Exhibit 99.2

FINANCIAL SUPPLEMENT TO SECOND QUARTER 2009 EARNINGS RELEASE

Summary

Quarterly loss of $0.28 per diluted share; solid underlying business performance offset by increased provision for loan losses

| • | Significant second quarter drivers include: $912 million loan loss provision ($421 million above net charge-offs);strong non-interest revenues, largely due to stronger service charges and brokerage income;3 percent increase in net interest income, as net interest margin steadied; Results include$61 million gain related to exchange of trust preferred securities; $80 million Visa share sale gain; $108 million of securities gains;$69 million securities related impairment; and $64 million FDIC special assessment expense |

| • | Pre-provision net revenue, excluding items listed above, rose 11 percent versus 1Q09 |

Deposits and households continue to grow; record customer satisfaction

| • | Average customer deposits grew 3% linked quarter, up 10% versus the year-ago quarter average |

| • | Average non-interest bearing deposits continue to rise, growing 8% linked quarter |

| • | A record 491,000 of new retail and business checking accounts opened year-to-date |

| • | Outstanding customer satisfaction; top quartile performance in latest Gallup poll; most improved retail bank according to latest J.D. Power and Associates survey |

Stabilizing net interest margin contributes to growth in net interest income

| • | Second quarter net interest income increased $22 million to $831 million |

| • | Net interest margin steadied, declining two basis points to 2.62 percent, reflecting continued low-cost deposit growth, especially in non-interest bearing products, and improved loan spreads due to better pricing discipline |

| • | Excluding the impact of the linked-quarter increase in excess liquidity holdings, net interest margin improved 6 basis points |

| • | Impact of the declining interest rate environment has largely worked its way through the Company’s asset sensitive balance sheet, which is well-positioned for an eventual rising rate environment |

| • | Trends in deposit pricing and loan spreads should continue to support a stable net interest margin during this period of historic low interest rates |

Strong underlying non-interest income; continued focus on performance and efficiency

| • | Non-interest revenues increased 12 percent versus the prior quarter; excluding the impact of leveraged lease terminations, security gains, Visa shares gain and gain on trust preferred exchange, non-interest revenues increased 10 percent on a linked-quarter basis |

| • | Service charges income increased $19 million or 7 percent to $288 million, benefited from a higher level of customer transactions, new account growth and seasonal factors |

| • | Brokerage income increased $46 million or 21 percent to $263 million, driven by strong fixed income results and an improved equity market environment |

| • | Mortgage income remained strong in the 2nd quarter, totaling $64 million, reflecting favorable mortgage interest rate environment |

| • | Non-interest income impacted by $189 million of income related to the Company’s unwinding of leveraged lease transactions; However, minimal bottom line impact as transactions were offset by $196 million in tax expense |

| • | In transactions related to the Company’s capital plan, recorded a $61 million pre-tax gain on the early extinguishment of debt (trust preferred securities), sold remaining interest in Visa shares, recognizing an $80 million pre-tax gain, and sold $1.4 billion of U.S. Government Agency debentures at a $108 million pre-tax gain, reinvesting the proceeds in U.S. Government Agency mortgage-backed securities |

| • | Higher non-interest expense level mainly attributable to increased salaries and benefits cost, primarily due to increased incentives tied to the increase in brokerage revenues, and higher FDIC insurance costs |

| • | Non-interest expenses include a $64 million special FDIC assessment and $69 million in other-than-temporary impairment charges on securities |

Provision for loan losses increased to $912 million, $421 million above net charge-offs; Allowance for credit losses increased to 2.43% of loans, primarily due to migration of commercial real estate into problem loan status and additions to non-performing loans

| • | Net charge-offs rose to 2.06 percent of loans in the second quarter versus 1.64% in the previous quarter; increase primarily attributable to most stressed portfolios - homebuilder, condo and home equity second liens in Florida |

| • | Non-performing loans increased $977 million in the second quarter, largely driven by homebuilder and condominium properties |

| • | Certain income producing lending types, including retail and multi-family commercial real estate portfolios, are also coming under pressure from the faltering economy |

| • | Allowance for credit losses increased $400 million in the second quarter to 2.43 percent of loans as compared to 2.02 percent in the first quarter |

| • | Allowance coverage ratio (ALL/NPL, excluding loans held for sale) at 0.87x as of June 30, 2009 |

Continued focus on stressed portfolio and balance sheet de-risking

| • | Residential homebuilder portfolio exposure declines $362 million, down $3.4 billion since the beginning of 2008 |

| • | Condominium exposure steadily declining, down another $139 million to $711 million; less than 1 percent of overall loan portfolio |

| • | Florida second lien home equity exposure down slightly, totaling $3.6 billion; net charge off rate rose to 7.89 percent, compared to 5.99 percent in the first quarter, mainly reflecting the impact of declining housing prices in Florida |

Capital position significantly strengthened

| • | Supervisory Capital Assessment Program (SCAP) requirements fully completed |

| • | Tier 1 capital ratio increased to 12.2 percent at June 30, 2009, $6.9 billion above “Well Capitalized” threshold |

| • | Tier 1 common ratio increased to 8.1 percent, up approximately 160 basis points versus the previous quarter (see non-GAAP reconciliation) |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 2

Regions Financial Corporation and Subsidiaries

Consolidated Balance Sheets

(Unaudited)

($ amounts in millions) | Quarter Ended | |||||||||||||||||||

| 6/30/09 | 3/31/09 | 12/31/08 | 9/30/08 | 6/30/08 | ||||||||||||||||

Assets: | ||||||||||||||||||||

Cash and due from banks | $ | 2,363 | $ | 2,429 | $ | 2,643 | $ | 2,986 | $ | 3,161 | ||||||||||

Interest-bearing deposits in other banks | 2,846 | 2,288 | 7,540 | 30 | 46 | |||||||||||||||

Federal funds sold and securities purchased under agreements to resell | 3,221 | 418 | 790 | 542 | 949 | |||||||||||||||

Trading account assets | 1,109 | 1,348 | 1,050 | 1,268 | 1,483 | |||||||||||||||

Securities available for sale | 19,681 | 20,970 | 18,850 | 17,633 | 17,725 | |||||||||||||||

Securities held to maturity | 43 | 45 | 47 | 50 | 48 | |||||||||||||||

Loans held for sale | 1,932 | 1,956 | 1,282 | 1,054 | 677 | |||||||||||||||

Loans, net of unearned income | 96,149 | 95,686 | 97,419 | 98,712 | 98,267 | |||||||||||||||

Allowance for loan losses | (2,282 | ) | (1,861 | ) | (1,826 | ) | (1,472 | ) | (1,472 | ) | ||||||||||

Net loans | 93,867 | 93,825 | 95,593 | 97,240 | 96,795 | |||||||||||||||

Other interest-earning assets | 829 | 849 | 897 | 587 | 534 | |||||||||||||||

Premises and equipment, net | 2,789 | 2,808 | 2,786 | 2,730 | 2,726 | |||||||||||||||

Interest receivable | 501 | 426 | 458 | 512 | 510 | |||||||||||||||

Goodwill | 5,556 | 5,551 | 5,548 | 11,529 | 11,515 | |||||||||||||||

Mortgage servicing rights (MSRs) | 202 | 161 | 161 | 263 | 271 | |||||||||||||||

Other identifiable intangible assets | 568 | 603 | 638 | 675 | 709 | |||||||||||||||

Other assets | 7,304 | 8,303 | 7,965 | 7,193 | 7,287 | |||||||||||||||

Total Assets | $ | 142,811 | $ | 141,980 | $ | 146,248 | $ | 144,292 | $ | 144,436 | ||||||||||

Liabilities and Stockholders’ Equity: | ||||||||||||||||||||

Deposits: | ||||||||||||||||||||

Non-interest-bearing | $ | 20,995 | $ | 19,988 | $ | 18,457 | $ | 18,045 | $ | 18,334 | ||||||||||

Interest-bearing | 73,731 | 73,548 | 72,447 | 71,176 | 71,570 | |||||||||||||||

Total deposits | 94,726 | 93,536 | 90,904 | 89,221 | 89,904 | |||||||||||||||

Borrowed funds: | ||||||||||||||||||||

Short-term borrowings: | ||||||||||||||||||||

Federal funds purchased and securities sold under agreements to repurchase | 2,265 | 2,828 | 3,143 | 10,427 | 8,664 | |||||||||||||||

Other short-term borrowings | 4,927 | 6,525 | 12,679 | 7,115 | 8,926 | |||||||||||||||

Total short-term borrowings | 7,192 | 9,353 | 15,822 | 17,542 | 17,590 | |||||||||||||||

Long-term borrowings | 18,238 | 18,762 | 19,231 | 14,168 | 13,319 | |||||||||||||||

Total borrowed funds | 25,430 | 28,115 | 35,053 | 31,710 | 30,909 | |||||||||||||||

Other liabilities | 3,918 | 3,512 | 3,478 | 3,656 | 3,915 | |||||||||||||||

Total Liabilities | 124,074 | 125,163 | 129,435 | 124,587 | 124,728 | |||||||||||||||

Stockholders’ equity: | ||||||||||||||||||||

Preferred stock, Series A | 3,325 | 3,316 | 3,307 | — | — | |||||||||||||||

Preferred stock, Series B | 278 | — | — | — | — | |||||||||||||||

Common stock | 12 | 7 | 7 | 7 | 7 | |||||||||||||||

Additional paid-in capital | 18,740 | 16,828 | 16,815 | 16,607 | 16,588 | |||||||||||||||

Retained earnings (deficit) | (2,169 | ) | (1,913 | ) | (1,869 | ) | 4,445 | 4,437 | ||||||||||||

Treasury stock, at cost | (1,413 | ) | (1,415 | ) | (1,425 | ) | (1,424 | ) | (1,371 | ) | ||||||||||

Accumulated other comprehensive income (loss), net | (36 | ) | (6 | ) | (22 | ) | 70 | 47 | ||||||||||||

Total Stockholders’ Equity | 18,737 | 16,817 | 16,813 | 19,705 | 19,708 | |||||||||||||||

Total Liabilities and Stockholders’ Equity | $ | 142,811 | $ | 141,980 | $ | 146,248 | $ | 144,292 | $ | 144,436 | ||||||||||

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 3

Regions Financial Corporation and Subsidiaries

Consolidated Statements of Operations (1)

(Unaudited)

| Quarter Ended | |||||||||||||||||||

($ amounts in millions, except per share data) | 6/30/09 | 3/31/09 | 12/31/08 | 9/30/08 | 6/30/08 | ||||||||||||||

Interest income on: | |||||||||||||||||||

Loans, including fees | $ | 1,073 | $ | 1,098 | $ | 1,328 | $ | 1,318 | $ | 1,375 | |||||||||

Securities: | |||||||||||||||||||

Taxable | 239 | 239 | 212 | 208 | 208 | ||||||||||||||

Tax-exempt | 5 | 7 | 9 | 11 | 10 | ||||||||||||||

Total securities | 244 | 246 | 221 | 219 | 218 | ||||||||||||||

Loans held for sale | 15 | 16 | 8 | 9 | 9 | ||||||||||||||

Federal funds sold and securities purchased under agreements to resell | 1 | 1 | 2 | 5 | 4 | ||||||||||||||

Trading account assets | 10 | 12 | 11 | 13 | 18 | ||||||||||||||

Other interest-earning assets | 8 | 6 | 11 | 5 | 6 | ||||||||||||||

Total interest income | 1,351 | 1,379 | 1,581 | 1,569 | 1,630 | ||||||||||||||

Interest expense on: | |||||||||||||||||||

Deposits | 330 | 366 | 408 | 391 | 422 | ||||||||||||||

Short-term borrowings | 16 | 20 | 69 | 102 | 85 | ||||||||||||||

Long-term borrowings | 174 | 184 | 180 | 154 | 144 | ||||||||||||||

Total interest expense | 520 | 570 | 657 | 647 | 651 | ||||||||||||||

Net interest income | 831 | 809 | 924 | 922 | 979 | ||||||||||||||

Provision for loan losses | 912 | 425 | 1,150 | 417 | 309 | ||||||||||||||

Net interest income (loss) after provision for loan losses | (81 | ) | 384 | (226 | ) | 505 | 670 | ||||||||||||

Non-interest income: | |||||||||||||||||||

Service charges on deposit accounts | 287 | 269 | 288 | 294 | 294 | ||||||||||||||

Brokerage, investment banking and capital markets | 264 | 217 | 241 | 241 | 272 | ||||||||||||||

Mortgage income | 64 | 73 | 34 | 33 | 25 | ||||||||||||||

Trust department income | 48 | 46 | 52 | 66 | 59 | ||||||||||||||

Securities gains, net | 108 | 53 | — | — | 1 | ||||||||||||||

Other | 428 | 408 | 87 | 85 | 93 | ||||||||||||||

Total non-interest income | 1,199 | 1,066 | 702 | 719 | 744 | ||||||||||||||

Non-interest expense: | |||||||||||||||||||

Salaries and employee benefits | 586 | 539 | 562 | 552 | 599 | ||||||||||||||

Net occupancy expense | 112 | 107 | 114 | 110 | 111 | ||||||||||||||

Furniture and equipment expense | 78 | 76 | 79 | 88 | 87 | ||||||||||||||

Impairment (recapture) of MSR’s | — | — | 99 | 11 | (67 | ) | |||||||||||||

Goodwill impairment | — | — | 6,000 | — | — | ||||||||||||||

Other-than-temporary impairments (2) | 69 | 3 | 13 | 9 | 1 | ||||||||||||||

Other | 386 | 333 | 406 | 358 | 410 | ||||||||||||||

Total non-interest expense (3) | 1,231 | 1,058 | 7,273 | 1,128 | 1,141 | ||||||||||||||

Income (loss) before income taxes from continuing operations | (113 | ) | 392 | (6,797 | ) | 96 | 273 | ||||||||||||

Income tax expense (benefit) | 75 | 315 | (579 | ) | 6 | 67 | |||||||||||||

Income (loss) from continuing operations | (188 | ) | 77 | (6,218 | ) | 90 | 206 | ||||||||||||

Discontinued operations: | |||||||||||||||||||

Loss from discontinued operations before income taxes | — | — | — | (18 | ) | — | |||||||||||||

Income tax benefit | — | — | — | (7 | ) | — | |||||||||||||

Loss from discontinued operations, net of tax | — | — | — | (11 | ) | — | |||||||||||||

Net income (loss) | $ | (188 | ) | $ | 77 | $ | (6,218 | ) | $ | 79 | $ | 206 | |||||||

Income (loss) from continuing operations available to common shareholders | $ | (244 | ) | $ | 26 | $ | (6,244 | ) | $ | 90 | $ | 206 | |||||||

Net income (loss) available to common shareholders | $ | (244 | ) | $ | 26 | $ | (6,244 | ) | $ | 79 | $ | 206 | |||||||

Weighted-average shares outstanding—during quarter: | |||||||||||||||||||

Basic | 876 | 693 | 693 | 696 | 696 | ||||||||||||||

Diluted | 876 | 694 | 693 | 696 | 696 | ||||||||||||||

Actual shares outstanding—end of quarter | 1,188 | 695 | 691 | 692 | 695 | ||||||||||||||

Earnings (loss) per common share (4): | |||||||||||||||||||

Basic | $ | (0.28 | ) | $ | 0.04 | $ | (9.01 | ) | $ | 0.11 | $ | 0.30 | |||||||

Diluted | $ | (0.28 | ) | $ | 0.04 | $ | (9.01 | ) | $ | 0.11 | $ | 0.30 | |||||||

Cash dividends declared per common share | $ | 0.01 | $ | 0.10 | $ | 0.10 | $ | 0.10 | $ | 0.38 | |||||||||

Taxable-equivalent net interest income from continuing operations | $ | 840 | $ | 817 | $ | 933 | $ | 931 | $ | 990 | |||||||||

| (1) | Certain amounts in the prior periods have been classified to reflect current period presentation |

| (2) | Includes $260 million of gross charges, net of $191 million noncredit related portion recognized in other comprehensive income, in 2Q09. |

| (3) | Merger-related charges total $25 million in 3Q08 and $100 million in 2Q08. See page 24 for additional detail. |

| (4) | Includes preferred stock dividends |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 4

Regions Financial Corporation and Subsidiaries

Consolidated Statements of Operations (1)

(Unaudited)

($ amounts in millions, except per share data) | Six Months Ended June 30 | |||||||

| 2009 | 2008 | |||||||

Interest income on: | ||||||||

Loans, including fees | $ | 2,171 | $ | 2,904 | ||||

Securities: | ||||||||

Taxable | 478 | 408 | ||||||

Tax-exempt | 12 | 20 | ||||||

Total securities | 490 | 428 | ||||||

Loans held for sale | 31 | 18 | ||||||

Federal funds sold and securities purchased under agreements to resell | 2 | 11 | ||||||

Trading account assets | 22 | 39 | ||||||

Other interest-earning assets | 14 | 13 | ||||||

Total interest income | 2,730 | 3,413 | ||||||

Interest expense on: | ||||||||

Deposits | 696 | 925 | ||||||

Short-term borrowings | 36 | 198 | ||||||

Long-term borrowings | 358 | 293 | ||||||

Total interest expense | 1,090 | 1,416 | ||||||

Net interest income | 1,640 | 1,997 | ||||||

Provision for loan losses | 1,337 | 490 | ||||||

Net interest income after provision for loan losses | 303 | 1,507 | ||||||

Non-interest income: | ||||||||

Service charges on deposit accounts | 556 | 566 | ||||||

Brokerage, investment banking and capital markets | 481 | 545 | ||||||

Mortgage income | 137 | 71 | ||||||

Trust department income | 94 | 116 | ||||||

Securities gains, net | 161 | 92 | ||||||

Other | 836 | 262 | ||||||

Total non-interest income | 2,265 | 1,652 | ||||||

Non-interest expense: | ||||||||

Salaries and employee benefits | 1,125 | 1,242 | ||||||

Net occupancy expense | 219 | 218 | ||||||

Furniture and equipment expense | 154 | 167 | ||||||

Recapture of MSR’s | — | (25 | ) | |||||

Other-than-temporary impairments (2) | 72 | 1 | ||||||

Other | 719 | 788 | ||||||

Total non-interest expense (3) | 2,289 | 2,391 | ||||||

Income (loss) before income taxes from continuing operations | 279 | 768 | ||||||

Income tax expense (benefit) | 390 | 225 | ||||||

Net income (loss) | ($111 | ) | $ | 543 | ||||

Income (loss) from continuing operations available to common shareholders | ($218 | ) | $ | 543 | ||||

Net income (loss) available to common shareholders | ($218 | ) | $ | 543 | ||||

Weighted-average shares outstanding—year-to-date: | ||||||||

Basic | 785 | 696 | ||||||

Diluted | 785 | 696 | ||||||

Actual shares outstanding—end of period | 1,188 | 695 | ||||||

Earnings (loss) per common share (4): | ||||||||

Basic | $ | (0.28 | ) | $ | 0.78 | |||

Diluted | $ | (0.28 | ) | $ | 0.78 | |||

Cash dividends declared per common share | $ | 0.11 | $ | 0.76 | ||||

Taxable equivalent net interest income from continuing operations | $ | 1,657 | $ | 2,016 | ||||

| (1) | Certain amounts in the prior periods have been classified to reflect current period presentation |

| (2) | Includes $263 million of gross charges, net of $191 million noncredit related portion recognized in other comprehensive income, in 2009. |

| (3) | Merger-related charges total $100 million in 2Q08. See page 24 for additional detail. |

| (4) | Includes preferred stock dividends |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 5

Regions Financial Corporation and Subsidiaries

Consolidated Average Daily Balances and Yield/Rate Analysis (1)

($ amounts in millions; | Quarter Ended | |||||||||||||||||||||||||||||||||||||||||||||||||

| 6/30/09 | 3/31/09 | 12/31/08 | 9/30/08 | 6/30/08 | ||||||||||||||||||||||||||||||||||||||||||||||

| Average Balance | Income/ Expense | Yield/ Rate | Average Balance | Income/ Expense | Yield/ Rate | Average Balance | Income/ Expense | Yield/ Rate | Average Balance | Income/ Expense | Yield/ Rate | Average Balance | Income/ Expense | Yield/ Rate | ||||||||||||||||||||||||||||||||||||

Assets | ||||||||||||||||||||||||||||||||||||||||||||||||||

Interest-earning assets: | ||||||||||||||||||||||||||||||||||||||||||||||||||

Federal funds sold and securities purchased under agreements to resell | $ | 508 | $ | 1 | 0.49 | % | $ | 545 | $ | 1 | 0.80 | % | $ | 608 | $ | 2 | 1.37 | % | $ | 1,000 | $ | 5 | 1.96 | % | $ | 883 | $ | 4 | 2.05 | % | ||||||||||||||||||||

Trading account assets | 1,221 | 11 | 3.58 | % | 1,234 | 13 | 4.21 | % | 1,334 | 12 | 3.50 | % | 1,348 | 14 | 4.06 | % | 1,400 | 19 | 5.53 | % | ||||||||||||||||||||||||||||||

Securities: | ||||||||||||||||||||||||||||||||||||||||||||||||||

Taxable | 19,453 | 239 | 4.92 | % | 19,160 | 239 | 5.06 | % | 17,081 | 212 | 4.92 | % | 16,962 | 208 | 4.88 | % | 16,978 | 208 | 4.93 | % | ||||||||||||||||||||||||||||||

Tax-exempt | 562 | 8 | 6.30 | % | 687 | 11 | 6.34 | % | 800 | 14 | 7.15 | % | 767 | 16 | 8.61 | % | 720 | 15 | 8.51 | % | ||||||||||||||||||||||||||||||

Loans held for sale | 1,790 | 16 | 3.41 | % | 1,819 | 15 | 3.45 | % | 823 | 8 | 4.17 | % | 563 | 9 | 6.02 | % | 650 | 9 | 5.94 | % | ||||||||||||||||||||||||||||||

Loans, net of unearned income (2) | 95,382 | 1,077 | 4.53 | % | 96,648 | 1,102 | 4.62 | % | 99,134 | 1,331 | 5.34 | % | 98,333 | 1,321 | 5.34 | % | 97,194 | 1,380 | 5.70 | % | ||||||||||||||||||||||||||||||

Other interest-earning assets | 9,700 | 8 | 0.36 | % | 5,599 | 6 | 0.40 | % | 5,604 | 11 | 0.78 | % | 582 | 5 | 3.37 | % | 636 | 6 | 3.61 | % | ||||||||||||||||||||||||||||||

Total interest-earning assets | 128,616 | $ | 1,360 | 4.24 | % | 125,692 | $ | 1,387 | 4.47 | % | 125,384 | $ | 1,590 | 5.05 | % | 119,555 | $ | 1,578 | 5.25 | % | 118,461 | $ | 1,641 | 5.57 | % | |||||||||||||||||||||||||

Allowance for loan losses | (1,917 | ) | (1,868 | ) | (1,456 | ) | (1,491 | ) | (1,371 | ) | ||||||||||||||||||||||||||||||||||||||||

Cash and due from banks | 2,269 | 2,396 | 2,499 | 2,421 | 2,425 | |||||||||||||||||||||||||||||||||||||||||||||

Other non-earning assets | 17,119 | 17,343 | 21,647 | 22,756 | 23,046 | |||||||||||||||||||||||||||||||||||||||||||||

| $ | 146,087 | $ | 143,563 | $ | 148,074 | $ | 143,241 | $ | 142,561 | |||||||||||||||||||||||||||||||||||||||||

Liabilities and Stockholders’ Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||

Interest-bearing liabilities: | ||||||||||||||||||||||||||||||||||||||||||||||||||

Savings accounts | $ | 4,029 | $ | 1 | 0.11 | % | $ | 3,804 | $ | 1 | 0.12 | % | $ | 3,691 | $ | 1 | 0.12 | % | $ | 3,774 | $ | 1 | 0.11 | % | $ | 3,810 | $ | 1 | 0.11 | % | ||||||||||||||||||||

Interest-bearing transaction accounts | 14,277 | 11 | 0.30 | % | 14,909 | 10 | 0.27 | % | 14,393 | 20 | 0.55 | % | 14,831 | 28 | 0.77 | % | 15,397 | 32 | 0.84 | % | ||||||||||||||||||||||||||||||

Money market accounts | 22,138 | 43 | 0.78 | % | 21,204 | 67 | 1.28 | % | 20,565 | 93 | 1.79 | % | 20,394 | 81 | 1.59 | % | 21,427 | 83 | 1.56 | % | ||||||||||||||||||||||||||||||

Time deposits | 33,442 | 275 | 3.30 | % | 32,894 | 288 | 3.55 | % | 31,849 | 293 | 3.65 | % | 30,168 | 273 | 3.60 | % | 29,933 | 292 | 3.93 | % | ||||||||||||||||||||||||||||||

Other | 728 | — | 0.14 | % | 530 | — | 0.07 | % | 1,262 | 1 | 0.42 | % | 1,733 | 8 | 1.71 | % | 2,523 | 14 | 2.20 | % | ||||||||||||||||||||||||||||||

Total interest-bearing deposits | 74,614 | 330 | 1.78 | % | 73,341 | 366 | 2.02 | % | 71,760 | 408 | 2.26 | % | 70,900 | 391 | 2.20 | % | 73,090 | 422 | 2.32 | % | ||||||||||||||||||||||||||||||

Federal funds purchased and securities sold under agreements to repurchase | 3,734 | 3 | 0.33 | % | 3,199 | 3 | 0.41 | % | 4,458 | 12 | 1.08 | % | 9,906 | 52 | 2.07 | % | 7,683 | 39 | 2.06 | % | ||||||||||||||||||||||||||||||

Other short-term borrowings | 7,427 | 13 | 0.71 | % | 9,023 | 17 | 0.73 | % | 14,260 | 57 | 1.59 | % | 8,014 | 50 | 2.49 | % | 7,097 | 46 | 2.61 | % | ||||||||||||||||||||||||||||||

Long-term borrowings | 18,829 | 174 | 3.70 | % | 18,958 | 184 | 3.95 | % | 16,069 | 180 | 4.47 | % | 13,364 | 154 | 4.58 | % | 12,926 | 144 | 4.46 | % | ||||||||||||||||||||||||||||||

Total interest-bearing liabilities | 104,604 | $ | 520 | 2.00 | % | 104,521 | $ | 570 | 2.21 | % | 106,547 | $ | 657 | 2.45 | % | 102,184 | $ | 647 | 2.52 | % | 100,796 | $ | 651 | 2.60 | % | |||||||||||||||||||||||||

Net interest spread | 2.24 | % | 2.26 | % | 2.60 | % | 2.73 | % | 2.97 | % | ||||||||||||||||||||||||||||||||||||||||

Non-interest-bearing deposits | 20,421 | 18,896 | 17,773 | 17,691 | 17,814 | |||||||||||||||||||||||||||||||||||||||||||||

Other liabilities | 3,567 | 3,436 | 3,344 | 3,652 | 4,169 | |||||||||||||||||||||||||||||||||||||||||||||

Stockholders’ equity | 17,495 | 16,710 | 20,410 | 19,714 | 19,782 | |||||||||||||||||||||||||||||||||||||||||||||

| $ | 146,087 | $ | 143,563 | $ | 148,074 | $ | 143,241 | $ | 142,561 | |||||||||||||||||||||||||||||||||||||||||

Net interest income/margin FTE basis | $ | 840 | 2.62 | % | $ | 817 | 2.64 | % | $ | 933 | 2.96 | % | $ | 931 | 3.10 | % | $ | 990 | 3.36 | % | ||||||||||||||||||||||||||||||

| (1) | Certain amounts in prior periods have been reclassified to reflect current period presentation |

| (2) | 3Q08 loan income includes a $43.1 million reduction for the impact of a leveraged lease tax settlement. The yield on loans adjusted to exclude the settlement would be 5.52% in 3Q08. |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 6

Regions Financial Corporation and Subsidiaries

Consolidated Average Daily Balances and Yield/Rate Analysis (1)

| Six Months Ended June 30 | ||||||||||||||||||||

| 2009 | 2008 | |||||||||||||||||||

($ amounts in millions; yields on taxable equivalent basis) | Average Balance | Revenue/ Expense | Yield/ Rate | Average Balance | Revenue/ Expense | Yield/ Rate | ||||||||||||||

Assets | ||||||||||||||||||||

Interest-earning assets: | ||||||||||||||||||||

Federal funds sold and securities purchased under agreements to resell | $ | 526 | $ | 2 | 0.65 | % | $ | 932 | $ | 11 | 2.50 | % | ||||||||

Trading account assets | 1,227 | 24 | 3.89 | % | 1,607 | 40 | 5.04 | % | ||||||||||||

Securities: | ||||||||||||||||||||

Taxable securities | 19,307 | 478 | 4.99 | % | 16,772 | 408 | 4.90 | % | ||||||||||||

Tax-exempt | 624 | 19 | 6.32 | % | 724 | 30 | 8.36 | % | ||||||||||||

Loans held for sale | 1,805 | 31 | 3.43 | % | 635 | 18 | 5.89 | % | ||||||||||||

Loans, net of unearned income | 96,012 | 2,179 | 4.58 | % | 96,456 | 2,912 | 6.07 | % | ||||||||||||

Other earning assets | 7,661 | 14 | 0.38 | % | 640 | 13 | 4.12 | % | ||||||||||||

Total interest-earning assets | 127,162 | 2,747 | 4.36 | % | 117,766 | 3,432 | 5.86 | % | ||||||||||||

Allowance for loan losses | (1,893 | ) | (1,352 | ) | ||||||||||||||||

Cash and due from banks | 2,333 | 2,586 | ||||||||||||||||||

Other non-earning assets | 17,230 | 23,218 | ||||||||||||||||||

| $ | 144,832 | $ | 142,218 | |||||||||||||||||

Liabilities and Stockholders’ Equity | ||||||||||||||||||||

Interest-bearing liabilities: | ||||||||||||||||||||

Savings accounts | $ | 3,917 | $ | 2 | 0.12 | % | $ | 3,755 | $ | 2 | 0.12 | % | ||||||||

Interest-bearing transaction accounts | 14,591 | 21 | 0.28 | % | 15,508 | 78 | 1.02 | % | ||||||||||||

Money market accounts | 21,674 | 110 | 1.03 | % | 21,721 | 199 | 1.84 | % | ||||||||||||

Time deposits | 33,169 | 563 | 3.42 | % | 29,753 | 608 | 4.11 | % | ||||||||||||

Other | 630 | — | 0.11 | % | 2,658 | 38 | 2.83 | % | ||||||||||||

Total interest-bearing deposits | 73,981 | 696 | 1.90 | % | 73,395 | 925 | 2.54 | % | ||||||||||||

Federal funds purchased and securities sold under agreements to repurchase | 3,468 | 6 | 0.37 | % | 8,218 | 107 | 2.63 | % | ||||||||||||

Other short-term borrowings | 8,221 | 30 | 0.72 | % | 6,244 | 91 | 2.93 | % | ||||||||||||

Long-term borrowings | 18,893 | 358 | 3.82 | % | 12,290 | 293 | 4.79 | % | ||||||||||||

Total interest-bearing liabilities | 104,563 | 1,090 | 2.10 | % | 100,147 | 1,416 | 2.84 | % | ||||||||||||

Net interest spread | 2.26 | % | 3.02 | % | ||||||||||||||||

Non-interest bearing deposits | 19,663 | 17,708 | ||||||||||||||||||

Other liabilities | 3,502 | 4,550 | ||||||||||||||||||

Stockholders’ equity | 17,104 | 19,813 | ||||||||||||||||||

| $ | 144,832 | $ | 142,218 | |||||||||||||||||

Net interest income/margin FTE basis | $ | 1,657 | 2.63 | % | $ | 2,016 | 3.44 | % | ||||||||||||

| (1) | Certain amounts in prior periods have been reclassified to reflect current period presentation |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 7

Regions Financial Corporation and Subsidiaries

Selected Ratios

| As of and for Quarter Ended | ||||||||||||||||||||

| 6/30/09 | 3/31/09 | 12/31/08 | 9/30/08 | 6/30/08 | ||||||||||||||||

Return on average assets* | (0.67 | %) | 0.07 | % | NM | 0.22 | % | 0.58 | % | |||||||||||

Return on average common equity* | (6.96 | %) | 0.77 | % | NM | 1.60 | % | 4.20 | % | |||||||||||

Return on average tangible common equity* (non-GAAP) | (12.34 | %) | 1.43 | % | NM | 4.20 | % | 10.98 | % | |||||||||||

Common equity per share | $ | 12.74 | $ | 19.43 | $ | 19.53 | $ | 28.48 | $ | 28.37 | ||||||||||

Tangible common book value per share (non-GAAP) | $ | 7.58 | $ | 10.57 | $ | 10.59 | $ | 10.84 | $ | 10.77 | ||||||||||

Stockholders’ equity to total assets | 13.12 | % | 11.84 | % | 11.50 | % | 13.66 | % | 13.65 | % | ||||||||||

Tangible common stockholders’ equity to tangible assets (non-GAAP) | 6.59 | % | 5.41 | % | 5.23 | % | 5.69 | % | 5.67 | % | ||||||||||

Tier 1 Common risk-based ratio (non-GAAP) (1) | 8.1 | % | 6.5 | % | 6.6 | % | 6.5 | % | 6.5 | % | ||||||||||

Tier 1 Capital (1) | 12.2 | % | 10.4 | % | 10.4 | % | 7.5 | % | 7.5 | % | ||||||||||

Total Risk-Based Capital (1) | 16.3 | % | 14.6 | % | 14.6 | % | 11.7 | % | 11.8 | % | ||||||||||

Allowance for credit losses as a percentage of loans, net of unearned income (2) | 2.43 | % | 2.02 | % | 1.95 | % | 1.57 | % | 1.56 | % | ||||||||||

Allowance for loan losses as a percentage of loans, net of unearned income | 2.37 | % | 1.94 | % | 1.87 | % | 1.49 | % | 1.50 | % | ||||||||||

Allowance for credit losses to non-performing loans | 0.89x | 1.18x | 1.81x | 1.07x | 1.09x | |||||||||||||||

Allowance for loan losses to non-performing loans | 0.87x | 1.13x | 1.74x | 1.02x | 1.04x | |||||||||||||||

Net interest margin (FTE) (3) | 2.62 | % | 2.64 | % | 2.96 | % | 3.10 | % | 3.36 | % | ||||||||||

Loans, net of unearned income, to total deposits | 101.50 | % | 102.30 | % | 107.17 | % | 110.64 | % | 109.30 | % | ||||||||||

Net charge-offs as a percentage of average loans* | 2.06 | % | 1.64 | % | 3.19 | % | 1.68 | % | 0.86 | % | ||||||||||

Non-performing assets (excluding loans 90 days past due) as a percentage of loans and other real estate | 3.55 | % | 2.43 | % | 1.76 | % | 1.79 | % | 1.65 | % | ||||||||||

Non-performing assets (excluding loans 90 days past due) as a percentage of loans and other real estate (4) | 3.17 | % | 2.02 | % | 1.33 | % | 1.66 | % | 1.65 | % | ||||||||||

Non-performing assets (including loans 90 days past due) as a percentage of loans and other real estate | 4.18 | % | 3.24 | % | 2.33 | % | 2.25 | % | 2.09 | % | ||||||||||

Non-performing assets (including loans 90 days past due) as a percentage of loans and other real estate (4) | 3.80 | % | 2.83 | % | 1.89 | % | 2.12 | % | 2.08 | % | ||||||||||

| * | Annualized |

| (1) | Current quarter Tier 1 Common, Tier 1 and Total Risk-based Capital ratios are estimated |

| (2) | The allowance for credit losses reflects the allowance related to both loans on the balance sheet and exposure related to unfunded commitments and standby letters of credit |

| (3) | 3Q08 lower by 14 bps resulting from the impact of a leveraged lease tax settlement in the quarter |

| (4) | Excludes loans held for sale |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 8

Loans (1)

Loan Portfolio - Period End Data

($ amounts in millions) | 6/30/09 | 3/31/09 | 12/31/08 | 9/30/08 | 6/30/08 | 6/30/09 vs. 3/31/09 | 6/30/09 vs. 6/30/08 | ||||||||||||||||||||||

Commercial and industrial | $ | 23,619 | $ | 22,585 | $ | 23,596 | $ | 23,511 | $ | 23,242 | $ | 1,034 | 4.6 | % | $ | 377 | 1.6 | % | |||||||||||

Commercial real estate - non-owner-occupied | 16,419 | 15,969 | 14,486 | 14,151 | 13,643 | 450 | 2.8 | % | 2,776 | 20.3 | % | ||||||||||||||||||

Commercial real estate - owner-occupied | 12,282 | 11,926 | 11,722 | 11,569 | 11,277 | 356 | 3.0 | % | 1,005 | 8.9 | % | ||||||||||||||||||

Construction - non-owner-occupied | 7,163 | 7,611 | 9,029 | 9,810 | 9,478 | (448 | ) | -5.9 | % | (2,315 | ) | -24.4 | % | ||||||||||||||||

Construction - owner-occupied | 1,060 | 1,328 | 1,605 | 1,810 | 2,523 | (268 | ) | -20.2 | % | (1,463 | ) | -58.0 | % | ||||||||||||||||

Residential first mortgage | 15,564 | 15,678 | 15,839 | 16,191 | 16,464 | (114 | ) | -0.7 | % | (900 | ) | -5.5 | % | ||||||||||||||||

Home equity | 15,796 | 16,023 | 16,130 | 15,849 | 15,447 | (227 | ) | -1.4 | % | 349 | 2.3 | % | |||||||||||||||||

Indirect | 3,099 | 3,464 | 3,854 | 4,211 | 4,145 | (365 | ) | -10.5 | % | (1,046 | ) | -25.2 | % | ||||||||||||||||

Other consumer | 1,147 | 1,102 | 1,158 | 1,610 | 2,048 | 45 | 4.1 | % | (901 | ) | -44.0 | % | |||||||||||||||||

| $ | 96,149 | $ | 95,686 | $ | 97,419 | $ | 98,712 | $ | 98,267 | $ | 463 | 0.5 | % | $ | (2,118 | ) | -2.2 | % | |||||||||||

Loan Portfolio - Average Balances

($ amounts in millions) | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | 2Q09 vs. 1Q09 | 2Q09 vs. 2Q08 | ||||||||||||||||||||||

Commercial and industrial | $ | 22,707 | $ | 23,095 | $ | 24,122 | $ | 22,916 | $ | 22,403 | $ | (388 | ) | -1.7 | % | $ | 304 | 1.4 | % | ||||||||||

Commercial real estate - non-owner-occupied | 16,081 | 15,215 | 14,313 | 13,836 | 13,521 | 866 | 5.7 | % | 2,560 | 18.9 | % | ||||||||||||||||||

Commercial real estate - owner-occupied | 11,983 | 11,773 | 11,574 | 11,371 | 11,220 | 210 | 1.8 | % | 763 | 6.8 | % | ||||||||||||||||||

Construction - non-owner-occupied | 7,474 | 8,420 | 9,802 | 9,837 | 9,476 | (946 | ) | -11.2 | % | (2,002 | ) | -21.1 | % | ||||||||||||||||

Construction - owner-occupied | 1,198 | 1,524 | 1,782 | 2,205 | 2,675 | (326 | ) | -21.4 | % | (1,477 | ) | -55.2 | % | ||||||||||||||||

Residential first mortgage | 15,593 | 15,708 | 16,005 | 16,304 | 16,578 | (115 | ) | -0.7 | % | (985 | ) | -5.9 | % | ||||||||||||||||

Home equity | 15,940 | 16,115 | 16,036 | 15,659 | 15,253 | (175 | ) | -1.1 | % | 687 | 4.5 | % | |||||||||||||||||

Indirect | 3,276 | 3,660 | 4,043 | 4,214 | 4,039 | (384 | ) | -10.5 | % | (763 | ) | -18.9 | % | ||||||||||||||||

Other consumer | 1,130 | 1,138 | 1,457 | 1,991 | 2,029 | (8 | ) | -0.7 | % | (899 | ) | -44.3 | % | ||||||||||||||||

| $ | 95,382 | $ | 96,648 | $ | 99,134 | $ | 98,333 | $ | 97,194 | $ | (1,266 | ) | -1.3 | % | $ | (1,812 | ) | -1.9 | % | ||||||||||

| (1) | Certain amounts in the prior periods have been reclassified to reflect current period presentation |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 9

Deposits (1)

Deposit Portfolio - Period End Data

($ amounts in millions) | 6/30/09 | 3/31/09 | 12/31/08 | 9/30/08 | 6/30/08 | 6/30/09 vs. 3/31/09 | 6/30/09 vs. 6/30/08 | ||||||||||||||||||||||

Customer Deposits | |||||||||||||||||||||||||||||

Interest-free deposits | $ | 20,995 | $ | 19,988 | $ | 18,457 | $ | 18,045 | $ | 18,334 | $ | 1,007 | 5.0 | % | $ | 2,661 | 14.5 | % | |||||||||||

Interest-bearing checking | 14,140 | 14,800 | 15,022 | 14,616 | 15,381 | (660 | ) | -4.5 | % | (1,241 | ) | -8.1 | % | ||||||||||||||||

Savings | 4,033 | 3,970 | 3,663 | 3,709 | 3,819 | 63 | 1.6 | % | 214 | 5.6 | % | ||||||||||||||||||

Money market - domestic | 21,571 | 19,969 | 19,471 | 17,098 | 17,993 | 1,602 | 8.0 | % | 3,578 | 19.9 | % | ||||||||||||||||||

Money market - foreign | 1,075 | 1,357 | 1,812 | 2,454 | 3,122 | (282 | ) | -20.8 | % | (2,047 | ) | -65.6 | % | ||||||||||||||||

Low-cost deposits | 61,814 | 60,084 | 58,425 | 55,922 | 58,649 | 1,730 | 2.9 | % | 3,165 | 5.4 | % | ||||||||||||||||||

Time deposits | 32,724 | 33,379 | 32,369 | 29,288 | 27,376 | (655 | ) | -2.0 | % | 5,348 | 19.5 | % | |||||||||||||||||

Total customer deposits | 94,538 | 93,463 | 90,794 | 85,210 | 86,025 | 1,075 | 1.2 | % | 8,513 | 9.9 | % | ||||||||||||||||||

Corporate Treasury Deposits | |||||||||||||||||||||||||||||

Time deposits | 188 | 73 | 110 | 1,123 | 3,086 | 115 | 156.0 | % | (2,898 | ) | -93.9 | % | |||||||||||||||||

Other | — | — | — | 2,888 | 793 | — | NM | (793 | ) | -100.0 | % | ||||||||||||||||||

Total corporate treasury deposits | 188 | 73 | 110 | 4,011 | 3,879 | 115 | 156.0 | % | (3,691 | ) | -95.2 | % | |||||||||||||||||

Total Deposits | $ | 94,726 | $ | 93,536 | $ | 90,904 | $ | 89,221 | $ | 89,904 | $ | 1,190 | 1.3 | % | $ | 4,822 | 5.4 | % | |||||||||||

| Deposit Portfolio - Average Balances | |||||||||||||||||||||||||||||

($ amounts in millions) | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | 2Q09 vs. 1Q09 | 2Q09 vs. 2Q08 | ||||||||||||||||||||||

Customer Deposits | |||||||||||||||||||||||||||||

Interest-free deposits | $ | 20,421 | $ | 18,896 | $ | 17,773 | $ | 17,691 | $ | 17,814 | $ | 1,525 | 8.1 | % | $ | 2,607 | 14.6 | % | |||||||||||

Interest-bearing checking | 14,277 | 14,909 | 14,393 | 14,831 | 15,397 | (632 | ) | -4.2 | % | (1,120 | ) | -7.3 | % | ||||||||||||||||

Savings | 4,029 | 3,804 | 3,691 | 3,774 | 3,810 | 225 | 5.9 | % | 219 | 5.7 | % | ||||||||||||||||||

Money market - domestic | 20,962 | 19,670 | 18,432 | 17,534 | 18,315 | 1,292 | 6.6 | % | 2,647 | 14.5 | % | ||||||||||||||||||

Money market - foreign | 1,176 | 1,534 | 2,133 | 2,860 | 3,112 | (358 | ) | -23.3 | % | (1,936 | ) | -62.2 | % | ||||||||||||||||

Low-cost deposits | 60,865 | 58,813 | 56,422 | 56,690 | 58,448 | 2,052 | 3.5 | % | 2,417 | 4.1 | % | ||||||||||||||||||

Time deposits | 33,221 | 32,814 | 31,442 | 27,770 | 27,248 | 407 | 1.2 | % | 5,973 | 21.9 | % | ||||||||||||||||||

Total customer deposits | 94,086 | 91,627 | 87,864 | 84,460 | 85,696 | 2,459 | 2.7 | % | 8,390 | 9.8 | % | ||||||||||||||||||

Corporate Treasury Deposits | |||||||||||||||||||||||||||||

Time deposits | 221 | 80 | 407 | 2,398 | 2,685 | 141 | 176.2 | % | (2,464 | ) | -91.8 | % | |||||||||||||||||

Other | 728 | 530 | 1,262 | 1,733 | 2,523 | 198 | 37.6 | % | (1,795 | ) | -71.1 | % | |||||||||||||||||

Total corporate treasury deposits | 949 | 610 | 1,669 | 4,131 | 5,208 | 339 | 55.7 | % | (4,259 | ) | -81.8 | % | |||||||||||||||||

Total Deposits | $ | 95,035 | $ | 92,237 | $ | 89,533 | $ | 88,591 | $ | 90,904 | $ | 2,798 | 3.0 | % | $ | 4,131 | 4.5 | % | |||||||||||

| (1) | Certain amounts in the prior periods have been reclassified to reflect current period presentation |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 10

Pre-Tax Pre-Provision Net Revenue (“PPNR”) (1)

($ amounts in millions) | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | 2Q09 vs. 1Q09 | 2Q09 vs. 2Q08 | ||||||||||||||||||||||||||

Net Interest Income | $ | 831 | $ | 809 | $ | 924 | $ | 922 | $ | 979 | 22 | 2.7 | % | $ | (148 | ) | -15.1 | % | |||||||||||||||

Non-Interest Income | 1,199 | 1,066 | 702 | 719 | 744 | 133 | 12.5 | % | 455 | 61.2 | % | ||||||||||||||||||||||

Total Revenue | 2,030 | 1,875 | 1,626 | 1,641 | 1,723 | 155 | 8.3 | % | 307 | 17.8 | % | ||||||||||||||||||||||

Non-Interest Expense | 1,231 | 1,058 | 7,273 | 1,128 | 1,141 | 173 | 16.4 | % | 90 | 7.9 | % | ||||||||||||||||||||||

Pre-tax Pre-provision Net Revenue | $ | 799 | $ | 817 | $ | (5,647 | ) | $ | 513 | $ | 582 | (18 | ) | -2.2 | % | 217 | 37.3 | % | |||||||||||||||

Adjustments: | |||||||||||||||||||||||||||||||||

Securities gains, net | (108 | ) | (53 | ) | — | — | (1 | ) | (55 | ) | 103.8 | % | (107 | ) | NM | ||||||||||||||||||

Gain on sale of Visa shares | (80 | ) | — | — | — | — | (80 | ) | NM | (80 | ) | NM | |||||||||||||||||||||

Leveraged lease termination gains | (189 | ) | (323 | ) | — | — | — | 134 | -41.5 | % | (189 | ) | NM | ||||||||||||||||||||

Gain on extinguishment of debt | (61 | ) | — | — | — | — | (61 | ) | NM | (61 | ) | NM | |||||||||||||||||||||

Impairment (recapture) of MSR’s | — | — | 99 | 11 | (67 | ) | — | NM | 67 | NM | |||||||||||||||||||||||

FDIC special assessment | 64 | — | — | — | — | 64 | NM | 64 | NM | ||||||||||||||||||||||||

Securities impairment, net | 69 | 3 | 13 | 9 | 1 | 66 | NM | 68 | NM | ||||||||||||||||||||||||

Merger-related charges | — | — | — | 25 | 100 | 0 | NM | (100 | ) | NM | |||||||||||||||||||||||

Goodwill impairment | — | — | 6,000 | — | — | 0 | NM | — | NM | ||||||||||||||||||||||||

Total adjustments | (305 | ) | (373 | ) | 6,112 | 45 | 33 | 68 | -18.2 | % | (338 | ) | NM | ||||||||||||||||||||

Adjusted PPNR | $ | 494 | $ | 444 | $ | 465 | $ | 558 | $ | 615 | $ | 50 | 11.3 | % | $ | (121 | ) | -19.7 | % | ||||||||||||||

| (1) | Certain amounts in the prior periods have been reclassified to reflect current period presentation |

| • | Adjusted PPNR increased 11% linked quarter. |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 11

Non-Interest Income and Expense from Continuing Operations (1)

Non-Interest Income and Expense

Non-Interest Income

($ amounts in millions) | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | 2Q09 vs. 1Q09 | 2Q09 vs. 2Q08 | |||||||||||||||||||||||

Service charges on deposit accounts | $ | 288 | $ | 269 | $ | 288 | $ | 294 | $ | 294 | $ | 19 | 7.1 | % | $ | (6 | ) | -2.0 | % | |||||||||||

Brokerage, investment banking and capital markets | 263 | 217 | 241 | 241 | 272 | 46 | 21.2 | % | (9 | ) | -3.3 | % | ||||||||||||||||||

Mortgage income | 64 | 73 | 34 | 33 | 25 | (9 | ) | -12.3 | % | 39 | 156.0 | % | ||||||||||||||||||

Trust department income | 48 | 46 | 52 | 66 | 59 | 2 | 4.3 | % | (11 | ) | -18.6 | % | ||||||||||||||||||

Securities gains, net | 108 | 53 | — | — | 1 | 55 | 103.8 | % | 107 | NM | ||||||||||||||||||||

Insurance income | 27 | 28 | 26 | 26 | 27 | (1 | ) | -3.6 | % | — | NM | |||||||||||||||||||

Leveraged lease termination gains | 189 | 323 | — | — | — | (134 | ) | -41.5 | % | 189 | NM | |||||||||||||||||||

Visa shares sale gain | 80 | — | — | — | — | 80 | NM | 80 | NM | |||||||||||||||||||||

Gain on early extinguishment of debt | 61 | — | — | — | — | 61 | NM | 61 | NM | |||||||||||||||||||||

Other | 71 | 57 | 61 | 59 | 66 | 14 | 24.6 | % | 5 | 7.6 | % | |||||||||||||||||||

Total non-interest income | $ | 1,199 | $ | 1,066 | $ | 702 | $ | 719 | $ | 744 | $ | 133 | 12.5 | % | $ | 455 | 61.2 | % | ||||||||||||

| Non-Interest Expense (2) | ||||||||||||||||||||||||||||||

($ amounts in millions) | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | 2Q09 vs. 1Q09 | 2Q09 vs. 2Q08 | |||||||||||||||||||||||

Salaries and employee benefits | $ | 586 | $ | 539 | $ | 562 | $ | 527 | $ | 552 | $ | 47 | 8.7 | % | $ | 34 | 6.2 | % | ||||||||||||

Net occupancy expense | 112 | 107 | 114 | 110 | 109 | 5 | 4.7 | % | 3 | 2.8 | % | |||||||||||||||||||

Furniture and equipment expense | 78 | 76 | 79 | 88 | 82 | 2 | 2.6 | % | (4 | ) | -4.9 | % | ||||||||||||||||||

Impairment (recapture) of MSR’s | — | — | 99 | 11 | (67 | ) | — | NM | 67 | -100.0 | % | |||||||||||||||||||

Professional fees | 50 | 53 | 74 | 52 | 49 | (3 | ) | -5.7 | % | 1 | 2.0 | % | ||||||||||||||||||

Marketing expense | 20 | 17 | 21 | 23 | 19 | 3 | 17.6 | % | 1 | 5.3 | % | |||||||||||||||||||

Amortization of core deposit intangible | 30 | 31 | 32 | 33 | 34 | (1 | ) | -3.2 | % | (4 | ) | -11.8 | % | |||||||||||||||||

Amortization of MSR’s | — | — | 16 | 13 | 22 | — | NM | (22 | ) | -100.0 | % | |||||||||||||||||||

Other real estate owned expense | 24 | 26 | 32 | 44 | 20 | (2 | ) | -7.7 | % | 4 | 20.0 | % | ||||||||||||||||||

Other-than-temporary impairments, net | 69 | 3 | 13 | 9 | 1 | 66 | NM | 68 | NM | |||||||||||||||||||||

FDIC premiums - special assessment | 64 | — | — | — | — | 64 | NM | 64 | NM | |||||||||||||||||||||

FDIC premiums | 43 | 10 | 6 | 4 | 2 | 33 | NM | 41 | NM | |||||||||||||||||||||

Other | 155 | 196 | 225 | 189 | 218 | (41 | ) | -20.9 | % | (63 | ) | -28.9 | % | |||||||||||||||||

Total non-interest expense, excluding merger and goodwill impairment charges | 1,231 | 1,058 | 1,273 | 1,103 | 1,041 | 173 | 16.4 | % | 190 | 18.3 | % | |||||||||||||||||||

Merger-related charges | — | — | — | 25 | 100 | — | NM | (100 | ) | -100.0 | % | |||||||||||||||||||

Goodwill impairment charge | — | — | 6,000 | — | — | — | NM | — | NM | |||||||||||||||||||||

Total non-interest expense | $ | 1,231 | $ | 1,058 | $ | 7,273 | $ | 1,128 | $ | 1,141 | $ | 173 | 16.4 | % | $ | 90 | 7.9 | % | ||||||||||||

| (1) | Certain amounts in prior periods have been reclassified to reflect current period presentation |

| (2) | Individual expense categories are presented excluding merger-related charges and goodwill impairment, which are presented in separate line items in the above table |

| • | Service charges increased $19 million linked quarter, largely reflecting higher customer transaction volumes, new account growth and seasonality |

| • | Brokerage, investment banking and capital markets income increased 21% linked quarter, primarily reflecting strong fixed income results and an improved equity market environment |

| • | Mortgage income remained strong, declining only $9 million after a record first quarter. Refinance activity remained solid, although moderating slightly, in the second quarter with the continuation of a relatively favorable mortgage rate environment. |

| • | 2Q09 reflects both the sale of approximately $1.4 billion of agency debentures ($108 million gain) and the sale of Visa shares ($80 million gain). The proceeds from the sale of the agency debentures were reinvested in U.S. Government Agency mortgage-backed securities classified as available for sale, as part of Regions’ asset/liability management strategy. |

| • | 1Q09 securities gains reflect sale of approximately $656 million of U.S. Treasury securities with the proceeds reinvested in U.S. government agency mortgage-backed securities classified as available for sale, as part of Regions’ asset/liability management strategy |

| • | Leveraged lease termination gains reflect revenue recorded as a result of Regions unwinding certain leveraged lease transactions. These amounts totaled $189 million in 2Q09 and $323 million in 1Q09; however these amounts were offset by $196 million and $315 million in increased tax expense, respectively, resulting in a nominal impact to net income. |

| • | On January 1, 2009, Regions began accounting for mortgage servicing rights at fair market value with any changes to fair value being recorded within mortgage income. Regions also entered into derivative transactions to mitigate the impact of market value fluctuations. Therefore, beginning in 1Q09 there is no expense for MSR impairment or amortization of MSRs. |

| • | Salaries and employee benefits increased $47 million linked quarter, or 9%, mainly reflecting higher commissions and incentives tied to the increase in brokerage income. |

| • | 2Q09 non-interest expense was negatively impacted by higher FDIC insurance expenses, including a $64 million special assessment, and $69 million of securities valuation charges. |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 12

Morgan Keegan

Morgan Keegan

Summary Income Statement (excluding merger-related charges) (1)

($ amounts in millions) | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | 2Q09 vs. 1Q09 | 2Q09 vs. 2Q08 | ||||||||||||||||||||||

Revenues: | |||||||||||||||||||||||||||||

Commissions | $ | 48 | $ | 49 | $ | 56 | $ | 61 | $ | 65 | $ | (1 | ) | -2.0 | % | $ | (16 | ) | -25.0 | % | |||||||||

Principal transactions | 122 | 94 | 98 | 46 | 55 | 28 | 29.8 | % | 69 | 130.2 | % | ||||||||||||||||||

Investment banking | 56 | 33 | 43 | 41 | 71 | 22 | 64.7 | % | (15 | ) | -21.1 | % | |||||||||||||||||

Interest | 19 | 22 | 29 | 37 | 43 | (3 | ) | -14.3 | % | (9 | ) | -33.3 | % | ||||||||||||||||

Trust fees and services | 44 | 41 | 45 | 61 | 53 | 13 | 31.7 | % | (3 | ) | -5.3 | % | |||||||||||||||||

Investment advisory | 32 | 29 | 50 | 49 | 54 | 3 | 10.3 | % | (23 | ) | -41.8 | % | |||||||||||||||||

Other | 16 | 7 | 13 | 8 | 9 | — | 0.0 | % | (6 | ) | -46.2 | % | |||||||||||||||||

Total revenues | 337 | 275 | 334 | 303 | 350 | 62 | 22.5 | % | (3 | ) | -0.9 | % | |||||||||||||||||

Expenses: | |||||||||||||||||||||||||||||

Interest expense | 5 | 6 | 14 | 20 | 21 | (1 | ) | -16.7 | % | (7 | ) | -58.3 | % | ||||||||||||||||

Non-interest expense | 285 | 248 | 277 | 234 | 268 | 37 | 14.9 | % | 18 | 6.7 | % | ||||||||||||||||||

Total expenses | 290 | 254 | 291 | 254 | 289 | 36 | 14.2 | % | 11 | 3.9 | % | ||||||||||||||||||

Income before income taxes | 47 | 21 | 43 | 49 | 61 | 26 | 123.8 | % | (14 | ) | -23.0 | % | |||||||||||||||||

Income taxes | 17 | 8 | 15 | 18 | 23 | 9 | 112.5 | % | (6 | ) | -26.1 | % | |||||||||||||||||

Net income | $ | 30 | $ | 13 | $ | 28 | $ | 31 | $ | 38 | $ | 17 | 130.8 | % | $ | (8 | ) | -21.1 | % | ||||||||||

Breakout of Revenue by Division

($ amounts in millions) | Private Client | Fixed- Income Capital Markets | Equity Capital Markets | Regions MK Trust | Asset Management | Interest & Other | ||||||||||||||||||

Three months ended June 30, 2009 | ||||||||||||||||||||||||

$ amount of revenue | $ | 78 | $ | 120 | $ | 26 | $ | 49 | $ | 43 | $ | 21 | ||||||||||||

% of gross revenue | 23.2 | % | 35.5 | % | 7.6 | % | 14.6 | % | 12.7 | % | 6.4 | % | ||||||||||||

Three months ended March 31, 2009 | ||||||||||||||||||||||||

$ amount of revenue | $ | 74 | $ | 105 | $ | 12 | $ | 48 | $ | 31 | $ | 5 | ||||||||||||

% of gross revenue | 26.9 | % | 38.4 | % | 4.5 | % | 17.4 | % | 11.4 | % | 1.4 | % | ||||||||||||

Six months ended June 30, 2009 | ||||||||||||||||||||||||

$ amount of revenue | $ | 152 | $ | 225 | $ | 38 | $ | 97 | $ | 74 | $ | 26 | ||||||||||||

% of gross revenue | 24.8 | % | 36.8 | % | 6.2 | % | 15.9 | % | 12.1 | % | 4.2 | % | ||||||||||||

Six months ended June 30, 2008 | ||||||||||||||||||||||||

$ amount of revenue | $ | 176 | $ | 187 | $ | 81 | $ | 111 | $ | 85 | $ | 64 | ||||||||||||

% of gross revenue | 25.0 | % | 26.6 | % | 11.5 | % | 15.8 | % | 12.1 | % | 9.0 | % | ||||||||||||

| (1) | Certain amounts in the prior periods have been reclassified to reflect current period presentation |

| • | Fixed Income Capital Markets revenue remained strong, improving on a linked quarter basis due to a larger volume of deals brought to the market |

| • | Equity Capital Markets revenue benefited in 2Q09 from an increase of market activity and the recent addition of Revolution Partners |

| • | 48,300 new accounts opened year-to-date, up 26 percent compared to the previous six months |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 13

Credit Quality (1)

Credit Quality

| As of and for Quarter Ended | ||||||||||||||||||||

($ in millions) | 6/30/09 | 3/31/09 | 12/31/08 | 9/30/08 | 6/30/08 | |||||||||||||||

Allowance for credit losses (ACL) | $ | 2,335 | $ | 1,935 | $ | 1,900 | $ | 1,546 | $ | 1,536 | ||||||||||

Provision for loan losses | $ | 912 | $ | 425 | $ | 1,150 | $ | 417 | $ | 309 | ||||||||||

Provision for unfunded credit losses | $ | (21 | ) | $ | — | $ | (1 | ) | $ | 9 | $ | 9 | ||||||||

Net loans charged-off:* | ||||||||||||||||||||

Commercial and industrial | $ | 84 | $ | 58 | $ | 73 | $ | 51 | $ | 26 | ||||||||||

Commercial real estate - non-owner-occupied | 90 | 87 | 245 | 50 | 23 | |||||||||||||||

Commercial real estate - owner-occupied | 15 | 12 | 32 | 9 | 9 | |||||||||||||||

Construction - non-owner-occupied | 111 | 66 | 301 | 194 | 46 | |||||||||||||||

Construction - owner-occupied | 3 | 4 | 4 | 5 | — | |||||||||||||||

Residential first mortgage | 51 | 39 | 41 | 18 | 12 | |||||||||||||||

Home equity | 113 | 95 | 69 | 63 | 73 | |||||||||||||||

Indirect | 11 | 16 | 15 | 10 | 8 | |||||||||||||||

Other consumer | 13 | 13 | 16 | 16 | 12 | |||||||||||||||

Total | $ | 491 | $ | 390 | $ | 796 | $ | 416 | $ | 209 | ||||||||||

Net loan charge-offs as a % of average loans, annualized* | ||||||||||||||||||||

Commercial and industrial | 1.49 | % | 1.02 | % | 1.20 | % | 0.89 | % | 0.47 | % | ||||||||||

Commercial real estate - non-owner-occupied | 2.23 | % | 2.30 | % | 6.80 | % | 1.45 | % | 0.68 | % | ||||||||||

Commercial real estate - owner-occupied | 0.51 | % | 0.42 | % | 1.10 | % | 0.31 | % | 0.32 | % | ||||||||||

Construction - non-owner-occupied | 5.94 | % | 3.18 | % | 12.20 | % | 7.83 | % | 1.95 | % | ||||||||||

Construction - owner-occupied | 1.00 | % | 1.06 | % | 0.89 | % | 0.90 | % | 0.00 | % | ||||||||||

Residential first mortgage | 1.31 | % | 1.02 | % | 1.05 | % | 0.45 | % | 0.28 | % | ||||||||||

Home equity | 2.85 | % | 2.38 | % | 1.72 | % | 1.59 | % | 1.94 | % | ||||||||||

Indirect | 1.31 | % | 1.74 | % | 1.43 | % | 0.96 | % | 0.80 | % | ||||||||||

Other consumer | 4.78 | % | 4.70 | % | 4.38 | % | 3.21 | % | 2.33 | % | ||||||||||

Total | 2.06 | % | 1.64 | % | 3.19 | % | 1.68 | % | 0.86 | % | ||||||||||

Non-accrual loans | $ | 2,618 | $ | 1,641 | $ | 1,052 | $ | 1,441 | $ | 1,410 | ||||||||||

Foreclosed properties | 439 | 294 | 243 | 201 | 211 | |||||||||||||||

Non-performing assets, excluding loans held for sale | $ | 3,057 | $ | 1,935 | $ | 1,295 | $ | 1,642 | $ | 1,621 | ||||||||||

Non-performing assets held for sale | 371 | 393 | 423 | 129 | 8 | |||||||||||||||

Non-performing assets (NPAs) | $ | 3,428 | $ | 2,328 | $ | 1,718 | $ | 1,771 | $ | 1,629 | ||||||||||

Loans past due > 90 days* | $ | 613 | $ | 782 | $ | 554 | $ | 457 | $ | 432 | ||||||||||

Restructured loans not included in categories above | $ | 1,178 | $ | 737 | $ | 455 | $ | 139 | $ | 102 | ||||||||||

Credit Ratios: | ||||||||||||||||||||

ACL/Loans, net | 2.43 | % | 2.02 | % | 1.95 | % | 1.57 | % | 1.56 | % | ||||||||||

ALL/Loans, net | 2.37 | % | 1.94 | % | 1.87 | % | 1.49 | % | 1.50 | % | ||||||||||

NPAs (ex. 90+ past due)/Loans and foreclosed properties | 3.55 | % | 2.43 | % | 1.76 | % | 1.79 | % | 1.65 | % | ||||||||||

NPAs (ex. 90+ past due)/Loans and foreclosed properties - excludes loans held for sale | 3.17 | % | 2.02 | % | 1.33 | % | 1.66 | % | 1.65 | % | ||||||||||

NPAs (inc. 90+ past due)/Loans and foreclosed properties | 4.18 | % | 3.24 | % | 2.33 | % | 2.25 | % | 2.09 | % | ||||||||||

NPAs (inc. 90+ past due)/Loans and foreclosed properties - excludes loans held for sale | 3.80 | % | 2.83 | % | 1.89 | % | 2.12 | % | 2.08 | % | ||||||||||

| * | See pages 14-17 for loan portfolio (risk view) breakout |

Allowance for Credit Losses

($ amounts in millions) | Six Months Ended June 30 | |||||||

| 2009 | 2008 | |||||||

Balance at beginning of year | $ | 1,900 | $ | 1,379 | ||||

Net loans charged-off | (881 | ) | (335 | ) | ||||

Allowance allocated to sold loans | — | (5 | ) | |||||

Provision for loan losses | 1,337 | 490 | ||||||

Provision for unfunded credit commitments | (21 | ) | 7 | |||||

Balance at end of period | $ | 2,335 | $ | 1,536 | ||||

Components: | ||||||||

Allowance for loan losses | $ | 2,282 | $ | 1,471 | ||||

Reserve for unfunded credit commitments | 53 | 65 | ||||||

Allowance for credit losses | $ | 2,335 | $ | 1,536 | ||||

| (1) | Certain amounts in prior periods have been reclassified to reflect current period presentation |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 14

Loan Portfolio - Risk View

Total Loan Portfolio

($ in millions) | Ending Balance | % of Total Loans | ||||||||||||||||||||||||||||

| 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | |||||||||||||||||||||

Commercial | ||||||||||||||||||||||||||||||

Commercial and Industrial/Leases | $ | 20,003 | $ | 18,853 | $ | 19,581 | $ | 19,221 | $ | 18,953 | 21 | % | 20 | % | 20 | % | 19 | % | 19 | % | ||||||||||

Commercial Real Estate - Owner-Occupied Mortgages | 5,573 | 5,147 | 4,780 | 4,646 | 4,612 | 6 | % | 5 | % | 5 | % | 5 | % | 5 | % | |||||||||||||||

Total Commercial | 25,576 | 24,000 | 24,361 | 23,867 | 23,565 | 27 | % | 25 | % | 25 | % | 24 | % | 24 | % | |||||||||||||||

Commercial Real Estate | ||||||||||||||||||||||||||||||

CRE - Non-Owner-Occupied Mortgages | 13,034 | 12,425 | 10,732 | 10,306 | 9,780 | 14 | % | 13 | % | 11 | % | 11 | % | 9 | % | |||||||||||||||

Non-Owner Occupied Construction | 6,961 | 7,316 | 8,624 | 9,325 | 8,887 | 7 | % | 8 | % | 9 | % | 10 | % | 10 | % | |||||||||||||||

Owner Occupied Construction | 807 | 1,023 | 1,235 | 1,353 | 1,971 | 1 | % | 1 | % | 1 | % | 1 | % | 2 | % | |||||||||||||||

Construction | 7,768 | 8,339 | 9,859 | 10,678 | 10,859 | 8 | % | 9 | % | 10 | % | 11 | % | 11 | % | |||||||||||||||

Total Commercial Real Estate | 20,802 | 20,765 | 20,591 | 20,984 | 20,639 | 22 | % | 22 | % | 21 | % | 22 | % | 21 | % | |||||||||||||||

Business and Community Banking | ||||||||||||||||||||||||||||||

Commercial and Industrial | 3,616 | 3,732 | 4,015 | 4,290 | 4,289 | 4 | % | 4 | % | 4 | % | 4 | % | 4 | % | |||||||||||||||

Commercial Real Estate - Owner-Occupied Mortgages | 6,709 | 6,779 | 6,942 | 6,923 | 6,665 | 7 | % | 7 | % | 7 | % | 7 | % | 7 | % | |||||||||||||||

CRE - Non-Owner-Occupied Mortgages | 3,385 | 3,543 | 3,754 | 3,845 | 3,863 | 4 | % | 4 | % | 4 | % | 4 | % | 4 | % | |||||||||||||||

Non-Owner Occupied Construction | 202 | 295 | 405 | 485 | 591 | 0 | % | 0 | % | 0 | % | 0 | % | 0 | % | |||||||||||||||

Owner Occupied Construction | 253 | 305 | 370 | 457 | 552 | 0 | % | 0 | % | 0 | % | 0 | % | 0 | % | |||||||||||||||

Construction | 455 | 600 | 775 | 942 | 1,143 | 0 | % | 1 | % | 1 | % | 1 | % | 1 | % | |||||||||||||||

Total Business and Community Banking | 14,165 | 14,654 | 15,486 | 16,000 | 15,960 | 15 | % | 15 | % | 16 | % | 16 | % | 16 | % | |||||||||||||||

Residential First Mortgage | ||||||||||||||||||||||||||||||

Alt-A | 2,359 | 2,451 | 2,549 | 2,615 | 2,660 | 2 | % | 2 | % | 2 | % | 2 | % | 3 | % | |||||||||||||||

Residential First Mortgage | 13,205 | 13,227 | 13,290 | 13,576 | 13,804 | 14 | % | 14 | % | 14 | % | 14 | % | 14 | % | |||||||||||||||

Total Residential First Mortgage | 15,564 | 15,678 | 15,839 | 16,191 | 16,464 | 16 | % | 16 | % | 16 | % | 16 | % | 17 | % | |||||||||||||||

Consumer | ||||||||||||||||||||||||||||||

Home Equity Lending | 15,796 | 16,023 | 16,130 | 15,849 | 15,447 | 16 | % | 17 | % | 17 | % | 16 | % | 16 | % | |||||||||||||||

Indirect Lending | 3,099 | 3,464 | 3,854 | 4,211 | 4,145 | 3 | % | 4 | % | 4 | % | 4 | % | 4 | % | |||||||||||||||

Direct Lending | 786 | 783 | 826 | 873 | 928 | 1 | % | 1 | % | 1 | % | 1 | % | 1 | % | |||||||||||||||

Other Consumer | 361 | 319 | 332 | 737 | 1,120 | 0 | % | 0 | % | 0 | % | 1 | % | 1 | % | |||||||||||||||

Total Other Consumer | 20,042 | 20,590 | 21,142 | 21,670 | 21,640 | 20 | % | 22 | % | 22 | % | 22 | % | 22 | % | |||||||||||||||

Total Loans | $ | 96,149 | $ | 95,686 | $ | 97,419 | $ | 98,712 | $ | 98,267 | 100 | % | 100 | % | 100 | % | 100 | % | 100 | % | ||||||||||

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 15

Loan Portfolio - Risk View

Net Charge-offs

($ in millions) | Net Charge-offs (1) | % of Loans* (1) | ||||||||||||||||||||||||||||

| 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | |||||||||||||||||||||

Commercial | ||||||||||||||||||||||||||||||

Commercial and Industrial/Leases | $ | 46 | $ | 27 | $ | 43 | $ | 28 | $ | 7 | 0.97 | % | 0.57 | % | 0.86 | % | 0.61 | % | 0.16 | % | ||||||||||

Commercial Real Estate - Owner-Occupied Mortgages | 14 | 10 | 26 | 8 | 8 | 1.06 | % | 0.86 | % | 2.21 | % | 0.72 | % | 0.70 | % | |||||||||||||||

Total Commercial | 60 | 37 | 69 | 36 | 15 | 0.99 | % | 0.63 | % | 1.11 | % | 0.63 | % | 0.27 | % | |||||||||||||||

Commercial Real Estate | ||||||||||||||||||||||||||||||

CRE - Non-Owner-Occupied Mortgages | 88 | 83 | 241 | 49 | 22 | 2.80 | % | 2.91 | % | 9.14 | % | 2.11 | % | 0.99 | % | |||||||||||||||

Non-Owner Occupied Construction | 110 | 66 | 300 | 189 | 45 | 6.08 | % | 3.30 | % | 12.77 | % | 7.52 | % | n/a | ||||||||||||||||

Owner Occupied Construction | 3 | 3 | 4 | 5 | — | 1.32 | % | 1.08 | % | 1.08 | % | 1.06 | % | n/a | ||||||||||||||||

Construction | 113 | 69 | 304 | 194 | 45 | 5.54 | % | 3.02 | % | 11.30 | % | 6.50 | % | 1.55 | % | |||||||||||||||

Total Commercial Real Estate | 201 | 152 | 545 | 243 | 67 | 3.88 | % | 2.96 | % | 10.23 | % | 4.58 | % | 1.31 | % | |||||||||||||||

Business and Community Banking | ||||||||||||||||||||||||||||||

Commercial and Industrial | 38 | 31 | 30 | 23 | 19 | 4.16 | % | 3.23 | % | 2.84 | % | 2.12 | % | 1.78 | % | |||||||||||||||

Commercial Real Estate - Owner-Occupied Mortgages | 1 | 2 | 6 | 1 | 1 | 0.08 | % | 0.11 | % | 0.36 | % | 0.06 | % | 0.07 | % | |||||||||||||||

CRE - Non-Owner-Occupied Mortgages | 2 | 4 | 4 | 1 | 1 | 0.15 | % | 0.39 | % | 0.35 | % | 0.15 | % | 0.06 | % | |||||||||||||||

Non-Owner Occupied Construction | 1 | — | 1 | 5 | 1 | 1.13 | % | 0.45 | % | 0.67 | % | 2.76 | % | n/a | ||||||||||||||||

Owner Occupied Construction | — | 1 | — | — | — | 0.55 | % | 0.99 | % | 0.34 | % | 0.10 | % | n/a | ||||||||||||||||

Construction | 1 | 1 | 1 | 5 | 1 | 0.82 | % | 0.72 | % | 0.51 | % | 1.38 | % | 0.30 | % | |||||||||||||||

Total Business and Community Banking | 42 | 38 | 41 | 30 | 22 | 1.16 | % | 1.01 | % | 1.02 | % | 0.75 | % | 0.55 | % | |||||||||||||||

Residential First Mortgage | ||||||||||||||||||||||||||||||

Alt-A | 17 | 13 | 6 | 4 | 3 | 2.91 | % | 2.20 | % | 1.03 | % | 0.60 | % | 0.45 | % | |||||||||||||||

Residential First Mortgage | 34 | 26 | 35 | 14 | 9 | 1.02 | % | 0.80 | % | 1.05 | % | 0.42 | % | 0.25 | % | |||||||||||||||

Total Residential First Mortgage | 51 | 39 | 41 | 18 | 12 | 1.31 | % | 1.02 | % | 1.05 | % | 0.45 | % | 0.28 | % | |||||||||||||||

Consumer | ||||||||||||||||||||||||||||||

Home Equity Lending | 113 | 95 | 69 | 63 | 73 | 2.85 | % | 2.38 | % | 1.72 | % | 1.59 | % | 1.94 | % | |||||||||||||||

Indirect Lending | 11 | 16 | 15 | 10 | 8 | 1.31 | % | 1.74 | % | 1.43 | % | 0.96 | % | 0.80 | % | |||||||||||||||

Direct Lending | 3 | 2 | 3 | 3 | 3 | 1.59 | % | 1.14 | % | 1.61 | % | 1.33 | % | 1.11 | % | |||||||||||||||

Other Consumer | 10 | 11 | 13 | 13 | 9 | 12.00 | % | 13.43 | % | 8.24 | % | 4.76 | % | 3.41 | % | |||||||||||||||

Total Other Consumer | 137 | 124 | 100 | 89 | 93 | 2.71 | % | 2.40 | % | 1.85 | % | 1.62 | % | 1.76 | % | |||||||||||||||

Total Loans | $ | 491 | $ | 390 | $ | 796 | $ | 416 | $ | 209 | 2.06 | % | 1.64 | % | 3.19 | % | 1.68 | % | 0.86 | % | ||||||||||

| * | Percentage of related loan category outstandings |

| (1) | Information prior to 4Q08 does not reflect reclassifications between various Commercial Real Estate and Business and Community Banking categories |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 16

Loan Portfolio - Risk View

90+ Days Past Due Loans

| 90+ Past Due (1) | % of Loans* (1) | |||||||||||||||||||||||||||||

($ in millions) | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | ||||||||||||||||||||

Commercial | ||||||||||||||||||||||||||||||

Commercial and Industrial/Leases | $ | 5 | $ | 28 | $ | 2 | $ | 2 | $ | 4 | 0.02 | % | 0.15 | % | 0.01 | % | 0.01 | % | 0.02 | % | ||||||||||

Commercial Real Estate - Owner-Occupied | 7 | 8 | 7 | — | 2 | 0.12 | % | 0.16 | % | 0.15 | % | 0.00 | % | 0.04 | % | |||||||||||||||

Total Commercial | 12 | 36 | 9 | 2 | 6 | 0.05 | % | 0.15 | % | 0.04 | % | 0.01 | % | 0.03 | % | |||||||||||||||

Commercial Real Estate | ||||||||||||||||||||||||||||||

CRE - Non-Owner-Occupied Mortgages | 36 | 62 | 7 | 8 | 4 | 0.27 | % | 0.50 | % | 0.07 | % | 0.08 | % | 0.04 | % | |||||||||||||||

Non-Owner Occupied Construction | 12 | 29 | 11 | — | 15 | 0.17 | % | 0.40 | % | 0.13 | % | 0.00 | % | 0.17 | % | |||||||||||||||

Owner Occupied Construction | 3 | 3 | 2 | 4 | 2 | 0.38 | % | 0.29 | % | 0.16 | % | 0.30 | % | 0.10 | % | |||||||||||||||

Construction | 15 | 32 | 13 | 4 | 17 | 0.19 | % | 0.38 | % | 0.13 | % | 0.04 | % | 0.16 | % | |||||||||||||||

Total Commercial Real Estate | 51 | 94 | 20 | 12 | 21 | 0.24 | % | 0.45 | % | 0.10 | % | 0.06 | % | 0.10 | % | |||||||||||||||

Business and Community Banking | ||||||||||||||||||||||||||||||

Commercial and Industrial | 9 | 14 | 12 | 8 | 7 | 0.25 | % | 0.38 | % | 0.30 | % | 0.19 | % | 0.16 | % | |||||||||||||||

Commercial Real Estate - Owner-Occupied Mortgages | 11 | 15 | 6 | 5 | 6 | 0.16 | % | 0.22 | % | 0.09 | % | 0.07 | % | 0.09 | % | |||||||||||||||

CRE - Non-Owner-Occupied Mortgages | 10 | 6 | 5 | 3 | 5 | 0.29 | % | 0.18 | % | 0.13 | % | 0.08 | % | 0.13 | % | |||||||||||||||

Non-Owner Occupied Construction | 1 | 0 | 1 | 1 | — | 0.49 | % | 0.13 | % | 0.25 | % | 0.21 | % | 0.00 | % | |||||||||||||||

Owner Occupied Construction | — | 1 | — | 3 | — | 0.00 | % | 0.21 | % | 0.00 | % | 0.66 | % | 0.00 | % | |||||||||||||||

Construction | 1 | 1 | 1 | 4 | — | 0.22 | % | 0.17 | % | 0.13 | % | 0.42 | % | 0.00 | % | |||||||||||||||

Total Business and Community Banking | 30 | 36 | 24 | 20 | 18 | 0.21 | % | 0.25 | % | 0.15 | % | 0.13 | % | 0.11 | % | |||||||||||||||

Residential First Mortgage | ||||||||||||||||||||||||||||||

Alt-A | 128 | 129 | 109 | 96 | 79 | 5.43 | % | 5.26 | % | 4.28 | % | 3.67 | % | 2.97 | % | |||||||||||||||

Residential First Mortgage | 232 | 230 | 163 | 144 | 131 | 1.76 | % | 1.74 | % | 1.23 | % | 1.06 | % | 0.95 | % | |||||||||||||||

Total Residential First Mortgage | 360 | 359 | 272 | 240 | 210 | 2.32 | % | 2.29 | % | 1.72 | % | 1.48 | % | 1.28 | % | |||||||||||||||

Consumer | ||||||||||||||||||||||||||||||

Home Equity Lending | 148 | 244 | 214 | 173 | 167 | 0.94 | % | 1.52 | % | 1.33 | % | 1.09 | % | 1.08 | % | |||||||||||||||

Indirect Lending | 5 | 6 | 8 | 4 | 5 | 0.15 | % | 0.16 | % | 0.21 | % | 0.09 | % | 0.12 | % | |||||||||||||||

Direct Lending | 2 | 3 | 3 | 3 | 2 | 0.21 | % | 0.38 | % | 0.36 | % | 0.34 | % | 0.22 | % | |||||||||||||||

Other Consumer | 5 | 4 | 4 | 3 | 3 | 1.33 | % | 1.13 | % | 1.20 | % | 0.41 | % | 0.27 | % | |||||||||||||||

Total Other Consumer | 160 | 257 | 229 | 183 | 177 | 0.80 | % | 1.25 | % | 1.08 | % | 0.84 | % | 0.82 | % | |||||||||||||||

Total Loans | $ | 613 | $ | 782 | $ | 554 | $ | 457 | $ | 432 | 0.64 | % | 0.82 | % | 0.57 | % | 0.46 | % | 0.44 | % | ||||||||||

| * | Percentage of related loan category outstandings |

| (1) | Information prior to 4Q08 does not reflect reclassifications between various Commercial Real Estate and Business and Community Banking categories |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 17

Loan Portfolio - Risk View

Non-accrual Loans

| Non-accrual loans (excludes held for sale) (1) | % of Loans* (1) | |||||||||||||||||||||||||||||

($ in millions) | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | ||||||||||||||||||||

Commercial | ||||||||||||||||||||||||||||||

Commercial and Industrial/Leases | $ | 300 | $ | 187 | $ | 118 | $ | 162 | $ | 133 | 1.50 | % | 0.99 | % | 0.60 | % | 0.84 | % | 0.70 | % | ||||||||||

Commercial Real Estate - Owner-Occupied | 257 | 190 | 131 | 149 | 138 | 4.60 | % | 3.69 | % | 2.74 | % | 3.21 | % | 2.99 | % | |||||||||||||||

Total Commercial | 557 | 377 | 249 | 311 | 271 | 2.18 | % | 1.57 | % | 1.02 | % | 1.30 | % | 1.15 | % | |||||||||||||||

Commercial Real Estate | ||||||||||||||||||||||||||||||

CRE - Non-Owner-Occupied Mortgages | 759 | 437 | 261 | 353 | 275 | 5.82 | % | 3.52 | % | 2.43 | % | 3.43 | % | 2.81 | % | |||||||||||||||

Non-Owner Occupied Construction | 864 | 493 | 269 | 518 | 640 | 12.41 | % | 6.73 | % | 3.12 | % | 5.55 | % | 7.20 | % | |||||||||||||||

Owner Occupied Construction | 44 | 29 | 23 | 27 | 29 | 5.45 | % | 2.81 | % | 1.86 | % | 2.00 | % | 1.47 | % | |||||||||||||||

Construction | 908 | 522 | 292 | 546 | 669 | 11.69 | % | 6.25 | % | 2.96 | % | 5.11 | % | 6.16 | % | |||||||||||||||

Total Commercial Real Estate | 1,667 | 959 | 553 | 899 | 944 | 8.01 | % | 4.62 | % | 2.69 | % | 4.28 | % | 4.57 | % | |||||||||||||||

Business and Community Banking | ||||||||||||||||||||||||||||||

Commercial and Industrial | 83 | 73 | 57 | 53 | 49 | 2.30 | % | 1.95 | % | 1.42 | % | 1.24 | % | 1.14 | % | |||||||||||||||

Commercial Real Estate - Owner-Occupied Mortgages | 115 | 81 | 66 | 48 | 38 | 1.71 | % | 1.20 | % | 0.95 | % | 0.69 | % | 0.57 | % | |||||||||||||||

CRE - Non-Owner-Occupied Mortgages | 52 | 38 | 31 | 25 | 18 | 1.55 | % | 1.06 | % | 0.83 | % | 0.65 | % | 0.47 | % | |||||||||||||||

Non-Owner Occupied Construction | 5 | 5 | 4 | 4 | 3 | 2.32 | % | 1.65 | % | 0.99 | % | 0.82 | % | 0.51 | % | |||||||||||||||

Owner Occupied Construction | 1 | 2 | 2 | 5 | 4 | 0.47 | % | 0.54 | % | 0.54 | % | 1.09 | % | 0.72 | % | |||||||||||||||

Construction | 6 | 7 | 6 | 9 | 7 | 1.29 | % | 1.09 | % | 0.77 | % | 0.96 | % | 0.61 | % | |||||||||||||||

Total Business and Community Banking | 256 | 199 | 160 | 135 | 112 | 1.81 | % | 1.36 | % | 1.03 | % | 0.84 | % | 0.70 | % | |||||||||||||||

Residential First Mortgage | ||||||||||||||||||||||||||||||

Alt-A | 51 | 39 | 31 | 24 | 20 | 2.16 | % | 1.59 | % | 1.22 | % | 0.92 | % | 0.75 | % | |||||||||||||||

Residential First Mortgage | 85 | 63 | 55 | 70 | 50 | 0.64 | % | 0.48 | % | 0.41 | % | 0.52 | % | 0.36 | % | |||||||||||||||

Total Residential First Mortgage | 136 | 102 | 86 | 94 | 70 | 0.87 | % | 0.65 | % | 0.54 | % | 0.58 | % | 0.43 | % | |||||||||||||||

Consumer | ||||||||||||||||||||||||||||||

Home Equity Lending | 2 | 4 | 4 | 2 | 13 | 0.01 | % | 0.03 | % | 0.02 | % | 0.01 | % | 0.08 | % | |||||||||||||||

Indirect Lending | — | — | — | — | — | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | |||||||||||||||

Direct Lending | — | — | — | — | — | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | |||||||||||||||

Other Consumer | — | — | — | — | — | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | |||||||||||||||

Total Other Consumer | 2 | 4 | 4 | 2 | 13 | 0.01 | % | 0.02 | % | 0.02 | % | 0.01 | % | 0.06 | % | |||||||||||||||

Total Loans | $ | 2,618 | $ | 1,641 | $ | 1,052 | $ | 1,441 | $ | 1,410 | 2.72 | % | 1.71 | % | 1.08 | % | 1.46 | % | 1.43 | % | ||||||||||

| * | Percentage of related loan category outstandings |

| (1) | Information prior to 4Q08 does not reflect reclassifications between various Commercial Real Estate and Business and Community Banking categories |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 18

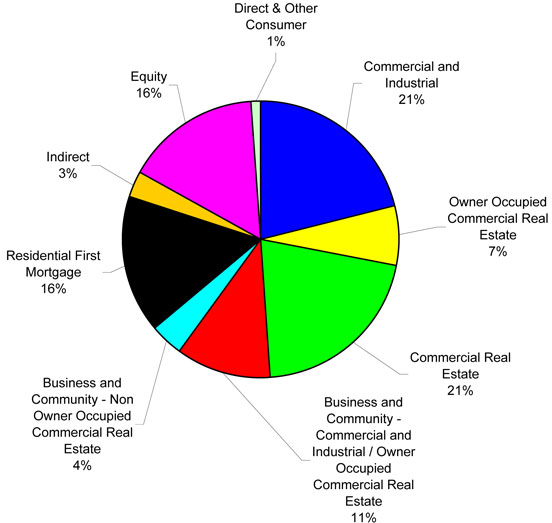

Diversified Loan Portfolio - $96.1 Billion (as of 6/30/09)

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 19

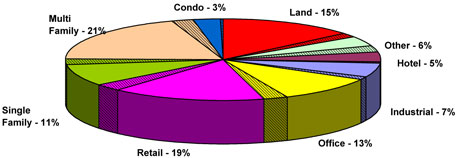

| Commercial Real Estate Non-Owner Occupied Mortgages and Construction - $23.6 Billion (as of 6/30/09) (shaded portion represents Business & Community Banking) |

|

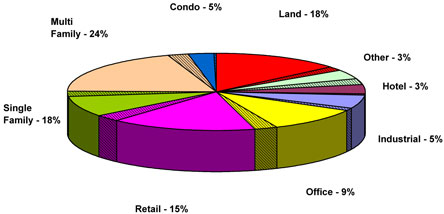

| Commercial Real Estate Non-Owner Occupied Construction - $7.2 Billion (as of 6/30/09) (shaded portion represents Business & Community Banking) |

|

| • | Portfolio well-diversified by product type |

| • | Includes $3.6 billion in Business and Community Banking Non-Owner Occupied Commercial Real Estate Loans which have different risk characteristics. They are underwritten not on a project basis but on the strength of the individual. |

| • | Proactively reducing certain concentrations |

| • | Land balances down $2.8 billion (45%) since December 2006 |

| • | Condominium balances down $1.5 billion (68%) since December 2006 |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 20

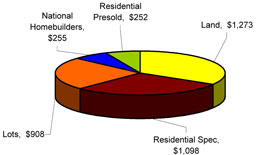

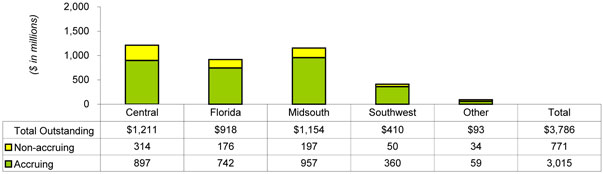

Residential Homebuilder Portfolio - $3.8 billion(as of 6/30/09)(1)

| Portfolio Breakout by Category |

| ($ in millions) |

|

| Geographic Breakout |

|

1 Central consists of Alabama, Georgia, and South Carolina

2 Midsouth consists of North Carolina, Virginia, Tennessee, Indiana, Illinois, Missouri, Iowa and Kentucky

3 Southwest consists of Louisiana, Mississippi, Texas and Arkansas |

Product Breakout

($ in millions - except for average note size)

| Lots | Residential Presold | Residential Spec | Land | National Homebuilders/Other | Total Portfolio | |||||||||||||||||||||||||

| $ | %* | $ | %* | $ | %* | $ | %* | $ | %* | $ | %* | |||||||||||||||||||

Ending Outstandings | 908 | 252 | 1,098 | 1,273 | 255 | 3,786 | ||||||||||||||||||||||||

Current Quarter Charge-offs | 25 | 10.56 | % | 3 | 4.13 | % | 18 | 6.55 | % | 36 | 10.76 | % | 2 | 2.70 | % | 84 | 8.53 | % | ||||||||||||

90+ Past Due | 3 | 0.32 | % | — | 0.00 | % | 3 | 0.31 | % | 8 | 0.59 | % | — | 0.00 | % | 14 | 0.36 | % | ||||||||||||

Non-Accruing Loans | 156 | 17.23 | % | 80 | 31.66 | % | 215 | 19.58 | % | 245 | 19.22 | % | 75 | 29.49 | % | 771 | 20.37 | % | ||||||||||||

Average Note Size (in thousands): | ||||||||||||||||||||||||||||||

Total Portfolio | 247 | — | 323 | — | 275 | — | 724 | — | 1,288 | — | 364 | — | ||||||||||||||||||

Central | 232 | — | 167 | — | 194 | — | 724 | — | 529 | — | 291 | — | ||||||||||||||||||

Florida | 502 | — | 1,181 | — | 658 | — | 1,646 | — | 285 | — | 878 | — | ||||||||||||||||||

| * | Percentage of related product outstandings; charge-offs shown as annualized, and calculated on an average outstandings balance |

| • | Average note size of the homebuilder portfolio is $363,990 |

| • | Non-accruing loans represent 20.4% of the total homebuilder portfolio with the highest concentrations in the Florida and Central (mainly Atlanta) regions |

| • | $3.8 billion residential homebuilder portfolio is a subset of the Commercial Real Estate portfolio (p. 19) with the majority of the residential homebuilder portfolio found in land and single family sectors |

| (1) | Excludes loans held for sale |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 21

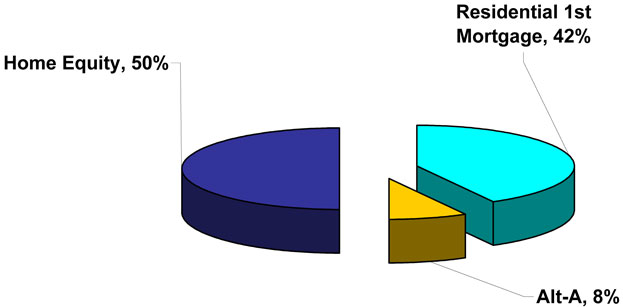

Consumer Real Estate - $31.4 billion (as of 6/30/09)

| Outstandings* | Wgtd Avg. LTV | Wgtd Avg. FICO | Avg. Loan Size | % in 1st Lien | ||||||||||

Home Equity Lending | $ | 15,796 | 74 | % | 738 | $ | 74,725 | 42 | % | |||||

Residential 1st Mortgage | 13,205 | 66 | % | 728 | 173,403 | 99 | % | |||||||

Alt-A | 2,359 | 70 | % | 705 | 178,148 | 100 | % | |||||||

Total Consumer RE Portfolio | $ | 31,360 | 70 | % | 732 | $ | 120,887 | 71 | % | |||||

| * | $ in millions |

FINANCIAL SUPPLEMENT TO

SECOND QUARTER 2009 EARNINGS RELEASE

PAGE 22

Home Equity Lending Net Charge-off Analysis

| 2Q09 | 1Q09 | 4Q08 | 3Q08 | 2Q08 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

($ in millions) | 1st Lien | 2nd Lien | Total | 1st Lien | 2nd Lien | Total | 1st Lien | 2nd Lien | Total | 1st Lien | 2nd Lien | Total | 1st Lien | 2nd Lien | Total | |||||||||||||||||||||||||||||||||||||||||||||||

Florida | Net Charge-off %* | 2.44 | % | 7.89 | % | 5.85 | % | 3.07 | % | 5.99 | % | 4.91 | % | 1.71 | % | 4.37 | % | 3.40 | % | 1.48 | % | 4.28 | % | 3.28 | % | 1.37 | % | 4.74 | % | 3.55 | % | |||||||||||||||||||||||||||||||

$ Losses | $ | 13.2 | $ | 72.0 | $ | 85.2 | $ | 16.4 | $ | 54.6 | $ | 71.0 | $ | 8.9 | $ | 39.9 | $ | 48.8 | $ | 7.2 | $ | 37.8 | $ | 45.0 | $ | 6.3 | $ | 40.2 | $ | 46.5 | ||||||||||||||||||||||||||||||||

Balance | $ | 2,171.3 | $ | 3,624.8 | $ | 5,796.1 | $ | 2,169.9 | $ | 3,677.5 | $ | 5,847.4 | $ | 2,121.6 | $ | 3,662.9 | $ | 5,784.5 | $ | 1,994.6 | $ | 3,578.8 | $ | 5,573.4 | $ | 1,922.2 | $ | 3,448.0 | $ | 5,370.2 | ||||||||||||||||||||||||||||||||

Original LTV | 65.4 | % | 76.2 | % | 72.2 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

All Other States | Net Charge-off %* | 0.63 | % | 1.50 | % | 1.11 | % | 0.52 | % | 1.27 | % | 0.93 | % | 0.52 | % | 1.00 | % | 0.79 | % | 0.39 | % | 0.93 | % | 0.69 | % | 0.60 | % | 1.47 | % | 1.08 | % | |||||||||||||||||||||||||||||||

$ Losses | $ | 7.2 | $ | 20.7 | $ | 27.9 | $ | 5.9 | $ | 17.7 | $ | 23.6 | $ | 6.0 | $ | 14.4 | $ | 20.4 | $ | 4.4 | $ | 13.1 | $ | 17.5 | $ | 6.7 | $ | 20.2 | $ | 26.9 | ||||||||||||||||||||||||||||||||

Balance | $ | 4,508.6 | $ | 5,491.6 | $ | 10,000.2 | $ | 4,569.4 | $ | 5,606.6 | $ | 10,176.0 | $ | 4,624.0 | $ | 5,721.7 | $ | 10,345.7 | $ | 4,584.2 | $ | 5,691.4 | $ | 10,275.6 | $ | 4,524.2 | $ | 5,552.2 | $ | 10,076.5 | ||||||||||||||||||||||||||||||||

Original LTV | 67.9 | % | 79.9 | % | 74.4 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Totals | Net Charge-off %* | 1.22 | % | 4.04 | % | 2.85 | % | 1.34 | % | 3.14 | % | 2.38 | % | 0.89 | % | 2.31 | % | 1.72 | % | 0.72 | % | 2.22 | % | 1.59 | % | 0.83 | % | 2.72 | % | 1.94 | % | |||||||||||||||||||||||||||||||

$ Losses | $ | 20.4 | $ | 92.6 | $ | 113.1 | $ | 22.3 | $ | 72.3 | $ | 94.6 | $ | 14.9 | $ | 54.3 | $ | 69.2 | $ | 11.6 | $ | 50.9 | $ | 62.5 | $ | 13.0 | $ | 60.4 | $ | 73.4 | ||||||||||||||||||||||||||||||||

Balance | $ | 6,679.9 | $ | 9,116.4 | $ | 15,796.3 | $ | 6,739.3 | $ | 9,284.1 | $ | 16,023.4 | $ | 6,745.6 | $ | 9,384.6 | $ | 16,130.2 | $ | 6,578.8 | $ | 9,270.2 | $ | 15,849.0 | $ | 6,446.4 | $ | 9,000.2 | $ | 15,446.7 | ||||||||||||||||||||||||||||||||

Original LTV | 67.1 | % | 78.4 | % | 73.5 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| • | 23% Florida second lien concentration driving results |

| • | Second lien, Florida net charge-offs represent 64% of 2Q09 net charge-offs but just 23% of outstanding balances |

| • | Net charge-offs in Florida approximately 5.3 times non-Florida net charge-off rate |