Exhibit (c)(5) *

Privileged and Confidential / Not to be Copied or Distributed

14 October 2010

PROJECT OSAKA - BOARD MATERIALS

Information presented may vary subject to legal advice

* Certain slides not materially related to the Rule 13e-3 transaction have been removed

5

Privileged and Confidential / Not to be Copied or Distributed

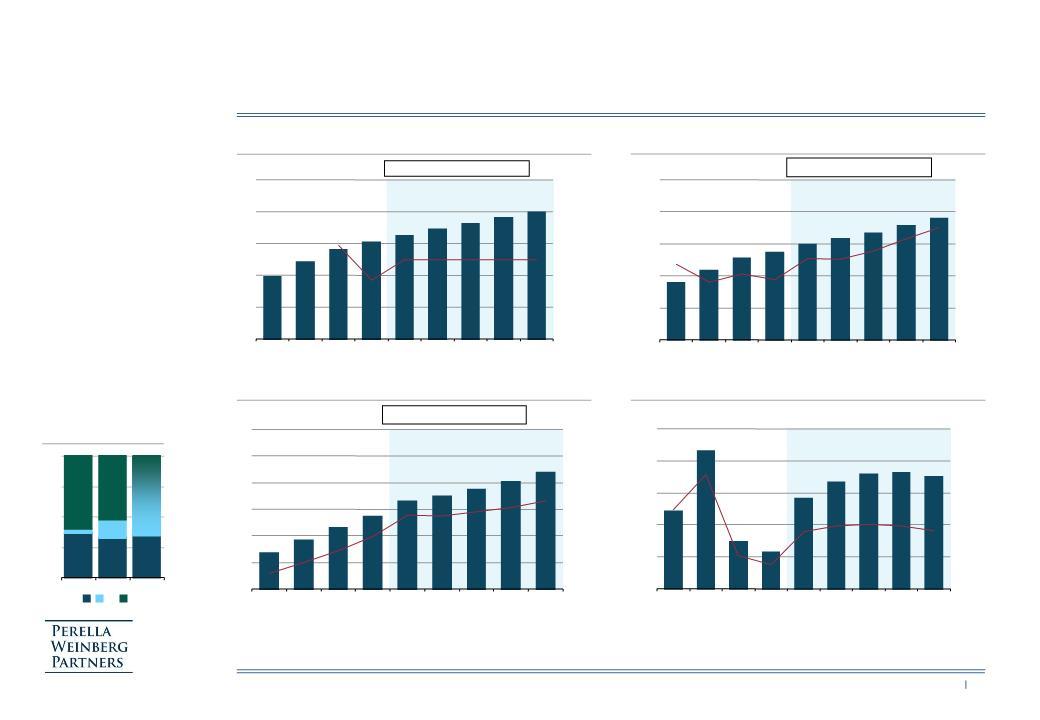

REVENUES

GROSS PROFIT

CAPITAL EXPENDITURE

EBITDA(2)

BASE CASE FINANCIALS (EXCL. SYNERGIES)

US$m

US$m

US$m

US$m

% Growth

% Revenues

% Revenues

% Revenues

Source: Shamrock filings, PWP analysis, FY 2009 financials pro forma adjusted for Australia and Thailand acquisitions

Note: (1) Organic revenue growth at constant FX rates; PwC analysis of organic revenue growth at constant FX rates for 2008 and 2009

(2) EBITDA on Non-GAAP basis but adjusted for stock option expenses (c. $0.5m per year)

– 5% organic growth consistent

with pro forma growth excl. FX

in 2008 (5.9%) and 2009

(3.7%), but at a discount to

growth observed in H1 2010

(8.5%) and to management

estimate for medium-term growth

(c. 9%)

with pro forma growth excl. FX

in 2008 (5.9%) and 2009

(3.7%), but at a discount to

growth observed in H1 2010

(8.5%) and to management

estimate for medium-term growth

(c. 9%)

– Margin developments in line

with management case

with management case

(1)

FX EXPOSURE 2010

CAGR 2010 - 2014: 5.2%

CAGR 2010 - 2014: 6.1%

CAGR 2010 - 2014: 7.3%

97

120

140

151

162

172

180

189

199

0

50

100

150

200

250

2006A

2007A

2008A

2009PF

2010E

2011E

2012E

2013E

2014E

0%

2%

4%

6%

8%

10%

53

65

76

81

89

94

100

106

113

0

30

60

90

120

150

2006A

2007A

2008A

2009PF

2010E

2011E

2012E

2013E

2014E

50%

52%

54%

56%

58%

60%

13.3

18.1

22.9

27.1

33.0

34.6

37.2

40.1

43.6

0

10

20

30

40

50

60

2006A

2007A

2008A

2009PF

2010E

2011E

2012E

2013E

2014E

12%

15%

18%

21%

24%

27%

30%

7.2

12.9

4.4

3.4

8.5

9.9

10.7

10.9

10.5

0

3

6

9

12

15

2006A

2007A

2008A

2009PF

2010B

2011E

2012E

2013E

2014E

0%

3%

6%

9%

12%

15%

37%

32%

34%

4%

16%

66%

60%

52%

0%

25%

50%

75%

100%

Sales

Opex

Capex

€

NIS

$/Other

6

Privileged and Confidential / Not to be Copied or Distributed

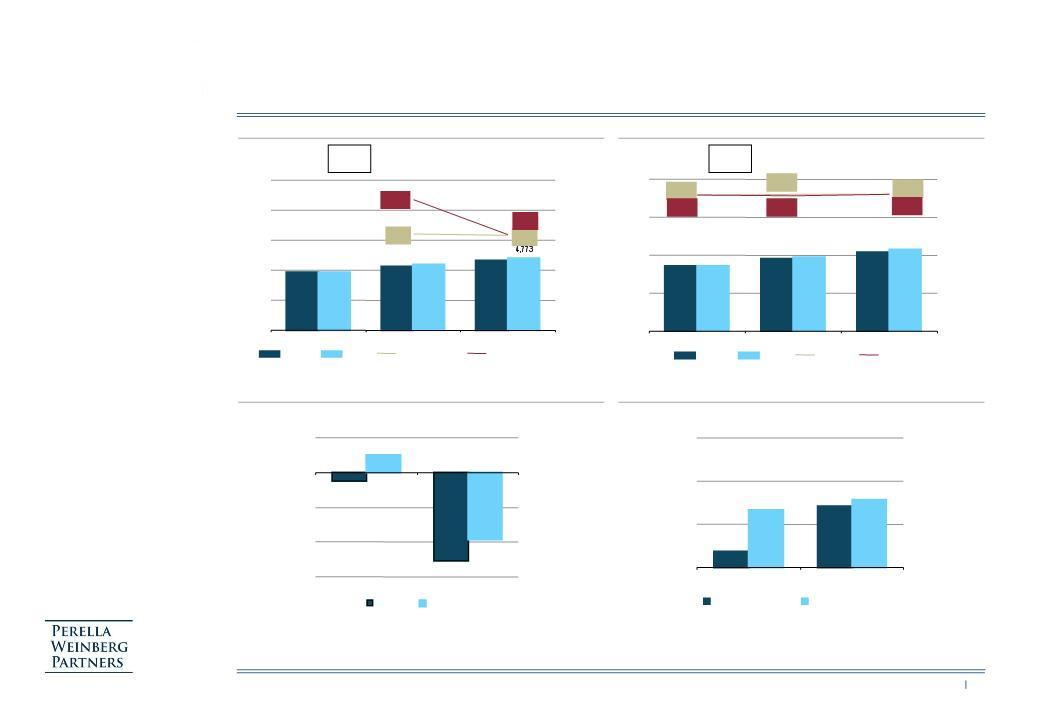

UPDATED VALUATION ANALYSIS (NET OF 2010 AGREED DIVIDEND)

Premium to current share price:

Sources: PWP analysis, Shamrock filings. All values net of agreed 2010 dividend of $0.8 per share.

Notes: (1) Enterprise value plus net cash ($16.8m), adjusted for 2010 dividend ($13.5m), less adjustments to net debt ($3.8m), less minorities ($10.5m; estimated by applying 11.0x EBIT multiple on 2010E

minority interest) plus associates ($1.3m) and less varying cost of buying out stock options (from $8.8m to $12.5m) . Based on 16.8m basic shares outstanding

minority interest) plus associates ($1.3m) and less varying cost of buying out stock options (from $8.8m to $12.5m) . Based on 16.8m basic shares outstanding

(2) Net of value attributed to the Definity® contract between Shamrock and Eric, representing $12.0m to $13.5m or $0.7 to $0.8 per share

(3) Base Case before adjustment for potential loss of Definity® contract; figures on Non-GAAP basis but adjusted for stock option expenses (c. $0.5m)

DCF range using

Eric WACC of 8.0%:

$18.3 - $21.2

Eric WACC of 8.0%:

$18.3 - $21.2

Dividend adjusted

current price: $10.09

current price: $10.09

Implied

(3)

(1),(2)

(2)

L3M

Trading Range

L3M trading (adjusted for 2010 dividend)

$7.10 - $10.11

129 - 179

2010E EV/EBITDA Comparable Multiples

8.0x - 9.0x

33.0

252 - 283

2010E EV/EBIT Multiples

11.0x - 12.0x

25.2

266 - 289

LFY EV/EBITDA transaction comparables

(LFY based on Dec-10 financials)

8.5x - 9.5x

33.0

268 - 300

LFY+1 EV/EBITDA transaction comparables

(LFY+1 based on Dec-11 financials)

8.0x - 9.0x

34.6

265 - 298

Discounted

Cash Flow

(2)

Based on 2011 - 2014 Base Case

Perpetuity growth methodology

1.5% - 2.5%

PGR

8.5% - 9.0%

WACC

272 - 334

Transaction

Valuation

(2)

Standalone

Market

Valuation

(2)

-50%

-25%

0%

25%

50%

75%

100%

125%

150%

15.7

14.7

14.9

14.0

7.1

19.3

16.5

16.6

16.0

15.7

10.1

14.7

Value Adjustment for Definity® Contract ($m)

Sales FY 2009

7.9

Assumed Gross Margin

22%

Estimated EBITDA impact

1.5

EBITDA Multiple Range

8.0x - 9.0x

Enterprise Value Range

12.0 - 13.5

Value Impact per Share ($)

0.7 - 0.8

7

Privileged and Confidential / Not to be Copied or Distributed

PRO FORMA SHAMROCK REVENUES

PRO FORMA SHAMROCK EBITDA(2)

PRELIMINARY ASSESSMENT OF POTENTIAL SYNERGIES

US$m

US$m

% Growth

% Revenues

Source: Shamrock filings, PWP analysis, FY 2009 financials pro forma adjusted for Australia and Thailand acquisitions

Note: (1) Organic revenue growth at constant FX rates; PwC analysis of organic revenue growth at constant FX rates for 2008 and 2009

(2) EBITDA on Non-GAAP basis but adjusted for stock option expenses (c. $0.5m per year)

(1)

CAGR 2010 - 2014: 8.5%

CAGR 2010 - 2014: 13.7%

Before synergies

Impact of synergies

Before synergies

Impact of synergies

Overview of Potential Synergies

Revenue Synergies

Cost Synergies

• Access to Eric distribution channels notably in the US

• Penetration of new markets (Asia, Central and Eastern

Europe)

Europe)

• Manufacturing subcontracting for Eric

• Increased sales through access to coating technology

(Crizal)

(Crizal)

• Reduction of raw materials costs (access to Eric’s

preferred terms)

preferred terms)

• Reduction in logistics costs

• Decrease in General & Administrative costs (delisting,

insurance)

insurance)

5

16

23

26

97

120

140

151

162

177

196

213

225

0

50

100

150

200

250

2006A

2007A

2008A

2009PF

2010E

2011E

2012E

2013E

2014E

0%

2%

4%

6%

8%

10%

4.3

9.5

10.9

11.4

13.3

18.1

22.9

27.1

33.0

38.9

46.7

51.1

55.0

0

10

20

30

40

50

60

2006A

2007A

2008A

2009PF

2010E

2011E

2012E

2013E

2014E

12%

15%

18%

21%

24%

27%

30%

8

Privileged and Confidential / Not to be Copied or Distributed

PRO FORMA IMPACT ON ERIC FINANCIAL PROFILE

Notes: (1) Shamrock financials converted to € at €/$1.35. Eric projections based on estimates from Jefferies 30-Aug10, UBS 27-Aug-10, Morgan Stanley 27-Aug-10 and Deutsche Bank 23-Aug10

(2) Contribution margin defined as operating profit before compensation costs of share-based payments, restructuring costs, other income and expense, and goodwill impairment. Corresponds to

Shamrock’s EBIT before stock option expense.

Shamrock’s EBIT before stock option expense.

(3) Based on an estimated net cash position for Shamrock of $12.8m at 31-Dec-10 plus payment of dividends for fiscal year 2011; Eric net debt projections excluding UBS forecasts

SALES EVOLUTION (1)

CONTRIBUTION MARGIN (1) (2)

€m

% Growth

€m

% Revenues

Standalone: 9.6%

Pro Forma: 11.3%

Pro Forma: 11.3%

Key Assumptions

– Assumed closing of

transaction 31-Dec-10

transaction 31-Dec-10

– Eric fully consolidates

Shamrock

Shamrock

– Purchase price financed

100% through debt

100% through debt

– Pre-tax interest rate on new

debt of 3%

debt of 3%

– Includes synergies net of

implementation costs

implementation costs

PPA

– Allocation to intangible

assets includes technology

($40.5m), brand ($15.8m)

and customer relationships

($7.2m)

assets includes technology

($40.5m), brand ($15.8m)

and customer relationships

($7.2m)

– Amortization periods:

technology 15 years, customer

relationships 12.5 years

technology 15 years, customer

relationships 12.5 years

– Revaluation of inventories of

$6.3m impacting 2011 gross

margin

$6.3m impacting 2011 gross

margin

– No amortization of brand

value and residual goodwill

value and residual goodwill

NET DEBT / (CASH)(3)

2011E - 2012E PRO FORMA EPS ACCRETION / DILUTION(1)

Transaction at $14.8 / share

CAGR

’10-‘12

’10-‘12

Standalone: 9.9%

Pro Forma: 11.5%

Pro Forma: 11.5%

CAGR

’10-‘12

’10-‘12

Transaction at $14.8 / share

3,855

4,628

3,855

4,226

4,357

9.5%

9.6%

9.5%

13.0%

0

2,000

4,000

6,000

8,000

10,000

2010

2011

2012

0%

3%

6%

9%

12%

15%

Standalone

Proforma

Standalone Growth

Proforma Growth

690

763

833

690

777

858

18.0%

18.0%

17.9%

18.0%

17.8%

17.9%

0

400

800

1,200

1,600

2010

2011

2012

0%

5%

10%

15%

20%

Standalone

Proforma

Standalone

Proforma

(25)

(254)

50

(194)

(300)

(200)

(100)

0

100

2011

2012

Standalone

Pro Forma

0.4%

1.4%

1.3%

1.6%

0%

1%

2%

3%

2011

2012

Incl. Amort. of Intangibles

Excl. Amort. of Intangibles

9

Privileged and Confidential / Not to be Copied or Distributed

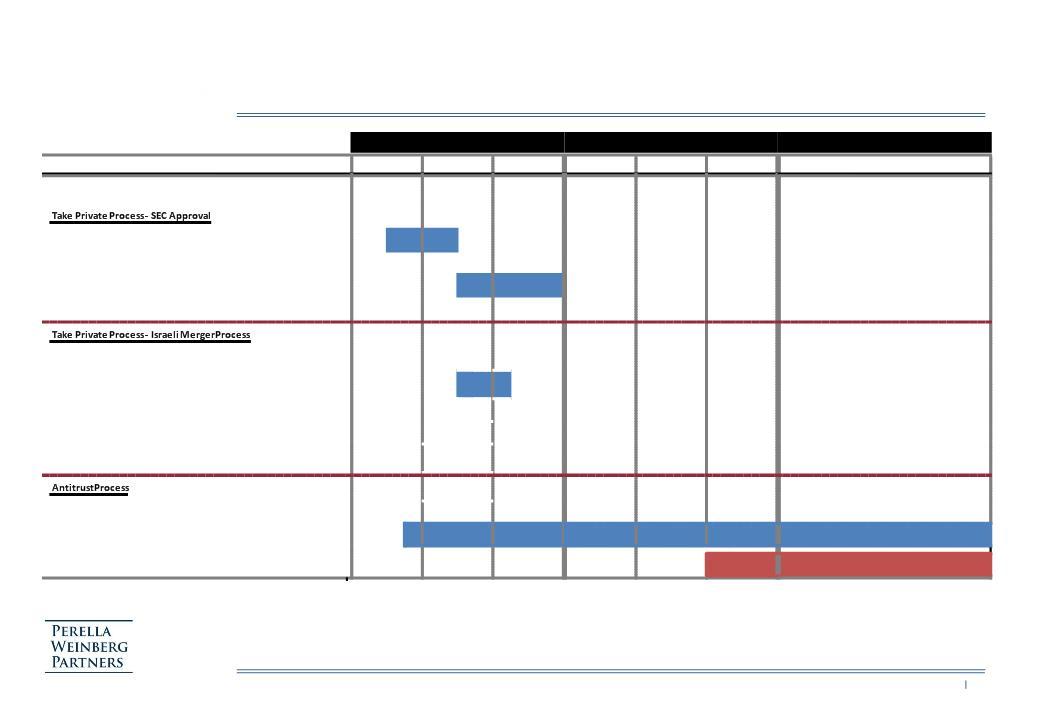

INDICATIVE TIMETABLE - KEY MILESTONES TO CLOSING

Q4 2010

Q1 2011

Q2 2011 - Q4 2011

Month

Oct

Nov

Dec

Jan

Feb

Mar

Transaction Announcement

(Subject to Shareholder Approval &

Antitrust Clearance)

Preparation of Proxy Statement

File Proxy Statement with SEC

SEC Review Period/ Incorporation of SEC Comments

SEC Approval of Proxy

u

Apply for Court Approval to Convene Shareholder Meeting

Court Reviews Merger Proposal & Authorizes Convening of

Shareholder Meeting

u

Convene Shareholder Meeting (Post SEC Approval)

u

Shareholder Meeting

Court Approval of Shareholder Meeting Resolution and

Merger Transaction (Subject to Antitrust Clearance)

u

Filing with Relevant Regulatory Authorities

u

Regulatory Review Process

Closing (Subject to Antitrust Clearance)

u

u

u

u

Privileged and Confidential / Not to be Copied or Distributed

APPENDIX

11

Privileged and Confidential / Not to be Copied or Distributed

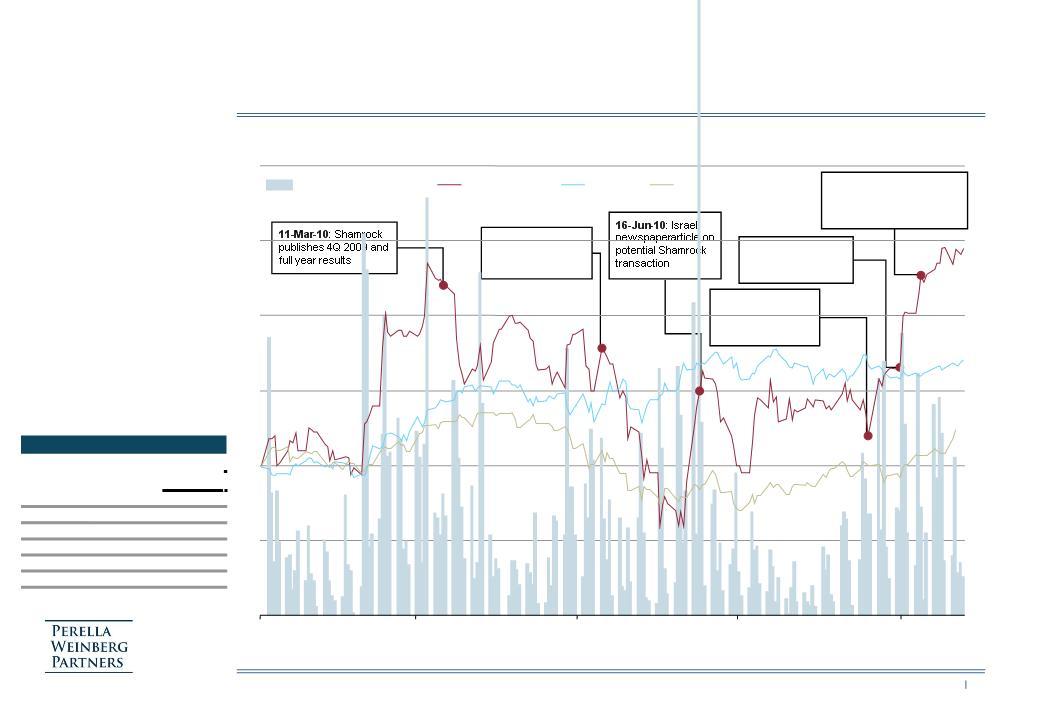

SHAMROCK YTD SHARE PRICE DEVELOPMENT

Source: Factset

US$

‘000s

08-Sep-10: Broker note

from CM-CIC on potential

Shamrock transaction

from CM-CIC on potential

Shamrock transaction

19-Aug-10:

Shamrock publishes

strong 1H 2010

results

Shamrock publishes

strong 1H 2010

results

10-May-10:

Shamrock publishes

1Q 2010 results

Shamrock publishes

1Q 2010 results

Rumours in the market have recently

supported the share price (up 26%

over the last 90 days)

supported the share price (up 26%

over the last 90 days)

31-Aug-10: Assumed

unaffected price

($9.33)

unaffected price

($9.33)

6

7

8

9

10

11

12

Jan-10

Mar-10

May-10

Jul-10

Sep-10

0

20

40

60

80

100

120

Shamrock Volume (RHS)

Shamrock (LHS)

Eric (LHS)

Tel Aviv 100 (LHS)

Shamrock Trading Statistics

Share

Performance

Last Week

(0.2%)

30 Days

18.4%

90 Days

26.0%

180 Days

19.1%

1 Year

59.0%

3 Years

(5.6%)