UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x | Filed by a Party other than the Registrant o | ||

| Check the appropriate box: | |||

o | Preliminary Proxy Statement | ||

x | Definitive Proxy Statement | o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

o | Definitive Additional Materials | ||

o | Soliciting Material Pursuant to §240.14a-12 | ||

MPG OFFICE TRUST, INC.

(Name of Registrant as Specified In Its Charter)

Payment of Filing Fee (Check the appropriate box):

x | No fee required. | |

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |

| (1) | Title of each class of securities to which transaction applies: | |

| (2) | Aggregate number of securities to which transaction applies: | |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): | |

| (4) | Proposed maximum aggregate value of transaction: | |

| (5) | Total fee paid: | |

o | Fee paid previously with preliminary materials. | |

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |

| (1) | Amount Previously Paid: | |

| (2) | Form, Schedule or Registration Statement No.: | |

| (3) | Filing Party: | |

| (4) | Date Filed: | |

June 14, 2012

Dear Stockholder:

You are invited to attend the 2012 Annual Meeting of Stockholders (the “Annual Meeting”) of MPG Office Trust, Inc. (the “Company”), to be held on Friday, July 27, 2012, at 8:00 A.M., local time, at the Omni Los Angeles Hotel, 251 South Olive Street, Los Angeles, California 90012 for holders of common stock, par value $0.01 per share, or 7.625% Series A Cumulative Redeemable Preferred Stock, par value $0.01 per share, of the Company.

The purposes of this year’s meeting are to:

Common Stock—

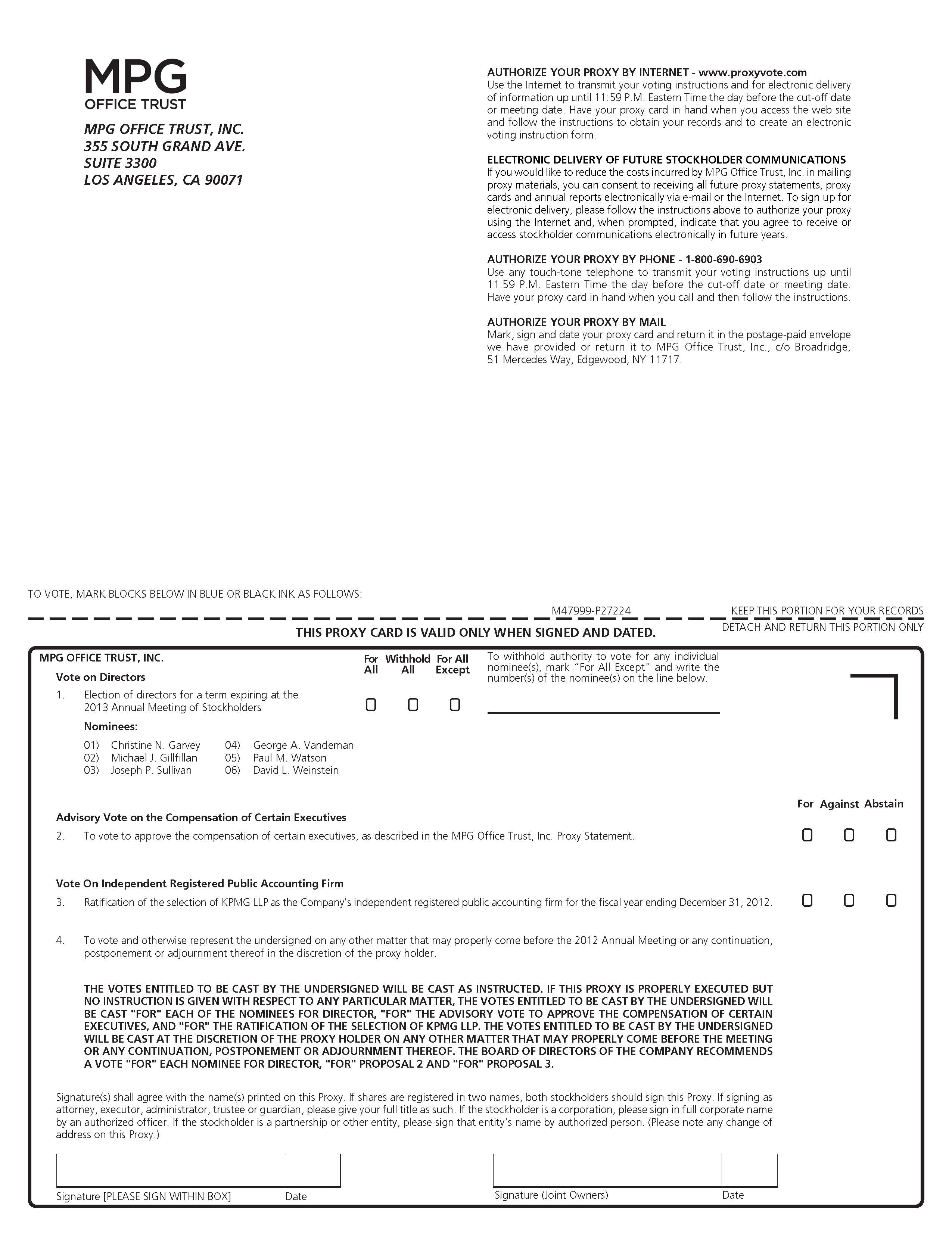

| (i) | Elect directors to serve until the 2013 Annual Meeting of Stockholders and until their successors are duly elected and qualify; |

| (ii) | Consider and vote on a resolution to approve, on an advisory (non-binding) basis, the compensation of certain executives of the Company (“say-on-pay vote”); |

| (iii) | Ratify the selection of the Company’s independent registered public accounting firm for the fiscal year ending December 31, 2012; and |

| (iv) | Transact such other business as may properly come before the meeting or any continuation, postponement or adjournment thereof. |

Series A Preferred Stock—

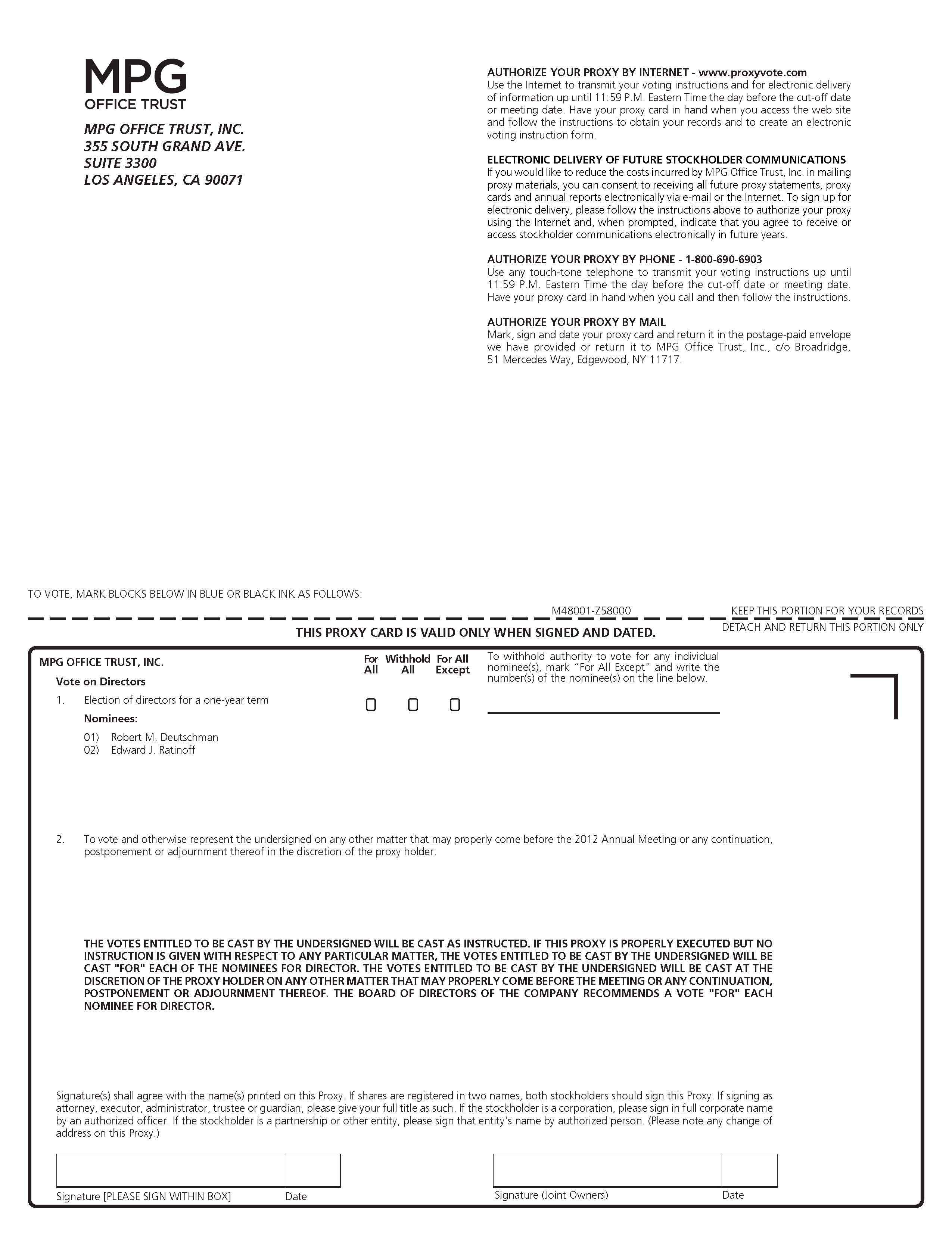

| (i) | Elect directors to serve a one-year term and until their successors are duly elected and qualify or, if earlier, until the full payment (or setting aside for payment) of all dividends on the Series A preferred stock that are in arrears, as wells as dividends for the then current period. |

The accompanying Notice of Annual Meeting and Proxy Statement describe these matters. We urge you to read this information carefully.

Page 2

June 14, 2012

It is important that your shares be represented and voted whether or not you plan to attend the Annual Meeting in person. If you choose not to attend and vote at the Annual Meeting in person, you may authorize your proxy on the Internet, or if you are receiving a paper copy of this Proxy Statement, by telephone or by completing and mailing a proxy card. Authorizing your proxy over the Internet, by telephone or by mailing a proxy card will ensure that your shares are represented at the Annual Meeting. Please review the instructions contained in the Notice of Internet Availability of Proxy Materials regarding each of these options.

Sincerely,

David L. Weinstein

President and Chief Executive Officer

NOTICE OF 2012 ANNUAL MEETING OF STOCKHOLDERS

TO BE HELD ON JULY 27, 2012

June 14, 2012

TO THE STOCKHOLDERS OF MPG OFFICE TRUST, INC.:

NOTICE IS HEREBY GIVEN that the 2012 Annual Meeting of Stockholders (the “Annual Meeting”) of MPG Office Trust, Inc., a Maryland corporation (the “Company”), will be held on Friday, July 27, 2012, at 8:00 A.M., local time, at the Omni Los Angeles Hotel, 251 South Olive Street, Los Angeles, California 90012, for holders of common stock, par value $0.01 per share, or 7.625% Series A Cumulative Redeemable Preferred Stock, par value $0.01 per share, of the Company to consider and vote on the following matters:

Common Stock—

| • | The election of six directors to serve until the 2013 Annual Meeting of Stockholders and until their successors are duly elected and qualify; |

| • | A resolution to approve, on an advisory (non-binding) basis, the compensation of certain executives of the Company, as more fully described in the accompanying Proxy Statement (“say-on-pay vote”); |

| • | The ratification of the selection of KPMG LLP as the Company’s independent registered public accounting firm for the fiscal year ending December 31, 2012; and |

| • | The transaction of such other business as may properly come before the meeting or any continuation, postponement or adjournment thereof. |

Series A Preferred Stock—

| • | The election of two directors to serve a one-year term and until their successors are duly elected and qualify or, if earlier, until the full payment (or setting aside for payment) of all dividends on the Series A preferred stock that are in arrears, as wells as dividends for the then current period. |

Our Board of Directors (the “Board”) has fixed the close of business on May 24, 2012 as the record date for the determination of stockholders entitled to notice of, and to vote at, the Annual Meeting and at any continuation, postponement or adjournment thereof.

Page 2

June 14, 2012

Proxies are being solicited by our Board, which recommends that our stockholders vote: FOR the election of the Board’s nominees named in the accompanying Proxy Statement; FOR the resolution to approve the compensation of certain executives of the Company; and FOR the ratification of the selection of KPMG LLP as the Company’s independent registered public accounting firm for the fiscal year ending December 31, 2012. Please refer to the attached Proxy Statement, which forms a part of this Notice of Annual Meeting and is incorporated herein by reference, for further information with respect to the business to be transacted at the Annual Meeting.

Stockholders are cordially invited to attend the Annual Meeting in person. Your vote is important. If you are viewing the Proxy Statement on the Internet, you may authorize your proxy electronically via the Internet by following the instructions on the Notice of Internet Availability of Proxy Materials mailed to you and the instructions listed on the Internet site. If you are receiving a paper copy of the Proxy Statement, you may authorize your proxy by completing and mailing the proxy card enclosed with the Proxy Statement, or you may authorize your proxy electronically via the Internet or by telephone by following the instructions on the proxy card. If your shares are held in “street name,” which means shares held of record through a broker, bank or other nominee, you should review the Notice of Internet Availability of Proxy Materials used by that firm to determine whether and how you will be able to authorize your proxy by telephone or over the Internet. Authorizing a proxy over the Internet, by telephone or by mailing a proxy card will ensure that your shares are represented at the Annual Meeting.

By Order of the Board of Directors,

Jonathan L. Abrams

Secretary

MPG OFFICE TRUST, INC.

355 South Grand Avenue, Suite 3300

Los Angeles, California 90071

____________________

PROXY STATEMENT

____________________

INFORMATION CONCERNING VOTING AND SOLICITATION

General

This Proxy Statement is furnished in connection with the solicitation by the Board of Directors (the “Board”) of MPG Office Trust, Inc., a Maryland corporation (the “Company”), of proxies from the holders of the Company’s issued and outstanding shares of common stock, par value $0.01 per share (the “common stock”) and 7.625% Series A Cumulative Redeemable Preferred Stock, $0.01 par value per share (the “Series A preferred stock”), to be exercised at the 2012 Annual Meeting of Stockholders (the “Annual Meeting”) to be held on Friday, July 27, 2012, at 8:00 A.M., local time, or at any continuation, postponement or adjournment thereof, for the purposes set forth in the accompanying Notice of Annual Meeting and as further discussed in this Proxy Statement. Proxies are solicited to give all stockholders of record an opportunity to vote on matters properly presented at the Annual Meeting and on which they are entitled to vote. The Annual Meeting will be held at the Omni Los Angeles Hotel, 251 South Olive Street, Los Angeles, California 90012.

Pursuant to the rules of the Securities and Exchange Commission (the “SEC”), we have elected to provide access to our proxy materials over the Internet. Accordingly, we are sending a Notice of Internet Availability of Proxy Materials (a “Notice”) to our stockholders of record, while brokers and other nominees who hold shares on behalf of beneficial owners will be sending their own similar Notice. All stockholders will have the ability to access proxy materials on the website referred to in the Notice or request to receive a printed set of the proxy materials. Instructions on how to request a printed copy by mail or electronically may be found in the Notice and on the website referred to in the Notice, including an option to request paper copies on an ongoing basis. We intend to make this Proxy Statement available on the Internet and to mail the Notice to all stockholders entitled to vote at the Annual Meeting on June 14, 2012. We intend to mail this Proxy Statement, together with a proxy card, to those stockholders entitled to vote at the Annual Meeting who have properly requested paper copies of such materials, within three business days of receipt of such request.

Who Can Vote

Common Stock—

You are entitled to vote in the election of six directors and on each other matter properly presented at the Annual Meeting (other than the election of two directors by the holders of Series A preferred stock) if you were a holder of record of our common stock as of the close of business on May 24, 2012, the record date for the determination of stockholders entitled to notice of and to vote at the Annual Meeting. Your shares can be voted at the Annual Meeting only if you are present in person or represented by a valid proxy. At the close of business on the record date, 50,794,133 shares of common stock were outstanding and entitled to vote.

Series A Preferred Stock—

You are entitled to vote in the election of two directors if you were a holder of record of our Series A preferred stock as of the close of business on May 24, 2012, the record date for the determination of stockholders entitled to notice of and to vote at the Annual Meeting. Your shares can be voted at the Annual Meeting only if you are present in person or represented by a valid proxy. At the close of business on the record date, 9,730,370 shares of Series A preferred stock were outstanding and entitled to vote.

1

Voting of Shares

Holders of record of common stock as of the close of business on May 24, 2012 are entitled to one vote for each of the six directors to be elected at the Annual Meeting by the holders of common stock and one vote on each other matter to be voted upon at the Annual Meeting (other than the election of two directors by the holders of Series A preferred stock).

Holders of record of Series A preferred stock as of the close of business on May 24, 2012 are entitled to one vote for each of the two directors to be elected at the Annual Meeting by the holders of Series A preferred stock.

You may vote by attending the Annual Meeting and voting in person or you may vote by authorizing a proxy. The method of voting by proxy differs (1) depending on whether you are viewing this Proxy Statement on the Internet or are receiving a paper copy, and (2) for shares held as a record holder and shares held in “street name.” If you hold your shares of stock as a record holder and you are viewing this Proxy Statement on the Internet, you may vote by authorizing a proxy over the Internet by following the instructions on the website referred to in the Notice previously mailed to you. If you hold your shares of stock as a record holder and you are receiving a paper copy of this Proxy Statement, you may vote your shares by completing, dating and signing the proxy card included with the Proxy Statement and promptly returning it in the pre-addressed, postage paid envelope provided to you, or by authorizing a proxy over the Internet or by telephone by following the instructions on the proxy card. If you hold your shares of stock in street name, which means your shares are held of record through a broker, bank or nominee, you will receive a Notice from your broker, bank or nominee that includes instructions on how to vote your shares. Your broker, bank or nominee will allow you to deliver your voting instructions over the Internet and may also permit you to authorize your proxy by telephone. In addition, you may request paper copies of the Proxy Statement and proxy card from your broker by following the instructions on the Notice provided to you by your broker.

The Internet and telephone voting facilities will close at 11:59 P.M., Eastern Time, on July 26, 2012. If you authorize your proxy through the Internet, you should be aware that you may incur costs to access the Internet, such as usage charges from telephone companies or Internet service providers, and that these costs must be borne by you. If you authorize your proxy by Internet or telephone, then you do not need to return a proxy card by mail.

All shares entitled to vote and represented by properly executed proxies received before the polls are closed at the Annual Meeting, and which proxies have not been revoked or superseded, will be voted at the Annual Meeting in accordance with the instructions indicated on those proxies. YOUR VOTE IS IMPORTANT.

Proxy Card and Revocation of Proxy

If you sign the proxy card but do not specify how you want your shares to be voted, your shares will be voted by the proxy holders named in the enclosed proxy (1) in the case of common stock, for the election of the six individuals nominated for election as directors by the holders of common stock, for the resolution to approve the compensation of certain executives of the Company, and for the ratification of the selection of KPMG LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2012 and (2) in the case of Series A preferred stock, for the election of the two individuals nominated for election as directors by the holders of Series A preferred stock. At their discretion, the proxy holders named in the enclosed proxy are authorized to vote on any other matters that may properly come before the Annual Meeting and at any continuation, postponement or adjournment thereof. The Board knows of no other items of business that will be presented for consideration at the Annual Meeting other than those described in this Proxy Statement. In addition, no stockholder proposals or nominations were received on a timely basis, and therefore no such matters may be brought to a vote at the Annual Meeting.

2

If you authorize a proxy, you may revoke that proxy at any time before it is voted at the Annual Meeting. You may revoke your proxy by sending a written notice of revocation or a duly executed proxy bearing a later date to the attention of Jonathan L. Abrams, Secretary, MPG Office Trust, Inc., 355 South Grand Avenue, Suite 3300, Los Angeles, California 90071, or by attending the Annual Meeting and voting in person. Attendance at the Annual Meeting will not, by itself, revoke a proxy.

Quorum; Counting of Votes

In order for there to be a vote on any matter at the Annual Meeting, there must be a quorum. In order to have a quorum for the transaction of business by the holders of common stock, holders of common stock entitled to cast a majority of all the votes entitled to be cast by the holders of common stock at the Annual Meeting must be present in person or by proxy. In order to have a quorum for the transaction of business by the holders of Series A preferred stock, holders of Series A preferred stock entitled to cast one-third of all the votes entitled to be cast by the holders of Series A preferred stock must be present in person or by proxy. In determining whether we have a quorum, shares held by persons attending the Annual Meeting but not voting, shares represented by proxies that reflect abstentions or withheld votes as to a particular proposal and broker “non-votes” will be counted as present for purposes of determining a quorum. A broker “non-vote” occurs when a broker or other nominee holding shares for a beneficial owner has not received instructions from the beneficial owner and does not have discretionary authority to vote the shares. If we fail to obtain a quorum for the transaction of business by the holders of either common stock or Series A preferred stock at the Annual Meeting, the chair of the Annual Meeting or the holders of a majority of shares of common stock or Series A preferred stock, as the case may be, present in person or by proxy, may adjourn the meeting to another place, date or time.

All votes will be tabulated by the inspector of election appointed for the Annual Meeting, a representative of Broadridge Financial Solutions, Inc., who will separately tabulate affirmative and negative votes and abstentions. We expect to pay Broadridge Financial Solutions, Inc. a fee of approximately $2,500 for these services.

Votes Required to Elect Directors and Adopt Other Proposals

In order to be elected as a director by the holders of common stock, a nominee must receive a plurality of all the votes cast by the holders of common stock at the Annual Meeting. The affirmative vote of a majority of the votes cast by the holders of common stock at the Annual Meeting is required for approval of the resolution to approve the compensation of certain executives of the Company and the ratification of the selection of KPMG LLP as our independent registered public accounting firm. In order to be elected as a director by the holders of Series A preferred stock, a nominee must receive a plurality of all the votes cast by the holders of Series A preferred stock at the Annual Meeting.

For purposes of calculating votes cast in the election of directors, votes withheld will not be counted as votes cast “for” or “against” a director and will have no effect on the election of directors. For purposes of calculating votes cast on the resolution to approve the compensation of certain executives of the Company and the ratification of the selection of KPMG LLP as our independent registered public accounting firm, abstentions or broker non-votes will not be counted as votes cast “for” or “against” a proposal and will have no effect on the result of such proposal.

3

Solicitation of Proxies

We will bear the entire cost of solicitation of proxies. These costs will include reimbursements paid to brokerage firms and others for their expenses incurred in forwarding solicitation material regarding the Annual Meeting to beneficial owners of the common stock and Series A preferred stock. Proxies may be solicited by directors, officers and employees of the Company in person or by mail, telephone, e-mail or facsimile transmission. No additional compensation will be paid to such directors, officers or employees for these services. In addition, we have retained MacKenzie Partners, Inc., a firm specializing in proxy solicitation, to solicit proxies and assist in the distribution and collection of proxy materials. We expect to pay MacKenzie Partners, Inc. a fee of approximately $10,000 for these services.

_________________

NO PERSON IS AUTHORIZED ON OUR BEHALF TO GIVE ANY INFORMATION OR TO MAKE ANY REPRESENTATIONS WITH RESPECT TO THE PROPOSALS TO BE VOTED ON AT THE ANNUAL MEETING, OTHER THAN THE INFORMATION AND REPRESENTATIONS CONTAINED IN THIS PROXY STATEMENT, AND, IF GIVEN OR MADE, SUCH INFORMATION AND/OR REPRESENTATIONS MUST NOT BE RELIED UPON AS HAVING BEEN AUTHORIZED. THE DELIVERY OF THIS PROXY STATEMENT SHALL UNDER NO CIRCUMSTANCES CREATE ANY IMPLICATION THAT THERE HAS BEEN NO CHANGE IN OUR AFFAIRS SINCE THE DATE OF THIS PROXY STATEMENT.

Our principal executive offices are located at 355 South Grand Avenue, Suite 3300, Los Angeles, California 90071, our telephone number is (213) 626-3300 and our website is located at http:// www.mpgoffice.com.1 References herein to the “Company” refer to MPG Office Trust, Inc. and its subsidiaries, unless the context indicates otherwise.

_________________

The date of this Proxy Statement is June 14, 2012.

__________

1 | Website addresses referred to in this Proxy Statement are not intended to function as hyperlinks, and the information contained on our website is not a part of this Proxy Statement. |

4

ITEM 1

ELECTION OF DIRECTORS

Under our charter and the Fourth Amended and Restated Bylaws (the “Bylaws”), other than with respect to our Preferred Directors (as described below under the heading “—Information Regarding Preferred Directors”), each member of the Board serves until the next annual meeting of stockholders and until his or her successor is duly elected and qualifies. Vacancies among directors elected by the holders of common stock may be filled only by individuals elected by a majority of the remaining directors. A director elected by the Board to fill a vacancy (including a vacancy created by an increase in the size of the Board) will serve until the next annual election of directors and until such director’s successor is elected and qualifies, or until such director’s earlier death, resignation or removal.

Information Regarding Common Directors

Directors are elected by a plurality of the votes cast at the Annual Meeting, which means the six individuals nominated for election as directors by the holders of common stock who receive the largest number of properly cast votes by the holders of common stock will be elected as directors. Each share of common stock is entitled to one vote for each of the six director nominees. Cumulative voting is not permitted. It is the intention of the proxy holders named in the enclosed proxy to vote the proxies received by them for the election of the nominees named below unless authorization to do so is withheld. If any nominee should become unavailable for election prior to the Annual Meeting, an event which the Board does not currently anticipate, the proxies will be voted for the election of a substitute nominee or nominees proposed by the Board.

Ms. Christine N. Garvey and Messrs. Michael J. Gillfillan, Joseph P. Sullivan, George A. Vandeman, Paul M. Watson and David L. Weinstein are our nominees for election to the Board by the holders of common stock. Each nominee has consented to be named in this Proxy Statement and to serve as a director if elected, and our management has no reason to believe that any nominee will be unable to serve. The information below relating to the nominees for election as directors by the holders of common stock has been furnished to us by the respective individuals. If elected at the Annual Meeting, Ms. Garvey and Messrs. Gillfillan, Sullivan, Vandeman, Watson and Weinstein would each serve until the 2013 Annual Meeting of Stockholders (the “2013 Annual Meeting”) and until their respective successors are duly elected and qualify.

The following table sets forth information regarding the individuals who are our nominees for election as directors of the Company by the holders of common stock:

| Name | Age | Position | Director Since | |||

| Christine N. Garvey | 66 | Director | 2008 | |||

| Michael J. Gillfillan | 64 | Director | 2009 | |||

| Joseph P. Sullivan | 69 | Director | 2009 | |||

| George A. Vandeman | 72 | Director | 2007 | |||

| Paul M. Watson | 72 | Chairman of the Board | 2008 | |||

| David L. Weinstein | 45 | Director (also President and Chief Executive Officer) | 2008 | |||

Christine N. Garvey has served on the Board since July 2008. Ms. Garvey retired from Deutsche Bank AG in May 2004, where she served as Global Head of Corporate Real Estate Services from May 2001. From December 1999 to April 2001, Ms. Garvey served as Vice President, Worldwide Real Estate and Workplace Resources for Cisco Systems, Inc. During her career, Ms. Garvey also held several positions with Bank of America, including Group Executive Vice President and Head of National Commercial Real Estate Services. Ms. Garvey holds a Bachelor of Arts degree, magna cum laude, from Immaculate Heart College in Los Angeles

5

and a Juris Doctor from Suffolk University Law School. She is currently a member of the board of directors of HCP, Inc., ProLogis, Toll Brothers, Inc. and UnionBanCal Corporation. She also served on the board of directors of Hilton Hotels Corporation until the company was taken private in October 2007. Our Board and Nominating and Corporate Governance Committee nominated Ms. Garvey to serve as a director based, among other factors, on her real estate experience and commercial banking expertise.

Michael J. Gillfillan has served on the Board since May 2009. Since April 2011, Mr. Gillfillan has been Chairman and Chief Executive Officer of Alostar Bank of Commerce. From December 2002 to December 2010, Mr. Gillfillan was a partner of Meriturn Partners, LLC, a private equity fund that purchases controlling interests in distressed middle market manufacturing and distribution companies. From March 2000 to January 2002, Mr. Gillfillan was a partner of Neveric, LLC. Mr. Gillfillan is the retired Vice Chairman and Chief Credit Officer of Wells Fargo Bank, N.A., where he was responsible for all facets of credit risk management, including direct oversight of the loan workout units that had peak problem assets in excess of $7 billion. During his tenure at Wells Fargo Bank, he also served as Vice Chairman and Group Head of the Commercial & Corporate Banking Group and Executive Vice President, Loan Adjustment Group, where he was responsible for marketing and servicing all bank loans, deposits and capital market products, as well as managing the loan workout function for the bank. Mr. Gillfillan holds a Bachelor of Arts degree from the University of California, Berkeley and a Master of Business Administration from the University of California, Los Angeles. He previously served on the board of directors of James Hardie Industries Limited and UnionBanCal Corporation. Our Board and Nominating and Corporate Governance Committee nominated Mr. Gillfillan to serve as a director based, among other factors, on his extensive experience in workouts and company turnarounds.

Joseph P. Sullivan has served on the Board since May 2009. Since 2003, Mr. Sullivan has been a private investor. Mr. Sullivan is the Chairman of the Board of Advisors of RAND Health, the largest non-profit institution dedicated to emerging health policy issues. From March 2000 through March 2003, Mr. Sullivan served as Chairman of the Board and Chief Executive Officer of Protocare, Inc., a health care clinical trials and consulting organization. Mr. Sullivan was Chairman of the Board, Chief Executive Officer and President of American Health Properties, Inc., a publicly-traded real estate investment trust (“REIT”) on the New York Stock Exchange (“NYSE”), from 1993 until it was acquired by HCP, Inc. in 1999. Mr. Sullivan has 20 years of investment banking experience with Goldman, Sachs & Co. Mr. Sullivan holds a Bachelor of Science degree and a Juris Doctor from the University of Minnesota Law School and a Master of Business Administration from the Harvard Graduate School of Business Administration. He serves as a member, and previously as Chairman, of the Board of Advisors for UCLA Medical Center. He is also a member of the board of directors of Amylin Pharmaceuticals, Inc., Cigna Corporation, and HCP, Inc. Our Board and Nominating and Corporate Governance Committee nominated Mr. Sullivan to serve as a director based, among other factors, on his investment banking expertise and experience in the real estate industry and with REITs.

George A. Vandeman has served on the Board since October 2007 and as Chairman of the Board from October 2008 to July 2009. Mr. Vandeman has been the principal of Vandeman & Co., a private investment firm, since he retired from Amgen, Inc. in July 2000. From 1995 to 2000, Mr. Vandeman was Senior Vice President and General Counsel of Amgen and a member of its Operating Committee. Immediately prior to joining Amgen in July 1995, Mr. Vandeman was a senior partner and head of the Mergers and Acquisitions Practice Group at the international law firm of Latham & Watkins LLP, where he worked for nearly three decades. Mr. Vandeman holds a Bachelor of Arts degree and a Juris Doctor from the University of Southern California. Mr. Vandeman is a member and past Chair of the Board of Councilors at the University of Southern California Law School. Mr. Vandeman is a former director of Rexair LLC, SymBio Pharmaceuticals Limited and ValueVision Media. Our Board and Nominating and Corporate Governance Committee nominated Mr. Vandeman to serve as a director based, among other factors, on his legal and corporate governance expertise and experience with complex strategic transactions.

6

Paul M. Watson has served on the Board since July 2008 and as Chairman of the Board since July 2009. Mr. Watson is the retired Vice Chairman of Wells Fargo Bank N.A., where he was responsible for wholesale and commercial banking, and headed Wells Fargo’s nationwide commercial, corporate and treasury management businesses. Prior to his 45-year tenure at Wells Fargo, Mr. Watson served as 1st Lieutenant in the United States Army. Mr. Watson holds a Bachelor of Arts degree from the University of San Francisco and a certificate from the Graduate School of Credit and Financial Management at Stanford University. Mr. Watson is the Chairman of the Finance Council of the Roman Catholic Archdiocese of Los Angeles. Mr. Watson is a director emeritus of the Hanna Boys Center and the Music Center of Los Angeles County. He previously served as a director of NorCal Environmental Corp. from February 2004 to September 2007. Our Board and Nominating and Corporate Governance Committee nominated Mr. Watson to serve as a director based, among other factors, on his commercial banking expertise.

David L. Weinstein has served as our President and Chief Executive Officer since November 2010 and as a member of our Board since August 2008. Since September 2008, Mr. Weinstein has been a partner at Belvedere Capital, a real estate investment firm based in New York. He remains a partner with limited responsibilities. From April 2007 until August 2008, Mr. Weinstein was a Managing Director of Westbridge Investment Group/Westmont Hospitality Group, a real estate investment fund focused on hospitality. From 1996 until January 2007, Mr. Weinstein worked at Goldman, Sachs & Co. in New York, first as a Vice President in the real estate investment banking group (focusing on mergers, asset sales and corporate finance) and then from 2004 as a Vice President in the Special Situations Group (focused on real estate debt investments). Mr. Weinstein holds a Bachelor of Science degree in Economics, magna cum laude, from The Wharton School and a Juris Doctor, cum laude, from the University of Pennsylvania Law School. He is a member of the New York State Bar Association. Our Board and Nominating and Corporate Governance Committee nominated Mr. Weinstein to serve as a director based, among other factors, on his knowledge of the Company, investment banking expertise and experience in the real estate industry.

OUR BOARD RECOMMENDS A VOTE “FOR” THE ELECTION OF EACH OF MS. GARVEY AND MESSRS. GILLFILLAN, SULLIVAN, VANDEMAN, WATSON AND WEINSTEIN TO SERVE ON OUR BOARD UNTIL THE 2013 ANNUAL MEETING AND UNTIL THEIR RESPECTIVE SUCCESSORS ARE DULY ELECTED AND QUALIFY.

Information Regarding Preferred Directors

As a result of our failure to pay dividends on our Series A preferred stock for six or more quarterly periods, the holders of our Series A preferred stock became entitled to elect two members to our Board (the “Preferred Directors”). At a special meeting of holders of the Series A Preferred Stock held on February 2, 2011, the holders of the Series A preferred stock elected Messrs. Robert M. Deutschman and Edward J. Ratinoff as the Preferred Directors. Each director elected by the holders of Series A preferred stock serves for a one-year term and until his successor is duly elected and qualifies, or, if earlier, until the full payment (or setting aside for payment) of all dividends on the Series A preferred stock that are in arrears, as well as dividends for the then current period. If there is a vacancy during the term of office of a director elected by the holders of Series A preferred stock, such vacancy must be filled by the written consent of the remaining director elected by the holders of Series A preferred stock or, if no such director remains in office, by a vote of the holders of record of a majority of the outstanding shares of Series A preferred stock.

Directors are elected by a plurality of the votes cast at the Annual Meeting, which means the two individuals nominated for election as directors by the holders of Series A preferred stock who receive the largest number of properly cast votes will be elected as directors. Each share of Series A preferred stock is entitled to one vote for each of the two director nominees. Cumulative voting is not permitted. It is the intention of the proxy holders named in the enclosed proxy to vote the proxies received by them for the election of the nominees named below unless authorization to do so is withheld. If any nominee should become

7

unavailable for election prior to the Annual Meeting, an event which the Board does not currently anticipate, the proxies will be voted for the election of a substitute nominee or nominees proposed by the Board.

Messrs. Deutschman and Ratinoff are our nominees for election to the Board by the holders of Series A preferred stock. Each nominee has consented to be named in this Proxy Statement and to serve as a director if elected, and our management has no reason to believe that either nominee will be unable to serve. The information below relating to the nominees for election as directors by the holders of Series A preferred stock has been furnished to us by the respective individuals. If elected at the Annual Meeting, Messrs. Deutschman and Ratinoff would each serve for a one-year term and until their respective successors are duly elected and qualify or, if earlier, until the full payment (or setting aside for payment) of all dividends on the Series A preferred stock that are in arrears, as well as dividends for the then current period.

The following table sets forth information regarding the individuals who are our nominees for election as directors of the Company by the holders of the Series A preferred stock:

| Name | Age | Position | Director Since | |||

| Robert M. Deutschman | 55 | Director | 2011 | |||

| Edward J. Ratinoff | 47 | Director | 2011 | |||

Robert M. Deutschman has served on the Board since February 2011. Since 1999, Mr. Deutschman has served as a Managing Director at Cappello Capital Corp., an investment banking firm, and as Vice Chairman of Cappello Group, Inc. since 2008. Mr. Deutschman holds a Bachelor of Arts degree from Haverford College, with honors, and a Juris Doctor from Columbia University School of Law, where he was a Harlan Fiske Stone scholar. Since 2004, Mr. Deutschman has served as the Vice Chairman of the Board of Directors of Enron Creditors Recovery Corp. (formerly Enron Corp.), a position he assumed upon Enron’s emergence from bankruptcy. Mr. Deutschman has also served on the Advisory Board of the RAND Center for Corporate Ethics and Governance since 2006. He formerly served as Chairman of the Board of First Bank of Beverly Hills, F.S.B. and as a member of the board of directors of Beverly Hills Bancorp Inc. from 1999 to 2004. Our Board and Nominating and Corporate Governance Committee nominated Mr. Deutschman to serve as a director based, among other factors, on his commercial real estate and public company experience.

Edward J. Ratinoff has served on the Board since February 2011. Since March 2010, Mr. Ratinoff has been the Managing Director and Head of Acquisitions for Phoenix Realty Group, an institutional real estate investment firm. From 2004 to 2009, Mr. Ratinoff held the position of Managing Director and West Coast Head for the J.E. Robert Companies, a global real estate investment management company. Prior to joining J.E. Roberts, Mr. Ratinoff served in a variety of senior management roles in real estate investment banking with Keybanc, Chase Securities and Bankers Trust. Mr. Ratinoff holds a Bachelor of Arts degree in Architecture from the University of California, Berkeley, and a Master of Business Administration from the J.L. Kellogg Graduate School of Management at Northwestern University. Since May 2010, Mr. Ratinoff has served as a member of the board of directors and Chairman of the Loan Committee of Bank of Internet. Our Board and Nominating and Corporate Governance Committee nominated Mr. Ratinoff to serve as a director based, among other factors, on his commercial real estate and extensive investment banking experience.

OUR BOARD RECOMMENDS A VOTE “FOR” THE ELECTION OF EACH OF MESSRS. DEUTSCHMAN AND RATINOFF TO SERVE ON OUR BOARD FOR A ONE-YEAR TERM AND UNTIL THEIR RESPECTIVE SUCCESSORS ARE DULY ELECTED AND QUALIFY OR, IF EARLIER, UNTIL THE FULL PAYMENT (OR SETTING ASIDE FOR PAYMENT) OF ALL DIVIDENDS ON THE SERIES A PREFERRED STOCK THAT ARE IN ARREARS, AS WELL AS DIVIDENDS FOR THE THEN CURRENT PERIOD.

8

Board Governance Documents

The Board maintains charters for each of its committees and has adopted written corporate governance guidelines and a code of business conduct and ethics applicable to independent directors, executive officers, employees and agents, each of which is available for viewing on the Company’s website at http:// www.mpgoffice.com under the heading “Investor Relations—Corporate Governance.” This document is also available in print to any person who sends a written request to that effect to the attention of Jonathan L. Abrams, Secretary, MPG Office Trust, Inc., 355 South Grand Avenue, Suite 3300, Los Angeles, California 90071.

Any amendment to, or waiver of, any provision of the code of business conduct and ethics applicable to our independent directors and executive officers must be approved by the Board. Any such amendment or waiver that would be required to be disclosed under SEC rules or NYSE listing standards or regulations will be promptly posted on our website.

Director Independence

The NYSE requires each NYSE-listed company to have a majority of independent board members and a nominating/corporate governance committee, compensation committee and audit committee each comprised solely of independent directors. The Board has adopted independence standards as part of its corporate governance guidelines, which can be accessed on our website at http://www.mpgoffice.com under the heading “Investor Relations—Corporate Governance.” This document is also available in print to any person who sends a written request to that effect to the attention of our Secretary, as provided for above under the heading “— Board Governance Documents.”

The independence standards contained in our corporate governance guidelines incorporate the categories of relationships between a director and a listed company that would make a director ineligible to be independent according to the standards issued by the NYSE.

In accordance with NYSE rules and our corporate governance guidelines, in March 2012 the Board affirmatively determined that each of the following directors is independent within the meaning of both our and the NYSE’s director independence standards, as then in effect:

Robert M. Deutschman

Christine N. Garvey

Michael J. Gillfillan

Edward J. Ratinoff

Joseph P. Sullivan

George A. Vandeman

Paul M. Watson

The persons listed above include all of our current directors, other than Mr. Weinstein, our President and Chief Executive Officer.

The Board has also determined that each of the current members of our Audit, Compensation, and Nominating and Corporate Governance Committees is independent within the meaning of both our and the NYSE’s director independence standards applicable to members of such committees. Additionally, our Audit Committee members satisfy the enhanced independence standards set forth in Rule 10A-3(b)(1)(i) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) and NYSE listing standards.

9

Board Meetings

The Board held nine meetings and the non-management directors (which includes all directors except for our Chief Executive Officer) met in executive session seven times during the fiscal year ended December 31, 2011. Mr. Watson, our Chairman of the Board, presided over such executive sessions. The number of meetings for each Board committee is set forth below under the heading “—Board Committees.” During the fiscal year ended December 31, 2011, all of our directors attended at least 75% of the total number of meetings of the Board and of the Board committees on which they served. The Board expects all nominees for director to attend the Annual Meeting in person barring unforeseen circumstances or irresolvable conflicts. All of our directors at the time of our 2011 Annual Meeting of Stockholders, which was held on June 16, 2011, were in attendance in person at such Annual Meeting.

Board Leadership Structure and Risk Oversight

The Board has a policy that the positions of Chairman of the Board and Chief Executive Officer should be held by different persons. The Board has determined that having an independent director serve as Chairman is in the best interests of the Company, providing enhanced board oversight as well as active independent director participation in setting board meeting agendas and establishing board priorities and procedures. This policy is subject to review in the future based on the Company’s then-current circumstances and Board membership.

The Board is actively involved in overseeing our risk management through the Audit Committee. Under its charter, the Audit Committee is responsible for discussing with management its policies with respect to risk assessment and management. The Audit Committee is also responsible for discussing with management any significant financial risk exposures and the actions management has taken to limit, monitor or control such exposures.

Board Committees

Audit Committee—

General

Our Audit Committee was established in accordance with Section 3(a)(58)(A) of the Exchange Act. The Audit Committee helps ensure the integrity of our financial statements, our compliance with legal and regulatory requirements, the qualifications and independence of our independent registered public accounting firm, and the performance of our internal audit function and independent registered public accounting firm. The Audit Committee selects, assists and meets with the independent registered public accounting firm, oversees each annual audit and quarterly review, oversees our internal audit function and prepares the report that federal securities laws require to be included in our proxy statement each year (see page 62 for the current Audit Committee Report). The Board has approved a charter of the Audit Committee, and the Audit Committee carries out its responsibilities in accordance with those terms. The charter is located on our website at http:// www.mpgoffice.com and is available in print to any person who requests it by writing to our Secretary, as provided for above under the heading “—Board Governance Documents.” Currently, Mr. Watson is Chair and Messrs. Gillfillan and Ratinoff are members of the Audit Committee, each of whom is an independent director. In 2011, Messrs. Gillfillan and Watson served on the Audit Committee for the entire year, while Messrs. Vandeman and Ratinoff served on the Audit Committee for a portion of the year. Mr. Vandeman served from January 1, 2011 until February 28, 2011, and Mr. Ratinoff served on the Audit Committee beginning on February 28, 2011. Based on his experience and expertise, the Board has determined that Mr. Gillfillan is an “audit committee financial expert” as defined by the SEC. The Audit Committee meets the NYSE composition requirements, including the requirements dealing with financial literacy and financial sophistication. The members of our Audit Committee satisfy the enhanced independence standards applicable to audit committees

10

set forth in Rule 10A-3(b)(i) under the Exchange Act and the NYSE listing standards. During the fiscal year ended December 31, 2011, the Audit Committee met nine times. The composition of the Audit Committee following the date of the Annual Meeting will be determined by the Board promptly after the Annual Meeting.

Pre-approval Policies and Procedures

Our Audit Committee charter provides that the Audit Committee is to pre-approve all audit services and permitted non-audit services to be performed for us by our independent registered public accounting firm, subject to the de minimis exceptions for non-audit services described in Section 10A(i)(1)(B) of the Exchange Act.

In addition, consistent with SEC rules regarding auditor independence, the Audit Committee has adopted an Audit and Non-Audit Services Pre-Approval Policy, which provides that the Audit Committee is required to pre-approve all audit and permitted non-audit services to be performed by our independent registered public accounting firm, subject to the de minimis exceptions for non-audit services described in Section 10A(i)(1)(B) of the Exchange Act. The pre-approval policy sets forth procedures to be used for pre-approval requests relating to audit services, audit-related services, tax services and all other services and provides that:

| • | The Audit Committee may consider the amount of fees as a factor in determining whether a proposed service would impair the independence of the independent registered public accounting firm; |

| • | Requests or applications to provide services that require specific pre-approval by the Audit Committee will be submitted to the Audit Committee by both the independent registered public accounting firm and the Chief Financial Officer, and must include a joint statement as to whether, in their view, the request or application is consistent with the SEC’s and Public Company Accounting Oversight Board’s rules on registered public accounting firm independence; |

| • | The Audit Committee may delegate pre-approval authority to one or more of its members, and if the Audit Committee does so, the member or members to whom such authority is delegated shall report any pre-approval decisions to the Audit Committee at or prior to its next scheduled meeting; and |

| • | The Audit Committee may not delegate to management its responsibilities to pre-approve services performed by the independent registered public accounting firm. |

During the fiscal years ended December 31, 2011 and 2010, all audit services provided to us by KPMG LLP were pre-approved by the Audit Committee, and no non-audit services were performed for us by KPMG LLP.

Compensation Committee—

The Compensation Committee assists the Board in discharging its responsibilities relating to compensation of the Company’s executives by designing and approving or recommending for the Board’s approval the compensation plans, policies and programs of the Company. The Compensation Committee establishes, reviews, modifies and approves the compensation and benefits of our executive officers, administers the Second Amended and Restated 2003 Incentive Award Plan (the “Incentive Award Plan”) of MPG Office Trust, Inc., MPG Office Trust Services, Inc. (the “Services Company”) and MPG Office, L.P. (the “Operating Partnership”), and any other incentive programs, produces an annual report on executive compensation for inclusion in our proxy statement each year (see page 35 for the current Compensation Committee Report on Executive Compensation), and reviews with the Company’s management the Compensation Discussion and Analysis to be included in the Company’s annual proxy statement or

11

Annual Report on Form 10-K. Our Compensation Committee Charter is located on our website at http:// www.mpgoffice.com and is available in print to any person who requests it by writing to our Secretary, as provided for above under the heading “—Board Governance Documents.” Currently, Ms. Garvey is Chair and Messrs. Sullivan and Vandeman are members of the Compensation Committee, each of whom is an independent director. In 2011, Ms. Garvey and Mr. Sullivan served on the Compensation Committee for the entire year, while Messrs. Gillfillan and Vandeman served for a portion of the year. Mr. Gillfillan served on the Compensation Committee from January 1, 2011 through February 28, 2011, and Mr. Vandeman served on the Compensation Committee beginning on February 28, 2011. During the fiscal year ended December 31, 2011, the Compensation Committee met seven times. The composition of the Compensation Committee following the date of the Annual Meeting will be determined by the Board promptly after the Annual Meeting. Further information regarding the specific functions performed by the Compensation Committee is set forth below under the headings “Compensation Discussion and Analysis” and “Compensation Committee Report on Executive Compensation.”

Nominating and Corporate Governance Committee—

The Nominating and Corporate Governance Committee develops and recommends to the Board a set of corporate governance principles, adopts a code of ethics, adopts policies with respect to conflicts of interest, monitors our compliance with corporate governance requirements of state and federal law and the rules and regulations of the NYSE, establishes criteria for prospective members of the Board, conducts candidate searches and interviews, oversees and evaluates the Board and management, evaluates from time to time the appropriate size and composition of the Board and recommends, as appropriate, increases, decreases and changes in the composition of the Board, and formally proposes the slate of directors to be elected at each annual meeting of stockholders. Our Nominating and Governance Committee Charter is located on our website at http:// www.mpgoffice.com and is available in print to any person who requests it by writing to our Secretary, as provided for above under the heading “—Board Governance Documents.” Currently, Mr. Vandeman is Chair and Messrs. Deutschman and Watson are members of the Nominating and Corporate Governance Committee, each of whom is an independent director. In 2011, Messrs. Vandeman and Watson served on the Nominating and Corporate Governance Committee for the entire year, while Ms. Garvey and Mr. Deutschman served for a portion of the year. Ms. Garvey served on the Nominating and Corporate Governance Committee from January 1, 2011 through February 28, 2011, and Mr. Deutschman served on the Nominating and Corporate Governance Committee beginning on February 28, 2011. The Nominating and Corporate Governance Committee did not meet during the fiscal year ended December 31, 2011. The composition of the Nominating and Corporate Governance Committee following the date of the Annual Meeting will be determined by the Board promptly after the Annual Meeting. Further information regarding the Nominating and Corporate Governance Committee is set forth below under the headings “—Qualifications of Director Nominees” and “— Nominating and Corporate Governance Committee’s Process for Considering Director Nominees.”

Finance Committee—

The Finance Committee oversees all areas of finance for the Company and its subsidiaries, including: capital structures; equity, debt and real estate financings; capital expenditures; cash management; banking activities and relationships; investments; foreign exchange activities; tender offers; stock repurchase activities; and other financing activities. The Finance Committee Charter is located on our website at http:// www.mpgoffice.com and is available in print to any person who requests it by writing to our Secretary, as provided for above under the heading “—Board Governance Documents.” Currently, Mr. Sullivan is Chair and Ms. Garvey and Messrs. Deutschman, Gillfillan and Weinstein are members of the Finance Committee. In 2011, Messrs. Gilfillan, Sullivan and Weinstein served on the Finance Committee for the entire year, while Mr. Deutschman served on the Finance Committee beginning on February 28, 2011. The Finance Committee did not meet during the fiscal year ended December 31, 2011. The composition of the Finance Committee following the date of the Annual Meeting will be determined by the Board promptly after the Annual Meeting.

12

Qualifications of Director Nominees

The Nominating and Corporate Governance Committee has not set forth minimum qualifications for Board nominees. However, pursuant to its charter, the Nominating and Corporate Governance Committee considers the following criteria:

| ▪ | Experience in corporate governance, such as service as an officer or former officer of a publicly-traded company; |

| ▪ | Experience in the real estate industry; |

| ▪ | Experience as a board member of another publicly-traded company; and |

| ▪ | Academic expertise in an area of our operations. |

The Nominating and Governance Committee has not adopted any formal policy regarding an attempt to maintain a pre-determined mix of backgrounds of our Board nominees as such backgrounds relate to education, geography, race, gender, national origin or other factors not bearing on expertise. Rather, the Nominating and Corporate Governance Committee looks to that level and type of experience, expertise and credentials of our nominees which we determine are necessary or desirable for the Board at the time.

Nominating and Corporate Governance Committee’s Process for Considering Director Nominees

At an appropriate time prior to each Annual Meeting of Stockholders at which directors are to be elected or re-elected, the Nominating and Corporate Governance Committee recommends to the Board for nomination by the Board such candidates as the Nominating and Corporate Governance Committee, in the exercise of its judgment, has found to be well qualified and willing and available to serve. The Nominating and Corporate Governance Committee evaluates the performance of each current director in considering its recommendations. In accordance with certain SEC disclosure rules regarding the qualification of candidates to be recommended by the Nominating and Corporate Governance Committee for nomination to the Board, the Nominating and Corporate Governance Committee has focused on the particular experience, qualifications and skills of each candidate that would qualify such candidate to serve on the Board. The basis for the Nominating and Corporate Governance Committee’s recommendation of each of Ms. Garvey and Messrs. Gillfillan, Sullivan, Vandeman, Watson, Weinstein, Deutschman and Ratinoff is described above in the respective director’s biography.

At an appropriate time after a vacancy arises on the Board or a director advises the Board of his or her intention to resign, the Nominating and Corporate Governance Committee recommends to the Board for election by the Board to fill such vacancy such prospective member of the Board as the Nominating and Corporate Governance Committee, in the exercise of its judgment, has found to be well qualified and willing and available to serve. In determining whether a prospective member is qualified to serve, the Nominating and Corporate Governance Committee considers the factors listed above under the heading “—Qualifications of Director Nominees.”

Notwithstanding the foregoing, if we are legally required by contract or otherwise to permit a third party to designate one or more of the directors to be elected (for example, pursuant to rights contained in the Articles Supplementary for the Series A preferred stock to elect directors upon non-payment of dividends or pursuant to a stockholder agreement), then the nomination or election of such directors shall be governed by such requirements. Any director nominations received from stockholders will be evaluated in the same manner that nominees suggested by our directors, management or other parties are evaluated.

13

Manner by Which Stockholders May Recommend Director Candidates

The Nominating and Corporate Governance Committee will consider director candidates recommended by our stockholders. All recommendations must be directed to the Chair of the Nominating and Corporate Governance Committee, c/o Jonathan L. Abrams, Secretary, MPG Office Trust, Inc., 355 South Grand Avenue, Suite 3300, Los Angeles, California 90071. Recommendations for director nominees to be considered at the 2013 Annual Meeting must be received in writing (i) not less than 60 days nor more than 90 days prior to the first anniversary of the date of the 2012 Annual Meeting or (ii) if the date of the 2013 Annual Meeting is advanced or delayed by more than 30 days from such anniversary date, not earlier than the 90th day prior to the 2013 Annual Meeting date and not later than the close of business on the later of the 60th day prior to the 2013 Annual Meeting date or the tenth day following the date on which public announcement of the 2013 Annual Meeting date is first made. Each stockholder recommending a person as a director candidate must provide us with the following information so that the Nominating and Corporate Governance Committee may determine whether the recommended director candidate is independent from the stockholder, or each member of the stockholder group, that has recommended the director candidate:

| • | If the recommending stockholder or any member of the recommending stockholder group is a natural person, whether the recommended director candidate is the recommending stockholder, a member of the recommending stockholder group, or a member of the immediate family of the recommending stockholder or any member of the recommending stockholder group; |

| • | If the recommending stockholder or any member of the recommending stockholder group is an entity, whether the recommended director candidate or any immediate family member of the recommended director candidate is or has been at any time during the current or preceding calendar year an employee of the recommending stockholder or any member of the recommending stockholder group; |

| • | Whether the recommended director candidate or any immediate family member of the recommended director candidate has accepted, directly or indirectly, any consulting, advisory, or other compensatory fees from the recommending stockholder or any member of the group of recommending stockholders, or any of their respective affiliates, during the current or preceding calendar year; |

| • | Whether the recommended director candidate is an executive officer or director (or person fulfilling similar functions) of the recommending stockholder or any member of the recommending stockholder group, or any of their respective affiliates; and |

| • | Whether the recommended director candidate controls the recommending stockholder or any member of the recommending stockholder group. |

The recommending stockholder must also provide supplemental information that the Nominating and Corporate Governance Committee may request to determine whether the recommended director candidate (i) is qualified to serve on the Audit Committee, (ii) meets the standards of an independent director, and (iii) satisfies the standards for our directors set forth above under the heading “—Qualifications of Director Nominees.” In addition, the recommending stockholder must include the consent of the recommended director candidate in the information provided to us and the recommended director candidate must make himself or herself reasonably available to be interviewed by the Nominating and Corporate Governance Committee. The Nominating and Corporate Governance Committee will consider all recommended director candidates submitted to it in accordance with these established procedures, though it will only recommend to the Board as potential nominees those candidates it believes are most qualified. However, the Nominating and Corporate Governance Committee will not consider any director candidate if such candidate’s candidacy or, if elected, Board membership, would violate controlling federal or state law.

14

Communications with the Board

Stockholders or other interested persons wishing to communicate with the Board may send correspondence directed to the Board, c/o Jonathan L. Abrams, Secretary, MPG Office Trust, Inc., 355 South Grand Avenue, Suite 3300, Los Angeles, California 90071. Mr. Abrams will review all correspondence addressed to the Board, or any individual Board member, for any inappropriate correspondence and correspondence more suitably directed to our management. Mr. Abrams will summarize all correspondence not forwarded to the Board and make the correspondence available to the Board for its review at the Board’s request. Mr. Abrams will forward all such communications to the Board prior to the next regularly scheduled meeting of the Board following the receipt of the communication, as appropriate. Correspondence intended for our non-management directors as a group should be delivered to the address above, “Attention: Non-Management Directors, c/o Jonathan L. Abrams, Secretary.”

Compensation of Directors

The following table summarizes the compensation earned by each of our independent directors during the fiscal year ended December 31, 2011:

DIRECTOR COMPENSATION

| Name (1) | Fees Earned or Paid in Cash ($) (2) | Stock Awards ($) (3) | Option Awards ($) (4) | Non-Equity Incentive Plan Compensation ($) | All Other Compensation ($) | Total ($) | ||||||||||||

| (a) | (b) | (c) | (d) | (e) | (f) | (g) | ||||||||||||

| Robert M. Deutschman (5) | 91,111 | 75,919 | — | — | — | 167,030 | ||||||||||||

| Christine N. Garvey | 125,000 | 69,000 | — | — | — | 194,000 | ||||||||||||

| Michael J. Gillfillan | 127,500 | 69,000 | — | — | — | 196,500 | ||||||||||||

| Edward J. Ratinoff (5) | 94,861 | 75,919 | — | — | — | 170,780 | ||||||||||||

| Joseph P. Sullivan | 125,000 | 69,000 | — | — | — | 194,000 | ||||||||||||

| George A. Vandeman | 111,250 | 69,000 | — | — | — | 180,250 | ||||||||||||

| Paul M. Watson | 157,500 | 69,000 | — | — | — | 226,500 | ||||||||||||

__________

| (1) | Our Chief Executive Officer, Mr. Weinstein, is a member of the Board. Mr. Weinstein does not receive any additional compensation for his services as a director. All compensation for his services an employee of our Company is shown in the Summary Compensation Table. |

| (2) | Amounts shown in Column (b) are those earned during the fiscal year ended December 31, 2011 for annual retainer fees, committee fees and/or chair fees. For further information, please see the discussion below under the heading “—Retainers and Fees.” |

| (3) | Amounts shown in Column (c) represent the aggregate grant date fair value of restricted stock units granted during the fiscal year ended December 31, 2011 computed in accordance with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (the “FASB Codification”) Topic 718, Compensation—Stock Compensation. For a discussion of the assumptions made in the valuation reflected in this column, see Part II, Item 8. “Financial Statements and Supplementary Data—Notes 2 and 8 to the Consolidated Financial Statements” of our Annual Report on Form 10-K filed with the SEC on March 15, 2012. Messrs. Deutschman, Gillfillan, Ratinoff, Sullivan, Vandeman and Watson and Ms. Garvey each received an annual grant of 25,000 restricted stock units upon their re-election to the Board on June 16, 2011 with a grant date fair value of $69,000. In addition, Messrs. Deutschman and Ratinoff each received an award of 1,875 restricted stock units upon their initial election to the Board on February 2, 2011 with a grant date fair value of $6,919. As of December 31, 2011, our directors held the following number of outstanding restricted stock units: Mr. Deutschman, 26,875; Ms. Garvey, 25,000; Mr. Gillfillan, 25,000; Mr. Ratinoff, 26,875; Mr. Sullivan, 25,000; Mr. Vandeman, 25,000; and Mr. Watson, 25,000. |

| (4) | We did not grant any option awards to members of the Board during the fiscal year ended December 31, 2011. As of December 31, 2011, our directors held the following number of outstanding nonqualified stock option awards: Mr. Deutschman, none; Ms. Garvey, 102,500; Mr. Gillfillan, 97,500; Mr. Ratinoff, none; Mr. Sullivan, 97,500; Mr. Vandeman, 72,500; and Mr. Watson, 102,500. |

| (5) | Messrs. Deutschman and Ratinoff joined the Board on February 2, 2011. |

15

Retainers and Fees

Our director compensation program provides for the following cash fees:

| Fee Type (1) | Amount per Year | |||

| Retainer | $ | 100,000 | ||

| Chairman | 45,000 | |||

| Committee Chair: | ||||

| Audit | 35,000 | |||

| Compensation | 25,000 | |||

| Finance | 25,000 | |||

| Nominating and Corporate Governance | 10,000 | |||

| Committee Member: | ||||

| Audit | 5,000 | |||

_________

| (1) | Our Board members do not receive any additional compensation for attending Board or committee meetings. |

On July 23, 2009, the Board adopted the MPG Office Trust, Inc. Director Stock Plan, which generally provides, for each calendar year, that each non-employee director may irrevocably elect in advance to apply between 10% and 50% of the total annual compensation otherwise payable to him or her in cash during such calendar year (including any annual retainer fee and compensation for services rendered as a member of a committee of the Board or a chair of such committee) towards the purchase of shares of our common stock. During the fiscal year ended December 31, 2011, all of the annual fees described above were paid in cash to our non-employee directors and none of them elected to apply such fees toward the purchase of common stock under this plan.

Equity Awards

During 2010, our Incentive Plan provided for formula grants of nonqualified stock options to non-employee directors as follows:

| • | Each new non-employee director would be granted a nonqualified stock option to purchase 50,000 shares of our common stock under our Incentive Plan on the date on which he or she initially became a non-employee director (no director received such a grant). |

| • | Each non-employee director was granted a nonqualified stock option to purchase 45,000 shares of our common stock under our Incentive Plan effective immediately following each annual meeting of stockholders, provided that he or she continued to serve as a non-employee director immediately following such annual meeting. |

During 2011, the Compensation Committee approved the following changes to our director compensation program and our Incentive Plan:

| • | Effective February 2, 2011, each individual who first becomes a non-employee director on or after such date will be granted an award of 1,875 restricted stock units, with dividend equivalents, on the date on which he or she initially becomes a non-employee director. |

16

| • | Commencing as of the date of the Company’s 2011 Annual Meeting of Stockholders (on June 16, 2011), each non-employee director will be granted an award of 25,000 restricted stock units, with dividend equivalents, effective immediately following each annual meeting of stockholders, provided that he or she continues to serve as a non-employee director immediately following such meeting. |

Subject to the director’s continued service, these restricted stock unit awards generally vest in equal annual installments on each of the first three anniversaries of the date of grant. Shares of our common stock, or at the Company’s option cash, are provided with respect to the vested portion of restricted stock unit awards to the non-employee director upon the earliest to occur of (i) the date of the director’s separation from service, (ii) the director’s death, or (iii) the occurrence of a change in control (as such term is defined in our Incentive Plan).

Non-employee directors no longer receive awards of stock options upon initial election or re-election to the Board.

Our Incentive Plan was amended on February 2, 2011 and April 25, 2011, respectively, to reflect these changes.

Compensation Committee Interlocks and Insider Participation

In 2011, Ms. Garvey and Messrs. Gillfillan, Sullivan and Vandeman served on the Compensation Committee. Ms. Garvey and Mr. Sullivan served on the Compensation Committee for the entire year, while Messrs. Gillfillan and Vandeman served for a portion of the year. Mr. Gillfillan served on the Compensation Committee from January 1, 2011 through February 28, 2011, and Mr. Vandeman served on the Compensation Committee beginning on February 28, 2011. During the fiscal year ended December 31, 2011, there were no interlocks with other companies requiring disclosure under applicable SEC rules and regulations. None of the members of the Compensation Committee is or has been an officer or employee of our Company or any of its subsidiaries.

While the Compensation Committee retains ultimate approval authority for executive compensation, it has delegated the authority to negotiate specific terms of certain executive employment agreements to the Chief Executive Officer and the General Counsel.

17

ITEM 2

ADVISORY (NON-BINDING) VOTE ON EXECUTIVE COMPENSATION (“SAY-ON-PAY” VOTE)

Background

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”) enables our stockholders to vote to approve, on an advisory (non-binding) basis, the compensation of our named executive officers as disclosed in this Proxy Statement in accordance with SEC rules.

At our 2011 Annual Meeting of Stockholders, over 89% of the votes cast by holders of our common stock were in favor of holding an annual say-on-pay vote. Based on these results, the Board determined that we will hold a say-on-pay vote every year until the next advisory (non-binding) vote on the frequency of holding a say-on-pay vote occurs. Unless the Board modifies its determination on the frequency of future say-on-pay votes, the next say-on-pay vote will be held at the 2013 Annual Meeting of Stockholders.

Summary

At our 2011 Annual Meeting of Stockholders, holders of our common stock overwhelmingly approved the compensation of our named executive officers, with over 98% of the votes cast in favor of the say-on-pay proposal.

We are asking holders of our common stock to consider and vote upon a resolution to approve the compensation of our named executive officers, which consist of our Chief Executive Officer, Chief Financial Officer and next three highest paid executive officers, as described in the “Compensation Discussion and Analysis” section of this Proxy Statement and the related executive compensation tables, beginning on page 26. Our executive compensation program is designed to enable us to recruit, retain and develop superior management talent, who are critical to our success. Such a program rewards our named executive officers for the achievement of specific short- and long-term goals, including overall company and personal goals. The following is a brief summary of some of the key points of our executive compensation program. We urge our stockholders to review the detailed “Compensation Discussion and Analysis” section of this Proxy Statement and executive-related compensation tables for more information.

We emphasize pay-for-performance. Our Compensation Committee carefully reviews prior performance in connection with any potential increase in an executive officer’s base salary. Our incentive program is performance-driven, as bonuses are awarded at the discretion of the Compensation Committee after evaluating the executive’s performance based on the Company’s achievement of its business plan, the particular executive’s contributions to the Company’s achievement of such business plan and other individual performance criteria deemed to be appropriate by the Compensation Committee.

Executives therefore have a significant portion of their annual compensation at risk depending upon performance. Equity awards are a key component of our executive compensation program, which we believe align the interests of our executive officers with those of our long-term stockholders by encouraging long-term performance.

18

We provide competitive pay opportunities that reflect best practices. We have a highly active Compensation Committee, which met seven times during the fiscal year ended December 31, 2011. The Compensation Committee consistently reviews our executive compensation program (together with our independent compensation consultant) to ensure that it not only provides competitive pay opportunities, but also reflects best practices. For example, on June 9, 2009, we adopted a policy that we will not enter into any new agreement with our executive officers that includes (i) any Internal Revenue Code of 1986, as amended (the “Code”), Section 280G excise tax gross-up provision with respect to payments contingent upon a change in control, except in unusual circumstances where the Compensation Committee determines that it is appropriate to do so in order to recruit a new executive officer (in which case, the excise tax gross-up will be limited to payments triggered by both a change in control and termination of employment, and will be subject to a three-year sunset provision), or (ii) a modified single trigger which provides for severance payments in the event that an executive officer voluntarily terminates employment without good reason within a specified period of time following a change in control of the Company.

We are committed to having strong governance standards with respect to our compensation program, procedures and practices. Pursuant to our commitment to strong governance standards, the Compensation Committee is comprised solely of independent directors. The Compensation Committee retains an independent compensation consultant to provide it with advice and guidance on our executive compensation program design and to evaluate our executive compensation program. The Compensation Committee oversees and periodically assesses the risks associated with our company-wide compensation policies and practices to determine whether such policies and practices encourage unnecessary or excessive risk taking. We have implemented equity compensation grant procedures that comply with evolving best practices.

Recommendation

The Board believes that the information provided above and within the “Compensation Discussion and Analysis” section of this Proxy Statement demonstrates that our executive compensation program was designed appropriately and is working to ensure that management’s interests are aligned with our stockholders’ interests to support long-term value creation and is consistent with a pay-for-performance philosophy.

The following resolution will be submitted for a vote of the holders of common stock at the Annual Meeting:

“RESOLVED, that holders of common stock of MPG Office Trust, Inc. approve, on an advisory (non-binding) basis, the compensation of the named executive officers of MPG Office Trust, Inc., as disclosed in the Compensation Discussion and Analysis, compensation tables and narrative discussion of this Proxy Statement.”

The say-on-pay vote is advisory, and therefore not binding on the Company, the Compensation Committee or the Board.

The affirmative vote of a majority of the votes cast by the holders of common stock at the Annual Meeting is required for the adoption of the resolution approving, on an advisory (non-binding) basis, the compensation of our named executive officers.

OUR BOARD RECOMMENDS A VOTE “FOR” ADOPTION OF THIS RESOLUTION APPROVING THE COMPENSATION OF MPG OFFICE TRUST’S NAMED EXECUTIVE OFFICERS.

19

ITEM 3

RATIFICATION OF SELECTION OF

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Audit Committee of the Board has selected KPMG LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2012, and has further directed that management submit the selection of the independent registered public accounting firm for ratification by holders of common stock at the Annual Meeting. KPMG LLP has audited our financial statements since our inception in 2002. A representative of KPMG LLP is expected to be present at the Annual Meeting, and, if present, will have an opportunity to make a statement if he or she so desires and will be available to respond to appropriate questions.

Principal Accounting Fees and Services

The following table summarizes the fees for professional services rendered by KPMG LLP:

| For the Year Ended December 31, | |||||||

| 2011 | 2010 | ||||||

| Audit fees (1) | $ | 1,044,000 | $ | 1,113,000 | |||

| Audit-related fees (2) | 290,000 | 294,000 | |||||

| Tax fees (3) | — | — | |||||

| All other fees | — | — | |||||

| $ | 1,334,000 | $ | 1,407,000 | ||||