Table of Contents

As filed with the Securities and Exchange Commission on December 2, 2010

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

HOST HOTELS & RESORTS, L.P.

(Exact name of registrant as specified in its charter)

| Delaware | 7011 | 52-2095412 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (IRS Employer Identification Number) |

For Co-Registrants, see “Table of Co-Registrants” on following page.

6903 Rockledge Drive, Suite 1500

Bethesda, Maryland 20817

(240) 744-1000

(Address, including zip code, telephone number, including area code, of registrant’s principal executive offices)

Elizabeth A. Abdoo

Executive Vice President, Secretary and

General Counsel

6903 Rockledge Drive, Suite 1500

Bethesda, Maryland 20817

(240) 744-1000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Scott C. Herlihy

Latham & Watkins LLP

555 Eleventh Street, NW, Suite 1000

Washington, DC 20004

(202) 637-2200

Approximate date of commencement of proposed sale to the public: as soon as practicable after this Registration Statement becomes effective.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

Title of each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price Per Note(1) | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee | ||||

6% Series V Senior Notes due 2020 (2) | $500,000,000 | 100.0% | $500,000,000 | $35,650 | ||||

Guarantees of the 6% Series V Senior Notes due 2020 (3) | N/A | N/A | N/A | N/A | ||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(f) of the Securities Act. |

| (2) | The 6% Series V Senior Notes due 2020 will be the obligations of Host Hotels & Resorts, L.P. |

| (3) | Each of the Co-Registrants listed on the “Table of Co-Registrants” on the following page will guarantee on an unconditional basis the obligations of Host Hotels & Resorts, L.P. under the 6% Series V Senior Notes due 2020. Pursuant to Rule 457(n), no additional registration fee is being paid in respect of the guarantees. The guarantees are not paid separately. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Table of Co-Registrants

Name | State of other Jurisdiction of Formation | Primary Standard Industrial Classification Code Number | IRS Employer Number | |||||||

HMH Rivers, L.P. | Delaware | 7011 | 52-2126158 | |||||||

HMH Marina LLC | Delaware | 7011 | 26-4511519 | |||||||

HMC SBM Two LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC PLP LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Retirement Properties, L.P. | Delaware | 7011 | 52-2126159 | |||||||

HMH Pentagon LP | Delaware | 7011 | 52-2095412 | |||||||

Airport Hotels LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Capital Resources LP | Delaware | 7011 | 26-4510555 | |||||||

YBG Associates LP | Delaware | 7011 | 52-2059377 | |||||||

Host Park Ridge LLC | Delaware | 7011 | 52-2095412 | |||||||

Host of Boston, Ltd. | Massachusetts | 7011 | 59-0164700 | |||||||

Host of Houston, Ltd. | Texas | 7011 | 52-1874039 | |||||||

Host of Houston 1979 LP | Delaware | 7011 | 95-3552476 | |||||||

Philadelphia Airport Hotel LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Suites LLC | Delaware | 7011 | 26-4511316 | |||||||

HMC Suites Limited Partnership | Delaware | 7011 | 52-1632307 | |||||||

Wellsford-Park Ridge HMC Hotel Limited Partnership | Delaware | 7011 | 52-6323494 | |||||||

HMC Burlingame LLC | Delaware | 7011 | 26-4510338 | |||||||

HMC Grand LP | Delaware | 7011 | 52-2285954 | |||||||

HMC Hotel Development LP | Delaware | 7011 | 52-2095412 | |||||||

HMC Mexpark LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Polanco LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC NGL LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC OLS I L.P. | Delaware | 7011 | 52-2095412 | |||||||

HMC Seattle LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Swiss GP LLC | Delaware | 7011 | 52-2095412 | |||||||

HMH Restaurants LP | Delaware | 7011 | 26-4511601 | |||||||

HMH Rivers LLC | Delaware | 7011 | 52-2095412 | |||||||

HMH WTC LLC | Delaware | 7011 | 52-2095412 | |||||||

Host La Jolla LLC | Delaware | 7011 | 52-2095412 | |||||||

City Center Hotel Limited Partnership | Minnesota | 7011 | 41-1449758 | |||||||

PM Financial LLC | Delaware | 7011 | 52-2095412 | |||||||

PM Financial LP | Delaware | 7011 | 52-2131022 | |||||||

HMC Chicago LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Desert LLC | Delaware | 7011 | 26-4510605 | |||||||

HMC Diversified LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Properties I LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Potomac LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Manhattan Beach LLC | Delaware | 7011 | 26-4510718 | |||||||

Chesapeake Hotel Limited Partnership | Delaware | 7011 | 52-1373476 | |||||||

HMH General Partner Holdings LLC | Delaware | 7011 | 26-4521901 | |||||||

S.D. Hotels LLC | Delaware | 7011 | 26-4522361 | |||||||

HMC Gateway LP | Delaware | 7011 | 52-2095412 | |||||||

HMC Market Street LLC | Delaware | 7011 | 52-2095412 | |||||||

New Market Street LP | Delaware | 7011 | 52-2131023 | |||||||

Host Times Square LP | Delaware | 7011 | 52-2095412 | |||||||

Times Square GP LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Atlanta LLC | Delaware | 7011 | 52-2095412 | |||||||

Ivy Street LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Georgia LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC SFO LP | Delaware | 7011 | 26-4511255 | |||||||

Market Street Host LLC | Delaware | 7011 | 52-2091669 | |||||||

HMC Property Leasing LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Host Restaurants LLC | Delaware | 7011 | 52-2095412 | |||||||

Durbin LLC | Delaware | 7011 | 52-2095412 | |||||||

Table of Contents

Name | State of other Jurisdiction of Formation | Primary Standard Industrial Classification Code Number | IRS Employer Number | |||||||

HMC HT LP | Delaware | 7011 | 52-2095412 | |||||||

HMC OLS I LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC OLS II L.P. | Delaware | 7011 | 52-2095412 | |||||||

HMC/Interstate Manhattan Beach, L.P. | Delaware | 7011 | 52-2033807 | |||||||

Ameliatel LP | Delaware | 7011 | 58-1861162 | |||||||

HMC Amelia II LLC | Delaware | 7011 | 52-2095412 | |||||||

Rockledge Hotel LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Copley LP | Delaware | 7011 | 52-2095412 | |||||||

HMC Headhouse Funding LLC | Delaware | 7011 | 52-2095412 | |||||||

Ivy Street Hopewell LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC Diversified American Hotels, L.P. | Delaware | 7011 | 52-1646207 | |||||||

Potomac Hotel Limited Partnership | Delaware | 7011 | 52-1240223 | |||||||

HMC AP GP LLC | Delaware | 7011 | 52-2171352 | |||||||

HMC AP LP | Delaware | 7011 | 52-2171371 | |||||||

HMC AP Canada Company | Nova Scotia | 7011 | 89-8505540 | |||||||

HMC Toronto Airport GP LLC | Delaware | 7011 | 52-2187400 | |||||||

HMC Toronto Airport LP | Delaware | 7011 | 52-2187401 | |||||||

HMC Toronto EC GP LLC | Delaware | 7011 | 52-2187402 | |||||||

HMC Toronto EC LP | Delaware | 7011 | 52-2187404 | |||||||

HMC Charlotte GP LLC | Delaware | 7011 | 52-2171369 | |||||||

HMC Charlotte LP | Delaware | 7011 | 52-2171370 | |||||||

HMC Charlotte (Calgary) Company | Nova Scotia | 7011 | 86-9552752 | |||||||

Calgary Charlotte Holdings Company | Nova Scotia | 7011 | 98-0588872 | |||||||

HMC Grace (Calgary) Company | Nova Scotia | 7011 | 87-1258026 | |||||||

HMC Maui LP | Delaware | 7011 | 52-2095412 | |||||||

Calgary Charlotte Partnership | Alberta | 7011 | 98-0588875 | |||||||

HMC Chicago Lakefront LLC | Delaware | 7011 | 52-2095412 | |||||||

HMC East Side LLC | Delaware | 7011 | 52-2171365 | |||||||

HMC Kea Lani LP | Delaware | 7011 | 52-2095412 | |||||||

East Side Hotel Associates, L.P. | Delaware | 7011 | 52-1892518 | |||||||

HMC O’Hare Suites Ground LP | Delaware | 7011 | 52-2095412 | |||||||

HMC Toronto Air Company | Nova Scotia | 7011 | 89-4596683 | |||||||

HMC Toronto EC Company | Nova Scotia | 7011 | 12-1597207 | |||||||

HMC Lenox LP | Delaware | 7011 | 52-2095412 | |||||||

Host Realty Partnership, L.P. | Delaware | 7011 | 95-4509413 | |||||||

Host Houston Briar Oaks, L.P. | Delaware | 7011 | 86-0901342 | |||||||

Cincinnati Plaza LLC | Delaware | 7011 | 91-1128920 | |||||||

Host Cincinnati II LLC | Delaware | 7011 | 86-0944822 | |||||||

Host Cincinnati Hotel LLC | Delaware | 7011 | 86-0944821 | |||||||

Host Financing LLC | Delaware | 7011 | 86-0834172 | |||||||

Host Fourth Avenue LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Indianapolis I LP | Delaware | 7011 | 86-0877687 | |||||||

Host Los Angeles LP | Delaware | 7011 | 95-4591657 | |||||||

Host Mission Hills II LLC | Delaware | 7011 | 86-0944817 | |||||||

Host Mission Hills Hotel LP | Delaware | 7011 | 86-0944816 | |||||||

Host Needham II LLC | Delaware | 7011 | 86-0944813 | |||||||

Host Needham Hotel LP | Delaware | 7011 | 86-0944812 | |||||||

Host Realty LLC | Delaware | 7011 | 58-2437600 | |||||||

Host Realty Hotel LLC | Delaware | 7011 | 58-2437602 | |||||||

Host Waltham II LLC | Delaware | 7011 | 86-0944811 | |||||||

Host Waltham Hotel LP | Delaware | 7011 | 86-0944810 | |||||||

HST LT LLC | Delaware | 7011 | 52-2095412 | |||||||

HST I LLC | Delaware | 7011 | 52-2095412 | |||||||

South Coast Host Hotel LP | Delaware | 7011 | 91-0902540 | |||||||

Starlex LP | Delaware | 7011 | 95-4534810 | |||||||

Airport Hotels Houston LLC | Delaware | 7011 | 52-2095412 | |||||||

BRE/Swiss LP | Delaware | 7011 | 13-3955642 | |||||||

Table of Contents

Name | State of other Jurisdiction of Formation | Primary Standard Industrial Classification Code Number | IRS Employer Number | |||||||

HHR Assets LLC | Delaware | 7011 | 52-2095412 | |||||||

HHR Harbor Beach LLC | Delaware | 7011 | 52-2095412 | |||||||

HHR Holdings Cooperatief U.A. | Netherlands | 7011 | 52-2095412 | |||||||

HHR Lauderdale Beach Limited Partnership | Delaware | 7011 | 52-2095412 | |||||||

HHR Singer Island GP LLC | Delaware | 7011 | 52-2095412 | |||||||

HHR Singer Island Limited Partnership | Delaware | 7011 | 52-2095412 | |||||||

HHR WRN GP LLC | Delaware | 7011 | 52-2095412 | |||||||

HHR WRN Limited Partnership | Delaware | 7011 | 52-2095412 | |||||||

HMC Cambridge LP | Delaware | 7011 | 52-2095412 | |||||||

HMC McDowell LP | Delaware | 7011 | 90-0197916 | |||||||

HMC Reston LP | Delaware | 7011 | 26-3876666 | |||||||

Host Atlanta Perimeter Ground GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Atlanta Perimeter Ground LP | Delaware | 7011 | 52-2095412 | |||||||

Host Cambridge GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Capitol Hill LLC | Delaware | 7011 | 20-5304861 | |||||||

Host City Center GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Copley GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Dallas Quorum Ground GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Dallas Quorum Ground LP | Delaware | 7011 | 52-2095412 | |||||||

Host GH Atlanta GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Grand GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Indianapolis GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Indianapolis Hotel Member LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Indianapolis LP | Delaware | 7011 | 52-2095412 | |||||||

Host Kea Lani GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Kierland GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Kierland LP | Delaware | 7011 | 52-2095412 | |||||||

Host Lenox Land GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Los Angeles GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Maui GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host McDowell GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Moscone GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host NY Downtown GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host O’Hare Suites Ground GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host OP BN GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Pentagon GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Restaurants GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Reston GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host SFO GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host South Coast GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Tampa GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host Times Square GP LLC | Delaware | 7011 | 52-2095412 | |||||||

Host WNY GP LLC | Delaware | 7011 | 52-2095412 | |||||||

IHP Holdings Partnership LP | Pennsylvania | 7011 | 23-2906092 | |||||||

Pacific Gateway, Ltd. | California | 7011 | 33-0093873 | |||||||

HHR Rio Holdings LLC | Delaware | 7011 | 52-2095412 | |||||||

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated December 2, 2010

Prospectus

Offer to Exchange all Outstanding

6% Series U Senior Notes due 2020

for

6% Series V Senior Notes due 2020

of

HOST HOTELS & RESORTS, L.P.

We are offering to exchange all of our outstanding 6% Series U senior notes for our 6% Series V senior notes. The terms of the Series V senior notes are substantially identical to the terms of the Series U senior notes except that the Series V senior notes are registered under the Securities Act of 1933, as amended, and are therefore freely transferable. The Series U senior notes were issued on October 25, 2010 and, as of the date of this prospectus, an aggregate principal amount of $500 million is outstanding.

Please consider the following:

| • | Our offer to exchange the notes expires at 5:00 p.m., New York City time, on , 2011, unless extended. |

| • | You should carefully review the procedures for tendering the Series U senior notes. If you do not follow those procedures, we may not exchange your Series U senior notes for Series V senior notes. |

| • | We will not receive any proceeds from the exchange offer. |

| • | If you fail to tender your Series U senior notes, you will continue to hold unregistered securities and your ability to transfer them could be adversely affected. |

| • | There is currently no public market for the Series V senior notes. We do not intend to list the Series V senior notes on any securities exchange. Therefore, we do not anticipate that an active public market for these notes will develop. |

Information about the Series V senior notes:

| • | The notes will mature on November 1, 2020. We will pay interest on the notes semi-annually in cash in arrears at the rate of 6% per year payable on February 1 and August 1, commencing February 1, 2011. |

| • | The notes are equal in right of payment with all of our unsubordinated indebtedness and senior to all of our subordinated obligations, subject to certain limitations set forth in the section entitled “Description of Series V Senior Notes.” For further information on ranking, see also the section entitled “Risk Factors.” |

| • | The Series V senior notes will be guaranteed by certain of our subsidiaries, comprising all of our subsidiaries that have also guaranteed our credit facility and other indebtedness. |

| • | As security for the notes, we have pledged the common equity interests of those of our direct and indirect subsidiaries which also secure, on an equal and ratable basis, our credit facility, approximately $3.8 billion of our other outstanding existing senior notes (excluding our Series U senior notes) as of November 30, 2010 and certain other indebtedness. |

Broker-dealers receiving Series V senior notes in exchange for Series U senior notes acquired for their own account through market-making or other trading activities must deliver a prospectus in any resale of the Series V senior notes.

Investing in the Series V senior notes involves risks. See “Risk Factors” beginning on page 9.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , .

Table of Contents

Each broker-dealer that receives the Series V senior notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such Series V senior notes. The letter of transmittal delivered with this prospectus states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act of 1933, as amended (the “Securities Act”). This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of Series V senior notes received in exchange for Series U senior notes where such Series U senior notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period ending on the earlier to occur of (1) the date when all the Series V senior notes held by a broker-dealer have been sold and (2) 180 days after consummation of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See “Plan of Distribution.”

We have not authorized any dealer, salesman or other person to give any information or to make any representation other than those contained in this prospectus. You must not rely upon any information or representation not contained in this prospectus as if we had authorized it. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities other than the registered securities to which it relates, nor does this prospectus constitute an offer to sell or a solicitation of an offer to buy securities in any jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such jurisdiction.

This prospectus contains registered trademarks that are the exclusive property of their respective owners, which are companies other than us, including Marriott®, Ritz-Carlton®, Hyatt®, Four Seasons®, Fairmont®, Hilton®, Westin®, Sheraton®, W®, The Luxury Collection®, St. Regis®, Swissôtel®, Accor®, Le Meridien® and Delta®. None of the owners of these trademarks, their affiliates or any of their respective officers, directors, agents or employees, is an issuer or underwriter of the Series V senior notes being offered. In addition, none of such persons has or will have any responsibility or liability for any information contained in this prospectus.

| Page | ||||

| 1 | ||||

| 9 | ||||

| 27 | ||||

| 29 | ||||

| 36 | ||||

Ratios of Earnings to Fixed Charges and Preferred OP Unit Distributions | 36 | |||

| 37 | ||||

| 39 | ||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 40 | |||

| 93 | ||||

| 95 | ||||

| 113 | ||||

| 119 | ||||

| 126 | ||||

| 128 | ||||

| 143 | ||||

Security Ownership of Certain Beneficial Owners and Management | 155 | |||

| 158 | ||||

| 162 | ||||

| 169 | ||||

| 221 | ||||

| 222 | ||||

| 223 | ||||

| 223 | ||||

| 223 | ||||

| F-1 | ||||

i

Table of Contents

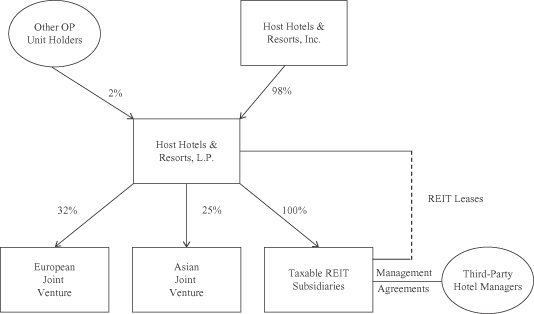

This summary highlights certain information contained in this prospectus, but it may not contain all of the information that is important to you. This summary is qualified in its entirety by the more detailed information and financial statements, including the notes to those financial statements, that are part of this prospectus. You should carefully consider the information contained in this prospectus, including the information set forth under the heading “Risk Factors”, beginning on page 9 of this prospectus. Host Hotels & Resorts, L.P. is a Delaware limited partnership operating through an umbrella partnership structure with Host Hotels & Resorts, Inc., a Maryland corporation (“Host REIT”), as its sole general partner. Together, we operate as a self-managed and self-administered real estate investment trust, or REIT. In addition to being our sole general partner, Host REIT holds approximately 98% of our partnership interests. Except as the context may otherwise require, references to “Host REIT” are to Host Hotels & Resorts, Inc., and references to “we,” “us,” and “our” or “Host L.P.” are to Host Hotels & Resorts, L.P. and its consolidated subsidiaries. References to “senior notes” herein include the senior notes outstanding under the indenture under which the Series U senior notes were issued and under which the Series V senior notes will be issued and any future senior notes that we may issue under that indenture, including the Exchangeable Senior Debentures (as defined below).

Company Overview

Host REIT is the largest lodging real estate investment trust and one of the largest owners of luxury and upper upscale hotels, which are held by Host L.P. As of November 30, 2010, our lodging portfolio consisted of 113 luxury and upper upscale hotels containing approximately 62,000 rooms. Substantially all of our portfolio is located in the U.S. and is geographically diverse with hotels in most of the major metropolitan areas in 25 states, Washington, D.C., Toronto and Calgary, Canada, Mexico City, Mexico, Santiago, Chile, London, England and Rio de Janeiro, Brazil. Additionally, we own a 32.1% interest in a European joint venture that owns 11 luxury and upper upscale hotels containing approximately 3,500 rooms located in cities in Italy, Spain, Poland, Belgium, The Netherlands and the United Kingdom. We are the general partner of the joint venture and act as asset manager for these hotels. We also own a 25% interest in an Asian joint venture that currently owns no hotels, but has reached an agreement to develop seven properties in India in a joint venture with Accor S.A. and InterGlobe Enterprises Limited.

Corporate Information

The address of our principal executive office is 6903 Rockledge Drive, Suite 1500, Bethesda, Maryland, 20817. Our phone number is (240) 744-1000. Host REIT’s Internet website address is www.hosthotels.com. The contents of Host REIT’s website are not part of this prospectus.

1

Table of Contents

THE EXCHANGE OFFER

Securities to be exchanged | On October 25, 2010 we sold $500 million in aggregate principal amount of Series U senior notes in a transaction exempt from the registration requirements of the Securities Act. The terms of the Series U senior notes and the Series V senior notes are substantially identical in all material respects, except that the Series V senior notes will be freely transferable by the holders thereof except as otherwise provided in this prospectus. |

The exchange offer | We are offering to exchange $500 million principal amount of Series U senior notes for a like principal amount of Series V senior notes. Series U senior notes may be exchanged only in multiples of $1,000 principal amount. |

Registration rights agreement | We sold the Series U senior notes on October 25, 2010 in a private placement in reliance on Section 4(2) of the Securities Act. The Series U senior notes were immediately resold by their initial purchasers in reliance on Securities Act Rule 144A. In connection with the sale, we entered into a registration rights agreement with the initial purchasers requiring us to make this exchange offer. Under the registration rights agreement, we are required to cause the registration statement, of which this prospectus forms a part, to become effective on or before the 260th day following the date on which we issued the Series U senior notes, and we are obligated to consummate the exchange offer on or before the 290th day following the issuance of the Series U senior notes. |

Expiration date | Our exchange offer will expire at 5:00 p.m., New York City time, , 2011, or at a later date and time to which we may extend it. |

Withdrawal | You may withdraw a tender of Series U senior notes pursuant to our exchange offer at any time before 5:00 p.m., New York City time, on , 2011, or such later date and time to which we extend the offer. We will return any Series U senior notes that we do not accept for exchange for any reason as soon as practicable after the expiration or termination of our exchange offer. |

Interest | Interest on the Series V senior notes will accrue from the date of the original issuance of the Series U senior notes or from the date of the last payment of interest on the Series U senior notes, whichever is later. We will not pay interest on Series U senior notes tendered and accepted for exchange. |

Conditions to our exchange offer | Our exchange offer is subject to customary conditions, which are discussed in the section entitled “The Exchange Offer.” As described in that section, we have the right to waive some of the conditions. |

2

Table of Contents

Procedures for tendering Series U senior notes | We will accept for exchange any and all Series U senior notes that are properly tendered (and not withdrawn) in the exchange offer prior to 5:00 p.m., New York City time, on , 2011. The Series V senior notes issued pursuant to our exchange offer will be delivered promptly following the expiration date. |

If you wish to accept our exchange offer, you must complete, sign and date the letter of transmittal, or a copy, in accordance with the instructions contained in this prospectus and therein, and mail or otherwise deliver the letter of transmittal, or the copy, together with the Series U senior notes and all other required documentation, to the exchange agent at the address set forth in this prospectus. If you are a person holding Series U senior notes through the Depository Trust Company (“DTC”), and wish to accept our exchange offer, you may do so pursuant to the DTC’s Automated Tender Offer Program (“ATOP”), by which you will agree to be bound by the letter of transmittal. By executing or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things:

| • | the Series V senior notes that you acquire pursuant to the exchange offer are being obtained by you in the ordinary course of your business, whether or not you are the registered holder of the Series V senior notes; |

| • | you are not engaging in and do not intend to engage in a distribution of Series V senior notes; |

| • | you do not have an arrangement or understanding with any person to participate in a distribution of Series V senior notes; and |

| • | you are not our “affiliate,” as defined under Securities Act Rule 405. |

Under the registration rights agreement we may be required to file a “shelf” registration statement for a continuous offering pursuant to Rule 415 under the Securities Act in respect of the Series U senior notes, if:

| • | we determine that we are not permitted to effect the exchange offer as contemplated by this prospectus because of any change in law or Securities and Exchange Commission policy; or |

| • | we have commenced and not consummated the exchange offer within 290 days following the date on which we issued the Series U senior notes. |

Exchange agent | The Bank of New York Mellon is serving as exchange agent in connection with the exchange offer. |

Federal income tax considerations | We believe the exchange of Series U senior notes for Series V senior notes pursuant to our exchange offer will not constitute a sale or an exchange for Federal income tax purposes. For further information, see the section entitled “Certain United States Federal Tax Consequences.” |

3

Table of Contents

Effect of not tendering | If you do not tender your Series U senior notes or if you do tender them but they are not accepted by us, your Series U senior notes will continue to be subject to the existing restrictions upon transfer. Except for our obligation to file a shelf registration statement under the circumstances described above, we will have no further obligation to provide for the registration under the Securities Act of Series U senior notes. |

Use of Proceeds | We will not receive any cash proceeds from the issuance of the Series V senior notes. |

4

Table of Contents

THE SERIES V SENIOR NOTES

The summary below describes the principal terms of the Series V senior notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. For a more detailed description of the terms and conditions of the Series V senior notes, see the section entitled “Description of Series V Senior Notes.”

Issuer | Host Hotels & Resorts, L.P., a Delaware limited partnership. |

Securities Offered | $500,000,000 aggregate principal amount of 6% Series V senior notes due 2020. |

Maturity | November 1, 2020. |

Interest | Interest on the Series V senior notes will accrue at an annual rate of 6%. We will pay interest on the Series V senior notes in arrears on February 1 and August 1 each year, commencing February 1, 2011. |

Ranking | The Series V senior notes and the related guarantees will be our and the guarantors’ unsubordinated obligations, will rank senior to all of our and the guarantors’ existing and future subordinated indebtedness and will rank equally in right of payment to our credit facility and our outstanding series of senior notes issued pursuant to our Amended and Restated Indenture dated August 5, 1998, as supplemented. The Series V senior notes and the existing senior notes effectively will be subordinated to all secured indebtedness that may be incurred under the indenture, to the extent of the value of the collateral securing such indebtedness (other than indebtedness that is secured by the stock pledge described above). See “Description of Series V Senior Notes—Ranking.” In addition, the Series V senior notes will be junior in right of payment to liabilities of our non-guarantor subsidiaries. For further information on ranking, see “Risk Factors—The Series V senior notes and the related subsidiary guarantees effectively will be junior in right of payment to some other liabilities,” “Description of Series V Senior Notes—General,” and “Description of Our Other Indebtedness.” |

As of September 10, 2010, as adjusted to give effect to the offering of the Series U senior notes, the use of proceeds therefrom to retire $250 million of Series K senior notes on November 29, 2010, as well as the defeasance of $115 million of mortgage debt in October 2010 and the irrevocable notice of our intent to repay on December 10, 2010 a $71 million mortgage loan, we and our subsidiaries would have had approximately $5.5 billion of total debt, of which approximately $4.3 billion would have been secured by the stock pledge described above, approximately $1.1 billion would have been secured by mortgage liens on various of our hotel properties and related assets of ours and our subsidiaries, and none of which would have been subordinated to the Series V senior notes. As of September 10, 2010, our non-guarantor subsidiaries had total indebtedness and liabilities of approximately $1.5 billion. See “Capitalization.”

5

Table of Contents

Guarantors | The Series V senior notes will be guaranteed by certain of our direct and indirect subsidiaries, representing all of our subsidiaries that also have guaranteed our credit facility, our existing senior notes and certain of our other indebtedness. The guarantees may be released without the consent of the holders of the Series V senior notes under certain circumstances. We generally are not required to cause future subsidiaries to become guarantors unless they secure our credit facility, our existing senior notes or certain of our other indebtedness. As of September 10, 2010, our non-guarantor subsidiaries held approximately 42% of our assets. |

| For more detail, see the section entitled “Risk Factors—The Series V senior notes and the related subsidiary guarantees effectively will be junior in right of payment to some other liabilities.” |

Security | The Series V senior notes will be secured by a pledge of the common equity interests of certain of our direct and indirect subsidiaries, which common equity interests also secure, on an equal and ratable basis, our credit facility and approximately $4.0 billion of our outstanding existing senior notes (as of September 10, 2010), including approximately $1.1 billion of exchangeable senior debentures net of original issue discount, and will secure certain other future unsubordinated indebtedness ranking equal in right of payment with the Series V senior notes. |

| The Series V senior notes and our existing senior notes effectively will be subordinated to all secured indebtedness (other than indebtedness that is secured by the stock pledge described above) that may be incurred under the indenture, to the extent of the value of the collateral securing such indebtedness. |

| Under the terms of the indenture governing our outstanding existing senior notes, we and the subsidiary guarantors may incur up to $400 million ($300 million in the case of certain series of our existing senior notes) of secured indebtedness, even when we are below the consolidated EBITDA-to-interest expense “coverage” ratio of at least 2.0 to 1.0, which would otherwise limit the incurrence of this new secured debt, so long as the proceeds are used to repay and permanently reduce indebtedness outstanding under our credit facility. In addition, when we are below such coverage ratio we may also incur up to $150 million ($100 million in the case of certain series of our existing senior notes) of indebtedness (which may be secured) without regard to use of proceeds. See “Description of Series V Senior Notes—Ranking” and “Description of Our Other Indebtedness.” |

Under the credit facility, we have the right to require the release of all pledges of capital stock in the event that our leverage ratio is below 6:00 to 1:00 for the two most recent consecutive quarters and no default or event of default exists. Effective October 12, 2005, we exercised this right for pledges of capital stock that would have been |

6

Table of Contents

otherwise required subsequent to this date. Hence, since October 12, 2005, no new pledges of capital stock have been made for the benefit of the credit facility banks and holders of senior notes. In certain cases, a requirement to pledge additional capital stock can otherwise result from the acquisition of entities owning hotel properties. We have not, however, released pledges of capital stock existing as of October 12, 2005, although we have the right to do so at any time that we continue to meet the conditions described above, as is currently the case because our leverage ratio is below 6:00 to 1:00, including after giving effect to this offering. No assurances can be made that we will not exercise this right in the future. The credit facility also requires us to reinstate the pledges of capital stock should our leverage ratio subsequently exceed 6:00 to 1:00 for two consecutive quarters. As of September 10, 2010, our leverage ratio was 5.6x. If we were required to reinstate these pledges, holders of our existing senior notes would also receive the benefit of the pledge. |

| For more detail, see the section entitled “Risk Factors—The Series V Senior Notes effectively will be junior in right of payment to some other liabilities.” |

Optional Redemption | At any time prior to November 1, 2015, the Series V senior notes will be redeemable at our option, in whole or in part, for 100% of their principal amount, plus the make-whole premium described in this prospectus, plus accrued and unpaid interest to the applicable redemption date. For more details, see the section entitled “Description of Series V Senior Notes—Optional Redemption.” |

| Beginning November 1, 2015, we may redeem, in whole or in part, the Series V senior notes at any time at the prices set forth in the section entitled “Description of Series V Senior Notes—Optional Redemption.” |

| In addition, prior to November 1, 2013, we may redeem up to 35% of the aggregate principal amount of the Series V senior notes at the price set forth in the section entitled “Description of Series V Senior Notes—Optional Redemption” together with any accrued and unpaid interest to the applicable redemption date with the net cash proceeds of certain sales of our or Host REIT’s equity securities. |

Mandatory Offer to Repurchase | If we sell certain assets or undergo certain kinds of changes of control, together with a change in the rating of the Series V senior notes, we must offer to repurchase the Series V senior notes as described in the section entitled “Description of Series V Senior Notes—Repurchase of Notes at the Option of the Holder upon a Change of Control Triggering Event.” See “Risk Factors—We may not have the ability to raise the funds necessary to finance the change of control offer required by the indenture” and “Risk Factors—We may be required to make an offer to repurchase all other series of our senior notes upon an asset sale but not from holders of Series U senior notes and Series V senior notes exchanged therefore.” |

7

Table of Contents

Basic Covenants of the Indenture | The indenture governing the Series V senior notes, among other things, restricts our ability and the ability of our restricted subsidiaries to: |

| • | incur additional indebtedness; |

| • | pay dividends on, redeem or repurchase our equity interests; |

| • | make investments; |

| • | allow payment or dividend restrictions to exist on certain of our subsidiaries; |

| • | sell assets; |

| • | in the case of our restricted subsidiaries, guarantee indebtedness; |

| • | create certain liens; and |

| • | sell certain assets or merge with or into other companies. |

All of these limitations are subject to important exceptions and qualifications and in certain instances, the application of these covenants will be suspended, as further described in the section entitled “Description of Series V Senior Notes—Covenants.”

Risk Factors | Investment in the Series V senior notes involves risks. You should carefully consider the information under the section entitled “Risk Factors” and all other information included in this prospectus before investing in the Series V senior notes. |

8

Table of Contents

You should carefully consider the risks described below. The risks and uncertainties described below are not the only ones related to our business or the Series V senior notes offered hereby. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business operations.

If any of the following risks actually occur, our business, financial condition or results of operations could be materially adversely affected. In that case, the trading price of the Series V senior notes could decline substantially or we could be unable to make payments under the Series V senior notes.

Risks Relating to this Offering

We have substantial leverage, which could adversely affect our cash flow and prevent us from fulfilling our obligations under the Series V senior notes.

We have significant indebtedness and we will continue to have significant indebtedness after the exchange of the Series U senior notes. As of September 10, 2010, we and our subsidiaries had total indebtedness of approximately $5.4 billion. As adjusted to give effect to the issuance of the Series U senior notes, the use of proceeds therefrom to redeem $250 million of Series K senior notes, as well as the defeasance of $115 million of mortgage debt on the W New York, Union Square in October 2010 and the irrevocable notice of our intent to repay on December 10, 2010 a $71 million mortgage on the JW Marriott, Desert Springs, we and our subsidiaries would have had total indebtedness of approximately $5.5 billion (of which approximately $4.3 billion would have consisted of senior notes and indebtedness under the credit facility secured by an equal and ratable pledge of the stock of certain of our subsidiaries, approximately $1.1 billion would have been secured by mortgage liens on various of our hotel properties and related assets, and would effectively be senior to the Series V senior notes to the extent of the value of those assets, and the balance would have consisted of other debt). Under the terms of the Series V senior notes and our existing indebtedness we will have the ability to incur significant amounts of additional indebtedness, including additional secured indebtedness, the collateral of which will not secure the Series V senior notes.

Our substantial indebtedness has important consequences. It currently requires us to dedicate a substantial portion of our cash flow from operations to payments of principal and interest on our indebtedness, which reduces the availability of our cash flow to fund working capital, capital expenditures, expansion efforts, distributions to our partners and other general purposes. Additionally, it could:

| • | make it more difficult for us to satisfy our obligations with respect to the Series V senior notes offered hereby; |

| • | limit our ability in the future to undertake refinancings of our debt or obtain financing for expenditures, acquisitions, development or other general business purposes on terms and conditions acceptable to us, or at all; or |

| • | affect adversely our ability to compete effectively or operate successfully under adverse economic conditions. |

Because Host REIT must distribute at least 90% of its annual taxable income, excluding net capital gain, in order to maintain its qualification as a REIT, we make significant distributions of cash to Host REIT and depend upon external sources of capital for future growth. If our cash flow and working capital were not sufficient to fund our expenditures or service our indebtedness, we would have to raise additional funds through:

| • | sales of operating partnership common units (“OP Units”); |

| • | the incurrence of additional permitted indebtedness by us; or |

| • | the sale of our assets. |

9

Table of Contents

We cannot assure you that any of these sources of funds would be available to us or, if available, would be on terms that we would find acceptable or in amounts sufficient for us to meet our obligations or fulfill our business plan. Under certain circumstances we would be required to use the cash from some of the events described above to repay other indebtedness.

The Series V senior notes and the related subsidiary guarantees effectively will be junior in right of payment to some other liabilities.

Only our subsidiaries that have guaranteed or will be required to guarantee payment of certain of our indebtedness ranking equal in priority to the Series V senior notes, including the credit facility, our existing senior notes and future indebtedness that is similarly guaranteed, have guaranteed, and are required to guarantee, our obligations under the Series V senior notes. Although the indenture governing the terms of the Series V senior notes places limits on the overall level of indebtedness that non-guarantor subsidiaries may incur, the Series V senior notes effectively will be junior in right of payment to liabilities of our non-guarantor subsidiaries and to any debt of ours or our subsidiaries that is secured by assets other than the equity interests in our subsidiaries securing the Series V senior notes, to the extent of the value of such assets. As of September 10, 2010, our non-guarantor subsidiaries had total debt and liabilities of approximately $1.5 billion. Since only those subsidiaries that guarantee the credit facility, the existing senior notes or certain of our other indebtedness are required to guarantee the Series V senior notes, there can be no assurance as to the number of subsidiaries that will be guarantors of the Series V senior notes at any point in time or as to the value of their assets or significance of their operations.

Under the terms of the indenture applicable to the Series V senior notes, subject to satisfaction of certain other requirements, we, the subsidiary guarantors and our respective restricted subsidiaries may incur debt secured by our respective assets (other than the equity interests of our subsidiaries securing the credit facility, the existing senior notes and the Series V senior notes). For a discussion of our ability to incur such secured debt, see “Description of Series V Senior Notes—Limitation on Incurrence of Indebtedness and Issuance of Disqualified Stock” and “Description of Our Other Indebtedness—Senior Notes—Differences Between Series V and All Other Series of Senior Notes.” Neither the Series V senior notes nor the related subsidiary guarantees thereof will be secured by those assets and the Series V senior notes and such subsidiary guarantees effectively will be junior in right of payment to this secured debt to the extent of the value of the assets securing such debt. As of November 30, 2010, we and our subsidiaries had approximately $1.2 billion of debt secured by mortgages on 12 of our hotels and related assets, which includes the $71 million mortgage on the JW Marriott, Desert Springs, for which we have given an irrevocable notice to repay on December 10, 2010.

In addition, under the indenture covenants that are applicable to our existing senior notes, and that will be applicable to the Series V senior notes, we and the subsidiary guarantors may also incur up to $400 million ($300 million in the case of certain series of our existing senior notes) of secured indebtedness, even when we are below the consolidated EBITDA-to-interest expense “coverage” ratio of at least 2.0 to 1.0, which would otherwise limit the incurrence of this new secured debt, so long as the proceeds are used to repay and permanently reduce indebtedness outstanding under our credit facility. In addition, when we are below such coverage ratio we may also incur up to $150 million ($100 million in the case of certain series of our existing senior notes) of indebtedness (which may be secured) without regard to use of proceeds. See “Description of Series V Senior Notes—Ranking.” The Series V senior notes will be subordinated to this and to all other secured indebtedness that may be incurred under the indenture governing the Series V senior notes, to the extent of the value of the collateral securing such secured indebtedness.

Under the credit facility, we have the right to require the release of all pledges of capital stock in the event that our leverage ratio is below 6:00 to 1:00 for the two most recent consecutive quarters and no default or event of default exists. Effective October 12, 2005, we exercised this right for pledges of capital stock that would have been otherwise required subsequent to this date. Hence, since October 12, 2005, no new pledges of capital stock have been made for the benefit of the credit facility banks and holders of senior notes. In certain cases, we would have otherwise been required to pledge additional capital stock resulting from the acquisition of entities owning hotel properties and, in addition, the capital stock of certain material subsidiaries has not been pledged. We have not,

10

Table of Contents

however, released pledges of capital stock existing as of October 12, 2005, although we have the right to do so at any time that we continue to meet the conditions described above as is currently the case because our leverage ratio is below 6:00 to 1:00, including after giving effect to this offering. No assurances can be made that we will not exercise this right in the future. The credit facility also requires us to reinstate the pledges of capital stock should our leverage ratio subsequently exceed 6:00 to 1:00 for two consecutive quarters. If we were required to reinstate these pledges holders of our existing senior notes would also receive the benefit of the pledge.

The terms of our debt place restrictions on us and our subsidiaries, reducing operational flexibility and creating default risks.

The documents governing the terms of the Series V senior notes, our existing senior notes and our credit facility and certain of our other outstanding indebtedness contain covenants that place restrictions on us and our subsidiaries. These covenants will restrict, among other things, our ability and the ability of our subsidiaries to:

| • | conduct acquisitions, mergers or consolidations unless the successor entity in such transaction assumes our indebtedness; |

| • | incur additional debt in excess of certain thresholds without satisfying certain financial metrics; |

| • | create liens securing indebtedness, unless effective provision is made to secure our other indebtedness by such liens; |

| • | sell assets without using the proceeds from such sales for certain permitted uses or to make an offer to repay or repurchase outstanding indebtedness; |

| • | make capital expenditures in excess of certain thresholds; |

| • | raise capital; |

| • | make distributions without satisfying certain financial metrics; and |

| • | conduct transactions with affiliates other than on an arms length basis and, in certain instances, without obtaining opinions as to the fairness of such transactions. |

In addition, certain covenants in the credit facility require us and our subsidiaries to meet financial performance tests. The restrictive covenants in the applicable indenture(s), the credit facility and the documents governing our other debt (including our mortgage debt) will reduce our flexibility in conducting our operations and will limit our ability to engage in activities that may be in our long-term best interest. Our failure to comply with these restrictive covenants could result in an event of default that, if not cured or waived, could result in the acceleration of all or a substantial portion of our debt. Under the indentures governing the Series V senior notes and certain series of our existing senior notes, if such series achieves investment grade status as described in “Description of Series V Senior Notes— Covenants upon Attainment and Maintenance of an Investment Grade Rating,” substantially all of the restrictive covenants applicable to such series will no longer be in effect. For a detailed description of the covenants and restrictions imposed by the documents governing our indebtedness, see “Description of Our Other Indebtedness.”

We will be permitted to make distributions to Host REIT under certain conditions even when we cannot otherwise make restricted payments under the indenture and the credit facility.

Under the indenture terms governing the Series V senior notes and our existing senior notes, we are only allowed to make restricted payments if, at the time we make such a restricted payment, we are able to incur at least $1.00 of indebtedness under the “Limitation on Incurrences of Indebtedness and Issuance of Disqualified Stock” covenant and we satisfy certain other requirements. This covenant requires us to meet certain conditions in order to incur additional debt, including that we have a consolidated EBITDA-to-interest expense “coverage” ratio of at least 2.0 to 1.0 in order to make a restricted payment; except that, in the case of a preferred stock distribution, the covenant applicable to the Series V senior notes and our outstanding senior notes provides that we are only required to have a consolidated coverage ratio of at least 1.7 to 1.0. For a more complete discussion of the restricted payment and debt incurrence covenants of the indenture applicable to the Series V senior notes, see the following sections of

11

Table of Contents

this prospectus: “Description of Series V Senior Notes—Limitation on Restriction Payments”; and “Description of Series V Senior Notes—Limitation on Incurrences of Indebtedness and Issuance of Disqualified Stock.”

Even when we are unable to make restricted payments during a period in which we are unable to incur $1.00 of indebtedness, the indenture terms governing the Series V senior notes and our outstanding senior notes permit us, so long as Host REIT believes in good faith after reasonable diligence that Host REIT qualifies as a REIT under the Internal Revenue Code of 1986, as amended (the “Code”), to make permitted REIT distributions, which are any distributions (1) to Host REIT equal to the greater of (a) the amount estimated by Host REIT in good faith after reasonable diligence to be necessary to permit Host REIT to distribute to its shareholders with respect to any calendar year (whether made during such year or after the end thereof) 100% of the “real estate investment trust taxable income” of Host REIT within the meaning of Section 857(b)(2) of the Code, determined without regard to deductions for dividends paid and the exclusions set forth in Code Sections 857(b)(2)(C), (D), (E) and (F) but including all net capital gains and net recognized built-in gains within the meaning of Treasury Regulations 1.337(d)-6 (whether or not such gains might otherwise be excluded or excludable therefrom); or (b) the amount that is estimated by Host REIT in good faith after reasonable diligence to be necessary either to maintain Host REIT’s status as a REIT under the Code for any calendar year or to enable Host REIT to avoid the payment of any tax for any calendar year that could be avoided by reason of a distribution by Host REIT to its shareholders, with such distributions to be made as and when determined by Host REIT, whether during or after the end of the relevant calendar year; in either the case of (a) or (b) above if: (x) the aggregate principal amount of all our outstanding indebtedness and that of our restricted subsidiaries, on a consolidated basis, at such time is less than 80% of our Adjusted Total Assets (as defined in the indenture) and (y) no Default or Event of Default (as defined in the indenture) shall have occurred and be continuing, and (2) to certain other holders of our partnership units where such distribution is required as a result of, or a condition to, the payment of distributions to Host REIT. We refer to the distributions that we are permitted to make which are summarized in this paragraph as “permitted REIT distributions.”

We may not have the ability to raise the funds necessary to finance the change of control offer required by the indenture.

Upon the occurrence of certain change of control events, we will be required to offer to repurchase all outstanding series of our senior notes and the Series V senior notes offered hereby. However, it is possible that we will not have sufficient funds at the time of the change of control to make the required repurchase of senior notes or that restrictions in our credit facility and other outstanding indebtedness at that time will not allow us to make such repurchases. See “Description of Series V Senior Notes—Repurchase of Notes at the Option of the Holder Upon a Change of Control Triggering Event.”

Our failure to repurchase any of the Series V senior notes would be a default under the indenture for all series of senior notes issued thereunder and also under our credit facility.

The Series V senior notes or a guarantee thereof may be deemed a fraudulent transfer.

Under the Federal bankruptcy laws and comparable provisions of state fraudulent transfer laws, a guarantee of the Series V senior notes could be voided, or claims on a guarantee of the Series V senior notes could be subordinated to all other debts of that guarantor if, among other things, the guarantor, at the time it incurred the indebtedness evidenced by its guarantee:

| (1) | received less than reasonably equivalent value or fair consideration for the incurrence of such guarantee; and |

| (2) | either: |

| (a) | was insolvent or rendered insolvent by reason of such incurrence; |

| (b) | was engaged in a business or transaction for which the guarantor’s remaining assets constituted unreasonably small capital; or |

| (c) | intended to incur, or believed that it would incur, debts beyond its ability to pay such debts as they mature. |

12

Table of Contents

If such circumstances were found to exist, or if a court were to find that the guarantee were issued with actual intent to hinder, delay or defraud creditors, the court could cause any payment by that guarantor pursuant to its guarantee to be voided and returned to the guarantor, or to a fund for the benefit of the creditors of the guarantor. In such event, the Series V senior notes would be structurally subordinated to the indebtedness and other liabilities of such subsidiary.

In addition, our obligations under the Series V senior notes may be subject to review under the same laws in the event of our bankruptcy or other financial difficulty. In that event, if a court were to find that when we issued the Series V senior notes the factors in clauses (1) and (2) above applied to us, or that the Series V senior notes were issued with actual intent to hinder, delay or defraud creditors, the court could void our obligations under the Series V senior notes, or direct the return of any amounts paid thereunder to us or to a fund for the benefit of our creditors.

The measures of insolvency for purposes of these fraudulent transfer laws will vary depending upon the law applied in any proceeding to determine whether a fraudulent transfer has occurred. Generally, however, the operating partnership or a guarantor would be considered insolvent if:

| • | the sum of its debts, including contingent liabilities, were greater than the fair saleable value of all of its assets; or |

| • | the present fair value of its assets were less than the amount that would be required to pay its probable liability on its existing debts, including contingent liabilities, as they become absolute and mature; or |

| • | it could not pay its debts as they become due. |

We can offer no assurance as to what standard a court would apply in making such determinations or that a court would agree with our conclusions in this regard.

An active trading market may not develop for the notes.

The Series U senior notes are not listed on any securities exchange. Since their issuance, there has been a limited trading market for such notes. To the extent that Series U senior notes are tendered and accepted in the exchange offer, the trading market for untendered and tendered but unaccepted Series U senior notes will be adversely affected. We cannot assure you that this market will provide liquidity for you if you want to sell your Series U senior notes.

We will not list the Series V senior notes on any securities exchange. These notes are new securities for which there is currently no market. The Series V senior notes may trade at a discount from their initial offering price, depending upon prevailing interest rates, the market for similar securities, our performance and other factors. We have been advised by the initial purchasers of the Series U senior notes that they intend to make a market in the Series V senior notes, as well as the Series U senior notes, as permitted by applicable laws and regulations. However, they are not obligated to do so and their market making activities may be discontinued at any time without notice. In addition, their market making activities may be limited during our exchange offer. Therefore, we cannot assure you that an active market for Series V senior notes will develop.

We may be required to make an offer to repurchase all other series of our senior notes upon an asset sale but not from holders of Series U senior notes and Series V senior notes exchanged therefor.

The covenant restricting our use of proceeds from asset sales under the Series U and Series V senior notes indenture only applies to the extent that the net cash proceeds from such sales during any 12-month period exceeds 5% of our total assets (using undepreciated asset values) whereas the covenant restricting our use of proceeds from asset sales under the indentures governing our other series of senior notes applies when net cash proceeds from such sales during any 12-month period exceeds 1% of our total assets (using undepreciated asset

13

Table of Contents

values). Accordingly, in certain instances, we may be required to make an offer to repurchase all existing series of senior notes other than the Series U and Series V senior notes with the excess proceeds from asset sales that are not reinvested or used to pay down our credit facility.

Financial Risks and Risks of Operation

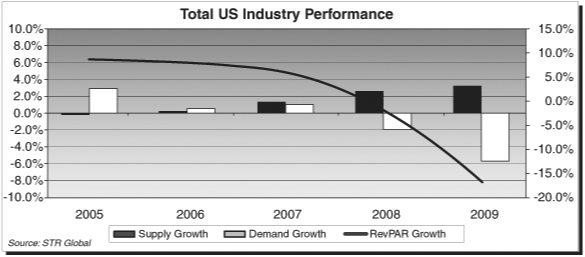

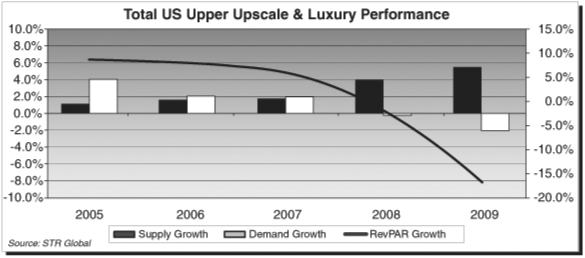

Our revenues and the value of our properties are also subject to other conditions affecting the lodging industry.

The lodging industry is subject to changes in the travel patterns of business and leisure travelers, both of which are affected by the strength of the economy, as well as other factors. Changes in travel patterns of both business and leisure travelers may create difficulties for the industry over the long-term and adversely affect our results. During the recession in 2008 and 2009, overall travel was reduced which had a significant effect on our results of operations. While operating results have improved during 2010, other factors such as low GDP growth, continued high unemployment and weak consumer spending continue to slow the overall economic recovery. For this reason, there can be no assurance that any increases in hotel revenues or earnings at our properties will continue for any number of reasons, including, but not limited to, slower than anticipated growth in the economy and changes in travel patterns. Therefore, our results of operations and any forecast we make, may be affected and can change based on the following risks:

| • | changes in the international, national, regional and local economic climate; |

| • | changes in business and leisure travel patterns; |

| • | the effect of terrorist attacks and terror alerts in the United States and internationally, as well as other geopolitical disturbances; |

| • | supply growth in markets where we own hotels which may adversely affect demand at our properties; |

| • | the attractiveness of our hotels to consumers relative to our competition; |

| • | the performance of the managers of our hotels; |

| • | outbreaks of disease; |

| • | changes in room rates and increases in operating costs due to inflation and other factors; and |

| • | unionization of the labor force at our hotels. |

A reduction in our revenue or earnings as a result of the above risks may reduce our working capital, impact our long-term business strategy, and impact the value of our assets and our ability to meet certain covenants in our existing debt agreements.

Economic conditions may adversely effect the value of our hotels which may result in impairment charges on our properties.

We analyze our assets for impairment in several situations, including when a property has current or projected losses from operations, when it becomes more likely than not that a hotel will be sold before the end of its previously estimated useful life, or when other material trends, contingencies or changes in circumstances indicate that a triggering event has occurred that indicate an asset’s carrying value may not be recoverable. For impaired assets, we record an impairment charge equal to the excess of the property’s carrying value over its fair value. Our operating results for 2009 included $131 million of impairment charges taken in the first half of 2009 related to our consolidated hotels and our European joint venture. We did not record any impairment charges in 2010. We may, however, incur additional impairment charges in the future, which will negatively affect our results of operations. We can provide no assurance that any impairment loss recognized would not be material to our results of operations. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies.”

14

Table of Contents

Disruptions in the financial markets may adversely affect our business and results of operations, our ability to obtain financing on reasonable and acceptable terms, our ability to hedge our foreign currency exchange risk and the value of our common OP units.

The United States and global stock and credit markets experienced significant price volatility, dislocations and liquidity disruptions, all of which caused market prices of the stocks of many companies to fluctuate substantially and the spreads on prospective and outstanding debt financings to widen considerably. These circumstances impacted liquidity in the financial markets, which made terms for certain financings less attractive, and, in some cases, resulted in the lack of availability of certain types of financing. While conditions in the credit markets have improved, continued uncertainty in the stock and credit markets may negatively impact our ability to access additional short-term and long-term financing on reasonable terms or at all, which would negatively impact our liquidity and financial condition. A prolonged downturn in the stock or credit markets may cause us to seek alternative sources of potentially less attractive financing and may negatively impact our ability to enter into derivative contracts in order to hedge risks associated with changes in interest rates and foreign currency exchange rates. These disruptions in the financial markets also may adversely affect our credit rating and the value of our common OP units. While we believe we have adequate sources of liquidity with which to meet our anticipated requirements for working capital, debt service and capital expenditures for the foreseeable future, if our operating results worsen significantly and our cash flow or capital resources prove inadequate, or if interest rates increase significantly, we could face liquidity problems that could materially and adversely affect our results of operations and financial condition.

We depend on external sources of capital for future growth and we may be unable to access capital when necessary.

Unlike regular C corporations, Host REIT must finance its growth and fund debt repayments largely with external sources of capital because it is required to distribute to its stockholders at least 90% of its taxable income (other than net capital gain) in order to qualify as a REIT, including taxable income recognized for federal income tax purposes but with regard to which it does not receive cash. Funds used by Host REIT to make required distributions are provided through distributions from Host L.P. Our ability to access the external capital we require could be hampered by a number of factors, many of which are outside of our control, including credit market conditions as discussed above, unfavorable market perception of our growth potential, decreases in our current and estimated future earnings, or decreases in the market price of Host REIT’s common stock. Our ability to access additional capital also may be limited by the terms of our existing indebtedness, which, under certain circumstances, restrict our incurrence of debt and the payment of distributions. The occurrence of any of these factors, individually or in combination, could prevent us from being able to obtain the external capital we require on terms that are acceptable to us or at all and the failure to obtain necessary external capital could have a material adverse effect on our ability to finance our future growth.

Our ability to make distributions may be limited or prohibited by the terms of our indebtedness or preferred OP units.

We are, and may in the future become, party to agreements and instruments that restrict or prevent the payment of distributions on classes of units. Under the terms of Host L.P.’s credit facility and senior notes indenture, distributions to our unitholders, including Host REIT, upon which Host REIT depends in order to obtain the cash necessary to pay dividends, are permitted only to the extent that, at the time of the distribution, Host L.P. can satisfy certain financial covenant tests (concerning leverage, fixed charge coverage and unsecured interest coverage) and meet other requirements.

Under the terms of our outstanding preferred OP units, we are not permitted to make distributions on our common OP units unless all cumulative distributions have been paid (or funds for payment have been set aside for payment) on our preferred OP units. In the event that we fail to pay the accrued distributions on our preferred OP units for any reason, including any restriction on making such distributions under the terms of our debt

15

Table of Contents

instruments (as discussed above), distributions will continue to accrue on such preferred OP units and we will be prohibited from making any distributions on our common OP units until all such accrued but unpaid distributions on our preferred OP units have been paid (or funds for such payment have been set aside).

Defaulting on our mortgage debt could adversely affect our business.

As of November 30, 2010, we and our subsidiaries had approximately $1.2 billion of debt secured by mortgages on 12 of our hotels and related assets. Although the debt is generally non-recourse to us, if these hotels do not produce adequate cash flow to service the debt secured by such mortgages, the mortgage lenders could call a default on these assets. Generally, we would expect to negotiate with the lender prior to the occurrence of a default to pursue other options, such as a deed in lieu of foreclosure. However, we may opt to allow such default to occur rather than make the necessary mortgage payments with funds from other sources. Our senior notes indenture and credit facility contain cross-default provisions, which, depending upon the amount of secured debt in default, could cause a cross-default under both of these agreements. Our credit facility, which contains a more restrictive cross-default provision than the senior notes indenture, provides that a credit facility default will occur in the event that we default on non-recourse secured indebtedness in excess of 1% (or approximately $150 million as of December 31, 2009) of our total assets (using undepreciated real estate book values). For this and other reasons, permitting a default could adversely affect our long-term business prospects.

Our mortgage debt contains provisions that may reduce our liquidity.

Certain of our mortgage debt requires that, to the extent cash flow from the hotels which secure such debt drops below stated levels, we escrow cash flow after the payment of debt service until operations improve above the stated levels. In some cases, the lender has the right under certain circumstances to apply the escrowed amount to the outstanding balance of the mortgage debt. If such provisions are triggered, there can be no assurance that the affected properties will achieve the minimum cash flow levels required to trigger a release of any escrowed funds. The amounts required to be escrowed may negatively affect our liquidity by limiting our access to cash flow after debt service from these mortgaged properties.

An increase in interest rates would increase our interest costs on our credit facility and on our floating rate debt and could adversely impact our ability to refinance existing debt or sell assets.

Interest payments for borrowings on our credit facility, the mortgages on two properties and the fixed-to- floating interest rate swaps linked to two other properties are based on floating rates. As a result, an increase in interest rates will reduce our cash flow available for other corporate purposes, including investments in our portfolio. Further, rising interest rates could limit our ability to refinance existing debt when it matures and increase interest costs on any debt that is refinanced. We may from time to time enter into agreements such as interest rate swaps, caps, floors and other interest rate hedging contracts. While these agreements may lessen the impact of rising interest rates, they also expose us to the risk that other parties to the agreements will not perform or that the agreements will be unenforceable. In addition, an increase in interest rates could decrease the amount third parties are willing to pay for our assets, thereby limiting our ability to dispose of assets as part of our business strategy.

Rating agency downgrades may increase our cost of capital.

Our senior notes are rated by Moody’s Investors Service, Standard & Poor’s Ratings Services and Fitch Ratings. These independent rating agencies may elect to downgrade their ratings on our senior notes at any time. Such downgrades may negatively affect our access to the capital markets and increase our cost of capital.

Our expenses may not decrease if our revenue decreases.

Many of the expenses associated with owning and operating hotels, such as debt service payments, property taxes, insurance, utilities, and employee wages and benefits, are relatively inflexible and do not necessarily

16

Table of Contents

decrease in tandem with a reduction in revenue at the hotels. Our expenses also will be affected by inflationary increases, and certain costs, such as wages, benefits and insurance, may exceed the rate of inflation in any given period and, in the event of a significant decrease in demand, we may not be able to reduce the size of hotel work-forces in order to decrease wages and benefits. Our managers may be unable to offset any such increased expenses with higher room rates. Any of our efforts to reduce operating costs or failure to make scheduled capital expenditures also could adversely affect the future growth of our business and the value of our hotel properties.

Our acquisition of additional properties may have a significant effect on our business, liquidity, financial position and/or results of operations.

As part of our business strategy, we seek to acquire luxury and upper upscale hotel properties. We may acquire properties through various structures, including transactions involving portfolios, single assets, joint ventures and acquisitions of all or substantially all of the securities or assets of REITs or similar real estate entities. We anticipate that our acquisitions will be financed through a combination of methods, including proceeds from Host REIT equity offerings, issuance of limited partnership interests of Host L.P., advances under our credit facility, the incurrence or assumption of indebtedness and proceeds from the sales of assets. Continued disruptions in credit markets may limit our ability to finance acquisitions and may limit the ability of purchasers to finance hotels and adversely affect our disposition strategy and our ability to use disposition proceeds to finance acquisitions.

We may, from time to time, be in the process of identifying, analyzing and negotiating possible acquisition transactions and we expect to continue to do so in the future. We cannot provide any assurances that we will be successful in consummating future acquisitions on favorable terms or that we will realize the benefits that we anticipate from the acquisitions that we consummate. Our inability to consummate one or more acquisitions on such terms, or our failure to realize the intended benefits from one or more acquisitions, could have a significant adverse effect on our business, liquidity, financial position and/or results of operations, including as a result of our incurrence of additional indebtedness and related interest expense and our assumption of unforeseen contingent liabilities.

We do not control our hotel operations and we are dependent on the managers of our hotels.