Aspen Insurance Holdings Limited

Credit Suisse Investor Conference

Chris O’Kane

Chief Executive Officer

15 November 2007

AHL: NYSE

Exhibit 99.1

Safe Harbor Disclosure

This slide presentation is for information purposes only. It should be read in conjunction with our financial supplement posted on our website on the Investor Relations page and with other documents filed or to be filed shortly by Aspen Insurance Holdings Limited (the “Company” or “Aspen”) with the U.S. Securities and Exchange Commission.

Non-GAAP Financial Measures

In presenting Aspen's results, management has included and discussed certain "non-GAAP financial measures", as such term is defined in Regulation G. Management believes that these non-GAAP measures, which may be defined differently by other companies, better explain Aspen's results of operations in a manner that allows for a more complete understanding of the underlying trends in Aspen's business. However, these measures should not be viewed as a substitute for those determined in accordance with GAAP. The reconciliation of such non-GAAP financial measures to their respective most directly comparable GAAP financial measures in accordance with Regulation G is included herein or in the financial supplement, as applicable, which can be obtained from the Investor Relations section of Aspen's website at www.aspen.bm.

Application of the Safe Harbor of the Private Securities Litigation Reform Act of 1995:

This presentation contains written or oral "forward-looking statements" within the meaning of the U.S. federal securities laws. These statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include all statements that do not relate solely to historical or current facts, and can be identified by the use of words such as "expect," "intend," "plan," "believe," "project," "anticipate," "seek," "will," "estimate," "may," "continue,“ “guidance," and similar expressions of a future or forward-looking nature.

In addition, any estimates relating to loss events involve the exercise of considerable judgment and reflect a combination of ground-up evaluations, information available to date from brokers and cedants, market intelligence, initial tentative loss reports and other sources. Due to the complexity of factors contributing to the losses and the preliminary nature of the information used to prepare these estimates, there can be no assurance that Aspen's ultimate losses will remain within the stated amount.

All forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause actual results to differ materially from those indicated in these statements. Aspen believes these factors include, but are not limited to: changes in the total industry losses resulting from Hurricanes Katrina, Rita and Wilma and any other events, and the actual number of Aspen's insureds incurring losses from these events; with respect to events such as Hurricanes Katrina, Rita and Wilma, Aspen’s reliance on loss reports received from cedants and loss adjustors, Aspen's reliance on industry loss estimates and those generated by modeling techniques, the impact of these events on Aspen's reinsurers, any changes in Aspen's reinsurers' credit quality, the amount and timing of reinsurance recoverables and reimbursements actually received by Aspen from its reinsurers and the overall level of competition and the related demand and supply dynamics as contracts come up for renewal; the impact that our future operating results, capital position and rating agency and other considerations have on the execution of any capital management initiatives; the impact of any capital management activities on our financial condition; the impact of acts of terrorism and related legislation and acts of war; the possibility of greater frequency or severity of claims and loss activity, including as a result of natural or man-made catastrophic events than our underwriting, reserving or investment practices have anticipated; evolving interpretive issues with respect to coverage as a result of Hurricanes Katrina, Rita and Wilma and any other events such as the UK floods; the level of inflation in repair costs due to limited availability of labor and materials after catastrophes; the effectiveness of Aspen's loss limitation methods; changes in the availability, cost or quality of reinsurance or retrocessional coverage, which may affect our decision to purchase such coverage; the reliability of, and changes in assumptions to, catastrophe pricing, accumulation and estimated loss models; loss of key personnel; a decline in our operating subsidiaries' ratings with Standard & Poor's, A.M. Best Company or Moody's Investors Service; changes in general economic conditions including inflation, foreign currency exchange rates, interest rates and other factors that could affect our investment portfolio; the number and type of insurance and reinsurance contracts that we wrote at the January 1st and other renewal periods in 2007 and the premium rates available at the time of such renewals within our targeted business lines; increased competition on the basis of pricing, capacity, coverage terms or other factors; decreased demand for Aspen’s insurance or reinsurance products and cyclical downturn of the industry; changes in governmental regulations, interpretations or tax laws in jurisdictions where Aspen conducts business; proposed and future changes to insurance laws and regulations, including with respect to U.S. state- and other government-sponsored reinsurance funds and primary insurers; Aspen or its Bermudian subsidiary becoming subject to income taxes in the United States or the United Kingdom; the effect on insurance markets, business practices and relationships of ongoing litigation, investigations and regulatory activity by the New York State Attorney General's office and other authorities concerning contingent commission arrangements with brokers and bid solicitation activities. For a more detailed description of these uncertainties and other factors, please see the "Risk Factors" section in Aspen's Annual Reports on Form 10-K as filed with the U.S. Securities and Exchange Commission on February 22, 2007. Aspen undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the dates on which they are made.

2

AHL: NYSE

Probability Distributions of 2008 ROAE and Return

on Allocated Equity: Disclaimers

3

This presentation includes slides relating to the probability distributions of the 2008 ROAE and Return on Allocated Equity based on model outputs only and are not, and should not be construed as guidance for 2008. The Company relies on the outputs of its Dynamic Financial Analysis (“DFA”) model in addition to other considerations in the establishment of its public guidance. No 2008 guidance is given in this presentation.

No representation or warranty of any kind is or can be made with respect to the accuracy or completeness of, and no representation or warranty should be inferred from, the probability distributions of the 2008 ROAE and Return on Allocated Equity in these slides or the assumptions underlying them or their suitability. No representation or warranty is or can be made as to the future operations or the amount of any future income or loss.

The figures shown are the result of numerous assumptions made within our DFA model, many of which are subject to uncertainty which could lead actual results to vary considerably from those indicated by the model, including our estimates of catastrophe and non-catastrophe losses, our estimates of reserve movements and our estimates of investment income.

No explicit allowance has been made within the modelling for the possibility that the model could be wrong or assumptions within the model incorrect. This includes the possibility that catastrophe models are incorrect.

Changes in market conditions and variations from expected underwriting and investment strategy may lead to results varying considerably from those indicated by the model.

No reliance should be placed on the accuracy of our DFA probability distributions of the 2008 ROAE and Return on Allocated Equity as they are based on (i) assumptions and other factors made at the time of modeling which may be subject to uncertainty or which may change subsequently, (ii) currently available information derived from modeling techniques, which may be incorrect, and (iii) modeling assumptions that may be inaccurate or incorrect. Therefore, the results of the model are illustrative and not to be viewed as facts or forecasts, and should not be relied upon as a representation of the future value of an investment in Aspen shares.

See Slide 2 – Safe Harbor Disclosure for reference to important factors that could cause actual results to differ from the probability distribution of 2008 ROAE and Return on Allocated Equity provided in the previous slides. Changes in market conditions and variations from expected underwriting and investment strategy may lead to results varying considerably from those indicated by the model.

For a more detailed description of these uncertainties and other factors, please see the “Risk Factors” section in Aspen’s Annual Reports on Form 10-K as filed with the U.S. Securities and Exchange Commission on February 22, 2007. Aspen undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the dates on which they were made.

AHL: NYSE

Contents

Aspen at a Glance

Key Performance Drivers

Tax

Capital Management and Financial Leverage

Investment Income

Underwriting Results

Business Enablement

Enterprise Risk Management

Diversification

Cycle Management

4

AHL: NYSE

Aspen at a Glance

5

A Bermuda based diversified Specialty Insurer and Reinsurer with particular strengths in

Marine, Energy and Transport Insurance

Specialty and Casualty Reinsurance

Property Catastrophe Insurance and Reinsurance

$2.5bn market cap

$2.3bn common equity and $3.0bn total capital, as of September 30, 2007

500 employees in 12 offices in 6 countries

Ratings of A (S&P), A2 (Moody’s) and A / A- (AM Best, for Aspen UK and Aspen

Bermuda)

$1.9bn Gross Written Premium (GWP) in 2006, estimate $1.8bn +/- 5% GWP for

2007

35% Insurance, 65% Reinsurance

43% Casualty, 57% Property

AHL: NYSE

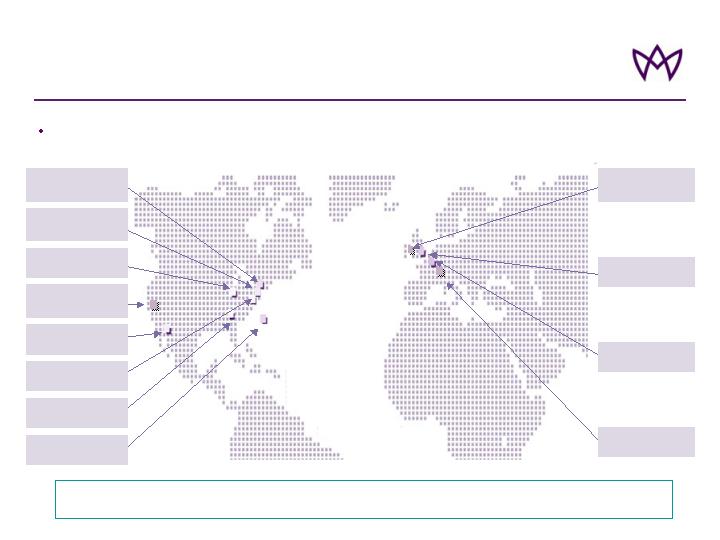

Aspen at a Glance:

Widespread distribution-efficient infrastructure

500 Employees Across Twelve Offices

129 Underwriters, 25 Actuaries and 29 Risk Management professionals

London

(294)

Paris

(3)

Zurich

(7)

Dublin

(6)

Bermuda

(56)

Atlanta

(18)

Connecticut

(34)

Arizona

(9)

Illinois

(2)

California

(6)

New York

(1)

Massachusetts

(63)

Key platforms in London, Bermuda and US with seven additional distribution centres

6

AHL: NYSE

Aspen at a Glance:

Key Performance Drivers - Framework

i. Asset Leverage defined as Invested Assets / Capital. Capital defined as Ordinary and Preferred Shareholders’ Equity plus Long-term Debt

ii. Leverage defined as (Preferred Shareholders’ Equity + Long-term Debt) / Capital

iii. Operating Leverage defined as Net Premium Earned / Average Ordinary Shareholders Equity

7

Targeted Management of Underlying Levers of ROAE to Enhance Performance

Pre

-

tax Return

on Capital

Leverage

(

1

–

Tax rate

)

Pre

-

tax

ROAE

x

Expense Ratio

Loss Ratio

Operating

Leverage

Asset Leverage

Investment Yield

+

x

x

+

–

Interest

Expense

Capital

Underwriting

Result

Capital

Investment

Income

Capital

(i)

(ii)

(iii)

ROAE

Tax

Capital Management and Financial Leverage

Investment Income

Underwriting Results

Key Performance Driver: Increasing Tax Efficiency

0%

5%

10%

15%

20%

25%

30%

2003

2004

2005*

2006

9mths 2007

Tax rate

* In 2005 Aspen Insurance Holdings Limited reported a loss before tax of $160.4 million. In addition to the loss, the group incurred a tax charge of $17.4

8

AHL: NYSE

million in relation to profits earned by Aspen Insurance UK Limited

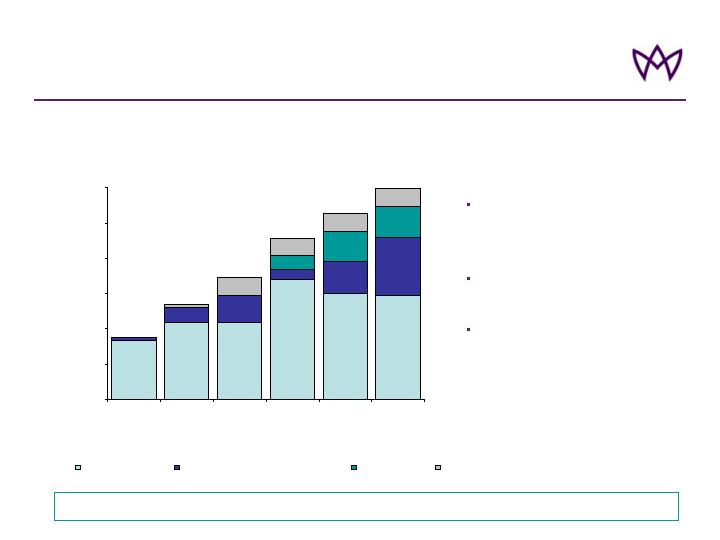

Key Performance Driver:

Capital Management and Financial Leverage

837

1,091

1,096

1,693

1,503

1,471

208

385

147

457

832

200

430

430

249

249

249

249

41

40

0

500

1,000

1,500

2,000

2,500

3,000

2002

2003

2004

2005

2006

Q3 2007

$ mil

Common share capital

Retained earnings inc OCI and issue costs

Preference shares

Debt

Capital Structure and Financial Leverage

9

Share buy back: completed

$300m program, final $50m on

November 9

Preference shares: issued

$200m Q4 2006

Strong balance sheet with

opportunity for further leverage

Active Balance Sheet Management to Deliver Consistent, Quality ROAE

878

1,339

1,731

2,289

2,639

2,983

22.8%

25.7%

19.6%

14.4%

3.0%

Leverage

AHL: NYSE

3.0%

3.5%

4.0%

4.5%

5.0%

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Fixed Income

Fixed income and cash and cash equivalents

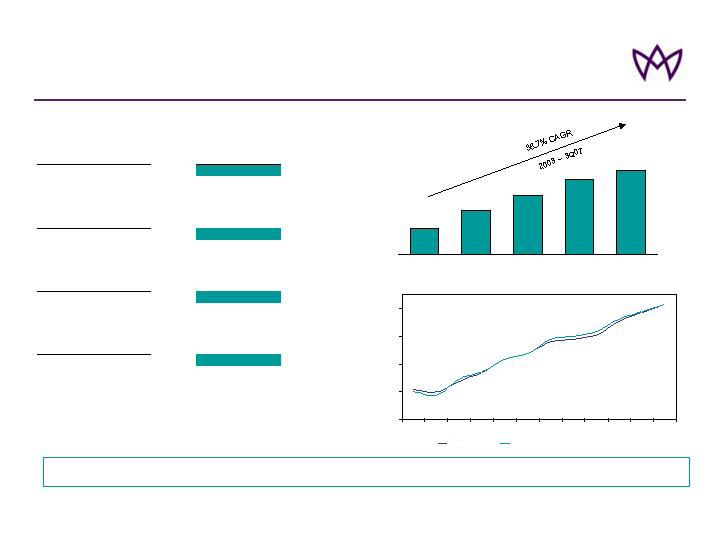

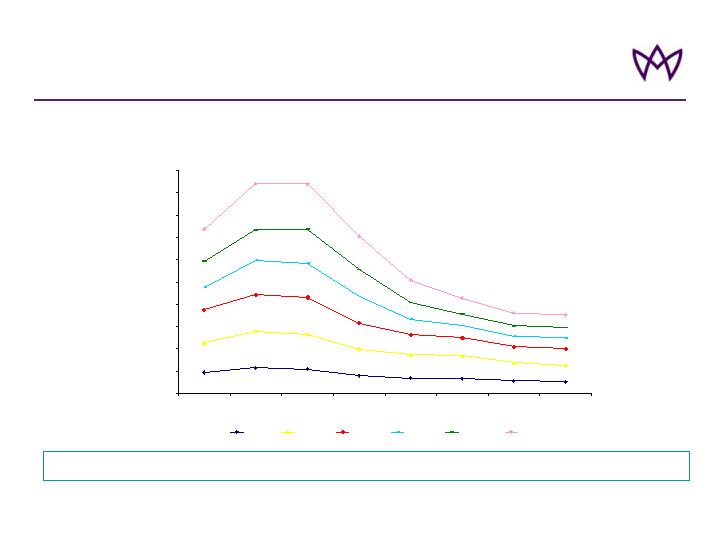

Key Performance Driver: Growing Investment Income

Average: 2003 – 2007 1H

4.4%

Peer Group Average

3.8%

ASPEN

4.0%

Peer Group Average

3.5%

ASPEN

2005

4.9%

Peer Group Average

4.4%

ASPEN

2006

5.4%

Peer Group Average

5.6%

ASPEN

Pre-tax Investment

Yield¹

2007 1H

$1,616

$2,736

$3,689

$4,681

$5,219

2003

2004

2005

2006

3Q 2007

Peer Group includes: ACE, ACGL, AXS, ORH, ENH, RE, IPCR, TRH, MXGL, MRH, PRE, PTP, AWH, RNR, XL

Source: Company Filings

1. Pre-Tax Investment Yield computed by dividing net investment income for the period by average invested assets and cash / cash equivalents for the applicable period. 2007 1H annualized by

compounding 1H investment return for two six month periods.

10

Total Investments have increased

Investment Yield improving

Increasing Investment Yield; Investment Income Increasing Component of Total Return

AHL: NYSE

Key Performance Driver:

Significant Improvement in Investment Performance

Improving Yields With Consistent Prudent Investment Management Approach

Fund of Hedge Funds Performance

$489m investment = 8.5% of investible assets; scope to increase to 10% of investible assets

21.3% of common equity

Multi manager, multi strategy approach

Performance: YTD Sep 30 2007, 10.0% (13.2% annualized)

-5%

0%

5%

10%

15%

20%

HFRI FOF: Conservative Index

Lehman Agg

S&P500

Aspen FOHF weighted

11

AHL: NYSE

Key Performance Driver: Strong Underwriting Results

95.4

Peer Median

117.6

Peer Median

84.6

Peer Median

85.6

Peer Median

Average: 2003 – 2007 1H

89.0%

ASPEN

117.2%

ASPEN

2005

82.4%

ASPEN

2006

83.9%

ASPEN

Combined Ratio (GAAP)

2007 1H

* Without taking into account variance in other performance measures

Source: SNL Financial

Peers include ACE, ACGL, AXS, ORH, ENH, RE, IPCR, TRH, MXGL, MRH, PRE, PTP, AWH, RNR, XL

12

80

90

100

110

120

20071H

2006

2005

2003-

20071H

Aspen

Median

Combined

Ratio

%

In 2008 We Require a Combined Ratio of 90% to Achieve an ROAE of 15%*

AHL: NYSE

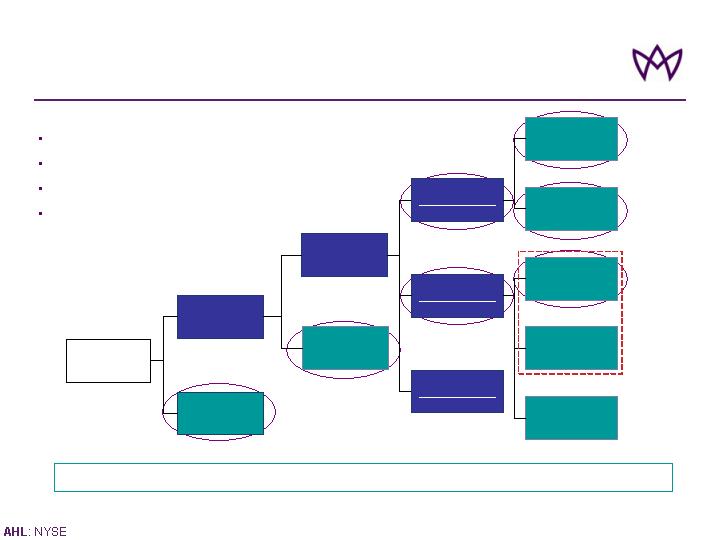

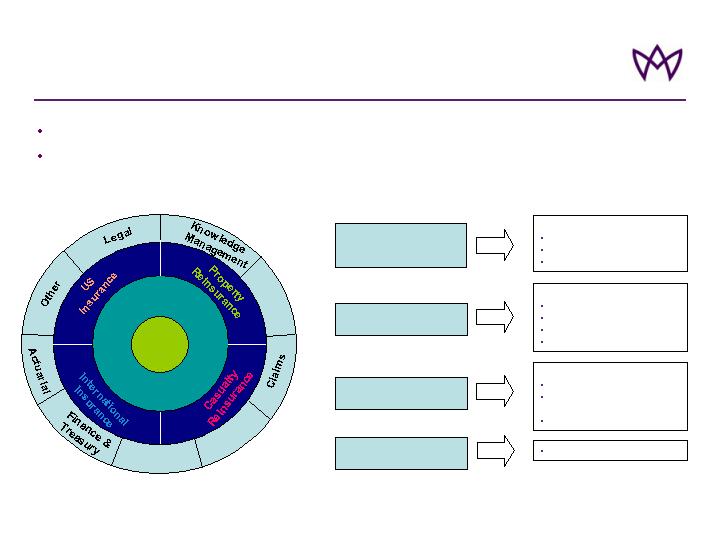

Business Enablement:

Enterprise Risk Management Core Strategic Enabler

Strong ERM framework

Recognised as an Aspen strength by S&P in 2006 and reaffirmed in 2007; awarded ‘strong rating’, second highest, only 3 out of 29 Global Reinsurance companies have higher rating

Managing risk is the job of everyone at Aspen,

- but 29 professionals work in our risk functions

13

AHL: NYSE

Enterprise Risk Management: Core Strategic Enabler

IT

Ceded

Reinsurance

Risk Management

Risk Management

Group

Executive

HR

Product Segments

145 people

Support Services

187 people

Risk Management

29 people

Board / Management

Team

14 People

Function

Responsibility

‘Implementing the rules’

Risk measurement

Risk monitoring

Control infra-structure

Risk governance

Business enablement

Production

Sales & marketing

Customer relationship

management

Product development

‘Setting the rules’

Strategy

Capital management

Capital allocation

A risk based approach to managing

Integrated Strategic Planning - Operational Management - Internal Control

14

AHL: NYSE

ERM in Practice - Key Stages

Strategic Planning

Operational Management

Internal Control

Group risk appetites set using

advanced simulation modelling

Stress tests used to understand

model weaknesses and tails

Risk limits set for underwriting,

investment and operations

management

Risk transfer plans for reinsurance

and capital markets

Issue Aspen ‘Licenses’ to risk

takers

Insurance product capacity

budgets

Technical price thresholds

Technical terms thresholds

Underwriting guidelines

Product portfolio optimisation

Risk and control schedules

Reinsurance placements

Capital market actions

Accumulation control

Price monitoring

Coverage monitoring

Underwriting quality reviews

Internal audits

Reserving Committee

Performance review

15

AHL: NYSE

Business Enablement: Understanding Catastrophe Risk

Significant Reduction in Exposure to Natural Catastrophes Post 2005 At All Return Periods

* Aggregate Exceedance Probability (excludes inwards reinstatement premiums, includes outwards reinstatement premiums, net of tax)

Note: For net figures applied 2007 reinsurance / retro program to reflect our previous exposure versus our current structure

Note that assumptions have been made to bring prior periods, modelled in old RMS versions, in line with RMS version 6.

Group Net AEP, Combined All Perils

“As-If” to RMS v6

16

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2004-08

2005-02

2005-08

2006-02

2006-08

2007-03

2007-06

2007-09

Date

Annual Cat Loss in USD m

Mean

1 in 10

1 in 25

1 in 50

1 in 100

1 in 250

AHL: NYSE

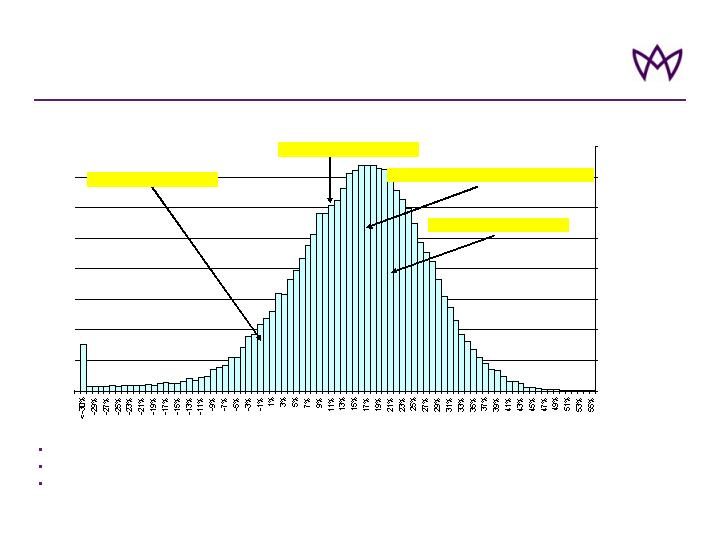

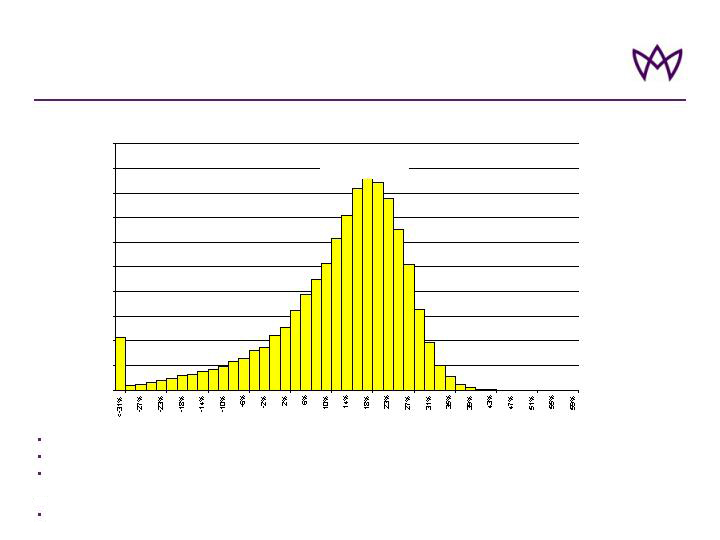

Business Enablement: Understanding Risk

Result of 50,000 simulations of the 2008 year net income using Aspen DFA model

Risks modelled include underwriting (cat and non cat), reserving, market, credit and operational

Subject to the caveats on slides 2 and 3, this represents our estimates of modelled outcomes for 2008

17

ROAE Distribution all Risks: 2008 Plan

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

ROAE

Probability

Chance of an ROAE < 0=9.2%

Chance of an ROAE > 10%=71%

Chance of an ROAE between 14% and 20%=25%

Chance of an ROAE > 20%=37%

AHL: NYSE

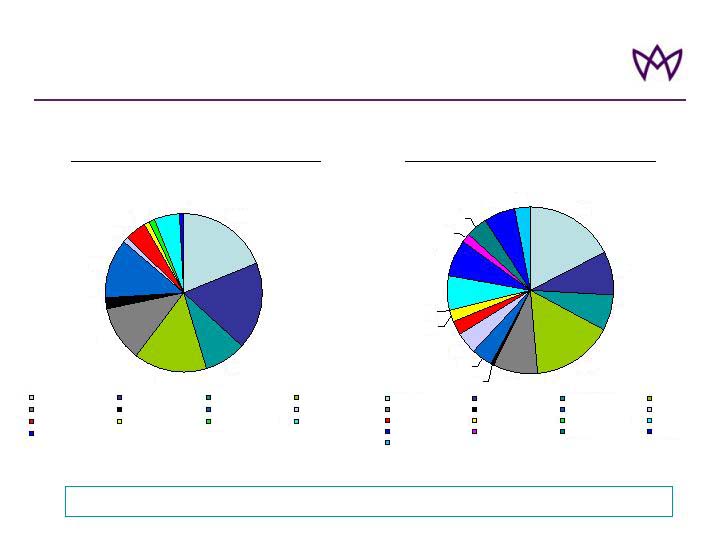

Improved Diversification

Targeted Growth in Specialty Lines And Improved Spread of Risk

$1.4bn split by Product Line

9 months to Sept 2004

$1.5bn split by Product Line

9 months to Sept 2007

18

17%

8%

7%

16%

9%

1%

4%

4%

3%

2%

0%

6%

7%

2%

4%

6%

3%

Catastrophe

Risk XS

Pro Rata Treaty

US Casualty

International Casualty

Casualty Facultative

UK Liability

US Liability

UK Commercial Property

US Commercial Property

Worldwide Property

Specialty RI

Marine Liability

Property Facultative

Aviation

Energy

Marine Hull

20%

18%

9%

15%

11%

2%

12%

1%

4%

1%

1%

5%

1%

Catastrophe

Risk XS

Pro Rata Treaty

US Casualty

International Casualty

Casualty Facultative

UK Liability

US Liability

UK Commercial Property

US Commercial Property

Worldwide Property

Specialty RI

Marine Liability

AHL: NYSE

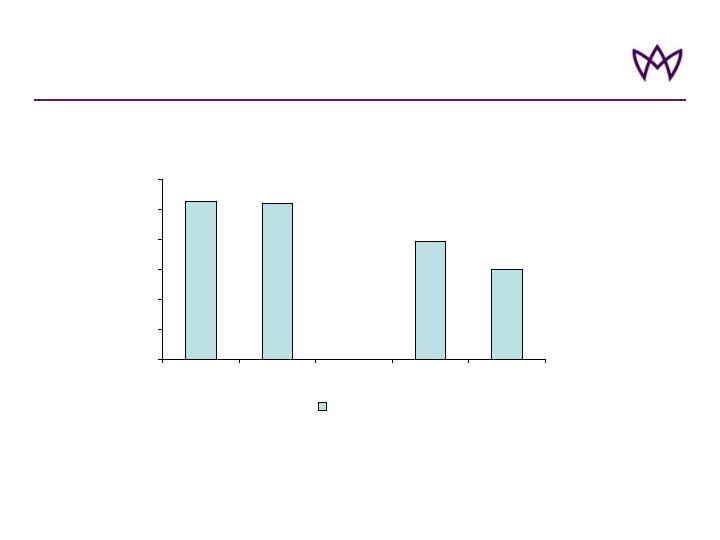

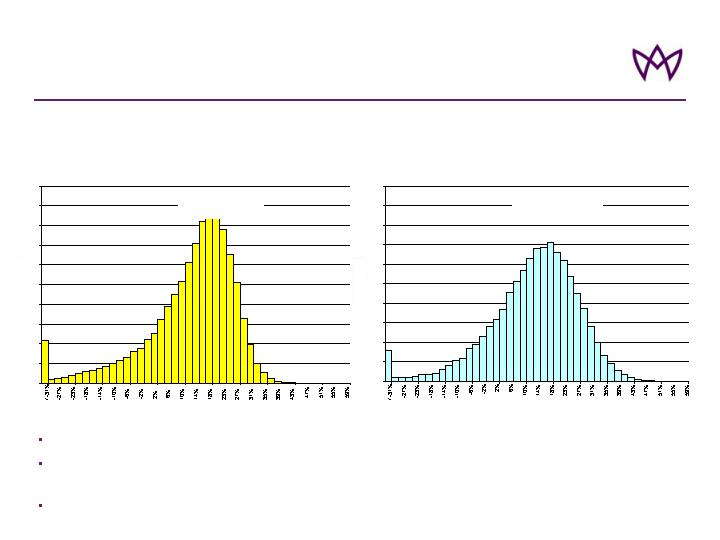

Business Enablement: Benefits of Diversification

Property Reinsurance product segment only

No diversification with other product segments

Relatively large tail and high volatility as measured by the Standard Deviation (“SD”) and the Sharpe Ratio

(calculated using return on allocated shareholders’ common equity)

Subject to the caveats on slides 2 and 3, this represents our estimates of modelled outcomes for 2008

19

Return on Allocated Equity – Property Reinsurance Only

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

Return On Allocated Equity (ROAE for segment)

Probabilities

SD = 13.1%

Sharpe Ratio = 0.69

AHL: NYSE

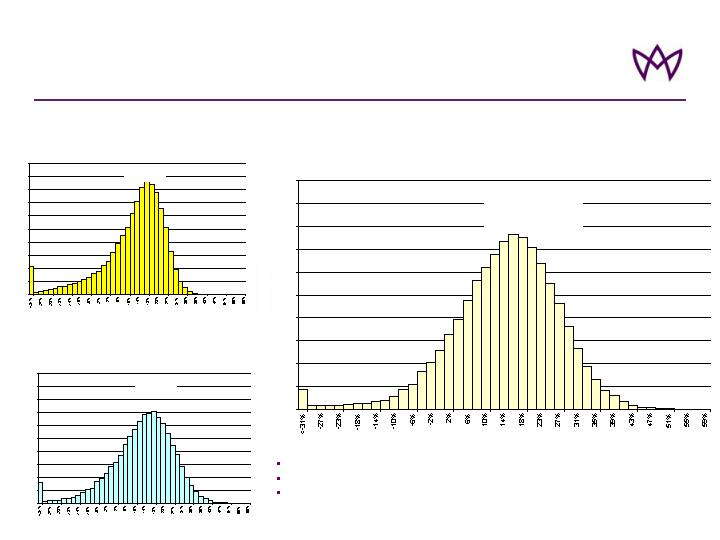

Business Enablement: Benefits of Diversification

20

Property Reinsurance and Casualty

Reinsurance

Property Reinsurance product

segment only

Diversification leads to a reduction of the risk of unfavourable outcomes

Return on allocated equity less volatile (SD reduces to 10.7% from 13.1%, Sharpe Ratio increases from

0.69 to 0.90)

Subject to the caveats on slides 2 and 3, this represents our estimates of modelled outcomes for 2008

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

Probabilities

6.00%

7.00%

8.00%

9.00%

10.00%

Return On Allocated Equity (ROAE for segment)

SD = 13.1%

Sharpe Ratio = 0.69

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

Probabilities

6.00%

7.00%

8.00%

9.00%

10.00%

Return On Allocated Equity (ROAE for segment)

SD = 10.7%

Sharpe Ratio = 0.90

AHL: NYSE

Business Enablement: Benefits of Diversification

21

Property Reinsurance and Casualty Reinsurance

Property Reinsurance product segment only

Reinsurance and Insurance Combined

SD reduces further to 9.4% and Sharpe Ratio increases to 1.16

Diversification reduces volatility and gives better risk / return balance

Subject to the caveats on slides 2 and 3, this represents our estimates of

modelled outcomes for 2008

0.00%

1.00%

2.00%

3.00%

4.00%

Probabilities

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

Return On Allocated Equity (ROAE for segment)

SD = 13.1%

Sharpe Ratio = 0.69

0.00%

1.00%

2.00%

3.00%

4.00%

Probabilities

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

Return On Allocated Equity (ROAE for segment)

SD = 10.7%

Sharpe Ratio = 0.90

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

Probabilities

6.00%

7.00%

8.00%

9.00%

10.00%

Total ROAE

SD = 9.4%

Sharpe Ratio = 1.16

AHL: NYSE

Approach to Cycle Management

Business pricing must meet or exceed adequacy levels

Key components

Underwriting integrity

Optimizing business mix

Strong risk management

Efficient use of reinsurance / retrocession purchasing

Expense control

Improving investment contribution

Return Excess Capital to Shareholders when Appropriate

22

AHL: NYSE

GWP and rate index

2001

2002*

2003

2004

2005

2006

2007**

Proactive Cycle Management

11

79

70

61

51

50

0

10

20

30

40

50

60

70

80

90

100

GWP

$millions

0

20

40

60

80

100

120

140

160

Rate

Index,

2001=100%

RRV

(right scale)

GWP

(left scale)

UK Commercial Property

% change ‘03-’07

Rates: -22%

GWP: -37%

GWP

$millions

76

223

213

171

125

87

0

50

100

150

200

250

2001

2002*

2003

2004

2005

2006

2007**

0

50

100

150

200

250

Rate

Index ,

2001=100%

RRV

(right scale)

GWP

(left scale)

UK Liability

% change ‘03-’07

Rates: -39%

GWP: -61%

Disciplined Underwriting and Cycle Management

* Since inception June 2002

** Projected year end 2007

23

AHL: NYSE

Conclusions

Strong underwriting performance

Improving investment contribution

Efficient in our use of capital

Effective enterprise risk management, core strategic enabler

High quality, diversified underwriting portfolio designed with the benefit of sophisticated

capital allocation models

Strong, quality, improving returns

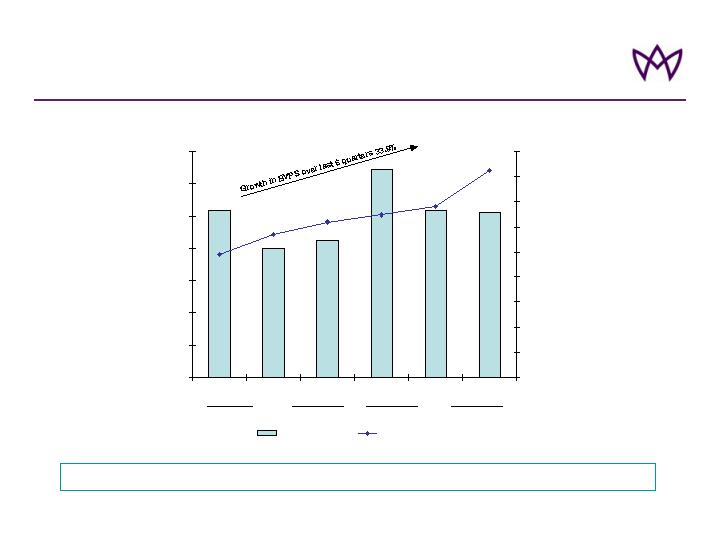

BVPS 33.9% growth over last 6 quarters

Annualised ROAE >18% over last 6 quarters

24

Well positioned to manage the cycle and generate attractive returns

AHL: NYSE

Aspen Insurance Holdings Limited

Credit Suisse Investor Conference

Chris O’Kane

Chief Executive Officer

15 November 2007

AHL: NYSE

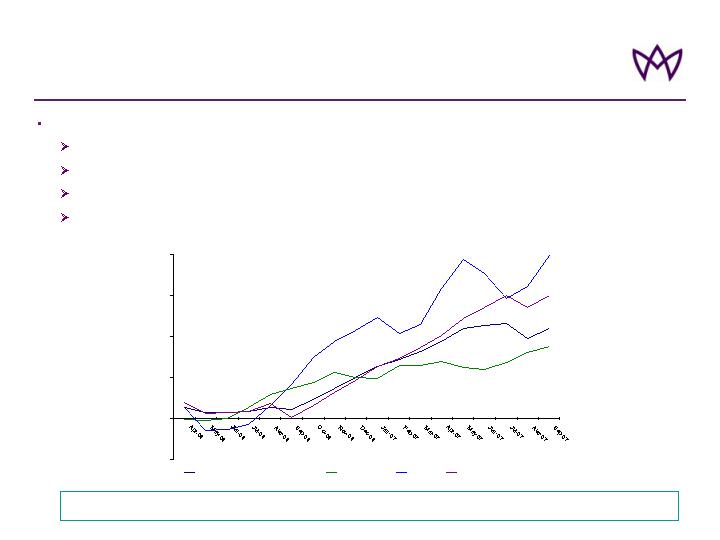

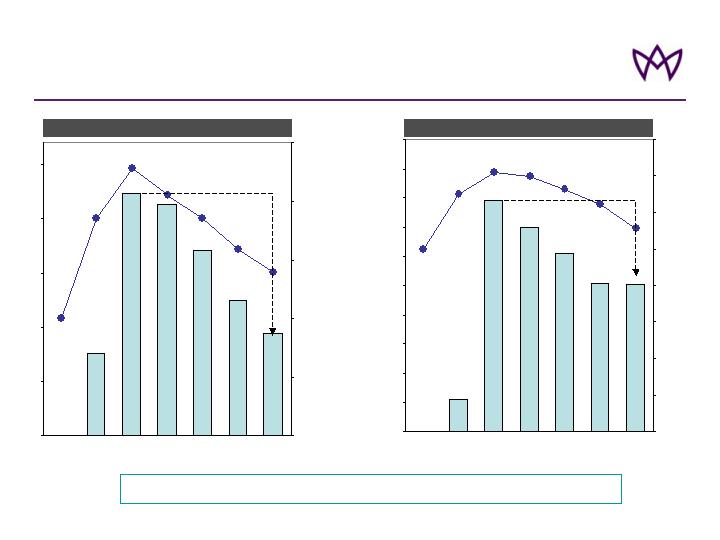

Growth in ROAE and Book Value Per Share

10%

12%

14%

16%

18%

20%

22%

24%

Q2

Q3

Q4

Q1

Q2

Q3

ROAE %

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

$ Diluted B/V Per Share

Annualised ROAE

Diluted BV Per Share*

06

07

Annualised ROAE >18% Over Last 6 Quarters

26

Note: See Aspen's quarterly financial supplement for a reconciliation of diluted book value per share to basic book value per share, reconciliation of average equity to closing

shareholders’ equity in the Investor Relations section of Aspen's website at www.aspen.bm

Appendix

AHL: NYSE

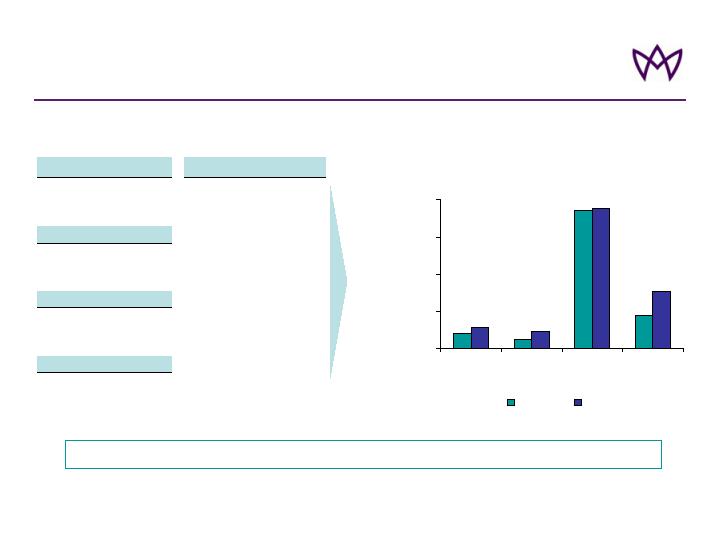

With increasing investment income contribution...

$178

$204

-$259

$296

$199

$208

$68

$121

$142

$30

$204

$219

2003

2004

2005

2006

9mths

2006

9mths

2007

Underwriting

Income

Investment Income

Resulting in improving ROAE

15.9%

14.0%

18.5%

16.4%

21.2%

-11.7%

2003

2004

2005

2006

9mths 2006

9mths 2007

Due to strong underwriting...

25%

25%

27%

29%

30%

29%

53%

59%

90%

55%

55%

53%

2003

2004

2005

2006

9mths

2006

9mths

2007

Expense Ratio

Loss Ratio

Profitability has increased substantially...

$152

$195

$378

$259

$354

($178)

2003

2004

2005

2006

9mths 2006

9mths 2007

Financial Performance

($ in millions)

27

Delivering Results

($ in millions – Net Income)

Note: Reconciliation of average equity to closing shareholders’ equity is provided in our quarterly financial supplements available in the Financial Results section of the Investor

Relations page of Aspen’s website, www.aspen.bm

Appendix

AHL: NYSE