Exhibit 99.1

ENTRÉE GOLD INC.

Annual Information Form

FOR THE YEAR ENDED

DECEMBER 31, 2008

DATED MARCH 26 2009

TABLE OF CONTENTS

| DATE OF INFORMATION | | | 2 | |

| FORWARD LOOKING STATEMENT | | | 2 | |

| CURRENCY AND EXCHANGE | | | 3 | |

| DEFINED TERMS AND ABBREVIATIONS | | | 3 | |

| CANADIAN DISCLOSURE STANDARDS FOR MINERAL RESOURCES AND MINERAL RESERVES | | | 3 | |

| CORPORATE STRUCTURE | | | 4 | |

| GENERAL DEVELOPMENT OF THE BUSINESS | | | 5 | |

| DESCRIPTION OF THE BUSINESS | | | 12 | |

| RISK FACTORS | | | 14 | |

| MINERAL PROPERTIES | | | 23 | |

| DIVIDENDS | | | 34 | |

| CAPITAL STRUCTURE | | | 34 | |

| MARKET FOR SECURITIES | | | 34 | |

| ESCROWED SECURITIES | | | 35 | |

| DIRECTORS AND OFFICERS | | | 36 | |

| PROMOTERS | | | 42 | |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | | | 42 | |

| INTEREST IN MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | | | 42 | |

| TRANSFER AGENTS AND REGISTRARS | | | 42 | |

| MATERIAL CONTRACTS | | | 43 | |

| INTEREST OF EXPERTS | | | 44 | |

| ADDITIONAL INFORMATION | | | 44 | |

APPENDIX

ENTRÉE GOLD INC.

ANNUAL INFORMATION FORM

DATE OF INFORMATION

Unless otherwise specified in this Annual Information Form, the information herein is presented as at December 31, 2008, the last date of the Company’s most recently completed financial year-end.

FORWARD LOOKING STATEMENT

This Annual Information Form (the “AIF”) and documents incorporated by reference herein contain “forward-looking statements” and “forward looking information” (together the “forward looking statements”) within the meaning of securities legislation and the United States Private Securities Litigation Reform Act of 1995. These forward-looking statements are made as of the date of this AIF or, in the case of documents incorporated by reference herein, as of the date of such documents and the Company does not intend, and does not assume any obligation, to update these forward-looking statements, except as required by applicable securities laws.

Forward-looking statements include, but are not limited to, the future price of gold and copper, the estimation of mineral reserves and resources, the realization of mineral reserve and resource estimates, the timing and amount of estimated future production, costs of production, capital expenditures, cost and timing of the development of new deposits, success of exploration activities, permitting time lines, currency fluctuations, requirements for additional capital, government regulation of mining operations, environmental risks, unanticipated reclamation expenses, title disputes or claims and limitations on insurance coverage. In certain cases, forward-looking statements can be identified by the use of words such as "plans", "expects" or “does not expect”, “is expected”, “budget”, “scheduled”, "estimates", “forecasts”, “intends”, “anticipates”, or “does not anticipate” or “believes” or variations of such words and phrases or statements that certain actions, events or results "may", “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”. While the Company has based these forward-looking statements on its expectations about future events as at the date that such statements were prepared, the statements are not a guarantee of the Company’s future performance and are subject to risks, uncertainties, assumptions and other factors which could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. Such factors and assumptions include, amongst others, the effects of general economic conditions, changing foreign exchange rates and actions by government authorities, uncertainties associated with legal proceedings and negotiations and misjudgments in the course of preparing forward-looking statements. In addition, there are also known and unknown risk factors which may cause the actual results, performances or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Such factors include, among others, risks related to international operations; actual results of current exploration activities; actual results of current reclamation activities; conclusions of economic evaluations; changes in project parameters as plans continue to be refined; future prices of gold and copper; possible variations in ore reserves, grade recovery and rates; failure of plant, equipment or processes to operate as anticipated; accidents, labour disputes and other risks of the mining industry; delays in obtaining government approvals or financing or in the completion of development or construction activities, as well as those factors discussed in the section entitled “Risk Factors” in this AIF. Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

CURRENCY AND EXCHANGE

Our financial statements are stated in United States dollars and are prepared in conformity with United States Generally Accepted Accounting Principles.

In this AIF, all dollar amounts are expressed in U.S. dollars unless otherwise specified. Because our principal executive office is located in Canada, many of our obligations are and will continue to be incurred in Canadian dollars (including, by way of example, salaries, rent and similar expenses). Where the disclosure is not derived from the annual financial statements for the year ended December 31, 2008, we have not converted Canadian dollars to U.S. dollars for purposes of making the disclosure in this AIF.

DEFINED TERMS AND ABBREVIATIONS

As used in this AIF, the terms "we", "us", "our", “the Company” and "Entrée" mean Entrée Gold Inc. and our wholly-owned subsidiaries Entrée LLC, Entrée Gold (US) Inc, Entrée Resources International Limited, Beijing Entrée Minerals Technology Company Limited and Entrée Holdings U.S. Inc. unless otherwise indicated.

CANADIAN DISCLOSURE STANDARDS FOR MINERAL RESOURCES AND MINERAL RESERVES

Canadian disclosure standard for the terms “Mineral Reserve,” “Proven Mineral Reserve” and “Probable Mineral Reserve” are Canadian mining terms as defined in accordance with National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”), which adopts the definitions of the terms ascribed by the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”) in the CIM Standards on Mineral Resources and Mineral Reserves, as may be amended from time to time by the CIM.

The definitions of proven and probable reserves used in NI 43-101 differ from the definitions in the United States Securities and Exchange Commission ("SEC") Industry Guide 7. Under SEC Guide 7 standards, a "Final" or "Bankable" feasibility study is required to report reserves, the three year historical average price is used in any reserve or cash flow analysis to designate reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority.

In addition, the terms "Mineral Resource", "Measured Mineral Resource", "Indicated Mineral Resource" and "Inferred Mineral Resource" are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and normally are not permitted to be used in reports and registration statements filed with the SEC. Investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into reserves. "Inferred Mineral Resources" may only be separately disclosed, have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases.

Accordingly, information contained in this report and the documents incorporated by reference herein containing descriptions of our mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

CORPORATE STRUCTURE

Name, Address and Incorporation

Entrée Gold Inc. is an exploration stage company engaged in the exploration of mineral resource properties located in Mongolia, China and the USA. Our principal executive office is located at Suite 1201 - 1166 Alberni Street, Vancouver, British Columbia, Canada V6E 3Z3. The telephone number for our principal executive office is (604) 687-4777 and our web site is located at www.entreegold.com. Information contained on our website does not form part of this AIF. Our registered and records office is at 2900-550 Burrard Street, Vancouver, BC, Canada V6C 0A3 and our agent for service of process in the United States of America is National Registered Agents, Inc., 1090 Vermont Avenue NW, Suite 910, Washington, DC 20005.

We maintain an administrative office in Ulaanbaatar, the capital of Mongolia, from which we support our Mongolian operations. The address of our Mongolian office is Jamyan Gun Street-5, Ar Mongol Travel Building, Suite #201, #202, Sukhbaatar District, 1st Khoroo, Ulaanbaatar, Mongolia. The telephone number for our Mongolian office is 976.11.318562.

We also maintain an administrative office in Beijing, China, from which we support our China operations. The address of our Beijing office is #2705 Tower 12, Wanda Plaza, Jianguo Road, Chaoyang District Beijing.

Our Company was incorporated in British Columbia, Canada, on July 19, 1995, under the name Timpete Mining Corporation. On February 5, 2001, we changed our name to Entrée Resources Inc. On October 9, 2002 we changed our name from Entrée Resources Inc. to Entrée Gold Inc. and, on January 22, 2003, we changed our jurisdiction of domicile from British Columbia to the Yukon Territory by continuing our company into the Yukon Territory. On May 27, 2005, the Company changed the governing jurisdiction from the Yukon Territory to British Columbia by continuing into British Columbia under the British Columbia Business Corporation Act.

At inception our Memorandum and Articles authorized our company to issue up to 20 million common shares without par value. On September 30, 1997, we subdivided our authorized capital on a two new shares for one old share basis, resulting in authorized capital of 40 million common shares without par value. On February 5, 2001, we subdivided our common shares on a four new shares for one old share basis, thus increasing authorized capital to 160 million common shares without par value and simultaneously reduced our authorized capital to 100 million common shares without par value. On October 9, 2002 we consolidated our authorized capital, both issued and unissued, on the basis of one new share for each two old shares, resulting in authorized capital of 50 million common shares without par value and simultaneously increased the authorized capital from 50 million common shares without par value to 100 million common shares without par value. On May 20, 2004, we received approval from our shareholders to increase our authorized share capital from 100 million common shares without par value to an unlimited number of common shares, all without par value. This increase became effective June 16, 2004, the date we filed the amendment to our Articles.

Intercorporate relationships

We have six wholly-owned subsidiary companies:

| | • | Entrée LLC, a Mongolian limited liability company formed July 25, 2002, which currently holds all of our assets in Mongolia but will eventually hold only those assets in Mongolia that are subject to the Entree-Ivanhoe Joint Venture. |

| | • | Entrée U.S. Holdings Inc., a British Columbia corporation organized on December 11, 2006, for the purpose of holding Entrée Gold (US) Inc. |

| | • | Entrée Gold (US) Inc. an Arizona corporation formed on December 22, 2006, for the purpose of conducting our United States operations. |

| | • | Beijing Entrée Minerals Technology Company Limited, a wholly foreign owned enterprise (WFOE) in China formed on May 27, 2008 for the purpose of conducting our China operations. |

| | • | Entrée Resources International Limited, a British Columbia corporation. |

| | • | Entrée Resources LLC, a Mongolian limited liability company formed to hold those Mongolian assets outside of the Entrée-Ivanhoe Joint Venture |

GENERAL DEVELOPMENT OF THE BUSINESS

Five Year History

In September 2003, the Company acquired a 100% interest in three mineral exploration licences (“MELs”) in Mongolia covering 179,590 hectares (collectively “Lookout Hill”) and a fourth mineral license (“Manlai”) for cash and stock.

In October 2004, the Company entered into an Equity Participation and Earn-in Agreement (“Earn-In Agreement”) with Ivanhoe Mines Ltd., through its wholly owned subsidiary Ivanhoe Mines Mongolia Inc. XXK (collectively, “Ivanhoe Mines”) to explore approximately 40,000 hectares of Lookout Hill (“Entrée-Ivanhoe Project Property”) in return for the right to earn a 70% or 80% interest in the Entrée-Ivanhoe Project Property depending on the depth of mineralization for the expenditure of $35 million in exploration (see below). Ivanhoe Mines also made an equity investment in the Company.

As of June 30, 2008, Ivanhoe Mines had expended a total of $35 million on exploration on the Entrée-Ivanhoe Project Property and in accordance with the Earn-In Agreement, Entrée and Ivanhoe Mines formed a joint venture on terms annexed to the Earn-In Agreement (the “Entrée-Ivanhoe Joint Venture”). During the year ended December 31, 2008, the Entree-Ivanhoe Joint Venture expended approximately $1.9 million. Ivanhoe has contributed Entrée’s 20% portion of the expenditures as an advance on future earnings.

During 2005, the Company raised $24,197,263 from the issuance of capital stock through an equity investment by Rio Tinto; through its wholly-owned Canadian subsidiary, Kennecott Canada Exploration Inc. (collectively, “Rio Tinto”), a further investment by Ivanhoe Mines (see below) and the exercise of warrants and stock options. Ivanhoe Mines carried out a drilling program on the Entrée-Ivanhoe Project Property, and Hugo North style-mineralization was first intersected in April 2005.

In March 2005, the Company became a Tier I Issuer on the TSX Venture Exchange. In July, 2005, the Company was approved for listing on the American Stock Exchange, now the NYSE Amex, under the trading symbol “EGI”. The Company is also traded on the Frankfurt Stock Exchange under the symbol “EKA, WKN:121411.” On April 24, 2006, the Company delisted from the TSX Venture Exchange and listed on the Toronto Stock Exchange (“TSX”), under the same symbol “ETG.”

In February 2006, the Company announced that a mineral resource estimate by AMEC Americas Limted (“AMEC”) had delineated an initial Inferred Resource for the Hugo North Extension. The Hugo North Extension is situated within the Entree-Ivanhoe Project Property on the Company’s Shivee Tolgoi MEL. An Inferred Resource of 190 million tonnes grading 1.57% copper and 0.53 grams per tonne (“g/t”) gold (a copper equivalent grade of 1.91%) was estimated to contain approximately 6.6 billion pounds of copper and 3.2 million ounces of gold.

During 2006, 11 diamond drill holes, totaling 8,614.1 metres and 18 shallow reverse circulation holes, totaling 3,290.0 metres, were completed by the Company on targets outside the Entrée-Ivanhoe Project Property on Lookout Hill. Additional work included IP and magnetometer geophysical surveys, soil and rock geochemical sampling, and geological mapping. The areas targeted by drilling included: West Grid geophysical, geological and geochemical anomalies; the large Ring Dyke geophysical anomaly and associated zones of alteration; the Zone III epithermal gold system; and the Zones I and II areas of associated alteration and geophysical targets.

In May 2006, the Company secured an option to acquire the Sol Dos copper prospect, located in the Safford district, of south-east Arizona. In February 2008, the Company chose to discontinue earning-in on this prospect due to the lack of favourable results and terminated this agreement.

In March 2007, the Company announced that an updated mineral resource estimate for the Hugo North Extension had been calculated, based on in-fill drilling conducted by Ivanhoe Mines to November 1, 2006. The updated mineral resource estimate was prepared by AMEC. At a 0.6% copper equivalent* (“CuEq”) cut-off, the Hugo North Extension is now estimated to hold an Indicated Resource of 117 million tonnes grading 1.80% copper and 0.61 g/t gold (a copper equivalent* grade of 2.19%). This Indicated Resource is estimated to contain 4.6 billion pounds of copper and 2.3 million ounces of gold. An Inferred Resource estimate for the Hugo North Extension is estimated to contain 95.5 million tonnes grading 1.15% copper and 0.31 g/t gold (a copper equivalent* grade of 1.35%). The contained metal estimated within the Inferred Resource portion of the Hugo North Extension is 2.4 billion pounds of copper and 950,000 ounces of gold. See Table 1 below.

Since the March 2007 announcement of the updated mineral resource estimate an additional 6 holes were drilled in the Hugo North Extension area for structure delineation, geotechnical and resource infill purposes. These holes have not been used in estimating resources at Hugo North. AMEC inspected the results of these holes and concluded they will have no material impact on the resource estimate.

Table 1: | Hugo North Extension Indicated and Inferred Mineral Resource on the Entrée-Ivanhoe Project Property as of February 20, 2007 |

| Class | CuEq Cut-off | Tonnage (tonnes) | Copper (%) | Gold (g/t) | CuEq* (%) | Contained Metal |

| Cu (‘000 lb) | Au (oz) | CuEq('000 lb) |

| Indicated | | | | | | | | |

| | 1.0 | 84,800,000 | 2.22 | 0.80 | 2.73 | 4,150,000 | 2,180,000 | 5,104,000 |

| | 0.6 | 117,000,000 | 1.80 | 0.61 | 2.19 | 4,643,000 | 2,290,000 | 5,649,000 |

| Inferred | | | | | | | | |

| | 1.0 | 62,200,000 | 1.39 | 0.39 | 1.64 | 1,906,000 | 780,000 | 2,249,000 |

| | 0.6 | 95,500,000 | 1.15 | 0.31 | 1.35 | 2,421,000 | 950,000 | 2,842,000 |

*Copper equivalent (CuEq) grades have been calculated using assumed metal prices (US$1.35/lb. for copper and US$650/oz. for gold); %CuEq = %Cu + [Au(g/t)x(18.98/29.76)]. The equivalence formula was calculated assuming that gold recovery was 91% of copper recovery.

On June 27, 2007, Rio Tinto exercised its “A” and “B” warrants and the Company issued 6,306,920 common shares for cash proceeds of $17,051,716. (See page 11 for details regarding warrants).

On June 29, 2007, Ivanhoe Mines exercised its “A” and “B” warrants purchased as part of a private placement in July 2005, and the Company issued 1,235,488 common shares for cash proceeds of $3,340,327.

On November 26, 2007, Entrée closed a short form prospectus offering of 10 million common shares at a price of C$3.00 per share for gross proceeds of C$30 million (the “Treasury Offering”) pursuant to an underwriting agreement between the Company and BMO Nesbitt Burns (the “Underwriter”). The Underwriter received a fee of C$1.8 million, being 6% of the gross proceeds of the Treasury Offering.

On November 26, 2007, in order to maintain its percentage ownership of Entrée’s issued and outstanding shares, at approximately 14.7%, Ivanhoe Mines exercised its pre-emptive rights and acquired, concurrently with the closing of the Treasury Offering, an aggregate of 2,128,356 shares of the Company at a price of C$3.00 per share for additional gross proceeds of C$6,385,068.

On November 26, 2007, in order to maintain its percentage ownership of Entrée’s issued and outstanding shares, at approximately 15.9%, Rio Tinto exercised its pre-emptive rights and acquired, concurrently with the closing of the Treasury Offering, an aggregate of 2,300,284 shares of the Company at a price of C$3.00 per share for additional gross proceeds of C$6,900,852.

In August 2007, the Company entered into an agreement with Empirical Discovery LLC (“Empirical”) to explore for and develop porphyry copper targets in southeastern Arizona and adjoining southwestern New Mexico. Under the terms of the agreement, Entrée has the option to acquire an 80% interest in any of the properties by incurring exploration expenditures totalling a minimum of $1.9 million and issuing 300,000 shares within 5 years of the anniversary of TSX acceptance of the agreement. If Entrée exercises its option, Empirical may elect within 90 days to retain a 20% participating interest or convert to a 2% net smelter returns (“NSR”) royalty, half of which may be purchased for $2 million.

Exploration at the Company’s Manlai project in 2007 focused on following up targets defined during the previous field season. Limited exploration was conducted at Manlai in 2008 as the Company focused on the Nomhkon Bohr target on the Togoot License (Lookout Hill Project).

In October 2007, Entrée received notice from Ivanhoe Mines that it had incurred the required expenditures ($20 million) to earn a 51% participating interest in the Entrée-Ivanhoe Project Property. On March 11, 2008, Ivanhoe Mines notified Entrée that it had incurred in excess of $27.5 million in expenditures, thus reaching a 60% participating interest. On June 30, 2008 Ivanhoe Mines notified Entrée that it had incurred expenditures of $35 million, fulfilling the requirement of the Earn-in Agreement and triggering the formation of an Entrée-Ivanhoe Joint Venture.

In November 2007, the Company entered into an agreement with the Zhejiang No. 11 Geological Brigade to explore for copper within three prospective, contiguous exploration licences, totaling approximately 61 square kilometres in Pingyang County, Zhejiang Province, People’s Republic of China. Entrée has agreed to spend $3 million to fund exploration activities on the licences (collectively known as “Huaixi” - see maps on www.entreegold.com) over a four year period. After Entrée has expended $3 million, the Company will have the right to earn a 78% interest and Zhejiang No. 11 Geological Brigade will hold a 22% interest in the project.

In January 2008, the Company entered into a second agreement with Empirical (the “Bisbee Agreement”) to explore for and test porphyry copper targets in a specified area near Bisbee, Arizona. Bisbee is located within a copper district that produced over 8 billion pounds of copper and 3 million ounces of gold in the last century. The Company intends to use the proprietary geophysical interpretation techniques developed by the principals of Empirical to locate buried porphyry targets. The area of interest covers over 10,800 acres (4,370 ha).

Under the terms of the Bisbee Agreement, Entrée has the option to acquire an 80% interest in any of the properties by incurring exploration expenditures totaling a minimum of $1.9 million and issuing 150,000 shares within 5 years of the anniversary of TSX acceptance of the agreement. If Entrée exercises its option, Empirical may elect within 90 days to retain a 20% participating interest or convert to a 2% NSR royalty half of which may be purchased for $2 million.

In March 2008, the Company received the first resource estimate prepared by Quantitative Geoscience Pty Ltd for the Heruga copper, gold, and molybdenum deposit. The Heruga deposit is situated within the Entrée-Ivanhoe Project Property on the Company’s Javhlant MEL, in southern Mongolia, immediately south of Ivanhoe Mines’ Oyu Tolgoi copper and gold deposit. Heruga is estimated to contain an Inferred Resource of 760 million tonnes grading 0.48% copper, 0.55 g/t gold and 142 ppm molybdenum for a copper equivalent* grade of 0.91%, using a 0.60% copper equivalent* cut-off grade, see Table 2 below. Based on these figures, the Heruga deposit is estimated to contain at least eight billion pounds of copper and 13.4 million ounces of gold. Drilling is being conducted by partner and project operator, Ivanhoe Mines.

Table 2. Heruga Inferred Resource - March 2008

| Cut-off | Tonnage | Cu | Au | Mo | Cu Eq* | Contained Metal |

CuEq % | 1000's (t) | % | g/t | ppm | % | Cu ('000 lb) | Au ('000 oz.) | CuEq ('000 lb) |

| >1.00 | 210,000 | 0.57 | 0.97 | 145 | 1.26 | 2,570,000 | 6,400 | 5,840,000 |

| >0.60 | 760,000 | 0.48 | 0.55 | 142 | 0.91 | 8,030,000 | 13,400 | 15,190,000 |

*Copper Equivalent estimated using $1.35/pound (“lb”) copper (“Cu”), $650/ounce (“oz”) gold (“Au”) and $10/lb molybdenum (“Mo”). The equivalence formula was calculated assuming that gold and molybdenum recovery was 91% and 72% of copper recovery respectively. CuEq was calculated using the formula CuEq = %Cu + ((g/t Au*18.98)+(%Mo*0.01586))/29.76.

The Company is actively engaged in looking for properties to acquire and manage, which are complementary to its existing projects, particularly large tonnage base and precious metal targets in eastern Asia and the Americas.

The commodities the Company is most likely to pursue include copper, gold and molybdenum, which are often associated with large tonnage, porphyry related environments. The Company has entered into agreements to acquire these types of targets over the past several months in the southwestern U.S and more recently in China. Other jurisdictions may be considered, depending on the merits of the potential asset.

Smaller, higher grade systems will be considered by the Company if they demonstrate potential for near-term production and cash-flow. If the Company is able to identify smaller, higher grade bodies that may be indicative of concealed larger tonnage mineralized systems, it may negotiate and enter into agreements to acquire them.

Significant Acquisitions in 2008

The Company made no significant acquisitions in 2008.

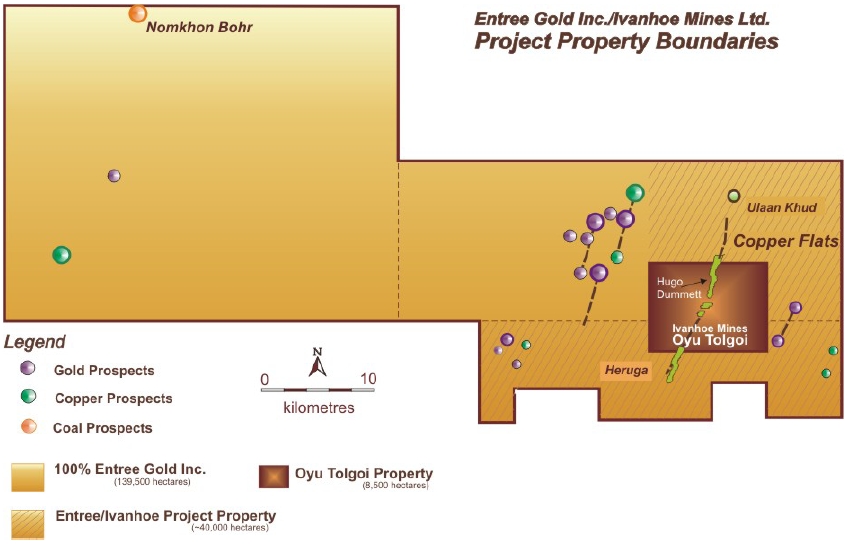

The Lookout Hill Property

The Company’s principal property is the Lookout Hill property in the Aimag of Omnogovi (also spelled Umnogobi) in the South Gobi region of Mongolia (an 'Aimag' is the local equivalent of a state or province),. Pursuant to an 'arms length' option agreement dated July 25, 2002, we purchased from Mongol Gazar Co., Ltd., (“Mongol Gazar”), an unrelated privately held Mongolian company, an option to acquire up to a 60% interest in three mineral licenses issued by the Mineral Resources and Petroleum Authority of Mongolia granting exploration rights, respectively, over three contiguous parcels of land known as Togoot (License No. 3136X), comprised of 104,484 hectares, Shivee Tolgoi (License No. 3148X), comprised of 54,760 hectares and Javhlant (License No. 3150X), comprised of 20,346 hectares. "Shivee Tolgoi" translates into English as "Lookout Hill" and we refer to all three of these parcels, collectively, as Lookout Hill. For a more detailed discussion of our Lookout Hill property please refer to the Property Description and Location section of this AIF, beginning at page 23, below.

Pursuant to a purchase agreement dated September 13, 2003 between our Company and our subsidiary Entrée LLC on the one hand, and Mongol Gazar and its Mongolian affiliate MGP LLC, on the other hand, we agreed to purchase a 100% interest in the Lookout Hill property, free of any NSR royalty, together with an additional mineral license (License No. 3045X) pertaining to a parcel of property known as the Manlai property, located in the Kharmagtai area of Mongolia in the Manlai and Tsogt-tsetsii Soums, Omnogovi Aimag (a 'Soum' is the local Mongolian term for a township or district), approximately 120 kilometres north of the Lookout Hill property (see below). In consideration for these properties we agreed to pay $5.5 million in cash and to issue 5 million common shares of our Company to Mongol Gazar. We also agreed that if Mongol Gazar sold these 5 million common shares at any time prior to November 30, 2004 for net proceeds of less than $5 million, we would pay them an amount equal to the difference between $5 million and the net proceeds they actually received. Although this purchase agreement superseded the option agreement dated July 25, 2002, we agreed that we would reinstate the option agreement if the transactions described in the purchase agreement did not close.

The purchase agreement provided that we could use the cash portion of the purchase price to clear any encumbrance on the Lookout Hill property, and that we were to pay the balance of the cash portion of the purchase price, and issue the 5 million common shares, fifteen days after we received notice from our Mongolian lawyers that satisfactory title to the Lookout Hill and Manlai properties had been transferred into the name of our Mongolian subsidiary, Entrée LLC, free of all liens, charges and encumbrances.

Because Mongol Gazar was still in the process of clearing title to the Manlai property at the time we were preparing to complete our acquisition of the Lookout Hill property, we entered into an Amending Agreement dated November 6, 2003 severing the Manlai property from the September 13, 2003 purchase agreement. We entered into a separate purchase agreement with respect to the Manlai property, pursuant to which we would acquire title to it for no additional consideration at such time as Mongol Gazar was able to transfer clear title. Title to this parcel was transferred to our subsidiary Entrée LLC on February 9, 2004.

Title to the Javhlant and Togoot parcels was transferred to our subsidiary, Entrée LLC, on September 30, 2003 and title to the third parcel comprising the Lookout Hill property, Shivee Tolgoi, was transferred to Entrée LLC on October 28, 2003. We paid the first part of the cash portion of the purchase price of $5.5 million, in the amount of $500,000, on September 19, 2003 and the balance of the cash portion of the purchase price on November 13, 2003.

In a subsequent agreement dated as of April 20, 2004, we agreed to issue to Mongol Gazar non-transferable share purchase warrants for the purchase of up to 250,000 of our common shares at a purchase price of $1.05 per share until expiration of the warrants on April 20, 2006 in consideration of (i) the waiver by Mongol Gazar of our obligation to pay to it the shortfall, if any, between $5 million and the net proceeds realized upon a sale of the 5 million common shares issued to them as part of the purchase price for the Lookout Hill property and (ii) a 100% interest in the Khatsavch Property (Licence #6500X, consisting of 632 hectares) located in Khanbogd and Bayan Ovoo Soums, Omnogovi, Mongolia. The share purchase warrants were issued on June 14, 2004, and title to the property has been registered in the name of Entrée LLC. Title to Khatsavch was subsequently returned to the Mongolian government in October 2007.

Equity Participation and Earn-in Agreement with Ivanhoe Mines Ltd.

Entrée entered into an arm’s-length Equity Participation and Earn-In Agreement (the “Earn-In Agreement”) in October 2004 with Ivanhoe Mines Ltd., title holder of the Oyu Tolgoi copper-gold deposit, which is located adjacent to and is surrounded by Entrée’s Lookout Hill property (see map on page 10). This agreement was subsequently assigned to a subsidiary of Ivanhoe Mines Ltd., Ivanhoe Mines Mongolia Inc. XXK, (collectively, “Ivanhoe Mines”).

The Earn-in Agreement provided that Ivanhoe Mines would have the right, subject to certain conditions outlined in the Earn-in Agreement, to earn a participating interest in a mineral exploration and, if warranted, development and mining project on a portion of the Lookout Hill property. Under the Earn-in Agreement, Ivanhoe Mines would conduct exploration activities in an effort to determine if the Oyu Tolgoi mineralized system extended onto the Entrée-Ivanhoe Project Property. Following execution of the Earn-in Agreement Ivanhoe Mines undertook an aggressive exploration program, which eventually confirmed the presence of two resources on Lookout Hill within the Entrée-Ivanhoe Project Property: the Hugo North Extension indicated and inferred resource to the north of Oyu Tolgoi and the inferred resource of the Heruga Deposit to the south of Oyu Tolgoi.

As of June 30, 2008, Ivanhoe Mines had expended a total of $35 million on exploration on the Entrée-Ivanhoe Project Property and in accordance with the Earn-In Agreement, Entrée and Ivanhoe Mines formed the Entrée-Ivanhoe Joint Venture. During the year ended December 31, 2008, the Entrée-Ivanhoe Joint Venture expended approximately $1.9 million. Ivanhoe has contributed Entrée’s 20% portion of the expenditures as an advance on future earnings.

Certain of Ivanhoe Mines' rights and obligations under the Earn-In Agreement, including a right to nominate one member of our Board of Directors, a pre-emptive right to enable them to preserve their ownership percentage in our Company, and an obligation to vote their shares as our Board of Directors directs on certain matters, expired with the formation of the joint venture. Ivanhoe’s right of first refusal to the remainder of Lookout Hill is maintained with the formation of the joint venture.

We believe that both the initial Earn-in Agreement and the joint venture are of significant benefit to our Company. The Earn-in Agreement enabled us to raise money that we used to pursue our exploration activities on the balance of our Lookout Hill property and elsewhere. It also enabled the exploration of the Entrée -Ivanhoe Project Property at little or no cost to our Company, leading to the delineation of indicated and inferred mineral resource estimates for the Hugo North Extension and the discovery and subsequent definition of a significant inferred resource on the Heruga deposit.

At December 31, 2008, Ivanhoe Mines owned approximately 14.6% of Entrée’s issued and outstanding shares.

At March 26, 2009, Ivanhoe Mines owned approximately 14.6% of Entrée’s issued and outstanding shares.

The area of Lookout Hill subject to the joint venture is shown below:

Investment by Rio Tinto in Entrée Gold Inc.

In June 2005, Rio Tinto, through its subsidiary Kennecott Canada Exploration (collectively, “Rio Tinto”), completed a private placement into Entrée, whereby they purchased 5,665,730 units at a price of C$2.20 per unit, which consisted of one Entrée common share and two warrants (one “A” warrant and one “B” warrant). Two “A” warrants entitle Rio Tinto to purchase one Entrée common share for C$2.75 within two years; two “B” warrants entitle Rio Tinto to purchase one Entrée common share for C$3.00 within two years. Proceeds from Rio Tinto’s investment were $10,170,207. In June 2005, Ivanhoe Mines exercised its unit warrants and purchase 4.6 million shares at C$1.10 per share, resulting in proceeds to Entrée of C$4,069,214. Ivanhoe Mines then exercised its pre-emptive right to maintain proportionate ownership of Entrée shares in July 2005 and took part in the private placement, purchasing 1,235,489 units, resulting in further proceeds to Entrée of $2,217,209. Rio Tinto purchased an additional 641,191 units of the private placement to maintain proportional ownership, resulting in further proceeds of $1,150,681.

On June 27, 2007, Rio Tinto exercised it’s “A” and “B” warrants and the Company issued 6,306,920 common shares for cash proceeds of $17,051,716.

On November 26, 2007, in order to maintain its ownership of Entrée’s issued and outstanding shares at approximately 15.9%, Rio Tinto exercised its pre-emptive rights and acquired, concurrently with the closing of the Treasury Offering, an aggregate of 2,300,284 shares of the Company at a price of C$3.00 per share for additional gross proceeds of C$6,900,852.

At December 31, 2008, Rio Tinto owned approximately 15.8% of Entrée’s issued and outstanding shares.

At March 26, 2009, Rio Tinto owned approximately 15.8% of Entrée’s issued and outstanding shares.

Rio Tinto is required to vote its shares as our board of directors directs on matters pertaining to fixing the number of directors to be elected, the election of directors, the appointment and remuneration of auditors and the approval of any corporate incentive compensation plan or any amendment thereof, provided the compensation plan could not result in any time in the number of common shares reserved for issuance under the plan exceeding 20% of the issued and outstanding common shares.

Investment by Rio Tinto in Ivanhoe Mines

In October 2006, Rio Tinto announced that it had agreed to invest up to $1.5 billion to acquire up to a 33.35% interest in Ivanhoe Mines. The proceeds from this investment were targeted to fund the joint development of the Oyu Tolgoi copper-gold project the “Oyu Tolgoin Project”). An initial tranche of $303 million was invested to acquire 9.95% of Ivanhoe Mines’ shares. It was further announced on September 12, 2007 that “Rio Tinto will provide Ivanhoe Mines Ltd. with a convertible credit facility of $350 million for interim financing for the Oyu Tolgoi copper-gold project in Mongolia. The credit facility is directed at maintaining the momentum of mine development activities at Oyu Tolgoi while Ivanhoe Mines and Rio Tinto continue to engage in finalising an Investment Agreement between Ivanhoe Mines and the government of Mongolia. If converted, this investment could result in Rio Tinto’s owning 46.65% of Ivanhoe Mines.” Entrée believes these investments represent, together with the exercise of the Entrée warrants, a major vote of confidence by one of the world’s pre-eminent mining companies in both the Oyu Tolgoi Project and in the country of Mongolia.

Mongolian Government

The Mongolian Parliament has been negotiating with Ivanhoe Mines for five years with regard to the Investment Agreement. The Investment Agreement is structured to stabilize tax, infrastructure and fiscal issues and guide the planned development and long-term operation of the Oyu Tolgoi Project. There was a general election in June 2008, that resulted in the return of the Mongolian People’s Revolutionary Party (“MPRP”) to a majority government. After a period of political unrest in the country, the government was formed and new cabinet ministers appointed. A Working Group was appointed to finalize negotiations with Ivanhoe Mines regarding the Investment Agreement. The Working Group forwarded their recommendation to the National Security Council, which then sent the agreement to Parliament on March 9, 2009. Parliament recessed on March 13, 2009, but gave assurances to Ivanhoe Mines that the Investment Agreement would be given priority in the next session, scheduled to begin in early April 2009.

Ivanhoe Mines and Rio Tinto have been meeting with Members of Parliament to discuss issues relating to the planned development of Oyu Tolgoi and lawmakers have visited the Oyu Tolgoi Project site to see work in progress. Ivanhoe Mines and Rio Tinto also have expressed their concerns to Members of Parliament, the Government’s Cabinet and the President about potential adverse impacts on the cost and timing for the Oyu Tolgoi project that would result from any further unexpected delays in the parliamentary approval process.

The draft agreement, once approved by Parliament, remains subject to approvals by the Ivanhoe Mines and Rio Tinto boards of directors.

Entrée continues to monitor developments in Mongolia, and maintains regular contact with Rio Tinto and Ivanhoe Mines regarding this matter.

DESCRIPTION OF THE BUSINESS

General

We are in the mineral resource business. This business generally consists of three stages: exploration, development and production. Mineral resource companies that are in the exploration stage have not yet found mineral resources in commercially exploitable quantities, and are engaged in exploring land in an effort to discover them. Mineral resource companies that have located a mineral resource in commercially exploitable quantities and are preparing to extract that resource are in the development stage, while those engaged in the extraction of a known mineral resource are in the production stage. Our Company is in the exploration stage.

Mineral resource exploration can consist of several stages. The earliest stage usually consists of the identification of a potential prospect through either the discovery of a mineralized showing on that property or as the result of a property being in proximity to another property on which exploitable resources have been identified, whether or not they are or have in the past been extracted.

After the identification of a property as a potential prospect, the next stage would usually be the acquisition of a right to explore the area for mineral resources. This can consist of the outright acquisition of the land or the acquisition of specific, but limited, rights to the land (e.g., a license, lease or concession). After acquisition, exploration would probably begin with a surface examination by a prospector or professional geologist with the aim of identifying areas of potential mineralization, followed by detailed geological sampling and mapping of this showing with possible geophysical and geochemical grid surveys to establish whether a known trend of mineralization continues through un-exposed portions of the property (i.e., underground), possibly trenching in these covered areas to allow sampling of the underlying rock. Exploration also commonly includes systematic regularly spaced drilling in order to determine the extent and grade of the mineralized system at depth and over a given area, as well as gaining underground access by ramping or shafting in order to obtain bulk samples that would allow one to determine the ability to recover various commodities from the rock. Exploration might culminate in a feasibility study to ascertain if the mining of the minerals would be economic. A feasibility study is a study that reaches a conclusion with respect to the economics of bringing a mineral resource to the production stage.

Our wholly-owned Mongolian subsidiary, Entrée LLC, is the registered owner of the three mineral exploration licences (Javhlant, Shivee Tolgoi and Togoot) comprising the Company’s principal property, the Lookout Hill property, permitting mineral exploration on three contiguous parcels of land located in Mongolia. The Company owns 100% interest in the portions of the licences outside the Entrée-Ivanhoe Project Property, and 20-30% interest in the Entrée-Ivanhoe Joint Venture, depending on depth of mineralization.

Entrée LLC is also the registered owner of a fourth mineral exploration licence (Ikh Ulziit Uul) in Mongolia, comprising the Manlai property. Entrée also has the right to earn direct or indirect interests in properties in China, Arizona and New Mexico.

Our company's exploration activities in Mongolia, China, and the USA are under the supervision of Robert Cann, P.Geo., Entrée's Vice President, Exploration. Mr. Cann is a "qualified person" as defined in NI 43-101. Except where otherwise noted, Mr. Cann is also responsible for the preparation of technical information in this AIF.

All mineral rock samples from our Mongolian properties are prepared and analyzed by SGS Mongolia LLC in Ulaanbaatar, Mongolia. All coal samples from Mongolia are prepared and analyzed by SGS Mongolia LLC and by SGS-CSTC Standards Technical Services Co., Ltd., Tianjin, China. Coal check samples were analyzed at Loring Laboratories Ltd. in Calgary, Canada. . Samples from Arizona and New Mexico are analyzed at ALS Chemex in Sparks, Nevada, at Skyline Assayer and Laboratories, Tuscon, Arizona and at Acme Analytical Laboratories, Vancouver, British Columbia, Canada. All samples from China are analyzed at ALS Chemex, Guangzhou and at SGS-CSTC Standards Technical Services Co., Ltd., Tianjin.

Environmental Compliance

Our current and future exploration and development activities, as well as our future mining and processing operations, if warranted, are subject to various federal, state and local laws and regulations in the countries in which we conduct our activities. These laws and regulations govern the protection of the environment, prospecting, development, production, taxes, labour standards, occupational health, mine safety, toxic substances and other matters. Our management expects to be able to comply with those laws and does not believe that compliance will have a material adverse effect on our competitive position. We intend to obtain all licenses and permits required by all applicable regulatory agencies in connection with our mining operations and exploration activities. We intend to maintain standards of compliance consistent with contemporary industry practice.

In Mongolia, mining companies are required to file an annual work plan with, and provide a summary report to, the local Soum upon the conclusion of exploration activities that includes a discussion of environmental impacts. In addition, mining companies are required to post a bond equal to 50% of the total estimated cost of any anticipated environmental reclamation, which is refunded upon completion of the reclamation work. We have filed our annual work plan for 2009 and we have posted a bond in Bayan Ovoo Soum equal to approximately $1,050. Although no work is planned in 2009 at Manlai, bonds remain in place at Tsogt Tsetsii Soum equal to approximately $490, and at Manlai Soum equal to approximately $490. These bonds cover environmental reclamation to the end of 2009. These amounts are refundable to us once we have completed all environmental work to the satisfaction of the local Soum (the local Mongolian equivalent of a township or district).

In Arizona and New Mexico, exploration companies are required to apply for a work permit that specifically details the proposed work program. A permit was granted in October 2008 for drilling on the Lordsburg property. A reclamation bond may be requested prior to the issuance of the appropriate permit but has not been requested to date.

Competition

The mineral exploration, development, and production industry is largely unintegrated. We compete with other exploration companies looking for mineral resource properties and the resources that can be produced from them. While we compete with other exploration companies in the effort to locate and license mineral resource properties, we do not compete with them for the removal or sale of mineral products from our properties, nor will we do so if we should eventually discover the presence of them in quantities sufficient to make production economically feasible. Readily available markets exist world-wide for the sale of gold and other mineral products. Therefore, we will likely be able to sell any gold or mineral products that we are able to identify and produce. Our ability to be competitive in the market over the long term is dependent upon the quality and amount of ore discovered, cost of production and proximity to our market. Due to the large number of companies and variables involved in the mining industry, it is not possible to pinpoint our direct competition.

Employees

At December 31, 2008, we had twenty-three employees working for us. We employ eleven employees in Vancouver, five employees in our office in Ulaanbaatar, Mongolia, two employees in our office in Beijing and five employees dedicated to our Mongolian and US field programs. During the 2008 field season, we also employed five contract expatriate geologists, geological technicians, camp support personnel and summer students at our Lookout Hill project. In addition to our expatriate employees, we hire up to 100 local personnel, including geologists, labourers, geophysical helpers, geochemical helpers, cooks, camp maintenance personnel, drivers and translators. These local personnel are hired as needed throughout each field season. The number of local hires fluctuates throughout the year, depending on the workload.

In the United States, our field operations are headed by a contract geologist who is supported by other contract geologists on an as-needed basis as well as a geologist and geological technician who also work on our Mongolian and China projects.

None of our employees belong to a union or are subject to a collective agreement. We consider our employee relations to be good.

RISK FACTORS

As stated on page 3, this AIF contains forward-looking statements, and any assumptions upon which they are based are made in good faith and reflect our current judgment regarding the direction of our business. Actual results will almost always vary, sometimes materially, from any estimates, predictions, projections, assumptions or other future performance suggested in this AIF. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

An investment in our common stock involves a number of very significant risks. You should carefully consider the following risks and uncertainties in addition to other information in this AIF in evaluating our Company and our business before purchasing shares of our Company's common stock. Our business, operating results and financial condition could be seriously harmed due to any of the following risks. The risks described below are not the only ones facing our Company. Additional risks not presently known to us may also impair our business operations. You could lose all or part of your investment due to any of these risks.

Risks Resulting From The Close Connection Between Ivanhoe Mines’ Oyu Tolgoi Project And The Company’s Shivee Tolgoi Earn-in Property.

As a result of the close connection between Ivanhoe Mines’ Oyu Tolgoi Project and the Entree-Ivanhoe Project Property, certain risk factors associated with Ivanhoe Mines are also applicable to the Company and may adversely affect the Company, including:

Ivanhoe Mines and Rio Tinto may be unsuccessful in completing an Investment Agreement with the Government of Mongolia for the Oyu Tolgoi Project or may only be able to complete the contract on terms that effectively impair the economic viability of the Oyu Tolgoi Project.

The Mongolian Parliament has been negotiating with Ivanhoe Mines for five years with regard to the Investment Agreement. The Investment Agreement is structured to stabilize tax and fiscal issues and guide the planned development and long-term operation of the Oyu Tolgoi Project. There was a general election in June 2008, that resulted in the return of the MPRP to a majority government. After a period of political unrest in the country, punctuated by a riot which resulted in the death of five people, the government was formed and new cabinet ministers appointed. A Working Group was appointed to finalize negotiations with Ivanhoe Mines regarding the Investment Agreement. The Working Group forwarded their recommendation to the National Security Council, which then sent the agreement to Parliament on March 09, 2009. Parliament recessed on March 13, 2009, but gave assurances to Ivanhoe Mines that the Investment Agreement would be given priority in the next session, scheduled to begin in early April 2009.

Ivanhoe Mines and Rio Tinto have been meeting with Members of Parliament to discuss issues relating to the planned development of Oyu Tolgoi and lawmakers have visited the Oyu Tolgoi Project site to see work in progress. Ivanhoe Mines and Rio Tinto also have expressed their concerns to Members of Parliament, the Government’s Cabinet and the President about potential adverse impacts on the cost and timing for the Oyu Tolgoi Project that would result from any further unexpected delays in the parliamentary approval process.

The draft agreement, once approved by Parliament, remains subject to approvals by the Ivanhoe Mines and Rio Tinto boards of directors.

An Investment Agreement addresses a broad range of matters relevant to Ivanhoe Mines’ Oyu Tolgoi Project, and the nature and scope of the Investment Agreement is of fundamental importance to the viability of the Oyu Tolgoi Project. Parliament may refuse to approve a draft Investment Agreement, may delay such approval, or may make its approval conditional upon substantive changes being made to the draft which may severely impact the economic viability of the Oyu Tolgoi Project or effectively prevent Ivanhoe Mines from coming to an agreement with the Government on the Investment Agreement. Any such result would have a significant adverse effect on the development of the Oyu Tolgoi Project and Ivanhoe Mines itself, and, would adversely affect the Company.

The Hugo Dummett Deposit mineral resources do not have demonstrated economic viability and the feasibility of mining has not been established.

A substantial portion of the mineral resources identified to date on the Oyu Tolgoi Project are not mineral reserves and do not yet have demonstrated economic viability. There can be no assurance that some or all of these resources will be upgraded to mineral reserves. With the exception of the Southern Oyu Deposits, the feasibility of mining from the Oyu Tolgoi Project has not been, and may never be, established. There is a degree of uncertainty attributable to the estimation of reserves, resources and corresponding grades being mined or dedicated to future production. Until reserves or resources are actually mined and processed, the quantity of reserves or resources and grades must be considered as estimates only. In addition, the quantity of reserves or resources may vary depending on the prevailing metals market. Any material change in the quantity of its reserves, resources, grades or stripping ratio may affect the economic viability of a particular property. In addition, there can be no assurance that metal recoveries in small-scale laboratory tests will be duplicated in larger scale tests under on-site conditions or during production.

The actual cost of developing the Oyu Tolgoi Project may differ significantly from Ivanhoe Mines’ estimates and involve unexpected problems or delays.

The estimates regarding the development and operation of the Oyu Tolgoi Project are based on Ivanhoe Mines’ Integrated Development Plan (“IDP”). This study establishes estimates of reserves and resources and operating costs and projects economic returns. These estimates are based, in part, on assumptions about future metal prices. The IDP derives estimates of average cash operating costs based upon, among other things: anticipated tonnage, grades and metallurgical characteristics of ore to be mined and processed; anticipated recovery rates of copper and gold from the ore; cash operating costs of comparable facilities and equipment; and anticipated climatic conditions. Actual operating costs, production and economic returns may differ significantly from those anticipated by the IDP and future development reports. There are also a number of uncertainties inherent in the development and construction of any new mine including the Oyu Tolgoi Project. These uncertainties include: the timing and cost, which can be considerable, of the construction of mining and processing facilities; the availability and cost of skilled labour, power, water and transportation; the availability and cost of appropriate smelting and refining arrangements; the need to obtain necessary environmental and other government permits, and the timing of those permits; and the availability of funds to finance construction and development activities. The cost, timing and complexities of mine construction and development are increased by the remote location of a property such as the Oyu Tolgoi Project. It is common in new mining operations to experience unexpected problems and delays during development, construction and mine start-up. In addition, delays in the commencement of mineral production often occur. Accordingly, there is no assurance that Ivanhoe Mines’ future development activities will result in profitable mining operations.

Lack of infrastructure in proximity to the material properties could adversely affect mining feasibility.

The Oyu Tolgoi Project is located in an extremely remote area, which currently lacks basic infrastructure, including sources of electric power, water, housing, food and transport, necessary to develop and operate a major mining project. While Ivanhoe Mines has established the limited infrastructure necessary to conduct its current exploration and development activities, substantially greater sources of power, water, physical plant and transport infrastructure in the area will need to be established before Ivanhoe Mines can conduct mining operations. Lack of availability of the means and inputs necessary to establish such infrastructure may adversely affect mining feasibility. Establishing such infrastructure will, in any event, require significant financing, identification of adequate sources of raw materials and supplies and necessary approvals from national and regional governments, none of which can be assured.

Risks Associated With Mining

All of our properties are in the exploration stage. There is no assurance that we can establish the existence of any mineral resource on any of our properties in commercially exploitable quantities. Until we can do so, we cannot earn any revenues from operations and if we do not do so we will lose all of the funds that we expend on exploration. If we do not discover any mineral resource in a commercially exploitable quantity, our business will fail.

Despite exploration work on our mineral properties, we have not established that any of them contain any mineral reserve, nor can there be any assurance that we will be able to do so. If we do not, our business will fail.

A mineral reserve is defined by the Securities and Exchange Commission in its Industry Guide 7 (which can be viewed over the Internet at http://www.sec.gov/divisions/corpfin/forms/industry.htm#secguide7) as that part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. The probability of an individual prospect ever having a "reserve" that meets the requirements of the Securities and Exchange Commission's Industry Guide 7 is extremely remote; in all probability our mineral resource property does not contain any 'reserve' and any funds that we spend on exploration will probably be lost.

Even if we do eventually discover a mineral reserve on one or more of our properties, there can be no assurance that we will be able to develop our properties into producing mines and extract those resources. Both mineral exploration and development involve a high degree of risk and few properties which are explored are ultimately developed into producing mines.

The commercial viability of an established mineral deposit will depend on a number of factors including, by way of example, the size, grade and other attributes of the mineral deposit, the proximity of the resource to infrastructure such as a smelter, roads and a point for shipping, government regulation and market prices. Most of these factors will be beyond our control, and any of them could increase costs and make extraction of any identified mineral resource unprofitable.

Our four exploration licences in Mongolia expire in March and April 2010.

All of our exploration licenses in Mongolia currently expire in March or April 2010. Exploration license holders are entitled to apply for conversion to a mining license before their exploration license has expired. In order to be granted a mining licence the holder must demonstrate, among other things, that the subject property contains reserves and resources. The Company has not yet demonstrated reserves and resources on all of its Mongolian exploration licences.

Mineral operations are subject to applicable law and government regulation. Even if we discover a mineral resource in a commercially exploitable quantity, these laws and regulations could restrict or prohibit the exploitation of that mineral resource. If we cannot exploit any mineral resource that we might discover on our properties, our business may fail.

Both mineral exploration and extraction require permits from various foreign, federal, state, provincial and local governmental authorities and are governed by laws and regulations, including those with respect to prospecting, mine development, mineral production, transport, export, taxation, labour standards, water right, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters. There can be no assurance that we will be able to obtain or maintain any of the permits required for the continued exploration of our mineral properties or for the construction and operation of a mine on our properties at economically viable costs. If we cannot accomplish these objectives, our business could fail.

We believe that we are in compliance with all material laws and regulations that currently apply to our activities but there can be no assurance that we can continue to do so. Current laws and regulations could be amended and we might not be able to comply with them, as amended. Further, there can be no assurance that we will be able to obtain or maintain all permits necessary for our future operations, or that we will be able to obtain them on reasonable terms. To the extent such approvals are required and are not obtained, we may be delayed or prohibited from proceeding with planned exploration or development of our mineral properties.

Environmental hazards unknown to us which have been caused by previous or existing owners or operators of the properties may exist on the properties in which we hold an interest. More specifically, we are required to deposit 50% of our proposed reclamation budget with the local Soum Governors office which will be refunded only on acceptable completion of land rehabilitation after mining operations have concluded. Even if we relinquish our licenses, we will still remain responsible for any required reclamation.

If we establish the existence of a mineral resource on any of our properties in a commercially exploitable quantity, we will require additional capital in order to develop the property into a producing mine. If we cannot raise this additional capital, we will not be able to exploit the resource, and our business could fail.

If we do discover mineral resources in commercially exploitable quantities on any of our properties, we will be required to expend substantial sums of money to establish the extent of the resource, develop processes to extract it and develop extraction and processing facilities and infrastructure. Although we may derive substantial benefits from the discovery of a major deposit, there can be no assurance that such a resource will be large enough to justify commercial operations, nor can there be any assurance that we will be able to raise the funds required for development on a timely basis. If we cannot raise the necessary capital or complete the necessary facilities and infrastructure, our business may fail.

Mineral exploration and development is subject to extraordinary operating risks. We do not currently insure against these risks. In the event of a cave-in or similar occurrence, our liability may exceed our resources, which would have an adverse impact on our company.

Mineral exploration, development and production involves many risks which even a combination of experience, knowledge and careful evaluation may not be able to overcome. Our operations will be subject to all the hazards and risks inherent in the exploration, development and production of resources, including liability for pollution, cave-ins or similar hazards against which we cannot insure or against which we may elect not to insure. Any such event could result in work stoppages and damage to property, including damage to the environment. We do not currently maintain any insurance coverage against these operating hazards. The payment of any liabilities that arise from any such occurrence would have a material, adverse impact on our Company.

Climatic Conditions can affect operations

Mongolia's weather varies to the extremes, with summer temperatures ranging up to 35° Celsius or more to winter lows of minus 31° Celsius. Such adverse conditions often preclude normal work patterns and can severely limit exploration and mining operations, usually making work impossible from November through to March. Although good project planning can ameliorate these factors, unseasonable weather can upset programs with resultant additional costs and delays.

Mineral prices are subject to dramatic and unpredictable fluctuations.

We expect to derive revenues, if any, from the extraction and sale of precious and base metals such as gold, silver, molybdenum, and copper. The price of those commodities has fluctuated widely in recent years, and is affected by numerous factors beyond our control including international economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates, global or regional consumptive patterns, speculative activities and increased production due to new extraction developments and improved extraction and production methods. Mongolian law requires the sale or export of gold mined in Mongolia to be made through the Central Bank of Mongolia and/or other authorized entities at world market prices. The effect of these factors on the price of base and precious metals, and, therefore, the economic viability of any of our exploration projects, cannot accurately be predicted.

The mining industry is highly competitive and there is no assurance that we will continue to be successful in acquiring mineral claims. If we cannot continue to acquire properties to explore for mineral resources, we may be required to reduce or cease operations.

The mineral exploration, development, and production industry is largely unintegrated. We compete with other exploration companies looking for mineral resource properties and the resources that can be produced from them. While we compete with other exploration companies in the effort to locate and license mineral resource properties, we do not compete with them for the removal or sales of mineral products from our properties if we should eventually discover the presence of them in quantities sufficient to make production economically feasible. Readily available markets exist worldwide for the sale of gold and other mineral products. Therefore, we will likely be able to sell any gold or mineral products that we identify and produce.

We compete with many companies possessing greater financial resources and technical facilities. This competition could adversely affect our ability to acquire suitable prospects for exploration in the future. Accordingly, there can be no assurance that we will acquire any interest in additional mineral resource properties that might yield reserves or result in commercial mining operations.

Our title to our resource properties may be challenged by third parties or the licenses that permit us to explore our properties may expire if we fail to timely renew them and pay the required fees.

We have investigated the status of our title to the four exploration licenses granting us the right to explore the Togoot (License 3136X), Shivee Tolgoi (License 3148X), Javhlant (License No. 3150X), and Manlai (License No. 3045X) mineral resource properties and we are satisfied that the title to these four licenses is properly registered in the name of our Mongolian subsidiary, Entrée LLC and that these licenses are currently in good standing.

We cannot guarantee that the rights to explore our properties will not be revoked or altered to our detriment. The ownership and validity of mining claims and concessions are often uncertain and may be contested. Should such a challenge to the boundaries or registration of ownership arise, the Government of Mongolia may declare the property in question a special reserve for up to three years to allow resolution of disputes or to clarify the accuracy of our mining license register. We are not aware of challenges to the location or area of any of the mining concessions and mining claims. There is, however, no guarantee that title to the claims and concessions will not be challenged or impugned in the future. Further, all of our licenses are exploration licenses, which were issued initially for a three-year term with a right of renewal for three more years, and a further right of renewal for three years, making a total of nine years. The total estimated annual fees in order to maintain the licenses in good standing is approximately $280,000. If we fail to pay the appropriate annual fees or if we fail to timely apply for renewal, then these licenses may expire or be forfeit.

Development of the Entree-Ivanhoe Project Property may be delayed by Ivanhoe Mines in favour of development of the Oyu Tolgoi Property.

Ivanhoe Mines has earned between a 70 and 80% interest in the Entree-Ivanhoe Project Property. Ivanhoe Mines has effective control of the development of both the Oyu Tolgoi Property, which it owns outright, and the Entree-Ivanhoe Project Property, in which the Company will maintain an interest. The development of the Entree-Ivanhoe Project Property may be adversely affected if Ivanhoe Mines decides to delay or reduce such development in favour of the immediate or complete development of the Oyu Tolgoi Property.

The Company’s ability to carry on business in Mongolia is subject to political and economic risk.

The Company holds its interest in its Mongolian exploration properties through exploration licences that enable it to conduct operations or development and exploration activities. Notwithstanding these arrangements, the Company’s ability to conduct operations or exploration and development activities is subject to changes in legislation or government regulations or shifts in political attitudes beyond the Company’s control. Government policy may change to discourage foreign investment, nationalization of mining industries may occur or other government limitations, restrictions or requirements not currently foreseen may be implemented. There can be no assurance that the Company’s assets will not be subject to nationalization, requisition or confiscation, whether legitimate or not, by any authority or body. There is no assurance that provisions under Mongolian law for compensation and reimbursement of losses to investors under such circumstances would be effective to restore the value of the Company’s original investment. Similarly, the Company’s operations may be affected in varying degrees by government regulations with respect to restrictions on production, price controls, export controls, income taxes, environmental legislation, mine safety and annual fees to maintain mineral licences in good standing. There can be no assurance that Mongolian laws protecting foreign investments will not be amended or abolished or that existing laws will be enforced or interpreted to provide adequate protection against any or all of the risks described above.

The Company’s business in Mongolia may be harmed if the country fails to complete its transition from state socialism and a planned economy to political democracy and a free market economy.

Since 1990, Mongolia has been in transition from state socialism and a planned economy to a political democracy and a free market economy. Much progress has been made in this transition but much remains to be done, particularly with respect to the rule of law. Many laws have been enacted, but in many instances they are neither understood nor enforced. For decades Mongolians have looked to politicians and bureaucrats as the sources of the “law”. This has changed in theory, but often not in practice. With respect to most day-to-day activities in Mongolia government civil servants interpret, and often effectively make, the law. This situation is gradually changing but at a relatively slow pace. Laws may be applied in an inconsistent, arbitrary and unfair manner and legal remedies may be uncertain, delayed or unavailable.

Recent and future amendments to Mongolian laws could adversely affect the Company’s mining rights or make it more difficult or expensive to develop the project and carry out mining.

In 2006, Mongolia implemented revisions to the Minerals Law. These revisions continue to preserve the substance of the original Minerals Law, which was drafted with the assistance of Western legal experts and is widely regarded as progressive, internally consistent and effective legislation, but the revisions have also increased the potential for political interference and weakened the rights of mineral holders in Mongolia. A number of the provisions will require further clarification from the Government about the manner in which the Government intends to interpret and apply the relevant law, which could have a significant effect on the Company’s Mongolian properties. The Mongolian government has, in the past, expressed its strong desire to foster, and has to date protected the development of, an enabling environment for foreign investment. However, there are political constituencies within Mongolia that have espoused ideas that would not be regarded by the international mining industry as conducive to foreign investment if they were to become law or official government policy. The Oyu Tolgoi Project (and with it the Hugo North Extension and the Heruga deposit on the Entree-Ivanhoe Mines Joint Venture) has a high profile among the citizens of Mongolia and, as a burgeoning democracy, Mongolia has recently demonstrated a degree of political volatility. Accordingly, until these issues are addressed and clarified, there can be no assurance that the present government or a future government will refrain from enacting legislation or adopting government policies that are adverse to the interest of Ivanhoe Mines or the Company or that impair Ivanhoe Mines’ ability to develop and operate the Oyu Tolgoi Project on the basis presently contemplated.

The Company may be unable to enforce its legal rights in certain circumstances.

In the event of a dispute arising at or in respect of, the Company’s foreign operations, the Company may be subject to the exclusive jurisdiction of foreign courts or may not be successful in subjecting foreign persons to the jurisdiction of courts in Canada or other jurisdictions. The Company may also be hindered or prevented from enforcing its rights with respect to a governmental entity or instrumentality because of the doctrine of sovereign immunity.

The Company may experience difficulties with its joint venture partners.

Ivanhoe Mines has earned an interest in the Entree-Ivanhoe Project Property from the Company. Ivanhoe Mines and the Company have formed a joint venture and the Company may in the future enter into additional joint ventures in respect of other properties with third parties. The Company is subject to the risks normally associated with the conduct of joint ventures, which include disagreements as to how to develop, operate and finance a project and possible litigation between the participants regarding joint venture matters. These matters may have an adverse effect on the Company’s ability to realize the full economic benefit of its interest in the property that is the subject of the joint venture, which could affect its results of operations and financial condition.

Risks Related To Our Company

We have a limited operating history on which to base an evaluation of our business and prospects.

Although we have been in the business of exploring mineral resource properties since 1995, we have not yet located any mineral reserves. As a result, we have never had any revenues from our operations. In addition, our operating history has been restricted to the acquisition and exploration of our mineral properties and this does not provide a meaningful basis for an evaluation of our prospects if we ever determine that we have a mineral reserve and commence the construction and operation of a mine. We have no way to evaluate the likelihood of whether our mineral properties contain any mineral reserve or, if they do that we will be able to build or operate a mine successfully. We anticipate that we will continue to incur operating costs without realizing any revenues during the period when we are exploring our properties. During the twelve months ending December 31, 2009, we expect to spend approximately $12 million on the maintenance and exploration of our mineral properties and the operation of our company. We therefore expect to continue to incur significant losses into the foreseeable future. We recognize that if we are unable to generate significant revenues from mining operations and any dispositions of our properties, we will not be able to earn profits or continue operations. At this early stage of our operation, we also expect to face the risks, uncertainties, expenses and difficulties frequently encountered by companies at the start up stage of their business development. We cannot be sure that we will be successful in addressing these risks and uncertainties and our failure to do so could have a materially adverse effect on our financial condition. There is no history upon which to base any assumption as to the likelihood that we will prove successful and we can provide investors with no assurance that we will generate any operating revenues or ever achieve profitable operations.

The fact that we have not earned any operating revenues since our incorporation raises substantial doubt about our ability to continue to explore our mineral properties as a going concern.