Exhibit 99.3

Group interim results

for the six months ended September 30, 2007

Telkom SA Limited

Providing for the Bandwidth Explosion

Cautionary statement on forward looking statements

All of the statements included in this presentation, as well as oral statements that may be made by us or by officers, directors or employees acting on behalf of us, that are not statements of historical facts constitute or are based on forward-looking statements within the meaning of the US Private Securities Litigation Reform Act of 1995, specifically Section 27A of the US Securities Act of 1933, as amended, and Section 21E of the US Securities Exchange Act of 1934, as amended. These forward-looking statements involve a number of known and unknown risks, uncertainties and other factors that could cause our actual results and outcomes to be materially different from historical results or from any future results expressed or implied by such forward-looking statements. Among the factors that could cause our actual results or outcomes to differ materially from our expectations are those risks identified in Item 3. “Key Information-Risk Factors,” of Telkom’s most recent Annual Report on Form 20-F filed with the US Securities and Exchange Commission (SEC) and its other filings and submissions with the SEC which are available on Telkom’s website at www.telkom.co.za/ir, including, but not limited to, any changes to Telkom’s mobile strategy and its ability to successfully implement such strategy and organisational changes thereto; increased competition in the South African telecommunications markets; developments in the regulatory environment; continued mobile growth and reductions in Vodacom’s and Telkom’s net interconnect margins; Vodacom’s and Telkom’s ability to expand their operations and make investments and acquisitions in other African countries and the general economic, political, social and legal conditions in South Africa and in other countries where Vodacom and Telkom invest; our ability to attract and retain key personnel; our inability to appoint a majority of Vodacom’s directors and the consensus approval rights at Vodacom that may limit our flexibility and ability to implement our preferred strategies; Vodacom’s continued payment of dividends or distributions to us; our ability to improve and maintain our management information and other systems; our negative working capital; changes in technology and delays in the implementation of new technologies; our ability to reduce theft, vandalism, network and payphone fraud and lost revenue to non-licensed operators; our ability to improve our internal control over financial reporting; health risks related to mobile handsets, base stations and associated equipment; risks related to our control by the Government of the Republic of South Africa and major shareholders and the South African Government’s other positions in the telecommunications industry; the outcome of regulatory, legal and arbitration proceedings, including tariff approvals, and the outcome of Telkom’s proceedings with Telcordia Technologies Incorporated and others and its hearing before the Competition Commission related to the VANs litigation; our ability to negotiate favourable terms, rates and conditions for the provision of interconnection services and facilities leasing services; our ability to implement and recover the substantial capital and operational costs associated with carrier pre-selection, Number Portability and the monitoring, interception and customer registration requirements contained in the South African Regulation of Interception of Communication and Provision of Communication – Related Information Act; Telkom’s ability to comply with the South African Public Finance Management Act and South African Public Audit Act and the impact of the Municipal Property Rates Act; fluctuations in the value of the Rand; the impact of unemployment, poverty, crime and HIV infection, labour laws and exchange control restrictions in South Africa; and other matters not yet known to us or not currently considered material by us.

We caution you not to place undue reliance on these forward-looking statements. All written and oral forward-looking statements

attributable to us, or persons acting on our behalf, are qualified in their entirety by these cautionary statements. Moreover, unless we are

required by law to update these statements, we will not necessarily update any of these statements after the date hereof, either to

conform them to actual results or to changes in our expectation.

Reuben September

Group Overview

Strategy

Core Strategy -

Defend & Grow

Revenues

Defend Revenues

Increase annuity revenues

Drive to increase

subscription revenues

Long term contracts

Rebalance tariffs

To align with cost structures

to combat arbitrage

Build retention through

bundling

Offer attractive value

propositions

Grow Revenues

Fixed/ Mobile

Geographic

Data

Fixed/Mobile Platform:

Become an Integrated Service

Provider across the Fixed and

Mobile value chain

Position entity as a competitive

convergence solutions provider

Geographic Reach

Expand into Africa through the

Integrated Service Provider

Strategy

Converged Services (Voice, Data,

Video & Internet)

Expand aggressively into

managed voice, managed data

and applications

Enabling strategies

NGN deployment

Product innovation through convergence and mobility

Competitive pricing models

Cost management

Stakeholder engagement

Customer centricity

Employee engagement

Acquisitive growth

Effective organisational structures

Protecting our EBITDA margin is vital

Fixed / Mobile growth

Improved

strength as an ICT

company

International

footprint for

enterprise

customers

Own the digital

home

Accelerated growth

Become an Integrated Service Provider across the fixed and

mobile value chain

Position entity as a competitive convergence solutions provider

Enable increased penetration in under serviced areas

Decrease cost of providing services in sparsely populated areas

Mobile strategy review in progress

Converged Services and Data growth

Connectivity

Managed

networks

Data centre

outsourcing

Desktop

support

Application

Services

Business

process

services

Telcos strengths

Commoditising IT infrastructure

Access

Diginet

DSL

VSAT

Transport

Circuit-

switched

ATM

Frame

relay

IP

Internet

access

provisioning

WAN/VPN

installation

monitoring

& support

security

LAN

installation

monitoring

& support

security

Server &

applications

hosting

Web-hosting

Data storage

Disaster

recovery

Desktop

installation

Desktop

management

upgrades

repairs

End-user

support

IT consulting

Systems

integration

Custom

software

development

ASP

eComm

billing &

payments

Business

process

consulting &

engineering

Business

applications

development

Business

process

outsourcing

Transaction

processing

Call centres

Pursuing international IT capabilities

Geographic growth

Goal is to cover major cities in Africa

Expand international connectivity of major cities through hub and cluster

strategy

Focus on data connectivity

Dual fixed/ wireless licenses

Expansion of Africa Online ISP services from 9 to 15 Africa countries

Pan African service provider strategy

Global footprint for SA multi-nationals

Hosting and managed solutions

Key Criteria For Optimal Geographic Reach

Financial criteria

Core geographical

areas

Core business areas

Management restructuring

The new EXCO structure has been designed to:

Create specialised focus areas to service

customer segments

Ensure a coherent Group approach to marketing,

pricing and product and services development

Enhance effective and efficient resource utilisation

Increase the coherence and speed of deployment

Create a unified view of software and systems

technology

Allow smoother integration of resource deployment

to Telkom’s subsidiaries

Better serve multi-national and wholesale

customers

Enhancing effectiveness

Financial summary

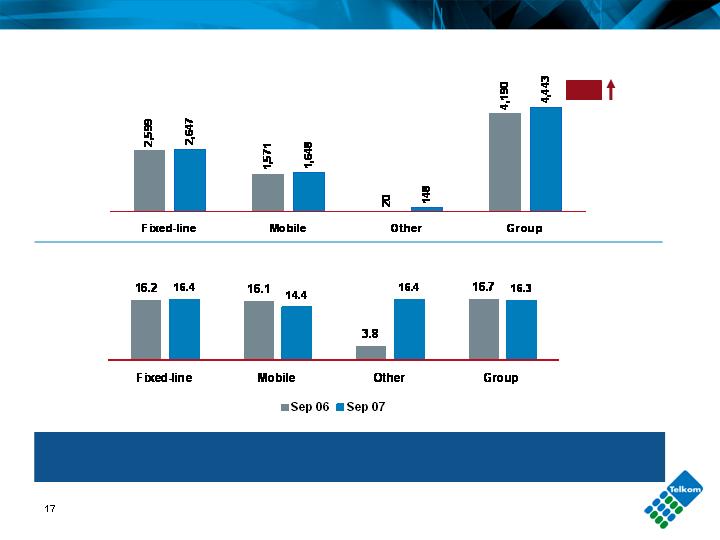

8.3% growth in Group operating revenue to R27.2bn

37.5% Group EBITDA margin

4.8% decrease in Group operating profit to R7.3bn

15.1% decrease in Group headline earnings per share to

742.3 cents per share

38.2% f ixed-line EBITDA margin

33.3% mobile EBITDA margin

Aggressive retention and loyalty drive

Deon Fredericks

Financial overview

Group income statement

HEPS

Cents

EBITDA margin

%

(16.6)

724.3

868.1

Basis earnings per

share (cents)

(17.1)

3,793

4,574

Net profit

(5.8)

(2,678)

(2,844)

Taxation

122.4

(972)

(437)

Finance charges

(0.1)

10,214

10,225

EBITDA

(23.5)

130

170

Investment income

(4.8)

7,313

7,685

Operating profit

13.8

(20,118)

(17,675)

Operating expenses

(4.2)

204

213

Other income

8.3

27,227

25,147

Operating revenue

%

Sep 07

Sep 06

ZAR million

Six months ended

Building the foundation for the future

Group balance sheet

60% net debt to equity

9% return on assets

(%)

(%)

Balance sheet remains strong

50.9

17,732

11,751

Net debt

14.9

63,595

55,351

Total equity & liabilities

59.1

24,182

15,203

Current liabilities

(19.0)

9,838

12,148

Non-current liabilities

5.6

29,575

28,000

Capital & reserves

14.9

63,595

55,351

Total assets

9.7

11,311

10,309

Current assets

16.1

52,284

45,042

Non-current assets

%

Sep 07

Sep 06

ZAR million

Six months ended

Group cash flow

Six months ended

(56.0)

(1,825)

(4,147)

Net increase in cash

(1,096.7)

(1,525)

153

Cash at the end of period

71.3

(7,028)

(4,102)

Investing activities

(145.3)

(633)

1,396

Free cash flow

(653.2)

4,520

(817)

Financing activities

(11.5)

683

772

Cash generated from operating activities

20.9

(5,712)

(4,726)

Dividend paid

(8.1)

8,313

9,046

Cash generated from operations

%

Sep 07

Sep 06

ZAR millions

Capex, acquisitive growth and dividend payment reduce cash flow

Group Capital investment

Expenditure

ZAR millions

Capex to revenue

%

Fixed and mobile investment a priority for growth

6.0%

Fixed-line business remains the major contributor to the Group

Operating revenue

Operating profit

Profit attributable to

equity holders

Segmental contribution

before eliminations

Fixed-line

Mobile

Other

Fixed-line business

Deon Fredericks

Fixed-line profitability

Six months ended

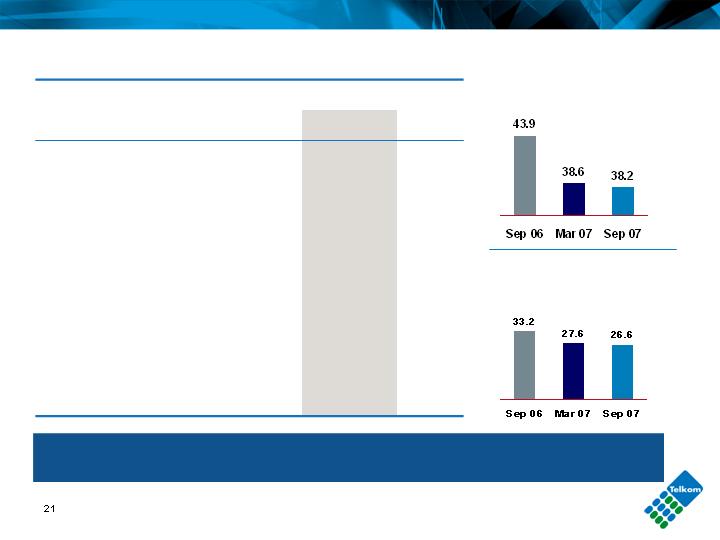

(12.5)

6,153

7,031

EBITDA

38.2

43.9

EBITDA margin (%)

26.6

33.2

Operating profit margin (%)

(19.4)

4,286

5,316

Operating profit

%

Sep 07

Sep 06

ZAR millions

EBITDA margin

%

Operating profit margin

%

(13.0%)

(19.9%)

Fixed-line income statement

Operating profit margin

%

Vodacom dividend declared after September 2007

EBITDA margin

%

(46.6)

2,623

4,909

Net profit

(1.8)

(1,798)

(1,831)

Taxation

65.3

(702)

(426)

Finance charges

(12.5)

6,153

7,031

EBITDA

(54.6)

839

1,850

Investment income

(19.4)

4,286

5,316

Operating profit

6.6

(12,011)

(11,272)

Operating expenses

(66.4)

189

563

Other income

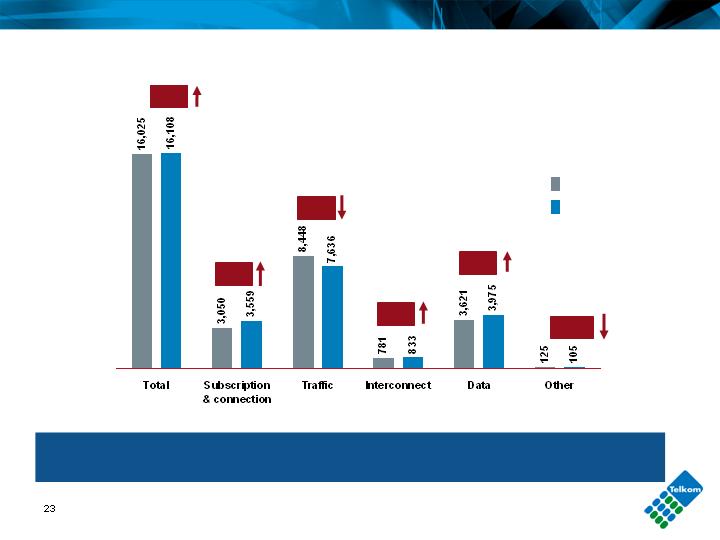

0.5

16,108

16,025

Operating revenue

%

Sep 07

Sep 06

ZAR million

Six months ended

(R1,030 million)

Fixed-line operating profit drivers

ZAR million

Fixed-line revenue

Competition and aggressive price reductions leading to revenue

pressure

ZAR million

Sep 06

Sep 07

6.7%

(9.6%)

16.7%

0.5%

(16.0%)

9.8%

Fixed-line traffic

Traffic revenue

Traffic volumes

ZAR millions

Millions of minutes

0.2%

(22.3%)

(14.9%)

1.0%

(17.8%)

15.1%

3.9%

Competition and term & volume discount plans affecting volume

& revenue

2.2%

Annuity revenue

9.1

12

11

International other

Six months ended

14.6

3,340

2,914

Total annuity revenue

7.8

165

153

Value added services

21.1

373

308

CPE rental

78.5

441

247

Calling Plans / packages

7.0

2,349

2,195

Line Rental

%

Sep 07

Sep 06

Annuity revenue

Annuity revenue includes all subscription revenue. It does not include usage or traffic

related revenue from calling plans/bundles, line installations, reconnection fees and

CPE sales

Recurring revenue continues to grow

Fixed-line operating expenses

6.6%

Six months ended

8.9

1,867

1,715

Depreciation, amortisation,

impairment and write-offs

(9.9)

337

374

Operating leases

10.9

1,186

1,069

Services rendered

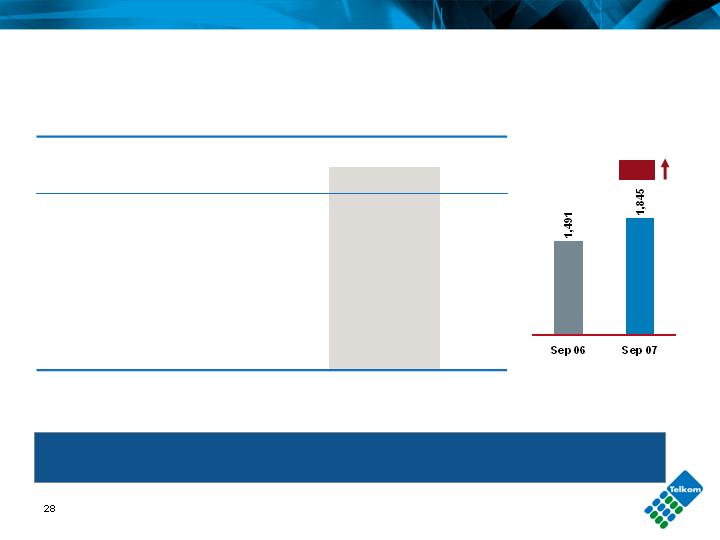

23.7

1,845

1,491

SG&A

8.6

3,362

3,097

Payments to other operators

(3.2)

3,414

3,526

Employee expenses

%

Sep 07

Sep 06

ZAR millions

Focus on customer service and network reliability

Total

(Rm)

Fixed-line Employee expenses

(78.6)

3

14

Other

Six months ended

18.0

(381)

(323)

Labour capitalised

(25.7)

1,022

1,375

Benefits

12.6

2,770

2,460

Salaries and wages

%

Sep 07

Sep 06

ZAR millions

Skills mix drives growth in salary expenses

(3.2%)

Total

(Rm)

Fixed-line Selling, General and Administrative expenses

23.7%

Total

(Rm)

Ensuring service reliability and product positioning

56.9

441

281

Other

43.5

89

62

Bad debts

25.5

271

216

Marketing

12.0

1,044

932

Materials & Maintenance

%

Sep 07

Sep 06

ZAR million

Six months ended

Capex to revenue ratio up to 16.4% from 16.2%

Fixed-line capex

Six months ended

64.3

23

14

Other

(34.1)

114

173

Sustainment

(93.5)

6

93

Revenue generation

(27.0)

89

122

Support

1.8

2,647

2,599

Total

(96.2)

5

130

Regulatory

(15.6)

352

417

Efficiencies & improvements

(25.3)

204

273

Network evolution

34.6

1,854

1,377

Baseline expansion

%

Sep 07

Sep 06

ZAR millions

Mobile business

Deon Fredericks

Mobile financial highlights

Investing to maintain strong revenue growth

ZAR million

ZAR million

ZAR million

ZAR million

17.2%

26.1%

4.9%

15.1%

100% Vodacom (50% consolidated)

1. Including intangibles

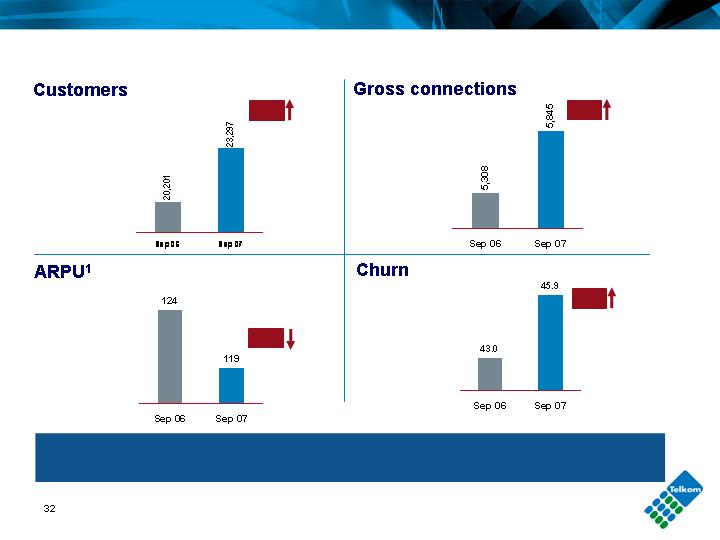

Leading the South African mobile market

New disconnection rules affect pre-paid churn

Thousands

Thousands

ZAR

%

15.3%

10.1%

(4.0%)

1. Blended ARPU

6.7%

Guidance for 2007/2008

EBITDA margin between 37% and 40%

Net debt to equity of 50% to 70%

Capex/revenue 18% – 22%

Fixed-line

Group

Reuben September

Operational Overview

2011 broadband plan

Up to 4Meg

Today

Legacy TDM network

Stand alone access, voice and Internet

value propositions

Limited content

Complex installation

Up to 10Meg

3rd Generation IP network

Integrated communication and

entertainment

Interactive IPTV and HDTV

“Better than” content strategy

Simplicity of use – plug and play

broadband in a box

2011

ADSL – 8.5% penetration of fixed

access lines

ADSL – 15-20% penetration of fixed

access lines

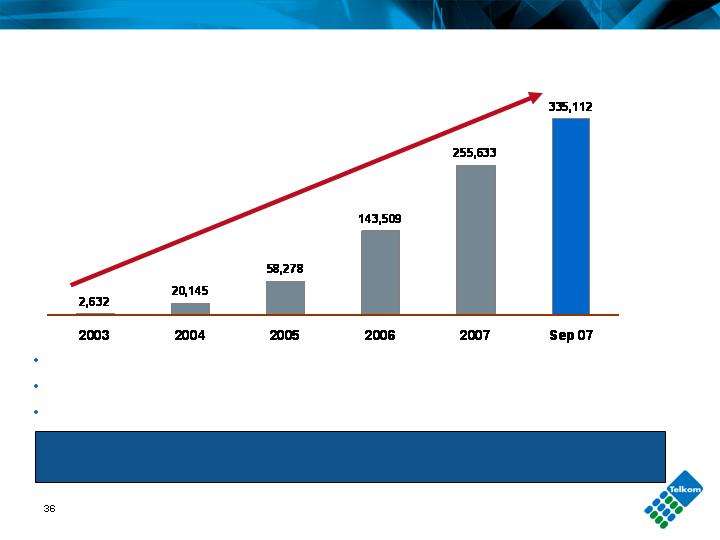

ADSL Year-On-Year Growth

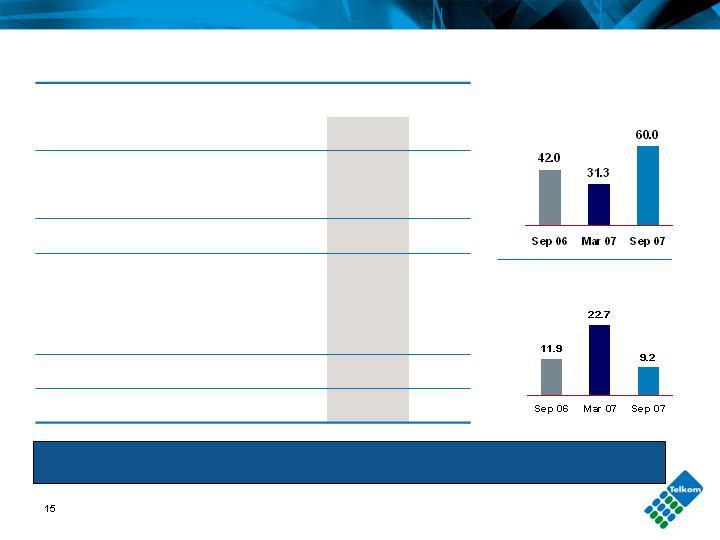

Significant growth driven by Self Install Option and growth in capacity

Increased ADSL footprint to 2,501 DSLAMs

4.9% growth in 2MB services to 163,430 over six months

76.2% growth in ADSL from Sept 2006 to Sept 2007

Self install update

Self Install Option (SIO) is a key enabler of accelerated ADSL growth

The YTD performance of SIO is 59% of all installations and growth

On target to reach 420,000 by March 2008

Do Broadband

Launched May 2007

Bundled DSL access and Telkom Internet

3 bundled options

Entry level option R199 per month

Host of value added services through Do Broadband Portal

Multimedia portal – driver for ADSL growth

WiMAX – complementing ADSL sweet spots

Balanced approach of wire and wireless technology

Additional 71 base stations targeted

27 sites fully operational

Internet WiMAX products launched

Voice service planned to be launched

by March 2008

Data Services

(25.5)

35

47

Multimedia services

Six months ended

4.7

2,191

2,093

Data connectivity

27.0

537

423

Internet access and related services

12.0

899

803

Leased lines facilities

22.7

313

255

Managed data networks

(Satellite & VPN Services)

%

Sep 07

Sep 06

ZAR millions

Data growth remains strong

Telkom currently has 227,066 dial-up subscribers and is maintaining its 24%

market share

Bundled packages

78,780

-

Do Broadband

92.6

5,144

2,671

Closer 1

162.7

166,144

63,223

Closer 2

57.2

179,599

114,274

Closer 3

39,674

-

Closer 4

6,028

-

Closer 5

Six months ended

452.3

11,250

2,037

SupremeCall

120.1

396,589

180,168

Telkom Closer

%

Sep 07

Sep 06

Subscriber numbers

Attractive value propositions increase uptake

Capabilities of NGN

Improved customer service

experience

Self-service

Flexible billing and bandwidth usage

Diversified offerings bring

convenience, flexibility and cost

saving benefits

Improved service delivery

Automation of service delivery

Self-service tools will reduce

operational load

Converged services

Providing customers with a global

experience

Quick deployment of new products &

services

Key NGN achievements

National and Local Transport Network

Network increased by 167 nodes

Bandwidth potential to increase by 1.2 Tbit/s - 17%

93 being installed, 128 being planned for next 6 months

Bandwidth potential to increase by 2.2 Tbit/s – 47% for

the next 12 months

Diginet services bandwidth potential to increase by 86 Gbit/s

8000 2MB/s equivalent links provided to mobile operators in last

6 months

52 Metro Ethernet sites rolled out in Western Cape and Gauteng

– ready to carry traffic

Increasing bandwidth to service explosive demand

Port Elizabeth

Capetown

Polokwane

Matching core capacity to meet explosive demand

National Layer – core bandwidth

1000% increase in

bandwidth potential over

the next 2 years

Metro Layer – core bandwidth

Aligning capacity to Metro demand

1600% increase in bandwidth

potential over the next 2

years

New NGN products

Easy VPN available to wholesale customers over ADSL network

VPN Lite recently launched (retail VPN for SMMEs using Easy VPN

with advanced self help and online charging solution)

Telkom Mobility enhanced to allow access via 3G. Allows

corporate employees to access head office network by number of

technologies including ADSL, dial-up and 3G

Wholesale VoIP Interconnect – allows all operators to interconnect

to PSTN via VoIP

Network Interactive Voice Response System – advanced speech

services

Product innovation provides revenue opportunities

Customer centricity

Customer Centricity at the core

of the Corporate Strategy

Established a Customer

Centricity Office in May 2006

Overseeing this strategic

drive at enterprise level

Designing processes from a customer perspective

Formulation of a Customer Centricity Roadmap

67 initiatives aimed at building foundational customer centricity

capabilities

38 have already kicked off

Key elements of journey towards Customer Centricity

Competitive

Advantage

On target to meet our roadmap

Time

Call Center

Quick wins

1-to-1 Marketing

Call Center

Master Plan design

Customer

Profitability

Customer

Insight

Customer

Segmentation

Value and Needs Based

Customer

Data Management

Churn Analysis

Organizational

Change

Data Quality

Management

Campaign

Management

Differentiated

treatment plan for high value

Residential Customers

Customer Portfolio

Management for

Mass & Enterprise markets

Customer

Promise

Management

Customer

Strategy

Service Delivery

Dashboard

Design

Productivity

Improvement

Current position

Customer segmentation

Segment customers according to

value and needs

Understand customer equity and

break-even points

Differentiated value and service to

high-value customers

Anticipate customer needs

Easily identify value enhancers and

cross selling opportunities

Call centre master plan – designed

around customer value groups

making it easier to do business with

us

“Treat different customers differently”

Telkom Media

Granted a commercial satellite and cable subscription broadcast license

in September 2007

License to be issued after negotiations with ICASA

Targeting the under-served LSM 5 – 8 market: over 40% of SA

households

Offering element of choice and value for money

Package flexibility paving the way to greater affordability

Joining Telkom to offer full suite of converged services

Complementing Telkom’s converged services offering

Telkom Media (cont)

Funding required R7.5 billion

Telkom Board approved funding of R800 million (Capex & Opex)

Business plan and go-to-market strategy being aligned with current

market dynamics

License fees and operational expenditure to September 30, 2007

- R55 million

Commencement of service expected in 2009 financial year

Multi-Links

A private telecommunications operator in Nigeria with a Unified Access

License allowing fixed, mobile, fixed-wireless, international and data

services

Acquired in April 2007 for R1,985 million

Contribution for 5 months to September 30, 2007

Revenue - R310 million

Net profit - - R5 million

Current subscribers – 262,000

Target for March 2008 – 812,000

Current ARPU – R220 (USD 32)

Expected ARPU March 2008 below R206 (USD 30)

Centre for West African switched hubbing strategy

Multi-Links (cont.)

Aggressive roll-out of NGN infrastructure

Allows maximum efficiency and minimal network opex cost

Expected capex at March 2008 – R1.6 billion (USD 228 million)

Suite of IP Enterprise Solutions allows differentiation in Nigerian

market

Plans to launch carrier quality wholesale voice, data and internet

services through SAT3 cable

Africa Online

An Internet Services Provider with operations in Kenya, Tanzania, Cote

d’Ivoire, Ghana, Uganda, Namibia, Swaziland, Zambia and Zimbabwe

Acquired for R150m in February 2007

Contributed to September 30, 2007

Revenue - R46 million

Opex - R53 million

Net loss - R7 million

Expecting net profit by March 2009

Expected positive cash flow by March 2010

Centre for East African switched hubbing strategy

Africa Online (cont.)

Focusing on aggressive wireless broadband infrastructure roll-out

Expected capex at March 2008 – R80 million (USD 11.6 million)

Expected capex at March 2010 – R137 million (USD 20 million)

Intends to grow presence from 9 – 15 countries within 3 years

Capitalising on synergies with Telkom

Driving broadband VSAT services to corporates and multi-nationals

Has partnerships with 5 major carriers, signing up a further 10

affiliates

Providing for the

bandwidth

explosion

Conclusion

Investor Relations

Nicola White

Tel: +27 12 311 5720

Fax: +27 12 311 5721

E-Mail: whitenh@telkom.co.za