UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21609

Salomon Brothers Variable Rate Strategic Fund Inc.

(Exact name of registrant as specified in charter)

125 Broad Street, New York, NY 10004

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

300 First Stamford Place,4th Fl.

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 725-6666

Date of fiscal year end: September 30

Date of reporting period: March 31, 2006

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Semi-Annual Report to Stockholders is filed herewith.

SEMI-ANNUAL

REPORT

MARCH 31, 2006

Salomon Brothers

Variable Rate Strategic Fund Inc.

INVESTMENT PRODUCTS: NOT FDIC INSURED Ÿ NO BANK GUARANTEE Ÿ MAY LOSE VALUE

Salomon Brothers Variable Rate Strategic Fund Inc.

Semi-Annual Report • March 31, 2006

What’s

Inside

Fund Objective

The Fund’s investment objective is to maintain a high level of current income.

“Smith Barney” and “Salomon Brothers” are service marks of Citigroup, licensed for use by Legg Mason as the names of funds and investment managers. Legg Mason and its affiliates, as well as the Fund’s investment manager, are not affiliated with Citigroup.

Letter from the Chairman

R. JAY GERKEN, CFA

Chairman, President and Chief Executive Officer

Dear Shareholder,

The U.S. economy was mixed during the six-month period of this report. After a 4.1% advance in the third quarter of 2005, fourth quarter gross domestic product (“GDP”)i growth slipped to 1.7%. This marked the first quarter in which GDP growth did not surpass 3.0% since the first three months of 2003. However, as expected, the economy rebounded sharply in the first quarter of 2006, with a preliminary estimate of 4.8% GDP growth. The economic turnaround was prompted by both strong consumer and business spending. In addition, the U.S. Labor Department reported that unemployment hit a five-year low in March.

As expected, the Federal Reserve Board (“Fed”)ii continued to raise interest rates during the reporting period. Despite the changing of the guard from Fed Chairman Alan Greenspan to Ben Bernanke in early 2006, it was business as usual for the Fed, as it raised short-term interest rates four times during this reporting period. Since it began its tightening campaign in June 2004, the Fed has raised rates 15 consecutive times, bringing the federal funds rateiii from 1.00% to 4.75% — its highest level since April 2001. After the end of the Fund’s reporting period, at its May meeting, the Fed once again raised the federal funds rates by an additional 0.25% to 5.00%.

As expected, both short- and long-term yields rose over the reporting period. During the six months ended March 31, 2006, two-year Treasury yields increased from 4.21% to 4.82%. Over the same period, 10-year Treasury yields moved from 4.39% to 4.86%. During much of this reporting period the yield curve was inverted, with the yield on two-year Treasuries surpassing that of 10-year Treasuries. This anomaly has historically foreshadowed an economic slowdown or recession. However, some experts, including new Chairman Bernanke, believe the inverted yield curve is largely a function of strong foreign demand for longer-term bonds. Looking at the six-month period as a whole, the

Salomon Brothers Variable Rate Strategic Fund Inc. I

overall bond market, as measured by the Lehman Brothers U.S. Aggregate Index,iv returned –0.06%.

The high yield market generated a positive return during the period of this report. The high yield market was supported by generally strong corporate profits and low default rates. In addition, there was overall solid demand and limited supply as new issuance waned. These factors tended to overshadow several company specific issues, mostly surrounding the automobile industry. For example, automobile parts supplier Dana Corp. recently filed for bankruptcy and there are ongoing concerns about the future prospects for General Motors Corp. During the six-month period ended March 31, 2006, the Citigroup High Yield Market Indexv returned 3.22%.

Emerging markets debt continued to produce solid results over the period of this report, as the JPMorgan Emerging Markets Bond Index Global (“EMBI Global”)vi returned 3.39% during the six-month reporting period. A strengthening global economy, solid domestic spending and high energy and commodity prices continue to support many emerging market countries. In addition, a number of these countries have strengthened their balance sheets in recent years. We believe that these positives more than offset the potential negatives associated with rising U.S. interest rates.

Performance Review

For the six months ended March 31, 2006, the Salomon Brothers Variable Rate Strategic Fund Inc. returned 3.73%, based on its net asset value (“NAV”)vii and 4.08% based on its New York Stock Exchange (“NYSE”) market price per share. In comparison, the Fund’s unmanaged benchmark, Lehman Brothers U.S. Aggregate Index, returned –0.06% for the same time frame. The Lipper Global Income Closed-End Funds Category Averageviii increased 2.16% over the same period. Please note that Lipper performance returns are based on each fund’s NAV per share.

During this six-month period, the Fund made distributions to shareholders totaling $0.6419 per share, (which may have included a return of capital). The performance table on the next page shows the Fund’s six-month total return based on its NAV and market price as of March 31, 2006. Past performance is no guarantee of future results.

II Salomon Brothers Variable Rate Strategic Fund Inc.

Performance Snapshot as of March 31, 2006 (unaudited)

| | | | |

| | |

Price

Per Share | | | | Six-Month

Total Return |

$19.54 (NAV) | | | | 3.73% |

|

$17.20 (Market Price) | | | | 4.08% |

|

| | | | |

| All figures represent past performance and are not a guarantee of future results. |

| Total returns are based on changes in NAV or market price, respectively. Total returns assume the reinvestment of all distributions, including returns of capital, if any, in additional shares. |

Special Shareholder Notice

On December 1, 2005, Citigroup Inc. (“Citigroup”) completed the sale of substantially all of its asset management business to Legg Mason, Inc. (“Legg Mason”). As a result, the Fund’s investment adviser (the “Manager”), previously an indirect wholly-owned subsidiary of Citigroup, has become a wholly-owned subsidiary of Legg Mason. Completion of the sale caused the Fund’s then existing investment management contract to terminate. The Fund’s shareholders approved a new investment management contract between the Fund and the Manager, which became effective on December 16, 2005.

As previously described in proxy statements that were mailed to shareholders of the Fund in connection with the transaction, Legg Mason intends to combine the fixed-income operations of the Manager with those of Legg Mason’s wholly-owned subsidiary, Western Asset Management Company, and its affiliates (“Western Asset”). This combination will involve Western Asset and the Manager sharing common systems and procedures, employees (including portfolio managers), investment trading platforms, and other resources. At a future date Legg Mason expects to recommend to the Board of Directors of the Fund that Western Asset be appointed as the advisor or sub-advisor to the Fund, subject to applicable regulatory requirements.

The portfolio management team of S. Kenneth Leech, Stephen A. Walsh, Keith J. Gardner and Michael C. Buchanan assumed portfolio management responsibilities for the Fund on March 31, 2006. These portfolio managers are employees of the Manager for purposes of carrying out their duties relating to the Fund and they also will continue to serve

Salomon Brothers Variable Rate Strategic Fund Inc. III

as employees of Western Asset. Messers. Leech, Walsh, and Gardner have each been employed by Western Asset for more than five years.

Prior to joining Western Asset as a portfolio manager and head of the U.S. High Yield team in 2005, Mr. Buchanan was a Managing Director and head of U.S. Credit Products at Credit Suisse Asset Management from 2003 to 2005. Mr. Buchanan served as Executive Vice President and portfolio manager for Janus Capital Management in 2003. Prior to joining Janus Capital Management, Mr. Buchanan was a Managing Director and head of High Yield Trading at Blackrock Financial Management from 1998 to 2003.

The Board is working with the Manager, Western Asset, and the portfolio managers to implement an orderly combination of the Manager’s fixed-income operations and Western Asset in the best interests of the Fund and its shareholders.

Information About Your Fund

As you may be aware, several issues in the mutual fund industry have recently come under the scrutiny of federal and state regulators. The Fund’s Manager and some of its affiliates have received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, the open end Funds’ response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The Fund has been informed that the Manager and its affiliates are responding to those information requests, but are not in a position to predict the outcome of these requests and investigations.

Important information concerning the Fund and its Manager with regard to recent regulatory developments is contained in the Notes to Financial Statements included in this report.

Looking for Additional Information?

The Fund is traded under the symbol “GFY” and its closing market price is available in most newspapers under the NYSE listings. The daily NAV is available on-line under symbol XGFYX. Barron’s and The Wall Street Journal’s Monday editions carry closed-end fund tables that will provide additional

IV Salomon Brothers Variable Rate Strategic Fund Inc.

information. In addition, the Fund issues a quarterly press release that can be found on most major financial websites as well as www.leggmason.com/InvestorServices.

In a continuing effort to provide information concerning the Fund, shareholders may call 1-888-777-0102 or 1-800-SALOMON (toll free), Monday through Friday from 8:00 a.m. to 6:00 p.m. Eastern Time, for the Fund’s current NAV, market price and other information.

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you continue to meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

May 10, 2006

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

RISKS: The Fund is a non-diversified, closed-end management investment company designed primarily as a long-term investment and not as a trading vehicle. The Fund is not intended to be a complete investment program and, due to the uncertainty inherent in all investments, there can be no assurance that the Fund will achieve its investment objective. Your common shares at any point in time may be worth less than you invested, even after taking into account the reinvestment of Fund dividends and distributions. The Fund may invest in high-yield and foreign securities, including emerging markets, which involve risks beyond those inherently in solely higher-rated and domestic investments. High-yield bonds involve greater credit and liquidity risks than investment grade bonds. Investing in foreign securities is subject to certain risks typically not associated with domestic investing, such as currency fluctuations and changes in political conditions. These risks are magnified in emerging or developing markets. Derivatives, such as options or futures, can be illiquid and hard to value, especially in declining markets. A small investment in certain derivatives may have a potentially large impact on the Fund’s performance.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | | Gross domestic product is a market value of goods and services produced by labor and property in a given country. |

| ii | | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

| iv | | The Lehman Brothers U.S. Aggregate Index is a broad-based bond index comprised of Government, Corporate, Mortgage and Asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| v | | The Citigroup High Yield Market Index is a broad-based unmanaged index of high yield securities. |

| vi | | JPMorgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for U.S. dollar denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds, and local market instruments. Countries covered are Algeria, Argentina, Brazil, Bulgaria, Chile, China, Colombia, Cote d’Ivoire, Croatia, Ecuador, Greece, Hungary, Lebanon, Malaysia, Mexico, Morocco, Nigeria, Panama, Peru, the Philippines, Poland, Russia, South Africa, South Korea, Thailand, Turkey and Venezuela. |

| vii | | NAV is calculated by subtracting total liabilities from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the Fund has invested. However, the price at which an investor may buy or sell shares of the Fund is at the Fund’s market price as determined by supply of and demand for the Fund’s shares. |

| viii | | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 6-month period ended March 31, 2006, including the reinvestment of distributions, including returns of capital, if any, calculated among the 12 funds in the Fund’s Lipper category, and excluding sales charges. |

Salomon Brothers Variable Rate Strategic Fund Inc. V

Fund at a Glance (unaudited)

Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report 1

Schedule of Investments (March 31, 2006) (unaudited)

SALOMON BROTHERS VARIABLE RATE STRATEGIC FUND INC.

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

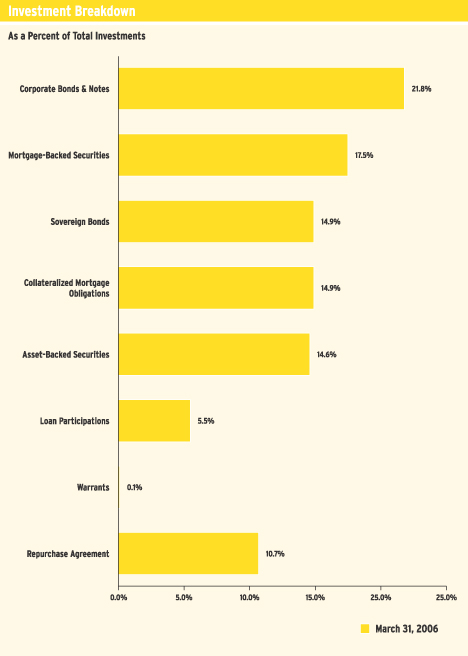

| | LOAN PARTICIPATIONS (a)(b) — 5.5% | | | | |

| | Auto Components — 0.5% | | | | |

| $ | 997,500 | | Delphi Corp., Term Loan, Tranche B, 13.000% due 6/14/11 (JPMorgan Chase & Co.) (c) | | $ | 1,036,777 | |

|

|

|

| | Electric Utilities — 0.1% | | | | |

| | 272,154 | | Reliant Energy Inc., Term Loans, Tranche B, 7.175% due 4/30/10 (Bank of America) | | | 272,154 | |

|

|

|

| | Energy Equipment & Services — 0.9% | | | | |

| | | | Key Energy Services Inc., Term Loans: | | | | |

| | 2,500 | | Delay Draw, 7.520% due 7/29/12 | | | 2,539 | |

| | | | Tranche B: | | | | |

| | 372,500 | | 7.520% due 7/29/12 (Lehman Brothers Inc.) | | | 378,320 | |

| | 625,000 | | 7.780% due 7/29/12 (Lehman Brothers Inc.) | | | 634,766 | |

| | | | Targa Resources Inc., Term Loans: | | | | |

| | 419,355 | | 7.230% due 10/28/12 (C.S. First Boston Corp.) | | | 425,907 | |

| | 129,032 | | 6.970% due 12/10/28 (C.S. First Boston Corp.) | | | 131,048 | |

| | 193,548 | | Tranche A, 4.402% due 10/28/12 (C.S. First Boston Corp.) | | | 196,573 | |

| | 6,048 | | Tranche B, 6.777% due 10/28/12 (C.S. First Boston Corp.) | | | 6,143 | |

| | 250,000 | | Tranche B 2, 6.918% due 12/10/28 (C.S. First Boston Corp.) | | | 253,906 | |

|

|

|

| | | | Total Energy | | | 2,029,202 | |

|

|

|

| | Health Care Providers and Services — 0.4% | | | | |

| | | | DaVita Inc., Term Loans: | | | | |

| | 39,216 | | 6.690% due 6/25/12 (JPMorgan Chase & Co.) | | | 39,775 | |

| | 61,569 | | Tranche B, 6.290% due 6/25/12 (JPMorgan Chase & Co.) | | | 62,447 | |

| | 5,882 | | Tranche B, 6.600% due 10/5/12 (JPMorgan Chase & Co.) | | | 5,966 | |

| | 156,863 | | Tranche B 1, 6.530% due 10/5/12 (JPMorgan Chase & Co.) | | | 159,102 | |

| | 156,863 | | Tranche B 2, 6.530% due 10/5/12 (JPMorgan Chase & Co.) | | | 159,101 | |

| | 96,078 | | Tranche B 3, 6.290% due 10/5/12 (JPMorgan Chase & Co.) | | | 97,450 | |

| | 47,059 | | Tranche B 4, 6.770% due 10/5/12 (JPMorgan Chase & Co.) | | | 47,731 | |

| | 39,216 | | Tranche B 5, 6.690% due 10/5/12 (JPMorgan Chase & Co.) | | | 39,775 | |

| | 39,216 | | Tranche B 6, 6.530% due 10/5/12 (JPMorgan Chase & Co.) | | | 39,775 | |

| | 47,059 | | Tranche B 7, 6.600% due 10/5/12 (JPMorgan Chase & Co.) | | | 47,731 | |

| | 29,412 | | Tranche B 8, 6.800% due 10/5/12 (JPMorgan Chase & Co.) | | | 29,832 | |

| | 39,216 | | Tranche B 9, 6.530% due 10/5/12 (JPMorgan Chase & Co.) | | | 39,775 | |

| | 85,833 | | Tranche B 10, 6.690% due 10/5/12 (JPMorgan Chase & Co.) | | | 87,058 | |

| | 58,824 | | Tranche B 11, 6.530% due 10/5/12 (JPMorgan Chase & Co.) | | | 59,663 | |

| | 39,216 | | Tranche B 12, 6.530% due 10/5/12 (JPMorgan Chase & Co.) | | | 39,775 | |

|

|

|

| | | | Total Health Care Providers and Services | | | 954,956 | |

|

|

|

| | Hotels, Restaurants & Leisure — 0.8% | | | | |

| | 750,000 | | BLB Worldwide Holdings Inc., Term Loan, 8.740% due 8/15/12 (Merrill Lynch) | | | 762,422 | |

| | | | Venetian Casino Resort LLC, Term Loans: | | | | |

| | 170,940 | | Tranche B, 6.730% due 6/15/11 (Bank of Nova Scotia) | | | 172,930 | |

See Notes to Financial Statements.

2 Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | Hotels, Restaurants & Leisure — 0.8% (continued) | | | | |

| $ | 829,060 | | Tranche L, 6.730% due 6/15/11 (Bank of Nova Scotia) | | $ | 838,711 | |

|

|

|

| | | | Total Hotels, Restaurants & Leisure | | | 1,774,063 | |

|

|

|

| | Media — 2.3% | | | | |

| | 983,740 | | Charter Communications Holdings LLC, Term Loan, Tranche B, 7.920% due 4/27/11 (C.S. First Boston Corp.) | | | 993,686 | |

| | 2,503 | | Charter Communications, Term Loan, Tranche B, 7.860% due 7/9/18 (C.S. First Boston Corp.) | | | 2,529 | |

| | | | Dex Media West Inc., Term Loans: | | | | |

| | 149,105 | | B 2, 6.110% due 2/15/10 (JPMorgan Chase & Co.) | | | 150,627 | |

| | 745,527 | | B 3, 6.250% due 2/15/10 (JPMorgan Chase & Co.) | | | 753,137 | |

| | 131,788 | | B 4, 6.180% due 2/15/10 (JPMorgan Chase & Co.) | | | 133,133 | |

| | 298,211 | | B 6, 6.250% due 2/15/10 (JPMorgan Chase & Co.) | | | 301,255 | |

| | 1,000,000 | | DIRECTV Holdings LLC, Term Loans, 6.276% due 4/20/06 (Bank of America) | | | 1,012,500 | |

| | 1,500,000 | | UPC Broadband Inc., Term Loan, Tranche H2, 7.280% due 3/15/12 (Bank of America) | | | 1,511,406 | |

|

|

|

| | | | Total Media | | | 4,858,273 | |

|

|

|

| | Machinery — 0.5% | | | | |

| | | | Mueller Group Inc., Term Loans: | | | | |

| | 238,095 | | 6.466% due 10/3/12 (Bank of America) | | | 241,560 | |

| | 503,810 | | 1 Month, 6.493% due 10/3/12 (Bank of America) | | | 511,142 | |

| | 238,095 | | 2 Month, 7.060% due 10/3/12 (Bank of America) | | | 241,560 | |

| | 17,500 | | 3 Month, 6.859% due 10/3/12 (Bank of America) | | | 17,755 | |

|

|

|

| | | | Total Metal Fabricate — Hardware | | | 1,012,017 | |

|

|

|

| | | | TOTAL LOAN PARTICIPATIONS

(Cost — $11,793,598) | | | 11,937,442 | |

|

|

|

| | CORPORATE BONDS & NOTES — 21.8% | | | | |

| | Aerospace & Defense — 0.5% | | | | |

| | 100,000 | | DRS Technologies Inc., Senior Subordinated Notes, 6.875% due 11/1/13 | | | 100,500 | |

| | 250,000 | | L-3 Communications Corp., Senior Subordinated Notes, 7.625% due 6/15/12 | | | 259,375 | |

| | 225,000 | | Moog Inc., Senior Subordinated Notes, 6.250% due 1/15/15 | | | 222,750 | |

| | 375,000 | | Sequa Corp., Senior Notes, Series B, 8.875% due 4/1/08 | | | 392,812 | |

|

|

|

| | | | Total Aerospace & Defense | | | 975,437 | |

|

|

|

| | Auto Components — 0.1% | | | | |

| | 100,000 | | Tenneco Automotive Inc., Senior Subordinated Notes, 8.625% due 11/15/14 | | | 100,500 | |

| | 125,000 | | TRW Automotive Inc., Senior Notes, 9.375% due 2/15/13 | | | 135,781 | |

|

|

|

| | | | Total Auto Components | | | 236,281 | |

|

|

|

| | Automobiles — 0.6% | | | | |

| | | | Ford Motor Co.: | | | | |

| | 50,000 | | Debentures, 6.625% due 10/1/28 | | | 33,750 | |

| | 850,000 | | Notes, 7.450% due 7/16/31 | | | 635,375 | |

| | 425,000 | | Senior Notes, 4.950% due 1/15/08 | | | 396,212 | |

| | | | General Motors Corp., Senior Debentures: | | | | |

| | 50,000 | | 8.250% due 7/15/23 | | | 36,250 | |

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report 3

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | Automobiles — 0.6% (continued) | | | | |

| $ | 410,000 | | 8.375% due 7/15/33 | | $ | 302,375 | |

|

|

|

| | | | Total Automobiles | | | 1,403,962 | |

|

|

|

| | Building Products — 0.4% | | | | |

| | | | Associated Materials Inc.: | | | | |

| | 200,000 | | Senior Discount Notes, step bond to yield 9.399% due 3/1/14 | | | 116,000 | |

| | 100,000 | | Senior Subordinated Notes, 9.750% due 4/15/12 | | | 104,250 | |

| | 500,000 | | Goodman Global Holding Co. Inc., Senior Subordinated Notes,

Series B, 7.491% due 6/15/12 (b) | | | 511,250 | |

| | 225,000 | | Nortek Inc., Senior Subordinated Notes, 8.500% due 9/1/14 | | | 230,062 | |

|

|

|

| | | | Total Building Products | | | 961,562 | |

|

|

|

| | Capital Markets — 0.1% | | | | |

| | 188,000 | | BCP Crystal U.S. Holdings Corp., Senior Subordinated Notes, 9.625% due 6/15/14 | | | 209,150 | |

|

|

|

| | Chemicals — 0.8% | | | | |

| | 200,000 | | Equistar Chemicals LP, Senior Notes, 10.625% due 5/1/11 | | | 217,500 | |

| | 200,000 | | Ethyl Corp., Senior Notes, 8.875% due 5/1/10 | | | 208,500 | |

| | | | Huntsman International LLC, Senior Subordinated Notes: | | | | |

| | 152,000 | | 10.125% due 7/1/09 | | | 156,560 | |

| | 75,000 | | 7.875% due 1/1/15 (d) | | | 76,125 | |

| | 100,000 | | Innophos Inc., Senior Subordinated Notes 8.875% due 8/15/14 | | | 104,500 | |

| | 375,000 | | Lyondell Chemical Co., Senior Secured Notes, 10.500% due 6/1/13 | | | 417,187 | |

| | 200,000 | | Nalco Co., Senior Subordinated Notes, 8.875% due 11/15/13 | | | 209,000 | |

| | 200,000 | | Resolution Performance Products LLC, Senior Subordinated Notes, 13.500% due 11/15/10 | | | 214,750 | |

| | 225,000 | | Rhodia SA, Senior Notes, 7.625% due 6/1/10 | | | 229,500 | |

|

|

|

| | | | Total Chemicals | | | 1,833,622 | |

|

|

|

| | Commercial Services & Supplies — 0.4% | | | | |

| | 100,000 | | Allied Security Escrow Corp., Senior Subordinated Notes, 11.375% due 7/15/11 | | | 95,500 | |

| | | | Allied Waste North America Inc., Senior Notes: | | | | |

| | 225,000 | | 7.875% due 4/15/13 | | | 235,969 | |

| | 175,000 | | 7.250% due 3/15/15 | | | 179,375 | |

| | 217,000 | | Series B, 9.250% due 9/1/12 | | | 235,174 | |

| | 125,000 | | Cenveo Corp., Senior Notes, 9.625% due 3/15/12 | | | 135,156 | |

|

|

|

| | | | Total Commercial Services & Supplies | | | 881,174 | |

|

|

|

| | Communications Equipment — 0.2% | | | | |

| | 475,000 | | Lucent Technologies Inc., Debentures, 6.450% due 3/15/29 | | | 431,063 | |

|

|

|

| | Computers & Peripherals — 0.1% | | | | |

| | 125,000 | | Seagate Technology HDD Holdings, Senior Notes, 8.000% due 5/15/09 | | | 130,469 | |

| | 50,000 | | SunGard Data Systems Inc., Senior Notes, 9.125% due 8/15/13 (d) | | | 53,125 | |

|

|

|

| | | | Total Computers & Peripherals | | | 183,594 | |

|

|

|

| | Construction Materials — 0.1% | | | | |

| | 125,000 | | Texas Industries Inc., Senior Notes, 7.250% due 7/15/13 | | | 129,375 | |

|

|

|

See Notes to Financial Statements.

4 Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | Containers & Packaging — 0.6% | | | | |

| $ | 150,000 | | Berry Plastics Corp., Senior Subordinated Notes, 10.750% due 7/15/12 | | $ | 165,750 | |

| | 225,000 | | Graphic Packaging International Corp., Senior Subordinated Notes, 9.500% due 8/15/13 | | | 211,500 | |

| | 225,000 | | JSG Funding PLC, Senior Notes, 9.625% due 10/1/12 | | | 239,062 | |

| | 375,000 | | Owens-Illinois Inc., Debentures, 7.500% due 5/15/10 | | | 381,562 | |

| | 35,000 | | Pliant Corp., Senior Secured Second Lien Notes, 11.125% due 9/1/09 (c) | | | 37,013 | |

| | 375,000 | | Smurfit-Stone Container Enterprises Inc., Senior Notes, 8.375% due 7/1/12 | | | 371,250 | |

|

|

|

| | | | Total Containers & Packaging | | | 1,406,137 | |

|

|

|

| | Diversified Financial Services — 4.8% | | | | |

| | 400,000 | | Alamosa Delaware Inc., Senior Notes, 11.000% due 7/31/10 | | | 447,000 | |

| | 125,000 | | Basell AF SCA, Senior Notes, 8.375% due 8/15/15 (d) | | | 124,687 | |

| | 100,000 | | CCM Merger Inc., Notes, 8.000% due 8/1/13 (d) | | | 100,000 | |

| | 250,000 | | Chukchansi Economic Development Authority, Senior Notes, 8.060% due 11/15/12 (b)(d) | | | 256,875 | |

| | | | Ford Motor Credit Co., Notes: | | | | |

| | 115,000 | | 6.625% due 6/16/08 | | | 108,900 | |

| | 3,000,000 | | 6.170% due 1/15/10 (b) | | | 2,717,100 | |

| | | | General Motors Acceptance Corp., Notes: | | | | |

| | 25,000 | | 7.250% due 3/2/11 | | | 23,715 | |

| | 500,000 | | 6.750% due 12/1/14 | | | 450,813 | |

| | 4,000,000 | | 7.020% due 12/1/14 (b) | | | 3,649,300 | |

| | 50,000 | | 8.000% due 11/1/31 | | | 47,379 | |

| | 81,000 | | Global Cash Access LLC/Global Cash Finance Corp., Senior Subordinated Notes, 8.750% due 3/15/12 | | | 87,379 | |

| | 200,000 | | Hexion US Finance Corp./Hexion Nova Scotia Finance ULC, Senior Secured Notes, 9.000% due 7/15/14 | | | 207,000 | |

| | 2,000,000 | | Residential Capital Corp., Notes 6.335% due 6/29/07 (b) | | | 2,015,596 | |

| | 325,000 | | Vanguard Health Holdings Co. I LLC, Senior Discount Notes, step bond to yield 9.915% due 10/1/15 | | | 238,875 | |

|

|

|

| | | | Total Diversified Financial Services | | | 10,474,619 | |

|

|

|

| | Diversified Telecommunication Services — 0.7% | | | | |

| | 175,000 | | AT&T Corp., Senior Notes, 9.750% due 11/15/31 | | | 209,588 | |

| | 275,000 | | IntelSat, Ltd., Senior Discount Notes, step bond to yield 9.462% due 2/1/15 (d) | | | 191,812 | |

| | 75,000 | | PanAmSat Corp., Senior Notes, 9.000% due 8/15/14 | | | 79,313 | |

| | 750,000 | | Qwest Corp., Notes, 8.160% due 6/15/13 (b) | | | 828,750 | |

| | 2,000,000MXN | | Telefonos de Mexico SA de CV, Senior Notes 8.750% due 1/31/16 | | | 177,523 | |

|

|

|

| | | | Total Diversified Telecommunication Services | | | 1,486,986 | |

|

|

|

| | Electric Utilities — 0.4% | | | | |

| | | | Edison Mission Energy, Senior Notes: | | | | |

| | 125,000 | | 7.730% due 6/15/09 | | | 128,750 | |

| | 250,000 | | 9.875% due 4/15/11 | | | 283,750 | |

| | | | Reliant Energy Inc., Senior Secured Notes: | | | | |

| | 250,000 | | 9.250% due 7/15/10 | | | 251,562 | |

| | 200,000 | | 9.500% due 7/15/13 | | | 201,250 | |

|

|

|

| | | | Total Electric Utilities | | | 865,312 | |

|

|

|

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report 5

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | Energy Equipment & Services — 0.3% | | | | |

| $ | 198,000 | | Dresser-Rand Group Inc., Senior Subordinated Notes, 7.625% due 11/1/14 (d) | | $ | 202,950 | |

| | 250,000 | | Hanover Compressor Co., Senior Notes, 9.000% due 6/1/14 | | | 270,000 | |

| | 200,000 | | Universal Compression Inc., Senior Notes, 7.250% due 5/15/10 | | | 204,000 | |

|

|

|

| | | | Total Energy Equipment & Services | | | 676,950 | |

|

|

|

| | Food & Staples Retailing — 0.2% | | | | |

| | 225,000 | | Jean Coutu Group (PJC) Inc., Senior Subordinated Notes, 8.500% due 8/1/14 | | | 207,563 | |

| | 175,000 | | Rite Aid Corp., Senior Secured Notes, 7.500% due 1/15/15 | | | 170,625 | |

|

|

|

| | | | Total Food & Staples Retailing | | | 378,188 | |

|

|

|

| | Food Products — 0.4% | | | | |

| | 125,000 | | Del Monte Corp., Senior Subordinated Notes, 8.625% due 12/15/12 | | | 132,656 | |

| | 200,000 | | Doane Pet Care Co., Senior Notes, 10.750% due 3/1/10 | | | 217,500 | |

| | 250,000 | | Dole Food Co. Inc., Debentures, 8.750% due 7/15/13 | | | 246,875 | |

| | 125,000 | | Pinnacle Foods Holding Corp., Senior Subordinated Notes, 8.250% due 12/1/13 | | | 124,375 | |

| | 90,000 | | United Agri Products Inc., Senior Notes, 8.250% due 12/15/11 | | | 94,050 | |

|

|

|

| | | | Total Food Products | | | 815,456 | |

|

|

|

| | Health Care Providers & Services — 0.9% | | | | |

| | 225,000 | | Community Health Systems Inc., Senior Subordinated Notes, 6.500% due 12/15/12 | | | 219,094 | |

| | 225,000 | | DaVita Inc., Senior Subordinated Notes, 7.250% due 3/15/15 | | | 227,250 | |

| | 200,000 | | Extendicare Health Services Inc., Senior Subordinated Notes, 6.875% due 5/1/14 | | | 207,000 | |

| | | | HCA Inc.: | | | | |

| | 200,000 | | Debentures, 7.050% due 12/1/27 | | | 183,432 | |

| | 250,000 | | Notes, 6.375% due 1/15/15 | | | 244,569 | |

| | 375,000 | | IASIS Healthcare LLC/IASIS Capital Corp., Senior Subordinated Notes, 8.750% due 6/15/14 | | | 376,875 | |

| | 100,000 | | National Mentor Inc., Senior Subordinated Notes, 9.625% due 12/1/12 | | | 113,500 | |

| | 375,000 | | Tenet Healthcare Corp., Senior Notes, 9.875% due 7/1/14 | | | 381,562 | |

|

|

|

| | | | Total Health Care Providers & Services | | | 1,953,282 | |

|

|

|

| | Hotels, Restaurants & Leisure — 1.8% | | | | |

| | 125,000 | | AMF Bowling Worldwide Inc., Senior Subordinated Notes, 10.000% due 3/1/10 | | | 128,750 | |

| | 175,000 | | Boyd Gaming Corp., Senior Subordinated Notes, 7.750% due 12/15/12 | | | 184,187 | |

| | 225,000 | | Carrols Corp., Senior Subordinated Notes, 9.000% due 1/15/13 | | | 227,250 | |

| | 250,000 | | Choctaw Resort Development Enterprise, Senior Notes, 7.250% due 11/15/19 (d) | | | 252,500 | |

| | 350,000 | | Cinemark Inc., Senior Discount Notes, step bond to yield 9.008% due 3/15/14 | | | 269,500 | |

| | | | Gaylord Entertainment Co., Senior Notes: | | | | |

| | 25,000 | | 8.000% due 11/15/13 | | | 26,188 | |

| | 125,000 | | 6.750% due 11/15/14 | | | 122,500 | |

| | 125,000 | | Herbst Gaming Inc., Senior Subordinated Notes, 7.000% due 11/15/14 | | | 125,313 | |

| | 225,000 | | Isle of Capri Casinos Inc., Senior Subordinated Notes, 7.000% due 3/1/14 | | | 223,312 | |

| | 70,000 | | Kerzner International Ltd., Senior Subordinated Notes, 6.750% due 10/1/15 | | | 74,025 | |

| | 250,000 | | Las Vegas Sands Corp., Senior Notes, 6.375% due 2/15/15 | | | 241,250 | |

| | 500,000 | | MGM MIRAGE Inc., Senior Notes, 6.750% due 9/1/12 | | | 501,875 | |

See Notes to Financial Statements.

6 Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | Hotels, Restaurants & Leisure — 1.8% (continued) | | | | |

| $ | 200,000 | | Mohegan Tribal Gaming Authority, Senior Subordinated Notes, 6.875% due 2/15/15 | | $ | 199,750 | |

| | 250,000 | | Penn National Gaming Inc., Senior Subordinated Notes, 6.750% due 3/1/15 | | | 251,250 | |

| | 200,000 | | Pinnacle Entertainment Inc., Senior Subordinated Notes, 8.250% due 3/15/12 | | | 210,500 | |

| | 125,000 | | Riddell Bell Holdings Inc., Senior Subordinated Notes, 8.375% due 10/1/12 | | | 126,562 | |

| | 200,000 | | Scientific Games Corp., Senior Subordinated Notes, 6.250% due 12/15/12 | | | 196,750 | |

| | | | Six Flags Inc., Senior Notes: | | | | |

| | 200,000 | | 9.750% due 4/15/13 | | | 202,500 | |

| | 25,000 | | 9.625% due 6/1/14 | | | 25,313 | |

| | 375,000 | | Station Casinos Inc., Senior Subordinated Notes, 6.875% due 3/1/16 | | | 378,750 | |

|

|

|

| | | | Total Hotels, Restaurants & Leisure | | | 3,968,025 | |

|

|

|

| | Household Durables — 0.2% | | | | |

| | 125,000 | | Interface Inc., Senior Notes, 10.375% due 2/1/10 | | | 137,500 | |

| | 225,000 | | Norcraft Cos. LP/Norcraft Finance Corp., Senior Subordinated Notes, 9.000% due 11/1/11 | | | 235,125 | |

| �� | 125,000 | | Sealy Mattress Co., Senior Subordinated Notes, 8.250% due 6/15/14 | | | 131,250 | |

|

|

|

| | | | Total Household Durables | | | 503,875 | |

|

|

|

| | Independent Power Producers & Energy Traders — 0.8% | | | | |

| | | | AES Corp., Senior Notes: | | | | |

| | 375,000 | | 9.375% due 9/15/10 | | | 410,625 | |

| | 25,000 | | 8.875% due 2/15/11 | | | 27,063 | |

| | 275,000 | | Calpine Corp., Second Priority Senior Secured Notes, 8.500% due 7/15/10 (c)(d) | | | 253,687 | |

| | | | Dynegy Holdings Inc.: | | | | |

| | 200,000 | | Senior Debentures, 7.625% due 10/15/26 | | | 184,000 | |

| | 500,000 | | Senior Notes, 6.875% due 4/1/11 | | | 485,000 | |

| | | | NRG Energy Inc., Senior Notes: | | | | |

| | 75,000 | | 7.250% due 2/1/14 | | | 76,406 | |

| | 225,000 | | 7.375% due 2/1/16 | | | 230,344 | |

|

|

|

| | | | Total Independent Power Producers & Energy Traders | | | 1,667,125 | |

|

|

|

| | Industrial Conglomerates — 0.2% | | | | |

| | 125,000 | | Blount Inc., Senior Subordinated Notes, 8.875% due 8/1/12 | | | 130,625 | |

| | 200,000 | | KI Holdings Inc., Senior Discount Notes, step bond to yield 9.995% due 11/15/14 | | | 146,000 | |

| | 75,000 | | Park-Ohio Industries Inc., Senior Subordinated Notes, 8.375% due 11/15/14 | | | 71,063 | |

|

|

|

| | | | Total Industrial Conglomerates | | | 347,688 | |

|

|

|

| | Insurance — 0.2% | | | | |

| | 500,000 | | Stingray Pass-Through Trust Certificates, Medium-Term Notes, 5.902% due 1/12/15 (d) | | | 481,223 | |

|

|

|

| | Internet & Catalog Retail — 0.1% | | | | |

| | 175,000 | | FTD Inc., Senior Subordinated Notes, 7.750% due 2/15/14 | | | 174,563 | |

|

|

|

| | IT Services — 0.3% | | | | |

| | 425,000 | | Iron Mountain Inc., Senior Subordinated Notes, 8.625% due 4/1/13 | | | 444,125 | |

| | 225,000 | | Unisys Corp., Senior Notes, 6.875% due 3/15/10 | | | 219,937 | |

|

|

|

| | | | Total IT Services | | | 664,062 | |

|

|

|

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report 7

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | Machinery — 0.3% | | | | |

| $ | 125,000 | | Invensys PLC, Senior Notes, 9.875% due 3/15/11 (d) | | $ | 133,438 | |

| | 125,000 | | Mueller Group Inc., Senior Subordinated Notes, 10.000% due 5/1/12 | | | 137,500 | |

| | 300,000 | | Terex Corp., Senior Subordinated Notes, 7.375% due 1/15/14 | | | 309,000 | |

|

|

|

| | | | Total Machinery | | | 579,938 | |

|

|

|

| | Media — 2.1% | | | | |

| | 50,000 | | AMC Entertainment Inc., Senior Subordinated Notes, 11.000% due 2/1/16 (d) | | | 51,875 | |

| | 225,000 | | Cadmus Communications Corp., Senior Subordinated Notes, 8.375% due 6/15/14 | | | 227,250 | |

| | 497,000 | | CCH I LLC, Senior Secured Notes, 11.000% due 10/1/15 | | | 415,616 | |

| | 225,000 | | Charter Communications Holdings II LLC/Charter Communications Holdings II Capital Corp., Senior Notes, 10.250% due 9/15/10 | | | 222,187 | |

| | 225,000 | | Charter Communications Operating LLC, Second Lien Senior Notes, 8.375% due 4/30/14 (d) | | | 225,562 | |

| | | | CSC Holdings Inc.: | | | | |

| | 75,000 | | Debentures, Series B, 8.125% due 8/15/09 | | | 77,813 | |

| | 125,000 | | Senior Debentures, 7.625% due 7/15/18 | | | 124,219 | |

| | 250,000 | | Senior Notes, Series B, 8.125% due 7/15/09 | | | 259,687 | |

| | | | Dex Media Inc., Discount Notes: | | | | |

| | 75,000 | | Step bond to yield 6.822% due 11/15/13 | | | 63,750 | |

| | 370,000 | | Step bond to yield 7.648% due 11/15/13 | | | 314,500 | |

| | | | DIRECTV Holdings LLC/DIRECTV Financing Co. Inc., Senior Notes: | | | | |

| | 81,000 | | 8.375% due 3/15/13 | | | 86,873 | |

| | 375,000 | | 6.375% due 6/15/15 | | | 372,187 | |

| | 375,000 | | EchoStar DBS Corp., Senior Notes, 6.625% due 10/1/14 | | | 364,219 | |

| | 50,000 | | Intelsat Subsidiary Holding Co. Ltd., Senior Notes, 9.614% due 1/15/12 (b) | | | 51,063 | |

| | 325,000 | | LodgeNet Entertainment Corp., Senior Subordinated Debentures, 9.500% due 6/15/13 | | | 352,625 | |

| | 75,000 | | Mediacom Broadband LLC/Mediacom Broadband Corp., Senior Notes, 11.000% due 7/15/13 | | | 80,250 | |

| | | | R.H. Donnelley Corp.: | | | | |

| | | | Senior Discount Notes: | | | | |

| | 50,000 | | Series A-1, 6.875% due 1/15/13 (d) | | | 47,000 | |

| | 75,000 | | Series A-2, 6.875% due 1/15/13 (d) | | | 70,500 | |

| | 125,000 | | Senior Notes, Series A-3, 8.875% due 1/15/16 (d) | | | 130,625 | |

| | 200,000 | | Salem Communications Holding Corp., Senior Subordinated Notes

Series B, 9.000% due 7/1/11 | | | 210,500 | |

| | 175,000 | | Sinclair Broadcast Group Inc., Senior Subordinated Notes, 8.000% due 3/15/12 | | | 179,375 | |

| | 375,000 | | Vertis Inc., Senior Secured Second Lien Notes, 9.750% due 4/1/09 | | | 386,250 | |

| | 225,000 | | Yell Finance BV, Senior Notes, 10.750% due 8/1/11 | | | 242,156 | |

|

|

|

| | | | Total Media | | | 4,556,082 | |

|

|

|

| | Metals & Mining — 0.2% | | | | |

| | 125,000 | | Aleris International Inc., Senior Secured Notes, 10.375% due 10/15/10 | | | 138,437 | |

| | 200,000 | | Corporacion Nacional del Cobre-Codelco, Notes, 5.500% due 10/15/13 (d) | | | 198,296 | |

| | 125,000 | | Vale Overseas Ltd., Notes 6.250% due 1/11/16 | | | 123,594 | |

|

|

|

| | | | Total Metals & Mining | | | 460,327 | |

|

|

|

See Notes to Financial Statements.

8 Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | Multiline Retail — 0.1% | | | | |

| $ | 100,000 | | Harry & David Operations, Senior Notes, 9.000% due 3/1/13 | | $ | 96,000 | |

| | 75,000 | | Neiman Marcus Group Inc., Senior Subordinated Notes, 10.375% due 10/15/15 (d) | | | 80,063 | |

|

|

|

| | | | Total Multiline Retail | | | 176,063 | |

|

|

|

| | Oil, Gas & Consumable Fuels — 1.4% | | | | |

| | | | Chesapeake Energy Corp., Senior Notes: | | | | |

| | 50,000 | | 6.375% due 6/15/15 | | | 49,438 | |

| | 375,000 | | 6.875% due 1/15/16 | | | 379,687 | |

| | | | El Paso Corp., Medium-Term Notes: | | | | |

| | 375,000 | | 7.375% due 12/15/12 | | | 383,437 | |

| | 300,000 | | 7.750% due 1/15/32 | | | 303,750 | |

| | 250,000 | | EXCO Resources Inc., Senior Notes, 7.250% due 1/15/11 | | | 250,000 | |

| | 475,000 | | Petronas Capital Ltd., Notes 7.875% due 5/22/22 (d) | | | 565,564 | |

| | 200,000 | | Stone Energy Corp., Senior Subordinated Notes, 8.250% due 12/15/11 | | | 202,000 | |

| | 250,000 | | Vintage Petroleum Inc., Senior Subordinated Notes, 7.875% due 5/15/11 | | | 260,030 | |

| | 500,000 | | Williams Cos. Inc., Notes, 8.750% due 3/15/32 | | | 587,500 | |

|

|

|

| | | | Total Oil, Gas & Consumable Fuels | | | 2,981,406 | |

|

|

|

| | Paper & Forest Products — 0.3% | | | | |

| | | | Appleton Papers Inc.: | | | | |

| | 100,000 | | Senior Notes, 8.125% due 6/15/11 | | | 101,000 | |

| | 125,000 | | Senior Subordinated Notes, Series B, 9.750% due 6/15/14 | | | 124,688 | |

| | 225,000 | | Boise Cascade, LLC, Senior Subordinated Notes, Series B, 7.125% due 10/15/14 | | | 217,687 | |

| | 200,000 | | Buckeye Technologies Inc., Senior Notes, 8.500% due 10/1/13 | | | 202,500 | |

|

|

|

| | | | Total Paper & Forest Products | | | 645,875 | |

|

|

|

| | Personal Products — 0.1% | | | | |

| | 200,000 | | Playtex Products Inc., Senior Subordinated Notes, 9.375% due 6/1/11 | | | 210,000 | |

|

|

|

| | Pharmaceuticals — 0.1% | | | | |

| | 125,000 | | Warner Chilcott Corp., Senior Subordinated Notes, 9.250% due 2/1/15 (d) | | | 124,688 | |

|

|

|

| | Real Estate — 0.6% | | | | |

| | 175,000 | | Felcor Lodging LP, Senior Notes, 9.000% due 6/1/11 | | | 192,500 | |

| | 425,000 | | Host Marriott LP, Senior Notes, 7.125% due 11/1/13 | | | 434,563 | |

| | 425,000 | | iStar Financial Inc., Senior Notes, 5.150% due 3/1/12 | | | 408,370 | |

| | 250,000 | | MeriStar Hospitality Corp., Senior Notes, 9.125% due 1/15/11 | | | 290,625 | |

|

|

|

| | | | Total Real Estate | | | 1,326,058 | |

|

|

|

| | Semiconductors & Semiconductor Equipment — 0.2% | | | | |

| | 400,000 | | Amkor Technology Inc., Senior Notes, 9.250% due 2/15/08 | | | 410,000 | |

|

|

|

| | Specialty Retail — 0.3% | | | | |

| | 225,000 | | CSK Auto Inc., Senior Subordinated Notes, 7.000% due 1/15/14 | | | 215,437 | |

| | 125,000 | | Eye Care Centers of America, Senior Subordinated Notes, 10.750% due 2/15/15 | | | 125,000 | |

| | 100,000 | | Finlay Fine Jewelry Corp., Senior Notes, 8.375% due 6/1/12 | | | 88,375 | |

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report 9

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | Specialty Retail — 0.3% (continued) | | | | |

| $ | 225,000 | | Jafra Cosmetics International Inc., Senior Subordinated Notes, 10.750% due 5/15/11 | | $ | 246,094 | |

|

|

|

| | | | Total Specialty Retail | | | 674,906 | |

|

|

|

| | Textiles, Apparel & Luxury Goods — 0.4% | | | | |

| | 225,000 | | Collins & Aikman Floor Covering Inc., Senior Subordinated Notes,

Series B, 9.750% due 2/15/10 | | | 213,750 | |

| | | | Levi Strauss & Co., Senior Notes: | | | | |

| | 25,000 | | 9.280% due 4/1/12 (b) | | | 26,000 | |

| | 25,000 | | 12.250% due 12/15/12 | | | 28,531 | |

| | 275,000 | | 9.750% due 1/15/15 | | | 290,813 | |

| | 125,000 | | Oxford Industries Inc., Senior Notes, 8.875% due 6/1/11 | | | 129,375 | |

| | 100,000 | | Simmons Bedding Co., Senior Subordinated Notes, 7.875% due 1/15/14 | | | 97,250 | |

| | 50,000 | | Simmons Co., Senior Discount Notes, step bond to yield 9.995% due 12/15/14 | | | 32,250 | |

|

|

|

| | | | Total Textiles, Apparel & Luxury Goods | | | 817,969 | |

|

|

|

| | Wireless Telecommunication Services — 0.5% | | | | |

| | 250,000 | | American Tower Corp., Senior Notes, 7.125% due 10/15/12 | | | 261,250 | |

| | 125,000 | | Centennial Communications Corp., Senior Notes, 10.125% due 6/15/13 | | | 137,187 | |

| | 75,000 | | Centennial Communications Corp./Centennial Cellular Operating Co. LLC/Centennial Puerto Rico Operations Corp., Senior Notes, 8.125% due 2/1/14 | | | 76,875 | |

| | 125,000 | | IWO Holdings Inc., Secured Notes, 8.350% due 1/15/12 (b) | | | 130,781 | |

| | 130,000 | | SBA Communications Corp., Senior Notes, 8.500% due 12/1/12 | | | 144,950 | |

| | 125,000 | | UbiquiTel Operating Co., Senior Notes, 9.875% due 3/1/11 | | | 137,188 | |

| | 175,000 | | US Unwired Inc., Second Priority Secured Notes, Series B, 10.000% due 6/15/12 | | | 197,094 | |

|

|

|

| | | | Total Wireless Telecommunication Services | | | 1,085,325 | |

|

|

|

| | | | TOTAL CORPORATE BONDS & NOTES

(Cost — $47,916,224) | | | 47,157,348 | |

|

|

|

| | ASSET-BACKED SECURITIES — 14.6% | | | | |

| | Home Equity — 14.6% | | | | |

| | | | Aegis Asset-Backed Securities Trust: | | | | |

| | 217,601 | | Series 2004-5N, 5.000% due 12/25/34 (d) | | | 215,833 | |

| | 560,017 | | Series 2004-6N, 4.750% due 3/25/35 (d) | | | 557,042 | |

| | 146,678 | | Series 2005-1N, Class N1, 4.250% due 3/25/35 (d) | | | 146,431 | |

| | | | Ameriquest Mortgage Securities Inc.: | | | | |

| | 1,500,000 | | Series 2004-R08, Class M10, 7.318% due 9/25/34 (b)(d) | | | 1,416,940 | |

| | 3,000,000 | | Series 2004-R1, Class M10, 7.475% due 2/25/34 (b)(d) | | | 2,927,520 | |

| | 2,000,000 | | Argent Securities Inc., Series 2004-W8, Class M10, 8.318% due 5/25/34 (b) | | | 1,973,502 | |

| | 196,378 | | Countrywide Asset-Backed Certificates, Series 2004-11N, Class N, 5.250% due 4/25/36 (d) | | | 195,777 | |

| | 3,000,000 | | Fremont Home Loan Trust, Series 2004-D, Class M5, 5.818% due 11/25/34 (b) | | | 3,024,747 | |

| | | | GSAMP Trust: | | | | |

| | 1,500,000 | | Series 2004-OPT, Class B1, 6.418% due 11/25/34 (b) | | | 1,509,997 | |

| | 180,353 | | Series 2005-OPTN, 5.000% due 11/25/34 (c) | | | 179,088 | |

| | 5,604,750 | | Lehman XS Trust, Series 2005-1, Class 2A2, 4.660% due 7/25/35 (b)(e) | | | 5,499,533 | |

See Notes to Financial Statements.

10 Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | Home Equity — 14.6% (continued) | | | | |

| $ | 757,184 | | Long Beach Asset Holdings Corp., Series 2004-06, Class N2, 7.500% due 11/25/34 (d) | | $ | 537,601 | |

| | 113,805 | | Merrill Lynch Mortgage Investors Inc., Series 2005-WM1N, Class N1, 5.000% due 9/25/35 (d) | | | 112,967 | |

| | | | Morgan Stanley Asset Backed Securities Capital I: | | | | |

| | 2,000,000 | | Series 2004-HE9, Class M6, 6.068% due 11/25/34 (b) | | | 2,024,982 | |

| | 1,000,000 | | Series 2004-OP1, Class M5, 5.868% due 11/25/34 (b) | | | 1,014,867 | |

| | | | Novastar Home Equity Loan: | | | | |

| | 1,500,000 | | Series 2004-4, Class M4, 5.918% due 3/25/35 (b) | | | 1,506,911 | |

| | 2,000,000 | | Series 2005-2, Class M11, 7.818% due 10/25/35 (b) | | | 1,756,551 | |

| | 1,500,000 | | Option One Mortgage Loan Trust, Series 2004-2, Class M7, 8.318% due 5/25/34 (b) | | | 1,456,738 | |

| | 2,000,000 | | Park Place Securities Inc., Series 2004-WWF1, Class M4, 5.918% due 2/25/35 (b) | | | 2,028,664 | |

| | 350,556 | | Park Place Securities NIM Trust, Series 2005-WHQ2, Class A, 5.192% due 5/25/35 (d) | | | 348,453 | |

| | | | Sail NIM Notes: | | | | |

| | 130,037 | | Series 2004-002A, Class A, 5.500% due 3/27/34 (d) | | | 126,202 | |

| | 300,171 | | Series 2004-010A, Class B, 7.000% due 11/27/34 (d) | | | 285,315 | |

| | | | Series 2004-BN2A: | | | | |

| | 91,703 | | Class A, 5.000% due 12/27/34 (d) | | | 91,518 | |

| | 274,967 | | Class B, 7.000% due 12/27/34 (d) | | | 249,497 | |

| | 294,397 | | Series 2005-1A, Class B, 7.500% due 2/27/35 (d) | | | 284,282 | |

| | 2,260,000 | | Structured Asset Investment Loan Trust, Series 2004-9, Class M4, 6.118% due 10/25/34 (b) | | | 2,277,569 | |

|

|

|

| | | | TOTAL ASSET-BACKED SECURITIES

(Cost — $31,822,705) | | | 31,748,527 | |

|

|

|

| | MORTGAGE-BACKED SECURITIES — 17.5% | | | | |

| | FHLMC — 9.6% | | | | |

| | | | Federal Home Loan Mortgage Corp. (FHLMC), Gold: | | | | |

| | 1,134,026 | | 7.000% due 6/1/17 | | | 1,167,616 | |

| | 802,418 | | 6.500% due 8/1/29 | | | 822,178 | |

| | 2,837,864 | | 6.000% due 2/1/33 (e) | | | 2,843,185 | |

| | 6,678,360 | | 6.500% due 11/1/34 (e) | | | 6,810,407 | |

| | 9,239,414 | | 5.500% due 6/1/35 (e) | | | 9,026,700 | |

|

|

|

| | | | TOTAL FHLMC | | | 20,670,086 | |

|

|

|

| | FNMA — 7.9% | | | | |

| | | | Federal National Mortgage Association (FNMA): | | | | |

| | 481,495 | | 5.500% due 1/1/14 | | | 480,140 | |

| | 2,033,855 | | 7.000% due 10/1/18-6/1/32 | | | 2,103,136 | |

| | 5,645,513 | | 6.000% due 5/1/33 (e) | | | 5,650,299 | |

| | 9,165,067 | | 5.500% due 4/1/35 (e) | | | 8,951,656 | |

|

|

|

| | | | TOTAL FNMA | | | 17,185,231 | |

|

|

|

| | | | TOTAL MORTGAGE-BACKED SECURITIES

(Cost — $38,984,055) | | | 37,855,317 | |

|

|

|

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report 11

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | COLLATERALIZED MORTGAGE OBLIGATIONS — 14.9% | | | | |

| $ | 410,000 | | American Home Mortgage Investment Trust, Series 2005-4, Class M3, 5.618% due 11/25/45 (b) | | $ | 410,125 | |

| | | | Federal Home Loan Mortgage Corp. (FHLMC): | | | | |

| | 7,108,499 | | Series 2638, Class DI, PAC IO, 5.000% due 5/15/23 (e) | | | 1,220,036 | |

| | 7,704,559 | | Series 2639, Class UI, PAC-1 IO, 5.000% due 3/15/22 (e) | | | 1,376,427 | |

| | 16,224,150 | | Series 2645, Class IW, PAC IO, 5.000% due 7/15/26 (e) | | | 1,608,141 | |

| | 15,484,713 | | Series 2684, Class PI, PAC, IO, 5.000% due 5/15/23 (e) | | | 779,028 | |

| | 11,583,552 | | Series 2777, Class PI, PAC, IO, 5.000% due 5/15/24 | | | 829,136 | |

| | 7,033,571 | | Series 2839, Class TX, PAC, IO, 5.000% due 1/15/19 (e) | | | 1,046,184 | |

| | 7,543,000 | | Series 2866, Class IC, PAC, IO, 5.000% due 1/15/24 (e) | | | 896,847 | |

| | 2,225,920 | | Series 2927, Class 0Q, PAC-1, IO, 5.000% due 8/15/19 | | | 107,634 | |

| | | | Federal National Mortgage Association (FNMA): | | | | |

| | 6,892,454 | | Series 339, Class 30, IO, 5.500% due 7/1/18 | | | 1,262,692 | |

| | 16,312,722 | | Strip, Series 337, Class 2, IO, 5.000% due 7/1/33 (e) | | | 3,939,431 | |

| | 145,330 | | Homestar NIM Trust, Series 2004-6, Class A1, 5.500% due 1/25/35 (c) | | | 145,262 | |

| | 5,469,984 | | Indymac Index Mortgage Loan Trust, Series 2005-AR21, Class 4A1, 5.451% due 10/25/35 (b)(e) | | | 5,400,107 | |

| | | | Structured Asset Securities Corp.: | | | | |

| | 855,552 | | Series 1998-2, Class M1, 5.918% due 2/25/28 (b) | | | 859,193 | |

| | 292,016 | | Series 1998-3, Class M1, 5.818% due 3/25/28 (b) | | | 292,283 | |

| | 582,342 | | Series 1998-8, Class M1, 5.758% due 8/25/28 (b) | | | 582,853 | |

| | 11,301,857 | | Series 2005-RF3, Class 2A, 5.222% due 6/25/35 (b)(d) | | | 11,471,384 | |

|

|

|

| | | | TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS

(Cost — $30,649,971) | | | 32,226,763 | |

|

|

|

| | SOVEREIGN BONDS — 14.9% | | | | |

| | Argentina — 0.6% | | | | |

| | | | Republic of Argentina: | | | | |

| | 200,000EUR | | 9.000% due 6/20/03 (c) | | | 72,221 | |

| | 575,000DEM | | 9.000% due 9/19/03 (c) | | | 107,055 | |

| | 400,000EUR | | 10.250% due 1/26/07 (c) | | | 155,973 | |

| | 730,625 | | 4.889% due 8/3/12 (b) | | | 680,130 | |

| | | | GDP Linked Securities: | | | | |

| | 275,000EUR | | 0.000% due 12/15/35 (b) | | | 30,375 | |

| | 270,000 | | 0.000% due 12/15/35 (b) | | | 24,840 | |

| | 50,385ARS | | 0.000% due 12/15/35 (b) | | | 1,506 | |

| | 475,000EUR | | Medium-Term Notes, 7.000% due 3/18/04 (c) | | | 178,011 | |

| | 90,000 | | Par Bonds, 1.330% due 12/31/38 | | | 34,178 | |

|

|

|

| | | | Total Argentina | | | 1,284,289 | |

|

|

|

| | Brazil — 2.9% | | | | |

| | | | Federative Republic of Brazil: | | | | |

| | | | Collective Action Securities: | | | | |

| | 1,000,000 | | 8.000% due 1/15/18 | | | 1,083,000 | |

| | 675,000 | | 8.750% due 2/4/25 | | | 776,250 | |

| | 4,435,376 | | DCB, Series L, 5.250% due 4/15/12 (b) | | | 4,434,267 | |

|

|

|

| | | | Total Brazil | | | 6,293,517 | |

|

|

|

See Notes to Financial Statements.

12 Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | |

| Bulgaria — 0.2% | | | | |

| 305,000 | | Republic of Bulgaria, 8.250% due 1/15/15 (d) | | $ | 357,613 | |

|

|

| Chile — 0.2% | | | | |

| 450,000 | | Republic of Chile, 5.500% due 1/15/13 | | | 450,711 | |

|

|

| China — 0.1% | | | | |

| 170,000 | | People’s Republic of China, 4.750% due 10/29/13 | | | 163,255 | |

|

|

| Colombia — 0.8% | | | | |

| | | Republic of Colombia: | | | | |

| 1,275,000 | | 10.750% due 1/15/13 | | | 1,587,375 | |

| 75,000 | | Medium-Term Notes, 11.750% due 2/25/20 | | | 106,950 | |

|

|

| | | Total Colombia | | | 1,694,325 | |

|

|

| Ecuador — 0.3% | | | | |

| 725,000 | | Republic of Ecuador, step bond to yield 7.325% due 8/15/30 (d) | | | 733,156 | |

|

|

| El Salvador — 0.3% | | | | |

| | | Republic of El Salvador: | | | | |

| 500,000 | | 7.750% due 1/24/23 (d) | | | 556,250 | |

| 90,000 | | 8.250% due 4/10/32 (d) | | | 102,150 | |

|

|

| | | Total El Salvador | | | 658,400 | |

|

|

| Indonesia — 0.1% | | | | |

| 125,000 | | Republic of Indonesia, 8.500% due 10/12/35 (d) | | | 139,606 | |

|

|

| Malaysia — 0.2% | | | | |

| 375,000 | | Federation of Malaysia, 7.500% due 7/15/11 | | | 408,105 | |

|

|

| Mexico — 2.8% | | | | |

| | | United Mexican States: | | | | |

| 165,000 | | 11.375% due 9/15/16 | | | 232,856 | |

| 2,650,000 | | 8.125% due 12/30/19 | | | 3,121,700 | |

| | | Medium-Term Notes: | | | | |

| 870,000 | | 5.625% due 1/15/17 | | | 843,465 | |

| | | Series A: | | | | |

| 959,000 | | 6.375% due 1/16/13 | | | 985,852 | |

| 745,000 | | 8.000% due 9/24/22 | | | 873,513 | |

|

|

| | | Total Mexico | | | 6,057,386 | |

|

|

| Panama — 0.5% | | | | |

| | | Republic of Panama: | | | | |

| 100,000 | | 7.250% due 3/15/15 | | | 106,375 | |

| 261,000 | | 6.700% due 1/26/36 | | | 260,739 | |

| 859,073 | | PDI, 5.563% due 7/17/16 (b) | | | 846,186 | |

|

|

| | | Total Panama | | | 1,213,300 | |

|

|

| Peru — 0.8% | | | | |

| | | Republic of Peru: | | | | |

| 10,000 | | 9.875% due 2/6/15 | | | 11,850 | |

| 185,000 | | 8.750% due 11/21/33 | | | 206,506 | |

| 1,164,000 | | FLIRB, 5.000% due 3/7/17 (b) | | | 1,102,890 | |

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report 13

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | |

| Peru — 0.8% (continued) | | | | |

| | | Global Bonds: | | | | |

| 80,000 | | 8.375% due 5/3/16 | | $ | 87,000 | |

| 350,000 | | 7.350% due 7/21/25 | | | 344,663 | |

|

|

| | | Total Peru | | | 1,752,909 | |

|

|

| Philippines — 0.7% | | | | |

| | | Republic of the Philippines: | | | | |

| 125,000 | | 8.250% due 1/15/14 | | | 135,703 | |

| 1,060,000 | | 9.875% due 1/15/19 | | | 1,277,274 | |

| 50,000 | | 10.625% due 3/16/25 | | | 64,906 | |

| 100,000 | | 9.500% due 2/2/30 | | | 118,875 | |

|

|

| | | Total Philippines | | | 1,596,758 | |

|

|

| Poland — 0.2% | | | | |

| 365,000 | | Republic of Poland, 5.250% due 1/15/14 | | | 359,306 | |

|

|

| Russia — 1.8% | | | | |

| | | Russian Federation: | | | | |

| 320,000 | | 8.250% due 3/31/10 (d) | | | 338,600 | |

| 1,075,000 | | 11.000% due 7/24/18 (d) | | | 1,542,625 | |

| 765,000 | | 12.750% due 6/24/28 (d) | | | 1,367,437 | |

| 675,000 | | Step bond to yield 5.000% due 3/31/30 (d) | | | 739,758 | |

|

|

| | | Total Russia | | | 3,988,420 | |

|

|

| South Africa — 0.2% | | | | |

| | | Republic of South Africa: | | | | |

| 125,000 | | 9.125% due 5/19/09 | | | 137,344 | |

| 375,000 | | 6.500% due 6/2/14 | | | 393,281 | |

|

|

| | | Total South Africa | | | 530,625 | |

|

|

| Turkey — 1.1% | | | | |

| | | Republic of Turkey: | | | | |

| 300,000 | | 7.250% due 3/15/15 | | | 313,500 | |

| 425,000 | | 7.000% due 6/5/20 | | | 431,375 | |

| 250,000 | | 11.875% due 1/15/30 | | | 387,812 | |

| 1,020,000 | | Collective Action Securities, Notes, 9.500% due 1/15/14 | | | 1,208,700 | |

|

|

| | | Total Turkey | | | 2,341,387 | |

|

|

| Ukraine — 0.2% | | | | |

| 335,000 | | Republic of Ukraine, 7.650% due 6/11/13 (d) | | | 351,750 | |

|

|

| Uruguay — 0.2% | | | | |

| | | Republic of Uruguay, Benchmark Bonds: | | | | |

| 175,000 | | 7.250% due 2/15/11 | | | 183,094 | |

| 250,000 | | 7.500% due 3/15/15 | | | 261,875 | |

|

|

| | | Total Uruguay | | | 444,969 | |

|

|

| Venezuela — 0.7% | | | | |

| | | Bolivarian Republic of Venezuela: | | | | |

| 100,000 | | 5.375% due 8/7/10 (d) | | | 96,875 | |

See Notes to Financial Statements.

14 Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report

Schedule of Investments (March 31, 2006) (unaudited) (continued)

| | | | | | | |

| | |

Face Amount† | | Security | | Value | |

| | | | | | | | |

| | Venezuela — 0.7% (continued) | | | | |

| | 175,000 | | 7.650% due 4/21/25 | | $ | 189,438 | |

| | | | Collective Action Securities: | | | | |

| | 675,000 | | 3.090% due 4/20/11 (b)(d) | | | 679,556 | |

| | 500,000 | | 10.750% due 9/19/13 | | | 623,876 | |

|

|

|

| | | | Total Venezuela | | | 1,589,745 | |

|

|

|

| | | | TOTAL SOVEREIGN BONDS (Cost — $31,077,558) | | | 32,409,532 | |

|

|

|

| | |

| Warrant | | | | | |

| | Warrants — 0.1% | | | | |

| | 1,250 | | Bolivarian Republic of Venezuela, Expires 4/15/20* | | | 42,500 | |

| | 7,000 | | United Mexican States, Series XW5, Expires 11/9/06* | | | 22,750 | |

| | 5,500 | | United Mexican States, Series XW10, Expires 10/10/06* | | | 29,150 | |

| | 5,000 | | United Mexican States, Series XW20, Expires 9/1/06* | | | 40,000 | |

|

|

|

| | | | TOTAL WARRANTS (Cost — $90,250) | | | 134,400 | |

|

|

|

| | | | TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENT (Cost — $192,334,361) | | | 193,469,329 | |

|

|

|

| | |

Face

Amount | | | | | |

| | SHORT-TERM INVESTMENT — 10.7% | | | | |

| | Repurchase Agreement — 10.7% | | | | |

| $ | 23,252,000 | | Merrill Lynch, Pierce, Fenner & Smith Inc. tri-party repurchase agreement dated 3/31/06, 4.790% due 4/3/06; Proceeds at maturity — $23,261,281;

(Fully collateralized by Federal National Mortgage Association Notes, 5.300% due 2/22/11; Market value — $23,717,522) (Cost — $23,252,000) | | | 23,252,000 | |

|

|

|

| | | | TOTAL INVESTMENTS — 100.0% (Cost — $215,586,361#) | | $ | 216,721,329 | |

|

|

|

| † | | Face amount denominated in U.S. dollars, unless otherwise noted. |

| * | | Non-income producing security. |

| (a) | | Participation interest was acquired through the financial institution indicated parenthetically. |

| (b) | | Variable rate security. Interest rate disclosed is that which is in effect at March 31, 2006. |

| (c) | | Security is currently in default. |

| (d) | | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Directors, unless otherwise noted. |

| (e) | | All or a portion of this security is segregated for reverse repurchase agreements and/or swap contracts. |

| # | | Aggregate cost for federal income tax purposes is substantially the same. |

| | |

Abbreviations used in this schedule:

|

| ARS | | — Argentine Peso |

| DCB | | — Debt Conversion Bond |

| DEM | | — German Mark |

| EUR | | — Euro |

| FLIRB | | — Front-Loaded Interest Reduction Bonds |

| GDP | | — Gross Domestic Product |

| IO | | — Interest Only |

| MXN | | — Mexican Peso |

| NIM | | — Net Interest Margin |

| PAC | | — Planned Amortization Cost |

| PDI | | — Past Due Interest |

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report 15

Statement of Assets and Liabilities (March 31, 2006) (unaudited)

| | | | |

| ASSETS: | | | | |

Investments, at value (Cost — $192,334,361) | | $ | 193,469,329 | |

Repurchase agreement, at value (Cost — $23,252,000) | | | 23,252,000 | |

Deposits with brokers for reverse repurchase agreement | | | 8,847,643 | |

Unrealized appreciation on swaps | | | 3,262,256 | |

Interest receivable | | | 2,166,978 | |

Interest receivable for open swap contracts (Note 3) | | | 1,222,223 | |

Receivable for securities sold | | | 217,213 | |

Prepaid expenses | | | 21,781 | |

|

|

Total Assets | | | 232,459,423 | |

|

|

| LIABILITIES: | | | | |

Payable for open reverse repurchase agreements (Notes 1 and 3) | | | 68,098,000 | |

Interest payable for open swap contracts (Note 3) | | | 1,061,278 | |

Interest payable for open reverse repurchase agreements (Note 3) | | | 228,306 | |

Due to custodian | | | 174,853 | |

Investment management fee payable | | | 146,980 | |

Directors’ fees payable | | | 4,825 | |

Accrued expenses | | | 92,438 | |

|

|

Total Liabilities | | | 69,806,680 | |

|

|

Total Net Assets | | $ | 162,652,743 | |

|

|

| NET ASSETS: | | | | |

Par value ($0.001 par value; 8,323,434 shares issued and outstanding; 100,000,000 shares authorized) | | $ | 8,323 | |

Paid-in capital in excess of par value | | | 158,195,188 | |

Overdistributed net investment income | | | (15,129 | ) |

Accumulated net realized gain on investments and foreign currency transactions | | | 67,209 | |

Net unrealized appreciation on investments, swap contracts and foreign currencies | | | 4,397,152 | |

|

|

Total Net Assets | | $ | 162,652,743 | |

|

|

Shares Outstanding | | | 8,323,434 | |

|

|

Net Asset Value | | | $19.54 | |

|

|

See Notes to Financial Statements.

16 Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report

Statement of Operations (For the six months ended March 31, 2006) (unaudited)

| | | | |

| INVESTMENT INCOME: | | | | |

Interest | | $ | 6,867,690 | |

|

|

| EXPENSES: | | | | |

Interest expense (Note 3) | | | 1,485,080 | |

Investment management fee (Note 2) | | | 860,300 | |

Directors’ fees | | | 38,136 | |

Audit and tax | | | 33,500 | |

Legal fees | | | 27,318 | |

Shareholder reports | | | 25,414 | |

Custody fees | | | 17,074 | |

Transfer agent fees | | | 11,481 | |

Stock exchange listing fees | | | 7,636 | |

Insurance | | | 328 | |

Miscellaneous expenses | | | 2,840 | |

|

|

Total Expenses | | | 2,509,107 | |

Less: Fee waivers and/or expense reimbursements (Note 2) | | | (3,564 | ) |

|

|

Net Expenses | | | 2,505,543 | |

|

|

Net Investment Income | | | 4,362,147 | |

|

|

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS, SWAP CONTRACTS AND FOREIGN CURRENCY TRANSACTIONS (NOTES 1 AND 3): | | | | |

Net Realized Gain (Loss) From: | | | | |

Investment transactions | | | 1,267,960 | |

Swap contracts | | | 110,371 | |

Foreign currency transactions | | | (4,381 | ) |

|

|

Net Realized Gain | | | 1,373,950 | |

|

|

Change in Net Unrealized Appreciation/Depreciation From: | | | | |

Investments | | | (1,648,409 | ) |

Swap contracts | | | 1,841,656 | |

Foreign currencies | | | 122 | |

|

|

Change in Net Unrealized Appreciation/Depreciation | | | 193,369 | |

|

|

Net Gain on Investments, Swap Contracts and Foreign Currency Transactions | | | 1,567,319 | |

|

|

Increase in Net Assets From Operations | | $ | 5,929,466 | |

|

|

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report 17

Statements of Changes in Net Assets

| | | | | | | | |

For the six months ended March 31, 2006 (unaudited)

and the period ended September 30, 2005† | | | | | | | | |

| | |

| | | 2006 | | | 2005 | |

| OPERATIONS: | | | | | | | | |

Net investment income | | $ | 4,362,147 | | | $ | 7,148,395 | |

Net realized gain (loss) | | | 1,373,950 | | | | (453,447 | ) |

Change in net unrealized appreciation/depreciation | | | 193,369 | | | | 4,203,783 | |

|

|

Increase in Net Assets From Operations | | | 5,929,466 | | | | 10,898,731 | |

|

|

| DISTRIBUTIONS TO SHAREHOLDERS FROM (NOTE 1): | | | | | | | | |

Net investment income | | | (4,369,803 | ) | | | (7,036,900 | ) |

Net realized gains | | | (973,009 | ) | | | — | |

Paid-in capital | | | — | | | | (407,388 | ) |

|

|

Decrease in Net Assets From

Distributions to Shareholders | | | (5,342,812 | ) | | | (7,444,288 | ) |

|

|

| FUND SHARE TRANSACTIONS: | | | | | | | | |

Net proceeds from sale of shares (8,200,000 shares issued, net of $328,000 offering cost) | | | — | | | | 156,292,000 | |

Proceeds from shares issued on reinvestment of distributions (118,188 shares issued) | | | — | | | | 2,219,646 | |

|

|

Increase in Net Assets From Fund Share Transactions | | | — | | | | 158,511,646 | |

|

|

Increase in Net Assets | | | 586,654 | | | | 161,966,089 | |

| NET ASSETS: | | | | | | | | |

Beginning of period | | | 162,066,089 | | | | 100,000 | |

|

|

End of period* | | $ | 162,652,743 | | | $ | 162,066,089 | |

|

|

* Includes overdistributed net investment income of: | | | $(15,129) | | | | $(7,473) | |

|

|

| † | | For the period October 26, 2004 (commencement of operations) to September 30, 2005. |

See Notes to Financial Statements.

18 Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report

Statement of Cash Flows (For the six months ended March 31, 2006) (unaudited)

| | | | |

| CASH FLOWS PROVIDED (USED) BY OPERATING ACTIVITIES: | | | | |

Interest received | | $ | 10,398,146 | |

Operating expenses paid | | | (1,015,283 | ) |

Net purchases of short-term investments | | | (19,548,000 | ) |

Realized loss on foreign currency transactions | | | (4,381 | ) |

Realized gain on swap contracts | | | 110,371 | |

Net change in unrealized appreciation on foreign currencies | | | 122 | |

Purchases of long-term investments | | | (37,219,407 | ) |

Proceeds from disposition of long-term investments | | | 63,087,018 | |

Change in payable for open forward currency contracts | | | (101 | ) |

Change in payable on interest rate swap contracts | | | (1,238,849 | ) |

Interest paid | | | (1,419,818 | ) |

|

|

Net Cash Flows Provided By Operating Activities | | | 13,149,818 | |

|

|

| CASH FLOWS USED BY FINANCING ACTIVITIES: | | | | |

Cash distributions paid on Common Stock | | | (5,342,812 | ) |

Deposits with brokers for reverse repurchase agreement | | | (8,151,643 | ) |

|

|

Net Cash Flows Used by Financing Activities | | | (13,494,455 | ) |

|

|

NET DECREASE IN CASH | | | (344,637 | ) |

Cash, Beginning of period | | | 169,784 | |

|

|

Cash, End of period | | $ | (174,853 | ) |

|

|

| RECONCILIATION OF INCREASE IN NET ASSETS FROM OPERATIONS TO NET CASH FLOWS PROVIDED (USED) BY OPERATING ACTIVITIES: | | | | |

Increase in Net Assets From Operations | | $ | 5,929,466 | |

|

|

Accretion of discount on investments | | | (208,052 | ) |

Amortization of premium on investments | | | 2,413,766 | |

Decrease in investments, at value | | | 8,292,753 | |

Decrease in payable for securities purchased | | | (5,236,316 | ) |

Decrease in interest receivable | | | 1,324,742 | |

Decrease in interest rate swap contracts payable | | | (1,238,849 | ) |

Decrease in receivable for securities sold | | | 1,801,967 | |

Decrease in payable for open forward currency contracts | | | (101 | ) |

Increase in prepaid expenses | | | (13,700 | ) |

Increase in interest payable | | | 65,262 | |

Increase in accrued expenses | | | 18,880 | |

|

|

Total Adjustments | | | 7,220,352 | |

|

|

Net Cash Flows Provided By Operating Activities | | $ | 13,149,818 | |

|

|

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report 19

Financial Highlights

For a share of capital stock outstanding throughout each year ended September 30, unless otherwise noted:

| | | | | | | | |

| | |

| | | 2006(1) | | | 2005(2) | |

Net Asset Value, Beginning of Period | | $ | 19.47 | | | $ | 19.06 | (3) |

|

|

Income From Operations: | | | | | | | | |

Net investment income | | | 0.52 | | | | 0.86 | |

Net realized and unrealized gain | | | 0.19 | | | | 0.45 | |

|

|

Total Income From Operations | | | 0.71 | | | | 1.31 | |

|

|

Less Distributions From: | | | | | | | | |

Net investment income | | | (0.52 | ) | | | (0.85 | ) |

Net realized gains | | | (0.12 | ) | | | — | |

Paid-in capital | | | — | | | | (0.05 | ) |

|

|

Total Distributions | | | (0.64 | ) | | | (0.90 | ) |

|

|

Net Asset Value, End of Period | | $ | 19.54 | | | $ | 19.47 | |

|

|

Market Price, End of Period | | $ | 17.20 | | | $ | 17.16 | |

|

|

Total Return(4) | | | 3.73 | % | | | 7.06 | % |

|

|

Total Return, Based on Market Price Per Share(4) | | | 4.08 | % | | | (9.82 | )% |

|

|

Net Assets, End of Period (000s) | | | $162,653 | | | | $162,066 | |

|

|

Ratios to Average Net Assets: | | | | | | | | |

Gross expenses(5) | | | 3.11 | % | | | 1.65 | % |

Gross expenses, excluding interest expense(5) | | | 1.27 | | | | 1.07 | |

Net expenses(5)(6) | | | 3.10 | | | | 1.65 | |

Net expenses, excluding interest expense(5)(6) | | | 1.26 | | | | 1.07 | |

Net investment income(5) | | | 5.40 | | | | 4.94 | |

|

|

Portfolio Turnover Rate | | | 16 | % | | | 46 | % |

|

|

| (1) | | For the six months ended March 31, 2006 (unaudited). |

| (2) | | For the period October 26, 2004 (commencement of operations) to September 30, 2005. |

| (3) | | Initial public offering price of $20.00 per share less offering costs and sales load totaling $0.94 per share. |

| (4) | | The total return calculation assumes that dividends are reinvested in accordance with the Fund’s dividend reinvestment plan. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

| (6) | | The investment manager voluntarily waived a portion of its fees. |

See Notes to Financial Statements.

20 Salomon Brothers Variable Rate Strategic Fund Inc. 2006 Semi-Annual Report

Notes to Financial Statements (unaudited)

| 1. | Organization and Significant Accounting Policies |

The Salomon Brothers Variable Rate Strategic Fund Inc. (the “Fund”) was incorporated in Maryland on August 3, 2004 and is registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended, (the “1940 Act”). The Board of Directors authorized 100 million shares of $0.001 par value common stock. The Fund’s primary investment objective is to maintain a high level of current income.

The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”). Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ.