EXHIBIT 99.5

Operational highlights

Alan Knott-Craig

Chief Executive Officer

Group highlights

For the year ended March 31, 2007 vs. prior year

Total customers (SIM cards)

30.2 million

28.2%

High gross connections: increase of 31.5% year on year to 15.6 million

Revenue

R41.1 billion

20.9%

Profit from operations

R10.9 billion

22.5%

EBITDA

R14.2 billion

20.5%

Net profit after tax

R6.6 billion

27.6%

Dividends

R5.4 billion

20.0%

South Africa

10.9 million

Gross connections

33.8%

Churn %

84%

Estimated mobile

penetration %

R10.3 billion

Profit from operations

23.0 million

Total customers

2007

20.1%

18.8%

13 pts

19.7%

16.1 pts

Tanzania

2.1 million

Gross connections

35.6%

Churn %

16%

Estimated mobile

penetration %

R346 million

Profit from operations

3.2 million

Total customers

2007

55.3%

54.6%

7 pts

31.6%

7.1 pts

Democratic Republic of Congo (DRC)

1.7 million

Gross connections

30.4%

Churn %

9%

Estimated mobile

penetration %

R277 million

Profit from operations

2.6 million

Total customers

2007

67.5%

89.2%

3 pts

136.8%

2.3 pts

Lesotho

119 thousand

Gross connections

19.0%

Churn %

17%

Estimated mobile

penetration %

R75 million

Profit from operations

279 thousand

Total customers

2007

35.4%

21.4%

4 pts

47.1%

Mozambique

R177 million

Loss from operations

797 thousand

Gross connections

41.7%

Churn %

14%

Estimated mobile

penetration %

R154 million

Loss from operations

(excluding impairment)

988 thousand

Total customers

2007

101.6%

133.0%

6 pts

9.5 pts

22.9%

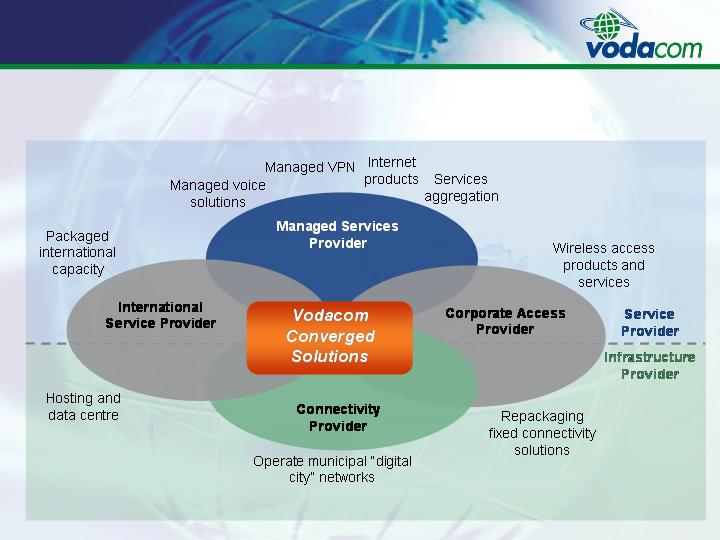

Pillars for continued growth

Loyalty programmes

Prepaid:

Yebo Millionaires

Vodacom Talking Points

Contract:

Onyx/Platinum

Credit card

South Africa

VodaMail: Free e-mail service to contract

customers

Bazza uau!: prepaid tariff rewarding customers

for receiving calls

Bazza bonus: rewarding previous day’s spend

with free airtime

60+: free SMSs for long duration calls

Mozambique

Innovative non-voice products and tariffs

Access content through

commercial arrangement

22 TV channels

Enter broadcasting /

multimedia market

Over 33 thousand Mobile

TV users

Mobile TV / DVB-H

Digital Satellite Pay TV

Personal services and

telemetry

Business customer needs:

offering full service to

corporate customers

ISP services

WiMax

VPNs

Future offerings

Over 139 thousand

3G/HSDPA users

Offer fast reliable and low

priced wireless data

product

Over 899 thousand

Vodafone live! users

Vodafone live!,

3G/HSDPA

Data revenue

Data revenue as a % of service

revenue

Tanzania launched

3G/HSDPA during the year

64%

year on

year

Expansion of distribution and support channels

Community service containers

Strong relationships with the distribution channels

Informal channels

Dual service providers

Branded franchised store points

Vodaworld cellular mall – biggest contract

connection centre

Distribution channels

Vodacare stores

Walk-in customer care centres

Dedicated data stores

IT support

Support channels

Further improve level of customer care and quality of service

Brand leadership

Voted most popular telecommunications brand and second most recognised brand

after Coca-Cola (Markinor / Sunday Times Top Brands)

Black Economic Empowerment (BEE)

Vodacom is developing a BEE transaction which will be completed towards the end of the

year, enabling employees and BEE partners to share in the success of the business

May well be one of the largest BEE equity transactions in South Africa (capped at R7.5

billion)

Being aligned with the DTI Codes of Good Practice

Implementation of the ICT Sector Code projected for end of 2007

BEE

Regulation

Reduction in mobile termination rates

Pro-actively engaged with regulator

Customer registration legislation and MNP

Affects informal distribution channel

Remains threat to industry

Government re-evaluating introduction

Vodacom pro-active in commencing registration process

MNP had no major impact as less than 1% of Vodacom customers utilised it

Contract: 4,283 (net porting in)

Prepaid: (10,301) (net porting out)

New licence regime / ECA

Will bring new players into the market

Facilitates MVNO access to market

Vodacom will be converting its licences into an electronic communications network and an electronic

communications service licence

Converting licences to new framework may be lengthy and complex

Regulation

Acquisitions

Acquired a 10% stake in iBurst through the WBS acquisition, with a further option to acquire

15.5%

In order to ensure growth within our area of focus, Vodacom made investments in

companies such as:

G-Mobile Holdings Ltd (Wi-Fi business)

Gogga Tracking Solutions (Pty) Ltd (Wi-Fi business)

Effective September 13, 2006, Vodacom Service Provider Company (Pty) Ltd acquired the

contract customer base of approximately 160 thousand from Smartcom (Pty) Ltd

Increased equity of Smartphone SP (Pty) Ltd from 51% to 70% on August 30, 2006

Acquisitions

Way forward

Way forward (continued)

Continue to seek financially viable opportunities in Africa

Seek out new associated business opportunities in South Africa

Gear up to provide total converged solutions to Corporates

Grow and consolidate current business

Focus on improving customer service and loyalty

Focus on data growth

Financial review

Leon Crouse

Chief Financial Officer

Group income statement

Extracts for the year ended March 31,

(147.9%)

(295)

(119)

(106)

Net finance (costs) / income

>200%

17

-

-

Profit on sale of investments

(143.4%)

(23)

53

(268)

Impairment

27.6%

6,560

5,143

3,888

Net profit

(24.4%)

(3,836)

(3,084)

(2,614)

Taxation

(21.1%)

(26,919)

(22,234)

(17,725)

Operating expenses excluding depreciation,

amortisation and impairment

20.5%

14,227

11,809

9,590

EBITDA

(12.2%)

(3,361)

(2,996)

(2,844)

Depreciation and amortisation

22.5%

10,860

8,866

6,478

Profit from operations

67.5%

(169)

(520)

130

IAS revaluations

26.4%

10,396

8,227

6,502

Profit before tax

20.9%

41,146

34,043

27,315

Revenue

2006

% change

2007

2005

R million

Effective tax rate 36.9% vs. 37.5% prior year

Group operational indicators

Gross connections up 31.5%

year on year to a record high of

15.6 million

Customers up 28.2% year on

year to 30.2 million

Total traffic in South Africa

increased by 19.4% year on

year to 20.4 billion minutes

Gross connections

Closing customers

ARPU by country

Declining ARPUs

SA decreased 10.1% to R125

DRC decreased 10.5% to R77

Lesotho decreased 3.8% to R75

Tanzania decreased 22.4% to R52

Mozambique decreased 22.2% to

R28

Vodacom Group consolidated

ARPU decreased 12.6% year on

year from R127 to R111

ARPU per month

South Africa ARPU

Contract ARPU decreased

9.6% year on year to R517

Prepaid ARPU decreased

8.7% year on year to R63

Total ARPU decreased

10.1% year on year to R125

Lower incoming revenue per customer

Lower average usage

Customer mix

South Africa ARPU per month

Group revenue

By country

43.5%

1,914

1,334

1,075

DRC

19.1%

37,007

31,069

25,041

South Africa, including holding companies

20.9%

41,146

34,043

27,315

70.3%

269

158

103

Mozambique

33.5%

227

170

137

Lesotho

31.8%

1,729

1,312

959

Tanzania

2006

%

change

2007

2005

R million

Revenue driven by strong customer growth

Non-South African operations contributing 10.1% (2006: 8.7%)

Group revenue

Revenue composition

34.5%

1,306

971

887

International airtime

17.9%

4,699

3,986

2,687

Equipment sales

17.0%

7,835

6,697

5,924

Interconnection

18.0%

23,708

20,085

16,191

Airtime, connection & access

20.9%

41,146

34,043

27,315

(3.8%)

256

266

286

Other sales and services

64.0%

3,342

2,038

1,340

Data

2006

%

change

2007

2005

R million

Revenue growth, excluding equipment sales was 21.3%

Group revenue (excluding equipment sales)

By revenue type

Revenue analysis – 2007

R36,447 million (excluding equipment sales)

Revenue analysis – 2006

R30,057 million (excluding equipment sales)

Airtime contribution down 1.8% points to 65.0%

Interconnect contribution down 0.8% points to 21.5%

Data contribution up 2.4% points to 9.2% (data revenue 9.4% of service revenue)

EBITDA and margin analysis

EBITDA margin by country

EBITDA performance

Increased 20.5% year on year to R14.2 billion

EBITDA margin decreased 0.1% points year on year to

34.6%

EBITDA margin 39.9%, when excluding cellular phone

and equipment sales

South Africa EBITDA

Increased 17.3% year on year to R13.0 billion

EBITDA margin decreased 0.6% points year on year to

35.0%

EBITDA for non-South African operations

Increased 56.6% year on year to R1.2 billion

Non-South African operations contributed 8.5% of total

vs. 6.6% for the same period in the previous financial

year

Mozambique EBITDA is negative R69 million

Tanzania EBITDA margin decreased: increase in

excise duty on airtime of 40%; drought; power

rationing; inflated fuel prices

20.5%

year on

year

EBITDA

Group profit from operations

By country

136.8%

277

117

50

DRC

>200%

46

(23)

56

Holding companies

31.6%

346

263

183

Tanzania

0.4% pts

26.4%

26.0%

23.7%

Profit from operations margin (%)

22.5%

10,860

8,866

6,478

(22.9%)

(177)

(144)

(454)

Mozambique

47.1%

75

51

25

Lesotho

19.7%

10,293

8,602

6,618

South Africa

2006

%

change

2007

2005

R million

Customer growth of 28.2% to 30.2 million

Revenue growth of 20.9% vs. operating expenses growth of 20.3%

Factors affecting trends and margins

South Africa traffic mix

Outgoing traffic increased 20.1% year on

year to 13.6 billion minutes:

Outgoing fixed increased by 2.6% to 1.2 billion

Outgoing mobile increased by 22.2% 12.4 billion

Incoming traffic increased 18.1% year on

year to 6.7 billion minutes:

Incoming fixed increased by 3.0% to 2.4 billion

Incoming mobile increased by 29.1% to 4.3 billion

Mobile to mobile traffic increased by 23.9%

to 16.7 billion minutes

Mobile/fixed traffic increased by 2.9% to 3.7

billion minutes

A 20% reduction in average mobile

termination rates will reduce profit

from operations by approximately

R430 million

South Africa net interconnect

Total South Africa traffic

19.4%

year on

year

10.0%

year on

year

Productivity measures

Consolidated customers

per employee

Increased 18.2% year on year to 5,093

based on 5,920 employees

Consolidated gross capex

additions as a % of revenue

increased to 16.4% from 15.1%

for the same period in the

previous financial year

Investment in new technologies

Increased capacity for data and voice

Gross capex additions was R6.7

billion vs R5.1 billion in the

previous financial year

Gross capex additions as a % of revenue

Gross capex additions as a % of revenue

Capex additions and composition

Including software

Capex gross additions – 2007

R6,748 million

Capex gross additions – 2006

R5,138 million

South Africa capex gross additions increased by 13.9% to R5.0 billion

Non-South African capex additions increased by 113.1% to R1.6 billion

Cash generation

EBITDA increased by R2.4 billion

Cash generated from operations

increased 25.0% to R13.9 billion

Free cash flow increased

13.8% to R3.7 billion

Cash generated from operations

Free cash flow

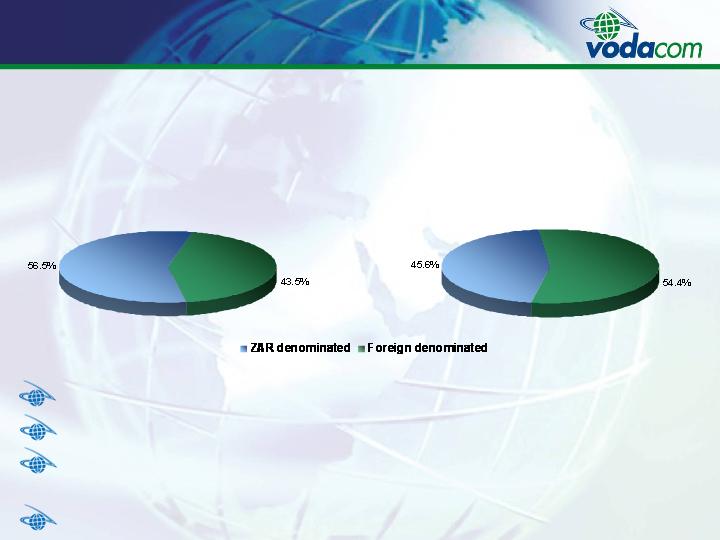

Debt composition

Gross debt composition

including bank overdrafts– 2007

R3,435 million

Gross debt composition

including bank overdrafts – 2006

R3,855 million

Net debt: R2,664 million (2006: R709 million)

Net debt to equity ratio 27.6% (2006: 8.2%)

Adjusting for dividends and STC on dividends payable: net debt to equity ratio of 72.8%

(2006: 50.5%)

Net debt to EBITDA ratio 18.7% (2006: 6.0%)

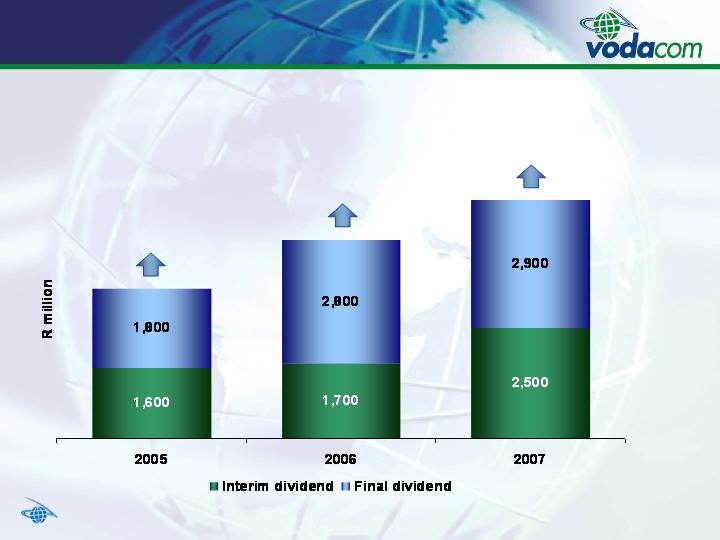

Group shareholder distributions

20.0%

year on

year

The level of future dividend payments is dependent on the extent of investment activities

32.4%

year on

year

61.9%

year on

year

Questions?

Group balance sheet

Extracts at March 31,

8.3%

15,011

13,860

11,474

Current liabilities

14.9%

28,470

24,768

22,595

Total equity and liabilities

70.5%

3,812

2,236

3,233

Non-current liabilities

11.2%

9,647

8,672

7,888

EQUITY AND LIABILITIES

Capital and reserves

14.9%

28,470

24,768

22,595

Total assets

(12.2%)

7,626

8,689

8,706

Current assets

29.6%

20,844

16,079

13,889

ASSETS

Non-current assets

2006

%

change

2007

2005

R million

Group cash flow statement

Extracts for the year ended March 31,

(106.1%)

(108)

1,760

2,173

Cash and cash equivalents at the

end of the year

>200%

58

(16)

(6)

Effect of foreign exchange rate changes

(19.0%)

1,760

2,173

1,598

Cash and cash equivalents at the

beginning of the year

(>200%)

(1,926)

(397)

581

Net increase in cash and cash

equivalents

(86.9%)

(200)

(107)

(195)

Net cash flows utilised in

financing activities

(37.4%)

(6,584)

(4,791)

(3,374)

Net cash flows utilised in investing

activities

7.9%

4,858

4,501

4,150

Net cash flows from operating activities

25.0%

13,866

11,090

10,012

Cash generated from operations

2006

%

change

2007

2005

R million

Disclaimer

This presentation has been prepared and published by Vodacom Group (Proprietary) Limited.

Vodacom Group (Proprietary) Limited is a private company and as such is not required by the

Companies Act 61 of 1973, as amended, to publish its results.

Vodacom Group (Proprietary) Limited makes no guarantee, assurance, representation and/or

warranty as to the accuracy of the information contained in this presentation and will not be

held liable for any reliance placed on the information contained in this presentation.

The information contained in this presentation is subject to change without notice and may be

incomplete or condensed. In addition, this presentation may not contain all material

information pertaining to Vodacom Group (Proprietary) Limited and its subsidiaries.

Without in any way derogating from the generality of the foregoing, it should be noted that:

Many of the statements included in this presentation are forward-looking statements that involve risks and/or uncertainties and caution must be exercised in placing any reliance on these statements. Moreover, Vodacom Group (Proprietary) Limited will not necessarily update any of these statements after the date of this presentation either to conform them to actual results or to changes in its expectations.

Insofar as the shareholders of Vodacom Group (Proprietary) Limited are listed and offer their shares publicly for sale on recognised stock exchanges locally and/or internationally, potential investors in the shares of Vodacom Group (Proprietary) Limited’s shareholders are cautioned not to place undue reliance on this presentation.

Thank you