Exhibit 99.1

March 31, 2010

ANNUAL INFORMATION FORM

For the year ended

December 31, 2009

IAMGOLD CORPORATION

Table of Contents

| ITEM I | NAME AND INCORPORATION | 12 | ||||

| ITEM II | GENERAL DEVELOPMENT OF THE BUSINESS | 12 | ||||

| 1. | THREE-YEAR HISTORY | 12 | ||||

| 2. | SIGNIFICANT ACQUISITIONS | 17 | ||||

| 3. | TRENDS | 18 | ||||

| 4. | RISK FACTORS | 18 | ||||

| ITEM III | DESCRIPTION OF THE BUSINESS | 39 | ||||

| 1. | MINING ACTIVITIES - CANADA | 39 | ||||

| 1.1 | Westwood Project | 39 | ||||

| 1.2 | Doyon Division - Doyon and Mouska Gold Mines | 47 | ||||

| 2. | MINING ACTIVITIES - INTERNATIONAL | 51 | ||||

| 2.1 | Africa: Burkina Faso - Essakane Project | 51 | ||||

| 2.2 | Africa: Ghana - Tarkwa Gold Mine | 63 | ||||

| 2.3 | Africa: Ghana - Damang Gold Mine | 69 | ||||

| 2.4 | Africa: Botswana - Mupane Gold Mine | 73 | ||||

| 2.5 | Africa: Republic of Mali - Sadiola Gold Mine | 76 | ||||

| 2.6 | Africa: Republic of Mali - Yatela Gold Mine | 83 | ||||

| 2.7 | Africa: Tanzania - Buckreef Project | 87 | ||||

| 2.8 | Africa: Tanzania - Kitongo Project | 87 | ||||

| 2.9 | South America: Suriname - Rosebel Gold Mine | 88 | ||||

| 2.10 | South America: Ecuador - Quimsacocha Project | 94 | ||||

| 2.11 | South America: French Guiana - Camp Caiman Project | 99 | ||||

| 2.12 | South America: Peru - La Arena Project | 102 | ||||

| 3. | NON-GOLD | 103 | ||||

| 3.1 | Ferroniobium Production - Niobec Mine | 103 | ||||

| 3.2 | Diamond Royalty - Diavik Project | 108 | ||||

| 4. | EXPLORATIONAND DEVELOPMENT | 109 | ||||

| 4.1 | General | 109 | ||||

| 4.2 | Capitalized Exploration and Development Projects | 109 | ||||

| 4.3 | Greenfields Exploration and Development Expensed | 110 | ||||

| 4.4 | Outlook | 114 | ||||

| 5. | MINERAL RESERVESAND RESOURCES | 114 | ||||

| 6. | OTHER ASPECTSOFTHE BUSINESS | 119 | ||||

| 6.1 | Marketing of Production | 119 | ||||

| 6.2 | Government Regulation | 120 | ||||

| 6.3 | Environment | 121 | ||||

| 6.4 | Community Relations | 122 | ||||

| 6.5 | Taxes | 122 | ||||

| 6.6 | Mining Development and Construction | 123 | ||||

| 6.7 | Intellectual Property | 123 | ||||

| 6.8 | Competition | 123 | ||||

| 6.9 | Sale of Production | 124 | ||||

| 6.10 | Employee Relations | 125 | ||||

| 7. | DIVIDENDS | 125 | ||||

| 8. | LITIGATION | 125 | ||||

| ITEM IV | DESCRIPTION OF CAPITAL STRUCTURE | 126 | ||||

| ITEM V | MARKET FOR SECURITIES | 127 | ||||

| ITEM VI | DIRECTORS AND OFFICERS | 128 | ||||

| 1. | DIRECTORS | 128 | ||||

| 2. | EXECUTIVE OFFICERS | 129 | ||||

| 3. | SHAREHOLDINGSOF DIRECTORSAND OFFICERS | 131 | ||||

| 4. | CORPORATE CEASE TRADE ORDERSOR BANKRUPTCIES | 131 | ||||

| ITEM VII | AUDIT AND FINANCE COMMITTEE | 132 | ||||

| 1. | COMPOSITIONAND RELEVANT EDUCATIONAND EXPERIENCEOF MEMBERS | 132 | ||||

| 2. | MANDATEOFTHE AUDITAND FINANCE COMMITTEE | 135 | ||||

| 3. | POLICIESAND PROCEDURESFORTHE ENGAGEMENTOF AUDITAND NON-AUDIT SERVICES | 135 | ||||

| 4. | EXTERNAL AUDITOR SERVICE FEES | 135 | ||||

| ITEM VIII | INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 136 | ||||

| ITEM IX | TRANSFER AGENT AND REGISTRAR | 136 | ||||

| ITEM X | MATERIAL CONTRACTS | 137 | ||||

| ITEM XI | INTERESTS OF EXPERTS | 139 | ||||

| ITEM XII | ADDITIONAL INFORMATION | 139 | ||||

| SCHEDULE A – ORGANIZATIONAL CHART | ||||||

| SCHEDULE B – AUDIT COMMITTEE CHARTER | ||||||

List of Maps and Tables

IAMGOLD’s Corporate Structure | 13 | |

MINERAL RESERVES AND RESOURCES | 115 |

Explanatory Notes:

| 1. | All dollar amounts presented in this Annual Information Form are expressed in US dollars, unless otherwise indicated. |

| 2. | Production results are in metric units, unless otherwise indicated. |

| 3. | IAMGOLD Corporation carries on business in Canada. The subsidiaries of IAMGOLD Corporation carry on business in Canada and elsewhere. In this Annual Information Form, the words “Company” and “IAMGOLD” are used interchangeably and in each case refer, as the context may require, to all or any of IAMGOLD Corporation and its subsidiaries. |

| 4. | Unless otherwise specified, reference herein to the 2009 Annual Report are references to IAMGOLD’s Annual Report for the year ended December 31, 2009. All such references are incorporated herein. |

| 5. | The information in this Annual Information Form is complemented by the Company’s Audited Consolidated Annual Financial Statements for the year ended December 31, 2009 and the management’s discussion and analysis thereon. |

| 6. | The 2009 Annual Report, the Company’s Annual Financial Statements for the year ended December 31, 2009 and the management’s discussion and analysis thereon, are available on SEDAR atwww.sedar.com and the Company’s website atwww.iamgold.com. |

Cautionary Note to US Investors Regarding Mineral Reporting Standards

The disclosure in this Annual Information Form has been prepared in accordance with the requirements of Canadian securities laws, which differ from the requirements of United States securities laws. Disclosure, including scientific or technical information, has been made in accordance with Canadian National Instrument 43-101 — Standards of Disclosure for Mineral Projects (“NI 43-101”). NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. For example, the terms “measured mineral resources”, “indicated mineral resources”, “inferred mineral resources”, “proven mineral reserves” and “probable mineral reserves”

are used in this Annual Information Form and documents incorporated herein by reference to comply with the reporting standards in Canada. While those terms are recognized and required by Canadian regulations, the United States Securities and Exchange Commission (the “SEC”) does not recognize them. Under United States standards, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. Investors are cautioned not to assume that all or any part of the mineral deposits in these categories will ever be converted into mineral reserves. These terms have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of measured mineral resources, indicated mineral resources, inferred mineral resources, proven mineral reserves or probable mineral reserves will ever be upgraded or mined. In accordance with Canadian rules, estimates of inferred mineral resources cannot form the basis of feasibility or other economic studies. Investors are cautioned not to assume that any part of the reported measured mineral resources, indicated mineral resources, or inferred mineral resources in this Annual Information Form is economically or legally mineable and will ever be classified as a reserve. In addition, the definitions of proven and probable mineral reserves used in NI 43-101 differ from the definitions in the SEC Industry Guide 7. Disclosure of “contained ounces” is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute reserves as in place tonnage and grade without reference to unit measures. Accordingly, information contained in this Annual Information Form containing descriptions of the Company’s mineral properties may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.US investors are urged to consider closely the disclosure on technical terminology under the heading “Technical Information” in the Glossary below.

Special Note Regarding Forward-Looking Statements

This Annual Information Form contains certain information that may constitute “forward looking information” and “forward-looking statements” within the meaning of applicable Canadian securities laws and the United States Private Securities Litigation Reform Act of 1995, respectively. Forward-looking statements are necessarily based on a number of estimates and assumptions that are inherently subject to significant business, economic and competitive uncertainties and contingencies. All statements other than statements which are reporting results as well as statements of historical fact set forth or incorporated herein by reference, are forward-looking statements that may involve a number of known and unknown risks, uncertainties and other factors; many of which are beyond the Company’s ability to control or predict. Forward-looking statements include, without limitation, statements regarding strategic plans, future production, sales targets (including market share evolution in regard to niobium), cost estimates and anticipated financial results; potential mineralization and evaluation and evolution of mineral reserves and resources (including, but not limited to, Rosebel’s potential for further increases) and expected mine life; expected exploration results, future work programs, capital expenditures and objectives, evolution and economic performance of development projects including, but not limited to, the Essakane, Westwood, Quimsacocha and La Arena projects and exploration budgets and targets; construction and production targets and timetables, as well as anticipated timing of grant of permits and governmental incentives including, but not limited to, with respect to the Camp Caiman Project; outcome of negotiations with the Government of Ghana regarding fiscal stability agreements for the Damang and Tarkwa Gold Mines; expected continuity of a favourable gold market; contractual commitments, royalty payments, litigation matters and measures of mitigating financial and operational risks; anticipated liabilities regarding site closure and employee benefits; continuous availability of required manpower; possible exercise of outstanding warrants; the integration of operations, technologies and personnel of acquired operations and properties and, more generally, continuous access to capital markets; and the Company’s global outlook and that of each of its mines. These statements relate to analysis and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements.

Statements concerning actual mineral reserves and resources estimates are also deemed to constitute forward-looking statements to the extent that they involve estimates of the mineralization that will be encountered if the relevant project or property is developed, and in the case of mineral reserves, such statements reflect the conclusion based on certain assumptions that the mineral deposit can be economically exploited.

Page 1

Forward-looking statements, which involve assumptions and describe the Company’s future plans, strategies and expectations, are generally identifiable by use of the words “may”, “will”, “should”, “continue”, “expect”, “anticipate”, “estimate”, “believe”, “intend”, “plan” or “project” or the negative of these words or other variations on these words or comparable terminology. There can be no assurance that such statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. The following are some of the important factors that could cause actual results or outcomes to differ materially from those discussed in the forward-looking statements: hazards normally encountered in the mining business including unusual or unexpected geological formations, rock bursts, cave ins, floods and other conditions; delays and repair costs resulting from equipment failure; changes to and differing interpretations of mining tax regimes in foreign jurisdictions; the market prices of gold, niobium and other minerals; recent unprecedented events in global financial markets; recent market events and conditions and the deterioration of general economic indicators; the ability of the Company to replace reserves depleted by production; over/underestimation of reserve and resource calculations; fluctuations in exchange rates of currencies; failure to obtain financing as and when required to fund exploration and development; default under the Company’s credit facility due to violation of covenants therein; failure to obtain financing to meet capital expenditure plans; risks associated with being a multinational company; differences between the assumption of fair value estimates with respect to the carrying amount of mineral interests (including goodwill) and actual fair values; inherent risks related to the use of derivative instruments; accuracy of mineral reserve and mineral resource estimates; uncertainties in the validity of mining interests and ability to acquire new properties and retain skilled and experienced employees; various risks and hazards beyond the Company’s control, many of which are not economically insurable; risks and hazards inherent to the mining industry, most of which are beyond the Company’s control; market prices and availability of commodities used by the Company in its operations; lack of infrastructure and other risks related to the geographical areas in which the Company carries out its operations; labour disruptions; health risks associated with the mining work force in Africa; disruptions created by surrounding communities; need to comply with the extensive laws and regulations governing the environment, health and safety of the Company’s mining and processing operations and exploration activities; risks normally associated with any conduct of business in foreign countries including varying degrees of political and economic risk; ability to obtain the required licenses and permits from various governmental authorities in order to exploit the Company’s properties; risks and expenses related to reclamation costs and related liabilities; continuously evolving legislation, such as the mining legislation in Ecuador and French Guiana, which may have unknown and negative impact on operations; risks normally associated with the conduct of joint ventures; inability to control standards of non-controlled assets; risk and unknown costs of litigation; undetected failures in internal controls over financial reporting; risks related to making acquisitions, including the integration of operations; risks related to the construction, development and start-up of the Essakane Project and the Westwood Project; the training of workers and the resettlement of local communities in connection with the Essakane Project; dependence on key personnel; and other related matters.

Page 2

Although the Company has attempted to identify important factors that could cause actual results to differ materially from expectations, intentions, estimates or forecasts, there may be other factors that could cause results to differ from what is anticipated, estimated or intended. Those factors are described or referred to below, under the heading “Risk Factors” in this Annual Information Form. Recent unprecedented events in global financial and credit markets have resulted in high market and commodity price volatility and contraction in credit markets. These on-going events could impact forward-looking statements contained in this Annual Information Form in an unpredictable and possibly detrimental manner. Accordingly, readers should not place undue reliance on forward-looking statements. Except as required under applicable securities legislation, the Company undertakes no obligation to publicly update or revise forward-looking statements, whether as a result of new information, future events or otherwise.

Page 3

Glossary

Mining Terms and Frequently Used Abbreviations

AC:Aircore.

By-product: a secondary metal or mineral product recovered in the milling process.

Carbon-in-leach (CIL) process:a process used to recover dissolved gold inside a cyanide leach circuit. Coarse activated carbon particles are introduced in the leaching circuit and are moved counter-current to the slurry, absorbing gold as they pass through the circuit. Loaded carbon is removed from the slurry by screening. Gold is recovered from the loaded carbon by stripping in a caustic cyanide solution followed by electrolysis. CIL is a process similar to CIP (carbon in pulp) except that the gold leaching and the gold absorption are done simultaneously in the same stage compared with CIP where the gold absorption stage follows the gold leaching stage.

Carbon-in-pulp (CIP) process: a process used to recover dissolved gold from a cyanide leach slurry. Coarse activated carbon particles are moved counter-current to the slurry, absorbing gold as they pass through the circuit. Loaded carbon is removed from the slurry by screening. Gold is recovered from the loaded carbon by stripping in a caustic cyanide solution followed by electrolysis.

Concentrate: a product containing the valuable metal and from which most of the waste material in the ore has been eliminated.

Contained ounces: ounces in the mineralized rock without reduction due to mining loss or processing loss.

Converter:a furnace in which the pyrochlore concentrate is converted into ferroniobium and heat is produced by the oxidation reaction.

Cut-off grade: the lowest grade of mineralized material considered economic; used in the estimation of mineral reserves in a given deposit.

DD:Diamond Drilling or Diamond Drill.

Deferred development: development of underground infrastructure to be used over an extended period. Costs related to this activity are capitalized.

Deferred stripping:The capitalization of additional waste material mined, deemed to be a betterment, in order to extract an ore body in an open pit operation.

Depletion: the decrease in quantity of mineral reserves in a deposit or property resulting from extraction or production.

Page 4

Dilution: an estimate of the amount of waste or low-grade mineralized rock which will be mined with the ore as part of normal mining practices in extracting an orebody.

EHS:environment, health and safety.

EMS: environmental management system.

g Au/t: gram of gold per tonne.

Grade: the relative quantity or percentage of metal or mineral content.

ISO 14001: a standard established by the International Organization for Standardization setting forth the guidelines for an environmental management system.

ISO 9001: a standard established by the International Organization for Standardization setting forth the guidelines for a quality management system.

Leach/heap leach: to dissolve minerals or metals out of ore with chemicals. Heap leaching gold involves the percolation of a cyanide solution through crushed ore heaped on an impervious pad or base.

MW: megawatts.

Mineral reserves:mineral reserves are divided into two categories; proven and probable mineral reserves, which are more particularly defined herein under Section 5 of Item III below.

Mineral resources: mineral resources are divided into three categories; measured, indicated and inferred, which are more particularly defined herein under Section 5 of Item III below.

Mtpa: Million tonnes per annum.

Ounce: refers to one troy ounce, which is equal to 31.103 grams.

QA-QC: quality-assurance / quality control.

Qualified person: an individual who is an engineer or geoscientist with at least five years of experience in mineral exploration, mine development or operation, mineral project assessment, or any combination thereof, has experience relevant to the subject matter of the project or report, and is a member in good standing of a self regulating organization, as more fully referenced in NI 43-101.

RAB:Rotary air blast.

RC: reversed circulation.

Page 5

Recovery: the proportion of valuable material obtained during the mining or processing. Generally expressed as a percentage of the material recovered compared to the total material present.

Restoration: operation consisting of restoring a mining site to a satisfactory condition.

SAG: Semi-autogenous grinding.

Stope: the underground excavation from which the ore is extracted.

Stoping: the process of mining an underground orebody.

Stripping: In Mining: the process of removing overburden or waste rock to expose ore.

In Processing: the process of removing the gold from loaded carbon by use of a hot caustic cyanide solution.

Tailings:the material that remains after metals or minerals considered economic have been removed from ore during milling.

Tailings pond or Tailings Storage Facility (TSF): a containment area used to deposit tailings from milling.

Tonne:by common convention refers to one Metric ton, equivalent to 1,000 kg.

Financial Terms

2008 Credit Facility: means the credit agreement providing for a revolving facility of up to C$140 million entered into by the Company and a syndicate of financial institutions led by The Bank of Nova Scotia and Société Générale on April 15, 2008.

2010 Amended Credit Facility: means the amended and restated 2008 Credit Facility including increasing the revolving facility to $350 million and changes to several terms and conditions, entered into by the Company and a syndicate of financial institutions led by The Bank of Nova Scotia, Société Générale and Canadian Imperial Bank of Commerce on March 24, 2010.

2010 Financial Creditors: means the syndicate of financial institutions party to the 2010 Amended Credit Facility.

Forward sales:the sale of a commodity for delivery at a specified future date and price, usually at a premium to the spot price.

Hedge: a risk management technique used to manage commodity price, interest rate, foreign currency exchange or other exposures arising from regular business transactions.

Page 6

Hedging: a future transaction made to protect the price of a commodity as revenue or cost and secure cash flows.

Margin: money or securities deposited with a broker as security against possible negative price fluctuations.

Royalty: cash payment or physical payment (in-kind) generally expressed as a percentage of Net Smelter Returns (“NSR”) or mine production.

Spot price: the current price of a metal for immediate delivery.

TSX: the Toronto Stock Exchange.

Volatility:propensity for variability. A market or share is volatile when it records rapid variations.

Technical Information

For the Sadiola and Yatela mines, refer to the definitions of the JORC Code (defined below) and for the Tarkwa and Damang mines, refer to the definitions of the SAMREC Code (defined below) under the headings “Australasian Code for Reporting of Mineral Resources and Ore Reserves – South African Code for Reporting of Mineral Resources Mineral Reserves” below.

Canadian Standards for Mineral Resources and Reserves

Unless otherwise indicated, in this Annual Information Form, the following terms have the meanings set forth below.Reference is made to the “Cautionary Note to US Investors Regarding Mineral Reporting Standards” at the beginning of this Annual Information Form.

Mineral Reserves

Mineral Reserves are sub-divided in order of increasing confidence into Probable Mineral Reserves and Proven Mineral Reserves. A Probable Mineral Reserve has a lower level of confidence than a Proven Mineral Reserve.

A Mineral Reserve is the economically mineable part of a Measured or Indicated Mineral Resource demonstrated by at least a preliminary feasibility study. This study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. A Mineral Reserve includes diluting materials and allowances for losses that may occur when the material is mined.

Proven Mineral Reserve

A Proven Mineral Reserve is the economically mineable part of a Measured Mineral Resource demonstrated by at least a preliminary feasibility study. This study must

Page 7

include adequate information on mining, processing, metallurgical, economic, and other relevant factors that demonstrate, at the time of reporting, that economic extraction is justified.

Probable Mineral Reserve

A Probable Mineral Reserve is the economically mineable part of an Indicated and, in some circumstances, a Measured Mineral Resource, demonstrated by at least a preliminary feasibility study. This study must include adequate information on mining, processing, metallurgical, economic, and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified.

Mineral Resources

Mineral Resources are sub-divided, in order of increasing geological confidence, into Inferred, Indicated and Measured categories. An Inferred Mineral Resource has a lower level of confidence than that applied to an Indicated Mineral Resource. An Indicated Mineral Resource has a higher level of confidence than an Inferred Mineral Resource but has a lower level of confidence than a Measured Mineral Resource.

A Mineral Resource is a concentration or occurrence of natural, solid, inorganic or fossilized organic material in or on the Earth’s crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. The location, quantity, grade, geological characteristics and continuity of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge.

Measured Mineral Resource

A Measured Mineral Resource is that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are so well established that they can be estimated with confidence sufficient to allow the appropriate application of technical and economic parameters to support production planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough to confirm both geological and grade continuity.

Indicated Mineral Resource

An Indicated Mineral Resource is that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics, can be estimated with a level of confidence sufficient to allow the appropriate application of technical and economic parameters, to support mine planning and evaluation of the economic viability of the deposit. The estimate is based on detailed and reliable exploration and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological and grade continuity to be reasonably assumed.

Page 8

Inferred Mineral Resource

An Inferred Mineral Resource is that part of a Mineral Resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes.

Metallurgical Recovery and Cut-off Grade

In calculating mineral reserves, cut-off grades are established using the Company’s long-term metal or mineral prices and foreign exchange assumptions, the average metallurgical recovery rates and estimated production costs over the life of the related operation. For an underground operation, a cut-off grade is calculated for each mining method, as production costs vary from one method to another. For a surface operation, production costs are determined for each block included in the block model of the relevant operation.

* * * * * * * * *

Australasian Code for Reporting of Mineral Resources and Ore Reserves – South African Code for Reporting of Mineral Resources and Mineral Reserves

The estimates of ore reserves and mineral resources for the Sadiola and Yatela mines, as set out in this Annual Information Form have been calculated in accordance with the Australasian Code for Reporting of Mineral Resources and Ore Reserves prepared by the Joint Ore Reserves Committee of the Australasian Institute of Mining and Metallurgy, the Australian Institute of Geoscientists and Minerals Council of Australia (the “JORC Code”). The estimates for mineral reserves and mineral resources for the Tarkwa and Damang mines set out in this Annual Information Form have been calculated in accordance with the South African Code for Reporting of Mineral Resources and Mineral Reserves as prepared by the South African Mineral Committee under the auspices of the South African Institute of Mining and Metallurgy (the “SAMREC Code”). The SAMREC Code was established in 1998 and was modeled on the JORC Code. NI 43-101 provides that companies may make disclosures using the reserve and resource categories of the JORC Code or the SAMREC Code, subject to the satisfaction of certain requirements.

The definitions ofore reserves(under the JORC Code) andmineral reserves (under the SAMREC Code) are as follows.

Ore reserve(under the JORC Code) andmineral reserve (under the SAMREC Code) is the economically mineable part of a measured or indicated mineral resource. It includes diluting materials and allowances for losses which may occur when the material is mined. Appropriate assessments, which may include feasibility studies, have been carried out, and include consideration of and modification by realistically assumed mining, metallurgical, economic, marketing, legal, environmental, social and

Page 9

governmental factors. These assessments demonstrate at the time of reporting that extraction could reasonably be justified. Ore reserves are subdivided in order of increasing confidence into probable ore reserves and proved ore reserves.

Probable ore reserve(under the JORC Code) andprobable mineral reserve (under the SAMREC Code) is the economically mineable part of an indicated, and in some circumstances measured, mineral resource. It includes diluting materials and allowances for losses which may occur when the material is mined. Appropriate assessments, which may include feasibility studies, have been carried out, and include consideration of and modification by realistically assumed mining, metallurgical, economic, marketing, legal, environmental, social and governmental factors. These assessments demonstrate at the time of reporting that extraction could reasonably be justified.

Proved ore reserve(under the JORC Code) andproved mineral reserve (under the SAMREC Code) is the economically mineable part of a measured mineral resource. It includes diluting materials and allowances for losses which may occur when the material is mined. Appropriate assessments, which may include feasibility studies, have been carried out, and include consideration of and modification by realistically assumed mining, metallurgical, economic, marketing, legal, environmental, social and governmental factors. These assessments demonstrate at the time of reporting that extraction could reasonably be justified.

The definitions ofmineral resourcesunder the JORC Code and the SAMREC Code are as follows:

Mineral resource is a concentration or occurrence of material of intrinsic economic interest in or on the Earth’s crust in such form and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade, geological characteristics and continuity of a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge. Mineral resources are subdivided, in order of increasing geological confidence, into inferred, indicated and measured categories.

Inferred mineral resource is that part of a mineral resource for which tonnage, grade and mineral content can be estimated with a low level of confidence. It is inferred from geological evidence and is assumed, but not verified, geological and/or grade continuity. It is based on information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes which may be limited or of uncertain quality and reliability.

Indicated mineral resource is that part of a mineral resource for which tonnage, densities, shape, physical characteristics, grade and mineral content can be estimated with a reasonable level of confidence. It is based on exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes. The locations are too widely or inappropriately spaced to confirm geological and/or grade continuity but are spaced closely enough for continuity to be assumed.

Page 10

Measured mineral resource is that part of a mineral resource for which tonnage, densities, shape, physical characteristics, grade and mineral content can be estimated with a high level of confidence. It is based on detailed and reliable exploration, sampling and testing information gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes. The locations are spaced closely enough to confirm geological and/or grade continuity.

Mineral resources, which are not ore reserves, do not have demonstrated economic viability.

The foregoing definitions of ore/mineral reserves and mineral resources as set forth in the JORC Code and the SAMREC Code have been reconciled to the definitions in the Canadian Institute of Mining, Metallurgy and Petroleum Standards on Mineral Resources and Reserves Definitions and Guidelines (the “CIM Standards”) adopted under NI 43-101. If ore/mineral reserves and mineral resources for the Tarkwa, Damang, Sadiola and Yatela gold mines were estimated in accordance with the definitions in the CIM Standards, there would be no substantive differences in the reserve and resources estimates for such mines set forth herein.

Symbols Used

| Ag | = | silver | ||

| Au | = | gold | ||

| Cu | = | copper | ||

| FeNb | = | ferroniobium | ||

| Nb | = | niobium | ||

| Nb2O5 | = | niobium pentoxide (pyrochlore) | ||

Page 11

Item I Name and Incorporation

The Company was incorporated under theCanada Business Corporations Act with the name “IAMGOLD International African Mining Gold Corporation” by articles of incorporation effective March 27, 1990. By articles of amendment effective June 23, 1995, the outstanding common shares of the Company (“Common Shares”) were consolidated on a one-for-4.45 basis. By articles of amendment effective July 19, 1995, the authorized capital of the Company was increased by the creation of an unlimited number of first preference shares (“First Preference Shares”), issuable in series, and an unlimited number of second preference shares (“Second Preference Shares”), issuable in series, and the “private company” restrictions were deleted. By articles of amendment effective June 27, 1997, the name of the Company was changed to “IAMGOLD Corporation”. By articles of amalgamation effective April 11, 2000, the Company amalgamated with its then wholly-owned subsidiary, 3740781 Canada Ltd. (formerly 635931 Alberta Ltd.). By articles of amalgamation effective January 1, 2004, the Company amalgamated with its then wholly-owned subsidiary, Repadre Capital Corporation (“Repadre”). Effective March 22, 2006, the Company completed a business combination transaction with Gallery Gold Limited (“Gallery Gold”) and effective November 8, 2006, the Company acquired Cambior Inc. (“Cambior”) by amalgamating a wholly-owned subsidiary, IAMGOLD-Québec Management Inc. (“IMG-Qc”), with Cambior pursuant to the terms of a court-sanctioned arrangement.

The registered and principal office of the Company is located at 401 Bay Street, Suite 3200, PO Box 153, Toronto, Ontario, Canada M5H 2Y4. The Company’s telephone number is (416) 360-4710 and its website address iswww.iamgold.com.

Item II General Development of the Business

| 1. | Three-Year History |

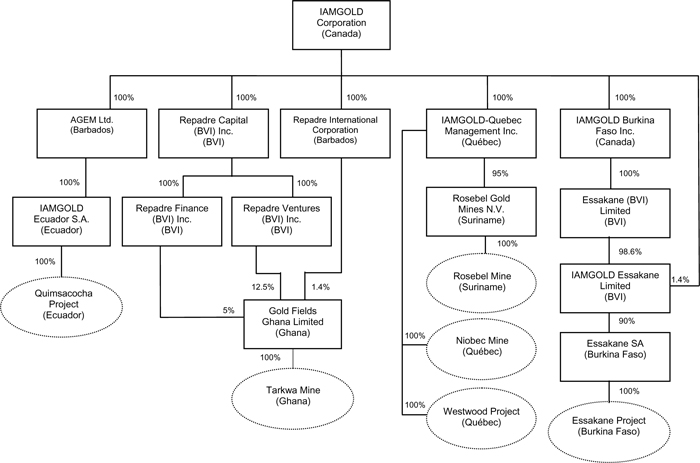

IAMGOLD is engaged primarily in the exploration for, and the development and production of, mineral resource properties throughout the world. Through its holdings, IAMGOLD has interests in various operations and exploration properties as well as a royalty interest on a property that produces diamonds. The following chart illustrates certain subsidiaries of IAMGOLD, together with the jurisdiction of incorporation of each such subsidiary and the percentage of voting securities beneficially owned or over which control or direction is exercised by IAMGOLD, and the material mineral projects of IAMGOLD held through such subsidiaries and the percentage of ownership interest that the relevant subsidiary of IAMGOLD has in such material mineral projects.

Page 12

Other property interests of IAMGOLD include the following:

| (a) | a 100% interest in the mining leases in the Province of Québec, Canada, on which the Doyon gold mine (the “Doyon Gold Mine”) and the Mouska gold mine (the “Mouska Gold Mine”, and together with the Doyon Mine (the “Doyon Division”) are located and which are held by IMG-Qc. |

| (b) | an indirect 18.9% interest (held through Repadre International Corporation) in Abosso Goldfields Limited (“Abosso”), the holder of the mineral rights to the Damang concession in Ghana on which the Damang gold mine is located (the “Damang Gold Mine”). The Damang concession is contiguous with the concession on which the Tarkwa gold mine is located; |

| (c) | an indirect 41% interest (held through AGEM Ltd. (“AGEM”), a wholly-owned subsidiary of the Company incorporated under the laws of Barbados) in Société d’Exploitation des Mines d’Or de Sadiola S.A. (“SEMOS”), the owner of the mining rights for the mining permit area (the “Sadiola Mining Permit”) in Mali on which the Sadiola gold mine (the “Sadiola Gold Mine”) is located; |

Page 13

| (d) | an indirect 50% interest (held through AGEM) in Sadiola Exploration Limited (“SADEX”) which holds an 80% interest in Societe d’Exploitation des Mines d’Or de Yatela S.A. (“YATELA”), the owner of the mining rights for the mining permit area in Mali that is immediately to the north of the Sadiola Mining Permit and on which the Yatela gold mine (the “Yatela Gold Mine”) is located; |

| (e) | an indirect 100% interest in IAMGOLD Guyane S.A.S., which owns the mining rights in connection with the Camp Caiman project (the “Camp Caiman Project”) in French Guiana; |

| (f) | an indirect 100% interest in La Arena S.A., subject to an option and earn-in agreement under which Rio Alto (as hereinafter defined) can acquire up to a 100% interest in La Arena S.A., the owner of the mining concessions relating to the La Arena gold-copper project (the “La Arena Project”) in Peru; and |

| (g) | a 1% royalty on the Diavik diamond property located in the Northwest Territories, Canada. |

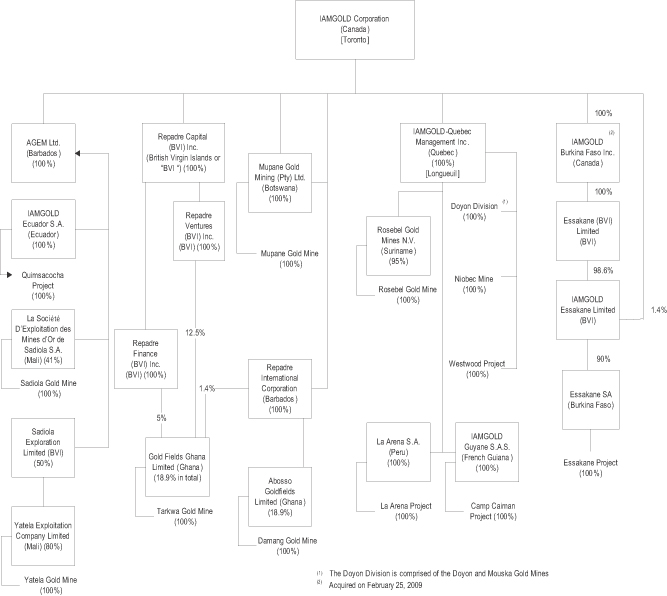

The Company is the operator of the Rosebel, Niobec, Mupane, Doyon and Mouska mines. The chart attached hereto as Schedule A sets out the subsidiaries of the Corporation, together with the jurisdiction of incorporation of each subsidiary and the percentage of voting securities beneficially owned or over which control or direction is exercised by IAMGOLD, and the material mineral projects and the other property interests of IAMGOLD held through such subsidiaries and the percentage of ownership interest that the relevant subsidiary of IAMGOLD has in such material mineral projects.

Effective March 21, 2007, the Company sold its 70% interest in Omai Bauxite Mining Inc. and its 100% interest in Omai Services Inc. to Bosai Minerals Group Co. Ltd. (“Bosai Minerals”) for cash proceeds of $28.5 million. Bosai Minerals assumed $17.7 million of third-party debt as part of the transaction.

Effective February 27, 2008, the Company sold its 34% interest in the Nyakafuru joint venture to Resolute Mining (Tanzania) Limited (“Resolute”) for $6.0 million in shares of Resolute and a retained $10/oz royalty on additional ounces discovered and attributable to the Company’s former interest capped at an amount of $3.75 million.

On March 5, 2008, the Company issued 928,962 flow-through Common Shares for proceeds of C$8,500,000. As of December 31, 2008, the Company had applied all of the flow-through share proceeds raised to fund prescribed resource expenditures on the Company’s Westwood Project in Québec, Canada. Prior to December 31, 2008, the Company filed with tax authorities the documents required to renounce the tax credits associated with these expenditures and thereby fulfilled its commitments under the subscription agreement and satisfied the requirements under applicable Canadian federal income tax legislation.

Page 14

On July 23, 2008, the Company acquired the participation royalty on production from the Doyon Gold Mine and the Westwood Project from Barrick Gold Corporation for $13 million in cash. The transaction eliminated the royalty obligation on production from the Doyon Gold Mine, which was 24.75% of the gold price above $375 per ounce. The participation royalty also extended to the Westwood Project, located two kilometres from the Doyon Gold Mine.

On October 31, 2008, the Company completed the sale of the Sleeping Giant Gold Mine and related milling facilities to Cadiscor Resources Inc. (“Cadiscor”). Following the sale, the Company held (i) 5,185,715 common shares of Cadiscor, (ii) warrants to purchase 1,000,000 common shares of Cadiscor, exercisable at C$0.70 per share and expiring on December 31, 2010; and (iii) a C$3.5 million debenture, convertible into common shares of Cadiscor.

On December 23, 2008, the Company announced that it had entered into a definitive option agreement to earn a 50% interest in the Siribaya gold project in Mali, West Africa, which is 100% controlled by Merrex Gold Inc. (“Merrex”). The Company can earn its interest by spending C$10.5 million over four years on the project. Pursuant to the definitive option agreement, the Company purchased 4,285,714 units on a private placement basis at a price of C$0.35 per unit. Each unit is comprised of one common share of Merrex and a warrant exercisable at C$0.45 per share for a period of 12 months. In December 2009, the Company exercised the warrants and now holds 8,571,428 shares of Merrex representing approximately 10% of the outstanding shares of Merrex.

On December 23, 2008, the French Autorité des marchés financiers published the final results for IAMGOLD’s public offer for Euro Ressources S.A. (“EURO”), including the re-opened offer. As a result of the offer, IAMGOLD controls 52.8 million shares of EURO representing 84.55% of the current share capital of EURO. EURO has a participation right royalty on production from the Rosebel Gold Mine that entitles EURO to payments of 10% of the gold price above $300 per ounce for production from soft rock and above $350 per ounce for production from hard rock. As at December 31, 2009, the remaining number of ounces of gold covered by the royalty agreement was approximately 5.1 million ounces. The Company may enter into transactions in the market in France that will impact its holdings in EURO.

On March 26, 2009, the Company completed a public offering (the “Offering”) of Common Shares through a syndicate of underwriters at a price of C$8.75 per share by way of a short form prospectus in all of the provinces and territories of Canada, except Québec, and a registration statement filed with the SEC under the multijurisdictional disclosure system. Including the Common Shares issued on the exercise of the over-allotment option, the Company issued 39,445,000 Common Shares for aggregate gross proceeds of C$345,143,750. Approximately C$250 million of the net proceeds from the Offering are expected to be used to fund the construction and development of the Essakane Project and the balance is expected to fund capital expenditures at the Company’s other properties and to be used for general corporate purposes including future acquisition opportunities.

Page 15

On June 5, 2009, the Company issued 1,379,310 flow-through Common Shares for proceeds of C$20,000,000. As of December 31, 2009, the Company had applied all of the flow-through share proceeds raised to fund prescribed resource expenditures on the Company’s Westwood Project in Québec, Canada. Subsequent to December 31, 2009, the Company filed with tax authorities the documents required to renounce the tax credits associated with these expenditures and thereby fulfilled its commitments under the subscription agreement and satisfied the requirements under applicable Canadian federal income tax legislation.

On June 19, 2009, the Company acquired 16,088,636 common shares at C$0.70 per share for a total investment of C$11,262,000 representing approximately 15.7% of the current issued and outstanding shares of Oromin Explorations Ltd. (“Oromin”). Oromin is a TSX-listed company with a joint venture interest in a property covering a large landholding in close proximaty to the Sabodala mine in Senegal. The Company acquired these common shares for investment purposes.

In June 2009, an option and earn-in agreement was entered into for the sale of the La Arena Project in Peru. The Company received 8,024,511 common shares (10.6% interest) and 1,500,000 warrants of Rio Alto Mining Limited (“Rio Alto”) for a total value of $1.4 million. Rio Alto has the option to purchase all of the outstanding shares of La Arena S.A., an IAMGOLD wholly-owned subsidiary, for a cash payment of $47.6 million. During the option term, Rio Alto may also earn-in newly issued shares of La Arena S.A. up to a maximum of 38.7% by incurring up to $30.0 million in expenditures on the La Arena Project. In 2009, Rio Alto was appointed the manager of La Arena S.A. and the La Arena Project and spent $3.7 million on the project under the earn-in agreement.

On July 29, 2009, the Company filed a base shelf prospectus with the securities regulators in each province and territory of Canada (except for Quebec) and a corresponding registration statement with the SEC in the United States. These filings allow the Company to make offerings of common shares, warrants, debt securities, subscription receipts or any combination thereof of up to $700 million until August 29, 2011.

In August 2009, the Company entered into an option agreement to acquire up to an initial 51% interest in Avnel Gold Limited (“Avnel”) and its 80% interest in a small operating gold mining company in southwest Mali. The 51% interest in Avnel will require spending $11.0 million on exploration activities over a three-year period, and delivering a National Instrument (NI 43-101) resource determination of at least 2 million ounces of gold. IAMGOLD can increase its interest to 70% by sole funding a feasibility study (or 65% if funded jointly), and by payment of a feasibility study fee determined upon the amount of reserves and resources outlined. The Company believes there is the potential for a large bulk tonnage operation in the immediate mine area, and significant upside in the large land package. IAMGOLD incurred $1.8 million in 2009 as part of a $2.5 million mandatory expenditure in the first year of the agreement.

Page 16

On December 29, 2009, IAMGOLD acquired an additional 3% interest in SEMOS from the International Finance Corporation (“IFC”) increasing the Sadiola joint venture ownership interest to 41%. AngloGold Ashanti acquired the other 3% interest. The Republic of Mali has until the end of March 2010 to elect whether it will take up its proportionate entitlement of 0.574% interest in SEMOS from each of the Company and AngloGold Ashanti.

The consideration for each 3% share in SEMOS was $6.0 million in cash followed by contingent payments of:

| • | $0.25 million in each of 2010, 2011 and 2012 for which the average gold price exceeds $900 per ounce, or $0.5 million in each of the aforementioned years that the average gold price exceeds $1,000 per ounce, and |

| • | $0.5 million upon approval by the board of directors of SEMOS and the Republic of Mali to proceed with the development of the Sadiola Deep Sulphide Project. |

| 2. | Significant Acquisitions |

On February 25, 2009, the Company acquired (the “Orezone Transaction”) all of the outstanding common shares of Orezone Resources Inc. (“Orezone Resources”) pursuant to an arrangement agreement (the “Arrangement Agreement”) dated December 10, 2008, as amended January 12, 2009, between the Company, Orezone Resources and Orezone Gold Corporation (“Orezone Gold”). The principal asset of Orezone Resources was a 90% interest in the Essakane gold project comprised of a mining permit covering 100.2 square kilometres and certain exploration permits in Burkina Faso, West Africa (the “Essakane Project”).

Pursuant to the Orezone Transaction, the holders (the “Orezone Shareholders”) of common shares of Orezone Resources (“Orezone Resources Shares”) received for each one Orezone Resources Share (i) 0.08 of a Common Share of IAMGOLD, and (ii) 0.125 of a common share of Orezone Gold, a new public exploration and development company. As part of the Orezone Transaction, the exploration properties of Orezone Resources that were not related to the Essakane Project were spun-out into Orezone Gold together with C$10 million in cash.

On the effective date of the Orezone Transaction, IAMGOLD, among other things:

| • | issued an aggregate of 28,817,244 Common Shares to acquire all of the outstanding Orezone Resources Shares; |

| • | issued 555,425 Common Shares and paid C$5,045,205 in satisfaction of the 6% convertible debenture dated July 1, 2008 in the principal amount of C$10 million issued by Orezone Resources; |

| • | reserved 282,656 Common Shares for issue upon the exercise of outstanding options granted by IAMGOLD to holders of options of Orezone Resources granted under the stock option plan of Orezone |

Page 17

Resources approved by the directors and shareholders of Orezone in 1997; |

| • | reserved 84,800 Common Shares for issue upon the exercise of outstanding options of Orezone Resources granted under the stock option plan of Orezone Resources approved by the directors and shareholders of Orezone Resources in 2008; and |

| • | reserved 160,000 Common Shares for issue upon the exercise of outstanding warrants to purchase Orezone Resources Shares. |

As a result of the Orezone Transaction, among other things:

| • | Orezone Resources was amalgamated with a wholly-owned subsidiary of the Company, incorporated for the purposes of the Orezone Transaction, to form IAMGOLD Burkina Faso Inc. (“IMG-BF”); |

| • | IMG-BF (together with IAMGOLD) indirectly holds a 90% interest in the Essakane Project; |

| • | IAMGOLD held approximately 16.6% of the outstanding common shares of Orezone Gold as of the effective date of the Orezone Transaction; and |

| • | the former Orezone Shareholders held approximately 9% of the outstanding Common Shares as of the effective date of the Orezone Transaction. |

In addition, on February 24, 2009, The Standard Bank of South Africa Limited (“Standard Bank”) effectively assigned to IAMGOLD the $40 million bridge loan payable by Orezone Essakane Limited (an indirect wholly-owned subsidiary of the Company now named IAMGOLD Essakane Limited) to Standard Bank in consideration for the payment by IAMGOLD of $40 million (plus accrued and unpaid interest outstanding on such loan). The $40 million bridge loan is now an inter-company loan from IAMGOLD to IAMGOLD Essakane Limited. The intercompany loan has subsequently been assigned to AGEM Ltd, a wholly-owned financing subsidiary of IAMGOLD.

| 3. | Trends |

IAMGOLD’s income, cash flow and gold bullion holdings are significantly affected by fluctuations in the price of gold which has experienced significant price movements over the past three years. During this period, the price of gold, based on the London PM Fix on the London Bullion Market, reached a low of $608.40 on January 10, 2007 and a high of $1,212.50 on December 2, 2009. While it appears that there is an upward trend in the price of gold since 2006, there has been significant volatility during this period, and future movements in the price of gold are beyond the control of IAMGOLD. See the discussion under the heading “Risk Factors” below.

Page 18

| 4. | Risk Factors |

The Company is subject to various financial and operational risks that could materially impact on, among other things, operating results, profitability and levels of operating cash flow, as described below. Any one of such risk factors could cause actual events to differ materially from those described in forward-looking statements relating to the Company.

Financial Risks

The Company’s earnings are directly related to the market prices for various minerals.

The Company’s revenues depend on the market prices for mine production from the Company’s producing properties. In 2009, approximately 82% of the Company’s revenues were attributable to gold sales. The gold market is highly volatile and is subject to various factors including political stability, general economic conditions, mine production, and intent of governments who own significant above-ground reserves. Gold prices fluctuate widely and are affected by numerous factors beyond the Company’s control, including central bank lending, sales and purchases of gold, producer hedging activities, expectations of inflation, the level of demand for gold as an investment, speculative trading, the relative exchange rate of the US dollar with other major currencies, interest rates, global and regional demand, political and economic conditions and uncertainties, industrial and jewellery demand, production costs in major gold producing regions and worldwide production levels. The aggregate effect of these factors is impossible to predict with accuracy. In addition, the price of gold has on occasion been subject to very rapid short-term changes because of speculative activities. Fluctuations in gold prices may materially adversely affect the Company’s financial performance or results of operations. If the world market price of gold was to drop and the prices realized by the Company on gold sales were to decrease significantly and remain at such a level for any substantial period, the profitability of the Company and cash flow would be negatively affected. The world market price of gold has fluctuated widely during the last several years. If the market price of gold falls significantly from its current level, the mine development projects may be rendered uneconomic and the development of the mine projects may be suspended or delayed. The profitability and economic viability of the Company’s niobium producing property, the Niobec mine, is subject to market fluctuations in the price of niobium. The niobium market is characterized by a dominant producer whose actions may affect the price of niobium. The Company is a relatively new entrant in the niobium market and could be negatively affected by its lack of market share.

Failure to obtain the financing necessary for the Company’s capital expenditure plans may result in a delay or indefinite postponement of exploration, development or production on any or all of the Company’s properties.

To fund growth, the Company may depend on securing the necessary capital through loans or other forms of permanent capital. The availability of this capital is subject to

Page 19

general economic conditions and lender and investor interest in the Company and its projects. The construction of mining facilities and commencement of mining operations, such as at the Essakane Project and the exploration and development of the Company’s properties, including continuing exploration and development projects in Québec and Ecuador, will require substantial capital expenditures. In addition, a portion of the Company’s activities is directed to the search for and the development of new mineral deposits. The Company may be required to seek additional financing to maintain its capital expenditures at planned levels. The Company will also have additional capital requirements to the extent that it decides to expand its present operations and exploration activities or construct additional new mining and processing operations at any of its properties or take advantage of opportunities for acquisitions, joint ventures or other business opportunities that may arise. Financing may not be available when needed or, if available, may not be available on terms acceptable to the Company. Failure to obtain any financing necessary for the Company’s capital expenditure plans may result in a delay of indefinite postponement of exploration, development or production on any or all of the Company’s properties.

In order to finance future operations and development efforts, the Company may raise funds through the issue of Common Shares of IAMGOLD or the issue of securities convertible into Common Shares of IAMGOLD, which would dilute the shareholdings of the then current shareholders.

In order to finance future operations and development efforts, the Company may raise funds through the issue of Common Shares or the issue of securities convertible into Common Shares. The constating documents of the Company allow it to issue, among other things, an unlimited number of Common Shares for such consideration and on such terms and conditions as may be established by the directors of the Company, in many cases, without the approval of shareholders. The Company cannot predict the size of future issues of Common Shares or the issue of securities convertible into Common Shares of IAMGOLD or the effect, if any, that future issues and sales of the Company’s Common Shares will have on the market price of its Common Shares. Due to recent market volatility and the devaluation of global stock markets, there may be an increased risk of dilution for existing shareholders should the Company need to issue additional Common Shares at a lower share price to meet its capital requirements. Any transaction involving the issue of previously authorized but unissued Common Shares or securities convertible into Common Shares, would result in dilution, possibly substantial, to present and prospective holders of shares.

The recent unprecedented events in global financial markets have had a profound impact on the global economy and the gold mining industry.

The recent unprecedented events in global financial markets have had a profound impact on the global economy. Many industries, including the gold mining industry, are impacted by these market conditions. Some of the key impacts of the current financial market turmoil include contraction in credit markets resulting in a widening of credit risk, devaluations and high volatility in global equity, commodity, foreign exchange and precious metal markets, and a lack of market liquidity. A continued or worsened slowdown in the financial markets or other economic conditions, including, but not

Page 20

limited to, consumer spending, employment rates, business conditions, inflation, fuel and energy costs, consumer debt levels, lack of available credit, the state of the financial markets, interest rates and tax rates may adversely affect the Company’s growth and profitability. Specifically the global credit/liquidity crisis could impact the cost and availability of financing and the Company’s overall liquidity; the volatility of gold prices impacts the Company’s revenues, profits and cash flow; volatile energy, commodity and consumables prices and currency exchange rates impact the Company’s production costs; and the devaluation and volatility of global stock markets impacts the valuation of the Company’s equity securities. These factors could have a material adverse effect on the Company’s financial condition and results of operations.

Recent market events and conditions and the deterioration of general economic indicators have led to a loss of confidence in global credit and financial markets, restricted access to capital and credit, and increased counterparty risk.

Beginning in 2007, the U.S. credit markets began to experience and continue to experience serious disruption due to a deterioration in residential property values, defaults and delinquencies in the residential mortgage market (particularly, sub-prime and non-prime mortgages) and a decline in the credit quality of mortgage backed securities. These problems led to a slow-down in residential housing market transactions, declining housing prices, delinquencies in non-mortgage consumer credit and a general decline in consumer confidence. These conditions continued and worsened in 2008, causing a loss of confidence in the broader U.S. and global credit and financial markets and resulting in the collapse of, and government intervention in, major banks, financial institutions and insurers and creating a climate of greater volatility, less liquidity, widening of credit spreads, a lack of price transparency, increased credit losses and tighter credit conditions. Notwithstanding various actions by the U.S. and foreign governments, concerns about the general condition of the capital markets, financial instruments, banks, investment banks, insurers and other financial institutions caused the broader credit markets to further deteriorate and stock markets to decline substantially. In addition, general economic indicators have deteriorated, including declining consumer sentiment, increased unemployment and declining economic growth and uncertainty about corporate earnings.

These unprecedented disruptions in the current credit and financial markets have had a significant material adverse impact on a number of financial institutions and several financial institutions have either gone into bankruptcy or have had to be rescued by governmental authorities. Access to capital and credit has been negatively impacted. These disruptions could, among other things, make it more difficult for the Company to obtain, or increase its cost of obtaining, capital and financing for its operations. The Company’s access to additional capital may not be available on terms acceptable to it or at all. Failure to raise capital when needed or on reasonable terms may have a material adverse effect on the Company’s business, financial condition and results of operations. In addition, recent market events and conditions have significantly raised the risk of counterparty default. The Company is subject to counterparty risk and may be impacted in the event that a counterparty, including suppliers and joint venture partners, becomes insolvent.

Page 21

These factors, as well as other related factors, may cause decreases in asset values that are deemed to be other than temporary, which may result in impairment losses. If such increased levels of volatility and market turmoil continue, the Company’s operations could be adversely impacted and the trading price of the Common Shares may be adversely affected.

Mining tax regimes in foreign jurisdictions are subject to differing interpretations and are subject to constant change.

Mining tax regimes in foreign jurisdictions are subject to differing interpretations and are subject to constant change and may include fiscal stability guarantees. The Company’s interpretation of taxation law as applied to its transactions and activities may not coincide with that of the tax authorities. As a result, transactions may be challenged by tax authorities and the Company’s operations may be assessed, which could result in significant additional taxes, penalties and interest.

The violation by the Company of covenants contained in the 2010 Amended Credit Facility may cause the Company to be in default under the terms of the facility.

The 2010 Amended Credit Facility contains certain limits, such as, the Company’s ability to incur additional indebtedness, enter into derivative transactions, make investments in a business, or carry on business, unrelated to mining, dispose of the Company’s material assets or, in certain circumstances, pay dividends. Further, the 2010 Amended Credit Facility requires the Company to maintain specified financial ratios and meet financial condition covenants. Events beyond the Company’s control, including changes in general economic and business conditions, may affect the Company’s ability to satisfy these covenants, which could result in a default under the 2010 Amended Credit Facility. As at March 31, 2010, there were no funds drawn against the 2010 Amended Credit Facility. Depending on its cash position and cash requirements, the Company may draw on the 2010 Amended Credit Facility to fund part of the capital expenditures required in connection with its current development projects. If an event of default under the 2010 Amended Credit Facility occurs, the Company would be unable to draw down further on the 2010 Amended Credit Facility and the lenders could elect to declare all principal amounts outstanding thereunder at such time, together with accrued interest, to be immediately due. An event of default under the 2010 Amended Credit Facility may also give rise to an event of default under existing and future debt agreements and, in such event, the Company may not have sufficient funds to repay amounts owing under such agreements.

The Company’s fair value estimates with respect to the carrying amount of mineral interests (including goodwill) are based on numerous assumptions and may differ significantly from actual fair values.

The Company evaluates the carrying amount of mineral interests (including goodwill) to determine whether current events and circumstances indicate such carrying amount may no longer be supportable, which becomes more of a risk in the global economic conditions that exist currently. The fair values of its reporting units are based, in part, on certain factors that may be partially or totally outside of the Company’s control.

Page 22

This evaluation involves a comparison of the estimated fair value of the Company’s reporting units to their carrying values. The Company’s fair value estimates are based on numerous assumptions and may differ from actual fair values and these differences may be significant and could have a material effect on the Company’s financial position and results of operation. If the Company fails to achieve its valuation assumptions or if any of its reporting units experiences a decline in its fair value, then this may result in an impairment charge, which would reduce the Company’s earnings.

Fluctuations in exchange rates of currencies directly impact the earnings of the Company.

Currency fluctuations may affect the revenues which the Company will realize from its operations since gold is sold in the world market in United States dollars. The costs of the Company are incurred principally in Canadian dollars, United States dollars, Euros and CFA francs. The appreciation of non-U.S. dollar currencies against the U.S. dollar increases the cost of gold production in U.S. dollar terms. While CFA francs currently have a fixed exchange rate to the euro and are currently convertible into Canadian and United States dollars, they may not always have a fixed exchange rate or be convertible in the future.

The Company is affected by movements in interest rates.

The Company is affected by movements in interest rates. Interest payments under the 2010 Amended Credit Facility are subject to fluctuation based on changes to specified interest rates. See the discussion below under the heading “Material Contracts – 2010 Amended Credit Facility”. A copy of the credit agreement in connection with the 2010 Amended Credit Facility is available under the Company’s profile on SEDAR atwww.sedar.com.

There are risks associated with being a multinational company.

The Company is a multinational company that conducts operations through mainly foreign subsidiaries, foreign companies and joint ventures, and substantially all of the assets of Company consist of equity in these entities. Accordingly, any limitations, or the perception of limitations, on transfer of cash or other assets between the parent company and these entities, or among these entities, could restrict the Company’s ability to fund its operations efficiently, or to repay its debts, and could impact negatively the Company’s valuation and share price.

The use of derivative instruments involves certain inherent risks including credit risk market liquidity risk and unrealized mark-to-market risk.

While the Company generally does not employ hedge (or derivative) products in respect of mineral production, the Company may from time to time employ hedge (or derivative) products in respect of other commodities, interest rates and/or currencies. Hedge (or derivative) products are generally used to manage the risks associated with, among other things, mineral price volatility, changes in commodity prices, interest rates, foreign currency exchange rates and energy prices. Where the Company holds such derivative

Page 23

positions, the Company will deliver into such arrangements in the prescribed manner. The use of derivative instruments involves certain inherent risks including: (a) credit risk – the risk of default on amounts owing to the Company by the counterparties with which the Company has entered into such transactions; (b) market liquidity risk – the risk that the Company has entered into a derivative position that cannot be closed out quickly, by either liquidating such derivative instrument or by establishing an offsetting position; and (c) unrealized mark-to-market risk – the risk that, in respect of certain derivative products, an adverse change in market prices for commodities, currencies or interest rates will result in the Company incurring an unrealized mark-to-market loss in respect of such derivative products.

In the case of a gold option based forward sales program, if the metal price rises above the price at which future production has been committed under an option based forward sales hedge program, the Company may have an opportunity loss. If the metal price falls below that committed price under an option based forward sales hedge program, revenues will be protected to the extent of such committed production. There can be no assurance that the Company will be able to achieve future realized prices for metal prices that may exceed the option based forward sales hedge program.

Operational Risks

The Company’s mineral reserves and mineral resources are estimates, and no assurance can be given that the estimated reserves and resources are accurate or that the indicated level of gold will be produced.

Reserves are statistical estimates of mineral content and ore based on limited information acquired through drilling and other sampling methods and require judgmental interpretations of geology. Successful extraction requires safe and efficient mining and processing. The Company’s mineral reserves and mineral resources are estimates, and no assurance can be given that the estimated reserves and resources are accurate or that the indicated level of gold will be produced. Such estimates are, in large part, based on interpretations of geological data obtained from drill holes and other sampling techniques. Actual mineralization or formations may be different from those predicted. Further, it may take many years from the initial phase of drilling before production is possible, and during that time the economic feasibility of exploiting a discovery may change. Mineral resource estimates for properties that have not commenced production are based, in many instances, on limited and widely spaced drill hole information, which is not necessarily indicative of the conditions between and around drill holes. Accordingly, such mineral resource estimates may require revision as more drilling information becomes available or as actual production experience is gained. It cannot be assumed that all or any part of the Company’s mineral resources constitute or will be converted into reserves. Market price fluctuations of gold or niobium, as applicable, as well as increased production and capital costs or reduced recovery rates, may render the Company’s proven and probable reserves unprofitable to develop at a particular site or sites for periods of time or may render mineral reserves containing relatively lower grade mineralization uneconomic. Moreover, short-term operating factors relating to the mineral reserves, such as the need for the orderly development of ore bodies or the processing of new or different ore grades, may cause

Page 24

mineral reserves to be reduced or the Company to be unprofitable in any particular accounting period. Estimated reserves may have to be recalculated based on actual production experience. Any of these factors may require the Company to reduce its mineral reserves and resources, which could have a negative impact on the Company’s financial results. Failure to obtain necessary permits or government approvals could also cause the Company to reduce its reserves. There is also no assurance that the Company will achieve indicated levels of gold or niobium recovery or obtain the prices for gold or niobium production assumed in determining the amount of such reserves. Level of production may also be affected by weather or supply shortages. The SEC does not permit mining companies in their filings with the SEC to disclose estimates other than mineral reserves. However, because the Company prepares its disclosure in accordance with Canadian disclosure requirements, the Company’s disclosure contains resource estimates in addition to reserve estimates, in accordance with NI 43-101. See the discussion above under the heading “Cautionary Note to U.S. Investors Regarding Mineral Reporting Standards”.

The Company must continually replace reserves depleted by production to maintain production levels over the long term.

The Company must continually replace reserves depleted by production to maintain production levels over the long term. The life-of-mine estimates for each of the material properties of the Company are based on a number of factors and assumptions and may prove to be incorrect. In addition, mine life would be shortened if we expand production. Reserves can be replaced by expanding known ore bodies, locating new deposits or making acquisitions. Exploration is highly speculative in nature. The Company’s exploration projects involve many risks and are frequently unsuccessful. Once a site with mineralization is discovered, it may take several years from the initial phases of drilling until production is possible, during which time the economic feasibility of production may change. Substantial expenditures are required to establish proven and probable reserves and to construct mining and processing facilities. As a result, there is no assurance that current or future exploration programs will be successful. There is a risk that depletion of reserves will not be offset by discoveries or acquisitions. The mineral base of the Company may decline if reserves are mined without adequate replacement and the Company may not be able to sustain production beyond the current mine lives, based on current production rates.

The ability of the Company to sustain or increase its present levels of gold production is dependent in part on the success of its projects, which are subject to numerous known and unknown risks.

The ability of the Company to sustain or increase its present levels of gold production is dependent in part on the success of its projects. Risks and unknowns inherent in all projects include: the accuracy of reserve estimates; metallurgical recoveries; capital and operating costs of such projects; and the future prices of the relevant minerals. Projects have no operating history upon which to base estimates of future cash flow. The capital expenditures and time required to develop new mines or other projects are considerable and changes in costs or construction schedules can affect project economics. It is not unusual in the mining industry for new mining operations to experience unexpected

Page 25

problems during the start-up phase, resulting in delays and requiring more capital than anticipated. Actual costs and economic returns may differ materially from the Company’s estimates or the Company could fail to obtain the governmental approvals necessary for the operation of a project, in which case, the project may not proceed, either on its original timing, or at all.

Reserve and resource calculations may be over/underestimated as a result of coarse gold at the Essakane Project.

The Essakane project is a “coarse gold” deposit with particles up to five millimetres in diameter. Attempts have been made to ensure that the grade samples used to determine mineral reserves and resources are representative by using various sample preparation and analytical techniques and by re-assaying many of the earlier samples using these sample preparation and analytical techniques. The grade of the deposit could be lower or higher than predicted by the grade model developed for the feasibility study and included in the Essakane Report.

The Company is subject to continuously evolving legislation, which may have unknown and negative impact on operations.