UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21295

JPMorgan Trust I

(Exact name of registrant as specified in charter)

270 Park Avenue

New York, NY 10017

(Address of principal executive offices) (Zip code)

Noah D. Greenhill, Esq.

270 Park Avenue

New York, NY 10017

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 480-4111

Date of fiscal year end: October 31

Date of reporting period: November 1, 2017 through October 31, 2018

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

Annual Report

J.P. Morgan Specialty Funds

October 31, 2018

JPMorgan Opportunistic Equity Long/Short Fund

JPMorgan Research Market Neutral Fund

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund’s website www.jpmorganfunds.com and you will be notified by mail each time a report is posted and provided with a website to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action.

You may elect to receive shareholder reports and other communications from the Fund electronically anytime by contacting your financial intermediary (such as a broker dealer, bank, or retirement plan) or, if you are a direct investor, by going to www.jpmorganfunds.com/edelivery.

You may elect to receive paper copies of all future reports free of charge. Contact your financial intermediary or, if you invest directly with the Fund, email us at funds.website.support@jpmorganfunds.com or call 1-800-480-4111. Your election to receive paper reports will apply to all funds held within your account(s).

CONTENTS

Investments in a Fund are not deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the FDIC, the Federal Reserve Board or any other government agency. You could lose money if you sell when a Fund’s share price is lower than when you invested.

Past performance is no guarantee of future performance. The general market views expressed in this report are opinions based on market and other conditions through the end of the reporting period and are subject to change without notice. These views are not intended to predict the future performance of a Fund or the securities markets. References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Such views are not meant as investment advice and may not be relied on as an indication of trading intent on behalf of any Fund.

Prospective investors should refer to the Funds’ prospectuses for a discussion of the Funds’ investment objectives, strategies and risks. Call J.P. Morgan Funds Service Center at 1-800-480-4111 for a prospectus containing more complete information about a Fund, including management fees and other expenses. Please read it carefully before investing.

CEO’S LETTER

November 30, 2018 (Unaudited)

Dear Shareholders,

While the global economic expansion continued, it also became less balanced as European economies slowed and several large emerging market nations struggled with rising interest rates, global trade tensions and/or political uncertainty.

| | |

| | “Record high corporate earnings and continued low inflation provided support for U.S. equity prices, but global financial markets experienced increased volatility throughout 2018 as equity and bond prices slumped in both developed and emerging markets.” |

U.S. growth largely outpaced other developed markets during the twelve months ended October 31, 2018 and the synchronized growth that characterized the global economy in 2017 had largely dissipated by the end of the period. Record high corporate earnings and continued low inflation provided support for U.S. equity prices, but global financial markets experienced increased volatility throughout 2018 as equity and bond prices slumped in both developed and emerging markets.

The current U.S. economic expansion became the second longest on record in May 2018 and in July 2018 entered its ninth year. Gross domestic product (GDP) in the U.S. rose an estimated 3.5% for the third quarter of 2018, following a strong showing of 4.2% growth in the second quarter. Already-low unemployment in the U.S. fell to 3.7% in the final two months of the reporting period — a level not seen since the late 1960s — and wage growth jumped 3.2% for production and nonsupervisory workers in October to its highest level since 2009. This helped drive U.S. consumer confidence to its highest levels in 18 years.

Against this backdrop, the U.S. Federal Reserve (the “Fed”) raised interest rates four times during the reporting period and indicated it would raise rates once more by the end of 2018. Importantly, inflation remained subdued throughout the reporting period, which allowed the Fed to provide investors with a relatively steady and predictable path toward higher interest rates.

Across Europe, economic growth slowed during the reporting period, pinched by trade tensions with the U.S. and political uncertainty within the European Union (EU). The 19-nation euro area’s GDP growth reached 2.7% in the fourth quarter of 2017, then slowed in subsequent quarters and fell to an estimated 1.6% in the third quarter of 2018. Unusually cold weather and labor unrest in France and Germany in early 2018 were initially blamed for slowing growth, but subsequent data pointed to a drop in export growth in the EU.

The impending U.K. “Brexit” from the EU — with or without a bilateral agreement — also weighed on investor and business

sentiment. While negotiations continued between the U.K. and the EU, disagreement over U.K. Prime Minister Theresa May’s draft agreement led to a rift within her Conservative Party subsequent to the end of the reporting period. The March 2018 election of a “euro-sceptic” populist government in Italy also added to uncertainty across Europe.

While rising global energy prices helped oil exporting nations, those emerging market nations that are most reliant on foreign debt financing were hurt by rising borrowing costs and a stronger U.S. dollar. Argentina, Brazil, Turkey, South Africa and Indonesia experienced weakness in their currencies as investors pulled capital out of those markets. While China’s economy continued to grow, policy curbs on domestic credit growth early in the reporting period and rising trade tariffs between China and the U.S. in the latter portion of the reporting period were believed to have weighed on China’s economy.

Overall, financial markets outside the U.S. suffered from increased volatility and capital outflows, particularly in the latter part of the reporting period. The MSCI Emerging Markets Index returned -12.2% and the MSCI EAFE Index of non-U.S. developed market equity returned -6.4%. The S&P 500 Index returned 7.35%. Bond markets also underperformed U.S. equity and the Bloomberg Barclays Emerging Markets Debt Index returned -3.39% and the Bloomberg Barclays U.S. Aggregate Index returned -2.05%.

In October 2018, the International Monetary Fund revised downward its forecast for global economic growth to 3.7% for both 2018 and 2019. The organization noted that as the global expansion has continued, the risks from rising trade barriers, higher borrowing costs, elevated petroleum prices and geo-political factors have increased while the potential for positive surprises has receded. Meanwhile, global unemployment continued to shrink through the end of October 2018 and corporate profits, particularly in the U.S., remained elevated.

We believe that among the best tools for navigating the current market environment are a well-diversified investment portfolio and a long term view. We look forward to managing your investment needs for years to come. Should you have any questions, please visit www.jpmorganfunds.com or contact the J.P. Morgan Funds Service Center at 1-800-480-4111.

Sincerely yours,

George C.W. Gatch

CEO, Global Funds Management

J.P. Morgan Asset Management

| | | | | | | | |

| | | |

| OCTOBER 31, 2018 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 1 | |

J.P. Morgan Specialty Funds

MARKET OVERVIEW

TWELVE MONTHS ENDED OCTOBER 31, 2018 (Unaudited)

U.S. equity markets outperformed other developed market equity as well as emerging markets equity during the reporting period. Record corporate profits, low unemployment rates and high levels of both consumer and business confidence helped propel U.S. equity prices higher. Globally, bond markets largely underperformed equity markets.

After reaching record highs in the final months of 2017, the S&P 500 Index closed in record high territory 14 times in January 2018. However, a sharp sell-off in both equity and bond markets in early February 2018 spread to other markets and helped lift market volatility from historic lows. While global equity and bond prices rebounded somewhat in subsequent months, it wasn’t until August 2018 that the S&P 500 Index returned to record highs. U.S. equity market volatility remained elevated in September and October 2018.

Meanwhile, economic growth in the European Union (EU) decelerated during the reporting period amid weakness in European exports and consumer confidence. Geo-political events, including a newly elected populist government in Italy and continued uncertainty over the final terms of a so-called Brexit agreement also weighed down equity and bond prices across the EU. Investor fears that the U.K. would leave the EU without an exit agreement also weighed on equity prices in London. For the reporting period, the MSCI EAFE Index returned -6.39%.

In emerging markets, a slowdown in credit growth in China and investor concerns about global trade tensions hurt equity prices. A stronger U.S. dollar and rising U.S. interest rates put further pressure on emerging markets, particularly those nations most reliant on foreign lending. For the reporting period, the MSCI Emerging Markets Index returned -12.19%, while the Bloomberg Barclays Emerging Markets Debt Index returned -3.39%.

For the twelve months ended October 31, 2018, the S&P 500 Index returned 7.35%, while the ICE BofAML 3-Month US Treasury Bill Index returned 1.68%.

| | | | | | |

| | | |

| 2 | | | | J.P. MORGAN SPECIALTY FUNDS | | OCTOBER 31, 2018 |

JPMorgan Opportunistic Equity Long/Short Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2018 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | | | |

| Fund (Class I Shares)* | | | 2.00% | |

| Standard & Poor’s 500 Index | | | 7.35% | |

| ICE BofAML 3-Month US Treasury Bill Index (formerly BofA Merrill Lynch U.S. 3-Month Treasury Bill Index) | | | 1.68% | |

| |

| Net Assets as of 10/31/2018 (In Thousands) | | $ | 262,093 | |

INVESTMENT OBJECTIVE**

The JPMorgan Opportunistic Equity Long/Short Fund (the “Fund”) seeks capital appreciation.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class I Shares underperformed the Standard & Poor’s 500 Index (the “Benchmark”) for the twelve months ended October 31, 2018.

The Fund’s long positions in the consumer discretionary and communication services sectors were leading detractors from performance relative to the Benchmark, while the Fund’s long positions and short positions within the health care sector were leading contributors to relative performance.

Leading individual detractors from relative performance included the Fund’s overweight long position in Melco Resorts and Entertainment Ltd. and its underweight long positions in Apple Inc. and Amazon.com Inc. Shares of Melco Resorts and Entertainment, a casino operator based in Hong Kong, fell after the company reported lower-than-expected earnings and revenue for the second quarter of 2018. Shares of Apple, a maker of smartphones and related devices that was not held in the Fund, rose amid continued earnings and revenue growth during the reporting period. Shares of Amazon.com, an Internet retailer, rose amid continued growth in sales and earnings.

Leading individual contributors to absolute performance included the Fund’s long positions in Northrop Grumman Corp.

and Cigna Corp. and its short position in Harley-Davidson Inc. Shares of Northrop Grumman, an aerospace and defense company, rose after the company reported better-than-expected earnings in the third quarter of 2018 and raised its profit forecast. Shares of Cigna, a health insurance provider, rose amid earnings growth and news about the company’s planned acquisition of Express Scripts Holding Co. Shares of Harley-Davidson, a motorcycle manufacturer, fell amid rising trade tariffs and a shrinking U.S. market for motorcycles.

HOW WAS THE FUND POSITIONED?

During the twelve months ended October 31, 2018, the Fund invested an average of 107% of its assets in long and short positions in equity securities, selecting from a universe of equity securities with market capitalizations similar to those included in the Russell 1000 Index and/or S&P 500 Index. The Fund’s manager sought to achieve lower volatility than the Benchmark through a disciplined research process, security selection and risk management. For the twelve month reporting period, the Fund’s average gross exposure was 107% and its average net exposure was 55%.

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| | | | | | | | |

| | | |

| OCTOBER 31, 2018 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 3 | |

JPMorgan Opportunistic Equity Long/Short Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2018 (Unaudited) (continued)

| | | | | | | | |

| TOP TEN LONG POSITIONS OF THE PORTFOLIO*** | |

| | 1. | | | Cigna Corp. | | | 8.9 | % |

| | 2. | | | Thermo Fisher Scientific, Inc. | | | 7.8 | |

| | 3. | | | UnitedHealth Group, Inc. | | | 7.1 | |

| | 4. | | | Express Scripts Holding Co. | | | 5.5 | |

| | 5. | | | Berkshire Hathaway, Inc., Class A | | | 4.3 | |

| | 6. | | | NextEra Energy, Inc. | | | 4.1 | |

| | 7. | | | Johnson & Johnson | | | 3.7 | |

| | 8. | | | Verizon Communications, Inc. | | | 3.7 | |

| | 9. | | | Altice USA, Inc., Class A | | | 3.2 | |

| | 10. | | | Berkshire Hathaway, Inc., Class B | | | 2.6 | |

| | | | | | | | |

| TOP TEN SHORT POSITIONS OF THE PORTFOLIO**** | |

| | 1. | | | Colgate-Palmolive Co. | | | 16.0 | % |

| | 2. | | | Illinois Tool Works, Inc. | | | 15.8 | |

| | 3. | | | Cummins, Inc. | | | 10.4 | |

| | 4. | | | Molson Coors Brewing Co., Class B | | | 9.3 | |

| | 5. | | | Schlumberger Ltd. | | | 7.0 | |

| | 6. | | | Sprint Corp. | | | 6.5 | |

| | 7. | | | Southern Co. (The) | | | 6.0 | |

| | 8. | | | Lam Research Corp. | | | 6.0 | |

| | 9. | | | Broadcom, Inc. | | | 5.8 | |

| | 10. | | | Kimberly-Clark Corp. | | | 4.3 | |

| | | | |

LONG POSITION PORTFOLIO COMPOSITION BY SECTOR*** | |

| Health Care | | | 33.0 | % |

| Communication Services | | | 11.6 | |

| Financials | | | 6.9 | |

| Information Technology | | | 4.5 | |

| Utilities | | | 4.1 | |

| Industrials | | | 1.0 | |

| Short-Term Investments | | | 38.9 | |

| | | | |

SHORT POSITION PORTFOLIO COMPOSITION BY SECTOR**** | |

| Materials | | | 3.1 | % |

| Communication Services | | | 6.5 | |

| Energy | | | 7.0 | |

| Utilities | | | 10.2 | |

| Information Technology | | | 14.4 | |

| Industrials | | | 29.2 | |

| Consumer Staples | | | 29.6 | |

| *** | | Percentages indicated are based on total long investments as of October 31, 2018. The Fund’s portfolio composition is subject to change. |

| **** | | Percentages indicated are based on total short investments as of October 31, 2018. The Fund’s portfolio composition is subject to change. |

| | | | | | |

| | | |

| 4 | | | | J.P. MORGAN SPECIALTY FUNDS | | OCTOBER 31, 2018 |

| | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF OCTOBER 31, 2018 | |

| | | |

| | | INCEPTION DATE OF

CLASS | | 1 YEAR | | | SINCE

INCEPTION | |

CLASS A SHARES | | August 29, 2014 | | | | | | | | |

With Sales Charge* | | | | | (3.62 | )% | | | 5.84 | % |

Without Sales Charge | | | | | 1.74 | | | | 7.22 | |

CLASS C SHARES | | August 29, 2014 | | | | | | | | |

With CDSC** | | | | | 0.21 | | | | 6.68 | |

Without CDSC | | | | | 1.21 | | | | 6.68 | |

CLASS I SHARES | | August 29, 2014 | | | 2.00 | | | | 7.48 | |

CLASS R2 SHARES | | August 29, 2014 | | | 1.48 | | | | 6.95 | |

CLASS R5 SHARES | | August 29, 2014 | | | 2.21 | | | | 7.70 | |

CLASS R6 SHARES | | August 29, 2014 | | | 2.26 | | | | 7.75 | |

| * | | Sales Charge for Class A Shares is 5.25%. |

| ** | | Assumes a 1% CDSC (contingent deferred sales charge) for the one year period and 0% CDSC thereafter. |

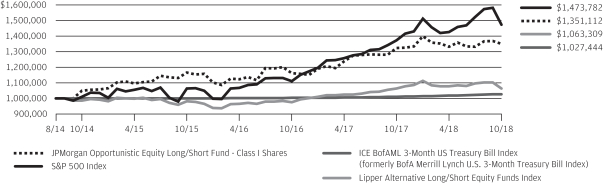

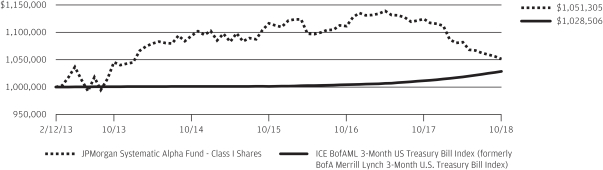

LIFE OF FUND PERFORMANCE (8/29/14 TO 10/31/18)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

The Fund commenced operations on August 29, 2014.

The graph illustrates comparative performance for $1,000,000 invested in Class I Shares of the JPMorgan Opportunistic Equity Long/Short Fund, the S&P 500 Index, the ICE BofAML 3-Month US Treasury Bill Index and Lipper Alternative Long/Short Equity Funds Index from August 29, 2014 to October 31, 2018. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the S&P 500 Index and ICE BofAML 3-Month US Treasury Bill Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of securities included in the benchmarks, if applicable. The performance of the Lipper Alternative Long/Short Equity Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The S&P 500 Index is an unmanaged index generally representative of the performance of large companies in the U.S. stock market. The ICE BofAML

3-Month US Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. Each month the index is rebalanced and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, 3 months from the rebalancing date. The Lipper Alternative Long/Short Equity Funds Index represents the total returns of the funds in the indicated category as defined by Lipper, Inc. Investors cannot invest directly in an index.

From the inception of the Fund through January 23, 2015, the Fund did not experience any shareholder activity. If such activity had occurred, the Fund’s performance may have been impacted.

Class I Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | | | |

| | | |

| OCTOBER 31, 2018 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 5 | |

JPMorgan Research Market Neutral Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2018 (Unaudited)

| | | | |

REPORTING PERIOD RETURN: | |

Fund (Class L Shares)* | | | 0.39% | |

ICE BofAML 3-Month US Treasury Bill Index (formerly BofA Merrill Lynch U.S. 3-Month Treasury Bill Index) | | | 1.68% | |

| |

Net Assets as of 10/31/2018 (In Thousands) | | $ | 185,205 | |

INVESTMENT OBJECTIVE**

The JPMorgan Research Market Neutral Fund (the “Fund”) seeks to provide long-term capital appreciation from a broadly diversified portfolio of U.S. stocks while neutralizing the general risks associated with stock market investing.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class L Shares underperformed the ICE BofAML 3-Month US Treasury Bill Index (the “Benchmark”) for the twelve months ended October 31, 2018.

The Fund’s security selection in the retail and basic materials sectors was a leading detractor from performance relative to the Benchmark, while the Fund’s security selection in the industrial cyclical and pharmaceutical/health care sectors was a leading contributor to relative performance.

Leading individual detractors from absolute performance included the Fund’s long position in Dollar Tree Inc. and its short positions in Boeing Co. and Chipotle Mexican Grill Inc. Shares of Dollar Tree, a discount variety store chain, fell after the company reported lower-than-expected first-quarter earnings and sales. Shares of Boeing, an aircraft manufacturer, rose after the company reported better-than-expected third-quarter earnings and raised its profit forecast amid strong demand. Shares of Chipotle Mexican Grill, a fast food chain, rose after the company reported sales growth for the third quarter.

Leading individual contributors to absolute performance included the Fund’s long positions in Union Pacific Corp. and

Norfolk Southern Corp. and its short position in General Electric Co. Shares of Union Pacific, a freight railroad operator, rose after the company unveiled share repurchase plan and news reports that the company would cut jobs to lower costs. Shares of Norfolk Southern, a freight railroad operator, rose after the company reported better-than-expected earnings for the third quarter. Shares of General Electric, an industrial conglomerate, fell after the company reported lower-than-expected results for several consecutive quarters and its credit rating was downgraded.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers aimed to construct a portfolio of long and short positions with a low correlation to the broader market for stocks and bonds. The Fund’s portfolio managers used fundamental research to estimate companies’ long-term earnings forecasts, ranking approximately 600 large and mid cap stocks into five quintiles. The Fund’s portfolio managers looked to the top two quintiles for potential long positions in stocks that they believed were undervalued and the bottom two quintiles for potential short positions in stocks that they believed were overvalued.

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| | | | | | |

| | | |

| 6 | | | | J.P. MORGAN SPECIALTY FUNDS | | OCTOBER 31, 2018 |

| | | | | | | | |

| TOP TEN LONG POSITIONS OF THE PORTFOLIO*** | |

| | 1. | | | Norfolk Southern Corp., (United States) | | | 3.0 | % |

| | 2. | | | Alphabet, Inc., Class C, (United States) | | | 2.9 | |

| | 3. | | | Union Pacific Corp., (United States) | | | 2.9 | |

| | 4. | | | Microsoft Corp., (United States) | | | 1.9 | |

| | 5. | | | NVIDIA Corp., (United States) | | | 1.9 | |

| | 6. | | | Amazon.com, Inc., (United States) | | | 1.7 | |

| | 7. | | | NextEra Energy, Inc., (United States) | | | 1.7 | |

| | 8. | | | Cigna Corp., (United States) | | | 1.7 | |

| | 9. | | | UnitedHealth Group, Inc., (United States) | | | 1.6 | |

| | 10. | | | Mondelez International, Inc., Class A, (United States) | | | 1.5 | |

| | | | | | | | |

| TOP TEN SHORT POSITIONS OF THE PORTFOLIO**** | |

| | 1. | | | Southern Co. (The), (United States) | | | 2.3 | % |

| | 2. | | | Schlumberger Ltd., (United States) | | | 2.0 | |

| | 3. | | | Chipotle Mexican Grill, Inc., (United States) | | | 1.7 | |

| | 4. | | | United Parcel Service, Inc., Class B, (United States) | | | 1.6 | |

| | 5. | | | Omnicom Group, Inc., (United States) | | | 1.6 | |

| | 6. | | | General Mills, Inc., (United States) | | | 1.6 | |

| | 7. | | | Heartland Express, Inc., (United States) | | | 1.6 | |

| | 8. | | | Exxon Mobil Corp., (United States) | | | 1.6 | |

| | 9. | | | Dominion Energy, Inc., (United States) | | | 1.5 | |

| | 10. | | | Canadian National Railway Co., (Canada) | | | 1.5 | |

| | | | |

LONG POSITION PORTFOLIO COMPOSITION BY SECTOR*** | |

Information Technology | | | 13.9 | % |

Industrials | | | 12.1 | |

Consumer Discretionary | | | 11.4 | |

Health Care | | | 8.7 | |

Financials | | | 8.3 | |

Communication Services | | | 7.5 | |

Energy | | | 7.2 | |

Utilities | | | 6.5 | |

Consumer Staples | | | 5.9 | |

Materials | | | 3.0 | |

Real Estate | | | 2.7 | |

Short-Term Investments | | | 12.8 | |

| | | | |

SHORT POSITION PORTFOLIO COMPOSITION BY SECTOR**** | |

Industrials | | | 14.7 | % |

Consumer Discretionary | | | 12.5 | |

Information Technology | | | 12.2 | |

Financials | | | 10.4 | |

Health Care | | | 9.1 | |

Energy | | | 8.9 | |

Communication Services | | | 7.9 | |

Utilities | | | 7.8 | |

Consumer Staples | | | 7.7 | |

Real Estate | | | 4.8 | |

Materials | | | 4.0 | |

| *** | | Percentages indicated are based on total long investments as of October 31, 2018. The Fund’s portfolio composition is subject to change. |

| **** | | Percentages indicated are based on total short investments as of October 31, 2018. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| OCTOBER 31, 2018 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 7 | |

JPMorgan Research Market Neutral Fund

FUND COMMENTARY

TWELVE MONTHS ENDED OCTOBER 31, 2018 (Unaudited) (continued)

| | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF OCTOBER 31, 2018 | |

| | | | |

| | | INCEPTION DATE OF

CLASS | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | | February 28, 2002 | | | | | | | | | | | | | |

With Sales Charge* | | | | | | | (5.23 | )% | | | (0.41 | )% | | | 0.35 | % |

Without Sales Charge | | | | | | | (0.01 | ) | | | 0.67 | | | | 0.89 | |

CLASS C SHARES | | | November 2, 2009 | | | | | | | | | | | | | |

With CDSC** | | | | | | | (1.53 | ) | | | 0.15 | | | | 0.38 | |

Without CDSC | | | | | | | (0.53 | ) | | | 0.15 | | | | 0.38 | |

CLASS I SHARES | | | November 2, 2009 | | | | 0.20 | | | | 0.92 | | | | 1.17 | |

CLASS L SHARES | | | December 31, 1998 | | | | 0.39 | | | | 1.11 | | | | 1.36 | |

| * | | Sales Charge for Class A Shares is 5.25%. |

| ** | | Assumes a 1% CDSC (contingent deferred sales charge) for the one year period and 0% CDSC thereafter. |

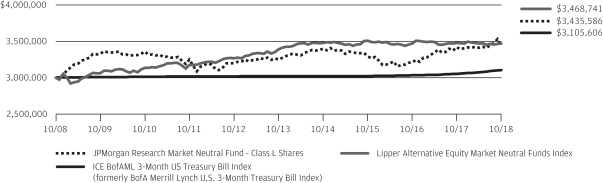

TEN YEAR FUND PERFORMANCE (10/31/08 TO 10/31/18)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class I Shares prior to its inception date are based on the performance of Class L Shares. The actual returns for Class I Shares would have been lower than shown because Class I Shares have higher expenses than Class L Shares.

Returns for Class C Shares prior to its inception date are based on the performance of Class B Shares, all of which converted to Class A Shares on June 19, 2015. The actual returns of Class C Shares would have been similar to those shown because Class C Shares have similar expenses to Class B Shares.

The graph illustrates comparative performance for $3,000,000 invested in Class L Shares of the JPMorgan Research Market Neutral Fund, ICE BofAML 3-Month US Treasury Bill Index and Lipper Alternative Equity Market Neutral Funds Index from October 31, 2008 to October 31, 2018. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the ICE BofAML 3-Month US Treasury Bill Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect

reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper Alternative Equity Market Neutral Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The ICE BofAML 3-Month US Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. Each month the index is rebalanced and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, 3 months from the rebalancing date. Investors cannot invest directly in an index. The Lipper Alternative Equity Market Neutral Funds Index is an average based on the total returns of all mutual funds within the Fund’s designated category as determined by Lipper, Inc.

Class L Shares have a $3,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 8 | | | | J.P. MORGAN SPECIALTY FUNDS | | OCTOBER 31, 2018 |

JPMorgan Opportunistic Equity Long/Short Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF OCTOBER 31, 2018

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Long Positions — 108.4% | | | | | |

Common Stocks — 66.2% | | | | | |

Diversified Financial Services — 7.5% | | | | | |

Berkshire Hathaway, Inc., Class A * | | | — | (a) | | | 12,308 | |

Berkshire Hathaway, Inc., Class B * | | | 36 | | | | 7,328 | |

| | | | | | | | |

| | | | | | | 19,636 | |

| | | | | | | | |

Diversified Telecommunication Services — 4.0% | | | | | |

Verizon Communications, Inc. (b) | | | 184 | | | | 10,531 | |

| | | | | | | | |

Electric Utilities — 4.4% | |

NextEra Energy, Inc. (b) | | | 68 | | | | 11,696 | |

| | | | | | | | |

Health Care Providers & Services — 23.3% | |

Cigna Corp. | | | 118 | | | | 25,224 | |

Express Scripts Holding Co. * | | | 162 | | | | 15,699 | |

UnitedHealth Group, Inc. (b) | | | 77 | | | | 20,089 | |

| | | | | | | | |

| | | | | | | 61,012 | |

| | | | | | | | |

Interactive Media & Services — 1.6% | |

Alphabet, Inc., Class A * | | | 4 | | | | 4,205 | |

| | | | | | | | |

IT Services — 3.4% | |

Fiserv, Inc. * (b) | | | 87 | | | | 6,915 | |

Mastercard, Inc., Class A (b) | | | 3 | | | | 641 | |

PayPal Holdings, Inc. * | | | 8 | | | | 665 | |

Visa, Inc., Class A (b) | | | 5 | | | | 659 | |

| | | | | | | | |

| | | | | | | 8,880 | |

| | | | | | | | |

Life Sciences Tools & Services — 8.5% | |

Thermo Fisher Scientific, Inc. (b) | | | 95 | | | | 22,276 | |

| | | | | | | | |

Media — 5.8% | |

Altice USA, Inc., Class A | | | 550 | | | | 8,977 | |

Discovery, Inc., Class A * | | | 191 | | | | 6,187 | |

| | | | | | | | |

| | | | | | | 15,164 | |

| | | | | | | | |

Pharmaceuticals — 4.0% | |

Johnson & Johnson (b) | | | 75 | | | | 10,562 | |

| | | | | | | | |

Road & Rail — 1.0% | |

Union Pacific Corp. (b) | | | 18 | | | | 2,704 | |

| | | | | | | | |

Software — 1.5% | |

Microsoft Corp. (b) | | | 37 | | | | 3,925 | |

| | | | | | | | |

Wireless Telecommunication Services — 1.2% | |

T-Mobile US, Inc. * | | | 45 | | | | 3,070 | |

| | | | | | | | |

Total Common Stocks

(Cost $158,051) | | | | 173,661 | |

| | | | | |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Short-Term Investments — 42.2% | | | | | |

Investment Companies — 42.2% | | | | | | | | |

JPMorgan U.S. Government Money Market Fund Class Institutional Shares, 2.02% (c) (d)

(Cost $110,482) | | | 110,482 | | | | 110,482 | |

| | | | | | | | |

Total Long Positions

(Cost $268,533) | | | | | | | 284,143 | |

| | | | | |

Short Positions — (17.0)% | | | | | |

Common Stocks — (17.0)% | | | | | |

Aerospace & Defense — (0.5)% | |

Raytheon Co. | | | (8 | ) | | | (1,320 | ) |

| | | | | | | | |

Beverages — (1.6)% | |

Molson Coors Brewing Co., Class B | | | (65 | ) | | | (4,163 | ) |

| | | | | | | | |

Chemicals — (0.5)% | |

Albemarle Corp. | | | (14 | ) | | | (1,384 | ) |

| | | | | | | | |

Electric Utilities — (1.0)% | |

Southern Co. (The) | | | (60 | ) | | | (2,679 | ) |

| | | | | | | | |

Energy Equipment & Services — (1.2)% | |

Schlumberger Ltd. | | | (60 | ) | | | (3,099 | ) |

| | | | | | | | |

Household Products — (3.4)% | |

Colgate-Palmolive Co. | | | (119 | ) | | | (7,104 | ) |

Kimberly-Clark Corp. | | | (18 | ) | | | (1,893 | ) |

| | | | | | | | |

| | | | | | | (8,997 | ) |

| | | | | | | | |

Machinery — (4.5)% | |

Cummins, Inc. | | | (34 | ) | | | (4,647 | ) |

Illinois Tool Works, Inc. | | | (55 | ) | | | (7,037 | ) |

| | | | | | | | |

| | | | | | | (11,684 | ) |

| | | | | | | | |

Multi-Utilities — (0.7)% | |

Consolidated Edison, Inc. | | | (21 | ) | | | (1,610 | ) |

Dominion Energy, Inc. | | | (4 | ) | | | (265 | ) |

| | | | | | | | |

| | | | | | | (1,875 | ) |

| | | | | | | | |

Semiconductors & Semiconductor Equipment — (2.5)% | |

Broadcom, Inc. | | | (12 | ) | | | (2,597 | ) |

Lam Research Corp. | | | (19 | ) | | | (2,657 | ) |

Micron Technology, Inc. * | | | (21 | ) | | | (793 | ) |

Texas Instruments, Inc. | | | (4 | ) | | | (372 | ) |

| | | | | | | | |

| | | | | | | (6,419 | ) |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| OCTOBER 31, 2018 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 9 | |

JPMorgan Opportunistic Equity Long/Short Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF OCTOBER 31, 2018 (continued)

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Short Positions — continued | | | | | |

Common Stocks — continued | | | | | |

Wireless Telecommunication Services — (1.1)% | |

Sprint Corp. * | | | (475 | ) | | | (2,910 | ) |

| | | | | | | | |

Total Common Stocks

(Proceeds $(46,461)) | | | | (44,530 | ) |

| | | | | |

Total Short Positions

(Proceeds $(46,461)) | | | | (44,530 | ) |

| | | | | |

Total Investments — 91.4%

(Cost $222,072) | | | | 239,613 | |

Other Assets Less Liabilities — 8.6% | | | | 22,480 | |

| | | | | |

Net Assets — 100.0% | | | | 262,093 | |

| | | | | |

Percentages indicated are based on net assets.

| | |

| (a) | | Amount rounds to less than one thousand. |

| (b) | | All or a portion of this security is segregated as collateral for short sales. The total value of securities and cash segregated as collateral is approximately $43,392,000 and $80,967,000, respectively. |

| (c) | | Investment in affiliate. Fund is registered under the Investment Company Act of 1940, as amended, and advised by J.P. Morgan Investment Management Inc. |

| (d) | | The rate shown is the current yield as of October 31, 2018. |

| * | | Non-income producing security. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 10 | | | | J.P. MORGAN SPECIALTY FUNDS | | OCTOBER 31, 2018 |

JPMorgan Research Market Neutral Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF OCTOBER 31, 2018

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Long Positions — 97.8% | |

Common Stocks — 85.3% | |

Aerospace & Defense — 2.0% | |

General Dynamics Corp. | | | 15 | | | | 2,577 | |

Northrop Grumman Corp. | | | 2 | | | | 444 | |

United Technologies Corp. | | | 5 | | | | 617 | |

| | | | | | | | |

| | | | | | | 3,638 | |

| | | | | | | | |

Airlines — 0.3% | |

Delta Air Lines, Inc. (a) | | | 12 | | | | 642 | |

| | | | | | | | |

Auto Components — 0.5% | |

Aptiv plc | | | 6 | | | | 427 | |

BorgWarner, Inc. | | | 11 | | | | 451 | |

| | | | | | | | |

| | | | | | | 878 | |

| | | | | | | | |

Banks — 3.3% | |

Bank of America Corp. (a) | | | 56 | | | | 1,540 | |

Citigroup, Inc. | | | 6 | | | | 368 | |

Comerica, Inc. | | | 4 | | | | 312 | |

KeyCorp | | | 59 | | | | 1,068 | |

Regions Financial Corp. | | | 40 | | | | 680 | |

SunTrust Banks, Inc. | | | 11 | | | | 717 | |

SVB Financial Group * | | | 6 | | | | 1,402 | |

| | | | | | | | |

| | | | | | | 6,087 | |

| | | | | | | | |

Beverages — 0.7% | |

Coca-Cola Co. (The) | | | 17 | | | | 810 | |

PepsiCo, Inc. | | | 5 | | | | 545 | |

| | | | | | | | |

| | | | | | | 1,355 | |

| | | | | | | | |

Biotechnology — 0.9% | |

Alexion Pharmaceuticals, Inc. * | | | 5 | | | | 513 | |

Biogen, Inc. * | | | 1 | | | | 310 | |

Vertex Pharmaceuticals, Inc. * | | | 5 | | | | 912 | |

| | | | | | | | |

| | | | | | | 1,735 | |

| | | | | | | | |

Capital Markets — 2.6% | |

Ameriprise Financial, Inc. | | | 5 | | | | 579 | |

CME Group, Inc. | | | 12 | | | | 2,263 | |

Morgan Stanley (a) | | | 29 | | | | 1,331 | |

S&P Global, Inc. | | | 3 | | | | 553 | |

| | | | | | | | |

| | | | | | | 4,726 | |

| | | | | | | | |

Chemicals — 1.7% | |

Celanese Corp. | | | 11 | | | | 1,040 | |

DowDuPont, Inc. (a) | | | 11 | | | | 571 | |

Eastman Chemical Co. | | | 19 | | | | 1,508 | |

| | | | | | | | |

| | | | | | | 3,119 | |

| | | | | | | | |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

| |

| |

Consumer Finance — 0.4% | |

American Express Co. | | | 8 | | | | 822 | |

| | | | | | | | |

Containers & Packaging — 1.3% | |

Avery Dennison Corp. | | | 12 | | | | 1,058 | |

Crown Holdings, Inc. * | | | 13 | | | | 551 | |

Packaging Corp. of America | | | 7 | | | | 652 | |

WestRock Co. | | | 2 | | | | 105 | |

| | | | | | | | |

| | | | | | | 2,366 | |

| | | | | | | | |

Diversified Telecommunication Services — 0.6% | |

Verizon Communications, Inc. | | | 19 | | | | 1,084 | |

| | | | | | | | |

Electric Utilities — 4.0% | |

Evergy, Inc. | | | 26 | | | | 1,460 | |

Exelon Corp. | | | 41 | | | | 1,782 | |

NextEra Energy, Inc. (a) | | | 18 | | | | 3,128 | |

Xcel Energy, Inc. (a) | | | 22 | | | | 1,080 | |

| | | | | | | | |

| | | | | | | 7,450 | |

| | | | | | | | |

Electrical Equipment — 0.2% | |

Eaton Corp. plc (a) | | | 6 | | | | 409 | |

| | | | | | | | |

Electronic Equipment, Instruments & Components — 0.0% (b) | |

Resideo Technologies, Inc. * | | | — | (c) | | | — | (c) |

| | | | | | | | |

Entertainment — 2.1% | |

Electronic Arts, Inc. * | | | 18 | | | | 1,679 | |

Twenty-First Century Fox, Inc., Class A | | | 35 | | | | 1,576 | |

Walt Disney Co. (The) (a) | | | 6 | | | | 711 | |

| | | | | | | | |

| | | | | | | 3,966 | |

| | | | | | | | |

Equity Real Estate Investment Trusts (REITs) — 2.6% | |

AvalonBay Communities, Inc. | | | 7 | | | | 1,140 | |

Brixmor Property Group, Inc. | | | 19 | | | | 305 | |

Federal Realty Investment Trust | | | 2 | | | | 273 | |

Host Hotels & Resorts, Inc. | | | 14 | | | | 274 | |

Prologis, Inc. | | | 20 | | | | 1,282 | |

Ventas, Inc. | | | 19 | | | | 1,088 | |

Vornado Realty Trust (a) | | | 8 | | | | 549 | |

| | | | | | | | |

| | | | | | | 4,911 | |

| | | | | | | | |

Food & Staples Retailing — 0.4% | |

Costco Wholesale Corp. | | | 3 | | | | 728 | |

| | | | | | | | |

Food Products — 2.1% | |

Conagra Brands, Inc. | | | 25 | | | | 906 | |

Mondelez International, Inc., Class A | | | 65 | | | | 2,710 | |

Post Holdings, Inc. * (a) | | | 2 | | | | 209 | |

| | | | | | | | |

| | | | | | | 3,825 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| OCTOBER 31, 2018 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 11 | |

JPMorgan Research Market Neutral Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF OCTOBER 31, 2018 (continued)

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Long Positions — continued | |

Common Stocks — continued | |

Health Care Equipment & Supplies — 2.3% | |

Boston Scientific Corp. * | | | 60 | | | | 2,161 | |

Medtronic plc | | | 2 | | | | 189 | |

Zimmer Biomet Holdings, Inc. | | | 17 | | | | 1,877 | |

| | | | | | | | |

| | | | | | | 4,227 | |

| | | | | | | | |

Health Care Providers & Services — 3.7% | |

Anthem, Inc. | | | 3 | | | | 945 | |

Cigna Corp. (a) | | | 14 | | | | 3,045 | |

UnitedHealth Group, Inc. (a) | | | 11 | | | | 2,848 | |

| | | | | | | | |

| | | | | | | 6,838 | |

| | | | | | | | |

Hotels, Restaurants & Leisure — 1.8% | |

Hilton Worldwide Holdings, Inc. | | | 18 | | | | 1,278 | |

Royal Caribbean Cruises Ltd. | | | 6 | | | | 677 | |

Yum! Brands, Inc. | | | 16 | | | | 1,404 | |

| | | | | | | | |

| | | | | | | 3,359 | |

| | | | | | | | |

Household Durables — 0.2% | |

MDC Holdings, Inc. | | | 15 | | | | 417 | |

| | | | | | | | |

Household Products — 0.5% | |

Energizer Holdings, Inc. | | | 14 | | | | 851 | |

| | | | | | | | |

Industrial Conglomerates — 0.9% | |

Honeywell International, Inc. | | | 12 | | | | 1,732 | |

| | | | | | | | |

Insurance — 1.8% | |

Allstate Corp. (The) | | | 15 | | | | 1,409 | |

Arthur J Gallagher & Co. | | | 6 | | | | 447 | |

Axis Capital Holdings Ltd. | | | 9 | | | | 529 | |

Principal Financial Group, Inc. | | | 9 | | | | 405 | |

Willis Towers Watson plc | | | 4 | | | | 528 | |

| | | | | | | | |

| | | | | | | 3,318 | |

| | | | | | | | |

Interactive Media & Services — 2.8% | |

Alphabet, Inc., Class C * (a) | | | 5 | | | | 5,247 | |

| | | | | | | | |

Internet & Direct Marketing Retail — 2.6% | |

Amazon.com, Inc. * | | | 2 | | | | 3,162 | |

Booking Holdings, Inc. * | | | — | (c) | | | 690 | |

Expedia Group, Inc. | | | 7 | | | | 913 | |

| | | | | | | | |

| | | | | | | 4,765 | |

| | | | | | | | |

IT Services — 4.7% | |

Anaplan, Inc. * | | | 36 | | | | 828 | |

Automatic Data Processing, Inc. | | | 15 | | | | 2,127 | |

Fidelity National Information Services, Inc. | | | 6 | | | | 574 | |

First Data Corp., Class A * | | | 14 | | | | 262 | |

Fiserv, Inc. * | | | 5 | | | | 366 | |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

| |

| |

IT Services — continued | |

Mastercard, Inc., Class A | | | 6 | | | | 1,223 | |

PayPal Holdings, Inc. * | | | 3 | | | | 255 | |

Visa, Inc., Class A | | | 8 | | | | 1,094 | |

WEX, Inc. * (a) | | | 5 | | | | 903 | |

Worldpay, Inc. * | | | 11 | | | | 1,028 | |

| | | | | | | | |

| | | | | | | 8,660 | |

| | | | | | | | |

Machinery — 1.5% | |

Ingersoll-Rand plc | | | 18 | | | | 1,775 | |

Stanley Black & Decker, Inc. (a) | | | 9 | | | | 1,071 | |

| | | | | | | | |

| | | | | | | 2,846 | |

| | | | | | | | |

Media — 1.0% | |

Charter Communications, Inc., Class A * | | | 4 | | | | 1,132 | |

Discovery, Inc., Class A * | | | 25 | | | | 799 | |

| | | | | | | | |

| | | | | | | 1,931 | |

| | | | | | | | |

Multiline Retail — 1.0% | |

Dollar General Corp. | | | 5 | | | | 559 | |

Dollar Tree, Inc. * | | | 16 | | | | 1,354 | |

| | | | | | | | |

| | | | | | | 1,913 | |

| | | | | | | | |

Multi-Utilities — 2.3% | |

Ameren Corp. | | | 13 | | | | 815 | |

NiSource, Inc. | | | 7 | | | | 173 | |

Public Service Enterprise Group, Inc. | | | 22 | | | | 1,166 | |

Sempra Energy | | | 12 | | | | 1,371 | |

WEC Energy Group, Inc. | | | 12 | | | | 817 | |

| | | | | | | | |

| | | | | | | 4,342 | |

| | | | | | | | |

Oil, Gas & Consumable Fuels — 7.0% | |

Chevron Corp. | | | 5 | | | | 512 | |

Cimarex Energy Co. | | | 3 | | | | 248 | |

Concho Resources, Inc. * | | | 3 | | | | 440 | |

Diamondback Energy, Inc. | | | 11 | | | | 1,277 | |

EOG Resources, Inc. | | | 23 | | | | 2,399 | |

Marathon Petroleum Corp. | | | 30 | | | | 2,143 | |

Occidental Petroleum Corp. (a) | | | 30 | | | | 2,036 | |

ONEOK, Inc. | | | 13 | | | | 854 | |

Parsley Energy, Inc., Class A * | | | 26 | | | | 618 | |

Pioneer Natural Resources Co. (a) | | | 17 | | | | 2,514 | |

| | | | | | | | |

| | | | | | | 13,041 | |

| | | | | | | | |

Pharmaceuticals — 1.6% | |

Eli Lilly & Co. | | | 6 | | | | 664 | |

Merck & Co., Inc. | | | 8 | | | | 607 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 12 | | | | J.P. MORGAN SPECIALTY FUNDS | | OCTOBER 31, 2018 |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Long Positions — continued | | | | | | | | |

Common Stocks — continued | | | | | | | | |

Pharmaceuticals — continued | | | | | | | | |

Pfizer, Inc. | | | 38 | | | | 1,631 | |

| | | | | | | | |

| | | | | | | 2,902 | |

| | | | | | | | |

Professional Services — 0.3% | |

TransUnion | | | 7 | | | | 490 | |

| | | | | | | | |

Road & Rail — 6.6% | |

Canadian Pacific Railway Ltd. (Canada) | | | 7 | | | | 1,523 | |

Norfolk Southern Corp. (a) | | | 32 | | | | 5,439 | |

Union Pacific Corp. (a) | | | 35 | | | | 5,185 | |

| | | | | | | | |

| | | | | | | 12,147 | |

| | | | | | | | |

Semiconductors & Semiconductor Equipment — 5.2% | |

Analog Devices, Inc. | | | 15 | | | | 1,215 | |

Broadcom, Inc. | | | 6 | | | | 1,413 | |

NVIDIA Corp. | | | 16 | | | | 3,354 | |

NXP Semiconductors NV (Netherlands) | | | 13 | | | | 996 | |

ON Semiconductor Corp. * | | | 33 | | | | 569 | |

Texas Instruments, Inc. (a) | | | 22 | | | | 2,020 | |

| | | | | | | | |

| | | | | | | 9,567 | |

| | | | | | | | |

Software — 3.8% | |

Adobe, Inc. * | | | 3 | | | | 628 | |

Microsoft Corp. (a) | | | 32 | | | | 3,465 | |

salesforce.com, Inc. * | | | 17 | | | | 2,367 | |

ServiceNow, Inc. * | | | 3 | | | | 565 | |

| | | | | | | | |

| | | | | | | 7,025 | |

| | | | | | | | |

Specialty Retail — 4.4% | |

Advance Auto Parts, Inc. | | | 2 | | | | 387 | |

AutoZone, Inc. * | | | 2 | | | | 1,231 | |

Best Buy Co., Inc. | | | 6 | | | | 439 | |

Lowe’s Cos., Inc. | | | 12 | | | | 1,187 | |

O’Reilly Automotive, Inc. * | | | 7 | | | | 2,239 | |

Ross Stores, Inc. | | | 19 | | | | 1,883 | |

TJX Cos., Inc. (The) | | | 7 | | | | 759 | |

| | | | | | | | |

| | | | | | | 8,125 | |

| | | | | | | | |

Textiles, Apparel & Luxury Goods — 0.7% | |

PVH Corp. | | | 10 | | | | 1,249 | |

| | | | | | | | |

Tobacco — 2.1% | |

Altria Group, Inc. | | | 28 | | | | 1,811 | |

Philip Morris International, Inc. | | | 24 | | | | 2,130 | |

| | | | | | | | |

| | | | | | | 3,941 | |

| | | | | | | | |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

| | | | | | | | |

| | | | | | | | |

Wireless Telecommunication Services — 0.8% | |

T-Mobile US, Inc. * | | | 21 | | | | 1,408 | |

| | | | | | | | |

Total Common Stocks

(Cost $131,855) | | | | 158,082 | |

| | | | | |

Short-Term Investments — 12.5% | |

Investment Companies — 12.4% | |

JPMorgan Prime Money Market Fund Class Institutional Shares, 2.25% (d) (e)

(Cost $22,863) | | | 22,862 | | | | 22,866 | |

| | | | | | | | |

| | |

| | | PRINCIPAL

AMOUNT

(000) | | | | |

U.S. Treasury Obligations — 0.1% | |

U.S. Treasury Bills 2.00%, 1/31/2019 (f) (g)

(Cost $232) | | | 233 | | | | 232 | |

| | | | | | | | |

Total Short-Term Investments

(Cost $23,095) | | | | | | | 23,098 | |

| | | | | | | | |

Total Long Positions

(Cost $154,950) | | | | 181,180 | |

| | | | | |

| | |

| | | SHARES

(000) | | | | |

Short Positions — (84.8)% | |

Common Stocks — (84.8)% | |

Aerospace & Defense — (1.8)% | |

Boeing Co. (The) | | | (1 | ) | | | (446 | ) |

Huntington Ingalls Industries, Inc. | | | (3 | ) | | | (565 | ) |

Lockheed Martin Corp. | | | (4 | ) | | | (1,183 | ) |

Raytheon Co. | | | (4 | ) | | | (707 | ) |

Textron, Inc. | | | (9 | ) | | | (481 | ) |

| | | | | | | | |

| | | | | | | (3,382 | ) |

| | | | | | | | |

Air Freight & Logistics — (1.9)% | |

CH Robinson Worldwide, Inc. | | | (5 | ) | | | (485 | ) |

Expeditors International of Washington, Inc. | | | (6 | ) | | | (412 | ) |

United Parcel Service, Inc., Class B | | | (24 | ) | | | (2,555 | ) |

| | | | | | | | |

| | | | | | | (3,452 | ) |

| | | | | | | | |

Auto Components — (0.2)% | |

Autoliv, Inc. (Sweden) | | | (3 | ) | | | (273 | ) |

Veoneer, Inc. (Sweden) * | | | (3 | ) | | | (110 | ) |

| | | | | | | | |

| | | | | | | (383 | ) |

| | | | | | | | |

Automobiles — (1.5)% | |

General Motors Co. | | | (34 | ) | | | (1,240 | ) |

Harley-Davidson, Inc. | | | (11 | ) | | | (409 | ) |

Tesla, Inc. * | | | (3 | ) | | | (1,119 | ) |

| | | | | | | | |

| | | | | | | (2,768 | ) |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| OCTOBER 31, 2018 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 13 | |

JPMorgan Research Market Neutral Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF OCTOBER 31, 2018 (continued)

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Short Positions — continued | | | | | | | | |

Common Stocks — continued | | | | | | | | |

Banks — (3.5)% | |

Associated Banc-Corp. | | | (61 | ) | | | (1,405 | ) |

BancorpSouth Bank | | | (31 | ) | | | (887 | ) |

Bank of Hawaii Corp. | | | (15 | ) | | | (1,191 | ) |

Commerce Bancshares, Inc. | | | (4 | ) | | | (223 | ) |

First Hawaiian, Inc. | | | (35 | ) | | | (861 | ) |

People’s United Financial, Inc. | | | (57 | ) | | | (896 | ) |

PNC Financial Services Group, Inc. (The) | | | (8 | ) | | | (1,041 | ) |

| | | | | | | | |

| | | | | | | (6,504 | ) |

| | | | | | | | |

Beverages — (0.7)% | |

Brown-Forman Corp., Class B | | | (29 | ) | | | (1,356 | ) |

| | | | | | | | |

Biotechnology — (2.0)% | |

AbbVie, Inc. | | | (24 | ) | | | (1,900 | ) |

Amgen, Inc. | | | (10 | ) | | | (1,832 | ) |

| | | | | | | | |

| | | | | | | (3,732 | ) |

| | | | | | | | |

Building Products — (0.5)% | |

Johnson Controls International plc | | | (30 | ) | | | (949 | ) |

| | | | | | | | |

Capital Markets — (2.9)% | |

FactSet Research Systems, Inc. | | | (3 | ) | | | (624 | ) |

Federated Investors, Inc., Class B | | | (23 | ) | | | (579 | ) |

Goldman Sachs Group, Inc. (The) | | | (2 | ) | | | (384 | ) |

Invesco Ltd. | | | (51 | ) | | | (1,115 | ) |

Legg Mason, Inc. | | | (19 | ) | | | (541 | ) |

Moody’s Corp. | | | (1 | ) | | | (174 | ) |

Nasdaq, Inc. | | | (4 | ) | | | (384 | ) |

Northern Trust Corp. | | | (5 | ) | | | (505 | ) |

State Street Corp. | | | (3 | ) | | | (223 | ) |

Waddell & Reed Financial, Inc., Class A | | | (47 | ) | | | (897 | ) |

| | | | | | | | |

| | | | | | | (5,426 | ) |

| | | | | | | | |

Chemicals — (2.2)% | |

Albemarle Corp. | | | (18 | ) | | | (1,736 | ) |

LyondellBasell Industries NV, Class A | | | (14 | ) | | | (1,293 | ) |

PPG Industries, Inc. | | | (11 | ) | | | (1,106 | ) |

| | | | | | | | |

| | | | | | | (4,135 | ) |

| | | | | | | | |

Communications Equipment — (1.3)% | |

Cisco Systems, Inc. | | | (33 | ) | | | (1,526 | ) |

Juniper Networks, Inc. | | | (33 | ) | | | (967 | ) |

| | | | | | | | |

| | | | | | | (2,493 | ) |

| | | | | | | | |

Consumer Finance — (0.5)% | |

Synchrony Financial | | | (33 | ) | | | (953 | ) |

| | | | | | | | |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

| | | | | | | | |

| | | | | | | | |

Diversified Telecommunication Services — (0.4)% | |

AT&T, Inc. | | | (24 | ) | | | (733 | ) |

| | | | | | | | |

Electric Utilities — (3.8)% | |

Duke Energy Corp. | | | (25 | ) | | | (2,104 | ) |

Pinnacle West Capital Corp. | | | (16 | ) | | | (1,304 | ) |

Southern Co. (The) | | | (79 | ) | | | (3,562 | ) |

| | | | | | | | |

| | | | | | | (6,970 | ) |

| | | | | | | | |

Electrical Equipment — (0.5)% | |

Rockwell Automation, Inc. | | | (5 | ) | | | (835 | ) |

| | | | | | | | |

Electronic Equipment, Instruments & Components — (0.4)% | |

Amphenol Corp., Class A | | | (9 | ) | | | (792 | ) |

| | | | | | | | |

Energy Equipment & Services — (2.6)% | |

Halliburton Co. | | | (17 | ) | | | (590 | ) |

Helmerich & Payne, Inc. | | | (17 | ) | | | (1,035 | ) |

Schlumberger Ltd. | | | (61 | ) | | | (3,130 | ) |

| | | | | | | | |

| | | | | | | (4,755 | ) |

| | | | | | | | |

Entertainment — (0.8)% | |

Cinemark Holdings, Inc. | | | (20 | ) | | | (835 | ) |

Viacom, Inc., Class A | | | — | (c) | | | (7 | ) |

Viacom, Inc., Class B | | | (19 | ) | | | (613 | ) |

| | | | | | | | |

| | | | | | | (1,455 | ) |

| | | | | | | | |

Equity Real Estate Investment Trusts (REITs) — (4.0)% | |

Alexandria Real Estate Equities, Inc. | | | (4 | ) | | | (534 | ) |

American Tower Corp. | | | (7 | ) | | | (1,070 | ) |

Apple Hospitality REIT, Inc. | | | (26 | ) | | | (426 | ) |

CBL & Associates Properties, Inc. | | | (30 | ) | | | (100 | ) |

Crown Castle International Corp. | | | (9 | ) | | | (994 | ) |

Extra Space Storage, Inc. | | | (2 | ) | | | (209 | ) |

Macerich Co. (The) | | | (10 | ) | | | (529 | ) |

Pennsylvania | | | (15 | ) | | | (133 | ) |

Regency Centers Corp. | | | (4 | ) | | | (257 | ) |

Simon Property Group, Inc. | | | (6 | ) | | | (1,148 | ) |

SL Green Realty Corp. | | | (7 | ) | | | (618 | ) |

Taubman Centers, Inc. | | | (3 | ) | | | (190 | ) |

Washington Prime Group, Inc. | | | (31 | ) | | | (201 | ) |

Welltower, Inc. | | | (16 | ) | | | (1,080 | ) |

| | | | | | | | |

| | | | | | | (7,489 | ) |

| | | | | | | | |

Food & Staples Retailing — (1.3)% | |

Kroger Co. (The) | | | (37 | ) | | | (1,110 | ) |

Walgreens Boots Alliance, Inc. | | | (15 | ) | | | (1,217 | ) |

| | | | | | | | |

| | | | | | | (2,327 | ) |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 14 | | | | J.P. MORGAN SPECIALTY FUNDS | | OCTOBER 31, 2018 |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Short Positions — continued | | | | | | | | |

Common Stocks — continued | | | | | | | | |

Food Products — (3.0)% | |

Campbell Soup Co. | | | (25 | ) | | | (945 | ) |

General Mills, Inc. | | | (58 | ) | | | (2,522 | ) |

Hershey Co. (The) | | | (19 | ) | | | (2,005 | ) |

| | | | | | | | |

| | | | | | | (5,472 | ) |

| | | | | | | | |

Gas Utilities — (0.6)% | |

National Fuel Gas Co. | | | (10 | ) | | | (527 | ) |

UGI Corp. | | | (9 | ) | | | (498 | ) |

| | | | | | | | |

| | | | | | | (1,025 | ) |

| | | | | | | | |

Health Care Equipment & Supplies — (2.1)% | |

Abbott Laboratories | | | (9 | ) | | | (653 | ) |

Baxter International, Inc. | | | (3 | ) | | | (190 | ) |

Becton Dickinson and Co. | | | (2 | ) | | | (526 | ) |

DENTSPLY SIRONA, Inc. | | | (11 | ) | | | (384 | ) |

Edwards Lifesciences Corp. * | | | (2 | ) | | | (278 | ) |

Stryker Corp. | | | (6 | ) | | | (946 | ) |

Varian Medical Systems, Inc. * | | | (8 | ) | | | (980 | ) |

| | | | | | | | |

| | | | | | | (3,957 | ) |

| | | | | | | | |

Health Care Providers & Services — (2.3)% | |

Cardinal Health, Inc. | | | (44 | ) | | | (2,207 | ) |

Henry Schein, Inc. * | | | (9 | ) | | | (783 | ) |

Humana, Inc. | | | (1 | ) | | | (467 | ) |

Patterson Cos., Inc. | | | (32 | ) | | | (729 | ) |

| | | | | | | | |

| | | | | | | (4,186 | ) |

| | | | | | | | |

Health Care Technology — (0.2)% | |

Cerner Corp. * | | | (6 | ) | | | (340 | ) |

| | | | | | | | |

Hotels, Restaurants & Leisure — (2.5)% | |

Aramark | | | (13 | ) | | | (457 | ) |

Bloomin’ Brands, Inc. | | | (13 | ) | | | (266 | ) |

Brinker International, Inc. | | | (7 | ) | | | (313 | ) |

Carnival Corp. | | | (6 | ) | | | (311 | ) |

Chipotle Mexican Grill, Inc. * | | | (6 | ) | | | (2,676 | ) |

McDonald’s Corp. | | | (3 | ) | | | (558 | ) |

| | | | | | | | |

| | | | | | | (4,581 | ) |

| | | | | | | | |

Household Durables — (0.3)% | |

Whirlpool Corp. | | | (5 | ) | | | (555 | ) |

| | | | | | | | |

Household Products — (1.6)% | |

Church & Dwight Co., Inc. | | | (12 | ) | | | (683 | ) |

Clorox Co. (The) | | | (8 | ) | | | (1,198 | ) |

Procter & Gamble Co. (The) | | | (13 | ) | | | (1,112 | ) |

| | | | | | | | |

| | | | | | | (2,993 | ) |

| | | | | | | | |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

| | | | | | | | |

| | | | | | | | |

Industrial Conglomerates — (1.7)% | |

3M Co. | | | (9 | ) | | | (1,636 | ) |

General Electric Co. | | | (144 | ) | | | (1,458 | ) |

| | | | | | | | |

| | | | | | | (3,094 | ) |

| | | | | | | | |

Insurance — (1.8)% | |

Aflac, Inc. | | | (12 | ) | | | (495 | ) |

Chubb Ltd. | | | (8 | ) | | | (1,028 | ) |

RenaissanceRe Holdings Ltd. (Bermuda) | | | (1 | ) | | | (164 | ) |

Torchmark Corp. | | | (6 | ) | | | (540 | ) |

Travelers Cos., Inc. (The) | | | (4 | ) | | | (555 | ) |

WR Berkley Corp. | | | (8 | ) | | | (601 | ) |

| | | | | | | | |

| | | | | | | (3,383 | ) |

| | | | | | | | |

Interactive Media & Services — (1.0)% | |

Facebook, Inc., Class A * | | | (9 | ) | | | (1,306 | ) |

Snap, Inc., Class A * | | | (72 | ) | | | (479 | ) |

| | | | | | | | |

| | | | | | | (1,785 | ) |

| | | | | | | | |

Internet & Direct Marketing Retail — (0.9)% | |

eBay, Inc. * | | | (59 | ) | | | (1,719 | ) |

| | | | | | | | |

IT Services — (1.3)% | |

Cognizant Technology Solutions Corp., Class A | | | (4 | ) | | | (272 | ) |

International Business Machines Corp. | | | (6 | ) | | | (646 | ) |

Paychex, Inc. | | | (22 | ) | | | (1,452 | ) |

| | | | | | | | |

| | | | | | | (2,370 | ) |

| | | | | | | | |

Leisure Products — (0.6)% | |

Mattel, Inc. * | | | (82 | ) | | | (1,118 | ) |

| | | | | | | | |

Machinery — (0.4)% | |

Donaldson Co., Inc. | | | (15 | ) | | | (763 | ) |

| | | | | | | | |

Media — (3.8)% | |

AMC Networks, Inc., Class A * | | | (30 | ) | | | (1,751 | ) |

Entercom Communications Corp., Class A | | | (36 | ) | | | (234 | ) |

Interpublic Group of Cos., Inc. (The) | | | (42 | ) | | | (970 | ) |

News Corp., Class A | | | (125 | ) | | | (1,653 | ) |

Omnicom Group, Inc. | | | (34 | ) | | | (2,524 | ) |

| | | | | | | | |

| | | | | | | (7,132 | ) |

| | | | | | | | |

Metals & Mining — (0.5)% | |

Compass Minerals International, Inc. | | | (18 | ) | | | (865 | ) |

| | | | | | | | |

Multi-Utilities — (2.3)% | |

CenterPoint Energy, Inc. | | | (25 | ) | | | (676 | ) |

Consolidated Edison, Inc. | | | (5 | ) | | | (370 | ) |

Dominion Energy, Inc. | | | (34 | ) | | | (2,407 | ) |

DTE Energy Co. | | | (8 | ) | | | (862 | ) |

| | | | | | | | |

| | | | | | | (4,315 | ) |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| OCTOBER 31, 2018 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 15 | |

JPMorgan Research Market Neutral Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF OCTOBER 31, 2018 (continued)

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Short Positions — continued | | | | | | | | |

Common Stocks — continued | | | | | | | | |

Oil, Gas & Consumable Fuels — (5.0)% | |

Anadarko Petroleum Corp. | | | (4 | ) | | | (237 | ) |

Apache Corp. | | | (32 | ) | | | (1,215 | ) |

Continental Resources, Inc. * | | | (4 | ) | | | (227 | ) |

Enbridge, Inc. (Canada) | | | (36 | ) | | | (1,126 | ) |

Exxon Mobil Corp. | | | (31 | ) | | | (2,459 | ) |

Hess Corp. | | | (37 | ) | | | (2,115 | ) |

Murphy Oil Corp. | | | (18 | ) | | | (577 | ) |

Range Resources Corp. | | | (77 | ) | | | (1,226 | ) |

| | | | | | | | |

| | | | | | | (9,182 | ) |

| | | | | | | | |

Paper & Forest Products — (0.7)% | |

Domtar Corp. | | | (29 | ) | | | (1,356 | ) |

| | | | | | | | |

Pharmaceuticals — (1.1)% | |

Johnson & Johnson | | | (14 | ) | | | (2,020 | ) |

| | | | | | | | |

Professional Services — (1.2)% | |

Nielsen Holdings plc | | | (38 | ) | | | (981 | ) |

Robert Half International, Inc. | | | (20 | ) | | | (1,235 | ) |

| | | | | | | | |

| | | | | | | (2,216 | ) |

| | | | | | | | |

Road & Rail — (3.8)% | |

Canadian National Railway Co. (Canada) | | | (27 | ) | | | (2,319 | ) |

Heartland Express, Inc. | | | (129 | ) | | | (2,510 | ) |

Knight-Swift Transportation Holdings, Inc. | | | (10 | ) | | | (313 | ) |

Ryder System, Inc. | | | (11 | ) | | | (628 | ) |

Schneider National, Inc., Class B | | | (34 | ) | | | (733 | ) |

Werner Enterprises, Inc. | | | (15 | ) | | | (495 | ) |

| | | | | | | | |

| | | | | | | (6,998 | ) |

| | | | | | | | |

Semiconductors & Semiconductor Equipment — (5.5)% | |

Applied Materials, Inc. | | | (34 | ) | | | (1,107 | ) |

Intel Corp. | | | (48 | ) | | | (2,239 | ) |

KLA-Tencor Corp. | | | (6 | ) | | | (580 | ) |

Lam Research Corp. | | | (12 | ) | | | (1,654 | ) |

Maxim Integrated Products, Inc. | | | (32 | ) | | | (1,623 | ) |

Micron Technology, Inc. * | | | (45 | ) | | | (1,709 | ) |

QUALCOMM, Inc. | | | (11 | ) | | | (709 | ) |

Xilinx, Inc. | | | (7 | ) | | | (556 | ) |

| | | | | | | | |

| | | | | | | (10,177 | ) |

| | | | | | | | |

Software — (0.1)% | |

Citrix Systems, Inc. * | | | (3 | ) | | | (277 | ) |

| | | | | | | | |

Specialty Retail — (2.4)% | |

Abercrombie & Fitch Co., Class A | | | (19 | ) | | | (374 | ) |

American Eagle Outfitters, Inc. | | | (9 | ) | | | (204 | ) |

Ascena Retail Group, Inc. * | | | (98 | ) | | | (376 | ) |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

| | | | | | | | |

| | | | | | | | |

Specialty Retail — continued | | | | | | | | |

AutoNation, Inc. * | | | (6 | ) | | | (235 | ) |

Bed Bath & Beyond, Inc. | | | (60 | ) | | | (829 | ) |

Buckle, Inc. (The) | | | (5 | ) | | | (105 | ) |

CarMax, Inc. * | | | (5 | ) | | | (307 | ) |

DSW, Inc., Class A | | | (28 | ) | | | (737 | ) |

Express, Inc. * | | | (42 | ) | | | (367 | ) |

L Brands, Inc. | | | (5 | ) | | | (166 | ) |

Williams-Sonoma, Inc. | | | (12 | ) | | | (720 | ) |

| | | | | | | | |

| | | | | | | (4,420 | ) |

| | | | | | | | |

Technology Hardware, Storage & Peripherals — (1.7)% | |

HP, Inc. | | | (23 | ) | | | (549 | ) |

NetApp, Inc. | | | (11 | ) | | | (880 | ) |

Seagate Technology plc | | | (29 | ) | | | (1,155 | ) |

Western Digital Corp. | | | (12 | ) | | | (512 | ) |

| | | | | | | | |

| | | | | | | (3,096 | ) |

| | | | | | | | |

Textiles, Apparel & Luxury Goods — (2.2)% | |

Carter’s, Inc. | | | (5 | ) | | | (458 | ) |

Hanesbrands, Inc. | | | (93 | ) | | | (1,603 | ) |

NIKE, Inc., Class B | | | (10 | ) | | | (748 | ) |

Under Armour, Inc., Class A * | | | (40 | ) | | | (892 | ) |

Under Armour, Inc., Class C * | | | (17 | ) | | | (345 | ) |

| | | | | | | | |

| | | | | | | (4,046 | ) |

| | | | | | | | |

Trading Companies & Distributors — (0.7)% | |

Air Lease Corp. | | | (17 | ) | | | (664 | ) |

GATX Corp. | | | (9 | ) | | | (658 | ) |

| | | | | | | | |

| | | | | | | (1,322 | ) |

| | | | | | | | |

Wireless Telecommunication Services — (0.7)% | |

Sprint Corp. * | | | (219 | ) | | | (1,341 | ) |

| | | | | | | | |

Total Common Stocks

(Proceeds $(171,281)) | | | | (156,993 | ) |

| | | | | |

Total Short Positions

(Proceeds $(171,281)) | | | | (156,993 | ) |

| | | | | |

Total Investments — 13.0%

(Cost $(16,331)) | | | | 24,187 | |

Other Assets Less Liabilities — 87.0% | | | | 161,018 | |

| | | | | |

Net Assets — 100.0% | | | | 185,205 | |

| | | | | |

Percentages indicated are based on net assets.

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 16 | | | | J.P. MORGAN SPECIALTY FUNDS | | OCTOBER 31, 2018 |

| | |

Abbreviations |

| REIT | | Real Estate Investment Trust |

| (a) | | All or a portion of this security is segregated as collateral for short sales. The total value of securities and cash segregated as collateral is approximately $33,612,000 and $163,657,000, respectively. |

| (b) | | Amount rounds to less than 0.1% of net assets. |

| (c) | | Amount rounds to less than one thousand. |

| (d) | | Investment in affiliate. Fund is registered under the Investment Company Act of 1940, as amended, and advised by J.P. Morgan Investment Management Inc. |

| (e) | | The rate shown is the current yield as of October 31, 2018. |

| (f) | | All or a portion of this security is deposited with the broker as initial margin for futures contracts. |

| (g) | | The rate shown is the effective yield as of October 31, 2018. |

| * | | Non-income producing security. |

| | | | | | | | | | | | | | | | | | | | |

| Futures contracts outstanding as of October 31, 2018 (amounts in thousands, except number of contracts): | |

| DESCRIPTION | | NUMBER OF

CONTRACTS | | | EXPIRATION

DATE | | | TRADING

CURRENCY | | | NOTIONAL

AMOUNT ($) | | | VALUE AND

UNREALIZED

APPRECIATION

(DEPRECIATION) ($) | |

Long Contracts | |

S&P 500 E-Mini Index | | | 7 | | | | 12/2018 | | | | USD | | | | 949 | | | | 15 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | 15 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | |

Abbreviations |

| USD | | United States Dollar |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| OCTOBER 31, 2018 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 17 | |

STATEMENTS OF ASSETS AND LIABILITIES

AS OF OCTOBER 31, 2018

(Amounts in thousands, except per share amounts)

| | | | | | | | |

| | | JPMorgan

Opportunistic

Equity

Long/Short Fund | | | JPMorgan

Research

Market

Neutral Fund | |

ASSETS: | |

Investments in non-affiliates, at value | | $ | 173,661 | | | $ | 158,314 | |

Investments in affiliates, at value | | | 110,482 | | | | 22,866 | |

Cash | | | — | | | | — | (a) |

Deposits at broker for securities sold short | | | 80,967 | | | | 163,657 | |

Receivables: | | | | | | | | |

Due from custodian | | | 745 | | | | — | |

Investment securities sold | | | 12,524 | | | | 17,866 | |

Fund shares sold | | | 442 | | | | 30 | |

Dividends from non-affiliates | | | 123 | | | | 354 | |

Dividends from affiliates | | | 140 | | | | 38 | |

Variation margin on futures contracts | | | — | | | | 10 | |

| | | | | | | | |

Total Assets | | | 379,084 | | | | 363,135 | |

| | | | | | | | |

|

LIABILITIES: | |

Payables: | | | | | | | | |

Securities sold short, at value | | | 44,530 | | | | 156,993 | |

Dividend expense to non-affiliates on securities sold short | | | 109 | | | | 190 | |

Investment securities purchased | | | 71,409 | | | | 19,992 | |

Fund shares redeemed | | | 465 | | | | 522 | |

Accrued liabilities: | | | | | | | | |

Investment advisory fees | | | 260 | | | | 91 | |

Administration fees | | | 17 | | | | — | |

Distribution fees | | | 15 | | | | 7 | |

Service fees | | | 42 | | | | 21 | |

Custodian and accounting fees | | | 6 | | | | 6 | |

Trustees’ and Chief Compliance Officer’s fees | | | — | (a) | | | — | |

Other | | | 138 | | | | 108 | |

| | | | | | | | |

Total Liabilities | | | 116,991 | | | | 177,930 | |

| | | | | | | | |

Net Assets | | $ | 262,093 | | | $ | 185,205 | |

| | | | | | | | |

| (a) | Amount rounds to less than one thousand. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 18 | | | | J.P. MORGAN SPECIALTY FUNDS | | OCTOBER 31, 2018 |

| | | | | | | | |

| | | JPMorgan

Opportunistic

Equity

Long/Short Fund | | | JPMorgan

Research

Market

Neutral Fund | |

NET ASSETS: | |

Paid-in-Capital | | $ | 245,166 | | | $ | 187,550 | |

Total distributable earnings (loss) (a) | | | 16,927 | | | | (2,345 | ) |

| | | | | | | | |

Total Net Assets | | $ | 262,093 | | | $ | 185,205 | |

| | | | | | | | |

|

Net Assets: | |

Class A | | $ | 50,803 | | | $ | 14,973 | |

Class C | | | 3,544 | | | | 6,155 | |

Class I | | | 151,261 | | | | 34,927 | |

Class L | | | — | | | | 129,150 | |

Class R2 | | | 24 | | | | — | |

Class R5 | | | 25 | | | | — | |

Class R6 | | | 56,436 | | | | — | |

| | | | | | | | |

Total | | $ | 262,093 | | | $ | 185,205 | |

| | | | | | | | |

|

Outstanding units of beneficial interest (shares) | |

($0.0001 par value; unlimited number of shares authorized): | | | | | | | | |

Class A | | | 2,788 | | | | 1,048 | |

Class C | | | 199 | | | | 462 | |

Class I | | | 8,209 | | | | 2,339 | |

Class L | | | — | | | | 8,477 | |

Class R2 | | | 1 | | | | — | |

Class R5 | | | 1 | | | | — | |

Class R6 | | | 3,029 | | | | — | |

| | |

Net Asset Value (b): | | | | | | | | |

Class A — Redemption price per share | | $ | 18.22 | | | $ | 14.29 | |

Class C — Offering price per share (c) | | | 17.83 | | | | 13.32 | |

Class I — Offering and redemption price per share | | | 18.43 | | | | 14.93 | |

Class L — Offering and redemption price per share | | | — | | | | 15.24 | |

Class R2 — Offering and redemption price per share | | | 18.03 | | | | — | |

Class R5 — Offering and redemption price per share | | | 18.59 | | | | — | |

Class R6 — Offering and redemption price per share | | | 18.63 | | | | — | |

Class A maximum sales charge | | | 5.25 | % | | | 5.25 | % |

Class A maximum public offering price per share

[net asset value per share/(100% — maximum sales charge)] | | $ | 19.23 | | | $ | 15.08 | |

| | | | | | | | |

| | |

Cost of investments in non-affiliates | | $ | 158,051 | | | $ | 132,087 | |

Cost of investments in affiliates | | | 110,482 | | | | 22,863 | |

Proceeds from securities sold short | | | 46,461 | | | | 171,281 | |

| (a) | Total distributable earnings has been aggregated to conform to the current presentation requirements for the adoption of the Securities and Exchange Commission’s Disclosure Update and Simplification Rule. See Note 8. |

| (b) | Per share amounts may not recalculate due to rounding of net assets and/or shares outstanding. |

| (c) | Redemption price for Class C Shares varies based upon length of time the shares are held. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| OCTOBER 31, 2018 | | J.P. MORGAN SPECIALTY FUNDS | | | | | 19 | |

STATEMENTS OF OPERATIONS

FOR THE YEAR ENDED OCTOBER 31, 2018

(Amounts in thousands)

| | | | | | | | |

| | | JPMorgan

Opportunistic

Equity

Long/Short Fund | | | JPMorgan

Research

Market

Neutral Fund | |

INVESTMENT INCOME: | |

Interest income from non-affiliates | | $ | — | | | $ | 4 | |

Interest income from affiliates | | | — | (a) | | | — | (a) |

Interest income from non-affiliates on securities sold short | | | 806 | | | | 2,480 | |

Dividend income from non-affiliates | | | 1,498 | | | | 2,731 | |