Exhibit (c)(3) *

Privileged and Confidential / Not to be Copied or Distributed

25 February 2010

PROJECT OSAKA

PRELIMINARY VALUE INDICATION

PRELIMINARY VALUE INDICATION

Information presented may vary subject to legal advice

* Certain slides not materially related to the Rule 13e-3 transaction have been removed

2

Privileged and Confidential / Not to be Copied or Distributed

§ Perella Weinberg Partners have prepared a preliminary valuation analysis of Osaka and a preliminary value range

recommendation for communication to Osaka

recommendation for communication to Osaka

– We believe the objective of this initial communication should be to ensure Osaka will engage into discussions while (i)

providing a value range consistent with the company’s performance and industry valuation metrics and (ii) retaining

flexibility with regards to valuation (notably to incorporate due diligence findings)

providing a value range consistent with the company’s performance and industry valuation metrics and (ii) retaining

flexibility with regards to valuation (notably to incorporate due diligence findings)

§ Our valuation analysis is solely based on Osaka’s 2009 performance and 2010-2014 forecasts excluding acquisitions, as

provided by Osaka management

provided by Osaka management

– Moderate top line growth

• 2009-2014 revenue CAGR of 8.1%, driven in part by 2010 - thereafter growth around 5-7%

– Significant margin improvement: 18.6% to 20.8% EBITDA margin from 2009 to 2014

• Significant expansion of gross margin in 2010 a key driver (from 53.7% to 55.4%)

– Top line growth and margin improvement in 2010 will require thorough investigation during due diligence

§ Valuation approach

– Valuation must factor in significant uncertainty around the Definity® business, a material contract between Osaka and

Essilor in the US market meant to expire in 2010

Essilor in the US market meant to expire in 2010

• Contract represents c. US$8m in annual sales for Osaka, at a gross margin estimated at a minimum of 60% (EBITDA

contribution of c. US$5m)

contribution of c. US$5m)

– DCF is used to derive intrinsic value of the business, but significant discount required given (i) execution risks associated

with high growth in cash flows, and (ii) absence of control

with high growth in cash flows, and (ii) absence of control

– Comparable company analysis and precedent transactions provide consistent benchmark to calibrate the DCF approach

• 2009 EBITDA multiple of 9.0-10.0x supported by both comparables and precedent transactions

• 2010 EBITDA multiple of 8.0-9.0x supported by both comparables and precedent transactions

– Current share price does not constitute a reliable valuation benchmark

• Limited free float, lack of analyst coverage and share price underperformance have resulted in very limited trading

volumes

volumes

INTRODUCTION

3

Privileged and Confidential / Not to be Copied or Distributed

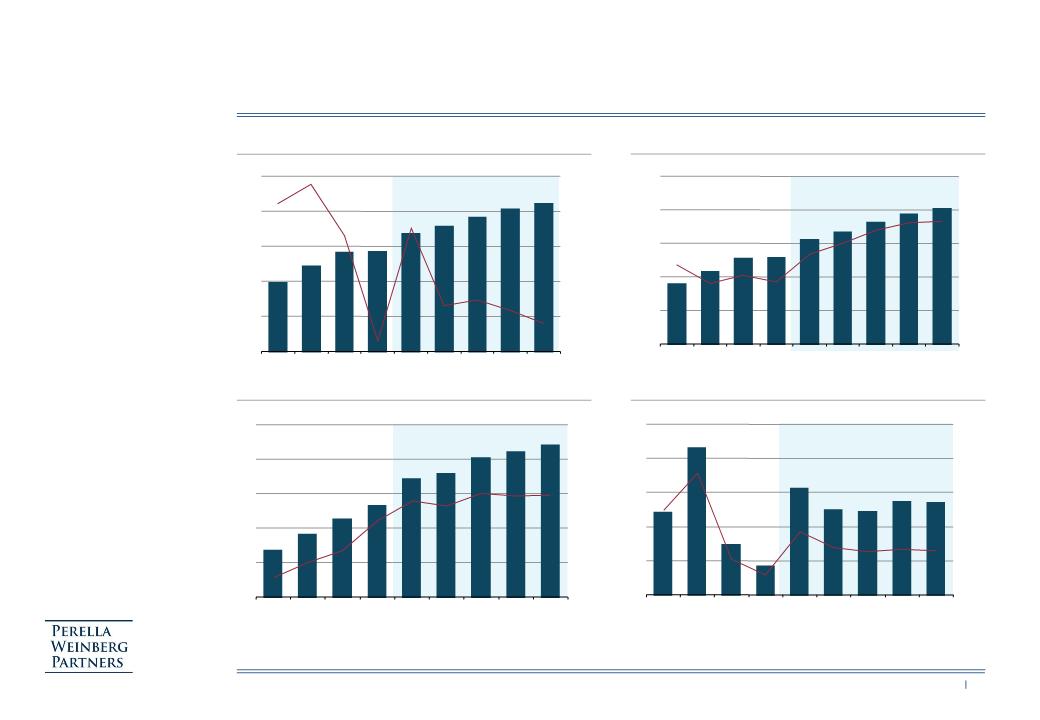

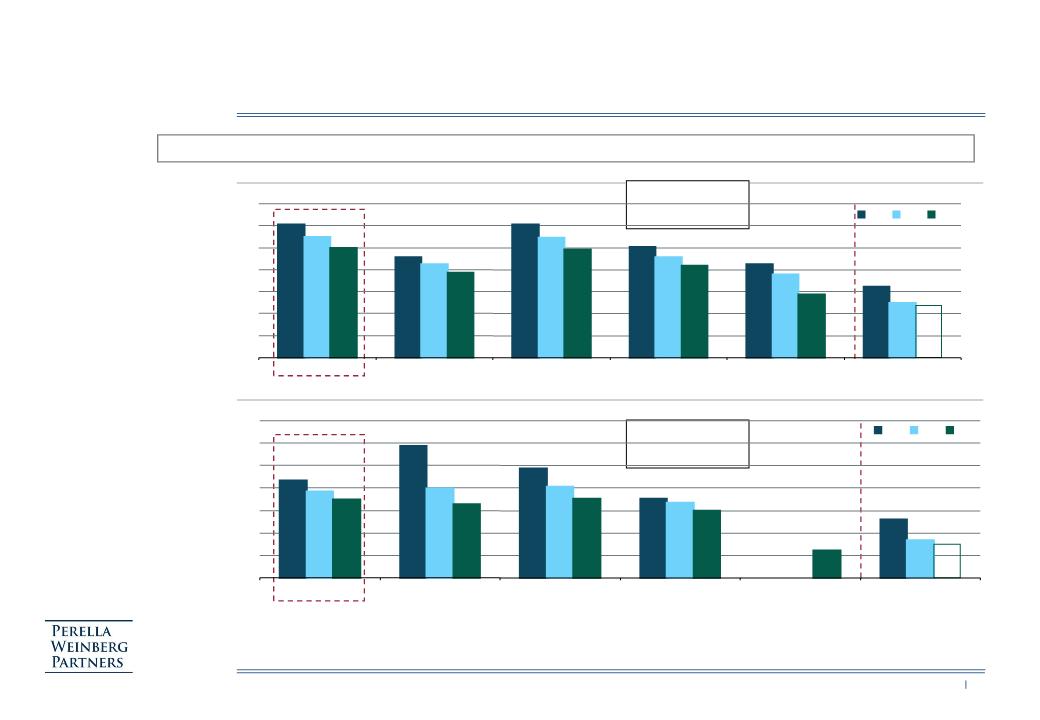

REVENUES

GROSS PROFIT

CAPEX

EBITDA

MANAGEMENT BUSINESS PLAN OVERVIEW

$m

$m

$m

$m

% Growth

% Revenues

% Revenues

% Revenues

Source: Company Filings, Osaka Business Plan (excluding acquisitions), not adjusted for potential loss of Definity® contract

– Significant gross margin

improvement projected in

forecast period - mostly

driven by 2010

improvement

improvement projected in

forecast period - mostly

driven by 2010

improvement

– Equally, strong EBITDA

growth projected for the

forecast period - with the

increase in 2010 followed

by almost flat 2011 despite

increasing revenues

growth projected for the

forecast period - with the

increase in 2010 followed

by almost flat 2011 despite

increasing revenues

– Capital expenditure

increase in 2010 justified

by investments in digital

surfacing machines - driver

of increased gross margin

(resulting higher sale of

prescription products) -

sustainability of medium

term capex levels around

4% of revenues

increase in 2010 justified

by investments in digital

surfacing machines - driver

of increased gross margin

(resulting higher sale of

prescription products) -

sustainability of medium

term capex levels around

4% of revenues

97

120

140

142

167

178

191

202

210

0

50

100

150

200

250

2006

2007

2008

2009

2010

2011

2012

2013

2014

0%

5%

10%

15%

20%

25%

53

65

76

76

93

100

109

116

121

0

30

60

90

120

150

2006

2007

2008

2009

2010

2011

2012

2013

2014

50%

52%

54%

56%

58%

60%

13

18

22

26

34

36

40

42

44

0

10

20

30

40

50

2006

2007

2008

2009

2010

2011

2012

2013

2014

12%

15%

18%

21%

24%

27%

7.2

12.9

4.4

2.5

9.3

7.4

7.3

8.2

8.1

0

3

6

9

12

15

2006

2007

2008

2009

2010

2011

2012

2013

2014

0%

3%

6%

9%

12%

15%

4

Privileged and Confidential / Not to be Copied or Distributed

PRELIMINARY VALUATION ANALYSIS

Premium to current share price:

Sources: Osaka Business Plan (excluding acquisitions), PWP assumptions

Notes: (1) Enterprise value less net cash ($2.2m), minorities ($10.5m; estimated by applying 11.0x EBIT multiple on 2010E minority interest) and plus associates ($1.3m); 16.6m shares outstanding

(2) Net of value attributed to the Definity® contract between Osaka and Essilor, representing $38.4m to $43.2m or $2.3 to $2.6 per share

(3) Before adjustment for potential loss of Definity® contract

Current share price: $9.80

No control

premium

reflected in

valuation

premium

reflected in

valuation

Valuation

reflects control

premium

reflects control

premium

DCF range using “Essilor WACC” of 8.0%:

($18.6 - $21.3)

($18.6 - $21.3)

Implied

Metric ($m)

(3)

Price per Share ($)

(1),(2)

Ent. Value ($m)

(2)

L3M

Trading Range

Last three months trading range of stock

$7.88 - $10.03

137 - 173

2009E EV/EBITDA Comparable Multiples

9.0x - 10.0x

26.4

201 - 221

2010E EV/EBITDA Comparable Multiples

8.0x - 9.0x

34.1

235 - 264

2010 EV/EBIT Multiples

11.0x - 12.0x

24.4

230 - 249

LFY EV/EBITDA transaction comparables

(LFY based on Dec-09 financials)

8.5x - 9.5x

26.4

187 - 208

LFY+1 EV/EBITDA transaction comparables

(LFY+1 based on Dec-10 financials)

8.0x - 9.0x

34.1

235 - 264

Discounted

Cash Flow

(2)

Based on 2010 - 2014 management forecasts

Perpetuity growth methodology

1.5% - 2.5%

PGR

8.5% - 9.0%

WACC

268 - 327

Transaction

Valuation

(2)

Standalone

Market

Valuation

(2)

15.8

13.8

10.9

13.8

11.7

7.9

19.3

15.5

12.1

14.6

15.5

12.9

10.0

13.5

6.4

9.8

13.2

16.7

20.1

23.5

27.0

(35%)

0%

35%

70%

105%

140%

175%

5

Privileged and Confidential / Not to be Copied or Distributed

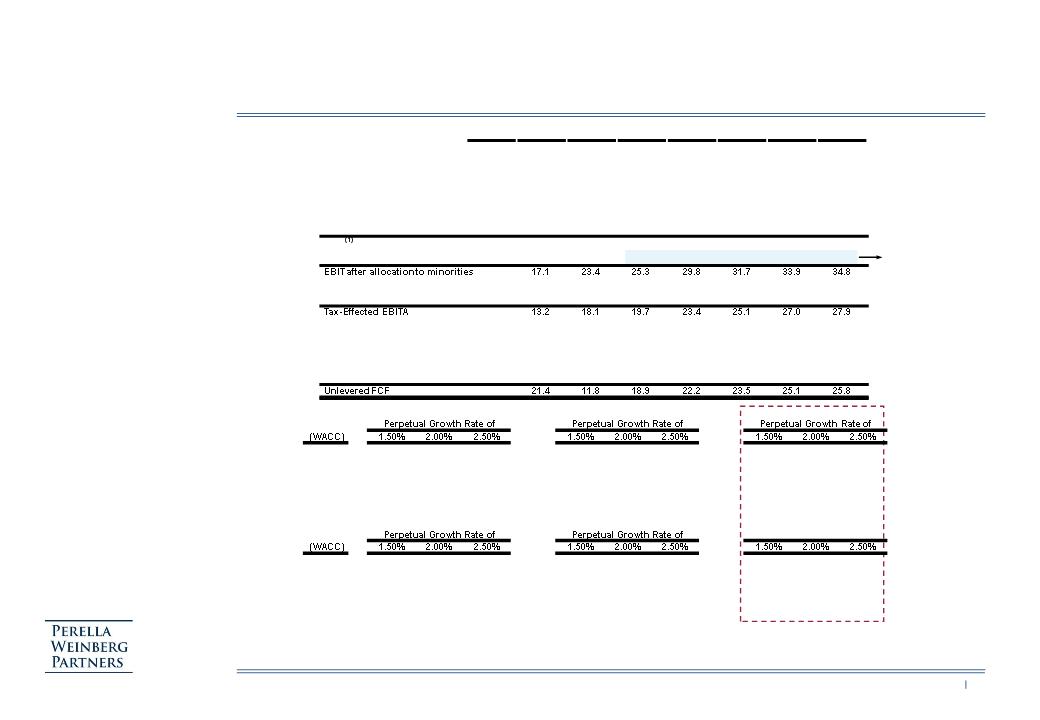

DCF ANALYSIS OF MANAGEMENT BUSINESS PLAN

Sources: Osaka Business Plan (excluding acquisitions), PWP assumptions

Notes: Valuation based on transaction in June 2010 - No adjustment for Definity® contract

(1) Includes option expense (treated as cash instead of incorporating the dilutive impact of options)

(2) Based on net debt of ($2.2m), associates of $1.3m and 16.6m shares outstanding

All value in US$m, FY Dec

2008A

2009A

2010E

2011E

2012E

2013E

2014E

Nrml

Revenues

140.3

142.4

167.4

178.3

191.2

202.4

210.5

210.5

Growth %

1.5%

17.6%

6.5%

7.3%

5.8%

4.0%

-

EBITDA

22.4

26.4

34.1

35.5

40.2

42.0

43.9

43.9

Margin %

16.0%

18.6%

20.4%

19.9%

21.0%

20.7%

20.8%

20.8%

Less: Depreciation

(9.1)

(8.8)

(9.7)

(9.2)

(9.2)

(9.0)

(8.6)

(7.7)

Depreciation / Capex %

350.0%

104.6%

124.1%

125.9%

109.9%

106.5%

95.0%

Depreciation / Revenues %

6.5%

6.1%

5.8%

5.2%

4.8%

4.4%

4.1%

3.6%

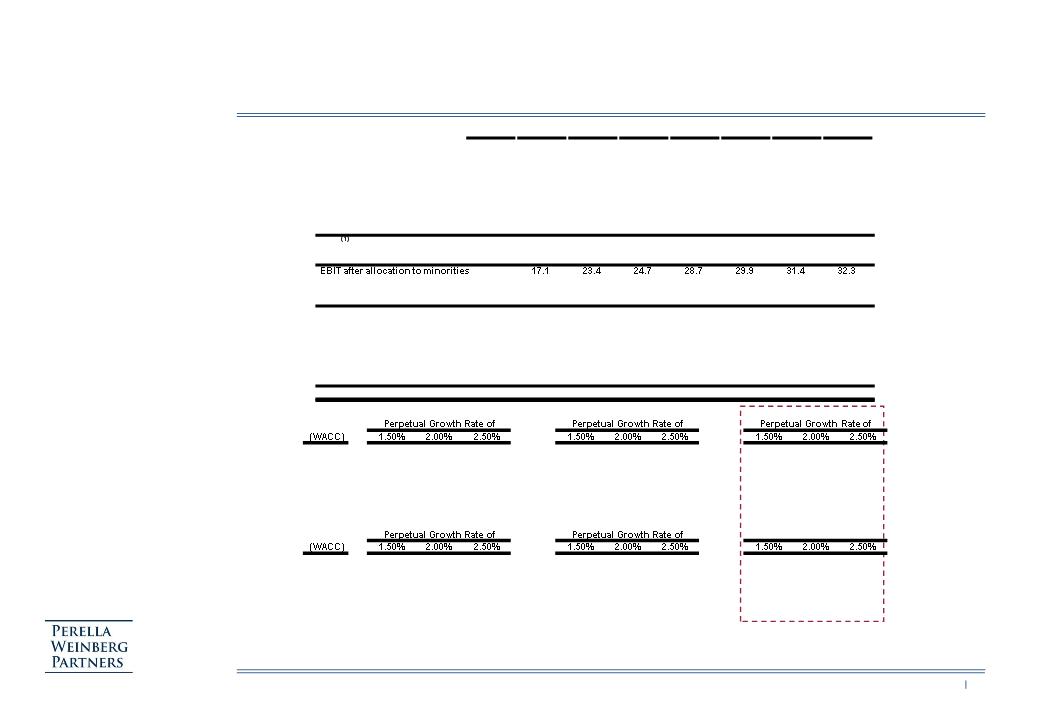

EBIT

17.7

24.4

26.3

31.0

33.0

35.3

36.2

Less: Allocation to minorities

(0.6)

(1.0)

(1.6)

(2.3)

(3.1)

(3.9)

(3.9)

Less: Tax Paid

(3.9)

(5.3)

(5.4)

(6.2)

(6.3)

(6.4)

(6.5)

Effective Tax Rate %

23.0%

22.5%

22.0%

21.5%

21.0%

20.5%

20.0%

Tax-Effected EBITA

13.2

18.1

19.2

22.5

23.6

25.0

25.9

Plus: Change in WC and Other

2.0

(6.8)

(2.6)

(3.1)

(2.4)

(2.4)

(1.6)

Change in WC / Change in Revenues

96.4%

(27.3%)

(23.6%)

(23.8%)

(21.5%)

(29.3%)

(20.0%)

Plus: Depreciation

8.8

9.7

9.2

9.2

9.0

8.6

7.7

Less: Cash Capex

(2.5)

(9.3)

(7.4)

(7.3)

(8.2)

(8.1)

(8.1)

Capex / Revenues %

1.8%

5.6%

4.2%

3.8%

4.0%

3.8%

3.8%

Unlevered FCF

21.4

11.8

18.5

21.3

22.0

23.1

23.8

Discount

Implied TV as % of EV

PV of Terminal Value

Enterprise Value

Rate

8.25%

76.3%

77.7%

79.2%

251

272

298

329

351

376

8.50%

75.5%

77.0%

78.4%

240

259

282

317

337

360

8.75%

74.8%

76.2%

77.7%

229

247

268

306

324

345

9.00%

74.1%

75.5%

76.9%

219

236

255

296

312

332

9.25%

73.3%

74.7%

76.1%

210

225

243

286

302

319

Discount

Implied TV EBITDA Multiple

EV / EBITDA 10E

Rate

Valuation per Share ($)

(2)

8.25%

8.2x

8.9x

9.7x

9.7x

10.3x

11.0x

20.1

21.4

22.9

8.50%

7.9x

8.5x

9.3x

9.3x

9.9x

10.6x

19.4

20.6

21.9

8.75%

7.6x

8.2x

8.9x

9.0x

9.5x

10.1x

18.7

19.8

21.1

9.00%

7.4x

7.9x

8.6x

8.7x

9.2x

9.7x

18.1

19.1

20.3

9.25%

7.1x

7.6x

8.3x

8.4x

8.8x

9.4x

17.5

18.4

19.5

6

Privileged and Confidential / Not to be Copied or Distributed

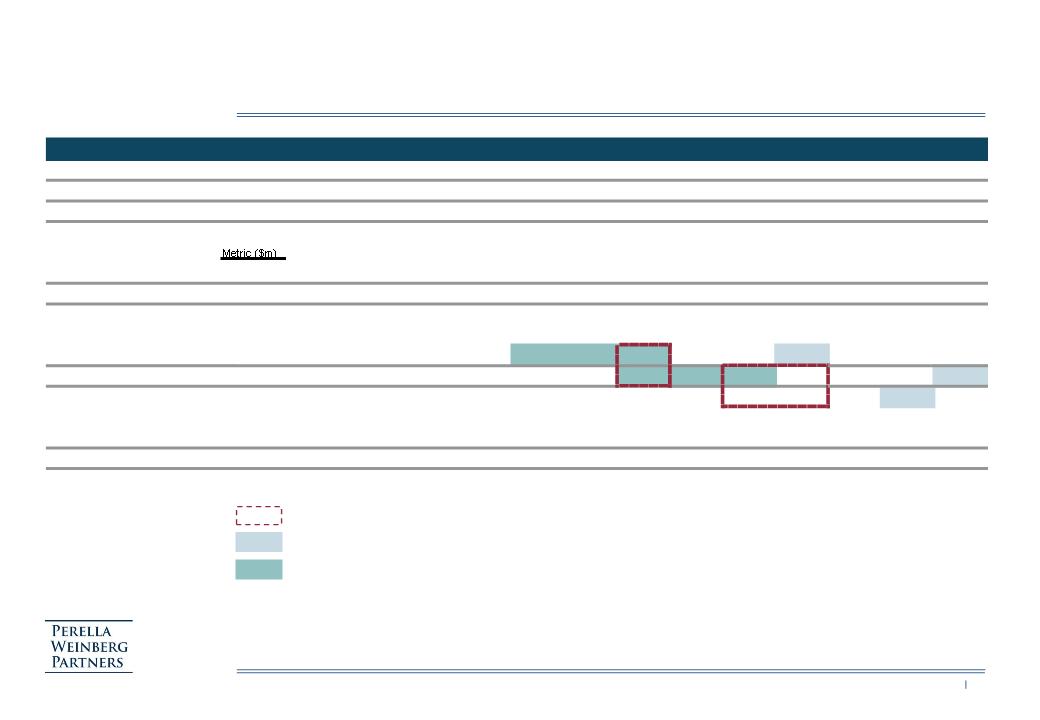

ANALYSIS AT VARIOUS PRICES (NO ADJUSTMENT FOR DEFINITY® CONTRACT)

Source: Osaka Business Plan (excluding acquisitions)

Notes: (1) Based on 16.6m shares outstanding

(2) Includes net debt of ($2.2m), minorities of $10.5m (estimated by applying 11.0x EBIT multiple on 2010E minority interest) and associates of ($1.3m)

(3) Not adjusted for loss of Definity® contract

Respective LTM and NTM EBITDA multiples of FGX transaction (assumed Osaka transaction in June 2010)

Essilor current trading ranges

Applicable multiple range (9.0x - 10.0x for 2009 EBITDA, 8.0x - 9.0x for 2010 EBITDA)

Offer Price ($/ Share)

9.8

11.0

12.0

13.0

14.0

15.0

16.0

17.0

18.0

19.0

20.0

21.0

22.0

Premium to Current Share Price ($9.80/share)

0.0%

12.2%

22.4%

32.7%

42.9%

53.1%

63.3%

73.5%

83.7%

93.9%

104.1%

114.3%

124.5%

Premium to 30 day average ($8.68/share)

12.8%

26.7%

38.2%

49.7%

61.2%

72.7%

84.2%

95.8%

107.3%

118.8%

130.3%

141.8%

153.3%

Implied Market Value ($m)

(1)

162

182

199

215

232

248

265

281

298

315

331

348

364

Implied Enterprise Value ($m)

(2)

169

189

206

222

239

255

272

288

305

322

338

355

371

(3)

Sales '09E

142

1.19x

1.33x

1.44x

1.56x

1.68x

1.79x

1.91x

2.03x

2.14x

2.26x

2.37x

2.49x

2.61x

Sales '10E

167

1.01x

1.13x

1.23x

1.33x

1.43x

1.53x

1.62x

1.72x

1.82x

1.92x

2.02x

2.12x

2.22x

Sales '11E

178

0.95x

1.06x

1.15x

1.25x

1.34x

1.43x

1.53x

1.62x

1.71x

1.80x

1.90x

1.99x

2.08x

EBITDA '09E

26.4

6.4x

7.2x

7.8x

8.4x

9.0x

9.7x

10.3x

10.9x

11.5x

12.2x

12.8x

13.4x

14.0x

EBITDA '10E

34.1

5.0x

5.5x

6.0x

6.5x

7.0x

7.5x

8.0x

8.5x

8.9x

9.4x

9.9x

10.4x

10.9x

EBITDA '11E

35.5

4.8x

5.3x

5.8x

6.3x

6.7x

7.2x

7.7x

8.1x

8.6x

9.0x

9.5x

10.0x

10.4x

EBIT '09E

17.7

9.6x

10.7x

11.6x

12.6x

13.5x

14.4x

15.4x

16.3x

17.2x

18.2x

19.1x

20.0x

21.0x

EBIT '10E

24.4

6.9x

7.8x

8.4x

9.1x

9.8x

10.5x

11.2x

11.8x

12.5x

13.2x

13.9x

14.6x

15.2x

EBIT'11E

26.3

6.4x

7.2x

7.8x

8.4x

9.1x

9.7x

10.3x

11.0x

11.6x

12.2x

12.9x

13.5x

14.1x

7

Privileged and Confidential / Not to be Copied or Distributed

ANALYSIS AT VARIOUS PRICES (WITH ADJUSTMENT FOR DEFINITY CONTRACT)

Source: Osaka Business Plan (excluding acquisitions)

Notes: (1) Based on 16.6m shares outstanding

(2) Includes net debt of ($2.2m), minorities of $10.5m (estimated by applying 11.0x EBIT multiple on 2010E minority interest) and associates of ($1.3m)

(3) Adjusted for loss of Definity® contract

Respective LTM and NTM EBITDA multiples of FGX transaction (assumed Osaka transaction in June 2010)

Essilor current trading ranges

Applicable multiple range (9.0x - 10.0x for 2009 EBITDA, 8.0x - 9.0x for 2010 EBITDA)

Offer Price ($/ Share)

9.8

11.0

12.0

13.0

14.0

15.0

16.0

17.0

18.0

19.0

20.0

21.0

22.0

Premium to Current Share Price ($9.80/share)

0.0%

12.2%

22.4%

32.7%

42.9%

53.1%

63.3%

73.5%

83.7%

93.9%

104.1%

114.3%

124.5%

Premium to 30 day average ($8.68/share)

12.8%

26.7%

38.2%

49.7%

61.2%

72.7%

84.2%

95.8%

107.3%

118.8%

130.3%

141.8%

153.3%

Implied Market Value ($m)

(1)

162

182

199

215

232

248

265

281

298

315

331

348

364

Implied Enterprise Value ($m)

(2)

169

189

206

222

239

255

272

288

305

322

338

355

371

(3)

Sales '09E

134

1.26x

1.41x

1.53x

1.65x

1.78x

1.90x

2.02x

2.15x

2.27x

2.39x

2.52x

2.64x

2.76x

Sales '10E

159

1.06x

1.19x

1.29x

1.39x

1.50x

1.60x

1.71x

1.81x

1.91x

2.02x

2.12x

2.22x

2.33x

Sales '11E

170

0.99x

1.11x

1.21x

1.31x

1.40x

1.50x

1.60x

1.69x

1.79x

1.89x

1.99x

2.08x

2.18x

EBITDA '09E

21.6

7.8x

8.7x

9.5x

10.3x

11.0x

11.8x

12.6x

13.3x

14.1x

14.9x

15.6x

16.4x

17.2x

EBITDA '10E

29.3

5.8x

6.5x

7.0x

7.6x

8.2x

8.7x

9.3x

9.8x

10.4x

11.0x

11.5x

12.1x

12.7x

EBITDA '11E

30.7

5.5x

6.2x

6.7x

7.2x

7.8x

8.3x

8.8x

9.4x

9.9x

10.5x

11.0x

11.5x

12.1x

EBIT '09E

12.9

13.1x

14.7x

16.0x

17.2x

18.5x

19.8x

21.1x

22.4x

23.7x

24.9x

26.2x

27.5x

28.8x

EBIT '10E

19.6

8.7x

9.7x

10.5x

11.4x

12.2x

13.1x

13.9x

14.7x

15.6x

16.4x

17.3x

18.1x

19.0x

EBIT'11E

21.5

7.9x

8.8x

9.6x

10.3x

11.1x

11.9x

12.6x

13.4x

14.2x

15.0x

15.7x

16.5x

17.3x

8

Privileged and Confidential / Not to be Copied or Distributed

§ Value range determination

– 50/50 transaction structure (joint instead of full control), requiring a discount to DCF

– Jump in 2010 performance a key driver of value, but uncertainty on ability of Osaka to deliver

– Objective to offer a fair price to obtain support from management for the transaction, whilst retaining some headroom to

improve the terms if required

improve the terms if required

– Absence of premium for synergies given they will be shared equally as a result of the envisaged 50/50 structure

§ Proposal for discussion

– Value range of US$12.0 to US$14.0 per share represents a 19% to 30% discount to the DCF mid-point of US$17.3

(US$19.8 less US$2.5 for the Definity® contract)

(US$19.8 less US$2.5 for the Definity® contract)

– Bottom end of the range based on actual 2009 EBITDA, plus some premium for joint control

– High end of the range gives full credit to the 2010 EBITDA (but below the bottom end of the DCF), and is only

achievable if due diligence can confirm the 2010 budget can be delivered, plus some premium for joint control

achievable if due diligence can confirm the 2010 budget can be delivered, plus some premium for joint control

§ Format of communication on value

– No written indication of interest (i) to mitigate risks of disclosure obligations and (ii) to retain flexibility going forward

• Conference call rather than meeting: best not to explain our methodology otherwise can be used against our position

going forward

going forward

• Follow-up meeting possible if required

– Value range required given (i) uncertainty on forecasts and assumptions underlying the forecasts, (ii) lack of public

information (no broker forecasts, limited guidance from company), and (iii) need to retain flexibility

information (no broker forecasts, limited guidance from company), and (iii) need to retain flexibility

– Osaka have asked for Essilor to provide a standalone value and the applicable premium: best to avoid providing such

breakdown as those elements could be used against Essilor in a second stage

breakdown as those elements could be used against Essilor in a second stage

VALUE PROPOSITION

Privileged and Confidential / Not to be Copied or Distributed

APPENDIX

12

Privileged and Confidential / Not to be Copied or Distributed

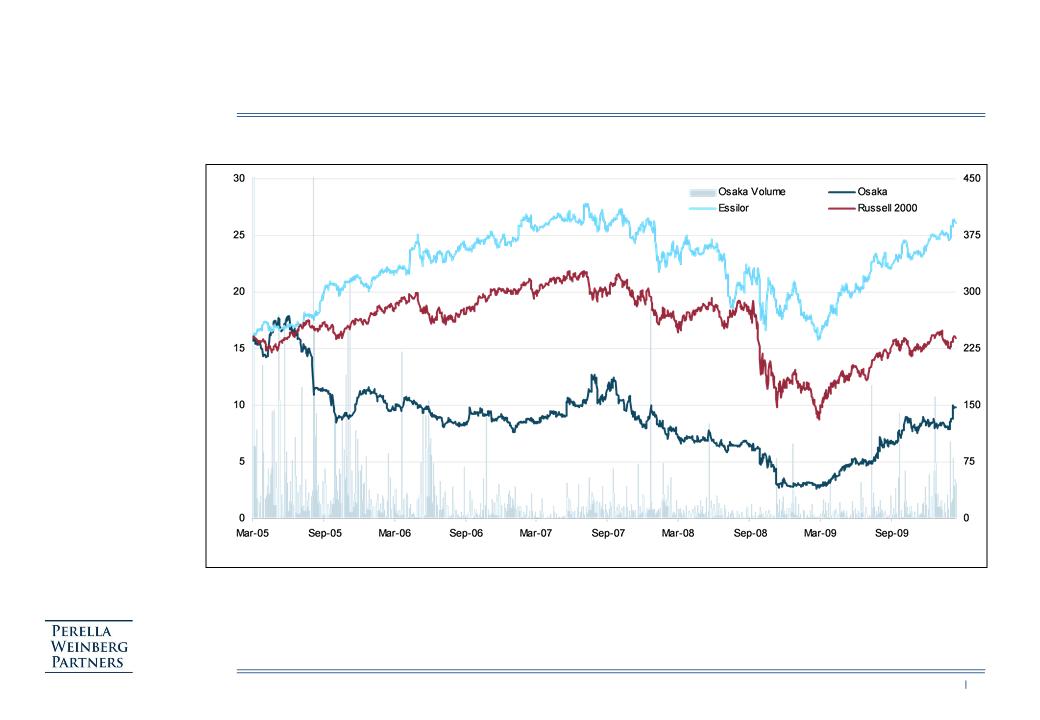

SHARE PRICE DEVELOPMENT

Share price (US$) - Rebased to Osaka

Trading Volume (‘000s)

Source: Factset

13

Privileged and Confidential / Not to be Copied or Distributed

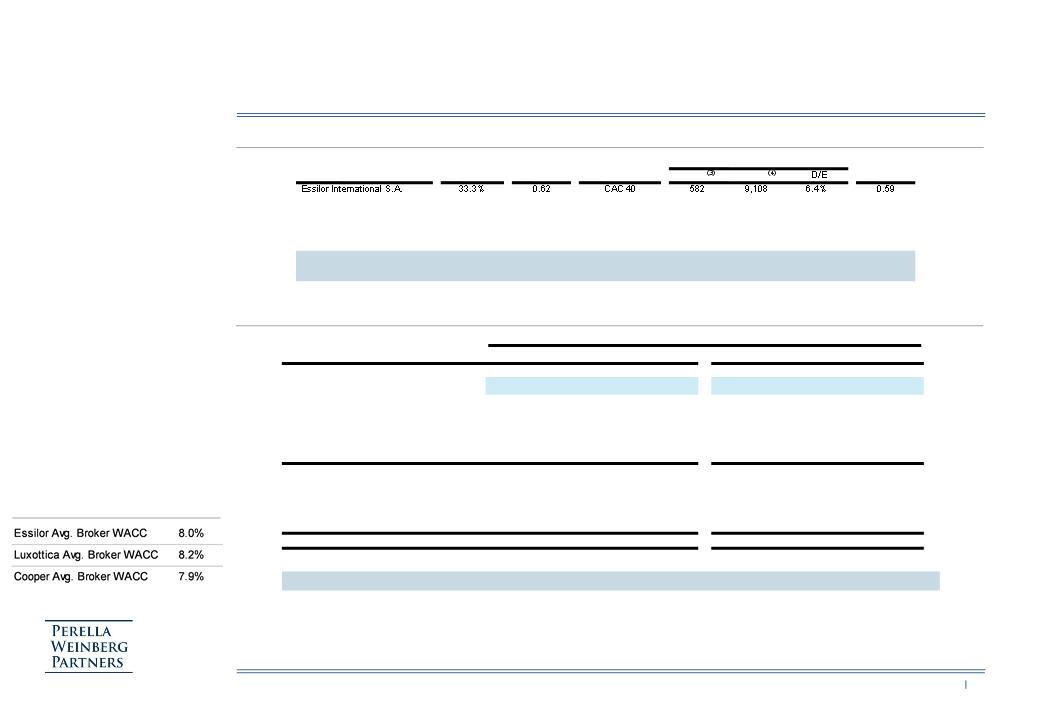

WACC ANALYSIS

Sources: Company Filings, Bloomberg, Factset, KPMG Tax Survey

Notes: (1) Effective corporate tax rates

(2) Bloomberg 10 year (or available for companies trading less than 10 years) adjusted beta relative to respective index

(3) Net financial debt as last reported

(4) Market capitalization as of 23-Feb-10

(5) Current yield on USD denominated 10 year Israeli government bond

WACC - BROKER BENCHMARKING

DERIVATION OF UNLEVERED BETA

WACC CALCULATION

– Based on a company specific

calculations and

benchmarking to

competitors, a WACC of

around 8.5% - 9.0% could

be justified

calculations and

benchmarking to

competitors, a WACC of

around 8.5% - 9.0% could

be justified

Leveraged

Benchmark

Debt/ Equity (€m)

Unlevered

Company

Tax Rate

(1)

Beta

(2)

Index

Debt

Equity

Beta

Hoya Corp.

40.7%

0.88

Topix

0

7,999

0.0%

0.88

Luxottica Group S.p.A.

31.4%

0.82

FTSE MIB

2,414

8,637

27.9%

0.69

Cooper Cos.

40.0%

0.79

Russell 2000

573

1,306

43.9%

0.62

Safilo Group S.p.A.

31.4%

1.21

FTSE MIB

586

90

n/m

n/m

Average

0.86

19.5%

0.70

Median

0.82

17.2%

0.65

Osaka

20.0%

0.63

Russell 2000

0

119

0.0%

0.63

Target Debt / Equity

0.0%

25.0%

50.0%

0.0%

25.0%

50.0%

Implied Debt / Enterprise Value

0.0%

20.0%

33.3%

0.0%

20.0%

33.3%

Selected Unlevered Beta

0.70

0.70

0.70

0.80

0.80

0.80

COST OF EQUITY

Implied Levered Beta

0.70

0.84

0.97

0.80

0.96

1.12

x Market Risk Premium

5.50%

5.50%

5.50%

5.50%

5.50%

5.50%

+ Risk Free Rate

(5)

4.74%

4.74%

4.74%

4.74%

4.74%

4.74%

Cost of Equity

8.57%

9.33%

10.10%

9.14%

10.02%

10.90%

COST OF DEBT

Risk Free Rate

4.74%

4.74%

4.74%

4.74%

4.74%

4.74%

Risk Premium

0.50%

1.00%

1.50%

0.50%

1.00%

1.50%

Pre Tax Cost of Debt

5.24%

5.74%

6.24%

5.24%

5.74%

6.24%

After Tax Cost of Debt

4.19%

4.59%

4.99%

4.19%

4.59%

4.99%

Weighted Average Cost of Capital

(3)

8.57%

8.39%

8.40%

9.14%

8.93%

8.93%

14

Privileged and Confidential / Not to be Copied or Distributed

PRELIMINARY DCF OF BUSINESS PLAN (ADJUSTED MINORITIES)

Sources: Osaka Business Plan (excluding acquisitions), PWP assumptions

Notes: Valuation based on transaction in June 2010 - No adjustment for Definity® contract

(1) Includes option expense (treated as cash instead of incorporating the dilutive impact of options)

(2) Based on net debt of ($2.2m), associates of $1.3m and 16.6m shares outstanding

Adjusted to grow in line

with EBIT

with EBIT

All value in US$m, FY Dec

2008A

2009A

2010E

2011E

2012E

2013E

2014E

Nrml

Revenues

140.3

142.4

167.4

178.3

191.2

202.4

210.5

210.5

Growth %

1.5%

17.6%

6.5%

7.3%

5.8%

4.0%

-

EBITDA

22.4

26.4

34.1

35.5

40.2

42.0

43.9

43.9

Margin %

16.0%

18.6%

20.4%

19.9%

21.0%

20.7%

20.8%

20.8%

Less: Depreciation

(9.1)

(8.8)

(9.7)

(9.2)

(9.2)

(9.0)

(8.6)

(7.7)

Depreciation / Capex %

350.0%

104.6%

124.1%

125.9%

109.9%

106.5%

95.0%

Depreciation / Revenues %

6.5%

6.1%

5.8%

5.2%

4.8%

4.4%

4.1%

3.6%

EBIT

17.7

24.4

26.3

31.0

33.0

35.3

36.2

Less: Allocation to minorities

(0.6)

(1.0)

(1.0)

(1.2)

(1.3)

(1.4)

(1.4)

Less: Tax Paid

(3.9)

(5.3)

(5.6)

(6.4)

(6.7)

(6.9)

(7.0)

Effective Tax Rate %

23.0%

22.5%

22.0%

21.5%

21.0%

20.5%

20.0%

Plus: Change in WC and Other

2.0

(6.8)

(2.6)

(3.1)

(2.4)

(2.4)

(1.6)

Change in WC / Change in Revenues

96.4%

(27.3%)

(23.6%)

(23.8%)

(21.5%)

(29.3%)

(20.0%)

Plus: Depreciation

8.8

9.7

9.2

9.2

9.0

8.6

7.7

Less: Cash Capex

(2.5)

(9.3)

(7.4)

(7.3)

(8.2)

(8.1)

(8.1)

Capex / Revenues %

1.8%

5.6%

4.2%

3.8%

4.0%

3.8%

3.8%

Discount

Implied TV as % of EV

PV of Terminal Value

Enterprise Value

Rate

8.25%

76.9%

78.3%

79.8%

272

295

322

354

377

404

8.50%

76.2%

77.6%

79.0%

260

281

306

341

362

387

8.75%

75.5%

76.8%

78.3%

248

268

291

329

348

371

9.00%

74.7%

76.1%

77.5%

237

256

277

318

336

357

9.25%

74.0%

75.4%

76.8%

227

244

264

307

324

343

Discount

Implied TV EBITDA Multiple

EV / EBITDA 10E

Rate

Valuation per Share ($)

(2)

8.25%

8.9x

9.6x

10.5x

10.4x

11.1x

11.9x

21.6

23.0

24.6

8.50%

8.5x

9.2x

10.1x

10.0x

10.6x

11.4x

20.8

22.1

23.6

8.75%

8.2x

8.9x

9.7x

9.6x

10.2x

10.9x

20.1

21.3

22.6

9.00%

8.0x

8.6x

9.3x

9.3x

9.8x

10.5x

19.4

20.5

21.8

9.25%

7.7x

8.3x

8.9x

9.0x

9.5x

10.1x

18.8

19.8

20.9

15

Privileged and Confidential / Not to be Copied or Distributed

TRADING COMPARABLES ANALYSIS

EV/ EBITDA(1)

PRICE/ EARNINGS

Sources: Company Filings, Factset, IBES estimates. Company estimates and PWP assumptions for Osaka

Notes: Share prices as of 23 February 2010. Financials calendarised to December year end

(1) Enterprise value calculated as market capitalisation plus net debt, minority interest, pensions and other post retirement obligations and less associates

(2) Net debt and financial forecasts pro forma for FGX acquisition

n/m

– Essilor is the best comparable

in optical lenses, but benefits

from a premium valuation due

to its financial track-record,

stability and firmly established

world leader position

in optical lenses, but benefits

from a premium valuation due

to its financial track-record,

stability and firmly established

world leader position

– Hoya includes pure play

Hoya Vision which however

only makes up 25% of total

turnover

Hoya Vision which however

only makes up 25% of total

turnover

– Luxottica, Cooper and Safilo

are secondary comparables due

to their focus on frames and

distribution

are secondary comparables due

to their focus on frames and

distribution

– Osaka trading well below its

broadly defined peer group

despite its good growth and

profitability track record

broadly defined peer group

despite its good growth and

profitability track record

(2)

(2)

Mean 2009: 10.4x

Mean 2010: 9.4x

Mean 2011: 8.3x

Mean 2009: 23.2x

Mean 2010: 19.0x

Mean 2011: 14.4x

10.8%

9.6%

22.1%

8.4%

10.2%

EBITDA CAGR ’09 - ’11

15.9%

n/m

12.1x

9.1x

12.1x

10.0x

8.5x

6.4x

10.9x

8.5x

10.9x

9.2x

7.6x

5.0x

10.0x

7.7x

9.8x

8.3x

5.7x

4.8x

-

2x

4x

6x

8x

10x

12x

14x

Essilor

Hoya

Luxottica

Cooper

Safilo

Osaka

2009

2010

2011

21.6x

29.2x

24.3x

17.5x

12.9x

19.2x

19.8x

20.3x

16.8x

8.4x

17.3x

16.3x

17.7x

14.9x

6.0x

7.5x

-

5x

10x

15x

20x

25x

30x

35x

Essilor

Hoya

Luxottica

Cooper

Safilo

Osaka

2009

2010

2011

16

Privileged and Confidential / Not to be Copied or Distributed

PRECEDENT TRANSACTIONS ANALYSIS

Sources: Company Filings, Factiva, Mergermarket

Notes: (1) Calculated using the share price 1 week prior to announcement

(2) EV of €600m based on Financial Times news article (27-Dec-06)

(3) Sales of ¥50 Bn based on Reuters news article (11-Dec-07)

(3)

(2)

– Recognizing differences in

products, FGX/ Essilor

likely to be a meaningful

precedent given recent deal

and similar strategic

rationale - will be used as

benchmark by minority

shareholders specifically

products, FGX/ Essilor

likely to be a meaningful

precedent given recent deal

and similar strategic

rationale - will be used as

benchmark by minority

shareholders specifically

– Multiples paid in main

precedent transactions are

broadly consistent with

trading multiples

precedent transactions are

broadly consistent with

trading multiples

(1)

Date

Premium to

Enterprise

Announced

Target

Acquiror

Rationale

Unaffected Share Price

Equity Value (€m)

Value (€m)

16-Dec-09

FGX International

Essilor

Leverage brands on distribution network

23.9%

300

371

16-Jun-08

Satisloh Holding

Essilor

Product expansion and leverage distribution

n/a

346

346

09-May-08

NH Techno Glass

Carlyle

Private equity acquisition

n/a

510

883

22-Dec-06

Rodenstock

Bridgepoint

Private equity acquisition

n/a

n/a

600

05-Dec-04

SOLA International

Carl Zeiss Vision/ EQT

Complementary overall portfolios

33.9%

675

888

Mean

28.9%

Date

EV / Sales

EV / EBITDA

EV / EBIT

P/E

EBITDA Margin (%)

Announced

Target

Acquiror

LTM

LFY+1

LTM

LFY+1

LTM

LFY+1

LTM

LFY+1

LTM

LFY+1

16-Dec-09

FGX International

Essilor

1.96x

2.06x

9.1x

9.2x

13.4x

13.1x

27.8x

20.4x

21.5%

22.4%

16-Jun-08

Satisloh Holding

Essilor

2.07x

n/a

12.2x

n/a

13.3x

n/a

n/a

n/a

16.9%

n/a

09-May-08

NH Techno Glass

Carlyle

2.81x

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

22-Dec-06

Rodenstock

Bridgepoint

1.74x

n/a

9.2x

n/a

n/a

n/a

n/a

n/a

18.9%

n/a

05-Dec-04

SOLA International

Carl Zeiss Vision/ EQT

1.78x

1.70x

12.2x

9.3x

17.0x

12.0x

n/m

n/a

14.6%

n/a

Mean

2.07x

1.88x

10.7x

9.3x

14.6x

12.5x

27.8x

20.4x

18.0%

22.4%

17

Privileged and Confidential / Not to be Copied or Distributed

OVERVIEW OF OSAKA OPTION HOLDERS

Source: Osaka 20-F FY 2008

Notes: Number of options outstanding as of 31 December 2008, but already reflecting announced cancellations and amendments having occurred in 2009

(1) All options will be terminated 31 March 2010

(1)

– The management team

would receive between

$6.8m and $10.5m in

proceeds at the suggested

range of $14-17 per share

(excludes the options of the

Ex CEO which lapse end

of March 2010)

would receive between

$6.8m and $10.5m in

proceeds at the suggested

range of $14-17 per share

(excludes the options of the

Ex CEO which lapse end

of March 2010)

Avg. Strike

Proceeds (US$m) at offer price of

Name

Function

Options

Price (US$)

US$14.0

US$15.0

US$16.0

US$17.0

Eyal Hayardeny

Ex President/ CEO

225,623

9.64

0.98

1.21

1.44

1.66

Dan Katzman

Chief Technology Officer

200,591

4.08

1.99

2.19

2.39

2.59

Michael Latzer

President Shamir USA

105,000

9.72

0.45

0.55

0.66

0.76

Yagen Moshe

Chief Financial Officer

100,000

9.25

0.47

0.57

0.67

0.77

Uzi Tzur

Chairman of Board

75,000

10.05

0.30

0.37

0.45

0.52

Dagan Avishai

Vice President of Marketing

66,973

10.06

0.26

0.33

0.40

0.46

Youval Katzman

Shamir Special Optical Products

35,000

9.58

0.15

0.19

0.22

0.26

Zohar Katzman

Shamir Special Optical Products

35,000

9.58

0.15

0.19

0.22

0.26

Rami Ben-Ze'ev

Vice President Business Management

23,540

9.75

0.10

0.12

0.15

0.17

Other directors & officers

Various

128,620

12.44

0.20

0.33

0.46

0.59

Subtotal

995,347

8.91

5.1

6.1

7.1

8.1

Executive officers & employees

(can not be assigned)

Various

256,000

5.00

2.3

2.6

2.8

3.1

R&D employees

(can not be assigned)

Various

214,312

12.19

0.39

0.60

0.82

1.03

Subtotal

470,312

8.27

2.7

3.2

3.6

4.1

Total options outstanding

1,465,659

8.70

7.8

9.2

10.7

12.2

18

Privileged and Confidential / Not to be Copied or Distributed

This Presentation has been provided to you by Perella Weinberg Partners and its affiliates (collectively “Perella Weinberg Partners” or the

“Firm”) and may not be used or relied upon for any purpose without the written consent of Perella Weinberg Partners. The information

contained herein (the “Information”) is confidential. By accepting this Information, you agree that you and your directors, partners, officers,

employees, attorney(s), agents and representatives agree to use it for informational purposes only and will not divulge any such Information to

any other party. Reproduction of this Information, in whole or in part, is prohibited. These contents are proprietary and a product of Perella

Weinberg Partners. The Information contained herein is not an offer to buy or sell or a solicitation of an offer to buy or sell any

corporate advisory services or security or to participate in any corporate advisory services or trading strategy. Any decision regarding

corporate advisory services or to invest in the investments described herein should be made after, as applicable, reviewing such definitive

offering memorandum, conducting such investigations as you deem necessary and consulting the investor’s own investment, legal, accounting

and tax advisors in order to make an independent determination of the suitability and consequences of an investment or service.

“Firm”) and may not be used or relied upon for any purpose without the written consent of Perella Weinberg Partners. The information

contained herein (the “Information”) is confidential. By accepting this Information, you agree that you and your directors, partners, officers,

employees, attorney(s), agents and representatives agree to use it for informational purposes only and will not divulge any such Information to

any other party. Reproduction of this Information, in whole or in part, is prohibited. These contents are proprietary and a product of Perella

Weinberg Partners. The Information contained herein is not an offer to buy or sell or a solicitation of an offer to buy or sell any

corporate advisory services or security or to participate in any corporate advisory services or trading strategy. Any decision regarding

corporate advisory services or to invest in the investments described herein should be made after, as applicable, reviewing such definitive

offering memorandum, conducting such investigations as you deem necessary and consulting the investor’s own investment, legal, accounting

and tax advisors in order to make an independent determination of the suitability and consequences of an investment or service.

The information used in preparing these materials may have been obtained from or through you or your representatives or from public sources.

Perella Weinberg Partners assumes no responsibility for independent verification of such information and has relied on such information being

complete and accurate in all material respects. To the extent such information includes estimates and/or forecasts of future financial

performance (including estimates of potential cost savings and synergies) prepared by or reviewed or discussed with the managements of your

company and/or other potential transaction participants or obtained from public sources, we have assumed that such estimates and forecasts

have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such managements (or, with respect to

estimates and forecasts obtained from public sources, represent reasonable estimates). The Firm has no obligation (express or implied) to update

any or all of the Information or to advise you of any changes; nor do we make any express or implied warranties or representations as to the

completeness or accuracy or accept responsibility for errors.

Perella Weinberg Partners assumes no responsibility for independent verification of such information and has relied on such information being

complete and accurate in all material respects. To the extent such information includes estimates and/or forecasts of future financial

performance (including estimates of potential cost savings and synergies) prepared by or reviewed or discussed with the managements of your

company and/or other potential transaction participants or obtained from public sources, we have assumed that such estimates and forecasts

have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such managements (or, with respect to

estimates and forecasts obtained from public sources, represent reasonable estimates). The Firm has no obligation (express or implied) to update

any or all of the Information or to advise you of any changes; nor do we make any express or implied warranties or representations as to the

completeness or accuracy or accept responsibility for errors.

Nothing contained herein should be construed as tax, accounting or legal advice. You (and each of your employees, representatives or other

agents) may disclose to any and all persons, without limitation of any kind, the tax treatment and tax structure of the transactions contemplated

by these materials and all materials of any kind (including opinions or other tax analyses) that are provided to you relating to such tax treatment

and structure. For this purpose, the tax treatment of a transaction is the purported or claimed U.S. federal income tax treatment of the

transaction and the tax structure of a transaction is any fact that may be relevant to understanding the purported or claimed U.S. federal income

tax treatment of the transaction.

agents) may disclose to any and all persons, without limitation of any kind, the tax treatment and tax structure of the transactions contemplated

by these materials and all materials of any kind (including opinions or other tax analyses) that are provided to you relating to such tax treatment

and structure. For this purpose, the tax treatment of a transaction is the purported or claimed U.S. federal income tax treatment of the

transaction and the tax structure of a transaction is any fact that may be relevant to understanding the purported or claimed U.S. federal income

tax treatment of the transaction.

LEGAL NOTICE