Exhibit 99.1

ABS East 2005

September 2005

Forward-Looking Statements

From time to time the Company may publish forward-looking statements relating to such matters as anticipated financial performance, business prospects and similar matters. The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements. In order to comply with the terms of the safe harbor, the Company notes that a variety of factors a could cause the Company’s actual results and experience to differ materially from the anticipated results or other expectations expressed in the Company’s forward-looking statements. The risks and uncertainties that may affect the operations, performance and results of the Company’s business include the following: increases in mortgage lending interest rates; adverse changes in the secondary market for mortgage loans; decline in real estate values; limited cash flow to fund operations; dependence on short-term financing facilities; concentration of operations in California, Florida, New York and Texas; the occurrence of natural disasters (including the adverse impact of hurricane Katrina); extensive government regulation; intense competition in the mortgage lending industry and the condition of the U.S. economy and financial system. For a more complete discussion of these risks and uncertainties, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations - Risk Factors” in the Company’s Annual Report on Form 10-K for the year ended December 31, 2004 and subsequent filings by the Company with the United States Securities and Exchange Commission

Page 2

Contents

Company Overview

Loan Production

Operations/Quality

Loan Servicing

Collateral Performance

Page 3

Company Overview

Page 4

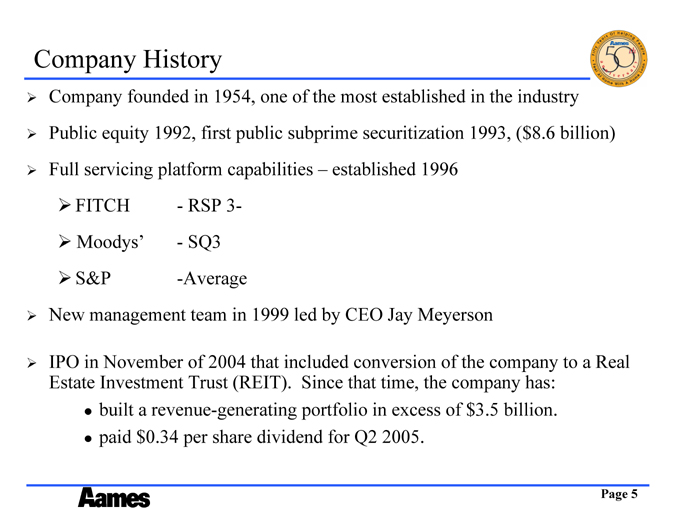

Company History

Company founded in 1954, one of the most established in the industry

Public equity 1992, first public subprime securitization 1993, ($8.6 billion)

Full servicing platform capabilities – established 1996

FITCH - RSP 3-

Moodys’ - SQ3

S&P -Average

New management team in 1999 led by CEO Jay Meyerson

IPO in November of 2004 that included conversion of the company to a Real Estate Investment Trust (REIT). Since that time, the company has:

built a revenue-generating portfolio in excess of $3.5 billion. paid $0.34 per share dividend for Q2 2005.

Page 5

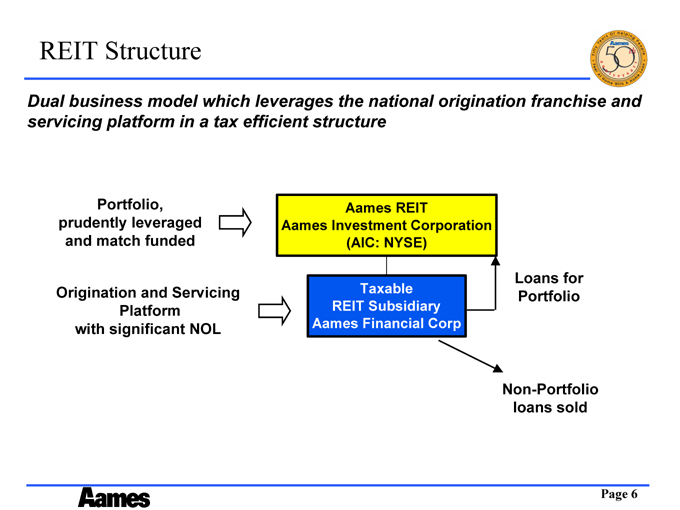

REIT Structure

Dual business model which leverages the national origination franchise and servicing platform in a tax efficient structure

Portfolio, prudently leveraged and match funded

Aames REIT

Aames Investment Corporation (AIC: NYSE)

Origination and Servicing Platform with significant NOL

Taxable REIT Subsidiary Aames Financial Corp

Loans for Portfolio

Non-Portfolio loans sold

Page 6

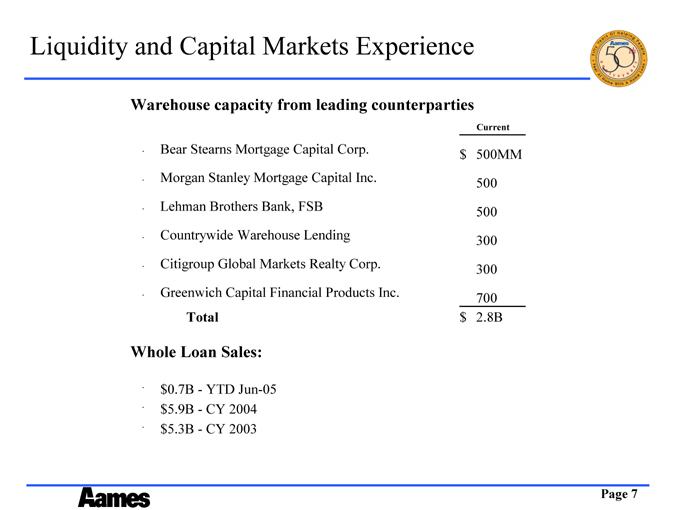

Liquidity and Capital Markets Experience

Warehouse capacity from leading counterparties

Current

Bear Stearns Mortgage Capital Corp. $500MM

Morgan Stanley Mortgage Capital Inc. 500

Lehman Brothers Bank, FSB 500

Countrywide Warehouse Lending 300

Citigroup Global Markets Realty Corp. 300

Greenwich Capital Financial Products Inc. 700

Total $2.8B

Whole Loan Sales:

$0.7B - YTD Jun-05

$5.9B - CY 2004

$5.3B - CY 2003

Page 7

Aames Direct Internet Homepage

Page 8

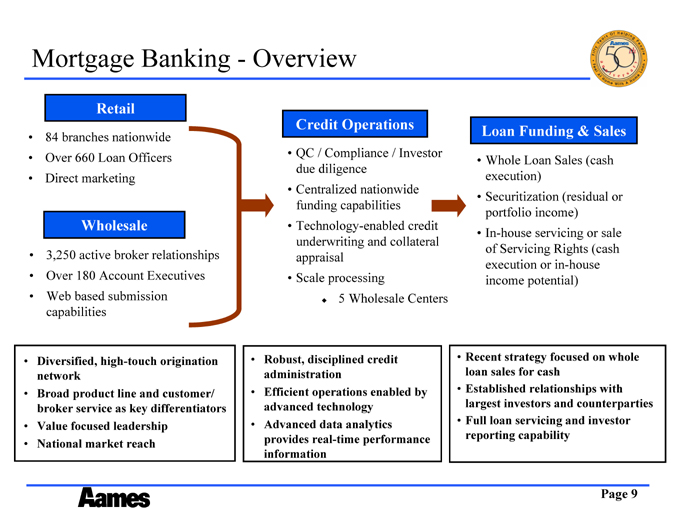

Mortgage Banking - Overview

Retail

84 branches nationwide

Over 660 Loan Officers

Direct marketing

Wholesale

3,250 active broker relationships

Over 180 Account Executives

Web based submission capabilities

Credit Operations

QC / Compliance / Investor / due diligence

Centralized nationwide funding capabilities

Technology-enabled credit underwriting and collateral appraisal

Scale processing

5 Wholesale Centers

Loan Funding & Sales

Whole Loan Sales (cash execution)

Securitization (residual or portfolio income)

In-house servicing or sale of Servicing Rights (cash execution or in-house - income potential)

Diversified, high-touch origination network

Broad product line and customer/ broker service as key differentiators

Value focused leadership

National market reach

Robust, disciplined credit administration

Efficient operations enabled by advanced technology

Advanced data analytics provides real-time performance information

Recent strategy focused on whole loan sales for cash

Established relationships with largest investors and counterparties

Full loan servicing and investor reporting capability

Page 9

Retail Overview

Aames Retail has built one of the largest independent retail franchises using sophisticated marketing, sales force management, and product / regional market optimization strategies

Retail Channel

#3 Independent sub-prime lender (#11 overall)

Sophisticated direct marketing management process

Multiple lead sources

Telemarketing lead origination

Leading-edge analytics & tracking

Direct mail targets 1.2 million households per month

Strong local presence: 84 branches with over 660 Loan Officers

Production Trends

Calendar Year Ended December YTD June

2002 2003 2004 2005

Volume ($MM) 1,776 1,987 2,414 1,140

Loans (000’s) 16.8 15.9 19.0 8.0

Avg Loan Size ($000’s) 106.0 125.1 126.9 142.1

Avg. LTV 76.4% 76.8% 76.8% 76.1%

Extensive, direct-to-consumer national retail platform

Note: Rankings from National Mortgage News 2Q05 report.

Page 10

Wholesale Overview

Aames Wholesale provides a broad product range and service to longstanding broker client franchise (tenure in AEs and customer base)

Wholesale Channel

#6 Independent wholesale originator (#17 overall) focused on serving needs of mortgage broker channel

National presence

3,250 broker relationships

Over 180 AEs

Significant market share with smaller and mid-sized brokers

No significant volume concentration in one broker

Rapidly emerging electronic/phone channel

Broker Direct 22 person Telesales unit focused on a service advantage

Aames Direct: fast pre-qualification & submission web site

High mix of Purchase business (>50%)

Production Trends

Calendar Year Ended December YTD June

2002 2003 2004 2005

Volume ($MM) 2,174 3,332 4,998 1,766

Loans (000’s) 16.0 23.8 34.1 12.8

Avg Loan Size ($000’s) 136.2 140.2 146.4 138.2

Avg. LTV 79.8% 81.5% 81.4% 81.6%

Rapidly growing wholesale network with broad coverage and established relationships

Note: Rankings from National Mortgage News 2Q05 report.

Page 11

Competitive Ranking - - Top Subprime Lenders

($ in millions)

Overall

Rank Organization Name Q2 05

1 Ameriquest Mortgage Corp. (E) (1) $17,500

2 New Century Financial Corp. $13,444

3 Countrywide Financial Corp. $10,436

4 Option One Mortgage Corp. (2) $10,041

5 Fremont Investment & Loan $9,244

6 Washington Mutual (3) $8,753

7 Wells Fargo Home Mortgage $8,520

8 WMC Mortgage Corp. (4) $8,151

9 First Franklin Financial (5) $8,086

10 HSBC Mortgage Services/Household (6) $5,087

11 GMAC-RFC $4,605

12 CitiFinancial (7) $4,313

13 BNC Mortgage, Inc. $4,255

14 Accredited Home Lenders $4,139

15 Decision One Mortgage $3,681

16 Encore Credit Corporation $3,163

17 Finance America Corporation (8) $2,752

18 Aegis Mortgage Corporation (E) $2,600

19 Chase Home Finance $2,501

20 NovaStar Mortgage, Inc. $2,339

21 Ownit Mortgage/Oakmont $2,082

22 ResMAE Mortgage Corp. $1,771

23 Fieldstone Mortgage $1,634

24 Aames Financial Corporation $1,597

25 First NLC Financial Services $1,462

Retail

Rank Organization Name Q2 05

1 Ameriquest Mortgage Corp. (E) $10,500

2 Wells Fargo Home Mortgage $6,001

3 Countrywide Financial Corp. $3,489

4 CitiFinancial $3,065

5 New Century Financial Corp. $1,313

6 Chase Home Finance $1,022

7 Option One Mortgage Corp. $926

8 Aegis Mortgage Corporation (E) $850

9 Centex Home Equity Company $843

10 H&R Block Mortgage (E) $750

11 Aames Financial Corporation $676

12 Ace Mortgage Funding, Inc. $579

13 First Franklin Financial $524

14 Delta Funding Corp. $390

15 NovaStar Mortgage, Inc. $383

16 Accredited Home Lenders $364

17 E-Loan $348

18 Equity One, Inc. $305

19 First NLC Financial Services (E) $292

20 Secured Funding $196

21 Saxon Mortgage $178

22 Fieldstone Mortgage $165

23 People’s Choice Home Loan, Inc (E) $130

24 Encore Credit Corporation $109

25 HSBC Mortgage Services/Household $99

Wholesale

Rank Organization Name Q2 05

1 New Century Financial Corp. $10,138

2 Fremont Investment & Loan $8,776

3 Option One Mortgage Corp. $8,678

4 First Franklin Financial $7,562

5 Ameriquest Mortgage Corp. (E) $7,000

6 BNC Mortgage, Inc. $4,045

7 Accredited Home Lenders $3,776

8 Countrywide Financial Corp. $3,735

9 Decision One Mortgage $3,340

10 Washington Mutual $3,063

11 Encore Credit Corporation $3,054

12 Finance America Corporation $2,703

13 Ownit Mortgage/Oakmont $2,082

14 Wells Fargo Home Mortgage $1,871

15 NovaStar Mortgage, Inc. $1,827

16 ResMAE Mortgage Corp. $1,771

17 Fieldstone Mortgage $1,469

18 Chase Home Finance $1,455

19 People’s Choice Home Loan, Inc (E) $1,170

20 MILA, Inc. $1,169

21 WMC Mortgage Corp. $1,146

22 First NLC Financial Services (E) $1,097

23 CIT Group Consumer Finance $1,027

24 Aegis Mortgage Corporation (E) $1,000

25 Aames Financial Corporation $921

Source: National Mortgage News 2Q05 Rankings

Page 12

Loan Production Overview

Page 13

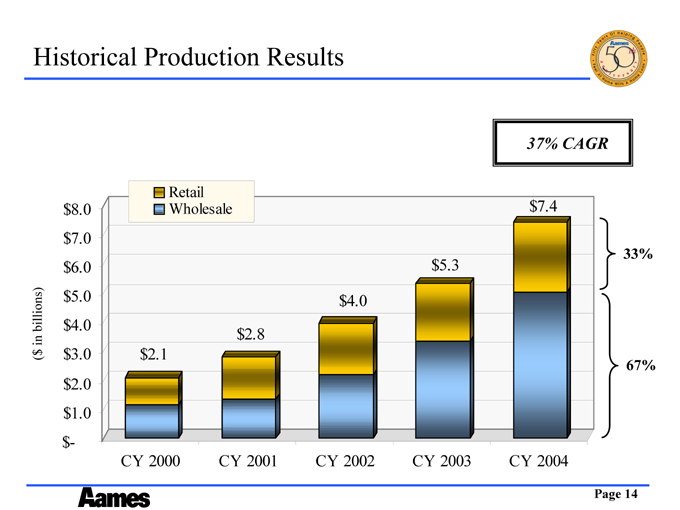

Historical Production Results

37% CAGR

($ in billions) $8.0

$7.0

$6.0

$5.0

$4.0

$3.0

$2.0

$1.0

$-

Retail

Wholesale

$2.1 $2.8 $4.0 $5.3 $7.4

33%

67%

CY 2000

CY 2001

CY 2002

CY 2003

CY 2004

Page 14

Production Profile - - YTD June 2005

Weighted Average

FICO 617

LTV 79.0%

IO 11.5%

Hybrid

Fixed

2nd Mortgage

Alt-A

79.4%

12.0%

8.5%

0.1%

Loan Purpose:

Cashout Refinance

Purchase

Rate/Term Refinance

39.0%

57.4%

3.6%

Page 15

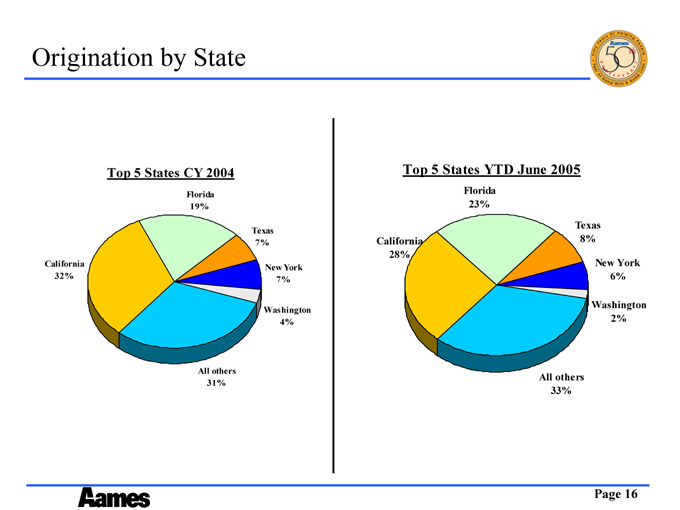

Origination by State

Top 5 States CY 2004

California 32%

Florida 19%

Texas 7%

New York 7%

Washington 4%

All others 31%

Top 5 States YTD June 2005

California 28%

Florida 23%

Texas 8%

New York 6%

Washington 2%

All others 33%

Page 16

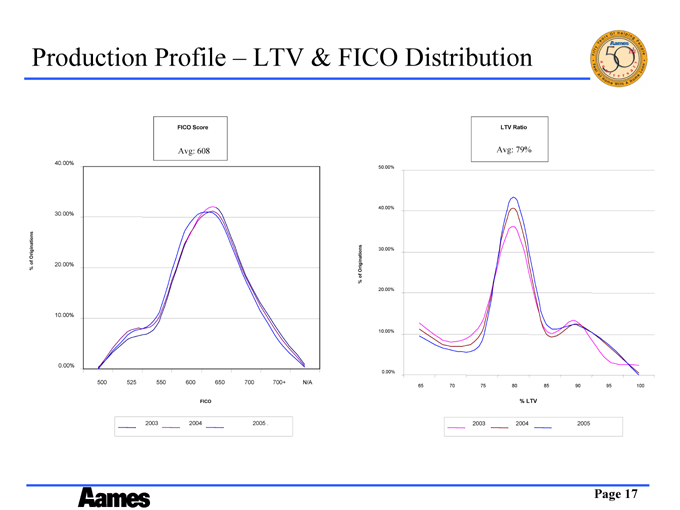

Production Profile – LTV & FICO Distribution

% of Originations

40.00%

30.00%

20.00%

10.00%

0.00%

FICO Score

Avg: 608

500

525

550

600

650

700

700+

N/A

FICO

2003

2004

2005

% of Originations

50.00%

40.00%

30.00%

20.00%

10.00%

0.00%

LTV Ratio

Avg: 79%

65 70 75 80 85 90 95 100

% LTV

2003

2004

2005

Page 17

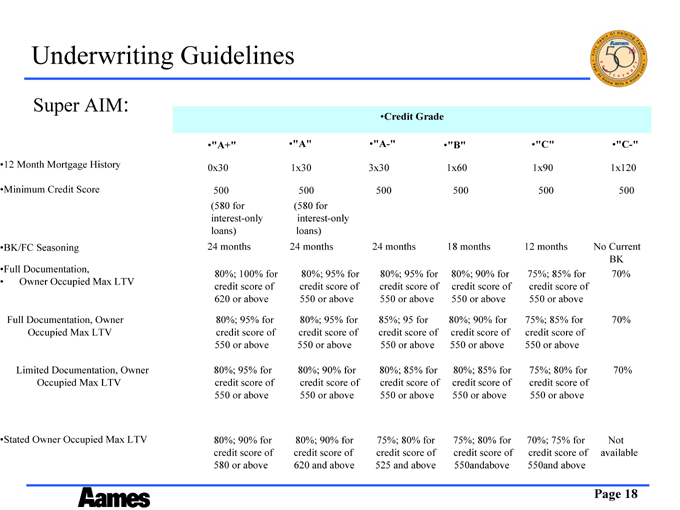

Underwriting Guidelines

Super AIM:

Credit Grade

“A+” “A” “A-” “B” “C” “C-”

12 Month Mortgage History 0x30 1x30 3x30 1x60 1x90 1x120

Minimum Credit Score 500 (580 for interest-only loans) 500 (580 for interest-only loans) 500 500 500 500

BK/FC Seasoning 24 months 24 months 24 months 18 months 12 months No Current BK

Full Documentation,

Owner Occupied Max LTV 80%; 100% for credit score of 620 or above 80%; 95% for credit score of 550 or above 80%; 95% for credit score of 550 or above 80%; 90% for credit score of 550 or above 75%; 85% for credit score of 550 or above or 70%

Full Documentation, Owner Occupied Max LTV 80%; 95% for credit score of 550 or above 80%; 95% for credit score of 550 or above 85%; 95 for credit score of 550 or above 80%; 90% for credit score of 550 or above 75%; 85% for credit score of 550 or above 70%

Limited Documentation, Owner Occupied Max LTV 80%; 95% for credit score of 550 or above 80%; 90% for credit score of 550 or above 80%; 85% for credit score of 550 or above 80%; 85% for credit score of 550 or above 75%; 80% for credit score of 550 or above 70%

Stated Owner Occupied Max LTV 80%; 90% for credit score of 580 or above 80%; 90% for credit score of 620 and above 75%; 80% for credit score of 525 and above 525 75%; 80% for credit score of 550andabove 70%; 75% for credit score of 550and above Not available

Page 18

Credit Profile of Aames Borrower

First Liens for All Channels:

2004

Credit Grade A+/A A- B C C- D Total

Total Origination Amt 84.6% 5.4% 6.5% 2.8% 0.7% - 100.0%

LTV 79.2% 77.4% 75.7% 70.5% 65.9% 71.0% 78.5%

FICO 618 560 560 550 541 503 608

% NIV or Light Doc 41.5% 33.8% 33.7% 33.2% 7.5% - 40.1%

% Multi-Family 7.3% 4.8% 4.3% 6.0% 4.9% - 6.9%

% Non-Owner 5.1% 4.1% 3.5% 3.8% 2.6% - 4.9%

YTD June 2005

Credit Grade A+/A A- B C C- Total

Total Origination Amt 86.6% 4.2% 5.9% 2.7% 0.6% 100.0%

LTV 77.6% 75.7% 75.6% 70.4% 64.9% 77.1%

FICO 624 561 559 552 544 615

% NIV or Light Doc 39.7% 34.6% 33.0% 35.5% 7.2% 38.8%

% Multi-Family 7.3% 6.4% 4.8% 5.7% 9.1% 4.1%

% Non-Owner 5.1% 3.3% 4.8% 3.7% 4.1% 5.0%

Page 19

Quality Initiatives

Page 20

Major Quality Initiatives

Collateral Evaluation

Hansen ProScore, a risk-based tool used to initially determine internal appraisal review process

All high-risk (0’s and 1’s) ProScores receive a full appraisal review

Moderate and low risk appraisals receive a full underwriter review in the Appraisal Management System (“AMS”) designed to further identify potentially high risk appraisals

Additional review of moderate and low risk (2’s, 3’s and 4’s) ProScores based on underwriter’s review

Page 21

Major Quality Initiatives

Post Funding Audit

100% post funding audit

Full compliance review with material issues referred to Loan Management Group (LMG), who specializes in remedying compliance findings

Credit and loan documentation review with material findings referred to LMG to remedy issues

Page 22

Major Quality Initiatives

Traditional Quality Control

QC Department utilizes the Cogent system to select loans for a statistical sampling. The key factor driving the sample size are the most recent 3 month defect rate and the annual production count forecast.

Additional target audits are based on observations, trends, previous audit findings, new brokers, new employees and new programs.

QC issues Resolution Alerts when fraud is discovered from a random, target or default audit.

Reports issued to Senior Management include monthly Random Audit Report, Monthly Default Report and Target Audit Summations

100% FPD and EPD audit

Page 23

Loan Servicing Overview

Page 24

Aames NLS Background/History

Loan Servicing team has been operating at Aames for 9 years

Original team formed in 1996

Transitioned to a national servicing platform

Fiserv (MortgageServ) System

Dialer, IVR and other system investments made to enhance group capability

Peaked at 60,000 loans, $4.5 billion, over 180 FTE

Page 25

Aames NLS Today

Mission: To employ the experience of the team for the benefit of our customers by providing timely, accurate and professional service and by fostering a culture that promotes the enjoyment of homeownership.

Total loans serviced: 36,052

Portfolio balance: $5,167,145,707

Team size: 96

LPE: 376

Turnover rate: 9.10%

Average Aames tenure: 6 years

Servicer Ratings:

Moody’s : SQ3

Fitch: RPS3-

S&P: Average

Page 26

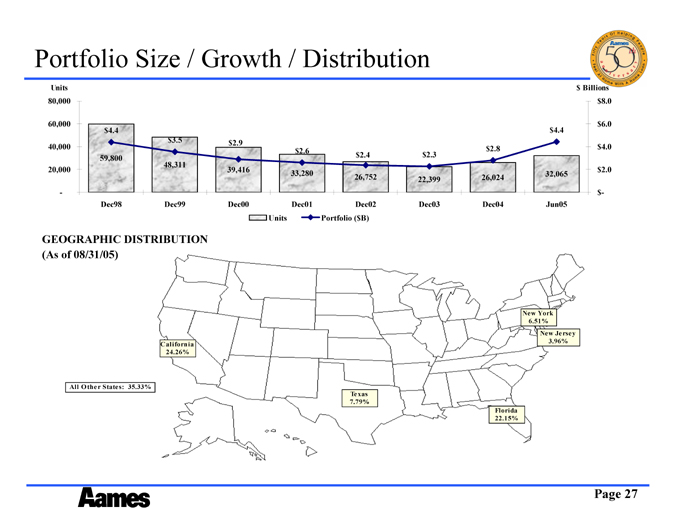

Portfolio Size / Growth / Distribution

Units

80,000 60,000 40,000 20,000 -$4.4 $4.4 $3.5 $2.9 $2.6 $2.8 59,800 $2.4 $2.3 48,311 39,416 33,280 26,752 26,024 32,065 22,399 $Billions $8.0 $6.0 $4.0 $2.0 $-

Dec98 Dec99 Dec00 Dec01 Dec02 Dec03 Dec04 Jun05

Units

Portfolio ($B)

GEOGRAPHIC DISTRIBUTION (As of 08/31/05)

All Other States: 35.33%

California 24.26%

Texas 7.79%

New York 6.51%

New Jersey 3.96%

Florida 22.15%

Page 27

Aames NLS Strengths

Experienced Management and Key Team Members

Proven Operating Strategies

Strong Customer Service Ethic

Solid Performance Results

Best-In-Class Loan Servicing Platform

Well-Positioned for Growth in REIT

Page 28

Collateral Performance

Page 29

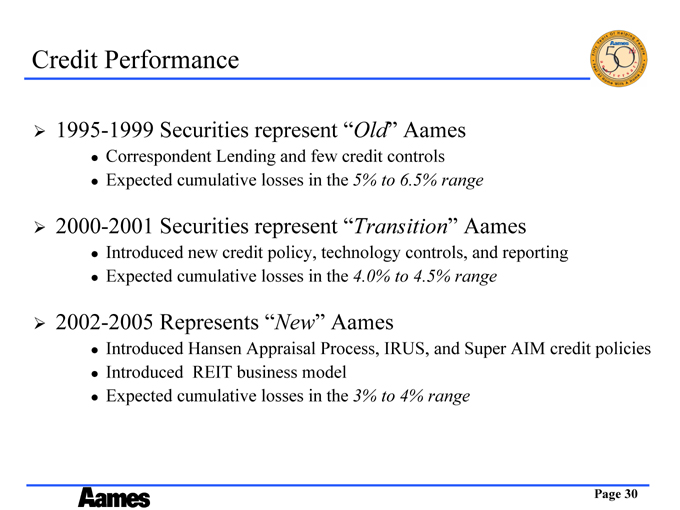

Credit Performance

1995-1999 Securities represent “Old” Aames

Correspondent Lending and few credit controls

Expected cumulative losses in the 5% to 6.5% range

2000-2001 Securities represent “Transition” Aames

Introduced new credit policy, technology controls, and reporting

Expected cumulative losses in the 4.0% to 4.5% range

2002-2005 Represents “New” Aames

Introduced Hansen Appraisal Process, IRUS, and Super AIM credit policies

Introduced REIT business model

Expected cumulative losses in the 3% to 4% range

Page 30

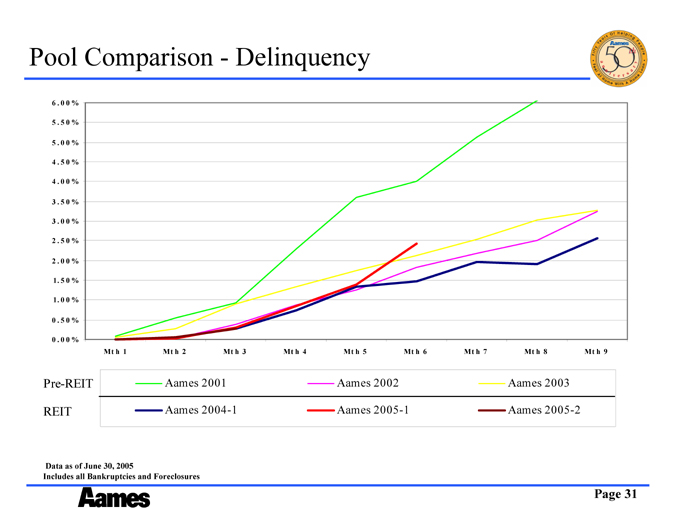

Pool Comparison - Delinquency

6.00%

5.50%

5.00% 4.50% 4.00%

3.50% 3.00% 2.50%

2.00% 1.50% 1.00%

0.50%

0.00%

Mth 1 Mth 2 Mth 3 Mth 4 Mth 5 Mth 6 Mth 7 Mth 8 Mth 9

Pre-REIT Aames 2001 Aames 2002 Aames 2003

REIT Aames 2004-1 Aames 2005-1 Aames 2005-2

Data as of June 30, 2005

Includes all Bankruptcies and Foreclosures

Page 31

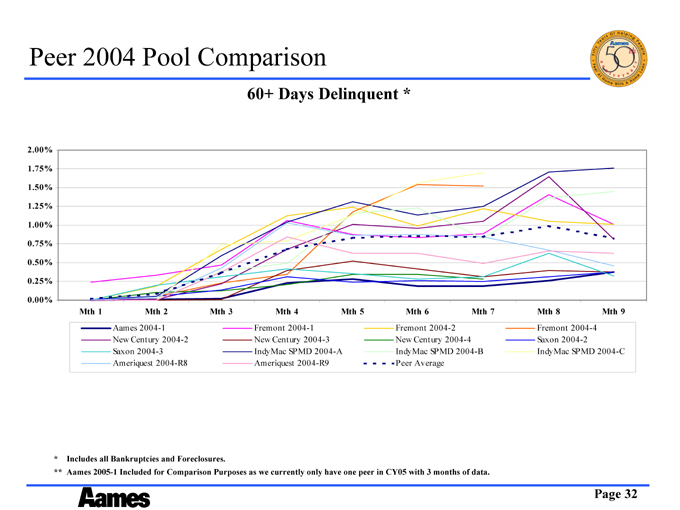

Peer 2004 Pool Comparison

60+ Days Delinquent *

2.00% 1.75% 1.50% 1.25% 1.00% 0.75% 0.50% 0.25% 0.00%

Mth 1 Mth 2 Mth 3 Mth 4 Mth 5 Mth 6 Mth 7 Mth 8 Mth 9

Aames 2004-1 Fremont 2004-1 Fremont 2004-2 Fremont 2004-4

New Century 2004-2 New Century 2004-3 New Century 2004-4 Saxon 2004-2

Saxon 2004-3 IndyMac SPMD 2004-A IndyMac SPMD 2004-B IndyMac SPMD 2004-C

Ameriquest 2004-R8 Ameriquest 2004-R9 Peer Average

* Includes all Bankruptcies and Foreclosures.

** Aames 2005-1 Included for Comparison Purposes as we currently only have one peer in CY05 with 3 months of data.

Page 32

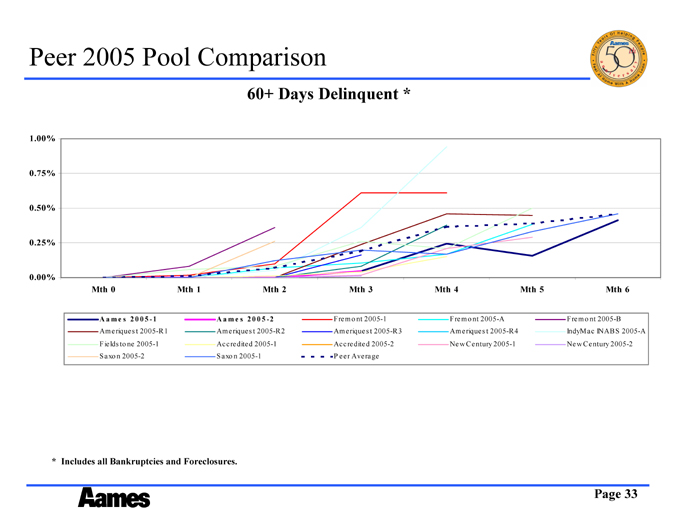

Peer 2005 Pool Comparison

60+ Days Delinquent *

1.00% 0.75% 0.50% 0.25% 0.00%

Mth 0 Mth 1 Mth 2 Mth 3 Mth 4 Mth 5 Mth 6

Aames 2005-1 Aames 2005-2 Fremo nt 2005-1 Fremo nt 2005-A Fremo nt 2005-B

Ameriquest 2005-R1 Ameriquest 2005-R2 Ameriquest 2005-R3 Ameriquest 2005-R4 IndyMac INABS 2005-A

Fieldstone 2005-1 Accredited 2005-1 Accredited 2005-2 New Century 2005-1 New Century 2005-2

Saxon 2005-2 Saxon 2005-1 Peer Average

* Includes all Bankruptcies and Foreclosures.

Page 33

Performance Reporting

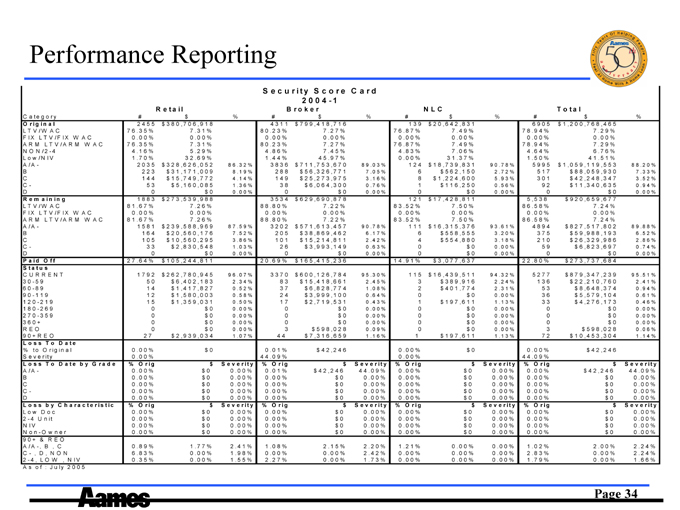

S e c u r i t y S c o r e C a r d

2 0 0 4 - 1

Retail Broker NLC Total

Category # $ % # $ % # $ % # $ %

Original 2455 $380,706,918 4311 $799,418,716 139 $20,642,831 6905 $1,200,768,465

LTV/WAC 76.35% 7.31% 80.23% 7.27% 76.87% 7.49% 78.94% 7.29%

FIXLTV/FIXWAC 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

ARMLTV/ARMWAC 76.35% 7.31% 80.23% 7.27% 76.87% 7.49% 78.94% 7.29%

NON/2 - 4 4.16% 5.29% 4.86% 7.45% 4.83% 7.06% 4.64% 6.76%

Low/NIV 1.70% 32.69% 1.44% 45.97% 0.00% 31.37% 1.50% 41.51%

A/A- 2035 $328,626,052 86.32% 3836 $711,753,670 89.03% 124 $18,739,831 90.78% 5995 $1,059,119,553 88.20%

B 223 $31,171,009 8.19% 288 $56,326,771 7.05% 6 $562,150 2.72% 517 $88,059,930 7.33%

C 144 $15,749,772 4.14% 149 $25,273,975 3.16% 8 $1,224,600 5.93% 301 $42,248,347 3.52%

C- 53 $5,160,085 1.36% 38 $6,064,300 0.76% 1 $116,250 0.56% 92 $11,340,635 0.94%

D 0 $0 0.00% 0 $0 0.00% 0 $0 0.00% 0 $0 0.00%

Remaining 1883 $273,539,988 3534 $629,690,878 121 $17,428,811 5,538 $920,659,677

LTV/WAC 81.67% 7.26% 88.80% 7.22% 83.52% 7.50% 86.58% 7.24%

FIXLTV/FIXWAC 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

ARMLTV/ARMWAC 81.67% 7.26% 88.80% 7.22% 83.52% 7.50% 86.58% 7.24%

A/A- 1581 $239,588,969 87.59% 3202 $571,613,457 90.78% 111 $16,315,376 93.61% 4894 $827,517,802 89.88%

B 164 $20,560,176 7.52% 205 $38,869,462 6.17% 6 $558,555 3.20% 375 $59,988,193 6.52%

C 105 $10,560,295 3.86% 101 $15,214,811 2.42% 4 $554,880 3.18% 210 $26,329,986 2.86%

C - 33 $2,830,548 1.03% 26 $3,993,149 0.63% 0 $0 0.00% 59 $6,823,697 0.74%

D 0 $0 0.00% 0 $0 0.00% 0 $0 0.00% 0 $0 0.00%

PaidOff 27.64% $105,244,811 20.69% $165,415,236 14.91% $3,077,637 22.80% $273,737,684

Status

CURRENT 1792 $262,780,945 96.07% 3370 $600,126,784 95.30% 115 $16,439,511 94.32% 5277 $879,347,239 95.51%

30 - 59 50 $6,402,183 2.34% 83 $15,418,661 2.45% 3 $389,916 2.24% 136 $22,210,760 2.41%

60 - 89 14 $1,417,827 0.52% 37 $6,828,774 1.08% 2 $401,774 2.31% 53 $8,648,374 0.94%

90 - 119 12 $1,580,003 0.58% 24 $3,999,100 0.64% 0 $0 0.00% 36 $5,579,104 0.61%

120 - 219 15 $1,359,031 0.50% 17 $2,719,531 0.43% 1 $197,611 1.13% 33 $4,276,173 0.46%

180 - 269 0 $0 0.00% 0 $0 0.00% 0 $0 0.00% 0 $0 0.00%

270 - 359 0 $0 0.00% 0 $0 0.00% 0 $0 0.00% 0 $0 0.00%

360+ 0 $0 0.00% 0 $0 0.00% 0 $0 0.00% 0 $0 0.00%

REO 0 $0 0.00% 3 $598,028 0.09% 0 $0 0.00% 3 $598,028 0.06%

90 + REO 27 $2,939,034 1.07% 44 $7,316,659 1.16% 1 $197,611 1.13% 72 $10,453,304 1.14%

LossToDate

% to Original 0.00% $0 0.01% $42,246 0.00% $0 0.00% $42,246

Severity 0.00% 44.09% 0.00% 44.09%

Loss To Date by Grade % Orig $ Severity % Orig $ Severity % Orig $ Severity % Orig $ Severity

A/A- 0.00% $0 0.00% 0.01% $42,246 44.09% 0.00% $0 0.00% 0.00% $42,246 44.09%

B 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00%

C 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00%

C- 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00%

D 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00%

Loss by Characteristic % Orig $ Severity % Orig $ Severity % Orig $ Severity % Orig $ Severity

Low Doc 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00%

2-4 Unit 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00%

NIV 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00%

Non-Owner 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00% 0.00% $0 0.00%

90+ & REO

A/A-, B, C 0.89% 1.77% 2.41% 1.08% 2.15% 2.20% 1.21% 0.00% 0.00% 1.02% 2.00% 2.24%

C-, D, NON 6.83% 0.00% 1.98% 0.00% 0.00% 2.42% 0.00% 0.00% 0.00% 2.83% 0.00% 2.24%

2-4, LOW, NIV 0.35% 0.00% 1.55% 2.27% 0.00% 1.73% 0.00% 0.00% 0.00% 1.79% 0.00% 1.66%

As of : July 2005

Page 34

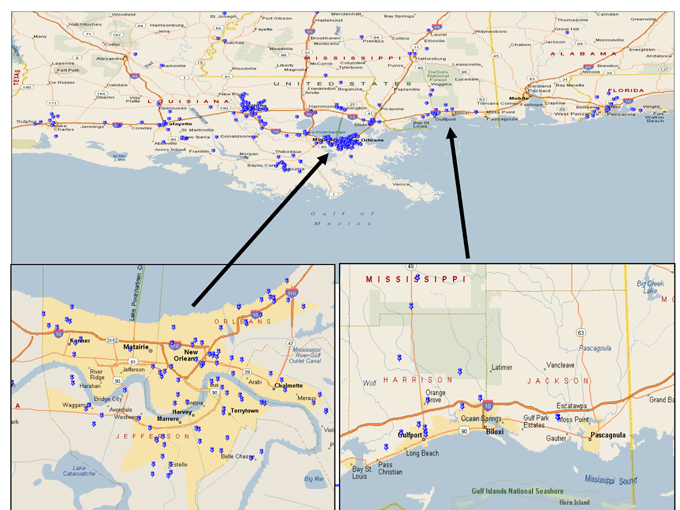

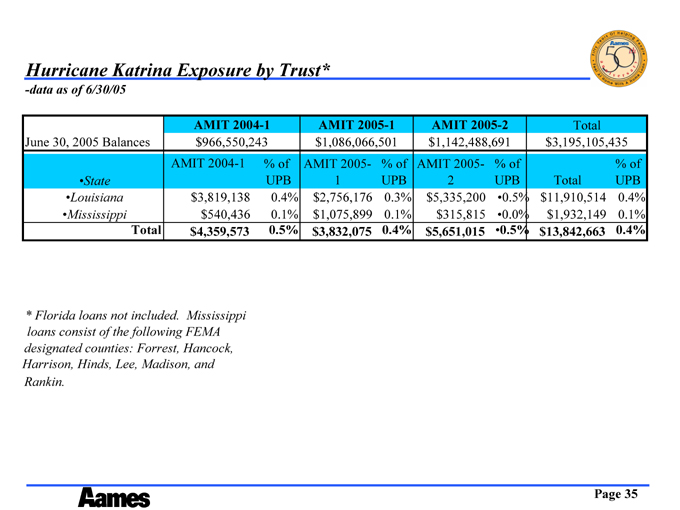

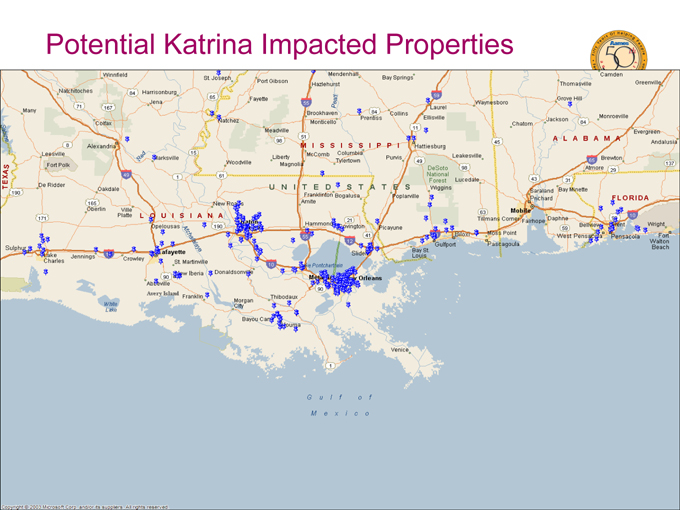

Hurricane Katrina Exposure by Trust*

data as of 6/30/05

AMIT 2004-1 AMIT 2005-1 AMIT 2005-2 Total

June 30, 2005 Balances $966,550,243 $1,086,066,501 $1,142,488,691 $3,195,105,435

AMIT 2004-1% of AMIT 2005- % of AMIT 2005- % of % of

State UPB 1 UPB 2 UPB Total UPB

Louisiana $3,819,138 0.4% $2,756,176 0.3% $5,335,200 0.5% $11,910,514 0.4%

Mississippi $540,436 0.1% $1,075,899 0.1% $315,815 0.0% $1,932,149 0.1%

Total $4,359,573 0.5% $3,832,075 0.4% $5,651,015 0.5% $13,842,663 0.4%

* Florida loans not included. Mississippi loans consist of the following FEMA designated counties: Forrest, Hancock, Harrison, Hinds, Lee, Madison, and Rankin.

Page 35

Potential Katrina Impacted Properties