| Citigroup Funding Inc. | November 29, 2012 Medium-Term Notes, Series D Pricing Supplement No. 2012—MTNDG0314 Filed Pursuant to Rule 424(b)(2) Registration Statement Nos. 333-172554 and 333-172554-01 |

528,000 Dual Directional Trigger PLUS Based on the Common Stock of Apple Inc. Due December 1, 2014

Trigger Performance Leveraged Upside SecuritiesSM

Overview

| · | The securities offered by this pricing supplement are unsecured senior debt securities issued by Citigroup Funding Inc. and guaranteed by Citigroup Inc. Unlike conventional debt securities, the securities do not pay interest and do not repay a fixed amount of principal at maturity. Instead, the securities offer a payment at maturity that may be greater than, equal to or less than the stated principal amount, depending on the performance of the shares of common stock of Apple Inc. (the “shares”) from their initial share price to their final share price. |

| · | The securities offer the potential for a positive return at maturity based on the absolute value, within a limited range, of the percentage change in the price of the shares from their initial share price to their final share price. If the shares appreciate, the securities provide leveraged positive exposure to a limited range of that appreciation, and if the shares depreciate, the securities provide unleveraged positive exposure to a limited range of that depreciation. In exchange for the upside leverage and the potential for a positive return at maturity even if the shares depreciate, investors in the securities must be willing to forgo (i) positive participation in the appreciation or depreciation of the shares outside of the limited range offered by the securities and (ii) any dividends that may be paid on the shares. Investors in the securities must also be willing to accept full downside exposure to the shares if they depreciate by more than 25%. If the final share price is less than the trigger price, you will lose 1% of the stated principal amount of your securities for every 1% by which the final share price is less than the initial share price. There is no minimum payment at maturity. |

| · | In order to obtain the modified exposure to the shares that the securities provide, investors must be willing to accept (i) an investment that may have limited or no liquidity and (ii) the risk of not receiving any amount due under the securities if we and Citigroup Inc. default on our obligations. |

| Shares: | Shares of common stock of Apple Inc. (the “underlying share issuer”) | ||

| Aggregate principal amount: | $5,280,000 | ||

| Stated principal amount: | $10 per security | ||

| Pricing date: | November 29, 2012 | ||

| Issue date: | December 4, 2012 | ||

| Valuation date: | November 25, 2014, subject to postponement if such date is not a scheduled trading day or if certain market disruption events occur | ||

| Maturity date: | December 1, 2014 | ||

| Payment at maturity: | For each $10 security you hold at maturity: ▪ If the final share price is greater than or equal to the initial share price: $10 + the leveraged upside payment, subject to the maximum return at maturity ▪ If the final share price is less than the initial share price but greater than or equal to the trigger price: $10 + ($10 × the absolute share return) ▪ If the final share price is less than the trigger price: $10 × the share performance factor If the final share price is less than the trigger price, your payment at maturity will be less, and possibly significantly less, than $7.50 per security. You should not invest in the securities unless you are willing and able to bear the risk of losing a significant portion and up to all of your investment. | ||

| Initial share price: | 589.36, the closing price of the shares on the pricing date | ||

| Final share price: | The closing price of the shares on the valuation date | ||

| Leveraged upside payment: | $10 × absolute share return × leverage factor | ||

| Absolute share return: | The absolute value of the share percent change | ||

| Share percent change: | (final share price – initial share price) / initial share price | ||

| Leverage factor: | 200% | ||

| Maximum return at maturity: | 34.25%, applicable when the final share price is greater than the initial share price. Because the trigger price is 75% of the initial share price, any positive return on the securities resulting from the depreciation of the shares will not exceed 25%. | ||

| Share performance factor: | final share price / initial share price | ||

| Trigger price: | 442.02, 75% of the initial share price | ||

| Listing: | The securities will not be listed on any securities exchange. | ||

| CUSIP / ISIN: | 17318Q392 / US17318Q3920 | ||

| Underwriter: | Citigroup Global Markets Inc., an affiliate of the issuer, acting as principal | ||

| Underwriting fee and issue price: | Price to public | Underwriting fee(1) | Proceeds to issuer |

| Per security: | $10.000 | $0.225 | $9.775 |

| Total: | $5,280,000 | $118,800 | $5,161,200 |

(1) For more information on the distribution of the securities, see “Supplemental Plan of Distribution” in this pricing supplement. In addition to the underwriting fee, Citigroup Global Markets Inc. and its affiliates may profit from expected hedging activity related to this offering, even if the value of the securities declines. See “Use of Proceeds and Hedging” in the accompanying prospectus.

Investing in the securities involves risks not associated with an investment in conventional debt securities. See “Summary Risk Factors” beginning on page PS-4.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the securities or determined that this pricing supplement and the accompanying product supplement, prospectus supplement and prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

You should read this pricing supplement together with the accompanying product supplement, prospectus supplement and prospectus, each of which can be accessed via the hyperlinks below.

Product Supplement No. EA-02-01 dated May 21, 2012 Prospectus Supplement and Prospectus dated May 12, 2011

The securities are not bank deposits and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank.

Citigroup Funding Inc.

528,000 Dual Directional Trigger PLUS Based on the Common Stock of Apple Inc. Due December 1, 2014

General. The terms of the securities are set forth in the accompanying product supplement, prospectus supplement and prospectus, as supplemented by this pricing supplement. The accompanying product supplement, prospectus supplement and prospectus contain important disclosures that are not repeated in this pricing supplement. For example, certain events may occur that could affect your payment at maturity or, in the case of a delisting of the shares, could give us the right to call the securities prior to maturity for an amount that may be less than the stated principal amount. These events, including market disruption events and other events affecting the shares, and their consequences are described in the accompanying product supplement in the sections “Description of the Securities—Certain Additional Terms for Securities Linked to ETF Shares or Company Shares—Consequences of a Market Disruption Event; Postponement of a Valuation Date,” “—Dilution and Reorganization Adjustments” and “—Delisting of Company Shares” and not in this pricing supplement. It is important that you read the accompanying product supplement, prospectus supplement and prospectus together with this pricing supplement in connection with your investment in the securities. Certain terms used but not defined in this pricing supplement are defined in the accompanying product supplement.

The initial share price and the trigger price are each a “Relevant Price” for purposes of the section “Description of the Securities—Certain Additional Terms for Securities Linked to ETF Shares or Company Shares—Dilution and Reorganization Adjustments” in the accompanying product supplement. Accordingly, the initial share price and the trigger price are each subject to adjustment upon the occurrence of any of the events described in that section.

Potential Future Events. It is possible that Citigroup Funding Inc. will merge into Citigroup Inc. in the near future. If a merger occurs, Citigroup Inc. will assume all the obligations of Citigroup Funding Inc. under the securities, as required by the indenture under which the securities are issued.

Hypothetical Examples

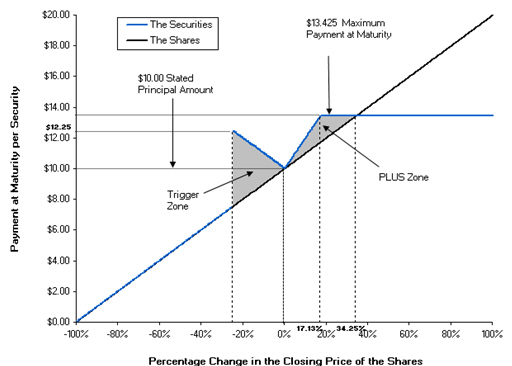

The diagram below illustrates your payment at maturity for a range of hypothetical percentage changes from the initial share price to the final share price.

Investors in the securities will not receive any dividends on the shares. The diagram and examples below do not show any effect of lost dividend yield over the term of the securities. See “Summary Risk Factors—You will not have voting rights, rights to receive dividends or other distributions or any other rights with respect to the shares” below.

| Dual Directional Trigger PLUS Payment at Maturity Diagram |

|

| November 2012 | PS-2 |

Citigroup Funding Inc.

528,000 Dual Directional Trigger PLUS Based on the Common Stock of Apple Inc. Due December 1, 2014

Your actual payment at maturity per security will depend on the actual final share price. The examples below are intended to illustrate how your payment at maturity will depend on whether the final share price is greater than or less than the initial share price and by how much.

Example 1—Upside Scenario A. The hypothetical final share price is $618.83 (a 5% increase from the initial share price), which is greater than the initial share price.

| Payment at maturity per security | = | $10 + the leveraged upside payment, subject to the maximum return at maturity of 34.25% |

| = | $10 + ($10 × absolute share return × leverage factor), subject to the maximum return at maturity of 34.25% | |

| = | $10 + ($10 × 5% × 200%) = $11.00, subject to the maximum return at maturity of 34.25% | |

| = | $11.00 |

Because the shares appreciated from their initial share price to their hypothetical final share price and the leveraged upside payment of $1.00 per security results in a total return at maturity of 10%, which is less than the maximum return at maturity of 34.25%, your payment at maturity in this scenario would be equal to $11.00 per security.

Example 2—Upside Scenario B. The hypothetical final share price is $884.04 (a 50% increase from the initial share price), which is greater than the initial share price.

| Payment at maturity per security | = | $10 + the leveraged upside payment, subject to the maximum return at maturity of 34.25% |

| = | $10 + ($10 × absolute share return × leverage factor), subject to the maximum return at maturity of 34.25% | |

| = | $10 + ($10 × 50% × 200%) = $20.00, subject to the maximum return at maturity of 34.25% | |

| = | $13.425 |

Because the shares appreciated from their initial share price to their hypothetical final share price and the leveraged upside payment of $10.00 per security would result in a total return at maturity of 100%, which is greater than the maximum return at maturity of 34.25%, your payment at maturity in this scenario would be equal to the maximum payment at maturity of $13.425 per security. In this scenario, an investment in the securities would underperform a hypothetical alternative investment providing 1-to-1 exposure to the appreciation of the shares without a maximum return.

Example 3—Upside Scenario C. The hypothetical final share price is $559.89 (a 5% decrease from the initial share price), which is less than the initial share price but greater than the trigger price.

| Payment at maturity per security | = | $10 + ($10 × the absolute share return) |

| = | $10 + ($10 × | −5% |) | |

| = | $10 + $0.50 = $10.50 |

Because the hypothetical final share price decreased from the initial share price by less than 25%, your payment at maturity in this scenario would reflect 1-to-1 positive exposure to the negative performance of the shares.

Example 4—Downside Scenario A. The hypothetical final share price is $412.55 (a 30% decrease from the initial share price), which is less than the trigger price.

| Payment at maturity per security | = | $10 × the share performance factor |

| = | $10 × 0.70 = $7.00 |

Because the hypothetical final share price decreased from the initial share price by more than 25%, your payment at maturity in this scenario would reflect 1-to-1 downside exposure to the negative performance of the shares.

| November 2012 | PS-3 |

Citigroup Funding Inc.

528,000 Dual Directional Trigger PLUS Based on the Common Stock of Apple Inc. Due December 1, 2014

Example 5—Downside Scenario B. The hypothetical final share price is $0.00 (a 100% decrease from the initial share price), which is less than the trigger price.

| Payment at maturity per security | = | $10 × the share performance factor |

| = | $10 × 0.00 = $0.00 |

Because the hypothetical final share price decreased from the initial share price by more than 25% and the shares are worth nothing on the valuation date, in this scenario, you would lose your entire investment in the securities.

Summary Risk Factors

An investment in the securities is significantly riskier than an investment in conventional debt securities. The securities are subject to all of the risks associated with an investment in our conventional debt securities, including the risk that we may default on our obligations under the securities, and are also subject to risks associated with the shares. Accordingly, the securities are suitable only for investors who are capable of understanding the complexities and risks of the securities. You should consult your own financial, tax and legal advisers as to the risks of an investment in the securities and the suitability of the securities in light of your particular circumstances.

The following is a summary of certain key risk factors for investors in the securities. You should read this summary together with the more detailed description of risks relating to an investment in the securities contained in the section “Risk Factors Relating to the Securities” beginning on page EA-6 in the accompanying product supplement. You should also carefully read the risk factors included in the documents incorporated by reference in the accompanying prospectus, including Citigroup Inc.’s most recent Annual Report on Form 10-K and any subsequent Quarterly Reports on Form 10-Q, which describe risks relating to the business of Citigroup Inc. more generally.

| ■ | You may lose some or all of your investment. Unlike conventional debt securities, the securities do not repay a fixed amount of principal at maturity. Instead, your payment at maturity will depend on the performance of the shares. If the final share price is less than the trigger price, you will lose 1% of the stated principal amount of the securities for every 1% by which the final share price is less than the initial share price. There is no minimum payment at maturity on the securities, and you may lose up to all of your investment. |

| ■ | The securities do not pay interest. Unlike conventional debt securities, the securities do not pay interest or any other amounts prior to maturity. You should not invest in the securities if you seek current income during the term of the securities. |

| ■ | Your potential return on the securities is limited. Your potential total return on the securities at maturity is limited by the maximum return at maturity of 34.25%, which is equivalent to a maximum payment at maturity of $13.425 per security. Because the leverage factor provides 200% exposure to any positive performance of the shares, any increase in the final share price over the initial share price by more than 17.125% will not increase your return on the securities. Moreover, the return potential of the securities in the event that the final share price is less than the initial share price is limited to 25%. Any decline in the final share price from the initial share price by more than 25% will result in a loss, rather than a positive return, on the securities. |

| ■ | The securities are subject to the credit risk of Citigroup Inc. If we default on our obligations and Citigroup Inc. defaults on its guarantee obligations under the securities, you may not receive any payments that become due under the securities. |

| ■ | The securities will not be listed on a securities exchange and you may not be able to sell them prior to maturity. The securities will not be listed on any securities exchange. Therefore, there may be little or no secondary market for the securities. |

Citigroup Global Markets Inc. intends to make a secondary market in relation to the securities and to provide an indicative bid price on a daily basis. Any indicative bid prices provided by Citigroup Global Markets Inc. shall be determined in Citigroup Global Markets Inc.’s sole discretion, taking into account prevailing market conditions, and shall not be a representation by Citigroup Global Markets Inc. that any instrument can be purchased or sold at such prices (or at all).

Notwithstanding the above, Citigroup Global Markets Inc. may suspend or terminate making a market and providing indicative bid prices without notice, at any time and for any reason. Consequently, there may be no market for the securities and investors should not assume that such a market will exist. Accordingly, an investor must be prepared to hold the securities until the maturity date. Where a market does exist, to the extent that an investor wants to sell the securities, the price may, or may not, be at a discount from the stated principal amount.

| ■ | The inclusion of underwriting fees and projected profit from hedging in the issue price is likely to adversely affect secondary market prices. Assuming no change in market conditions or other relevant factors, the price, if any, at which Citigroup Global Markets Inc. may be willing to purchase the securities in secondary market transactions will likely be lower than the issue price because the issue price includes, and secondary market prices are likely to exclude, underwriting fees and the cost of hedging our obligations under the securities. The cost of hedging includes the projected profit that our affiliates may realize in consideration for assuming the risks inherent in managing the hedging transactions. Any secondary market price is also likely to be reduced by the costs of unwinding the related hedging transactions. Any secondary market prices may differ from values determined by pricing models used by Citigroup Global Markets Inc. as a result of dealer discounts, mark-ups or other transaction costs. |

| November 2012 | PS-4 |

Citigroup Funding Inc.

528,000 Dual Directional Trigger PLUS Based on the Common Stock of Apple Inc. Due December 1, 2014

| ■ | Your payment at maturity depends on the closing price of the shares on a single day. Because your payment at maturity depends on the closing price of the shares solely on the valuation date, you are subject to the risk that the closing price on that day may be lower, and possibly significantly lower, than on one or more other dates during the term of the securities. If you had invested directly in the shares or in another instrument linked to the shares that you could sell for full value at a time selected by you, or if the payment at maturity were based on an average of closing prices of the shares, you might have achieved better returns. |

| ■ | The value of the securities prior to maturity will fluctuate based on many unpredictable factors. The value of your securities prior to maturity will fluctuate based on the price and volatility of the shares and a number of other factors, including the dividend yield on the shares, interest rates generally, the time remaining to maturity and our creditworthiness. Historically, the price of the shares has been extremely volatile. From January 3, 2007 to November 29, 2012, the price of the shares has been as low as $78.20 and as high as $702.10. You should understand that the value of your securities at any time prior to maturity may be significantly less than the stated principal amount. |

| ■ | You will not have voting rights, rights to receive dividends or other distributions or any other rights with respect to the shares. As of November 29, 2012, the 12-month trailing dividend yield of the shares was 1.80%. While it is impossible to know the future dividend yield of the shares, if this dividend yield were to remain constant for the term of the securities, you would be forgoing an aggregate yield of approximately 3.60% (assuming no reinvestment of dividends) by investing in the securities instead of investing directly in the shares or in another investment linked to the shares that provides for a pass-through of dividends. The payment scenarios described in this pricing supplement do not show any effect of lost dividend yield over the term of the securities. |

| ■ | Our offering of the securities is not a recommendation of the shares. The fact that we are offering the securities does not mean that we believe that investing in an instrument linked to the shares is likely to achieve favorable returns. In fact, as we are part of a global financial institution, our affiliates may have positions (including short positions) in the shares or in instruments related to the shares, and may publish research or express opinions, that in each case are inconsistent with an investment linked to the shares. These and other activities of our affiliates may affect the price of the shares in a way that may have a negative impact on your interests as a holder of the securities. |

| ■ | The price of the shares may be adversely affected by our or our affiliates’ hedging and other trading activities. We have hedged our obligations under the securities through affiliated or unaffiliated counterparties, who may take positions directly in the shares or in instruments related to the shares. Our affiliates also trade the shares and other financial instruments related to the shares on a regular basis (taking long or short positions or both), for their accounts, for other accounts under their management or to facilitate transactions on behalf of customers. These activities could affect the price of the shares in a way that negatively affects the value of the securities. They could also result in substantial returns for us or our affiliates while the value of the securities declines. |

| ■ | We may have economic interests that are adverse to yours as a result of our affiliates’ business activities. Our affiliates may currently or from time to time engage in business with the underlying share issuer, including extending loans to, making equity investments in or providing advisory services to the underlying share issuer. In the course of this business, our affiliates may acquire non-public information about the underlying share issuer, which we will not disclose to you. Moreover, if any of our affiliates becomes a creditor of the underlying share issuer, they may exercise any remedies against the underlying share issuer that are available to them without regard to your interests. |

| ■ | An adjustment will not be made for all events that may have a dilutive effect on or otherwise adversely affect the price of the shares. For example, we will not make any adjustment for ordinary dividends, partial tender offers or additional public offerings of the shares. Moreover, the adjustments we do make may not fully offset the dilutive or adverse effect of the particular event. Investors in the securities may be adversely affected by such an event in a circumstance in which a direct holder of the shares would not. |

| ■ | If the shares are delisted, we may call the securities prior to maturity for an amount that may be less than the stated principal amount. If we exercise this call right, you will receive the amount described under "Description of the Securities—Certain Additional Terms for Securities Linked to ETF Shares or Company Shares—Delisting of Company Shares" in the accompanying product supplement. This amount may be less, and possibly significantly less, than the stated principal amount of the securities. |

| ■ | The securities may become linked to shares of an issuer other than the original underlying share issuer upon the occurrence of a reorganization event or upon the delisting of the shares. For example, if the underlying share issuer enters into a merger agreement that provides for holders of its common stock to receive stock of another entity, the stock of such other entity will become the common stock represented by the shares for all purposes of the securities upon consummation of the merger. Additionally, if the shares are delisted and we do not exercise our call right, the calculation agent may, in its sole discretion, select shares representing the common stock of another issuer to be successor shares. See "Description of the Securities—Certain Additional Terms for Securities Linked to ETF Shares or Company Shares—Delisting of Company Shares" in the accompanying product supplement. |

| ■ | The calculation agent, which is an affiliate of ours, will make important determinations with respect to the securities. If certain events occur, such as market disruption events, corporate events with respect to the underlying share issuer that may require a dilution adjustment or the delisting of the shares, Citigroup Global Markets Inc., as calculation agent, will be required to |

| November 2012 | PS-5 |

Citigroup Funding Inc.

528,000 Dual Directional Trigger PLUS Based on the Common Stock of Apple Inc. Due December 1, 2014

| make certain judgments that could significantly affect your payment at maturity. In making these judgments, the calculation agent’s interests as an affiliate of ours could be adverse to your interests as a holder of the securities. |

| ■ | The U.S. federal tax consequences of an investment in the securities are unclear. There is no direct legal authority regarding the proper U.S. federal tax treatment of the securities, and we do not plan to request a ruling from the Internal Revenue Service (the “IRS”). Consequently, significant aspects of the tax treatment of the securities are uncertain, and the IRS or a court might not agree with the treatment of the securities as prepaid forward contracts. If the IRS were successful in asserting an alternative treatment of the securities, the tax consequences of the ownership and disposition of the securities might be materially and adversely affected. As described below under “United States Federal Tax Considerations,” in 2007, the U.S. Treasury Department and the IRS released a notice requesting comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments. Any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the securities, including the character and timing of income or loss and the degree, if any, to which income realized by non-U.S. persons should be subject to withholding tax, possibly with retroactive effect. You should read carefully the discussion under "United States Federal Tax Considerations" and “Risk Factors Relating to the Securities” in the accompanying product supplement and “United States Federal Tax Considerations” in this pricing supplement. You should consult your tax adviser regarding the U.S. federal tax consequences of an investment in the securities, as well as tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction. |

| November 2012 | PS-6 |

Citigroup Funding Inc.

528,000 Dual Directional Trigger PLUS Based on the Common Stock of Apple Inc. Due December 1, 2014

Apple Inc. (the “underlying share issuer”) is a provider of personal computers and mobile communication and media devices. The shares are registered under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Information provided to or filed with the SEC by the underlying share issuer pursuant to the Exchange Act can be located by reference to the SEC file number 000-10030, through the SEC’s Web site at http://www.sec.gov. In addition, information regarding the underlying share issuer may be obtained from other sources including, but not limited to, press releases, newspaper articles and other publicly disseminated documents.

This pricing supplement relates only to the securities offered hereby and does not relate to the shares or other securities of the underlying share issuer. We have derived all disclosures contained in this pricing supplement regarding the shares and the underlying share issuer from the publicly available documents described in the preceding paragraph. In connection with the offering of the securities, none of Citigroup Funding Inc., Citigroup Inc. or Citigroup Global Markets Inc. has participated in the preparation of such documents or made any due diligence inquiry with respect to the underlying share issuer.

The securities represent obligations of Citigroup Funding Inc. only. The underlying share issuer is not involved in any way in this offering and has no obligation relating to the securities or to holders of the securities.

Neither we nor any of our affiliates make any representation to you as to the performance of the shares.

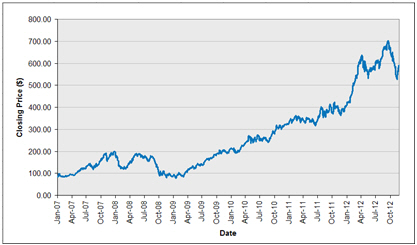

Historical Information

The graph below shows the closing price of the shares for each day such price was available from January 3, 2007 to November 29, 2012. The table that follows shows the high, low and end-of-period closing prices of the shares for each quarter in that same period. We obtained the closing prices and other information below from Bloomberg L.P., without independent verification. You should not take the historical prices of the shares as an indication of future performance.

Apple Inc. Historical Closing Prices January 3, 2007 to November 29, 2012 |

|

| November 2012 | PS-7 |

Citigroup Funding Inc.

528,000 Dual Directional Trigger PLUS Based on the Common Stock of Apple Inc. Due December 1, 2014

| Apple Inc. | High ($) | Low ($) | Period End ($) |

| 2007 | |||

| First Quarter | 97.13 | 83.27 | 92.91 |

| Second Quarter | 125.09 | 90.24 | 122.04 |

| Third Quarter | 154.50 | 117.05 | 153.54 |

| Fourth Quarter | 199.83 | 153.76 | 198.08 |

| 2008 | |||

| First Quarter | 194.97 | 119.15 | 143.50 |

| Second Quarter | 189.96 | 147.14 | 167.44 |

| Third Quarter | 179.69 | 105.26 | 113.66 |

| Fourth Quarter | 111.04 | 80.49 | 85.35 |

| 2009 | |||

| First Quarter | 109.87 | 78.20 | 105.12 |

| Second Quarter | 144.67 | 108.69 | 142.43 |

| Third Quarter | 186.15 | 135.40 | 185.37 |

| Fourth Quarter | 211.64 | 180.76 | 210.86 |

| 2010 | |||

| First Quarter | 235.83 | 192.00 | 234.93 |

| Second Quarter | 274.16 | 235.86 | 251.53 |

| Third Quarter | 292.46 | 240.16 | 283.75 |

| Fourth Quarter | 325.47 | 278.64 | 322.56 |

| 2011 | |||

| First Quarter | 363.13 | 326.72 | 348.45 |

| Second Quarter | 353.10 | 315.32 | 335.67 |

| Third Quarter | 413.45 | 343.23 | 381.18 |

| Fourth Quarter | 422.24 | 363.50 | 405.00 |

| 2012 | |||

| First Quarter | 617.62 | 411.23 | 599.47 |

| Second Quarter | 636.23 | 530.12 | 584.00 |

| Third Quarter | 702.10 | 574.88 | 667.26 |

| Fourth Quarter (through November 29, 2012) | 671.74 | 526.05 | 589.36 |

The closing price of the shares on November 29, 2012 was $589.36. We make no representation as to the amount of dividends that may be paid on the shares in the future. In any event, as an investor in the securities, you will not be entitled to receive dividends that may be payable on the shares.

United States Federal Tax Considerations

You should read carefully the discussion under "United States Federal Tax Considerations" and “Risk Factors Relating to the Securities” in the accompanying product supplement and “Summary Risk Factors” in this pricing supplement.

In the opinion of our counsel, Davis Polk & Wardwell LLP, which is based on current market conditions, a security should be treated as a prepaid forward contract for U.S. federal income tax purposes. By purchasing the securities, you agree (in the absence of an administrative determination or judicial ruling to the contrary) to this treatment. There is uncertainty regarding this treatment, and the IRS or a court might not agree with it.

Assuming this treatment of the securities is respected and subject to the discussion in “United States Federal Tax Considerations” in the accompanying product supplement, the following U.S. federal income tax consequences should result under current law:

| · | You should not recognize taxable income over the term of the securities prior to maturity, other than pursuant to a sale or exchange. |

| · | Upon a sale or exchange of the securities, or retirement of the securities at maturity, you should recognize capital gain or loss equal to the difference between the amount realized and your tax basis in the securities. Such gain or loss should be long-term capital gain or loss if you held the securities for more than one year. |

Under current law, if you are a Non-U.S. Holder (as defined in the accompanying product supplement) of the securities, subject to the possible application of Section 871(m) of the Internal Revenue Code (as discussed in "United States Federal Tax Considerations" in the accompanying product supplement), you generally should not be subject to U.S. federal withholding or income tax in respect of amounts paid to you with respect to the securities provided that (i) income in respect of the securities is not effectively connected with your conduct of a trade or business in the United States, and (ii) you comply with the applicable certification requirements.

| November 2012 | PS-8 |

Citigroup Funding Inc.

528,000 Dual Directional Trigger PLUS Based on the Common Stock of Apple Inc. Due December 1, 2014

In 2007, the U.S. Treasury Department and the IRS released a notice requesting comments on the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments. The notice focuses in particular on whether to require holders of these instruments to accrue income over the term of their investment. It also asks for comments on a number of related topics, including the character of income or loss with respect to these instruments; whether short-term instruments should be subject to any such accrual regime; the relevance of factors such as the exchange-traded status of the instruments and the nature of the underlying property to which the instruments are linked; the degree, if any, to which income (including any mandated accruals) realized by non-U.S. investors should be subject to withholding tax; and whether these instruments are or should be subject to the “constructive ownership” regime, which very generally can operate to recharacterize certain long-term capital gain as ordinary income and impose an interest charge. While the notice requests comments on appropriate transition rules and effective dates, any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the securities, including the character and timing of income or loss and the degree, if any, to which income realized by non-U.S. persons should be subject to withholding tax, possibly with retroactive effect.

You should read the section entitled "United States Federal Tax Considerations" in the accompanying product supplement. The preceding discussion, when read in combination with that section, constitutes the full opinion of Davis Polk & Wardwell LLP regarding the material U.S. federal tax consequences of owning and disposing of the securities.

You should consult your tax adviser regarding all aspects of the U.S. federal income and estate tax consequences of an investment in the securities and any tax consequences arising under the laws of any state, local or foreign taxing jurisdiction.

Supplemental Plan of Distribution

Citigroup Global Markets Inc., an affiliate of Citigroup Funding Inc. and the underwriter of the sale of the securities, is acting as principal and will receive an underwriting fee of $0.225 for each security sold in this offering. From this underwriting fee, Citigroup Global Markets Inc. will pay selected dealers, including its affiliate Morgan Stanley Smith Barney LLC, and their financial advisors collectively a fixed selling concession of $0.225 for each security they sell.

Citigroup Global Markets Inc. is an affiliate of ours. Accordingly, this offering will conform with the requirements addressing conflicts of interest when distributing the securities of an affiliate set forth in Rule 5121 of the Financial Industry Regulatory Authority. Client accounts over which Citigroup Inc. or its subsidiaries have investment discretion will not be permitted to purchase the securities, either directly or indirectly, without the prior written consent of the client.

See “Plan of Distribution; Conflicts of Interest” in each of the accompanying product supplement, prospectus supplement and prospectus for additional information.

A portion of the net proceeds from the sale of the securities will be used to hedge our obligations under the securities. We may hedge our obligations under the securities through an affiliate of Citigroup Global Markets Inc. and us or through unaffiliated counterparties, and our counterparties may profit from such expected hedging activity even if the value of the securities declines. This hedging activity could affect the closing price of the shares and, therefore, the value of and your return on the securities. For additional information on the ways in which we may hedge our obligations under the securities, see “Use of Proceeds and Hedging” in the accompanying prospectus.

Contact

Clients of Morgan Stanley Wealth Management may contact their local Morgan Stanley branch office or the Morgan Stanley principal executive offices at 1585 Broadway, New York, New York 10036 (telephone number (914) 225-2700). All other clients may contact their local brokerage representative.

Validity of the Securities

In the opinion of Davis Polk & Wardwell LLP, as special products counsel to Citigroup Funding Inc., when the securities offered by this pricing supplement have been executed and issued by Citigroup Funding Inc. and authenticated by the trustee pursuant to the indenture, and delivered against payment therefor, such securities and the related guarantee of Citigroup Inc. will be valid and binding obligations of Citigroup Funding Inc. and Citigroup Inc. respectively, enforceable in accordance with their respective terms, subject to applicable bankruptcy, insolvency and similar laws affecting creditors’ rights generally, concepts of reasonableness and equitable principles of general applicability (including, without limitation, concepts of good faith, fair dealing and the lack of bad faith), provided that such counsel expresses no opinion as to the effect of fraudulent conveyance, fraudulent transfer or similar provision of applicable law on the conclusions expressed above. This opinion is given as of the date of this pricing supplement and is limited to the laws of the State of New York, except that such counsel expresses no opinion as to the application of state securities or Blue Sky laws to the securities.

In giving this opinion, Davis Polk & Wardwell LLP has assumed the legal conclusions expressed in the opinion set forth below of Martha D. Bailey, Associate General Counsel—Capital Markets and Corporate Reporting of Citigroup Inc. and counsel to Citigroup Funding Inc. In addition, this opinion is subject to the assumptions set forth in the letter of Davis Polk & Wardwell LLP dated April 26, 2012,

| November 2012 | PS-9 |

Citigroup Funding Inc.

528,000 Dual Directional Trigger PLUS Based on the Common Stock of Apple Inc. Due December 1, 2014

which has been filed as an exhibit to a Current Report on Form 8-K filed by Citigroup Inc. on April 26, 2012, that the indenture has been duly authorized, executed and delivered by, and is a valid, binding and enforceable agreement of the trustee and that none of the terms of the securities nor the issuance and delivery of the securities and the related guarantee, nor the compliance by Citigroup Funding Inc. and Citigroup Inc. with the terms of the securities and the related guarantee respectively, will result in a violation of any provision of any instrument or agreement then binding upon Citigroup Funding Inc. and Citigroup Inc., as applicable, or any restriction imposed by any court or governmental body having jurisdiction over Citigroup Funding Inc. and Citigroup Inc., as applicable.

In the opinion of Martha D. Bailey, Associate General Counsel—Capital Markets and Corporate Reporting of Citigroup Inc. and counsel to Citigroup Funding Inc., (i) the Board of Directors (or a duly authorized committee thereof) of Citigroup Funding Inc. has duly established the terms of the securities offered by this pricing supplement and duly authorized the issuance and sale of such securities and such authorization has not been modified or rescinded; (ii) each of Citigroup Funding Inc. and Citigroup Inc. is validly existing and in good standing under the laws of the State of Delaware; (iii) the indenture dated as of June 1, 2005, among Citigroup Funding Inc., as issuer, Citigroup Inc., as guarantor, and The Bank of New York Mellon, as successor trustee to JPMorgan Chase Bank, N.A., has been duly authorized, executed, and delivered by Citigroup Funding Inc. and Citigroup Inc.; and (iv) the execution and delivery of such indenture by Citigroup Funding Inc. and Citigroup Inc. and of the securities offered by this pricing supplement by Citigroup Funding Inc., and the performance by each such party of its obligations thereunder, are within its corporate powers and do not contravene its certificate of incorporation or bylaws or other constitutive documents. This opinion is given as of the date of this pricing supplement and is limited to the General Corporation Law of the State of Delaware.

Martha D. Bailey, or other internal attorneys with whom she has consulted, has examined and is familiar with originals, or copies certified or otherwise identified to her satisfaction, of such corporate records of Citigroup Funding Inc. and Citigroup Inc., certificates or documents as she has deemed appropriate as a basis for the opinions expressed above. In such examination, she or such persons has assumed the legal capacity of all natural persons, the genuineness of all signatures (other than those of officers of Citigroup Funding Inc. or Citigroup Inc.), the authenticity of all documents submitted to her or such persons as originals, the conformity to original documents of all documents submitted to her or such persons as certified or photostatic copies and the authenticity of the originals of such copies.

PLUSSM is a service mark of Morgan Stanley. Used under license.

© 2012 Citigroup Global Markets Inc. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

| November 2012 | PS-10 |