UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-21563

Eaton Vance Short Duration Diversified Income Fund

(Exact Name of Registrant as Specified in Charter)

Two International Place, Boston, Massachusetts 02110

(Address of Principal Executive Offices)

Maureen A. Gemma

Two International Place, Boston, Massachusetts 02110

(Name and Address of Agent for Services)

(617) 482-8260

(Registrant’s Telephone Number)

October 31

Date of Fiscal Year End

April 30, 2021

Date of Reporting Period

| Item 1. | Reports to Stockholders |

Eaton Vance

Short Duration Diversified Income Fund (EVG)

Semiannual Report

April 30, 2021

Commodity Futures Trading Commission Registration. The Commodity Futures Trading Commission (“CFTC”) has adopted regulations that subject registered investment companies and advisers to regulation by the CFTC if a fund invests more than a prescribed level of its assets in certain CFTC-regulated instruments (including futures, certain options and swap agreements) or markets itself as providing investment exposure to such instruments. The investment adviser has claimed an exclusion from the definition of “commodity pool operator” under the Commodity Exchange Act with respect to its management of the Fund. Accordingly, neither the Fund nor the adviser with respect to the operation of the Fund is subject to CFTC regulation. Because of its management of other strategies, the Fund’s adviser is registered with the CFTC as a commodity pool operator and a commodity trading advisor.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

Semiannual Report April 30, 2021

Eaton Vance

Short Duration Diversified Income Fund

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Performance1,2

Portfolio Managers Catherine C. McDermott, Andrew Szczurowski, CFA, Eric Stein, CFA and Sarah C. Orvin, CFA

| | | | | | | | | | | | | | | | | | | | |

| % Average Annual Total Returns | | Inception Date | | | Six Months | | | One Year | | | Five Years | | | Ten Years | |

| | | | | |

Fund at NAV | | | 02/28/2005 | | | | 7.58 | % | | | 21.66 | % | | | 5.14 | % | | | 4.12 | % |

Fund at Market Price | | | — | | | | 16.18 | | | | 26.41 | | | | 6.79 | | | | 4.73 | |

|

| |

| | | | | |

Blended Index | | | — | | | | 4.66 | % | | | 13.01 | % | | | — | | | | — | |

| | | | | |

| % Premium/Discount to NAV3 | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | | | –3.27 | % |

| | | | | |

| Distributions4 | | | | | | | | | | | | | | | |

| | | | | |

Total Distributions per share for the period | | | | | | | | | | | | | | | | | | $ | 0.450 | |

Distribution Rate at NAV | | | | | | | | | | | | | | | | | | | 6.55 | % |

Distribution Rate at Market Price | | | | | | | | | | | | | | | | | | | 6.77 | |

| | | | | |

| % Total Leverage5 | | | | | | | | | | | | | | | |

| | | | | |

Derivatives | | | | | | | | | | | | | | | | | | | 20.89 | % |

Borrowings | | | | | | | | | | | | | | | | | | | 7.56 | |

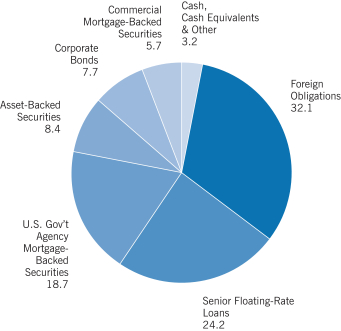

Fund Profile

Asset Allocation (% of total leveraged assets)6

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees and other expenses by determining the percentage change in net asset value (NAV) or market price (as applicable) with all distributions reinvested in accordance with the Fund’s Dividend Reinvestment Plan. Performance at market price will differ from performance at NAV due to variations in the Fund’s market price versus NAV, which may reflect factors such as fluctuations in supply and demand for Fund shares, changes in Fund distributions, shifting market expectations for the Fund’s future returns and distribution rates, and other considerations affecting the trading prices of closed-end funds. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Endnotes and Additional Disclosures

| 1 | S&P/LSTA Leveraged Loan Index is an unmanaged index of the institutional leveraged loan market. S&P/LSTA Leveraged Loan indices are a product of S&P Dow Jones Indices LLC (“S&P DJI”) and have been licensed for use. S&P® is a registered trademark of S&P DJI; Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); LSTA is a trademark of Loan Syndications and Trading Association, Inc. S&P DJI, Dow Jones, their respective affiliates and their third party licensors do not sponsor, endorse, sell or promote the Fund, will not have any liability with respect thereto and do not have any liability for any errors, omissions, or interruptions of the S&P Dow Jones Indices. ICE BofA U.S. Mortgage-Backed Securities Index is an unmanaged index of fixed rate residential mortgage pass-through securities issued by U.S. agencies. ICE® BofA® indices are not for redistribution or other uses; provided “as is”, without warranties, and with no liability. Eaton Vance has prepared this report and ICE Data Indices, LLC does not endorse it, or guarantee, review, or endorse Eaton Vance’s products. BofA® is a licensed registered trademark of Bank of America Corporation in the United States and other countries. The J.P. Morgan Emerging Market Bond Index (EMBI) Global Diversified Spread is the spread component of the J.P. Morgan EMBI Global Diversified. J.P. Morgan EMBI Global Diversified is a market-cap weighted index that measures USD-denominated Brady Bonds, Eurobonds, and traded loans issued by sovereign entities. The J.P. Morgan EMBI Global Diversified Spread commenced on July 27, 2016; accordingly, the Five and Ten Years returns are not available. Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. The Index is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright 2021, J.P. Morgan Chase & Co. All rights reserved. The Blended Index consists of 33.33% S&P/LSTA Leveraged Loan Index, 33.33% ICE BofA U.S. Mortgage-Backed Securities Index and 33.34% J.P. Morgan Emerging Market Bond Index (EMBI) Global Diversified Spread, rebalanced monthly. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. |

| 2 | Performance results reflect the effects of leverage. Absent an expense waiver by the investment adviser, if applicable, the returns would be lower. |

| 3 | The shares of the Fund often trade at a discount or premium to their net asset value. The discount or premium may vary over time and may be higher or lower than what is quoted in this report. For up-to-date premium/discount information, please refer to https://funds.eatonvance.com/closed-end-fund-prices.php. |

| 4 | The Distribution Rate is based on the Fund’s last regular distribution per share in the period (annualized) divided by the Fund’s NAV or market price at the end of the period. The Fund’s distributions may be comprised of amounts characterized for federal income tax purposes as qualified and non-qualified ordinary dividends, capital gains and nondividend distributions, also known as return of capital. The Fund will determine the federal income tax character of distributions paid to a shareholder after the end of the calendar year. This is reported on the IRS form 1099-DIV and provided to the shareholder shortly after each year-end. For information about the tax character of distributions made in prior calendar years, please refer to Performance-Tax Character of Distributions on the Fund’s webpage available at eatonvance.com. The Fund’s distributions are determined by the investment adviser. Fund distributions may be affected by numerous factors including changes in Fund performance, the cost of financing for leverage, portfolio holdings, realized and projected returns, and other factors. As portfolio and market conditions change, the rate of distributions paid by the Fund could change. |

| 5 | The Fund employs leverage through derivatives and borrowings. Total leverage is shown as a percentage of the Fund’s aggregate net assets plus the absolute notional value of long and short derivatives and borrowings outstanding. Use of leverage creates an opportunity for income, but creates risks including greater price volatility. The cost of borrowings rises and falls with changes in short-term interest rates. The Fund may be required to maintain prescribed asset coverage for its leverage and may be required to reduce its leverage at an inopportune time. |

| 6 | Total leveraged assets include all assets of the Fund (including those acquired with financial leverage) and derivatives held by the Fund. Asset Allocation as a percentage of the Fund’s net assets amounted to 139.8%. Please refer to the definition of total leveraged assets within the Notes to Financial Statements included herein. |

Fund profile subject to change due to active management.

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited)

| | | | | | | | | | |

| Asset-Backed Securities — 11.8% | |

| Security | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

AMMC CLO 15, Ltd., Series 2014-15A, Class ERR, 7.094%, (3 mo. USD LIBOR + 6.91%), 1/15/32(1)(2) | | | | $ | 2,000 | | | $ | 1,972,946 | |

| | | |

AMMC CLO XII, Ltd., Series 2013-12A, Class ER, 6.375%, (3 mo. USD LIBOR + 6.18%), 11/10/30(1)(2) | | | | | 1,000 | | | | 912,621 | |

| | | |

Ares LII CLO, Ltd., Series 2019-52A, Class E, 6.734%, (3 mo. USD LIBOR + 6.55%), 4/22/31(1)(2) | | | | | 1,000 | | | | 1,000,613 | |

| | | |

Ares XXXIIR CLO, Ltd., Series 2014-32RA, Class D, 6.044%, (3 mo. USD LIBOR + 5.85%), 5/15/30(1)(2) | | | | | 1,000 | | | | 980,052 | |

| | | |

BlueMountain CLO XXIV, Ltd., Series 2019-24A, Class E, 6.948%, (3 mo. USD LIBOR + 6.76%), 4/20/31(1)(2) | | | | | 1,250 | | | | 1,251,564 | |

|

| Carlyle Global Market Strategies CLO, Ltd.: | |

| | | |

Series 2012-3A, Class DR2, 6.686%, (3 mo. USD LIBOR + 6.50%), 1/14/32(1)(2) | | | | | 2,000 | | | | 1,898,576 | |

| | | |

Series 2014-4RA, Class D, 5.834%, (3 mo. USD LIBOR + 5.65%), 7/15/30(1)(2) | | | | | 1,000 | | | | 906,906 | |

| | | |

Series 2015-5A, Class DR, 6.888%, (3 mo. USD LIBOR + 6.70%), 1/20/32(1)(2) | | | | | 1,000 | | | | 957,124 | |

| | | |

Galaxy XV CLO, Ltd., Series 2013-15A, Class ER, 6.829%, (3 mo. USD LIBOR + 6.65%), 10/15/30(1)(2) | | | | | 1,440 | | | | 1,416,898 | |

| | | |

Galaxy XXI CLO, Ltd., Series 2015-21A, Class ER, 5.438%, (3 mo. USD LIBOR + 5.25%), 4/20/31(1)(2) | | | | | 1,000 | | | | 950,446 | |

| | | |

Galaxy XXV CLO, Ltd., Series 2018-25A, Class E, 6.126%, (3 mo. USD LIBOR + 5.95%), 10/25/31(1)(2) | | | | | 1,250 | | | | 1,208,169 | |

| | | |

Golub Capital Partners CLO 22B, Ltd., Series 2015-22A, Class ER, 6.188%, (3 mo. USD LIBOR + 6.00%), 1/20/31(1)(2) | | | | | 2,000 | | | | 1,848,968 | |

| | | |

Golub Capital Partners CLO 23M, Ltd., Series 2015-23A, Class ER, 5.938%, (3 mo. USD LIBOR + 5.75%), 1/20/31(1)(2) | | | | | 2,000 | | | | 1,853,946 | |

| | | |

Madison Park Funding XXV, Ltd., Series 2017-25A, Class D, 6.276%, (3 mo. USD LIBOR + 6.10%), 4/25/29(1)(2) | | | | | 3,000 | | | | 2,986,968 | |

| | | |

Neuberger Berman CLO XVIII, Ltd., Series 2014-18A, Class DR2, 6.106%, (3 mo. USD LIBOR + 5.92%), 10/21/30(1)(2) | | | | | 3,000 | | | | 2,952,546 | |

| | | |

Palmer Square CLO, Ltd., Series 2013-2A, Class DRR, 6.04%, (3 mo. USD LIBOR + 5.85%), 10/17/31(1)(2) | | | | | 2,000 | | | | 1,969,976 | |

| | | |

Regatta IX Funding, Ltd., Series 2017-1A, Class E, 6.19%, (3 mo. USD LIBOR + 6.00%), 4/17/30(1)(2) | | | | | 2,000 | | | | 1,967,174 | |

| | | | | | | | | | |

| Security | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

Voya CLO, Ltd., Series 2015-3A, Class DR, 6.388%, (3 mo. USD LIBOR + 6.20%), 10/20/31(1)(2) | | | | $ | 2,000 | | | $ | 1,897,390 | |

| |

Total Asset-Backed Securities

(identified cost $29,324,901) | | | $ | 28,932,883 | |

|

| Collateralized Mortgage Obligations — 10.8% | |

| Security | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

| Federal Home Loan Mortgage Corp.: | | | | | | | | |

| | | |

Series 2113, Class QG, 6.00%, 1/15/29 | | | | $ | 285 | | | $ | 319,129 | |

| | | |

Series 2167, Class BZ, 7.00%, 6/15/29 | | | | | 283 | | | | 319,641 | |

| | | |

Series 2182, Class ZB, 8.00%, 9/15/29 | | | | | 449 | | | | 514,629 | |

| | | |

Series 4273, Class PU, 4.00%, 11/15/43 | | | | | 420 | | | | 448,859 | |

| | | |

Series 4337, Class YT, 3.50%, 4/15/49 | | | | | 311 | | | | 310,876 | |

| | | |

Series 4452, Class ZJ, 3.00%, 11/15/44 | | | | | 1,180 | | | | 1,184,818 | |

| | | |

Series 4608, Class TV, 3.50%, 1/15/55 | | | | | 790 | | | | 796,728 | |

| | | |

Series 4626, Class UZ, 3.50%, 1/15/55 | | | | | 498 | | | | 499,493 | |

| | | |

Series 4774, Class QD, 4.50%, 1/15/43 | | | | | 277 | | | | 278,340 | |

| | | |

Series 4980, Class ZP, 2.50%, 7/25/49 | | | | | 472 | | | | 472,372 | |

| | | |

Series 5035, Class AZ, 2.00%, 11/25/50 | | | | | 1,260 | | | | 1,211,447 | |

| | | |

| Interest Only:(3) | | | | | | | | |

| | | |

Series 362, Class C7, 3.50%, 9/15/47 | | | | | 2,061 | | | | 245,541 | |

| | | |

Series 2631, Class DS, 6.985%, (7.10% - 1 mo. USD LIBOR), 6/15/33(4) | | | | | 530 | | | | 73,476 | |

| | | |

Series 2770, Class SH, 6.985%, (7.10% - 1 mo. USD LIBOR), 3/15/34(4) | | | | | 857 | | | | 196,225 | |

| | | |

Series 2981, Class CS, 6.605%, (6.72% - 1 mo. USD LIBOR), 5/15/35(4) | | | | | 474 | | | | 90,223 | |

| | | |

Series 3114, Class TS, 6.535%, (6.65% - 1 mo. USD LIBOR), 9/15/30(4) | | | | | 1,041 | | | | 148,430 | |

| | | |

Series 3339, Class JI, 6.475%, (6.59% - 1 mo. USD LIBOR), 7/15/37(4) | | | | | 1,531 | | | | 311,946 | |

| | | |

Series 4109, Class ES, 6.035%, (6.15% - 1 mo. USD LIBOR), 12/15/41(4) | | | | | 32 | | | | 7,443 | |

| | | |

Series 4121, Class IM, 4.00%, 10/15/39 | | | | | 508 | | | | 4,413 | |

| | | |

Series 4163, Class GS, 6.085%, (6.20% - 1 mo. USD LIBOR), 11/15/32(4) | | | | | 2,296 | | | | 411,214 | |

| | | |

Series 4169, Class AS, 6.135%, (6.25% - 1 mo. USD LIBOR), 2/15/33(4) | | | | | 1,228 | | | | 211,844 | |

| | | |

Series 4180, Class GI, 3.50%, 8/15/26 | | | | | 591 | | | | 21,332 | |

| | | |

Series 4203, Class QS, 6.135%, (6.25% - 1 mo. USD LIBOR), 5/15/43(4) | | | | | 1,097 | | | | 170,509 | |

| | | |

Series 4332, Class KI, 4.00%, 9/15/43 | | | | | 237 | | | | 10,201 | |

| | | |

Series 4370, Class IO, 3.50%, 9/15/41 | | | | | 423 | | | | 23,610 | |

| | | |

Series 4497, Class CS, 6.085%, (6.20% - 1 mo. USD LIBOR), 9/15/44(4) | | | | | 874 | | | | 87,757 | |

| | | | |

| | 4 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | |

| Security | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

| Interest Only:(3) (continued) | | | | | | | | |

| | | |

Series 4507, Class EI, 4.00%, 8/15/44 | | | | $ | 1,805 | | | $ | 215,810 | |

| | | |

Series 4535, Class JS, 5.985%, (6.10% - 1 mo. USD LIBOR), 11/15/43(4) | | | | | 769 | | | | 29,432 | |

| | | |

Series 4548, Class JS, 5.985%, (6.10% - 1 mo. USD LIBOR), 9/15/43(4) | | | | | 778 | | | | 24,130 | |

| | | |

Series 4629, Class QI, 3.50%, 11/15/46 | | | | | 1,339 | | | | 126,280 | |

| | | |

Series 4644, Class TI, 3.50%, 1/15/45 | | | | | 986 | | | | 76,241 | |

| | | |

Series 4653, Class PI, 3.50%, 7/15/44 | | | | | 432 | | | | 3,334 | |

| | | |

Series 4667, Class PI, 3.50%, 5/15/42 | | | | | 1,137 | | | | 30,594 | |

| | | |

Series 4676, Class DI, 4.00%, 7/15/44 | | | | | 936 | | | | 24,555 | |

| | | |

Series 4744, Class IO, 4.00%, 11/15/47 | | | | | 1,100 | | | | 154,178 | |

| | | |

Series 4749, Class IL, 4.00%, 12/15/47 | | | | | 843 | | | | 118,197 | |

| | | |

Series 4767, Class IM, 4.00%, 5/15/45 | | | | | 590 | | | | 15,826 | |

| | | |

Series 4768, Class IO, 4.00%, 3/15/48 | | | | | 1,014 | | | | 142,879 | |

| | | |

Series 4772, Class PI, 4.00%, 1/15/48 | | | | | 734 | | | | 102,294 | |

| | | |

Series 4966, Class SY, 5.944%, (6.05% - 1 mo. USD LIBOR), 4/25/50(4) | | | | | 3,501 | | | | 628,388 | |

| | | |

| Principal Only:(5) | | | | | | | | |

| | | |

Series 3309, Class DO, 0.00%, 4/15/37 | | | | | 716 | | | | 645,722 | |

| | | |

Series 4478, Class PO, 0.00%, 5/15/45 | | | | | 358 | | | | 314,796 | |

| |

| | | | $ | 11,023,152 | |

| | | |

Federal Home Loan Mortgage Corp. Structured Agency Credit Risk Debt Notes, Series 2020-DNA4, Class M2, 3.856%, (1 mo. USD LIBOR + 3.75%), 8/25/50(1)(2) | | | | $ | 3,000 | | | $ | 2,821,344 | |

| |

| | | | $ | 2,821,344 | |

| | | |

| Federal National Mortgage Association: | | | | | | | | |

| | | |

Series 1991-122, Class N, 7.50%, 9/25/21 | | | | $ | 0 | (6) | | | 446 | |

| | | |

Series 1994-42, Class K, 6.50%, 4/25/24 | | | | | 68 | | | | 72,438 | |

| | | |

Series 1997-38, Class N, 8.00%, 5/20/27 | | | | | 155 | | | | 175,678 | |

| | | |

Series 2007-74, Class AC, 5.00%, 8/25/37 | | | | | 783 | | | | 875,076 | |

| | | |

Series 2011-49, Class NT, 6.00%, (66.00% - 1 mo. USD LIBOR x 10.00, Cap 6.00%), 6/25/41(4) | | | | | 229 | | | | 250,151 | |

| | | |

Series 2012-134, Class ZT, 2.00%, 12/25/42 | | | | | 759 | | | | 729,834 | |

| | | |

Series 2013-6, Class TA, 1.50%, 1/25/43 | | | | | 604 | | | | 609,350 | |

| | | |

Series 2013-52, Class MD, 1.25%, 6/25/43 | | | | | 684 | | | | 672,797 | |

| | | |

Series 2015-74, Class SL, 2.287%, (2.349% - 1 mo. USD LIBOR x 0.587), 10/25/45(4) | | | | | 867 | | | | 642,239 | |

| | | |

Series 2017-15, Class LE, 3.00%, 6/25/46 | | | | | 311 | | | | 316,980 | |

| | | |

Series 2018-18, Class QD, 4.50%, 5/25/45 | | | | | 435 | | | | 441,365 | |

| | | |

| Interest Only:(3) | | | | | | | | |

| | | |

Series 2004-46, Class SI, 5.894%, (6.00% - 1 mo. USD LIBOR), 5/25/34(4) | | | | | 646 | | | | 99,374 | |

| | | |

Series 2005-17, Class SA, 6.594%, (6.70% - 1 mo. USD LIBOR), 3/25/35(4) | | | | | 755 | | | | 164,081 | |

| | | | | | | | | | |

| Security | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

| Interest Only:(3) (continued) | | | | | | | | |

| | | |

Series 2006-42, Class PI, 6.484%, (6.59% - 1 mo. USD LIBOR), 6/25/36(4) | | | | $ | 1,104 | | | $ | 231,044 | |

| | | |

Series 2006-44, Class IS, 6.494%, (6.60% - 1 mo. USD LIBOR), 6/25/36(4) | | | | | 898 | | | | 195,006 | |

| | | |

Series 2007-50, Class LS, 6.344%, (6.45% - 1 mo. USD LIBOR), 6/25/37(4) | | | | | 681 | | | | 139,018 | |

| | | |

Series 2008-26, Class SA, 6.094%, (6.20% - 1 mo. USD LIBOR), 4/25/38(4) | | | | | 1,062 | | | | 218,514 | |

| | | |

Series 2008-61, Class S, 5.994%, (6.10% - 1 mo. USD LIBOR), 7/25/38(4) | | | | | 1,570 | | | | 273,960 | |

| | | |

Series 2010-109, Class PS, 6.494%, (6.60% - 1 mo. USD LIBOR), 10/25/40(4) | | | | | 1,609 | | | | 326,317 | |

| | | |

Series 2010-124, Class SJ, 5.944%, (6.05% -1 mo. USD LIBOR), 11/25/38(4) | | | | | 97 | | | | 936 | |

| | | |

Series 2010-147, Class KS, 5.844%, (5.95% - 1 mo. USD LIBOR), 1/25/41(4) | | | | | 2,101 | | | | 329,776 | |

| | | |

Series 2012-52, Class AI, 3.50%, 8/25/26 | | | | | 566 | | | | 25,952 | |

| | | |

Series 2012-63, Class EI, 3.50%, 8/25/40 | | | | | 100 | | | | 0 | |

| | | |

Series 2012-103, Class GS, 5.994%, (6.10% - 1 mo. USD LIBOR), 2/25/40(4) | | | | | 15 | | | | 106 | |

| | | |

Series 2012-112, Class SB, 6.044%, (6.15% - 1 mo. USD LIBOR), 9/25/40(4) | | | | | 827 | | | | 37,734 | |

| | | |

Series 2012-118, Class IN, 3.50%, 11/25/42 | | | | | 2,139 | | | | 336,601 | |

| | | |

Series 2012-150, Class PS, 6.044%, (6.15% - 1 mo. USD LIBOR), 1/25/43(4) | | | | | 2,571 | | | | 429,460 | |

| | | |

Series 2012-150, Class SK, 6.044%, (6.15% - 1 mo. USD LIBOR), 1/25/43(4) | | | | | 1,432 | | | | 245,689 | |

| | | |

Series 2013-23, Class CS, 6.144%, (6.25% - 1 mo. USD LIBOR), 3/25/33(4) | | | | | 1,229 | | | | 213,751 | |

| | | |

Series 2013-54, Class HS, 6.194%, (6.30% - 1 mo. USD LIBOR), 10/25/41(4) | | | | | 460 | | | | 23,781 | |

| | | |

Series 2014-32, Class EI, 4.00%, 6/25/44 | | | | | 368 | | | | 43,734 | |

| | | |

Series 2014-55, Class IN, 3.50%, 7/25/44 | | | | | 988 | | | | 161,065 | |

| | | |

Series 2014-80, Class BI, 3.00%, 12/25/44 | | | | | 1,855 | | | | 248,948 | |

| | | |

Series 2014-89, Class IO, 3.50%, 1/25/45 | | | | | 691 | | | | 93,003 | |

| | | |

Series 2015-14, Class KI, 3.00%, 3/25/45 | | | | | 1,907 | | | | 268,321 | |

| | | |

Series 2015-17, Class SA, 6.094%, (6.20% - 1 mo. USD LIBOR), 11/25/43(4) | | | | | 566 | | | | 21,779 | |

| | | |

Series 2015-52, Class MI, 3.50%, 7/25/45 | | | | | 924 | | | | 133,691 | |

| | | |

Series 2015-57, Class IO, 3.00%, 8/25/45 | | | | | 4,619 | | | | 588,184 | |

| | | |

Series 2015-93, Class BS, 6.044%, (6.15% - 1 mo. USD LIBOR), 8/25/45(4) | | | | | 1,046 | | | | 115,676 | |

| | | |

Series 2017-46, Class NI, 3.00%, 8/25/42 | | | | | 583 | | | | 13,738 | |

| | | |

Series 2018-21, Class IO, 3.00%, 4/25/48 | | | | | 1,603 | | | | 150,139 | |

| | | |

Series 2020-23, Class SP, 5.944%, (6.05% - 1 mo. USD LIBOR), 2/25/50(4) | | | | | 3,038 | | | | 534,630 | |

| | | |

Series 2020-45, Class IJ, 2.50%, 7/25/50 | | | | | 3,422 | | | | 388,391 | |

| | | | |

| | 5 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | | | |

| Security | | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

| Principal Only:(5) | | | | | | | | | |

| | | |

Series 2006-8, Class WQ, 0.00%, 3/25/36 | | | | | | $ | 635 | | | $ | 561,444 | |

| |

| | | | $ | 11,400,197 | |

| | | |

| Government National Mortgage Association: | | | | | | | | | |

| | | |

Series 2011-156, Class GA, 2.00%, 12/16/41 | | | | | | $ | 87 | | | $ | 79,223 | |

| | | |

Series 2013-131, Class GS, 3.385%, (3.50% - 1 mo. USD LIBOR), 6/20/43(4) | | | | | | | 397 | | | | 253,024 | |

| | | |

| Interest Only:(3) | | | | | | | | | |

| | | |

Series 2017-121, Class DS, 4.384%, (4.50% - 1 mo. USD LIBOR), 8/20/47(4) | | | | | | | 1,788 | | | | 201,303 | |

| | | |

Series 2020-146, Class IQ, 2.00%, 10/20/50 | | | | | | | 7,841 | | | | 847,176 | |

| | | |

| | | | | | | | | | | $ | 1,380,726 | |

| |

Total Collateralized Mortgage Obligations

(identified cost $37,134,142) | | | $ | 26,625,419 | |

|

| Commercial Mortgage-Backed Securities — 7.9% | |

| Security | | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

| BAMLL Commercial Mortgage Securities Trust: | | | | | | | | | |

| | | |

Series 2019-BPR, Class ENM, 3.843%, 11/5/32(1)(7) | | | | | | $ | 795 | | | $ | 672,617 | |

| | | |

Series 2019-BPR, Class FNM, 3.843%, 11/5/32(1)(7) | | | | | | | 1,605 | | | | 1,302,788 | |

| | | |

Citigroup Commercial Mortgage Trust, Series 2015-P1, Class D, 3.225%, 9/15/48(1) | | | | | | | 2,000 | | | | 1,796,835 | |

| | | |

COMM Mortgage Trust, Series 2013-CR11, Class D, 5.285%, 8/10/50(1)(7) | | | | | | | 2,858 | | | | 2,671,390 | |

| | | |

Federal National Mortgage Association Multifamily Connecticut Avenue Securities Trust, Series 2020-01, Class M10, 3.856%, (1 mo. USD LIBOR + 3.75%), 3/25/50(1)(2) | | | | | | | 1,000 | | | | 1,044,576 | |

| | | |

| JPMBB Commercial Mortgage Securities Trust: | | | | | | | | | |

| | | |

Series 2014-C22, Class D, 4.705%, 9/15/47(1)(7) | | | | | | | 1,850 | | | | 1,377,441 | |

| | | |

Series 2014-C25, Class D, 4.095%, 11/15/47(1)(7) | | | | | | | 360 | | | | 280,282 | |

| | | |

JPMorgan Chase Commercial Mortgage Securities Trust, Series 2011-C5, Class D, 5.607%, 8/15/46(1)(7) | | | | | | | 1,850 | | | | 1,592,205 | |

| | | |

| Morgan Stanley Bank of America Merrill Lynch Trust: | | | | | | | | | |

| | | |

Series 2015-C23, Class D, 4.282%, 7/15/50(1)(7)(8) | | | | | | | 1,500 | | | | 1,496,316 | |

| | | |

Series 2016-C29, Class D, 3.00%, 5/15/49(1)(8) | | | | | | | 1,000 | | | | 861,324 | |

| | | |

Series 2016-C32, Class D, 3.396%, 12/15/49(1)(7)(8) | | | | | | | 250 | | | | 204,573 | |

| | | |

Morgan Stanley Capital I Trust, Series 2016-UBS12, Class D, 3.312%, 12/15/49(1)(8) | | | | | | | 1,000 | | | | 566,117 | |

| | | |

UBS Commercial Mortgage Trust, Series 2012-C1, Class D, 5.754%, 5/10/45(1)(7) | | | | | | | 2,000 | | | | 1,772,291 | |

| | | | | | | | | | |

| Security | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

UBS-Barclays Commercial Mortgage Trust, Series 2013-C6, Class D, 4.449%, 4/10/46(1)(7) | | | | $ | 1,000 | | | $ | 767,218 | |

| | | |

| Wells Fargo Commercial Mortgage Trust: | | | | | | | | |

| | | |

Series 2013-LC12, Class D, 4.405%, 7/15/46(1)(7) | | | | | 2,000 | | | | 1,079,341 | |

| | | |

Series 2015-C31, Class D, 3.852%, 11/15/48 | | | | | 922 | | | | 832,531 | |

| | | |

Series 2016-C35, Class D, 3.142%, 7/15/48(1) | | | | | 1,000 | | | | 825,680 | |

| | | |

Series 2016-C36, Class D, 2.942%, 11/15/59(1) | | | | | 500 | | | | 373,194 | |

| |

Total Commercial Mortgage-Backed Securities

(identified cost $20,595,359) | | | $ | 19,516,719 | |

|

| U.S. Government Agency Mortgage-Backed Securities — 15.4% | |

| Security | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

| Federal Home Loan Mortgage Corp.: | | | | | | | | |

| | | |

2.801%, (COF + 1.25%), 1/1/35(9) | | | | $ | 707 | | | $ | 726,373 | |

| | | |

3.00%, 5/1/50 | | | | | 1,576 | | | | 1,653,759 | |

| | | |

4.50%, with various maturities to 2048 | | | | | 200 | | | | 213,960 | |

| | | |

6.00%, 3/1/29 | | | | | 700 | | | | 793,762 | |

| | | |

6.15%, 7/20/27 | | | | | 148 | | | | 163,066 | |

| | | |

6.50%, 7/1/32 | | | | | 564 | | | | 638,462 | |

| | | |

7.00%, 4/1/36 | | | | | 670 | | | | 777,311 | |

| | | |

7.50%, 11/17/24 | | | | | 153 | | | | 157,482 | |

| | | |

9.00%, 3/1/31 | | | | | 6 | | | | 6,718 | |

| | | |

9.50%, 12/1/22 | | | | | 0 | (6) | | | 1 | |

| |

| | | | $ | 5,130,894 | |

| | | |

| Federal National Mortgage Association: | | | | | | | | |

| | | |

30-Year, 2.50%, TBA(10) | | | | $ | 8,550 | | | $ | 8,852,326 | |

| | | |

1.876%, (6 mo. USD LIBOR + 1.54%), 9/1/37(9) | | | | | 177 | | | | 184,400 | |

| | | |

2.50%, with various maturities to 2051 | | | | | 13,281 | | | | 13,799,848 | |

| | | |

3.00%, 6/1/50 | | | | | 3,264 | | | | 3,427,012 | |

| | | |

5.00%, with various maturities to 2040 | | | | | 1,071 | | | | 1,220,221 | |

| | | |

5.50%, with various maturities to 2033 | | | | | 820 | | | | 932,010 | |

| | | |

6.00%, 11/1/23 | | | | | 210 | | | | 220,869 | |

| | | |

6.332%, (COF + 2.00%, Floor 6.332%), 7/1/32(9) | | | | | 210 | | | | 233,282 | |

| | | |

6.50%, with various maturities to 2036 | | | | | 1,436 | | | | 1,637,221 | |

| | | |

7.00%, with various maturities to 2037 | | | | | 654 | | | | 745,604 | |

| | | |

10.00%, 8/1/31 | | | | | 9 | | | | 10,441 | |

| |

| | | | $ | 31,263,234 | |

| | | |

| Government National Mortgage Association: | | | | | | | | |

| | | |

4.50%, 10/15/47 | | | | $ | 505 | | | $ | 568,836 | |

| | | |

7.50%, 8/15/25 | | | | | 173 | | | | 182,869 | |

| | | |

8.00%, 3/15/34 | | | | | 565 | | | | 635,773 | |

| | | | |

| | 6 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | |

| Security | | | | Principal

Amount

(000’s omitted) | | | Value | |

|

| Government National Mortgage Association: (continued) | |

| | | |

9.50%, 7/15/25 | | | | $ | 3 | | | $ | 3,003 | |

| |

| | | | $ | 1,390,481 | |

| |

Total U.S. Government Agency Mortgage-Backed Securities

(identified cost $37,063,646) | | | $ | 37,784,609 | |

|

| Common Stocks — 0.3% | |

| Security | | | | Shares | | | Value | |

|

| Automotive — 0.0%(11) | |

| | | |

Dayco Products, LLC(12)(13) | | | | | 8,898 | | | $ | 26,694 | |

| |

| | | | $ | 26,694 | |

|

| Electronics / Electrical — 0.1% | |

| | | |

Software Luxembourg Holding S.A., Class A(12)(13) | | | | | 1,872 | | | $ | 327,600 | |

| |

| | | | $ | 327,600 | |

|

| Health Care — 0.1% | |

| | | |

Akorn Holding Company, LLC, Class A(12)(13) | | | | | 6,053 | | | $ | 94,200 | |

| |

| | | | $ | 94,200 | |

|

| Nonferrous Metals / Minerals — 0.0%(11) | |

| | | |

ACNR Holdings, Inc., Class A(12)(13) | | | | | 587 | | | $ | 8,805 | |

| |

| | | | $ | 8,805 | |

|

| Oil and Gas — 0.0%(11) | |

| | | |

AFG Holdings, Inc.(12)(13)(14) | | | | | 3,122 | | | $ | 34,061 | |

| | | |

McDermott International, Ltd.(12)(13) | | | | | 12,407 | | | | 5,583 | |

| | | |

RDV Resources, Inc., Class A(12)(13) | | | | | 4,228 | | | | 740 | |

| | | |

Sunrise Oil & Gas, Inc., Class A(12)(13) | | | | | 9,281 | | | | 2,784 | |

| |

| | | | $ | 43,168 | |

|

| Publishing — 0.0%(11) | |

| | | |

Tweddle Group, Inc.(12)(13)(14) | | | | | 333 | | | $ | 1,589 | |

| |

| | | | $ | 1,589 | |

|

| Radio and Television — 0.1% | |

| | | |

Clear Channel Outdoor Holdings, Inc.(12)(13) | | | | | 11,266 | | | $ | 28,278 | |

| | | |

Cumulus Media, Inc., Class A(12)(13) | | | | | 6,722 | | | | 64,598 | |

| | | |

iHeartMedia, Inc., Class A(12)(13) | | | | | 4,791 | | | | 91,700 | |

| |

| | | | $ | 184,576 | |

| | | | | | | | | | | | |

| Security | | | | | Shares | | | Value | |

|

| Retailers (Except Food and Drug) — 0.0% | |

| | | |

David’s Bridal, LLC(12)(13)(14) | | | | | | | 4,108 | | | $ | 0 | |

| |

| | | | $ | 0 | |

|

| Telecommunications — 0.0%(11) | |

| | | |

GEE Acquisition Holdings Corp.(12)(13)(14) | | | | | | | 3,588 | | | $ | 72,262 | |

| |

| | | | $ | 72,262 | |

| |

Total Common Stocks

(identified cost $1,111,966) | | | $ | 758,894 | |

|

| Corporate Bonds — 10.8% | |

| Security | | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

| Aerospace and Defense — 0.7% | | | | | | | | | |

| | | |

| Bombardier, Inc.: | | | | | | | | | |

| | | |

6.00%, 10/15/22(1) | | | | | | $ | 313 | | | $ | 313,470 | |

| | | |

6.125%, 1/15/23(1) | | | | | | | 229 | | | | 240,342 | |

| | | |

| TransDigm, Inc.: | | | | | | | | | |

| | | |

6.25%, 3/15/26(1) | | | | | | | 179 | | | | 189,740 | |

| | | |

6.50%, 5/15/25 | | | | | | | 1,000 | | | | 1,015,323 | |

| | | |

| | | | | | | | | | | $ | 1,758,875 | |

| | | |

| Automotive — 0.3% | | | | | | | | | |

| | | |

| Clarios Global, L.P.: | | | | | | | | | |

| | | |

6.25%, 5/15/26(1) | | | | | | $ | 129 | | | $ | 136,990 | |

| | | |

8.50%, 5/15/27(1) | | | | | | | 642 | | | | 694,162 | |

| | | |

| | | | | | | | | | | $ | 831,152 | |

| | | |

| Building and Development — 0.1% | | | | | | | | | |

| | | |

Five Point Operating Co., L.P./Five Point Capital Corp., 7.875%, 11/15/25(1) | | | | | | $ | 84 | | | $ | 88,987 | |

| | | |

Greystar Real Estate Partners, LLC, 5.75%, 12/1/25(1) | | | | | | | 187 | | | | 193,545 | |

| | | |

| | | | | | | | | | | $ | 282,532 | |

|

| Business Equipment and Services — 0.7% | |

| | | |

GEMS MENASA Cayman, Ltd./GEMS Education Delaware, LLC, 7.125%, 7/31/26(1) | | | | | | $ | 460 | | | $ | 485,808 | |

| | | |

ServiceMaster Co., LLC (The), 7.45%, 8/15/27 | | | | | | | 1,000 | | | | 1,173,560 | |

| | | |

| | | | | | | | | | | $ | 1,659,368 | |

|

| Cable and Satellite Television — 0.9% | |

| | | |

Altice France S.A., 7.375%, 5/1/26(1) | | | | | | $ | 200 | | | $ | 207,610 | |

| | | | |

| | 7 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | | | |

| Security | | | | | Principal

Amount

(000’s omitted) | | | Value | |

|

| Cable and Satellite Television (continued) | |

| | | |

CCO Holdings, LLC/CCO Holdings Capital Corp.: | | | | | | | | | | | | |

| | | |

4.75%, 3/1/30(1) | | | | | | $ | 75 | | | $ | 78,375 | |

| | | |

5.50%, 5/1/26(1) | | | | | | | 1,000 | | | | 1,033,250 | |

| | | |

| CSC Holdings, LLC: | | | | | | | | | |

| | | |

5.75%, 1/15/30(1) | | | | | | | 200 | | | | 212,875 | |

| | | |

7.50%, 4/1/28(1) | | | | | | | 500 | | | | 551,860 | |

| | | |

TEGNA, Inc., 5.00%, 9/15/29 | | | | | | | 56 | | | | 58,197 | |

| | | |

| | | | | | | | | | | $ | 2,142,167 | |

|

| Conglomerates — 0.2% | |

| | | |

Spectrum Brands, Inc., 5.00%, 10/1/29(1) | | | | | | $ | 530 | | | $ | 561,800 | |

| | | |

| | | | | | | | | | | $ | 561,800 | |

|

| Distribution & Wholesale — 0.0%(11) | |

| | | |

Performance Food Group, Inc., 5.50%, 10/15/27(1) | | | | | | $ | 69 | | | $ | 72,841 | |

| | | |

| | | | | | | | | | | $ | 72,841 | |

|

| Drugs — 0.2% | |

| | | |

Bausch Health Americas, Inc., 8.50%, 1/31/27(1) | | | | | | $ | 63 | | | $ | 70,245 | |

|

| Bausch Health Companies, Inc.: | |

| | | |

5.75%, 8/15/27(1) | | | | | | | 31 | | | | 33,318 | |

| | | |

9.00%, 12/15/25(1) | | | | | | | 338 | | | | 367,220 | |

| | | |

| | | | | | | | | | | $ | 470,783 | |

|

| Ecological Services and Equipment — 0.6% | |

| | | |

Covanta Holding Corp., 5.875%, 7/1/25 | | | | | | $ | 1,000 | | | $ | 1,046,395 | |

| | | |

GFL Environmental, Inc., 8.50%, 5/1/27(1) | | | | | | | 285 | | | | 312,609 | |

| | | |

Waste Pro USA, Inc., 5.50%, 2/15/26(1) | | | | | | | 25 | | | | 25,573 | |

| | | |

| | | | | | | | | | | $ | 1,384,577 | |

|

| Electronics / Electrical — 0.0%(11) | |

| | | |

Sensata Technologies, Inc., 4.375%, 2/15/30(1) | | | | | | $ | 45 | | | $ | 47,132 | |

| | | |

| | | | | | | | | | | $ | 47,132 | |

|

| Financial Services — 0.4% | |

| | | |

Vietnam Debt and Asset Trading Corp., 1.00%, 10/10/25(15) | | | | | | $ | 1,060 | | | $ | 954,000 | |

| | | |

| | | | | | | | | | | $ | 954,000 | |

| | | | | | | | | | | | |

| Security | | | | | Principal

Amount

(000’s omitted) | | | Value | |

|

| Food Products — 0.2% | |

| | | |

JBS USA LUX S.A./JBS USA Food Co./JBS USA Finance, Inc., 5.50%, 1/15/30(1) | | | | | | $ | 353 | | | $ | 388,745 | |

| | | |

| | | | | | | | | | | $ | 388,745 | |

|

| Health Care — 1.2% | |

|

| Centene Corp.: | |

| | | |

3.00%, 10/15/30 | | | | | | $ | 624 | �� | | $ | 620,100 | |

| | | |

5.375%, 8/15/26(1) | | | | | | | 45 | | | | 47,261 | |

| | | |

HCA, Inc., 5.875%, 2/1/29 | | | | | | | 753 | | | | 889,482 | |

| | | |

LifePoint Health, Inc., 5.375%, 1/15/29(1) | | | | | | | 447 | | | | 447,648 | |

| | | |

Molina Healthcare, Inc., 3.875%, 11/15/30(1) | | | | | | | 296 | | | | 305,250 | |

| | | |

MPH Acquisition Holdings, LLC, 5.75%, 11/1/28(1) | | | | | | | 529 | | | | 522,345 | |

| | | |

| | | | | | | | | | | $ | 2,832,086 | |

| | | |

| Insurance — 0.4% | | | | | | | | | |

| | | |

Hub International, Ltd., 7.00%, 5/1/26(1) | | | | | | $ | 948 | | | $ | 983,465 | |

| | | |

| | | | | | | | | | | $ | 983,465 | |

| | | |

| Internet Software & Services — 0.1% | | | | | | | | | |

| | | |

Netflix, Inc., 5.875%, 11/15/28 | | | | | | $ | 230 | | | $ | 280,140 | |

| | | |

| | | | | | | | | | | $ | 280,140 | |

| | | |

| Leisure Goods / Activities / Movies — 0.2% | | | | | | | | | |

| | | |

Viking Cruises, Ltd., 5.875%, 9/15/27(1) | | | | | | $ | 540 | | | $ | 529,867 | |

| | | |

| | | | | | | | | | | $ | 529,867 | |

| | | |

| Lodging and Casinos — 0.6% | | | | | | | | | |

| | | |

Caesars Resort Collection, LLC/CRC Finco, Inc., 5.25%, 10/15/25(1) | | | | | | $ | 657 | | | $ | 663,168 | |

| | | |

MGM Growth Properties Operating Partnership, L.P./MGP Finance Co-Issuer, Inc., 5.75%, 2/1/27 | | | | | | | 44 | | | | 49,143 | |

| | | |

Stars Group Holdings B.V./Stars Group US Co-Borrower, LLC, 7.00%, 7/15/26(1) | | | | | | | 500 | | | | 524,050 | |

| | | |

Wynn Las Vegas, LLC/Wynn Las Vegas Capital Corp., 5.25%, 5/15/27(1) | | | | | | | 113 | | | | 119,573 | |

| | | |

| | | | | | | | | | | $ | 1,355,934 | |

| | | |

| Media — 0.2% | | | | | | | | | |

| | | |

Scripps Escrow, Inc., 5.875%, 7/15/27(1) | | | | | | $ | 477 | | | $ | 502,608 | |

| | | |

| | | | | | | | | | | $ | 502,608 | |

| | | | |

| | 8 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | | | |

| Security | | | | | Principal

Amount

(000’s omitted) | | | Value | |

| | | |

| Metals / Mining — 0.0%(11) | | | | | | | | | |

| | | |

Cleveland-Cliffs, Inc., 6.75%, 3/15/26(1) | | | | | | $ | 112 | | | $ | 121,660 | |

| | | |

| | | | | | | | | | | $ | 121,660 | |

| | | |

| Nonferrous Metals / Minerals — 0.2% | | | | | | | | | |

| | | |

First Quantum Minerals, Ltd., 7.25%, 4/1/23(1) | | | | | | $ | 441 | | | $ | 449,820 | |

| | | |

| | | | | | | | | | | $ | 449,820 | |

| | | |

| Oil and Gas — 0.6% | | | | | | | | | |

| | | |

Archrock Partners L.P./Archrock Partners Finance Corp., 6.875%, 4/1/27(1) | | | | | | $ | 250 | | | $ | 266,680 | |

| | | |

Great Western Petroleum, LLC/Great Western Finance Corp., 12.00%, 9/1/25(1) | | | | | | | 592 | | | | 515,040 | |

| | | |

Petroleos Mexicanos, 6.75%, 9/21/47 | | | | | | | 784 | | | | 694,201 | |

| | | |

| | | | | | | | | | | $ | 1,475,921 | |

| | | |

| Packaging & Containers — 0.1% | | | | | | | | | |

| | | |

ARD Finance S.A., 6.50%, (6.50% cash or 7.25% PIK), 6/30/27(1)(16) | | | | | | $ | 341 | | | $ | 357,197 | |

| | | |

| | | | | | | | | | | $ | 357,197 | |

| | | |

| Pipelines — 0.1% | | | | | | | | | |

| | | |

Cheniere Energy Partners, L.P., 4.50%, 10/1/29 | | | | | | $ | 71 | | | $ | 74,233 | |

| | | |

Crestwood Midstream Partners, L.P./Crestwood Midstream Finance Corp., 5.625%, 5/1/27(1) | | | | | | | 83 | | | | 84,636 | |

| | | |

| | | | | | | | | | | $ | 158,869 | |

|

| Radio and Television — 0.6% | |

| | | |

Diamond Sports Group, LLC/Diamond Sports Finance Co., 5.375%, 8/15/26(1) | | | | | | $ | 146 | | | $ | 106,763 | |

|

| iHeartCommunications, Inc.: | |

| | | |

6.375%, 5/1/26 | | | | | | | 27 | | | | 28,916 | |

| | | |

8.375%, 5/1/27 | | | | | | | 49 | | | | 52,756 | |

| | | |

Nexstar Broadcasting, Inc., 5.625%, 7/15/27(1) | | | | | | | 62 | | | | 65,585 | |

|

| Sirius XM Radio, Inc.: | |

| | | |

4.125%, 7/1/30(1) | | | | | | | 124 | | | | 124,155 | |

| | | |

4.625%, 7/15/24(1) | | | | | | | 124 | | | | 127,410 | |

| | | |

5.50%, 7/1/29(1) | | | | | | | 500 | | | | 540,937 | |

| | | |

Terrier Media Buyer, Inc., 8.875%, 12/15/27(1) | | | | | | | 443 | | | | 481,763 | |

| | | |

| | | | | | | | | | | $ | 1,528,285 | |

|

| Real Estate Investment Trusts (REITs) — 0.3% | |

| | | |

Service Properties Trust, 3.95%, 1/15/28 | | | | | | $ | 591 | | | $ | 547,783 | |

| | | | | | | | | | | | |

| Security | | | | | Principal

Amount

(000’s omitted) | | | Value | |

|

| Real Estate Investment Trusts (REITs) (continued) | |

| | | |

Uniti Group, L.P./Uniti Fiber Holdings, Inc./CSL Capital, LLC, 7.125%, 12/15/24(1) | | | | | | $ | 72 | | | $ | 74,423 | |

| | | |

| | | | | | | | | | | $ | 622,206 | |

|

| Steel — 0.5% | |

| | | |

Allegheny Technologies, Inc., 7.875%, 8/15/23 | | | | | | $ | 453 | | | $ | 494,384 | |

| | | |

Infrabuild Australia Pty, Ltd., 12.00%, 10/1/24(1) | | | | | | | 664 | | | | 673,960 | |

| | | |

| | | | | | | | | | | $ | 1,168,344 | |

|

| Surface Transport — 0.1% | |

| | | |

XPO Logistics, Inc., 6.125%, 9/1/23(1) | | | | | | $ | 346 | | | $ | 351,233 | |

| | | |

| | | | | | | | | | | $ | 351,233 | |

|

| Technology — 0.4% | |

| | | |

Dell International, LLC/EMC Corp., 7.125%, 6/15/24(1) | | | | | | $ | 895 | | | $ | 920,485 | |

| | | |

| | | | | | | | | | | $ | 920,485 | |

|

| Telecommunications — 0.8% | |

| | | |

Altice France Holding S.A., 10.50%, 5/15/27(1) | | | | | | $ | 269 | | | $ | 303,369 | |

| | | |

Connect Finco S.a.r.l./Connect US Finco, LLC, 6.75%, 10/1/26(1) | | | | | | | 200 | | | | 209,190 | |

| | | |

Hughes Satellite Systems Corp., 6.625%, 8/1/26 | | | | | | | 470 | | | | 520,925 | |

| | | |

Lumen Technologies, Inc., 7.50%, 4/1/24 | | | | | | | 66 | | | | 73,941 | |

| | | |

Sprint Capital Corp., 6.875%, 11/15/28 | | | | | | | 191 | | | | 240,904 | |

| | | |

Sprint Communications, Inc., 6.00%, 11/15/22 | | | | | | | 25 | | | | 26,722 | |

| | | |

Sprint Corp., 7.875%, 9/15/23 | | | | | | | 533 | | | | 608,286 | |

| | | |

ViaSat, Inc., 5.625%, 4/15/27(1) | | | | | | | 62 | | | | 65,078 | |

| | | |

| | | | | | | | | | | $ | 2,048,415 | |

|

| Utilities — 0.1% | |

| | | |

Calpine Corp., 5.25%, 6/1/26(1) | | | | | | $ | 51 | | | $ | 52,460 | |

|

| TerraForm Power Operating, LLC: | |

| | | |

4.25%, 1/31/23(1) | | | | | | | 45 | | | | 46,266 | |

| | | |

5.00%, 1/31/28(1) | | | | | | | 70 | | | | 75,206 | |

| | | |

| | | | | | | | | | | $ | 173,932 | |

| | | |

Total Corporate Bonds

(identified cost $25,322,572) | | | | | | | | | | $ | 26,414,439 | |

| | | | |

| | 9 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | | | |

| Preferred Stocks — 0.0%(11) | |

| Security | | | | | Shares | | | Value | |

|

| Financial Services — 0.0% | |

| | | |

DBI Investors, Inc., Series A-1(12)(13)(14) | | | | | | | 194 | | | $ | 0 | |

| | | |

| | | | | | | | | | | $ | 0 | |

|

| Nonferrous Metals / Minerals — 0.0%(11) | |

| | | |

ACNR Holdings, Inc., 15.00% (PIK)(12)(13) | | | | | | | 277 | | | $ | 24,515 | |

| | | |

| | | | | | | | | | | $ | 24,515 | |

|

| Retailers (Except Food and Drug) — 0.0% | |

| | | |

David’s Bridal, LLC, Series A, 8.00% (PIK)(12)(13)(14) | | | | | | | 114 | | | $ | 0 | |

| | | |

David’s Bridal, LLC, Series B, 10.00% (PIK)(12)(13)(14) | | | | | | | 466 | | | | 0 | |

| | | |

| | | | | | | | | | | $ | 0 | |

| | | |

Total Preferred Stocks

(identified cost $37,727) | | | | | | | | | | $ | 24,515 | |

|

| Senior Floating-Rate Loans — 33.9%(17) | |

| Borrower/Description | | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Aerospace and Defense — 0.7% | |

| | | |

AI Convoy (Luxembourg) S.a.r.l., Term Loan, 4.50%, (USD LIBOR + 3.50%, Floor 1.00%), 1/17/27(18) | | | | | | | 99 | | | $ | 99,093 | |

| | | |

Brown Group Holding, LLC,

Term Loan, 4/27/28(19) | | | | | | | 175 | | | | 174,366 | |

| | | |

Dynasty Acquisition Co., Inc.: Term Loan, 3.703%, (3 mo. USD LIBOR + 3.50%), 4/6/26 | | | | | | | 43 | | | | 41,971 | |

| | | |

Term Loan, 3.703%, (3 mo. USD LIBOR + 3.50%), 4/6/26 | | | | | | | 80 | | | | 78,066 | |

| | | |

| TransDigm, Inc.: | | | | | | | | | |

| | | |

Term Loan, 2.363%, (1 mo. USD LIBOR + 2.25%), 8/22/24 | | | | | | | 478 | | | | 473,205 | |

| | | |

Term Loan, 2.363%, (1 mo. USD LIBOR + 2.25%), 12/9/25 | | | | | | | 943 | | | | 932,680 | |

| | | |

| | | | | | | | | | | $ | 1,799,381 | |

|

| Air Transport — 0.3% | |

| | | |

JetBlue Airways Corporation, Term Loan, 6.25%, (3 mo.

USD LIBOR + 5.25%, Floor 1.00%), 6/17/24 | | | | | 168 | | | $173,030 | |

| | | |

Mileage Plus Holdings, LLC, Term Loan, 6.25%, (3 mo.

USD LIBOR + 5.25%, Floor 1.00%), 6/21/27 | | | | | 125 | | | 133,555 | |

| | | |

SkyMiles IP, Ltd., Term Loan, 4.75%, (3 mo. USD LIBOR + 3.75%, Floor 1.00%), 10/20/27 | | | | | | | 300 | | | | 315,812 | |

| | | |

| | | | | | | | | | | $ | 622,397 | |

| | | | | | | | | | | | |

| Borrower/Description | | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Automotive — 1.4% | |

| | | |

Adient US, LLC, Term Loan, 3.61%, (1 mo. USD LIBOR + 3.50%), 4/8/28 | | | | | | | 125 | | | $ | 125,098 | |

| | | |

Autokiniton US Holdings, Inc., Term Loan, 5.00%, (3 mo. USD LIBOR + 4.50%, Floor 0.50%), 4/6/28 | | | | | | | 175 | | | | 176,750 | |

| | | |

Belron Finance US, LLC, Term Loan, 3.25%, (3 mo. USD LIBOR + 2.75%, Floor 0.50%), 4/13/28 | | | | | | | 125 | | | | 124,648 | |

| | | |

Clarios Global L.P., Term Loan, 3.363%, (1 mo. USD LIBOR + 3.25%), 4/30/26 | | | | | | | 532 | | | | 527,233 | |

| | | |

Dayco Products, LLC, Term Loan, 4.44%, (3 mo. USD LIBOR + 4.25%), 5/19/23 | | | | | | | 168 | | | | 154,331 | |

| | | |

Garrett LX I S.a.r.l., Term Loan, 3/5/28(19) | | | | | | | 100 | | | | 99,500 | |

| | | |

Gates Global, LLC, Term Loan, 3.50%, (1 mo. USD LIBOR + 2.75%, Floor 0.75%), 3/31/27 | | | | | | | 295 | | | | 294,252 | |

| | | |

Goodyear Tire & Rubber Company (The), Term Loan - Second Lien, 2.12%, (1 mo. USD LIBOR + 2.00%), 3/7/25 | | | | | | | 383 | | | | 375,746 | |

| | | |

Les Schwab Tire Centers, Term Loan, 4.25%, (6 mo. USD LIBOR + 3.50%, Floor 0.75%), 11/2/27 | | | | | | | 399 | | | | 400,330 | |

| | | |

Tenneco, Inc., Term Loan, 3.113%, (1 mo. USD LIBOR + 3.00%), 10/1/25 | | | | | | | 513 | | | | 502,374 | |

| | | |

Thor Industries, Inc., Term Loan, 3.125%, (1 mo. USD LIBOR + 3.00%), 2/1/26 | | | | | | | 142 | | | | 142,013 | |

| | | |

TI Group Automotive Systems, LLC, Term Loan, 3.75%, (3 mo. USD LIBOR + 3.25%, Floor 0.50%), 12/16/26 | | | | | | | 100 | | | | 100,125 | |

| | | |

Truck Hero, Inc., Term Loan, 4.50%, (1 mo. USD LIBOR + 3.75%, Floor 0.75%), 1/31/28 | | | | | | | 200 | | | | 199,863 | |

| | | |

Wheel Pros, LLC, Term Loan, 4/23/28(19) | | | | | | | 125 | | | | 125,078 | |

| | | |

| | | | | | | | | | | $ | 3,347,341 | |

| | | |

| Beverage and Tobacco — 0.1% | | | | | | | | | |

| | | |

Arterra Wines Canada, Inc., Term Loan, 4.25%, (3 mo. USD LIBOR + 3.50%, Floor 0.75%), 11/24/27 | | | | | | | 150 | | | $ | 149,859 | |

| | | |

City Brewing Company, LLC, Term Loan, 4.25%, (3 mo. USD LIBOR + 3.50%, Floor 0.75%), 4/5/28 | | | | | | | 125 | | | | 125,469 | |

| | | |

| | | | | | | | | | | $ | 275,328 | |

|

| Brokerage / Securities Dealers / Investment Houses — 0.2% | |

| | | |

Advisor Group, Inc., Term Loan, 4.613%, (1 mo. USD LIBOR + 4.50%), 7/31/26 | | | | | | | 173 | | | $ | 172,975 | |

| | | |

Hudson River Trading, LLC, Term Loan, 3.113%, (1 mo. USD LIBOR + 3.00%), 3/20/28 | | | | | | | 300 | | | | 297,750 | |

| | | |

| | | | | | | | | | | $ | 470,725 | |

| | | | |

| | 10 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | | | |

| Borrower/Description | | | | | Principal

Amount*

(000’s omitted) | | | Value | |

| | | |

| Building and Development — 1.5% | | | | | | | | | |

| | | |

American Builders & Contractors Supply Co., Inc., Term Loan, 2.113%, (1 mo. USD LIBOR + 2.00%), 1/15/27 | | | | | | | 345 | | | $ | 342,517 | |

| | | |

American Residential Services, LLC, Term Loan, 4.25%, (2 mo. USD LIBOR + 3.50%, Floor 0.75%), 10/15/27 | | | | | | | 100 | | | | 99,937 | |

| | | |

APi Group DE, Inc., Term Loan, 2.613%, (1 mo. USD LIBOR + 2.50%), 10/1/26 | | | | | | | 222 | | | | 221,424 | |

| | | |

Brookfield Property REIT, Inc., Term Loan, 2.613%, (1 mo. USD LIBOR + 2.50%), 8/27/25 | | | | | | | 146 | | | | 139,120 | |

| | | |

Core & Main L.P., Term Loan, 3.75%, (USD LIBOR + 2.75%, Floor 1.00%), 8/1/24(18) | | | | | | | 170 | | | | 169,186 | |

| | | |

CP Atlas Buyer, Inc., Term Loan, 4.25%, (3 mo. USD LIBOR + 3.75%, Floor 0.50%), 11/23/27 | | | | | | | 175 | | | | 174,727 | |

| | | |

CPG International, Inc., Term Loan, 3.25%, (6 mo. USD LIBOR + 2.50%, Floor 0.75%), 5/5/24 | | | | | | | 221 | | | | 220,724 | |

| | | |

Cushman & Wakefield U.S. Borrower, LLC, Term Loan, 2.863%, (1 mo. USD LIBOR + 2.75%), 8/21/25 | | | | | | | 782 | | | | 765,154 | |

| | | |

Foundation Building Materials Holding Company, LLC, Term Loan, 3.75%, (3 mo. USD LIBOR + 3.25%, Floor 0.50%), 2/3/28 | | | | | | | 175 | | | | 173,781 | |

| | | |

Northstar Group Services, Inc., Term Loan, 6.50%, (3 mo. USD LIBOR + 5.50%, Floor 1.00%), 11/9/26 | | | | | | | 199 | | | | 199,992 | |

| | | |

Park River Holdings, Inc., Term Loan, 4.00%, (3 mo. USD LIBOR + 3.25%, Floor 0.75%), 12/28/27 | | | | | | | 100 | | | | 99,625 | |

| | | |

Quikrete Holdings, Inc., Term Loan, 2.613%, (1 mo. USD LIBOR + 2.50%), 2/1/27 | | | | | | | 427 | | | | 423,598 | |

| | | |

RE/MAX International, Inc., Term Loan, 3.50%, (3 mo. USD LIBOR + 2.75%, Floor 0.75%), 12/15/23 | | | | | | | 385 | | | | 384,558 | |

| | | |

White Cap Buyer, LLC, Term Loan, 4.50%, (3 mo. USD LIBOR + 4.00%, Floor 0.50%), 10/19/27 | | | | | | | 323 | | | | 323,820 | |

| | | |

| | | | | | | | | | | $ | 3,738,163 | |

|

| Business Equipment and Services — 3.4% | |

| | | |

AlixPartners, LLP, Term Loan, 3.25%, (1 mo. USD LIBOR + 2.75%, Floor 0.50%), 2/4/28 | | | | | | | 225 | | | $ | 224,234 | |

| | | |

Allied Universal Holdco, LLC, Term Loan, 4.363%, (1 mo. USD LIBOR + 4.25%), 7/10/26 | | | | | | | 469 | | | | 468,858 | |

| | | |

AppLovin Corporation, Term Loan, 3.363%, (1 mo. USD LIBOR + 3.25%), 8/15/25 | | | | | | | 417 | | | | 416,371 | |

| | | |

ASGN Incorporated, Term Loan, 1.863%, (1 mo. USD LIBOR + 1.75%), 4/2/25 | | | | | | | 45 | | | | 44,879 | |

| | | |

Asplundh Tree Expert, LLC, Term Loan, 1.863%, (1 mo. USD LIBOR + 1.75%), 9/7/27 | | | | | | | 174 | | | | 173,744 | |

| | | |

Bracket Intermediate Holding Corp., Term Loan, 4.444%, (3 mo. USD LIBOR + 4.25%), 9/5/25 | | | | | | | 122 | | | | 121,799 | |

| | | | | | | | | | |

| Borrower/Description | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Business Equipment and Services (continued) | |

|

| Camelot U.S. Acquisition 1 Co.: | |

| | | |

Term Loan, 3.113%, (1 mo. USD LIBOR + 3.00%), 10/30/26 | | | | | 272 | | | $ | 269,356 | |

| | | |

Term Loan, 4.00%, (1 mo. USD LIBOR + 3.00%, Floor 1.00%), 10/30/26 | | | | | 175 | | | | 174,955 | |

| | | |

CCC Information Services, Inc., Term Loan, 4.00%, (1 mo. USD LIBOR + 3.00%, Floor 1.00%), 4/29/24 | | | | | 291 | | | | 291,085 | |

| | | |

Ceridian HCM Holding, Inc., Term Loan, 2.587%, (1 week USD LIBOR + 2.50%), 4/30/25 | | | | | 219 | | | | 216,050 | |

| | | |

CoreLogic, Inc., Term Loan, 4/13/28(19) | | | | | 775 | | | | 772,094 | |

| | | |

Deerfield Dakota Holding, LLC, Term Loan, 4.75%, (1 mo. USD LIBOR + 3.75%, Floor 1.00%), 4/9/27 | | | | | 323 | | | | 323,705 | |

| | | |

EAB Global, Inc., Term Loan, 4.75%, (USD LIBOR + 3.75%, Floor 1.00%), 11/15/24(18) | | | | | 194 | | | | 193,919 | |

| | | |

Endure Digital, Inc., Term Loan, 4.25%, (3 mo. USD LIBOR + 3.50%, Floor 0.75%), 2/10/28 | | | | | 450 | | | | 447,328 | |

| | | |

Garda World Security Corporation, Term Loan, 4.36%, (1 mo. USD LIBOR + 4.25%), 10/30/26 | | | | | 120 | | | | 120,562 | |

| | | |

Grab Holdings, Inc., Term Loan, 5.50%, (6 mo. USD LIBOR + 4.50%, Floor 1.00%), 1/29/26 | | | | | 350 | | | | 357,438 | |

| | | |

Greeneden U.S. Holdings II, LLC, Term Loan, 4.75%, (1 mo. USD LIBOR + 4.00%, Floor 0.75%), 12/1/27 | | | | | 125 | | | | 125,139 | |

| | | |

IG Investment Holdings, LLC, Term Loan, 5.00%, (3 mo. USD LIBOR + 4.00%, Floor 1.00%), 5/23/25 | | | | | 421 | | | | 421,998 | |

| | | |

Intrado Corp., Term Loan, 5.00%, (3 mo. USD LIBOR + 4.00%, Floor 1.00%), 10/10/24 | | | | | 169 | | | | 165,585 | |

| | | |

IRI Holdings, Inc., Term Loan, 4.363%, (1 mo. USD LIBOR + 4.25%), 12/1/25 | | | | | 220 | | | | 219,938 | |

| | | |

Iron Mountain, Inc., Term Loan, 1.863%, (1 mo. USD LIBOR + 1.75%), 1/2/26 | | | | | 121 | | | | 120,265 | |

|

| Ivanti Software, Inc.: | |

| | | |

Term Loan, 4.75%, (3 mo. USD LIBOR + 4.00%, Floor 0.75%), 12/1/27 | | | | | 100 | | | | 98,625 | |

| | | |

Term Loan, 5.75%, (3 mo. USD LIBOR + 4.75%, Floor 1.00%), 12/1/27 | | | | | 400 | | | | 398,833 | |

| | | |

KAR Auction Services, Inc., Term Loan, 2.375%, (1 mo. USD LIBOR + 2.25%), 9/19/26 | | | | | 99 | | | | 97,351 | |

|

| KUEHG Corp.: | |

| | | |

Term Loan, 4.75%, (3 mo. USD LIBOR + 3.75%, Floor 1.00%), 2/21/25 | | | | | 309 | | | | 305,990 | |

| | | |

Term Loan - Second Lien, 9.25%, (3 mo. USD LIBOR + 8.25%, Floor 1.00%), 8/22/25 | | | | | 50 | | | | 48,458 | |

| | | |

Magnite, Inc., Term Loan, 3/31/28(19) | | | | | 100 | | | | 99,750 | |

| | | |

Monitronics International, Inc., Term Loan, 7.75%, (1 mo. USD LIBOR + 6.50%, Floor 1.25%), 3/29/24 | | | | | 198 | | | | 194,847 | |

| | | |

Nielsen Consumer, Inc., Term Loan, 4.111%, (1 mo. USD LIBOR + 4.00%), 3/6/28 | | | | | 100 | | | | 99,927 | |

| | | | |

| | 11 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | | | |

| Borrower/Description | | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Business Equipment and Services (continued) | |

| | | |

Packaging Coordinators Midco, Inc., Term Loan, 4.50%, (3 mo. USD LIBOR + 3.75%, Floor 0.75%), 11/30/27 | | | | | | | 175 | | | $ | 175,191 | |

| | | |

PGX Holdings, Inc., Term Loan, 10.50%, (12 mo. USD LIBOR + 9.50%, Floor 1.00%), 6.25% cash, 4.25% PIK, 9/29/23 | | | | | | | 174 | | | | 166,073 | |

| | | |

Red Ventures, LLC, Term Loan, 2.613%, (1 mo. USD LIBOR + 2.50%), 11/8/24 | | | | | | | 183 | | | | 180,939 | |

| | | |

Spin Holdco, Inc., Term Loan, 4.75%, (3 mo. USD LIBOR + 4.00%, Floor 0.75%), 3/1/28 | | | | | | | 600 | | | | 598,178 | |

| | | |

Techem Verwaltungsgesellschaft 675 mbH, Term Loan, 2.625%, (3 mo. EURIBOR + 2.625%), 7/15/25 | | | EUR | | | | 111 | | | | 132,940 | |

| | | |

Tempo Acquisition, LLC, Term Loan, 3.75%, (1 mo. USD LIBOR + 3.25%, Floor 0.50%), 11/2/26 | | | | | | | 127 | | | | 127,220 | |

| | | |

| | | | | | | | | | | $ | 8,393,624 | |

|

| Cable and Satellite Television — 1.5% | |

| | | |

Charter Communications Operating, LLC, Term Loan, 1.87%, (1 mo. USD LIBOR + 1.75%), 2/1/27 | | | | | | | 532 | | | $ | 530,384 | |

|

| CSC Holdings, LLC: | |

| | | |

Term Loan, 2.365%, (1 mo. USD LIBOR + 2.25%), 7/17/25 | | | | | | | 441 | | | | 437,582 | |

| | | |

Term Loan, 2.365%, (1 mo. USD LIBOR + 2.25%), 1/15/26 | | | | | | | 147 | | | | 145,388 | |

| | | |

Term Loan, 2.615%, (1 mo. USD LIBOR + 2.50%), 4/15/27 | | | | | | | 195 | | | | 194,335 | |

| | | |

Numericable Group S.A., Term Loan, 2.936%, (3 mo. USD LIBOR + 2.75%), 7/31/25 | | | | | | | 312 | | | | 306,384 | |

| | | |

Telenet Financing USD, LLC, Term Loan, 2.115%, (1 mo. USD LIBOR + 2.00%), 4/30/28 | | | | | | | 575 | | | | 568,082 | |

|

| UPC Broadband Holding B.V.: | |

| | | |

Term Loan, 2.365%, (1 mo. USD LIBOR + 2.25%), 4/30/28 | | | | | | | 125 | | | | 123,266 | |

| | | |

Term Loan, 3.607%, (1 mo. USD LIBOR + 3.50%), 1/31/29 | | | | | | | 442 | | | | 442,446 | |

|

| Virgin Media Bristol, LLC: | |

| | | |

Term Loan, 2.615%, (1 mo. USD LIBOR + 2.50%), 1/31/28 | | | | | | | 650 | | | | 645,450 | |

| | | |

Term Loan, 1/31/29(19) | | | | | | | 175 | | | | 174,984 | |

| | | |

Virgin Media SFA Finance Limited, Term Loan, 2.50%, (6 mo. EURIBOR + 2.50%), 1/31/29 | | | EUR | | | | 175 | | | | 209,678 | |

| | | |

| | | | | | | | | | | $ | 3,777,979 | |

|

| Chemicals and Plastics — 1.5% | |

| | | |

Aruba Investments, Inc., Term Loan, 4.75%, (3 mo. USD LIBOR + 4.00%, Floor 0.75%), 11/24/27 | | | | | | | 100 | | | $ | 100,125 | |

| | | | | | | | | | | | |

| Borrower/Description | | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Chemicals and Plastics (continued) | |

| | | |

Atotech B.V., Term Loan, 3.00%, (3 mo. USD LIBOR + 2.50%, Floor 0.50%), 3/18/28 | | | | | | | 150 | | | $ | 149,250 | |

| | | |

CPC Acquisition Corp., Term Loan, 4.50%, (6 mo. USD LIBOR + 3.75%, Floor 0.75%), 12/29/27 | | | | | | | 125 | | | | 123,828 | |

| | | |

Emerald Performance Materials, LLC, Term Loan, 5.00%, (1 mo. USD LIBOR + 4.00%, Floor 1.00%), 8/12/25 | | | | | | | 239 | | | | 239,657 | |

|

| Ferro Corporation: | |

| | | |

Term Loan, 2.453%, (3 mo. USD LIBOR + 2.25%), 2/14/24 | | | | | | | 22 | | | | 21,685 | |

| | | |

Term Loan, 2.453%, (3 mo. USD LIBOR + 2.25%), 2/14/24 | | | | | | | 22 | | | | 22,156 | |

| | | |

Gemini HDPE, LLC, Term Loan, 3.50%, (3 mo. USD LIBOR + 3.00%, Floor 0.50%), 12/31/27 | | | | | | | 123 | | | | 123,320 | |

| | | |

H.B. Fuller Company, Term Loan, 2.116%, (1 mo. USD LIBOR + 2.00%), 10/20/24 | | | | | | | 174 | | | | 173,991 | |

| | | |

Hexion, Inc., Term Loan, 3.71%, (3 mo. USD LIBOR + 3.50%), 7/1/26 | | | | | | | 123 | | | | 122,915 | |

| | | |

Illuminate Buyer, LLC, Term Loan, 3.613%, (1 mo. USD LIBOR + 3.50%), 6/30/27 | | | | | | | 125 | | | | 123,986 | |

| | | |

INEOS Enterprises Holdings II Limited, Term Loan, 3.25%, (3 mo. EURIBOR + 3.25%), 8/31/26 | | | EUR | | | | 25 | | | | 30,044 | |

| | | |

INEOS Styrolution US Holding, LLC, Term Loan, 3.25%, (3 mo. USD LIBOR + 2.75%, Floor 0.50%), 1/29/26 | | | | | | | 400 | | | | 399,000 | |

| | | |

INEOS US Finance, LLC, Term Loan, 2.11%, (1 mo. USD LIBOR + 2.00%), 4/1/24 | | | | | | | 508 | | | | 503,378 | |

| | | |

Lonza Group AG, Term Loan, 4/29/28(19) | | | | | | | 200 | | | | 199,500 | |

| | | |

LSF11 Skyscraper Holdco S.a.r.l., Term Loan, 4.50%, (3 mo. USD LIBOR + 3.75%, Floor 0.75%), 9/29/27 | | | | | | | 125 | | | | 125,000 | |

| | | |

Messer Industries GmbH, Term Loan, 2.703%, (3 mo. USD LIBOR + 2.50%), 3/1/26 | | | | | | | 168 | | | | 166,122 | |

|

| PQ Corporation: | |

| | | |

Term Loan, 2.436%, (3 mo. USD LIBOR + 2.25%), 2/7/27 | | | | | | | 175 | | | | 173,859 | |

| | | |

Term Loan, 4.00%, (3 mo. USD LIBOR + 3.00%, Floor 1.00%), 2/7/27 | | | | | | | 232 | | | | 232,147 | |

| | | |

Pregis TopCo Corporation, Term Loan, 3.863%, (1 mo. USD LIBOR + 3.75%), 7/31/26 | | | | | | | 99 | | | | 98,519 | |

| | | |

Starfruit Finco B.V., Term Loan, 2.865%, (1 mo. USD LIBOR + 2.75%), 10/1/25 | | | | | | | 358 | | | | 353,878 | |

| | | |

Tronox Finance, LLC, Term Loan, 2.657%, (3 mo. USD LIBOR + 2.50%), 3/13/28 | | | | | | | 300 | | | | 298,018 | |

| | | |

| | | | | | | | | | | $ | 3,780,378 | |

|

| Containers and Glass Products — 0.4% | |

| | | |

BWAY Holding Company, Term Loan, 3.443%, (3 mo. USD LIBOR + 3.25%), 4/3/24 | | | | | | | 232 | | | $ | 224,089 | |

| | | | |

| | 12 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | | | |

| Borrower/Description | | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Containers and Glass Products (continued) | |

| | | |

Flex Acquisition Company, Inc., Term Loan, 3.452%, (3 mo. USD LIBOR + 3.25%), 6/29/25 | | | | | | | 218 | | | $ | 214,625 | |

| | | |

Reynolds Consumer Products, LLC, Term Loan, 1.863%, (1 mo. USD LIBOR + 1.75%), 2/4/27 | | | | | | | 304 | | | | 302,935 | |

| | | |

Reynolds Group Holdings, Inc., Term Loan, 3.363%, (1 mo. USD LIBOR + 3.25%), 2/5/26 | | | | | | | 224 | | | | 222,778 | |

|

| TricorBraun Holdings, Inc.: | |

| | | |

Term Loan, 1.696%, (3 mo. USD LIBOR + 3.25%, Floor 0.50%), 3/3/28(20) | | | | | | | 18 | | | | 18,217 | |

| | | |

Term Loan, 3.75%, (3 mo. USD LIBOR + 3.25%, Floor 0.50%), 3/3/28 | | | | | | | 82 | | | | 80,991 | |

| | | |

| | | | | | | | | | | $ | 1,063,635 | |

|

| Cosmetics / Toiletries — 0.1% | |

| | | |

Kronos Acquisition Holdings, Inc., Term Loan, 4.25%, (3 mo. USD LIBOR + 3.75%, Floor 0.50%), 12/22/26 | | | | | | | 200 | | | $ | 197,110 | |

| | | |

| | | | | | | | | | | $ | 197,110 | |

|

| Drugs — 1.5% | |

| | | |

Akorn, Inc., Term Loan, 8.50%, (3 mo. USD LIBOR + 7.50%, Floor 1.00%), 10/1/25 | | | | | | | 71 | | | $ | 73,148 | |

| | | |

Alkermes, Inc., Term Loan, 3.00%, (3 mo. USD LIBOR + 2.50%, Floor 0.50%), 3/9/26 | | | | | | | 69 | | | | 69,108 | |

| | | |

Amneal Pharmaceuticals, LLC, Term Loan, 3.625%, (1 mo. USD LIBOR + 3.50%), 5/4/25 | | | | | | | 508 | | | | 499,278 | |

| | | |

Arbor Pharmaceuticals, Inc., Term Loan, 6.00%, (3 mo. USD LIBOR + 5.00%, Floor 1.00%), 7/5/23 | | | | | | | 107 | | | | 105,453 | |

| | | |

Bausch Health Companies, Inc., Term Loan, 3.113%, (1 mo. USD LIBOR + 3.00%), 6/2/25 | | | | | | | 630 | | | | 629,660 | |

| | | |

Catalent Pharma Solutions, Inc., Term Loan, 2.50%, (1 mo. USD LIBOR + 2.00%, Floor 0.50%), 2/22/28 | | | | | | | 148 | | | | 148,182 | |

| | | |

Elanco Animal Health Incorporated, Term Loan, 1.865%, (1 mo. USD LIBOR + 1.75%), 8/2/27 | | | | | | | 291 | | | | 287,681 | |

| | | |

Grifols Worldwide Operations USA, Inc., Term Loan, 2.087%, (1 week USD LIBOR + 2.00%), 11/15/27 | | | | | | | 123 | | | | 122,175 | |

|

| Horizon Therapeutics USA, Inc.: | |

| | | |

Term Loan, 2.125%, (1 mo. USD LIBOR + 2.00%), 5/22/26 | | | | | | | 331 | | | | 329,996 | |

| | | |

Term Loan, 2.50%, (1 mo. USD LIBOR + 2.00%, Floor 0.50%), 3/15/28 | | | | | | | 325 | | | | 324,255 | |

| | | |

Jazz Financing Lux S.a.r.l., Term Loan, 4/22/28(19) | | | | | | | 250 | | | | 250,875 | |

|

| Mallinckrodt International Finance S.A.: | |

| | | |

Term Loan, 5.75%, (6 mo. USD LIBOR + 5.00%, Floor 0.75%), 2/24/25 | | | | | | | 216 | | | | 211,599 | |

| | | |

Term Loan, 6.00%, (6 mo. USD LIBOR + 5.25%, Floor 0.75%), 9/24/24 | | | | | | | 649 | | | | 636,770 | |

| | | |

| | | | | | | | | | | $ | 3,688,180 | |

| | | | | | | | | | | | |

| Borrower/Description | | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Ecological Services and Equipment — 0.2% | |

| | | |

EnergySolutions, LLC, Term Loan, 4.75%, (3 mo. USD LIBOR + 3.75%, Floor 1.00%), 5/9/25 | | | | | | | 170 | | | $ | 169,709 | |

| | | |

GFL Environmental, Inc., Term Loan, 3.50%, (1 mo. USD LIBOR + 3.00%, Floor 0.50%), 5/30/25 | | | | | | | 200 | | | | 200,268 | |

| | | |

TruGreen Limited Partnership, Term Loan, 4.75%, (1 mo. USD LIBOR + 4.00%, Floor 0.75%), 11/2/27 | | | | | | | 100 | | | | 99,854 | |

| | | |

| | | | | | | | | | | $ | 469,831 | |

|

| Electronics / Electrical — 5.8% | |

|

| Applied Systems, Inc.: | |

| | | |

Term Loan, 3.50%, (3 mo. USD LIBOR + 3.00%, Floor 0.50%), 9/19/24 | | | | | | | 687 | | | $ | 685,212 | |

| | | |

Term Loan - Second Lien, 6.25%, (3 mo. USD LIBOR + 5.50%, Floor 0.75%), 9/19/25 | | | | | | | 74 | | | | 75,187 | |

| | | |

AQA Acquisition Holding, Inc., Term Loan, 4.75%, (3 mo. USD LIBOR + 4.25%, Floor 0.50%), 3/3/28 | | | | | | | 125 | | | | 125,052 | |

| | | |

Astra Acquisition Corp., Term Loan, 5.50%, (1 mo. USD LIBOR + 4.75%, Floor 0.75%), 3/1/27 | | | | | | | 124 | | | | 124,993 | |

| | | |

Banff Merger Sub, Inc., Term Loan, 3.863%, (1 mo. USD LIBOR + 3.75%), 10/2/25 | | | | | | | 352 | | | | 350,359 | |

| | | |

Cambium Learning Group, Inc., Term Loan, 4.703%, (3 mo. USD LIBOR + 4.50%), 12/18/25 | | | | | | | 190 | | | | 190,375 | |

| | | |

CentralSquare Technologies, LLC, Term Loan, 3.953%, (3 mo. USD LIBOR + 3.75%), 8/29/25 | | | | | | | 122 | | | | 116,995 | |

| | | |

Cloudera, Inc., Term Loan, 3.25%, (1 mo. USD LIBOR + 2.50%, Floor 0.75%), 12/22/27 | | | | | | | 100 | | | | 99,532 | |

| | | |

Cohu, Inc., Term Loan, 3.113%, (1 mo. USD LIBOR + 3.00%), 10/1/25 | | | | | | | 65 | | | | 65,063 | |

| | | |

CommScope, Inc., Term Loan, 3.363%, (1 mo. USD LIBOR + 3.25%), 4/6/26 | | | | | | | 271 | | | | 269,499 | |

|

| Constant Contact, Inc.: | |

| | | |

Term Loan, 4.50%, 2/10/28(20) | | | | | | | 58 | | | | 58,090 | |

| | | |

Term Loan, 4.75%, (3 mo. USD LIBOR + 4.00%, Floor 0.75%), 2/10/28 | | | | | | | 217 | | | | 216,223 | |

| | | |

Cornerstone OnDemand, Inc., Term Loan, 3.36%, (1 mo. USD LIBOR + 3.25%), 4/22/27 | | | | | | | 233 | | | | 232,568 | |

|

| Delta TopCo, Inc.: | |

| | | |

Term Loan, 4.50%, (3 mo. USD LIBOR + 3.75%, Floor 0.75%), 12/1/27 | | | | | | | 225 | | | | 225,375 | |

| | | |

Term Loan - Second Lien, 8.00%, (3 mo. USD LIBOR + 7.25%, Floor 0.75%), 12/1/28 | | | | | | | 300 | | | | 307,500 | |

| | | |

E2open, LLC, Term Loan, 4.00%, (3 mo. USD LIBOR + 3.50%, Floor 0.50%), 10/29/27 | | | | | | | 125 | | | | 125,000 | |

| | | |

ECI Macola Max Holdings, LLC, Term Loan, 4.50%, (3 mo. USD LIBOR + 3.75%, Floor 0.75%), 11/9/27 | | | | | | | 175 | | | | 175,053 | |

| | | | |

| | 13 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | |

| Borrower/Description | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Electronics / Electrical (continued) | |

| | | |

Electro Rent Corporation, Term Loan, 6.00%, (3 mo. USD LIBOR + 5.00%, Floor 1.00%), 1/31/24 | | | | | 265 | | | $ | 265,331 | |

| | | |

Epicor Software Corporation, Term Loan, 4.00%, (1 mo. USD LIBOR + 3.25%, Floor 0.75%), 7/30/27 | | | | | 99 | | | | 98,853 | |

| | | |

EXC Holdings III Corp., Term Loan, 4.50%, (3 mo. USD LIBOR + 3.50%, Floor 1.00%), 12/2/24 | | | | | 73 | | | | 72,563 | |

| | | |

Finastra USA, Inc., Term Loan, 4.50%, (6 mo. USD LIBOR + 3.50%, Floor 1.00%), 6/13/24 | | | | | 389 | | | | 383,257 | |

| | | |

Gainwell Acquisition Corp., Term Loan, 4.75%, (3 mo. USD LIBOR + 4.00%, Floor 0.75%), 10/1/27 | | | | | 849 | | | | 850,397 | |

|

| Go Daddy Operating Company, LLC: | |

| | | |

Term Loan, 1.863%, (1 mo. USD LIBOR + 1.75%), 2/15/24 | | | | | 595 | | | | 591,125 | |

| | | |

Term Loan, 2.113%, (1 mo. USD LIBOR + 2.00%), 8/10/27 | | | | | 174 | | | | 172,806 | |

| | | |

Hyland Software, Inc., Term Loan, 4.25%, (1 mo. USD LIBOR + 3.50%, Floor 0.75%), 7/1/24 | | | | | 518 | | | | 519,056 | |

| | | |

Imperva, Inc., Term Loan, 5.00%, (3 mo. USD LIBOR + 4.00%, Floor 1.00%), 1/12/26 | | | | | 99 | | | | 99,763 | |

| | | |

Imprivata, Inc., Term Loan, 4.25%, (1 mo. USD LIBOR + 3.75%, Floor 0.50%), 12/1/27 | | | | | 175 | | | | 175,219 | |

| | | |

Informatica, LLC, Term Loan, 3.363%, (1 mo. USD LIBOR + 3.25%), 2/25/27 | | | | | 916 | | | | 908,596 | |

| | | |

LogMeIn, Inc., Term Loan, 4.86%, (1 mo. USD LIBOR + 4.75%), 8/31/27 | | | | | 274 | | | | 274,263 | |

|

| MA FinanceCo., LLC: | |

| | | |

Term Loan, 2.863%, (1 mo. USD LIBOR + 2.75%), 6/21/24 | | | | | 24 | | | | 23,859 | |

| | | |

Term Loan, 5.25%, (3 mo. USD LIBOR + 4.25%, Floor 1.00%), 6/5/25 | | | | | 270 | | | | 271,755 | |

| | | |

Maverick Bidco, Inc., Term Loan, 4/28/28(19) | | | | | 125 | | | | 124,375 | |

| | | |

Mirion Technologies, Inc., Term Loan, 4.203%, (3 mo. USD LIBOR + 4.00%), 3/6/26 | | | | | 124 | | | | 124,723 | |

| | | |

NCR Corporation, Term Loan, 2.69%, (3 mo. USD LIBOR + 2.50%), 8/28/26 | | | | | 147 | | | | 145,525 | |

| | | |

Panther Commercial Holdings L.P., Term Loan, 5.00%, (1 mo. USD LIBOR + 4.50%, Floor 0.50%), 1/7/28 | | | | | 75 | | | | 75,023 | |

| | | |

PointClickCare Technologies, Inc., Term Loan, 3.75%, (6 mo. USD LIBOR + 3.00%, Floor 0.75%), 12/29/27 | | | | | 100 | | | | 100,062 | |

| | | |

ProQuest, LLC, Term Loan, 3.363%, (1 mo. USD LIBOR + 3.25%), 10/23/26 | | | | | 259 | | | | 257,249 | |

| | | |

Rackspace Technology Global, Inc., Term Loan, 3.50%, (3 mo. USD LIBOR + 2.75%, Floor 0.75%), 2/15/28 | | | | | 225 | | | | 223,622 | |

| | | |

RealPage, Inc., Term Loan, 3.75%, (1 mo. USD LIBOR + 3.25%, Floor 0.50%), 4/24/28 | | | | | 350 | | | | 348,882 | |

| | | |

Renaissance Holding Corp., Term Loan, 3.363%, (1 mo. USD LIBOR + 3.25%), 5/30/25 | | | | | 270 | | | | 266,726 | |

| | | | | | | | | | | | |

| Borrower/Description | | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Electronics / Electrical (continued) | |

| | | |

Seattle Spinco, Inc., Term Loan, 2.863%, (1 mo. USD LIBOR + 2.75%), 6/21/24 | | | | | | | 163 | | | $ | 161,125 | |

|

| SkillSoft Corporation: | |

| | | |

Term Loan, 8.50%, (3 mo. USD LIBOR + 7.50%, Floor 1.00%), 12/27/24 | | | | | | | 60 | | | | 62,043 | |

| | | |

Term Loan - Second Lien, 8.50%, (3 mo. USD LIBOR + 7.50%, Floor 1.00%), 4/27/25 | | | | | | | 199 | | | | 199,287 | |

| | | |

Skopima Merger Sub, Inc., Term Loan, 4/30/28(19) | | | | | | | 150 | | | | 149,672 | |

| | | |

SolarWinds Holdings, Inc., Term Loan, 2.863%, (1 mo. USD LIBOR + 2.75%), 2/5/24 | | | | | | | 169 | | | | 167,281 | |

| | | |

Solera, LLC, Term Loan, 2.863%, (1 mo. USD LIBOR + 2.75%), 3/3/23 | | | | | | | 121 | | | | 120,487 | |

| | | |

SS&C European Holdings S.a.r.l., Term Loan, 1.863%, (1 mo. USD LIBOR + 1.75%), 4/16/25 | | | | | | | 146 | | | | 144,469 | |

| | | |

SS&C Technologies, Inc., Term Loan, 1.863%, (1 mo. USD LIBOR + 1.75%), 4/16/25 | | | | | | | 197 | | | | 194,770 | |

| | | |

SurveyMonkey, Inc., Term Loan, 3.84%, (1 week USD LIBOR + 3.75%), 10/10/25 | | | | | | | 215 | | | | 214,232 | |

| | | |

Symplr Software, Inc., Term Loan, 5.25%, (6 mo. USD LIBOR + 4.50%, Floor 0.75%), 12/22/27 | | | | | | | 125 | | | | 125,437 | |

| | | |

Tech Data Corporation, Term Loan, 3.613%, (1 mo. USD LIBOR + 3.50%), 6/30/25 | | | | | | | 174 | | | | 174,909 | |

| | | |

Tibco Software, Inc., Term Loan, 3.87%, (1 mo. USD LIBOR + 3.75%), 6/30/26 | | | | | | | 195 | | | | 194,145 | |

|

| Uber Technologies, Inc.: | |

| | | |

Term Loan, 3.606%, (1 mo. USD LIBOR + 3.50%), 4/4/25 | | | | | | | 219 | | | | 218,904 | |

| | | |

Term Loan, 3.606%, (1 mo. USD LIBOR + 3.50%), 2/16/27 | | | | | | | 310 | | | | 310,209 | |

|

| Ultimate Software Group, Inc. (The): | |

| | | |

Term Loan, 3.863%, (1 mo. USD LIBOR + 3.75%), 5/4/26 | | | | | | | 246 | | | | 246,693 | |

| | | |

Term Loan, 4.00%, (3 mo. USD LIBOR + 3.25%, Floor 0.75%), 5/4/26 | | | | | | | 622 | | | | 623,378 | |

| | | |

Ultra Clean Holdings, Inc., Term Loan, 3.863%, (1 mo. USD LIBOR + 3.75%), 8/27/25 | | | | | | | 196 | | | | 196,619 | |

| | | |

Valkyr Purchaser, LLC, Term Loan, 4.75%, (3 mo. USD LIBOR + 4.00%, Floor 0.75%), 10/29/27 | | | | | | | 125 | | | | 125,703 | |

| | | |

Verifone Systems, Inc., Term Loan, 4.182%, (3 mo. USD LIBOR + 4.00%), 8/20/25 | | | | | | | 171 | | | | 168,200 | |

| | | |

Veritas US, Inc., Term Loan, 6.00%, (3 mo. USD LIBOR + 5.00%, Floor 1.00%), 9/1/25 | | | | | | | 398 | | | | 401,796 | |

| | | |

VS Buyer, LLC, Term Loan, 3.113%, (1 mo. USD LIBOR + 3.00%), 2/28/27 | | | | | | | 173 | | | | 172,239 | |

| | | |

Vungle, Inc., Term Loan, 5.607%, (1 mo. USD LIBOR + 5.50%), 9/30/26 | | | | | | | 99 | | | | 98,993 | |

| | | |

| | | | | | | | | | | $ | 14,285,697 | |

| | | | |

| | 14 | | See Notes to Financial Statements. |

Eaton Vance

Short Duration Diversified Income Fund

April 30, 2021

Portfolio of Investments (Unaudited) — continued

| | | | | | | | | | | | |

| Borrower/Description | | | | | Principal

Amount*

(000’s omitted) | | | Value | |

|

| Equipment Leasing — 0.2% | |

| | | |

Avolon TLB Borrower 1 (US), LLC, Term Loan, 3.25%, (1 mo. USD LIBOR + 2.50%, Floor 0.75%), 12/1/27 | | | | | | | 299 | | | $ | 299,522 | |

| | | |

Delos Finance S.a.r.l., Term Loan, 1.953%, (3 mo. USD LIBOR + 1.75%), 10/6/23 | | | | | | | 298 | | | | 297,420 | |

| | | |

| | | | | | | | | | | $ | 596,942 | |

|

| Financial Intermediaries — 1.0% | |

| | | |