Filed by PartnerRe Ltd.

pursuant to Rule 425 of the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: AXIS Capital Holdings Limited

Commission File No.: 001-31721

| GRAPHIC OMMITTED Unacceptable Risks Posed by the EXOR Offer June 2015 |

| DISCLAIMER Participants in Solicitation PartnerRe, AXIS, their respective directors and certain of their respective executive officers may be considered participants in the solicitation of proxies in connection with the proposed transaction. Information about the directors and executive officers of PartnerRe is set forth in its Annual Report on Form 10-K for the year ended December 31, 2014, which was filed with the SEC on February 26, 2015, its proxy statement for its 2014 annual meeting of stockholders, which was filed with the SEC on April 1, 2014, its Quarterly Report on Form 10-Q for the quarter ended March 31, 2015, which was filed with the SEC on May 4, 2015 and its Current Reports on Form 8-K, which were filed with the SEC on January 29, 2015, May 16, 2014 and March 27, 2014. Information about the directors and executive officers of AXIS is set forth in its Annual Report on Form 10-K for the year ended December 31, 2014, which was filed with the SEC on February 23, 2015, its proxy statement for its 2014 annual meeting of stockholders, which was filed with the SEC on March 28, 2014, its Quarterly Report on Form 10-Q for the quarter ended March 31, 2015, which was filed with the SEC on May 4, 2015 and its Current Reports on Form 8-K, which were filed with the SEC on March 11, 2015, January 29, 2015, August 7, 2014, June 26, 2014, March 27, 2014 and February 26, 2014. These documents can be obtained free of charge from the sources indicated above. Additional information regarding the participants in the proxy solicitations and a description of their direct and indirect interests, by security holdings or otherwise, is contained in the joint proxy statement/prospectus and other relevant materials filed with the SEC. |

|

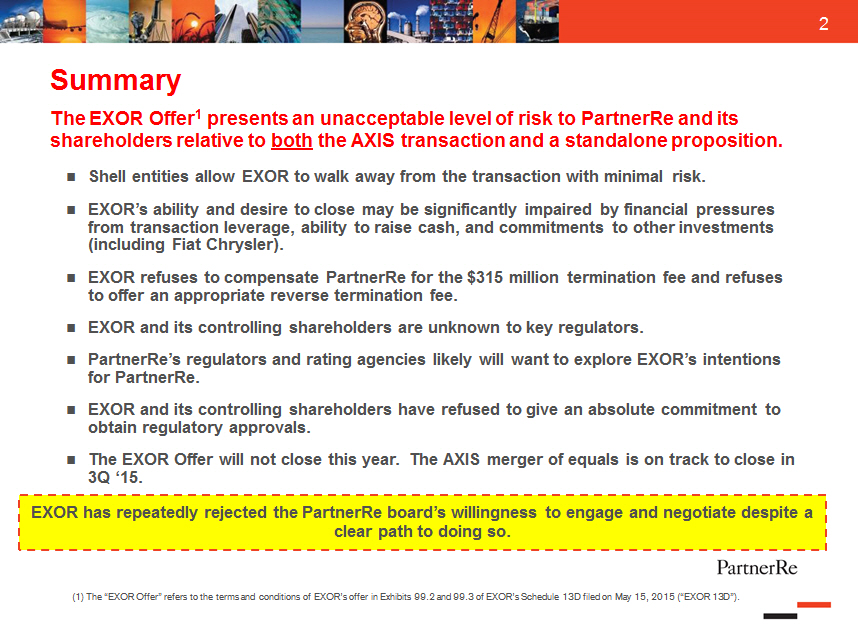

Summary

The EXOR Offer(1) presents an unacceptable level of risk to PartnerRe and its

shareholders relative to both the AXIS transaction and a standalone

proposition.

[] Shell entities allow EXOR to walk away from the transaction with minimal

risk.

[] EXOR's ability and desire to close may be significantly impaired by

financial pressures from transaction leverage, ability to raise cash, and

commitments to other investments (including Fiat Chrysler) .

[] EXOR refuses to compensate PartnerRe for the $315 million termination fee

and refuses to offer an appropriate reverse termination fee.

[] EXOR and its controlling shareholders are unknown to key regulators.

[] PartnerRe's regulators and rating agencies likely will want to explore

EXOR's intentions for PartnerRe.

[] EXOR and its controlling shareholders have refused to give an absolute

commitment to obtain regulatory approvals.

[] The EXOR Offer will not close this year. The AXIS merger of equals is on

track to close in 3Q '15.

EXOR has repeatedly rejected the PartnerRe board's willingness to engage and

negotiate despite a clear path to doing so.

(1) The "EXOR Offer" refers to the terms and conditions of EXOR's offer in

Exhibits 99.2 and 99.3 of EXOR's Schedule 13D filed on May 15, 2015 ("EXOR

13D").

|

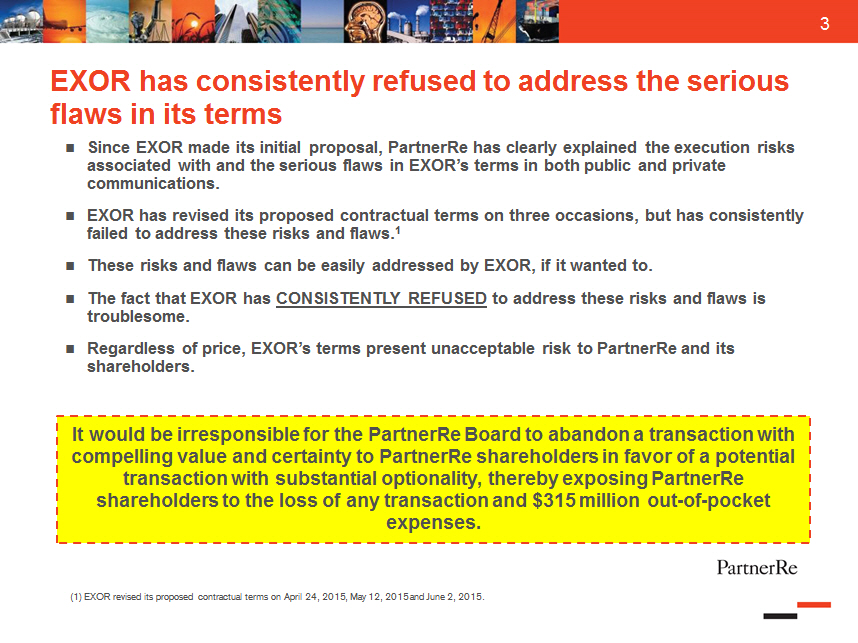

| EXOR has consistently refused to address the serious flaws in its terms [] Since EXOR made its initial proposal, PartnerRe has clearly explained the execution risks associated with and the serious flaws in EXOR's terms in both public and private communications. [] EXOR has revised its proposed contractual terms on three occasions, but has consistently failed to address these risks and flaws.(1)[] These risks and flaws can be easily addressed by EXOR, if it wanted to. [] The fact that EXOR has CONSISTENTLY REFUSED to address these risks and flaws is troublesome. [] Regardless of price, EXOR's terms present unacceptable risk to PartnerRe and its shareholders. It would be irresponsible for the PartnerRe Board to abandon a transaction with compelling value and certainty to PartnerRe shareholders in favor of a potential transaction with substantial optionality, thereby exposing PartnerRe shareholders to the loss of any transaction and $315 million out-of-pocket expenses. (1) EXOR revised its proposed contractual terms on April 24, 2015, May 12, 2015 and June 2, 2015. |

| Walkaway Risks |

|

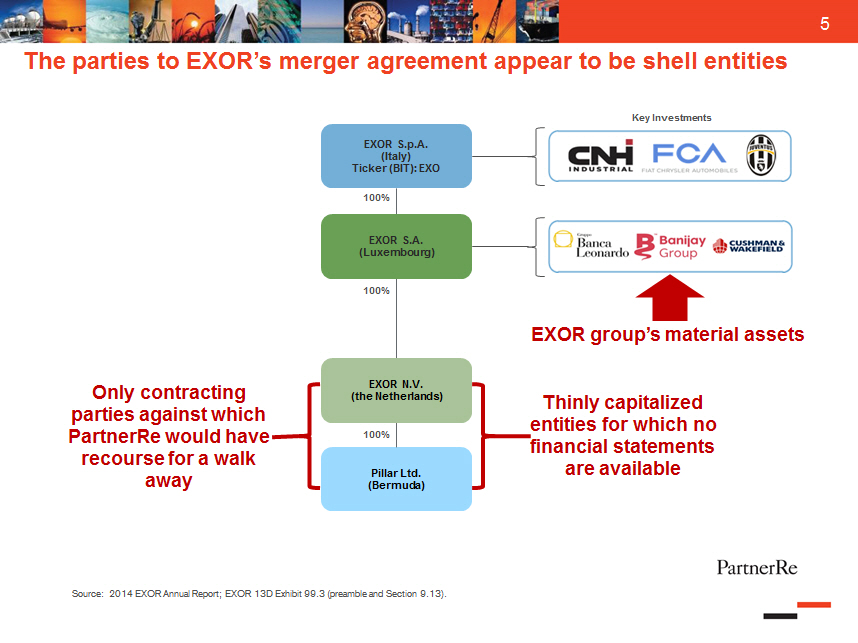

The parties to EXOR's merger agreement appear to be shell entities

Only contracting parties against which PartnerRe would have recourse for

a walk away

EXOR S.p.A. (Italy) Ticker (BIT): EXO

100%

EXOR S.A.

(Luxembourg)

100%

EXOR N.V.

(the Netherlands)

100%

Pillar Ltd.

(Bermuda)

Key Investments

EXOR group's material assets

Thinly capitalized entities for which no financial statements are available

Source: 2014 EXOR Annual Report; EXOR 13D Exhibit 99.3 (preamble and Section

9.13) .

|

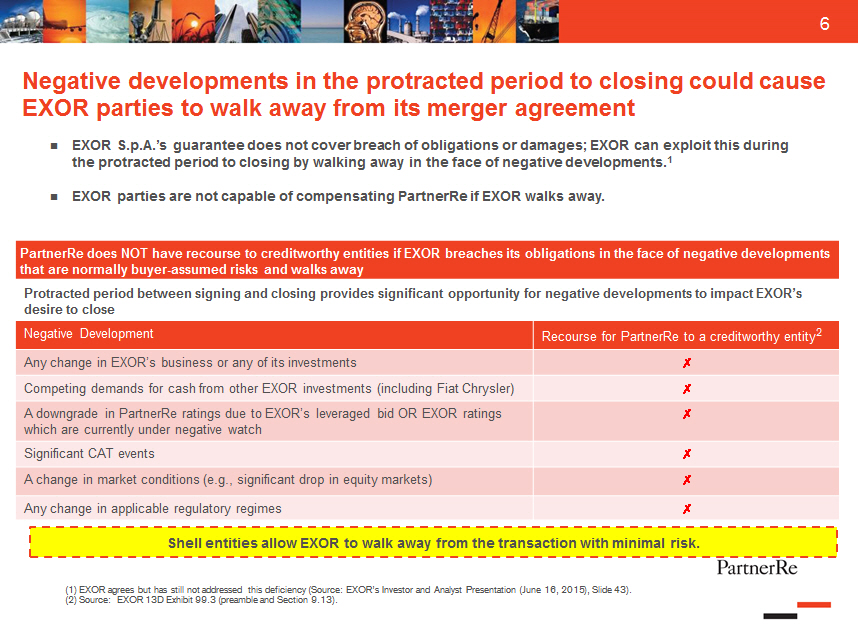

| Negative developments in the protracted period to closing could cause EXOR parties to walk away from its merger agreement [] EXOR S.p.A.'s guarantee does not cover breach of obligations or damages; EXOR can exploit this during the protracted period to closing by walking away in the face of negative developments. (1) [] EXOR parties are not capable of compensating PartnerRe if EXOR walks away. PartnerRe does NOT have recourse to creditworthy entities if EXOR breaches its obligations in the face of negative developments that are normally buyer-assumed risks and walks away Protracted period between signing and closing provides significant opportunity for negative developments to impact EXOR's desire to close Negative Development Recourse for PartnerRe to a creditworthy entity(2) Any change in EXOR's business or any of its investments Competing demands for cash from other EXOR investments (including Fiat Chrysler) A downgrade in PartnerRe ratings due to EXOR's leveraged bid OR EXOR ratings which are currently under negative watch Significant CAT events A change in market conditions (e.g., significant drop in equity markets) Any change in applicable regulatory regimes Shell entities allow EXOR to walk away from the transaction with minimal risk. (1) EXOR agrees but has still not addressed this deficiency (Source: EXOR's Investor and Analyst Presentation (June 16, 2015), Slide 43). (2) Source: EXOR 13D Exhibit 99.3 (preamble and Section 9.13) . |

|

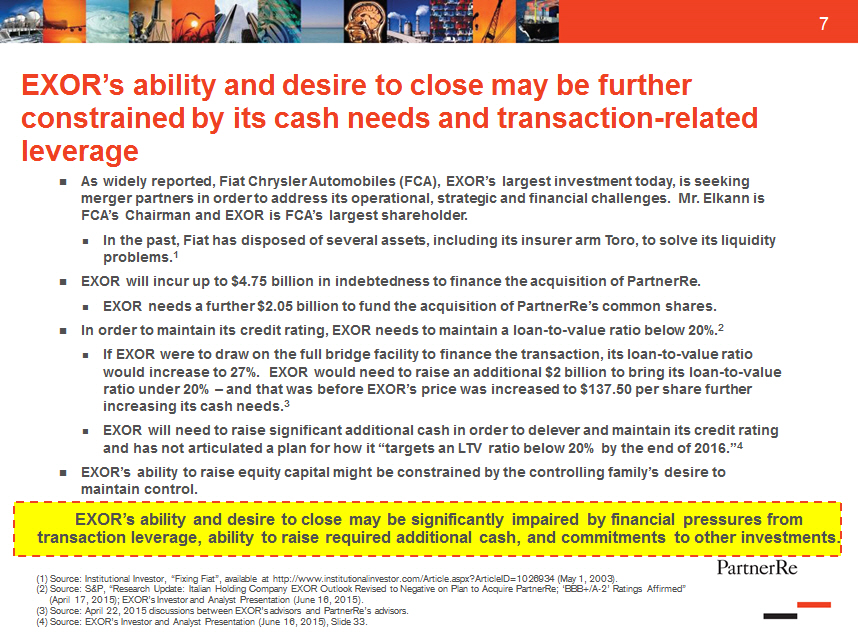

EXOR's ability and desire to close may be further constrained by its cash needs

and transaction -related leverage

[] As widely reported, Fiat Chrysler Automobiles (FCA), EXOR's largest

investment today, is seeking merger partners in order to address its

operational, strategic and financial challenges. Mr. Elkann is FCA's Chairman

and EXOR is FCA's largest shareholder.

[] In the past, Fiat has disposed of several assets, including its insurer

arm Toro, to solve its liquidity problems. (1)[] EXOR will incur up to $4.75

billion in indebtedness to finance the acquisition of PartnerRe.

[] EXOR needs a further $2.05 billion to fund the acquisition of

PartnerRe's common shares.[] In order to maintain its credit rating, EXOR needs

to maintain a loan-to-value ratio below 20%.(2)[] If EXOR were to draw on the

full bridge facility to finance the transaction, its loan-to-value ratio would

increase to 27%. EXOR would need to raise an additional $2 billion to bring its

loan-to-value ratio under 20% [] and that was before EXOR's price was increased

to $137.50 per share further increasing its cash needs. (3)[] EXOR will need to

raise significant additional cash in order to delever and maintain its credit

rating and has not articulated a plan for how it "targets an LTV ratio below

20% by the end of 2016."(4)[] EXOR's ability to raise equity capital might be

constrained by the controlling family's desire to maintain control.

EXOR's ability and desire to close may be significantly impaired by

financial pressures from transaction leverage, ability to raise required

additional cash, and commitments to other investments.

(1) Source: Institutional Investor, "Fixing Fiat", available at http://www.

institutionalinvestor. com/Article. aspx?ArticleID=1026934 (May 1, 2003).

(2) Source: S&P, "Research Update: Italian Holding Company EXOR Outlook Revised

to Negative on Plan to Acquire PartnerRe; 'BBB+/A -2' Ratings Affirmed" (April

17, 2015); EXOR's Investor and Analyst Presentation (June 16, 2015).

(3) Source: April 22, 2015 discussions between EXOR's advisors and PartnerRe's

advisors.

(4) Source: EXOR's Investor and Analyst Presentation (June 16, 2015), Slide

33.

|

| Regulatory Risk |

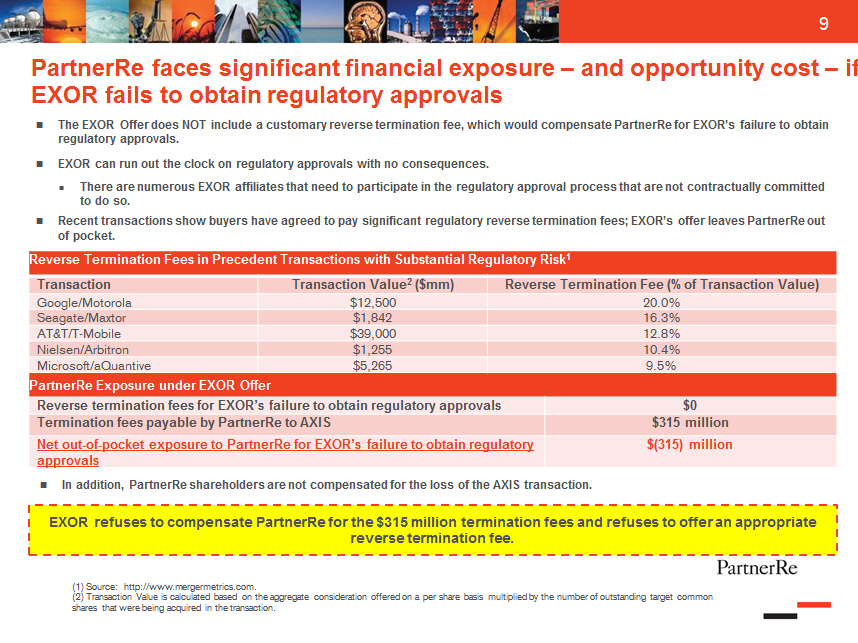

| PartnerRe faces significant financial exposure -- and opportunity cost -- if EXOR fails to obtain regulatory approvals [] The EXOR Offer does NOT include a customary reverse termination fee, which would compensate PartnerRe for EXOR's failure to obtain regulatory approvals. [] EXOR can run out the clock on regulatory approvals with no consequences. [] There are numerous EXOR affiliates that need to participate in the regulatory approval process that are not contractually committed to do so. [] Recent transactions show buyers have agreed to pay significant regulatory reverse termination fees; EXOR's offer leaves PartnerRe out of pocket. Reverse Termination Fees in Precedent Transactions with Substantial Regulatory Risk(1) Transaction Transaction Value(2) ($mm) Reverse Termination Fee (% of Transaction Value) Google/Motorola $12,500 20.0% Seagate/Maxtor $1,842 16.3% AT&T/T -Mobile $39,000 12.8% Nielsen/Arbitron $1,255 10.4% Microsoft/aQuantive $5,265 9.5% PartnerRe Exposure under EXOR Offer Reverse termination fees for EXOR's failure to obtain regulatory approvals $0 Termination fees payable by PartnerRe to AXIS $315 million Net out-of-pocket exposure to PartnerRe for EXOR's failure to obtain regulatory $(315) million approvals [] In addition, PartnerRe shareholders are not compensated for the loss of the AXIS transaction. EXOR refuses to compensate PartnerRe for the $315 million termination fees and refuses to offer an appropriate reverse termination fee. (1) Source: http://www. mergermetrics. com. (2) Transaction Value is calculated based on the aggregate consideration offered on a per share basis multiplied by the number of outstanding target common shares that were being acquired in the transaction. |

|

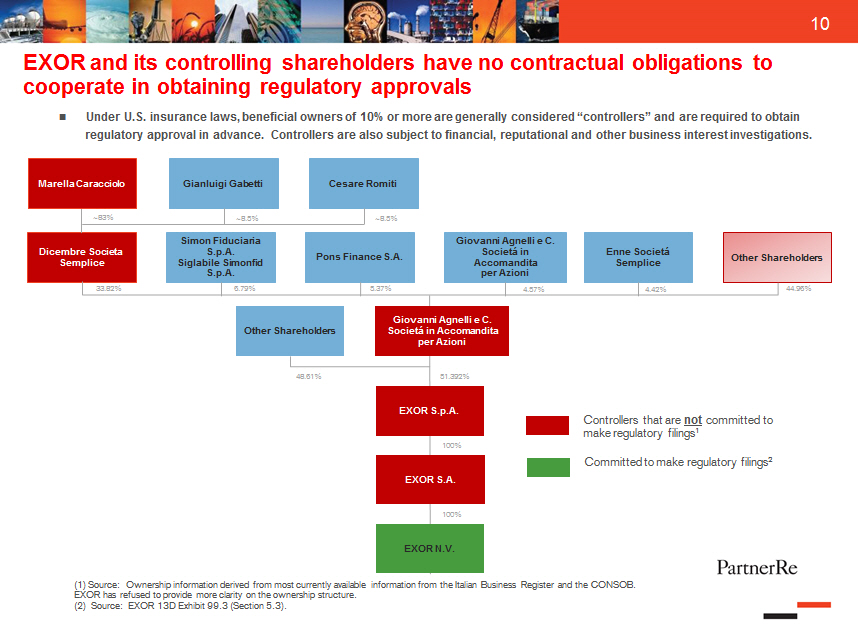

EXOR and its controlling shareholders have no contractual obligations to

cooperate in obtaining regulatory approvals

[] Under U.S. insurance laws, beneficial owners of 10% or more are generally

considered "controllers" and are required to obtain regulatory approval in

advance. Controllers are also subject to financial, reputational and other

business interest investigations.

Marella Caracciolo Gianluigi Gabetti Cesare Romiti

83% 8.5% 8.5%

-------------------- -------------------

Simon Fiduciaria Giovanni Agnelli e C.

Dicembre Societa S.p.A. Societ[] in Enne Societ[]

Pons Finance S.A. Other Shareholders

Semplice Siglabile Simonfid Accomandita Semplice

S.p.A. per Azioni

33.82% 6.79% 5.37% 4.57% 4.42% 44.96%

Giovanni Agnelli e C.

Other Shareholders Societ[] in Accomandita

per Azioni

------------------ -----------------------

48.61% 51.392%

EXOR S.p.A.

Controllers that are not committed to

make regulatory filings(1)

100%

Committed to make regulatory filings(2)

EXOR S.A.

100%

EXOR N.V.

(1) Source: Ownership information derived from most currently available

information from the Italian Business Register and the CONSOB. EXOR has refused

to provide more clarity on the ownership structure.

(2) Source: EXOR 13D Exhibit 99.3 (Section 5.3) .

|

| EXOR and its controlling shareholders are unknown to key insurance regulators [] Jurisdictions where regulatory approvals/filings are required but EXOR does NOT own, and has not owned in the last 10+ years, any insurance companies:[] US -- New York, Delaware, Montana and Ohio;[] Ireland;[] UK;[] Hong Kong;[] Singapore; and[] Bermuda. [] EXOR and its controlling shareholders will need to submit financial statements. [] Directors and officers and individuals who are controlling shareholders will also need to provide bios, undergo background checks and be fingerprinted. [] EXOR and its controlling shareholders will also be subject to financial, reputational and other business interest investigations. Because EXOR and its controlling shareholders are unknown to key regulators, the regulatory approval process may be protracted and complicated. Source: Public filings; confirmed by EXOR's advisors in private meetings with PartnerRe and conceded in EXOR's Investor and Analyst Presentation (June 16, 2015), Slide 42. |

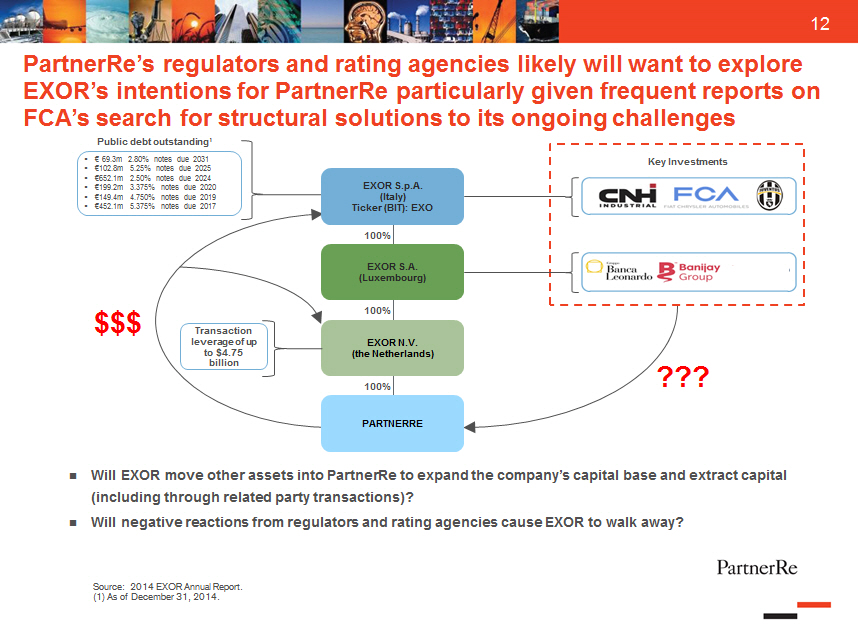

| PartnerRe's regulators and rating agencies likely will want to explore EXOR's intentions for PartnerRe particularly given frequent reports on FCA's search for structural solutions to its ongoing challenges Public debt outstanding 1 * [] 69.3m 2.80% notes due 2031* []102.8m 5.25% notes due 2025* []652.1m 2.50% notes due 2024* []199.2m 3.375% notes due 2020* []149.4m 4.750% notes due 2019* []452.1m 5.375% notes due 2017 EXOR S.p.A. (Italy) Ticker (BIT): EXO 100% EXOR S.A. (Luxembourg) 100% EXOR N.V. (the Netherlands) 100% PARTNERRE [] Will EXOR move other assets into PartnerRe to expand the company's capital base and extract capital (including through related party transactions)? [] Will negative reactions from regulators and rating agencies cause EXOR to walk away? Source: 2014 EXOR Annual Report. (1) As of December 31, 2014. |

| Increased U.S. regulation of acquisitions of insurers by financial buyers may delay the closing of EXOR Offer and adversely impact the ability of EXOR to complete the transaction [] U.S. regulators are focused on analyzing, exposing and reducing risks associated with financial and family-controlled acquirers with the assistance of outside legal and financial advisors. [] "Best practices" with respect to acquirers like EXOR will include increased capital and strengthened filing and disclosure requirements; and focus on insurance and non-insurance affiliate activities and their potential impact on PartnerRe's financial position and operations. [] Regulators may be more likely to impose: [] financial and operating conditions and restrictions post-acquisition, including requiring trust accounts to assure performance;[] restrictions on the structuring of deals and on the payment of dividends;[] increased regulation of affiliated reinsurance and service agreements; and [] enhanced or more frequent financial reporting. [] Post-acquisition related party transactions in general could be subject to greater regulatory scrutiny as a result of (i) stipulations or commitment letters required as a condition of regulatory approval of a PartnerRe -EXOR transaction and (ii) additional mandatory regulatory reviews of such affiliate transactions. Exor has not articulated any plan by which it, its controlling shareholders and its lenders will address these stringent regulatory approval requirements. Source: Proposed NAIC's Private Equity Issues Working Group Guidelines. |

|

EXOR has refused to give an absolute commitment to obtain regulatory approvals

[] Not all filing parties are obligated to file under EXOR's merger agreement.

1

[] "Reasonable best efforts" commitments by subsidiaries to obtain regulatory

approvals are meaningless as they have no control over the parent and its

controlling shareholders that need to obtain those approvals.

[] EXOR's financing sources have a veto over potentially critical concessions

required to obtain regulatory approvals. (2)[] No "hell or high water"

commitment.

[] EXOR and its controlling shareholders have consistently refused to agree to

do everything necessary to obtain regulatory approvals.

[] EXOR and its controlling shareholders present significant risks in their

ability to secure regulatory approvals.

[] "Hell or high water" was not required in AXIS transaction due to

significantly lower regulatory risk profile for two well-established insurance

companies.

[] No reverse termination fee if EXOR fails to obtain regulatory approvals.

[] $315 million out-of-pocket exposure to PartnerRe if EXOR does not obtain

regulatory approvals.

Significant risk to PartnerRe of deal failure and loss of the upside of

the AXIS transaction, in addition to out-of-pocket loss of $315 million.

PartnerRe not compensated by appropriate reverse termination fee.

(1) Source: EXOR 13D Exhibit 99.3 (Section 5.3); see also Slide 10.

(2) Source: EXOR 13D Exhibit 99.4 (Section 21.7(b)) .

|

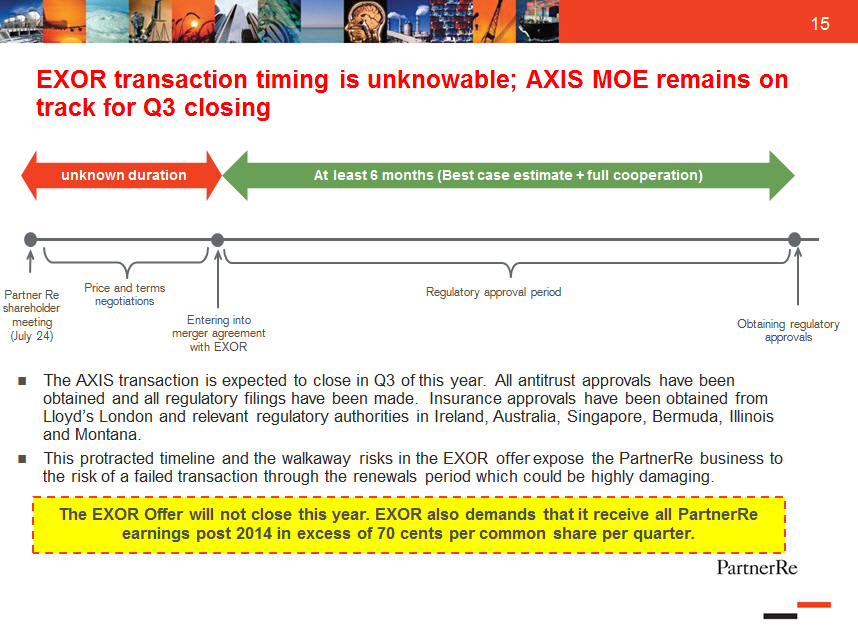

| EXOR transaction timing is unknowable; AXIS MOE remains on track for Q3 closing unknown duration At least 6 months (Best case estimate + full cooperation) Partner Re shareholder meeting (July 24) Price and terms negotiations Entering into merger agreement with EXOR Regulatory approval period Obtaining regulatory approvals [] The AXIS transaction is expected to close in Q3 of this year. All antitrust approvals have been obtained and all regulatory filings have been made. Insurance approvals have been obtained from Lloyd's London and relevant regulatory authorities in Ireland, Australia, Singapore, Bermuda, Illinois and Montana. [] This protracted timeline and the walkaway risks in the EXOR offer expose the PartnerRe business to the risk of a failed transaction through the renewals period which could be highly damaging. The EXOR Offer will not close this year. EXOR also demands that it receive all PartnerRe earnings post 2014 in excess of 70 cents per common share per quarter. |

| PartnerRe Board Process Protected Shareholders' Interests |

| The PartnerRe board sought to engage with EXOR to improve EXOR's price and terms [] After EXOR announced its original $130.00 per share proposal, PartnerRe's board authorized engagement with EXOR pursuant to a waiver from AXIS. [] Even though the price and terms of the EXOR proposal were unacceptable, the board authorized engagement in good faith to seek improvements to the EXOR proposal. [] EXOR maintained that it had no flexibility on price and that it would not negotiate the proposed terms unless PartnerRe would permit EXOR to start due diligence. [] Because the price of EXOR's proposal was unacceptable, PartnerRe did not proceed to due diligence. [] After EXOR announced its revised no-due-diligence $137.50 per share offer, the PartnerRe board obtained another waiver from AXIS to further engage with EXOR. [] The AXIS waiver allowed for ALL necessary engagement and due diligence to determine whether EXOR was prepared to improve its offer to become a transaction that was in the best interests of PartnerRe shareholders. [] In response to PartnerRe board's invitation to engage, EXOR repeatedly and publicly stated that it had no flexibility on the $137.50 per share price. [] EXOR has CONSISTENTLY REFUSED to negotiate with PartnerRe pursuant to the waiver from AXIS. EXOR has repeatedly rejected PartnerRe board's willingness to engage and negotiate despite a clear path to doing so. |

|

DISCLAIMER

Important Information for Investors and Shareholders

This communication does not constitute an offer to buy or sell or the

solicitation of an offer to buy or sell any securities or a solicitation of any

vote or approval. This communication relates to a proposed business combination

between PartnerRe Ltd. ("PartnerRe ") and AXIS Capital Holdings Limited

("AXIS"). In connection with this proposed business combination, PartnerRe and

AXIS have filed a registration statement on Form S-4 with the Securities and

Exchange Commission (the "SEC"), and a definitive joint proxy

statement/prospectus of PartnerRe and AXIS and other documents related to the

proposed transaction. This communication is not a substitute for any such

documents. The registration statement was declared effective by the SEC on June

1, 2015 and the definitive proxy statement/prospectus has been mailed to

shareholders of PartnerRe and AXIS. INVESTORS AND SECURITY HOLDERS OF PARTNERRE

AND AXIS ARE URGED TO READ THE REGISTRATION STATEMENT, JOINT PROXY

STATEMENT/PROSPECTUS AND OTHER DOCUMENTS THAT HAVE BEEN OR MAY BE FILED WITH

THE SEC CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY CONTAIN OR WILL CONTAIN

IMPORTANT INFORMATION. A definitive proxy statement has been mailed to

shareholders of PartnerRe and AXIS. Investors and security holders may obtain

free copies of these documents and other documents filed with the SEC by

PartnerRe and/or AXIS through the website maintained by the SEC at http://www.

sec.gov. Copies of the documents filed with the SEC by PartnerRe are available

free of charge on PartnerRe's internet website at http://www. partnerre. com or

by contacting PartnerRe's Investor Relations Director by email at

robin.sidders@partnerre. com or by phone at 1-441-294-5216. Copies of the

documents filed with the SEC by AXIS are available free of charge on AXIS'

internet website at http://www. axiscapital. com or by contacting AXIS'

Investor Relations Contact by email at linda.ventresca@axiscapital. com or by

phone at 1-441-405-2727.

|

| DISCLAIMER Forward Looking Statements Certain statements in this communication regarding the proposed transaction between PartnerRe and AXIS are "forward -looking" statements. The words "anticipate," "believe," "ensure," "expect," "if," "illustrative," "intend," "estimate," "probable," "project," "forecasts," "predict," "outlook," "aim," "will," "could," "should," "would," "potential," "may," "might," "anticipate," "likely" "plan," "positioned," "strategy," and similar expressions, and the negative thereof, are intended to identify forward -looking statements. These forward -looking statements, which are subject to risks, uncertainties and assumptions about PartnerRe and AXIS, may include projections of their respective future financial performance, their respective anticipated growth strategies and anticipated trends in their respective businesses. These statements are only predictions based on current expectations and projections about future events. There are important factors that could cause actual results, level of activity, performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied by the forward -looking statements, including the risk factors set forth in PartnerRe's and AXIS' most recent reports on Form 10-K, Form 10-Q and other documents on file with the SEC and the factors given below:[] the failure to obtain the approval of shareholders of PartnerRe or AXIS in connection with the proposed transaction;[] the failure to consummate or delay in consummating the proposed transaction for other reasons;[] the timing to consummate the proposed transaction;[] the risk that a condition to closing of the proposed transaction may not be satisfied;[] the risk that a regulatory approval that may be required for the proposed transaction is delayed, is not obtained, or is obtained subject to conditions that are not anticipated;[] AXIS' or PartnerRe's ability to achieve the synergies and value creation contemplated by the proposed transaction;[] the ability of either PartnerRe or AXIS to effectively integrate their businesses; and[] the diversion of management time on transaction -related issues. PartnerRe's forward -looking statements are based on assumptions that PartnerRe believes to be reasonable but that may not prove to be accurate. AXIS' forward -looking statements are based on assumptions that AXIS believes to be reasonable but that may not prove to be accurate. Neither PartnerRe nor AXIS can guarantee future results, level of activity, performance or achievements. Moreover, neither PartnerRe nor AXIS assumes responsibility for the accuracy and completeness of any of these forward -looking statements. PartnerRe and AXIS assume no obligation to update or revise any forward -looking statements as a result of new information, future events or otherwise, except as may be required by law. Readers are cautioned not to place undue reliance on these forward -looking statements that speak only as of the date hereof. |