UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21681

Guggenheim Enhanced Equity Income Fund

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

227 West Monroe Street, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

Amy J. Lee

227 West Monroe Street, Chicago, IL 60606

(Name and address of agent for service)

(Name and address of agent for service)

Registrant's telephone number, including area code: (312) 827-0100

Date of fiscal year end: December 31

Date of reporting period: January 1, 2020 to December 31, 2020

Item 1. Reports to Stockholders.

The registrant's annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

Section 19(a) Notices

Guggenheim Enhanced Equity Income Fund’s (the “Fund”) reported amounts and sources of distributions are estimates and are not being provided for tax reporting purposes. The actual amounts and sources for tax reporting purposes will depend upon the Fund’s investment experience during the year and may be subject to changes based on the tax regulations. The Fund will provide a Form 1099-DIV each calendar year that will explain the character of these dividends and distributions for federal income tax purposes.

December 31, 2020 | |||||||||

| Total Cumulative Distribution | % Breakdown of the Total Cumulative | ||||||||

| For the Fiscal Year | Distributions for the Fiscal Year | ||||||||

| Net | Net | Net | Net | ||||||

| Realized | Realized | Realized | Realized | ||||||

| Net | Short-Term | Long-Term | Total per | Net | Short-Term | Long-Term | Total per | ||

| Investment | Capital | Capital | Return of | Common | Investment | Capital | Capital | Return of | Common |

| Income | Gains | Gains | Capital | Share | Income | Gains | Gains | Capital | Share |

$0.0446 | $0.0000 | $0.0000 | $0.5554 | $0.6000 | 7.43% | 0.00% | 0.00% | 92.57% | 100.00% |

If the Fund has distributed more than its income and net realized capital gains, a portion of the distribution may be a return of capital. A return of capital may occur, for example, when some or all of a shareholder’s investment in a Fund is returned to the shareholder. A return of capital distribution does not necessarily reflect a Fund’s investment performance and should not be confused with “yield” or “income.”

Section 19(a) notices for the Fund are available on the Fund’s website at guggenheiminvestments.com/gpm.

Section 19(b) Disclosure

The Fund, acting pursuant to a Securities and Exchange Commission (“SEC”) exemptive order and with the approval of the Fund’s Board of Trustees (the “Board”), has adopted a plan, consistent with its investment objectives and policies to support a level distribution of income, capital gains and/or return of capital (the “Plan”). In accordance with the Plan, the Fund currently distributes a fixed amount per share, $0.1200, on a quarterly basis.

The fixed amounts distributed per share are subject to change at the discretion of the Fund’s Board. Under its Plan, the Fund will distribute all available investment income to its shareholders, consistent with its primary investment objectives and as required by the Internal Revenue Code of 1986, as amended (the “Code”). If sufficient investment income is not available on a quarterly basis, the Fund will distribute capital gains and/or return of capital to shareholders in order to maintain a level distribution. Each quarterly distribution to shareholders is expected to be at the fixed amount established by the Board, except for extraordinary distributions and potential distribution rate increases or decreases to enable the Fund to comply with the distribution requirements imposed by the Code.

Shareholders should not draw any conclusions about the Fund’s investment performance from the amount of these distributions or from the terms of the Plan. The Fund’s total return performance on net asset value is presented in its financial highlights table.

The Board may amend, suspend or terminate the Fund’s Plan without prior notice if it deems such actions to be in the best interests of the Fund or its shareholders. The suspension or termination of the Plan could have the effect of creating a trading discount (if the Fund’s stock is trading at or above net asset value) or widening an existing trading discount. The Fund is subject to risks that could have an adverse impact on its ability to maintain level distributions. Examples of potential risks include, but are not limited to, economic downturns impacting the markets, decreased market volatility, companies suspending or decreasing corporate dividend distributions and changes in the Code. Please refer to the Fund’s prospectus and its website, guggenheiminvestments.com/gpm for a more complete description of its risks.

GUGGENHEIMINVESTMENTS.COM/GPM

...YOUR LINK TO THE LATEST, MOST UP-TO-DATE INFORMATION ABOUT GUGGENHEIM ENHANCED EQUITY INCOME FUND

The shareholder report you are reading right now is just the beginning of the story.

Online at guggenheiminvestments.com/gpm, you will find:

| • | Daily, weekly and monthly data on share prices, distributions and more |

| • | Portfolio overviews and performance analyses |

| • | Announcements, press releases and special notices |

| • | Fund and adviser contact information |

Guggenheim Partners Investment Management, LLC and Guggenheim Funds Investment Advisors, LLC are constantly updating and expanding shareholder information services on the Fund’s website in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed and the results of our efforts. It is just one more small way we are working to keep you better informed about your investment in the Fund.

| (Unaudited) | December 31, 2020 |

DEAR SHAREHOLDER:

We thank you for your investment in the Guggenheim Enhanced Equity Income Fund (the “Fund”). This report covers the Fund’s performance for the one-year period ended December 31, 2020, which concluded on a cautious note.

The recovery from the COVID shock has been faster than expected, with consumer confidence holding up well as massive fiscal support drove positive personal income growth and a swift monetary policy response led to gains in household net worth. However, the latest COVID wave is the largest yet, which has led to renewed lockdowns and a setback in the recovery this winter. The recovery will resume with more fiscal support being deployed, and with vaccinations now underway. Vaccinating the elderly first should dramatically cut the fatality and hospitalization risk, allowing for higher economic activity even amid high cases.

These events affected performance of the Fund for the period. To learn more about the Fund’s performance and investment strategy, we encourage you to read the Economic and Market Overview and the Questions & Answers sections of this report, which begin on page 7. You’ll find information on Guggenheim’s investment philosophy, views on the economy and market environment, and detailed information about the factors that impacted the Fund’s performance.

The Fund’s primary investment objective is to seek a high level of current income and gains with a secondary objective of long-term capital appreciation. Guggenheim Partners Investment Management LLC (“GPIM” or the “Sub-Adviser”) seeks to achieve the Fund’s investment objective by obtaining broadly diversified exposure to the equity markets and utilizing an option writing strategy developed by GPIM. The Fund may seek to obtain exposure to equity markets through investments in individual equity securities, through investments in exchange-traded funds (“ETFs”) or other investment funds that track equity market indices, and/or through derivative instruments that replicate the economic characteristics of exposure to equity securities or markets.

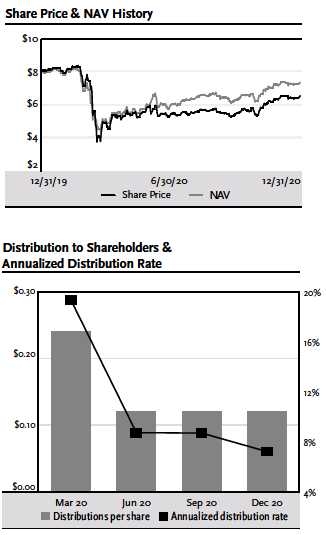

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the one-year period ended December 31, 2020, the Fund provided a total return based on market price of -9.16% and a total return net of fees based on NAV of 2.16%. As of December 31, 2020, the Fund’s closing market price of $6.55 per share represented a discount of 11.13% to its NAV of $7.37 per share.

Past performance is not a guarantee of future results. All NAV returns include the deduction of management fees, operating expenses, and all other Fund expenses. The market price of the Fund’s shares fluctuates from time to time, and may be higher or lower than the Fund’s NAV.

The Fund paid a distribution in each quarter of the period. On March 31, 2020, the distribution was $0.24 per share. On June 30, 2020, the distribution was reduced to $0.12 per share, and $0.12 per share was paid on September 30, 2020, and on December 31, 2020. The most recent distribution represents an

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 5

| (Unaudited) continued | December 31, 2020 |

annualized distribution rate of 7.33% based on the Fund’s closing market price of $6.55 per share as of December 31, 2020. There is no guarantee of any future distribution or that the current returns and distribution rate will be maintained. The Fund’s distribution rate is not constant and the amount of distributions, when declared by the Fund’s Board of Trustees, is subject to change based on the performance of the Fund. Please see Note 2(d) on page 44 for more information on distributions for the period.

Guggenheim Funds Investment Advisors, LLC (“GFIA” or the “Adviser”) serves as the investment adviser to the Fund. GPIM serves as the Fund’s Sub-Adviser and is responsible for the management of the Fund’s portfolio of investments. Both the Adviser and the Sub-Adviser are affiliates of Guggenheim Partners, LLC (“Guggenheim”), a global diversified financial services firm.

We encourage shareholders to consider the opportunity to reinvest their distributions from the Fund through the Dividend Reinvestment Plan (“DRIP”), which is described in detail on page 62 of this report. When shares trade at a discount to NAV, the DRIP takes advantage of the discount by reinvesting the monthly distribution in common shares of the Fund purchased in the market at a price less than NAV. Conversely, when the market price of the Fund’s common shares is at a premium above NAV, the DRIP reinvests participants’ distributions in newly-issued common shares at the greater of NAV per share or 95% of the market price per share. The DRIP provides a cost-effective means to accumulate additional shares and enjoy the benefits of compounding returns over time. Since the Fund endeavors to maintain a stable monthly distribution, the DRIP effectively provides an income averaging technique, which causes shareholders to accumulate a larger number of Fund shares when the market price is depressed than when the price is higher.

We appreciate your investment and look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the Fund’s website at guggenheiminvestments.com/gpm.

Sincerely,

Guggenheim Funds Investment Advisors, LLC

Guggenheim Enhanced Equity Income Fund

January 31, 2021

January 31, 2021

6 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| ECONOMIC AND MARKET OVERVIEW (Unaudited) | December 31, 2020 |

In what could have been one of the worst years on record for equity investors due to the devastating human and economic cost of the COVID-19 pandemic combined with political unrest in the U.S., the 12-month period ended December 31, 2020, witnessed the Standard & Poor’s (“S&P 500®”) Index reach a record high of 3,756.07 from 3,234.85 at the start of the year. This was despite plummeting to 2,237.40 on March 23, 2020 as the effects of the pandemic caused the U.S. economy to stall. This dramatic change in fortune for equity markets was due in large part by a swift, sweeping response to the economic shutdown in March 2020 by the U.S. Federal Reserve (the “Fed”), which has continued to signal its intention to use ultra-accommodative monetary policy to strive toward full employment and 2% inflation via unprecedented measures. The central bank’s commitment to keeping interest rates near zero and its bond-buying program to lessen the risk of corporate defaults resulted in bountiful debt issuance by corporate borrowers and a growing confidence among equity investors that the investment environment would remain benign for the foreseeable future.

As such, our economic outlook for the coming year is positive, owing to another round of COVID-19 relief and more planned by the new administration, plus the expectation for a successful vaccine distribution. The new package, titled the Coronavirus Response and Relief Supplemental Appropriations Act, delivers a $900 billion injection into the economy, bringing total COVID-related aid to over $3.5 trillion including the 2020 bill, or roughly 8.5% of 2020–2021 gross domestic product (“GDP”). On this measure, it is already 3.5x more than the stimulus delivered in the five years following the financial crisis.

The latest round of fiscal stimulus should cause a surge in personal income during the first quarter, and a significant percentage of the population should be vaccinated or immune from prior infection by mid-2021. It is likely that local governments will be able to begin to relax restrictions even before herd immunity is reached since hospitalizations should fall once the elderly are vaccinated. As we move through the year, consumer spending growth should start to accelerate, spurred on by elevated personal savings and strong gains in household net worth. Elsewhere, the housing market will continue to benefit from tight supply and low interest rates, and business investment should rebound as corporations look to put to work record levels of precautionary cash. As a result, we expect real GDP growth to be well above potential for the year.

If the unemployment rate continues to fall at its recent pace and inflation picks up with its usual six-quarter lag behind economic activity, the experience of prior cycles would suggest that the Fed could start its hiking cycle as early as late-2022. However, the change in the Fed’s playbook will keep it sidelined for years as it looks to make up for shortfalls related to its 2% inflation target and no longer worries about an overly tight labor market.

This means the Fed is likely to keep rates at zero for several years beyond the late-2023 liftoff currently priced into the bond market. Similarly, the odds are low of a tapering of the Fed’s bond purchases in 2021. While we believe the government response to the pandemic was necessary and appropriate, investors are already paying some price with more elevated valuations due in part to the Fed’s aggressive relaunch of quantitative easing. Under these circumstances, investors will likely continue to

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 7

| ECONOMIC AND MARKET OVERVIEW (Unaudited) continued | December 31, 2020 |

take on more risk as long as more fiscal support is underway and while the Fed remains willing to backstop credit markets to support financial conditions.

The opinions and forecasts expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

8 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| QUESTIONS & ANSWERS (Unaudited) | December 31, 2020 |

The Guggenheim Enhanced Equity Income Fund (the “Fund” or “GPM”) is managed by a team of seasoned professionals at Guggenheim Partners Investment Management, LLC (“GPIM” or the “Sub-Adviser”). This team includes Farhan Sharaff, Assistant Chief Investment Officer, Equities; Qi Yan, Managing Director and Portfolio Manager; Daniel Cheeseman, Director and Portfolio Manager; and Perry Hollowell, Director and Portfolio Manager. In the following interview, the investment team discusses the market environment and the Fund’s performance for the one-year period ended December 31, 2020.

Please describe the Fund’s investment objective and explain how GPIM’s investment strategy seeks to achieve it.

The Fund’s primary investment objective is to seek a high level of current income and gains with a secondary objective of long-term capital appreciation. Under normal market conditions, the Fund invests at least 80% of its net assets, plus the amount of any borrowings for investment purposes, in equity securities. GPIM seeks to achieve the Fund’s investment objective by obtaining broadly diversified exposure to the equity markets and utilizing an option-writing strategy developed by GPIM (the “portable alpha model”). The Fund may seek to obtain exposure to equity markets through investments in individual equity securities, through investments in exchange-traded funds (“ETFs”) or other investment funds that track equity market indices, and/or through derivative instruments that replicate the economic characteristics of exposure to equity securities or markets.

The Fund utilizes leverage to seek to deliver excess returns from the portable alpha model while maintaining a risk profile similar to the large cap U.S. equity market, presenting the potential benefit of greater income and a focus on capital appreciation. Although the use of financial leverage by the Fund may create an opportunity for increased return for the Fund’s common shares, it may also result in additional risks and may magnify the effect of any losses. There can be no assurance that a leveraging strategy will be successful during any period during which it is employed.

For more information regarding Principal Investment Strategies and Fundamental Investment Restrictions of the Fund, please see the Additional Information Regarding the Fund section of this report.

Can you describe the options strategy in more detail?

The Fund has the ability to write call options on the ETFs or on indices that the ETFs may track, which will typically be at- or out-of-the-money. GPIM’s strategy typically targets one-month options, although options of any strike price or maturity may be used. The Fund may, but does not have to, write options on 100% of the equity holdings in its portfolio. The typical hedge ratio (i.e., the percentage of the Fund’s equity holdings on which options are written) for the Fund is 67%, which is designed to produce a portfolio that, inclusive of leverage, has a beta of one to broad market indices. The hedge ratio, however, may be adjusted depending on the investment team’s view of the market and GPIM’s macroeconomic views. Changing the hedge ratio will impact the beta (represents the systematic risk of a portfolio and measures its sensitivity to a benchmark) of the portfolio resulting in a portfolio that has either higher or lower risk-adjusted exposure to broad market equities.

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 9

| QUESTIONS & ANSWERS (Unaudited) continued | December 31, 2020 |

GPIM may engage in selling call options on indices, which could include securities that are not specifically held by the Fund. An option on an index is considered covered if the Fund also holds shares of a passively managed ETF that fully replicates the respective index and has a value at least equal to the notional value of the option written.

The Fund may also write call options on securities, including ETFs, that are not held by the Fund, or on indices other than the indices tracked by the ETFs held by the Fund. As such transactions would involve uncovered option writing, they may be subject to more risks compared to the Fund’s covered call option strategies involving writing options on securities, including ETFs, held by the Fund or indices tracked by the ETFs held by the Fund. When the Fund writes uncovered call options, it will earmark or segregate cash or liquid securities in accordance with applicable guidance provided by the staff of the U.S. Securities and Exchange Commission (“SEC”).

The Fund seeks to achieve its primary investment objective of seeking a high level of current income through premiums received from selling options and dividends paid on securities owned by the Fund. Although the Fund will receive premiums from the options written, by writing a covered call option, the Fund forgoes any potential increase in value of the underlying securities above the strike price specified in an option contract through the expiration date of the option.

How are managed assets allocated?

The Fund seeks to have ~67% of total assets (~100% of net assets) invested in the 500 individual stocks comprising the S&P 500 in equal weights (i.e., the S&P 500 Equal Weight Index) and ~33% of total assets (~50% of net assets) invested in a basket of broad index ETFs (S&P 500, Russell 2000, and NASDAQ-100). The hedge ratio remains ~67%, with options primarily written on indexes tracked by the ETFs in which the Fund invests.

The long equity exposure (100% of net assets) comes from an allocation to the stocks, equally weighted and rebalanced quarterly, in the S&P 500 Equal Weight Index (the “Equal Weight Index”). The exposure to the Equal Weight Index is expected to provide a higher level of beta than the capitalization weighted S&P 500 Index, as the Equal Weight Index has outperformed the market-capitalization weighted S&P 500 Index in most years since its introduction in 1990.

The other 50% of net assets is allocated in accordance with GPIM’s portable alpha model, which in this strategy currently consists of ETFs tracking the S&P 500, Russell 2000, and NASDAQ-100 Indices paired with options written for a notional amount of 100% of net assets against the S&P 500, Russell 2000, and NASDAQ-100 Indices. This portfolio will be actively rebalanced to maintain a constant net market exposure similar to the large cap U.S. equity market, which GPIM believes will allow the Fund to dynamically capture the volatility risk premium in both rising and falling equity markets.

How did the Fund perform for the one-year period ended December 31, 2020?

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the one-year period ended December 31, 2020, the Fund provided a total return based on market price of -9.16% and a total return net of fees based on NAV of 2.16%. As of

10 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| QUESTIONS & ANSWERS (Unaudited) continued | December 31, 2020 |

December 31, 2020, the Fund’s closing market price of $6.55 per share represented a discount of 11.13% to its NAV of $7.37 per share. As of December 31, 2019, the Fund’s closing market price of $8.06 per share represented a premium of 1.00% to its NAV of $7.98 per share.

Past performance is not a guarantee of future results. All NAV returns include the deduction of management fees, operating expenses, and all other Fund expenses. The market price of the Fund’s shares fluctuates from time to time, and may be higher or lower than the Fund’s NAV.

What were the Fund’s distributions during the period?

The Fund paid a distribution in each quarter of the period. On March 31, 2020, the distribution was $0.24 per share. On June 30, 2020, the distribution was reduced to $0.12 per share, and $0.12 per share was paid on September 30, 2020, and on December 31, 2020. The most recent distribution represents an annualized distribution rate of 7.33% based on the Fund’s closing market price of $6.55 per share as of December 31, 2020.

The Fund adopted a managed distribution policy effective with the June 30, 2017 distribution, under which the Fund will pay a quarterly distribution in a fixed amount until such amount is modified by the Fund’s Board of Trustees. If sufficient net investment income is not available, the distribution will be supplemented by capital gains and, to the extent necessary, return of capital. For the year ended December 31, 2020, 93% of the distributions were estimated to be characterized as a return of capital. The Fund will provide a Form 1099-DIV each calendar year that will explain the character of these distributions for federal income tax purposes.

There is no guarantee of any future distribution or that the current returns and distribution rate will be maintained. The Fund’s distribution rate is not constant and the amount of distributions, when declared by the Fund’s Board of Trustees, is subject to change based on the performance of the Fund. Please see Note 2(d) on page 44 for more information on distributions for the period.

How did other markets perform in this environment for the one-year period ended December 31, 2020?

| Index | Total Return |

Chicago Board Options Exchange Volatility Index (“VIX”) | 65.09% |

Dow Jones Industrial Average | 9.72% |

NASDAQ-100 Index | 48.88% |

Russell 2000 Index | 19.96% |

S&P 500 Equal Weight Index | 12.83% |

S&P 500 Index | 18.40% |

Discuss market volatility over the period.

A key story of the market for 2020 was that volatility ebbed, despite stocks climbing to record highs. The difficult market conditions created by the pandemic drove the VIX during the period to its highest level since the Great Recession of 2008. With the VIX gauging the richness of S&P 500 at-the-money puts and calls, the higher the VIX, the more expensive options are on it, which typically reflects uncertainty and

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 11

| QUESTIONS & ANSWERS (Unaudited) continued | December 31, 2020 |

fear of future extreme price movement. From a February low of 15, it shot up to 85 in five weeks, then almost as quickly fell once the Fed and U.S. Treasury introduced their credit market support facilities. It slumped to the mid-twenties in June and remained in that range for the rest of the period, except for a jump at the end of October, when there was concern over the outcome of the election, or at least a delay in determining it.

Still, the VIX rose 65% over the year to around 23, signaling to some investors the all-clear sign for the market. It languished in the low- to mid-teens for many years before the COVID crisis, and the long-term average is around 19. The current level could suggest the start of another stretch of low volatility, conveying optimism that vaccines were coming to the rescue, even as the caseload grew through the end of 2020. Alternatively, it could be establishing a new baseline for volatility in the coming months, reflecting the most optimism possible in a market that may be dealing with the effects of the pandemic for some time to come.

What most influenced the Fund’s performance?

For the period, the return on the underlying portfolio holdings detracted most from performance, falling to levels in the first quarter of the year that could not be overcome by strongly rising markets over the rest of the period. The Fund was helped from the allocation to ETFs that track NASDAQ-100 Index, which notably outperformed all other major indexes. The Fund’s long equity exposure is tied to the Equal Weight Index, which underperformed the cap-weighted S&P 500 Index.

The Fund’s derivative use, consisting mostly of options sold to generate income and gains, also detracted from return. Before the spell of heightened volatility in March, the VIX traded near historic lows, with realized volatility even lower, as the S&P 500 continued its upward climb. Conditions moderated after the March highs, but it remained challenging to capture the implied-realized volatility spread.

The Fund typically does better in a sustained volatility environment, whether at a low or a high level, rather than in a sharp market move, such as that in March.

Can you discuss the Fund’s approach to leverage?

Leverage was a detractor to return during the period, as the Fund’s total return was below that of the cost of leverage. Leverage at the end of the period was about 31% of the Fund’s total managed assets.

There is no guarantee that the Fund’s leverage strategy will be successful, and the Fund’s use of leverage may cause the Fund’s NAV and market price of common shares to be more volatile. Please see Note 7 on page 49 for more information on the Fund’s credit facility agreement.

Our approach to leverage is dynamic, and we tend to have a higher level of leverage when we are more constructive on equity market returns in accordance with our macroeconomic outlook and when we believe volatility is most attractive. Guggenheim maintains a favorable outlook on the equity market, especially on a 12- to 24- month time horizon. While the market has certainly staged an impressive rally off the March lows, in reality we are not much above peak levels reached in mid-February. Vaccines and fiscal stimulus should drive strong growth in 2021, with gains in income, net worth, and over $1.5

12 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| QUESTIONS & ANSWERS (Unaudited) continued | December 31, 2020 |

trillion in excess savings strengthening consumption growth by the second half of the year as spending opportunities normalize.

Index Definitions

Indices are unmanaged, reflect no expenses and it is not possible to invest directly in an index.

CBOE (Chicago Board Options Exchange) Volatility Index, often referred to as the VIX (its ticker symbol), the fear index or the fear gauge, is a measure of the implied volatility of S&P 500 Index options. It represents a measure of the market’s expectation of stock market volatility over the next 30-day period. Quoted in percentage points, the VIX represents the expected daily movement in the S&P 500 Index over the next 30-day period, which is then annualized.

Dow Jones Industrial Average® is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq.

NASDAQ-100® Index includes 100 of the largest domestic and international non-financial securities listed on the Nasdaq Stock Market based on market capitalization. The Index reflects companies across major industry groups including computer hardware and software, telecommunications, retail/wholesale trade and biotechnology. It does not contain securities of financial companies including investment companies.

Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe.

S&P 500® Equal Weight Index has the same constituents as the S&P 500, but each company is assigned a fixed equal weight.

S&P 500® Index is an unmanaged, capitalization-weighted index of 500 stocks. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Risks and Other Considerations

The global ongoing crisis caused by the outbreak of COVID-19 is causing materially reduced consumer demand and economic output, disrupting supply chains, resulting in market closures, travel restrictions and quarantines, and adversely impacting local and global economies. Investors should be aware that in light of the current uncertainty, volatility and distress in economies, financial markets, and labor and health conditions all over the world, the Fund’s investments and a shareholder’s investment in the Fund are subject to sudden and substantial losses, increased volatility and other adverse events. Firms through which investors invest with the Fund, the Fund, its service providers, the markets in which it invests and market intermediaries are also impacted by quarantines and similar measures intended to contain the ongoing pandemic, which can obstruct their functioning and subject them to heightened operational risks.

The views expressed in this report reflect those of the portfolio managers only through the report period as stated on the cover. These views are subject to change at any time, based on market and other

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 13

| QUESTIONS & ANSWERS (Unaudited) continued | December 31, 2020 |

conditions and should not be construed as a recommendation of any kind. The material may also include forward looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come to pass.

There can be no assurance that the Fund will achieve its investment objectives. The value of the Fund will fluctuate with the value of the underlying securities. Risk is inherent in all investing, including the loss of your entire principal. Therefore, before investing you should consider the risks carefully. The Fund is subject to several risk factors. Certain of these risk factors are described below. Please see the Additional Information Regarding the Fund section of this report, the Fund’s Prospectus, Statement of Additional Information (SAI) and guggenheiminvestments.com/gpm for a more detailed description of the risks of investing in the Fund. Shareholders may access the Fund’s Prospectus and SAI on the EDGAR Database on the Securities and Exchange Commission’s website at www.sec.gov.

Investors should be aware that in light of the current uncertainty, volatility and distress in economies, financial markets, and labor and health conditions around the world, the risks below are heightened significantly compared to normal conditions and therefore subject the Fund’s investments and a shareholder’s investment in the Fund to sudden and substantial losses. The fact that a particular risk below is not specifically identified as being heightened under current conditions does not mean that the risk is not greater than under normal conditions.

Covered Call Option Strategy Risk. The ability of the Fund to achieve its investment objective is partially dependent on the successful implementation of its covered call option strategy. The Fund may write call options on individual securities. The buyer of an option acquires the right to buy (a call option) or sell (a put option) a certain quantity of a security (the underlying security) or instrument, at a certain price up to a specified point in time or on expiration, depending on the terms. The seller or writer of an option is obligated to sell (a call option) or buy (a put option) the underlying instrument. A call option is “covered” if the Fund owns the security underlying the call or has an absolute right to acquire the security without additional cash consideration (or, if additional cash consideration is required, cash or cash equivalents in such amount are segregated by the Fund’s custodian). As a seller of covered call options, the Fund faces the risk that it will forgo the opportunity to profit from increases in the market value of the security covering the call option during an option’s life. As the Fund writes covered calls over more of its portfolio, its ability to benefit from capital appreciation becomes more limited.

Derivatives Transactions Risk. The Fund may utilize derivatives, including forwards, swaps, futures contracts and other strategic transactions, to seek to earn income, facilitate portfolio management and mitigate risks. Participation in derivatives markets transactions involves investment risks and transaction costs to which the Fund would not be subject absent the use of these strategies (other than its covered call writing strategy and put option writing strategy). If the Sub-Adviser or GPIM is incorrect about its expectations of market conditions, the use of derivatives could also result in a loss, which in some cases may be unlimited.

Forwards Risk. The Fund may enter into forward contracts. A forward contract is an over-the-counter derivative transaction between two parties to buy or sell a specified amount of an underlying reference at a specified price (or rate) on a specified date in the future. Forward contracts are negotiated on an

14 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| QUESTIONS & ANSWERS (Unaudited) continued | December 31, 2020 |

individual basis and are not standardized or traded on exchanges. Forwards used for hedging or to increase income or investment gains may not be successful, resulting in losses to the Fund, and the cost of such strategies may reduce the Fund’s returns. Forwards are subject to the risks associated with derivatives.

Swap Risk. The Fund may enter into swap transactions, including credit default swaps, total return swaps, index swaps, currency swaps, commodity swaps and interest rate swaps, as well as options thereon, and may purchase or sell interest rate caps, floors and collars. Swap transactions are subject to market risk, counterparty credit, correlation, valuation, liquidity and leveraging risks and could result in substantial losses to the Fund. Swaps generally do not involve the delivery of securities, other underlying assets or principal. Accordingly, the risk of loss with respect to swaps generally is limited to the net amount of payments that the Fund is contractually obligated to make, or in the case of the other party to a swap defaulting, the net amount of payments that the Fund is contractually entitled to receive. Total return swaps may effectively add leverage to the Fund’s portfolio because the Fund would be subject to investment exposure on the full notional amount of the swap. Total return swaps are subject to the risk that a counterparty will default on its payment obligations to the Fund thereunder.

Futures Risk. The Fund may invest in futures contracts. Futures and options on futures entail certain risks, including but not limited to the following:

| ● | no assurance that futures contracts or options on futures can be offset at favorable prices; |

| ● | possible reduction of the return of the Fund due to their use for hedging; |

| ● | possible reduction in value of both the securities hedged and the hedging instrument; |

| ● | possible lack of liquidity due to daily limits on price fluctuations; |

| ● | imperfect correlation between the contracts and the securities being hedged; and |

| ● | losses from investing in futures transactions that are potentially unlimited and the segregation requirements for such transactions. |

Synthetic Investment Risk. As an alternative to holding investments directly, the Fund may also obtain investment exposure to income securities and common equity securities through the use of customized derivative instruments (including swaps, options, forwards or other financial instruments) to replicate, modify or replace the economic attributes associated with an investment in income securities and common equity securities. The Fund may be exposed to certain additional risks to the extent the Sub-Adviser uses derivatives as a means to synthetically implement the Fund’s investment strategies. If the Fund enters into a derivative instrument whereby it agrees to receive the return of a security or financial instrument or a basket of securities or financial instruments, it will typically contract to receive such returns for a predetermined period of time. During such period, the Fund may not have the ability to increase or decrease its exposure. In addition, such customized derivative instruments will likely be highly illiquid, and it is possible that the Fund will not be able to terminate such derivative instruments prior to their expiration date or that the penalties associated with such a termination might impact the Fund’s performance in a material adverse manner. Furthermore, derivative instruments typically contain

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 15

| QUESTIONS & ANSWERS (Unaudited) continued | December 31, 2020 |

provisions giving the counterparty the right to terminate the contract upon the occurrence of certain events. Such events may include a decline in the value of the reference securities and material violations of the terms of the contract or the portfolio guidelines as well as other events determined by the counterparty. If a termination were to occur, the Fund’s return could be adversely affected as it would lose the benefit of the indirect exposure to the reference securities and it may incur significant termination expenses.

Equity Securities Risk. Equity securities include common stocks and other equity and equity-related securities (and securities convertible into stocks) such as limited liability company interests and trust certificates. The prices of equity securities generally fluctuate in value more than fixed-income investments, may rise or fall rapidly or unpredictably and may reflect real or perceived changes in the issuing company’s financial condition and changes in the overall market or economy. Equity securities have experienced heightened volatility over recent periods and therefore, the Fund’s investments in equity securities are subject to heightened risks related to volatility. A decline in the value of equity securities held by the Fund will adversely affect the value of your investment in the Fund.

Investment Funds Risk/Other Investment Companies Risk. As an alternative to holding investments directly, the Fund may invest in securities of other open- or closed-end investment companies, including exchange-traded funds. Investments in investment funds present certain special considerations and risks not present in making direct investments in credit securities and common equity securities. Investments in other investment companies involve operating expenses and fees that are in addition to the expenses and fees borne by the Fund. Such expenses and fees attributable to the Fund’s investments in other investment companies are borne indirectly by common shareholders. The Fund and its shareholders will incur its pro rata share of the expenses of the underlying investment companies or vehicles in which the Fund invests, such as investment advisory and other management expenses operating expense. To the extent management fees of other investment companies are based on total gross assets, it may create an incentive for such entities’ managers to employ financial leverage, thereby adding additional expense and increasing volatility and risk. Investments in other investment companies also expose the Fund to additional management risk; the success of the Fund’s investments in other investment companies will depend in large part on the investment skills and implementation abilities of the advisers or managers of such entities. Decisions made by the advisers or managers of such entities may cause the Fund to incur losses or to miss profit opportunities.

Leverage Risk. The Fund’s use of leverage, through indebtedness or instruments such as derivatives, causes the Fund to be more volatile and riskier than if it had not been leveraged. Although the use of leverage by the Fund may create an opportunity for increased return, it also results in additional risks and can magnify the effect of any losses. The effect of leverage in a declining market is likely to cause a greater decline in the net asset value of the Fund than if the Fund were not leveraged, which may result in a greater decline in the market price of the Fund shares. There can be no assurance that a leveraging strategy will be implemented or that it will be successful during any period during which it is employed. Recent economic and market events have contributed to severe market volatility and caused severe liquidity strains in the credit markets. If dislocations in the credit markets continue, the Fund’s leverage costs may increase and there is a risk that the Fund may not be able to renew or replace existing

16 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| QUESTIONS & ANSWERS (Unaudited) continued | December 31, 2020 |

leverage on favorable terms or at all. If the cost of leverage is no longer favorable, or if the Fund is otherwise required to reduce its leverage, the Fund may not be able to maintain distributions at historical levels and common shareholders will bear any costs associated with selling portfolio securities. The Fund’s total leverage may vary significantly over time. To the extent the Fund increases its amount of leverage outstanding, it will be more exposed to these risks.

Management Risk. The Fund is actively managed, which means that investment decisions are made based on investment views. There is no guarantee that the investment views will produce the desired results or expected returns, causing the Fund to fail to meet its investment objective or underperform its benchmark index or funds with similar investment objectives and strategies.

Market Risk. The value of, or income generated by, the investments held by the Fund are subject to the possibility of rapid and unpredictable fluctuation. The value of certain investments (e.g., equity securities) tends to fluctuate more dramatically over the shorter term than do the value of other asset classes. These movements may result from factors affecting individual companies, or from broader influences, including real or perceived changes in prevailing interest rates, changes in inflation or expectations about inflation, investor confidence or economic, political, social or financial market conditions, natural/environmental disasters, cyber attacks, terrorism, governmental or quasi-governmental actions, public health emergencies (such as the spread of infectious diseases, pandemics and epidemics) and other similar events, each of which may be temporary or last for extended periods. For example, the crisis initially caused by the outbreak of COVID-19 is causing materially reduced consumer demand and economic output, disrupting supply chains, resulting in market closures, travel restrictions and quarantines, and adversely impacting local and global economies. As with other serious economic disruptions, governmental authorities and regulators are responding to this crisis with significant fiscal and monetary policy changes, which could further increase volatility in securities and other financial markets, reduce market liquidity, heighten investor uncertainty and adversely affect the value of the Fund’s investments and the performance of the Fund. Administrative changes, policy reform and/or changes in law or governmental regulations can result in expropriation or nationalization of the investments of a company in which the Fund invests.

Mid-Cap And Small-Cap Company Risk. Investing in the securities of medium-sized or small market capitalizations (“mid-cap” and “small-cap” companies, respectively) presents some particular investment risks. The Fund is subject to the risk that mid-cap and small-cap securities may underperform other segments of the equity market or the equity market as a whole. Securities of mid-cap and small-cap companies may be more speculative, volatile and less liquid than securities of large companies. Mid-cap and small-cap companies tend to have inexperienced management as well as limited product and market diversification and financial resources, and may be more vulnerable to adverse developments than large capitalization companies.

In addition to the foregoing risks, investors should note that the Fund reserves the right to merge or reorganize with another fund, liquidate or convert into an open-end fund, in each case subject to applicable approvals by shareholders and the Fund’s Board of Trustees as required by law and the Fund’s governing documents.

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 17

| QUESTIONS & ANSWERS (Unaudited) continued | December 31, 2020 |

This material is not intended as a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes only and is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

18 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| FUND SUMMARY (Unaudited) | December 31, 2020 |

| Fund Statistics | ||||

Share Price | $6.55 | |||

Net Asset Value | $7.37 | |||

Discount to NAV | -11.13% | |||

Net Assets ($000) | $356,074 |

AVERAGE ANNUAL TOTAL RETURNS1 | ||||

| FOR THE PERIOD ENDED DECEMBER 31, 2020 | ||||

| One | Three | Five | Ten | |

| Year | Year | Year | Year | |

Guggenheim Enhanced | ||||

Equity Income Fund | ||||

| NAV | 2.16% | 4.65% | 9.05% | 8.47% |

| Market | (9.16%) | 1.48% | 8.90% | 8.10% |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. All NAV returns include the deduction of management fees, operating expenses and all other Fund expenses. The deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares is not reflected in the total returns. For the most recent month-end performance figures, please visit guggenheiminvestments.com/gpm. The investment return and principal value of an investment will fluctuate with changes in market conditions and other factors so that an investor’s shares, when sold, may be worth more or less than their original cost.

1 Performance prior to June 22, 2010, under the name Old Mutual/Claymore Long-Short Fund was achieved through an investment strategy of a long-short strategy and an opportunistic covered call writing strategy by the previous investment sub-adviser, Analytic Investors, LLC, and factors in the Fund’s fees and expenses.

| Portfolio Breakdown | % of Net Assets |

Common Stocks | |

| Consumer, Non-cyclical | 21.1% |

| Financial | 18.7% |

| Industrial | 13.9% |

| Consumer, Cyclical | 13.6% |

| Technology | 11.3% |

| Communications | 6.3% |

| Utilities | 5.5% |

| Other | 8.2% |

Exchange-Traded Funds | 45.1% |

Money Market Fund | 3.2% |

| Total Investments | 146.9% |

Options Written | -1.7% |

Other Assets & Liabilities, net | -45.2% |

| Net Assets | 100.0% |

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 19

| FUND SUMMARY (Unaudited) concluded | December 31, 2020 |

Portfolio breakdown is subject to change daily. For more information, please visit guggenheiminvestments.com/gpm. The above summaries are provided for informational purposes only and should not be viewed as recommendations. Past performance does not guarantee future results. All or a portion of the above distributions may be characterized as a return of capital. For the year ended December 31, 2020, 93% of the distributions were characterized as return of capital.

20 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| SCHEDULE OF INVESTMENTS | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% | ||

| Consumer, Non-cyclical – 21.1% | ||

Alexion Pharmaceuticals, Inc.*,1 | 5,697 | $ 890,099 |

ABIOMED, Inc.*,1 | 2,667 | 864,641 |

Global Payments, Inc.1 | 3,589 | 773,142 |

IDEXX Laboratories, Inc.*,1 | 1,510 | 754,804 |

PayPal Holdings, Inc.*,1 | 3,220 | 754,124 |

Catalent, Inc.* | 7,237 | 753,154 |

Nielsen Holdings plc1 | 36,086 | 753,115 |

Zimmer Biomet Holdings, Inc.1 | 4,865 | 749,648 |

DaVita, Inc.*,1 | 6,363 | 747,016 |

Edwards Lifesciences Corp.* | 8,188 | 746,991 |

Estee Lauder Companies, Inc. — Class A1 | 2,805 | 746,663 |

Illumina, Inc.*,1 | 2,015 | 745,550 |

Viatris, Inc.*,1 | 39,749 | 744,896 |

Intuitive Surgical, Inc.*,1 | 907 | 742,017 |

Teleflex, Inc. | 1,798 | 740,003 |

West Pharmaceutical Services, Inc. | 2,611 | 739,722 |

Cooper Companies, Inc.1 | 2,032 | 738,266 |

Verisk Analytics, Inc. — Class A1 | 3,553 | 737,567 |

Boston Scientific Corp.*,1 | 20,513 | 737,442 |

Incyte Corp.*,1 | 8,478 | 737,416 |

IQVIA Holdings, Inc.* | 4,107 | 735,851 |

Constellation Brands, Inc. — Class A1 | 3,357 | 735,351 |

Rollins, Inc. | 18,796 | 734,360 |

DexCom, Inc.* | 1,982 | 732,785 |

Moody’s Corp.1 | 2,510 | 728,502 |

Stryker Corp. | 2,968 | 727,279 |

Eli Lilly & Co.1 | 4,306 | 727,025 |

Vertex Pharmaceuticals, Inc.* | 3,074 | 726,509 |

Align Technology, Inc.*,1 | 1,359 | 726,222 |

Monster Beverage Corp.* | 7,831 | 724,211 |

Humana, Inc.1 | 1,762 | 722,896 |

HCA Healthcare, Inc.1 | 4,374 | 719,348 |

Medtronic plc1 | 6,133 | 718,420 |

MarketAxess Holdings, Inc.1 | 1,258 | 717,765 |

UnitedHealth Group, Inc. | 2,045 | 717,141 |

Brown-Forman Corp. — Class B1 | 9,025 | 716,856 |

ResMed, Inc. | 3,370 | 716,327 |

Universal Health Services, Inc. — Class B | 5,208 | 716,100 |

Zoetis, Inc. | 4,320 | 714,960 |

Gartner, Inc.*,1 | 4,453 | 713,326 |

Avery Dennison Corp.1 | 4,595 | 712,731 |

Becton Dickinson and Co.1 | 2,840 | 710,625 |

See notes to financial statements.

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 21

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Consumer, Non-cyclical – 21.1% (continued) | ||

Anthem, Inc.1 | 2,213 | $ 710,572 |

Johnson & Johnson1 | 4,506 | 709,154 |

Coca-Cola Co.1 | 12,919 | 708,478 |

Bio-Rad Laboratories, Inc. — Class A* | 1,215 | 708,272 |

Conagra Brands, Inc.1 | 19,498 | 706,997 |

Equifax, Inc.1 | 3,663 | 706,373 |

Campbell Soup Co.1 | 14,599 | 705,862 |

McCormick & Company, Inc.1 | 7,378 | 705,337 |

Abbott Laboratories1 | 6,440 | 705,116 |

PepsiCo, Inc. | 4,754 | 705,018 |

Bristol-Myers Squibb Co.1 | 11,351 | 704,103 |

Hershey Co.1 | 4,622 | 704,069 |

Procter & Gamble Co.1 | 5,049 | 702,518 |

Lamb Weston Holdings, Inc. | 8,919 | 702,282 |

Mondelez International, Inc.— Class A | 12,008 | 702,108 |

STERIS plc | 3,701 | 701,488 |

Kraft Heinz Co.1 | 20,230 | 701,172 |

Church & Dwight Company, Inc.1 | 8,028 | 700,282 |

Automatic Data Processing, Inc.1 | 3,972 | 699,867 |

Biogen, Inc.*,1 | 2,855 | 699,075 |

Kroger Co.1 | 21,993 | 698,498 |

Cintas Corp.1 | 1,974 | 697,730 |

S&P Global, Inc. | 2,122 | 697,565 |

Archer-Daniels-Midland Co.1 | 13,837 | 697,523 |

Baxter International, Inc.1 | 8,687 | 697,045 |

Amgen, Inc.1 | 3,031 | 696,888 |

Colgate-Palmolive Co.1 | 8,139 | 695,966 |

Corteva, Inc.1 | 17,954 | 695,179 |

AbbVie, Inc.1 | 6,481 | 694,439 |

Regeneron Pharmaceuticals, Inc.* | 1,436 | 693,746 |

IHS Markit Ltd. | 7,715 | 693,039 |

J M Smucker Co. | 5,984 | 691,750 |

Varian Medical Systems, Inc.* | 3,948 | 690,940 |

Kellogg Co.1 | 11,097 | 690,566 |

Clorox Co.1 | 3,417 | 689,961 |

Quanta Services, Inc. | 9,563 | 688,727 |

Laboratory Corporation of America Holdings*,1 | 3,376 | 687,185 |

AmerisourceBergen Corp. — Class A1 | 7,029 | 687,155 |

FleetCor Technologies, Inc.*,1 | 2,518 | 686,986 |

McKesson Corp. | 3,946 | 686,288 |

Cigna Corp.1 | 3,292 | 685,329 |

Danaher Corp.1 | 3,080 | 684,191 |

See notes to financial statements.

22 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Consumer, Non-cyclical – 21.1% (continued) | ||

Kimberly-Clark Corp.1 | 5,068 | $ 683,318 |

General Mills, Inc.1 | 11,619 | 683,197 |

Centene Corp.*,1 | 11,353 | 681,521 |

Dentsply Sirona, Inc.1 | 13,014 | 681,413 |

Thermo Fisher Scientific, Inc. | 1,462 | 680,970 |

Hormel Foods Corp.1 | 14,602 | 680,599 |

Merck & Company, Inc. | 8,308 | 679,594 |

Cardinal Health, Inc.1 | 12,639 | 676,945 |

Hologic, Inc.*,1 | 9,274 | 675,425 |

Sysco Corp. | 9,083 | 674,504 |

Quest Diagnostics, Inc. | 5,647 | 672,953 |

Philip Morris International, Inc. | 8,109 | 671,344 |

Robert Half International, Inc. | 10,736 | 670,785 |

United Rentals, Inc.* | 2,863 | 663,958 |

Gilead Sciences, Inc.1 | 11,344 | 660,902 |

Henry Schein, Inc.* | 9,853 | 658,772 |

Molson Coors Beverage Co. — Class B | 14,572 | 658,509 |

CVS Health Corp.1 | 9,629 | 657,661 |

Altria Group, Inc.1 | 16,029 | 657,189 |

Perrigo Company plc1 | 14,416 | 644,683 |

Tyson Foods, Inc. — Class A | 9,947 | 640,985 |

Pfizer, Inc.1 | 16,762 | 617,009 |

| Total Consumer, Non-cyclical | 75,077,941 | |

| Financial – 18.7% | ||

First Republic Bank | 5,317 | 781,227 |

SVB Financial Group* | 1,970 | 764,025 |

Goldman Sachs Group, Inc.1 | 2,872 | 757,375 |

Mastercard, Inc. — Class A | 2,105 | 751,359 |

Cincinnati Financial Corp.1 | 8,597 | 751,120 |

Discover Financial Services1 | 8,258 | 747,597 |

Cboe Global Markets, Inc.1 | 8,017 | 746,543 |

Morgan Stanley | 10,885 | 745,949 |

Synchrony Financial | 21,359 | 741,371 |

Charles Schwab Corp. | 13,944 | 739,590 |

Capital One Financial Corp.1 | 7,478 | 739,200 |

Digital Realty Trust, Inc. REIT1 | 5,291 | 738,147 |

JPMorgan Chase & Co.1 | 5,765 | 732,559 |

Bank of America Corp.1 | 24,125 | 731,229 |

Visa, Inc. — Class A | 3,342 | 730,996 |

Comerica, Inc.1 | 13,081 | 730,705 |

Intercontinental Exchange, Inc.1 | 6,334 | 730,247 |

See notes to financial statements.

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 23

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Financial – 18.7% (continued) | ||

Hartford Financial Services Group, Inc.1 | 14,906 | $ 730,096 |

Nasdaq, Inc. | 5,484 | 727,946 |

Bank of New York Mellon Corp.1 | 17,128 | 726,912 |

Allstate Corp.1 | 6,600 | 725,538 |

Extra Space Storage, Inc. REIT1 | 6,243 | 723,314 |

Public Storage REIT | 3,132 | 723,273 |

Weyerhaeuser Co. REIT | 21,539 | 722,203 |

Progressive Corp. | 7,302 | 722,022 |

Citigroup, Inc.1 | 11,696 | 721,175 |

Duke Realty Corp. REIT | 17,977 | 718,541 |

Zions Bancorp North America1 | 16,536 | 718,324 |

Mid-America Apartment Communities, Inc. REIT | 5,665 | 717,699 |

Travelers Companies, Inc. | 5,107 | 716,869 |

Wells Fargo & Co. | 23,702 | 715,326 |

BlackRock, Inc. — Class A1 | 991 | 715,046 |

Regions Financial Corp. | 44,353 | 714,970 |

PNC Financial Services Group, Inc. | 4,798 | 714,902 |

Equinix, Inc. REIT1 | 1,000 | 714,180 |

Raymond James Financial, Inc. | 7,464 | 714,081 |

KeyCorp1 | 43,513 | 714,048 |

Aon plc — Class A1 | 3,377 | 713,459 |

Northern Trust Corp. | 7,650 | 712,521 |

Alexandria Real Estate Equities, Inc. REIT1 | 3,994 | 711,811 |

Arthur J Gallagher & Co.1 | 5,747 | 710,961 |

Loews Corp.1 | 15,787 | 710,731 |

Willis Towers Watson plc1 | 3,372 | 710,413 |

Healthpeak Properties, Inc. REIT1 | 23,500 | 710,405 |

Assurant, Inc.1 | 5,213 | 710,115 |

Realty Income Corp. REIT1 | 11,400 | 708,738 |

Franklin Resources, Inc.1 | 28,329 | 707,942 |

W R Berkley Corp. | 10,638 | 706,576 |

Berkshire Hathaway, Inc. — Class B*,1 | 3,044 | 705,812 |

SBA Communications Corp. REIT | 2,501 | 705,607 |

Prologis, Inc. REIT | 7,079 | 705,493 |

American Tower Corp. — Class A REIT1 | 3,135 | 703,682 |

Truist Financial Corp. | 14,662 | 702,750 |

Kimco Realty Corp. REIT1 | 46,729 | 701,402 |

Principal Financial Group, Inc. | 14,132 | 701,088 |

U.S. Bancorp | 15,036 | 700,527 |

Marsh & McLennan Companies, Inc.1 | 5,971 | 698,607 |

Globe Life, Inc. | 7,356 | 698,526 |

Ameriprise Financial, Inc.1 | 3,594 | 698,422 |

See notes to financial statements.

24 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Financial – 18.7% (continued) | ||

M&T Bank Corp.1 | 5,477 | $ 697,222 |

Citizens Financial Group, Inc. | 19,487 | 696,855 |

Everest Re Group Ltd. | 2,975 | 696,418 |

CME Group, Inc. — Class A1 | 3,823 | 695,977 |

Crown Castle International Corp. REIT1 | 4,371 | 695,819 |

Fifth Third Bancorp1 | 25,210 | 695,040 |

Host Hotels & Resorts, Inc. REIT1 | 47,501 | 694,940 |

UDR, Inc. REIT | 18,071 | 694,469 |

Equity Residential REIT1 | 11,694 | 693,220 |

Welltower, Inc. REIT1 | 10,727 | 693,179 |

American Express Co.1 | 5,732 | 693,056 |

SL Green Realty Corp. REIT | 11,612 | 691,843 |

Chubb Ltd.1 | 4,483 | 690,023 |

Ventas, Inc. REIT | 14,052 | 689,110 |

State Street Corp. | 9,468 | 689,081 |

T. Rowe Price Group, Inc. | 4,550 | 688,824 |

MetLife, Inc. | 14,606 | 685,752 |

Prudential Financial, Inc. | 8,771 | 684,752 |

People’s United Financial, Inc. | 52,937 | 684,475 |

Aflac, Inc.1 | 15,371 | 683,548 |

Western Union Co. | 31,145 | 683,321 |

AvalonBay Communities, Inc. REIT1 | 4,245 | 681,025 |

Unum Group | 29,619 | 679,460 |

Lincoln National Corp.1 | 13,428 | 675,563 |

Huntington Bancshares, Inc.1 | 53,306 | 673,255 |

American International Group, Inc.1 | 17,769 | 672,734 |

Invesco Ltd.1 | 38,592 | 672,659 |

Essex Property Trust, Inc. REIT1 | 2,825 | 670,711 |

Iron Mountain, Inc. REIT1 | 22,687 | 668,813 |

Simon Property Group, Inc. REIT | 7,841 | 668,680 |

Regency Centers Corp. REIT | 14,640 | 667,438 |

Vornado Realty Trust REIT | 17,764 | 663,308 |

CBRE Group, Inc. — Class A*,1 | 10,419 | 653,480 |

Boston Properties, Inc. REIT1 | 6,894 | 651,690 |

Federal Realty Investment Trust REIT1 | 7,646 | 650,827 |

| Total Financial | 66,457,859 | |

| Industrial – 13.9% | ||

Howmet Aerospace, Inc.1 | 26,078 | 744,266 |

Vontier Corp.*,2 | 22,105 | 738,307 |

Vulcan Materials Co. | 4,963 | 736,063 |

Martin Marietta Materials, Inc.1 | 2,580 | 732,643 |

See notes to financial statements.

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 25

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Industrial – 13.9% (continued) | ||

Allegion plc1 | 6,290 | $ 732,030 |

Otis Worldwide Corp. | 10,815 | 730,553 |

Deere & Co.1 | 2,695 | 725,090 |

Expeditors International of Washington, Inc.1 | 7,617 | 724,453 |

FLIR Systems, Inc. | 16,469 | 721,836 |

Keysight Technologies, Inc.* | 5,457 | 720,815 |

Dover Corp.1 | 5,679 | 716,974 |

Eaton Corporation plc1 | 5,962 | 716,275 |

Kansas City Southern1 | 3,506 | 715,680 |

Trane Technologies plc1 | 4,925 | 714,913 |

Xylem, Inc.1 | 6,999 | 712,428 |

Fortive Corp. | 10,054 | 712,024 |

IDEX Corp. | 3,572 | 711,542 |

Pentair plc1 | 13,394 | 711,087 |

Fortune Brands Home & Security, Inc.1 | 8,281 | 709,847 |

Waters Corp.* | 2,868 | 709,601 |

Amcor plc | 60,249 | 709,131 |

TransDigm Group, Inc.* | 1,145 | 708,583 |

Ingersoll Rand, Inc.*,1 | 15,552 | 708,549 |

Union Pacific Corp. | 3,394 | 706,699 |

TE Connectivity Ltd.1 | 5,837 | 706,686 |

Roper Technologies, Inc. | 1,639 | 706,557 |

Johnson Controls International plc1 | 15,131 | 704,953 |

Sealed Air Corp. | 15,395 | 704,937 |

Waste Management, Inc. | 5,972 | 704,278 |

AMETEK, Inc.1 | 5,822 | 704,113 |

Stanley Black & Decker, Inc. | 3,934 | 702,455 |

Packaging Corporation of America | 5,084 | 701,134 |

Rockwell Automation, Inc. | 2,794 | 700,763 |

Caterpillar, Inc.1 | 3,844 | 699,685 |

Carrier Global Corp. | 18,548 | 699,631 |

Textron, Inc. | 14,471 | 699,383 |

Republic Services, Inc. — Class A | 7,257 | 698,849 |

Northrop Grumman Corp. | 2,293 | 698,723 |

Teledyne Technologies, Inc.* | 1,779 | 697,332 |

Masco Corp.1 | 12,682 | 696,622 |

Norfolk Southern Corp. | 2,930 | 696,197 |

CH Robinson Worldwide, Inc.1 | 7,398 | 694,450 |

Ball Corp.1 | 7,445 | 693,725 |

Garmin Ltd.1 | 5,795 | 693,430 |

3M Co. | 3,960 | 692,168 |

CSX Corp.1 | 7,622 | 691,697 |

See notes to financial statements.

26 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Industrial – 13.9% (continued) | ||

Jacobs Engineering Group, Inc.1 | 6,344 | $ 691,242 |

Illinois Tool Works, Inc.1 | 3,386 | 690,337 |

United Parcel Service, Inc. — Class B | 4,093 | 689,261 |

Agilent Technologies, Inc.1 | 5,817 | 689,256 |

Westrock Co. | 15,834 | 689,254 |

L3Harris Technologies, Inc. | 3,643 | 688,600 |

Amphenol Corp. — Class A1 | 5,261 | 687,981 |

Mettler-Toledo International, Inc.* | 602 | 686,087 |

Flowserve Corp.1 | 18,583 | 684,784 |

Parker-Hannifin Corp. | 2,509 | 683,477 |

Honeywell International, Inc. | 3,211 | 682,980 |

J.B. Hunt Transport Services, Inc.1 | 4,962 | 678,057 |

General Dynamics Corp.1 | 4,555 | 677,875 |

PerkinElmer, Inc. | 4,719 | 677,176 |

Lockheed Martin Corp.1 | 1,905 | 676,237 |

Raytheon Technologies Corp. | 9,456 | 676,199 |

Westinghouse Air Brake Technologies Corp.1 | 9,208 | 674,026 |

Emerson Electric Co.1 | 8,362 | 672,054 |

A O Smith Corp. | 12,229 | 670,394 |

Old Dominion Freight Line, Inc. | 3,432 | 669,858 |

General Electric Co.1 | 61,761 | 667,019 |

Huntington Ingalls Industries, Inc.1 | 3,878 | 661,121 |

Snap-on, Inc. | 3,813 | 652,557 |

Boeing Co.1 | 2,992 | 640,468 |

FedEx Corp.1 | 2,381 | 618,155 |

| Total Industrial | 49,531,612 | |

| Consumer, Cyclical – 13.6% | ||

Tesla, Inc.* | 1,130 | 797,407 |

Pool Corp. | 2,040 | 759,900 |

Ross Stores, Inc. | 6,109 | 750,246 |

Copart, Inc.* | 5,892 | 749,757 |

Ulta Beauty, Inc.* | 2,597 | 745,755 |

Leggett & Platt, Inc.1 | 16,742 | 741,671 |

Chipotle Mexican Grill, Inc. — Class A*,1 | 530 | 734,956 |

Aptiv plc1 | 5,638 | 734,575 |

Hilton Worldwide Holdings, Inc. | 6,580 | 732,091 |

Tapestry, Inc. | 23,500 | 730,380 |

BorgWarner, Inc.1 | 18,873 | 729,253 |

Darden Restaurants, Inc.1 | 6,115 | 728,419 |

Hasbro, Inc.1 | 7,744 | 724,374 |

Las Vegas Sands Corp. | 12,145 | 723,842 |

See notes to financial statements.

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 27

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Consumer, Cyclical – 13.6% (continued) | ||

Lennar Corp. — Class A1 | 9,473 | $ 722,127 |

Mohawk Industries, Inc.* | 5,115 | 720,959 |

Hanesbrands, Inc.1 | 49,373 | 719,858 |

MGM Resorts International | 22,838 | 719,625 |

Alaska Air Group, Inc.1 | 13,818 | 718,536 |

Starbucks Corp.1 | 6,692 | 715,910 |

Cummins, Inc.1 | 3,152 | 715,819 |

Live Nation Entertainment, Inc.* | 9,717 | 714,005 |

Newell Brands, Inc. | 33,605 | 713,434 |

Genuine Parts Co.1 | 7,101 | 713,153 |

TJX Companies, Inc. | 10,434 | 712,538 |

McDonald’s Corp.1 | 3,317 | 711,762 |

NIKE, Inc. — Class B | 5,016 | 709,613 |

Target Corp. | 4,014 | 708,591 |

AutoZone, Inc.*,1 | 597 | 707,708 |

Marriott International, Inc. — Class A1 | 5,363 | 707,487 |

Yum! Brands, Inc.1 | 6,503 | 705,966 |

Ralph Lauren Corp. — Class A | 6,801 | 705,536 |

PulteGroup, Inc. | 16,275 | 701,778 |

NVR, Inc.* | 172 | 701,736 |

Dollar General Corp.1 | 3,336 | 701,561 |

Lowe’s Companies, Inc.1 | 4,367 | 700,947 |

Wynn Resorts Ltd.1 | 6,210 | 700,674 |

Carnival Corp.1 | 32,329 | 700,246 |

Southwest Airlines Co. | 15,023 | 700,222 |

Dollar Tree, Inc.*,1 | 6,469 | 698,911 |

Tractor Supply Co. | 4,971 | 698,823 |

WW Grainger, Inc.1 | 1,708 | 697,445 |

O’Reilly Automotive, Inc.* | 1,538 | 696,053 |

PACCAR, Inc. | 8,065 | 695,848 |

CarMax, Inc.*,1 | 7,338 | 693,148 |

Costco Wholesale Corp.1 | 1,837 | 692,145 |

Home Depot, Inc.1 | 2,605 | 691,940 |

Tiffany & Co. | 5,252 | 690,375 |

Domino’s Pizza, Inc. | 1,798 | 689,461 |

Advance Auto Parts, Inc.1 | 4,372 | 688,634 |

PVH Corp. | 7,307 | 686,054 |

General Motors Co.1 | 16,442 | 684,645 |

Fastenal Co.1 | 14,006 | 683,913 |

Best Buy Company, Inc.1 | 6,851 | 683,661 |

DR Horton, Inc.1 | 9,859 | 679,482 |

See notes to financial statements.

28 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Consumer, Cyclical – 13.6% (continued) | ||

VF Corp. | 7,953 | $ 679,266 |

Whirlpool Corp. | 3,747 | 676,296 |

Walmart, Inc. | 4,689 | 675,919 |

Royal Caribbean Cruises Ltd. | 9,014 | 673,256 |

Ford Motor Co.1 | 76,413 | 671,671 |

Gap, Inc.1 | 33,057 | 667,421 |

Delta Air Lines, Inc.1 | 16,513 | 663,988 |

LKQ Corp.*,1 | 18,801 | 662,547 |

Walgreens Boots Alliance, Inc. | 16,596 | 661,848 |

Norwegian Cruise Line Holdings Ltd.* | 26,000 | 661,180 |

L Brands, Inc.1 | 17,431 | 648,259 |

American Airlines Group, Inc.1 | 40,425 | 637,502 |

United Airlines Holdings, Inc.* | 14,252 | 616,399 |

Under Armour, Inc. — Class A* | 21,049 | 361,411 |

Under Armour, Inc. — Class C* | 21,711 | 323,060 |

| Total Consumer, Cyclical | 48,462,978 | |

| Technology – 11.3% | ||

Fortinet, Inc.*,1 | 5,370 | 797,606 |

Cadence Design Systems, Inc.* | 5,815 | 793,340 |

Activision Blizzard, Inc.1 | 8,237 | 764,805 |

Skyworks Solutions, Inc. | 4,950 | 756,756 |

Synopsys, Inc.* | 2,916 | 755,944 |

Take-Two Interactive Software, Inc.*,1 | 3,623 | 752,823 |

Autodesk, Inc.*,1 | 2,464 | 752,358 |

Qorvo, Inc.* | 4,515 | 750,709 |

ANSYS, Inc.*,1 | 2,056 | 747,973 |

Western Digital Corp. | 13,491 | 747,266 |

Apple, Inc.1 | 5,630 | 747,045 |

Broadcom, Inc.1 | 1,698 | 743,469 |

DXC Technology Co.1 | 28,803 | 741,677 |

NetApp, Inc. | 11,149 | 738,510 |

IPG Photonics Corp.*,1 | 3,297 | 737,836 |

Oracle Corp. | 11,372 | 735,655 |

Paycom Software, Inc.* | 1,626 | 735,358 |

Micron Technology, Inc.* | 9,772 | 734,659 |

MSCI, Inc. — Class A | 1,643 | 733,649 |

HP, Inc.1 | 29,825 | 733,397 |

Accenture plc — Class A1 | 2,804 | 732,433 |

Electronic Arts, Inc.1 | 5,075 | 728,770 |

QUALCOMM, Inc. | 4,777 | 727,728 |

Cerner Corp.1 | 9,250 | 725,940 |

See notes to financial statements.

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 29

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Technology – 11.3% (continued) | ||

Maxim Integrated Products, Inc. | 8,185 | $ 725,600 |

Adobe, Inc.* | 1,448 | 724,174 |

Analog Devices, Inc.1 | 4,883 | 721,366 |

Cognizant Technology Solutions Corp. — Class A1 | 8,779 | 719,439 |

Microsoft Corp. | 3,232 | 718,861 |

Intuit, Inc.1 | 1,892 | 718,676 |

Jack Henry & Associates, Inc.1 | 4,423 | 716,482 |

Teradyne, Inc. | 5,974 | 716,223 |

Broadridge Financial Solutions, Inc. | 4,669 | 715,291 |

ServiceNow, Inc.* | 1,282 | 705,651 |

Texas Instruments, Inc. | 4,291 | 704,282 |

Xerox Holdings Corp. | 30,283 | 702,263 |

Zebra Technologies Corp. — Class A* | 1,825 | 701,402 |

Paychex, Inc. | 7,506 | 699,409 |

Akamai Technologies, Inc.*,1 | 6,657 | 698,918 |

International Business Machines Corp.1 | 5,546 | 698,130 |

KLA Corp.1 | 2,675 | 692,584 |

NVIDIA Corp. | 1,324 | 691,393 |

Intel Corp.1 | 13,860 | 690,505 |

Advanced Micro Devices, Inc.* | 7,520 | 689,659 |

salesforce.com, Inc.*,1 | 3,099 | 689,620 |

Leidos Holdings, Inc.1 | 6,538 | 687,275 |

Citrix Systems, Inc.1 | 5,276 | 686,408 |

Fiserv, Inc.*,1 | 6,003 | 683,502 |

Hewlett Packard Enterprise Co.1 | 57,485 | 681,197 |

Xilinx, Inc.1 | 4,792 | 679,362 |

Microchip Technology, Inc. | 4,902 | 677,015 |

Applied Materials, Inc.1 | 7,806 | 673,658 |

Tyler Technologies, Inc.* | 1,529 | 667,439 |

Lam Research Corp.1 | 1,402 | 662,123 |

Seagate Technology plc1 | 10,643 | 661,569 |

Fidelity National Information Services, Inc.1 | 4,662 | 659,487 |

| Total Technology | 40,174,669 | |

| Communications – 6.3% | ||

Expedia Group, Inc.1 | 5,603 | 741,837 |

Netflix, Inc.* | 1,370 | 740,800 |

Booking Holdings, Inc.*,1 | 330 | 734,999 |

NortonLifeLock, Inc. | 35,183 | 731,103 |

Twitter, Inc.*,1 | 13,399 | 725,556 |

Arista Networks, Inc.*,1 | 2,485 | 722,066 |

ViacomCBS, Inc. — Class B | 19,361 | 721,391 |

See notes to financial statements.

30 l GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Communications – 6.3% (continued) | ||

Etsy, Inc.* | 4,054 | $ 721,247 |

Amazon.com, Inc.*,1 | 221 | 719,782 |

Walt Disney Co.*,1 | 3,922 | 710,588 |

VeriSign, Inc.* | 3,282 | 710,225 |

Comcast Corp. — Class A1 | 13,533 | 709,129 |

T-Mobile US, Inc.* | 5,252 | 708,232 |

Juniper Networks, Inc.1 | 31,444 | 707,804 |

eBay, Inc.1 | 14,029 | 704,957 |

F5 Networks, Inc.*,1 | 3,998 | 703,408 |

Charter Communications, Inc. — Class A*,1 | 1,057 | 699,258 |

Corning, Inc.1 | 19,339 | 696,204 |

Motorola Solutions, Inc. | 4,093 | 696,056 |

Cisco Systems, Inc.1 | 15,552 | 695,952 |

CDW Corp. | 5,273 | 694,929 |

Facebook, Inc. — Class A*,1 | 2,520 | 688,363 |

Interpublic Group of Companies, Inc.1 | 28,815 | 677,729 |

Verizon Communications, Inc. | 11,421 | 670,984 |

Omnicom Group, Inc. | 10,671 | 665,550 |

Lumen Technologies, Inc.1 | 67,639 | 659,480 |

AT&T, Inc.1 | 22,227 | 639,249 |

DISH Network Corp. — Class A*,1 | 19,140 | 618,988 |

News Corp. — Class A | 29,266 | 525,910 |

Fox Corp. — Class A | 16,252 | 473,258 |

Discovery, Inc. — Class C*,1 | 17,038 | 446,225 |

Alphabet, Inc. — Class A*,1 | 196 | 343,517 |

Alphabet, Inc. — Class C*,1 | 191 | 334,609 |

Discovery, Inc. — Class A*,1 | 8,818 | 265,334 |

Fox Corp. — Class B | 7,407 | 213,914 |

News Corp. — Class B | 9,162 | 162,809 |

| Total Communications | 22,381,442 | |

| Utilities – 5.5% | ||

NRG Energy, Inc.1 | 20,773 | 780,026 |

AES Corp.1 | 32,588 | 765,818 |

NextEra Energy, Inc. | 9,339 | 720,504 |

American Water Works Company, Inc.1 | 4,648 | 713,329 |

Public Service Enterprise Group, Inc. | 12,203 | 711,435 |

CMS Energy Corp.1 | 11,607 | 708,143 |

Xcel Energy, Inc.1 | 10,604 | 706,969 |

Exelon Corp.1 | 16,733 | 706,467 |

Southern Co. | 11,407 | 700,732 |

Eversource Energy1 | 8,034 | 695,021 |

See notes to financial statements.

GPM l GUGGENHEIM ENHANCED EQUITY INCOME FUND ANNUAL REPORT l 31

| SCHEDULE OF INVESTMENTS continued | December 31, 2020 |

| Shares | Value | |

COMMON STOCKS† – 98.6% (continued) | ||

| Utilities – 5.5% (continued) | ||

Ameren Corp.1 | 8,897 | $ 694,500 |

FirstEnergy Corp.1 | 22,687 | 694,449 |

Evergy, Inc. | 12,502 | 693,986 |

American Electric Power Company, Inc.1 | 8,328 | 693,473 |

PPL Corp. | 24,546 | 692,197 |

Dominion Energy, Inc. | 9,201 | 691,915 |

Pinnacle West Capital Corp.1 | 8,646 | 691,248 |

NiSource, Inc. | 30,111 | 690,746 |

Edison International1 | 10,975 | 689,449 |

Duke Energy Corp.1 | 7,529 | 689,355 |

WEC Energy Group, Inc. | 7,472 | 687,648 |

Alliant Energy Corp.1 | 13,330 | 686,895 |

Sempra Energy | 5,385 | 686,103 |

CenterPoint Energy, Inc.1 | 31,690 | 685,772 |

Consolidated Edison, Inc.1 | 9,421 | 680,856 |

Entergy Corp.1 | 6,706 | 669,527 |

DTE Energy Co.1 | 5,511 | 669,090 |

Atmos Energy Corp. | 6,957 | 663,907 |

| Total Utilities | 19,559,560 | |

| Energy – 4.5% | ||

Phillips 66 | 9,916 | 693,525 |

Pioneer Natural Resources Co. | 5,964 | 679,240 |

Devon Energy Corp.1 | 42,651 | 674,312 |

TechnipFMC plc1 | 71,277 | 670,004 |

Diamondback Energy, Inc. | 13,755 | 665,742 |

Marathon Petroleum Corp.1 | 16,063 | 664,366 |

NOV, Inc. | 48,132 | 660,852 |

Valero Energy Corp. | 11,676 | 660,511 |

Cabot Oil & Gas Corp. — Class A1 | 40,544 | 660,056 |

Halliburton Co.1 | 34,758 | 656,926 |

Schlumberger N.V. | 30,045 | 655,882 |

Marathon Oil Corp.1 | 97,627 | 651,172 |

Exxon Mobil Corp.1 | 15,736 | 648,638 |

HollyFrontier Corp. | 25,082 | 648,370 |

Hess Corp.1 | 12,171 | 642,507 |

EOG Resources, Inc.1 | 12,859 | 641,278 |

Kinder Morgan, Inc.1 | 46,729 | 638,786 |

ONEOK, Inc. | 16,580 | 636,340 |

Concho Resources, Inc.1 | 10,894 | 635,665 |

ConocoPhillips1 | 15,852 | 633,922 |

Baker Hughes Co.1 | 30,403 | 633,903 |

See notes to financial statements.