Filed by PartnerRe Ltd.

pursuant to Rule 425 of the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: AXIS Capital Holdings Limited

Commission File No.: 001-31721

Preferred Shareholder FAQ

1. What is the status of the planned merger with AXIS Capital that you announced in January?

After carefully evaluating the alternatives, the PartnerRe Board has reaffirmed its recommendation of the AXIS transaction and on May 22, 2015 we announced our intent to proceed to a shareholder vote to approve the merger with AXIS Capital.

Our Board of Directors has affirmed its recommendation of the AXIS transaction and we recommend that our shareholders vote in favor of the AXIS merger and help tocreate one of the world’s preeminent specialty insurance and reinsurance companies, with gross premiums written in excess of $10 billion, total capital of more than $14 billion, and cash and invested assets of more than $31 billion.

2. I read that EXOR S.p.A made an unsolicited offer to acquire PartnerRe. What is the Company’s view on this offer?

We have made it very clear that EXOR’s proposed price and terms are unacceptable to us and are not in the best interests of our shareholders – including our Preferred Shareholders. EXOR has made it abundantly clear that it does not intend to improve the terms of its offer.

3. What does the merger with AXIS Capital mean for me as a Preferred Shareholder?

It is important that you, as a Preferred Shareholder, understand thesuperior protection afforded your investment by the AXIS transaction we are pursuing.

PartnerRe and AXIS currently have A- Long-Term Ratings from S&P, both with “Stable Outlooks.” In addition, both PartnerRe and AXIS are currently rated A+ by AM Best and S&P with respect to each Company’s financial strength. These strong ratings from leading global investor rating services result in a rating for your preferred securities of BBB, reflecting the meaningful security of your dividends and the value of your investment.

Based on our analysis and initial feedback from the rating agencies after their review of our capital plans, we are confident that these ratings would remain at their current strong levels upon closing of the agreed transaction with AXIS and into the future.Importantly, in the case of the AXIS merger the current BBB rating on your preferred securities is unlikely to change.

In addition, your investment in the capital structure of the new merged Company will be supported by a stronger combined balance sheet, an increased equity base, and your dividend stream will be supported by the greater earnings of the merged Company.

4. What would an acquisition by EXOR mean for me as a PartnerRe Preferred Shareholder?

While we believe EXOR’s offer for PartnerRe is inferior for all of our shareholders,it is particularly disadvantageous to our Preferred Shareholders.

Filed by PartnerRe Ltd.

pursuant to Rule 425 of the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: AXIS Capital Holdings Limited

Commission File No.: 001-31721

First, as a Preferred Shareholder, your shares would not be acquired by EXOR and you would not benefit from the EXOR’s cash offer for PartnerRe’s common shares of $137.50.

Second, you would likely be exposed to a lower credit rating, and PartnerRe would become a subsidiary of a highly leveraged group as a result of the transaction financing that EXOR needs to incur.

Furthermore, it is wholly unclear what the level of dividends from PartnerRe to the EXOR holding company will be. In addition to extensive debt, EXOR is engaged in a number of challenged and highly capital intensive businesses that create uncertainty as to how PartnerRe’s earnings are to be used. Indeed, a key rationale for EXOR’s proposal to acquire PartnerRe is the “high cash generation and capital generation to shareholders”.In essence a vote in favor of the AXIS merger is the best way to protect your investment.

5. What would the leverage of PartnerRe be under an acquisition by EXOR?

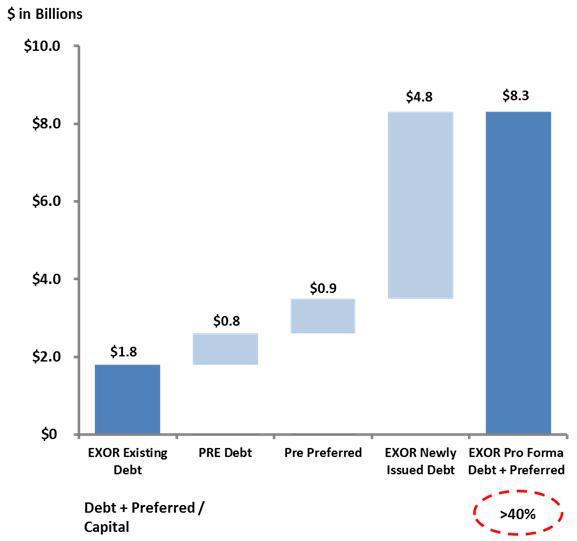

The leverage ratio (calculated as the sum of debt and preferred securities, divided by total book capitalization) is an important metric used by rating agencies in determining the credit worthiness of an insurance holding company

In assessing the financial strength of an insurance company, ratings agencies take into account the credit worthiness of the holding company and the extent to which debt at the holding company is used to fund the operations of the insurance company (so-called “double leverage”). This focus on double leverage and the need for the insurance company to service the debt of the holding company means that any debt that exists at the EXOR level would likely be considered by the ratings agencies as they consider the rating of PartnerRe.

The chart below shows the comprehensive manner in which to account for the high level of leverage that EXOR would incur under its proposal to acquire PartnerRe.

Filed by PartnerRe Ltd.

pursuant to Rule 425 of the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: AXIS Capital Holdings Limited

Commission File No.: 001-31721

Pro forma for the acquisition of PartnerRe and sale of Cushman & Wakefield, EXOR’s leverage ratio could exceed 40%. EXOR may have other assets that it is looking to sell to reduce the leverage ratio but there is no visibility on what these assets are, the timetable, pricing or achievability of such sales.

By comparison, the pro forma leverage ratio for the combined AXIS / PartnerRe at 31 March 2015 is 23.1%.

6. Won’t PartnerRe have significantly less debt under an acquisition by EXOR?

There are two key items to note when comparing the level of debt under the ParterRe/AXIS merger vs. the EXOR acquisition.

1. The merger of PartnerRe and AXIS would not involve taking on any additional debt, at any level, compared to that currently held by the two entities on a standalone level. In addition, the merged PartnerRe/AXIS will be nearly twice as large ($12.9bn pro forma equity capitalization vs. $7.3bn

Filed by PartnerRe Ltd.

pursuant to Rule 425 of the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: AXIS Capital Holdings Limited

Commission File No.: 001-31721

standalone), with nearly 2.5x the earnings power by 2017 (>$1.2bn pro forma earnings including synergies and growth opportunities vs. $479mm standalone) which is more than sufficient to support the combined senior debt of both PartnerRe and AXIS.

The combined company will also benefit from much higher interest and preferred dividend coverage ratios (earnings before tax, interest expense and preferred dividends, divided by interest expense and preferred dividends). The interest and preferred dividend coverage ratio would increase from 9.2x in 2014 for the standalone scenario to 11.0x in the combined company pro forma for synergies and new growth opportunities – the higher coverage ratio indicates that there is more protection afforded to your preferred dividend.

2. As noted above, an acquisition of PartnerRe by EXOR would introduce significant existing debt ($1.8bn) and new acquisition debt (up to $4.75bn) at the EXOR holding company level, which will have major implications for you as a preferred shareholder. While there may not be any incremental debt taken on at the PartnerRe Ltd entity initially, the debt held by EXOR will need to be serviced by dividends from PartnerRe, which will impact you as a preferred shareholder.

7. How will the capital management plans of the combined PartnerRe/AXIS impact me as a preferred shareholder?

Our ability to return high levels of capital to our shareholders results from the ability of the combined PartnerRe/AXIS to operate and support further growth while maintaining an inherently conservative reserving philosophy, and diligent risk management practices. Additionally, our plan maintains capital for the combined PartnerRe/AXIS at above “AA” levels, leaving a significant buffer above the expected “A-“ S&P ratings for the combined Company.

As noted, preferred shareholders will be protected by their enhanced interest coverage ratios in the combined company. The capital management plans recognize the significant cash flows produced by the combined company after preferred dividends.

Further, the rating agencies have reviewed the capital management plan of the pro forma company, and given their favorable responses we remain confident that our ratings will be maintained.

8. What is my exposure to the integration process between PartnerRe and AXIS?

Our management teams have a high level of cultural compatibility with key members of management having direct work experience at both companies, and extensive experience in successful expense reduction initiatives.

The integration process is well under way, with a developed operating model for each business unit and a support team of over 150 people involved.

The concrete and identified synergies (at least $200 million) support the credit profile of the combined company, with further upside from new growth opportunities.

Filed by PartnerRe Ltd.

pursuant to Rule 425 of the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: AXIS Capital Holdings Limited

Commission File No.: 001-31721

9. What have the ratings agencies said about the PartnerRe/AXIS merger and the potential acquisition by EXOR?

Rating agencies have highlighted the weakness in the EXOR proposal:

| · | “We could consider a negative rating action if, following reinvestment of its liquidity, EXOR were unable to restore its portfolio quality and diversityor if the company's LTV ratio were to exceed 20%.” S&P, Nov 14, 2014 |

| · | “The negative outlook reflects our view that if the PartnerRe acquisition is completed, EXOR’s LTV may exceed our 20% threshold for the ratings. It also reflects our view that EXOR’s listed assets may fall below 60% of total assets, which we believewould not be commensurate with our current assessment of a ‘satisfactory’ business risk profile.” S&P, Apr 17, 2015 |

| · | “We would also likely revise the outlook to stable if the [PRE] acquisition does not close.” S&P, Apr 17, 2015 |

| · | “On balance,we see [a successful EXOR bid] as credit negative since PartnerRe would miss out on an opportunity to strengthen its market position and improve its product diversification by gaining access to AXIS Capital’s profitable specialty primary insurance platform. In an increasingly competitive and tiered insurance marketplace, a PartnerRe-AXIS Capital combination would provide the scale and breadth of product offerings that are highly valued by brokers and clients.” Moody’s, Apr 20, 2015 |

Conversely, rating agencies have been positive on the AXS / PRE amalgamation:

| · | “Despite the announced approximately $560 million special cash dividend, we expect the combined company’s capitalization will remain very strong and materially redundant to ‘AA’ level after the deal closes and through 2017.” S&P, May 4, 2015 |

| · | “…if the transaction with AXIS closes as planned, Fitch would likely affirm PRE's current ratings…” Fitch, May 4, 2015 |

10. What is the impact to my rights as a preferred shareholder under the EXOR offer?

As a preferred shareholder, you have a vote that has meaningful value. Your ability to cast a vote to approve the amalgamation between PartnerRe and AXIS, and in doing so protect your investment and your dividend, is an example of this valuable vote in action.

However, if EXOR acquires all of the common shares in PartnerRe, your vote would effectively be nullified. In future, EXOR will be able to vote the block of common shares as one, and remove the significant say that you have in the strategic direction of PartnerRe and the protection of your investment and dividend.

Filed by PartnerRe Ltd.

pursuant to Rule 425 of the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: AXIS Capital Holdings Limited

Commission File No.: 001-31721

11. What is the potential impact on the trading liquidity and valuation of my preferred shares under the EXOR offer?

It is highly unusual for listed retail preferred securities such as the PartnerRe preferred securities to not be supported by publicly traded common equity. Under an EXOR acquisition, there would be no publicly traded common equity and hence it is impossible to say what impact this would have on the trading liquidity and hence valuation of your preferred shares.

12. Would an acquisition by EXOR put my dividend at risk?

Given EXOR’s lower Long-Term Ratings from S&P (BBB+ with a “Negative Outlook”) compared to that of PartnerRe and AXIS, and the meaningful additional debt contemplated in EXOR’s proposed transaction financing, we believe there is considerable risk that the rating of your preferred shares would be downgraded under EXOR’s proposed transaction.

Also importantly, EXOR’s proposed transaction would include up to $4.75bn of acquisition financing, which would impose significant debt servicing requirements. In contrast, the merger with AXIS would not result in a noticeable change to PartnerRe’s current capital structure and leverage. Voting in favor of the AXIS merger is the best way to protect your investment.

13. What steps should I take to protect my investment in PartnerRe’s Preferred Shares?

The merger of PartnerRe and AXIS will create a stronger, more stable and diversified company and will protect your investment. We strongly recommend that you vote in favor of this transaction prior to our upcoming Special General Meeting of Shareholders on July 24, 2015.

You will receive a proxy voting card in the mail.

Important Information For Investors And Shareholders

This communication does not constitute an offer to buy or sell or the solicitation of an offer to buy or sell any securities or a solicitation of any vote or approval. This communication relates to a proposed business combination between PartnerRe Ltd. (“PartnerRe”) and AXIS Capital Holdings Limited (“AXIS”). In connection with this proposed business combination, PartnerRe and AXIS have filed a registration statement on Form S-4 with the Securities and Exchange Commission (the “SEC”), and a definitive joint proxy statement/prospectus of PartnerRe and AXIS and other documents related to the proposed transaction. This communication is not a substitute for any such documents. The registration statement was declared effective by the SEC on June 1, 2015 and the definitive proxy statement/prospectus has been mailed to shareholders of PartnerRe and AXIS. INVESTORS AND SECURITY HOLDERS OF PARTNERRE AND AXIS ARE URGED TO READ THE REGISTRATION STATEMENT, JOINT PROXY STATEMENT/PROSPECTUS AND OTHER DOCUMENTS THAT HAVE BEEN OR MAY BE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION. A definitive proxy statement has been mailed to shareholders of PartnerRe and AXIS.

Filed by PartnerRe Ltd.

pursuant to Rule 425 of the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: AXIS Capital Holdings Limited

Commission File No.: 001-31721

Investors and security holders may obtain free copies of these documents and other documents filed with the SEC by PartnerRe and/or AXIS through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by PartnerRe are available free of charge on PartnerRe’s internet website at http://www.partnerre.com or by contacting PartnerRe’s Investor Relations Director by email at robin.sidders@partnerre.com or by phone at 1-441-294-5216. Copies of the documents filed with the SEC by AXIS are available free of charge on AXIS’ internet website at http://www.axiscapital.com or by contacting AXIS’ Investor Relations Contact by email at linda.ventresca@axiscapital.com or by phone at 1-441-405-2727.

Participants in Solicitation

PartnerRe, AXIS, their respective directors and certain of their respective executive officers may be considered participants in the solicitation of proxies in connection with the proposed transaction. Information about the directors and executive officers of PartnerRe is set forth in its Annual Report on Form 10-K for the year ended December 31, 2014, which was filed with the SEC on February 26, 2015, its proxy statement for its 2014 annual meeting of stockholders, which was filed with the SEC on April 1, 2014, its Quarterly Report on Form 10-Q for the quarter ended March 31, 2015, which was filed with the SEC on May 4, 2015 and its Current Reports on Form 8-K, which were filed with the SEC on January 29, 2015, May 16, 2014 and March 27, 2014. Information about the directors and executive officers of AXIS is set forth in its Annual Report on Form 10-K for the year ended December 31, 2014, which was filed with the SEC on February 23, 2015, its proxy statement for its 2014 annual meeting of stockholders, which was filed with the SEC on March 28, 2014, its Quarterly Report on Form 10-Q for the quarter ended March 31, 2015, which was filed with the SEC on May 4, 2015 and its Current Reports on Form 8-K, which were filed with the SEC on March 11, 2015, January 29, 2015, August 7, 2014, June 26, 2014, March 27, 2014 and February 26, 2014.

These documents can be obtained free of charge from the sources indicated above. Additional information regarding the participants in the proxy solicitations and a description of their direct and indirect interests, by security holdings or otherwise, is contained in the joint proxy statement/prospectus and other relevant materials filed with the SEC.

Forward Looking Statements

Certain statements in this communication regarding the proposed transaction between PartnerRe and AXIS are “forward-looking” statements. The words “anticipate,” “believe,” “ensure,” “expect,” “if,” “illustrative,” “intend,” “estimate,” “probable,” “project,” “forecasts,” “predict,” “outlook,” “aim,” “will,” “could,” “should,” “would,” “potential,” “may,” “might,” “anticipate,” “likely” “plan,” “positioned,” “strategy,” and similar expressions, and the negative thereof, are intended to identify forward-looking statements. These forward-looking statements, which are subject to risks, uncertainties and assumptions about PartnerRe and AXIS, may include projections of their respective future financial performance, their respective anticipated growth strategies and anticipated trends in their respective businesses. These statements are only predictions based on current expectations and projections about future events. There are important factors that could cause actual results, level of activity, performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied by the forward-looking statements, including the risk factors set forth in PartnerRe’s and AXIS’ most recent reports on Form 10-K, Form 10-Q and other documents on file with the SEC and the factors given below:

• the failure to obtain the approval of shareholders of PartnerRe or AXIS in connection with the proposed transaction;

• the failure to consummate or delay in consummating the proposed transaction for other reasons;

Filed by PartnerRe Ltd.

pursuant to Rule 425 of the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: AXIS Capital Holdings Limited

Commission File No.: 001-31721

• the timing to consummate the proposed transaction;

• the risk that a condition to closing of the proposed transaction may not be satisfied;

• the risk that a regulatory approval that may be required for the proposed transaction is delayed, is not obtained, or is obtained subject to conditions that are not anticipated;

• AXIS’ or PartnerRe’s ability to achieve the synergies and value creation contemplated by the proposed transaction;

• the ability of either PartnerRe or AXIS to effectively integrate their businesses; and

• the diversion of management time on transaction-related issues.

PartnerRe’s forward-looking statements are based on assumptions that PartnerRe believes to be reasonable but that may not prove to be accurate. AXIS’ forward-looking statements are based on assumptions that AXIS believes to be reasonable but that may not prove to be accurate. Neither PartnerRe nor AXIS can guarantee future results, level of activity, performance or achievements. Moreover, neither PartnerRe nor AXIS assumes responsibility for the accuracy and completeness of any of these forward-looking statements. PartnerRe and AXIS assume no obligation to update or revise any forward-looking statements as a result of new information, future events or otherwise, except as may be required by law. Readers are cautioned not to place undue reliance on these forward-looking statements that speak only as of the date hereof.