Use these links to rapidly review the document

TABLE OF CONTENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

| Filed by the Registrantý | ||

Filed by a Party other than the Registranto | ||

Check the appropriate box: | ||

o | Preliminary Proxy Statement | |

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

ý | Definitive Proxy Statement | |

o | Definitive Additional Materials | |

o | Soliciting Material Pursuant to §240.14a-12 | |

VIRGIN MEDIA INC. | ||||

(Name of Registrant as Specified In Its Charter) | ||||

N/A | ||||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

ý | No fee required. | |||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies: | |||

| (2) | Aggregate number of securities to which transaction applies: | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| (4) | Proposed maximum aggregate value of transaction: | |||

| (5) | Total fee paid: | |||

o | Fee paid previously with preliminary materials. | |||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

(1) | Amount Previously Paid: | |||

| (2) | Form, Schedule or Registration Statement No.: | |||

| (3) | Filing Party: | |||

| (4) | Date Filed: | |||

909 Third Avenue, Suite 2863

New York, New York 10022

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

To Be Held on May 21, 2008

To Our Stockholders:

The annual meeting of stockholders of Virgin Media Inc. will be held at 10.15 a.m., local time, on Wednesday, May 21, 2008, at the offices of Fried, Frank, Harris, Shriver & Jacobson LLP at 375 Park Avenue, New York, New York 10152, 36th Floor, for the following purposes:

- 1.

- To elect two Class I directors to hold office until the annual meeting of stockholders that is to be held in 2011 or until their respective successors are duly elected and qualify;

- 2.

- To ratify the appointment by the audit committee of Ernst & Young LLP as independent auditors for the fiscal year ending December 31, 2008; and

- 3.

- To transact any other business that may properly be brought before the meeting or any adjournment or postponement of the meeting.

Holders of our common stock as of the close of business on April 3, 2008 will be entitled to notice of, and to vote at, the annual meeting and at any adjournments or postponements of the annual meeting. The stock transfer books will not be closed. A list of the stockholders entitled to vote at the meeting will be available at our principal executive offices at 909 Third Avenue, Suite 2863, New York, New York 10022, at least ten days prior to the meeting and will also be available for inspection at the meeting.

In accordance with new rules approved by the Securities and Exchange Commission, we will be sending a Notice of Internet Availability of Proxy Materials ("Notice") to our beneficial stockholders on or about April 11, 2008 and will provide access to our proxy materials over the internet, beginning April 11, 2008. Instructions on how to access the proxy materials over the internet or to request a printed set of the proxy materials are included in the Notice. The purpose of the annual meeting is set forth in the Notice. The proxy materials (including the proxy statement and form of proxy) will be first mailed to our registered stockholders on or about April 11, 2008.

It is important that your shares be represented at the annual meeting. Whether or not you plan to attend the meeting, you are urged to vote by telephone, via the internet or by completing the proxy card in accordance with the instructions stated thereon. You may revoke any proxy given by you at any time prior to exercise of the proxy.

By order of the Board of Directors,

James F. Mooney

Chairman

New York, New York

April 8, 2008

i

909 Third Avenue, Suite 2863

New York, New York 10022

PROXY STATEMENT

This proxy statement is being furnished in connection with the solicitation of proxies by our board of directors for use at our annual meeting of stockholders to be held at 10.15 a.m., local time, on Wednesday, May 21, 2008, at the offices of Fried, Frank, Harris, Shriver & Jacobson LLP at 375 Park Avenue, New York, New York 10152, 36th Floor, and at any adjournments or postponements of that meeting.

In order to conduct business at the annual meeting, the holders of a majority of our outstanding shares of common stock entitled to vote at the meeting must be present in person or represented by proxy. To ensure a quorum and to avoid expenses and delay, the board of directors urges you to promptly submit your proxy by telephone, via the internet or by completing the proxy card in accordance with the instructions stated thereon.

Holders of our common stock at the close of business on April 3, 2008 will be entitled to vote at the annual meeting and at any adjournments or postponements of the annual meeting. At the close of business on March 31, 2008, we had 328,011,216 shares of our common stock outstanding and entitled to vote at the annual meeting. Each share of our common stock is entitled to one vote.

In accordance with new rules approved by the Securities and Exchange Commission, we will be sending a Notice of Internet Availability of Proxy Materials ("Notice") to our beneficial stockholders on or about April 11, 2008 and will provide access to our proxy materials over the internet, beginning April 11, 2008. Instructions on how to access the proxy materials over the internet or to request a printed set of the proxy materials are included in the Notice. The purpose of the annual meeting is set forth in the Notice. The proxy materials (including the proxy statement and form of proxy) will be first mailed to our registered stockholders on or about April 11, 2008.

Each properly submitted proxy will be voted in accordance with the instructions contained within it. Your proxy is revocable on written instruction from you. You may also revoke your proxy by voting again on a later date by telephone or via the internet or by submitting another properly signed proxy card with a more recent date. Your revocation must be received by the office of the corporate secretary before voting is conducted on the matter with respect to which your proxy is to be exercised. If you attend the annual meeting, you may revoke your proxy by voting in person.

The solicitation of proxies will be by mail, telephone, internet and facsimile. We will pay all expenses of soliciting proxies, including clerical work, printing and postage. We will also reimburse brokers and other persons holding shares in their names or in the names of nominees for their expenses for sending material to principals and obtaining their proxies. The solicitation of proxies may be done by our directors, officers and other employees. We have also retained D.F. King & Co., Inc. to assist in the solicitation of proxies from stockholders for a fee of approximately $7,500, plus reasonable expenses.

Our company was formerly known as NTL Incorporated and, prior to that, as Telewest Global, Inc. On March 3, 2006, Telewest Global, Inc. and NTL Incorporated completed a merger transaction structured as a reverse acquisition by NTL Incorporated (the "Merger"). Upon completion, Telewest Global, Inc. ("Telewest") changed its name to NTL Incorporated ("New NTL"). The old NTL Incorporated, which had become a subsidiary of New NTL, changed its name to NTL Holdings Inc. ("Old NTL"). On February 6, 2007, New NTL changed its name to Virgin Media Inc. ("Virgin Media") and Old NTL changed its name to Virgin Media Holdings Inc. ("Virgin Media Holdings"). In this

1

proxy statement, references to the Company, "us", "our", "we" and similar words refer to Virgin Media but all historical information prior to the Merger is provided for Old NTL as if Old NTL had been the acquiror.

As a result of the Merger on March 3, 2006, the share capitalization of New NTL (now known as Virgin Media) was changed so that each share of Old NTL was converted into the right to receive 2.5 shares of Virgin Media stock. Each share of Telewest common stock outstanding prior to the merger was reclassified into (i) 0.2875 shares of Virgin Media stock following the Merger and (ii) one share of Telewest redeemable common stock that was automatically redeemed at the time of the Merger for $16.25 in cash. We have adjusted all share, option, exercise price and other historical data contained in this proxy statement to show the figures taking into account the conversion of shares in the Merger.

Unless otherwise noted, all amounts in this proxy statement translated from pounds sterling to U.S. dollars have been translated at a rate of $2.0017 per £1.00, which is the average annual exchange rate for the year ended December 31, 2007 used by the Company in its 2007 audited financial statements.

PROPOSAL 1

ELECTION OF DIRECTORS

Election of Directors Proposal

The first proposal is to elect two directors to hold offices until the annual meeting of stockholders that is to be held in 2011, or until their respective successors are duly elected and qualify.

Board of Directors

Our amended and restated certificate of incorporation provides for a classified board of directors consisting of three classes as nearly equal in number as possible. Directors in each class serve staggered three-year terms. Our Class I Directors are William R. Huff and James F. Mooney and their terms terminate on the date of this year's annual meeting of stockholders. Our Class II Directors are Edwin M. Banks, George R. Zoffinger and Neil A. Berkett and their terms terminate on the date of our 2009 annual meeting of stockholders. Our Class III Directors are Jeffrey D. Benjamin and Gordon D. McCallum and their terms terminate on the date of our 2010 annual meeting of stockholders. At each annual meeting of stockholders, successors to the class of directors whose term expires at that annual meeting are elected for a three-year term. Consistent with our certificate of incorporation, in order to have a more equal number of directors in each class of directors after the resignations of Charles K. Gallagher and David Elstein, on February 6, 2008, Mr. Zoffinger resigned as a Class I Director and was appointed by the board of directors as a Class II Director. Neil A. Berkett was appointed as a Class II Director on April 7, 2008 in connection with his appointment as our chief executive officer.

Messrs. Huff and Mooney, whose terms expire at this annual meeting, are each nominated for re-election at this annual meeting and, if elected, their new terms of office will expire at the annual meeting of stockholders to be held in 2011, or until their successors are elected and qualified. Both nominees have consented to be named in the proxy statement and to serve if elected.

2

Information regarding the nominees for election at the meeting, including present business experience and business experience during the past five years, follows:

Nominees for Directors for Terms Expiring in 2011

William R. Huff

Mr. Huff, age 58, has been a director since January 10, 2003 and chairs our executive committee and nominating sub-committee. He served as our interim chairman of the board of directors from January to March 2003, when Mr. Mooney became chairman. Mr. Huff is the president of the managing member of W.R. Huff Asset Management Co., L.L.C., an investment management firm. Mr. Huff founded W.R. Huff Asset Management Co., L.L.C. in 1984. W.R. Huff Asset Management's managed accounts and affiliates collectively historically constituted one of our stockholders.

James F. Mooney

Mr. Mooney, age 53, has been a director and chairman of the board of directors since March 2003, and serves on the executive committee. From April 2001 to September 2002, Mr. Mooney was the executive vice president and chief operating officer of Nextel Communications Inc. Prior to joining Nextel, from January 2000 to January 2001, Mr. Mooney was first the chief financial officer, then the chief executive officer and chief operating officer of Tradeout Inc., an asset management firm jointly owned by GE Capital Corp., EBay Inc. and Benchmark Capital. From April 1999 to January 2000, Mr. Mooney was the chief financial officer at Baan Company, a business management software provider that had dual headquarters in Amsterdam and Virginia. From 1980 to March 1999, Mr. Mooney held a number of positions with IBM Corporation, including his last position as the chief financial officer of the Americas. Mr. Mooney is also a director of Sirius Satellite Radio and was the chairman of RCN Corporation, a telecommunications service provider based in the U.S., until December 2007.

Information regarding directors not standing for election at the meeting, including present business experience and business experience during the past five years, follows:

Continuing Directors Whose Terms Expire in 2009

Edwin M. Banks

Mr. Banks, age 45, has been a director since May 7, 2003, chairs our compensation committee, and serves on the executive and audit committees and the nominating sub-committee. Mr. Banks is the founder of Washington Corner Capital Management, L.L.C, an investment management firm. From 1988 to October 2006, Mr. Banks served as a portfolio manager for W.R. Huff Asset Management Co., L.L.C. Mr. Banks is currently a director of CKX, Inc. and CVS/Caremark Corp.

George R. Zoffinger

Mr. Zoffinger, age 60, has been a director since January 10, 2003, chairs our audit committee, and serves on the executive and compensation committees and the nominating sub-committee. From March 2002 until December 2007, he served as the president and chief executive officer of the New Jersey Sports and Exposition Authority. From March 1998 to March 2002, he served as president and chief executive officer of Constellation Capital Corporation, a financial services company. Mr. Zoffinger is currently a director of New Jersey Resources Inc.

Neil A. Berkett

Mr. Berkett, age 52, was appointed as a director by the board on April 7, 2008, and has been our chief executive officer since March 6, 2008. Prior to that, he served as our acting chief executive officer

3

from August 2007 to March 2008 and as our chief operating officer from September 26, 2005 to August 2007. Prior to joining us, Mr. Berkett was managing director of distribution at Lloyds TSB since 2003. From 2002 to 2003, he was chief operating officer of Prudential Assurance Company Limited. From 1997 to 2002, he was a principal at Marsh Mill Consulting Ltd, and from 1998 to 2002, he was also chief executive of Trek Investco Ltd.

Continuing Directors Whose Terms Expire in 2010

Jeffrey D. Benjamin

Mr. Benjamin, age 46, has been a director since January 10, 2003 and serves on the audit and compensation committees. He is currently a senior advisor to Apollo Management, LP, a private investment fund, and has held that position since September 2002. Mr. Benjamin currently serves on the boards of directors of Exco Resources, Inc. and Harrah's Entertainment, Inc.

Gordon D. McCallum

Mr. McCallum, age 48, has been a director since September 11, 2006. Since September 2005, he has been chief executive officer of Virgin Management, Virgin Group's U.K.-based management services company providing corporate services and general management oversight of Virgin's investment portfolio. From January 1998 to September 2005, Mr. McCallum was group strategy director of Virgin Management and prior to that, he worked for Virgin Management as a freelance consultant.

Executive Officers Who Are Not Directors

A description of our executive officers who are not directors, including present business experience and business experience during the past five years, follows:

Andrew Barron

Mr. Barron, age 42, became our managing director of strategy and corporate development on March 17, 2008. Before he joined us Mr. Barron was chief executive officer of the Viasat broadcasting division of Scandinavian broadcaster MTG from September 2002. From January 2003 to September 2003, he served as chief operating officer of the MTG group. Prior to that, Mr. Barron was chief executive officer of Chello Media, a division of United-PanEurope Communications, from November 1999 to June 2002. Prior to that, Mr. Barron was executive vice president of new media and business development at Walt Disney Europe.

Robert C. Gale

Mr. Gale, age 47, became our vice president—controller on June 17, 2003 and prior to that was the group director of financial control for our U.K. operations since October 2000. Mr. Gale joined us in May 2000 when we acquired the cable operations of Cable & Wireless Communications plc, where he had held a number of senior financial positions since 1998. Prior to that, Mr. Gale was chief financial officer of Comtel, a cable operator subsequently acquired by us, from 1995 to 1997.

Charles K. Gallagher

Mr. Gallagher, age 42, became senior vice president—finance on December 18, 2007. Mr. Gallagher served on our board of directors from August 2003 until December 2007 and was the chairman of our audit committee during that period. From September 2001 to March 2007, Mr. Gallagher was chief financial officer of Viewpointe Archive Services, a joint venture among Bank of America, JP Morgan Chase & Co., U.S. Bancorp, SunTrust Banks, Inc., Wells Fargo and IBM that engages in the imaging and archiving of digital copies of checks.

4

Bryan H. Hall

Mr. Hall, age 45, became our secretary and general counsel on June 15, 2004. From September 2000 to June 2004, Mr. Hall was a partner in the corporate department of the law firm Fried, Frank, Harris, Shriver & Jacobson LLP in New York, specializing in public and private acquisitions and acquisition financings. Mr. Hall is an attorney licensed to practice in the State of New York.

Mark Schweitzer

Mr. Schweitzer, age 48, became our chief commercial officer on October 1, 2007. Before he joined us, Mr. Schweitzer was chief marketing officer of Sprint Nextel, a wireless communications company, from August 2005 to June 2007. Prior to that, he was senior vice president of marketing of Nextel Communications from April 1997 to August 2005. Mr. Schweitzer has been managing marketing, sales and customer operations functions in the communications industry since 1981, including experience with Time Warner Cable, MCI Communications and McCaw Wireless.

Malcolm R. Wall

Mr. Wall, age 51, became the chief executive officer of our content division on March 3, 2006. Prior to that, he was the chief executive officer of the content division at Telewest since January 31, 2006. Mr. Wall served as chief operating officer at United Business Media plc from 2001 to 2005. Prior to that, he was chief executive officer of United Broadcasting and Entertainment Ltd from 1996 to 2000.

Howard Watson

Mr. Watson, age 45, became our chief technology and information officer on March 3, 2006. Prior to that, Mr. Watson was the managing director of network technology and IT at Telewest where he had a number of key technical and managerial roles since 1993. In 1997, Mr. Watson became managing director—networks at Telewest and led the build and operation of all of Telewest's network including the build of the national network and the digital television and broadband platforms. In 2001, Mr. Watson also became responsible for IT for Telewest.

Independence of Directors

Our board of directors currently consists of seven members. In evaluating directors' independence, the board uses the independence criteria set forth in the Nasdaq Global Select Market listing standards currently applicable to us. The board has surveyed each of our directors and has determined that, Messrs. Banks, Benjamin, Huff and Zoffinger are independent and Messrs. Berkett, McCallum and Mooney are not independent within the meaning of the Nasdaq Global Select Market listing standards. Messrs. Connors, Elstein and Gallagher were considered to be independent while they served on our board of directors in 2007. Messrs. Burch, Huff and Duffy were not considered to be independent while they served on our board of directors in 2007. On February 8, 2008, it was determined by the board that Mr. Huff was an independent director as of January 1, 2008 within the meaning of the Nasdaq Global Select Market listing standards since more than three full calendar years had elapsed since the receipt of a payment by his affiliate in 2004 that had resulted in the previous determination that he was not independent.

Meetings of the Board of Directors

During the year ended December 31, 2007, the board of directors held eight meetings and acted by way of unanimous written consent pursuant to Section 141(f) of the General Corporation Law of the State of Delaware on three occasions. All directors attended, in the aggregate, 75% or more of all

5

board meetings and of all meetings of committees of which they were a member during the period for which they were a director.

Compensation of Directors

We use a combination of cash and stock-based compensation to attract and retain qualified candidates to serve on our board of directors. We reimburse our directors for out-of-pocket expenses related to attending meetings of our board of directors and committees. Our non-employee board members are paid quarterly based on an annual fee of £50,000, which is paid in U.S. dollars (converted at an average exchange rate for the relevant quarter) to our directors who are based in the United States. Our directors who are our employees do not receive additional compensation for their service as a member of our board of directors. The chairman of our audit committee receives an additional fee of $20,000 per year and the chairman of our compensation committee receives an additional fee of $15,000 per year.

As adjusted for the conversion of shares in the Merger, in 2003, we granted each of our non-employee board members who was then in office options to purchase 187,500 shares of our common stock at the time of their election to our board of directors. These director options vested in equal installments on the first three anniversaries of the date of grant and fully vested in 2006. Except in the case of Mr. Gallagher, whose options were granted at an exercise price of $16.00 per share, these options were granted at an exercise price of $6.00 per share. As a result of changes in U.S. federal income tax laws by the adoption of section 409A of the Internal Revenue Code, option holders who held options with exercise prices below the market price at the time of issuance that had not vested prior to January 1, 2005 faced substantial additional tax and penalties. On December 21, 2007, the Company and Mr. Banks agreed to increase the exercise price of his 125,000 options that fell within this category from $6.00 to $7.82 per share to reflect the market price of the Company's common stock at the time of issuance and the Company and Mr. Gallagher agreed to increase the exercise price of his 125,000 options that fell within this category from $16.00 to $17.53 to reflect the market price of the Company's common stock at the time of issuance. As compensation for this adjustment, on March 3, 2008, the Company issued to Mr. Banks 14,996 shares of the Company's common stock with a market value of $227,500 and issued to Mr. Gallagher 12,623 shares of the Company's common stock with a market value of $191,500.

At the March 16, 2006 board meeting, each non-employee board member who was then in office was granted options to purchase an additional 187,500 shares. These options have an exercise price of $29.06 per share and vest in equal installments on the first three anniversaries of the grant date. These options are intended to reward the non-employee directors for the significant time and attention required of them in connection with the integration of the businesses of NTL and Telewest and our other business activities, to encourage them to remain on the board of directors and to provide them with appropriate incentives to increase the value of the Company to its stockholders. The directors who were employees of the Company did not receive these awards. It was agreed at a subsequent board meeting as a matter of policy that new non-employee directors who join the board of directors after that date, but during the three-year vesting period, would be granted a prorated number of options with an exercise price that is the higher of the price on March 16, 2006 and the price on the date of grant, and with the same vesting schedule as the March 16, 2006 grant. Gordon D. McCallum joined the board of directors of the Company on September 11, 2006 and on September 14, 2007, the Company granted Mr. McCallum options to purchase 156,250 shares of the Company's common stock at an exercise price of $29.06 per share. Mr. McCallum advised the Company that he and Virgin Enterprises Limited are parties to an arrangement pursuant to which he holds these options in trust for the benefit of Virgin Enterprises Limited.

6

Director Summary Compensation Table

The table below summarizes the compensation paid by us to non-employee directors for the fiscal year ended December 31, 2007.It should be noted in reviewing the table below that the amounts included under the column heading "Option Awards" represent the dollar amounts recognized for financial statement reporting purposes in accordance with FAS 123(R). These amounts do not necessarily reflect the current market value or fair value of these awards. For example, many of the exercise prices of the option awards included below are above the closing share price at December 31, 2007.

Unless otherwise noted, all amounts in this table paid in pounds sterling have been translated into U.S. dollars at a rate of $2.0017 per £1.00.

| Name(1) (a) | Fees Earned or Paid in Cash ($) (b) | Stock Awards ($) (c) | Option Awards(2) ($) (d) | Non-Equity Incentive Plan Compensation ($) (e) | Change in Pension Value and Nonqualified Deferred Compensation Earnings (f) | All Other Compensation(3) ($) (g) | Total ($) (h) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Edwin M. Banks(4) | 115,364 | — | 506,128 | — | — | — | 621,492 | ||||||||

| Jeffrey D. Benjamin | 100,364 | — | 506,128 | — | — | — | 606,492 | ||||||||

| William J. Connors(5) | 37,016 | — | (294,293 | ) | — | — | — | (257,277 | ) | ||||||

| Simon Duffy(6) | 42,344 | — | — | — | — | 19,307 | 61,651 | ||||||||

| David Elstein | 100,085 | — | 506,128 | — | — | — | 606,213 | ||||||||

| Charles K. Gallagher(7) | 119,045 | — | 506,128 | — | — | — | 625,173 | ||||||||

| William R. Huff | 100,364 | — | 506,128 | — | — | — | 606,492 | ||||||||

| Gordon D. McCallum(8) | 100,085 | — | 256,072 | — | — | — | 356,157 | ||||||||

| George R. Zoffinger | 101,683 | — | 506,128 | — | — | — | 607,811 |

- (1)

- Messrs. Burch and Mooney are not included in this table as they were our employees and therefore received no separate compensation for their services as directors and the compensation received by Messrs. Burch and Mooney is shown under the "Summary Compensation Table" in this proxy statement. Messrs. Connors, Duffy, Elstein and Gallagher no longer serve on our board of directors.

- (2)

- Reflects the dollar amount recognized for financial statement reporting purposes for the fiscal year ended December 31, 2007 in accordance with Statement of Financial Accounting Standards ("SFAS") No. 123R, "Share-based Payments", or FAS 123(R), and therefore may include amounts from awards granted in and prior to 2007. As of December 31, 2007, each director had the following aggregate number of options outstanding: Mr. Banks—375,000; Mr. Benjamin—375,000; Mr. Connors—0; Mr. Duffy—0; Mr. Elstein—187,500; Mr. Gallagher—500,000 (this includes 125,000 options granted to Mr. Gallagher when he joined us as senior vice president—finance on December 18, 2007); Mr. Huff—375,000; Mr. McCallum—156,250; and Mr. Zoffinger—375,000. As compensation for the adjustment of the exercise price of their options, on March 3, 2008, the Company issued to Mr. Banks 14,996 shares of the Company's common stock with a market value of $227,500 and issued to Mr. Gallagher 12,623 shares of the Company's common stock with a market value of $191,500.

- (3)

- The value of all perquisites and personal benefits for each director was less than $10,000 in 2007.

- (4)

- On December 21, 2007, the Company and Mr. Banks agreed to increase the exercise price of the 125,000 options granted to him at the time of his election to our board of directors from $6.00 to $7.82 to reflect the market price of the Company's common stock at the time of issuance. As this repricing involved an increase in the exercise price, there was no incremental fair value recognized in accordance with FAS 123(R).

7

- (5)

- Mr. Connors' term expired on May 16, 2007. On this date, Mr. Connors' 125,000 unvested options were forfeited.

- (6)

- Mr. Duffy, our former executive vice chairman, left the Company and resigned from the board of directors on January 15, 2007. The amount included under column (b) includes Mr. Duffy's base salary of £500,000 in respect of his employment with the Company pro rata to January 15, 2007. Mr. Duffy's All Other Compensation for the 2007 fiscal year includes $16,681 in pension contributions by the Company and $2,626 in health insurance and income protection benefits.

- (7)

- On December 21, 2007, the Company and Mr. Gallagher agreed to increase the exercise price of the 125,000 options granted to him at the time of his election to our board of directors from $16.00 to $17.53 to reflect the market price of the Company's common stock at the time of issuance. As this repricing involved an increase in the exercise price, there was no incremental fair value recognized in accordance with FAS 123(R).

- (8)

- The grant date fair value of the 156,250 options granted to Mr. McCallum on September 14, 2007 was $560,299.

Staggered Board

Our amended and restated certificate of incorporation provides for a classified board of directors consisting of three classes as nearly equal in number as possible. Directors in each class serve staggered three-year terms. Our Class I Directors are William R. Huff and James F. Mooney and their terms terminate on the date of this year's annual meeting of stockholders. Our Class II Directors are Edwin M. Banks, George R. Zoffinger and Neil A. Berkett and their terms terminate on the date of our 2009 annual meeting of stockholders. Our Class III Directors are Jeffrey D. Benjamin and Gordon D. McCallum and their terms will terminate on the date of our 2010 annual meeting of stockholders. At each annual meeting of stockholders, successors to the class of directors whose term expires at that annual meeting are elected for a three-year term. Consistent with our certificate of incorporation, in order to have a more equal number of directors in each class of directors after the resignations of Charles K. Gallagher and David Elstein, on February 6, 2008, Mr. Zoffinger resigned as a Class I Director and was appointed by the board of directors as a Class II Director. Neil A. Berkett was appointed as a Class II Director on April 7, 2008 in connection with his appointment as our chief executive officer.

Board of Directors Committees

The board of directors has an audit committee established in accordance with Section 3(a)(58)(A) of the Securities Exchange Act of 1934, as amended, which we refer to as the Exchange Act, a compensation committee and an executive committee. Our executive committee has a nominating sub-committee. From time to time the board of directors may establish other committees as it deems necessary.

Audit Committee

The audit committee of the board of directors reviews, acts on and reports to our board of directors with respect to various auditing and accounting matters. The audit committee is directly responsible for the appointment, compensation and oversight of the independent auditors; pre-approves all audit and permissible non-audit services provided by the independent auditors; reviews and approves the Company's financial statements; reviews and evaluates the Company's internal control structure and procedures for financial reporting and disclosure controls and procedures; monitors compliance with the Company's code of ethics; sets procedures for the receipt and treatment of complaints regarding accounting, controls and auditing matters; and retains professional advisors. The current members of the audit committee are George R. Zoffinger, who was appointed as its chairman on December 7,

8

2007, Edwin M. Banks and Jeffrey D. Benjamin. Mr. Banks was added as a committee member on December 7, 2007. Our former audit committee chairman, Charles K. Gallagher, resigned from the audit committee on December 7, 2007 prior to his appointment as our senior vice president—finance. David Elstein left the audit committee on February 4, 2008 in connection with his resignation from our board of directors. The board of directors has affirmatively determined that Mr. Zoffinger satisfies the definition of "audit committee financial expert" for purposes of the Exchange Act and the Nasdaq Global Select Market listing standards. The members of the audit committee are independent within the meaning of the Nasdaq Global Select Market listing standards currently applicable to us and Rule 10A-3(b)(1) of the Exchange Act. The audit committee held eleven meetings during 2007. Our board of directors has adopted a written charter for the audit committee. A copy of the audit committee charter is attached to this proxy statement as Appendix A.

Compensation Committee

The compensation committee determines the annual compensation for our executive officers. The compensation committee consists of Edwin M. Banks, who is its chairman, Jeffrey D. Benjamin and George R. Zoffinger. Mr. Benjamin was added as a committee member on December 7, 2007. David Elstein left the compensation committee on February 4, 2008 in connection with his resignation from our board of directors. The members of the compensation committee are independent within the meaning of the Nasdaq Global Select Market listing standards. Both prior to and following the Merger, the compensation committee has served as the compensation and option committee under the Virgin Media Inc. 2006 Stock Incentive Plan (which is the former NTL Incorporated 2006 Stock Incentive Plan), the Amended and Restated Virgin Media Inc. 2004 Stock Incentive Plan (which is the former NTL Incorporated 2004 Stock Incentive Plan), and the Virgin Media Inc. 2004 Stock Incentive Plan (which is the former Telewest Global, Inc. 2004 Stock Incentive Plan). The compensation committee held ten meetings during 2007 and acted by way of unanimous written consent pursuant to Section 141(f) of the General Corporation Law of the State of Delaware on four occasions. Our board of directors has adopted a written charter for the compensation committee. A copy of the compensation committee charter is attached to this proxy statement as Appendix B.

Executive Committee

The executive committee is responsible for recommending individuals to serve on the board of directors and as our executive officers, advising the board with respect to the board's committees and other structural issues, overseeing our management, approving budgets and recommending other changes in our management, operations, strategy and business. The executive committee consists of William R. Huff, who is its chairman, Edwin M. Banks, James F. Mooney and George R. Zoffinger. On March 15, 2004, we established a sub-committee of the executive committee to serve as the nominating committee and the responsibility for recommending individuals to serve on the board of directors was delegated to the nominating sub-committee. Further information regarding the nominating sub-committee is provided below. The executive committee held three meetings during 2007. The executive committee held one additional meeting in 2007 through a sub-committee.

Nominating Sub-Committee

Our nominating committee is a sub-committee of the executive committee. It consists of all of the members of the executive committee who are independent directors within the meaning of the Nasdaq Global Select Market listing standards. Presently, its members consist of William R. Huff, who is its chairman, Edwin M. Banks and George R. Zoffinger. The nominating sub-committee considers and recommends nominees for election to the board of directors, consistent with the board's criteria for selecting new directors and independence requirements imposed by law and the Nasdaq Global Select Market listing standards. In addition, the nominating sub-committee will review the suitability for

9

continued service of each existing director when his or her term expires or there is a significant change in his or her status, including his or her outside employment. The nominating sub-committee held one meeting during 2007. Our board of directors has adopted a written charter for the nominating sub-committee. A copy of the nominating sub-committee charter is attached to this proxy statement as Appendix C.

The nominating sub-committee will consider recommendations for director nominees proposed by directors, management or stockholders. Stockholders may recommend nominees by giving timely notice of such recommendation in proper written form to our corporate secretary at Virgin Media Inc., 909 Third Avenue, Suite 2863, New York, New York 10022. You must be one of our stockholders of record on the date you give the notice and on the record date for the determination of stockholders entitled to notice of, and to vote at, the relevant meeting. On occasion, the nominating sub-committee may consider retaining a third party to identify candidates and would, in such circumstances, pay an appropriate fee to the third party for that service. The nominating sub-committee did not engage a third party for that purpose during 2007 or in connection with the nomination of directors for election at this year's annual meeting of stockholders.

In evaluating nominees, the nominating sub-committee will generally consider the current size and composition of the board, including the current number of independent directors and whether there is a vacancy on the board. The nominating sub-committee will also consider the skills and experience of the existing directors and the nominee relative to our business and its needs, the nominee's individual reputation for integrity, honesty and adherence to high ethical standards, the nominee's demonstrated business acumen and ability to exercise sound judgments that relate to our current and long-term objectives, the nominee's ability to act in the interests of all stockholders and the presence or absence of conflicts of interest that would or might impair the nominee's ability to represent the interests of all our stockholders and to fulfill the responsibilities of a director. There is no difference in the evaluation of a nominee recommended by board members, management or stockholders.

Stockholder Nominations

Pursuant to the advance notice requirements set forth in Article II, Section 5 of our by-laws, in the case of a stockholder notice of a nomination of a director at an annual meeting, we will consider the notice timely if we receive such notice not less than 75 days nor more than 90 days prior to the first anniversary of the date of the preceding year's annual meeting of stockholders. However, if the date of the annual meeting is advanced more than 30 days prior to, or delayed by more than 30 days after, the anniversary of the preceding year's annual meeting, we will consider notices of stockholder proposals to be timely if we receive them not later than the close of business on the tenth day following the day on which notice of the date of the annual meeting was mailed or public disclosure of the date of the annual meeting is first given or made, whichever first occurs.

In the case of a stockholder nomination of a director at a special meeting called for the purpose of electing directors, we will consider the notice timely if we receive such notice not later than the close of business on the tenth day following the day on which notice of the date of the special meeting was mailed or public disclosure of the date of the special meeting is first given or made.

The stockholder's notice must in each case set forth as to each person the stockholder proposes to nominate for election as a director:

- •

- the name, age, business address and residence address of the person;

- •

- the principal occupation or employment of the person;

- •

- the class or series and number of shares of our capital stock which are owned beneficially or of record by the person; and

10

- •

- any other information relating to the person that would be required to be disclosed in a proxy statement or other filings required to be made in connection with solicitations of proxies for election of directors pursuant to Section 14 of the Exchange Act and the rules and regulations promulgated under the Exchange Act.

As to the stockholder giving the notice, the notice should set forth:

- •

- the name and record address of the stockholder proposing the nomination;

- •

- the class or series and number of shares of our capital stock which are owned beneficially or of record by the stockholder;

- •

- a description of all arrangements or understandings between the stockholder and each proposed nominee and any other person or persons (including their names) pursuant to which the nomination(s) are to be made by the stockholder;

- •

- a representation that the stockholder intends to appear in person or by proxy at the meeting to nominate the persons named in its notice; and

- •

- any other information relating to the stockholder that would be required to be disclosed in a proxy statement or other filings required to be made in connection with solicitations of proxies for election of directors pursuant to Section 14 of the Exchange Act and the rules and regulations promulgated under the Exchange Act.

The notice must be accompanied by a written consent of each proposed nominee to being named or referred to in our proxy statement as a nominee of the board of directors and to serve as a director if elected. We may require any proposed nominee to furnish other information (which may include meetings to discuss the information) as may reasonably be required by us to determine the eligibility of the proposed nominee to serve as one of our directors.

No person is eligible for election as one of our directors unless he or she has been nominated in accordance with the procedures set forth in Article II, Section 5 of our by-laws and summarized above. An officer of ours presiding at the meeting shall, if the facts warrant, determine and declare to the meeting that the nomination was defective in accordance with the provisions of Article II, Section 5 of our by-laws, and if the officer shall also determine, the officer shall so declare to the meeting that the defective nomination be disregarded.

Compensation Committee Interlocks and Insider Participation

The compensation committee of our board consists of Edwin M. Banks, who is its chairman, Jeffrey D. Benjamin and George R. Zoffinger. David Elstein resigned from our board of directors and its audit and compensation committees on February 4, 2008. None of the members of the compensation committee has, at any time, been an officer or employee of ours and none has any relationship requiring disclosure under Item 404 of Regulation S-K under the Exchange Act. No interlocking relationship exists between our board of directors or compensation committee and the board of directors or compensation committee of any other company nor has any relationship existed in the past.

Stockholder Communications with the Board of Directors

Stockholders, employees and members of the public generally are encouraged to communicate to management, or directly to any member of the board of directors, any concerns which they may have about us, our management, business activities, practices or conduct, although the board believes that communications regarding auditing matters, our accounting practices, internal controls and compliance with ethical standards are best directed to the chairman of the audit committee.

11

Communications may be addressed to the board of directors and any individual director or member of management, c/o Virgin Media Inc., 909 Third Avenue, Suite 2863, New York, New York 10022. The identity of persons expressing concerns that are critical of our board of directors, management or us, or that relate to violations of law or ethical standards of conduct, will be treated as confidential except to the extent necessary to evaluate and, if appropriate, investigate and address the questions or concerns raised. There will be no retaliation taken against persons who raise questions or concerns about us lawfully and in good faith.

Code of Ethics

We have adopted a code of ethics for our principal executive officer, principal financial officer, and principal accounting officer or controller, or persons performing similar functions. Our code of ethics establishes policies to promote honest and ethical conduct and to deter wrongdoing, including policies governing actual or apparent conflicts of interest, compliance with laws and prompt internal reporting for violations.

Our code of ethics is posted on our website atwww.virginmedia.com/investors under "Corporate Governance". In the event that we amend our code of ethics or grant a waiver from its restrictions to a person covered by the code of ethics, we will provide this information on our website within four business days following the date of the amendment or waiver.

We will provide to any person without charge, upon request, a copy of our code of ethics. Requests should be sent to Richard Williams, Virgin Media Inc.—Director Investor Relations, 909 Third Avenue, Suite 2863, New York, New York 10022, tel: +1 212 906 8447, fax: +1 212 752 1157.

Director Attendance at Annual Meetings of Stockholders

We encourage all of our directors to attend the annual meeting of stockholders. All of our directors attended the annual meeting held in 2007 with the exception of William J. Connors whose term ended on the date of the 2007 annual meeting.

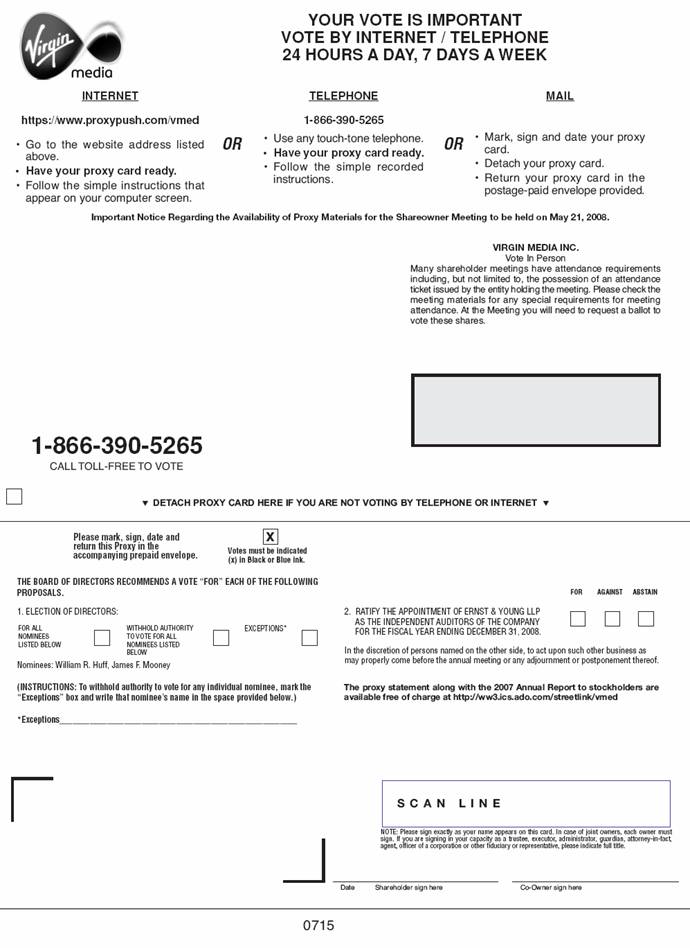

Stockholder Approval

Directors are elected by a plurality of the votes cast by the holders of shares of our common stock present in person or represented by proxy at the annual meeting and entitled to vote.Unless you indicate otherwise in your proxy, the proxy holders intend to vote the shares they represent "FOR" the election of each of Messrs. Huff and Mooney. In tabulating the vote, abstentions from voting and broker non-votes will be disregarded and will have no effect on the outcome of the vote.

Recommendation of the Board of Directors

The board of directors recommends that stockholders vote "FOR" the election of each of the nominees to the board of directors.

12

PROPOSAL 2

RATIFICATION OF APPOINTMENT OF

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The second proposal is to ratify the appointment by the audit committee of Ernst & Young LLP as the independent auditors for the fiscal year ending December 31, 2008.

Subject to ratification by the stockholders, the audit committee is reappointing Ernst & Young LLP as independent registered public accounting firm to audit our financial statements for the fiscal year ending December 31, 2008.

Representatives of the firm of Ernst & Young LLP are expected to be available by telephone at the annual meeting and will have an opportunity to make a statement if they so desire and are expected to be available to respond to appropriate questions.

Audit Fees

Ernst & Young LLP are our principal accountants. We provide in the table below an analysis of the fees billed to us by Ernst & Young LLP in each of the two years ended December 31, 2006 and December 31, 2007 (in millions). All of these services were pre-approved by the audit committee.All amounts in this table that originated in pounds sterling in respect of the year ended December 31, 2007 have been translated into U.S. dollars at a rate of $2.0017 per £1.00 and in respect of the year ended December 31, 2006 have been translated at a rate of $1.8429 per £1.00.

| | December 31, | |||||

|---|---|---|---|---|---|---|

| | 2007 | 2006 | ||||

| | (in millions) | |||||

| Audit fees | $ | 7.6 | $ | 10.9 | ||

| Audit-Related fees | 0.1 | 0.7 | ||||

| Tax fees | 2.7 | 6.5 | ||||

| All other fees | 0.1 | — | ||||

| $ | 10.5 | $ | 18.1 | |||

Audit fees. Audit fees represent the aggregate fees incurred for audit services provided to us by Ernst & Young LLP. Audit services included the audit of our annual financial statements included in our Form 10-K, the audit of our internal controls over financial reporting as required by Section 404 of the Sarbanes-Oxley Act of 2002, the quarterly review of financial statements included in our Forms 10-Q, the audit of the annual financial statements of Virgin Media Investment Holdings Limited ("VMIH") included in our Form 10-K, the quarterly review of the financial statements of VMIH included in our Forms 10-Q, the audit of the annual financial statements of South Hertfordshire United Kingdom Fund, Ltd. ("South Herts") included in its Form 10-K, the quarterly review of the financial statements of South Herts included in its Forms 10-Q, the statutory audits of the financial statements of our affiliates and subsidiaries as required under the U.K. Companies Act, the provision of reports provided to support statutory declarations made in connection with the U.K. financial assistance rules and services provided in connection with various regulatory filings in connection with the Merger and the acquisition of Virgin Mobile (UK) Holdings plc (the "Acquisition") including the provision of comfort and consent letters.

Audit-Related fees. Audit-Related fees represent the aggregate fees incurred for assurance and related services by Ernst & Young LLP that are related to the audit or review of our financial statements. Audit-Related services included the audit of our pension schemes together with advisory services provided in connection with the Merger and the Acquisition, including due diligence reviews.

13

Tax fees. Tax fees represent the aggregate fees incurred for professional services rendered by Ernst & Young LLP for tax compliance and tax advice. Tax services included compliance work regarding the preparation and filing of our U.S. tax returns, advice on various employee tax matters and advising on various corporate tax issues, in particular relating to various corporate transactions, including the Merger and the Acquisition and related financing arrangements.

All Other fees. All other fees represent the aggregate fees billed for all other products and services provided by Ernst & Young LLP. For the year ended December 31, 2007, this represented fees in respect of real estate advisory services. There were no such services provided in 2006.

Audit Committee's Pre-approval Policies and Procedures

The Audit Committee's policy on pre-approval requirements for audit and non-audit services provided to us by our independent registered public accounting firm was amended in March 2007 and is summarized as follows:

- •

- Annually, the Audit Committee will agree on the scope and terms, including the fees, of the engagement for the services to be provided by the Auditors as part of the recurring annual audit of the Company ("Annual Audit Services"). The services included as part of the Annual Audit Services include: the audit of the Company's consolidated financial statements and its internal control over financial reporting; the audit of the separate financial statements of South Herts, VMIH and Subsidiaries, Virgin Media Finance PLC and any other subsidiaries or affiliates which may require audits in relation to securities issued or to be issued, including, if required, the audits of their internal control over financial reporting; the review of interim unaudited financial statements of the Company and the separate interim unaudited financial statements of South Herts and VMIH and any other subsidiaries or affiliates which may require reviews in relation to securities issued or to be issued; and the statutory audits of the financial statements of the Company's subsidiaries and affiliates.

- •

- Annually, the Audit Committee will pre-approve, on a category basis, additional audit services, such as correspondence with regulatory agencies, consents to registration statements, comfort letters, and other financial reports required by regulatory bodies ("Additional Audit Services").

- •

- Quarterly, the Audit Committee will pre-approve, on an engagement specific basis, the Audit-Related services, Tax services and Other services for permissible services as set forth in the pre-approval policy, plus any additional categories of Additional Audit Services not included in the annual pre-approval (collectively, inclusive of those additional categories of Additional Audit Services, "Permitted Services") to be provided by the Auditors to the Company in respect of Permitted Services which are expected to commence during the following three months.

- •

- Each request for pre-approval of Permitted Services will be accompanied by an estimate of the related fee although such fee estimate will not represent the maximum fee that may be incurred unless the Audit Committee expressly requests that a limit be imposed in respect of a specific service.

- •

- Between meetings, the Chairman of the Audit Committee has delegated authority to pre-approve Services within the scope of Permitted Services on an ad-hoc basis to meet specific needs with estimated fees of up to £100,000 per engagement. The Chairman will report any such services approved in this manner to the next meeting.

- •

- The Audit Committee will be informed routinely as to the audit and non-audit services actually provided by the Auditors pursuant to this policy, including details of the fees billed for such services.

14

Stockholder Approval

The ratification of the appointment of Ernst & Young LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2008 will require the affirmative vote of the holders of a majority of our outstanding shares of common stock present at the annual meeting in person or represented by proxy at the annual meeting and entitled to vote.Unless you indicate otherwise in your proxy, the proxy holders intend to vote the shares they represent "FOR" the ratification of the appointment of Ernst & Young LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2008. In tabulating the vote, abstentions from voting will be counted and will have the same effect as a vote against the proposal; broker non-votes will be disregarded and will have no effect on the outcome of the vote.

Recommendation of the Board of Directors

The board of directors recommends that stockholders vote "FOR" the ratification of the appointment of Ernst & Young LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2008.

15

COMPENSATION DISCUSSION AND ANALYSIS

Executive Summary

The following discussion and analysis by our compensation committee is intended to provide a basis for understanding the factors influencing the determination of compensation of our named executive officers with respect to the 2007 fiscal year. More specific compensation information and discussion of the terms of our plans can be found in the tables, plan descriptions and other analysis that follow this report.

The current design of the Company's executive compensation programs utilizes a mix of base salary, variable annual bonus, equity-based incentives and other benefits. The Company believes that this design properly motivates its senior executives to perform and to seek to produce strong returns for the Company and its stockholders. In the view of the compensation committee, our current programs and level of compensation are appropriate for purposes of recruiting, retaining and incentivizing the named executive officers, consistent with the Company's compensation philosophy.

Compensation Committee Procedures

In accordance with its charter, the compensation committee has responsibility for establishing, implementing and monitoring adherence to the compensation philosophy set out below, and approving the compensation arrangements for our named executive officers, among others.

The compensation committee considers recommendations from the chief executive officer as to compensation of other named executive officers except for the chairman. The chief executive officer also participates in compensation committee discussions regarding the compensation of those officers. The chief executive officer does not participate in compensation committee discussion of his own or the chairman's compensation. The compensation committee also considers recommendations from the chairman as to executive compensation of other named executive officers. The compensation committee approves the chairman's compensation but receives recommendations from the executive committee (excluding the chairman), including in respect of certain performance objectives and achievements of the chairman relating to his performance-based restricted stock. The compensation committee also reviews information provided by the Company's human resources department.

For the 2007 fiscal year, the compensation committee, together with the Company, retained external advisors, including Deloitte Consulting LLP ("Deloitte"), to provide advice on a variety of compensation matters at its management's request. The advice provided by Deloitte was mainly with regard to named executive officer compensation trends and levels, and the design of the Company's incentive plans. In late 2007, the compensation committee engaged Deloitte to undertake a review of the reward strategy for the organization and expects to receive the results of the analysis in mid-2008.

The Company also consults with its executive search consultants in order to structure compensation packages for new hires at a level required to achieve its recruitment needs while maintaining its philosophical objectives. This information is reviewed by the compensation committee in approving proposed compensation arrangements.

The compensation committee considers all information provided to it by its external advisors, the Company's human resources department and the chief executive officer and/or the chairman, however, it makes the final decision with regard to overall executive compensation strategy and individual executive remuneration having considered all information provided as well as its own collective experience and judgment. It may also, where appropriate, consult with other members of the board of directors.

16

General Compensation Philosophy

The compensation committee aims to ensure that the Company's compensation program is aligned with its overall business strategy and culture. As a leading entertainment and communications business providing the first "quad-play" offering of television, broadband, fixed line telephone and mobile telephone services in the United Kingdom, the Company's compensation plans and practices are designed to fulfill the following core objectives:

- (1)

- attract and retain talented executives to drive achievement of the Company's business objectives;

- (2)

- provide fair, competitive compensation to the executive officers and other employees based upon their performance and contributions to the Company; and

- (3)

- align the incentives of the executive officers with the interests of stockholders and develop a sense of Company ownership through the use of annual and long-term cash and stock incentives.

1. Attract and Retain Talented Executives

In 2006 and 2007, the Company faced increased competition as more companies began offering "triple-play" television, broadband and fixed line telephony services that competed directly with its product offering. The changing nature of the industry and the intensely competitive marketplace enhanced our need to use more market driven compensation arrangements in order to recruit and retain the right individuals. The following factors remain relevant to the Company's approach in 2007:

- •

- the need to recruit talented, experienced senior executives by attracting them from existing positions in more established, stable organizations, and in some instances, to compensate them for arrangements they were leaving behind; and

- •

- the need to attract a small number of expatriates from the United States to grow the business, given that: (a) the U.S. is a key talent pool for the cable industry because of the longer historical success of cable companies and the subsequent opportunity to develop best practices across the cable industry there; and (b) Virgin Media Inc. is a U.S. public company, with primarily a U.S. investor base, and consequently, its senior executives need to be experienced and comfortable in addressing the relevant U.S. securities law requirements, corporate law issues and the expectations of both its equity and debt holders.

2. Provide Fair, Competitive Compensation Based upon Performance

The Company's incentive compensation programs are designed to measure and reward annual performance and long-term performance. Annual performance targets are included in the annual bonus scheme covering a majority of the Company's employees and provide the primary link between incentive compensation and the Company's business strategy and operational results for the fiscal year. The performance targets under the annual programs are reviewed and established each year based on the Company's business goals and the competitive environment. Long-term performance targets are also included in the equity-based long-term incentive plans. Many of the named executive officers also have performance-based restricted stock awards which vest based on annual or longer term performance targets. These compensation programs and the principal measures used to implement them are described in further detail in the following sections.

17

3. Align the Incentives of Executive Officers with the Interests of Stockholders and Develop a Sense of Company Ownership

Commencing with the restructuring of its legacy companies in 2003-2004, the Company has focused on aligning the incentives of its senior executives with stockholder value creation through compensation packages that are heavily weighted toward non-equity and equity incentive compensation. The compensation committee also believes that it is important that the named executive officers have the opportunity to build a meaningful ownership stake in the Company through restricted stock, restricted stock units and stock options. The issuance of these awards under the incentive plans is intended to align the executives' interests with stockholders' interests by placing this part of the executives' compensation "at risk" for any share price decline that may occur.

The compensation committee believes that structuring executive incentive programs to align with the interests of the stockholders and to develop in the executives a sense of Company ownership should play a significant part in the Company's performance and success. Executive compensation is aligned with the interests of the stockholders by linking incentive compensation performance measures to metrics that are indicators of the Company's financial and operational performance, including for example:

- •

- group operating profit before depreciation, amortization and other charges ("Group OCF");

- •

- group simple cash flow, being Group OCF less fixed asset additions on an accrual basis less cash payments in respect of merger-related redundancies ("Group SCF");

- •

- divisional financial measures, including revenue, gross margin, operating costs, working capital, simple cash flow, capital expenditure and profitability measures;

- •

- customer service measures, including fault rates, customer advocacy, customer satisfaction and net promoter measures;

- •

- average revenue per customer ("ARPU"), or average contribution per customer ("ACPU"); and

- •

- net additions to revenue generating units ("RGUs").

The performance criteria vary depending upon the particular executive in question, but focus on the enhancement of cash flow, and may also include long-term performance criteria.

Elements of Compensation

The Company seeks to achieve its compensation objectives through four core compensation elements:

- •

- base salary;

- •

- variable, annual, performance-based cash bonus;

- •

- periodic grants of long-term equity-based compensation such as stock options, restricted stock units and/or shares of restricted stock; and

- •

- benefits and retirement plans.

18

These elements are designed to combine to promote the objectives referred to above. The following table illustrates how each element of compensation is related to the Company's objectives:

| | | | Reward for Performance | | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Compensation Element | Attract | Retain | Short Term | Long Term | Alignment with Stockholder Interests | |||||

| Base salary | X | X | ||||||||

| Performance-based cash bonus | X | X | X | X | ||||||

| Equity-based awards | X | X | X | X | X | |||||

| Benefits/retirement | X | X | ||||||||

The combination of base salary, retirement plans and benefits provide a minimum level of compensation to help attract and retain experienced, well-qualified executives. The performance-based cash bonus is designed to reward achievement of annual goals central to the business and creation of stockholder value. For the named executive officers and other senior employees, the Company believes that equity and performance-based compensation relate most directly to the achievement of operational and financial targets, as well as building stockholder value.

We generally review the market competitiveness of our executive officer compensation programs annually and after any major restructuring programs. Where a review shows that the executive compensation programs are not competitive, management may recommend changes to the compensation committee.

The Company's philosophy is to target total compensation (base salary, bonus, equity awards, benefits and retirement plans) above the median of companies similar in size and complexity to help ensure its ability to attract and retain the talent required to achieve its business strategy. The competition for senior executive talent within the technology and telecommunications industry in the U.K. and in the U.S. is high. A named executive officer's experience, performance, specific skill set, or the unique nature of the scope of responsibilities, significantly influences that individual's total compensation.

Base Salary

The objective of base salary is to provide a fixed compensation to an individual reflecting their job responsibilities, experience, value to the organization and demonstrated performance. In reviewing the salary positioning for the named executive officers, the compensation committee considers the Company's profile, which is:

- (i)

- U.K.-based. The Company's customers and employees are based in the U.K., with headquarters located in Hook, Hampshire and London. The Company largely competes for talent in the U.K. marketplace, with a need to attract a small number of senior executives from the U.S. (or elsewhere outside of the U.K.), due to their breadth of experience in the cable market or familiarity with the U.S. legal system and financial markets;

- (ii)

- U.S.-listed. The Company is incorporated in the U.S., listed on the Nasdaq stock exchange, and subject to the U.S. regulations and corporate governance requirements; and

- (iii)

- Converging Telecoms Industry. The Company was the first to offer the "quad-play" bundle of television, broadband, fixed line telephone and mobile telephone services to customers in the U.K. and is one of a very few major consumer telecoms companies in the U.K. It therefore does not have a large pool of executives experienced in its industry to draw from, particularly in the U.K.

19

The basic salary element of the compensation package, after initially attracting and retaining the executive, is the fixed and guaranteed element of a named executive officer's annual cash compensation, serving as the baseline from which the calculation for other elements are made. Each of the named executive officers is party to a negotiated employment agreement, which provides for a specified or minimum base salary. More detailed descriptions of the non-equity terms of the employment agreements with each of the named executive officers can be found in the section entitled "Summary Compensation Table—Summary of Non-Equity Compensation Terms of Employment Agreements".

Prior to entry into each employment agreement, the compensation committee establishes the base salary by consideration of:

- •

- the Company's overall compensation philosophy;

- •

- the nature of the role and the accountabilities associated with the position;

- •

- the individual's experience, expertise, knowledge, and qualifications;

- •

- the salaries of the Company's other executives;

- •

- market salary ranges; and

- •

- any recommendation from the chief executive officer and/or chairman.

Salary Reviews

The compensation committee annually reviews the base salaries of all the named executive officers in June of each year and any adjustments are at the committee's discretion. Any salary adjustments are usually made effective from July 1st; however, in 2007, the salary adjustments were effective September 1st. The factors considered at any review include, but are not limited to:

- •

- individual performance in the prior year;

- •

- any changes in the level of accountabilities;

- •

- how the executive's salary compares with the salaries of the Company's other executives;

- •

- market salary ranges;

- •

- cost of living and inflation;

- •

- retention considerations; and

- •

- recommendations from the chief executive officer and/or chairman.

20

The following table details the base salaries of the named executive officers for the 2007 fiscal year as well as any increases made in the 2007 fiscal year:

| Name | Salary | Adjusted Salary Effective September 1, 2007 | |||

|---|---|---|---|---|---|

| James F. Mooney, chairman | $1,250,000 | $ | 1,250,000 | ||

Stephen A. Burch, president and chief executive officer to August 21, 2007 | $750,000 | N/A | |||

Neil A. Berkett, chief operating officer to August 21, 2007, acting chief executive officer to March 6, 2008, chief executive officer from March 6, 2008 | £425,000 | £425,000 | |||

Jacques D. Kerrest, chief financial officer to March 31, 2008 | £330,000 | £339,900 | |||

Bryan H. Hall, general counsel | £320,000 | £329,600 | |||

Malcolm R. Wall, CEO—content division | £350,000 | £360,500 | |||

Messrs. Kerrest, Hall and Wall were the only named executive officers in 2007 to benefit from base salary increases. A decision was made by the compensation committee to increase these salaries by three percent, taking into account market factors (including the cost of living and inflation), prior salary changes, individual performance and salary increases across the broader business (which were generally at three percent).

Changes in Named Executive Officers

During 2007, Mr. Burch left the Company, Mr. Berkett was promoted to acting chief executive officer and Mr. Kerrest's employment term was extended. In each case, this had impact upon the affected employee's compensation, as discussed below.

Mr. Burch's employment terminated by mutual agreement on August 21, 2007 and, in connection with the termination, we entered into an agreement with Mr. Burch. Under the agreement and upon the execution of a general release in favor of the Company, Mr. Burch was paid $1.5 million, representing two times his base salary, which is the amount he would have received had his contract been terminated without cause. Mr. Burch also received the right to retain:

- •

- 250,000 vested shares of restricted stock; and

- •

- 250,000 unvested shares of restricted stock of which: 125,000 shares vested on January 15, 2008 and 125,000 vested on March 15, 2008, subject to Mr. Burch not having breached any provision of the agreement entered into upon his termination or the restrictive covenants under his employment agreement.

Mr. Burch forfeited 625,000 unvested shares of restricted stock and all rights thereto and all remaining options and shares. In addition, Mr. Burch is subject to non-competition and non-solicitation covenants that survive for eighteen months following termination of employment.

Mr. Berkett was promoted to acting chief executive officer in August 2007, replacing Mr. Burch. An additional option award was provided to Mr. Berkett; however, the compensation committee did not change Mr. Berkett's base salary or bonus percentage.

The term of Mr. Kerrest's employment agreement was extended in December 2007. In connection with his extension, the committee did not alter his base salary or bonus percentage and did not grant additional options. However, the compensation committee did alter other compensation arrangements as part of the extension, such as amending his severance arrangements.

21

Variable Annual Bonus

The compensation committee designs an annual incentive bonus program for the named executive officers intended to reward them for achieving specific quantitative and qualitative goals, aligned with driving significant operational performance to increase stockholder value. This is underpinned by the belief that at the higher levels of accountability, the executive officers and senior managers have more direct influence on the achievement of the Company's strategy, and subsequently, the compensation committee believes that a larger proportion of the executive's total compensation should be variable and based upon the Company's performance. The on-target bonus potential is agreed as part of each named executive officer's employment. This is represented as a target percentage of his or her base salary—for our senior executives this ranges from 50% to 100% of base salary depending on the position. For outstanding performance, the executive is entitled to receive up to a cap of double the on-target bonus percentage.

Bonuses are based upon performance by the Company in a given calendar year, but are paid in the March or April following completion of the year-end audit. Therefore, the 2006 bonus was paid in 2007 and the 2007 bonus would have been paid in 2008.

Individual bonus entitlements for the named executive officers for the 2007 fiscal year were as follows:

| Name | Bonus Entitlement | |

|---|---|---|

| James F. Mooney, chairman | 100% on-target based on an assumed base salary of $400,000 | |

Stephen A. Burch, president and chief executive officer to August 21, 2007 | 0–200% of base salary | |

Neil A. Berkett, chief operating officer to August 21, 2007, acting chief executive officer to March 6, 2008, chief executive officer from March 6, 2008 | 0–200% of base salary | |

Jacques D. Kerrest, chief financial officer to March 31, 2008 | 0–150% of base salary | |

Bryan H. Hall, general counsel | 0–150% of base salary | |

Malcolm R. Wall, CEO—content division | 0–150% of base salary |

In 2007, the compensation committee approved the Company's 2007 annual bonus scheme (the "2007 Bonus Scheme") covering the majority of the Company's employees, including the Company's named executive officers. In order for any bonuses to be payable under the 2007 Bonus Scheme, the Company needed to achieve a qualifying performance target of Group OCF for the 2007 fiscal year of £1,335 million (the "Qualifying Gate"). If the Qualifying Gate was achieved, bonuses would be payable according to achievement against various performance targets specific to each of the Company's key operating divisions.