UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-21359

Managed Duration Investment Grade Municipal Fund

(Exact name of registrant as specified in charter)

227 West Monroe Street, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Amy J. Lee

227 West Monroe Street, Chicago, IL 60606

(Name and address of agent for service)

Registrant's telephone number, including area code: (312) 827-0100

Date of fiscal year end: July 31

Date of reporting period: August 1, 2013 to July 31, 2014

Item 1. Reports to Stockholders.

The registrant's annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

GUGGENHEIMINVESTMENTS.COM/MZF

. . .YOUR WINDOW TO THE LATEST, MOST UP-TO-DATE INFORMATION ABOUT THE MANAGED

DURATION INVESTMENT GRADE MUNICIPAL FUND

The shareholder report you are reading right now is just the beginning of the story. Online at guggenheiminvestments.com/mzf, you will find:

| · | Daily, weekly and monthly data on share prices, distributions and more |

| · | Portfolio overviews and performance analyses |

| · | Announcements, press releases and special notices and tax characteristics |

Cutwater Investor Services Corp. and Guggenheim Investments are continually updating and expanding shareholder information services on the Fund’s website, in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed, and the results of our efforts. It is just one more way we are working to keep you better informed about your investment in the Fund.

DEAR SHAREHOLDER

We thank you for your investment in Managed Duration Investment Grade Municipal Fund (the “Fund”). This report covers performance for the 12-month period ended July 31, 2014.

The Fund’s investment objective is to provide high current income exempt from regular federal income tax while seeking to protect the value of the Fund’s assets during periods of interest rate volatility. Under normal market conditions, the Fund seeks to achieve this objective by investing substantially all of its assets in municipal bonds of investment-grade quality.

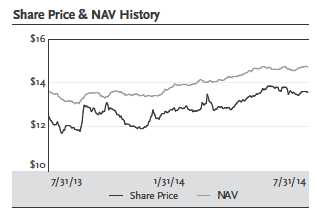

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the 12-month period ended July 31, 2014, the Fund provided a total return based on market price of 16.29% and a total return of 14.87% based on NAV. Past performance is not a guarantee of future results. As of July 31, 2014, the Fund’s last closing market price of $13.57 represented a discount of 7.81% to NAV of $14.72. The market value and NAV of the Fund’s shares fluctuate from time to time, and the Fund’s market value may be higher or lower than its NAV. The Fund’s NAV performance data reflects fees and expenses of the Fund.

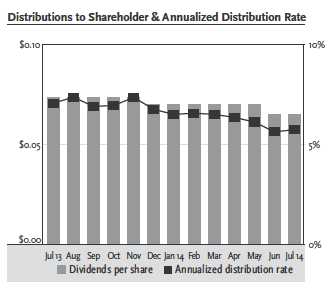

Distributions of $0.0735 were paid in each of the first four months of the period, $0.0700 in each of the next six, and $0.0650 in each of the last two. The current distribution represents an annualized distribution rate of 5.75% based on the last closing market price of $13.57 on July 31, 2014.

Cutwater Investor Services Corp. (“Cutwater”) serves as the Fund’s Investment Adviser. With over $22 billion in assets under management as of July 31, 2014, Cutwater Asset Management is one of the largest institutional fixed income investment managers in the world. Cutwater’s parent company, MBIA Inc., is listed on the New York Stock Exchange.

Guggenheim Funds Distributors, LLC (“GFD”) serves as the Servicing Agent to the Fund. GFD is part of Guggenheim Investments. Guggenheim Investments represents the investment management division of Guggenheim Partners, LLC.

We encourage shareholders to consider the opportunity to reinvest their distributions from the Fund through the Dividend Reinvestment Plan (“DRIP”), which is described in detail on page 26 of this report. When shares trade at a discount to NAV, the DRIP takes advantage of the discount by reinvesting the monthly dividend distribution in common shares of the Fund purchased in the market at a price less than NAV. Conversely, when the market price of the Fund’s common shares is at a premium above NAV, the DRIP reinvests participants’ dividends in newly-issued common shares at the greater of NAV per share or 95% of the market price per share. The DRIP provides a cost-effective means to accumulate additional shares and enjoy the benefits of compounding returns over time. Since the Fund endeavors to maintain a steady monthly distribution rate, the DRIP effectively provides an income averaging technique, which causes shareholders to accumulate a larger number of Fund shares when the market price is depressed than when the price is higher.

To learn more about the Fund’s performance, we encourage you to read the Questions & Answers section of this report, which begins on page 4 of this report. You will find information about how the Fund is managed, what affected the performance of the Fund during the 12-month period ended July 31, 2014, and Cutwater’s views on the market environment.

We appreciate your investment, and we look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the Fund’s website at guggenheiminvestments.com/mzf.

Sincerely,

Clifford D. Corso

President and Chief Executive Officer

Managed Duration Investment Grade Municipal Fund

August 31, 2014

MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT l 3

| QUESTIONS & ANSWERS | July 31, 2014 |

Clifford D. Corso

Portfolio Manager

Mr. Corso joined the firm in 1994, establishing the company’s asset management platform and building it into one of the largest fixed income managers in the world. With a staff of 85 people, he now oversees the investment of over $22 billion in assets as of July 31, 2014, and directs the investment strategies of Cutwater’s clients, including pension funds, global banks, corporations, Taft Hartley and insurance companies as well as hundreds of municipalities across the U.S. Mr. Corso also initiated and managed the expansion of the asset manager’s international asset management business from a principal office in London, now a multi-billion dollar platform.

Prior to joining the firm, Mr. Corso served as co-head of a fixed income division at Alliance Capital Management. In his 28-year career, he has held positions as a credit analyst, restructuring specialist, trader and portfolio manager. Mr. Corso graduated from Yale University with a degree in economics and earned an MBA from Columbia University. He has lectured on topics from leadership to finance at many academic institutions, including Columbia University and New York University, where he taught a course on financial derivatives.

James B. DiChiaro

Portfolio Manager

Mr. DiChiaro joined Cutwater in 1999 and is a director. He currently manages Cutwater’s municipal assets under management (taxable and tax-exempt) and has extensive experience managing money-market portfolios. He constructs and implements portfolio strategies for a diverse client base including insurance companies, separately managed accounts and closed-end bond funds. Mr. DiChiaro began his career at Cutwater working with the conduit group structuring medium-term notes for Meridian Funding Company and performing the treasury role for an MBIA sponsored asset-backed commercial paper conduit, Triple-A One Funding Corporation.

Prior to joining Cutwater he worked for Merrill Lynch supporting their asset-backed securities trading desk. Mr. DiChiaro has a bachelor’s degree from Fordham University and a master’s degree from Pace University.

Matthew J. Bodo

Portfolio Manager

Mr. Bodo joined the firm in 2002 and is a vice president in Cutwater’s portfolio management group. He participates in biweekly corporate credit and portfolio strategy meetings and supports the portfolio managers’ implementation of those strategies for Cutwater’s third-party accounts. As part of his daily responsibilities, Mr. Bodo actively manages the local government investment pool portfolios, specializing in high-grade commercial paper, investment grade corporates, U.S. Treasury and instrumentality bonds. Prior to this role, Mr. Bodo served as an investment accountant performing accounting related functions for mutual funds and MBIA insurance portfolios. He has a bachelor’s degree from the State University of New York at Albany.

In the following interview Portfolio Managers Clifford D. Corso, James B. DiChiaro and Matthew J. Bodo discuss the market environment and the performance of the Managed Duration Investment Grade Municipal Fund (the “Fund”) for the annual period ended July 31, 2014.

Please provide an overview of the economy and the municipal market during the 12-month period ended July 31, 2014.

The U.S. economy expanded over the period, as low interest rates and an improving picture for employment and manufacturing helped overcome a weather-related soft patch in the first quarter of 2014. Treasury yields were volatile last summer when the U.S. Federal Reserve (“Fed”) signaled it would eventually wind down its quantitative easing program. But after a recent peak in the 10-year Treasury yield at the end of 2013, when the Fed began reducing asset purchases by $10 billion a month, the yield fell steadily in 2014 amid geopolitical tension and safe-haven buying.

After subdued performance for the last half of 2013, the municipal market in 2014 continued its grind toward lower yields and tighter credit spreads. Municipal market performance was helped by limited new issuance and refunding supply, as municipalities reduce borrowing, as well as by increased demand by investors looking for shelter from higher federal income taxes. This positive supply/demand dynamic and the supportive Treasury yield environment carried the return for the key municipal index to above 6% for the first seven months of 2014, outperforming many other fixed and equity asset classes.

For the 12-month period ended July 31, 2014, the Barclays Municipal Bond Index (the “Index”), a widely used measure of the municipal bond market as a whole, returned 7.27%. For comparison, the broader Barclays U.S. Aggregate Bond Index returned 3.97%.

Tax-exempt issuance for the first half of 2014 was approximately $150 billion, trailing the prior year by roughly 15%. The stubbornly low yield environment has encouraged issuers to refund previously issued debt, but net supply for the year remains negative and may approach negative $20 billion during the summer months. The appealing relative value offered by the tax-exempt sector has attracted retail investors back to this market evidenced by mutual fund inflows of approximately $5.7 billion through the first half of 2014.

Fundamentals for municipals did weaken in mid-2014, as certain states recognized that they had overestimated their tax revenues for 2013. The revenue shortfalls have opened up budget gaps in states such as New Jersey that skipped their actuarial required contribution to their pension fund in favor of plugging their budget gap. Despite what should prove to be a transient slowdown in the growth rate of tax revenues, gross tax receipts remain high relative to historic metrics and are above pre-recession levels. Revenues for local municipalities have been less volatile given their reliance on property taxes. Property tax revenues have stabilized and local governments have shifted their focus to conservative budgeting such as minimizing expenditures through staff reductions and opting to build reserve balances with surplus revenues.

4 l MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT

| QUESTIONS & ANSWERS continued | July 31, 2014 |

The Commonwealth of Puerto Rico introduced the Puerto Rico Public Corporation Debt Enforcement and Recovery Act, which was perceived as negative for certain Puerto Rico revenue bond issuers. The intent of the legislation was to provide certain revenue bond issuers the ability to restructure their debt. The island’s general obligation bonds and sales-tax backed issues were excluded from the Act. The passage of this Act inspired the rating agencies to downgrade many Puerto Rican issuers, resulting in significant decreases in market value and a widening of their credits spreads. Puerto Rico’s malaise spilled over in to the tax-exempt high yield market, where credit spreads also widened. Among other troubled issuers, the City of Detroit filed a Plan of Adjustment with the U.S. Bankruptcy court, but it has not been approved.

How did the Fund perform in this market environment?

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the 12-month period ended July 31, 2014, the Fund provided a total return based on market price of 16.29% and a total return of 14.87% based on NAV. Past performance is not a guarantee of future results.

As of July 31, 2014, the Fund’s last closing market price of $13.57 represented a discount of 7.81% to NAV of $14.72. As of July 31, 2013, the Fund’s last closing market price of $12.46 represented a discount of 8.45% to NAV of $13.61. The market value and NAV of the Fund’s shares fluctuate from time to time, and the Fund’s market value may be higher or lower than its NAV. The Fund’s NAV performance data reflects fees and expenses of the Fund.

Distributions of $0.0735 were paid in each of the first four months of the period, $0.0700 in each of the next six, and $0.0650 in each of the last two. The current distribution represents an annualized distribution rate of 5.75% based on the last closing market price of $13.57 on July 31, 2014.

What drove the Fund’s significant outperformance against the Barclays Municipal Index?

The Fund outperformed its benchmark during the period (MZF NAV returned 14.87% versus 7.27% for the Index). The continued growth of the U.S. economy and state and local government revenues have contributed to lower credit spreads within the tax-exempt space. The Fund’s shorter duration position relative to the Index was negative for performance; however, the barbelled-duration positioning of the portfolio more than offset this. This barbelled stance means that the Fund has more exposure to the short (less than 2 years) and long (over eight years) end of the curve versus the Index. The long-end of the tax-exempt yield curve decisively outperformed the general Index in excess of 300 basis points during the period. Additionally, the Fund’s leverage was a significant contributor to performance versus the benchmark during the year. The Fund’s overweight to A-rated and BBB-rated securities were also additive to the Fund’s performance during the period, as credit spreads recovered from previously oversold levels. New issue supply has decreased relative to the prior year, which also helped this market achieve positive total returns during the period. Overall, the Fund was able to outperform its benchmark without a significant change to the credit quality of the portfolio.

How is the Fund’s portfolio structured, and what has that structure meant for performance?

The Fund has a high quality portfolio that is diversified across issuers, sectors and states. In selecting securities for the portfolio, the portfolio management team is supported by Cutwater’s team of credit analysts, who evaluate the credit quality of sectors and individual issuers, going far beyond the bond ratings provided by rating agencies. Cutwater’s proprietary quantitative models help to evaluate the risk of individual securities as well as the overall portfolio, supplementing the judgment of the experienced team. Thorough quantitative and qualitative analysis helps ensure that the desired level of credit quality is maintained in the Fund’s portfolio while yield is added, as appropriate, by buying higher-yielding bonds at what are considered to be attractive prices.

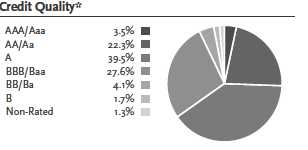

The relatively high average credit quality of the Fund’s portfolio has helped the Fund maintain a high distribution rate while outperforming its benchmark, which has an even higher quality profile. In recent months, the average quality has been increased, with an intentional rotation into AA-rated bonds given high valuations for A-rated and to a lesser degree BBB-rated securities. The improvement in the credit quality of the portfolio was achieved in part through a reduction to certain BBB-rated and non-investment grade rated corporate-backed exposures.

During the period certain positions in International Paper Company were called, and a position in Alcoa Inc. was sold. The proceeds were redeployed into AA-rated water/sewer bonds as well as general obligation credits. Despite low primary market issuance, we believe tax-exempt interest rates and credit spreads will rise from current levels, which was a motivation for reducing the Fund’s lower-quality exposures.

The Fund’s sector composition was mostly unchanged, but there was a reduction to the development (corporate-backed) sector. Part of the risk-reducing strategy mentioned earlier included lowering the allocation to the corporate-backed sector in favor of the water/sewer and general obligation sectors. The water/sewer and general obligation sectors are generally regarded as being less risky municipal sectors given the essentiality of the services they provide, and the full faith and credit pledge of unlimited ad valorem property taxes provided by the Fund’s general obligation holdings.

The Fund’s duration decreased from 7.72 to 7.09 during the period, and the Fund maintained a shorter duration relative to the Index throughout the period. The Fund’s shorter duration is indicative of a reduction in the portfolio’s interest rate sensitivity during a time of low interest rates. Some of this shortening was a function of lower interest rates inferring a greater probability of a bond option being exercised, but the majority of the shortening was intentional.

Cutwater has structured this Fund with a barbelled-duration positioning versus the Index. We have selectively added an approximately 10% exposure to floating-rate securities, which has benefitted the performance of the Fund. We also increased the Fund’s exposure to the 30-year part of the curve, which we expect will outperform the belly of the curve given our rate forecast.

MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT l 5

| QUESTIONS & ANSWERS continued | July 31, 2014 |

The Fund holds $2 million par in City of Detroit water and sewer bonds. What is the status of the bonds?

The Fund’s exposure to the City of Detroit resides in two securities issued by the City of Detroit’s Water and Sewerage Department (DWSD). The City of Detroit has filed a Plan of Adjustment (the “Plan”) that has not yet been approved by the U.S. Bankruptcy court. Recently, the DWSD announced an invitation to tender the water and sewer bonds. The invitation contained a tender price at a premium for the Fund’s DWSD bonds. After reviewing the offer, the Adviser elected to tender the Fund’s holdings of the DWSD securities in late August. Detroit accepted the tender and the Fund’s securities were retired in early September.

What effect did the Fund’s leverage have on Fund return?

The Fund utilizes leverage (borrowing) as part of its investment strategy, to finance the purchase of additional securities that provide increased income and potentially greater appreciation potential to common shareholders than could be achieved from a portfolio that is not leveraged.

Leverage adds to performance only when the cost of leverage is less than the total return generated by investments. The use of financial leverage creates an opportunity for increased income and capital appreciation but, at the same time, creates special risks. There can be no assurance that a leveraging strategy will be utilized or will be successful. Financial leverage may cause greater changes in the Fund’s net asset value and returns than if financial leverage had not been used.

As of July 31, 2014, the Fund had $69.45 million of leverage outstanding in the form of Auction Market Preferred Shares (“AMPS”). Since the Fund’s NAV return was greater than the cost of leverage during the period, leverage was a contributor to the Fund’s total return.

Index Definitions

All indices are unmanaged. It is not possible to invest in an index.

The Barclays Municipal Bond Index is a rules-based, market-value weighted index engineered for the long-term tax-exempt bond market. To be included in the index, bonds must be rated investment-grade (Baa3/BBB- or higher) by at least two of the following ratings agencies: Moody’s Investor Services, Inc., Standard & Poor’s Rating Group or Fitch Ratings, Inc.

The Barclays U.S. Aggregate Bond Index represents securities that are U.S. domestic, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

Risks and Other Considerations

The views expressed in this report reflect those of the portfolio managers only through the report period as stated on the cover. These views are subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any kind. The material may also include forward looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come to pass.

There can be no assurance that the Fund will achieve its investment objectives. The value of the Fund will fluctuate with the value of the underlying securities. Closed-end funds often trade at a discount to their net asset value. There can be no assurance that the Fund will achieve its investment objectives.

Risk is inherent in all investing, including the loss of your entire principal. Therefore, before investing you should consider the risks carefully. Please see guggenheiminvestments.com/mzf for a detailed discussion of the Fund’s risks and considerations.

6 l MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT

| FUND SUMMARY (Unaudited) | July 31, 2014 |

Fund Information | |

Symbol on New York Stock Exchange: | MZF |

Initial Offering Date: | August 27, 2003 |

Closing Market Price as of 7/31/14: | $13.57 |

Net Asset Value as of 7/31/14: | $14.72 |

Yield on Closing Market Price as of 7/31/14: | 5.75% |

Taxable Equivalent Yield on Closing Market Price | |

as of 7/31/141: | 10.16% |

Monthly Distribution Per Common Share2: | $0.0650 |

Leverage as of 7/31/143: | 41% |

Percentage of total investments subject to | |

alternative minimum tax as of 7/31/14: | 17.0% |

1 Taxable equivalent yield is calculated assuming a 43.4% federal income tax bracket

2 Monthly distribution is subject to change.

3 As a percentage of total investments.

| | | |

Total Returns | | |

(Inception 8/27/03) | Market | NAV |

One Year | 16.29% | 14.87% |

Three Year - average annual | 6.97% | 8.25% |

Five Year - average annual | 9.90% | 9.96% |

Ten Year - average annual | 6.81% | 6.59% |

Since Inception - average annual | 5.26% | 6.10% |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. NAV total returns reflect fees and expenses of the Fund. For the most recent month-end performance figures, please visit guggenheiminvestments.com/mzf. The investment return and principal value of an investment will fluctuate with changes in the market conditions and other factors so that an investor’s shares, when sold, may be worth more or less than their original cost.

*Ratings shown are assigned by one or more Nationally Recognized Statistical Credit Rating Organizations (“NRSRO”), such as S&P, Moody’s and Fitch. The ratings are an indication of an issuer’s creditworthiness and typically range from AAA or Aaa (highest) to D (lowest). When two or more ratings are available, the lower rating is used; and when only one is available, that rating is used. The Non-Rated category consists of securities that have not been rated by an NRSRO. US Treasury securities and US Government Agency securities are not rated but deemed to be equivalent to securities rated AA+/Aaa.

MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT l 7

| PORTFOLIO OF INVESTMENTS | July 31, 2014 |

| | Description | Rating* | Coupon | Maturity | Optional Call Provisions** | Value |

| | | Long-Term Investments – 167.0% | | | | | |

| | | Municipal Bonds – 164.9% | | | | | |

| | | Alabama – 0.8% | | | | | |

$ 845,000 | | Courtland Industrial Development Board, AMT, Series B | BBB | 6.250% | 08/01/2025 | 08/01/15 @ 100 | $ 847,636 |

| | | Alaska – 0.9% | | | | | |

750,000 | | Alaska Municipal Bond Bank Authority, Series 1 | AA+ | 5.750% | 09/01/2033 | 09/01/18 @ 100 | 868,687 |

| | | Arizona – 6.6% | | | | | |

2,500,000 | | Arizona Health Facilities Authority(a) | AA– | 0.967% | 01/01/2037 | 01/01/17 @ 100 | 2,175,525 |

2,000,000 | | Arizona Health Facilities Authority, Series A3(a) | BBB+ | 1.910% | 02/01/2048 | 08/05/22 @ 100 | 1,982,800 |

1,250,000 | | Glendale Municipal Property Corp., Series B | AA+ | 5.000% | 07/01/2033 | 01/01/23 @ 100 | 1,360,775 |

1,000,000 | | Industrial Development Authority of the City of Phoenix | A+ | 5.250% | 06/01/2034 | 06/01/22 @ 100 | 1,075,540 |

| | | | | | | | 6,594,640 |

| | | California – 18.0% | | | | | |

1,000,000 | | Bay Area Toll Authority, Series A(a) | AA | 1.310% | 04/01/2036 | 10/01/26 @ 100 | 999,950 |

1,500,000 | | California Health Facilities Financing Authority, Series B | AA– | 5.875% | 08/15/2031 | 08/15/20 @ 100 | 1,786,260 |

1,000,000 | | California Pollution Control Financing Authority, AMT(b) | Baa3 | 5.000% | 07/01/2030 | 07/01/22 @ 100 | 1,050,560 |

2,500,000 | | California Statewide Communities Development Authority(a) | A+ | 0.937% | 04/01/2036 | 08/05/14 @ 100 | 2,040,750 |

2,500,000 | | City of Chula Vista CA, AMT, Series B | A | 5.500% | 12/01/2021 | 06/02/15 @ 101 | 2,557,250 |

3,750,000 | | Desert Community College District, (AGM)(c) | AA | 0.000% | 08/01/2046 | 08/01/17 @ 21 | 664,950 |

1,000,000 | | Los Angeles County Public Works Financing Authority | AA | 4.000% | 08/01/2042 | 08/01/22 @ 100 | 975,300 |

2,525,000 | | Los Angeles Unified School District, Series F | AA– | 5.000% | 01/01/2034 | 07/01/19 @ 100 | 2,807,270 |

3,500,000 | | Sacramento County Sanitation Districts Financing Authority, Series B, (AGC-ICC FGIC)(a) | AA | 0.682% | 12/01/2035 | 06/01/17 @ 100 | 3,134,880 |

1,000,000 | | San Bernardino City Unified School District, Series A, (AGM) | AA | 5.000% | 08/01/2028 | 08/01/23 @ 100 | 1,136,300 |

3,145,000 | | San Diego Unified School District(c) | AA– | 0.000% | 07/01/2038 | 01/01/24 @ 45 | 894,752 |

| | | | | | | | 18,048,222 |

| | | Colorado – 2.2% | | | | | |

1,000,000 | | City & County of Denver CO Airport System Revenue, Series B | A | 5.000% | 11/15/2043 | 11/15/23 @ 100 | 1,085,700 |

1,000,000 | | Colorado Health Facilities Authority, Series A | A+ | 5.250% | 01/01/2045 | 01/01/23 @ 100 | 1,087,700 |

| | | | | | | | 2,173,400 |

| | | Connecticut – 1.7% | | | | | |

1,750,000 | | Connecticut Housing Finance Authority, Series D 2 | AAA | 4.000% | 11/15/2034 | 05/15/21 @ 100 | 1,742,878 |

| | | Delaware – 1.7% | | | | | |

1,500,000 | | Delaware State Economic Development Authority | BBB+ | 5.400% | 02/01/2031 | 08/01/20 @ 100 | 1,674,225 |

| | | District of Columbia – 2.0% | | | | | |

2,000,000 | | District of Columbia Housing Finance Agency, AMT, (FHA) | Aaa | 5.100% | 06/01/2037 | 06/01/15 @ 102 | 2,026,060 |

| | | Florida – 11.9% | | | | | |

1,000,000 | | County of Broward FL, AMT, Series A, (AGM) | AA | 5.000% | 04/01/2038 | 04/01/23 @ 100 | 1,078,580 |

2,200,000 | | County of Miami-Dade FL, Aviation Revenue, AMT, Series A, (CIFG) | A | 5.000% | 10/01/2038 | 10/01/15 @ 100 | 2,277,792 |

1,500,000 | | JEA Water & Sewer System Revenue, Series B | AA | 4.000% | 10/01/2041 | 10/01/17 @ 100 | 1,502,145 |

2,000,000 | | Miami-Dade County Educational Facilities Authority, Series A | A– | 5.000% | 04/01/2042 | 04/01/23 @ 100 | 2,157,160 |

1,500,000 | | Miami-Dade County School Board Foundation, Inc., Series A, (Assured Gty) | AA | 5.375% | 02/01/2034 | 02/01/19 @ 100 | 1,619,130 |

1,000,000 | | Seminole Tribe of Florida, Inc., Series A(b) | BBB– | 5.250% | 10/01/2027 | 10/01/17 @ 100 | 1,046,320 |

1,000,000 | | Tampa-Hillsborough County Expressway Authority, Series B | A | 5.000% | 07/01/2042 | 07/01/22 @ 100 | 1,066,470 |

1,000,000 | | Town of Davie FL, Series A | BBB | 6.000% | 04/01/2042 | 04/01/23 @ 100 | 1,152,950 |

| | | | | | | | 11,900,547 |

| | | Hawaii – 1.1% | | | | | |

1,000,000 | | Hawaii Pacific Health, Series B | A– | 5.625% | 07/01/2030 | 07/01/20 @ 100 | 1,120,950 |

| |

See notes to financial statements. | | | | | |

8 l MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT | | | |

| PORTFOLIO OF INVESTMENTS continued | July 31, 2014 |

| | Description | Rating* | Coupon | Maturity | Optional Call Provisions** | Value |

| | | Illinois – 12.0% | | | | | |

$ 1,000,000 | | Chicago Board of Education, General Obligation, Series A | A+ | 5.000% | 12/01/2041 | 12/01/21 @ 100 | $ 1,002,360 |

1,750,000 | | Chicago O’Hare International Airport, Series C | A– | 5.500% | 01/01/2031 | 01/01/21 @ 100 | 1,944,985 |

2,000,000 | | Illinois Finance Authority, Roosevelt University Revenue | Baa3 | 5.500% | 04/01/2037 | 04/01/17 @ 100 | 2,007,180 |

1,000,000 | | Illinois Finance Authority, Rush University Medical Center Revenue, Series C | A | 6.375% | 11/01/2029 | 05/01/19 @ 100 | 1,141,830 |

670,000 | | Illinois Housing Development Authority, AMT, Series A-2 | AA | 5.000% | 08/01/2036 | 02/01/16 @ 100 | 673,270 |

2,000,000 | | Metropolitan Pier & Exposition Authority, Series A | AAA | 5.000% | 06/15/2042 | 06/15/22 @ 100 | 2,100,620 |

1,000,000 | | Railsplitter Tobacco Settlement Authority | A– | 6.000% | 06/01/2028 | 06/01/21 @ 100 | 1,164,340 |

2,000,000 | | State of Illinois, General Obligation, Series A | A– | 5.000% | 03/01/2028 | 03/01/15 @ 100 | 2,003,100 |

| | | | | | | | 12,037,685 |

| | | Indiana – 1.1% | | | | | |

1,000,000 | | Indiana Finance Authority | BB– | 6.000% | 12/01/2026 | 06/01/20 @ 100 | 1,078,130 |

| | | Iowa – 4.5% | | | | | |

1,090,000 | | Iowa Finance Authority | A+ | 5.000% | 08/15/2029 | 08/15/22 @ 100 | 1,174,290 |

1,500,000 | | Iowa Higher Education Loan Authority | BB | 5.500% | 09/01/2025 | 09/01/20 @ 100 | 1,589,490 |

2,000,000 | | Iowa Tobacco Settlement Authority, Series B | B+ | 5.600% | 06/01/2034 | 06/01/17 @ 100 | 1,748,480 |

| | | | | | | | 4,512,260 |

| | | Kentucky – 2.2% | | | | | |

1,000,000 | | County of Owen KY, Waterworks System Revenue, Series B | A– | 5.625% | 09/01/2039 | 09/01/19 @ 100 | 1,077,710 |

1,000,000 | | Kentucky Economic Development Finance Authority, Series A | A2 | 5.625% | 08/15/2027 | 08/15/18 @ 100 | 1,115,370 |

| | | | | | | | 2,193,080 |

| | | Louisiana – 9.8% | | | | | |

1,000,000 | | East Baton Rouge Sewerage Commission, Series A | AA– | 5.250% | 02/01/2034 | 02/01/19 @ 100 | 1,108,460 |

3,000,000 | | Louisiana Local Government Environmental Facilities & Community | | | | | |

| | | Development Authority | BBB | 6.750% | 11/01/2032 | 11/01/17 @ 100 | 3,340,650 |

1,000,000 | | Louisiana Public Facilities Authority, Hospital Revenue | A3 | 5.250% | 11/01/2030 | 05/01/20 @ 100 | 1,044,690 |

1,000,000 | | Parish of DeSoto LA, AMT, Series A | BBB | 5.850% | 11/01/2027 | 11/01/14 @ 100 | 1,000,600 |

1,500,000 | | Parish of St John the Baptist LA, Series A | BBB | 5.125% | 06/01/2037 | 06/01/17 @ 100 | 1,570,230 |

1,600,000 | | State of Louisiana Gasoline & Fuels Tax Revenue, Series C1 | AA | 5.000% | 05/01/2043 | 05/01/23 @ 100 | 1,751,504 |

| | | | | | | | 9,816,134 |

| | | Maryland – 0.5% | | | | | |

500,000 | | Maryland Economic Development Corp. | BB | 5.750% | 09/01/2025 | 09/01/20 @ 100 | 545,335 |

| | | Massachusetts – 6.1% | | | | | |

1,800,000 | | Commonwealth of Massachusetts, (BHAC-CR FGIC)(a) | AA+ | 0.731% | 05/01/2037 | 05/01/17 @ 100 | 1,601,352 |

915,000 | | Massachusetts Educational Financing Authority, AMT, Series JJ | AA | 5.375% | 07/01/2025 | 07/01/21 @ 100 | 1,001,779 |

1,295,000 | | Massachusetts Educational Financing Authority, AMT, Series JJ | AA | 4.700% | 07/01/2026 | 07/01/21 @ 100 | 1,349,183 |

1,000,000 | | Massachusetts Health & Educational Facilities Authority, Series A | BBB | 6.250% | 07/01/2030 | 07/01/19 @ 100 | 1,171,580 |

950,000 | | Massachusetts Housing Finance Agency, AMT | AA– | 5.100% | 12/01/2027 | 06/01/17 @ 100 | 972,220 |

| | | | | | | | 6,096,114 |

| | | Michigan – 4.8% | | | | | |

1,000,000 | | City of Detroit MI, Sewer Disposal Revenue, Series B, (AGM) | AA | 7.500% | 07/01/2033 | 07/01/19 @ 100 | 1,096,580 |

1,000,000 | | City of Detroit MI, Water Supply System Revenue, (AGM) | AA | 7.000% | 07/01/2036 | 07/01/19 @ 100 | 1,084,190 |

500,000 | | Detroit Wayne County Stadium Authority, (AGM) | AA | 5.000% | 10/01/2026 | 10/01/22 @ 100 | 527,355 |

1,000,000 | | Michigan Finance Authority | AA– | 5.000% | 12/01/2031 | 12/01/21 @ 100 | 1,103,580 |

1,030,000 | | Michigan Finance Authority | A– | 5.000% | 07/01/2044 | 07/01/24 @ 100 | 1,045,234 |

| | | | | | | | 4,856,939 |

| | | Minnesota – 1.4% | | | | | |

1,500,000 | | St. Paul Port Authority, AMT | BBB– | 4.500% | 10/01/2037 | 10/01/22 @ 100 | 1,370,805 |

See notes to financial statements. | | | | | |

| | | MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT l 9 |

| PORTFOLIO OF INVESTMENTS continued | July 31, 2014 |

| | Description | Rating* | Coupon | Maturity | Optional Call Provisions** | Value |

| | | Mississippi – 1.1% | | | | | |

$ 1,000,000 | | County of Warren MS, Series A | BBB | 6.500% | 09/01/2032 | 09/01/18 @ 100 | $ 1,114,110 |

| | | Nevada – 1.6% | | | | | |

1,435,000 | | Las Vegas Valley Water District, Series C | AA+ | 5.000% | 06/01/2031 | 06/01/21 @ 100 | 1,585,646 |

| | | New Hampshire – 1.0% | | | | | |

1,000,000 | | New Hampshire Health and Education Facilities Authority Act | BBB | 5.000% | 01/01/2034 | 01/01/22 @ 100 | 1,033,060 |

| | | New Jersey – 8.4% | | | | | |

3,000,000 | | New Jersey Economic Development Authority, Series I(a) | A | 1.660% | 03/01/2028 | 03/01/23 @ 100 | 2,952,540 |

500,000 | | New Jersey Economic Development Authority, Series C | BBB– | 5.000% | 07/01/2032 | 07/01/22 @ 100 | 503,220 |

1,500,000 | | New Jersey Health Care Facilities Financing Authority, (Prerefunded @ 7/1/2019)(d) | NR | 5.750% | 07/01/2039 | 07/01/19 @ 100 | 1,816,215 |

3,000,000 | | New Jersey Transportation Trust Fund Authority, Series A | A | 5.000% | 06/15/2042 | 06/15/22 @ 100 | 3,140,700 |

| | | | | | | | 8,412,675 |

| | | New York – 12.7% | | | | | |

2,750,000 | | Long Island Power Authority, Series A, (Prerefunded @ 9/1/2014)(d) | A– | 5.100% | 09/01/2029 | 09/01/14 @ 100 | 2,759,872 |

2,000,000 | | Metropolitan Transportation Authority, Series E | AA– | 5.000% | 11/15/2043 | 11/15/23 @ 100 | 2,168,160 |

300,000 | | New York City Industrial Development Agency, American Airlines, | | | | | |

| | | JFK International Airport, AMT | NR | 7.500% | 08/01/2016 | N/A | 314,250 |

1,930,000 | | New York City Water & Sewer System, Series FF | AA+ | 5.000% | 06/15/2045 | 06/15/22 @ 100 | 2,090,113 |

1,000,000 | | New York City Water & Sewer System, Series BB | AA+ | 5.000% | 06/15/2047 | 12/15/22 @ 100 | 1,085,970 |

600,000 | | New York State Dormitory Authority, Series B | A– | 5.250% | 07/01/2024 | 07/01/17 @ 100 | 648,930 |

1,000,000 | | New York State Dormitory Authority, Series A | BBB | 5.000% | 07/01/2032 | 07/01/22 @ 100 | 1,051,930 |

1,500,000 | | Suffolk County Industrial Development Agency, AMT | A– | 5.250% | 06/01/2027 | 06/01/15 @ 100 | 1,502,175 |

1,000,000 | | Troy Industrial Development Authority | A– | 5.000% | 09/01/2031 | 09/01/21 @ 100 | 1,103,110 |

| | | | | | | | 12,724,510 |

| | | Ohio – 3.2% | | | | | |

2,000,000 | | American Municipal Power, Inc., Series B | A | 5.000% | 02/15/2042 | 02/15/22 @ 100 | 2,123,540 |

1,000,000 | | Ohio Air Quality Development Authority | BBB– | 5.625% | 06/01/2018 | N/A | 1,111,660 |

| | | | | | | | 3,235,200 |

| | | Oklahoma – 1.1% | | | | | |

1,000,000 | | Oklahoma Development Finance Authority | AA | 5.000% | 02/15/2034 | 02/15/22 @ 100 | 1,067,120 |

| | | Pennsylvania – 7.7% | | | | | |

1,110,000 | | City of Philadelphia PA, General Obligation, Series A, (Assured Gty) | AA | 5.375% | 08/01/2030 | 08/01/19 @ 100 | 1,225,351 |

1,100,000 | | City of Philadelphia PA, General Obligation | A+ | 5.875% | 08/01/2031 | 08/01/16 @ 100 | 1,183,380 |

1,000,000 | | County of Lehigh PA | A+ | 4.000% | 07/01/2043 | 07/01/22 @ 100 | 953,780 |

1,500,000 | | Delaware River Port Authority | BBB | 5.000% | 01/01/2027 | 01/01/23 @ 100 | 1,622,820 |

1,000,000 | | Pennsylvania Higher Educational Facilities Authority, Series B | AA– | 6.000% | 08/15/2026 | 08/15/18 @ 100 | 1,149,450 |

1,000,000 | | Pennsylvania Higher Educational Facilities Authority, Series A | BBB | 5.000% | 05/01/2037 | 11/01/17 @ 100 | 1,044,250 |

500,000 | | State Public School Building Authority | A+ | 5.000% | 04/01/2032 | 04/01/22 @ 100 | 534,370 |

| | | | | | | | 7,713,401 |

| | | Puerto Rico – 1.0% | | | | | |

1,215,000 | | Puerto Rico Sales Tax Financing Corp. | BBB | 5.250% | 08/01/2040 | 08/01/21 @ 100 | 972,340 |

| | | Rhode Island – 1.4% | | | | | |

1,300,000 | | Rhode Island Convention Center Authority, Series A, (Assured Gty) | AA | 5.500% | 05/15/2027 | 05/15/19 @ 100 | 1,435,070 |

| | | South Carolina – 4.6% | | | | | |

2,500,000 | | County of Florence SC, Series A, (AGM) | AA | 5.250% | 11/01/2027 | 11/01/14 @ 100 | 2,518,550 |

1,000,000 | | County of Georgetown SC, AMT, Series A | BBB | 5.300% | 03/01/2028 | 03/01/15 @ 100 | 1,000,590 |

1,000,000 | | South Carolina State Public Service Authority, Series E | AA– | 5.000% | 12/01/2048 | 12/01/23 @ 100 | 1,070,690 |

| | | | | | | | 4,589,830 |

See notes to financial statements. | | | | | |

10 l MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT | | | |

| PORTFOLIO OF INVESTMENTS continued | July 31, 2014 |

| | Description | Rating* | Coupon | Maturity | Optional Call Provisions** | Value |

| | | South Dakota – 1.2% | | | | | |

$ 1,200,000 | | South Dakota Health & Educational Facilities Authority, Series A | A+ | 5.250% | 11/01/2034 | 11/01/14 @ 100 | $ 1,203,948 |

| | | Tennessee – 3.3% | | | | | |

2,500,000 | | Knox County Health Educational & Housing Facility Board | BBB+ | 5.250% | 04/01/2027 | 04/01/17 @ 100 | 2,622,875 |

620,000 | | Metropolitan Nashville Airport Authority | Baa3 | 5.200% | 07/01/2026 | 07/01/20 @ 100 | 662,464 |

| | | | | | | | 3,285,339 |

| | | Texas – 13.2% | | | | | |

1,000,000 | | Fort Bend County Industrial Development Corp., Series B | Baa3 | 4.750% | 11/01/2042 | 11/01/22 @ 100 | 1,021,130 |

2,000,000 | | Lower Colorado River Authority | A | 6.250% | 05/15/2028 | 05/15/18 @ 100 | 2,342,760 |

2,315,000 | | Matagorda County Navigation District No. 1, AMT, (AMBAC) | A | 5.125% | 11/01/2028 | N/A | 2,590,670 |

2,000,000 | | North Texas Tollway Authority, Series A | A– | 5.625% | 01/01/2033 | 01/01/18 @ 100 | 2,225,620 |

2,100,000 | | San Leanna Educational Facilities Corp. | BBB+ | 5.125% | 06/01/2036 | 06/01/17 @ 100 | 2,139,858 |

480,000 | | Tarrant County Cultural Education Facilities Finance Corp., (Assured Gty) | AA | 5.750% | 07/01/2018 | N/A | 539,717 |

150,000 | | Tarrant County Cultural Education Facilities Finance Corp., | | | | | |

| | | (Prerefunded @ 7/1/2016), (Assured Gty)(d) | AA | 5.750% | 07/01/2018 | N/A | 157,308 |

2,000,000 | | Tarrant County Cultural Education Facilities Finance Corp. | AA– | 5.000% | 10/01/2043 | 10/01/23 @ 100 | 2,163,120 |

| | | | | | | | 13,180,183 |

| | | Vermont – 2.8% | | | | | |

2,800,000 | | Vermont Student Assistance Corp., AMT, Series B-A2(a) (e) | A | 3.238% | 12/03/2035 | 09/01/14 @ 100 | 2,809,100 |

| | | Virginia – 1.5% | | | | | |

1,250,000 | | Washington County Industrial Development Authority, Series C | BBB+ | 7.500% | 07/01/2029 | 01/01/19 @ 100 | 1,466,938 |

| | | Washington – 3.3% | | | | | |

1,000,000 | | Spokane Public Facilities District, Series A | A+ | 5.000% | 12/01/2038 | 06/01/23 @ 100 | 1,083,720 |

1,000,000 | | Tes Properties | AA+ | 5.625% | 12/01/2038 | 06/01/19 @ 100 | 1,129,450 |

1,000,000 | | Washington Higher Education Facilities Authority, Series A | A3 | 5.250% | 04/01/2043 | 04/01/23 @ 100 | 1,090,640 |

| | | | | | | | 3,303,810 |

| | | Wisconsin – 2.4% | | | | | |

1,250,000 | | Wisconsin Health & Educational Facilities Authority, Series A | AA+ | 5.000% | 11/15/2036 | 11/15/16 @ 100 | 1,323,000 |

1,000,000 | | WPPI Energy, Series A | A | 5.000% | 07/01/2037 | 07/01/23 @ 100 | 1,085,190 |

| | | | | | | | 2,408,190 |

| | | Wyoming – 4.1% | | | | | |

4,000,000 | | County of Sweetwater WY, AMT(e) | A– | 5.600% | 12/01/2035 | 12/01/15 @ 100 | 4,066,400 |

| | | Total Municipal Bonds – 164.9% | | | | | |

| | | (Cost $155,539,492) | | | | | 165,110,597 |

| | | Preferred Shares – 2.1% | | | | | |

| | | Diversified Financial Services – 2.1% | | | | | |

2,000,000 | | Centerline Equity Issuer Trust(b) | Aaa | 5.750% | 05/15/2015 | N/A | 2,051,600 |

| | | (Cost $2,000,000) | | | | | |

| | | Total Long-Term Investments - 167.0% | | | | | |

| | | (Cost $157,539,492) | | | | | 167,162,197 |

| |

| |

| |

| |

See notes to financial statements. | | | | | |

| | | MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT l 11 |

| PORTFOLIO OF INVESTMENTS continued | July 31, 2014 |

| | Description | Value |

| | | Money Market – 0.7% | |

| 718,921 | | JPMorgan Tax Free Money Market | $ 718,921 |

| | | (Cost $718,921) | |

| | | Total Investments – 167.7% | |

| | | (Cost $158,258,413) | 167,881,118 |

| | | Other Assets in excess of Liabilities – 1.7% | 1,694,304 |

| | | Preferred Shares, at redemption value – (-69.4% of Net Assets | |

| | | Applicable to Common Shareholders or -41.4% of Total Investments) | (69,450,000) |

| | | Net Assets Applicable to Common Shareholders – 100.0% | $ 100,125,422 |

AGM – Insured by Assured Guaranty Municipal Corporation | |

AMBAC – Insured by Ambac Assurance Corporation | |

AMT – Income from this security is a preference item under the Alternative Minimum Tax. | |

BHAC – Insured by Bershire Hathaway Assurance Corp. | |

Assured Gty – Insured by Assured Guaranty Corporation | |

CIFG – Insured by CIFG Assurance North America, Inc. | |

FGIC – Insured by Financial Guaranty Insurance Company | |

FHA – Guaranteed by Federal Housing Administration | |

N/A – Not Applicable | |

| * | Ratings shown are per Standard & Poor’s Rating Group (“S&P”), Moody’s Investor Services, Inc. (“Moody’s”) or Fitch Ratings (“Fitch”). Securities classified as NR are not rated. (For securities not rated by S&P, the rating by Moody’s is provided. Likewise, for securities not rated by S&P and Moody’s, the rating by Fitch is provided.) All ratings are unaudited. The ratings apply to the credit worthiness of the issuers of the underlying securities and not to the Fund or its shares. |

| ** | Date and price of the earliest optional call or put provision. There may be other call provisions at varying prices at later dates. |

| | All percentages shown in the Portfolio of Investments are based on Net Assets Applicable to Common Shareholders, unless otherwise noted. |

| (a) | Floating or variable rate coupon. The rate shown is as of July 31, 2014. |

| (b) | Securities are exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At July 31, 2014 these securities amounted to $4,148,480, which represents 4.1% of net assets applicable to common shares. |

| (c) | Zero coupon bond. |

| (d) | The bond is prerefunded. U.S. government or U.S. government agency securities, held in escrow, are used to pay interest on this security, as well as to retire the bond in full at the date and price indicated under the Optional Call Provisions. |

| (e) | All or a portion of these securities have been physically segregated as collateral for borrowings outstanding, of which there were none as of year end. As of July 31, 2014, the total amount seg- regated was $6,875,500. |

See notes to financial statements.

12 l MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT

| PORTFOLIO OF INVESTMENTS continued | July 31, 2014 |

Portfolio composition and holdings are subject to change daily. For more information, please visit guggenheiminvestments.com/mzf. The above summaries are provided for informational purposes only and should not be viewed as recommendations. Past performance does not guarantee future results.

See notes to financial statements.

MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT l 13

STATEMENT OF ASSETS AND LIABILITIES | | July 31, 2014 |

| | |

| | |

Assets | | | |

Investments, at value (cost $158,258,413) | | $ | 167,881,118 | |

Interest receivable | | | 1,865,185 | |

Other assets | | | 11,581 | |

Total assets | | | 169,757,884 | |

Liabilities | | | | |

Investment advisory fee payable | | | 43,134 | |

Servicing agent fee payable | | | 28,716 | |

Distributions payable - preferred shareholders | | | 31,475 | |

Administration fee payable | | | 3,564 | |

Accrued expenses and other liabilities | | | 75,573 | |

Total liabilities | | | 182,462 | |

Preferred Shares, at redemption value | | | | |

$.001 par value per share; 2,778 Auction Market Preferred Shares authorized, | | | | |

issued and outstanding at $25,000 per share liquidation preference | | | 69,450,000 | |

Net Assets Applicable to Common Shareholders | | $ | 100,125,422 | |

Composition of Net Assets Applicable to Common Shareholders | | | | |

Common stock, $.001 par value per share; unlimited number of shares authorized, | | | | |

6,800,476 shares issued and outstanding | | $ | 6,800 | |

Additional paid-in capital | | | 95,359,485 | |

Net unrealized appreciation on investments | | | 9,622,705 | |

Accumulated net investment loss | | | (20,377 | ) |

Accumulated net realized loss on investments | | | (4,843,191 | ) |

Net Assets Applicable to Common Shareholders | | $ | 100,125,422 | |

Net Asset Value Applicable to Common Shareholders (based on 6,800,476 common shares outstanding) | | $ | 14.72 | |

See notes to financial statements.

14 l MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT

STATEMENT OF OPERATIONS For the year ended July 31, 2014 | July 31, 2014 |

Investment Income | | | | | | |

Interest | | | | | $ | 7,818,352 | |

Expenses | | | | | | �� | |

Investment advisory fee | | $ | 639,871 | | | | | |

Servicing agent fee | | | 426,581 | | | | | |

Professional fees | | | 120,265 | | | | | |

Auction agent fees - preferred shares | | | 119,233 | | | | | |

Fund accounting | | | 66,683 | | | | | |

Trustees’ fees and expenses | | | 46,708 | | | | | |

Administrative fee | | | 45,119 | | | | | |

Printing expenses | | | 34,238 | | | | | |

NYSE listing fee | | | 21,863 | | | | | |

Transfer agent fee | | | 21,079 | | | | | |

Insurance | | | 15,008 | | | | | |

Custodian fee | | | 6,369 | | | | | |

Line of credit fee | | | 416 | | | | | |

Miscellaneous | | | 6,588 | | | | | |

Total expenses | | | | | | | 1,570,021 | |

Investment advisory fee waived | | | | | | | (147,662 | ) |

Servicing agent fee waived | | | | | | | (98,442 | ) |

Net expenses | | | | | | | 1,323,917 | |

Net investment income | | | | | | | 6,494,435 | |

Realized and Unrealized Gain on Investments | | | | | | | | |

Net realized gain | | | | | | | 273,476 | |

Net change in unrealized appreciation | | | | | | | 7,409,664 | |

Net realized and unrealized gain on investments | | | | | | | 7,683,140 | |

Distributions to Auction Market Preferred Shareholders from | | | | | | | | |

Net investment income | | | | | | | (886,027 | ) |

Net Increase in Net Assets Applicable to Common Shareholders Resulting from Operations | | | | | | $ | 13,291,548 | |

See notes to financial statements.

MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT l 15

STATEMENTS OF CHANGES IN NET ASSETS | | July 31, 2014 |

| | |

| | |

| | | | | | | |

Increase (decrease) in Net Assets Applicable to Common | | | | | | |

Shareholders Resulting from Operations: | | | | | | |

Net investment income | | $ | 6,494,435 | | | $ | 6,912,678 | |

Net realized gain on investments | | | 273,476 | | | | 1,224,194 | |

Net change in unrealized appreciation (depreciation) on investments | | | 7,409,664 | | | | (13,043,021 | ) |

Distributions to auction market preferred shareholders from net investment income | | | (886,027 | ) | | | (942,583 | ) |

Net increase (decrease) in net assets applicable to common shareholders | | | | | | | | |

resulting from operations | | | 13,291,548 | | | | (5,848,732 | ) |

Distributions to common shareholders from | | | | | | | | |

Net investment income | | | (5,739,602 | ) | | | (6,400,922 | ) |

Capital share transactions | | | | | | | | |

Reinvestment of dividends | | | – | | | | 200,761 | |

Total change in net assets applicable to common shareholders | | | 7,551,946 | | | | (12,048,893 | ) |

Net assets applicable to common shareholders: | | | | | | | | |

Beginning of period | | | 92,573,476 | | | | 104,622,369 | |

End of period (including undistributed net investment income | | | | | | | | |

(loss) of ($20,377) and $110,817, respectively) | | $ | 100,125,422 | | | $ | 92,573,476 | |

See notes to financial statements.

16 l MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT

FINANCIAL HIGHLIGHTS | | | | | | | | July 31, 2014 |

| | |

| | |

Per share operating performance for one common share outstanding throughout each period | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 13.61 | | | $ | 15.41 | | | $ | 14.02 | | | $ | 14.40 | | | $ | 12.73 | |

Investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (a) | | | 0.95 | | | | 1.02 | | | | 1.09 | | | | 1.12 | | | | 1.06 | |

Net realized and unrealized gain/(loss) on investments | | | 1.13 | | | | (1.74 | ) | | | 1.43 | | | | (0.36 | ) | | | 1.72 | |

Distributions to preferred shareholders from net investment income (common share equivalent basis) | | | (0.13 | ) | | | (0.14 | ) | | | (0.14 | ) | | | (0.15 | ) | | | (0.14 | ) |

Total from investment operations | | | 1.95 | | | | (0.86 | ) | | | 2.38 | | | | 0.61 | | | | 2.64 | |

| | |

Distributions to common shareholders from net investment income | | | (0.84 | ) | | | (0.94 | ) | | | (0.99 | ) | | | (0.99 | ) | | | (0.97 | ) |

Net asset value, end of period | | $ | 14.72 | | | $ | 13.61 | | | $ | 15.41 | | | $ | 14.02 | | | $ | 14.40 | |

Market value, end of period | | $ | 13.57 | | | $ | 12.46 | | | $ | 16.21 | | | $ | 13.48 | | | $ | 14.53 | |

Total investment return (b) | | | | | | | | | | | | | | | | | | | | |

Net asset value | | | 14.87 | % | | | -6.01 | % | | | 17.50 | % | | | 4.57 | % | | | 21.21 | % |

Market value | | | 16.29 | % | | | -18.13 | % | | | 28.56 | % | | | -0.32 | % | | | 31.45 | % |

Ratios and supplemental data | | | | | | | | | | | | | | | | | | | | |

Net assets, end of period (thousands) | | $ | 100,125 | | | $ | 92,573 | | | $ | 104,622 | | | $ | 94,913 | | | $ | 97,190 | |

Ratio of expenses to average net assets (including interest expense and net of fee waivers) (c)(d) | | | 1.40 | % | | | 1.33 | % | | | 1.36 | % | | | 1.46 | % | | | 1.35 | % |

Ratio of expenses to average net assets (including interest expense and excluding fee waivers) (c)(d) | | | 1.66 | % | | | 1.58 | % | | | 1.62 | % | | | 1.72 | % | | | 1.69 | % |

Ratio of net investment income to average net assets (c) | | | 6.86 | % | | | 6.70 | % | | | 7.38 | % | | | 8.09 | % | | | 7.68 | % |

Portfolio turnover | | | 15 | % | | | 23 | % | | | 15 | % | | | 8 | % | | | 6 | % |

Preferred shares, at redemption value ($25,000 per share liquidation preference) (thousands) | | $ | 69,450 | | | $ | 69,450 | | | $ | 69,450 | | | $ | 69,450 | | | $ | 69,450 | |

Preferred shares asset coverage per share | | $ | 61,042 | | | $ | 58,324 | | | $ | 62,661 | | | $ | 59,166 | | | $ | 59,986 | |

| (a) | Based on average shares outstanding during the period. |

| (b) | Total investment return is calculated assuming a purchase of a common share at the beginning of the period and a sale on the last day of the period reported either at net asset value (NAV) or market price per share. Dividends and distributions are assumed to be reinvested at NAV for returns at NAV or in accordance with the Fund’s dividend reinvestment plan for returns at market value. Total investment return does not reflect brokerage commissions. A return calculated for a period of less than one year is not annualized. |

| (c) | Calculated on the basis of income and expenses applicable to both common and preferred shares relative to average net assets of common shareholders. |

| (d) | The impact of interest expense is less than 0.01%. |

See notes to financial statements.

MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT l 17

| NOTES TO FINANCIAL STATEMENTS | July 31, 2014 |

Note 1 – Organization:

The Managed Duration Investment Grade Municipal Fund (the “Fund”) was organized as a Delaware statutory trust on May 20, 2003. The Fund is registered as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended. The Fund’s investment objective is to provide its common shareholders with high current income exempt from regular federal income tax while seeking to protect the value of the Fund’s assets during periods of interest rate volatility. Prior to commencing operations on August 27, 2003, the Fund had no operations other than matters relating to its organization and registration and the sale and issuance of 6,981 common shares of beneficial interest to MBIA Capital Management Corp. (now known as Cutwater Investor Services Corp.).

Note 2 – Accounting Policies:

The preparation of financial statements in accordance with US generally accepted accounting principles (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from those estimates.

The following is a summary of significant accounting policies followed by the Fund.

(a) Valuation of Investments: The Board of Trustees of the Fund (the “Board”) has adopted policies and procedures for the valuation of the Fund’s investments (the “Valuation Procedures”). Pursuant to the Valuation Procedures, while the Board retains responsibility for the valuation process, the Board has delegated to Cutwater Investor Services Corp. (the “Adviser”), the day-to-day responsibility for implementing the Valuation Procedures, including, under most circumstances, the responsibility for determining the fair value of the Fund’s securities or other assets.

The municipal bonds and preferred shares in which the Fund invests are traded primarily in the over-the-counter markets. In determining net asset value, the Fund uses the valuations of portfolio securities furnished by a pricing service approved by the Board of Trustees. The pricing service typically values portfolio securities at the bid price or the yield equivalent when quotations are readily available. Securities for which quotations are not readily available are valued at fair market value on a consistent basis as determined by the pricing service using a matrix system to determine valuations. The procedures of the pricing service and its valuations are reviewed by the officers of the Fund under the general supervision of the Board of Trustees.

Investments for which market quotations are not readily available are fair valued as determined in good faith by the Adviser, pursuant to methods established or ratified by the Board. Valuations in accordance with these methods are intended to reflect each security’s (or asset’s) “fair value.” Each such determination is based on a consideration of all relevant factors, which are likely to vary from one pricing context to another. Examples of such factors may include, but are not limited to: (i) the type of security, (ii) the initial cost of the security, (iii) the existence of any contractual restrictions on the security’s disposition, (iv) the price and/or yield and extent of public trading in similar securities of the issuer or of comparable companies, (v) quotations or evaluated prices from broker-dealers and/or pricing services, (vi) information obtained from the issuer, analysts, and/or the appropriate stock exchange (for exchange traded securities), (vii) an analysis of the company’s financial statements, and (viii) an evaluation of the forces that influence the issuer and the market(s) in which the security is purchased and sold (e.g. the existence of pending merger activity, public offerings or tender offers that might affect the value of the security).

There are three different categories for valuations. Level 1 valuations are those based upon quoted prices in active markets. Level 2 valuations are those based upon quoted prices in inactive markets or based upon significant observable inputs (e.g. yield curves; benchmark interest rates; indices). Level 3 valuations are those based upon unobservable inputs (e.g. discounted cash flow analysis; non-market based methods used to determine fair valuation).

The Fund values Level 1 securities using readily available market quotations in active markets. Money market funds are valued at net asset value. The Fund values Level 2 fixed income securities using independent pricing providers who employ matrix pricing models utilizing market prices, broker quotes and prices of securities with comparable maturities and qualities. The Fund values Level 2 equity securities using various observable market inputs as described above. The Fund did not have any Level 3 securities during the period ended July 31, 2014.

Transfers between valuation levels, if any, are in comparison to the valuation levels at the end of the previous fiscal year, and are effective using the fair value as of the end of the current fiscal period.

The following table represents the Fund’s investments carried on the Statement of Assets and Liabilities by caption and by level within the fair value hierarchy as of July 31, 2014:

Valuations (in $000s) | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Description | | | | | | | | | | | | |

Assets: | | | | | | | | | | | | |

Municipal Bonds | | $ | – | | | $ | 165,110 | | | $ | – | | | $ | 165,110 | |

Preferred Shares | | | – | | | | 2,052 | | | | – | | | | 2,052 | |

Money Market | | | 719 | | | | – | | | | – | | | | 719 | |

Total | | $ | 719 | | | $ | 167,162 | | | $ | – | | | $ | 167,881 | |

There were no transfers between levels for the year ended July 31, 2014.

(b) Investment Transactions and Investment Income: Investment transactions are accounted for on the trade date. Realized gains and losses on investments are determined on the identified cost basis. Interest income, including the amortization of premiums and accretion of discount, is accrued daily.

18 l MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT

| NOTES TO FINANCIAL STATEMENTS continued | July 31, 2014 |

(c) Dividends and Distributions: The Fund declares and pays on a monthly basis dividends from net investment income to common shareholders. Distributions of net realized capital gains, if any, will be paid at least annually. Dividends and distributions to shareholders are recorded on the ex-dividend date. Dividends and distributions to preferred shareholders are accrued and determined as described in Note 6.

(d) Inverse Floating Rate Investments and Floating Rate Note Obligations: Inverse floating rate instruments are notes whose coupon rate fluctuates inversely to a predetermined interest rate index. These instruments typically involve greater risks than a fixed rate municipal bond. In particular, the holder of these inverse floating rate instruments retain all credit and interest rate risk associated with the full underlying bond and not just the par value of the inverse floating rate instrument. As such, these instruments should be viewed as having inherent leverage and therefore involve many of the risks associated with leverage. Leverage is a speculative technique that may expose the Fund to greater risk and increased costs. Leverage may cause the Fund’s net asset value to be more volatile than if it had not been leveraged because leverage tends to magnify the effect of any increases or decreases in the value of the Fund’s portfolio securities. The use of leverage may also cause the Fund to liquidate portfolio positions when it may not be advantageous to do so in order to satisfy its obligations with respect to inverse floating rate instruments.

The Fund may invest in inverse floating rate securities through either a direct purchase or through the transfer of bonds to a dealer trust in exchange for cash and/or residual interests in the dealer trust. For those inverse floating rate securities purchased directly, the instrument is included in the Portfolio of Investments with income recognized on an accrual basis. The Fund did not invest in inverse floating rate securities during the year ended July 31, 2014.

Note 3 – Agreements:

Pursuant to an Investment Advisory Agreement (the “Advisory Agreement”) between the Adviser and the Fund, the Adviser is responsible for the daily management of the Fund’s portfolio, which includes buying and selling securities for the Fund, as well as investment research, subject to the direction of the Fund’s Board of Trustees. The Adviser is a subsidiary of Cutwater Holdings, LLC which, in turn, is a wholly-owned subsidiary of MBIA, Inc. The Advisory Agreement provides that the Fund shall pay to the Adviser a monthly fee for its services at the annual rate of 0.39% of the sum of the Fund’s average daily managed assets. (“Managed Assets” represent the Fund’s total assets including the assets attributable to the proceeds from any financial leverage but excluding the assets attributable to floating rate note obligations, minus liabilities, other than debt representing financial leverage.) The Adviser contractually agreed to waive a portion of the management fees it is entitled to receive from the Fund at the annual rate of 0.09% of the Fund’s average daily Managed Assets.

Pursuant to a Servicing Agreement, Guggenheim Funds Distributors, LLC (the “Servicing Agent”) acts as servicing agent to the Fund. The Servicing Agent receives an annual fee from the Fund, payable monthly in arrears, in an amount equal to 0.26% of the average daily value of the Fund’s Managed Assets. The Servicing Agent contractually agreed to waive a portion of the servicing fee it is entitled to receive from the Fund at the annual rate of 0.06% of the average daily value of the Fund’s Managed Assets.

Rydex Fund Services, LLC (“RFS”), an affiliate of the Servicing Agent, provides fund administration services to the Fund. As compensation for these services RFS receives a fund administration fee payable monthly at the annual rate set forth below as a percentage of the average daily managed assets of the Fund:

Managed Assets | Rate |

First $200,000,000 | 0.0275% |

Next $300,000,000 | 0.0200% |

Next $500,000,000 | 0.0150% |

Over $1,000,000,000 | 0.0100% |

The Bank of New York Mellon (“BNY”) acts as the Fund’s custodian, accounting agent and auction agent. As custodian, BNY is responsible for the custody of the Fund’s assets. As accounting agent, BNY is responsible for maintaining the books and records of the Fund. As auction agent, BNY is responsible for conducting the auction of the preferred shares.

Certain officers and/or trustees of the Fund are officers and/or directors of the Adviser and the Servicing Agent. The Fund does not compensate its officers or trustees who are officers, directors and/or employees of the aforementioned firms.

Note 4 – Federal Income Taxes:

The Fund intends to comply with the requirements of Subchapter M of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies. Accordingly, no provision for US federal income taxes is required. In addition, by distributing substantially all of its ordinary income and long-term capital gains, if any, during each calendar year, the Fund intends not to be subject to U.S. federal excise tax.

At July 31, 2014, the following reclassification was made to the capital accounts of the Fund to reflect permanent book/tax differences relating to expired capital loss carryovers. Net investment income, net realized gains and net assets were not affected by these changes.

Accumulated Net Investment Loss | Accumulated Net Realized Loss | Additional Paid-In Capital |

$ – | $504,962 | $(504,962) |

Information on the tax components of investments as of July 31, 2014 is as follows:

| | | |

$158,291,623 | $10,899,524 | $(1,310,029) | $9,589,495 |

The difference between book and tax basis cost of investments is due to book/tax differences on the recognition of partnership/trust income.

MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT l 19

| NOTES TO FINANCIAL STATEMENTS continued | July 31, 2014 |

As of July 31, 2014, the components of accumulated earnings/(losses) on a tax basis were as follows:

| | | | | | |

2014 | $59,450 | $ – | $(4,858,333) | $9,589,495 | $(31,475) |

The cumulative timing differences under tax basis accumulated capital and other losses as of July 31, 2014 are due to investments in partnerships/trusts.

As of July 31, 2014, the Fund had a capital loss carryforward of $4,772,269 available to offset possible future capital gains. For the year ended July 31, 2014, $864,502 of the capital loss carryforward was utilized or expired. The $4,772,269 capital loss carryforward is set to expire on July 31, 2017. Per the Regulated Investment Company Modernization Act of 2010, capital loss carryforwards generated in taxable years beginning after December 22, 2010 must be fully used before capital loss carryforwards generated in taxable years prior to December 22, 2010, therefore, under certain circumstances, capital loss carryforwards available as of the report date may expire unused.

Capital losses incurred after October 31 (“post-October losses”) within the taxable year are deemed to arise on the first business day of the Fund’s next tax year. For the year ended July 31, 2014, the Funds incurred and will elect to defer $86,064 as post-October losses.

Distributions paid to shareholders during the tax years ended July 31, 2014 and 2013, were characterized as follows:

| | | | |

2014 | $6,510,284 | $115,345 | $6,625,629 |

2013 | $7,336,722 | $6,783 | $7,343,505 |

For all open tax years and all major jurisdictions, management of the Fund has concluded that there are no significant uncertain tax positions that would require recognition in the financial statements. Uncertain tax positions are tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns that would not meet a more-likely-than-not threshold of being sustained by the applicable tax authority and would be recorded as a tax expense in the current year. Open tax years are those years that are open for examination by taxing authorities (i.e. generally the last four tax year ends and the interim tax period since then). Furthermore, management of the Fund is also not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

Note 5 – Investment Transactions:

Purchases and sales of investment securities, excluding short-term investments, for the year ended July 31, 2014, aggregated $24,645,043 and $25,362,989, respectively.

Note 6 – Capital:

There are an unlimited number of $.001 par value common shares of beneficial interest authorized and 6,800,476 common shares outstanding at July 31, 2014, of which the Adviser owned 13,446 shares.

Transactions in common shares were as follows: |

| | | |

| | | |

Beginning shares | 6,800,476 | 6,787,494 |

Shares issued through dividend reinvestment | – | 12,982 |

Ending shares | 6,800,476 | 6,800,476 |

On October 27, 2003, the Fund issued 1,389 shares of Auction Market Preferred Shares (“AMPS”), Series M7 and 1,389 shares of AMPS, Series W28. The preferred shares have a liquidation value of $25,000 per share plus any accumulated unpaid dividends. As of July 31, 2014, the Fund had 1,389 shares each of AMPS, Series M7 and W28, outstanding. Dividends on the preferred shares are cumulative at a rate that is set by auction procedures. Distributions of net realized capital gains, if any, are made annually.

The broad auction-rate preferred securities market, including the Fund’s AMPS, has experienced considerable disruption since mid-February 2008. The result has been failed auctions on nearly all auction-rate preferred shares, including the Fund’s AMPS. A failed auction is not a default, nor does it require the redemption of the Fund’s AMPS.

Provisions in the AMPS offering documents establish a maximum rate in the event of a failed auction. The AMPS reference rate is the higher of LIBOR or 90% of the taxable equivalent of the short-term municipal bond rate. The maximum rate, for auctions for which the Fund has not given notice that the auction will consist of net capital gains or other taxable income, is the higher of the reference rate times 125% or the reference rate plus 1.25%.

Management will continue to monitor events in the marketplace and continue to evaluate the Fund’s leverage as well as any alternative that may be available.

The range of dividend rates on the Fund’s AMPS for the year ended July 31, 2014, were as follows:

Series | Low | High | At 7/31/14 | |

M7 | 1.218% | 1.429% | 1.372% | 8/4/14 |

W28 | 1.218% | 1.373% | 1.373% | 8/6/14 |

The Fund is subject to certain limitations and restrictions while the AMPS are outstanding. Failure to comply with these limitations and restrictions could preclude the Fund from declaring any dividends or distributions to common shareholders or repurchasing common shares and/or could trigger the mandatory redemption of AMPS at their liquidation value plus any accrued dividends.

On April 1, 2014, Standard & Poor’s Ratings Services (“S&P”) notified the Servicing Agent and Cutwater that S&P downgraded the Fund’s AMPS from ‘AAA’ to ‘AA’.

20 l MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT

| NOTES TO FINANCIAL STATEMENTS continued | July 31, 2014 |

The Fund’s AMPS, which are entitled to one vote per share, generally vote with the common shares but vote separately as a class to elect two Trustees and on any matters affecting the rights of the Fund’s AMPS.

Note 7 – Borrowings:

The Fund has an uncommitted $2,000,000 line of credit with BNY. Interest on the amount borrowed is based on the Federal Funds Rate plus a spread on outstanding balances. At July 31, 2014, there was a $0 balance in connection with the Fund’s uncommitted line of credit. The average daily amount of borrowings during the year ended July 31, 2014 was $48,877 with a related weighted average interest rate of 0.84%. The maximum amount outstanding during the year ended July 31, 2014, was $950,000.

Note 8 – Indemnifications:

In the normal course of business, the Fund enters into contracts that contain a variety of representations, which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would require future claims that may be made against the Fund that have not yet occurred. However, the Fund expects the risk of loss to be remote.

Note 9 – Subsequent Events:

The Fund evaluated subsequent events through the date the financial statements were available for issue and determined there were no additional material events that would require recognition or disclosure in the Fund’s financial statements, except as noted below.

Dividend Declarations – Common Shareholders

The Fund has declared the following dividends to common shareholders:

| | | | |

$0.0650 | 8/01/14 | 8/13/14 | 8/15/14 | 8/29/14 |

$0.0650 | 9/02/14 | 9/11/14 | 9/15/14 | 9/30/14 |

MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT l 21

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | July 31, 2014 |

The Board of Trustees and Shareholders of

Managed Duration Investment Grade Municipal Fund

We have audited the accompanying statement of assets and liabilities of Managed Duration Investment Grade Municipal Fund (the Fund), including the portfolio of investments, as of July 31, 2014, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of July 31, 2014, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Managed Duration Investment Grade Municipal Fund at July 31, 2014, the results of its operations for the year then ended, the changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended in conformity with U.S. generally accepted accounting principles.

Chicago, Illinois

September 24, 2014

22 l MZF l MANAGED DURATION INVESTMENT GRADE MUNICIPAL FUND ANNUAL REPORT

SUPPLEMENTAL INFORMATION (Unaudited) | July 31, 2014 |

Federal Income Tax Information

Subchapter M of the Internal Revenue Code of 1986, as amended, requires the Fund to advise shareholders within 60 days of the Fund’s tax year end (July 31, 2014) as to the federal tax status of dividends and distributions received by shareholders during such tax period. Accordingly, please note that the majority of dividends paid from net investment income from the Fund during the tax period ended July 31, 2014 was federally exempt interest dividends. The Fund has invested in municipal bonds containing market discount, whose accretion is taxable and accordingly, 1.74% of the dividends paid from net investment income during the tax period are attributable to this taxable income. Therefore, the Fund designated $6,510,284 as tax-exempt income.