A Global Leader in Specialty Insurance and Reinsurance March 18, 2015 PartnerRe and AXIS: Filed by AXIS Capital Holdings Limited Pursuant to Rule 425 of the Securities Act of 1933 and deemed filed pursuant to Rule 14a-12 of the Securities Exchange Act of 1934 Subject Company: PartnerRe Ltd. Commission File No.: 001-14536 |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 2 Agenda 1. Amalgamation Overview 2. Combined Company Strategy and Outlook 3. Capital Management 4. Investment Strategy 5. Conclusion |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 3 Agenda 1. Amalgamation Overview 2. Combined Company Strategy and Outlook 3. Capital Management 4. Investment Strategy 5. Conclusion |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 4 Amalgamation Overview 100% stock Merger of Equals structured as an amalgamation Shares in PartnerRe and AXIS to convert to new shares in the Amalgamated company at a fixed exchange ratio Preferred shares to remain outstanding as preferred shares of the Amalgamated company $11 billion pro forma market capitalization AXIS shareholders will receive 1 common share and PartnerRe shareholders will receive 2.18 common shares in the amalgamated company for each share they own PartnerRe will own approximately 51.6 percent of the amalgamated company AXIS will own approximately 48.4 percent of the amalgamated company Board of Directors to comprise 14 members, consisting of seven AXIS appointees and seven PartnerRe appointees Management teams to reflect balance, leveraging talent from both organizations Customary regulatory approvals PartnerRe and AXIS shareholder approvals Expected close in the second half of 2015 Structure Deal Value Pro Forma Ownership Corporate Governance of Combined Company Approvals |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 5 World-Class Management Team * Assuming the role of CFO no later than July, 2016 Jean-Paul L. Montupet, Non-executive Chairman Michael A. Butt, Chairman Emeritus Albert A. Benchimol, President & CEO Joseph Henry, CFO Bill Babcock, Deputy CFO & Lead Integration Officer* Emmanuel Clarke, CEO, Reinsurance Peter Wilson, CEO, Insurance Chris DiSipio, CEO, Life, Accident & Health John “Jay” Nichols, Head of Strategic Business Development & Capital Solutions Eric Gesick, Chief Risk & Actuarial Officer Rick Gieryn, General Counsel Noreen McMullen, Chief Human Resources Officer David Phillips, Chief Investment Officer Richard Strachan, Chief Operations Officer |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 6 Strategic Rationale » Sustainable, long-term commercial growth prospects through combined scale, efficiencies and expanded product capability » Meaningful capital synergies generating further flexibility to support growth and capital management initiatives Financial Strength » Combination of two high-quality and conservative balance sheets » No external equity or debt financing required in Merger of Equals » $14.7 billion of combined capital with low leverage ERM » Integrated Enterprise Risk Management practices in each organization to be strengthened by best practices of each company Limited Execution Risk of Integration » Shared philosophy of underwriting conservatism » Familiarity between the companies’ management teams » True merger of equals led by CEO with deep knowledge of both organizations. Other key executives have also held senior roles at both companies: AXIS Chief Risk and Actuarial Officer AXIS Chief Investment Officer Compelling Amalgamation Benefits |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 7 Both companies benefit from strong ratings, supporting customer confidence in their ability to market insurance and reinsurance products and compete with other insurance and reinsurance companies The insurance financial strength ratings assigned in respect of PartnerRe and AXIS by certain rating organizations are detailed in the table below: Strong Ratings AXIS Ratings PartnerRe Ratings Agency's Rating Definition Rating Review Status Standard & Poor's A+ A+ "Strong financial security characteristics" Both companies have been affirmed with stable outlook A.M. Best A+ A+ "Superior ability to meet ongoing insurance obligations" Under review with negative implications for both companies Moody's Investor Services A2 A1 "Insurance companies offer good financial strength" AXIS rating under review with possible upgrade. PartnerRe rating has been affirmed with stable outlook Fitch A+ A+ "Strong capacity to meet policyholder and contract obligations" AXIS rating placed on Rating Watch Positive and PartnerRe rating placed on Rating Watch Negative |

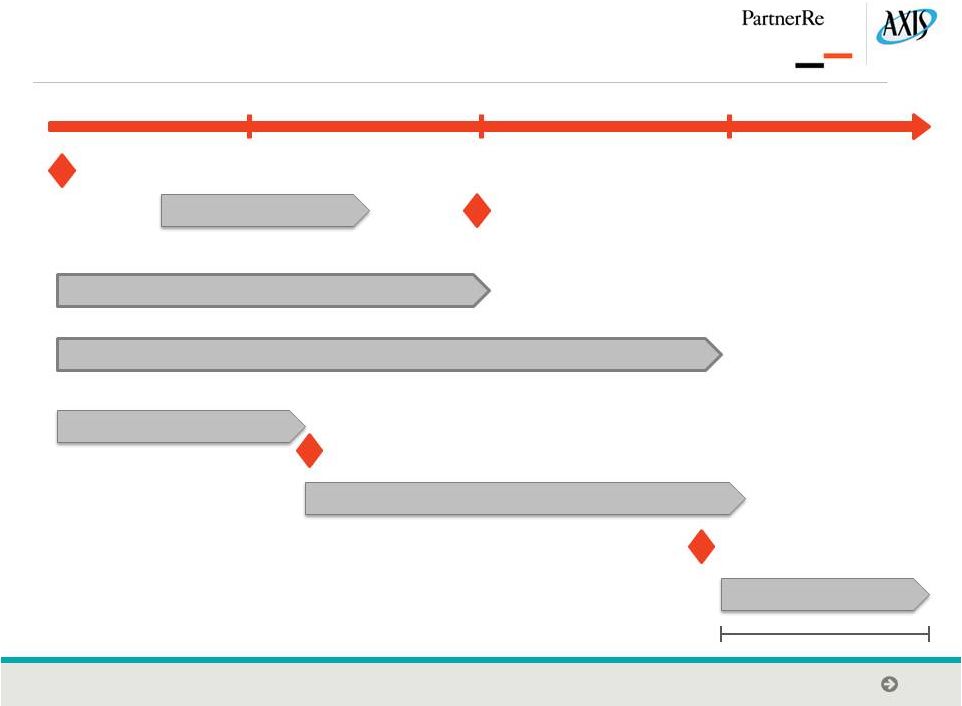

8 PartnerRe/AXIS Capital High-Level Amalgamation Process Estimated Transaction Close 18+ months Q1 Q2 Q3 Q4 Finalize Integration Structure Announcement Shareholder vote S4 filing and SEC review Antitrust approvals Regulatory approvals Integration Readiness Integration Planning Integration Execution © 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 9 Agenda 1. Amalgamation Overview 2. Combined Company Strategy and Outlook 3. Capital Management 4. Investment Strategy 5. Conclusion |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 10 A Global Leader in Specialty Insurance and Reinsurance Combination will be a (re)insurance powerhouse with approximately $13bn combined shareholders equity (1) » Brings together two strong, world-class, successful companies building on existing strengths » Transaction creates a top 5 global reinsurance franchise with leading position in the broker channel » Primary specialty platform with $2.5bn+ in premiums across a diversified array of product lines » Top 10 Life, Accident & Health reinsurer Value creation through combined franchise strengths including significant capital efficiencies and meaningful synergies » Expanded ability to invest in growing specialty franchises » Enhanced ability to partner with other capital providers to deliver value to all stakeholders » Over $200 million in identifiable, actionable and concrete expense savings » Transaction expected to be meaningfully accretive to earnings and return on equity Clear common vision accelerates strategies for both companies » Growth accompanied by excellence in risk management » Best-in-class talent across all aspects of business » Compatible cultures facilitate integration (1) Financial data as of 12/31/14 |

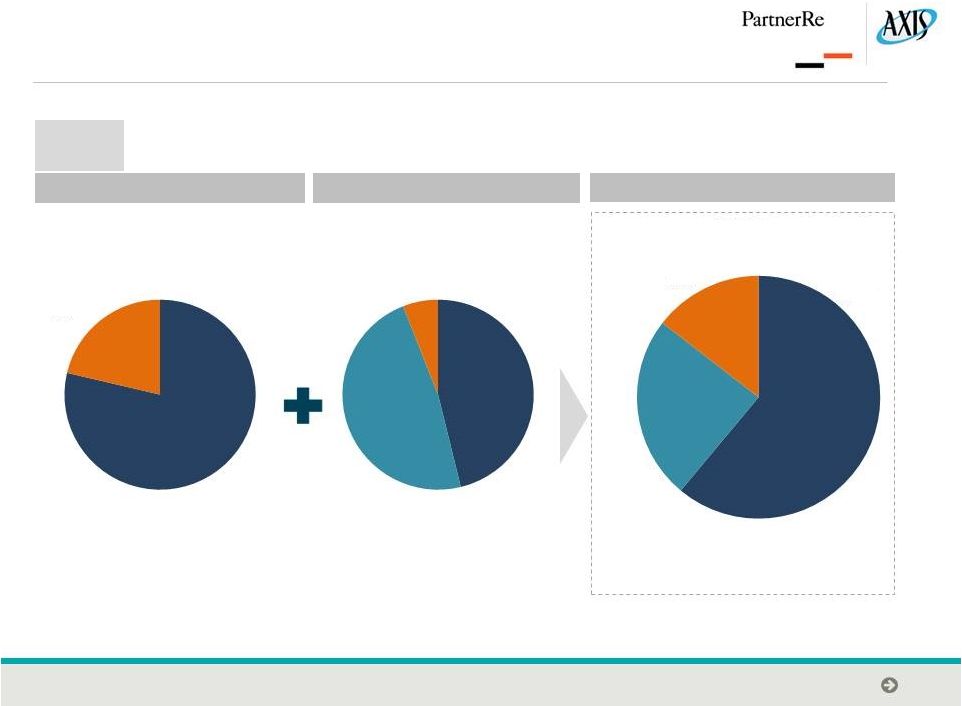

Strong Position in Three Attractive Businesses PartnerRe Pro Forma Combined AXIS 2014 GPW BUSINESS OVERVIEW $5.9B $4.7B $10.6B P&C Reinsurance 46% Insurance 48% A&H 6% P&C Reinsurance 61% Insurance 24% Life, A&H 15% Non-Life Reinsurance 79% Life and Health 21% © 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 11 |

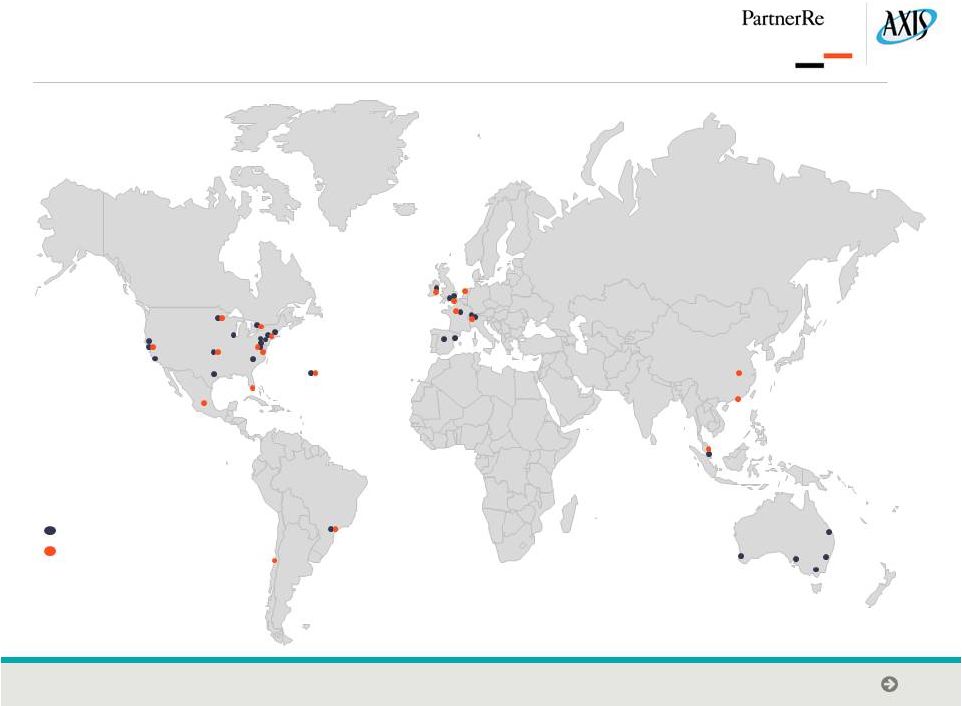

Global Reach with Opportunities for Consolidating Locations AXIS Office Locations PartnerRe Office Locations © 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 12 |

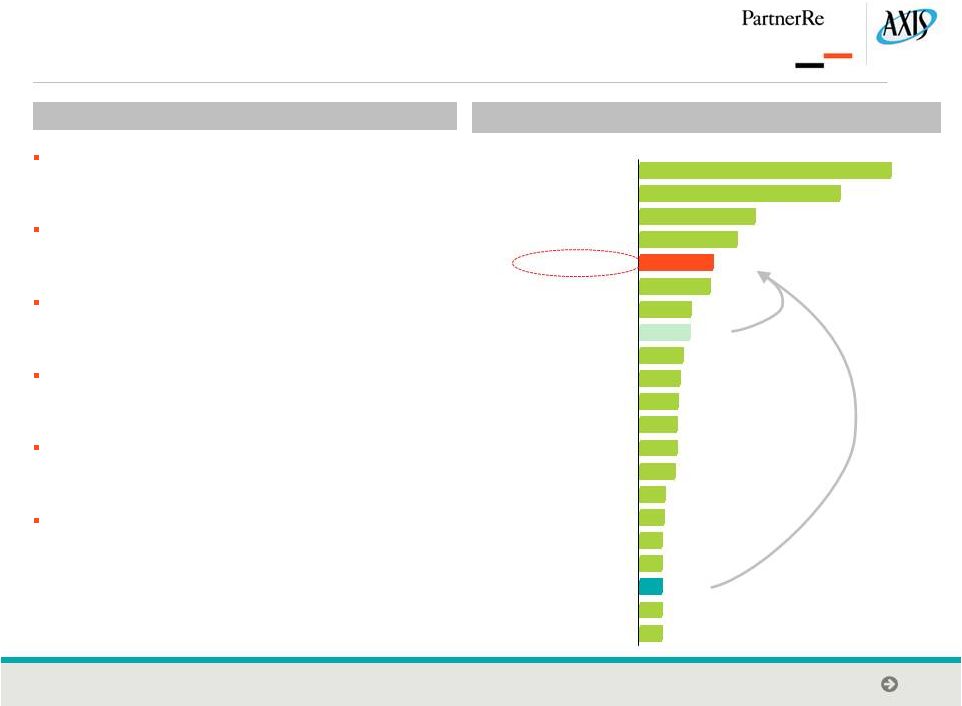

Transformative Combination Creating a Leading Global Reinsurance Platform Top 5 global reinsurer with approximately $7 billion in GPW Leading position among broker-based reinsurers Strong positions in specialty reinsurance lines Combination of two additive platforms with highly regarded UW and service capabilities Limited overlap in current portfolios suggesting manageable attrition Ability to leverage third-party capital to deliver expanded client solutions Note: Chart excludes life and health reinsurance GPW if publicly disclosed. Excludes Lloyd’s. (1) Rankings are by 2013 GPW. (2) Berkshire Hathaway Reinsurance includes General Re. Corp. (3) GPW not disclosed. Indicated values are on a NPW basis. Market position Top Global P&C Reinsurers by P&C Reinsurance GPW (1) ($ in billions) (2) (3) © 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 13 $2.1 $2.1 $2.1 $2.1 $2.1 $2.3 $2.4 $3.3 $3.4 $3.4 $3.5 $3.7 $4.0 $4.6 $4.7 $6.4 $6.7 $8.8 $10.4 $18.0 $22.6 Generali RenRe / Platinum AXIS Mitsui Sumitomo Fairfax Financial Sompo Japan General Insurance Co. of India Mapfre Allianz Alleghany Korean Re XL / Catlin Everest Re PartnerRe China Re SCOR PartnerRe + AXIS Berkshire Re Hannover Re Swiss Re Munich Re |

Diversified Global Specialty Insurance Business Balanced portfolio mix between segments Almost no business overlap in existing books* Optionality to further accelerate growth in desirable segments Growing visibility among clients / distribution partners / talent PartnerRe’s D&F business complementary to insurance Pro Forma Combined Insurance Breakdown 2014 GPW By Line of Business Total Insurance GPW: $2.6B * With exception of Energy although not material to overall portfolio © 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 14 Professional Lines 33% Property 25% Liability 14% PartnerRe's D&F, Wholesale & Other Insurance 14% Marine 9% Aviation 2% Credit and Political Risk 2% Terrorism 1% |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 15 Strategy Remains Appropriate Leadership in Life and A&H with High Growth Potential A leading Life, Accident & Health franchise with limited product overlap with truly global reach $1.5 billion in combined premium Top 10 Life & Health reinsurer (7th or 8th) #1 health reinsurer in US One of industry’s broadest product portfolios Immediate and complementary global footprint Minimal overlap in customers, distribution and risk tolerance Each company fills the gaps of the other – highly complementary organizations Accelerates achievement of original strategies Customer-centric service model Broad set of products and services Diverse distribution Global reach/local service Insurance and reinsurance capabilities (hybrid model) Entrepreneurship Scale provides operational efficiency |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 16 Global Reinsurance Success in a very competitive market Key factors in Reinsurance: Broad access to business » Preferred market, positioned to see all business – geographies and products » Ability to generate new business – providing client solutions Underwriting outperformance » Ability to outperform market by disciplined underwriting (price), cycle management execution, large mistakes avoidance, portfolio optimization and macro positions Capital efficiency / flexibility » Ability to reduce cost of capital to sell competitive solutions to our clients and optimize ROE » Ability to leverage all sources of capital to respond to opportunities, optimize gross to net. Cost efficiency » Ability to operate with lean resources in order to remain competitive A PartnerRe/ AXIS combination enhances our ability to succeed in the current environment |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 17 Merger strengthens relationships with brokers & cedants Creation of a credible and sizeable broker-committed underwriter aligns us with reinsurance brokers in competition with top-four reinsurers » Both organizations have a commitment to a broker based distribution » Combined company will be leading broker-based reinsurer by GPW » Putting together sizeable capacity is a challenge in the highly fragmented state of broker market reinsurers. A PartnerRe/ AXIS combination will ensure: Larger capital base to take sizeable participations for its own account A larger available selection of 3 rd party capital providers The underwriting reputation that will allow brokers to easily fill in following shares Cedants & reinsurance buyer trends include 1) panel consolidation and 2) expectation of value added service from reinsurance partners » In both cases size, financial strength and expertise clearly matter » Combined company provides similar culture, brand values as well as continuity and longevity in the market |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 18 Agenda 1. Amalgamation Overview 2. Combined Company Strategy and Outlook 3. Capital Management 4. Investment Strategy 5. Conclusion |

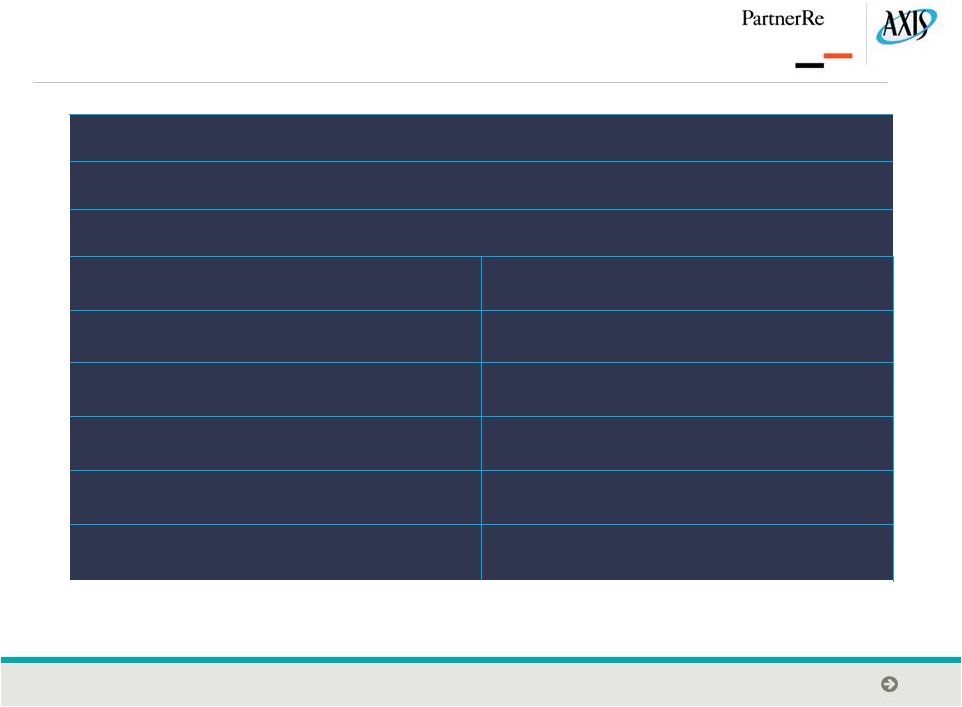

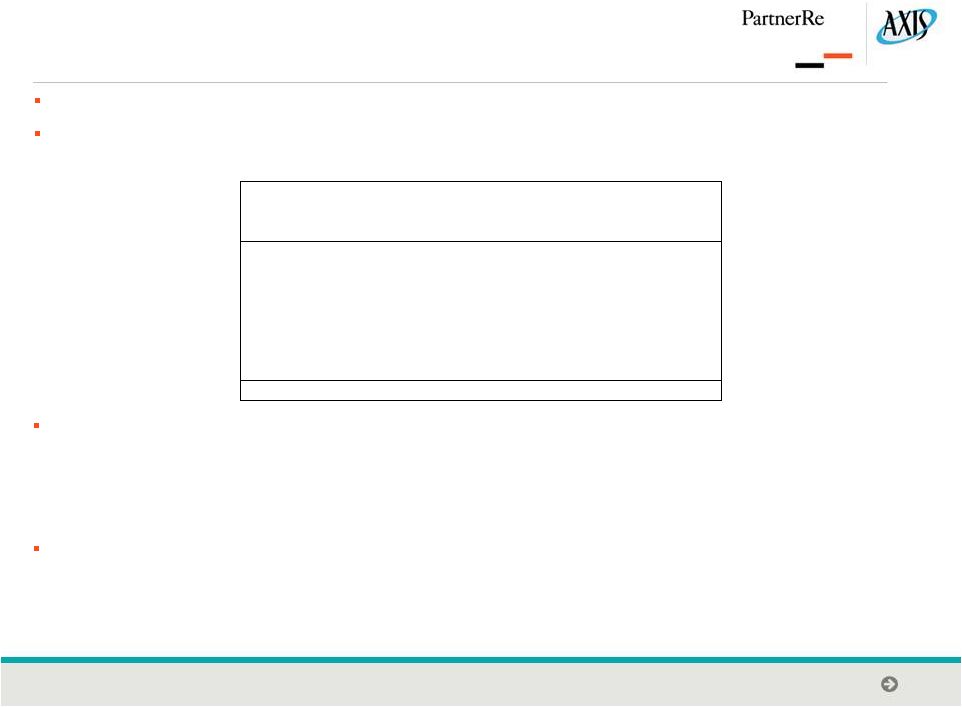

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 19 Capital Management Capital Security Maturity PRE AXS Combined % of 2014 Capital Senior Debt 2018 250 $ - $ 250 $ 1.7% Senior Debt 2019 - 250 250 1.7% Senior Debt 2020 500 500 1,000 6.8% Senior Debt 2045 - 250 250 1.7% Capital Efficient Notes 2066 63 - 63 0.4% Cumulative Preferred Perpetual 854 628 1,482 10.0% Common Equity* 6,251 5,252 11,503 77.7% Total 7,917 $ 6,880 $ 14,797 $ 100.0% 12/31/2014 * Includes non-controlling interests Management is committed to retaining robust capital in excess of our three principle thresholds: » Regulatory capital requirements » Internal economic capital model » Rating agency targets Exceptional capital position provides strategic flexibility to fund growth and return capital to shareholders » Current capital positions strong at both companies » Share repurchases for both companies have been suspended until transaction close » Capital synergies created through combination enhance capital margins High-quality, permanent capital structure with no immediate refinancing risk. No maturing debt until 2018 Low financial leverage for combined company: Debt / total capital of 12.3% Debt + preferred leverage of 22.3% |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 20 Agenda 1. Amalgamation Overview 2. Combined Company Strategy and Outlook 3. Capital Management 4. Investment Strategy 5. Conclusion |

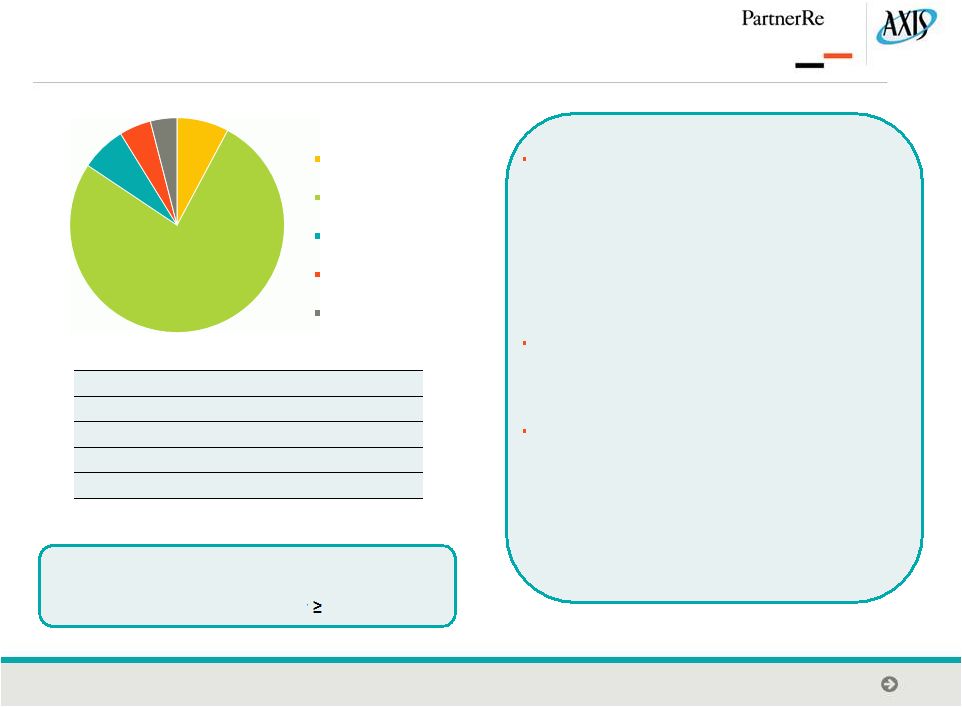

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 21 Conservative, Diversified Investment Portfolio Strong risk cultures and conservative approach to investments reflect primary objective of the investment function as a support to the companies’ core (re)insurance activities » Both companies invest substantially more than the value of their (re)insurance reserves in high quality, standard Fixed Income instruments, making sure to match currency and duration exposures of their liabilities » The combined entity is likely to maintain a credit quality of A+ or above and will continue to have its allowable duration range centered at the duration of its liabilities Both companies emphasize internal management to construct and shape the overall portfolio. Activities such as asset allocation, benchmark construction, risk and compliance monitoring and performance attribution / monitoring are performed internally The majority of security selection in PartnerRe is done internally. AXIS Capital uses third party managers for security selection in all of its strategies » The combined entity will follow a similar approach. The enhanced scale will allow the combined entity to take greater advantage of the control benefits of internal management and to supplement its capabilities (and gain attendant diversification) through the use of specialist external managers Total: $31.6 billion Duration: ~3.3 years Average credit quality A+ Investment Grade Fixed Income $24,202 Cash & ST Investments $2,467 Non-Investment Grade Fixed Income $2,164 Equities $1,514 Other $1,266 $ in millions 12/31/2014 8% 77% 7% 5% 4% Cash & ST Investments Investment Grade Fixed Income Non-Investment Grade Fixed Income Equities Other |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 22 Agenda 1. Amalgamation Overview 2. Combined Company Strategy and Outlook 3. Capital Management 4. Investment Strategy 5. Conclusion |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 23 Strategic Rationale » Sustainable, long-term commercial growth prospects through combined scale, efficiencies and expanded product capability » Meaningful capital synergies generating further flexibility to support growth and capital management initiatives Financial Strength » Combination of two high-quality and conservative balance sheets » No external equity or debt financing required in Merger of Equals » $14.7 billion of combined capital with low leverage Enterprise Risk Management » Integrated ERM practices in each organization to be strengthened by best practices of each company Limited Execution Risk of Integration » Shared philosophy of underwriting conservatism » Familiarity between the companies’ management teams » True merger of equals led by CEO with deep knowledge of both organizations. Other key executives have also held senior roles at both companies: AXIS Chief Risk and Actuarial Officer AXIS Chief Investment Officer Strength of Ratings » The clients of AXIS and PartnerRe value the high quality ratings of the stand-alone companies » The combined entity will be in an improved position to compete and management expects this increased strength to support positive rating developments over the coming years Compelling Amalgamation Benefits |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 24 connection with this proposed business combination, PartnerRe and/or AXIS may file one or more proxy statements, registration statements, proxy statement/prospectus or other documents with the Securities and Exchange Commission (the “SEC”). This communication is not a substitute for any proxy statement, registration statement, proxy statement/prospectus or other document PartnerRe and/or AXIS may file with the SEC in connection with the proposed transaction. INVESTORS AND SECURITY HOLDERS OF PARTNERRE AND AXIS ARE URGED TO READ THE PROXY STATEMENT(S), REGISTRATION STATEMENT(S), PROXY STATEMENT/PROSPECTUS AND OTHER DOCUMENTS THAT MAY BE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Any definitive proxy statement(s) (if and when available) will be mailed to stockholders of PartnerRe and/or AXIS, as applicable. Investors and security holders will be able to obtain free copies of these documents (if and when available) and other documents filed with the SEC by PartnerRe and/or AXIS through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by PartnerRe will be available free of charge on PartnerRe’s internet website at http://www.partnerre.com or by contacting PartnerRe’s Investor Relations Director by email at robin.sidders@partnerre.com or by phone at 1-441-294-5216. Copies of the documents filed with the SEC by AXIS will be available free of charge on AXIS’ internet website at http://www.axiscapital.com or by contacting AXIS’ Investor Relations Contact by email at linda.ventresca@axiscapital.com or by phone at 1-441-405-2727. Important Information For Investors And Stockholders This communication does not constitute an offer to buy or sell or the solicitation of an offer to buy or sell any securities or a solicitation of any vote or approval. This communication relates to a proposed business combination between PartnerRe Ltd. (“PartnerRe”) and AXIS Capital Holdings Limited (“AXIS”). In |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 25 Participants in Solicitation PartnerRe, AXIS, their respective directors and certain of their respective executive officers may be considered participants in the solicitation of proxies in connection with the proposed transaction. Information about the directors and executive officers of PartnerRe is set forth in its Annual Report on Form 10-K for the year ended December 31, 2014, which was filed with the SEC on February 26, 2015, its proxy statement for its 2014 annual meeting of stockholders, which was filed with the SEC on April 1, 2014, its Quarterly Report on Form 10-Q for the quarter ended September 30, 2014, which was filed with the SEC on October 31, 2014 and its Current Reports on Form 8-K, which were filed with the SEC on March 27, 2014, May 16, 2014 and January 29, 2015. Information about the directors and executive officers of AXIS is set forth in its Annual Report on Form 10-K for the year ended December 31, 2014, which was filed with the SEC on February 23, 2015, its proxy statement for its 2014 annual meeting of stockholders, which was filed with the SEC on March 28, 2014, its Quarterly Report on Form 10-Q for the quarter ended September 30, 2014, which was filed with the SEC on October 31, 2014 and its Current Reports on Form 8-K, which were filed with the SEC on March 11, 2015, January 29, 2015, August 7, 2014, June 26, 2014, March 27, 2014 and February 26, 2014. These documents can be obtained free of charge from the sources indicated above. Additional information regarding the participants in the proxy solicitations and a description of their direct and indirect interests, by security holdings or otherwise, will be contained in the proxy statement/prospectus and other relevant materials to be filed with the SEC when they become available. |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 26 Forward Looking Statements Certain statements in this communication regarding the proposed transaction between PartnerRe and AXIS are “forward-looking” statements. The words “anticipate,” “believe,” “ensure,” “expect,” “if,” “intend,” “estimate,” “probable,” “project,” “forecasts,” “predict,” “outlook,” “aim,” “will,” “could,” “should,” “would,” “potential,” “may,” “might,” “anticipate,” “likely,” “plan,” “positioned,” “strategy,” and similar expressions, and the negative thereof, are intended to identify forward-looking statements. These forward-looking statements, which are subject to risks, uncertainties and assumptions about PartnerRe and AXIS, may include projections of their respective future financial performance, their respective anticipated growth strategies and anticipated trends in their respective businesses. These statements are only predictions based on current expectations and projections about future events. There are important factors that could cause actual results, level of activity, performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied by the forward-looking statements, including the risk factors set forth in PartnerRe’s and AXIS’ most recent reports on Form 10-K, Form 10-Q and other documents on file with the SEC and the factors given below: • the failure to obtain the approval of shareholders of PartnerRe or AXIS in connection with the proposed transaction; • the failure to consummate or delay in consummating the proposed transaction for other reasons; • the timing to consummate the proposed transaction; • the risk that a condition to closing of the proposed transaction may not be satisfied; |

© 2015. PartnerRe and AXIS Capital. All rights reserved. Proprietary and confidential. 27 PartnerRe’s forward-looking statements are based on assumptions that PartnerRe believes to be reasonable but that may not prove to be accurate. AXIS’ forward-looking statements are based on assumptions that AXIS believes to be reasonable but that may not prove to be accurate. Neither PartnerRe nor AXIS can guarantee future results, level of activity, performance or achievements. Moreover, neither PartnerRe nor Forward Looking Statements • the risk that a regulatory approval that may be required for the proposed transaction is delayed, is not obtained, or is obtained subject to conditions that are not anticipated; • AXIS’ or PartnerRe’s ability to achieve the synergies and value creation contemplated by the proposed transaction; • the ability of either PartnerRe or AXIS to effectively integrate their businesses; and • the diversion of management time on transaction-related issues. AXIS assumes responsibility for the accuracy and completeness of any of these forward-looking statements. PartnerRe and AXIS assume no obligation to update or revise any forward-looking statements as a result of new information, future events or otherwise, except as may be required by law. Readers are cautioned not to place undue reliance on these forward-looking statements that speak only as of the date hereof. |