EXHIBIT 99.3

Group annual results

Provisional results for the year ended March 31, 2007

Telkom SA Limited

Building for a converged future.

13 June 2007

Cautionary statement on forward

looking statements

All of the statements included in this presentation, as well as oral statements that may be made by us or by officers, directors or employees acting on behalf of us, that are not statements of historical facts constitute or are based on forward-looking statements within the meaning of the US Private Securities Litigation Reform Act of 1995, specifically Section 27A of the US Securities Act of 1933, as amended, and Section 21E of the US Securities Exchange Act of 1934, as amended. These forward-looking statements involve a number of known and unknown risks, uncertainties and other factors that could cause our actual results and outcomes to be materially different from historical results or from any future results expressed or implied by such forward-looking statements. Among the factors that could cause our actual results or outcomes to differ materially from our expectations are those risks identified in Item 3. “Key Information-Risk Factors,” of Telkom’s most recent Annual Report on Form 20-F filed with the US Securities and Exchange Commission (SEC) and its other filings and submissions with the SEC which are available on Telkom’s website at www.telkom.co.za/ir, including, but not limited to, increased competition in the South African telecommunications markets; developments in the regulatory environment; continued mobile growth and reductions in Vodacom’s and Telkom’s net interconnect margins; Vodacom’s and Telkom’s ability to expand their operations and make investments and acquisitions in other African countries and the general economic, political, social and legal conditions in South Africa and in other countries where Vodacom and Telkom invest; our ability to attract and retain key personnel; our inability to appoint a majority of Vodacom’s directors and the consensus approval rights at Vodacom that may limit our flexibility and ability to implement our preferred strategies; Vodacom’s continued payment of dividends or distributions to us; our ability to improve and maintain our management information and other systems; our negative working capital; changes in technology and delays in the implementation of new technologies; our ability to reduce theft, vandalism, network and payphone fraud and lost revenue to non-licensed operators; our ability to improve our internal control over financial reporting; health risks related to mobile handsets, base stations and associated equipment; risks related to our control by the Government of the Republic of South Africa and major shareholders and the South African Government’s other positions in the telecommunications industry; the outcome of regulatory, legal and arbitration proceedings, including tariff approvals, and the outcome of Telkom’s proceedings with Telcordia Technologies Incorporated and others and its hearing before the Competition Commission related to the VANs litigation; our ability to negotiate favourable terms, rates and conditions for the provision of interconnection services and facilities leasing services; our ability to implement and recover the substantial capital and operational costs associated with carrier pre-selection, Number Portability and the monitoring, interception and customer registration requirements contained in the South African Regulation of Interception of Communication and Provision of Communication – Related Information Act; Telkom’s ability to comply with the South African Public Finance Management Act and South African Public Audit Act and the impact of the Municipal Property Rates Act; fluctuations in the value of the Rand; the impact of unemployment, poverty, crime and HIV infection, labour laws and exchange control restrictions in South Africa; and other matters not yet known to us or not currently considered material by us.

We caution you not to place undue reliance on these forward-looking statements. All written and oral forward-looking statements attributable to us, or persons acting on our behalf, are qualified in their entirety by these cautionary statements. Moreover, unless we are required by law to update these statements, we will not necessarily update any of these statements after the date hereof, either to conform them to actual results or to changes in our expectation.

Group highlights

Reuben September

Group overview

Financial summary

8.4% growth in Group operating revenue

to R51.6bn

38.3% Group EBITDA margin

39.6% Fixed-line EBITDA margin

excluding Telcordia

1.4% decrease in Group operating profit

to R14.5bn

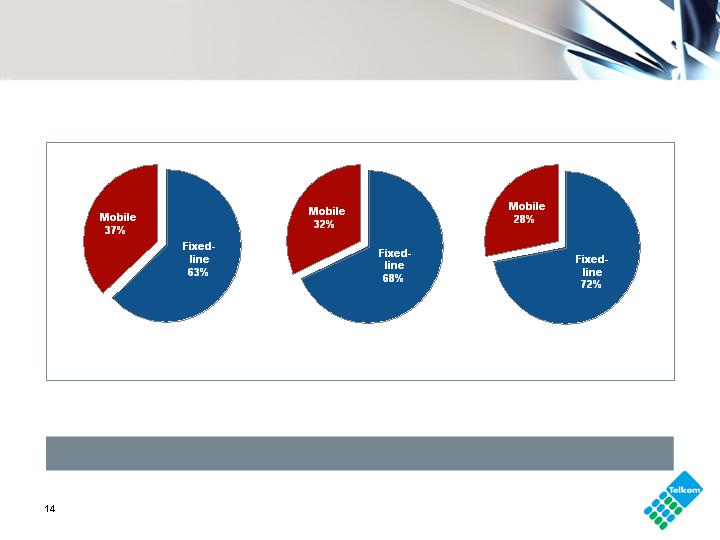

20.9% growth in mobile revenue to

R41.1bn1

22.4% growth in mobile operating profit

to R10.9bn1

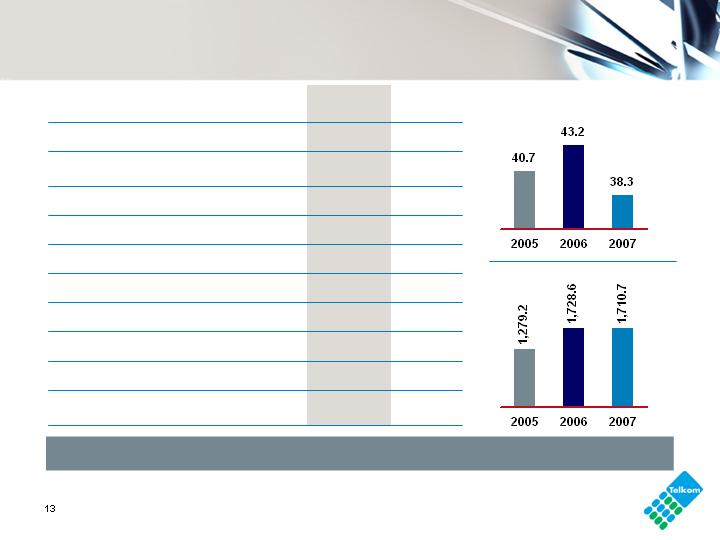

Headline earnings per share decrease

1.0% to 1,710.7 cents per share

Total dividend

1,100 cents per share

up 22%

Telcordia provision US$70m (R527m)

12,089,371

shares bought back

for R1.6bn

1. 100% Vodacom (50% consolidated)

Board approved

R2.4bn for share

buy-backs in

2007/2008

Operational highlights

Annuity revenue

13.5%

R5,137.1m

to

VPN & MPN services

27.2%

R340.9m

to

Managed data sites

29.6%

21,879

to

ADSL services

78.1%

255,633

to

Mobile leased lines

29.3%

60,000

to

Bundled packages

149.5%

R634.6m

to

Total mobile customers

28.2%

30.2m

to

Defensive strategies delivering results

Corporate market responding well to value added data services

Mobile growth remains strong

Operational highlights (continued)

82% of network with ADSL and WiMAX coverage

60% of local loop under 2.5km

250% growth on sales of ‘term and volume’ contracts

288,881 Closer Plan subscriptions – 18% penetration of consumer lines

88.7% increase in fibre optic network from 6.7m to 12.7m loop km

Acquisitions – Africa Online & Multi-Links

Swiftnet BEE transaction concluded – awaiting ICASA approval

Consumer demand remains strong

Telkom driving hard to build out network, products and services

Growth profile

Data

Mobile

Geographic

Employee engagement

Customer centricity

NGN deployment

Stakeholder management

Cost management

Acquisition growth

Capitalising on convergence

& mobility

Roll-out of key enablers progressing well

Strategic pillars - key enablers

for revenue growth and

retention

Group growth initiatives

Accelerating data growth – ADSL, VPN, MPN & Mobile leased lines

IT – Managed hosting environments

Driving Broadband penetration

Convergence – expanding into the application layer by integrating

fixed-line and mobile

Establish and grow Telkom Media – key convergence enabler

Increasing capacity and speed on the network

Evolving into a Pan-African service provider

Aggressively expanding Africa Online and Multi-Links

Pricing for volume, penetration and loyalty

Defending traditional and aggressively building for the new

Mobile strategy

Reviewing mobile partnership to achieve a

fixed-mobile service provider model across

the fixed and mobile value chain

Maximise services into the growing

converged solutions market

Integrate capabilities into the managed

hosting environment

Offer Swiftnet services into the fixed-mobile

service provider model

Speed of action is imperative

Cost initiatives

Renegotiate service and equipment contracts

Focussed move to automate assurance and fulfilment

Equipment sourced directly from original equipment manufacturers

Pursue turnkey capital programmes

Improve maintenance support and licensing models

The move to NGN creates operational cost saving opportunities

Cost management remains a key focus area

Mobile business – highlights

Operating revenue1

20.9%

R41,146m

to

Total customers

20.1%

23.0m

to

ARPU2

10.7%

R125

to

EBITDA margin

0.1%

34.6%

to

Data revenue1

64.0%

R3,342m

to

Remains market leader in South Africa

Churn2

33.8%

17.7%

from

1. 100% Vodacom (50% consolidated) 2. South Africa

Group highlights

Kaushik Patel

Financial overview

Group income statement

(3.7)

19,785

20,553

EBITDA

(5.1)

8,849

9,328

Net profit

4.6

(4,731)

(4,523)

Taxation

(3.7)

1,681.0

1,746.1

Basic earnings per

share (cents)

(8.0)

(1,125)

(1,223)

Finance charges

(40.8)

235

397

Investment income

(1.4)

14,470

14,677

Operating profit

(20.0)

384

480

Other income

12.3

(37,533)

(33,428)

Operating expenses

8.4

51,619

47,625

Operating revenue

%

2007

2006

ZAR million

EBITDA margin

%

HEPS

Cents

Building the foundation for the future

Segmental contribution

after inter-segmental eliminations

Operating revenue

Operating profit

Profit attributable to

equity holders

Fixed-line business remains the major contributor to the Group

Fixed-line revenue

Steady growth of annuity revenue and data services

ZAR million

2006

2007

(1.0%)

(4.7%)

8.3%

1.7%

6.4%

12.6%

Fixed-line traffic

Traffic revenue

Traffic volumes

ZAR millions

Millions of minutes

0.0%

(6.4%)

(13.9%)

(1.3%)

(8.8%)

8.3%

1.0%

(4.4%)

Tariff reduction, ADSL rollout and cannibalisation by bundled

products contribute to a decrease-in-traffic revenue

Fixed-line revenue (continued)

(1.0)

1,638

1,654

Interconnection revenue

(7.9)

823

894

International

7.2

815

760

Mobile

%

2007

2006

ZAR millions

21.7

1,664

1,367

Mobile leased facilities

10.2

5,820

5,282

Leased lines

%

2007

2006

ZAR millions

Interconnection

Data

Strong growth in mobile data

Regulatory changes may be beneficial to fixed-line margin

Total millions of minutes

Total

(Rm)

2.4%

12.6%

Fixed-line operating expenses

7.2%

(17.7)

3,623

4,404

Depreciation, amortisation,

impairment and write-offs

1.3

787

777

Operating leases

7.9

2,212

2,050

Services rendered

37.5

4,244

3,086

SG&A

5.1

6,463

6,150

Payments to other operators

12.3

7,268

6,470

Employee expenses

%

2007

2006

ZAR millions

Focus on service delivery, network reliability and new products and services

to satisfy and anticipate the needs of our customers

Total

(Rm)

Employee expenses

12.3

(696)

(620)

Labour capitalised

(72.7)

24

88

Workforce reduction

12.7

2,715

2,410

Benefits

13.8

5,225

4,592

Salaries and wages

%

2007

2006

ZAR millions

Employee expenses: building skills and meeting sophisticated

and time dependent customer demands

12.3%

Total

(Rm)

Selling, general and administrative expenses

55.4

642

413

Marketing

(24.6)

141

187

Bad debts

78.7

1,553

869

Other (including Telcordia

provision)

18.0

1,908

1,617

Materials & Maintenance

%

2007

2006

ZAR millions

Maintaining competitive edge and marketing for competition

37.5%

Total

(Rm)

Group balance sheet

45.0

9,901

6,828

Net debt

2.8

59,146

57,544

Total equity & liabilities

18.5

18,584

15,687

Current liabilities

(31.0)

8,554

12,391

Non-current liabilities

8.6

32,008

29,466

Capital & reserves

(18.5)

10,376

12,731

Current assets

2.8

59,146

57,544

Total assets

8.8

48,770

44,813

Non-current assets

%

2007

2006

ZAR million

31% net debt to equity

23% return on assets

(%)

(%)

Majority spent on baseline expansion

Capex program frontloaded where possible

Capex/revenue ratio 20.0%

Fixed-line capex

22.1

43

36

Other

(30.2)

416

596

Sustainment

(57.5)

159

374

Revenue generation

33.2

501

376

Support

34.6

6,641

4,935

Total

1,153.3

188

15

Regulatory

5.6

1,141

1,080

Efficiencies & improvements

137.6

784

330

Network evolution

60.2

3,409

2,128

Baseline expansion

%

2007

2006

ZAR millions

Group cash flow

(302.7)

(3,976)

1,962

Net increase/(decrease) in cash

(92.8)

308

4,255

Cash at the end of the year

42.9

(10,412)

(7,286)

Investing activities

(47.5)

3,728

7,104

Free cash flow

1,031.8

(2,920)

(258)

Financing activities

(1.6)

9,356

9,506

Cash generated from operating activities

(2.1)

(4,784)

(4,884)

Dividend paid

4.0

20,520

19,724

Cash generated from operations

%

2007

2006

ZAR millions

Cash utilised to repay debt, tax and fund dividends and capex

Mobile financial highlights

Profit from operations increased by 22.5% to R10.9 billion

ZAR million

ZAR million

ZAR million

ZAR million

20.9%

25.0%

40.3%

22.5%

100% Vodacom (50% consolidated)

1. Including intangibles

Leading the South African mobile market

South African market continues to grow strongly

Thousands

Thousands

ZAR

%

20.1%

18.8%

91.0%

10.7%

1. Blended ARPU

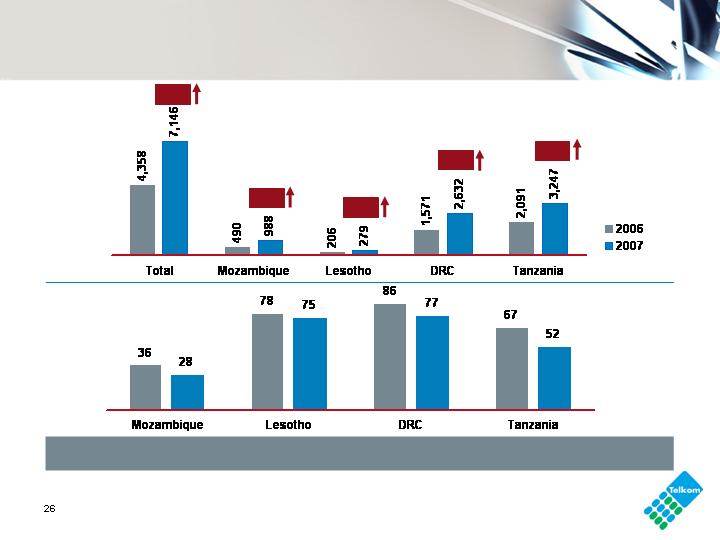

Performance in other African countries

Customers

Thousands

ARPU1

ZAR

Impressive performance from the African portfolio

64%

102%

55%

68%

35%

1. Blended ARPU

Guidance for 2007/2008

EBITDA margin between 37% and 40%

Net debt to equity of 50% to 70%

Capex/revenue 18% – 22%

Fixed-line

Group

Reuben September

Fixed-line business

Pricing strategy

Extend value

and savings

Broadband price

reduction

Rebalance

tariffs

Aligning tariffs with cost

Reduce broadband prices to remain competitive – drive

volumes and leverage our growing economies of scale

Improving the value offered by our calling plans and

bundles, especially on the entry level packages

Rebalance to

reduce arbitrage

risk

Further rebalancing to reduce arbitrage risks include

reduction in long distance and international usage fees

Reduce prices

of data services

To reduce the prices of data services – our data portfolio

pricing will decrease

Pricing for volume, penetration, loyalty and up-scaling

Pricing

% Difference between Basket Tariff change and CPI

Telkom will file an overall

price decrease of 1.2%

against an allowable basket

increase of 8.7%1 including

the carry-over

The productivity offset figure

(X-factor) is 3.5%

Telkom has reduced prices 13% effectively

1. Allowable increase = 3.5%, carry-over = 5.2%

Strong data growth

Telkom continues to offer premium data service

29.6%

7.1%

11.2%

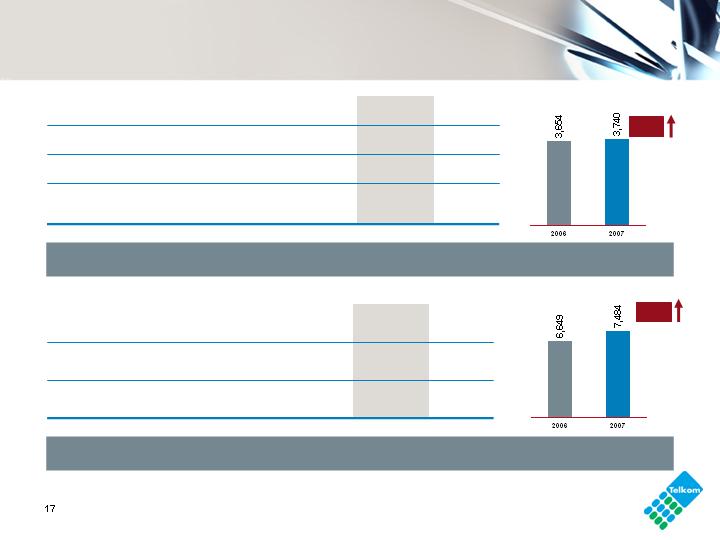

78.1% growth in ADSL subscribers to 255,633

14.3% growth in 64 kbit/sec equivalent circuits 19,247

22.2% growth in Internet satellite subscribers to 2,420

1. Includes dialup, ADSL and satellite internet users

DSL performance

ADSL year-on-year growth

Creating niches for best in class prices

ADSL service initiatives

Introduction of ADSL Self Install Option

to improve Average-Time-To-Install

40% of new orders now done through

Self Install

Reduced ADSL Average-Time-To-Install

from 31 to 23 days on average, where

infrastructure is available

Broadband Demand Register to capture

and identify areas of growth for future build

Pre-provisioning of the network will

drastically shorten installation days

do Broadband – premium quality

Differentiating on content, quality and speed

Moving into the converged future

March 31, 2008 target – 420,000 subscribers

Bundles

2008 Target: 530,000 up 84%

Closer 1

Designed to suit your pocket at only

R120 per month

Closer 2

Unlimited calls anywhere in SA during

Callmore time limited to 1 hour per call

for R145

Closer 3

For R300 per month get all the benefits

plus cellular savings with pure per

second billing

Closer 4

For R499 per month receive all plan 3

benefits plus DSL up to 384kbps

Closer 5

For R699 per month you get all the

benefits of plan 3 bundles with DSL up to

1024kbps

2,997

0

Closer 5

288,881 base end March 2007

43,196

8,514

Internet

add on

18,973

0

Closer 4

157,957

49,950

Closer 3

105,885

11,863

Closer 2

3,069

990

Closer 1

2007

2006

Key NGN achievements

National IP Network (IPNet)

Bandwidth increased from 18.9 Gbit/s to 28.9 Gbit/s

Growth of 53%

International IP Network (IPNet)

Bandwidth increased from 1.5 Gbit/s to 2.4 Gbit/s

Growth of 60%

National Transport Network

Bandwidth increased from 1.0 Tbit/s to 1.2 Tbit/s

Growth of 20%

Local Transport Network

Bandwidth increased from 5.1 Tbit/s to 5.7 Tbit/s

Growth of 12%

Aggressively expanding capacity to cater for converged services

Key NGN achievements (continued)

Diginet and Diginet Plus Services

Bandwidth increased from 17.3 Gbit/s to 20.8 Gbit/s

Growth of 20%

ATM Network

Bandwidth increased from 80 Gbit/s to 104 Gbit/s

Growth of 30%

SAT-3/WASC was upgraded from 40 Gbit/s to 120 Gbit/s

SAFE was upgraded from 30 Gbit/s to 90 Gbit/s

International connectivity and speed is key for data growth and

the Pan African strategy

Moving legacy voice and leased line services to NGN platform

Key NGN developments

Development in progress for Voice over IP portfolio

NG Voice on IMAX

Voice over Broadband

Voice over WiMAX

Development of New Generation Diginet capability

NGD Frame based on ATM

NGD LAN based on Metro Ethernet

The PSTN is connected to NGN core via Media gateways (softswitch

operational for Voice Interconnect)

WiMAX – complementing ADSL sweet spots

Holistic wire-line and wireless approach to broadband

14 base stations commissioned

Target of 57 base stations to

be built

Internet WiMAX products

launched

Voice service planned to be

launched in the last quarter of

the 2007/2008 financial year

Telkom Media

To be Africa’s Digital Media Provider of Choice

Diversifying revenue

streams for Telkom

Becoming the

partner of choice for

the media industry

Delivering excellent

customer service

and a high quality

customer experience

Providing an

integrated, multi-

platform approach

Open access to

unaddressed pay-TV

market in emerging

middle class

Developing South

Africa’s media

economy through

content, service and

technology innovation

Telkom Media

Digital services via Internet, satellite and IPTV

TV content, video-on-demand and interactive services (portals,

music, games)

Planned basic bouquet of channels estimated to cost no more than

R100 per month

Peak funding of R7bn over 8 years

Breakeven anticipated 2013

Video On

Demand

User Generated

Content

Portal Services

Interactive

Services

Converged Services

Internet Services and Value Added Service

Portal Services (Blogging, Podcasting, Messaging)

Premium Portal (WebTV, Radio Streaming, Event Streaming, etc.)

High Speed Broadband Access

Pan-Africa strategy

Lead the expansion in Africa through

a Service Provider Strategy

Aggressively expand Africa Online

footprint into the continent

Aligned with domestic Fixed/Mobile

Service Provider Strategy

Acquisitions focussed on key

regional hubs

Fixed and Mobile voice for Africa

Global connectivity for Africa

Internet and Data services for Africa

Pay TV for Africa

Multi-Links

Acquired for USD280m in April 2007

USD1bn Capex planned over 5 years

Cashflow positive by 2010

Fixed, mobile, data subscribers:

816,000

1,500km of fibre optic cable

Management team established

Multi-Links is a PTO in Nigeria with a Unified Access License allowing

fixed, mobile, international and data services

Established key regional footprint on West Coast of Africa

Multi-Links – focus for the future

Increase revenue of fixed wireless and mobile customer through national

brand awareness and promotion campaign

To provide easy-to-understand high-value bundles, differentiated on

voice quality and service

Introduce Broadband Internet with ISP services to offer high-value bundles

Launch high quality IP NGN services to Government, Corporate and

Business customers

Deploy Metro Ethernet services in Lagos to attract high-end Corporate users

Introduce a Carrier Class wholesale product and service offering by

establishing an earth station to provide international connectivity

Africa Online

Africa Online is an Internet Service Provider based in Kenya, Tanzania,

Cote d’Ivoire, Ghana, Uganda, Namibia, Swaziland, and Zimbabwe

Key financial data

Acquired for R150m (GBP10.3m) in March 2007

Month of March 2007

Revenue R7.6m

Operating loss R394,586

Capex planned over 5 years USD10.8m

Cashflow positive by 2008/2009

Internet subscribers:160,000 at March 31, 2007

Aggressively expand ISP services in conjunction with

Telkom and Telkom Media

Africa Online – focus for the future

Investment approach focuses on

brand development

creation and development of

customer channels

market expansion

improvement of network systems

human resource development

Joint venture with Verizon in Kenya

Expanding wireless broadband (InfiNet)

in Kenya, Ghana and Tanzania

Large African footprint of ISP services provides multiple opportunities

Key regulatory issues

Impact on Telkom:

Licenses to be converted to network license and service license

Deadline July 2008

Uncertainty as to impacts of conversion

Electronics Communications Act

Telkom and Vodacom remain in consultation with the Office of Interception

Centres and DOC

RICA Act

Interconnection agreements with Neotel and major VANS concluded

Interconnection

Facilities leasing

Facilities leasing agreement concluded with Neotel

Telkom to provide shared access to the local loop to Neotel for the first 2 years

Awaiting clarity on facilities leasing to other licensees

Key regulatory issues (continued)

Unbundling of the local loop

Government expects it to be completed by 2011

Awaiting decision on:

Technical and functional regulations

Where the local loop is to be unbundled

Costing, dealing with access line deficit

Operational systems still to be developed

Outstanding matters

“Significant Market Power” analysis

Mobile termination investigations – likely to be margin enhancing for fixed-line

Possibility of asymmetrical cost based interconnection prices for

smaller operators

End of exclusivity on November 1, 2007

SAT-3

Key regulatory issues (continued)

VANS licensees may be authorised to provide services as well as

provide and operate facilities/networks

Attempt to have Infraco deemed as “holder of an individual

electronic communications network service license”

Frequency spectrum allocations

USAL licenses to merge and Provincial Under-Serviced Area

Network Operator licenses to be issued

SAT-3 monopoly to end, ICASA to prescribe all facilities connected

to cable as essential facilities

Reiterated announcement by President to provide special rate

for call centres

Minister of Communication’s budget speech 2007

Customer centricity

Sustainable profitable growth in

customer base requires creating and

strengthening capabilities focused

on managing customer relationships

and learning from acquired customer

information

Anticipating

customer needs

Revenue

Growth

Revenue

retention

Customer

satisfaction

through managing

customer

experience

Impacts

Protection of

customer base

Customer driven culture

Sense of mission,

motivation

High quality network,

innovative “solutions”

Improved Company

perception

Retention &

growth

Employee

engagement

NGN

Stakeholder

management

Roadmap for the journey

An intensive 2 year programme

Foundation 1

Foundation 2

Quick-wins and

momentum

programs

Enhancing 1 to 1

treatment

capabilities

Building the foundation of

customer centricity

Competitive

advantage

Time

36 initiatives from Phase

1 & 2 already kicked-off

Building 1 to 1 treatment capabilities

Oct 06 – Jul 07

Jan 07 – Mar 08

Aug 07 – Feb 09

Feb 08 – Mar 09

Thank you

Investor Relations:

Nicola White

Tel: +27 12 311 5720

Fax: +27 12 311 5721

E-Mail: whitenh@telkom.co.za

Building for a converged future.