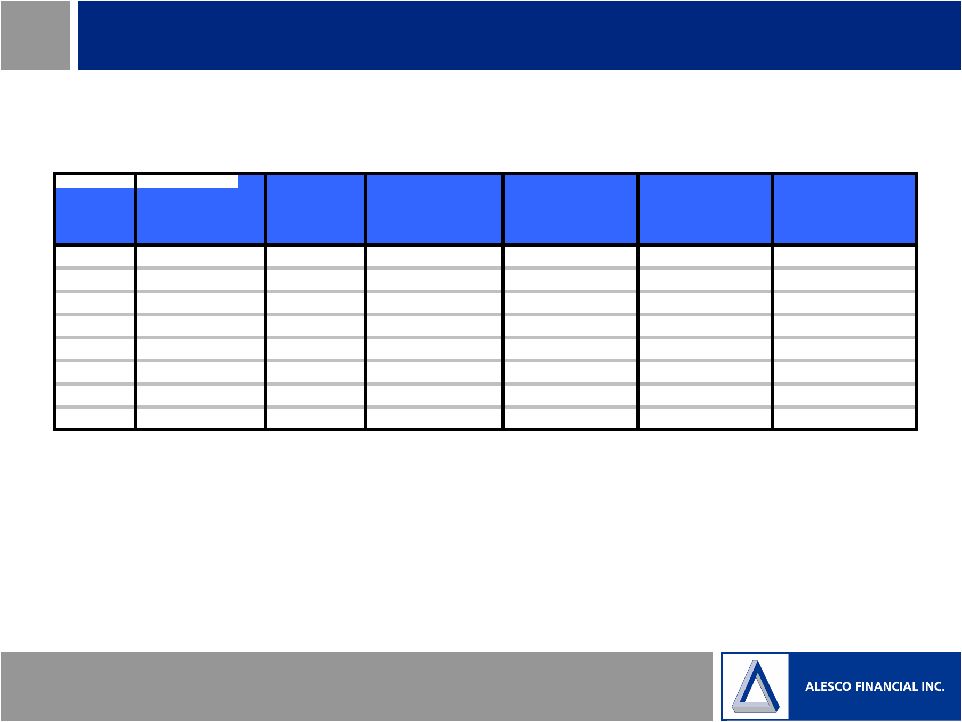

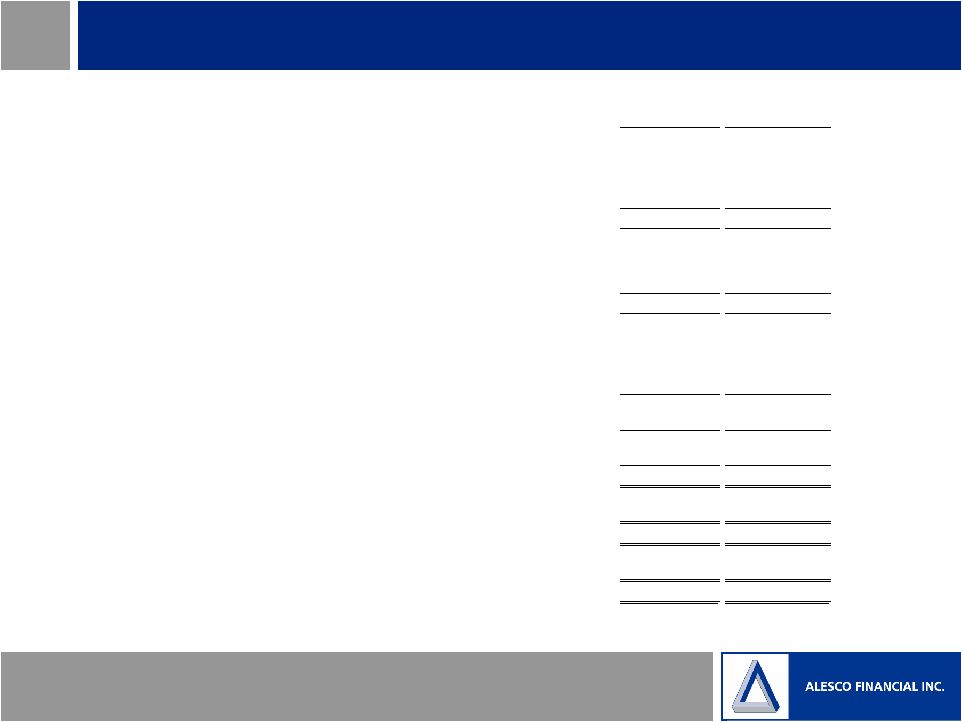

Alesco Financial – Balance Sheet as of December 31, 2006 Asof December31,2006 Assets Investments in debt securities and related receivables Available-for -sale debt securities ................................ ................................ ............. $ 6,771,914 Security-related receivables ................................ ................................ ....................... 1,170,210 Total investment in debt securities and security- related receivables ...................... 7,942,124 Investments in residential and commercial mortgages and leveraged loans Residential mortgages ................................ ................................ ................................ 1,773,147 Commercial mortgages ................................ ................................ ............................... 9,500 Leveraged loans ................................ ................................ ................................ ......... 314,077 Loan loss reserve ................................ ................................ ................................ ....... (2,130) Total investmen ts in residential and commercial mortgages and leveraged loans, net ................................ ................................ ................................ ............................ 2,094,594 Cash and cash equivalents ................................ ................................ ............................ 51,821 Restricted cash and warehouse deposits ................................ ................................ ...... 349,113 Accrued interest receivable ................................ ................................ ............................ 46,654 Other assets................................ ................................ ................................ ................... 30,621 Deferred financing costs, netof accumulated amortization of $ 2,762 ......................... 87,423 Total assets ................................ ................................ ................................ .................. $10,602,350 Liabilities and stockholders’ equity Indebtedness Repurchase agreements ................................ ................................ ................................ $3,024,269 Trust preferred obligations ................................ ................................ ........................... 273,097 CDO notes payable ................................ ................................ ................................ ...... 6,496,748 Warehouse credit facility ................................ ................................ .............................. 167,158 Junior subordinated notes ................................ ................................ .............................. 20,619 Total indebtedness ................................ ................................ ................................ ....... 9,981,891 Accrued interest payable ................................ ................................ ................................ 42,163 Related party payable ................................ ................................ ................................ .. 879 Other liabilities ................................ ................................ ................................ ............. 50,017 Total liabilities ................................ ................................ ................................ ............ 10,074,950 Minority interest ................................ ................................ ................................ ........... 98,598 Stockholder’s equity Preferred shares, $0.001 par value per share, 50,000,000 shares authorized, no shares issued and outstanding ................................ ................................ .................. — Common shares, $0.001 par value per share, 100,000,000 shares authorized, 54,922,071 issued and outstanding, including 193,457 unvested restricted share awards ................................ ................................ ................................ ............ 55 Additional paid in capital ................................ ................................ ................................ 447,442 Accumulated other comprehensive loss ................................ ................................ ...... (14,628) Cumulative distributions ................................ ................................ ................................ (26,098) Cumulative earnings ................................ ................................ ................................ .... 22,031 Total stockholders’ equity ................................ ................................ ........................... 428,802 Total liabilities and stockholders’ equity ................................ ................................ $10,602,350 |