| | | | | | | | | | | | | | | |

Nicholas-Applegate International & Premium Strategy Fund Financial Highlights |

| | Six Months

ended

August 31, 2009

(unaudited) | | Year ended | | For the period

April 29, 2005*

through

February 28, 2006 |

| | | |

| | | February 28,

2009 | | February 29,

2008 | | February 28,

2007 | |

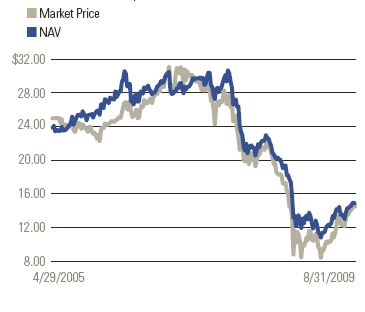

Net asset value, beginning of period | | $11.23 | | | $21.75 | | | $28.52 | | | $27.35 | | | $23.88 | ** |

| | | | | | | | | | | | | | | |

Investment Operations: | | | | | | | | | | | | | | | |

Net investment income | | 0.24 | | | 0.48 | | | 0.49 | | | 0.33 | | | 0.16 | |

Net realized and change in unrealized gain (loss) on investments, call options written and foreign currency transactions | | 4.29 | | | (8.93 | ) | | (1.48 | ) | | 4.77 | | | 4.81 | |

Total from investment operations | | 4.53 | | | (8.45 | ) | | (0.99 | ) | | 5.10 | | | 4.97 | |

| | | | | | | | | | | | | | | |

Dividends and Distributions to Shareholders from: | | | | | | | | | | | | | | | |

Net investment income | | (0.30 | ) | | (0.46 | ) | | (0.48 | ) | | (1.11 | ) | | (0.12 | ) |

Net realized gains | | (0.62 | ) | | (1.61 | ) | | (5.29 | ) | | (2.82 | ) | | (1.33 | ) |

Return of capital | | — | | | — | | | (0.01 | ) | | — | | | — | |

Total dividends and distributions to common shareholders | | (0.92 | ) | | (2.07 | ) | | (5.78 | ) | | (3.93 | ) | | (1.45 | ) |

| | | | | | | | | | | | | | | |

Capital Share Transactions: | | | | | | | | | | | | | | | |

Offering costs charged to paid-in capital in excess of par | | — | | | — | | | — | | | — | | | (0.05 | ) |

Net asset value, end of period | | $14.84 | | | $11.23 | | | $21.75 | | | $28.52 | | | $27.35 | |

Market price, end of period | | $14.50 | | | $9.48 | | | $20.81 | | | $30.45 | | | $24.64 | |

Total Investment Return (1) | | 65.94 | % | | (48.14 | )% | | (14.25 | )% | | 42.23 | % | | 4.66 | % |

| | | | | | | | | | | | | | | |

RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | |

Net assets end of period (000) | | $145,112 | | | $109,823 | | | $212,627 | | | $277,930 | | | $262,668 | |

Ratio of expenses to average net assets (2) | | 1.31 | %(3) | | 1.32 | % | | 1.25 | % | | 1.22 | % | | 1.19 | %(3) |

Ratio of net investment income to average net assets | | 3.68 | %(3) | | 2.70 | % | | 1.78 | % | | 1.12 | % | | 0.79 | %(3) |

Portfolio turnover | | 12 | % | | 152 | % | | 179 | % | | 203 | % | | 192 | % |

|

Nicholas-Applegate International & Premium Strategy Fund |

Matters Relating to the Trustees’ Consideration of the Investment |

Management and Portfolio Management Agreements (unaudited) |

The Investment Company Act of 1940 requires that both the full Board of Trustees (the “Trustees”) and a majority of the non-interested Trustees (the “Independent Trustees”), voting separately, approve the Fund’s Management Agreement (the “Advisory Agreement”) with the Investment Manager and Portfolio Management Agreement (the “Sub-Advisory Agreement”, and together with the Advisory Agreement, the “Agreements”) between the Investment Manager and the Sub-Adviser. The Trustees met in person on June 16-17, 2009 (the “contract review meeting”) for the specific purpose of considering whether to approve the continuation of the Advisory Agreement and the Sub-Advisory Agreement. The Independent Trustees were assisted in their evaluation of the Agreements by independent legal counsel, from whom they received separate legal advice and with whom they met separately from Fund management during the contract review meeting.

Based on their evaluation of factors that they deemed to be material, including those factors described below, the Board of Trustees, including a majority of the Independent Trustees, concluded that the continuation of the Fund’s Advisory Agreement and the Sub-Advisory Agreement, as amended, should be approved for a one-year period commencing July 1, 2009.

In connection with their deliberations regarding the continuation of the Agreements, the Trustees, including the Independent Trustees, considered such information and factors as they believed, in light of the legal advice furnished to them and their own business judgment, to be relevant. As described below, the Trustees considered the nature, quality, and extent of the various investment management, administrative and other services performed by the Investment Manager or the Sub-Adviser under the applicable Agreement.

In connection with their contract review meeting, the Trustees received and relied upon materials provided by the Investment Manager which included, among other items: (i) information provided by Lipper Inc. (“Lipper”) on the total return investment performance (based on net assets) of the Fund for various time periods and the investment performance of a group of funds with substantially similar investment classifications/objectives as the Fund identified by Lipper and the performance of applicable benchmark indices, (ii) information provided by Lipper on the Fund’s management fees and other expenses and the management fees and other expenses of comparable funds identified by Lipper, (iii) information regarding the investment performance and management fees of comparable portfolios of other clients of the Sub-Advisers, including institutional separate accounts and other clients, (iv) the profitability to the Investment Manager and the Sub-Adviser from their relationship with the Fund for the one year period ended March 31, 2009, (v) descriptions of various functions performed by the Investment Manager and the Sub-Adviser for the Fund, such as portfolio management, compliance monitoring and portfolio trading practices, and (vi) information regarding the overall organization of the Investment Manager and the Sub-Adviser, including information regarding senior management, portfolio managers and other personnel providing investment management, administrative and other services to the Fund.

The Trustees’ conclusions as to the continuation of the Agreements were based on a comprehensive consideration of all information provided to the Trustees and not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations are described below, although individual Trustees may have evaluated the information presented differently from one another, giving different weights to various factors.

As part of their review, the Trustees examined the Investment Manager’s and the Sub-Adviser’s abilities to provide high quality investment management and other services to the Fund. The Trustees considered the investment philosophy and research and decision-making processes of the Sub-Adviser; the experience of key advisory personnel of the Sub-Adviser responsible for portfolio management of the Fund; the ability of the Investment Manager and the Sub-Adviser to attract and retain capable personnel; the capability and integrity of the senior management and staff of the Investment Manager and the Sub-Adviser; and the level of skill required to manage the Funds. In addition, the Trustees reviewed the quality of the Investment Manager’s and the Sub-Adviser’s services with respect to regulatory compliance and compliance with the investment policies of the Fund; the nature and quality of certain administrative services the Investment Manager is responsible for providing to the Fund; and conditions that might affect the Investment Manager’s or the Sub-Adviser’s ability to provide high quality services to the Funds in the future under the Agreements, including each organization’s respective business reputation, financial condition and operational stability. Based on the foregoing, the Trustees concluded that the Sub-Adviser’s investment process, research capabilities and philosophy were well suited to the Fund given its respective investment objectives and policies, and that the Investment Manager and the Sub-Adviser would be able to continue to meet any reasonably foreseeable obligations under the Agreements.

22 Nicholas-Applegate International & Premium Strategy Fund Semi-Annual Report | 8.31.09 |

|

Nicholas-Applegate International & Premium Strategy Fund |

Matters Relating to the Trustees’ Consideration of the Investment |

Management and Portfolio Management Agreements (unaudited) (continued) |

Based on information provided by Lipper, the Trustees also reviewed each Fund’s total return investment performance as well as the performance of comparable funds identified by Lipper. In the course of their deliberations, the Trustees took into account information provided by the Investment Manager in connection with the contract review meeting, as well as during investment review meetings conducted with portfolio management personnel during the course of the year regarding the Fund’s performance.

In assessing the reasonableness of the Fund’s fees under the Agreements, the Trustees considered, among other information, the Fund’s management fee and the total expense ratio as a percentage of average net assets attributable to common shares and the management fee and total expense ratios of comparable funds identified by Lipper.

For the Fund, the Trustees specifically took note of how the Fund compared to its Lipper peers as to performance, management fee expenses and total expenses. The Trustees noted that the Investment Manager had provided a memorandum containing comparative information on the performance and expenses information of the Fund compared to its Lipper peer categories. The Trustees noted that while the Fund is not charged a separate administration fee, it was not clear whether the peer funds in the Lipper categories were charged such a fee by their investment managers.

The Trustees noted that the expense group for the Fund is small, consisting of six funds. The Trustees also noted that the actual management fees and total actual expenses were both above the median. The Trustees also noted that the Fund had bottom quintile performance for the 1-and 3-year periods, ranking twenty-seventh out of thirty-two peer funds for the 1-year period and twentieth out of twenty-second for the 3-year period. As of May 31, 2009, the Fund moved into the top quintile for the 3-months and year-to-date periods and moved into the fourth quintile for the 1- and 3-year periods.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding the Agreements, that they were satisfied with the Investment Manager’s and the Sub-Adviser’s responses and efforts to continue to improve the Fund’s investment performance. The Trustees agreed to reassess the services provided by the Investment Manager and Sub-Adviser under the Agreements in light of the Fund’s ongoing performance at each quarterly Board meeting.

The Trustees also considered the management fees charged by the Sub-Adviser to other clients, including institutional separate accounts with investment strategies similar to those of the Fund. Regarding the institutional separate accounts, they noted that the management fees paid by the Fund are generally higher than the fees paid by these clients of the Sub-Adviser, but the Trustees were advised by the Sub-Adviser that the administrative burden for the Investment Manager and the Sub-Adviser with respect to the Fund is also relatively higher, due in part to the more extensive regulatory regime to which the Fund is subject in comparison to institutional separate accounts. The Trustees noted that the management fees paid by the Fund is generally higher than the fees paid by the open-end funds offered for comparison but were advised that there are additional portfolio management challenges in managing the Fund, such as meeting a regular dividend.

Based on a profitability analysis provided by the Investment Manager, the Trustees also considered the profitability of the Investment Manager and the Sub-Adviser from their relationship with the Fund and determined that such profitability was not excessive.

The Trustees also took into account that, as closed-end investment companies, the Fund does not currently intend to raise additional assets, so the assets of the Fund will grow (if at all) only through the investment performance of the Fund. Therefore, the Trustees did not consider potential economies of scale as a principal factor in assessing the fee rates payable under the Agreements.

Additionally, the Trustees considered so-called “fall-out benefits” to the Investment Manager and the Sub-Adviser, such as reputational value derived from serving as Investment Manager and Sub-Adviser to the Fund.

After reviewing these and other factors described herein, the Trustees concluded with respect to the Fund, within the context of their overall conclusions regarding the Agreements, that the fees payable under the Agreements represent reasonable compensation in light of the nature and quality of the services being provided by the Investment Manager and Sub-Adviser to the Fund.

| 8.31.09 | Nicholas-Applegate International & Premium Strategy Fund Semi-Annual Report 23

|

Nicholas-Applegate International & Premium Strategy Fund |

Annual Shareholder Meeting Results/Proxy Voting Policies & Procedures |

(unaudited) |

Annual Shareholder Meeting Results:

The Fund held its annual meeting of shareholders on July 14, 2009. Shareholders voted as indicated below:

| | | | | | | |

| | Affirmative | | Withheld

Authority | |

Re-election of Paul Belica – Class I to serve until 2012 | | | 8,447,412 | | | 358,583 | |

Re-election of Hans W. Kertess – Class I to serve until 2012 | | | 8,444,890 | | | 361,105 | |

Re-election of William B. Ogden, IV – Class I to serve until 2012 | | | 8,438,335 | | | 367,660 | |

Messrs. Robert E. Connor, John C. Maney* and R. Peter Sullivan continue to serve as Trustees of the Fund.

Diana L. Taylor resigned as Trustee of the Fund on September 10, 2009.

| |

* | John C. Maney is an Interested Trustee of the Fund. |

| |

Proxy Voting Policies & Procedures:

A description of the policies and procedures that the Fund has adopted to determine how to vote proxies relating to portfolio securities and information about how the Fund voted proxies relating to portfolio securities held during the most recent twelve month period ended June 30 is available (i) without charge, upon request, by calling the Fund’s shareholder servicing agent at (800) 254-5197; (ii) on the Fund’s website at www.allianzinvestors.com/closedendfunds;and (iii) on the Securities and Exchange Commission website at www.sec.gov

24 Nicholas-Applegate International & Premium Strategy Fund Semi-Annual Report | 8.31.09 |

| |

Trustees | Fund Officers |

Hans W. Kertess | Brian S. Shlissel |

Chairman of the Board of Trustees | President & Chief Executive Officer |

Paul Belica | Lawrence G. Altadonna |

Robert E. Connor | Treasurer, Principal Financial & Accounting Officer |

John C. Maney | Thomas J. Fuccillo |

William B. Ogden, IV | Vice President, Secretary & Chief Legal Officer |

R. Peter Sullivan III | Scott Whisten |

| Assistant Treasurer |

| Richard J. Cochran |

| Assistant Treasurer |

| Youse E. Guia |

| Chief Compliance Officer |

| Kathleen A. Chapman |

| Assistant Secretary |

| Lagan Srivastava |

| Assistant Secretary |

Investment Manager | |

Allianz Global Investors Fund Management LLC | |

1345 Avenue of the Americas | |

New York, NY 10105 | |

| |

Sub-Adviser | |

Nicholas-Applegate Capital Management LLC | |

600 West Broadway, 30th Floor | |

San Diego, CA 92101 | |

| |

Custodian & Accounting Agent | |

State Street Bank & Trust Co. | |

225 Franklin Street | |

Boston, MA 02110 | |

| |

Transfer Agent, Dividend Paying Agent and Registrar | |

PNC Global Investment Servicing | |

P.O. Box 43027 | |

Providence, RI 02940-3027 | |

| |

Independent Registered Public Accounting Firm | |

PricewaterhouseCoopers LLP | |

300 Madison Avenue | |

New York, NY 10017 | |

| |

Legal Counsel | |

Ropes & Gray LLP | |

One International Place | |

Boston, MA 02110-2624 | |

This report, including the financial information herein, is transmitted to the shareholders of Nicholas-Applegate International & Premium Strategy Fund for their information. It is not a prospectus, circular or representation intended for use in the purchase of shares of the Fund or any securities mentioned in this report.

The financial information included herein is taken from the records of the Fund without examination by an independent registered public accounting firm, who did not express an opinion.

Notice is hereby given in accordance with Section 23(c) of the Investment Company Act of 1940, as amended, that from time to time the Fund may purchase shares of its stock in the open market.

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of its fiscal year on Form N-Q. The Fund’s Form N-Q is available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. The information on Form N-Q is also available on the Fund’s website at www.allianzinvestors.com/closedendfunds.

On July 22, 2009, the Fund submitted CEO annual certification to the New York Stock Exchange (“NYSE”) on which the Fund’s principal executive officer certified that he was not aware, as of the date, of any violation by the Fund of the NYSE’s Corporate Governance listing standards. In addition, as required by Section 302 of the Sarbanes-Oxley Act of 2002 and related SEC rules, the Fund’s principal executive and principal financial officer made quarterly certifications, included in filings with the SEC on Forms N-CSR and N-Q relating to, among other things, the Fund’s disclosure controls and procedures and internal control over financial reporting, as applicable.

Information on the Fund is available at www.allianzinvestors.com/closedendfunds or by calling the Fund’s shareholder servicing agent at (800) 254-5197.

Receive this report electronically and eliminate paper mailings.

To enroll, go to www.allianzinvestors.com/edelivery.

ITEM 2. CODE OF ETHICS

Not required in this filing.

ITEM 3. AUDIT COMMITTEE FINANCIAL EXPERT

Not required in this filing.

ITEM 4. PRINCIPAL ACCOUNTANT FEES AND SERVICES

Not required in this filing.

ITEM 5. AUDIT COMMITTEE OF LISTED REGISTRANT

Not required in this filing.

ITEM 6. SCHEDULE OF INVESTMENTS

Schedule of Investments is included as part of the Report to Shareholders filed under Item 1 of this form.

ITEM 7. DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES

Not required in this filing.

ITEM 8. PORTFOLIO MANAGERS OF CLOSED-END MANAGEMENT INVESTMENT COMPANIES

Not required in this filing.

ITEM 9. PURCHASES OF EQUITY SECURITIES BY CLOSED-END MANAGEMENT INVESTMENT COMPANY AND AFFILIATED COMPANIES.

None.

ITEM 10. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

There have been no material changes to the procedures by which shareholders may recommend nominees to the Fund’s Board of Trustees since the Fund last provided disclosure in response to this item.

ITEM 11. CONTROLS AND PROCEDURES

(a) The registrant’s President & Chief Executive Officer and Treasurer, Principal Financial & Accounting Officer have concluded that the registrant’s disclosure controls and procedures (as defined in Rule 30a-2(c) under the Act (17 CFR 270.30a-3(c))), as amended are effective based on their evaluation of these controls and procedures as of a date within 90 days of the filing date of this document.

(b) There were no significant changes over financial reporting (as defined in rule 30a-3(d) under the Act (17 CFR 270.30a -3(d))) that occurred during the registrant’s second fiscal quarter of the period covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting.

ITEM 12. EXHIBITS

| (a) (1) | Exhibit 99.302 CERT – Certification pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 |

| |

| (b) | Exhibit 99.906 Cert. – Certification pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 |

| |

Signature

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

(Registrant) Nicholas-Applegate International & Premium Strategy Fund

By: /s/ Brian S. Shlissel

Brian S. Shlissel

President and Chief Executive Officer

Date: October 29, 2009

By: /s/ Lawrence G. Altadonna

Lawrence G. Altadonna

Treasurer, Principal Financial & Accounting Officer

Date: October 29, 2009

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

By: /s/ Brian S. Shlissel

Brian S. Shlissel

President and Chief Executive Officer

Date: October 29, 2009

By: /s/ Lawrence G. Altadonna

Lawrence G. Altadonna

Treasurer, Principal Financial & Accounting Officer

Date: October 29, 2009