1 1 Mining the Past…Powering the Future April 7, 2008 Howard Weil 36th Annual Energy Conference New Orleans, LA Exhibit 99.1 |

2 Statements in this presentation which are not statements of historical fact are “forward-looking statements” within the “safe harbor” provision of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on the information available to, and the expectations and assumptions deemed reasonable by, Foundation Coal Holdings, Inc. at the time this presentation was made. Although Foundation Coal Holdings, Inc. believes that the assumptions underlying such statements are reasonable, it can give no assurance that they will be attained. Factors that could cause actual results to differ materially from expectations include the risks detailed under the section “Risk Factors” in the company’s Form 10-K filed with the Securities and Exchange Commission. Also, this presentation contains certain financial measures, such as EBITDA. As required by Securities and Exchange Commission Regulation G, reconciliations of these measures to figures reported in Foundation Coal’s consolidated financial statements are provided in the company’s annual and quarterly earnings releases. FORWARD-LOOKING STATEMENTS AND RECONCILIATION OF NON-GAAP MEASURES |

3 PRESENTATION OVERVIEW Industry Overview Global Demand Growth U.S. Market Projections Foundation Coal Investment Highlights Strong Safety Record Attractive Asset Base Positive Outlook for Organic Growth Significant Leverage to Rising Price Environment Track Record of Financial Performance Summary |

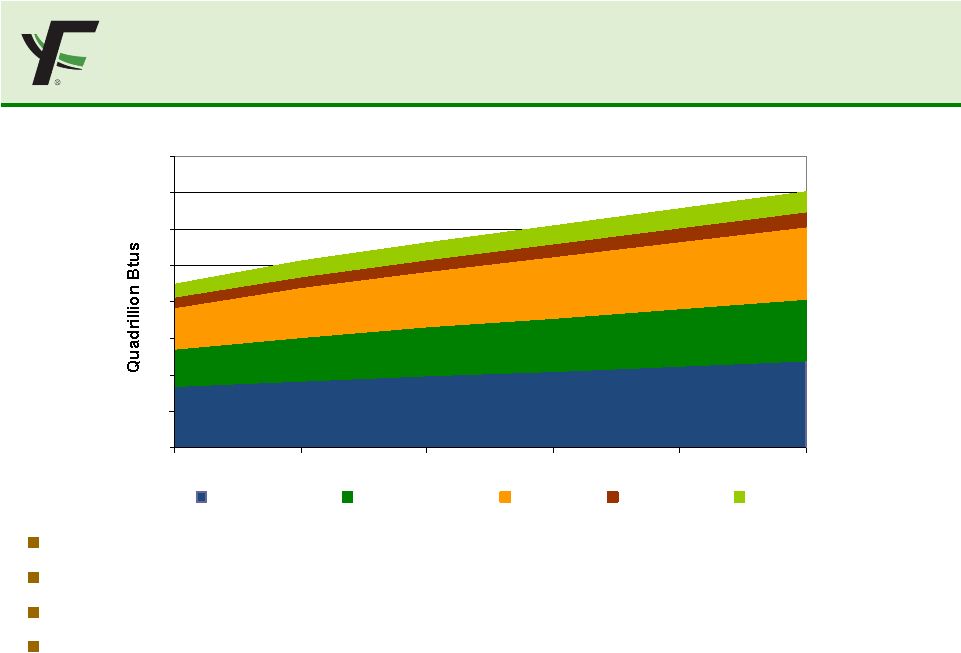

4 WORLD ENERGY CONSUMPTION EXPECTED TO INCREASE DRAMATICALLY Source: Energy Information Administration, International Energy Outlook 2007 Economic & population growth expected to drive energy consumption up 57% by 2030 Coal demand is expected to increase 72% from 2004 to 2030 Demand is expected to grow 132% in China, and 87% in India, from 2004 to 2030 Together, China and India accounted for 42% of 2004 demand, rising to 54% by 2030 (contributing 71% of all growth) World Primary Energy Consumption 0 100 200 300 400 500 600 700 800 2004 2010 2015 2020 2025 2030 Petroleum Natural Gas Coal Nuclear Other |

5 CATALYSTS DRIVING THE MARKET Current Market Fundamentals • Favorable US currency • Relatively high natural gas prices • Favorable ocean freight rates • Close to normal domestic stockpiles • Lead time to increase U.S. production Recent Events Have Accelerated International Market Tightness • China – Projected net importer beginning in 2008 • China – Curtailed coal exports through February/March • India – Utility stockpiles low • Venezuela – State-ordered contract re-pricing • Australia – January/February monsoons resulted in multiple force majeures • South Africa – Production issues, low utility inventories & power outages |

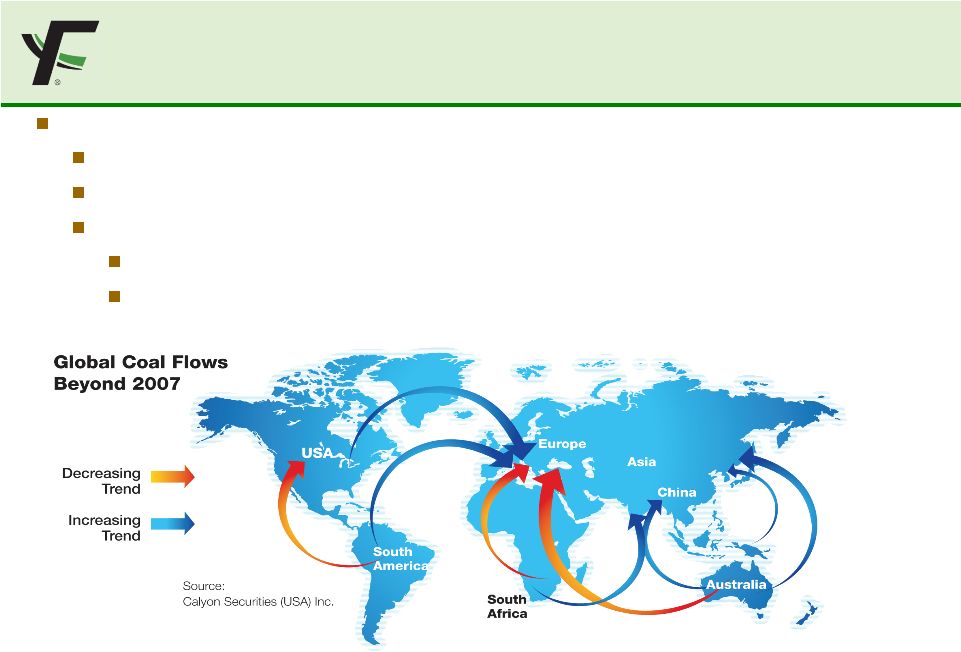

6 IMPACT OF INCREASING GLOBAL DEMAND Asian demand is key Asia naturally draws from Australia, but export growth is overwhelming infrastructure Asia now drawing thermal coal from South Africa, historically a supplier for Europe Europe is relying increasingly on coal from the Americas U.S. exports in 2007 were 59.1mm tons, a 19% increase YOY U.S. exports should rise, tightening supply: 75-80mm tons projected in 2008 Source: Simmons & Company International Research and Various News Reports |

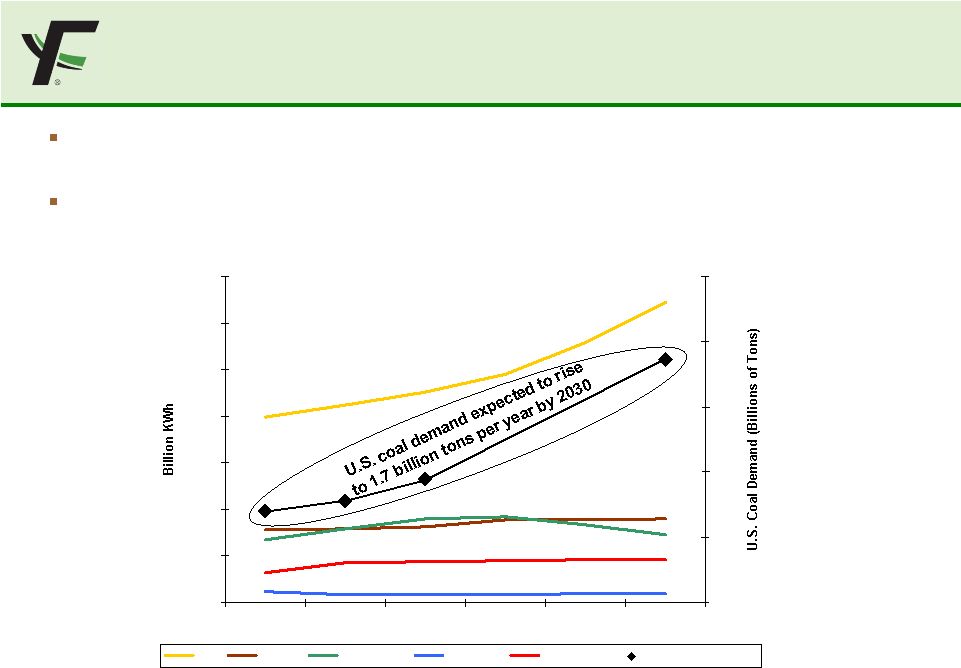

7 U.S. ELECTRICITY GENERATION Source: DOE and Energy Information Administration, Annual Energy Outlook 2007, Reference Case Coal now provides 50% of electricity generation in the U.S., anticipated to increase to approximately 60% in 2030 U.S. coal demand is expected to rise from 1.1 billion tons per year today to approximately 1.7 billion tons per year in 2030 0 500 1,000 1,500 2,000 2,500 3,000 3,500 2005 2010 2015 2020 2025 2030 0.75 1.00 1.25 1.50 1.75 2.00 Coal Nuclear Natural Gas Petroleum Renewables U.S. Coal Demand U.S. Electricity Generation by Source +62% |

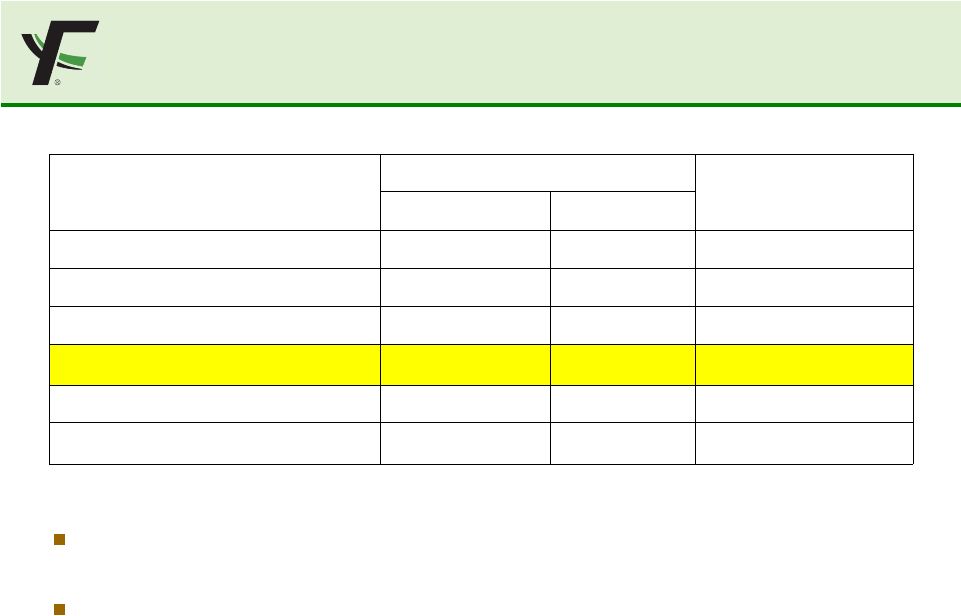

8 Source: United States Department of Energy, National Energy Technology Laboratory, “Tracking New Coal-Fired Power Plants”, December 2007 U.S. COAL-FIRED GENERATION GROWTH Despite the cancellation or postponement of some projects, the U.S. is experiencing the largest expansion of coal-fired generation in 25 years 47 projects, representing over 23GWs of new generation and 70 – 80 million tons of new annual coal demand, are moving forward 200 - 220 million 65,560 114 TOTAL 42,394 67 Announced (uncertain potential and timing) 70 - 80 million 23,166 47 SUBTOTAL 6,422 13 Permitted 1,859 6 Near Construction 14,885 28 Under Construction Consumption (Tons) Capacity (MW) Number of Plants Implied Annual December 2007 Report |

9 PRICES HAVE INCREASED IN ALL REGIONS Northern Appalachia (NAPP) More scrubbers Increasing exports (crossover Pittsburgh #8) Lead times for production expansion Coal inventories at utilities served by NAPP Central Appalachia (CAPP) Regulation threatens to impede future production Strong worldwide demand for met coal Powder River Basin (PRB) Most new coal-fired generation under construction is in the Midwest and West Western coal reaching wider market in part due to the pull of Eastern coal exports PRB prices tend to follow and lag Eastern coal prices—beginning to show strength 19 34 34 10 16 0 6 12 18 24 30 36 2008 2009 2010 2011 2012 Newly Scrubbed Capacity (GWs) coal currently well below the 5-year average |

10 FOUNDATION COAL OVERVIEW |

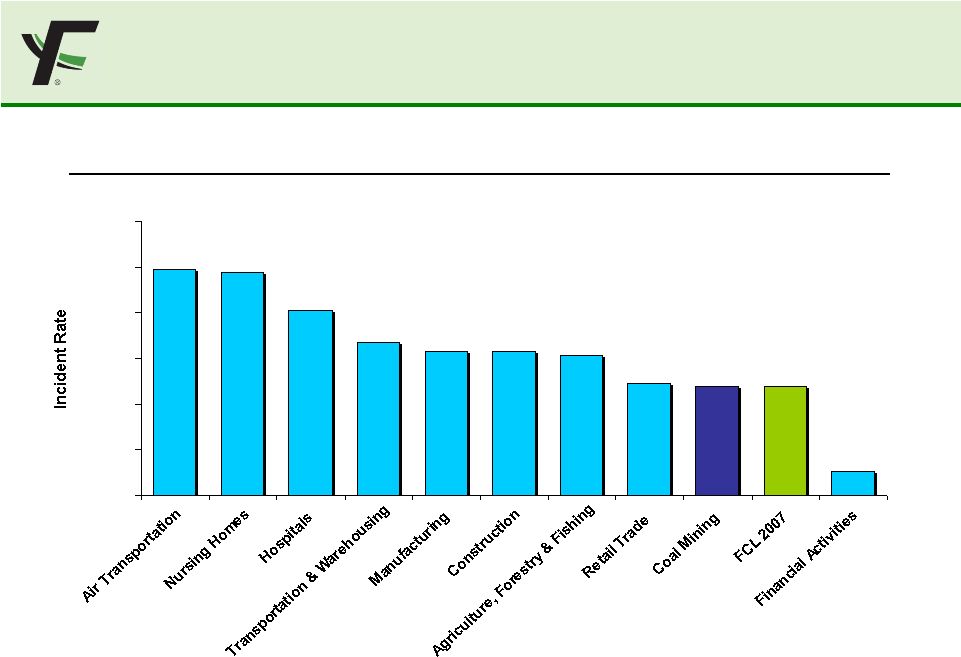

11 A COMMITMENT TO SAFETY Incident Rates of Non-Fatal Occupational Injuries by Industrial Category Source: Bureau of Labor Statistics, 2006; Foundation Coal 2007 0 2 4 6 8 10 12 |

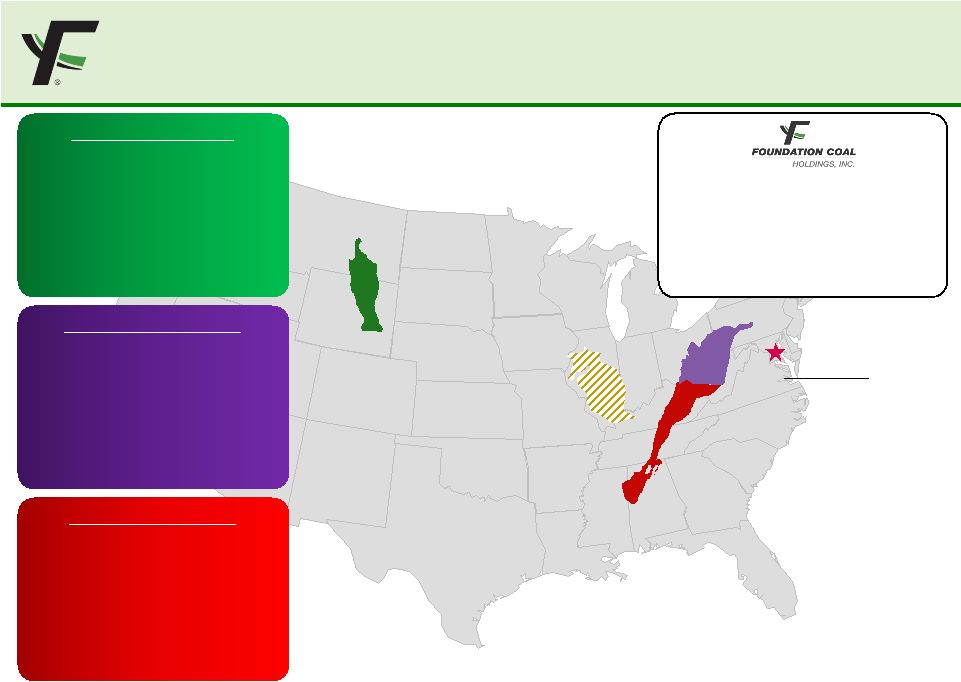

12 Headquarters Baltimore, MD Notes: Shipments, sales, average realization for the twelve months ended 12/31/07, reserve figures as of 2/25/08. (1) Shipments, sales, and average realization include tons that were purchased and resold. (2) Includes Illinois Basin Powder River Basin (PRB) Production Capacity (tons MM) 55.0 LTM Shipments (tons MM) 51.6 LTM Sales ($ MM) $468.9 LTM Avg. Realization ($/Ton) $9.08 Reserves (tons MM) 844 Btu Low Sulfur Content Compliance Central Appalachia (CAPP) Production Capacity (tons MM) 7.0 LTM Shipments (tons MM) 8.5 LTM Sales ($ MM) $446.2 LTM Avg. Realization ($/Ton) $52.60 Reserves (tons MM) 191 Btu High Sulfur Content Compliance & Low Northern Appalachia (NAPP) Production Capacity (tons MM) 14.0 LTM Shipments (tons MM) 13.0 LTM Sales ($ MM) $521.6 LTM Avg. Realization ($/Ton) $40.14 Reserves (tons MM) 742 Btu High Sulfur Content Medium Production Capacity (tons MM) 76.0 LTM Shipments 1,2 (tons MM) 73.6 LTM Sales 1,2 ($ MM) $1,453 LTM Avg. Realization 1,2 ($/Ton) $19.74 Reserves² (tons MM) 1,840 Illinois Basin Reserves ~ 65 MM tons DIVERSIFIED OPERATIONS |

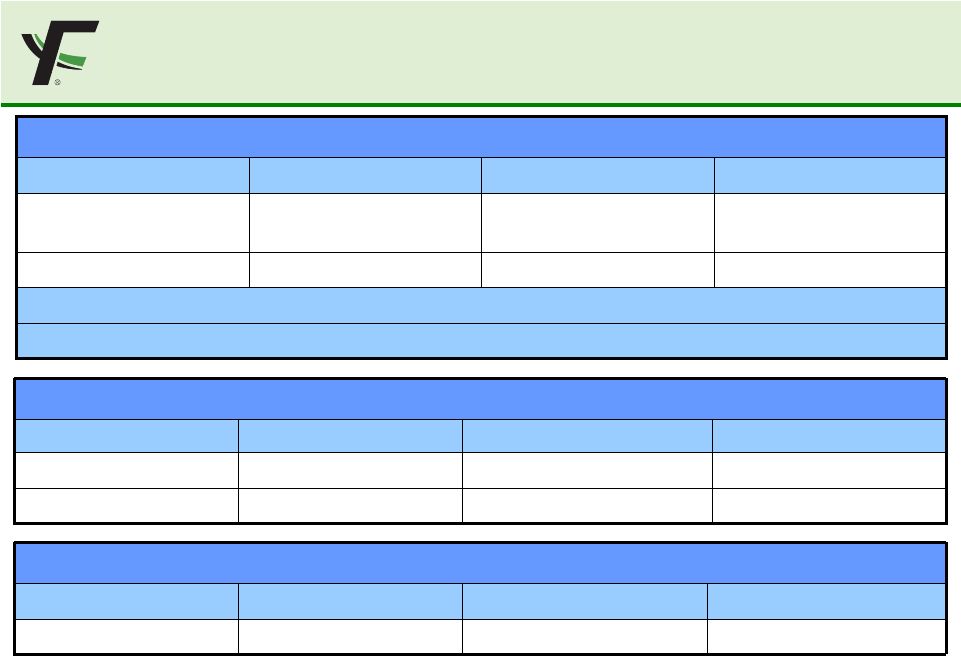

13 Belle Ayr LBA Eagle Butte LBA Phase III (2011) Phase I & II (completed 2006-2007) Wyoming Operations Powder River Basin Powder River Basin $180 Million 2008 Sale (Successful) 255 Million Tons ~ $100 Million 65 MTPY 10 Cost of Expansion Annual Capacity Expansion (MM tons/yr) 200 Million Tons 10 ?? 2009 Sale 55 MTPY Harts Creek Mine Central Appalachia Central Appalachia ~ 64 Million Current Reserve (tons) Capital Expenditure Annual Production ~ $120 Million 2 MTPY (New) Freeport (Steam/Met) Foundation Mine Northern Appalachia Northern Appalachia ~ $400 Million 7 – 14 MTPY (potential 21) ~ 420 Million ~ 68 Million Current Reserve (tons) Capital Expenditure Annual Production ~ $300 Million 2 – 3 MTPY (New) FUTURE PRODUCTION POTENTIAL |

14 RECENT SALES ACTIVITY REFLECTIVE OF CURRENT MARKET TIGHTNESS Significant RFP activity during 1Q08 among Eastern utilities Customers signing long-term contracts, especially in the East Strong $200+ spot pricing realized on limited volume of CAPP met coal during 1Q08 Modest volume of Northern Appalachian Pittsburgh #8 seam coal sold into met market during 1Q08 Significant increase in international requests for met coal during 1Q08 Evidence of supply shortage on the Norfolk Southern Uptick in PRB test burns |

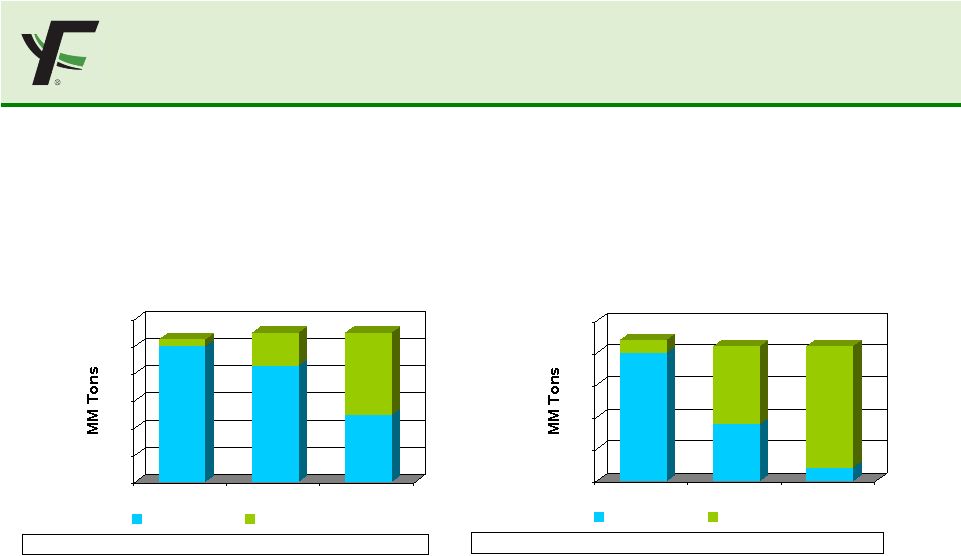

15 PROVEN MARKET STRATEGY PROVIDES OPPORTUNITY IN RISING PRICE ENVIRONMENT * Midpoint of 2/14/08 coal shipment guidance Foundation is poised to benefit from significant open positions in 2009 and 2010, particularly in the East, relative to the peer group 52.5MM* 55MM* 55MM* West (Powder River Basin) Avg. realization** $9.95 $10.18 $10.55 50 (95%) 3 (5%) 43 (78%) 12 (22%) 25 (45%) 30 (55%) 0 10 20 30 40 50 60 2008 2009 2010 Priced Tons Unpriced Tons Avg. realization** $46.99 22MM* 21MM* 21MM* East (Central & Northern App.) $44.62 $47.24 20 (91%) 2 (9%) 9 (42%) 12 (58%) 2 (10%) 19 (90%) 0 5 10 15 20 25 2008 2009 2010 Priced Tons Unpriced Tons ** Average realization per ton for priced tons |

16 UNPRICED TONS & RECENT SPOT PRICES Note: recent prices as reported in Platts Coal Trader $12 $75 $85 $140+ $0 $50 $100 $150 PRB 8400 NAPP Steam CAPP Steam Capp Met Recent Spot Prices Per Ton • Significant unpriced tons in 2009 and 2010 enable FCL to benefit from the strong pricing environment • Most unpriced tons are uncommitted and open to pricing at today’s market • For comparative purposes, priced tons in the East in 2009 & 2010 carry embedded average realizations per ton in the $45 - $47 range 2.6 2.0 12.1 12.2 30.3 18.9 0 12 24 36 2008 2009 2010 Unpriced Tons by Year West (PRB) East (Central & Northern App.) |

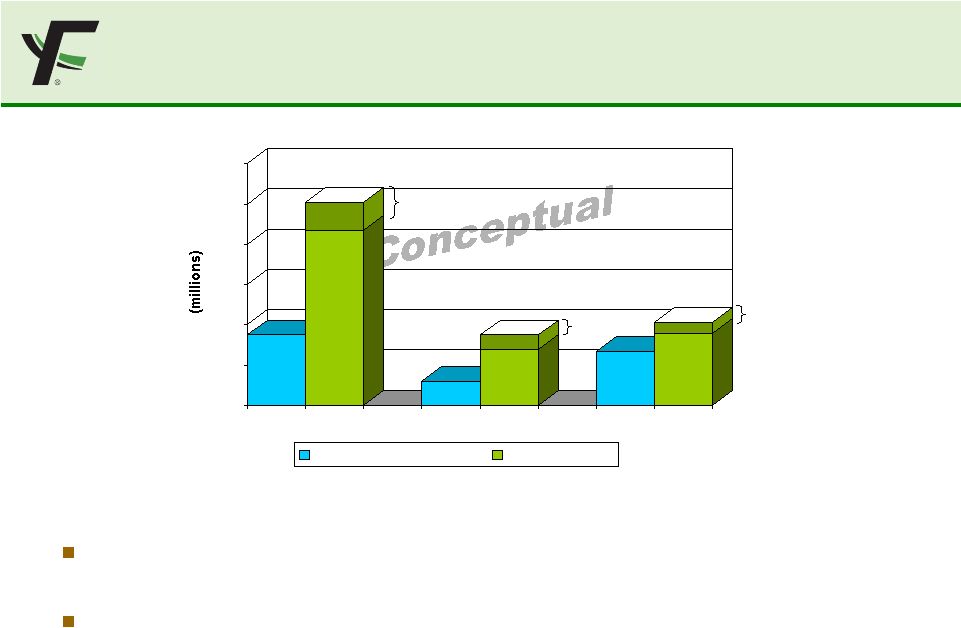

17 SIGNIFICANT EBITDA OPPORTUNITY Tremendous EBITDA potential exists assuming all unpriced and uncommitted tons are able to be contracted at current prices At current prices, NAPP conceptually has substantial upside NAPP CAPP PRB Note: 2007 amounts reflect adjusted EBITDA as defined in our bank credit agreement for all production regions, but do not include the adjusted EBITDA impact of the “other” segment. Hashed sections represent likely ranges of possible outcomes 175 60 133 $0 $100 $200 $300 $400 $500 $600 2007 Adjusted EBITDA 2010 Potential |

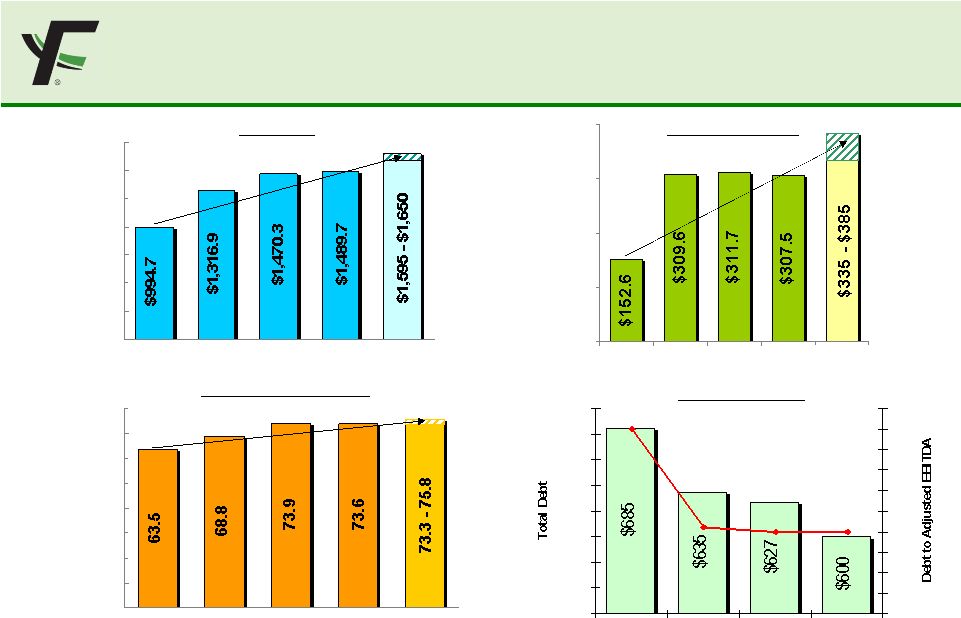

18 0 250 500 750 1,000 1,250 1,500 1,750 2004 2005 2006 2007 2008 0 100 200 300 400 2004 2005 2006 2007 2008 Notes: In millions, except percentage increases and debt to adjusted EBITDA ratios 2004 data on a non-GAAP combined basis 2005-07 data reflect results for successor company 2008 data per 2/14/08 guidance Percentage increases based on mid-point of 2/14/08 guidance Revenues Adjusted EBITDA 0 10 20 30 40 50 60 70 80 2004 2005 2006 2007 2008 Coal Shipments (tons) 4.5 2.1 2.0 2.0 540 560 580 600 620 640 660 680 700 Q4 04 Q4 05 Q4 06 Q4 07 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 Debt Repayment + 63% + 136% + 17% KEY PERFORMANCE HIGHLIGHTS |

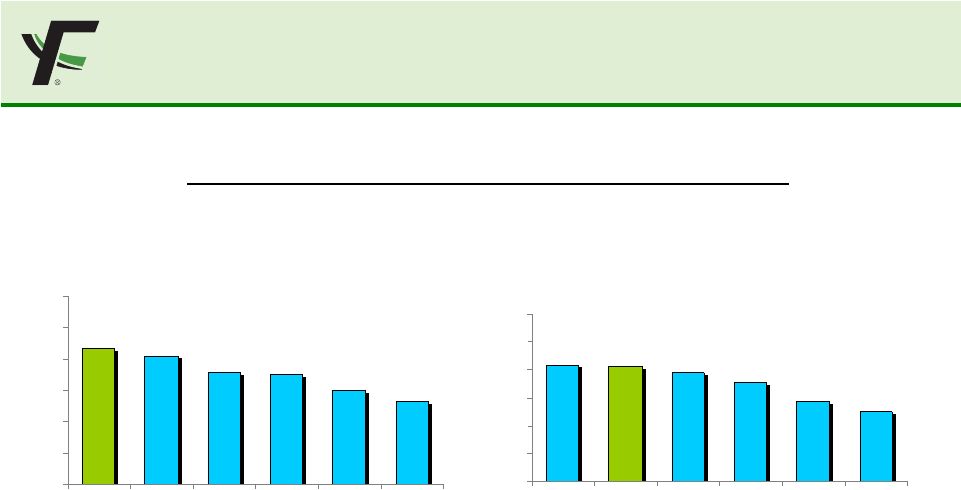

19 INDUSTRY-LEADING MARGINS Calendar Year 2007 20.9% 20.6% 19.5% 17.6% 14.4% 12.5% 0 5 10 15 20 25 30 A FCL C B D* E Adjusted EBITDA to Revenue Margin—FCL vs. Peers Note: * Excludes margin from non-coal related core assets Source: Public company filings and press releases; EBITDA adjusted for unusual and one-time items Three-Year Average (2005-07) 21.7% 20.5% 17.8% 17.5% 15.0% 13.2% 0 5 10 15 20 25 30 FCL A B C D* E |

20 SUMMARY OF INVESTMENT HIGHLIGHTS Excellent Industry Position Among the largest producers – fourth by volume Nationally diversified – only producer with a major presence in NAPP & PRB Strong Financial Performance Consistent out-performance: leading adjusted EBITDA margins 2007 adjusted EBITDA in-line with beginning-of-year guidance Low 2.0x debt/Adjusted EBITDA ratio provides significant financial flexibility Current Strategy Continuing to execute our successful marketing strategy--leveraging our significant 2009 & 2010 unpriced positions Delivering future growth by: Expanding production in 2008 in the high margin NAPP region Growing organic production approximately 20% near-term, with opportunities for increased met production and export Selectively pursuing growth through acquisition Managing our costs to maintain our position as a low-cost provider Attractive Valuation* 2009 EV/EBITDA of 6.0x for FCL versus 8.0x for other companies producing greater than 50 million tons per year * Calculated using FirstCall consensus 2009 EBITDA estimates and enterprise values based on April 2, 2008 closing prices. |

Mining the Past…Powering the Future |