Exhibit 99.5

VODACOM GROUP (PROPRIETARY) LIMITED

INTERIM RESULTS

FOR THE SIX MONTHS ENDED SEPTEMBER 30, 2007

Operational highlights

Alan Knott-Craig

Chief Executive Officer

Group highlights

For the six months ended September 30, 2007 vs. prior year

Total customers

31.6 million

22.6%

High gross connections: increase of 19.4% year on year to 8.7 million

Revenue

R22.8 billion

17.2%

Profit from operations

R5.7 billion

15.1%

EBITDA

R7.6 billion

15.5%

Net profit after tax

R3.7 billion

17.5%

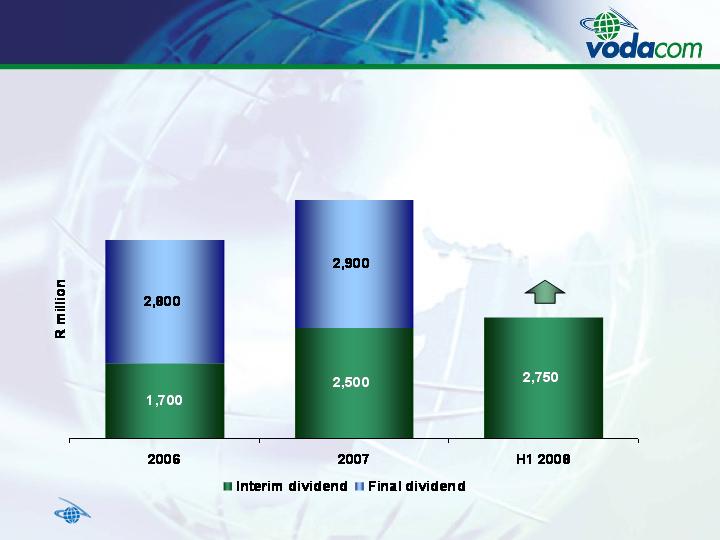

Interim dividend

(declared October 2007)

R2.75 billion

10.0%

Inactive customers – South Africa

Current rule

Call forwarding to voicemail is classified as a revenue generating activity

Disconnect inactive prepaid SIM cards after (6 + 1) months with no revenue generating activity on

the network

Supplementary rule

Disconnect inactive prepaid SIM cards after (12 + 1) months if only call forwarding to voicemail

and no other activity

Impact of supplementary rule

Disconnection of 2.9 million prepaid SIM cards in September 2007

Prepaid churn is expected to increase

South Africa

For the six months ended September 30, 2007 vs. prior year

5.8 million

Gross connections

45.9%

Churn %

86.8%

Mobile penetration %

R5.4 billion

Profit from operations

23.3 million

Total customers

H1 2008

15.3%

10.1%

14.6 pts

13.6%

2.9 pts

Tanzania

For the six months ended September 30, 2007 vs. prior year

1.2 million

Gross connections

46.8%

Churn %

17.3%

Mobile penetration %

R180 million

Profit from operations

3.7 million

Total customers

H1 2008

41.8%

36.6%

4.7 pts

34.3%

11.6 pts

3G has been launched in Dar es Salaam on March 1, 2007 (6,500 customers)

Democratic Republic of Congo (DRC)

For the six months ended September 30, 2007 vs. prior year

1.2 million

Gross connections

43.3%

Churn %

11.0%

Mobile penetration %

R172 million

Profit from operations

3.2 million

Total customers

H1 2008

56.8%

63.3%

4.4 pts

29.3%

13.3 pts

Lesotho

For the six months ended September 30, 2007 vs. prior year

80 thousand

Gross connections

17.9%

Churn %

22.1%

Mobile penetration %

R56 million

Profit from operations

332 thousand

Total customers

H1 2008

39.5%

45.5%

7.4 pts

64.7%

Mozambique

For the six months ended September 30, 2007 vs. prior year

R56 million

Loss from operations

391 thousand

Gross connections

57.3%

Churn %

13.7%

Mobile penetration %

R75 million

Loss from operations

(excluding impairment)

1.1 million

Total customers

H1 2008

55.5%

19.6%

3.0 pts

15.5 pts

Innovative non-voice products in South-Africa

Voted no 1 brand in telecommunication

Voted no 3 brand overall

Voted no 1 advertising company

Brand and marketing

More than 35 thousand unique Mobile TV users

26 TV channels

More than 4 thousand DSTV pay TV customers

Mobile TV / DVB-H

Changing media landscape: mobile

advertising and marketing

Mobile advertising launched on June 1, 2007

New products and services

Retail SMS 51.8% and bulk SMS 5.1% of data

revenue

Over 265 thousand data card and USB

modem users

Over 1.2 million Vodafone live! users

Vodafone live! / 3G / HSDPA

Group data revenue

Group data revenue as a % of

service revenue

45.3%

year on

year

Acquisitions of subsidiaries

On August 31, 2007 the Group increased its interest in the equity of Smartphone

SP (Proprietary) Limited from 70% to 100%

On September 1, 2007 the Group increased its interest in the equity of Smartcom

(Proprietary) Limited from 88% to 100%

Vodacom BEE equity transaction

Our envisaged BEE transaction has been impacted by pending shareholder

activity for the past four months

We are now pleased to announce that the Vodacom Group Board has given the

go ahead to proceed with the envisaged BEE equity transaction of R7.5 billion

Regulatory

Regulatory environment affecting the future potential earnings of the company:

Convergence Bill

Interconnect and wholesale rate regulations / mobile termination rates

Customer registrations (RICA)

EASSY cable delayed due to uncertainty as to landing rights

Current affairs

Vodacom Converged Solutions in place

Converged network services; managed hosting services; mobile and application services

Integrated into Vodacom South Africa

WiMax launch due early next year

Self provisioning of fiber rings underway. As at end October 2007, 15 km

completed and as at November 15, 2007, 23 km completed

Yebo radio launched on November 3, 2007. Destined for distribution channel, staff

and streaming to handsets

Earth station for international traffic completed in Midrand

Acquisitions for latest expansions underway

Financial review

Leon Crouse

Chief Financial Officer

Group income statement

For the six months ended September 30

n/a

(445)

4

(383)

Net finance (costs) / income

n/a

18

(38)

68

Impairment

17.5%

3,658

3,114

2,387

Net profit

13.2%

(1,611)

(1,855)

(1,455)

Taxation

(18.1%)

(15,215)

(12,888)

(10,612)

Operating expenses excluding depreciation,

amortisation and impairment

15.5%

7,600

6,578

5,563

EBITDA

(20.9%)

(1,904)

(1,575)

(1,406)

Depreciation and amortisation

15.1%

5,714

4,965

4,225

Profit from operations

6.0%

5,269

4,969

3,842

Profit before tax

17.2%

22,815

19,466

16,175

Revenue

H1 2007

%

change

H1 2008

H1 2006

R million

Effective tax rate 30.6% vs. 37.3% prior year, due to interim dividend declared in

October 2007

Group revenue

By country

23.4%

1,108

898

649

DRC

15.5%

20,299

17,580

14,764

South Africa, including holding companies

17.2%

22,815

19,466

16,175

69.4%

183

108

74

Mozambique

32.4%

139

105

77

Lesotho

40.1%

1,086

775

611

Tanzania

H1 2007

%

change

H1 2008

H1 2006

R million

Revenue driven by strong customer growth

Non-South African operations contributing 11.0% (H1 2007: 9.7%)

Group revenue

Composition

71.5%

952

555

485

International airtime

3.5%

2,393

2,312

1,910

Equipment sales

15.6%

4,304

3,723

3,186

Interconnection

14.4%

12,947

11,313

9,581

Airtime, connection & access

17.2%

22,815

19,466

16,175

2.5%

123

120

120

Other sales and services

45.3%

2,096

1,443

893

Data

H1 2007

%

change

H1 2008

H1 2006

R million

Revenue growth, excluding equipment sales was 19.1% (H1 2007: 20.3%)

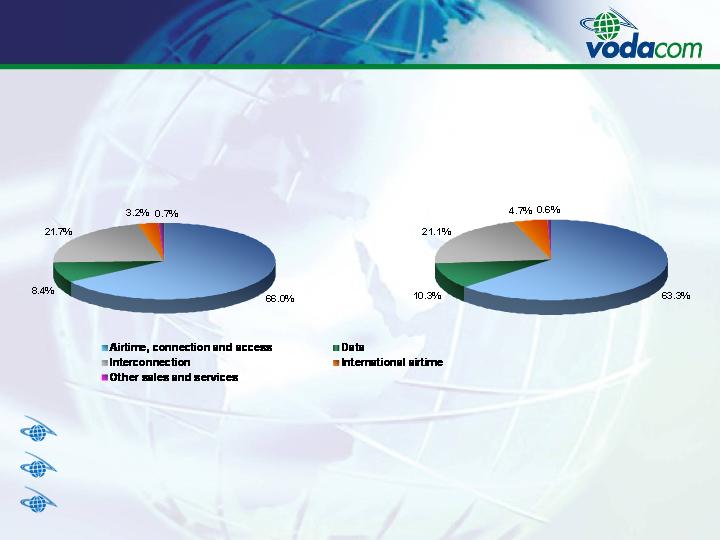

Group revenue (excluding equipment sales)

By revenue type

Revenue analysis – H1 2008

R20,422 million (excluding equipment sales)

Revenue analysis – H1 2007

R17,154 million (excluding equipment sales)

Airtime contribution down 2.7% points to 63.3%

Interconnect contribution down 0.6% points to 21.1%

Data contribution up 1.9% points to 10.3%

Group operational indicators

Gross connections up

19.4% year on year to a high of

8.7 million

Customers up 22.6% year on

year to 31.6 million

Total traffic in South Africa

increased by 14.0% year on

year to 11.0 billion minutes vs.

customer growth of 15.3%

Gross connections

Closing customers

Factors affecting trends and margins

South Africa traffic mix

Outgoing traffic increased 14.2% year on

year to 7.4 billion minutes:

Outgoing fixed increased by 3.8% to 624 million

Outgoing mobile increased by 15.3% to 6.8 billion

Incoming traffic increased 13.6% year on

year to 3.6 billion minutes:

Incoming fixed increased by 4.0% to 1.3 billion

Incoming mobile increased by 19.5% to 2.4 billion

Mobile to mobile traffic increased by 16.4%

to 9.1 billion minutes

Mobile/fixed traffic increased by 3.9% to 1.9

billion minutes

South Africa net interconnect

Total South Africa traffic

14.0%

year on

year

9.0%

year on

year

ARPU by country

Declining ARPUs

SA decreased 4.0% to R119

DRC decreased 22.9% to R64

Lesotho decreased 5.3% to R72

Tanzania decreased 9.4% to R48

Mozambique stable at R27

Vodacom Group consolidated

ARPU decreased 7.2% year on

year from R111 to R103

ARPU per month

South Africa ARPU

Contract ARPU decreased

7.8% year on year to R487

Prepaid ARPU decreased

3.3% year on year to R59

Total ARPU decreased

4.0% year on year to R119

South Africa ARPU per month

EBITDA and margin analysis

EBITDA margin by country

EBITDA performance

Increased 15.5% year on year to R7.6 billion

EBITDA margin decreased 0.5% points year on year to

33.3%

EBITDA margin 38.3%, when excluding cellular phone

and equipment sales

South Africa EBITDA

Increased 14.9% year on year to R6.9 billion

EBITDA margin decreased 0.2% points year on year to

34.0%

EBITDA for non-South African operations

Increased 40.7% year on year to R719 million

Non-South African operations contributed 9.5% of total

vs. 7.8% for the same period in the previous financial

year

Tanzania EBITDA margin decreased: increase in excise

duty on airtime; inflated fuel prices; competition

15.5%

year on

year

EBITDA

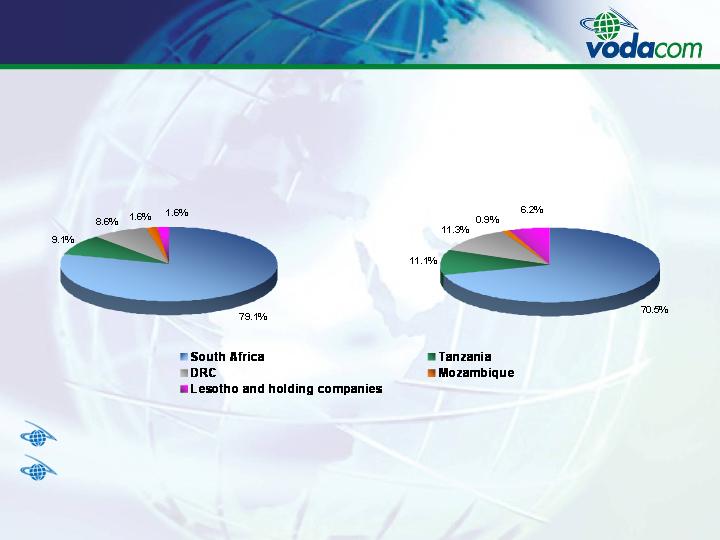

Group profit from operations

By country

29.3%

172

133

47

DRC

(147.4%)

(27)

57

2

Holding companies

34.3%

180

134

115

Tanzania

(0.5% pts)

25.0%

25.5%

26.1%

Profit from operations margin (%)

15.1%

5,714

4,965

4,225

59.4%

(56)

(138)

(25)

Mozambique

64.7%

56

34

26

Lesotho

13.6%

5,389

4,745

4,060

South Africa

H1 2007

%

change

H1 2008

H1 2006

R million

Customer growth of 22.6% to 31.6 million

Revenue growth of 17.2%; operating expenses growth of 18.1%; depreciation, amortisation

and impairment growth of 16.9%

Productivity measures

Consolidated customers

per employee

Increased 8.0% year on year to 5,058 based

on 6,240 employees

Consolidated gross capex

additions as a % of revenue

decreased to 10.0% from 16.1%

for the same period in the

previous financial year

Gross capex additions at R2.3

billion vs. R3.1 billion for the same

period in the previous financial

year

Gross capex additions as a % of revenue

Gross capex additions as a % of revenue

Capex additions and composition

Including software

Capex gross additions – H1 2008

R2,289 million

Capex gross additions – H1 2007

R3,142 million

South Africa capex gross additions decreased by 35.1% to R1.6 billion

Non-South African capex additions decreased by 10.7% to R551 million

Cash generation

EBITDA increased by R1.0 billion

Cash generated from operations

increased by 26.1% to R6.9 billion

Free cash flow decreased from

R837 million to negative R582

million

Net investments increased by R948 million

Capex payments increased by R1.0 billion

or 39.9%

Cash generated from operations

Free cash flow

26.1%

year on

year

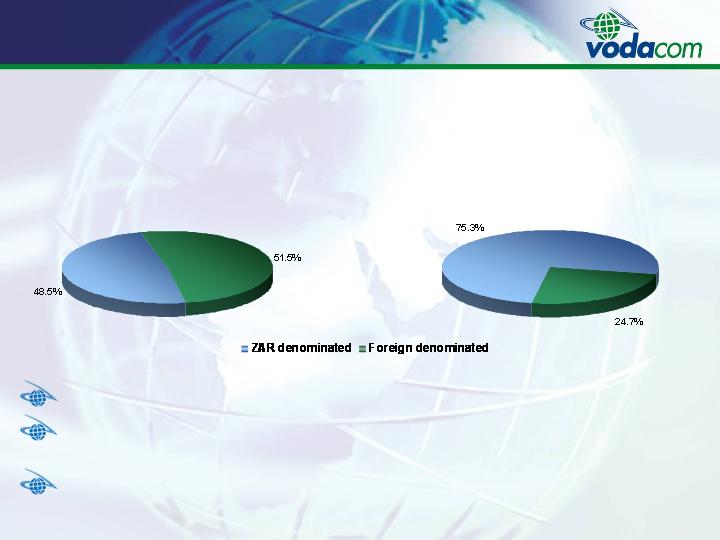

Debt composition

Gross debt composition

including bank overdrafts – H1 2008

R6,949 million

Gross debt composition

including bank overdrafts – H1 2007

R3,873 million

Net debt: R6,150 million (H1 2007: R3,006 million)

Net debt to adjusted equity ratio of 56.6% (H1 2007: 37.5%); 118.4% when including the

dividend declared in October (H1 2007: 72.6%)

Net debt to EBITDA ratio of 40.5% (H1 2007: 45.7%)

Group shareholder distributions

Interim dividend declared in October 2007

10.0%

year on

year

Questions?

Group balance sheet

Extracts as at

(5.7%)

14,155

15,011

13,513

Current liabilities

8.8%

30,984

28,470

26,586

Total equity and liabilities

(5.4%)

3,607

3,812

3,705

Non-current liabilities

37.1%

13,222

9,647

9,368

EQUITY AND LIABILITIES

Equity

8.8%

30,984

28,470

26,586

Total assets

19.7%

9,125

7,626

8,062

Current assets

4.9%

21,859

20,844

18,524

ASSETS

Non-current assets

March 2007

%

change

H1 2008

H1 2007

R million

Group cash flow statement

Extracts for the six months ended

n/a

763

(261)

1,372

Cash and cash equivalents at the

end of the year

(116.7%)

(15)

90

(12)

Effect of foreign exchange rate changes

(106.1%)

(108)

1,760

2,173

Cash and cash equivalents at the

beginning of the period

142.0%

886

(2,111)

(789)

Net increase in cash and cash

equivalents

n/a

4,458

(112)

(35)

Net cash flows utilised in

financing activities

(75.4%)

(4,641)

(2,646)

(2,231)

Net cash flows utilised in investing

activities

65.2%

1,069

647

1,477

Net cash flows from operating activities

26.1%

6,879

5,454

4,922

Cash generated from operations

H1 2007

%

change

H1 2008

H1 2006

R million

Disclaimer

This presentation has been prepared and published by Vodacom Group (Proprietary) Limited.

Vodacom Group (Proprietary) Limited is a private company and as such is not required by the Companies Act 61 of 1973, as amended, to publish its results.

Vodacom Group (Proprietary) Limited makes no guarantee, assurance, representation and/or warranty as to the accuracy of the information contained in this presentation and will not be held liable for any reliance placed on the information contained in this presentation.

The information contained in this presentation is subject to change without notice and may be incomplete or condensed. In addition, this presentation may not contain all material information pertaining to Vodacom Group (Proprietary) Limited and its subsidiaries.

Without in any way derogating from the generality of the foregoing, it should be noted that:

Many of the statements included in this presentation are forward-looking statements that involve risks and/or uncertainties and caution must be exercised in placing any reliance on these statements. Moreover, Vodacom Group (Proprietary) Limited will not necessarily update any of these statements after the date of this presentation either to conform them to actual results or to changes in its expectations.

Insofar as the shareholders of Vodacom Group (Proprietary) Limited are listed and offer their shares publicly for sale on recognised stock exchanges locally and/or internationally, potential investors in the shares of Vodacom Group (Proprietary) Limited’s shareholders are cautioned not to place undue reliance on this presentation.