OMB APPROVAL

OMB Number: 3235-0570

Expires: August 31, 2010

Estimated average burden hours per response...18.9

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21713

Madison Strategic Sector Premium Fund

(Exact name of registrant as specified in charter)

550 Science Drive, Madison, WI 53711

(Address of principal executive offices)(Zip code)

Pamela M. Krill

Madison/Mosaic Legal and Compliance Department

550 Science Drive

Madison, WI 53711

(Name and address of agent for service)

Registrant's telephone number, including area code: 608-274-0300

Date of fiscal year end: December 31

Date of reporting period: December 31, 2009

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. s 3507.

Item 1

Annual Report

December 31, 2009

Madison Strategic Sector

Premium Fund (MSP)

Active Equity Management combined with a

Covered Call Option Strategy

Madison Investment Advisors, Inc.

www.madisonfunds.com

MSP/Madison Strategic Sector Premium Fund

Table of Contents

Management’s Discussion of Fund Performance | 1 |

| Portfolio of Investments | 4 |

| Statement of Assets and Liabilities | 7 |

| Statement of Operations | 8 |

| Statements of Changes in Net Assets | 9 |

| Financial Highlights | 10 |

| Notes to Financial Statements | 11 |

| Report of Independent Registered Public Accounting Firm | 16 |

| Other Information | 17 |

| Trustees and Officers | 18 |

| Dividend Reinvestment Plan | 21 |

MSP/Madison Strategic Sector Premium Fund

Management’s Discussion of Fund Performance

What happened in the market during 2009?

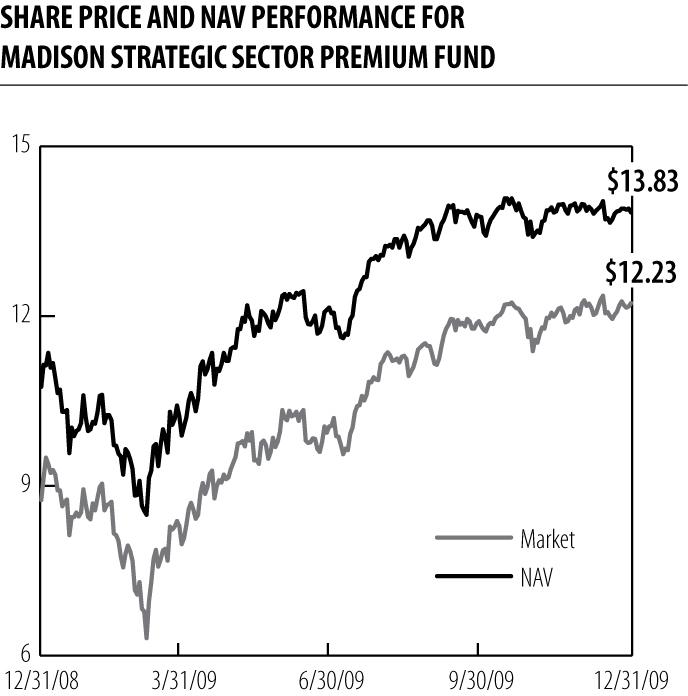

With a sense of relief, U.S. equity markets ended the year in much better form than they began. In the first months of 2009, the U.S. economy was in a very deep recession, which some were characterizing as the start of a new depression. Housing was in disarray, the auto market had serious problems, unemployment was rising and the credit markets were deteriorating. There was widespread fear that the major banks would be nationalized and by early March, these factors had driven the market down by some 25%. Since then, we’ve experienced a sizable recovery, a record rally in a very short time. Massive government stimulus has unfrozen credit markets, economic recovery is underway and market psychology has shifted from fear to optimism, some would say hyper-optimism. As a result, the S&P 500 managed a very strong 26.46% return in 2009 with a 6% boost coming in the fourth quarter.

Although defensive sectors led the way in the early portion of the year as the market continued to swoon, once the recovery gathered steam, cyclical sectors began to assert leadership. The technology, consumer discretionary and materials sectors were the ultimate leaders over the full year as expectations grew for a global economic recovery. The financial sector, which had been decimated in late 2008 and early 2009, rebounded sharply in the second and third quarter as a semblance of stability returned to the banking system. Despite its defensive nature and the specter of dramatic reform, the health care sector also rebounded strongly, particularly late in the year as reform efforts seemed to lose momentum.

Given the dire environment as the year began, investor fear was very high and as a result, market volatility was near the all-time highs reached in late 2008. The CBOE Market Volatility Index (VIX) traded in the range of 40 to 50 early in the year but trended lower as the stock market recovered and fear subsided, ending the year just above 20.

How did the fund perform given the marketplace conditions during 2009?

We are very pleased to report that MSP had a tremendous year, outperforming through the market declines in the first quarter and the rally that followed. For the year ended December 31, 2009, the fund provided a total return of 55.81% based on market price. This compared highly favorably to the S&P 500 Index which returned 26.46% and the CBOE S&P BuyWrite Index (BXM) which posted a 25.91% return over the same period. Closed-end funds in general, and MSP specifically, were pushed to deep discounts by the fear-inspired selling environment of 2008 and early 2009. A significant portion of the fund’s total return for this annual period was a reduction of the trading discount. The underlying Net Asset Value (ÒNAVÓ) showed a robust return of 41.21%, so that about a quarter of the trading price total return in 2009 was due to a reduction of trading discount. The fund’s strong performance during the period was powered by a combination of very favorable underlying stock performance coupled with an option strategy that allowed the fund to participate in the market rally.

Much transpired throughout the year from a portfolio strategy standpoint. Early in the year, the portfolio was structured to provide the most protection possible by taking advantage of the extremely high option premiums that resulted from the excessively high level of market volatility. As the market bottomed, call options were written meaningfully out-of-the-money in order for the portfolio to participate in the market rebound. This strategy worked extremely well and allowed the fund’s NAV to recover as the market advanced. Through mid-year, as the market continued its recovery, the fund shifted to a more defensive posture as concerns grew that the market may have moved too far ahead of actual underlying economic and corporate fundamentals. Call options were written closer-to-the-money and on a larger portion of the portfolio holdings and proceeds from option assignments were used to steadily reduce the fund’s leverage, which began the year at approximately 13% of total investments and was ultimately eliminated in October.

Describe the fund’s portfolio equity and option structure:

As of December 31, 2009, the fund held 48 equity securities and unexpired covered call options had been

MSP | Madison Strategic Sector Premium Fund | Management’s Discussion of Fund Performance | continued

written against 82% of the fund’s stock holdings. During 2009, the fund generated premiums of $8.6 million from its covered call writing activities. It is the strategy of the fund to write Òout-of-the-moneyÓ call options and as of December 31, 49.3% of the fund’s call options (37 of 75 different options) remained Òout-of-the-money.Ó (Out-of-the-money means the stock price is below the strike price at which the shares could be called away by the option holder.) The number of Òout-of-the-moneyÓ options has declined from the beginning of the year as the strength of the market rally has moved many share prices above their corresponding option strike prices. The fund’s managers have also begun writing options Òcloser-to-the-moneyÓ in order to capture higher premium income and provide the fund added protection from a reversal in the market’s upward surge.

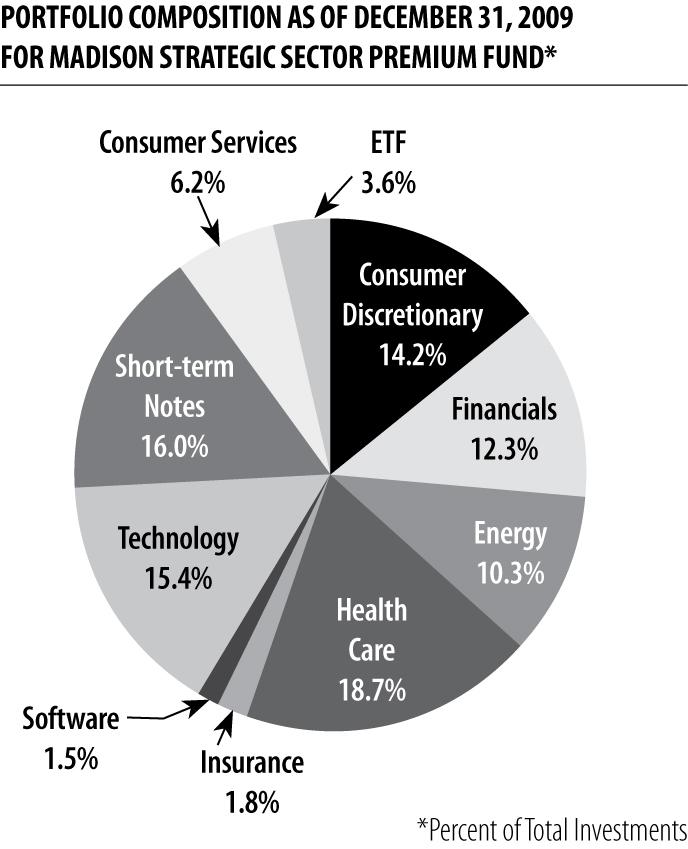

Which sectors are prevalent in the fund?

From a sector perspective, MSP’s largest exposure as of December 31, 2009 was to industries in the health care sector, followed by those in technology (and technology related), consumer discretionary, financials and energy sectors. The fund was not invested in industries in the materials, consumer staples, telecommunication services and utilities sectors of the economy as of year-end.

Discuss the fund’s security and option selection process.

The fund is supported by two teams of investment professionals. We like to think of these teams as a Òright handÓ and Òleft handÓ meaning they work together to make common stock and option decisions. We use fundamental analysis to select solid companies with good growth prospects and attractive valuations. We then seek attractive call options to write on those stocks. It is our belief that this partnership of active management between the equity and option teams provides investors with an innovative, risk-moderated approach to equity investing. The fund’s portfolio managers seek to invest in a portfolio of common stocks that have favorable PEG ratios (Price-Earnings ratio to Growth rate) as well as financial strength and industry leadership. As bottom-up investors, we focus on the fundamental businesses of our companies. Our stock selection philosophy strays away from the Òbeat the streetÓ mentality, as we seek companies that have sustainable competitive advantages, predictable cash flows, solid balance sheets and high-quality management teams. By concentrating on long-term prospects and circumventing the Òinstant gratificationÓ school of thought,

MSP | Madison Strategic Sector Premium Fund | Management’s Discussion of Fund Performance | concluded

we believe we bring elements of consistency, stability and predictability to our shareholders.

Once we have selected attractive and solid names for the fund, we employ our call writing strategy. This procedure entails selling calls that are primarily out-of the-money, meaning that the strike price is higher than the common stock price, so that the fund can participate in some stock appreciation. By receiving option premiums, the fund receives a high level of investment income and adds an element of downside protection. Call options may be written over a number of time periods and at differing strike prices in an effort to maximize the protective value to the strategy and spread income evenly throughout the year.

What is management’s outlook for the market and fund in 2010?

With 2009 providing a turning point in the stock market and economy, our outlook for 2010 is optimistic, although tempered by the fact that the market has already enjoyed such a strong recovery. We expect the economy to improve in 2010, especially internationally. Corporate profitability should continue to expand behind solid margins, productivity gains and improving revenue growth. Even though interest rates may move upward, they should remain at a relatively low level, which is positive for valuations. We also see substantial assets still in cash and lower yielding bonds which could come back into the stock market, providing support. Although deep recessions, such as the one we have recently experienced, are historically followed by steep recoveries, we believe the current recovery will likely be slower than history might suggest due to some lingering headwinds. High unemployment, stagnant wage growth and the prospect of higher taxes are causing consumers to save more and spend less, crimping a key economic driver. Additionally, the financial system, while recovering, remains wounded as does the housing market. In general, we expect economic growth to be moderately positive but below the long-term trend line of 3-4%.

The explosive rally from the March 2009 lows was focused on lower quality and economically sensitive areas with the expectation that the economy would bounce back. This is characteristic of the first leg of a recovery. As we move to the next leg, the market should take its direction from actual signs of improving economic and company fundamentals which should bring the spotlight to higher quality, blue chip companies which remain the focus within MSP’s portfolio.

Over the near term, we expect the stock market to consolidate its significant gains from the market lows with increasing risk relating to the possibility that lofty expectations of economic growth may be overly optimistic. While we wait for economic and corporate reality to catch up with expectations, we remain relatively defensively postured.

TOP TEN STOCK HOLDINGS AS OF DECEMBER 31, 2009

FOR MADISON STRATEGIC SECTOR PREMIUM FUND

| % of net assets |

| Cisco Systems, Inc. | 5.08% |

| EMC Corp. | 4.02% |

| eBay Inc. | 3.73% |

| Apache Corp. | 3.60% |

| Bed Bath & Beyond Inc. | 3.37% |

| UnitedHealth Group, Inc. | 3.27% |

| Capital One Financial Corp. | 3.24% |

| Lowe's Companies, Inc. | 3.21% |

| Target Corp. | 3.02% |

| Transocean Inc | 2.99% |

Portfolio of Investments | December 31, 2009

| | | |

| | | COMMON STOCKS: 96.5% of net assets | |

| | | CONSUMER DISCRETIONARY: 16.3% | |

| 33,100 | | American Eagle Outfitters, Inc. | $ 562,038 |

| 70,000 | | Bed Bath & Beyond Inc.* | 2,704,100 |

| 30,100 | | Best Buy Co., Inc. | 1,187,746 |

| 30,300 | | Home Depot Inc. | 876,579 |

| 29,000 | | Kohls Corp.* | 1,563,970 |

| 110,000 | | Lowe’s Companies, Inc. | 2,572,900 |

| 28,500 | | Starbucks Corp.* | 657,210 |

| 50,000 | | Target Corp. | 2,418,500 |

| 25,000 | | Williams-Sonoma, Inc. | 519,500 |

| | | | |

| | | CONSUMER SERVICES: 7.2% | |

| 127,000 | | eBay Inc.* | 2,989,580 |

| 60,000 | | Garmin Ltd. | 1,842,000 |

| 30,000 | | Intuit Inc.* | 921,300 |

| | | | |

| | | ENERGY: 11.8% | |

| 28,000 | | Apache Corp. | 2,888,760 |

| 22,000 | | Schlumberger Ltd. | 1,431,980 |

| 29,000 | | Transocean Ltd.* | 2,401,200 |

| 50,000 | | Weatherford International Ltd.* | 895,500 |

| 40,000 | | XTO Energy Inc. | 1,861,200 |

| | | | |

| | | EXCHANGE TRADED FUNDS: 4.1% | |

| 35,000 | | Powershares QQQ | 1,607,200 |

| 15,000 | | SPDR Trust Series 1 | 1,671,600 |

| | | | |

| | | FINANCIALS: 14.1% | |

| 16,300 | | Affiliated Managers Group, Inc.* | 1,097,805 |

| 61,867 | | Bank of America Corp. | 931,717.02 |

| 67,800 | | Capital One Financial Corp. | 2,599,452 |

| 190,000 | | Citigroup Inc. | 628,900 |

| 95,000 | | Marshall & Ilsley Corp. | 517,750 |

| 68,000 | | Morgan Stanley | 2,012,800 |

| 50,000 | | State Street Corp. | 2,177,000 |

| 50,000 | | Wells Fargo & Co. | 1,349,500 |

| | | | |

| | | HEALTH CARE: 21.6% | |

| 43,100 | | Biogen Idec* | 2,305,850 |

| 36,000 | | Genzyme Corp.* | 1,764,360 |

| 45,000 | | Gilead Sciences, Inc.* | 1,947,600 |

| 35,000 | | Medtronic Inc. | 1,539,300 |

| 121,600 | | Mylan, Inc.* | 2,241,088 |

| 109,800 | | Pfizer Inc. | 1,997,262 |

| | | |

| 86,000 | | UnitedHealth Group, Inc. | $ 2,621,280 |

| 12,900 | | Waters Corp.* | 799,284 |

| 35,000 | | Zimmer Holdings Inc.* | 2,068,850 |

| | | | |

| | | INSURANCE: 2.0% | |

| 32,000 | | Aflac Inc. | 1,480,000 |

| 25,000 | | MGIC Investment Corp.* | 144,500 |

| | | | |

| | | SOFTWARE: 1.7% | |

| 700 | | Check Point Software Technologies Ltd.* | 23,716 |

| 75,000 | | Symantec Corp.* | 1,341,750 |

| | | | |

| | | TECHNOLOGY: 17.7% | |

| 40,000 | | Applied Materials, Inc. | 557,600 |

| 170,000 | | Cisco Systems, Inc.* | 4,069,800 |

| 100,000 | | Dell Inc.* | 1,436,000 |

| 184,400 | | EMC Corp.* | 3,221,468 |

| 260,000 | | Flextronics International Ltd.* | 1,900,600 |

| 38,100 | | Microsoft Corp. | 1,161,669 |

| 60,000 | | Yahoo! Inc.* | 1,006,800 |

| 30,000 | | Zebra Technologies Corp.-Class A* | |

| | | | |

| | | TOTAL COMMON STOCKS (Cost $102,123,369) | $77,367,364 |

| | | | |

| | | SHORT-TERM INVESTMENTS: | |

| | | | |

| | | Repurchase Agreement - 18.4% | |

| | | US Bank issued 12/31/09 at 0.01%, due 1/4/10, collateralized by $15,033,612 in Fannie Mae MBS #555745 due 9/1/18. Proceeds at maturity are $14,738,629 (Cost $14,738,613). | |

| | | | |

| | | TOTAL INVESTMENTS: 114.9% of net assets (Cost $116,861,981) | $92,105,977 |

| | | | |

| | | CASH AND OTHER ASSETS LESS LIABILITIES: (7.1%) | (5,667,982) |

| | | TOTAL CALL OPTIONS WRITTEN: (7.8%) | |

| | | | |

| | | NET ASSETS: 100% | |

| *Non-income producing |

See notes to financial statements.

MSP | Madison Strategic Sector Premium Fund | Portfolio of Investments | continued

Contracts (100 shares per contract) | | | | | |

| 53.00 | | Affiliated Managers Group, Inc. | January 2010 | $50.00 | $91,955 |

| 110.00 | | Affiliated Managers Group, Inc. | March 2010 | 70.00 | 36,850 |

| 150.00 | | Aflac Inc. | January 2010 | 30.00 | 244,500 |

| 170.00 | | Aflac Inc. | May 2010 | 49.00 | 41,650 |

| 17.00 | | American Eagle Outfitters, Inc. | January 2010 | 12.50 | 7,650 |

| 149.00 | | American Eagle Outfitters, Inc. | January 2010 | 15.00 | 31,290 |

| 165.00 | | American Eagle Outfitters, Inc. | May 2010 | 17.50 | 24,750 |

| 146.00 | | Apache Corp. | April 2010 | 95.00 | 170,090 |

| 134.00 | | Apache Corp. | April 2010 | 105.00 | 77,720 |

| 400.00 | | Applied Materials, Inc. | January 2010 | 12.50 | 61,000 |

| 400.00 | | Bed Bath & Beyond, Inc. | January 2010 | 30.00 | 346,000 |

| 50.00 | | Bed Bath & Beyond, Inc. | January 2010 | 32.00 | 33,500 |

| 246.00 | | Bed Bath & Beyond, Inc. | February 2010 | 38.00 | 50,430 |

| 3.00 | | Best Buy Co., Inc. | January 2010 | 35.00 | 1,372 |

| 150.00 | | Best Buy Co., Inc. | March 2010 | 39.00 | 39,300 |

| 148.00 | | Best Buy Co., Inc. | June 2010 | 48.00 | 13,024 |

| 295.00 | | Biogen Idec | January 2010 | 55.00 | 19,175 |

| 136.00 | | Biogen Idec | July 2010 | 50.00 | 90,440 |

| 178.00 | | Capital One Financial Corp. | March 2010 | 38.00 | 53,756 |

| 300.00 | | Capital One Financial Corp. | June 2010 | 40.00 | 105,000 |

| 1,000.00 | | Cisco Systems, Inc. | January 2010 | 20.00 | 397,500 |

| 400.00 | | Cisco Systems, Inc. | April 2010 | 24.00 | 52,600 |

| 400.00 | | Dell Inc. | January 2010 | 15.00 | 5,600 |

| 620.00 | | eBay Inc. | January 2010 | 20.00 | 220,100 |

| 200.00 | | eBay Inc. | April 2010 | 24.00 | 29,100 |

| 250.00 | | eBay Inc. | July 2010 | 25.00 | 42,625 |

| 464.00 | | EMC Corp. | January 2010 | 12.50 | 230,840 |

| 380.00 | | EMC Corp. | January 2010 | 16.00 | 57,190 |

| 700.00 | | EMC Corp. | July 2010 | 18.00 | 95,200 |

| 500.00 | | Flextronics International Ltd. | January 2010 | 5.00 | 116,000 |

| 200.00 | | Garmin Ltd. | January 2010 | 30.00 | 26,000 |

| 200.00 | | Garmin Ltd. | April 2010 | 34.00 | 28,500 |

| 200.00 | | Garmin Ltd. | July 2010 | 33.00 | 57,500 |

| 200.00 | | Genzyme Corp. | January 2010 | 55.00 | 2,500 |

| 160.00 | | Genzyme Corp. | April 2010 | 52.50 | 30,800 |

| 350.00 | | Gilead Sciences, Inc. | February 2010 | 49.00 | 10,500 |

| 300.00 | | Home Depot Inc. | February 2010 | 28.00 | 46,050 |

| 300.00 | | Intuit Inc. | January 2010 | 27.50 | 96,000 |

| 290.00 | | Kohl’s Corp. | January 2010 | 50.00 | 121,800 |

| 400.00 | | Lowe’s Companies, Inc. | January 2010 | 24.00 | 8,000 |

| 700.00 | | Lowe’s Companies, Inc. | July 2010 | 25.00 | 94,500 |

| 350.00 | | Medtronic Inc | May 2010 | 46.00 | 73,500 |

| 381.00 | | Microsoft Corp. | January 2010 | 25.00 | 210,503 |

| 300.00 | | Morgan Stanley | July 2010 | 32.00 | 62,550 |

| 200.00 | | Morgan Stanley | July 2010 | 34.00 | 28,700 |

| 666.00 | | Mylan, Inc. | January 2010 | 12.50 | 399,600 |

| 250.00 | | Mylan, Inc. | January 2010 | 15.00 | 86,250 |

See notes to financial statements.

MSP | Madison Strategic Sector Premium Fund | Portfolio of Investments | concluded

Contracts (100 shares per contract) | | | | | |

| 300.00 | | Mylan, Inc. | April 2010 | $17.50 | $54,750 |

| 350.00 | | Powershares QQQ | March 2010 | 47.00 | 42,350 |

| 150.00 | | Schlumberger Ltd | February 2010 | 65.00 | 47,250 |

| 70.00 | | Schlumberger Ltd | May 2010 | 65.00 | 40,075 |

| 150.00 | | SPDR Trust Series 1 | February 2010 | 114.00 | 30,150 |

| 285.00 | | Starbucks Corp. | January 2010 | 12.50 | 302,100 |

| 100.00 | | State Street Corp. | January 2010 | 55.00 | 500 |

| 200.00 | | State Street Corp. | May 2010 | 46.00 | 60,000 |

| 200.00 | | State Street Corp. | August 2010 | 47.00 | 72,000 |

| 500.00 | | Symantec Corp. | January 2010 | 15.00 | 146,250 |

| 250.00 | | Symantec Corp. | July 2010 | 18.00 | 40,625 |

| 200.00 | | Target Corp. | January 2010 | 45.00 | 71,000 |

| 300.00 | | Target Corp. | April 2010 | 49.00 | 74,700 |

| 290.00 | | Transocean Ltd | February 2010 | 90.00 | 34,800 |

| 400.00 | | UnitedHealth Group, Inc. | March 2010 | 30.00 | 94,600 |

| 200.00 | | UnitedHealth Group, Inc. | June 2010 | 33.00 | 38,800 |

| 129.00 | | Waters Corp. | January 2010 | 45.00 | 218,655 |

| 400.00 | | Weatherford International Ltd | August 2010 | 20.00 | 64,000 |

| 300.00 | | Wells Fargo & Co. | January 2010 | 30.00 | 2,850 |

| 200.00 | | Wells Fargo & Co. | April 2010 | 29.00 | 27,300 |

| 250.00 | | Williams-Sonoma, Inc. | February 2010 | 17.50 | 87,500 |

| 320.00 | | XTO Energy Inc. | February 2010 | 44.00 | 105,600 |

| 80.00 | | XTO Energy Inc. | May 2010 | 47.00 | 20,000 |

| 300.00 | | Yahoo! Inc. | April 2010 | 19.00 | 9,000 |

| 300.00 | | Zebra Technologies Corp. - Class A | February 2010 | 25.00 | 106,500 |

| 140.00 | | Zimmer Holdings Inc. | January 2010 | 45.00 | 197,400 |

| 110.00 | | Zimmer Holdings Inc. | March 2010 | 55.00 | 61,600 |

| 100.00 | | Zimmer Holdings Inc. | June 2010 | 60.00 | |

| | | | | | |

| | | TOTAL CALL OPTIONS WRITTEN (Premiums Received $4,874,874) | | | |

See notes to financial statements.

Statement of Assets and Liabilities | December 31, 2009

| ASSETS | |

| Investments, at value (Note 2) | |

| Short term investments | $14,738,613 |

| Investment securities | |

Total investments (cost $116,861,981) | 92,105,977 |

| Receivables | |

| Investment securities sold | 1,282,420 |

| Dividends and interest | |

| Total assets | 93,406,045 |

| | |

| LIABILITIES | |

| Options written, at value (premiums received of $4,874,874) | 6,259,815 |

| Payables | |

| Investment securities purchased | 6,948,103 |

| Auditor fees | 15,200 |

| Independent trustee fees | 4,500 |

| Other expenses | |

| Total liabilities | |

| | |

| NET ASSETS | $80,178,180 |

| | |

| Net assets consist of: | |

| Paid in capital | 110,544,278 |

| Accumulated net realized loss on investments and options transactions | (4,225,153) |

| Accumulated net unrealized depreciation on investments and options transactions | |

| Net assets | |

| | |

| CAPITAL SHARES ISSUED AND OUTSTANDING | |

| An unlimited number of capital shares authorized,$.01 par value per share (Note 8) | 5,798,291 |

| | |

| NET ASSETS VALUE PER SHARE | |

See notes to financial statements.

Statement of Operations | For the year ended December 31, 2009

INVESTMENT INCOME (Note 2) | |

| Interest income | $ 2,219 |

| Dividend income | |

| Total investment income | 670,918 |

| | |

EXPENSES (Note 3) | |

| Investment advisory | 609,407 |

| Interest on loan | 128,454 |

| Administration | 19,041 |

| Fund accounting | 19,387 |

| Auditor fees | 22,700 |

| Independent trustee fees | 18,000 |

| Other | |

| Total expenses | 864,760 |

| | |

| NET INVESTMENT LOSS | (193,842) |

| | |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | |

| Net realized gain (loss) on: | |

| Investments | (7,684,228) |

| Options | 3,459,075 |

| Net unrealized appreciation (depreciation) on: | |

| Investments | 30,828,452 |

| Options | |

| | |

| NET GAIN ON INVESTMENTS AND OPTIONS TRANSACTIONS | |

| | |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | |

See notes to financial statements.

Statements of Changes in Net Assets

| | Year Ended December 31, |

| | | |

| INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS | | |

| Net investment income (loss) | $ (193,842) | $ 170,259 |

| Net realized gain (loss) on investments and options transactions | (4,225,153) | 13,461,989 |

| Net unrealized appreciation (depreciation) on investments and options transactions | | |

| Net Increase (decrease) in net assets resulting from operations | 24,501,987 | (30,576,241) |

| | | |

| DISTRIBUTION TO SHAREHOLDERS | | |

| From net investment income | -- | (170,259) |

| From net capital gains | | |

| Total distributions | (6,656,638) | (8,697,436) |

| | | |

| CAPITAL SHARE TRANSACTIONS | | |

| | | |

| NET INCREASE (DECREASE) IN NET ASSETS | 17,845,349 | (39,273,677) |

| | | |

| NET ASSETS | | |

| Beginning of period | | |

| End of period | | |

See notes to financial statements.

Financial Highlights

Per Share Operating Performance for One Share Outstanding Throughout the Period

| | Year Ended December 31, | For the Period April 27, 20051 through December 31, |

| | | | | | |

| Net asset value, beginning of period | $10.75 | $17.52 | $20.25 | $19.87 | $19.102 |

| Investment operations: | | | | | |

| Net investment income (loss) | (0.03) | 0.03 | 0.28 | 0.06 | 0.03 |

Net realized and unrealized gain (loss) on investments and options transactions | | | | | |

| Total from investment operations | 4.23 | (5.27) | (0.93) | 2.18 | 1.71 |

| Less distributions from: | | | | | |

| Net investment income | -- | (0.03) | (0.28) | (0.06) | (0.03) |

| Capital gains | | | | | |

| Total distributions | (1.15) | (1.50) | (1.80) | (1.80) | (0.90) |

| Net asset value, end of period | $13.83 | $10.75 | $17.52 | $20.25 | $19.87 |

| Market value, end of period | $12.23 | $8.75 | $15.53 | $20.60 | $20.28 |

| Total investment return | | | | | |

| Net asset value (%) | 41.21 | (31.94) | (5.07) | 11.61 | 8.83 |

| Market value (%) | 55.81 | (36.18) | (16.85) | 11.30 | 5.29 |

| Ratios and supplemental data | | | | | |

Net assets, end of period (thousands) | $80,178 | $62,333 | $101,607 | $116,223 | $111,507 |

| Ratios to Average Net Assets: | | | | | |

| Total expenses, excluding interest expense (%) | 1.04 | 1.07 | 0.98 | 0.98 | 0.973 |

| Total expenses, including interest expense (%) | 1.23 | 1.50 | 0.98 | 0.98 | 0.973 |

| Net investment income, including interest expense (%) | (0.27) | 0.19 | 1.41 | 0.33 | 0.253 |

Ratios to Average Managed Assets:4 | | | | | |

| Total expenses, excluding interest expense (%) | 0.97 | 0.96 | -- | -- | -- |

| Total expenses, including interest expense (%) | 1.13 | 1.35 | -- | -- | -- |

| Net investment income, including interest expense (%) | (0.25) | 0.17 | -- | -- | -- |

| Portfolio turnover (%) | 25 | 41 | 93 | 64 | 49 |

| Senior Indebtedness | | | | | |

| Outstanding balance, end of period (thousands) | -- | 10,000 | -- | -- | -- |

| Average outstanding balance during the period (thousands) | 5,671 | 9,706 | -- | -- | -- |

| Average fund shares during the period (thousands) | 5,798 | 5,798 | -- | -- | -- |

| Average indebtedness per share | 0.98 | 1.67 | -- | -- | -- |

| Asset coverage per $1,000 of indebtedness | -- | 7,2335 | -- | -- | -- |

1Commencement of operations.

2Before deduction of offering costs charged to capital.

3Annualized.

4Managed assets is equal to net assets plus average outstanding leverage.

5Calculated by subtracting the fund’s total liabilities (not including borrowings) from the fund’s total assets and dividing by the total borrowings at year-end.

Net asset value figures are based on average daily shares outstanding during the year.

See notes to financial statements.

Notes to Financial Statements | December 31, 2009

Note 1 – Organization.

Madison Strategic Sector Premium Fund (the ÒFundÓ) was organized as a Delaware statutory trust on February 4, 2005. The Fund is registered as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended, and the Securities Act of 1933, as amended. The Fund commenced operations on April 27, 2005. The Fund’s primary investment objective is to provide a high level of current income and current gains, with a secondary objective of long-term capital appreciation.

The Fund will pursue its investment objectives by investing in a portfolio consisting primarily of common stocks of large and mid-capitalization issuers that are, in the view of the Fund’s Investment Adviser, selling at a reasonable price in relation to their long-term earnings growth rates. Under normal market conditions, the Fund will seek to generate current earnings from option premiums by writing (selling) covered call options on a substantial portion of its portfolio securities. There can be no assurance that the Fund will achieve its investment objectives. The Fund’s investment objectives are considered fundamental and may not be changed without shareholder approval.

Note 2 – Significant Accounting Policies.

(a) Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions. Such estimates affect the reported amounts of assets and liabilities and reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

(b) Valuation of Investments

The Fund adopted Financial Accounting Standards Board (ÒFASBÓ) guidance on fair value measurements effective January 2008. In accordance with this guidance, fair value is defined as the price that the Fund would receive to sell an investment or pay to transfer a liability in an orderly transaction with an independent buyer in the principal market, or in the absence of a principal market the most advantageous market for the investment or liability. This guidance establishes a three-tier hierarchy to distinguish between (1) inputs that reflect the assumptions market participants would use in pricing an asset or liability developed based on market data obtained from sources independent of the reporting entity (observable inputs) and (2) inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing an asset or liability developed based on the best information available in the circumstances (unobservable inputs) and to establish classification of fair value measurements for disclosure purposes.

Various inputs as noted above are used in determining the value of the Fund’s investments and other financial instruments. These inputs are summarized in the three broad levels listed below.

| | Level 1: Quoted prices in active markets for identical securities |

| | Level 2: Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| | Level 3: Significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

MSP | Madison Strategic Sector Premium Fund | Notes to Financial Statements | continued

The following table represents the Fund’s investments carried on the Statement of Assets and Liabilities by caption and by level within the fair value hierarchy as of December 31, 2009:

| | | | |

| Assets: | | | | |

| Common Stocks | $77,367,364 | $ -- | $ -- | $77,367,364 |

| Repurchase Agreement | | | | |

| Total | | | | |

| | | | | |

| Liabilities: | | | | |

| Written optons | | | | |

| Total | | | | |

| Please see Portfolio of Investments for common stock sector breakdown and listing of all securities within each caption. |

In March 2008, the FASB issued guidance intended to enhance financial statement disclosures for derivative instruments and hedging activities and enable investors to understand: a) how and why a fund uses derivative instruments, b) how derivative instruments and related hedge fund items are accounted for, and c) how derivative instruments and related hedge items affect a fund’s financial position, results of operations and cash flows. This guidance is effective for financial statements issued for fiscal years and interim periods beginning after November 15, 2008. The Fund adopted this guidance effective January 2009.

The following table presents the types of derivatives in the Fund by location as presented on the Statement of Assets and Liabilities as of December 31, 2009:

Statement of Asset & Liability Presentation of Fair Values of Derivative Instruments |

| | | |

Derivatives not accounted for as hedging instruments | Statement of Assets and Liabilities Location | | Statement of Assets and Liabilities Location | |

| Equity contracts | -- | -- | Options written | |

The following table presents the effect of Derivative Instruments on the Statement of Operations for the year ended December 31, 2009:

| | Realized Gain on Derivatives: | Change in Unrealized Depreciation on Derivatives |

Derivatives not accounted for as hedging instruments | | |

| Equity contracts – options | | |

In January 2010, amended guidance was issued by FASB for fair value measurement disclosures about transfers into and out of Levels 1 and 2 and separate disclosures about purchases, sales, issuances and settlements relating to Level 3 measurements. It also clarifies existing fair value disclosures about the level of disaggregation, inputs and valuation techniques used to measure fair value. The amended guidance is effective for financial statements for fiscal years and interim periods beginning after December 15, 2009 except for disclosures about purchases, sales, issuances and settlements relating to Level 3 measurements, which are effective for fiscal years beginning after December 15, 2010, and for interim periods within those fiscal years. Earlier adoption is permitted. In the period of initial adoption, the Fund will not be required to provide the amended disclosures for any previous periods presented for comparative purposes. However, those disclosures are required for periods ending after initial adoption. The impact of this guidance on the Fund’s financial statements and disclosures, if any, is currently being assessed.

MSP | Madison Strategic Sector Premium Fund | Notes to Financial Statements | continued

(c) Investment Transactions and Investment Income

Investment transactions are accounted for on the trade date. Realized gains and losses on investments are determined on the identified cost basis. Dividend income is recorded net of applicable withholding taxes on the ex-dividend date and interest income is recorded on an accrual basis.

(d) Repurchase Agreements

The Fund may invest in repurchase agreements, which are short-term investments in which the Fund acquires ownership of a debt security and the seller agrees to repurchase the security at a future time and specified price. Repurchase agreements are fully collateralized by the underlying debt security. The Fund will make payment for such securities only upon physical delivery or evidence of book entry transfer to the account of the custodian bank. The seller is required to maintain the value of the underlying security at not less than the repurchase proceeds due the Fund.

Note 3 – Investment Advisory Agreement and Other Transactions with Affiliates.

Pursuant to an Investment Advisory Agreement between the Fund and Madison Asset Management, LLC, a controlled subsidiary of Madison Investment Advisors, Inc. (the ÒAdviserÓ), the Adviser, under the supervision of the Fund’s Board of Trustees, will provide a continuous investment program for the Fund’s portfolio; provide investment research and make and execute recommendations for the purchase and sale of securities; and provide certain facilities and personnel, including officers required for the Fund’s administrative management and compensation of all officers and trustees of the Fund who are its affiliate. For these services, the Fund will pay the Adviser a fee, payable monthly, in an amount equal to 0.80% of the Fund’s average daily managed assets.

Under a separate Services Agreement, effective April 26, 2005, the Adviser provides fund administration services, fund accounting services, and arranges to have all other necessary operational and support services, for a fee, to the Fund. Such services include transfer agent, custodian, legal, and other operational expenses. These fees are accrued daily and shall not exceed 0.18% of the Fund’s average daily net assets. The Adviser assumes responsibility for payment of all expenses greater than 0.18% of average daily net assets for the first five years of the Fund’s operations, other than investment expenses such as brokerage commission costs or interest and fees on loans. The Adviser has agreed to renew this expense limit for another year through April 26, 2011.

Note 4 – Federal Income Taxes.

No provision is made for federal income taxes since it is the intention of the Fund to comply with the provisions of Subchapter M of the internal Revenue Code available to investment companies and to make the requisite distribution to shareholders of taxable income which will be sufficient to relieve it from all or substantially all federal income taxes.

The Fund adopted the provisions of FASB guidance on accounting for uncertainty in income taxes. The implementation of this guidance resulted in no material liability for unrecognized tax benefits and no material change to the beginning net asset value of the Fund.

As of and during the year ended December 31, 2009, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the period, the Fund did not incur any interest or penalties.

As of December 31, 2009, the Fund had available for federal income tax purposes $3,853,762 of capital loss carryovers which will expire December 31, 2017.

Information on the tax components of investments, excluding option contracts, as of December 31, 2009 is as follows:

| Aggregate Cost | |

| Gross unrealized appreciation | 2,507,833 |

| Gross unrealized depreciation | |

| Net unrealized depreciation | |

Net realized gains or losses may differ for financial reporting and tax purposes primarily as a result of the deferral of losses relating to wash sale transactions and post-October transactions.

Due to inherent differences in the recognition of income, expenses, and realized gains/losses under U.S. generally accepted accounting principles and federal

MSP | Madison Strategic Sector Premium Fund | Notes to Financial Statements | continued

income tax purposes, permanent differences between book and tax basis reporting have been identified and appropriately reclassified on the Statement of Assets and Liabilities. A permanent book and tax difference relating to net investment losses in the amount of $193,842 was reclassified from accumulated undistributed net investment income to paid in capital.

For the years ended December 31, 2009 and 2008, the tax character of distributions paid to shareholders was $6,656,638 of short-term capital gains for 2009 and $8,697,436 of ordinary income for 2008, respectively. The Fund designates 7.48% of dividends declared from net investment income and short-term capital gains during the year ended December 31, 2009 as qualified income under the Jobs and Growth Tax Relief Reconciliation Act of 2003.

As of December 31, 2009, the components of distributable earnings on a tax basis were as follows:

| Accumulated net realized losses | $ (3,853,762) |

| Net unrealized depreciation on investments | |

| | |

Note 5 – Investment Transactions.

During the year ended December 31, 2009, the cost of purchases and proceeds from sales of investments, excluding short-term investments, were $17,413,567 and $31,938,304, respectively. No long term U.S. Government securities were purchased or sold during the period.

Note 6 – Covered Call Options.

The Fund will pursue its primary objective by employing an option strategy of writing (selling) covered call options on common stocks. The number of call options the Fund can write (sell) is limited by the amount of equity securities the Fund holds in its portfolio. The Fund will not write (sell) ÒnakedÓ or uncovered call options. The Fund seeks to produce a high level of current income and gains generated from option writing premiums and, to a lesser extent, from dividends.

Transactions in option contracts during the year ended

December 31, 2009 were as follows:

| | | |

Options outstanding beginning of period | | |

| Options written | 33,290 | 8,585,553 |

| Options expired | (9,738) | (2,358,483) |

| Options closed | (18,424) | (4,789,121) |

| Options assigned | | |

| Options outstanding end of period | | |

Note 7 – Capital.

The Fund has an unlimited amount of common shares, $0.01 par value, authorized and 5,798,291 shares issued and outstanding as of December 31, 2009.

In connection with the Fund’s dividend reinvestment plan, there were no shares reinvested for the years ended December 31, 2009 and 2008, respectively.

Note 8 – Indemnifications.

In the normal course of business, the Fund enters into contracts that provide general indemnifications. The Fund’s maximum exposure under these arrangements is dependent upon claims that may be made against the Fund in the future and, therefore cannot be estimated; however, the risk of material loss from such claims is considered remote.

Note 9 – Leverage.

The Fund has a $25 million revolving credit facility with a bank to permit it to leverage its portfolio under favorable market conditions. The interest rate on the outstanding principal amount is equal to the prime rate less 1%. During the year ended December 31, 2009, the Fund did not draw on the facility and has paid back $10,000,000 of previously made draws. The Fund paid interest of $128,454 during 2009. The full facility is available to draw upon as of December 31, 2009.

MSP | Madison Strategic Sector Premium Fund | Notes to Financial Statements | concluded

Note 10 – Subsequent Events. Management has evaluated the impact of all subsequent events on the Fund’s financial statements through February 25, 2010, the date the financial statements were issued, and has determined that there were no subsequent events requiring adjustment or disclosure in the financial statements.

Report of Independent

Registered Public Accounting Firm | December 31, 2009

To the Board of Trustees and Shareholders of Madison Strategic Sector Premium Fund

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments of the Madison Strategic Sector Premium Fund (the ÒFundÓ), as of December 31, 2009 and the related statement of operations for the year then ended and the statements of changes in net assets for each of the two years in the period then ended, and financial highlights for the four years in the period then ended and for the period from April 27, 2005 (commencement of operations) through December 31, 2005. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2009 by correspondence with the Fund’s custodian and brokers. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Fund as of December 31, 2009, and the results of its operations for the year then ended and the changes in its net assets for each of the two years in the period then ended, and financial highlights for the four years in the period then ended and for the period from April 27, 2005 (commencement of operations) through December 31, 2005, in conformity with accounting principles generally accepted in the United States of America.

Grant Thornton LLP

(signature)

Chicago, Illinois

February 25, 2010

Other Information

Results of Shareholder Vote. The Annual Meeting of shareholders of the Fund was held on July 22, 2009. At the meeting, shareholders voted on the election of one trustee, Philip E. Blake. The votes cast in favor of election for Mr. Blake were 4,417,902 with 711,742 shares withheld. The other trustees of the Fund whose terms did not expire in 2009 are James R. Imhoff, Jr., Katherine L. Frank, Frank E. Burgess and Lorence D. Wheeler.

Additional Information. Notice is hereby given in accordance with Section 23(c) of the Investment Company Act of 1940 that from time to time, the Fund may purchase shares of its common stock in the open market at prevailing market prices.

Forward-Looking Statement Disclosure.

One of our most important responsibilities as investment company managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered Òforward-looking statements.Ó Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as Òestimate,Ó Òmay,Ó Òwill,Ó Òexpect,Ó Òbelieve,Ó ÒplanÓ and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

Proxy Voting Information.

The Fund adopted policies that provide guidance and set forth parameters for the voting of proxies relating to securities held in the Fund’s portfolios. Additionally, information regarding how the Fund voted proxies related to portfolio securities, if applicable, during the period ended June 20, 2009, is available upon request and free of charge, by writing to Madison Strategic Sector Premium Fund, 550 Science Drive, Madison, WI 53711 or by calling toll-free at 1-800-368-3195. The Fund’s proxy voting policies and voting information may also be obtained by visiting the Securities and Exchange Commission (ÒSECÓ) web site at www.sec.gov. The Fund will respond to shareholder requests for copies of our policies within two business days of request by first-class mail or other means designed to ensure prompt delivery.

N-Q Disclosure.

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the SEC’s website. The Fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information about the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. Form N-Q and other information about the Fund are available on the EDGAR Database on the SEC’s Internet site at http://www.sec.gov. Copies of this information may also be obtained, upon payment of a duplicating fee, by electronic request at the following email address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Section, Washington, DC 20549-0102. Finally, you may call the Fund at 800-368-3195 if you would like a copy of Form N-Q and we will mail one to you at no charge.

Trustees and Officers

Interested Trustees and Officers

Name and Year of Birth | Position(s) and Length of Time Served | Principal Occupation(s) During Past Five Years | Other Directorships/Trusteeships |

Katherine L. Frank1 1960 | President, 2005 - Present, and Trustee, 2005- Present | Madison Investment Advisors, Inc. (ÒMIAÓ), Managing Director and Vice President, 1986 - Present; Madison Asset Management, LLC (ÒMAMÓ), Director and Vice President, 2004 - Present; Madison Mosaic, LLC, President, 1996 - Present; Madison Mosaic Funds (13 funds) and Madison Strategic Sector Premium Fund (closed end fund), President, 1996 - Present; Madison/Claymore Covered Call and Equity Strategy Fund (closed end fund), Vice President, 2005 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19) (mutual funds), President, 2009 - Present | Madison Mosaic Funds (all but Equity Trust) and Madison Strategic Sector Premium Fund, 1996 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), 2009 - Present |

Frank E. Burgess1 1942 | Trustee and Vice President, 2005 - Present | MIA, Founder, President and Director, 1973 - Present; MAM, President and Director, 2004 - Present; Madison Mosaic Funds (13 funds) and Madison Strategic Sector Premium Fund, Vice President, 1996 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), Vice President, 2009 - Present | Madison Mosaic Funds (13), Madison Strategic Sector Premium Fund, and Madison/Claymore Covered Call & Equity Strategy Fund, 1996 - Present; Capitol Bank of Madison, WI, 1995 - Present; American Riviera Bank of Santa Barbara, CA, 2006 - Present |

Jay R. Sekelsky 1959 | Vice President, 2005 - Present | MIA, Managing Director and Vice President, 1990 - Present; MAM, Director, 2009 - Present; Madison Mosaic, LLC, Vice President, 1996 - Present; Madison Mosaic Funds (13 funds) and Madison Strategic Sector Premium Fund, Vice President, 1996 - Present; Madison/Claymore Covered Call & Equity Strategy Fund, Vice President, 2004 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), Vice President, 2009 - Present | N/A |

Paul Lefurgey 1964 | Vice President, 2010 - Present | MIA, Managing Director, Head of Fixed Income, 2005 - Present; Madison Mosaic Funds (13 funds, including the Trust), Vice President, 2009 - Present; Madison Strategic Sector Premium Fund, Vice President, 2010 - Present; MEMBERS Capital Advisors, Inc. (ÒMCAÓ) (investment advisory firm), Madison, WI, Vice President 2003 - 2005; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), Vice President, 2009 - Present | N/A |

Ray DiBernardo 1959 | Vice President, 2005 - Present | MIA, Vice President - Present; Madison Strategic Sector Premium Fund, Vice President, 2005 - Present | N/A |

Greg D. Hoppe 1969 | Treasurer, 2009 - Present Chief Financial Officer, 2005 - 2009 | MIA, Vice President, 1999 - Present; MAM, Vice President, 2009 - Present; Madison Mosaic, LLC, Vice President, 1999 - Present; Madison Mosaic Funds (13 funds), Treasurer, 2009 - Present; Chief Financial Officer, 1999 - 2009; Madison Strategic Sector Premium Fund, Treasurer, 2005 - Present; Chief Financial Officer, 2005 - 2009; Madison/Claymore Covered Call & Equity Strategy Fund, Vice President, 2008 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), Treasurer, 2009 - Present | N/A |

1 ÒInterested personÓ as defined in the Investment Company Act of 1940. Considered an interested Trustee because of the position held with the investment adviser of the Fund.

MSP | Madison Strategic Sector Premium Fund | Trustees and Officers | continued

| Position(s) and Length of Time Served | Principal Occupation(s) During Past Five Years | Other Directorships/Trusteeships |

Holly S. Baggot 1960 | Secretary and Assistant Treasurer, 2009 - Present | MAM, Vice President, 2009 - Present; MCA, Director-Mutual Funds, 2008 - 2009; Director-Mutual Fund Operations, 2006 - 2008; Operations Officer-Mutual Funds, 2005 - 2006; Senior Manager-Product & Fund Operations, 2001 - 2005; Madison Mosaic Funds (13 funds), Secretary and Assistant Treasurer, 2009 - Present; Madison Strategic Sector Premium Fund, Secretary and Assistant Treasurer, 2010 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), Assistant Treasurer, 2009 - Present; Secretary, 1999 - Present; Treasurer, 2008 - 2009; Assistant Treasurer, 1997 - 2007 | N/A |

W. Richard Mason 1960 | Chief Compliance Officer, 2005 - Present Corporate Counsel and Assistant Secretary, 2009 - Present General Counsel and Secretary, 2005 - 2009 | MIA, MAM, Madison Scottsdale, LC (an affiliated investment advisory firm of MIA) and Madison Mosaic, LLC, General Counsel and Chief Compliance Officer, 1996 - 2009; Chief Compliance Officer and Corporate Counsel, 2009 - Present; Mosaic Funds Distributor, LLC (an affiliated brokerage firm of MIA), Principal, 1998 - Present; Concord Asset Management (ÒConcordÓ) (an affiliated investment advisory firm of MIA), LLC, General Counsel, 1996 - 2009; Madison Mosaic Funds (13 funds) and Madison Strategic Sector Premium Fund, General Counsel, Chief Compliance Officer, 1992 - 2009; Chief Compliance Officer, Corporate Counsel, Secretary and Assistant Secretary, 2009 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), Chief Compliance Officer, Corporate Counsel and Assistant Secretary, 2009 - Present | N/A |

Pamela M. Krill 1966 | General Counsel, Chief Legal Officer and Assistant Secretary, 2009 - Present | MIA, MAM, Madison Scottsdale, LC, Madison Mosaic, LLC, Mosaic Funds Distributor, and Concord, General Counsel and Chief Legal Officer, 2009 - Present; Madison Mosaic Funds (13 funds), General Counsel, Chief Legal Officer and Assistant Secretary, 2009 - Present; Madison Strategic Sector Premium Fund, General Counsel, Chief Legal Officer and Assistant Secretary, 2010 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), General Counsel, Chief Legal Officer and Assistant Secretary, 2009 - Present; CUNA Mutual Insurance Society (insurance company with affiliated investment advisory, brokerage and mutual fund operations), Madison, WI, Managing Associate General Counsel-Securities & Investments, 2007 - 2009; Godfrey & Kahn, S.C. (law firm), Madison and Milwaukee, WI, Shareholder, Securities Practice Group, 1994-2007 | N/A |

MSP | Madison Strategic Sector Premium Fund | Trustees and Officers | concluded

Independent Trustees

Name and Year of Birth | Position(s) and Length of Time Served1 | Principal Occupation(s) During Past Five Years | Portfolios Overseen in Fund Complex2 | Other Directorships/Trusteeships |

Philip E. Blake 1944 | Trustee, 2005 - Present | Retired investor; Lee Enterprises, Inc (news and advertising publisher), Madison, WI, Vice President, 1998 - 2001; Madison Newspapers, Inc., Madison, WI, President and Chief Executive Officer, 1993 - 2000 | 46 | Madison Newspapers, Inc., 1993 - Present; Meriter Hospital & Health Services, 2000 - Present; Edgewood College, 2003 - Present; Madison Mosaic Funds (13 funds) and Madison Strategic Sector Premium Fund, 1996 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), 2009 - Present |

James R Imhoff, Jr. 1944 | Trustee, 2005 - Present | First Weber Group (real estate brokers), Madison, WI, Chief Executive Officer, 1996 - Present | 46 | Park Bank, 1978 - Present; Madison Mosaic Funds (13 funds) and Madison Strategic Sector Premium Fund, 1996 - Present; Madison/Claymore Covered Call and Equity Strategy Fund, 1996 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), 2009 - Present |

Lorence D. Wheeler 1938 | Trustee, 2005 - Present | Retired investor; Credit Union Benefits Services, Inc. (a provider of retirement plans and related services for credit union employees nationwide), Madison, WI, President, 1997 - 2001 | 46 | Grand Mountain Bank FSB and Grand Mountain Bancshares, Inc. 2003 - Present; Madison Mosaic Funds (13 funds) and Madison Strategic Sector Premium Fund, 1996 - Present; Madison/Claymore Covered Call and Equity Strategy Fund, 1996 - Present; MEMBERS Mutual Funds (13) and Ultra Series Fund (19), 2009 - Present |

1 Independent Trustees serve in such capacity until the Trustee reaches the age of 76, unless retirement is waived by unanimous vote of the remaining Trustees on an annual basis.

2 As of the date of this Annual Report, the Fund Complex consists of the Fund, the MEMBERS Mutual Funds with 13 portfolios, the Ultra Series Fund with 19 portfolios, and the Madison Mosaic Equity, Income, Tax-Free and Government Money Market Trusts, which together have 13 portfolios, for a grand total of 46 separate portfolios in the Fund Complex.

The Statement of Additional Information contains more information about the Trustees and is available upon request. To request a free copy, call Madison Mosaic Funds at 1-800-368-3195.

Dividend Reinvestment Plan | December 31, 2009

Unless the registered owner of common shares elects to receive cash by contacting Computershare Trust Company, Inc. (the ÒPlan AdministratorÓ), all dividends declared on common shares of the Fund will be automatically reinvested by the Plan Administrator in the Fund’s Dividend Reinvestment Plan (the ÒPlanÓ) in additional common shares of the Fund. Participation in the Plan is completely voluntary and may be terminated or resumed at any time without penalty by notice if received and processed by the Plan Administrator prior to the dividend record date; otherwise such termination or resumption will be effective with respect to any subsequently declared dividend or other distribution. Some brokers may automatically elect to receive cash on your behalf and may re-invest that cash in additional common shares of the Fund for you. If you wish for all dividends declared on your common shares of the Fund to be automatically reinvested pursuant to the Plan, please contact your broker.

The Plan Administrator will open an account for each common shareholder under the Plan in the same name in which such common shareholder’s common shares are registered. Whenever the Fund declares a dividend or other distribution (together, a ÒDividendÓ) payable in cash, non-participants in the Plan will receive cash and participants in the Plan will receive the equivalent in common shares. The common shares will be acquired by the Plan Administrator for the participants’ accounts, depending upon the circumstances described below, either (i) through receipt of additional unissued but authorized common shares from the Fund (ÒNewly Issued Common SharesÓ) or (ii) by purchase of outstanding common shares on the open market (ÒOpen-Market PurchasesÓ) on the New York Stock Exchange or elsewhere. If, on the payment date for any Dividend, the closing market price plus estimated brokerage commission per common share is equal to or greater than the net asset value per common share, the Plan Administrator will invest the Dividend amount in Newly Issued Common Shares on behalf of the participants. The number of Newly Issued Common Shares to be credited to each participant’s account will be determined by dividing the dollar amount of the Dividend by the net asset value per common share on the payment date; provided that, if the net asset value is less than or equal to 95% of the closing market value on the payment date, the dollar amount of the Dividend will be divided by 95% of the closing market price per common share on the payment date. If, on the payment date for any Dividend, the net asset value per common share is greater than the closing market value plus estimated brokerage commission, the Plan Administrator will invest the Dividend amount in common shares acquired on behalf of the participants in Open-Market Purchases.

If, before the Plan Administrator has completed its Open-Market Purchases, the market price per common share exceeds the net asset value per common share, the average per common share purchase price paid by the Plan Administrator may exceed the net asset value of the common shares, resulting in the acquisition of fewer common shares than if the Dividend had been paid in Newly Issued Common Shares on the Dividend payment date. Because of the foregoing difficulty with respect to Open-Market Purchases, the Plan provides that if the Plan Administrator is unable to invest the full Dividend amount in Open-Market Purchases during the purchase period or if the market discount shifts to a market premium during the purchase period, the Plan Administrator may cease making Open-Market Purchases and may invest the uninvested portion of the Dividend amount in Newly Issued Common Shares at net asset value per common share at the close of business on the Last Purchase Date provided that, if the net asset value is less than or equal to 95% of the then current market price per common share; the dollar amount of the Dividend will be divided by 95% of the market price on the payment date.

The Plan Administrator maintains all shareholders’ accounts in the Plan and furnishes written confirmation of all transactions in the accounts, including information needed by shareholders for tax records. Common shares in the account of each Plan participant will be held by the Plan Administrator on behalf of the Plan participant, and each shareholder proxy will include those shares purchased or received pursuant to the Plan. The Plan Administrator will forward all proxy solicitation materials to participants and vote proxies for shares held under the Plan in accordance with the instruction of the participants.

There will be no brokerage charges with respect to common shares issued directly by the Fund. However, each participant will pay a pro rata share of brokerage commission incurred in connection with Open-Market Purchases. The automatic reinvestment of Dividends will not relieve participants of any Federal, state or local income tax that may be payable (or required to be withheld) on such Dividends.

The Fund reserves the right to amend or terminate the Plan. There is no direct service charge to participants with regard to purchases in the Plan; however, the Fund reserves the right to amend the Plan to include a service charge payable by the participants.

All correspondence or questions concerning the Plan should be directed to the Plan Administrator, Computershare Trust Company, Inc., 250 Royall St., Canton, MA 02021, Phone Number: (781) 575-4523.

Board of Trustees

Philip E. Blake

Frank Burgess

James Imhoff, Jr.

Katherine Frank

Lorence Wheeler

Officers

Katherine L. Frank

President

Frank Burgess

Senior Vice President

Ray DiBernardo

Vice President

Paul Lefurgey

Vice President

Jay Sekelsky

Vice President

Holly Baggot

Secretary

Greg Hoppe

Chief Financial Officer & Treasurer

Pamela M. Krill

General Counsel , CLO & Asst Secretary

W. Richard Mason

Chief Compliance Officer & Asst Secretary

Investment Advisor

Madison Asset Management, LLC

550 Science Drive

Madison, WI 53711

Administrator

Madison Investment Advisors, Inc.

550 Science Drive

Madison, WI 53711

Custodian

US Bank NA

Milwaukee, Wisconsin

Transfer Agent

Computershare Investor Services, LLC

Canton, Massachusetts

Independent Registered Public Accounting Firm

Grant Thornton LLP

Chicago, Illinois

Privacy Principles of Madison Strategic Sector Premium Fund for Shareholders

The Fund is committed to maintaining the privacy of shareholders and to safeguarding its non-public information. The following information is provided to help you understand what personal information the Fund collects, how we protect that information and why, in certain cases, we may share information with select other parties.

Generally, the Fund does not receive any nonpublic personal information relating to its shareholders, although certain nonpublic personal information of its shareholders may become available to the Fund. The Fund does not disclose any nonpublic personal information about its shareholders or former shareholders to anyone, except as permitted by law or as is necessary in order to service shareholder accounts (for example, to a transfer agent or third party administrator).

The Fund restricts access to nonpublic personal information about the shareholders to Madison Asset Management, LLC and Madison Investment Advisors, Inc. employees with a legitimate business need for the information. The Fund maintains physical, electronic and procedural safeguards designed to protect the nonpublic personal information of its shareholders.

Question concerning your shares of Madison Strategic Sector Premium Fund?

| · | If your shares are held in a Brokerage Account, contact your Broker |

| · | If you have physical possession of your shares in certificate form, contact the Fund's Transfer Agent: Computershare Investor Services, LLC, 2 North LaSalle Street, Chicago, Illinois 60602 781-575-4523 |

This report is sent to shareholders of Madison Strategic Sector Premium Fund for their information. It is not a Prospectus, circular or representation intended for use in the purchase or sale of shares of the Fund or of any securities mentioned in this report.

In July 2009, the Fund submitted a CEO annual certification to the NYSE in which the Fund's principle executive officer certified that she was not aware, as of the date of the certification, of any violation by the Fund of the NYSE's Corporate Governance listing standards. In addition, as required by Section 302 of the Sarbanes-Oxley Act of 2002 and related SEC rules, the Fund's principle executive and principle financial officer have made quarterly certifications, including in filings with the SEC on forms N-CSR and N-Q, relating to, among other things, the Fund's disclosure controls and procedures and internal control over financial reporting.

Madison Investment Advisors, Inc.

550 SCIENCE DRIVE

MADISON, WISCONSIN 53711

1-800-767-0300

www.madisonfunds.com

Item 2. Code of Ethics.

(a) The Madison Strategic Sector Premium Fund (hereinafter referred to either as the "Trust" or the "Fund") has adopted a code of ethics that applies to the Trust’s principal executive officer, principal financial officer, principal accounting officer or controller or persons performing similar functions, regardless of whether these individuals are employed by the Trust or a third party. The code was first adopted during the fiscal year ended December 31, 2005.

(c) The code has not been amended since it was initially adopted.

(d) The Trust granted no waivers from the code during the period covered by this report.

(f) Any person may obtain a complete copy of the code without charge by calling the Trust at 800-767-0300 and requesting a copy of the "Madison Strategic Sector Premium Fund Sarbanes Oxley Code of Ethics."

Item 3. Audit Committee Financial Expert.

In July 2009, James R. Imhoff, Jr., an “independent” Trustee and a member of the Trust’s audit committee, was elected to serve as the Trust’s audit committee financial expert among the three Madison Mosaic independent Trustees who so qualify to serve in that capacity. He succeeded Lorence D. Wheeler who served in that capacity from August 2008 through July 2009.

Item 4. Principal Accountant Fees and Services.

(a) Total audit fees paid to the registrant's principal accountant for the fiscal year ended December 31, 2009 were approved not to exceed $22,700 (plus typical expenses in connection with the audit such as postage, photocopying, etc.). For the fiscal year ended December 31, 2008, this amount was $25,250. The registrant is affiliated with the Madison Mosaic family of open-end investment companies which paid the registrant's principal accountant an additional $85,300 and $88,500, respectively, for audit services provided to such funds for such periods.

(b) Audit-Related Fees. None.

(c) Tax-Fees. None incurred during the period covered by this report.

(d) All Other Fees. None.

(e) (1) Before any accountant is engaged by the registrant to render audit or non-audit services, the engagement must be approved by the audit committee as contemplated by paragraph (c)(7)(i)(A) of Rule 2-01of Regulation S-X.

(2) Not applicable.

(f) Not applicable.

(g) Not applicable.

(h) Not applicable.

Item 5. Audit Committee of Listed Registrants.

(a) The registrant has a separately-designated standing audit committee established in accordance with Section 3(a)(58)(A) of the Exchange Act (15 U.S.C. 78c(a)(58)(A)). The members of the committee include all the disinterested Trustees of the registrant, namely, Philip Blake, James Imhoff and Lorence Wheeler.

(b) Not applicable.

Item 6. Schedule of Investments

Included in report to shareholders (Item 1) above.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

The following discloses our current policies and procedures that we use to determine how to vote proxies relating to portfolio securities. Because we manage portfolios for clients in addition to the registrant, the policies and procedures are not specific to the registrant except as indicated.

Proxy Voting Policies

Our policies regarding voting the proxies of securities held in client accounts depend on the nature of our relationship to the client. When we are an ERISA fiduciary of an account, there are additional considerations and procedures than for all other (regular) accounts. In all cases, when we vote client proxies, we must do so in the client's best interests as described below by these policies.

Regular Accounts

We do not assume the role of an active shareholder when managing client accounts. If we are dissatisfied with the performance of a particular company, we will generally reduce or terminate our position in the company rather than attempt to force management changes through shareholder activism.

Making the Initial Decision on How to Vote the Proxy

As stated above, our goal and intent is to vote all proxies in the client's best interests. For practical purposes, unless we make an affirmative decision to the contrary, when we vote a proxy as the Board of Directors of a company recommends, it means we agree with the Board that voting in such manner is in the interests of our clients as shareholders of the company for the reasons stated by the Board. However, if we believe that voting as the Board of Directors recommends would not be in a client's best interests, then we must vote against the Board's recommendation.

As a matter of standard operating procedure, all proxies received shall be voted (by telephone or Internet or through a proxy voting service), unless we are not authorized to vote proxies. When the client has reserved the right to vote proxies in his/her/its account, we must make arrangements for proxies to be delivered directly to such client from its custodian and, to the extent any such proxies are received by us inadvertently, promptly forward them to the client.

Documenting our Decisions

In cases where a proxy will NOT be voted or, as described below, voted against the Board of Directors recommendation, our policy is to make a notation to the file containing the records for such security (e.g., Corporation X research file, since we may receive numerous proxies for the same company and it is impractical to keep such records in the file of each individual client) explaining our action or inaction, as the case may be. Alternatively, or in addition to such notation, we may include a copy of the rationale for such decision in the appropriate equity correspondence file.

Why would voting as the Board recommends NOT be in the client's best interests?

Portfolio management must, at a minimum, consider the following questions before voting any proxy:

1. Is the Board of Directors recommending an action that could dilute or otherwise diminish the value of our position? (This question is more complex than it looks: We must consider the time frames involved for both the client and the issuer. For example, if the Board of Directors is recommending an action that might initially cause the position to lose value but will increase the value of the position in the long-term, we would vote as the Board recommended for if we are holding the security for clients as a long-term investment. However, if the investment is close to our valuation limits and we are anticipating eliminating the position in the short-term, then it would be in our clients' best interests to vote against management's recommendation.)

2. If so, would we be unable to liquidate the affected securities without incurring a loss that would not otherwise have been recognized absent management's proposal?

3. Is the Board of Directors recommending an action that could cause the securities held to lose value, rights or privileges and there are no comparable replacement investments readily available on the market? (For example, a company can be uniquely positioned in the market because of its valuation compared with otherwise comparable securities such that it would not be readily replaceable if we were to liquidate the position. In such a situation, we might vote against management's recommendation if we believe a "No" vote could help prevent future share price depreciation resulting from management's proposal or if we believe the value of the investment will appreciate if management's proposal fails. A typical recent example of this type of decision is the case of a Board recommendation not to expense stock options, where we would vote against management's recommendation because we believe expensing such options will do more to enhance shareholder value going forward.)

4. Would accepting the Board of Directors recommendation cause us to violate our client's investment guidelines? (For example, a Board may recommend merging the company into one that is not permitted by client investment guidelines, e.g. a tobacco product company, a foreign security that is not traded on any US exchange or in US dollars, etc., restrictions often found in client investment guidelines. This would be an unusual situation and it is possible we would, nevertheless, vote in favor of a Board's recommendation in anticipation of selling the investment prior to the date any vote would effectively change the nature of the investment as described. Moreover, this does not mean we will consider any client-provided proxy voting guidelines. Our policy is that client investment guidelines may not include proxy voting guidelines if our firm will vote account proxies. Rather, we will only vote client proxies in accordance with these guidelines. Clients who wish their account proxies to be voted in accordance with their own proxy voting guidelines must retain proxy voting authority for themselves.)

Essentially, we must "second guess" the Board of Directors to determine if their recommendation is in the best interests of our clients, regardless of whether the Board thinks their recommendation is in the best interests of shareholders in general. The above questions should apply no matter the type of action subject to the proxy. For example, changes in corporate governance structures, adoption or amendments to compensation plans (including stock options) and matters involving social issues or corporate responsibility should all be reviewed in the context of how it will affect our clients' investment.

In making our decisions, to the extent we rely on any analysis outside of the information contained in the proxy statements, we must retain a record of such information in the same manner as other books and records (2 years in the office, 5 years in an easily accessible place). Also, if a proxy statement is NOT available on the SEC's EDGAR database, we must keep a copy of the proxy statement.

Addressing Conflicts of Interest