UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-09997

Baird Funds, Inc.

(Exact name of registrant as specified in charter)

777 East Wisconsin Avenue

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Charles M. Weber

Robert W. Baird & Co. Incorporated

777 East Wisconsin Avenue

Milwaukee, WI 53202

(Name and address of agent for service)

1-866-442-2473

Registrant's telephone number, including area code

Date of fiscal year end: December 31, 2008

Date of reporting period: December 31, 2008

Item 1. Reports to Stockholders.

Annual Report - Baird Funds

Baird Intermediate Bond Fund

Baird Aggregate Bond Fund

Baird Intermediate Municipal Bond Fund

Baird Core Plus Bond Fund

Baird Short-Term Bond Fund

TABLE OF CONTENTS

| Page | |

| Letter to Shareholders | 1 |

| 2008 Bond Market Overview | 2 |

| Baird Intermediate Bond Fund | 6 |

| Baird Aggregate Bond Fund | 23 |

| Baird Intermediate Municipal Bond Fund | 45 |

| Baird Core Plus Bond Fund | 57 |

| Baird Short-Term Bond Fund | 74 |

| Additional Information on Fund Expenses | 87 |

| Statements of Assets and Liabilities | 89 |

| Statements of Operations | 90 |

| Statements of Changes in Net Assets | 91 |

| Financial Highlights | 96 |

| Notes to the Financial Statements | 105 |

| Report of Independent Registered Public Accounting Firm | 118 |

| Directors and Officers | 119 |

| Disclosure Regarding the Board of Directors’ Approval | |

| of the Investment Advisory Agreement for Baird Bond Funds | 121 |

| Additional Information | 124 |

This report has been prepared for shareholders and may be distributed to others only if preceded or accompanied by a current prospectus.

Cautionary Note on Analyses, Opinions and Outlooks: In this report we offer analyses and opinions on the performance of individual securities, companies, industries, sectors, markets, interest rates and governmental policies, including predictions, forecasts and outlooks regarding possible future events. These can generally be identified as such because the context of the statements may include such words as “believe,” “should,” “will,” “expects,” “anticipates,” “hopes” and words of similar effect. These statements reflect the portfolio managers’ good faith beliefs and judgments and involve risks and uncertainties, including the risk that the portfolio managers’ analyses, opinions and outlooks are or will prove to be inaccurate. It is inherently difficult to correctly assess and explain the performance of particular securities, sectors, markets, interest rate movements, governmental actions or general economic trends and conditions, and many unforeseen factors contribute to the performance of Baird Funds. Investors are, therefore, cautioned not to place undue reliance on subjective judgments contained in this report.

Baird Funds

1-866-442-2473

www.bairdfunds.com

February 28, 2009

Dear Shareholder,

We appreciate the trust you have placed in us to help you achieve your financial goals. We are pleased to report that, despite a very difficult year, the aggregate net assets of the eight mutual funds in our family have grown to more than $1.9 billion as of the end of 2008, an increase of 19% over the prior year.

In this Annual Report we review the bond market in 2008 and the performance and composition of each of the Baird Bond Funds. Though the year was extremely challenging, we believe that patience will eventually be rewarded for bond investors as unprecedented volatility and market dislocation begin to subside. Thank you again for choosing Baird Funds.

Sincerely,

Mary Ellen Stanek, CFA

President

Baird Funds

Page 1

2008 Bond Market Overview

2008 – A Year to Remember (or Forget)

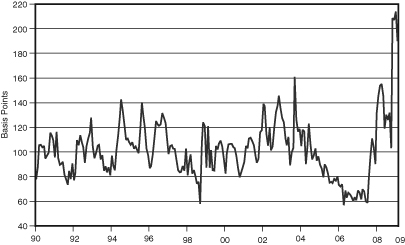

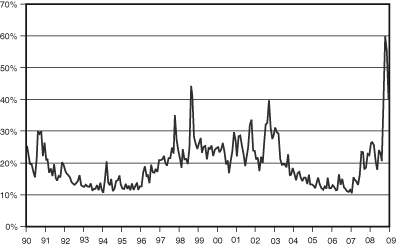

2008 was a year that will be remembered for a long time by investors, but also a year that many would prefer to forget. The “uptick” in volatility in 2007 was merely a preview of the tumultuous chaos that became daily life for investors in 2008 as monumental deleveraging led to unprecedented volatility (see market volatility charts below) and illiquidity that shook the very foundations of the financial markets and eventually stalled the engines of the world economies. Shock waves emanating from Wall Street swiftly spread to Main Street leaving virtually no one unscathed.

| Bond Market Volatility – MOVE Index | CBOE S&P 500 Volatility Index (VIX) |

|  |

| Source: Bloomberg, Merrill Lynch | Source: Bloomberg/CBOE |

Deleveraging and Concerns of Deflation

Deleveraging proved to be most painful for the highly-leveraged, and corporate obituaries of 2008 included several household names that were unable to raise the precious liquidity needed to survive (e.g. Bear Stearns, Lehman Brothers, Countrywide, Washington Mutual, National City). Deleveraging also rendered tremendous destruction of wealth in 2008 (e.g. S&P 500 -37%; S&P/Case-Shiller Home Price Index -18% thru 10/31/08) which severely damaged consumer sentiment, raising concerns that reduced consumer spending could trigger general deflation (while year-over-year CPI was still positive 0.1% through December, forecasts looking forward are slightly negative).

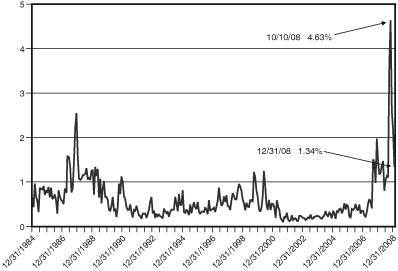

Unprecedented Policy Response

To counter the powerful forces of deleveraging, the U.S. Government pulled out all the stops in efforts to stabilize the markets and the economy: bailouts of FNMA and FHLMC, money market guarantees, purchases of commercial paper, TAF, TSLF, PDCF, TARP, TARF, bridge loans to the Big 3 automakers and reducing the Fed Funds rate to a range of 0-0.25%. Essentially, the Government leveraged its balance sheet to facilitate a more orderly deleveraging of everything else. While the jury is still out on whether these unprecedented efforts will ultimately succeed, one key measure suggests the medicine is beginning to work. The TED Spread (3 mo. LIBOR minus 3 mo. T-bill yield), a

TED Spread

Source: Bloomberg

Page 2

2008 Bond Market Overview

common measure of confidence in the banking system, retreated sharply to 1.34% at year end after spiking to 4.63% at the peak of the financial crisis in mid-October (see chart on prior page). Confidence in the banking system is key to the orderly functioning of the financial markets, and while not back to “normal” levels, improvement in the TED Spread is very encouraging. Possibly the most effective move on the Fed’s part to improve market liquidity was to reduce its target for the Fed Funds rate to 0-0.25% in mid-December. This move pushed money market rates painfully close to zero and effectively flushed money out of money market funds and into other sectors of the bond market as investors began looking for more attractive opportunities for their cash (see positive excess returns of non-Treasury sectors in December on next page).

Flight to Quality, Disparity in Returns

As confidence in the financial markets unraveled over the course of 2008, a full-fledged flight to quality developed and U.S. Treasury yields plunged nearly 300 bps to all-time lows near the end of the year (see chart and table below). Treasuries were

Treasury Yields (Source: Bloomberg)

| Dec 31, | Sep 30, | Dec 31, | Q4 | 2008 | |

| Maturity | 2007 | 2008 | 2008 | Change | Change |

| 1 | 3.30% | 1.79% | 0.34% | -1.45 | -2.96 |

| 2 | 3.05% | 1.96% | 0.76% | -1.20 | -2.29 |

| 3 | 3.03% | 2.28% | 0.97% | -1.31 | -2.06 |

| 5 | 3.44% | 2.98% | 1.55% | -1.43 | -1.89 |

| 10 | 4.02% | 3.82% | 2.21% | -1.61 | -1.81 |

| 30 | 4.45% | 4.31% | 2.68% | -1.63 | -1.77 |

the primary beneficiary of the flight to quality and posted impressive returns of 8.75% for the fourth quarter and 13.74% for the year (see table below). Government Agencies (Q4: +6.10%, 2008: + 9.08%) and Agency-guaranteed MBS (Q4: +4.34%, 2008: +8.34%) were secondary beneficiaries of the flight to quality as investors became confident that the U.S. Government would stand firm behind the debt of FNMA and FHLMC. All other sectors produced negative returns in 2008 as shattered confidence, forced selling and severe illiquidity led to broad price declines. Despite a sharp rebound in December (+7.68%), the High Yield sector was decimated in the fourth quarter (-17.9%) and suffered one of its worst years ever (-26.16%). Forced sales of Asset-Backed Securities (ABS) weighed on this sector throughout the year (2008: -12.72%), while downgrades and rising concern about consumer finance receivables also depressed prices in December (-0.59%). Forced liquidations of leveraged municipal strategies overwhelmed tepid demand resulting in negative returns (2008: -2.47%) for a sector that usually correlates more closely with Treasuries. TIPS rebounded in December (+4.96%) but had a weak fourth quarter (-3.48%) and year (-2.35%) as investors feared deflation over inflation. Annual and fourth quarter returns of various sectors and indices appear in the table below.

Page 3

2008 Bond Market Overview

Total Returns of Selected Barclays Capital (BC) Indices and Subsectors

| Index/Sector | Q4 2008 | Year 2008 | |||||||

| BC Aggregate Index | 4.58 | % | 5.24 | % | |||||

| BC Gov’t/Credit Index | 6.42 | % | 5.70 | % | |||||

| BC Int. Gov’t/Credit Index | 4.84 | % | 5.08 | % | |||||

| BC 1-3 yr. Gov’t/Credit Index | 2.68 | % | 4.97 | % | |||||

| US Treasury Sector | 8.75 | % | 13.74 | % | |||||

| Gov’t Agency Sector | 6.10 | % | 9.08 | % | |||||

| Corporate Sector | 3.98 | % | -4.94 | % | |||||

| MBS Sector | 4.34 | % | 8.34 | % | |||||

| ABS Sector | -6.82 | % | -12.72 | % | |||||

| Municipal Sector | 0.74 | % | -2.47 | % | |||||

| TIPS | -3.48 | % | -2.35 | % | |||||

| High Yield Sector | -17.88 | % | -26.16 | % | |||||

Price Dislocation

Deleveraging caused dramatic widening in yield spreads of most non-Treasury sectors and as liquidity all but vanished late in the year with investors struggling to reduce exposure to risk, price dislocations developed in several sectors. The chart below shows option-adjusted yield spreads (versus similar duration Treasuries) at the end of the second, third and fourth quarters and “excess” returns (versus Treasuries) for the last three months and the entire year of 2008. Yields spreads on Asset-Backed Securities widened sharply throughout the year to 955 bps resulting in 2223 bps of underperformance relative to Treasuries. Spreads in the Finance sector, which came under intense pressure in September, doubled in the second half of the year (from 315 bps to 629 bps) leading to underperformance of 2209 bps versus Treasuries for the year.

| OAS and Excess Returns (in bps) | |||||||||||||

| Option Adjusted Spreads | Excess Returns vs U.S. Treasuries | ||||||||||||

| 6/30/08 | 9/30/08 | 12/31/08 | October | November | December | 2008 | |||||||

| U.S. Aggregate Index | 129 | 176 | 213 | -252 | -163 | 136 | -710 | ||||||

| U.S. Agency | |||||||||||||

| (non-mortgage) Sector | 67 | 115 | 93 | -123 | -9 | 179 | -110 | ||||||

| Mortgage and ABS Sectors | |||||||||||||

| Mortgage-Backed Securities | 127 | 135 | 145 | -152 | -68 | 33 | -232 | ||||||

| Asset-Backed Securities | 353 | 584 | 955 | -665 | -316 | -190 | -2223 | ||||||

| CMBS | 288 | 480 | 1010 | -1020 | -2259 | 1514 | -3274 | ||||||

| Credit Sectors | |||||||||||||

| U.S. Investment Grade | 238 | 385 | 493 | -580 | -183 | 276 | -1786 | ||||||

| Industrial | 226 | 325 | 500 | -884 | -218 | 337 | -1756 | ||||||

| Utility | 232 | 335 | 537 | -992 | -157 | 126 | -2039 | ||||||

| Financial Institutions | 315 | 613 | 629 | -243 | -131 | 349 | -2209 | ||||||

| U.S. High Yield | 708 | 1020 | 1669 | -1650 | -1362 | 568 | -3832 | ||||||

| Source: Barclays Capital | |||||||||||||

Page 4

2008 Bond Market Overview

Industrials and Utilities fell hard in October and finished the year with excess returns of - -1756 bps and -2039 bps, respectively, while the entire investment grade credit sector underperformed Treasuries by 1786 bps. Commercial Mortgage Backed Securities (CMBS) and High Yield got crushed in October and November and finished 2008 with excess returns of -3274 bps and -3832 bps, respectively. Benefiting from government guarantees, Government Agencies and Agency Mortgage-Backed Securities (ABS) saw only modest widening of spreads in 2008 and underperformed Treasuries by just 110 bps and 232 bps respectively. While the positive excess returns of several sectors in December were encouraging, the underperformance of most non-Treasury sectors in 2008 was unprecedented.

Summary

The powerful forces of deleveraging brought the bond market to its knees in 2008. Weakness centered in the financial sector swiftly spread to all corners of the economy and market liquidity all but vanished. Asset prices tumbled and inflation concerns gave way to new worries of deflation. Investor confidence was shattered as several stalwart institutions collapsed and a monumental flight to quality brought Treasury yields to all-time lows while forced liquidations in other areas of the market left huge disparities in sector returns. Pricing services and rating agencies struggled to reflect the changes that were occurring and mark-to-market accounting put additional stress on already dysfunctional and dislocated markets.

Outlook

We believe patience will be rewarded for unleveraged investors in 2009 as severely dislocated prices of bonds in several sectors do not reflect sound credit fundamentals and “quality is on sale”. We believe that deleveraging presents a significant headwind to the economy and the stock market but see great value in investment grade bonds after the price declines of last year. While market and credit risks cannot be ignored, we see exceptional value in well-structured non-Agency MBS and ABS with fixed-rate collateral and believe well-diversified investment grade corporate exposure will excel as liquidity improves. We think Treasuries are poised to underperform in 2009 given increases in supply that are coming and remain cautious of risks in high yield bonds.

A Note on Securities Prices

The unprecedented financial market volatility and lack of liquidity in certain sectors of the bond markets may cause the prices of some of the securities held by the Funds to fluctuate significantly from day to day and from period to period. Nearly all of the securities held by the Funds are priced by Interactive Data Corporation (IDC), an independent pricing service, using evaluation methodologies that integrate information from various market sources, such as observed market data, credit quality information, perceived market movements, news and other relevant information into analytical pricing models to derive market prices for bonds on a daily basis. Although many other mutual fund companies and institutions use IDC to price their securities, the pricing of certain securities – particularly under current conditions – is subject to some extent to the price evaluator’s judgment and IDC’s prices may vary significantly on any given day from prices obtained from other sources and from prices that may be obtained from an actual sale of securities. In addition, certain securities held by the Funds are priced at fair value by the Valuation Committee as delegated by the Funds’ Board of Directors.

Page 5

Baird Intermediate Bond Fund

The Baird Intermediate Bond Fund seeks an annual rate of total return, before Fund expenses, greater than the annual rate of total return of the Barclays Capital Intermediate Government/Credit Bond Index. The Barclays Capital Intermediate Government/Credit Bond Index is an unmanaged, market value weighted index of investment grade, fixed-rate debt issues, including government and corporate securities, with maturities between one and ten years.

Extreme volatility in the financial markets led to severely dislocated prices of bonds in several sectors that we believe do not reflect sound credit fundamentals. The Fund underperformed its benchmark index in 2008. The primary factors for the underperformance were:

| • | The Fund’s underweight to U.S. Treasuries which outperformed all other market sectors due to a flight to quality by investors; |

| • | Exposure to non-Agency mortgage-backed and asset-backed securities; and |

| • | The Fund’s overweighting to the finance sector relative to the benchmark. |

The Fund maintained its duration-neutral strategy, holding a broadly diversified portfolio of over 270 securities at year end.

The Fund ended 2008 with a yield advantage versus its benchmark index. Despite the unprecedented market volatility, we are confident of the integrity of the issues we hold and the structure of the Fund overall. We feel very strongly that the Fund will realize its sizeable yield advantage over time and outperform its benchmark through the completion of this historic and severe credit cycle.

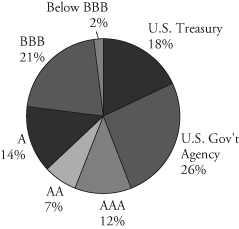

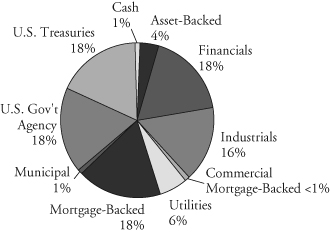

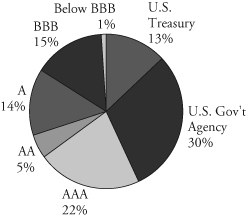

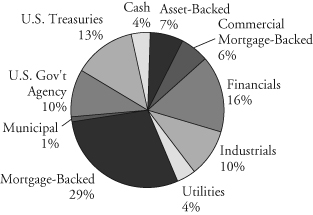

Portfolio Characteristics

| Quality Distribution* | Sector Weightings* | ||||

|  | ||||

| Net Assets: | $405,932,700 | Annualized Expense Ratio: | |||

SEC 30-Day Yield:** | Institutional Class: | 0.30% | |||

| Institutional Class: | 6.18% | Investor Class: | 0.55% | *** | |

| Investor Class: | 5.99% | Portfolio Turnover Rate: | 32.9% | ||

| Average Effective Duration: | 3.82 years | Total Number of Holdings: | 276 | ||

| Average Effective Maturity: | 4.74 years | ||||

| * | Percentages shown are based on the Fund’s total net assets. |

| ** | SEC yields are based on SEC guidelines and are calculated for the 30 days ended December 31, 2008. |

| *** | Includes 0.25% 12b-1 fee. |

Page 6

Baird Intermediate Bond Fund

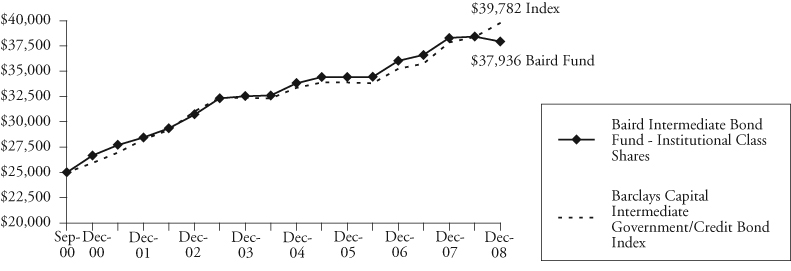

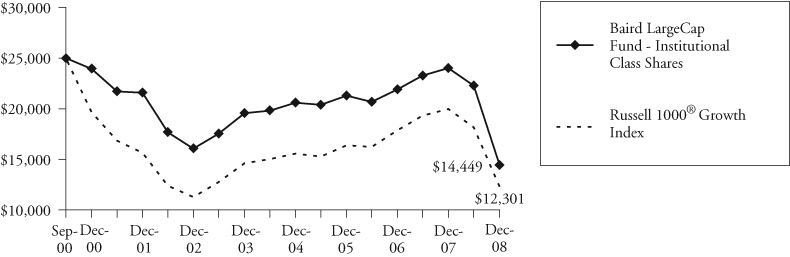

| Institutional Class |

| Value of a $25,000 Investment |

|

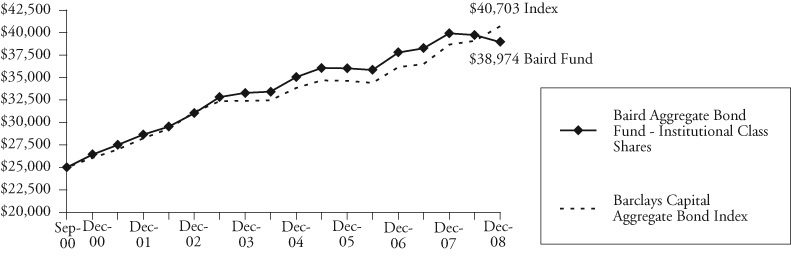

Growth of a hypothetical investment of $25,000 made on the Fund’s inception date (9/29/00), assuming reinvestment of all distributions.

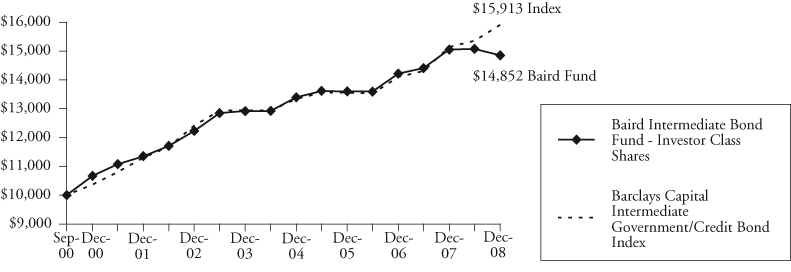

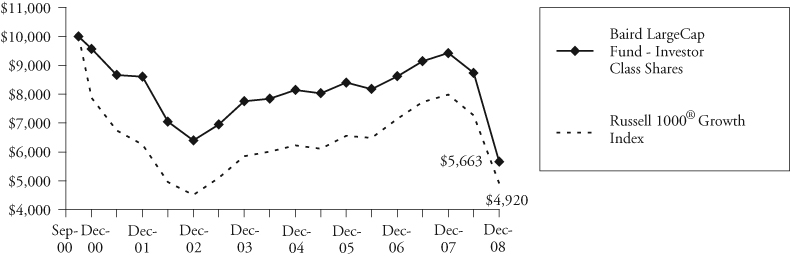

| Investor Class |

| Value of a $10,000 Investment |

|

Growth of a hypothetical investment of $10,000 made on the Fund’s inception date (9/29/00), assuming reinvestment of all distributions.

Page 7

Baird Intermediate Bond Fund

Average Annual Total Returns

| Since | |||

| For the Periods Ended December 31, 2008 | One Year | Five Years | Inception(1) |

| Institutional Class Shares | -0.91% | 3.11% | 5.18% |

| Investor Class Shares | -1.31% | 2.82% | 4.91% |

Barclays Capital Intermediate Government/Credit Bond Index(2) | 5.08% | 4.21% | 5.79% |

| (1) | For the period from September 29, 2000 (commencement of operations) through December 31, 2008. |

| (2) | The Barclays Capital Intermediate Government/Credit Bond Index is an unmanaged, market value weighted index of investment grade, fixed-rate debt including government and corporate securities with maturities between one and 10 years. This index does not reflect any deduction for fees, expenses or taxes. A direct investment in an index is not possible. |

The returns shown in the table above and line graphs on the previous page reflect reinvestment of dividends and/or capital gains distributions in additional shares. The returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

For information about the performance of the Fund as of the most recent month-end, please call 1-866-44BAIRD or visit www.bairdfunds.com. Mutual fund performance changes over time and current performance may be lower or higher than that stated.

Page 8

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% | |||||||

| Asset Backed Securities – 3.3% | |||||||

| $ | 925,000 | American Express Credit | |||||

| Account Master Trust, | |||||||

| Series 2005-5, Class A, | |||||||

| 1.235%, 02/15/2013 | $ | 848,518 | |||||

| 184,464 | Amresco Residential | ||||||

| Securities Mortgage | |||||||

| Loan Trust, | |||||||

| Series 1998-1, Class A6, | |||||||

| 6.51%, 08/25/2027 | 183,814 | ||||||

| 1,144,305 | CitiFinancial Mortgage | ||||||

| Securities, Inc., | |||||||

| Series 2004-1, Class AF2, | |||||||

| 2.645%, 04/25/2034 | 1,039,898 | ||||||

| 70 | Contimortgage Home | ||||||

| Equity Trust, | |||||||

| Series 1999-1, Class A7, | |||||||

| 6.97%, 12/25/2013 | 69 | ||||||

| Countrywide Asset-Backed | |||||||

| Certificates: | |||||||

| 2,215,000 | Series 2006-S3, Class A2, | ||||||

| 6.085%, 06/25/2021 | 950,475 | ||||||

| 2,024,513 | Series 2005-12, Class 1A2, | ||||||

| 4.847%, 02/25/2036 | 1,990,175 | ||||||

| 4,000,000 | Series 2006-13, Class 1AF2, | ||||||

| 5.884%, 01/25/2037 | 3,756,080 | ||||||

| 375,000 | Series 2006-13, Class 1AF3, | ||||||

| 5.944%, 01/25/2037 | 272,963 | ||||||

| 1,380,000 | Series 2006-9, Class 1AF3, | ||||||

| 5.859%, 10/25/2046 | 803,458 | ||||||

| Delta Funding Home | |||||||

| Equity Loan Trust: | |||||||

| 77,421 | Series 1997-2, Class A6, | ||||||

| 7.04%, 06/25/2027 | 77,495 | ||||||

| 49,386 | Series 1999-1, Class A6F, | ||||||

| 6.34%, 12/15/2028 | 47,342 | ||||||

| 538,268 | Series 1999-2, Class A7F, | ||||||

| 7.03%, 08/15/2030 | 537,459 | ||||||

| 175,000 | Discover Card | ||||||

| Master Trust I, | |||||||

| Series 2005-2, Class A, | |||||||

| 1.23%, 04/17/2012 | 167,594 | ||||||

| 31,479 | Equivantage Home | ||||||

| Equity Loan Trust, | |||||||

| Series 1996-3, Class A3, | |||||||

| 7.70%, 09/25/2027 | 24,814 | ||||||

| GMAC Mortgage | |||||||

| Corporation Loan Trust: | |||||||

| 490,447 | Series 2004-GH1, | ||||||

| Class A2, 4.39%, | |||||||

| 12/25/2025 | 476,383 | ||||||

| 238,615 | Series 2005-HE3, | ||||||

| Class A2, 1.12%, | |||||||

| 02/25/2036 | 101,922 | ||||||

| Green Tree Financial | |||||||

| Corporation: | |||||||

| 61,657 | Series 1993-4, Class A5, | ||||||

| 7.05%, 01/15/2019 | 53,355 | ||||||

| 933,992 | Series 1998-2, Class A5, | ||||||

| 6.24%, 12/01/2028 | 708,160 | ||||||

| 1,216,032 | Series 1998-3, Class A5, | ||||||

| 6.22%, 03/01/2030 | 883,919 | ||||||

| 453,908 | Series 1998-4, Class A5, | ||||||

| 6.18%, 04/01/2030 | 290,983 | ||||||

| 65,966 | IMC Home Equity | ||||||

| Loan Trust, | |||||||

| Series 1998-1, Class A6, | |||||||

| 7.02%, 06/20/2029 | 58,671 | ||||||

| 194,957 | Oakwood Mortgage | ||||||

| Investors, Inc., | |||||||

| Series 1999-B, Class A3, | |||||||

| 6.45%, 11/15/2017 | 129,626 | ||||||

The accompanying notes are an integral part of these financial statements.

Page 9

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Asset Backed Securities – 3.3% (cont.) | |||||||

| $ | 21,280 | Residential Asset | |||||

| Mortgage Products, Inc., | |||||||

| Series 2003-RS7, | |||||||

| Class AI6, 5.34%, | |||||||

| 08/25/2033 | $ | 19,931 | |||||

| 163,503 | Structured Asset | ||||||

| Securities Corporation, | |||||||

| Series 2005-2XS, | |||||||

| Class 1A2A, 4.51%, | |||||||

| 02/25/2035 | 143,483 | ||||||

| 13,566,587 | |||||||

| Financial – 18.4% | |||||||

| 875,000 | Allfirst Financial, Inc. | ||||||

| Subordinated Notes, | |||||||

| 6.875%, 06/01/2009 | 890,245 | ||||||

| American General Finance | |||||||

| Corporation Notes: | |||||||

| 25,000 | 4.625%, 09/01/2010 | 12,665 | |||||

| 550,000 | 4.00%, 03/15/2011 | 266,729 | |||||

| 630,000 | AmSouth Bancorporation | ||||||

| Subordinated Debentures, | |||||||

| 6.75%, 11/01/2025 | 556,881 | ||||||

| 1,335,000 | Anthem, Inc., | ||||||

| 6.80%, 08/01/2012 | 1,319,646 | ||||||

| 525,000 | Banco Santander Chile, | ||||||

7.375%, 07/18/2012 f | 537,669 | ||||||

| 760,000 | Bank of America | ||||||

| Corporation | |||||||

| Subordinated Notes, | |||||||

| 10.20%, 07/15/2015 | 833,600 | ||||||

| 1,450,000 | Bank of Tokyo- | ||||||

| Mitsubishi UFJ NY, | |||||||

7.40%, 06/15/2011 f | 1,403,790 | ||||||

| Bank One Corporation | |||||||

| Subordinated Notes: | |||||||

| 180,000 | 6.00%, 02/17/2009 | 180,009 | |||||

| 1,043,000 | 10.00%, 08/15/2010 | 1,099,070 | |||||

| 125,000 | Bank United | ||||||

| Subordinated Notes, | |||||||

| 8.00%, 03/15/2009 @ | 13 | ||||||

| 2,695,000 | BankAmerica Institutional, | ||||||

| 8.07%, 12/31/2026 | |||||||

| (Acquired 01/04/2006 – | |||||||

| 11/06/2007, Aggregate | |||||||

| Cost $2,781,965)* | 2,210,296 | ||||||

| 2,500,000 | Banponce Trust I, Series A, | ||||||

| 8.327%, 02/01/2027 | |||||||

| (Callable 03/02/2009) | 2,063,025 | ||||||

| 1,000,000 | Bear Stearns Cos., Inc., | ||||||

| 6.40%, 10/02/2017 | 1,039,178 | ||||||

| 1,000,000 | BOI Capital | ||||||

| Funding No. 2, | |||||||

| 5.571%, 02/01/2049 | |||||||

| (Acquired 01/20/2006; | |||||||

| Cost $1,000,000) | |||||||

(Callable 02/01/2016)* f | 219,807 | ||||||

| 520,000 | CIT Group Company | ||||||

| of Canada, | |||||||

5.20%, 06/01/2015 f | 365,068 | ||||||

| CIT Group, Inc.: | |||||||

| 200,000 | 5.40%, 01/30/2016 | 139,258 | |||||

| 1,500,000 | 6.10%, 03/15/2067 | ||||||

| (Callable 03/15/2017) | 463,190 | ||||||

| 1,000,000 | Citigroup, Inc., | ||||||

| 5.50%, 04/11/2013 | 973,684 | ||||||

| 1,000,000 | Compass Bank | ||||||

| Subordinated Notes, | |||||||

| 8.10%, 08/15/2009 | 976,425 | ||||||

The accompanying notes are an integral part of these financial statements.

Page 10

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Financial – 18.4% (cont.) | |||||||

| $ | 1,760,000 | Corestates Capital Trust I, | |||||

| 8.00%, 12/15/2026 | |||||||

| (Acquired 11/29/2005 | |||||||

| and 10/10/2007; | |||||||

| Cost $268,040 | |||||||

| and $1,546,382)* | $ | 1,445,523 | |||||

| 275,000 | Corp Andina De | ||||||

| Fomento Notes, | |||||||

7.375%, 01/18/2011 f | 276,995 | ||||||

| 1,900,000 | Countrywide | ||||||

| Financial Corporation | |||||||

| Subordinated Notes, | |||||||

| 6.25%, 05/15/2016 | 1,804,065 | ||||||

| 1,000,000 | Export Import | ||||||

| Bank Korea, | |||||||

| 5.125%, 02/14/2011 | 965,610 | ||||||

| 416,065 | First National | ||||||

| Bank of Chicago | |||||||

| Pass-Thru Certificates, | |||||||

| Series 1993-A, | |||||||

| 8.08%, 01/05/2018 | 541,655 | ||||||

| 2,600,000 | First National | ||||||

| Bank of Omaha | |||||||

| Subordinated Notes, | |||||||

| 7.32%, 12/01/2010 | 2,619,679 | ||||||

| 2,025,000 | First Union | ||||||

| Capital I, Series A, | |||||||

| 7.935%, 01/15/2027 | |||||||

| (Callable 03/27/2009) | 1,680,659 | ||||||

| 775,000 | FMR LLC Notes, | ||||||

| 4.75%, 03/01/2013 | |||||||

| (Acquired 02/26/2003; | |||||||

| Cost $776,147)* | 712,588 | ||||||

| 2,300,000 | GE Global Insurance | ||||||

| Holding Corp., | |||||||

| 7.50%, 06/15/2010 | 2,282,870 | ||||||

| 800,000 | General Electric Capital | ||||||

| Corporation Notes, | |||||||

| 6.00%, 06/15/2012 | 820,838 | ||||||

| 2,000,000 | Genworth Financial, Inc., | ||||||

| 4.75%, 06/15/2009 | 1,964,938 | ||||||

| 1,100,000 | Genworth Financial Inc. | ||||||

| Notes, 5.75%, 06/15/2014 | 422,490 | ||||||

| 1,975,000 | Glencore Funding LLC, | ||||||

| 6.00%, 04/15/2014 | |||||||

| (Acquired 03/31/2004, | |||||||

| 02/02/2005, 04/26/2006 | |||||||

| and 12/04/2006; | |||||||

| Cost $794,280, $146,738, | |||||||

| $287,643 and $720,432, | |||||||

| respectively)* | 799,476 | ||||||

| GMAC LLC: | |||||||

| 1,025,000 | 7.75%, 01/19/2010 | 914,181 | |||||

| 80,000 | 7.50%, 12/31/2013 | ||||||

| (Acquired 12/31/2008, | |||||||

| Cost $344,425)* # | 58,365 | ||||||

| 200,000 | 6.75%, 12/01/2014 | 136,729 | |||||

| 96,000 | 8.00%, 12/31/2018 | ||||||

| (Acquired 12/31/2008, | |||||||

| Cost $413,311)* # | 50,336 | ||||||

| 1,125,000 | Goldman Sachs | ||||||

| Group, Inc., | |||||||

| 5.15%, 01/15/2014 | 1,013,208 | ||||||

| 1,800,000 | Great West Life & | ||||||

| Annuity Insurance, | |||||||

| 7.153%, 05/16/2046 | |||||||

| (Acquired 05/16/2006 | |||||||

| and 11/08/2007; | |||||||

| Cost $1,000,000 | |||||||

| and $792,736)* | 983,729 | ||||||

The accompanying notes are an integral part of these financial statements.

Page 11

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Financial – 18.4% (cont.) | |||||||

| HSBC Finance | |||||||

| Corporation Notes: | |||||||

| $ | 2,000,000 | 8.00%, 07/15/2010 | $ | 2,033,262 | |||

| 25,000 | 5.00%, 06/30/2015 | 22,191 | |||||

| 2,000,000 | Huntington National | ||||||

| Bank Notes, | |||||||

| 8.00%, 04/01/2010 | 1,833,640 | ||||||

| 500,000 | Invesco Ltd., | ||||||

5.375%, 02/27/2013 f | 444,095 | ||||||

| Istar Financial, Inc.: | |||||||

| 2,300,000 | 4.875%, Series B, | ||||||

| 01/15/2009 | 2,087,250 | ||||||

| 1,050,000 | 5.95%, 10/15/2013 | 330,750 | |||||

| 500,000 | J.P. Morgan | ||||||

| Chase & Company | |||||||

| Subordinated Notes, | |||||||

| 6.625%, 03/15/2012 | 512,199 | ||||||

| 2,000,000 | Key Bank NA, | ||||||

| 7.413%, 05/06/2015 | 1,716,804 | ||||||

| Korea Development | |||||||

Bank Notes: f | |||||||

| 1,275,000 | 3.875%, 03/02/2009 | 1,268,559 | |||||

| 350,000 | 4.625%, 09/16/2010 | 339,629 | |||||

| 846,000 | Lehman Brothers | ||||||

| Holdings, Inc. Notes, | |||||||

| 8.50%, 08/01/2015 @ | 80,370 | ||||||

| 1,735,000 | Lehman Brothers | ||||||

| Holdings Senior Notes, | |||||||

| 8.80%, 03/01/2015 @ | 164,825 | ||||||

| 546,000 | Liberty Mutual Group, | ||||||

| 7.25%, 09/01/2012 | |||||||

| (Acquired 08/03/2004, | |||||||

| Cost $583,994)* | 477,750 | ||||||

| Marsh & McLennan | |||||||

| Companies, Inc.: | |||||||

| 1,000,000 | 7.125%, 06/15/2009 | 997,341 | |||||

| 700,000 | 5.375%, 07/15/2014 | 621,025 | |||||

| 500,000 | MBIA Insurance Corp., | ||||||

| 14.00%, 01/15/2033 | |||||||

| (Callable 01/15/2013) | |||||||

| (Acquired 01/11/2008; | |||||||

| Cost $500,000)* | 255,000 | ||||||

| Merrill Lynch & Co, Inc.: | |||||||

| 1,000,000 | 5.70%, 05/02/2017 | 885,956 | |||||

| 1,000,000 | 6.875%, 04/25/2018 | 1,046,026 | |||||

| 375,000 | Met Life Global | ||||||

| Funding Senior Notes, | |||||||

| 4.50%, 05/05/2010 | |||||||

| (Acquired 08/04/2005 and | |||||||

| 03/22/2007; Cost $123,925 | |||||||

| and $248,188)* | 359,749 | ||||||

| 1,075,000 | The Mony Group, Inc., | ||||||

| 8.35%, 03/15/2010 | 1,063,069 | ||||||

| Morgan Stanley Senior | |||||||

| Unsecured Notes: | |||||||

| 1,000,000 | 5.625%, 01/09/2012 | 948,307 | |||||

| 1,400,000 | 6.625%, 04/01/2018 | 1,228,206 | |||||

| 25,000 | Morgan Stanley | ||||||

| Subordinated Notes, | |||||||

| 4.75%, 04/01/2014 | 19,047 | ||||||

| 1,530,000 | National Australia Bank Ltd. | ||||||

| Subordinated Notes, Series A, | |||||||

8.60%, 05/19/2010 f | 1,560,949 | ||||||

| 350,000 | National Bank of Hungary | ||||||

| Yankee Debentures, | |||||||

8.875%, 11/01/2013 f | 369,867 | ||||||

| 2,725,000 | National City | ||||||

| Bank of Cleveland, | |||||||

| 4.50%, 03/15/2010 | 2,623,695 | ||||||

| 534,000 | National City | ||||||

| Bank of Kentucky | |||||||

| Subordinated Notes, | |||||||

| 6.30%, 02/15/2011 | 514,436 | ||||||

The accompanying notes are an integral part of these financial statements.

Page 12

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Financial – 18.4% (cont.) | |||||||

| $ | 2,300,000 | Navigators Group Inc. | |||||

| Senior Unsecured Notes, | |||||||

| 7.00%, 05/01/2016 | $ | 1,463,205 | |||||

| 1,260,000 | NB Capital Trust IV, | ||||||

| 8.25%, 04/15/2027 | |||||||

| (Callable 03/27/2009) | 1,042,331 | ||||||

| 1,000,000 | North Fork | ||||||

| Capital Trust II, | |||||||

| 8.00%, 12/15/2027 | |||||||

| (Callable 03/27/2009) | 459,690 | ||||||

| 1,319,000 | PNC Funding | ||||||

| Corporation, | |||||||

| 7.50%, 11/01/2009 | 1,317,131 | ||||||

| 1,500,000 | Premium Asset Senior | ||||||

| Notes, 4.125%, 03/12/2009 | |||||||

| (Acquired 12/20/2006 and | |||||||

| 05/10/2007; Cost $993,963 | |||||||

| and $497,795)* | 181,875 | ||||||

| 75,000 | Protective Life | ||||||

| Corporation Senior Notes, | |||||||

| 4.30%, 06/01/2013 | 61,145 | ||||||

| 1,650,000 | Regions Bank, | ||||||

| 7.50%, 05/15/2018 | 1,418,063 | ||||||

| 800,000 | Santander | ||||||

| Financial Issuances, | |||||||

6.375%, 02/15/2011 f | 832,539 | ||||||

| 1,300,000 | Schwab Capital Trust I, | ||||||

| 7.50%, 11/15/2037 | |||||||

| (Callable 11/15/2017) | 650,143 | ||||||

| SLM Corporation Notes: | |||||||

| 1,516,000 | 4.50%, 07/26/2010 | 1,315,686 | |||||

| 200,000 | 5.375%, 05/15/2014 | 134,975 | |||||

| 1,000,000 | Sovereign Bank, Inc., | ||||||

| 8.75%, 05/30/2018 | 987,935 | ||||||

| 1,000,000 | St. Paul Travelers, Inc., | ||||||

| 6.25%, 06/20/2016 | 1,000,251 | ||||||

| 1,046,000 | Toll Road Inv. | ||||||

| Partnership II, | |||||||

| 0.00%, 02/15/2011 | |||||||

| (Acquired 09/28/2004; | |||||||

| Cost $946,449)* ^ | 935,812 | ||||||

| 1,320,000 | Transamerica Finance | ||||||

| Corporation Debentures, | |||||||

| 0.00%, 03/01/2010 ^ | 1,154,215 | ||||||

| 850,000 | UFJ Finance Aruba AEC, | ||||||

6.75%, 07/15/2013 f | 830,788 | ||||||

| 500,000 | Washington Mutual Bank | ||||||

| Subordinated Notes, | |||||||

| 6.875%, 06/15/2011 | 50 | ||||||

| Westdeutsche Landesbank | |||||||

| Subordinated Notes: | |||||||

| 246,000 | 6.05%, 01/15/2009 | 246,308 | |||||

| 1,495,000 | 4.796%, 07/15/2015 | 1,686,933 | |||||

| 74,567,254 | |||||||

| Industrial – 16.8% | |||||||

| 450,000 | Alcan, Inc., Notes, | ||||||

5.00%, 06/01/2015 f | 333,212 | ||||||

| 2,000,000 | American Standard Inc., | ||||||

| 8.25%, 06/01/2009 | 2,012,138 | ||||||

| Ameritech Capital | |||||||

| Funding Debentures: | |||||||

| 1,158,879 | 9.10%, 06/01/2016 | 1,224,826 | |||||

| 1,008,000 | 6.45%, 01/15/2018 | 996,898 | |||||

| 2,250,000 | British Sky | ||||||

| Broadcasting Group, | |||||||

8.20%, 07/15/2009 f | 2,287,222 | ||||||

| 2,000,000 | British | ||||||

| Telecommunications PLC, | |||||||

5.95%, 01/15/2018 f | 1,739,934 | ||||||

The accompanying notes are an integral part of these financial statements.

Page 13

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Industrial – 16.8% (cont.) | |||||||

| Bunge Ltd. Finance | |||||||

| Corporation Notes: | |||||||

| $ | 800,000 | 5.35%, 04/15/2014 | $ | 573,932 | |||

| 1,085,000 | 5.10%, 07/15/2015 | 789,259 | |||||

| 1,650,000 | CBS Corporation, | ||||||

| 7.70%, 07/30/2010 | 1,612,847 | ||||||

| 1,250,000 | Clear Channel | ||||||

| Communications Senior | |||||||

| Unsubordinated Notes, | |||||||

| 5.50%, 12/15/2016 | 143,750 | ||||||

| Comcast Cable Holdings, | |||||||

| 550,000 | 7.875%, 08/01/2013 | 565,519 | |||||

| 125,000 | Comcast Cable | ||||||

| Communication Holdings, | |||||||

| 8.375%, 03/15/2013 | 129,316 | ||||||

| 525,000 | Comcast Corporation, | ||||||

| 6.50%, 01/15/2017 | 518,550 | ||||||

| 50,000 | Comcast Holdings | ||||||

| Corporation, | |||||||

| 10.625%, 07/15/2012 | 53,103 | ||||||

| 1,062,000 | Computer Sciences | ||||||

| Corporation Notes, | |||||||

| 6.25%, 03/15/2009 | 1,058,504 | ||||||

| 1,281,000 | COX Communications Inc., | ||||||

| 7.125%, 10/01/2012 | 1,225,939 | ||||||

| 750,000 | COX Communications | ||||||

| Inc. Notes, | |||||||

| 7.875%, 08/15/2009 | 737,242 | ||||||

| CSX Corporation: | |||||||

| 1,700,000 | 5.75%, 03/15/2013 | 1,597,356 | |||||

| 450,000 | 6.25%, 04/01/2015 | 441,725 | |||||

| 1,250,000 | Deutsche Telekom | ||||||

| International Finance BV, | |||||||

8.50%, 06/15/2010 f | 1,287,593 | ||||||

| Donnelley (R.R.) | |||||||

| & Sons Co.: | |||||||

| 1,500,000 | 3.75%, 04/01/2009 | 1,471,599 | |||||

| 875,000 | 6.125%, 01/15/2017 | 622,557 | |||||

| 1,000,000 | D.R. Horton Inc. | ||||||

| Unsubordinated Notes, | |||||||

| 6.50%, 04/15/2016 | 630,000 | ||||||

| 2,225,000 | Fiserv, Inc., | ||||||

| 6.125%, 11/20/2012 | 2,090,465 | ||||||

| 623,000 | Ford Capital BV | ||||||

| Debentures, | |||||||

| 9.50%, 06/01/2010 | 271,005 | ||||||

| 300,000 | Ford Motor Company | ||||||

| Debentures, | |||||||

| 9.215%, 09/15/2021 | 69,000 | ||||||

| 1,260,000 | GTE Corporation, | ||||||

| 6.84%, 04/15/2018 | 1,276,201 | ||||||

| 675,000 | Halliburton Company Notes, | ||||||

| 5.50%, 10/15/2010 | 689,432 | ||||||

| 1,325,000 | Hanson Australia Funding, | ||||||

5.25%, 03/15/2013 f | 450,521 | ||||||

| 650,000 | Hanson PLC Notes, | ||||||

6.125%, 08/15/2016 f | 226,360 | ||||||

| 1,195,000 | Health Care Service | ||||||

| Corporation Notes, | |||||||

| 7.75%, 06/15/2011 | |||||||

| (Acquired 06/20/2001, | |||||||

| 01/26/2005, and | |||||||

| 10/19/2006; Cost | |||||||

| $497,765, $350,953, and | |||||||

| $383,154, respectively)* | 1,274,844 | ||||||

| 420,000 | Highmark, Inc. Notes, | ||||||

| 6.80%, 08/15/2013 | |||||||

| (Acquired 08/14/2003 and | |||||||

| 03/13/2008; Cost $399,088 | |||||||

| and $20,744)* | 400,151 | ||||||

The accompanying notes are an integral part of these financial statements.

Page 14

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Industrial – 16.8% (cont.) | |||||||

| $ | 2,000,000 | Humana Inc., | |||||

| 7.20%, 06/15/2018 | $ | 1,608,376 | |||||

| 975,000 | Hutchison Whampoa | ||||||

| International Limited, | |||||||

| 6.25%, 01/24/2014 | |||||||

| (Acquired 11/19/2003 | |||||||

| and 02/08/2005; | |||||||

| Cost $749,228 | |||||||

and $237,149)* f | 932,468 | ||||||

| 1,000,000 | Ingersoll-Rand | ||||||

| Company Debentures, | |||||||

6.391%, 11/15/2027 f | 1,006,247 | ||||||

| 1,850,000 | International Paper | ||||||

| Company Notes, | |||||||

| 4.25%, 01/15/2009 | 1,849,362 | ||||||

| 1,100,000 | Johnson Controls Inc. | ||||||

| Senior Notes, | |||||||

| 5.50%, 01/15/2016 | 852,431 | ||||||

| 1,000,000 | Kraft Foods, Inc., | ||||||

| 6.125%, 08/23/2018 | 985,874 | ||||||

| 675,000 | Laboratory Corporation | ||||||

| of America Holdings, | |||||||

| 5.50%, 02/01/2013 | 647,681 | ||||||

| 550,000 | Lafarge S.A. Notes, | ||||||

6.50%, 07/15/2016 f | 371,098 | ||||||

| 500,000 | Limited Brands, Inc., | ||||||

| 5.25%, 11/01/2014 | 288,435 | ||||||

| 400,000 | Marathon Global | ||||||

| Funding Corp, | |||||||

| 6.00%, 07/01/2012 | 404,376 | ||||||

| 1,550,000 | Masco Corporation, | ||||||

| 6.125%, 10/03/2016 | 1,063,844 | ||||||

| 650,000 | Nabors Industrials, Inc., | ||||||

| 6.15%, 02/15/2018 | |||||||

| (Acquired 02/14/2008; | |||||||

| Cost $649,480)* | 559,223 | ||||||

| 650,000 | New York Telephone | ||||||

| Company Debentures, | |||||||

| 8.625%, 11/15/2010 | 675,867 | ||||||

| 2,307,000 | Nextel Communications | ||||||

| Senior Notes, | |||||||

| 6.875%, 10/31/2013 | 980,475 | ||||||

| 700,000 | PCCW Capital II Ltd., | ||||||

| 6.00%, 07/15/2013 | |||||||

| (Acquired 07/10/2003; | |||||||

Cost $696,731)* f | 598,955 | ||||||

| 925,000 | Pearson Dollar Finance PLC, | ||||||

| 5.70%, 06/01/2014 | |||||||

| (Acquired 09/28/2005 and | |||||||

| 12/14/2007; Cost $612,344 | |||||||

and $321,181)* f | 814,547 | ||||||

| 1,850,000 | PEMEX Project | ||||||

| Funding Master Trust, | |||||||

| 9.125%, 10/13/2010 | 1,947,125 | ||||||

| 1,770,000 | Plum Creek Timberlands, | ||||||

| 5.875%, 11/15/2015 | 1,445,663 | ||||||

| Qwest Capital | |||||||

| Funding, Inc.: | |||||||

| 350,000 | 7.00%, 08/03/2009 | 343,000 | |||||

| 100,000 | 7.25%, 02/15/2011 | 84,000 | |||||

| 1,000,000 | Reed Elsevier Capital Notes, | ||||||

| 4.625%, 06/15/2012 | 879,814 | ||||||

| 1,800,000 | Rio Tinto Financial | ||||||

| USA Ltd., | |||||||

6.50%, 07/15/2018 f | 1,319,708 | ||||||

| 500,000 | Sprint Nextel Corporation, | ||||||

| 6.00%, 12/01/2016 | 352,500 | ||||||

| 1,100,000 | Sunoco, Inc. Senior | ||||||

| Unsecured Notes, | |||||||

| 5.75%, 01/15/2017 | 914,180 | ||||||

| TCI Communications, | |||||||

| Inc. Debentures: | |||||||

| 583,000 | 8.75%, 08/01/2015 | 620,579 | |||||

The accompanying notes are an integral part of these financial statements.

Page 15

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Industrial – 16.8% (cont.) | |||||||

Telecom Italia Capital: f | |||||||

| $ | 1,360,000 | 4.95%, 09/30/2014 | $ | 1,035,300 | |||

| 650,000 | 5.25%, 10/01/2015 | 494,812 | |||||

| 906,000 | Tele-Communications, | ||||||

| Inc. Debentures, | |||||||

| 9.80%, 02/01/2012 | 955,110 | ||||||

| 1,650,000 | Telefonica | ||||||

| Emisiones, S.A.U., | |||||||

6.421%, 06/20/2016 f | 1,647,136 | ||||||

| 1,000,000 | Time Warner Cable, Inc., | ||||||

| 5.85%, 05/01/2017 | 913,553 | ||||||

| 250,000 | Time Warner | ||||||

| Companies, Inc., | |||||||

| 6.875%, 06/15/2018 | 223,222 | ||||||

| 1,747,000 | Time Warner Companies | ||||||

| Inc. Debentures, | |||||||

| 9.125%, 01/15/2013 | 1,731,287 | ||||||

| 1,470,000 | Transocean, Inc., | ||||||

6.625%, 04/15/2011 f | 1,501,110 | ||||||

| 500,000 | Tyco Electronics | ||||||

| Group S. A., | |||||||

| 6.55%, 10/01/2017 | |||||||

| (Acquired 09/26/2007; | |||||||

Cost $504,926)* f | 420,201 | ||||||

| Tyco International | |||||||

Finance: f | |||||||

| 1,525,000 | 6.375%, 10/15/2011 | 1,498,990 | |||||

| 650,000 | 6.00%, 11/15/2013 | 609,905 | |||||

| United AirLines, Inc. | |||||||

| Pass-Thru Certificates: | |||||||

| 207,039 | Series 1991-A, Class A-2, | ||||||

| 10.02%, 03/22/2014 | 85,403 | ||||||

| 188,541 | Series 2001-1, Class A-2, | ||||||

| 6.201%, 12/31/2049 | 175,343 | ||||||

| 245,275 | Series 2000-2, Class C, | ||||||

| 7.762%, 12/31/2049 | 206,644 | ||||||

| 1,500,000 | Vale Overseas Limited, | ||||||

6.25%, 01/23/2017 f | 1,414,200 | ||||||

| 250,000 | Verizon Communications | ||||||

| Senior Unsecured Notes, | |||||||

| 5.55%, 02/15/2016 | 244,254 | ||||||

| 2,000,000 | Vulcan Materials Co., | ||||||

| 7.00%, 06/15/2018 | 1,564,806 | ||||||

| Waste Management, Inc.: | |||||||

| 2,510,000 | 6.875%, 05/15/2009 | 2,498,346 | |||||

| 25,000 | 5.00%, 03/15/2014 | 21,451 | |||||

| 500,000 | Willamette Industries, | ||||||

| Inc. Notes, | |||||||

| 6.60%, 06/05/2012 | 421,592 | ||||||

| 68,009,493 | |||||||

| Mortgage Backed Securities – 18.4% | |||||||

| Bank of America | |||||||

| Alternative Loan Trust: | |||||||

| 442,579 | Series 2003-11, Class 4A1, | ||||||

| 4.75%, 01/25/2019 | 423,217 | ||||||

| 1,280,243 | Series 2004-2, Class 5A1, | ||||||

| 5.50%, 03/25/2019 | 1,191,116 | ||||||

| 1,470,321 | Series 2004-11, Class 4A1, | ||||||

| 5.50%, 12/25/2019 | 1,396,346 | ||||||

| 827,056 | Series 2006-2, Class 7A1, | ||||||

| 6.00%, 03/25/2021 | 693,492 | ||||||

| 1,292,339 | Series 2006-3, Class 6A1, | ||||||

| 6.00%, 04/25/2036 | 936,945 | ||||||

| 1,252,258 | Series 2006-4, Class 3CB4, | ||||||

| 6.00%, 05/25/2046 | 855,086 | ||||||

| 941,584 | Bank of America | ||||||

| Funding Corporation, | |||||||

| Series 2003-3, Class 1A41, | |||||||

| 5.50%, 10/25/2033 | 884,366 | ||||||

The accompanying notes are an integral part of these financial statements.

Page 16

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Mortgage Backed Securities – 18.4% (cont.) | |||||||

| Citicorp Mortgage | |||||||

| Securities, Inc.: | |||||||

| $ | 1,369,050 | Series 2004-5, Class 1A25, | |||||

| 5.50%, 10/25/2014 | $ | 1,292,261 | |||||

| 1,246,317 | Series 2004-4, Class A5, | ||||||

| 5.50%, 06/25/2034 | 1,148,953 | ||||||

| Countrywide Alternative | |||||||

| Loan Trust: | |||||||

| 359,863 | Series 2005-5R, Class A2, | ||||||

| 4.75%, 12/25/2018 | 323,024 | ||||||

| 1,301,983 | Series 2005-50CB, | ||||||

| Class 4A1, 5.00%, | |||||||

| 11/25/2020 | 1,095,080 | ||||||

| 1,374,576 | Series 2005-85CB, Class | ||||||

| 3A1, 5.25%, 02/25/2021 | |||||||

| (Acquired 09/26/2007, | |||||||

| 10/11/2007 and 06/19/2008; | |||||||

| Cost $273,511, $42,626 | |||||||

| and $957,934)* | 1,234,182 | ||||||

| 2,202,610 | Series 2006-7CB, | ||||||

| Class 3A1, 5.25%, | |||||||

| 05/25/2021 | 1,497,087 | ||||||

| 50,000 | Series 2005-10CB, | ||||||

| Class 1A6, 5.50%, | |||||||

| 05/25/2035 | 39,028 | ||||||

| 175,675 | Series 2005-11CB, | ||||||

| Class 2A1, 5.50%, | |||||||

| 06/25/2035 | 143,342 | ||||||

| 1,515,520 | Series 2005-34CB, | ||||||

| Class 1A6, 5.50%, | |||||||

| 09/25/2035 | 1,333,092 | ||||||

| 1,340,478 | Countrywide Home | ||||||

| Loans, Inc., | |||||||

| Series 2003-18, Class A3, | |||||||

| 5.25%, 07/25/2033 | 1,231,190 | ||||||

| 126,312 | Credit Suisse First Boston | ||||||

| Mortgage Securities Corp., | |||||||

| Series 2005-3, Class 3A27, | |||||||

| 5.50%, 07/25/2035 | 101,255 | ||||||

| Federal Gold | |||||||

| Loan Mortgage | |||||||

| Corporation (FGLMC) | |||||||

| Pass-Thru Certificates: | |||||||

| 1,319,023 | 6.00%, 06/01/2021 | 1,367,856 | |||||

| 49,146 | 6.00%, 07/01/2028 | 50,983 | |||||

| Federal Home | |||||||

| Loan Mortgage | |||||||

| Corporation (FHLMC): | |||||||

| 1,259,494 | Series 3033, Class LU, | ||||||

| 5.50%, 03/15/2013 | 1,294,696 | ||||||

| 1,364,124 | Series 2695, Class UA, | ||||||

| 5.50%, 09/15/2014 | 1,407,805 | ||||||

| 7,907,888 | Series R014, Class AL, | ||||||

| 5.50%, 10/15/2014 | 8,015,224 | ||||||

| 545,700 | Series R001, Class AE, | ||||||

| 4.375%, 04/15/2015 | 551,470 | ||||||

| 1,929,468 | Series R003, Class VA, | ||||||

| 5.50%, 08/15/2016 | 2,009,864 | ||||||

| 2,189,810 | Series 3122, Class VA, | ||||||

| 6.00%, 01/15/2017 | 2,271,177 | ||||||

| 1,714,239 | Series R010, Class VA, | ||||||

| 5.50%, 04/15/2017 | 1,785,807 | ||||||

| 4,089,752 | Series R009, Class AJ, | ||||||

| 5.75%, 12/15/2018 | 4,176,181 | ||||||

| 41,540 | Series 1395, Class G, | ||||||

| 6.00%, 10/15/2022 | 41,490 | ||||||

| 462,742 | Series 2970, Class DA, | ||||||

| 5.50%, 01/15/2023 | 472,359 | ||||||

| Federal National Mortgage | |||||||

| Association (FNMA): | |||||||

| 955,138 | Series 2006-B2, Class AB, | ||||||

| 5.50%, 05/25/2014 | 977,866 | ||||||

The accompanying notes are an integral part of these financial statements.

Page 17

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Mortgage Backed Securities – 18.4% (cont.) | |||||||

| $ | 975,598 | Series 2003-24, Class PC, | |||||

| 5.00%, 11/25/2015 | $ | 988,272 | |||||

| 1,773,427 | Series 2006-B1, Class AB, | ||||||

| 6.00%, 06/25/2016 | 1,812,256 | ||||||

| 50,000 | Series 2003-35, Class TD, | ||||||

| 5.00%, 12/25/2016 | 50,667 | ||||||

| 148,980 | Series 1991-137, Class H, | ||||||

| 7.00%, 10/25/2021 | 159,403 | ||||||

| 134,276 | Series 1992-136, Class PK, | ||||||

| 6.00%, 08/25/2022 | 139,781 | ||||||

| 72,379 | Series 1993-32, Class H, | ||||||

| 6.00%, 03/25/2023 | 74,373 | ||||||

| 6,500,000 | Series 2002-85, Class PD, | ||||||

| 5.50%, 05/25/2031 | 6,632,129 | ||||||

| 2,457,185 | Series 2004-W6, Class 1A6, | ||||||

| 5.50%, 07/25/2034 | 2,284,120 | ||||||

| 4,050,000 | Series 2004-W10, Class A24, | ||||||

| 5.00%, 08/25/2034 | 3,993,016 | ||||||

| GMAC Mortgage | |||||||

| Corporation Loan Trust: | |||||||

| 154,933 | Series 2003-J1, Class A2, | ||||||

| 5.25%, 03/25/2018 | 157,421 | ||||||

| 1,418,314 | Series 2004-J4, Class A2, | ||||||

| 5.50%, 09/25/2034 | 1,332,141 | ||||||

| 389,314 | Government National | ||||||

| Mortgage Association | |||||||

| (GNMA), | |||||||

| Series 1999-4, Class ZB, | |||||||

| 6.00%, 02/20/2029 | 401,390 | ||||||

| J.P. Morgan Alternative | |||||||

| Loan Trust: | |||||||

| 3,363,682 | Series 2005-S1, Class 3A1, | ||||||

| 5.50%, 10/25/2020 | 2,622,623 | ||||||

| 1,299,269 | Series 2006-A1, Class 2A1, | ||||||

| 5.80%, 03/25/2036 | 650,997 | ||||||

| 2,691,777 | Series 2006-S2, Class A2, | ||||||

| 5.81%, 05/25/2036 | 2,151,578 | ||||||

| 746,443 | Lehman Mortgage Trust, | ||||||

| Series 2006-4, Class 3A1, | |||||||

| 5.00%, 08/25/2021 @ | 542,104 | ||||||

| Master Alternative | |||||||

| Loans Trust: | |||||||

| 2,105,726 | Series 2004-1, Class 1A1, | ||||||

| 5.00%, 01/25/2019 | 1,845,143 | ||||||

| 468,934 | Series 2004-3, Class 1A1, | ||||||

| 5.00%, 03/25/2019 | 410,903 | ||||||

| 268,825 | Series 2005-3, Class 4A1, | ||||||

| 5.50%, 03/25/2020 | 233,110 | ||||||

| 346,724 | Salomon Brothers | ||||||

| Mortgage Securities VII, | |||||||

| Series 2003-UP2, Class A2, | |||||||

| 4.00%, 06/25/2033 | 320,202 | ||||||

| Washington Mutual, Inc. | |||||||

| Pass-Thru Certificates: | |||||||

| 2,157,163 | Series 2004-CB1, | ||||||

| Class 5A, 5.00%, | |||||||

| 06/25/2019 | 2,105,930 | ||||||

| 3,057,898 | Series 2004-CB3, | ||||||

| Class 3A, 5.50%, | |||||||

| 10/25/2019 | 2,995,786 | ||||||

| 1,166,356 | Series 2004-CB3, | ||||||

| Class 4A, 6.00%, | |||||||

| 10/25/2019 | 1,000,151 | ||||||

| 745,649 | Series 2004-CB4, | ||||||

| Class 21A, 5.50%, | |||||||

| 12/25/2019 | 677,829 | ||||||

| 955,675 | Series 2004-CB4, | ||||||

| Class 22A, 6.00%, | |||||||

| 12/25/2019 | 880,054 | ||||||

| 74,703,219 | |||||||

The accompanying notes are an integral part of these financial statements.

Page 18

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Taxable Municipal Bonds – 0.5% | |||||||

| $ | 1,595,000 | Tobacco Settlement | |||||

| Authority Iowa, | |||||||

| 6.50%, 06/01/2023 | $ | 1,152,292 | |||||

| 708,752 | Tobacco Settlement | ||||||

| Financing Corporation, | |||||||

| Series 2001-A, Class A, | |||||||

| 6.36%, 05/15/2025 | 688,829 | ||||||

| 1,841,121 | |||||||

| Utilities – 5.6% | |||||||

| 2,415,000 | Baltimore Gas | ||||||

| & Electic Co., | |||||||

| 6.125%, 07/01/2013 | 2,234,493 | ||||||

| 1,715,000 | Cilcorp Inc. Senior Notes, | ||||||

| 8.70%, 10/15/2009 | 1,577,800 | ||||||

| 50,000 | Commonwealth Edison, | ||||||

| 5.95%, 08/15/2016 | 46,660 | ||||||

| Dominion Resources Inc.: | |||||||

| 450,000 | 6.25%, 06/30/2012 | 451,427 | |||||

| 1,000,000 | 5.15%, 07/15/2015 | 929,110 | |||||

| 600,000 | Energy Transfer Partners, | ||||||

| 5.65%, 08/01/2012 | 535,670 | ||||||

| 600,000 | Exelon Corporation | ||||||

| Senior Notes, | |||||||

| 6.75%, 05/01/2011 | 585,580 | ||||||

| 2,500,000 | Kinder Morgan Finance, | ||||||

5.70%, 01/05/2016 f | 1,862,500 | ||||||

| 315,054 | Kiowa Power Partners LLC, | ||||||

| 4.811%, 12/30/2013 | |||||||

| (Acquired 11/19/2004; | |||||||

| Cost $327,791)* | 294,575 | ||||||

| 300,000 | Korea Electric Power | ||||||

| Corporation, | |||||||

6.75%, 08/01/2027 f | 224,716 | ||||||

| 1,400,000 | National Grid PLC | ||||||

| Senior Unsecured Notes, | |||||||

6.30%, 08/01/2016 f | 1,219,896 | ||||||

| 25,000 | National Rural Utilities, | ||||||

| 4.375%, 10/01/2010 | 24,818 | ||||||

| 100,000 | NiSource Finance | ||||||

| Corporation, | |||||||

| 7.875%, 11/15/2010 | 91,509 | ||||||

| 400,000 | ONEOK, Inc. | ||||||

| Senior Notes, | |||||||

| 7.125%, 04/15/2011 | 376,435 | ||||||

| 1,800,000 | ONEOK Partners | ||||||

| LP Notes, | |||||||

| 5.90%, 04/01/2012 | 1,742,377 | ||||||

| 1,700,000 | PPL Energy Supply, LLC | ||||||

| Bonds, Series A, | |||||||

| 5.70%, 10/15/2015 | 1,400,866 | ||||||

| 388,000 | PPL Energy Supply, LLC | ||||||

| Senior Notes, | |||||||

| 6.40%, 11/01/2011 | 381,631 | ||||||

| 900,000 | Progress Energy, Inc. | ||||||

| Senior Notes, | |||||||

| 6.85%, 04/15/2012 | 902,557 | ||||||

| 175,000 | PSE&G Energy Holdings | ||||||

| LLC Senior Notes, | |||||||

| 8.50%, 06/15/2011 | 164,958 | ||||||

| PSE&G Power LLC: | |||||||

| 275,000 | 7.75%, 04/15/2011 | 274,684 | |||||

| 425,000 | 5.00%, 04/01/2014 | 381,331 | |||||

| 806,208 | RGS (I&M) Funding | ||||||

| Corporation Debentures, | |||||||

| 9.82%, 12/07/2022 | 952,518 | ||||||

| 1,500,000 | Rockies Express | ||||||

| Pipeline LLC, | |||||||

| 5.10%, 08/20/2009 | |||||||

| (Acquired 09/17/2007; | |||||||

| Cost $1,498,364)* | 1,500,744 | ||||||

| 1,400,000 | Spectra Energy Capital, | ||||||

| 5.668%, 08/15/2014 | 1,227,957 | ||||||

The accompanying notes are an integral part of these financial statements.

Page 19

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 97.1% (cont.) | |||||||

| Utilities – 5.6% (cont.) | |||||||

| $ | 1,340,000 | Transcontinental Gas | |||||

| Pipe Line Corporation | |||||||

| Senior Notes, | |||||||

| 8.875%, 07/15/2012 | $ | 1,307,697 | |||||

| Vectren Utility Holdings: | |||||||

| 900,000 | 6.625%, 12/01/2011 | 901,754 | |||||

| 525,000 | 5.250%, 08/01/2013 | 501,437 | |||||

| 600,000 | Williams Companies, Inc. | ||||||

| Notes, 8.125%, 03/15/2012 | 552,750 | ||||||

| 251,896 | Yosemite Securities Trust I, | ||||||

| 8.25%, 11/15/2004 | |||||||

| (Acquired 04/26/2001; | |||||||

| Cost $251,896) f @ | 630 | ||||||

| 22,649,080 | |||||||

| U.S. Government Agency Issues – 16.2% | |||||||

| Federal National Mortgage | |||||||

| Association (FNMA): | |||||||

| 17,950,000 | 6.00%, 05/15/2011 | 19,839,830 | |||||

| 43,500,000 | 3.625%, 02/12/2013 | 46,036,876 | |||||

| 65,876,706 | |||||||

| U.S. Treasury Obligations – 17.9% | |||||||

| 47,075,000 | U.S. Treasury Bonds, | ||||||

| 9.125%, 05/15/2018 | 72,800,734 | ||||||

| Total Long-Term | |||||||

| Investments | |||||||

| (Cost $422,868,516) | 394,014,194 | ||||||

| Shares | |||||||

| SHORT-TERM INVESTMENTS – 2.8% | |||||||

| Money Market Fund – 2.8% | |||||||

| 11,392,906 | Short-Term Investment | ||||||

| Company Liquid Assets | |||||||

| Portfolio - AIM Fund | 11,392,906 | ||||||

| Total Short-Term | |||||||

| Investments | |||||||

| (Cost $11,392,906) | 11,392,906 | ||||||

| Principal | |||||||

| Amount | |||||||

| INVESTMENTS PURCHASED | |||||||

| WITH CASH PROCEEDS FROM | |||||||

| SECURITIES LENDING – 34.7% | |||||||

| Certificates of Deposit – 6.3% | |||||||

| $ | 5,704,752 | Abbey National Treasury | |||||

| Service, Series YCD1, | |||||||

| 1.09%, 02/20/09 | 5,704,296 | ||||||

| 5,704,752 | Barclays Bank, | ||||||

| 3.3615%, 03/16/09 | 5,700,245 | ||||||

| Natixis Bank of New York, | |||||||

| Series YCD1: | |||||||

| 4,026,884 | 0.89%, 02/18/09 | 4,026,642 | |||||

| 3,355,737 | 0.89%, 06/30/09 | 3,361,240 | |||||

| 5,033,606 | Royal Bank of | ||||||

| Scotland Group PLC, | |||||||

| 2.9944%, 05/06/09 | 5,033,506 | ||||||

| 1,677,868 | Societe Generale of | ||||||

| New York, Series YCD1, | |||||||

| 2.0625%, 02/20/09 | 1,677,767 | ||||||

| 25,503,696 | |||||||

| Commercial Paper – 0.8% | |||||||

| 3,381,314 | Atlantic East | ||||||

| Funding, LLC, | |||||||

| 3.0588%, 03/25/09 # | 3,381,314 | ||||||

| 3,381,314 | |||||||

The accompanying notes are an integral part of these financial statements.

Page 20

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| INVESTMENTS PURCHASED | |||||||

| WITH CASH PROCEEDS FROM | |||||||

| SECURITIES LENDING – 34.7% (cont.) | |||||||

| Corporate Bonds and Notes – 3.4% | |||||||

| Allstate Life GL: | |||||||

| $ | 3,691,310 | 3.0575%, 03/20/09 | $ | 3,667,059 | |||

| 1,677,868 | 1.775%, 07/21/09 | 1,646,308 | |||||

| 3,355,737 | Svenska Handelsbanken, | ||||||

| 4.410%, 08/06/09 | 3,354,024 | ||||||

| 5,033,606 | Wachovia Bank NA, | ||||||

| 3.0013%, 05/01/09 | 4,978,184 | ||||||

| 13,645,575 | |||||||

| Government Agencies – 2.3% | |||||||

| 9,396,063 | Federal Home Loan Banks, | ||||||

| 0.645%, 03/02/09 | 9,390,707 | ||||||

| 9,390,707 | |||||||

| Shares | |||||||

| Investment Companies – 21.9% | |||||||

| 86,621,880 | Mount Vernon Securities | ||||||

| Lending Trust - | |||||||

| Prime Portfolio | 86,621,880 | ||||||

| 2,263,281 | Reserve Primary Fund # | 2,263,281 | |||||

| 88,885,161 | |||||||

| Total Investments | |||||||

| Purchased With Cash | |||||||

| Proceeds From | |||||||

| Securities Lending | |||||||

| (Cost $140,806,453) | 140,806,453 | ||||||

| Total Investments | |||||||

| (Cost $575,067,875) – | |||||||

| 134.6% | 546,213,553 | ||||||

| Other Liabilities in Excess | |||||||

| of Assets - (34.6)% | (140,280,853 | ) | |||||

| TOTAL NET | |||||||

| ASSETS - 100.0% | $ | 405,932,700 | |||||

| * | Restricted Security Deemed Liquid |

| f | Foreign Security |

| ^ | Non-Income Producing |

| # | Priced at Fair Value by the Valuation Committee as delegated by the Baird Funds’ Board of Directors |

| @ | Security in Default |

The accompanying notes are an integral part of these financial statements.

Page 21

Baird Intermediate Bond Fund

Schedule of Investments December 31, 2008 |

SFAS 157 – Summary of Fair Value Exposure at December 31, 2008

In September 2006, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 157, “Fair Value Measurements” (“SFAS 157”) effective for fiscal years beginning after November 15, 2007. SFAS 157 defines fair value, establishes a framework for measuring fair value in generally accepted accounting principles (GAAP), and expands disclosures about fair value measurements. The Fund adopted SFAS 157 as of January 1, 2008. Under SFAS 157, various inputs are used in determining the value of the Fund’s investments. These inputs are summarized into three broad levels and described below:

| Level 1 – | Quoted prices in active markets for identical securities |

| Level 2 – | Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| Level 3 – | Significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The following is a summary of the inputs used to value the Fund’s investments as of December 31, 2008:

| Description | Investments, at Value | |||

| Level 1 - Quoted prices | $ | 98,014,786 | ||

| Level 2 - Other significant observable inputs | 445,826,785 | |||

| Level 3 - Significant unobservable inputs | 2,371,982 | |||

| Total | $ | 546,213,553 | ||

Following is a reconciliation of Level 3 investments for which significant unobservable inputs were used to determine fair value.

| Investments, at Value | ||||

| Balance as of 12/31/07 | $ | 4,002,071 | ||

| Accrued discounts / premiums | — | |||

| Realized gain (loss) | — | |||

| Change in unrealized appreciation (depreciation) | — | |||

| Net purchases (sales/paydowns) | — | |||

| Transfers in and / or out of Level 3* | (1,630,089 | ) | ||

| Balance as of 12/31/08 | $ | 2,371,982 | ||

| * | The information used in the above reconciliation represents fiscal year to date activity for any investments identified as using Level 3 inputs at either the beginning or end of the current fiscal period. Transfers in or out of Level 3 represents either the beginning value (for transfers in) or ending value (for transfers out) of any security or instrument where a change in the pricing level occurred from the beginning to the end of the period. |

Page 22

Baird Aggregate Bond Fund

The Baird Aggregate Bond Fund seeks an annual rate of total return, before Fund expenses, greater than the annual rate of total return of the Barclays Capital Aggregate Bond Index. The Barclays Capital Aggregate Bond Index is an unmanaged, market value weighted index of investment grade, fixed-rate debt issues, including government, corporate, asset-backed and mortgage-backed securities, with maturities of at least one year.

Extreme volatility in the financial markets led to severely dislocated prices of bonds in several sectors that we believe do not reflect sound credit fundamentals. The Fund underperformed its benchmark index in 2008. The primary factors for the underperformance were:

| • | The Fund’s underweight to U.S. Treasuries which outperformed all other market sectors due to a flight to quality by investors; |

| • | Exposure to non-Agency mortgage-backed and asset-backed securities; and |

| • | The Fund’s overweighting to the finance sector relative to the benchmark. |

The Fund maintained its duration-neutral strategy, holding a broadly diversified portfolio of over 390 securities at year end.

The Fund ended 2008 with a yield advantage versus its benchmark index. Despite the unprecedented market volatility, we are confident of the integrity of the issues we hold and the structure of the Fund overall. We feel very strongly that the Fund will realize its sizeable yield advantage over time and outperform its benchmark through the completion of this historic and severe credit cycle.

Portfolio Characteristics

| Quality Distribution* | Sector Weightings* | ||||

|  | ||||

| Net Assets: | $871,870,881 | Annualized Expense Ratio: | |||

SEC 30-Day Yield:** | Institutional Class: | 0.30% | |||

| Institutional Class: | 6.16% | Investor Class: | 0.55% | *** | |

| Investor Class: | 5.92% | Portfolio Turnover Rate: | 21.91% | ||

| Average Effective Duration: | 3.71 years | Total Number of Holdings: | 392 | ||

| Average Effective Maturity: | 5.80 years | ||||

| * | Percentages shown are based on the Fund’s total net assets. |

| ** | SEC yields are based on SEC guidelines and are calculated for the 30 days ended December 31, 2008. |

| *** | Includes 0.25% 12b-1 fee. |

Page 23

Baird Aggregate Bond Fund

| Institutional Class |

| Value of a $25,000 Investment |

|

Growth of a hypothetical investment of $25,000 made on the Fund’s inception date (9/29/00), assuming reinvestment of all distributions.

| Investor Class |

| Value of a $10,000 Investment |

|

Growth of a hypothetical investment of $10,000 made on the Fund’s inception date (9/29/00), assuming reinvestment of all distributions.

Page 24

Baird Aggregate Bond Fund

Average Annual Total Returns

| Since | |||

| For the Periods Ended December 31, 2008 | One Year | Five Years | Inception(1) |

| Institutional Class Shares | -2.36% | 3.21% | 5.53% |

| Investor Class Shares | -2.63% | 2.99% | 5.29% |

Barclays Capital Aggregate Bond Index(2) | 5.24% | 4.65% | 6.08% |

| (1) | For the period from September 29, 2000 (commencement of operations) through December 31, 2008. |

| (2) | The Barclays Capital Aggregate Bond Index is an unmanaged, market value weighted index of investment grade, fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities, with maturities of at least one year. This index does not reflect any deduction for fees, expenses or taxes. A direct investment in an index is not possible. |

The returns shown in the table above and line graphs on the previous page reflect reinvestment of dividends and/or capital gains distributions in additional shares. The returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

For information about the performance of the Fund as of the most recent month-end, please call 1-866-44BAIRD or visit www.bairdfunds.com. Mutual fund performance changes over time and current performance may be lower or higher than that stated.

Page 25

Baird Aggregate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 94.8% | |||||||

| Asset Backed Securities – 6.2% | |||||||

| $ | 8,000,000 | American Express Credit | |||||

| Account Master Trust, | |||||||

| Series 2005-5, Class A, | |||||||

| 1.235%, 02/15/2013 | $ | 7,338,534 | |||||

| 2,000,000 | Bayview Financial | ||||||

| Acquisition Trust, | |||||||

| Series 2006-A, Class 1A2, | |||||||

| 5.483%, 02/28/2041 | 1,556,628 | ||||||

| Contimortgage Home | |||||||

| Equity Trust: | |||||||

| 95 | Series 1999-1, Class A7, | ||||||

| 6.97%, 12/25/2013 | 94 | ||||||

| 1,073 | Series 1997-2, Class A9, | ||||||

| 7.09%, 04/15/2028 | 1,072 | ||||||

| 12,440 | Series 1999-3, Class A8, | ||||||

| 1.03%, 05/25/2029 | 12,138 | ||||||

| Countrywide | |||||||

| Asset-Backed Certificates: | |||||||

| 4,100,000 | Series 2006-S2, Class A2, | ||||||

| 5.627%, 07/25/2027 | 3,165,909 | ||||||

| 1,865,261 | Series 2005-17, | ||||||

| Class 1AF2, 5.363%, | |||||||

| 05/25/2036 | 1,604,655 | ||||||

| 1,448,560 | Series 2004-15, | ||||||

| Class AF6, 4.613%, | |||||||

| 04/25/2035 | 1,367,016 | ||||||

| 4,889,002 | Series 2005-1, Class AF6, | ||||||

| 5.03%, 07/25/2035 | 3,478,210 | ||||||

| 4,999,048 | Series 2005-10, | ||||||

| Class AF6, 4.915%, | |||||||

| 02/25/2036 | 4,367,824 | ||||||

| 2,000,000 | Series 2005-17, | ||||||

| Class 1AF5, 5.564%, | |||||||

| 05/25/2036 | 1,261,275 | ||||||

| 2,923,601 | Series 2007-S1, Class A6, | ||||||

| 5.693%, 11/25/2036 | 1,256,254 | ||||||

| 7,000,000 | Series 2006-13, | ||||||

| Class 1AF2, 5.884%, | |||||||

| 01/25/2037 | 6,573,139 | ||||||

| 1,500,000 | Series 2006-10, | ||||||

| Class 1AF3, 5.971%, | |||||||

| 09/25/2046 | 1,339,083 | ||||||

| 1,124,263 | Credit-Based Asset | ||||||

| Servicing and Securities, | |||||||

| Series 2005-CB8, | |||||||

| Class AF2, 5.303%, | |||||||

| 12/25/2035 | 1,015,580 | ||||||

| Discover Card | |||||||

| Master Trust I: | |||||||

| 2,000,000 | Series 2004-2, Class A2, | ||||||

| 1.26%, 05/15/2012 | 1,619,084 | ||||||

| 1,700,000 | Series 2003-4,Class A2, | ||||||

| 1.38%, 05/15/2013 | 1,778,561 | ||||||

| 257,385 | Equivantage Home | ||||||

| Equity Loan Trust, | |||||||

| Series 1996-3, Class A3, | |||||||

| 7.70%, 09/25/2027 | 202,888 | ||||||

| GE Capital Mortgage | |||||||

| Services, Inc.: | |||||||

| 2,777 | Series 1997-HE4, Class A7, | ||||||

| 6.735%, 12/25/2028 | 2,773 | ||||||

| 36,788 | Series 1999-HE1, Class A7, | ||||||

| 6.265%, 04/25/2029 | 36,721 | ||||||

| 193,597 | GMAC Mortgage | ||||||

| Corporation Loan Trust, | |||||||

| Series 2004-GH1, | |||||||

| Class A2, 4.39%, | |||||||

| 12/25/2025 | 188,046 | ||||||

| Green Tree Financial | |||||||

| Corporation: | |||||||

| 833,912 | Series 1993-3, Class A7, | ||||||

| 6.40%, 10/15/2018 | 746,689 | ||||||

The accompanying notes are an integral part of these financial statements.

Page 26

Baird Aggregate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 94.8% (cont.) | |||||||

| Asset Backed Securities – 6.2% (cont.) | |||||||

| $ | 857,029 | Series 1993-4, Class A5, | |||||

| 7.05%, 01/15/2019 | $ | 741,629 | |||||

| 2,091,712 | Series 1998-2, Class A5, | ||||||

| 6.24%, 12/01/2028 | 1,585,953 | ||||||

| 149,313 | Series 1997-6, Class A8, | ||||||

| 7.07%, 01/15/2029 | 126,717 | ||||||

| 1,702,000 | Series 1998-3, Class A5, | ||||||

| 6.22%, 03/01/2030 | 1,237,163 | ||||||

| 1,022,427 | Series 1998-4, Class A5, | ||||||

| 6.18%, 04/01/2030 | 655,439 | ||||||

| 1,377,024 | GSAA Home Equity Trust, | ||||||

| Series 2005-1, Class AF2, | |||||||

| 4.316%, 11/25/2034 | 1,254,476 | ||||||

| 132,762 | IMC Home Equity | ||||||

| Loan Trust, | |||||||

| Series 1997-5, Class A10, | |||||||

| 5.749%, 11/20/2028 | 132,459 | ||||||

| 229,735 | Impac CMB Trust, | ||||||

| Series 2004-4, Class 2A2, | |||||||

| 5.75%, 09/25/2034 | 202,984 | ||||||

| 3,200,000 | MBNA Master | ||||||

| Credit Card Trust, | |||||||

| Series 2005 A4, Class A4, | |||||||

| 1.24%, 11/15/2012 | 2,949,889 | ||||||

| 97,478 | Oakwood Mortgage | ||||||

| Investors, Inc., | |||||||

| Series 1999-B, Class A3, | |||||||

| 6.45%, 11/15/2017 | 64,813 | ||||||

| RAAC Series: | |||||||

| 10,443 | Series 2004-SP1, | ||||||

| Class AI2, 4.38%, | |||||||

| 01/25/2022 | 10,358 | ||||||

| 1,156,267 | Series 2004-SP1, | ||||||

| Class AI4, 5.285%, | |||||||

| 08/25/2027 | 931,261 | ||||||

| 3,000,000 | Renaissance Home Equity | ||||||

| Loan Trust, Series 2007-1, | |||||||

| Class AF3, 5.612%, | |||||||

| 04/25/2037 | 1,593,374 | ||||||

| Residential Asset | |||||||

| Mortgage Products, Inc.: | |||||||

| 1,387,455 | Series 2003-RS7, Class | ||||||

| AI6, 5.34%, 08/25/2033 | 1,299,483 | ||||||

| 928,669 | Series 2005-RS1, | ||||||

| Class AI6, 4.713%, | |||||||

| 01/25/2035 | 693,704 | ||||||

| Residential Asset | |||||||

| Securities Corporation: | |||||||

| 270,613 | Series 2003-KS5, | ||||||

| Class AI6, 3.62%, | |||||||

| 07/25/2033 | 164,680 | ||||||

| 267,676 | Series 2004-KS2, | ||||||

| Class AI6, 4.30%, | |||||||

| 03/25/2034 | 193,209 | ||||||

| 2,600,000 | Stingray | ||||||

| Pass-Thru Certificates, | |||||||

| Series 2005, 5.902%, | |||||||

| 01/12/2015 (Acquired | |||||||

| 05/10/2007 and | |||||||

| 09/19/2007; Cost | |||||||

| $1,533,934 and $803,343, | |||||||

| respectively)* # | 390,000 | ||||||

| Structured Asset | |||||||

| Securities Corporation: | |||||||

| 109,917 | Series 2004-11XS, | ||||||

| Class 1A3A, 4.76%, | |||||||

| 06/25/2034 | 109,606 | ||||||

| 1,445,095 | Series 2005-7XS, | ||||||

| Class 1A4B, 5.44%, | |||||||

| 04/25/2035 | 1,090,627 | ||||||

| 54,339,997 | |||||||

The accompanying notes are an integral part of these financial statements.

Page 27

Baird Aggregate Bond Fund

Schedule of Investments December 31, 2008 |

| Principal | |||||||

| Amount | Value | ||||||

| LONG-TERM INVESTMENTS – 94.8% (cont.) | |||||||

| Financial – 15.5% | |||||||

| $ | 2,450,000 | American Express Credit | |||||

| Corporation, Series C, | |||||||

| 7.30%, 08/20/2013 | $ | 2,507,800 | |||||

| American General | |||||||

| Finance Corporation | |||||||

| Senior Notes: | |||||||

| 1,250,000 | 8.45%, 10/15/2009 | 900,012 | |||||

| 1,150,000 | 4.875%, 05/15/2010 | 684,426 | |||||

| 1,000,000 | 5.85%, 06/01/2013 | 379,814 | |||||

| 500,000 | 6.90%, 12/15/2017 | 216,386 | |||||

| 1,000,000 | American International | ||||||

| Group, 8.175%, | |||||||

| 05/15/2058 (Callable | |||||||

| 05/15/2038) (Acquired | |||||||

| 05/13/2008; | |||||||

| Cost $1,000,000)* | 389,025 | ||||||

| 250,000 | AmSouth Bancorporation | ||||||

| Subordinated Debentures, | |||||||

| 6.75%, 11/01/2025 | 220,984 | ||||||

| 300,000 | BAC Capital Trust VI, | ||||||

| 5.625%, 03/08/2035 | 252,026 | ||||||

| 1,065,000 | Bank of America | ||||||

| Corporation | |||||||

| Subordinated Notes, | |||||||

| 10.20%, 07/15/2015 | 1,168,137 | ||||||

| 1,435,000 | Bank of Tokyo- | ||||||

| Mitsubishi UFJ NY, | |||||||

7.40%, 06/15/2011 f | 1,389,268 | ||||||

| 929,000 | Bank One Corporation | ||||||

| Subordinated Notes, | |||||||

| 10.00%, 08/15/2010 | 978,941 | ||||||

| 2,175,000 | Banponce Trust I, | ||||||

| Series A, 8.327%, | |||||||

| 02/01/2027 (Callable | |||||||

| 03/02/2009) | 1,794,832 | ||||||

| 2,400,000 | Bear Stearns Cos., | ||||||

| Inc., Series B, | |||||||

| 6.95%, 08/10/2012 | 2,492,575 | ||||||

| 1,500,000 | BOI Capital | ||||||

| Funding No. 2, | |||||||

| 5.571%, 02/01/2016 | |||||||

| (Acquired 09/03/2008; | |||||||

Cost $966,760)* f | 329,710 | ||||||

| 2,000,000 | BOI Capital | ||||||

| Funding No. 3, | |||||||

| 6.107%, 02/04/2016 | |||||||

| (Acquired 08/25/2008 | |||||||

| and 08/26/2008; | |||||||