UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21295

JPMorgan Trust I

(Exact name of registrant as specified in charter)

270 Park Avenue

New York, NY 10017

(Address of principal executive offices) (Zip code)

Frank J. Nasta

270 Park Avenue

New York, NY 10017

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 480-4111

Date of fiscal year end: December 31

Date of reporting period: January 1, 2013 through December 31, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

Annual Report

J.P. Morgan Specialty Funds

December 31, 2013

Security Capital U.S. Core Real Estate Securities Fund

CONTENTS

Investments in a Fund are not bank deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the FDIC, the Federal Reserve Board or any other government agency. You could lose money if you sell when the Fund’s share price is lower than when you invested.

Past performance is no guarantee of future performance. The general market views expressed in this report are opinions based on market and other conditions through the end of the reporting period and are subject to change without notice. These views are not intended to predict the future performance of a Fund or the securities markets. References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Such views are not meant as investment advice and may not be relied on as an indication of trading intent on behalf of any Fund.

Prospective investors should refer to the Fund’s prospectus for a discussion of the Fund’s investment objectives, strategies and risks. Call J.P. Morgan Funds Service Center at 1-800-480-4111 for a prospectus containing more complete information about the Fund, including management fees and other expenses. Please read it carefully before investing.

CEO’S LETTER

JANUARY 23, 2014 (Unaudited)

Dear Shareholder,

Equities markets in developed economies performed strongly in the face of periodic spikes in volatility throughout the twelve months ended December 31, 2013. Healthy corporate earnings and incremental but steady improvements in a range of economic indicators provided a positive backdrop for investors seeking returns in the low interest rate environment. While political discord in Washington injected volatility into the market, a bipartisan budget agreement at the end of the year relieved much of the political uncertainty created by partisan brinkmanship over the so-called fiscal cliff and the partial shutdown of the federal government in October. In the first half of the year, the U.S. Federal Reserve (“Fed”) announced its intention to taper off its $85 billion in monthly asset purchases and the statement weakened investor sentiment and set off widespread speculation about the timing and magnitude of such a move. The Fed followed through in December, deciding to reduce its monthly purchases by $10 billion. The news, along with robust gains in jobs, housing and consumer sentiment, drove U.S. equities to new highs. The S&P 500 stock index hit seven closing highs in the final month of the reporting period, finishing 2013 with its best performance since 1997.

| | |

| | |

Overseas, the European Central Bank reaffirmed its commitment to accommodative monetary policy and to the euro itself. In the second quarter of the year, the European Union (EU) returned to positive growth and at the end of the year, Ireland became the first nation to exit from its European Union bailout program. The Fed’s decision to curb its asset purchases also sent equities higher in Europe, as investors viewed the move as a sign of further economic stability. In Japan, equity markets rebounded to their best year since 1988, benefitting from Prime Minister Shinzo Abe’s efforts to revive the economy. Low returns on bonds and short-term debt instruments also drove investors into stocks.

Emerging market equities were weaker overall. As of December 31, 2013, the MSCI Emerging Markets Index returned -2.3% for the year. China’s economy showed signs of slower growth during the year and the Fed’s decision to taper its asset purchase program set off speculation that the maturation of the emerging markets credit cycle would push yield-seeking investors to rotate into developed markets.

Taper Talk Pressures Bonds

Fixed income markets generally remained weak during the year, as central bankers across the globe held interest rates at

historic lows. However, benchmark bond yields rose on an annual basis for the first time since 2009. During the year, the Fed’s talk of tapering off its Quantitative Easing (QE) program hurt fixed income markets. U.S. Treasury security yields continued to be low from a historical perspective, but ended the period higher. The yield for 10-year U.S. Treasury securities ended December 31, 2013 at 3.04%, while the yields for 2- and 30-year U.S. Treasury securities finished the reporting period at 0.38% and 3.96%, respectively. High-yield debt returned 7.4% for the year, as measured by the Barclays US High Yield Corporate Index, while other U.S. debt securities and emerging market debt both had negative returns.

While global economic growth accelerated during the year, the U.S. recovery in particular showed stronger fundamentals and the Fed’s decision to taper its QE program was a response to the improved picture. Europe emerged from its lengthy recession and the worst of the fiscal crises seem to be behind it, though unemployment remains strikingly high in many EU nations. Japan made progress toward ending persistent deflation, but Tokyo’s monetary and fiscal stimulus has sharply weakened the yen, putting other Asian exporting nations — notably China and South Korea — at a competitive disadvantage. Emerging market economies may face further headwinds as foreign investment shrinks and economic growth moderates from recent strength. Moreover, political instability — already apparent in Thailand and Turkey — may surface in other emerging market nations as governments struggle to deliver improved living standards and respond to demands for political reforms.

The Long-Term Lens

We welcome the Fed’s move to curb its QE program as a sign that the U.S. economy’s need for artificial stimulus is waning. While a repeat of the equity performance we experienced in 2013 may be a tall order, we believe stocks in the U.S. and Europe may continue to show gains. In the fixed-income market, persistent weakness has led to attractive valuations in some sectors. The past year’s market swings and intermittent volatility underlined the importance of maintaining a long-term view of your investment portfolio and the benefits derived from diversified holdings.

On behalf of everyone at J.P. Morgan Asset Management, thank you for your continued support. We look forward to managing your investment needs for years to come. Should you have any questions, please visit www.jpmorganfunds.com or contact the J.P. Morgan Funds Service Center at 1-800-480-4111.

Sincerely yours,

George C.W. Gatch

CEO, Global Funds Management

J.P. Morgan Asset Management

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 1 | |

J.P. Morgan Specialty Funds

MARKET OVERVIEW

TWELVE MONTHS ENDED DECEMBER 31, 2013

Returns for U.S. real estate investment trusts (REITs) underperformed the broader equity market in 2013 for the first time in five years, with the Wilshire U.S. Real Estate Securities Index posting a gain of 2.15%, compared with a 32.39% return for the Standard & Poor’s 500 Index. While the REIT sector overall had a strong start to the year, the U.S. Federal Reserve Board’s announcement in late-May that it might begin tapering its monthly asset purchases later in the year left investors worried about the impact on financial markets.

Despite the volatility in REIT valuations, the fundamental and financial positioning of publicly traded real estate companies remained strongly positive, the Fund’s manager believe. Low borrowing costs, accommodating debt markets, low levels of new construction and stable-to-improving rent/occupancy levels represent a potent force behind long-term real estate values, in the opinion of the Fund’s managers.

By major property type, lodging/resorts and industrial/office and self-storage companies were the relative outperformers, while the weakest sectors were residential, health care and retail were relative underperformers.

| | | | | | |

| | | |

| 2 | | | | J.P. MORGAN SPECIALTY FUNDS | | DECEMBER 31, 2013 |

Security Capital U.S. Core Real Estate Securities Fund

FUND COMMENTARY

TWELVE MONTHS ENDED DECEMBER 31, 2013 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Select Class Shares)* | | | 0.69% | |

| Wilshire U.S. Real Estate Securities Index | | | 2.15% | |

| Barclays REIT Bond Index | | | –0.05% | |

| Security Capital U.S. Core Real Estate Securities Composite Benchmark | | | 0.95% | |

| |

| Net Assets as of 12/31/2013 (In Thousands) | | $ | 56,386 | |

INVESTMENT OBJECTIVE**

The Security Capital U.S. Core Real Estate Securities Fund (the “Fund”) seeks a risk-adjusted total return over the long term by investing primarily in real estate securities.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund (Select Class Shares) posted a modestly positive absolute return, outperforming the Barclays REIT Bond Index, yet underperforming the Wilshire U.S. Real Estate Securities Index (“WILRESI”) and the Security Capital U.S. Core Real Estate Securities Composite Benchmark for the year. The Fund invests in equity and fixed income securities and, therefore, its performance is compared to multiple benchmarks, including broad-based equity and fixed income benchmarks as well as a blended composite benchmark.

The majority of the return of the Fund for the reporting period was sourced from its common equity holdings, which represented 59% of the portfolio at year end. Individual common stock holdings that contributed to performance relative to the WILRESI included: Host Hotels and Resorts Inc., an owner-operator of luxury properties mainly in North America and Europe; Healthcare Realty Trust Inc., which is primarily focused on outpatient facilities; and RLJ Lodging Trust, which holds a portfolio of full-service hotels.

Individual common stock holdings that detracted from performance relative to the WILRESI included: Equity Residential, an

owner-operator of apartment properties; Mack-Cali Realty Corp., a commercial property owner and manager; and Avalonbay Communities Inc., which owns and operates multifamily communities.

Among the fixed income investments, the Fund’s bond investments outperformed the Barclays REIT Bond Index for the reporting period, benefiting from the profitable sale of a targeted convertible debt investment. The Fund continues to position its debt holdings with a more defensive shorter-maturity stance, with average duration of 2.0 years in the portfolio, compared with the Barclays REIT Bond Index’s average duration of 6.9 years. The Fund’s targeted preferred equity investments garnered a positive absolute return for the reporting period, outperforming the Wells Fargo Hybrid and Preferred Securities REIT Index (“WHPSR”), which was burdened by weaker performance from highly-rated, low coupon preferreds issued over the last two years. The Fund remained overweight to preferred securities relative to the composite blended benchmark.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilized a bottom-up process to inform both security selection and security type (common equity, preferred equity or debt). They relied on proprietary cash flow models, extensive field work and internal real estate market research to target what they believed to be attractive long-term investment opportunities, emphasizing quality real estate portfolios, flexible balance sheets and transparent business models.

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 3 | |

Security Capital U.S. Core Real Estate Securities Fund

FUND COMMENTARY

TWELVE MONTHS ENDED DECEMBER 31, 2013 (Unaudited) (continued)

| | | | | | | | |

| TOP TEN HOLDINGS OF THE PORTFOLIO*** | |

| | 1. | | | Simon Property Group, Inc. | | | 6.1 | % |

| | 2. | | | Prologis, Inc. | | | 3.9 | |

| | 3. | | | Equity Residential | | | 3.7 | |

| | 4. | | | Health Care REIT, Inc., 5.875%, 05/15/15 | | | 3.6 | |

| | 5. | | | AvalonBay Communities, Inc. | | | 2.8 | |

| | 6. | | | Public Storage | | | 2.6 | |

| | 7. | | | Vornado Realty Trust | | | 2.6 | |

| | 8. | | | HCP, Inc. | | | 2.5 | |

| | 9. | | | Host Hotels & Resorts, Inc. | | | 2.5 | |

| | 10. | | | Health Care REIT, Inc. | | | 2.4 | |

| | | | |

PORTFOLIO COMPOSITION BY SECURITY TYPE*** | |

| Common Stocks | | | 59.4 | % |

| Preferred Stocks | | | 21.6 | |

| Corporate Bonds | | | 16.4 | |

| Short-Term Investment | | | 2.6 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2013. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

GEOGRAPHIC DIVERSIFICATION | |

| | | Security Capital U.S. Core Real Estate Securities Fund (a) | | | NCREIF (b) | |

East | | | 34.6 | % | | | 34.3 | % |

Northeast | | | 21.9 | | | | 20.5 | % |

Mideast | | | 12.7 | | | | 13.8 | % |

West | | | 29.0 | % | | | 34.9 | % |

Pacific | | | 23.4 | | | | 29.2 | % |

Mountain | | | 5.6 | | | | 5.7 | % |

South | | | 19.6 | % | | | 21.3 | % |

Southeast | | | 11.7 | | | | 10.4 | % |

Southwest | | | 7.9 | | | | 10.9 | % |

Midwest | | | 13.0 | % | | | 9.5 | % |

East North Central | | | 10.1 | | | | 7.7 | % |

West North Central | | | 2.9 | | | | 1.8 | % |

Non-U.S. | | | 3.8 | % | | | 0.0 | % |

| (a) | | Percentages indicated are based on total investments as of December 31, 2013. The Fund’s portfolio composition is subject to change. |

| (b) | | Reflects the industry average of institutions belonging to the National Council of Real Estate Investment Fiduciaries. |

| | | | | | |

| | | |

| 4 | | | | J.P. MORGAN SPECIALTY FUNDS | | DECEMBER 31, 2013 |

| | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2013 | |

| | | |

| | | INCEPTION DATE

OF CLASS | | | 1 YEAR | | | SINCE

INCEPTION | |

CLASS A SHARES | | | 8/31/11 | | | | | | | | | |

Without Sales Charge | | | | | | | 0.46 | % | | | 6.01 | % |

With Sales Charge* | | | | | | | (4.84 | ) | | | 3.60 | |

CLASS C SHARES | | | 8/31/11 | | | | | | | | | |

Without CDSC | | | | | | | (0.04 | ) | | | 5.48 | |

With CDSC** | | | | | | | (1.04 | ) | | | 5.48 | |

CLASS R5 SHARES | | | 8/31/11 | | | | 0.94 | | | | 6.51 | |

CLASS R6 SHARES | | | 8/31/11 | | | | 0.98 | | | | 6.56 | |

SELECT SHARES | | | 8/31/11 | | | | 0.69 | | | | 6.29 | |

| * | | Sales Charge for Class A Shares is 5.25%. |

| ** | | Assumes a 1% CDSC (contingent deferred sales charge) for the one year period and 0% CDSC thereafter. |

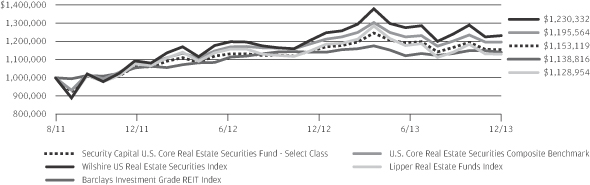

LIFE OF FUND PERFORMANCE (8/31/11 TO 12/31/13)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

The Fund commenced operations on August 31, 2011.

The graph illustrates comparative performance for $1,000,000 invested in Select Class Shares of the Security Capital U.S. Core Real Estate Securities Fund, the Wilshire US Real Estate Securities Index, Barclays Investment Grade REIT Index, U.S. Core Real Estate Securities Composite Benchmark and the Lipper Real Estate Funds Index from August 31, 2011 to December 31, 2013. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the indices, other than the Lipper Real Estate Funds Index, does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper Real Estate Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Wilshire US Real Estate Securities Index is an unmanaged, float-adjusted market capitalization-weighted index comprising publicly traded REITs and real estate operating

companies, not including special purpose REITs. It is comprised of major companies engaged in the equity ownership and operation of commercial real estate. The Barclays Investment Grade REIT Index publicly includes issued U.S. corporate and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered or 144a securities with registration rights and only includes the portion of the Barclays U.S. Corporate Index deemed to be a Real Estate Investment Trust. The U.S. Core Real Estate Securities Composite Benchmark is a composite benchmark comprised of unmanaged indices that includes 60% Wilshire US Real Estate Securities Index, 10% Wells Fargo Hybrid and Preferred Securities REIT Index and 30% Barclays Investment Grade REIT Index. The Lipper Real Estate Funds Index represents the total returns of the funds in the indicated category as defined by Lipper, Inc. Investors cannot invest directly in an index.

Select Class Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 5 | |

Security Capital U.S. Core Real Estate Securities Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2013

(Amounts in thousands)

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Common Stocks — 59.4% | |

| | | | Apartments — 0.6% | | | | |

| | 6 | | | Home Properties, Inc. | | | 316 | |

| | | | | | | | |

| | | | Diversified — 4.8% | | | | |

| | 6 | | | Digital Realty Trust, Inc. | | | 287 | |

| | 27 | | | Duke Realty Corp. | | | 401 | |

| | 17 | | | Liberty Property Trust | | | 586 | |

| | 17 | | | Vornado Realty Trust | | | 1,466 | |

| | | | | | | | |

| | | | | | | 2,740 | |

| | | | | | | | |

| | | | Health Care — 7.0% | | | | |

| | 39 | | | HCP, Inc. | | | 1,434 | |

| | 25 | | | Health Care REIT, Inc. | | | 1,342 | |

| | 20 | | | Ventas, Inc. | | | 1,167 | |

| | | | | | | | |

| | | | | | | 3,943 | |

| | | | | | | | |

| | | | Hotels — 5.0% | | | | |

| | 2 | | | Hilton Worldwide Holdings, Inc. (a) | | | 48 | |

| | 73 | | | Host Hotels & Resorts, Inc. | | | 1,412 | |

| | 30 | | | RLJ Lodging Trust | | | 723 | |

| | 46 | | | Sunstone Hotel Investors, Inc. | | | 614 | |

| | | | | | | | |

| | | | | | | 2,797 | |

| | | | | | | | |

| | | | Industrial — 3.9% | | | | |

| | 60 | | | Prologis, Inc. | | | 2,205 | |

| | | | | | | | |

| | | | Multifamily — 10.6% | | | | |

| | 48 | | | Apartment Investment & Management Co., Class A | | | 1,246 | |

| | 13 | | | AvalonBay Communities, Inc. | | | 1,553 | |

| | 41 | | | Equity Residential | | | 2,104 | |

| | 3 | | | Essex Property Trust, Inc. | | | 396 | |

| | 30 | | | UDR, Inc. | | | 704 | |

| | | | | | | | |

| | | | | | | 6,003 | |

| | | | | | | | |

| | | | Office — 7.2% | | | | |

| | 9 | | | Alexandria Real Estate Equities, Inc. | | | 545 | |

| | 33 | | | BioMed Realty Trust, Inc. | | | 599 | |

| | 9 | | | Boston Properties, Inc. | | | 910 | |

| | 25 | | | Brookfield Office Properties, Inc. | | | 479 | |

| | 28 | | | Douglas Emmett, Inc. | | | 651 | |

| | 5 | | | Kilroy Realty Corp. | | | 268 | |

| | 7 | | | SL Green Realty Corp. | | | 611 | |

| | | | | | | | |

| | | | | | | 4,063 | |

| | | | | | | | |

| | | | Regional Malls — 11.4% | | | | |

| | 49 | | | General Growth Properties, Inc. | | | 984 | |

| | 22 | | | Macerich Co. (The) | | | 1,287 | |

| | 23 | | | Simon Property Group, Inc. | | | 3,470 | |

| | 10 | | | Taubman Centers, Inc. | | | 665 | |

| | | | | | | | |

| | | | | | | 6,406 | |

| | | | | | | | |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Shopping Centers — 4.8% | | | | |

| | 3 | | | Brixmor Property Group, Inc. (a) | | | 51 | |

| | 46 | | | DDR Corp. | | | 709 | |

| | 52 | | | Kimco Realty Corp. | | | 1,021 | |

| | 11 | | | Regency Centers Corp. | | | 502 | |

| | 15 | | | Weingarten Realty Investors | | | 413 | |

| | | | | | | | |

| | | | | | | 2,696 | |

| | | | | | | | |

| | | | Storage — 4.1% | | | | |

| | 27 | | | CubeSmart | | | 429 | |

| | 10 | | | Extra Space Storage, Inc. | | | 431 | |

| | 10 | | | Public Storage | | | 1,479 | |

| | | | | | | | |

| | | | | | | 2,339 | |

| | | | | | | | |

| | | | Total Common Stocks

(Cost $32,953) | | | 33,508 | |

| | | | | | | | |

| | |

PRINCIPAL AMOUNT($) | | | | | | |

| Corporate Bonds — 16.4% | |

| | | | Health Care — 9.7% | | | | |

| | | | HCP, Inc., | | | | |

| | 500 | | | Series E, 6.000%, 06/15/14 | | | 512 | |

| | 900 | | | 6.000%, 03/01/15 | | | 952 | |

| | 250 | | | 6.300%, 09/15/16 | | | 282 | |

| | | | Health Care REIT, Inc., | | | | |

| | 175 | | | 3.625%, 03/15/16 | | | 183 | |

| | 1,888 | | | 5.875%, 05/15/15 | | | 2,012 | |

| | 458 | | | 6.200%, 06/01/16 | | | 509 | |

| | 350 | | | Healthcare Realty Trust, Inc., 6.500%, 01/17/17 | | | 393 | |

| | 580 | | | Senior Housing Properties Trust, 4.300%, 01/15/16 | | | 604 | |

| | | | | | | | |

| | | | | | | 5,447 | |

| | | | | | | | |

| | | | Industrial — 2.4% | | | | |

| | | | ProLogis LP, | | | | |

| | 78 | | | 4.500%, 08/15/17 | | | 84 | |

| | 1,100 | | | 5.625%, 11/15/16 | | | 1,224 | |

| | 60 | | | 6.625%, 05/15/18 | | | 70 | |

| | | | | | | | |

| | | | | | | 1,378 | |

| | | | | | | | |

| | | | Office — 3.8% | | | | |

| | 275 | | | Brandywine Operating Partnership LP, 5.700%, 05/01/17 | | | 303 | |

| | 100 | | | CommonWealth REIT, 6.250%, 08/15/16 | | | 106 | |

| | 900 | | | Kilroy Realty LP, 5.000%, 11/03/15 | | | 959 | |

| | 700 | | | Reckson Operating Partnership LP, 6.000%, 03/31/16 | | | 758 | |

| | | | | | | | |

| | | | | | | 2,126 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 6 | | | | J.P. MORGAN SPECIALTY FUNDS | | DECEMBER 31, 2013 |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Corporate Bonds — Continued | |

| | | | Shopping Centers — 0.5% | | | | |

| | 200 | | | DDR Corp., 7.500%, 04/01/17 | | | 233 | |

| | 70 | | | Equity One, Inc., 6.000%, 09/15/16 | | | 78 | |

| | | | | | | | |

| | | | | | | 311 | |

| | | | | | | | |

| | | | Total Corporate Bonds

(Cost $9,155) | | | 9,262 | |

| | | | | | | | |

| | |

| SHARES | | | | | | |

| Preferred Stocks ($25 par value) — 21.7% | |

| | | | Apartments — 0.5% | | | | |

| | 12 | | | Campus Crest Communities, Inc., Series A, 8.000%, 02/09/17 @ | | | 295 | |

| | | | | | | | |

| | | | Diversified — 0.6% | | | | |

| | 3 | | | Duke Realty Corp., Series L, 6.600%,

02/03/14 @ | | | 58 | |

| | 6 | | | PS Business Parks, Inc., Series S, 6.450%, 01/18/17 @ | | | 141 | |

| | 2 | | | PS Business Parks, Inc., Series T, 6.000%, 05/14/17 @ | | | 43 | |

| | 2 | | | Vornado Realty Trust, Series G, 6.625%, 02/03/14 @ | | | 55 | |

| | 2 | | | Vornado Realty Trust, Series K, 5.700%, 07/18/17 @ | | | 36 | |

| | | | | | | | |

| | | | | | | 333 | |

| | | | | | | | |

| | | | Hotels — 2.9% | | | | |

| | 12 | | | Ashford Hospitality Trust, Inc., Series D, 8.450%, 02/03/14 @ | | | 290 | |

| | 31 | | | Strategic Hotels & Resorts, Inc., Series B, 8.250%, 02/03/14 @ | | | 724 | |

| | 24 | | | Sunstone Hotel Investors, Inc., Series D, 8.000%, 04/06/16 @ | | | 590 | |

| | | | | | | | |

| | | | | | | 1,604 | |

| | | | | | | | |

| | | | Industrial — 0.7% | | | | |

| | 9 | | | STAG Industrial, Inc., Series A, 9.000%, 11/02/16 @ | | | 239 | |

| | 7 | | | Terreno Realty Corp., Series A, 7.750%, 07/19/17 @ | | | 169 | |

| | | | | | | | |

| | | | | | | 408 | |

| | | | | | | | |

| | | | Multifamily — 0.1% | | | | |

| | 2 | | | Equity Lifestyle Properties, Inc., Series C, 6.750%, 09/07/17 @ | | | 53 | |

| | | | | | | | |

| | | | Office — 3.9% | | | | |

| | 2 | | | Alexandria Real Estate Equities, Inc., Series E, 6.450%, 03/15/17 @ | | | 35 | |

| | 15 | | | Boston Properties, Inc., 5.250%, 03/27/18 @ | | | 281 | |

| | 10 | | | Brandywine Realty Trust, Series E, 6.900%, 04/11/17 @ | | | 218 | |

| | | | | | | | |

SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Office — Continued | | | | |

| | 11 | | | CommonWealth REIT, 7.500%, 11/15/19 | | | 231 | |

| | 34 | | | Corporate Office Properties Trust, Series L, 7.375%, 06/27/17 @ | | | 805 | |

| | 20 | | | Hudson Pacific Properties, Inc., Series B, 8.375%, 12/10/15 @ | | | 524 | |

| | 5 | | | SL Green Realty Corp., Series I, 6.500%, 08/10/17 @ | | | 110 | |

| | | | | | | | |

| | | | | | | 2,204 | |

| | | | | | | | |

| | | | Regional Malls — 8.1% | | | | |

| | 39 | | | CBL & Associates Properties, Inc., Series D, 7.375%, 02/03/14 @ | | | 926 | |

| | 59 | | | General Growth Properties, Inc., Series A, 6.375%, 02/13/18 @ | | | 1,195 | |

| | 8 | | | Glimcher Realty Trust, 6.875%, 03/27/18 @ | | | 173 | |

| | 4 | | | Glimcher Realty Trust, Series G, 8.125%, 02/03/14 @ | | | 99 | |

| | 18 | | | Glimcher Realty Trust, Series H, 7.500%, 08/10/17 @ | | | 406 | |

| | 25 | | | Taubman Centers, Inc., Series J, 6.500%, 08/14/17 @ | | | 519 | |

| | 63 | | | Taubman Centers, Inc., Series K, 6.250%, 03/15/18 @ | | | 1,246 | |

| | | | | | | | |

| | | | | | | 4,564 | |

| | | | | | | | |

| | | | Shopping Centers — 3.7% | | | | |

| | 8 | | | DDR Corp., Series H, 7.375%, 02/03/14 @ | | | 212 | |

| | 7 | | | DDR Corp., Series J, 6.500%, 08/01/17 @ | | | 148 | |

| | 3 | | | DDR Corp., Series K, 6.250%, 04/09/18 @ | | | 53 | |

| | 17 | | | Inland Real Estate Corp., Series A, 8.125%, 10/06/16 @ | | | 437 | |

| | 14 | | | Kite Realty Group Trust, Series A, 8.250%, 12/07/15 @ | | | 354 | |

| | 14 | | | Regency Centers Corp., Series 6, 6.625%, 02/16/17 @ | | | 302 | |

| | 13 | | | Urstadt Biddle Properties, Inc., Series F, 7.125%, 10/24/17 @ | | | 291 | |

| | 12 | | | Weingarten Realty Investors, Series F, 6.500%, 02/03/14 @ | | | 272 | |

| | | | | | | | |

| | | | | | | 2,069 | |

| | | | | | | | |

| | | | Storage — 1.2% | | | | |

| | 16 | | | CubeSmart, Series A, 7.750%, 11/02/16 @ | | | 395 | |

| | 8 | | | Public Storage, Series Q, 6.500%, 04/14/16 @ | | | 187 | |

| | 4 | | | Public Storage, Series R, 6.350%, 07/26/16 @ | | | 97 | |

| | | | | | | | |

| | | | | | | 679 | |

| | | | | | | | |

| | | | Total Preferred Stocks

(Cost $13,154) | | | 12,209 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 7 | |

Security Capital U.S. Core Real Estate Securities Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2013 (continued)

(Amounts in thousands)

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Short-Term Investment — 2.6% | |

| | | | Investment Company — 2.6% | | | | |

| | 1,488 | | | JPMorgan Prime Money Market Fund, Institutional Class Shares, 0.010% (b) (l) (Cost $1,488) | | | 1,488 | |

| | | | | | | | |

| | | | Total Investments — 100.1%

(Cost $56,750) | | | 56,467 | |

| | | | Liabilities in Excess of

Other Assets — (0.1)% | | | (81 | ) |

| | | | | | | | |

| | | | NET ASSETS — 100.0% | | $ | 56,386 | |

| | | | | | | | |

Percentages indicated are based on net assets.

NOTES TO SCHEDULE OF PORTFOLIO INVESTMENTS:

| | |

| REIT | | — Real Estate Investment Trust |

| |

| (a) | | — Non-income producing security. |

| (b) | | — Investment in affiliate. Money market fund registered under the Investment Company Act of 1940, as amended, and advised by J.P. Morgan Investment Management Inc. |

| (l) | | — The rate shown is the current yield as of December 31, 2013. |

| @ | | — The date shown reflects the next call date on which the issuer may redeem the security at par value. The coupon rate for this security is based on par value and is currently in effect as of December 31, 2013. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 8 | | | | J.P. MORGAN SPECIALTY FUNDS | | DECEMBER 31, 2013 |

STATEMENT OF ASSETS AND LIABILITIES

AS OF DECEMBER 31, 2013

(Amounts in thousands, except per share amounts)

| | | | |

| | | U.S. Core Real

Estate Securities

Fund | |

ASSETS: | | | | |

Investments in non-affiliates, at value | | $ | 54,979 | |

Investments in affiliates, at value | | | 1,488 | |

| | | | |

Total investment securities, at value | | | 56,467 | |

Receivables: | | | | |

Fund shares sold | | | 40 | |

Interest and dividends from non-affiliates | | | 352 | |

Dividends from affiliates | | | — | (a) |

| | | | |

Total Assets | | | 56,859 | |

| | | | |

| |

LIABILITIES: | | | | |

Payables: | | | | |

Investment securities purchased | | | 293 | |

Fund shares redeemed | | | 94 | |

Accrued liabilities: | | | | |

Investment advisory fees | | | 9 | |

Shareholder servicing fees | | | 10 | |

Distribution fees | | | 1 | |

Custodian and accounting fees | | | 13 | |

Audit Fees | | | 39 | |

Other | | | 14 | |

| | | | |

Total Liabilities | | | 473 | |

| | | | |

Net Assets | | $ | 56,386 | |

| | | | |

| (a) | Amount rounds to less than $1,000. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 9 | |

STATEMENT OF ASSETS AND LIABILITIES

AS OF DECEMBER 31, 2013 (continued)

(Amounts in thousands, except per share amounts)

| | | | |

| | | U.S. Core Real

Estate Securities

Fund | |

NET ASSETS: | | | | |

Paid-in-Capital | | $ | 57,518 | |

Accumulated undistributed (distributions in excess of) net investment income | | | 69 | |

Accumulated net realized gains (losses) | | | (918 | ) |

Net unrealized appreciation (depreciation) | | | (283 | ) |

| | | | |

Total Net Assets | | $ | 56,386 | |

| | | | |

| |

Net Assets: | | | | |

Class A | | $ | 4,270 | |

Class C | | | 88 | |

Class R5 | | | 58 | |

Class R6 | | | 7,630 | |

Select | | | 44,340 | |

| | | | |

Total | | $ | 56,386 | |

| | | | |

| |

Outstanding units of beneficial interest (shares) | | | | |

($0.0001 par value; unlimited number of shares authorized): | | | | |

Class A | | | 272 | |

Class C | | | 5 | |

Class R5 | | | 4 | |

Class R6 | | | 485 | |

Select | | | 2,820 | |

| |

Net Asset Value (a): | | | | |

Class A — Redemption price per share | | $ | 15.70 | |

Class C — Offering price per share (b) | | | 15.70 | |

Class R5 — Offering and redemption price per share | | | 15.73 | |

Class R6 — Offering and redemption price per share | | | 15.74 | |

Select — Offering and redemption price per share | | | 15.72 | |

Class A maximum sales charge | | | 5.25 | % |

Class A maximum public offering price per share | | | | |

[net asset value per share/(100% — maximum sales charge)] | | $ | 16.57 | |

| | | | |

| |

Cost of investments in non-affiliates | | $ | 55,262 | |

Cost of investments in affiliates | | | 1,488 | |

| (a) | Per share amounts may not recalculate due to rounding of net assets and/or shares outstanding. |

| (b) | Redemption price for Class C Shares varies based upon length of time the shares are held. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 10 | | | | J.P. MORGAN SPECIALTY FUNDS | | DECEMBER 31, 2013 |

STATEMENT OF OPERATIONS

FOR THE YEAR ENDED DECEMBER 31, 2013

(Amounts in thousands)

| | | | |

| | | U.S. Core Real

Estate Securities

Fund | |

INVESTMENT INCOME: | | | | |

Interest income from non-affiliates | | $ | 265 | |

Dividend income from non-affiliates | | | 1,353 | |

Dividend income from affiliates | | | 6 | |

| | | | |

Total investment income | | | 1,624 | |

| | | | |

| |

EXPENSES: | | | | |

Investment advisory fees | | | 333 | |

Administration fees | | | 47 | |

Distribution fees: | | | | |

Class A | | | 11 | |

Class C | | | 1 | |

Shareholder servicing fees: | | | | |

Class A | | | 11 | |

Class C | | | — | (a) |

Class R5 | | | — | (a) |

Select | | | 116 | |

Custodian and accounting fees | | | 37 | |

Professional fees | | | 58 | |

Trustees’ and Chief Compliance Officer’s fees | | | 1 | |

Printing and mailing costs | | | 12 | |

Registration and filing fees | | | 76 | |

Transfer agent fees | | | 14 | |

Other | | | 7 | |

| | | | |

Total expenses | | | 724 | |

| | | | |

Less amounts waived | | | (47 | ) |

Less expense reimbursements | | | (169 | ) |

| | | | |

Net expenses | | | 508 | |

| | | | |

Net investment income (loss) | | | 1,116 | |

| | | | |

| |

REALIZED/UNREALIZED GAINS (LOSSES): | | | | |

Net realized gain (loss) on transactions from investments in non-affiliates | | | 734 | |

Change in net unrealized appreciation/depreciation of investments in non-affiliates | | | (2,160 | ) |

| | | | |

Net realized/unrealized gains (losses) | | | (1,426 | ) |

| | | | |

Change in net assets resulting from operations | | $ | (310 | ) |

| | | | |

| (a) | Amount rounds to less than $1,000. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 11 | |

STATEMENTS OF CHANGES IN NET ASSETS

FOR THE PERIODS INDICATED

(Amounts in thousands)

| | | | | | | | |

| | | U.S. Core Real Estate Securities Fund | |

| | | Year Ended

12/31/2013 | | | Year Ended

12/31/2012 | |

CHANGE IN NET ASSETS RESULTING FROM OPERATIONS: | | | | | | | | |

Net investment income (loss) | | $ | 1,116 | | | $ | 769 | |

Net realized gain (loss) | | | 734 | | | | 639 | |

Change in net unrealized appreciation/depreciation | | | (2,160 | ) | | | 1,635 | |

| | | | | | | | |

Change in net assets resulting from operations | | | (310 | ) | | | 3,043 | |

| | | | | | | | |

| | |

DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | |

Class A | | | | | | | | |

From net investment income | | | (73 | ) | | | (60 | ) |

From net realized gains | | | (114 | ) | | | (67 | ) |

Return of capital | | | (4 | ) | | | | |

Class C | | | | | | | | |

From net investment income | | | (1 | ) | | | (1 | ) |

From net realized gains | | | (2 | ) | | | (1 | ) |

Return of capital | | | — | (a) | | | | |

Class R5 | | | | | | | | |

From net investment income | | | (2 | ) | | | (1 | ) |

From net realized gains | | | (1 | ) | | | (1 | ) |

Return of capital | | | — | (a) | | | | |

Class R6 | | | | | | | | |

From net investment income | | | (124 | ) | | | (1 | ) |

From net realized gains | | | (196 | ) | | | (1 | ) |

Return of capital | | | (5 | ) | | | | |

Select | | | | | | | | |

From net investment income | | | (900 | ) | | | (685 | ) |

From net realized gains | | | (1,187 | ) | | | (712 | ) |

Return of capital | | | (44 | ) | | | | |

| | | | | | | | |

Total distributions to shareholders | | | (2,653 | ) | | | (1,530 | ) |

| | | | | | | | |

| | |

CAPITAL TRANSACTIONS: | | | | | | | | |

Change in net assets resulting from capital transactions | | | 13,941 | | | | 33,947 | |

| | | | | | | | |

| | |

NET ASSETS: | | | | | | | | |

Change in net assets | | | 10,978 | | | | 35,460 | |

Beginning of period | | | 45,408 | | | | 9,948 | |

| | | | | | | | |

End of period | | $ | 56,386 | | | $ | 45,408 | |

| | | | | | | | |

Accumulated undistributed (distributions in excess of) net investment income | | $ | 69 | | | $ | 48 | |

| | | | | | | | |

| (a) | Amount rounds to less than $1,000. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 12 | | | | J.P. MORGAN SPECIALTY FUNDS | | DECEMBER 31, 2013 |

| | | | | | | | |

| | | U.S. Core Real Estate Securities Fund | |

| | | Year Ended

12/31/2013 | | | Year Ended

12/31/2012 | |

CAPITAL TRANSACTIONS: | | | | | | | | |

Class A | | | | | | | | |

Proceeds from shares issued | | $ | 488 | | | $ | 1,020 | |

Distributions reinvested | | | 191 | | | | 127 | |

Cost of shares redeemed | | | (96 | ) | | | (60 | ) |

| | | | | | | | |

Change in net assets resulting from Class A capital transactions | | $ | 583 | | | $ | 1,087 | |

| | | | | | | | |

Class C | | | | | | | | |

Proceeds from shares issued | | $ | 33 | | | $ | — | |

Distributions reinvested | | | 3 | | | | 2 | |

Cost of shares redeemed | | | — | (a) | | | — | |

| | | | | | | | |

Change in net assets resulting from Class C capital transactions | | $ | 36 | | | $ | 2 | |

| | | | | | | | |

Class R5 | | | | | | | | |

Distributions reinvested | | $ | 3 | | | $ | 2 | |

| | | | | | | | |

Change in net assets resulting from Class R5 capital transactions | | $ | 3 | | | $ | 2 | |

| | | | | | | | |

Class R6 | | | | | | | | |

Proceeds from shares issued | | $ | 9,609 | | | $ | — | |

Distributions reinvested | | | 325 | | | | 2 | |

Cost of shares redeemed | | | (1,702 | ) | | | — | |

| | | | | | | | |

Change in net assets resulting from Class R6 capital transactions | | $ | 8,232 | | | $ | 2 | |

| | | | | | | | |

Select | | | | | | | | |

Proceeds from shares issued | | $ | 11,609 | | | $ | 31,899 | |

Distributions reinvested | | | 2,005 | | | | 1,334 | |

Cost of shares redeemed | | | (8,527 | ) | | | (379 | ) |

| | | | | | | | |

Change in net assets resulting from Select capital transactions | | $ | 5,087 | | | $ | 32,854 | |

| | | | | | | | |

Total change in net assets resulting from capital transactions | | $ | 13,941 | | | $ | 33,947 | |

| | | | | | | | |

| (a) | Amount rounds to less than $1,000. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 13 | |

STATEMENTS OF CHANGES IN NET ASSETS

FOR THE PERIODS INDICATED (continued)

(Amounts in thousands)

| | | | | | | | |

| | | U.S. Core Real Estate Securities Fund | |

| | | Year Ended

12/31/2013 | | | Year Ended

12/31/2012 | |

SHARE TRANSACTIONS: | | | | | | | | |

Class A | | | | | | | | |

Issued | | | 30 | | | | 62 | |

Reinvested | | | 12 | | | | 8 | |

Redeemed | | | (6 | ) | | | (4 | ) |

| | | | | | | | |

Change in Class A Shares | | | 36 | | | | 66 | |

| | | | | | | | |

Class C | | | | | | | | |

Issued | | | 2 | | | | — | |

Reinvested | | | — | (a) | | | — | (a) |

Redeemed | | | — | (a) | | | — | |

| | | | | | | | |

Change in Class C Shares | | | 2 | | | | — | (a) |

| | | | | | | | |

Class R5 | | | | | | | | |

Reinvested | | | 1 | | | | — | (a) |

| | | | | | | | |

Change in Class R5 Shares | | | 1 | | | | — | (a) |

| | | | | | | | |

Class R6 | | | | | | | | |

Issued | | | 564 | | | | — | |

Reinvested | | | 20 | | | | — | (a) |

Redeemed | | | (102 | ) | | | — | |

| | | | | | | | |

Change in Class R6 Shares | | | 482 | | | | — | (a) |

| | | | | | | | |

Select | | | | | | | | |

Issued | | | 679 | | | | 1,984 | |

Reinvested | | | 125 | | | | 82 | |

Redeemed | | | (510 | ) | | | (23 | ) |

| | | | | | | | |

Change in Select Shares | | | 294 | | | | 2,043 | |

| | | | | | | | |

| (a) | Amount rounds to less than 1,000. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 14 | | | | J.P. MORGAN SPECIALTY FUNDS | | DECEMBER 31, 2013 |

THIS PAGE IS INTENTIONALLY LEFT BLANK

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 15 | |

FINANCIAL HIGHLIGHTS

FOR THE PERIODS INDICATED

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Per share operating performance | |

| | | | | | Investment operations | | | Distributions | |

| | | Net asset

value,

beginning

of period | | | Net

investment

income

(loss) | | | Net realized

and unrealized

gains

(losses) on

investments | | | Total from

investment

operations | | | Net

investment

income | | | Net

realized

gain | | | Return

of

capital | | | Total

distributions | |

U.S. Core Real Estate Securities Fund | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Class A | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Year Ended December 31, 2013 | | $ | 16.36 | | | $ | 0.29 | (f) | | $ | (0.21 | ) | | $ | 0.08 | | | $ | (0.28 | ) | | $ | (0.44 | ) | | $ | (0.02 | ) | | $ | (0.74 | ) |

Year Ended December 31, 2012 | | | 14.98 | | | | 0.34 | (f) | | | 1.62 | | | | 1.96 | | | | (0.29 | ) | | | (0.29 | ) | | | — | | | | (0.58 | ) |

August 31, 2011 (g) through December 31, 2011 | | | 15.00 | | | | 0.35 | (f) | | | (0.23 | ) | | | 0.12 | | | | (0.10 | ) | | | — | (h) | | | (0.04 | ) | | | (0.14 | ) |

| | | | | | | | |

Class C | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Year Ended December 31, 2013 | | | 16.37 | | | | 0.22 | (f) | | | (0.22 | ) | | | — | (h) | | | (0.21 | ) | | | (0.44 | ) | | | (0.02 | ) | | | (0.67 | ) |

Year Ended December 31, 2012 | | | 15.00 | | | | 0.25 | (f) | | | 1.62 | | | | 1.87 | | | | (0.21 | ) | | | (0.29 | ) | | | — | | | | (0.50 | ) |

August 31, 2011 (g) through December 31, 2011 | | | 15.00 | | | | 0.11 | (f) | | | (0.01 | ) | | | 0.10 | | | | (0.06 | ) | | | — | (h) | | | (0.04 | ) | | | (0.10 | ) |

| | | | | | | | |

Class R5 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Year Ended December 31, 2013 | | | 16.39 | | | | 0.37 | (f) | | | (0.22 | ) | | | 0.15 | | | | (0.35 | ) | | | (0.44 | ) | | | (0.02 | ) | | | (0.81 | ) |

Year Ended December 31, 2012 | | | 15.00 | | | | 0.41 | (f) | | | 1.62 | | | | 2.03 | | | | (0.35 | ) | | | (0.29 | ) | | | — | | | | (0.64 | ) |

August 31, 2011 (g) through December 31, 2011 | | | 15.00 | | | | 0.16 | (f) | | | (0.02 | ) | | | 0.14 | | | | (0.10 | ) | | | — | (h) | | | (0.04 | ) | | | (0.14 | ) |

| | | | | | | | |

Class R6 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Year Ended December 31, 2013 | | | 16.39 | | | | 0.43 | (f) | | | (0.26 | ) | | | 0.17 | | | | (0.36 | ) | | | (0.44 | ) | | | (0.02 | ) | | | (0.82 | ) |

Year Ended December 31, 2012 | | | 15.00 | | | | 0.42 | (f) | | | 1.62 | | | | 2.04 | | | | (0.36 | ) | | | (0.29 | ) | | | — | | | | (0.65 | ) |

August 31, 2011 (g) through December 31, 2011 | | | 15.00 | | | | 0.16 | (f) | | | (0.02 | ) | | | 0.14 | | | | (0.10 | ) | | | — | (h) | | | (0.04 | ) | | | (0.14 | ) |

| | | | | | | | |

Select | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Year Ended December 31, 2013 | | | 16.38 | | | | 0.33 | (f) | | | (0.21 | ) | | | 0.12 | | | | (0.32 | ) | | | (0.44 | ) | | | (0.02 | ) | | | (0.78 | ) |

Year Ended December 31, 2012 | | | 15.00 | | | | 0.41 | (f) | | | 1.59 | | | | 2.00 | | | | (0.33 | ) | | | (0.29 | ) | | | — | | | | (0.62 | ) |

August 31, 2011 (g) through December 31, 2011 | | | 15.00 | | | | 0.19 | (f) | | | (0.05 | ) | | | 0.14 | | | | (0.10 | ) | | | — | (h) | | | (0.04 | ) | | | (0.14 | ) |

| (a) | Annualized for periods less than one year. |

| (b) | Not annualized for periods less than one year. |

| (c) | Includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset values for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

| (d) | Includes earnings credits and interest expense, if applicable, each of which is less than 0.01% unless otherwise noted. |

| (e) | Portfolio turnover is calculated by dividing the lesser of total purchases or sales of portfolio securities for the reporting period by the monthly average value of portfolio securities owned during the reporting period. Excluded from both the numerator and denominator are amounts relating to derivatives and securities whose maturities or expiration dates at the time of acquisition were one year or less. |

| (f) | Calculated based upon average shares outstanding. |

| (g) | Commencement of operations. |

| (h) | Amount rounds to less than $0.01. |

| (i) | Certain non-recurring expenses incurred by the Fund were not annualized for the period ended December 31, 2011. |

| (j) | The Net investment income (loss) ratios for Class A and Select Class are disproportionate due to the timing of shareholder capital transactions and when the Fund earned income over the period. |

| (k) | Ratios are disproportionate between classes due to the size of net assets and fixed expense. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 16 | | | | J.P. MORGAN SPECIALTY FUNDS | | DECEMBER 31, 2013 |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Ratios/Supplemental data | |

| | | | | | | | | | Ratios to average net assets (a) | | | | |

Net asset

value,

end of

period | | | Total return

(excludes

sales charge) (b)(c) | | |

Net assets,

end of

period

(000’s) | | | Net

expenses (d) | | | Net

investment

income

(loss) | | | Expenses

without waivers,

reimbursements and

earnings credits | | | Portfolio

turnover

rate (b)(e) | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| $ | 15.70 | | | | 0.46 | % | | $ | 4,270 | | | | 1.17 | % | | | 1.75 | % | | | 1.56 | % | | | 106 | % |

| | 16.36 | | | | 13.14 | | | | 3,867 | | | | 1.17 | | | | 2.11 | | | | 2.33 | | | | 74 | |

| | 14.98 | | | | 0.83 | | | | 2,548 | | | | 1.18 | (i) | | | 7.03 | (i)(j) | | | 5.74 | (i)(k) | | | 8 | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 15.70 | | | | (0.04 | ) | | | 88 | | | | 1.67 | | | | 1.30 | | | | 2.05 | | | | 106 | |

| | 16.37 | | | | 12.53 | | | | 57 | | | | 1.67 | | | | 1.56 | | | | 2.90 | | | | 74 | |

| | 15.00 | | | | 0.69 | | | | 50 | | | | 1.68 | (i) | | | 2.29 | (i) | | | 11.12 | (i)(k) | | | 8 | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 15.73 | | | | 0.87 | | | | 58 | | | | 0.72 | | | | 2.18 | | | | 1.11 | | | | 106 | |

| | 16.39 | | | | 13.65 | | | | 57 | | | | 0.72 | | | | 2.52 | | | | 1.94 | | | | 74 | |

| | 15.00 | | | | 1.01 | | | | 50 | | | | 0.73 | (i) | | | 3.24 | (i) | | | 10.27 | (i)(k) | | | 8 | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 15.74 | | | | 0.98 | | | | 7,630 | | | | 0.67 | | | | 2.60 | | | | 1.04 | | | | 106 | |

| | 16.39 | | | | 13.70 | | | | 57 | | | | 0.67 | | | | 2.57 | | | | 1.89 | | | | 74 | |

| | 15.00 | | | | 1.02 | | | | 51 | | | | 0.68 | (i) | | | 3.29 | (i) | | | 10.22 | (i)(k) | | | 8 | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 15.72 | | | | 0.69 | | | | 44,340 | | | | 0.92 | | | | 1.98 | | | | 1.31 | | | | 106 | |

| | 16.38 | | | | 13.42 | | | | 41,370 | | | | 0.92 | | | | 2.53 | | | | 1.91 | | | | 74 | |

| | 15.00 | | | | 0.97 | | | | 7,249 | | | | 0.93 | (i) | | | 3.82 | (i)(j) | | | 9.39 | (i)(k) | | | 8 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 17 | |

NOTES TO FINANCIAL STATEMENTS

AS OF DECEMBER 31, 2013

1. Organization

JPMorgan Trust I (the “Trust”) was formed on November 12, 2004, as Delaware statutory trust, pursuant to a Declaration of Trust dated November 5, 2004 and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company.

The following is a separate fund of the Trust (the “Fund”) covered by this report:

| | | | |

| Fund | | Classes Offered | | Diversified/Non-Diversified |

| Security Capital U.S. Core Real Estate Securities Fund | | Class A, Class C, Class R5, Class R6 and Select Class | | Non-Diversified |

The investment objective of the Fund is to seek a risk-adjusted total return over the long term by investing primarily in real estate securities.

Class A Shares generally provide for a front-end sales charge while Class C Shares provide for a contingent deferred sales charge (“CDSC”). No sales charges are assessed with respect to Class R5, Class R6 and Select Class Shares. All classes of shares have equal rights as to earnings, assets and voting privileges, except that each class may bear different distribution and shareholder servicing fees and each class has exclusive voting rights with respect to its distribution plan and shareholder servicing agreements. Certain Class A Shares, for which front-end sales charges have been waived, may be subject to a CDSC as described in the Fund’s prospectus.

2. Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. The policies are in accordance with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

A. Valuation of Investments — Equity securities listed on a North American, Central American, South American or Caribbean securities exchange shall generally be valued at the last sale price on the exchange on which the security is principally traded that is reported before the time when the net assets of the Fund are valued. Securities listed on the NASDAQ Stock Market LLC are generally valued at the NASDAQ Official Closing Price. Fixed income securities (other than certain short-term investments maturing in less than 61 days) are valued each day based on prices received from independent or affiliated pricing services approved by the Board of Trustees or third party broker-dealers. The pricing services or broker-dealers use multiple valuation techniques to determine fair value. In instances where sufficient market activity exists, the pricing services or broker-dealers may utilize a market-based approach through which quotes from market makers are used to determine fair value. In instances where sufficient market activity may not exist or is limited, the pricing services or broker-dealers also utilize proprietary valuation models which may consider market transactions in comparable securities and the various relationships between securities in determining fair value and/or market characteristics such as benchmark yield curves, option-adjusted spreads, credit spreads, estimated default rates, coupon rates, anticipated timing of principal repayments, underlying collateral, and other unique security features in order to estimate the relevant cash flows, which are then discounted to calculate the fair values. Generally, short-term investments of sufficient credit quality maturing in less than 61 days are valued at amortized cost, which approximates fair value. Investments in open-end investment companies are valued at each investment company’s net asset value per share (“NAV”) as of the report date.

Certain investments of the Fund may, depending upon market conditions, trade in relatively thin markets and/or in markets that experience significant volatility. As a result of these conditions, the prices used by the Fund to value these securities may differ from the value that would be realized if these securities were sold, and the differences could be material. Futures and options are generally valued on the basis of available market quotations. Swaps and other derivatives are valued daily, primarily using independent or affiliated pricing services approved by the Board of Trustees. If valuations are not available from such pricing services or values received are deemed not representative of fair value, values will be obtained from a third party broker-dealer or counterparty.

Securities or other assets for which market quotations are not readily available or for which market quotations are deemed to not represent the fair value of the security or asset at the time of pricing (including certain illiquid securities) are fair valued in accordance with procedures established by and under the supervision and responsibility of the Board of Trustees. The Board of Trustees has established an Audit and Valuation Committee to assist with the oversight of the valuation of the Fund’s securities. JPMorgan Funds Management, Inc. (the “Administrator” or “JPMFM”) (“JPMorgan”), has established a Valuation Committee (“VC”) that is comprised of senior representatives from JPMFM, J.P. Morgan Investment Management Inc., (“JPMIM”), and J.P. Morgan Asset Management’s Legal, Compliance and Risk Management groups and the Fund’s Chief Compliance Officer. The VC’s responsibilities include making determinations regarding Level 3 fair value measurements (“Fair Values”) and/or providing recommendations for approval to the Board of Trustees’ Audit and Valuation Committee, in accordance with the Fund’s valuation policies.

The VC or Board of Trustees, as applicable, primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. The VC or Board of Trustees may also use an income-based valuation approach in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Valuations may be based upon current market prices of securities that are comparable in coupon, rating, maturity and industry.

| | | | | | |

| | | |

| 18 | | | | J.P. MORGAN SPECIALTY FUNDS | | DECEMBER 31, 2013 |

It is possible that the estimated values may differ significantly from the values that would have been used had a ready market for the investments existed, and such differences could be material. JPMFM and JPMIM are responsible for monitoring developments that may impact Fair Values and for discussing and assessing Fair Values on an ongoing, and at least a quarterly, basis with the VC and Board of Trustees, as applicable. The appropriateness of Fair Values is assessed based on results of unchanged price review and consideration of macro or security specific events, back testing and broker and vendor due diligence.

Valuations reflected in this report are as of the report date. As a result, changes in valuation due to market events and/or issuer related events after the report date and prior to issuance of the report, are not reflected herein.

The various inputs that are used in determining the fair value of the Fund’s investments are summarized into the three broad levels listed below.

| Ÿ | | Level 1 — quoted prices in active markets for identical securities |

| Ÿ | | Level 2 — other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| Ÿ | | Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

A financial instrument’s level within the fair value hierarchy is based on the lowest level of any input, both individually and in the aggregate, that is significant to the fair value measurement. The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following table represents each valuation input as presented on the Schedule of Portfolio Investments (“SOI”) (amounts in thousands):

| | | | | | | | | | | | | | | | |

| | | Level 1

Quoted prices | | | Level 2

Other significant

observable inputs | | | Level 3

Significant

unobservable inputs | | | Total | |

Investments in Securities | | | | | | | | | | | | | | | | |

Common Stocks | | $ | 33,508 | | | $ | — | | | $ | — | | | $ | 33,508 | |

Preferred Stocks | | | 12,209 | | | | — | | | | — | | | | 12,209 | |

Corporate Bonds | | | — | | | | 9,262 | | | | — | | | | 9,262 | |

Short-Term Investment | | | | | | | | | | | | | | | | |

Investment Company | | | 1,488 | | | | — | | | | — | | | | 1,488 | |

| | | | | | | | | | | | | | | | |

Total Investments in Securities | | $ | 47,205 | | | $ | 9,262 | | | $ | — | | | $ | 56,467 | |

| | | | | | | | | | | | | | | | |

There were no transfers among any levels during the year ended December 31, 2013.

B. Security Transactions and Investment Income — Investment transactions are accounted for on the trade date (the date the order to buy or sell is executed). Securities gains and losses are calculated on a specifically identified cost basis. Interest income is determined on the basis of coupon interest accrued using the effective interest method which adjusts for amortization of premiums and accretion of discounts. Dividend income, net of foreign taxes withheld, if any, are recorded on the ex-dividend date or when the Fund first learns of the dividend.

To the extent such information is publicly available, the Fund records distributions received in excess of income earned from underlying investments as a reduction of cost of investments and/or realized gain. Such amounts are based on estimates if actual amounts are not available and actual amounts of income, realized gain and return of capital may differ from the estimated amounts. The Fund adjusts the estimated amounts of the components of distributions (and consequently their net investment income) as necessary once the issuers provide information about the actual composition of the distributions.

C. Allocation of Income and Expenses — Expenses directly attributable to a fund are charged directly to that fund, while the expenses attributable to more than one fund of the Trust are allocated among the respective funds. In calculating the NAV of each class, investment income, realized and unrealized gains and losses and expenses, other than class specific expenses, are allocated daily to each class of shares based upon the proportion of net assets of each class at the beginning of each day.

D. Federal Income Taxes — The Fund is treated as a separate taxable entity for Federal income tax purposes. The Fund’s policy is to comply with the provisions of the Internal Revenue Code of 1986, as amended (the “Code”), applicable to regulated investment companies and to distribute to shareholders all of its distributable net investment income and net realized gain on investments. Accordingly, no provision for Federal income tax is necessary. Management has reviewed the Fund’s tax positions for all open tax years and has determined that as of December 31, 2013, no liability for income tax is required in the Fund’s financial statements for net unrecognized tax benefits. However, management’s conclusions may be subject to future review based on changes in, or the interpretation of, the accounting standards or tax laws and regulations. The Fund’s Federal tax returns for the prior three fiscal years, or since inception if shorter, remain subject to examination by the Internal Revenue Service.

E. Distributions to Shareholders — Distributions from net investment income are generally declared and paid quarterly and are declared separately for each class. No class has preferential dividend rights; differences in per share rates are due to differences in separate class expenses. Net realized capital gains, if any, are distributed at least annually. The amount of distributions from net investment income and net realized capital gains is determined in accordance with Federal income tax regulations, which may differ from GAAP. To the extent these “book/tax” differences are permanent in nature (i.e., that they result from other than timing of recognition — “temporary differences”), such amounts are reclassified within the capital accounts based on their Federal tax-basis treatment.

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 19 | |

NOTES TO FINANCIAL STATEMENTS

AS OF DECEMBER 31, 2013 (continued)

The following amounts were reclassified within the capital accounts (amounts in thousands):

| | | | | | | | | | | | |

| | | Paid-in-Capital | | | Accumulated undistributed (distributions in

excess of) net investment income | | | Accumulated net realized gains (losses) | |

| | $ | (— | )(a) | | $ | 5 | | | $ | (5 | ) |

The reclassifications for the Fund relate primarily to redesignation of distributions.

| (a) | Amount rounds to less than $1,000. |

3. Fees and Other Transactions with Affiliates

A. Investment Advisory Fee — Pursuant to the Investment Advisory Agreement, Security Capital Research & Management Incorporated (the “Adviser”) acts as the investment adviser to the Fund. The Adviser is a direct, wholly-owned subsidiary of JPMorgan Asset Management Holdings Inc. The Adviser supervises the investments of the Fund and for such services is paid a fee. The fee is accrued daily and paid monthly based on the Fund’s average daily net assets at an annual rate of 0.60%.

B. Administration Fee — Pursuant to an Administration Agreement, the Administrator, an indirect, wholly-owned subsidiary of JPMorgan provides certain administration services to the Fund. In consideration of these services, the Administrator receives a fee accrued daily and paid monthly at an annual rate of 0.15% of the first $25 billion of the average daily net assets of all funds in the J.P. Morgan Funds Complex covered by the Administration Agreement (excluding certain funds of funds and money market funds) and 0.075% of the average daily net assets in excess of $25 billion of all such funds. For the year ended December 31, 2013, the effective rate was 0.08% of the Fund’s average daily net assets, notwithstanding any fee waivers and/or expense reimbursements.

The Administrator waived Administration fees as outlined in Note 3.F.

JPMorgan Chase Bank, N.A. (“JPMCB”), a wholly-owned subsidiary of JPMorgan, serves as the Fund’s sub-administrator (the “Sub-administrator”). For its services as Sub-administrator, JPMCB receives a portion of the fees payable to the Administrator.

C. Distribution Fees — Pursuant to a Distribution Agreement, JPMorgan Distribution Services, Inc. (the “Distributor”), a wholly-owned subsidiary of JPMorgan, serves as the Trust’s exclusive underwriter and promotes and arranges for the sale of the Fund’s shares.

The Board of Trustees has adopted a Distribution Plan (the “Distribution Plan”) for Class A and Class C Shares of the Fund in accordance with Rule 12b-1 under the 1940 Act. The Distribution Plan provides that each Fund shall pay distribution fees, including payments to the Distributor, at annual rates of 0.25% and 0.75% of the average daily net assets of Class A and Class C Shares, respectively.

In addition, the Distributor is entitled to receive the front-end sales charges from purchases of Class A Shares and the CDSC from the redemptions of Class C Shares and certain Class A Shares for which front-end sales charges have been waived. For the year ended December 31, 2013, the Distributor retained the following amounts (in thousands):

| | | | | | | | |

| | | Front-End Sales Charges | | | CDSC | |

| | $ | — | (a) | | $ | — | |

| (a) | Amount rounds to less than $1,000. |

D. Shareholder Servicing Fees — The Trust, on behalf of the Fund, has entered into a Shareholder Servicing Agreement with the Distributor under which the Distributor provides certain support services to the shareholders. The Class R6 Shares do not participate in the Shareholder Servicing Agreement. For performing these services, the Distributor receives a fee that is accrued daily and paid monthly equal to a percentage of the average daily net assets as shown in the table below:

| | | | | | | | | | | | | | | | |

| | | Class A | | | Class C | | | Class R5 | | | Select Class | |

| | | 0.25 | % | | | 0.25 | % | | | 0.05 | % | | | 0.25 | % |

The Distributor has entered into shareholder services contracts with affiliated and unaffiliated financial intermediaries who provide shareholder services and other related services to their clients or customers who invest in the Fund under which the Distributor will pay all or a portion of such fees earned to financial intermediaries for performing such services.

The Distributor waived Shareholder Servicing fees as outlined in Note 3.F.

E. Custodian and Accounting Fees — JPMCB provides portfolio custody and accounting services to the Fund. The amounts paid directly to JPMCB by the Fund for custody and accounting services are included in Custodian and accounting fees in the Statement of Operations. Payments to the custodian may be reduced by credits earned by the Fund, based on uninvested cash balances held by the custodian. Such earnings credits, if any, are presented separately in the Statement of Operations.

Interest expense, if any, paid to the custodian related to cash overdrafts is included in Interest expense to affiliates in the Statement of Operations.

| | | | | | |

| | | |

| 20 | | | | J.P. MORGAN SPECIALTY FUNDS | | DECEMBER 31, 2013 |

F. Waivers and Reimbursements — The Adviser, Administrator and Distributor have contractually agreed to waive fees and/or reimburse the Fund to the extent that total annual operating expenses (excluding acquired fund fees and expenses, dividend expenses related to short sales, interest, taxes, expenses related to litigation and potential litigation, extraordinary expenses and expenses related to the Board of Trustees’ deferred compensation plan) exceed the percentages of the Fund’s respective average daily net assets as shown in the table below:

| | | | | | | | | | | | | | | | | | | | |

| | | Class A | | | Class C | | | Class R5 | | | Class R6 | | | Select Class | |

| | | 1.18 | % | | | 1.68 | % | | | 0.73 | % | | | 0.68 | % | | | 0.93 | % |

The expense limitation agreement was in effect for the year ended December 31, 2013. The contractual expense limitation percentages in the table above are in place until at least April 30, 2014.

For the year ended December 31, 2013, the Fund’s service providers waived fees and/or reimbursed expenses for the Fund as follows (amounts in thousands). None of these parties expect the Fund to repay any such waived fees and reimbursed expenses in future years.

| | | | | | | | | | | | | | | | |

| | | Contractual Waivers | | | | |

| | | Administration | | | Shareholder Servicing | | | Total | | | Contractual Reimbursements | |

| | $ | 41 | | | $ | — | | | $ | 41 | | | $ | 169 | |

Additionally, the Fund may invest in one or more money market funds advised by the Adviser or its affiliates. The Adviser, Administrator and Distributor, as shareholder servicing agent, waive fees in an amount sufficient to offset the respective fees each charges to the affiliated money market fund on the Fund’s investment in such affiliated money market fund. A portion of the waiver and/or reimbursement is voluntary.

The amount of waivers resulting from investments in these money market funds for the year ended December 31, 2013 was approximately $6,000.

G. Other — Certain officers of the Trust are affiliated with the Adviser, the Administrator and the Distributor. Such officers, with the exception of the Chief Compliance Officer, receive no compensation from the Fund for serving in their respective roles.

The Board of Trustees appointed a Chief Compliance Officer to the Fund in accordance with Federal securities regulations. The Fund, along with other affiliated funds, makes reimbursement payments, on a pro-rata basis, to the Administrator for a portion of the fees associated with the Office of the Chief Compliance Officer. Such fees are included in Trustees’ and Chief Compliance Officer’s fees in the Statement of Operations.

The Trust adopted a Trustee Deferred Compensation Plan (the “Plan”) which allows the Independent Trustees to defer the receipt of all or a portion of compensation related to performance of their duties as Trustees. The deferred fees are invested in various J.P. Morgan Funds until distribution in accordance with the Plan.

During the year ended December 31, 2013, the Fund may have purchased securities from an underwriting syndicate in which the principal underwriter or members of the syndicate are affiliated with the Adviser.

The Fund may use related party broker-dealers. For the year ended December 31, 2013, the Fund did not incur any brokerage commissions with broker-dealers affiliated with the Adviser.

The Securities and Exchange Commission (“SEC”) has granted an exemptive order permitting the Fund to engage in principal transactions with J.P. Morgan Securities, Inc., an affiliated broker, involving taxable money market instruments, subject to certain conditions.

4. Investment Transactions

During the year ended December 31, 2013, purchases and sales of investments (excluding short-term investments) were as follows (amounts in thousands):

| | | | | | | | |

| | | Purchases

(excluding U.S.

Government) | | | Sales

(excluding U.S.

Government) | |

| | $ | 68,619 | | | $ | 54,554 | |

During the year ended December 31, 2013, there were no purchases or sales of U.S. Government securities.

5. Federal Income Tax Matters

For Federal income tax purposes, the cost and unrealized appreciation (depreciation) in value of investment securities held at December 31, 2013 were as follows (amounts in thousands):

| | | | | | | | | | | | | | | | |

| | | Aggregate

Cost | | | Gross

Unrealized

Appreciation | | | Gross

Unrealized

Depreciation | | | Net Unrealized

Appreciation

(Depreciation) | |

| | $ | 57,565 | | | $ | 972 | | | $ | 2070 | | | $ | (1,098 | ) |

The difference between book and tax basis appreciation (depreciation) on investments is primarily attributed to wash sale loss deferrals.

| | | | | | | | |

| | | |

| DECEMBER 31, 2013 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 21 | |

NOTES TO FINANCIAL STATEMENTS

AS OF DECEMBER 31, 2013 (continued)

The tax character of distributions paid during the year ended December 31, 2013 was as follows (amounts in thousands):

| | | | | | | | | | | | | | | | |

| | | Ordinary Income | | | Net Long-Term Capital Gains | | | Return

of

Capital | | | Total Distributions Paid | |

| | $ | 1,577 | | | $ | 1,023 | | | $ | 53 | | | $ | 2,653 | |

The tax character of distributions paid during the year ended December 31, 2012 was as follows (amounts in thousands):

| | | | | | | | | | | | |

| | | Ordinary Income | | | Net Long-Term Capital Gains | | | Total Distributions Paid | |

| | $ | 1,351 | | | $ | 179 | | | $ | 1,530 | |

As of December 31, 2013, the components of net assets (excluding paid-in-capital) on a tax basis were as follows (amounts in thousands):

| | | | | | | | | | | | |

| | | Current Distributable Ordinary Income | | | Current Distributable Long-Term Capital Gain or (Tax Basis Capital Loss Carryover) | | | Unrealized Appreciation (Depreciation) | |

| | $ | — | | | $ | — | | | $ | (1,098 | ) |

The cumulative timing differences primarily consist of wash sale loss deferrals, Deferred REIT Dividends and post-October loss deferrals.

Under the Regulated Investment Company Modernization Act of 2010 (the “Act”), net capital losses recognized by the Fund are carried forward indefinitely, and retain their character as short-term and/or long-term losses.

As of December 31, 2013, the Fund did not have any post-enactment net capital loss carryforwards.

6. Borrowings