 82,592 | 116,689 | |||

| Reinvested | - | 7,238 | - | |||

| Redeemed | (71,262) | (5,324) | (828) | |||

| Net Increase (Decrease) in Shares | (68,898) | 84,506 | 115,861 | |||

| Shares Outstanding Beginning of Period | 244,716 | 160,210 | - | |||

| Shares Outstanding End of Period | 175,818 | 244,716 | 115,861 | |||

| *Commencement of operations. The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 25

Paradigm Value Fund | ||||||||||

| Financial Highlights - Paradigm Value Fund | ||||||||||

| Selected data for a share outstanding | 1/1/2008 | 1/1/2007 | 1/1/2006 | 1/1/2005 | 1/1/2004 | |||||

| throughout the period: | to | to | to | to | to | |||||

| 12/31/2008 | 12/31/2007 | 12/31/2006 | 12/31/2005 | 12/31/2004 | ||||||

| Net Asset Value - Beginning of Period | $ 49.27 | $ 48.55 | $ 42.90 | $ 37.51 | $ 28.83 | |||||

| Net Investment Loss ** | (0.22) | (0.40) | (0.47) | (0.40) | (0.44) | |||||

| Net Gains (Loss) on Securities (realized and unrealized) | (16.52) | 2.84 | 8.69 | 7.75 | 9.69 | |||||

| Total from Investment Operations | (16.74) | 2.44 | 8.22 | 7.35 | 9.25 | |||||

| Distributions (From Net Investment Income) | - | - | - | - | - | |||||

| Distributions (From Capital Gains) | (0.07) | (1.73) | (2.58) | (1.96) | (0.57) | |||||

| Total Distributions | (0.07) | (1.73) | (2.58) | (1.96) | (0.57) | |||||

| Proceeds from Redemption Fee (Note 2) | 0.05 | 0.01 | 0.01 | - | - | |||||

| Net Asset Value - End of Period | $ 32.51 | $ 49.27 | $ 48.55 | $ 42.90 | $ 37.51 | |||||

| Total Return *** | (33.88)% | 5.03% | 19.19% | 19.61% | 32.09% | |||||

| Ratios/Supplemental Data | ||||||||||

| Net Assets - End of Period (Thousands) | $ 85,018 | $ 116,247 | $ 56,743 | $ 24,002 | $ 14,528 | |||||

| Ratio of Expenses to Average Net Assets, | ||||||||||

| Excluding Dividends on Securities Sold Short | ||||||||||

| and Interest Expense | 1.99% | 2.00% | 2.00% | 2.00% | 1.99% | |||||

| Ratio of Dividend Expense on Securities Sold Short | ||||||||||

| and Interest Expense to Average Net Assets | 0.00% | + | 0.02% | 0.02% | 0.06% | 0.04% | ||||

| Ratio of Expenses to Average Net Assets | 1.99% | 2.02% | 2.02% | 2.06% | 2.03% | |||||

| Ratio of Net Investment Loss to Average Net Assets | -0.52% | -0.78% | -1.02% | -0.98% | -1.34% | |||||

| Portfolio Turnover Rate | 67.84% | 59.75% | 69.95% | 67.39% | 91.66% | |||||

| Paradigm Select Fund | ||||||||

| Financial Highlights - Paradigm Select Fund | ||||||||

| Selected data for a share outstanding throughout the period: | 1/1/2008 | 1/1/2007 | 1/1/2006 | 1/1/2005* | ||||

| to | to | to | to | |||||

| 12/31/2008 | 12/31/2007 | 12/31/2006 | 12/31/2005 | |||||

| Net Asset Value - Beginning of Period | $ 27.91 | $ 26.48 | $ 22.33 | $ 20.00 | ||||

| Net Investment Loss ** | 0.03 | (0.06) | (0.08) | (0.08) | ||||

| Net Gains (Loss) on Securities (realized and unrealized) | (9.41) | 1.54 | 4.92 | 2.49 | ||||

| Total from Investment Operations | (9.38) | 1.48 | 4.84 | 2.41 | ||||

| Distributions (From Net Investment Income) | - | - | - | - | ||||

| Distributions (From Capital Gains) | - | (0.05) | (0.69) | (0.08) | ||||

| Total Distributions | $ - | (0.05) | (0.69) | (0.08) | ||||

| Proceeds from Redemption Fee (Note 2) | - | - | - | - | ||||

| Net Asset Value - End of Period | $ 18.53 | $ 27.91 | $ 26.48 | $ 22.33 | ||||

| Total Return *** | (33.61)% | 5.57% | 21.67% | 12.06% | ||||

| Ratios/Supplemental Data | ||||||||

| Net Assets - End of Period (Thousands) | $ 2,031 | $ 11,109 | $ 6,674 | $ 2,521 | ||||

| Ratio of Expenses to Average Net Assets | 1.50% | 1.50% | 1.50% | 1.50% | ||||

| Ratio of Net Investment Loss to Average Net Assets | 0.13% | -0.23% | -0.30% | -0.36% | ||||

| Portfolio Turnover Rate | 47.71% | 64.68% | 72.15% | 68.56% | ||||

| * Commencement of operations. ** Per share amount calculated using the average shares method. *** Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund assuming reinvestment of dividends. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or redemption of Fund shares. + Amount calculated is less than 0.005% . |

| The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 26

Paradigm Opportunity Fund | ||||||||

| Financial Highlights - Paradigm Opportunity Fund | ||||||||

| Selected data for a share outstanding throughout the period: | 1/1/2008 | 1/1/2007 | 1/1/2006 | 1/1/2005* | ||||

| to | to | to | to | |||||

| 12/31/2008 | 12/31/2007 | 12/31/2006 | 12/31/2005 | |||||

| Net Asset Value - Beginning of Period | $ 22.94 | $ 23.21 | $ 21.33 | $ 20.00 | ||||

| Net Investment Income (Loss) ** | (0.13) | (0.04) | (0.04) | 0.04 | ||||

| Net Gains (Loss) on Securities (realized and unrealized) | (9.02) | 0.47 | 2.47 | 1.49 | ||||

| Total from Investment Operations | (9.15) | 0.43 | 2.43 | 1.53 | ||||

| Distributions (From Net Investment Income) | - | - | - | (0.02) | ||||

| Distributions (From Capital Gains) | - | (0.70) | (0.55) | (0.18) | ||||

| Total Distributions | $ - | (0.70) | (0.55) | (0.20) | ||||

| Proceeds from Redemption Fee (Note 2) | - | - | - | - | ||||

| Net Asset Value - End of Period | $ 13.79 | $ 22.94 | $ 23.21 | $ 21.33 | ||||

| Total Return *** | (39.89)% | 1.85% | 11.39% | 7.65% | ||||

| Ratios/Supplemental Data | ||||||||

| Net Assets - End of Period (Thousands) | $ 2,425 | $ 5,613 | $ 3,719 | $ 3,289 | ||||

| Before Reimbursement | ||||||||

| Ratio of Expenses to Average Net Assets | 2.00% | 2.00% | 2.00% | 2.00% | ||||

| Ratio of Net Investment Loss to Average Net Assets | -1.17% | -0.67% | -0.68% | -0.11% | ||||

| After Reimbursement | ||||||||

| Ratio of Expenses to Average Net Assets **** | 1.50% | 1.50% | 1.50% | 1.69% | ||||

| Ratio of Net Investment Income (Loss) to Average Net Assets **** | -0.67% | -0.17% | -0.18% | 0.21% | ||||

| Portfolio Turnover Rate | 164.89% | 169.26% | 122.62% | 129.06% | ||||

| Paradigm Intrinsic Value Fund | ||

| Financial Highlights - Paradigm Intrinsic Value Fund | ||

| Selected data for a share outstanding throughout the period: | 1/1/2008* | |

| to | ||

| 12/31/2008 | ||

| Net Asset Value - Beginning of Period | $ 20.00 | |

| Net Investment Income (Loss) ** | 0.15 | |

| Net Gains (Loss) on Securities (realized and unrealized) | (6.17) | |

| Total from Investment Operations | (6.02) | |

| Distributions (From Net Investment Income) | - | |

| Distributions (From Capital Gains) | - | |

| Total Distributions | - | |

| Proceeds from Redemption Fee (Note 2) | - | |

| Net Asset Value - End of Period | $ 13.98 | |

| Total Return *** | (30.10)% | |

| Ratios/Supplemental Data | ||

| Net Assets - End of Period (Thousands) | $ 1,620 | |

| Ratio of Expenses to Average Net Assets | 1.25% | |

| Ratio of Net Investment Income to Average Net Assets | 0.86% | |

| Portfolio Turnover Rate | 70.57% | |

| * Commencement of operations. ** Per share amount calculated using the average shares method. *** Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund assuming reinvestment of dividends. Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or redemption of Fund shares. **** Such percentages reflect an expense waiver by the Advisor. |

| The accompanying notes are an integral part of these financial statements. |

2008 Annual Report 27

NOTES TO THE FINANCIAL STATEMENTS PARADIGM FUNDS December 31, 2008 |

1.) ORGANIZATION

The Paradigm Funds (the "Trust”) is an open-end management investment company organized in Ohio as a business trust on September 13, 2002 that may offer shares of beneficial interest in a number of separate series, each series representing a distinct fund with its own investment objectives and policies. The Paradigm Value Fund (“Value”) commenced operations on January 1, 2003. The Paradigm Value Fund's investment objective is long-term capital appreciation. The Paradigm Opportunity Fund (“Opportunity”) and Paradigm Select Fund (“Select”) both commenced operations on January 1, 2005 with long-term capital appreciation as their objective. The Paradigm Intrinsic Value Fund (“Intrinsic Value”) commenced operations on January 1, 2008. The Paradigm Intrinsic Value Fund's investment objective is long-term capital appreciation. The Advisor to Value, Opportunity, Select and Intrinsic Value (collectively the “Funds”) is Paradigm Funds Ad visor LLC (the “Advisor”).

2.) SIGNIFICANT ACCOUNTING POLICIES

SECURITY VALUATION: Securities that are traded on any exchange, including the NASDAQ, are generally valued by a pricing service at the last quoted sale price. Lacking a last sale price, an equity security is valued at its last bid price except when, in the Advisor's opinion, the last bid price does not accurately reflect the current value of the security. All other securities for which over-the-counter market quotations are readily available are valued at their last bid price. When market quotations are not readily available, when the Advisor determines the last bid price does not accurately reflect the current value or when restricted securities are being valued, such securities are valued as determined in good faith by the Advisor, in conformity with guidelines adopted by and subject to review of the Board of Trustees of the Trust.

Fixed income securities generally are valued on the basis of prices furnished by a pricing service when the Advisor believes such prices accurately reflect the fair market value of such securities. A pricing service utilizes electronic data processing techniques based on yield spreads relating to securities with similar characteristics to determine prices for normal institutional-size trading units of debt securities without regard to sale or bid prices. If the Advisor decides that a price provided by the pricing service does not accurately reflect the fair market value of the securities, or when prices are not readily available from a pricing service or when restricted or illiquid securities are being valued, securities are valued at fair value as determined in good faith by the Advisor, in conformity with guidelines adopted by and subject to review of the Board of Trustees. Short term investments in fixed income securities with maturities of less than 60 days when acqui red, or which subsequently are within 60 days of maturity, are valued by using the amortized cost method of valuation, which the Board of Trustees has determined will represent fair value.

In accordance with the Trust's good faith pricing guidelines, the Advisor is required to consider all appropriate factors relevant to the value of securities for which it has determined other pricing sources are not available or reliable as described above. No single standard for determining fair value controls, since fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of an issue of securities being valued by the Advisor would appear to be the amount which the owner might reasonably expect to receive for them upon their current sale. Methods which are in accord with this principle may, for example, be based on (i) a multiple of earnings; (ii) a discount from market of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or (iii) yield to maturity with respect to debt issues, or a combination of these and other methods.

The Funds adopted Financial Accounting Standards Board (FASB) Statement on Financial Accounting Standards (SFAS) No. 157 "Fair Value Measurements" effective January 1, 2008. This standard establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosure about fair value measurements. SFAS No. 157 applies to fair value measurements already required or permitted by existing standards. In accordance with SFAS No. 157, fair value is defined as the price that would be received by the Funds upon selling an asset or paid by the Funds to transfer a liability in an orderly transaction between market participants at the measurement date. In the absence of a principal market for the asset or liability, the assumption is that the transaction occurs on the most advantageous market for the asset or liability. SFAS No. 157 established a three-tier fair value hierarchy that prioritizes the assumptions, also known as "inputs", to valuation techniques used by market participants to measure fair value. The term "inputs" refers broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique

2008 Annual Report 28

Notes to the Financial Statements - continued

used to measure fair value (such as a pricing model) and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity's own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. The valuation techniques used to measure fair value should maximize the use of observable inputs and minimize the use of unobservable inputs. The three-tier hierarchy of inputs is summarized in three levels with the highest priority given to Level 1 and the lowest priority given to Level 3: Level 1 - quoted prices in active markets for identical securities, Level 2 - o ther significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) and Level 3 - significant unobservable inputs (including the Fund's own assumptions in determining the fair value of investments). The following is a summary of the inputs used as of December 31, 2008 in valuing the Funds’ assets carried at fair value:

| Value | Select | |||

| Investments | Investments | |||

| Valuation Inputs | in Securities | in Securities | ||

| Level 1- Quoted Prices | $84,371,474 | $2,221,474 | ||

| Level 2- Significant Other Observable Inputs | 1,066,644 | - | ||

| Level 3- Significant Unobservable Inputs | - | - | ||

| Total | $85,438,118 | $2,221,474 | ||

| Opportunity | Intrinsic Value | |||

| Investments | Investments | |||

| Valuation Inputs | in Securities | in Securities | ||

| Level 1- Quoted Prices | $2,491,684 | $1,618,165 | ||

| Level 2- Significant Other Observable Inputs | - | - | ||

| Level 3- Significant Unobservable Inputs | - | - | ||

| Total | $2,491,684 | $1,618,165 | ||

The Funds did not hold any Level 3 assets during the year ended December 31, 2008.

In March 2008, the Financial Accounting Standards Board issued the Statement of Financial Accounting Standards No.161, "Disclosures about Derivative Instruments and Hedging Activities" ("SFAS 161"). SFAS 161 is effective for fiscal years and interim periods beginning after November 15, 2008. SFAS 161 requires enhanced disclosures about the Funds’ derivative and hedging activities, including how such activities are accounted for and their effect on the Funds’ financial position, performance and cash flows. Management is currently evaluating the impact the adoption of SFAS 161 will have on the Funds’ financial statements and related disclosures.

SECURITY TRANSACTIONS AND OTHER: Security transactions are recorded based on a trade date. Dividend income is recognized on the ex-dividend date. Interest income is recognized on an accrual basis. The Funds use the specific identification basis in computing gain or loss on sale of investment securities. Discounts and premiums on fixed income securities purchased are amortized over the lives of the respective securities. Withholding taxes on foreign dividends have been provided for in accordance with the Funds’ understanding of the applicable country’s tax rules and rates. The Funds may invest in real estate investment trusts (“REITs”) that pay distributions to their shareholders based on available funds from operations. It is common for these distributions to exceed the REITs taxable earnings and profits resulting in the excess portion of such distribution to be designated as return of capital.

SHARE VALUATION: The net asset value (the “NAV”) is generally calculated as of the close of trading on the New York Stock Exchange (normally 4:00 p.m. Eastern time) every day the Exchange is open. The NAV for each fund is calculated by taking the total value of the fund’s assets, subtracting its liabilities, and then dividing by the total number of shares outstanding, rounded to the nearest cent. The offering price and redemption price per share is equal to the net asset value per share, except that shares of each fund are subject to a redemption fee of 2% if redeemed within 90 days of purchase. During fiscal year ended December 31, 2008 proceeds from redemption fees were $118,899, $0, $385 and $0 for Value, Select, Opportunity and Intrinsic Value, respectively.

SHORT SALES: A Fund may sell a security it does not own in anticipation of a decline in the fair value of the security. When a Fund sells a security short, it must borrow the security sold short and deliver it to the broker-dealer through which it made the short sale. A gain, limited to the price at which a Fund sold the security short, or a loss, unlimited in size, will be recognized upon the termination of a short sale.

2008 Annual Report 29

Notes to the Financial Statements - continued

INCOME TAXES: The Funds’ policy is to continue to comply with the requirements of Subchapter M of the Internal Revenue Code that are applicable to regulated investment companies and to distribute all of their taxable income to their shareholders. The Funds also intend to distribute sufficient net investment income and net capital gains, if any, so that they will not be subject to excise tax on undistributed income and gains. Therefore, no federal income tax or excise provision is required.

The Funds adopted the provisions of Financial Accounting Standards Board Interpretation No. 48 (“FIN 48”), Accounting for Uncertainty in Income Taxes, on June 29, 2007. The implementation of FIN 48 resulted in no material liability for unrecognized tax benefits and no material change to the beginning net asset value of the Funds.

As of and during the period ended December 31, 2008, the Funds did not have a liability for any unrecognized tax benefits. The Funds recognize interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the period, the Funds did not incur any interest or penalties.

The Funds are not subject to examination by U.S. federal and state tax authorities for tax years before 2005.

ESTIMATES: The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

DISTRIBUTIONS TO SHAREHOLDERS: Distributions to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the year from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified in the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassification will have no effect on net assets, results of operations or net asset values per share of any Fund. For the fiscal year ended December 31, 2008 net investment loss of $581,716 and $25,513 was reclassifi ed to paid in capital for Value and Opportunity, respectively.

3.) INVESTMENT ADVISORY AGREEMENTS