The following table sets forth information relating to our outstanding equity compensation plans as of December 31, 2008:

A description of our 2005 Equity Incentive Compensation Plan is contained later in this Report under Part III, Item 11 – “Executive Compensation - Stock Option Plans”.

None.

As a smaller reporting company, we are not required to provide the information required under this item.

The following discussion and analysis of our consolidated financial conditions and results of operations for the year ended December 31, 2008 and 2007 should be read in conjunction with the consolidated financial statements and the related notes to our consolidated financial statements and other information presented elsewhere in this Report. The following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to those discussed below and elsewhere in this Report, particularly in the item entitled “Risk Factors” beginning on page 8 of this Report. Our consolidated audited financial statements are stated in United States Dollars and are prepared in accordance with United States Generally Accepted Accounting Principles.

Our strategic plan is, with respect to our gold projects: (i) to define potential reserves on our exploration projects; (ii) to mine the mineralized material, where possible, to generate cash proceeds to assist funding of our exploration programs; and (iii) to acquire further interests in gold mineralized projects and oil and gas prospects that fall within the criteria of providing a geological basis for development of drilling initiatives that can enhance shareholder value by demonstrating potential to define reserves.

We anticipate that our ongoing efforts, subject to adequate funding being available, will continue to be focused on the exploration and development of our properties and completing acquisitions in strategic areas.

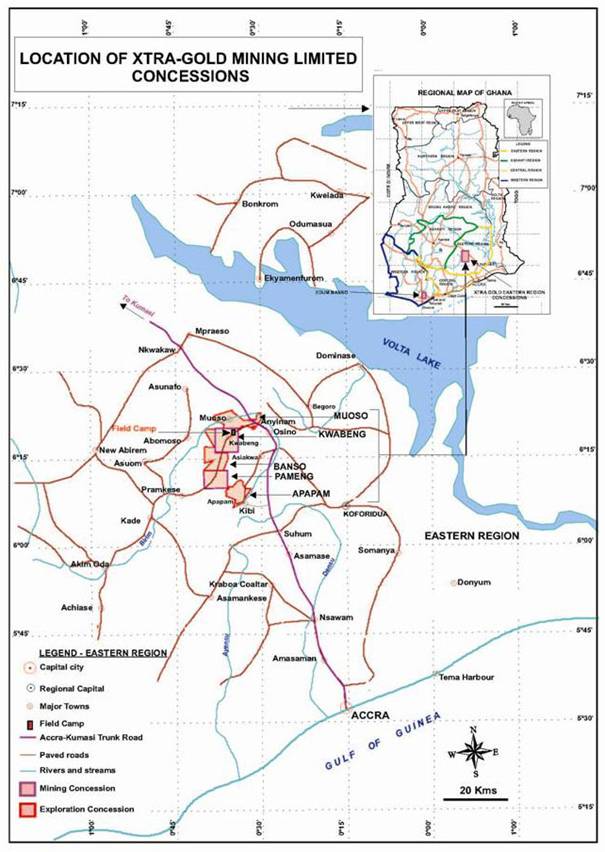

Our ability to continue to expand land acquisitions and drilling opportunities during the next 12 months is dependent on adequate capital resources being available. In October 2008, we temporarily suspended our operations at the Kwabeng Project while Management considers a more economic and efficient manner in which to extract and process the gold recovered from the mineralized material at this Project. Assuming that we will be able to continue to derive cash proceeds from the sale of the gold recovered from the mineralized material at our Kwabeng Project, we intend to continue to advance operations at our Kwabeng Project, recover gold for sale and acquire further interests in mineral projects by way of acquisition or joint venture participation.

We anticipate that, over the next 12 months, we will spend an aggregate of $2,000,000 comprised of $500,000 for mining operating, capital and administrative costs at our Kwabeng Project, $1,000,000 for exploration expenses and approximately $500,000 for general and administrative expenses. However, we would not expend this amount unless we are able to derive cash proceeds from the sale of the gold recovered from the mineralized material at our Kwabeng Project or raise additional capital.

We require additional capital to implement our plan of operations. We anticipate that these funds primarily will be raised through equity and debt financing or from other available sources of financing. If we raise additional funds through the issuance of equity or convertible debt securities, it may result in the dilution in the equity ownership of investors in our common stock. There can be no assurance that additional financing will be available upon acceptable terms, if at all. If adequate funds are not available or are not available on acceptable terms, we may be unable to take advantage of prospective new opportunities or acquisitions, which could significantly and materially restrict our operations, or we may be forced to discontinue our current projects.

We do not expect to purchase significant ore processing and gold recovery equipment as our Wash Plant has sufficient capacity to handle our processing requirements at our Kwabeng Project. We rent our earthmoving and ancillary earthmoving equipment fleet in connection with our operations at our Kwabeng Project. We plan to increase the number of key mining personnel including technical consultants, contractors and skilled laborers during the next 12 months. Our current business strategy is that we plan to continue engaging technical personnel under contract where possible as Management believes that this strategy, at its current level of development, provides the best services available in the circumstances, leads to lower overall costs, and provides the best flexibility for our business operations.

The cash proceeds derived from the sale of 608.50 fine ounces of gold recovered from the mineralized material at our Kwabeng Project during the Bulk Test (defined herein), as discussed elsewhere in this Report, was categorized as Recovery of Gold. The Bulk Test was only a pre-production stage test that was completed on March 25, 2007. Since April 24, 2007 to December 31, 2008, we have recovered 8,162.84 fine ounces of gold from the mineralized material at our Kwabeng Project and derived cash proceeds of $6,441,593 from the related gold sales.

Results of Operations for the Year Ended December 31, 2008 Compared to the Year Ended December 31, 2007

Our loss for the year ended December 31, 2008 was $3,231,403 as compared to a loss of $1,874,757 for the year ended December 31, 2007, an increase of $1,356,646. We incurred expenses of $6,239,722 in the year ended December 31, 2008 as compared to $5,319,503 in the year ended December 31, 2007, an increase of $920,219. The increase in expenses in the year ended December 31, 2008 can be primarily attributed to exploration costs of $5,140,679 incurred mostly in connection with (a) exploration programs at our Banso and Muoso Project, our Apapam Project and our Edum Banso Project; (b) a drilling program of 3,001 meters; and (c) operational costs for our Kwabeng Project as compared to $3,932,845 expended on these projects in the year ended December 31, 2007. Exploration costs were incurred in connection with our exploration programs at our Banso and Muoso, Apapam and Edum Banso Projects and costs associated with extracting and producing the mineralized material at our Kwabeng Project which we have booked as exploration expenses. General and administrative expenses (“G&A”) were $1,035,369 as compared to $1,348,898 for the year ended December 31, 2007. A down-sizing of management consultants, a significant reduction in legal costs and labor costs at our Kwabeng Project in the year ended December 31, 2008 attributed to the decrease in G&A.

- 44 -

Our loss for the year ended December 31, 2008 was greater than our loss for the year ended December 31, 2007 due to (i) a significant net unrealized loss on trading securities of $857,980 (compared to a gain of $389,793 in 2007); and (ii) a foreign exchange loss of $424,559 (compared to a foreign exchange gain of $366,687 in 2007). Trading securities were comprised mostly of investments in common shares and income trust units of resource companies. The net unrealized loss can be attributed to a decrease in the market value of those securities due to poor market conditions and economic strain, in particular, the significant weakening of the Canadian dollar in which our marketable securities are denominated.

Other items totaled a gain of $3,008,319 for the year ended December 31, 2008 compared to a gain of $3,444,746 for the year ended December 31, 2007. In particular, during the year ended December 31, 2008, we recovered and sold 4,809.02 fine ounces of gold recovered from the mineralized material at our Kwabeng Project for cash proceeds of $4,140,765 which was booked as Recovery of Gold as compared to $2,692,242 for the year ended December 31, 2007. We had a foreign exchange loss of $424,559 for the year ended December 31, 2008 (2007 – gain of $366,687) which can be attributed to the weakening of the Canadian dollar. Our portfolio of marketable securities is largely Canadian currency denominated. The sharp depreciation of the Canadian dollar resulted in the bulk of the foreign exchange loss. Additionally, the continuing strength of the US dollar increased our expenses that are denominated in other foreign currencies. Consequently, transactions denominated in US dollars would be more expensive.

Our portfolio of marketable securities had an unrealized loss of $857,980 (compared to an unrealized gain of $389,793 in 2007) due to declining market conditions and economic strain which commenced in the summer of 2008. Our securities portfolio realized a gain of $2,585 on the sale of trading securities during the year ended December 31, 2008 compared to a loss in 2007 of $94,855. Other income derived from dividends increased slightly (2007 - $196,621; 2007 - $163,119). The decrease in our interest expense (2008 - $49,113; 2007 - $72,240) is largely attributable to our convertible debentures which interest we ceased paying from the end of the second quarter due to the automatic conversion of the debentures.

Our basic and diluted loss per share for the year ended December 31, 2008 was $0.11 compared to $0.07 per share for the year ended December 31, 2007. The weighted average number of shares outstanding was 30,389,400 at December 31, 2008 compared to 28,216,728 for the year ended December 31, 2007. The increase in the weighted average number of shares outstanding can be attributed to the issuance of (i) 1,062,000 shares in connection with a private placement financing completed during fiscal 2008; (ii) 100,000 shares in connection with an exercise of stock options; (iii) 650,000 shares in connection with an automatic conversion of debentures; (iv) 631,000 shares in connection with an exercise of warrants; and (v) 131,243 shares in connection with a settlement of outstanding accounts for services rendered to our subsidiary, XG Mining.

Liquidity and Capital Resources

Historically, our principal source of funds is our available resources of cash and cash equivalents and investments, as well as debt and equity financings. During the year ended December 31, 2008, we received cash proceeds of $4,140,765 derived from the sale of gold recovered from the mineralized material at our Kwabeng Project during this financial reporting period.

Unrealized Gain on Trading Securities

Unrealized gain on trading securities represents the change in value of securities as of the end of the financial reporting period. For the year ended December 31, 2008, we recognized an unrealized loss of $857,980 on trading securities, as compared to an unrealized gain of $389,793 for the year ended December 31, 2007. The change reflects a significant decline in the value of our resource company investments following a significant rebound during 2007. Trading securities were comprised mostly of investments in common shares and income trust units of resource companies.

Liquidity Discussion

Net cash provided by financing activities for the year ended December 31, 2008 was $2,489,460 (2007 - $812,540).

As of December 31, 2008, we had working capital equity of $1,299,625, comprised of current assets of $1,834,897 less current liabilities of $535,272. Our current assets were comprised mostly of $271,573 in cash and cash equivalents and $1,470,382 in trading securities, which is based on our analysis of the ready saleable nature of the securities including an existing market for the securities, the lack of any restrictions for resale of the securities and sufficient active volume of trading in the securities. Our trading securities are held in our investment portfolio with an established brokerage in Canada in which we primarily invest in the common shares and income trust fund units of publicly traded resource companies.

- 45 -

We have historically relied on equity and debt financings to finance our ongoing operations. Existing working capital, possible debt instruments, anticipated warrant exercises, further private placements and anticipated cash flow are expected to be adequate to fund our operations over the next year. We have no lines of credit or other bank financing arrangements. Generally, we have financed operations to date through the proceeds of the private equity financings and a convertible debt financing. In connection with our business plan, Management anticipates operating expenses and capital expenditures as follows: (i) $1,000,000 for exploration; (ii) $500,000 for mine operating, capital and administration costs at our Kwabeng Project; and (iii) $500,000 for general and administrative costs.

Until we achieve profitability, we will need to raise additional capital for our exploration programs. We intend to finance these expenses with our cash proceeds and to the extent that our cash proceeds are not sufficient, then from further sales of our equity securities or debt securities, or from investment income. Thereafter, we may need to raise additional capital to meet long-term operating requirements. Additional financing may not be available upon acceptable terms, or at all. If adequate funds are not available or are not available on acceptable terms, we may not be able to take advantage of prospective new business endeavors or opportunities or existing agreements and projects which could significantly and materially restrict our business operations.

The independent auditors’ report accompanying our December 31, 2008 and December 31, 2007 consolidated financial statements contains an explanatory paragraph expressing doubt about our ability to continue as a going concern. The consolidated financial statements have been prepared “assuming that we will continue as a going concern”, which contemplates that we will realize our assets and satisfy our liabilities and commitments in the ordinary course of business.

Material Commitments

Mineral Property Commitments

Save and except for fees payable from time to time to (i) the Minerals Commission for an extension of an expiry date of a prospecting license (current consideration fee payable is $15,000) or mining lease or annual operating permits; (ii) the EPA for the issuance of permits prior to the commencement of any work at a particular concession or the posting of a bond in connection with any mining operations undertaken by our company; and (iii) a legal obligation associated with our mineral properties for clean up costs when work programs are completed, we are committed to expend an aggregate of less than $500 in connection with annual or ground rent and mining permits to enter upon and gain access to the following concessions and such other financial commitments arising out of any approved exploration programs in connection therewith:

| (i) | the Kwabeng concession (Kwabeng Project); |

| (ii) | the Pameng concession (Pameng Project); |

| (iii) | the Banso and Muoso concessions (Banso and Muoso Project); |

| (iv) | the Apapam concession (Apapam Project); and |

| (v) | the Edum Banso concession (Edum Banso Project). |

With respect to the Kwabeng, Pameng and Apapam Projects, upon and following the commencement of gold production, a royalty of 3% of the net smelter returns is payable quarterly to the Government of Ghana.

With respect to the Edum Banso Project:

| (a) | $5,000 is payable to Adom Mining Limited (“Adom”) on the anniversary date of the Option Agreement in each year that we hold an interest in the agreement; |

| (b) | $200,000 is payable to Adom when the production of gold is commenced (or $100,000 in the event that less than 2 million ounces of proven and probable reserves are discovered on our project at this concession; and |

| (c) | an aggregate production royalty of 2% of the net smelter returns (“NSR”) from all ores, minerals and other products mined and removed from the project, except if less than 2 million ounces of proven and probable reserved are discovered in or at the Project, then the royalty shall be 1% of the NSR. |

- 46 -

Repayment of Convertible Debentures and Accrued Interest

We are committed to repay our Convertible Debenture holders outstanding amounts of principal and interest calculated at 7% per annum on an aggregate face value of $900,000. Interest only payments are payable quarterly on the last days of September, December, March and June in each year of the term or until such time that the principal has been repaid in the full. The Convertible Debenture holders are entitled, at their option, to convert, at any time and from time to time, until payment in full of their respective Convertible Debentures, all or any part of the outstanding principal amount of the Convertible Debenture, plus the Accrued Interest, into shares (the “Conversion Shares”) of our common stock at the conversion price of $1.00 per share (the “Conversion Price”). Provided there is a registration statement then in effect covering the Conversion Shares, or the Conversion Shares may otherwise be resold pursuant to Rule 144, the outstanding principal amount of each Convertible Debenture, and all accrued but unpaid interest, shall automatically be converted into shares of our common stock, at the Conversion Price, in the event that our common stock trade for 20 consecutive trading days (a) with a closing bid price of at least $1.50 per share and (b) a cumulative trading volume during such twenty (20) trading day period of at least 1,000,000 shares.

In June 2008, we provided notice of automatic conversion of the Convertible Debentures and in July 2008 we converted $650,000 of the aggregate principal of the Convertible Debentures by way of the issuance of 650,000 Conversion Shares.

Purchase of Significant Equipment

We do not expect to purchase significant ore processing and gold recovery equipment as our Wash Plant has sufficient capacity to handle our processing requirements at our Kwabeng Project. We rent our earthmoving and ancillary earthmoving equipment fleet in connection with our ongoing operations at our Kwabeng Project.

Off Balance Sheet Arrangements

We have no off balance sheet arrangements.

Significant Accounting Applications

Application of Critical Accounting Policies

We believe the following critical accounting policies affect our more significant judgments and estimates used in the preparation of our financial statements.

Mineral Properties

The valuation of our mineral properties (the “Assets”) is based upon the fair value of cash or securities issued as consideration for the purchase of the Assets.

Asset Retirement Obligation

The fair value of our asset retirement obligation is recorded as liabilities when they are incurred. As such, the valuation could be affected by the following:

Costs - When work actually commences on asset retirement obligations, actual costs could materially differ from what has been projected. This would materially affect the value of the obligation.

Ghanaian laws and regulations - If the Government of Ghana approves or changes laws and regulations that affect mining operations in Ghana, the cost of meeting our asset retirement obligations could change materially.

Deferred Income Taxes

As we have no history of profitability and currently have derived limited cash proceeds, we have recognized a 100% valuation on our future tax assets. If our company becomes profitable in the future, a material amount of these future tax assets could actually be realized.

- 47 -

Recent Accounting Pronouncements

In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging Activities”. SFAS No. 161 changes the disclosure requirements for derivative instruments and hedging activities by requiring enhanced disclosures about how and why an entity uses derivative instruments, how derivative instruments and related hedged items are accounted for under SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities,” and how derivative instruments and related hedged items affect an entity’s operating results, financial position, and cash flows.

SFAS No. 161 is effective for fiscal years beginning after November 15, 2008. Early adoption is permitted. The Company is currently reviewing the provisions of SFAS No. 161 and have not yet adopted the statement. However, as the provisions of SFAS No. 161 are only related to disclosure of derivative and hedging activities, the Company does not believe the adoption of SFAS No. 161 will have a material impact on the consolidated operating results, financial position, or cash flows.

In April 2008, the FASB issued FSP FAS 142-3, Determination of the Useful Life of Intangible Assets or FSP FAS 142-3. FSP FAS 142-3 amends the factors that should be considered in developing renewal or extension assumptions used to determine the useful life of a recognized intangible asset under SFAS No. 142, Goodwill and Other Intangible Assets. The intent of the position is to improve the consistency between the useful life of a recognized intangible asset under SFAS No. 142 and the period of expected cash flows used to measure the fair value of the intangible asset. FSP FAS 142-3 is effective for fiscal years beginning after December 15, 2008. The Company is assessing the potential impact that the adoption of FSP FAS 142-3 may have on the Company’s consolidated financial position, results of operations or cash flows.

In May 2008, the FASB issued SFAS No. 162, The Hierarchy of Generally Accepted Accounting Principles or SFAS No. 162. SFAS No. 162 identifies the sources of accounting principles and the framework for selecting the principles used in the preparation of financial statements of nongovernmental entities that are presented in conformity with GAAP. This statement shall be effective 60 days following the Securities and Exchange Commission’s approval of the Public Company Accounting Oversight Board amendments to AU Section 411, The Meaning of Present Fairly in Conformity With Generally Accepted Accounting Principles. The Company does not believe that implementation of this standard will have a material impact on the consolidated financial position, results of operations or cash flows.

In June 2008, the FASB issued FSP No. EITF 03-6-1, “Determining Whether Instruments Granted in Share-Based Payment Transactions Are Participating Securities,” (FSP EITF 03-6-1). FSP EITF 03-6-1 states that unvested share-based payment awards that contain nonforfeitable rights to dividends or dividend equivalents (whether paid or unpaid) are participating securities and shall be included in the computation of earnings per share pursuant to the two-class method. FSP EITF 03-6-1 is effective for fiscal years beginning after December 15, 2008. Management has determined that the adoption of FSP EITF 03-6-1 will not have an impact on the Financial Statements.

We do not anticipate that the adoption of the foregoing pronouncements will have a material effect on our company’s consolidated financial position or results of operations.

Item 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

As a smaller reporting company, we are not required to provide the information required under this item.

Item 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA |

Our financial statements are contained in pages F-1 through F-24, which appear at the end of this annual report.

- 48 -

Item 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

There have been no changes in and disagreements with our accountants on accounting and financial disclosure from the inception of our company through to the date of this Report.

Item 9A(T). | CONTROLS AND PROCEDURES |

Disclosure Controls and Procedures

Our management, including our Chief Executive Officer who also serves as our Chief Financial Officer, evaluated the effectiveness of our disclosure controls and procedures (as defined in Exchange Act Rule 13a-15(e)) as of the end of the period covered by this Report. Based on that evaluation, our Chief Executive Officer concluded that as of the end of the period covered by this Report our disclosure controls and procedures were not effective such that the information required to be disclosed in our Securities and Exchange Commission reports (i) is recorded, processed, summarized and reported within the time periods specified in SEC rules and forms; and (ii) is accumulated and communicated to our management, including our Chief Executive Officer, to allow timely decisions regarding required disclosure. Our Chief Executive Officer is not a financial or accounting professional, and we lack any accounting staff who are sufficiently trained in the application of U.S. generally accepted accounting principles. Until such time as we hire a chief financial officer or similarly titled person with the requisite experience in the application of U.S. GAAP, there is a likelihood that we may experience material weaknesses in our disclosure controls that may result in errors in our financial statements in future periods.

Our management, including our Chief Executive Officer, does not expect that our disclosure controls and procedures or our internal controls will prevent all error and all fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints and the benefits of controls must be considered relative to their costs. Due to the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within our company have been detected.

Management’s Report on Internal Control over Financial Reporting

As we were not subject to the reporting requirements of the Securities Exchange Act of 1934 at December 31, 2008, our management was not then required to assess the effectiveness of our internal control over financial reporting as of December 31, 2008 pursuant to Section 404 of the Sarbanes-Oxley Act of 2002.

This annual report does not include an attestation report of the Registrant’s independent registered public accounting firm regarding internal control over financial reporting. Management’s report was not subject to attestation by the Registrant’s registered public accounting firm pursuant to temporary rules of the Securities and Exchange Commission that permit the Registrant to provide only management’s report in this annual report.

Changes in Internal Control over Financial Reporting

There has been no change in our internal control over financial reporting identified in connection with our evaluation that occurred during the last fiscal quarter that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

Item 9B. | OTHER INFORMATION |

None.

- 49 -

PART III

Item 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE |

Directors and Executive Officers

The following individuals serve as our executive officers and members of our Board:

Name | Age | Position |

James Longshore | 42 | President, Chief Executive Officer, Chief Financial Officer and Director |

Richard Grayston | 64 | Chairman of the Board and Director |

Peter Minuk | 44 | Director |

Rebecca Kiomi Mori | 58 | Secretary and Treasurer |

Robert H. Montgomery | 47 | Director |

Yves Pierre Clement | 44 | Vice-President, Exploration |

Alhaji Nantogma Abudulai | 66 | Vice-President, Ghana Operations |

James Werth Longshore, BA, Economics

President (Principal Executive Officer), Principal Financial Officer and Director

Mr. Longshore is one of the founders of our company and was appointed as President in March 2007 and a director in November 2006. Mr. Longshore has been a director of our Ghanaian subsidiaries, XGEL and XOG Ghana, since April 2006 and XG Mining, since June 2006 and an officer and director of Xtra Energy since March 2007. Mr. Longshore has approximately 17 years of business experience. Since 1995 to the present, Mr. Longshore has been President of Brokton International Ltd. (“Brokton”), a Turks & Caicos Islands, British West Indies based private investment company focused on investing in natural resource companies. Since February 2004 until February 2006, Mr. Longshore has provided financial advisory consulting services to our company through his corporation, Brokton. From 1990 to 1995, he was a salesman for UNUM Insurance Company selling in both the United States and Canada.

In August 2002, Mr. Longshore, formerly known as James Pincock, entered into a settlement agreement and order with the Ontario Securities Commission (the “OSC”). Pursuant to a settlement agreement reached between the OSC and Mr. Longshore, he voluntarily agreed to abide by the order which included, among other things, that he cease trading in securities for five years from the date of the order (until August 27, 2007), with the exception that after three years he can trade in securities beneficially owned by him in his personal accounts in his name, and that he be prohibited from becoming or acting as an officer or director of any issuer in Ontario or an officer or director of any issuer which has an interest directly or indirectly in any registrant, for a period of five years. Mr. Longshore paid the OSC approximately $17,740 for cost incurred by the OSC and its Staff with respect to the proceeding. Mr. Longshore disclosed this matter to the company prior to his appointment as a director and advised that as he was a non-resident of Ontario at the relevant time, he had sought, relied and acted upon poor financial and legal advice of Ontario advisors and completed certain securities transactions which ultimately gave rise to the Order.

Mr. Longshore devotes approximately 90% of his time to our company. He currently provides 10% of his time to unrelated companies. He has not entered into a management consulting agreement with our company.

Richard W. Grayston

Chairman and Director

Mr. Grayston was appointed as Chairman and a director of our company in March 2007. Since 1985, Mr. Grayston has been a self-employed business consultant with more than 23 years of experience in financial and economic consulting and public company management including preparation of valuations, feasibility studies, capital budgeting, financial reorganizations, profit improvement studies and business plans and going public and business brokerage during which time he has provided his consulting services to oil and gas, mineral exploration, technology, manufacturing, retail and wholesale consumer businesses. Since May 2008, Mr. Grayston has been a director of Ranger Canyon Energy Inc., a private Alberta, Canada oil and gas company seeking listing on the TSX Venture

- 50 -

Exchange (the “TSXV”) and was appointed its Chief Executive Officer and Chief Financial Officer in October 2008. Since September 2008, he has been the Vice President, Finance and Chief Financial Officer of Ruby Red Resources Inc., a TSXV listed issuer. Since January 1991 to May 2008, Mr. Grayston was a director of New Cantech Ventures Inc., an oil and gas and mineral exploration (diamonds and gold) company listed on the TSXV. From April 1980 to September 1985, Mr. Grayston served as the Executive Vice President, Secretary and a director of Brent Resources Group Ltd., a TSXV and NASDAQ listed junior oil company with operations in Canada, the U.S.A. and Australia. Mr. Grayston received a Ph.D. in Business Administration, Finance and Economics from the University of Chicago in 1971, a MBA from the University of Chicago in 1969, a BA, in Commerce and Business Administration from the University of British Columbia in 1966 and has been a certified general accountant since 1977.

Peter Minuk

Director

Mr. Minuk was appointed as Vice-President, Finance (“VP, Finance”) and a director of our company in March 2007. He resigned as VP, Finance effective January 31, 2009. Mr. Minuk has more than 21 years of experience in finance and investment as well as experience in project management, training and developing staff and client relationships. Prior to joining our company, from 1990 to 2006, Mr. Minuk was employed by BMO InvestorLine (“BMO”) in connection with implementing project management protocols. Mr. Minuk received a Masters Certificate in Project Management from the Schulich School of Business, York University in 2005. He obtained his FCSI (Fellow of the Canadian Securities Institute) in 1989 and completed the Business Administration program from Southern Alberta Institute of Technology in 1985.

Rebecca Kiomi Mori

Secretary and Treasurer

Ms. Mori was appointed Secretary and Treasurer of our company in September 2005 and was further appointed as a director of our company in April 2006. . Ms. Mori resigned as a director of our company in July 2008. Since March 2007, Ms. Mori has been a director of Verbina Resources Inc. (“Verbina”) and was appointed Secretary-Treasurer in August 2007. Verbina is a uranium and silica exploration company listed on the TSXV. Ms. Mori has approximately 26 years of legal experience. During the last 14 years, she has worked exclusively with both public and private mining companies and also at a Toronto, Ontario, Canada corporate securities law firm. Prior to joining our company as Secretary and Treasurer, Ms. Mori was (i) the Corporate Securities Legal Assistant for Roxy Resources Inc., a private Canadian mining company from December 2003 to May 2005, (ii) a consultant to our company from June 2005 to August 2005 for purposes of becoming Secretary and Treasurer, and (iv) responsible for the corporate operations including the maintenance of corporate records and regulatory reporting requirements for Valucap Investments Inc. from July 1997 to June 2004 and Romarco Minerals Inc. from May 1997 to March 2003. Prior thereto, she was a corporate securities legal assistant and/or law clerk at numerous Toronto, Canada law firms. Ms. Mori has diverse legal experience with respect to securities, corporate, accounting, finance and litigation matters and is knowledgeable and experienced in Canadian and U.S. securities matters.

As of the date of this Report, Ms. Mori devotes a variable percentage of her time in consulting services to our company and provides her services on an “as needed” basis. She provides the majority of her time to unrelated companies. There is no management consulting agreement in force at this time. She previously entered into a non-disclosure agreement with our company which remains in force.

Robert H. Montgomery, CA

Director

Mr. Montgomery was appointed as a director of our company in March 2007. Mr. Montgomery has more than 14 years of experience as a chartered accountant and auditor and since February 2004 to the present time, he has been a Sarbanes Oxley contractor to the Canadian Imperial Bank of Commerce (CIBC), from February 2004 to January 2005, the Bank of Montreal (BMO) from January to September 2005 and a major Canadian investment dealer from September 2005 to December 2006 where he was responsible for documentation and testing of key financial and non-financial controls for various lines of business and assisted in the preparation and transfer of Sarbanes Oxley audit files and supporting documentation from their project groups to internal and external auditors.

- 51 -

Mr. Montgomery assisted in the design of process narrative and control testing documents, planned and supervised the control testing program at a major Canadian investment dealer and assisted in the remediation of control gaps and weaknesses identified during the testing process and as identified by its external auditors. At CIBC, Mr. Montgomery assisted in the update and maintenance a database identifying key accounts, linking them to controls procedures, testing and lines of business and assisted in the remediation of control gaps and weaknesses identified during the testing process. He was not employed during the periods December 2006 to March 2007 and August 2003 to February 2004. Prior thereto, from January 2001 to August 2003, Mr. Montgomery was the Manager, Financial Operations of Ellis Entertainment Corporation, Toronto where he was responsible for accounting and financial reporting. Mr. Montgomery was a Senior Auditor and Auditor of the US/Canada Regional Audit Group of Walt Disney Company in Toronto from 1998 to 2000 and 1996 to 1997 respectively where he conducted contractual compliance audits for the product licensing divisions throughout the U.S. and Canada assessing audit risk factors and developing methodologies to validate information supplied by licensees relating to royalty reporting and maintenance of quality controls for licensed products. Prior thereto, Mr. Montgomery was a Senior Staff Accountant - Audit from 1994 to 1995 at Price Waterhouse LLP, Toronto, an audit and tax contractor from 1992 to 1994 and a Staff Accountant - Audit at Deloitte & Touche LLP, Toronto from 1990 to 1992. He obtained his Chartered Accountant designation from the Institute of Chartered Accountants of Ontario in 1994 and a BA, Double Major Economics and Geography from the University of Victoria, Victoria, British Columbia in 1985

Yves Pierre Clement, P. Geo.

Vice-President, Exploration of the Registrant

Mr. Clement was appointed Vice-President, Exploration of our company in May 2006. Mr. Clement has over 20 years experience in the generation, evaluation and development of a wide variety of mineral resources hosted by a broad spectrum of geological environments in Canada and South America. Prior to joining our company, Mr. Clement was senior project geologist for Lake Shore Gold Corp. in the Timmins lode gold camp from August 2005 to April 2006 and was formerly exploration manager for Aurora Platinum Corp.’s Sudbury operations from August 2000 to July 2005. Prior to joining Aurora, Mr. Clement was senior project geologist/exploration manager for Southwestern Resources Corp. where he was responsible for the generation of precious and base metal exploration opportunities in Peru and Chile. Mr. Clement’s experience will allow us to further maximize the value of our existing portfolio of projects, as well as allowing us to expand our strategy of growth through strategic acquisitions.

Mr. Clement devotes approximately 50% of his time in consulting services to our company. He provides 50% of his time to an unrelated company. He has entered into a management consulting agreement but has not entered into a non-competition and non-disclosure agreement with our company.

Alhaji Nantogma Abudulai, BA

Vice-President, Ghana Operations

Mr. Abudulai was appointed as Vice-President, Ghana Operations of our company in April 2005. He is also the Secretary and the President, Community Relations and a director of our Ghanaian subsidiaries. Mr. Abudulai has more than 13 years of business experience in the mining industry. Since 1994 to the present, he has been the managing director of CME (Ghana) Ltd. and a director of CME (Nigeria) Ltd. where his responsibilities included protocol and coordination of government and local authority affairs in Ghana and overseeing logistical support. Mr. Abudulai is familiar and experienced with respect to obtaining mining permits, prospecting and reconnaissance licenses and the government regulations relating thereto and is knowledgeable in connection with environmental and forestry issues, immigration and customs affairs. He is also the President of the Canadian Business Association in Ghana. Mr. Abudulai’s primary responsibilities with our company is the continued improvement of community and government relations on behalf of our Ghanaian subsidiaries. His experience and background will assist us with respect to acquiring approvals, prospecting licenses, mining leases and related permits and renewals from the relevant government authorities in order to advance our operations in Ghana and acting as our primary government liaison in connection therewith.

As at the date of this Report, Mr. Abudulai devotes a variable amount of his time in consulting services to our company, as he is currently engaged on an “as needed” basis. He provides the majority of his time to unrelated companies. There is no management consulting agreement in force at this time. He previously entered into a non-disclosure agreement with our company which remains in force.

There are no family relationships between any of the executive officers and directors. Each director currently holds office until he resigns or his successor is elected at an annual stockholders’ meeting.

- 52 -

Consultants

One of our business strategies is to outsource other services as required by our company from time to time by engaging consultants on an “as needed” basis or entering into special purpose contracts with a view to maintaining our overhead at a reasonable, affordable cost.

Compliance with Section 16(a) of the Exchange Act

We are not currently subject to Section 16(a) of the Securities Exchange Act of 1934, and, therefore, our directors and executive officers, and persons who own more than 10% of our common stock are not required to file with the Securities and Exchange Commission reports disclosing their initial ownership and changes in their ownership of our common stock.

Corporate Governance Matters

Committees Generally

Our Board has not established any committees. In March 2007, we expanded our Board by appointing two independent directors, Mr. Richard Grayston and Mr. Robert Montgomery, and we intend to establish audit and compensation committees in the future.

Audit Committee

Our Board has not yet established an audit committee. The functions of the audit committee are currently performed by the entire Board. We are not currently subject to any law, rule or regulation requiring that we establish or maintain an audit committee. We may establish an audit committee in the future if the Board determines it to be advisable or we are otherwise required to do so by applicable law, rule or regulation.

Board of Directors Independence

Our Board consists of four members. Although, we are not currently subject to any law, rule or regulation requiring that all or any portion of our Board include “independent” directors, two of our directors are considered to be an “independent” director, within the meaning of Nasdaq Marketplace Rule 4200.

Audit Committee Financial Expert

While we have not yet established an audit committee, Robert Montgomery is an “audit committee financial expert” within the meaning of Item 401(h)(1) of Regulation S-K. In general, an “audit committee financial expert” is an individual member of the audit committee (board of directors) who (a) understands generally accepted accounting principles and financial statements, (b) is able to assess the general application of such principles in connection with accounting for estimates and accruals, (c) has experience preparing, auditing, analyzing or evaluating financial statements comparable to the breadth and complexity of issues that can reasonably be expected to be raised by the company’s financial statements, (d) understands internal controls over financial reporting (e) understands audit committee functions, and (f) is an independent director.

Code of Ethics

Effective May 12, 2008, we adopted a Code of Ethics applicable to our principal executive officer, principal financial and accounting officers and persons performing similar functions. A Code of Ethics is a written standard designed to deter wrongdoing and to promote (a) honest and ethical conduct, (b) full, fair, accurate, timely and understandable disclosure in regulatory filings and public statements, (c) compliance with applicable laws, rules and regulations, (d) the prompt reporting violation of the code and (e) accountability for adherence to the Code. We will provide a copy of our Code of Ethics, without charge, to any person desiring a copy of the Code of Ethics, by written request to us at our principal offices.

Nominating Committee

We have not yet established a nominating committee. Our Board, sitting as a board, performs the role of a nominating committee. We are not currently subject to any law, rule or regulation requiring that we establish a nominating committee.

- 53 -

Compensation Committee

We have not yet established a compensation committee. Our Board, sitting as a board, performs the role of a compensation committee. We are not currently subject to any law, rule or regulation requiring that we establish a compensation committee.

Nomination of Directors

We do not have a policy regarding the consideration of any director candidates which may be recommended by our stockholders, including the minimum qualifications for director candidates, nor has our Board established a process for identifying and evaluating director nominees. We have not adopted a policy regarding the handling of any potential recommendation of director candidates by our stockholders, including the procedures to be followed. Our Board has not considered or adopted any of these policies as we have never received a recommendation from any stockholder for any candidate to serve on our Board. Given our relative size, we do not anticipate that any of our stockholders will make such a recommendation in the near future. While there have been no nominations of additional directors proposed, in the event such a proposal is made, all members of our Board will participate in the consideration of director nominees.

Item 11. | EXECUTIVE COMPENSATION |

Summary Compensation Table

The following table sets forth information relating to all compensation awarded to, earned by or paid by us during each of the two fiscal years ended December 31, 2008 and 2007 respectively, to: (a) our chief (principal) executive officer; (b) each of our executive officers who was awarded, earned or we paid more than $100,000; and (c) up to two additional individuals for whom disclosure would have been made in this table but for the fact that the individual was not serving as an executive officer of our company at December 31, 2008. The value attributable to any option awards is computed in accordance with FAS 123R.

SUMMARY COMPENSATION TABLE

NAME AND

PRINCIPAL

POSITION

(A) | YEAR

(B) | SALARY

($)

(C) | BONUS

($)

(D) | STOCK AWARDS

($)

(E) | OPTION AWARDS

($)

(F) | NON-EQUITY

INCENTIVE PLAN COMPENSATION

($)

(G) | NONQUALIFIED DEFERRED COMPENSATION EARNINGS

($)

(H) | ALL OTHER COMPENSATION

($)

(I) | TOTAL

($)

(J) |

| | | | | | | | | |

James Longshore

CEO, CFO (1) | 2008 2007 | 0 0 | 0 0 | 0 0 | 13,948 14,040 | 0 0 | 0 0 | 0 0 | 13,948 14,040 |

| | | | | | | | | |

William Edward

McKechnie,

CEO, CFO and

Chairman (2) | 2008 2007 | 22,000 (3) | 0 0 | 0 0 | 0 0 | 0 0 | 0 0 | 0 0 | 0 22,000 |

(1) | Mr. Longshore was appointed as our CEO and CFO on March 3, 2007. |

(2) | Mr. McKechnie served as our CEO, CFO and Chairman from August 26, 2005 to March 2007. Our company had entered into a management consulting agreement with Goldeye Consultants Ltd., a corporation of which Mr. McKechnie is a director and from which Mr. McKechnie received this compensation. Mr. McKechnie has executed a non-disclosure and non-competition agreement. |

(3) | All of the 716,000 nonqualified stock options previously granted to Mr. McKechnie on June 21, 2005, April 21, 2006 and August 1, 2006 were cancelled in March 2007. |

- 54 -

As of the date of this Report, Mr. Longshore does not receive any monetary compensation in his capacity as our Chief Executive Officer and we are not a party to any management consulting agreement with Mr. Longshore. The terms of any future compensation to be paid to Mr. Longshore will be determined by our Board of which he is a member. At such time, the Board will consider a number of factors in determining Mr. Longshore’s compensation including the scope of his duties and responsibilities to our company and the time he devotes to our business. At the Board’s discretion, it will be determined whether to consult with any experts or other third parties in fixing the amount of Mr. Longshore’s compensation. During fiscal 2008, Mr. Longshore did not receive any compensation package. He was reimbursed for out-of-pocket expenses incurred on behalf of our company in connection with carrying out his duties and responsibilities.

Management Consulting Agreements

As of the date of this Report, we have entered into the following management consulting agreement with an officer of our company.

Management Consulting Agreement with Vice-President, Exploration

We entered into a management consulting agreement with our Vice-President, Exploration (VPE”), Yves Clement, on May 1, 2006 for a term of 36 months which will expire on May 1, 2009. We plan to negotiate terms for renewal of this agreement with our VPE prior to the expiration of the term. Our VPE is paid approximately $4,720 (Cdn$5,000) per month and is reimbursed for expenses incurred by him on behalf of our company. Our VPE shall be paid compensation equivalent to 18 months’ fees, based on the rate of compensation being paid at the relevant time in the event of (i) termination without cause; or (ii) a Change of Control. Our VPE shall provide certain services to our company including, but not limited to, making project or property site attendances as may be required from time to time, preparing progress reports with respect to our mineral exploration projects, conducting due diligence as may be required from time to time in connection with potential mineral properties; reviewing geological data and liaising with principal owners of mineral properties in which our company may wish to acquire an interest, meeting with government authorities and retaining technical experts, making recommendations to the Board and its relevant committees with respect to the acquisition and/or abandonment of mineral exploration properties and preparing and implementing, subject to Board approval, plans for the operation of our company including plans for exploration programs, costs of operations and other expenditures in connection with our mineral projects.

Compensation of Management

The terms of the foregoing management consulting agreement was determined at the time by our then constituted Board. Our Board has complete authority in determining the amount of compensation to be paid and the other terms of management compensation. At the time of entering into the foregoing agreement, our Board did not consult with any consultants or other third parties in determining the amount of compensation to be paid under the management consulting agreement.

Termination Agreements

On July 1, 2007, we entered into a new management consulting agreement with our former VP, Finance, Peter Minuk, for a term of one year expiring on July 1, 2008 which was subsequently extended on mutual agreement to January 1, 2009. On mutual agreement, both parties agreed to terminate this agreement. Mr. Minuk resigned as an officer of the company in January 2009. As of the date of this Report, Mr. Minuk continues to provide limited services to our company on an “as needed” basis, and is paid approximately $472 per month (Cdn$500) for such services.

On November 1, 2007, we renewed a management consulting agreement with our VP, Ghana Operations, Alhaji Abudulai for a further one year term expiring on November 1, 2008. On mutual agreement, both parties agreed to terminate this agreement. As of the date of this Report, Mr. Abudulai will provide certain services to our company on an “as needed”, non-compensatory basis including, but not necessarily limited to, improving community and government relations in Ghana.

On December 1, 2007, we entered into a new management consulting agreement with our Secretary and Treasurer (the “ST”), Kiomi Mori, for a term of one year. On mutual agreement, both parties agreed to terminate this agreement in September 2008. As of the date of this Report, our ST continues to provide certain consulting services to our company on an “as needed” basis including, but not necessarily limited to, preparing corporate documents and regulatory filings, and is paid approximately $47 per hour (Cdn$50) for such services.

- 55 -

Outstanding Equity Awards at Fiscal Year End

The following table sets forth information concerning our grant of options to purchase shares of our common stock during the fiscal year ended December 31, 2008 to each person named in the Summary Compensation table.

NAME

(A) | NUMBER OF SECURITIES UNDERLYING UNEXERCISED OPTIONS

(#)

EXERCISABLE

(B) | NUMBER OF SECURITIES UNDERLYING UNEXERCISED OPTIONS

(#)

UNEXERCISABLE

(C) | EQUITY INCENTIVE PLAN AWARDS NUMBER OF SECURITIES UNDERLYING UNEXERCISED UNEARNED OPTIONS

(#)

(D) | OPTION EXERCISE PRICE

($)

(E) | OPTION EXPIRATION DATE

(F) | NUMBER OF SHARES OR UNITS OF STOCK THAT

HAVE

NOT

VESTED

(#)

(G) | MARKET VALUE OF SHARES OR UNITS OF STOCK THAT

HAVE

NOT

VESTED

($)

(H) | EQUITY INCENTIVE PLANA AWARDS NUMBER OF UNEARNED SHARES, UNITS OR OTHER RIGHTS THAT

HAVE

NOT

VESTED

(#)

(I) | EQUITY INCENTIVE PLAN AWARDS MARKET OR PAYOUT VALUE OF UNEARNED SHARES, UNITS OR OTHER RIGHTS THAT

HAVE

NOT

VESTED

(#)

(J) |

| | | | | | | | | |

James Longshore | 0 | 0 | 0 | N/A | N/A | 0 | 0 | 0 | 0 |

2005 Equity Incentive Compensation Plan

On June 21, 2005, our Board authorized, approved and adopted, our 2005 Equity Incentive Compensation Plan. As the Plan was not submitted to our shareholders for approval and was not approved by our shareholders, we are not permitted to issue any options qualifying as incentive stock options under Section 422 of the Internal Revenue Code of 1986, as amended. A total of 3,000,000 shares of our common stock have been reserved for issuance under the Plan. As at the date of this Report, we have granted options to purchase an aggregate of 1,080,000 shares of our common stock. During 2008, 300,000 options were cancelled pursuant to Board approval and 100,000 options were exercised by a former consultant of the company.

The purpose of the Plan is to encourage stock ownership by our officers, directors, key employees and consultants, and to give such persons a greater personal interest in the success of our business and an added incentive to continue to advance and contribute to us. Our Board, or a committee of the Board, will administer the Plan including, without limitation, the selection of the persons who will be awarded stock grants and granted options, the type of options to be granted, the number of shares subject to each option and the exercise price.

Plan options may only be non-qualified options. In addition, the Plan allows for the inclusion of a reload option provision, which permits an eligible person to pay the exercise price of the option with shares of common stock owned by the eligible person and receive a new option to purchase shares of common stock equal in number to the tendered shares. Furthermore, compensatory stock amounts may also be issued. The term of each plan option and the manner in which it may be exercised is determined by our Board or a committee of the Board. All awards granted under the Plan are made on a case by case basis, and the Board does not have any policy regarding timing of grants, amount of shares subject to any option to be granted or the exercise price, except that the Board does consider and/or approve option grants to incoming officers and directors at the time of their appointment.

Eligibility

Our officers, directors, key employees and consultants are eligible to receive stock grants and non-qualified options under the Plan.

- 56 -

Administration

The Plan will be administered by our Board or an underlying committee. The Board or an underlying committee determines from time to time those of our officers, directors, key employees and consultants to whom stock grants or plan options are to be granted, the terms and provisions of the respective option agreements, the time or times at which such options shall be granted, the dates such Plan options become exercisable, the number of shares subject to each option, the purchase price of such shares and the form of payment of such purchase price. All other questions relating to the administration of the Plan, and the interpretation of the provisions thereof and of the related option agreements, are resolved by our Board or an underlying committee. As of the date of this Report, the entire Board administers the Plan.

Shares Subject to Awards

We have currently reserved 3,000,000 of our authorized but unissued shares of common stock for issuance under the Plan, and a maximum of 3,000,000 shares may be issued, unless the Plan is subsequently amended, subject to adjustment in the event of certain changes in our capitalization, without further action by our Board and stockholders, as required. Subject to the limitation on the aggregate number of shares issuable under the Plan, there is no maximum or minimum number of shares as to which a stock grant or Plan option may be granted to any person. Shares used for stock grants and Plan options may be authorized and unissued shares or shares reacquired by us. Shares covered by Plan options which terminate unexercised or shares subject to stock awards which are forfeited or cancelled will again become available for grant as additional options or stock awards, without decreasing the maximum number of shares issuable under the Plan.

The Plan provides that, if our outstanding shares are increased, decreased, exchanged or otherwise adjusted due to a share dividend, forward or reverse share split, recapitalization, reorganization, merger, consolidation, combination or exchange of shares, an appropriate and proportionate adjustment shall be made in the number or kind of shares subject to unexercised options and in the purchase price per share under such options. Any adjustment, however, does not change the total purchase price payable for the shares subject to outstanding options. In the event of our proposed dissolution or liquidation, a proposed sale of all or substantially all of our assets, a merger or tender offer for our shares of common stock, the option may be assumed, converted or replaced by the successor corporation (if any) or may substitute equivalent awards or provide substantially similar consideration to awardees. In the event such successor corporation (if any) refuses or otherwise declines to assume or substitute awards, as provided above, (i) the vesting of any or all Awards granted pursuant to this Plan will accelerate immediately prior to the effective date of a transaction described above and (ii) any or all Options granted pursuant to the Plan will become exercisable in full prior to the consummation of such event at such time and on such conditions as our Board or an underlying committee determines. If such Options are not exercised prior to the consummation of the corporate transaction, they shall terminate at such time as determined by our Board or an underlying committee.

Terms of Exercise

The Plan provides that the options granted thereunder shall be exercisable from time to time in whole or in part, unless otherwise specified by our Board or an underlying committee.

Exercise Price

The purchase price for shares subject to options is determined by our Board or an underlying committee and may be below fair market value on the day of grant. If the purchase price is paid with consideration other than cash, our Board or an underlying committee shall determine the fair value of such consideration to us in monetary terms.

The per share purchase price of shares issuable upon exercise of a plan option may be adjusted in the event of certain changes in our capitalization, but no such adjustment shall change the total purchase price payable upon the exercise in full of options granted under the Plan.

Manner of Exercise

Plan options are exercisable by delivery of written notice to us stating the number of shares with respect to which the option is being exercised, together with full payment of the purchase price therefor. Payment shall be in cash, checks, certified or bank cashier’s checks, promissory notes secured by the shares issued through exercise of the related options, shares of common stock or in such other form or combination of forms which shall be acceptable to our Board or an underlying committee.

- 57 -

Option Period

The term of each non-qualified stock option is determined and fixed by our Board or an underlying committee.

Termination

Except as otherwise expressly provided in the option agreement, all Plan options are nonassignable and nontransferable, except by will or by the laws of descent and distribution, and during the lifetime of the optionee, may be exercised only by such optionee. If an optionee shall die while our employee or within three months after termination of employment by us because of disability, or retirement or otherwise, such options may be exercised, to the extent that the optionee shall have been entitled to do so on the date of death or termination of employment, by the person or persons to whom the optionee’s right under the option pass by will or applicable law, or if no such person has such right, by his executors or administrators.

In the event of termination of employment because of death while an employee or because of disability, an optionee’s options may be exercised not later than the expiration date specified in the option or one year after the optionee’s death, whichever date is earlier, or in the event of termination of employment because of retirement or otherwise, not later than the expiration date specified in the option or three months after the optionee’s retirement, whichever date is earlier.

If an optionee’s employment by us terminates because of disability and such optionee has not died within the following three months, the options may be exercised, to the extent that the optionee shall have been entitled to do so at the date of the termination of employment, at any time, or from time to time, but not later than the expiration date specified in the option or one year after termination of employment, whichever date is earlier.

If an optionee’s employment shall terminate for any reason other than death or disability, such optionee may exercise the options to the same extent that the options were exercisable on the date of termination, for up to three months following such termination, or on or before the expiration date of the options, whichever occurs first. In the event that the optionee was not entitled to exercise the options at the date of termination or if the optionee does not exercise such options (which were then exercisable) within the time specified herein, the options shall terminate.

If an optionee’s employment with us is terminated for any reason whatsoever, and within three months after the date thereof the optionee either (i) accepts employment with any competitor of, or otherwise engages in competition with us, or (ii) discloses to anyone outside our company or uses any confidential information or material of our company in violation of our policies or any agreement between the optionee and our company, the committee, in its sole discretion, may terminate any outstanding stock option and may require the optionee to return to us the economic value of any award that was realized or obtained by the optionee at any time during the period beginning on that date that is six months prior to the date the optionee’s employment with us is terminated.

Our Board or an underlying committee may, if an optionee’s employment with us is terminated for cause, annul any award granted under the Plan to such employee and, in such event, our Board or an underlying committee, in its sole discretion, may require the optionee to return to us the economic value of any award that was realized or obtained by an optionee at any time during the period beginning on that date that is six months prior to the date the optionee’s employment with us is terminated.

Modification and Termination of Plan

Our Board or an underlying committee may amend, suspend or terminate the Plan at any time. However, no such action may prejudice the rights of any holder of a stock grant or an optionee who has prior thereto been granted options under the Plan. Any such termination of the Plan shall not affect the validity of any stock grants or options previously granted thereunder. Unless terminated by our Board, the Plan shall continue to remain effective until such time as no further awards may be granted and all awards granted under the Plan are no longer outstanding.

- 58 -

Compensation of Directors

We established compensation arrangements for our directors for each individual’s service and expense on our Board in March 2007. Directors’ fees are paid on a quarterly basis. As of December 31, 2008, we did not pay fees to directors for their attendance at Board meetings. As an austerity measure, the Board agreed to reduce their respective directors’ fees by 50% in and from the fourth quarter ended December 31, 2008.

The following table sets forth information relating to the compensation paid to our directors for the fiscal year ended December 31, 2008:

DIRECTOR COMPENSATION

NAME

(A) | FEES

EARNED

OR PAID

IN CASH

($)

(B) | STOCK

AWARDS

($)

(C) | OPTION

AWARDS

($)

(D) | NON-EQUITY

INCENTIVE PLAN

COMPENSATION

($)

(E) | NON-QUALIFIED DEFERRED COMPENSATION EARNNGS

($)

(F) | ALL OTHER

COMPENSATION

($)

(G) | TOTAL

($)

(H) |

| | | | | | | |

James Longshore | 7,239 | 0 | 0 | 0 | 0 | 0 | 7,239 |

| | | | | | | |

Richard Grayston | 7,239 | 0 | 0 | 0 | 0 | 0 | 7,239 |

| | | | | | | |

Peter Minuk | 5,428 | 0 | 0 | 0 | 0 | 0 | 5,428 |

| | | | | | | |

Robert Montgomery | 5,428 | 0 | 0 | 0 | 0 | 0 | 5,428 |

| | | | | | | |

Rebecca Kiomi Mori (1) | 3,305 | 0 | 0 | 0 | 0 | 0 | 3,305 |

(1) | Ms. Mori resigned as a director in July 2008. |

Item 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

At March 27, 2009, we had 31,330,602 shares of common stock issued and outstanding. The following table sets forth information known to us as of March 27, 2009 relating to the beneficial ownership of shares of our common stock by:

| ● | each person who is known by us to be the beneficial owner of more than 5% of our outstanding common stock; |

| ● | each named executive officer; and |

| ● | all named executive officers and directors as a group. |

- 59 -

Unless otherwise indicated, the business address of each person listed is in care of Suite 301, 360 Bay Street, Toronto, Ontario, Canada, M5H 2V6, except for our President whose address is Lot 3, Rose Island Estates, Nassau, Bahamas. The percentages in the table have been calculated on the basis of treating as outstanding for a particular person, all shares of our common stock outstanding on that date and all shares of our common stock issuable to that holder in the event of exercise of outstanding options, warrants, rights or conversion privileges owned by that person at that date which are exercisable within 60 days of that date. Except as otherwise indicated, the persons listed below have sole voting and investment power with respect to all shares of our common stock owned by them, except to the extent that power may be shared with a spouse.

NAME OF BENEFICIAL OWNER | AMOUNT AND NATURE

OF BENEFICIAL OWNERSHIP | PERCENTAGE

OF CLASS |

James Longshore | 2,117,000 shares (1) | 6.77% |

Rebecca Kiomi Mori | 108,000 shares (2) | .34% |

Yves Pierre Clement | 324,000 shares (3) | 1.03% |

Alhaji Nantogma Abudulai | 208,000 shares (4) | .66% |

Richard W. Grayston | 142,000 shares (5) | .45% |

Peter Minuk | 80,000 shares (6) | .26% |

Robert H. Montgomery | 78,000 shares (7) | .25% |

Officers and Directors as a Group (7 persons) | 3,057,000 shares (1) to (7) | 9.76% |

5% Stockholders | | |

Brokton International Ltd. | 2,117,000 shares (1) | 6.77% |

Mark T. McGinnis | 2,084,855 shares (8) | 6.53% |

(1) | Consists of (a) 2,000,000 shares which are owned by Brokton International Ltd.; (b) Consists of 108,000,000 shares which are issuable upon the exercise of options that have vested and are currently exercisable; and (c) 9,000 shares which shall become issuable upon options that shall vest and be exercisable within 60 days following the date of this Report; namely April 12 and May 12, 2009. Does not include 45,000 shares issuable upon the exercise of options that have not yet vested and will vest monthly as to 4,500 in each month. Brokton International Ltd. (“Brokton”) is a British West Indies corporation, whose sole beneficial owner is James Longshore. Mr. Longshore exercises sole investment, voting and disposition powers over the shares included in the table. |

(2) | Consists of 105,000 shares which are issuable upon the exercise of options that have vested and are currently exercisable; and (c) 3,000 shares which shall become issuable upon options that shall vest and be exercisable within 30 days following the date of this Report; namely April 21, 2009 at which time all of the options will have vested. |

(3) | Consists of (a) 306,000 shares which are issuable upon the exercise of options that have vested and are currently exercisable; and (b) 18,000 shares which shall become issuable upon options that shall vest and be exercisable within 60 days following the date of this Report; namely April 1 and May 1, 2009. Does not include 90,000 shares issuable upon the exercise of options that have not yet vested and will vest monthly as to 9,000 in each month. |

(4) | Consists of (a) 100,000 shares of common stock; (b) 102,000 shares which are issuable upon the exercise of options that have vested and are currently exercisable; and (c) 6,000 shares which shall become issuable upon options that shall vest and be exercisable within 60 days following the date of this Report; namely April 1 and May 1, 2009 at which time all of the options will have vested. |

(5) | Consists of (a) 25,000 shares of common stock; (b) 108,000 shares which are issuable upon the exercise of options that have vested and are currently exercisable; and (c) 9,000 shares which shall become issuable upon options that shall vest and be exercisable within 60 days following the date of this Report; namely April 5 and May 5, 2009. Does not include 45,000 shares issuable upon the exercise of options that have not yet vested and will vest monthly as to 4,500 in each month. |

(6) | Consists of (a) 2,000 shares of common stock; (b) 72,000 shares which are issuable upon the exercise of options that have vested and are currently exercisable; and (c) 6,000 shares which shall become issuable upon options that shall vest and be exercisable within 60 days following the date of this Report; namely April 5 and May 5, 2009. Does not include 30,000 shares issuable upon the exercise of options that have not yet vested and will vest monthly as to 3,000 in each month. |

- 60 -

(7) | Consists of (a) 72,000 shares which are issuable upon the exercise of options that have vested and are currently exercisable; and (b) 6,000 shares which shall become issuable upon options that shall vest and be exercisable within 60 days following the date of this Report; namely April 12 and May 12, 2009. Does not include 30,000 shares issuable upon the exercise of options that have not yet vested and will vest monthly as to 3,000 in each month. |

(8) | Consists of (a) 2,024,826 shares of common stock held by Mark McGinnis of which an aggregate of 70,000 shares of common stock is held by Mr. McGinnis in trust for his children; and (b) 60,029 shares of common stock held by his spouse. |

Item 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

Consulting Agreement with Principal Shareholder

From February 1, 2004 through February 1, 2006, we were a party to a consulting agreement with Brokton, a company which, as of the date of this Report, owns 6.77% of our common stock and one of only two shareholders that owns more than 5% of our issued and outstanding shares of common stock. Under the terms of this agreement, we engaged Brokton as a consultant to advise our Management with respect to hiring additional qualified management, providing support with respect to operational matters and government compliance in Ghana, mergers and acquisitions and financial advisory. James Longshore, our President and one of the directors of our company, is the President of Brokton and exercises sole investment, voting and disposition powers over the shares of Brokton. Mr. Longshore is also a director of our wholly-owned subsidiaries, XGEL and XOG Ghana (since April 2006) and Chief Operating Officer (since February 2007) and a director of XG Mining (since June 2006) and Chief Operating Officer (since February 2007) and a director and officer of Xtra Energy (since March 2007). From February 2004 to February 2006, we paid Brokton an aggregate of $53,176 for its consulting services and reimbursed Brokton for expenses incurred by Brokton on behalf of our company.

A Principal Shareholder Manages our Investment Portfolio

We currently, and since approximately five years ago, maintain our brokerage account with Haywood Securities Inc. (“Haywood”) in connection with our investment accounts. Haywood provides us with investment recommendations and custodial services. Haywood is a member of the Toronto Stock Exchange, the TSXV, the Montreal Exchange, the Canadian Trading and Quotation System, the Canadian Investor Protection Fund, and the Investment Dealers Association of Canada. In addition, Haywood Securities (USA) Inc., a wholly owned subsidiary is a broker-dealer registered to transact securities business in the United States and a member of the National Association of Securities Dealers. We pay Haywood ordinary brokerage commissions on trade transactions and our accounts with Haywood can be terminated at any time. Mark McGinnis, a shareholder who, as at the date of this Report, owns 6.53% of our common stock and one of only two shareholders that owns more than 5% of our issued and outstanding shares of common stock, is an investment advisor with Haywood and is the manager of our accounts with Haywood.

Director Independence

Two of the members of our Board (Robert H. Montgomery and Richard W, Grayston) are “independent” within the meaning of Marketplace Rule 4200 of the National Association of Securities Dealers, Inc.

Item 14. | PRINCIPAL ACCOUNTING FEES AND SERVICES |

Davidson & Company LLP is our principal accountant for our audit of annual financial statements and review of the financial statements included in this Report and served as our independent registered public accounting firm for 2008 and 2007. The following table shows the fees that were billed for the audit and other services provided by such firm for 2008 and 2007.

| | 2008 | | 2007 | |

Audit Fees | | $ | 55,000 | | $ | 69,800 | |

Audit-Related Fees | | | 18,000 | | | 23,000 | |

Tax Fees | | | 0 | | | 0 | |

All Other Fees | | | 0 | | | 4,500 | |

Total | | $ | 73,000 | | $ | 97,300 | |

- 61 -

Audit Fees

This category includes the audit of our annual financial statements, review of financial statements included in this Report and services that are normally provided by the independent auditors in connection with their engagements for those fiscal years. This category also includes advice on audit and accounting matters that arose during, or as a result of, the audit or the review of our interim financial statements.

Audit-Related Fees

This category consists of assurance and related services by the independent auditors that are reasonably related to the performance of the audit or review of our financial statements and are not reported above under “Audit Fees.” The services for the fees disclosed under this category include consultation regarding our correspondence with the SEC and other accounting consulting.

Tax Fees

This category consists of professional services rendered by our independent auditors for tax compliance and tax advice. The services for the fees disclosed under this category include tax return preparation and technical tax advice.

All Other Fees

This category consists of fees for other miscellaneous items.

Our Board has adopted a procedure for pre-approval of all fees charged by our independent auditors. Under the procedure, the Board approves the engagement letter with respect to audit, tax and review services. Other fees are subject to pre-approval by the Board, or, in the period between meetings, by a designated member of our Board. Any such approval by the designated member is disclosed to the entire Board at the next meeting. The audit and tax fees paid to the auditors with respect to 2008 were pre-approved by the entire Board.

PART IV

Item 15. | EXHIBITS, FINANCIAL STATEMENT SCHEDULES |

Exhibit No. | Description of Document |

2.1 | Stock Exchange Agreement dated October 31, 2003, by and between Xtra-Gold Resources Corp. and the former shareholders of Xtra Energy Corp. (formerly Xtra-Gold Resources, Inc.) (1) |

3.1 | Articles of Incorporation of Silverwing Systems Corporation filed on September 1, 1998 (1) |

3.2 | Articles of Amendment filed on August 19, 1999 to change our name to Advertain On-Line Inc. (1) |

3.3 | Articles of Amendment filed June 18, 2001 to change our name to RetinaPharma International, Inc. (1) |