February 14, 2018

VIA EMAIL AND EDGAR

Ms. Lisa Vanjoske and Mr. Jim Rosenberg

Division of Corporation Finance

Office of Healthcare & Insurance

United States Securities and Exchange Commission

100 F Street N.E.

Washington D.C. 20549

Re: Letter Dated January 23, 2018

Aspen Insurance Holdings Limited

Form 10-K for the Fiscal Year Ended December 31, 2016

Filed February 22, 2017

File No. 001-31909

Dear Ms. Vanjoske and Mr. Rosenberg:

We are responding to the letter dated January 23, 2018 (the “Letter”) from the staff (the “Staff”) of the United States Securities and Exchange Commission (the “Commission”) which was in response to our letter dated January 9, 2018 concerning the Form 10-K for the year ended December 31, 2016 of Aspen Insurance Holdings Limited and its subsidiaries (collectively, the “Company”, “we” or “our”).

Set forth below are the Company’s responses to the comments raised by the Staff in the Letter. For the convenience of the Staff, we have repeated the Commission’s comments (displayed in italics) immediately prior to our responses.

Form 10-K for Fiscal Year Ended December 31, 2016

Notes to the Audited Consolidated Financial Statements

12. Reserves for Losses and Loss Adjustment Expenses, page F-41

| 1. | “We note from the tables you provided us in response to our prior comment 2 that: |

| • | Claims payment patterns and duration vary considerably among lines of business within both the Aspen Insurance and Aspen Re reporting segments. |

| • | Development for each line of business differs significantly both in amount and directionally (i.e. favorably versus unfavorably) among the lines of business within both the Aspen Insurance and Aspen Re reporting segments. For example: |

| ◦ | For accident year 2014 for Aspen Insurance, 2015 favorable development occurred mainly in Property & Casualty, and 2016 favorable development in Marine Energy was substantively offset by 2016 unfavorable development in Property & Casualty. |

| ◦ | For accident year 2015 for Aspen Re, 2016 significant favorable development in Property was partially offset by 2016 unfavorable development in both the Casualty and Specialty lines. |

Accordingly, it appears that the aggregation of lines of business obscures meaningful trending information. As a result, we believe that further disaggregation of Aspen Insurance and Aspen RE in the tables presenting incurred claims and cumulative paid claims is necessary pursuant to ASC 944-40-50-4H. Please tell us the separate tables

1

you intend to present beginning with your Form 10-K for the year ended December 31, 2017 upon disaggregating. Also as you did not explain within Aspen Insurance why Property & Casualty should not be disaggregated, please provide us information such as claims payment pattern and duration and development amounts and trends to support why aggregating these lines is appropriate.”

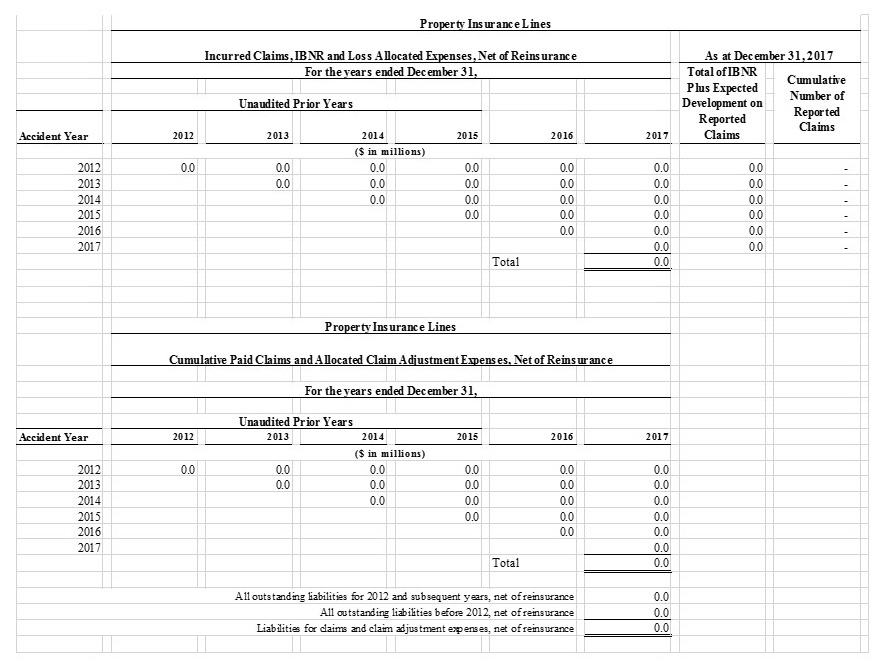

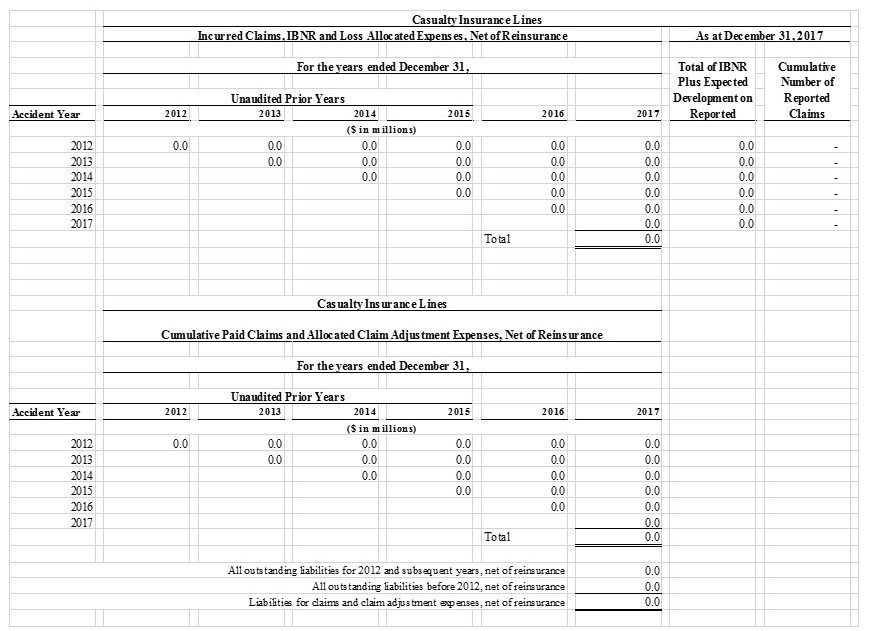

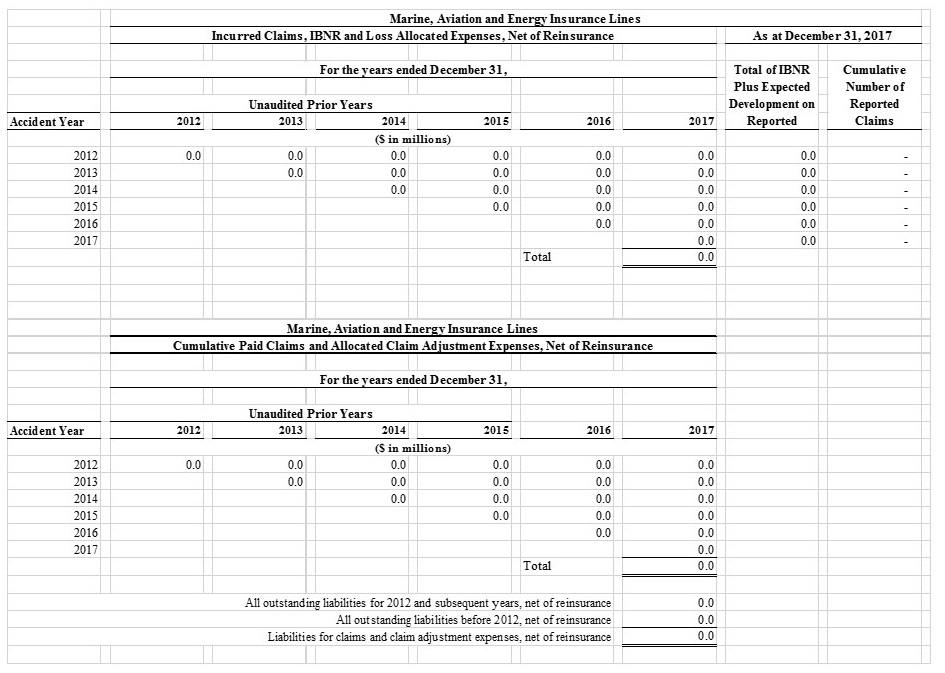

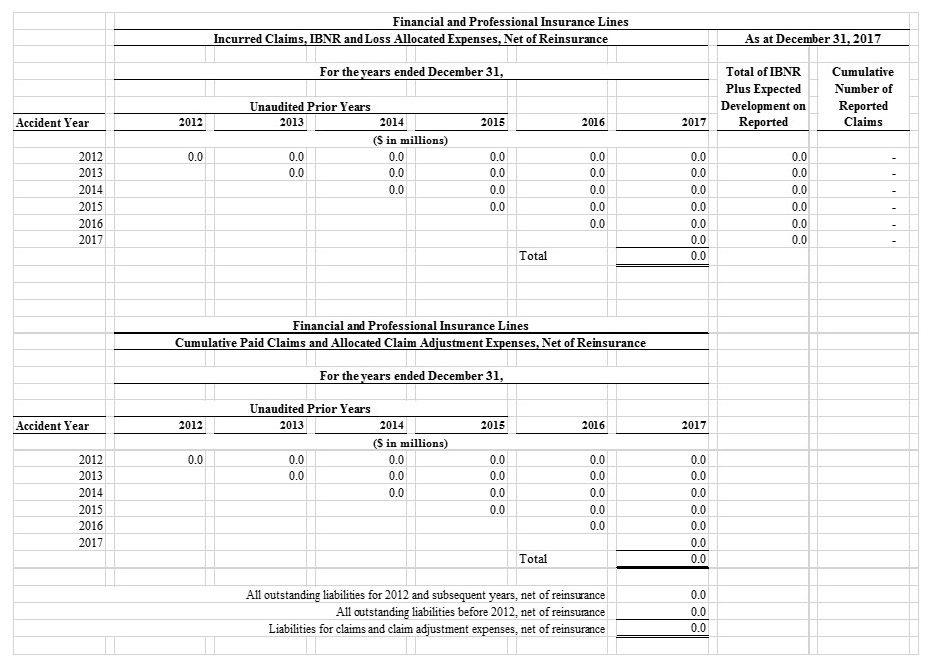

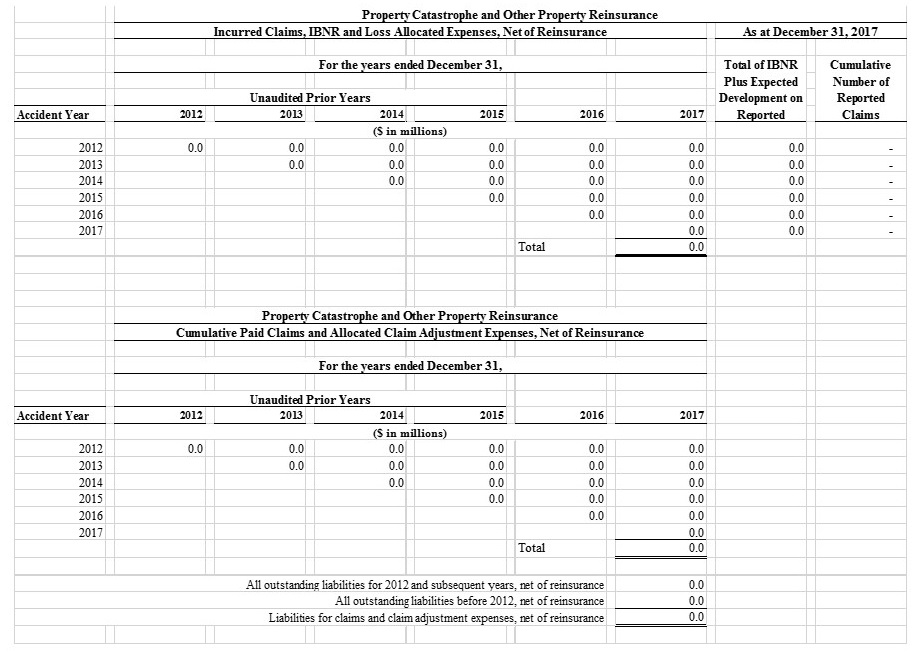

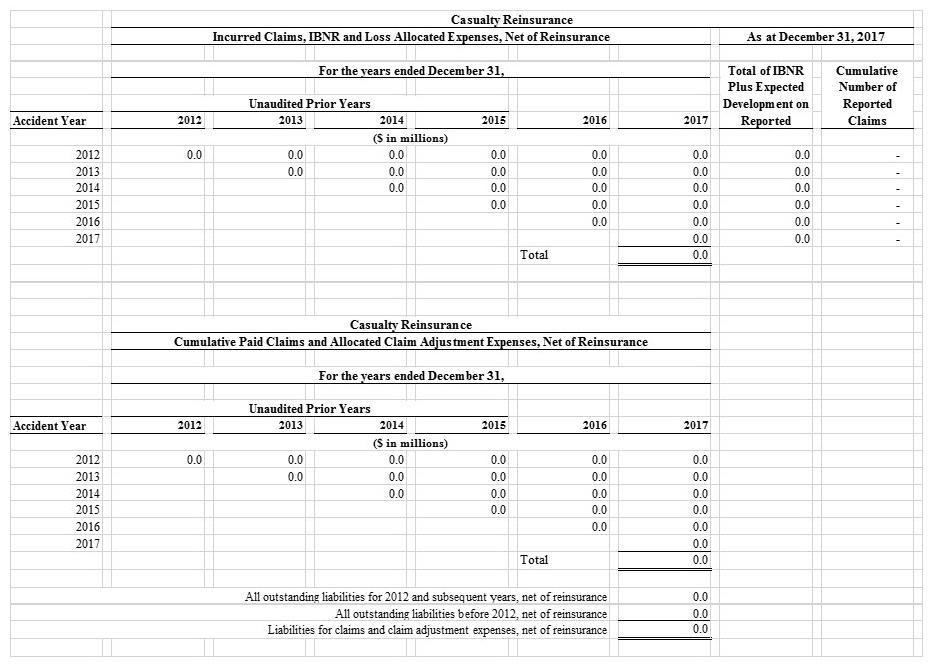

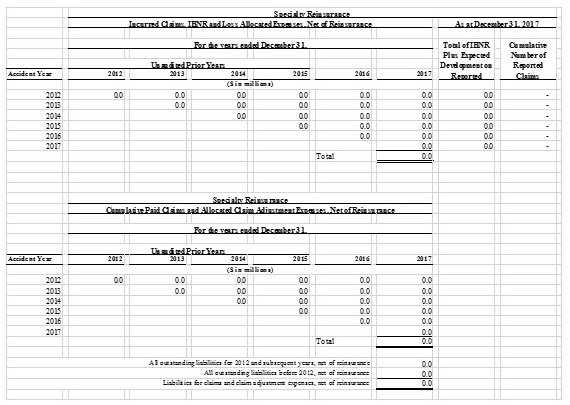

Having considered the Staff’s comments, the Company will disaggregate the lines of business within our reporting segments, Aspen Insurance and Aspen Re, disclosing incurred claims and cumulative paid claims on a net of reinsurance basis by line of business within the Form 10-K for the year ended December 31, 2017. The Company will also disaggregate property insurance lines from casualty insurance lines, providing separate tabular disclosure for each.

Accordingly, separate claims development triangles for the following lines of business will be disclosed:

| • | Property Insurance Lines |

| • | Casualty Insurance Lines |

| • | Marine, Aviation and Energy Insurance Lines |

| • | Financial and Professional Insurance Lines |

| • | Property Catastrophe and Other Property Reinsurance |

| • | Casualty Reinsurance |

| • | Specialty Reinsurance |

Presented below are illustrative claims development triangles, by the lines of business described above, that will be disclosed in the Form 10-K for the year ended December 31, 2017 which we intend to file on or about February 22, 2018.

2

3

4

5

Thank you for your consideration of the responses. If you have any further questions or comments, please contact me at 011-44-207-184-8804, Joseph Ferraro of Willkie Farr & Gallagher LLP at 011-44-203-580-4707 or Michael Groll of Willkie Farr & Gallagher LLP at 1-212-728-8616.

Yours sincerely,

Scott Kirk

Chief Financial Officer

Aspen Insurance Holdings Limited

| Cc: | Michael Cain |

Grahame Dawe

Silvia Martinez

Marc MacGillivray

Aspen Insurance Holdings Limited

Salim Tharani

KPMG LLP

Joseph Ferraro

Michael Groll

Willkie Farr & Gallagher LLP

6