Western Investment LLC (“Western Investment”), together with the other participants named herein, is filing materials contained in this Schedule 14A with the Securities and Exchange Commission (the “SEC”) in connection with the solicitation of proxies by Western Investment at the 2010 annual meeting of shareholders (the “Annual Meeting”) of DWS Dreman Value Income Edge Fund, Inc. (the “Fund”). Western Investment has filed a definitive proxy statement with the SEC with regard to the Annual Meeting.

Item 1: On April 27, 2010, Western Investment delivered the following letter to shareholders of the Fund:

DEUTSCHE SHOULD NOT BE MANAGING YOUR FUND. VOTE WITH

WESTERN INVESTMENT TO HELP MAKE THAT HAPPEN

Dear Fellow Shareholder:

We have lost all confidence in Deutsche Investment Management Americas Inc. (“Deutsche”), the investment advisor for your Fund, and its handpicked Board of Directors. We believe Deutsche’s history clearly shows it is unfit to manage closed-end funds. They disdain the most basic principles of American democracy.

This solicitation is an important step in Western Investment’s campaign to oust Deutsche from managing U.S. closed-end funds. Please vote the GOLD proxy. Together we will knock down the undemocratic hurdles erected by Deutsche and its board, which are designed to block YOU from exercising your basic voting rights as shareholders.

Western Investment is the largest shareholder of DWS Dreman Value Income Edge Fund, Inc. (the “Fund”). We are seeking your support on the GOLD proxy card FOR the election of four INDEPENDENT nominees to the Fund’s Board of Directors. Our group currently owns over 11.2% of the Fund’s shares.

We are investors specializing in investing in closed-end funds. In addition to our investment in the Fund, we have large investments in other funds managed or controlled by Deutsche, a subsidiary of Deutsche Bank AG, the German banking conglomerate. Deutsche is taking advantage of YOU and its other shareholders in its closed-end funds, maximizing its profits at YOURS and their expense.

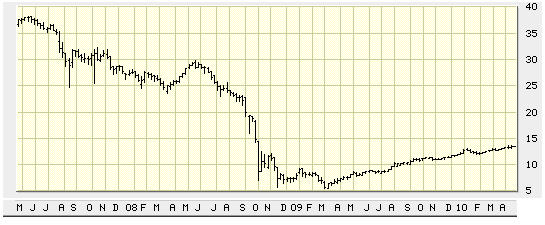

UNACCEPTABLE PERFORMANCE: Deutsche has utterly failed the Fund’s shareholders. Original investors in the Fund have lost two-thirds of their investment. The Fund trades at unacceptably steep discounts to its net asset value, a situation that disadvantages shareholders and is exacerbated by the Board and Deutsche’s apparent do-nothing strategy.

This picture tells the story:

Shareholders paid (split-adjusted) $40 per share in the Fund’s public offering. It is trading today at about $13.50. The Fund has had a negative -19.19% annualized return. Since inception, the Fund’s total return has been a negative -51.33%.

DEUTSCHE BANK AG HAS NUMEROUS SEC AND LEGAL PROBLEMS AND

SHOULD NOT BE MANAGING SHAREHOLDERS’ INVESTMENTS

Only your vote can stop Deutsche from exploiting this Fund for its own benefit as it has with so many others. We are reaching out to shareholders of a number of Deutsche managed funds to share our concerns that Deutsche is unfit to manage closed-end funds. These include

| | · | DWS High Income Trust (KHI); |

| | · | DWS Strategic Income Trust (KST); |

| | · | DWS Multi-Market Income Trust (KMM); |

| | · | DWS Enhanced Commodity Strategy Fund, Inc. (GCS); |

| | · | DWS RREEF World Real Estate & Tactical Strategies Fund, Inc. (DRP); and |

| | · | DWS Global High Income Fund, Inc. (LBF). |

We have never felt compelled to take such widespread action before. However, we believe that the actions by this Board and Deutsche can no longer be tolerated.

Consider lowlights of Deutsche Bank AG’s troubled history:

| | · | Since 2003, Deutsche Bank AG and its affiliates has been censured by the SEC three times – |

| | o | For trading “proxy votes” for banking business. |

| | · | An affiliate of Deutsche, in an agreement with the Attorney General of the State of New York, paid $250 million and reduced advisory fees to settle charges arising from the adverse effects of “market–timing” relationships this affiliate had with select trading partners, allowing it to make essentially riskless trades at the expense of its mutual fund clients. |

| | · | Deutsche liquidated two of the Fund’s sister funds, DWS RREEF Real Estate Fund, Inc. (“SRQ”) and DWS RREEF Real Estate Fund II, Inc. (“SRO”), in the face of losses of 88% and 95%, respectively, of their net asset values. |

| | · | An affiliate of Deutsche received a cease and desist order from the West Virginia Securities Commissioner in connection with its marketing and sales of auction rate securities. |

| | · | Deutsche and its affiliates are the subject of numerous lawsuits, most brought by its own fund shareholders, including Western Investment LLC, over the management of the Fund and Deutsche’s market timing activities. |

DO YOU TRUST DEUTSCHE TO MANAGE YOUR INVESTMENT?

The Fund’s Handpicked Board: Stacking the Deck Against You. While the Fund’s shareholders were being punished with miserable performance, its Directors have done quite well. Each of the Fund’s Directors serve on the boards of at least 126 other funds in Deutsche’s fund complex and receive directors’ fees of over $200,000 per year. While the Fund has only been in business for three and a half years, the directors have served Deutsche for far longer. Their average servitude to Deutsche is 13.5 years. Under these conditions, we do not believe they can maintain their impartiality and true independence. We question their ability to decide matters that may benefit shareholders of the Fund, but that may negatively impact Deutsche and its fee income.

SHOULDN’T THE FUND HAVE AT LEAST A MINORITY OF DIRECTORS WITH NO TIES TO DEUTSCHE AND ITS OTHER CLOSED-END FUNDS, AND WHOSE SOLE ALLEGIANCE IS TO THE SHAREHOLDERS?

The Fund has a history of disregarding best practice corporate governance recommendations, which is indicative of a board that does not place shareholders’ interests first. The Fund has enacted a number of hurdles to dilute shareholders’ voting rights at Fund elections. This damages shareholders and protects the incumbency of Deutsche and its captive directors. These hurdles include:

| | · | Implementing an absolute majority vote rule in contested elections; and |

| | · | Preventing some shareholders from voting all of their shares. |

Many of you bought shares when the Fund went public three and a half years ago. At that time, the entire Board was elected each year by the vote of the majority of shares represented at the annual shareholders meeting. However, following the Fund’s poor performance, we believe Deutsche and the directors realized the risk that they could be replaced by a shareholder vote. So they changed the rules. First, they amended the By-laws so that shareholders are now permitted to elect only one-third of the Board each year, and extended their terms to 3 years. However, even that proved to be insufficient. Next, in early 2009, they amended the By-laws again. The By-laws were amended to require the vote of a majority of all of the Fund’s shares outstanding, not just the shares represented at the annual shareholders meeting, to elect directors. It sounds innocuous, but the difference is crucial. It almost guarantees that if a shareholder nominates candidates for the Board and campaigns for their election, as we are doing here, neither side will gain the votes needed for election. Should that happen, the incumbents simply retain their seats as holdovers, even if they were out-voted. This is precisely what happened at GCS, another Deutsche closed-end fund. There, the entire Deutsche board has remained in office since 2008, even though Western Investment’s nominees received more votes than the incumbents by a vast margin at the 2008 annual meeting. Since then, Deutsche and its board, not wishing to risk the repeat of that embarrassment, have simply skipped holding another annual meeting. These unelected GCS incumbents are th e same directors who serve on this Board and whom you can oust by voting the GOLD proxy. Most recently, Deutsche adopted a state law provision to limit Western Investment’s right to vote its GCS shares. Will Deutsche and the incumbent board do anything to prevent shareholders from having a meaningful right to vote? We must vote them out, now. Please vote the GOLD proxy.

We are not the only ones who believe that the Fund’s corporate governance practices prevent shareholders from fully exercising their rights. Deutsche’s own Global Proxy Voting Guideline “is to vote against proposals to classify the board and for proposals to repeal classified boards and elect directors annually” because “directors should be held accountable on an annual basis. By entrenching the incumbent board, a classified board may be used as an anti-takeover device to the detriment of the shareholders in a hostile take-over situation.” Amazingly and against their own global guidelines, which apparently do not apply to closed-end funds, the Fund chose to classify the Board in March 2009. WHAT HYPOCRITES!

THIS BOARD HAS TRASHED GOOD GOVERNANCE PRINCIPLES AND SOLIDLY ENTRENCHED ITSELF WITHOUT A SINGLE SHAREHOLDER VOTE!