Table of Contents

As filed with the Securities and Exchange on July 5, 2005

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F/A

Amendment No. 1

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(B) OR (G) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2004

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-32305

CORPBANCA

(Exact name of Registrant as specified in its charter)

Republic of Chile

(Jurisdiction of incorporation or organization)

Huérfanos 1072

Santiago, Chile

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

TITLE OF EACH CLASS | NAME OF EACH EXCHANGE ON WHICH REGISTERED | |

| American Depositary Shares representing Common Stock | New York Stock Exchange | |

| Common Stock, no par value* | New York Stock Exchange* |

| * | Not for trading purposes, but only in connection with the registration of American Depositary Shares pursuant to the requirements of the Securities and Exchange Commission. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None.

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Shares of Common Stock: 226,909,290,577

Indicate by check mark whether the registrant (1) has filed all required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such report(s), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ¨ Item 18 x

Table of Contents

EXPLANATORY NOTE

Corpbanca hereby amends and restates in its entirety our Annual Report on Form 20-F filed on July 1, 2005 for our fiscal year ended December 30, 2004 as set forth in this Amendment No. 1 to Form 20-F/A. This amended Annual Report on Form 20-F/A includes the following exhibits, which were available for inclusion in the Annual Report on Form 20-F and were intended to be included as part of the original filing, but were inadvertently omitted from our Annual Report on Form 20-F as filed on July 1, 2005 because of technical problems that were beyond our control:

| · | Exhibit 12.1. Certification of the principal executive officer of Corpbanca required under Rule 13a-14(a) or Rule 15d-14(a), pursuant to Section 302 of the Sarbanes Oxley Act of 2002. |

| · | Exhibit 12.2. Certification of the principal financial officer of Corpbanca required under Rule 13a-14(a) or Rule 15d-14(a), pursuant to Section 302 of the Sarbanes Oxley Act of 2002. |

| · | Exhibit 13.1. Certification of the principal executive officer of Corpbanca, pursuant to 18 U.S.C. § 1350, as adopted pursuant to § 906 of the Sarbanes Oxley Act of 2002. |

| · | Exhibit 13.2. Certification of the principal financial officer of Corpbanca, pursuant to 18 U.S.C. § 1350, as adopted pursuant to § 906 of the Sarbanes Oxley Act of 2002. |

Table of Contents

CAUTIONARY LANGUAGE REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains statements that constitute forward-looking statements. These statements appear throughout this annual report, including, without limitation, under “Item 3. Key Information—Risk Factors,” “Item 4. Information on the Company” and “Item 5. Operating and Financial Review and Prospects” and include statements regarding our current intent, belief or expectations with respect to (1) our asset growth and financing plans, (2) trends affecting our financial condition or results of operations, (3) the impact of competition and regulations, (4) projected capital expenditures and (5) liquidity. Such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and actual results may differ materially from those described in such forward-looking statements included in this annual report as a result of various factors (including, without limitation, the actions of competitors, future global economic conditions, market conditions, foreign exchange rates and operating and financial risks), many of which are beyond our control. The occurrence of any such factors not currently expected by us would significantly alter the results set forth in these statements.

Factors that could cause actual results to differ materially and adversely include, but are not limited to:

| • | changes in general economic, business or political or other conditions in Chile or changes in general economic or business conditions in Latin America, |

| • | changes in capital markets in general that may affect policies or attitudes towards lending to Chile or Chilean companies or securities issued by Chilean companies, |

| • | the monetary and interest rate policies of theBanco Central de Chile (the Central Bank of Chile), or the Central Bank, |

| • | inflation, |

| • | deflation, |

| • | unemployment, |

| • | unanticipated increases in financing and other costs or the inability to obtain additional debt or equity financing on attractive terms, |

| • | unanticipated turbulence in interest rates, |

| • | movements in foreign exchange rates, |

| • | movements in equity prices or other rates or prices, |

| • | changes in Chilean and foreign laws and regulations, |

| • | changes in taxes, |

| • | competition, changes in competition and pricing environments, |

| • | our inability to hedge certain risks economically, |

| • | the adequacy of loss allowances or provisions, |

| • | technological changes, |

| • | changes in consumer spending and saving habits, |

| • | successful implementation of new technologies, |

| • | loss of market share, |

| • | changes in, or failure to comply with banking regulations, and |

| • | the factors discussed under “Item 3. Key Information—Risk Factors” in this annual report. |

You should not place undue reliance on such statements, which speak only as of the date that they were made. These cautionary statements should be considered in connection with any written or oral forward-looking statements that we may issue in the future. We do not undertake any obligation to release publicly any revisions to such forward-looking statements after the date of this annual report to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

-2-

Table of Contents

ENFORCEABILITY OF CIVIL LIABILITIES

We are asociedad anónima (corporation) organized under the laws of the Republic of Chile. None of our directors or executive officers are residents of the United States and a substantial portion of our assets and these individuals are located outside the United States. As a result, it may be difficult for you to effect service of process within the United States upon such persons or to enforce against them or us in the United States courts, judgment obtained in the United States predicated upon the civil liability provisions of the federal securities laws of the United States.

No treaty exists between the United States and Chile for the reciprocal enforcement of judgments. Chilean courts, however, have enforced final judgments rendered in the United States by virtue of the legal principles of reciprocity and comity, subject to the review in Chile of the United States judgment in order to ascertain whether certain basic principles of due process and public policy have been respected without reviewing the merits of the subject matter of the case. If a U.S. court grants a final judgment in an action based on the civil liability provisions of the federal securities laws of the United States, enforceability of this judgment in Chile will be subject to the obtaining of the relevant“exequatur” (i.e. recognition and enforcement of the foreign judgment) according to Chilean civil procedure law in force at that time, and consequently, subject to the satisfaction of certain factors. Currently, the most important of these factors are the existence of reciprocity, the absence of a conflicting judgment by a Chilean court relating to the same parties and arising from the same facts and circumstances, the Chilean courts’ determination that the U.S. courts had jurisdiction, that process was appropriately serviced on the defendant and that the defendant was afforded a real opportunity to appear before the court and defend its case; and that enforcement would not violate Chilean public policy.

If an action is started before Chilean courts, there is doubt as to the enforceability of liabilities based on the U.S. federal securities laws and as to the enforceability in Chilean courts of judgments of United States courts obtained in actions based upon civil liability provisions of the federal securities laws of the United States.

-3-

Table of Contents

-4-

Table of Contents

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

We prepare our consolidated financial statements in Chilean pesos and in conformity with generally accepted accounting principles in Chile, or Chilean GAAP, and the relevant rules of the ChileanSuperintendencia de Bancos e Instituciones Financieras, or the Chilean Superintendency of Banks, which together differ in certain respects from accounting principles generally accepted in the United States, or U.S. GAAP. References to Chilean GAAP in this annual report are to Chilean GAAP, as supplemented by the applicable rules of the Chilean Superintendency of Banks. See note 27 to our audited consolidated financial statements included herein for a description of the principal differences between Chilean GAAP and U.S. GAAP, as they relate to us and our consolidated subsidiaries, and a reconciliation to U.S. GAAP of net income and shareholders’ equity as of and for each of the two years ended December 31, 2004.

Our audited consolidated financial statements as of December 31, 2004 and 2003 and for each of the three years ended December 31, 2004 are referred to herein as our financial statements. Pursuant to Chilean GAAP, unless otherwise indicated, financial data as of December 31, 2004, 2003, 2002, 2001 and 2000 and for each of the five years in the period ended December 31, 2004 included in our financial statements and elsewhere throughout this annual report have been expressed in constant pesos as of December 31, 2004.

In this annual report, references to “$,” “U.S.$,” “U.S. dollars” and “dollars” are to United States dollars, references to “pesos” or “Ch$” are to Chilean pesos, and references to “UF” are toUnidades de Fomento. The UF is an inflation-indexed, peso-denominated unit that is linked to, and adjusted daily to reflect changes in, the previous month’s Chilean consumer price index. As of June 15, 2005, UF1.00 was equivalent to U.S.$29.63 and Ch$17,463.08. See “Item 5. Operating and Financial Review and Prospects.”

Unless otherwise specified, all references in this annual report (except in our financial statements) to loans are to loans, contingent loans and financial leases before deduction for allowances for loan losses, and, except as otherwise specified, all market share data presented herein are based on information published periodically by the Chilean Superintendency of Banks on an unconsolidated basis. Non-performing loans that are not yet 90 days or more overdue have been included in each of the various categories of loans, and therefore affect the various averages. Non-performing loans consist of commercial loans included in Categories C4, D1 and D2 and loans (or portions thereof) that are overdue. We cease to accrue interest on loans as soon as they become overdue. For a description of the loan categories applicable to our business, see “Item 4. Information on the Company—Selected Statistical Information—Analysis of Our Loan Classification.” Past due loans include, with respect to any loan, the portion of principal or interest that is 90 or more days overdue, and do not include the portion of such loan that is not overdue or that is less than 90 days overdue, unless legal proceedings have been commenced for the entire outstanding balance according to the terms of the loan. This practice differs from that normally followed in the United States where the amount classified as past due would include the total principal and interest on all loans which have any portion overdue. See “Item 4. Information on the Company—Selected Statistical Information—Classification of Loan Portfolio Based on Borrower’s Payment Performance.” For a description of our major types of loans, as well as tables showing their maturities, see “Item 4. Information on the Company—Selected Statistical Information—Loan Portfolio” and “Item 4. Information on the Company—Selected Statistical Information —Maturity and Interest Rate Sensitivity.”

Unless otherwise specified, all references to “shareholders’ equity” as of December 31 of any year are to shareholders’ equity as stated in our financial statements, excluding dividends paid, if any, in respect of the year then ended, such dividends having been paid in the following year.

-5-

Table of Contents

Certain figures included in this annual report and in our financial statements have been rounded for ease of presentation. Percentage figures included in this annual report have not in all cases been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this annual report may vary from those obtained by performing the same calculations using the figures in our financial statements. Certain other amounts that appear in this annual report may not sum due to rounding.

This annual report contains translations of certain peso amounts into U.S. dollars at specified rates solely for the convenience of the reader. These translations should not be construed as representations that the peso amounts actually represent such U.S. dollar amounts, were converted from U.S. dollars at the rate indicated in preparing our financial statements or could be converted into U.S. dollars at the rate indicated. Unless otherwise indicated, U.S. dollar amounts as of December 31, 2000, 2001, 2002, 2003 and 2004 and for each of the five years in the period ended December 31, 2004 have been translated from pesos based on thedólar observado, or observed exchange rate, of Ch$559.83 per U.S.$1.00 as reported by theBanco Central de Chile (the Central Bank of Chile, or the Central Bank) as of December 31, 2004. The observed exchange rate reported by the Central Bank is based on the average rate for the prior business day in Chile and is the exchange rate specified by the Chilean Superintendency of Banks for use by Chilean banks in the preparation of their financial statements. The Federal Reserve Bank of New York does not report a noon buying rate for pesos. See “—Exchange Rate Information” below.

In this annual report, all macro-economic data related to the Chilean economy is based on information published by the Central Bank, and all market share and other data related to the Chilean financial system is based on information published by the Chilean Superintendency of Banks as well as other publicly available information. Information regarding the consolidated risk index of the Chilean financial system as a whole is not available. The Chilean Superintendency of Banks publishes the unconsolidated risk index for the financial system three times yearly in February, June and October.

EXCHANGE RATE INFORMATION

Chile has two currency markets, the Formal Exchange Market and theMercado Cambiario Informal, or the Informal Exchange Market. The Central Bank is empowered to determine that certain purchases and sales of foreign currencies must be carried out in the Formal Exchange Market. Pursuant to Central Bank regulations which are currently in effect, all payments, remittances or transfers of foreign currency abroad which are required to be effected through the Formal Exchange Market may be effected with foreign currency procured outside the Formal Exchange Market. The Formal Exchange Market is comprised of the banks and other entities so authorized by the Central Bank. Current regulations require that the Central Bank be informed of certain transactions and that they be effected through the Formal Exchange Market.

The reference exchange rate for the Formal Exchange Market is reset daily by the Central Bank, taking internal and external inflation into account, and is adjusted daily to reflect variations in parities between the peso and each of the U.S. dollar, the Euro and the Japanese yen. The observed exchange rate for a given date is the average exchange rate of the transactions conducted in the Formal Exchange Market on the immediately preceding banking day, as certified by the Central Bank.

Prior to September 2, 1999, authorized transactions by banks were generally transacted within a certain band above or below the reference exchange rate. In order to maintain the average exchange rate within such limits, the Central Bank intervened by selling and buying foreign currencies on the Formal Exchange Market. On September 2, 1999, the Central Bank eliminated the exchange rate band as an instrument of exchange rate policy, introducing more flexibility to the exchange market. The Central Bank announced that it will intervene in the exchange market only in special and qualified cases.

Purchases and sales of foreign currencies which may be effected outside the Formal Exchange Market can be carried out in the Informal Exchange Market. The Informal Exchange Market reflects transactions carried out at informal exchange rates by entities not expressly authorized to operate in the Formal Exchange Market, such as certain foreign exchange houses and travel agencies. There are no limits imposed on the extent to which the rate of exchange in the Informal Exchange Market can fluctuate above or below the observed exchange rate. On December 31, 2004, the average exchange rate in the Informal Exchange Market was approximately the same as the published observed exchange rate for such date of Ch$559.83 per U.S.$1.00.

-6-

Table of Contents

The following table sets forth the annual low, high, average and period-end observed exchange rate for U.S. dollars for the periods set forth below, as reported by the Central Bank.

| Daily Observed Exchange Rate Ch$ per U.S.$(1) | ||||||||||||

Year | Low(2) | High(2) | Average(3) | Period End | ||||||||

2000 | C | h$501.04 | C | h$580.37 | C | h$539.49 | C | h$572.68 | ||||

2001 | 557.13 | 716.62 | 634.94 | 656.20 | ||||||||

2002 | 641.75 | 756.56 | 688.94 | 712.38 | ||||||||

2003 | 593.10 | 758.21 | 691.40 | 599.42 | ||||||||

2004 | 559.21 | 649.45 | 609.53 | 559.83 | ||||||||

December 2004 | 559.66 | 597.27 | 576.17 | 559.83 | ||||||||

January 2005 | 557.40 | 586.18 | 574.12 | 586.18 | ||||||||

February 2005 | 563.22 | 585.40 | 573.58 | 577.52 | ||||||||

March 2005 | 573.55 | 591.69 | 586.48 | 586.45 | ||||||||

April 2005 | 572.75 | 588.95 | 580.46 | 582.87 | ||||||||

May 2005 | 570.83 | 583.59 | 578.31 | 580.20 | ||||||||

June 2005 (4) | 583.00 | 592.75 | 589.36 | 589.38 | ||||||||

| (1) | Nominal figures. |

| (2) | Exchange rates are the actual low and high, on a day-by-day basis for each period. |

| (3) | The average of monthly average rates during the year. |

| (4) | Through June 15, 2005. |

The observed exchange rate for June 15, 2005 was Ch$589.38 = U.S.$1.00.

A. SELECTED FINANCIAL DATA

The following tables present our selected consolidated financial and operating information as of the dates and for the periods indicated. You should read the following information together with the financial statements, including the notes thereto, included in this annual report and the information set forth in “Item 5. Operating and Financial Review and Prospects.”

The selected consolidated income statement and balance sheet data as of and for the years ended December 31, 2004, 2003, 2002, 2001 and 2000 appearing herein have been derived from our consolidated financial statements which have been audited by Deloitte & Touche Sociedad de Auditores y Consultores Ltda., or Deloitte.

-7-

Table of Contents

Our audited consolidated income statements for the years ended December 31, 2004, 2003 and 2002, and our audited consolidated balance sheets as of December 31, 2004 and 2003, which we refer to as our financial statements, and the reports of Deloitte thereon, appear elsewhere in this annual report. The selected consolidated income statement data for the years ended December 31, 2001 and 2000, and the selected consolidated balance sheet data as of December 31, 2002, 2001 and 2000 have been derived from financial statements which have been audited by Deloitte and which do not appear elsewhere in this annual report.

Our financial statements have been prepared in accordance with Chilean GAAP (including the rules of the Chilean Superintendency of Banks), which differs in certain significant respects from U.S. GAAP. See note 27 to our financial statements for a description of the principal differences between Chilean GAAP and U.S. GAAP as they relate to us, and a reconciliation to U.S. GAAP of net income and shareholders’ equity.

Unless otherwise indicated, U.S. dollar amounts as of December 31, 2004, 2003, 2002, 2001 and 2000 and for each of the five years ended December 31, 2004 have been translated from pesos based on thedólar observado, or observed exchange rate, of Ch$559.83 per U.S.$1.00 as reported by the Central Bank on December 31, 2004. The rate reported by the Central Bank is based on the average rate for the prior business day in Chile and is the exchange rate specified by the Chilean Superintendency of Banks for use by Chilean banks in the preparation of their financial statements. The Federal Reserve Bank of New York does not report a noon buying rate for pesos.

U.S. GAAP data for 2000 and 2001 does not appear in the following table or elsewhere in this annual report because we have not previously prepared such data for periods prior to 2002.

| As of and for the Year Ended December 31, | ||||||||||||||||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | |||||||||||||||||||

| (in millions of constant Ch$ as of December 31, 2004)(1) | (in thousands of U.S.$)(1)(2) | |||||||||||||||||||||||

CONSOLIDATED INCOME STATEMENT DATA | ||||||||||||||||||||||||

Chilean GAAP | ||||||||||||||||||||||||

Net interest revenue | Ch $ | 90,823 | Ch$ | 97,060 | Ch$ | 102,310 | Ch$ | 97,991 | Ch$ | 111,926 | Ch$ | 199,929 | ||||||||||||

Provisions for loan losses | (20,345 | ) | (21,937 | ) | (23,739 | ) | (26,179 | ) | (18,119 | ) | (32,365 | ) | ||||||||||||

Fees and income from services (net) | 16,979 | 17,545 | 20,372 | 22,535 | 18,854 | 33,678 | ||||||||||||||||||

Other operating income (net) | 2,865 | 7,092 | 10,797 | 19,149 | 6,673 | 11,920 | ||||||||||||||||||

Other income and expenses (net) | (7,097 | ) | (7,016 | ) | (18,895 | ) | (1,675 | ) | (1,764 | ) | (3,151 | ) | ||||||||||||

Operating expenses | (69,974 | ) | (61,342 | ) | (54,645 | ) | (56,023 | ) | (53,838 | ) | (96,169 | ) | ||||||||||||

Net loss from price-level restatement | (695 | ) | (1,766 | ) | (2,092 | ) | (2,294 | ) | (6,453 | ) | (11,527 | ) | ||||||||||||

Income before income taxes | 12,556 | 29,636 | 34,108 | 53,504 | 57,279 | 102,315 | ||||||||||||||||||

Income tax (expense) benefit | 1,520 | 497 | 1,543 | (2,127 | ) | (6,512 | ) | (11,632 | ) | |||||||||||||||

Revenues of voluntary reserves | 2,031 | 160 | 1,146 | — | — | — | ||||||||||||||||||

Net income | Ch$ | 16,107 | Ch$ | 30,293 | Ch$ | 36,797 | Ch$ | 51,377 | Ch$ | 50,767 | Ch$ | 90,683 | ||||||||||||

Net income per share of common stock | 0.09 | 0.18 | 0.16 | 0.23 | 0.22 | 0.00039 | ||||||||||||||||||

Dividends per share of common stock(3) | — | — | 0.08 | 0.08 | 0.11 | 0.00020 | ||||||||||||||||||

Dividends per ADS(4) | — | — | 400.00 | 400.00 | 550.00 | 0.98 | ||||||||||||||||||

Shares of common stock outstanding (in thousands) | 170,382,765.6 | 170,449,290.6 | 226,909,290.6 | 226,909,290.6 | 226,909,290.6 | — | ||||||||||||||||||

U.S. GAAP | ||||||||||||||||||||||||

Net interest income(5) | — | — | 100,218 | 95,697 | 105,473 | 188,402 | ||||||||||||||||||

Provisions for loan losses | — | — | (22,593 | ) | (26,179 | ) | (18,119 | ) | (32,365 | ) | ||||||||||||||

Amortization of goodwill | — | — | — | — | — | — | ||||||||||||||||||

Long-term borrowings | — | — | 345,884 | 438,235 | 544,733 | 973,033 | ||||||||||||||||||

Net income | — | — | 50,291 | 56,411 | 58,637 | 104,741 | ||||||||||||||||||

Net income per share of common stock(6) | — | — | 0.28 | 0.25 | 0.26 | 0.0005 | ||||||||||||||||||

Net income per ADS(6) | — | — | 1,400.0 | 1,250.0 | 1,300.0 | 2.3 | ||||||||||||||||||

Weighted average ADS outstanding (in millions) | — | — | 36 | 45 | 45 | — | ||||||||||||||||||

-8-

Table of Contents

| As of and for the Year Ended December 31, | ||||||||||||||||||

| 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | |||||||||||||

| (in millions of constant Ch$ as of December 31, 2004)(1) | (in thousands of U.S.$)(1)(2) | |||||||||||||||||

| CONSOLIDATED BALANCE SHEET DATA | ||||||||||||||||||

| Chilean GAAP | ||||||||||||||||||

Cash and due from banks | 104,212 | 112,155 | 145,614 | 118,158 | 158,602 | 283,304 | ||||||||||||

Investments | 299,633 | 295,250 | 283,967 | 471,812 | 529,409 | 945,660 | ||||||||||||

Total loans | 1,321,980 | 1,539,571 | 1,769,821 | 2,144,926 | 2,443,649 | 4,364,984 | ||||||||||||

Allowances for loan losses | (28,849 | ) | (33,907 | ) | (39,249 | ) | (45,308 | ) | (41,611 | ) | (74,328 | ) | ||||||

Other assets(7) | 140,466 | 149,381 | 144,491 | 166,739 | 111,535 | 199,230 | ||||||||||||

Total assets | 1,837,442 | 2,062,450 | 2,304,644 | 2,856,327 | 3,201,584 | 5,718,850 | ||||||||||||

Deposits | 1,147,423 | 1,253,794 | 1,371,151 | 1,658,633 | 1,872,426 | 3,344,633 | ||||||||||||

Other interest-bearing liabilities | 419,164 | 479,560 | 445,042 | 641,307 | 726,316 | 1,297,386 | ||||||||||||

Shareholders’ equity | 150,589 | 180,872 | 314,453 | 347,496 | 376,396 | 672,340 | ||||||||||||

| U.S. GAAP | ||||||||||||||||||

Total loans | — | — | 1,623,024 | 1,942,392 | 2,246,882 | 4,013,508 | ||||||||||||

Allowances for loan losses | — | — | (39,249 | ) | (45,308 | ) | (41,611 | ) | (74,328 | ) | ||||||||

Total assets | — | — | 2,150,163 | 2,644,665 | 2,994,470 | 5,348,892 | ||||||||||||

Shareholders’ equity | — | — | 288,838 | 315,138 | 344,602 | 615,548 | ||||||||||||

Goodwill | — | — | — | — | — | — | ||||||||||||

| SELECTED CONSOLIDATED RATIOS | ||||||||||||||||||

| Profitability and Performance | ||||||||||||||||||

Net interest margin(8) | 6.3 | % | 5.9 | % | 5.3 | % | 4.1 | % | 4.0 | % | — | |||||||

Return on average total assets(9) | 0.7 | % | 1.2 | % | 1.3 | % | 1.6 | % | 1.5 | % | — | |||||||

Return on average shareholders’ equity(10) | 12.3 | % | 17.6 | % | 18.2 | % | 15.3 | % | 14.0 | % | — | |||||||

Efficiency ratio (consolidated)(11) | 63.2 | % | 50.4 | % | 40.9 | % | 40.1 | % | 39.2 | % | — | |||||||

Dividend payout ratio(12) | — | — | 50.0 | % | 50.0 | % | 50.0 | % | — | |||||||||

| Capital | ||||||||||||||||||

Average shareholders’ equity as a percentage of average total assets | 6.0 | % | 6.8 | % | 7.2 | % | 10.5 | % | 10.5 | % | — | |||||||

Total liabilities as a multiple of shareholders’ equity | 11.2 | 10.4 | 6.3 | 7.2 | 7.5 | — | ||||||||||||

| Asset Quality | ||||||||||||||||||

Allowances for loan losses as a percentage of overdue loans(13) | 83.9 | % | 103.3 | % | 96.9 | % | 105.8 | % | 122.9 | % | — | |||||||

Overdue loans as a percentage of total loans(13) | 2.6 | % | 2.1 | % | 2.3 | % | 2.0 | % | 1.4 | % | — | |||||||

Allowances for loan losses as a percentage of total loans | 2.2 | % | 2.2 | % | 2.2 | % | 2.1 | % | 1.7 | % | — | |||||||

Past due loans as a percentage of total loans(14) | 1.7 | % | 1.5 | % | 1.7 | % | 1.2 | % | 0.8 | % | — | |||||||

| U.S. GAAP | ||||||||||||||||||

| Profitability and Performance | ||||||||||||||||||

Net interest margin(15) | — | — | 5.2 | % | 4.0 | % | 3.8 | % | — | |||||||||

Return on average total assets(16) | — | — | — | 2.4 | % | 2.1 | % | — | ||||||||||

Return on average shareholders’ equity(17) | — | — | — | 18.7 | % | 17.8 | % | — | ||||||||||

| Asset Quality | ||||||||||||||||||

Past due loans as a percentage of total loans(14) | — | — | 2.8 | % | 2.4 | % | 2.0 | % | — | |||||||||

| OTHER DATA | ||||||||||||||||||

Inflation rate | 4.5 | % | 2.6 | % | 2.8 | % | 1.1 | % | 2.4 | % | — | |||||||

Revaluation (Devaluation) rate (Ch$/U.S.$) | (8.5 | )% | (14.6 | )% | (8.6 | )% | 15.9 | % | 6.6 | % | — | |||||||

Number of employees | 1,926 | 1,810 | 1,759 | 1,860 | 1,963 | — | ||||||||||||

Number of branches and offices | 66 | 67 | 67 | 66 | 63 | — | ||||||||||||

| (1) | Except per share data, percentages and ratios, share amounts, employee numbers and numbers of branch offices. |

| (2) | Amounts stated in U.S. dollars as of and for the year ended December 31, 2004 have been translated from pesos at the observed exchange rate of Ch$ 559.83 U.S.$1.00 as of December 31, 2004. |

| (3) | Represents dividends paid in respect of net income earned in the prior fiscal year. |

| (4) | Each ADS represents 5,000 shares of common stock. |

| (5) | Net interest income and total assets on a U.S. GAAP basis have been determined by applying the relevant U.S. GAAP adjustments to net interest income presented in accordance with Article 9 of Regulation S-X. See note 27 to our financial statements. |

| (6) | Net income per share of common stock in accordance with U.S. GAAP has been calculated on the basis of the weighted average number of shares outstanding for the period. One ADS equals 5,000 shares of common stock. |

| (7) | This line item is comprised primarily of bank premises and equipment, assets received in lieu of payment (repossessed assets), assets to be leased, amounts received under spot foreign exchange transactions, transactions in process, prepaid and deferred expenses, deferred income taxes and goodwill. |

| (8) | Net interest margin is defined as net interest revenue divided by average interest-earning assets. |

| (9) | Return on average total assets is defined as net income divided by average total assets. |

| (10) | Return on average shareholders’ equity is defined as net income divided by average shareholders’ equity. |

-9-

Table of Contents

| (11) | Operating expenses as a percentage of operating revenue. Operating revenue is the aggregate of net interest revenue, fees and income from service (net) and other operating income (net). |

| (12) | Represents the ratio of dividends declared per share divided by net income per share. |

| (13) | Overdue loans consist of all non-current loans. |

| (14) | Past due loans include, with respect to any loan, the amount of principal or interest that is 90 days or more overdue, and do not include the installments of such loan that are not overdue or that are less than 90 days overdue, unless legal proceedings have been commenced for the entire outstanding balance according to the terms of the loan. Under U.S. GAAP, non-performing loans would include the total outstanding amount of the loan if any principal or interest payment was 90 days or more past due. |

| (15) | Net interest margin on a U.S. GAAP basis has been determined by applying the relevant U.S. GAAP adjustments to net interest income presented in accordance with Article 9 of Regulation S-X. See note 26 to our financial statements. |

| (16) | Net income divided by average total assets. Average total assets were calculated as an average of the beginning and ending balance for each year, and total assets on a U.S. GAAP basis have been determined by applying the relevant U.S. GAAP adjustments to shareholders’ equity. See note 27 to our financial statements. |

| (17) | Average shareholders’ equity was calculated as an average of the beginning and ending balance for each year. Shareholders’ equity on a U.S. GAAP basis has been determined by applying the relevant U.S. GAAP adjustments to shareholders’ equity. See note 27 to our financial statements. |

B. CAPITALIZATION AND INDEBTEDNESS

Not applicable.

C. REASONS FOR THE OFFER AND USE OF PROCEEDS

Not applicable.

D. RISK FACTORS

RISKS ASSOCIATED WITH OUR BUSINESS

The growth of our loan portfolio may expose us to increased loan losses.

From December 31, 1995 to December 31, 2004, our aggregate loan portfolio grew by 476.9% in nominal terms to Ch$ 2,443,649 million. Our business strategy provides for the increase in our market share through an increase in our loan portfolio. The growth of our loan portfolio (particularly in the lower-middle to middle income consumer and small and medium-sized corporate business segments) may expose us, in an economic downturn, to a higher level of loan losses and require us to establish proportionately higher levels of provisions for loan losses, which will partially offset the increased income that we can expect to receive as the loan portfolio grows.

Our loan portfolio may not continue to grow at the same rate.

There can be no assurance that in the future our loan portfolio will continue to grow at the same or similar rates as the growth rate that we historically experienced. Due to the economic slowdown in Chile in recent years and the recession of 1999, loan demand has not been as strong as it was in the mid-1990s. Average loan growth has, however, remained significant in the last five years. According to the Chilean Superintendency of Banks, from December 31, 1999 to December 31, 2004, the aggregate amount of loans in the Chilean banking system (on an unconsolidated basis) grew 47.2% in nominal terms to Ch$ 37,832.9 million as of December 31, 2004. A reversal of the rate of growth of the Chilean economy could adversely affect the rate of growth of our loan portfolio and our risk index and, accordingly, increase our required allowance for loan losses.

Increased competition and industry consolidation may adversely affect the results of our operations.

The Chilean market for financial services is highly competitive. We compete with other Chilean private sector domestic and foreign banks, with BancoEstado (a public-sector bank) and with large department stores that make consumer loans to a large portion of the Chilean population. Since 2001, three new private sector banks affiliated with Chile’s largest department stores initiated their operations mainly as consumer and medium-sized corporate niche banks. The lower-middle to middle income segments of the Chilean population and the small and medium-sized corporate segments have become the target markets of several banks, and competition in these segments is likely to increase. As a result, net interest margins in these segments are likely to decline. Although we believe that demand for financial products and services from the lower-middle to middle income market segments and for small and medium-sized companies will continue to grow during the remainder of the decade, we cannot assure you that net interest margins will be maintained at their current levels. We believe that our principal competitors are Banco de Crédito e Inversiones (BCI), Banco Bilbao Vizcaya Argentaria, Chile S.A., or BBVA, Banco del Desarrollo, Citibank and Scotiabank Sudamericano, but we also face competition from larger banks such as Banco de Chile and Banco Santander Santiago, among others.

-10-

Table of Contents

We also face competition from non-bank and non-finance competitors with respect to some of our credit products, such as credit cards and consumer loans. Non-bank competition from large department stores has become increasingly significant in the consumer lending sector. In addition, we face competition from non-bank finance competitors, such as leasing, factoring and automobile finance companies, with respect to credit products, and mutual funds, pension funds and insurance companies, with respect to savings products and mortgage loans. Currently, banks continue to be the main suppliers of leasing, factoring and mutual funds, and the insurance sales business has seen rapid growth. Nevertheless, non-banking competition, especially department stores, may be able to engage in some types of advertising and promotion in which, by virtue of Chilean banking rules and regulations, we are prohibited from engaging.

The increase in competition within the Chilean banking industry in recent years has led to, among other things, consolidation in the industry. In 2002 Banco Santiago and Banco Santander-Chile, the then second and third largest private banks in Chile, respectively, merged to become Chile’s largest bank. In 2002, Banco de Chile and Banco de A. Edwards, then the third and fifth largest private banks in Chile respectively, merged to become the second largest Chilean bank. In 2004, Banco de Crédito e Inversiones (BCI) purchased 99.9% of the shares of Banco Conosur. Consolidation, which can result in the creation of larger and stronger competitors, may adversely affect our financial condition and results of operations by decreasing the net interest margins we are able to generate and increasing our costs of operation.

Our exposure to individuals and small and medium-sized businesses could lead to higher levels of past due loans and subsequent loan losses.

A substantial number of our customers consists of individuals and small and medium-sized companies (those with annual sales between Ch$600 million and Ch$5,999 million). As part of our business strategy, we seek to increase lending and other services to small and medium-sized companies and individuals. Our business results relating to our individual and small and medium-sized company customers are, however, more likely to be adversely affected by downturns in the Chilean economy, including increases in unemployment, than our business from large corporations and high-income individuals. For example, unemployment directly affects the capacity of individuals to obtain and repay consumer loans. Consequently, in the future we may experience higher levels of past due loans, which could result in higher provisions for loan losses. In 1997, the Chilean Superintendency of Banks increased the level of provisions required for consumer loans (including loans to high income individuals) due to concerns regarding the levels of consumer indebtedness and vulnerability of the banking sector in an economic downturn. There can be no assurance that the levels of past due loans and subsequent loan losses will not be materially higher in the future.

Our results of operations are affected by interest rate volatility.

Our results of operations depend to a great extent on our net interest revenue. In 2003 and 2004, net interest revenue represented 70.2% and 81.4% of our operating revenues, respectively. Changes in market interest rates could affect the interest rates earned on our interest-earning assets differently from the interest rates paid on our interest-bearing liabilities leading to a reduction in our net interest revenue. Interest rates are highly sensitive to many factors beyond our control, including the reserve policies of the Central Bank, deregulation of the financial sector in Chile, domestic and international economic and political conditions and other factors. Any volatility in interest rates could adversely affect our business, our future financial performance and the price of our securities. Over the period from December 31, 1998 to December 31, 2004, yields on the Chilean government’s 90-day note as reported on those dates moved from 13.49% to 2.58%, decreasing every year, with a high of 8.69% and low of 6.14% in 2001, a high of 6.00% and a low of 2.87% in 2002, a high of 2.97% and a low of 2.48% in 2003, a high of 2.35% and a low of 1.31% in 2004 and a high of 3.24% and a low of 2.49% in the first five months of 2005.

RISKS RELATING TO CHILE

Our growth and profitability depend on the level of economic activity in Chile and other emerging markets.

A substantial amount of our loans are to borrowers doing business in Chile. Accordingly, the recoverability of these loans in particular, our ability to increase the amount of loans outstanding and our results of operations and financial condition in general, are dependent to a significant extent on the level of economic activity in Chile. The Chilean economy has been influenced, to varying degrees, by economic conditions in other emerging market

-11-

Table of Contents

countries. We cannot assure you that the Chilean economy will continue to grow in the future or that future developments in or affecting the Chilean economy, including further consequences of continuing economic difficulties in Brazil, Argentina and other emerging markets, will not materially and adversely affect our business, financial condition or results of operations.

According to data published by the Central Bank, the Chilean economy contracted at a rate of 0.8% in 1999 and grew at a rate of 4.5% in 2000, 3.4% in 2001, 2.2% in 2002, 3.3% in 2003 and 6.1% in 2004. Historically, lower economic growth has adversely affected the overall asset quality of the Chilean banking system and that of our portfolios. According to information published by the Chilean Superintendency of Banks, the unconsolidated risk index of the components of the Chilean financial system as a whole deteriorated from 1.98% as of October 31, 1999, to 2.08% as of October 31, 2000, improved to 1.90% as of October 2001, deteriorated to 1.95% as of October 31, 2002, improved to 1.82% as of October 31, 2003 and deteriorated to 1.99% as of December 31, 2004. Our unconsolidated risk index as of December 31, 2004 was 1.58%. Our results of operations and financial condition could also be affected by changes in economic or other policies of the Chilean government, which has exercised and continues to exercise a substantial influence over many aspects of the private sector, or other political or economic developments in Chile.

Although economic conditions are different in each country, investors’ reactions to developments in one country may affect the securities of issuers in other countries, including Chile. For instance, the devaluation of the Mexican peso in December 1994 set off an economic crisis in Mexico that negatively affected the market value of securities in many countries throughout Latin America. The crisis in the Asian markets, beginning in July 1997, resulted in sharp devaluations of other Asian currencies and negatively affected markets throughout Asia, as well as many markets in Latin America, including Chile. Similar adverse consequences resulted from the 1998 crisis in Russia and the devaluation of the Brazilian real in 1999. In part due to the Asian and Russian crises, the Chilean stock market declined significantly in 1998 to levels equivalent to 1994.

Economic problems in Argentina and Brazil may have an adverse effect on the Chilean economy and on our results of operations and the share price of our ADSs and shares.

If Argentina’s economic environment deteriorates or does not continue to improve, the economy in Chile, as both a neighboring country and a trading partner, could also be affected and could experience slower growth than in recent years.

Our business could be affected by political uncertainty and economic weakness in Brazil. This could result in the need for us to increase our loan allowances and provisions thus affecting our financial condition, our results of operations and the price of our shares and ADSs, or our business.

Securities prices of Chilean companies including banks are, to varying degrees, influenced by economic and market considerations in other emerging market countries and by the U.S. economy. We cannot assure you that the weak Argentine economy and related economic uncertainty and the political and economic uncertainty in Brazil will not have an adverse effect on Chile, the price of our securities, or our business.

Currency fluctuations could adversely affect our financial condition and results of operations and the value of our shares and ADSs.

The Chilean government’s economic policies and any future changes in the value of the peso against the U.S. dollar could affect the dollar value of our securities. The peso has been subject to large devaluations in the past and could be subject to significant fluctuations in the future. In the period from December 31, 1997 to December 31, 2004, the value of the peso relative to the U.S. dollar decreased 27.3%, as compared to an 8.8% decrease in value in the period from December 31, 1994 to December 31, 1997. The observed exchange rate for June 15, 2005 was Ch$589.38 = U.S.$1.00, reflecting an appreciation of the peso against the U.S. dollar of 1.70% since December 31, 2003. Our results of operations may be affected by fluctuations in the exchange rates between the peso and the dollar despite our policy and Chilean regulations relating to the general avoidance of material exchange rate mismatches. In order to avoid material exchange rate mismatches, we enter into forward exchange transactions. As of December 31, 2004, our foreign currency denominated assets and peso-denominated assets that contain repayment terms linked to changes in foreign currency exchange rates exceeded our foreign currency denominated liabilities and peso-denominated liabilities that contain repayment terms linked to changes in foreign currency exchange rates by Ch$13,798 million (approximately U.S.$24.6 million).

-12-

Table of Contents

We may decide to change our policy regarding exchange rate mismatches. Regulations that limit such mismatches may also be amended or eliminated. Greater exchange rate mismatches will increase our exposure to the devaluation of the peso, and any such devaluation may impair our capacity to service our foreign-currency obligations and may, therefore, materially and adversely affect our financial condition and results of operation. Notwithstanding the existence of general policies and regulations that limit material exchange rate mismatches, the economic policies of the Chilean government and any future fluctuations of the peso against the dollar could affect our financial condition and results of operations.

Trading transactions in Chile of the shares of common stock underlying our ADSs are denominated in pesos. Cash distributions with respect to our shares of common stock are received in Chilean pesos by the depositary, which then converts such amounts to U.S. dollars at the then-prevailing exchange rate for the purpose of making payments in respect of our ADSs. If the value of the Chilean peso falls relative to the U.S. dollar, the dollar value of our ADSs and any distributions to be received from the depositary will be reduced. In addition, the depositary will incur customary currency conversion costs (to be borne by the holders of our ADSs) in connection with the conversion and subsequent distribution of dividends or other payments.

High levels of inflation could adversely affect our financial condition and results of operations.

Although Chilean inflation has moderated in recent years, Chile has experienced high levels of inflation in the past. High levels of inflation in Chile could adversely affect the Chilean economy and have an adverse effect on our results of operations and, indirectly, the value of our securities. The following table shows the annual rate of inflation (as measured by changes in the Chilean consumer price index, or CPI, and as reported by the ChileanInstituto Nacional de Estadísticas, or the Chilean National Institute of Statistics, during the last six years ended December 31 and through May 31, 2005).

Year | Inflation (CPI) | |

| (in percentages) | ||

1999 | 2.3 | |

2000 | 4.5 | |

2001 | 2.6 | |

2002 | 2.8 | |

2003 | 1.1 | |

2004 | 2.4 | |

2005 (through May 31) | 1.4 |

There can be no assurance that our operating results will not be adversely affected by changing levels of inflation, or that Chilean inflation will not change significantly from the current level.

Banking regulations may adversely affect our financial condition and results of operations.

We are subject to regulation by the Chilean Superintendency of Banks. In addition, we are subject to regulation by the Central Bank with regard to certain matters, including interest rates and foreign exchange. During the Chilean financial crisis of 1982 and 1983, the Central Bank and the Chilean Superintendency of Banks strictly controlled the funding, lending and general business matters of the banking industry in Chile.

Pursuant to the ChileanLey General de Bancos, Decreto con Fuerza de Ley No. 3 de 1997, or the General Banking Law, all Chilean banks, subject to the approval of the Chilean Superintendency of Banks, may engage in certain businesses other than commercial banking depending on the risk associated with such business and the financial strength of the bank. Such additional businesses include securities brokerage, mutual fund management, securitization, insurance brokerage, leasing, factoring, financial advisory, custody and transportation of securities, loan collection and financial services. The General Banking Law also applies to the Chilean banking system a modified version of the capital adequacy guidelines issued by the Basle Committee on Banking Regulation and Supervisory Practices and limits the discretion of the Chilean Superintendency of Banks to deny new banking licenses. There can be no assurance that regulators will not in the future impose more restrictive limitations on the activities of banks, including us, than those currently in effect. Any change in applicable banking regulations could have a material adverse effect on our financial condition or results of operations.

Historically, Chilean banks have not paid interest on amounts deposited in checking accounts. However, effective June 1, 2002, the Central Bank allowed banks to pay interest on checking accounts. Currently, there are no

-13-

Table of Contents

applicable restrictions on the interest that may be paid on checking accounts. If competition or other factors lead us to pay interest on checking accounts, to relax the conditions under which we pay interest or to increase the number of checking accounts on which we pay interest, any such change could have a material adverse effect on our financial condition or results of operations.

Chile has different corporate disclosure and accounting standards than those you may be familiar with in the United States.

The accounting, financial reporting and securities disclosure requirements in Chile differ from those in the United States. Accordingly, the information about us available to you will not be the same as the information available to shareholders of a U.S. company.

Chilean financial statements and reported earnings generally differ from those reported based on U.S. accounting and reporting standards. See “Item 5. Operating and Financial Review and Prospects—Operating Results—Chilean and U.S. GAAP Reconciliation” and note 27 to our financial statements for a description of the principal differences between Chilean GAAP and U.S. GAAP as such differences relate to us, and a reconciliation to U.S. GAAP of shareholders’ equity and net income as of and for each of the years ended December 31, 2004 and 2003.

As a regulated financial institution, we are required to submit to the Chilean Superintendency of Banks unaudited unconsolidated balance sheets and income statements, excluding any related footnote disclosure, prepared in accordance with Chilean GAAP and the rules of the Chilean Superintendency of Banks on a monthly basis. This information is made public by the Chilean Superintendency of Banks within approximately three months of receipt. The Chilean Superintendency of Banks also makes summary financial information available within three weeks of receipt. Such disclosure differs in a number of significant respects from information generally available in the United States with respect to U.S. financial institutions.

The securities laws of Chile, which govern open or publicly listed companies such as us, have as a principal objective promoting disclosure of all material corporate information to the public. Chilean disclosure requirements, however, differ from those in the United States in some important respects. In addition, although Chilean law imposes restrictions on insider trading and price manipulation, applicable Chilean laws are different from those in the United States and in certain respects the Chilean securities markets are not as highly regulated and supervised as the U.S. securities markets.

Chile imposes controls on foreign investment and repatriation of investments that may affect your investment in, and earnings from, our ADSs.

Equity investments in Chile by persons who are not Chilean residents have generally been subject to various exchange control regulations which restrict the repatriation of the investments and earnings therefrom. In April 2001, the Central Bank eliminated the regulations that affected foreign investors except that investors are still required to provide the Central Bank with information related to equity investments and conduct such operations within Chile’sMercado Cambiario Formal, or Formal Exchange Market. See “Item 10. Additional Information—D. Exchange Controls” for a discussion of the types of information required to be provided.

Owners of ADSs are entitled to receive dividends on the underlying shares to the same extent as the holders of shares. Dividends received by holders of ADSs will be converted into U.S. dollars and distributed net of foreign currency exchange fees and fees of the depositary and will be subject to Chilean withholding tax, currently imposed at a rate of 35.0% (subject to credits in certain cases). If for any reason, including changes in Chilean laws or regulations, the depositary were unable to convert pesos to U.S. dollars, investors may receive dividends and other distributions, if any, in pesos.

We cannot assure you that additional Chilean restrictions applicable to holders of our ADSs, the disposition of the shares underlying them or the repatriation of the proceeds from such disposition or the payment of dividends will not be imposed in the future, nor can we advise you as to the duration or impact of such restrictions if imposed.

-14-

Table of Contents

RISKS RELATING TO OUR ADSs

There may be a lack of liquidity and market for our shares and ADSs.

We cannot assure you as to the liquidity of any markets that may develop for our ADSs, the ability of the holders to sell our ADSs or the price at which holders of our ADSs will be able to sell them. Future trading prices of our ADSs will depend on many factors including, among other things, prevailing interest rates, our operating results and the market for similar securities.

Our common stock underlying the ADSs is listed and traded on the Santiago Stock Exchange and the Chilean Electronic Exchange, although the trading market for the common stock is small by international standards. As of June 15, 2005, we had 226,909,290,577 shares of common stock outstanding. The Chilean securities markets are substantially smaller, less liquid and more volatile than major securities markets in the United States. In addition, according to Article 14 of theLey de Mercado de Valores, Ley No. 18,045, or the Chilean Securities Market Law, the Superintendencia de Valores y Seguros, or the Chilean Superintendency of Securities and Insurance, may suspend the offer, quotation or trading of shares of any company listed on the Chilean stock exchanges for up to 30 days if, in its opinion, such suspension is necessary to protect investors or is justified for reasons of public interest. Such suspension may be extended for up to 120 days. If, at the expiration of the extension, the circumstances giving rise to the original suspension have not changed, the Chilean Superintendency of Securities and Insurance will then cancel the relevant listing in the registry of securities. Furthermore, the Santiago Stock Exchange may inquire as to any movement in the price of any securities in excess of 10% and suspend trading in such securities for a day if it deems necessary. These and other factors may substantially limit your ability to sell the common stock underlying your ADSs at a price and time at which you wish to do so.

There can be no assurance that a liquid trading market for the common stock in Chile will continue. Approximately 42.5% of our outstanding common stock was held by the public as of June 15, 2005. A limited trading market in general and our concentrated ownership in particular may impair the ability of an ADS holder to sell in the Chilean market shares of common stock obtained upon withdrawal of such shares from the ADR facility in the amount and at the price and time such holder desires, and could increase the volatility of the price of the ADSs.

Certain actions by our principal shareholder may have an adverse effect on the future market price of our ADSs and shares.

Alvaro Saieh Bendeck, through Corp Group Banking S.A. and Compañía Inmobiliaria y de Inversiones Saga S.A., or Saga, indirectly beneficially owns approximately 57.48% of our outstanding voting rights. The sale or disposition by Mr. Saieh Bendeck of our shares or ADSs that he indirectly owns, or the perception in the marketplace that such a sale or disposition may occur, may adversely affect the trading price of our shares on the Santiago Stock Exchange and, consequently, the market price of the ADSs.

You may be unable to exercise preemptive rights.

TheLey Sobre Sociedades Anónimas, Ley No. 18,046and theReglamento de Sociedades Anónimas, which we refer to collectively as the Chilean Corporations Law, and applicable regulations require that whenever we issue new common stock for cash, we grant preemptive rights to all of our shareholders (including holders of ADSs), giving them the right to purchase a sufficient number of shares to maintain their existing ownership percentage. Such an offering would not be possible unless a registration statement under the Securities Act of 1933, as amended, or the Securities Act, were effective with respect to such rights and common stock or an exemption from the registration requirements thereunder were available.

Since we are not obligated to file a registration statement with respect to such rights and the common stock, you may not be able to exercise your preemptive rights. If a registration statement is not filed and an applicable exemption is not available, the depositary will attempt to sell such holders’ preemptive rights and distribute the proceeds thereof, after deducting its expenses and fees, if a premium can be recognized over the cost of any such sale.

-15-

Table of Contents

You may have fewer and less well defined shareholders’ rights than with shares of a company in the United States.

Our corporate affairs are governed by ourestatutos, or by-laws, and the laws of Chile. Under such laws, our shareholders may have fewer or less well-defined rights than they might have as shareholders of a corporation incorporated in a U.S. jurisdiction. For example, under legislation applicable to Chilean banks, our shareholders would not be entitled to appraisal rights in the event of a merger or other business combination undertaken by us.

Holders of ADSs are not entitled to attend shareholders’ meetings, and they may only vote through the depositary.

Under Chilean law, a shareholder is required to be registered in our shareholders’ registry at least five business days before a shareholders’ meeting in order to vote at such meeting. A holder of ADSs will not be able to meet this requirement and accordingly is not entitled to vote at shareholders’ meetings because the shares underlying the ADSs will be registered in the name of the depositary. While a holder of ADSs is entitled to instruct the depositary as to how to vote the shares represented by ADSs in accordance with the procedures provided for in the deposit agreement, a holder of ADSs will not be able to vote its shares directly at a shareholders’ meeting or to appoint a proxy to do so. In certain instances, a discretionary proxy may vote our shares underlying the ADSs if a holder of ADSs does not instruct the depositary with respect to voting.

It may be difficult to enforce civil liabilities against us or our directors, officers and controlling persons.

We are organized under the laws of Chile, and all of our directors, officers and controlling persons reside outside the United States. In addition, all or a substantial portion of our assets are located in Chile. As a result, it may be difficult for investors to effect service of process within the United States on such persons or to enforce judgments against them, including in any action based on civil liabilities under the U.S. federal securities laws. There is doubt as to the enforceability against such persons in Chile, whether in original actions or in actions to enforce judgments of U.S. courts, of liabilities based solely on the U.S. federal securities laws.

ITEM 4. INFORMATION ON THE COMPANY

A. HISTORY AND DEVELOPMENT OF THE COMPANY

We are asociedad anónima (corporation) organized under the laws of the Republic of Chile and licensed by the Chilean Superintendency of Banks to operate as a commercial bank. Our principal executive offices are located at Huérfanos 1072, Santiago, Chile. Our telephone number is 56-2-687-8000 and our website is www.corpbanca.cl. Information set forth at our website does not constitute a part of this annual report. Corpbanca and all our subsidiaries are organized under the laws of Chile. The terms “Corpbanca,” “Bank,” “we,” “us” and “our” in this annual report refer to Corpbanca together with its subsidiaries unless otherwise specified.

History

Corpbanca is Chile’s oldest currently operating bank—we were founded as Banco de Concepción in 1871 by a group of residents of the City of Concepción, Chile led by Aníbal Pinto, who would later become President of Chile. In 1971, Banco de Concepción was transferred to a government agency,Corporación de Fomento de la Producción (the Chilean Corporation for the Development of Production, or CORFO). Also in 1971, Banco de Concepción acquired Banco Francés e Italiano en Chile, which provided for the expansion of Banco de Concepción into Santiago. In 1972 and 1975, the bank acquired Banco de Chillán and Banco de Valdivia, respectively. In November 1975, CORFO sold its shares of the bank to private business persons, who took control of the bank in 1976. In 1980 the name of the bank was changed to Banco Concepción. In 1983, control of Banco Concepción was assumed by the Chilean Superintendency of Banks. The bank remained under the control of the Chilean Superintendency of Banks through 1986, when it was acquired bySociedad Nacional de Minería (the Chilean National Mining Society, or SONAMI). Under SONAMI’s control, Banco Concepción focused on providing financing to small- and medium-sized mining interests, increased its capital and sold a portion of its high-risk portfolio to the Central Bank. Investors led by Mr. Alvaro Saieh Bendeck purchased a majority interest of Banco Concepción from SONAMI in 1996. During the last 16 years, Mr. Saieh Bendeck has directed the acquisition, creation and operation of a number of commercial banks, mutual fund companies, insurance companies and other financial entities in Chile and other parts of Latin America.

-16-

Table of Contents

Following our acquisition in 1996, we began to take significant steps to improve our credit risk policies, increase operating efficiency and expand our operations. These steps included applying stricter provisioning and charge-off standards to our loan portfolio, cost cutting measures and technological improvements. We also changed our name to Corpbanca and hired a management team with substantial experience in the Chilean financial services industry. Several of our senior officers, prior to joining Corpbanca, were employed by Banco Osorno prior to its merger with Banco Santander-Chile in 1996. In addition, we significantly expanded our operations in 1998 through the acquisition of the Consumer Loan Division of Corfinsa (which was formerly a consumer loan division of Banco Sudamericano, currently Scotiabank Sudamericano) and the finance company Financiera Condell S.A. In November 2002, we completed the largest equity capital-raising transaction in Chile in that year, providing us with Ch$111,732 million (approximately U.S.$153 million using the exchange rate that was in effect as of December 31, 2002) in capital to help implement our growth strategies. We continue to consolidate our information technology systems into a single, integrated platform, Integrated Banking System, or IBS, providing us with a single, central electronic database that gives us up-to-date customer information in each of our business lines and calculates net earnings and profitability of each product and client segment.

As a result of the steps we have taken since the 1996 acquisition, we have developed a number of significant competitive strengths that we believe will continue to contribute to our growth potential. These include operating efficiencies, improved asset quality, an experienced management team, and a strong technological infrastructure. As of December 31, 2004, our efficiency ratio and our return on assets was the best among our peers (Banco Santander Chile, Banco de Chile, Banco de Crédito e Inversiones, BBVA, Scotiabank Sudamericano, Citibank, Banco del Desarrollo). Since 1996 we continue to be the fastest-growing bank in Chile in terms of loan portfolio size. In addition, our asset quality, as reflected by our risk index and our risk classification by the Chilean Superintendency of Banks, is comparable to that of our principal competitors, and our capitalization places us in a strong position among Chilean banks in terms of ability to fund growth. In recent years, our cost of funding has decreased as a result of improvements in our ratings. We believe that these strengths position us well for continued growth in the Chilean financial services industry.

As of December 31, 2004, our loan portfolio amounted to Ch$2,443,649 million, as compared to Ch$423,592 million as of December 31, 1995, representing 476.9% growth in nominal terms (314.4% in real terms). In 2004, our consolidated efficiency ratio (operating expenses as a percentage of operating revenue which is the aggregate of net interest revenue, fees and income from services (net) and other operating income (net)) was 39.2%, which represents a significant improvement over our unconsolidated efficiency ratio of 81.3% for 1995 (when we were not required to present consolidated financial statements). In addition, during the period from 1995 through 2004, our return on average total assets increased from 0.5% to 1.5% and our unconsolidated risk index improved from 3.20% as of December 31, 1995 to 1.58% as of December 31, 2004.

As of December 31, 2004, we had total assets of Ch$3,201,584 million (approximately U.S.$5,718,9 million) and shareholders’ equity (excluding net income for the year to date) of Ch$325,629 million (approximately U.S.$582 million). Our net income for 2004 was Ch$50,767 million (approximately U.S.$90.7 million), our return on average total assets was 1.5% and our return on average shareholders’ equity was 14.0%.

Strategy

Our primary business objectives include enhancing our market position in the Chilean financial services industry in terms of market share, service coverage and profitability by providing high quality financial products and services through efficient distribution channels to our customer base. We intend to achieve these objectives through the following strategies:

Continue to grow our operations profitably

We seek to achieve organic growth by offering competitive products and services in all of our lines of business. Our capital structure currently provides us with a strong basis upon which to grow our loan portfolio and expand our operations and branch network. We believe that our strong franchise in the retail banking segment offers the potential for significant growth in our loan portfolio. We are also focusing our marketing efforts on potential clients among small and medium-sized companies, large corporate clients and private banking customers. In addition, we may seek to expand through strategic acquisitions over time.

-17-

Table of Contents

Capitalize on customer loyalty through cross-selling

We intend to increase our market share and profitability by continuing to cross-sell services and products to our existing clients. We have instituted processes that facilitate our ability to offer additional financial services to our clients, with an emphasis on increasing our revenues from fees from services. For example, we aim to increase our portfolio of mortgage loans by cross-selling mortgage products to our banking clients. In addition, we cross-sell loan products to our checking and savings account customers that are tailored to their individual needs and financial situation. We plan to continue these and other cross-selling efforts.

Increase operating efficiency through technological advances

We intend to maintain our position as the most efficient bank among our peers. We seek to achieve this goal by continuing to reduce costs, broadening our array of distribution channels and enhancing our distribution network through the adoption of cost-saving technologies. We continue to update our branch operations to allow for an increased level of customer “ self-help.” We are also working to increase use of internet banking by our customers. Currently, our customers are able to obtain account information, make bill payments, transfer funds and perform other transactions through our internet site. In addition, our recent implementation of IBS, a central information system that replaced a number of systems, providing us with a single, central electronic database that gives us up-to-date customer information in each of our business lines and calculates net earnings and profitability of each product and client segment, has resulted in additional cost savings. We have enhanced and continue to enhance our IBS network by implementing management information system software that we believe allows us to better assess the profitability of our customer relationships. We believe that the implementation of these and other technological advances will continue to improve our cost structure by minimizing the number of transactions that are initiated through our traditional branch network while at the same time responding to our customers’ evolving needs.

Actively manage risk exposure

We have a dedicated risk management team that focuses on monitoring risks across all areas of our business. Our credit committee meets weekly to review and approve or decline new credit proposals. We intend to continue to maintain what we believe to be conservative credit approval standards and reserve policies, enabling us to minimize the risk of ultimate loss. As of December 31, 2004, we had allowances for loan losses of Ch$41,611 million, representing 1.7% of total loans, charge-offs for 2004 of Ch$21,923 million, representing 1.3% of average loans for the period, and direct charge-offs for 2004 of Ch$2,762 million, representing 0.2% of average loans for 2004.

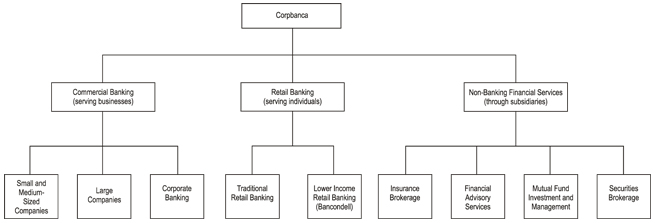

B. BUSINESS OVERVIEW

Principal Business Activities

We provide a broad range of commercial and retail banking services to our customers. In addition, we provide financial advisory services, mutual fund management, insurance brokerage and securities brokerage services through our subsidiaries. The following chart sets forth our principal lines of business:

-18-

Table of Contents

As of December 31, 2004, we have a nationwide network of 63 branches in Chile, including 25 branches operating under the Corpbanca name, 17 branches operating under the Bancondell name, and 21 integrated branches, which operate under both the Corpbanca and Bancondell names. In addition, we owned and operated 158 ATMs in Chile as of December 31, 2004, and our customers have access to thousands of ATMs in Chile through our agreement with Redbanc S.A., or Redbanc. We utilize a number of different sales channels including account executives, telemarketing and the internet to attract new clients.

The following table provides information on the composition of our loan portfolio and other revenue-producing assets as of December 31, 2003 and December 31, 2004:

Loan/Asset Category | As of December 31, | As of December 31, | Variation | Variation (expressed as a percentage) | |||||||||

| (in millions of constant Ch$ as of December 31, 2004) | |||||||||||||

Commercial loans | |||||||||||||

General commercial loans | Ch$ | 994,496 | Ch$ | 1,123,389 | Ch$ | 128,893 | 13.0 | % | |||||

Foreign trade loans | 142,975 | 178,662 | 35,687 | 25.0 | |||||||||

Interbank loans | 4,100 | 20,003 | 15,903 | 387.9 | |||||||||

Leasing contracts | 157,801 | 179,009 | 21,208 | 13.4 | |||||||||

Factoring | 38,172 | 60,118 | 21,946 | 57.5 | |||||||||

Other outstanding loans | 41,529 | 85,891 | 44,362 | 106.8 | |||||||||

Subtotal commercial loans | 1,379,073 | 1,647,072 | 267,999 | 19.4 | |||||||||

Mortgage loans | |||||||||||||

Residential | 102,756 | 92,594 | (10,162 | ) | (9.9 | ) | |||||||

Commercial | 210,463 | 200,756 | (9,707 | ) | (4.6 | ) | |||||||

Subtotal mortgage loans | 313,219 | 293,350 | (19,869 | ) | (6.3 | ) | |||||||

Consumer loans | 223,580 | 286,817 | 63,237 | 28.3 | |||||||||

Past due loans | |||||||||||||

Commercial loans | 17,957 | 10,072 | (7,885 | ) | (43.9 | ) | |||||||

Residential mortgage loans | 7,507 | 8,589 | 1,082 | 14.4 | |||||||||

Consumer loans | 1,056 | 982 | (74 | ) | (7.0 | ) | |||||||

Past due loans | 26,520 | 19,643 | (6,877 | ) | (25.9 | ) | |||||||

Subtotal | 1,942,392 | 2,246,882 | 304,490 | 15.7 | |||||||||

Contingent loans(1) | 202,534 | 196,767 | (5,767 | ) | (2.8 | ) | |||||||

Total loans(2) | Ch$ | 2,144,926 | Ch$ | 2,443,649 | Ch$ | 298,723 | 13.9 | ||||||

| (1) | For purposes of loan classification, contingent loans are considered as commercial loans. |

| (2) | All of the above categories except mortgage loans, past due loans and contingent loans are combined into “Loans.” |

Commercial Banking

In order to better serve businesses, we have divided our commercial banking services into the following divisions: small and medium-sized companies, large companies, corporate banking, leasing and factoring. In the 1996-2004 period, loans made to businesses, including commercial loans, trade finance, leasing agreements and contingent loans, experienced significant growth. As of December 31, 2004, we had aggregate commercial loans (including leasing, factoring, commercial mortgage and commercial past due loans) in the amount of Ch$2,054,667 million, comprising 84.1% of our total loan portfolio.

Small and Medium-Sized Companies. Our small and medium-sized companies business area services businesses with annual sales between Ch$600 million and Ch$5,999 million. We believe that the close relationships we have developed with our small and medium-sized business customers over the years provides us with a significant competitive advantage in this business area.

Our small and medium-sized companies business division offers its customers a broad range of financial products, including general commercial loans, working capital loans, trade finance, on-lending of financing originated by CORFO, overdraft credit lines, letters of credit, and mortgage loans. As of December 31, 2004, we had approximately 6,397 small and medium-sized company loan customers.

Large Companies. Our large companies business area services domestic companies with annual sales between and including Ch$6,000 million and Ch$60,000 million. This business area offers these companies a broad range of services tailored to their specific needs. These services include deposit-taking and lending in both pesos

-19-

Table of Contents

and foreign currency, trade financing, general commercial loans, working capital loans, letters of credit, interest and exchange rate insurance and cash flow management, among others. As of December 31, 2004, we had 520 large company debtors.

Corporate Banking. Our corporate banking business area is responsible for serving corporations having annual sales in excess of Ch$60,000 million. Our corporate banking division is focused on offering these clients a broad range of products, including working capital loans, credit lines, financial services, special advisory services, trade finance, syndicated loans and currency forwards. As of December 31, 2004, we had 54 corporate banking customers.

Leasing. This business division consists of providing leasing services relating to commercial real estate, vehicles, machinery and other items to our customers. As of December 31, 2004, we had total assets outstanding in our leasing division of Ch$179,009 million, comprising 7.3% of our total loan portfolio.