UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number:

811-21732

Mercer Funds

(Exact Name of Registrant as Specified in Charter)

99 High Street

Boston, MA 02110

(Address of Principal Executive Offices) (Zip Code)

Scott M. Zoltowski, Esq.

Mercer Investment Management, Inc.

99 High Street

Boston, MA 02110

(Name and Address of Agent for Service)

Registrant’s Telephone Number, including Area Code:

(617) 747-9500

Date of Fiscal Year End: March 31, 2013

Date of Reporting Period: March 31, 2013

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

Mercer Funds™

Annual Report

Mercer US Large Cap Growth Equity Fund

Mercer US Large Cap Value Equity Fund

Mercer US Small/Mid Cap Growth Equity Fund

Mercer US Small/Mid Cap Value Equity Fund

Mercer Non-US Core Equity Fund

Mercer Core Opportunistic Fixed Income Fund

Mercer Emerging Markets Equity Fund

Mercer Global Low Volatility Equity Fund

Mercer US Short Maturity Fixed Income Fund

This report has been prepared for Mercer Funds shareholders. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current Mercer Funds prospectus. The prospectus contains more complete information about the Funds’ investment objectives, risks, and expenses. Investors are reminded to read the prospectus carefully before investing.

March 31, 2013

MERCER FUNDS

TABLE OF CONTENTS

| Page | ||

| 1 | ||

| 27 | ||

| 160 | ||

| 164 | ||

| 167 | ||

| 172 | ||

| 181 | ||

| 215 | ||

| 216 | ||

| 222 | ||

| 225 | ||

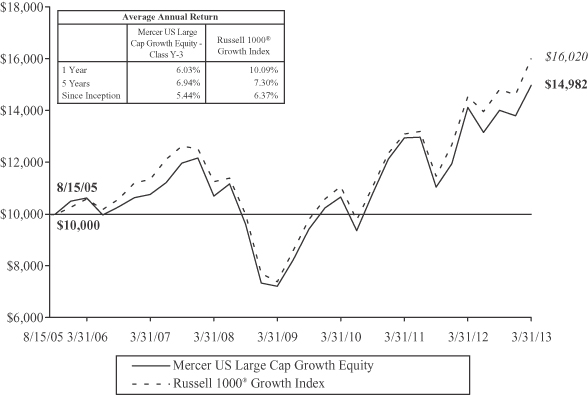

Mercer US Large Cap Growth Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is long-term total return, which includes capital appreciation and income. The benchmark for the Fund is the Russell 1000® Growth Index.

Investment Strategy

The Fund invests principally in equity securities issued by large capitalization U.S. companies. The companies will generally have higher earnings and/or revenue growth histories or expectations relative to the Russell 1000® Growth Index.

Performance

For the fiscal year ended March 31, 2013, the Fund’s Y-3 share class performance was 6.03% compared to its benchmark return of 10.09%. Performance for the Fund is reported net of operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisors

As of March 31, 2013, the Fund employed four sub-advisors, Atlanta Capital Management Company, LLC (Atlanta), Neuberger Berman Management LLC( Neuberger Berman), Sands Capital Management, LLC (Sands) and Winslow Capital Management, LLC (Winslow). Atlanta manages its allocated portion of the Fund using high quality securities as a key part of their selection criteria. The firm seeks companies that have a demonstrated history of consistent growth (typically greater than 8%) and earnings stability. Neuberger Berman uses a fundamental process to identify companies with accelerating earnings while seeking to avoid those companies with decelerating earnings. Sands manages a concentrated portfolio using a fundamental, bottom-up approach to identify leading companies in various industries. Winslow manages a portfolio of securities across a range of market capitalizations, earnings growth, market valuations and industry sectors.

Market Commentary and Fund Performance

For the Fund’s fiscal year, the market, as measured by the S&P 500 Index, rose 14.0% continuing the rise which started in March 2009. The now four-year bull market has brought returns of 114% for the four-year period ending March 2013. For the prior fiscal year, it was split into distinct periods as economic news impacted investor’s views regarding which type of investments were most attractive. The fiscal year began with negative returns in the first fiscal quarter as the market digested a European debt crisis and the resulting global slowdown. Investors favored defensive type of equities and the perceived lower risk of U.S. treasuries. The fiscal year was marked by reassurance from the world’s central banks that they would do whatever was necessary to improve global economic growth, including an unprecedented conditional commitment from the U.S. Federal Reserve to maintain low interest rates until unemployment falls below 6.5% or the inflation rate exceeds 2.5%. These commitments coupled with an improving U.S. economic outlook initiated the latter half of the fiscal year in the equity markets. While economic news was mixed over the fiscal year, there was continued and modest growth in nonfarm payrolls, a falling unemployment rate and an improved housing outlook. Growth expectations notched higher and this helped advance the U.S. equity market. Increased expectations were tempered by concerns over the ability of the two major political parties to settle issues regarding the federal budget — issues that must bridge deep philosophical differences. For the full fiscal year, large cap growth stocks, as measured by the Russell 1000® Growth Index provided the weakest returns among major indices rising 10.1%, while the Russell 1000® Value Index gained 18.8%. In addition defensive type stocks outperformed on the year and this is evident in sector performance as telecom, health care and consumer staples sectors outperformed. The Federal Reserve’s decision to keep interest rates lower for the foreseeable future has made riskier assets more attractive and despite some downturns during the period in reaction to poor economic news, the US equity markets have been trending upward.

Within the Russell 1000® Growth Index, the best performing sectors for the fiscal year were health care, telecommunications services, and energy, posting gains of 26.0%, 21.6%, and 20.2% respectively. Nine of ten sectors generated positive returns, with information technology the only sector posting a negative result for the year.

The Mercer Large Cap Growth Equity Fund underperformed the Russell 1000® Growth Index during this fiscal year. This was a difficult market environment for growth portfolios generally; defensive type stocks outperformed the broad market. On a sector attribution basis, the primary driver of the Fund’s underperformance was stock selection in the consumer

1

Mercer US Large Cap Growth Equity Fund

discretionary sector. Notable detractors in the sector included Netflix, Coach and priceline.com, which all posted declines for the Fund. At March 31, 2013 the Fund no longer held Netflix. The timing of the Fund’s purchase and sale of its Netflix holding was an additional source of underperformance for the Fund. A significant underweight to media companies in the consumer discretionary sector (0.9% vs. 3.7%) hampered relative results for the fiscal year and cost the Fund 55 basis points in return. Good stock selection in the information technology and materials sectors was not enough to offset underperformance in other sectors of the portfolio.

The Winslow portion of the Fund underperformed the Russell 1000® Growth Index for the fiscal year. Stock selection in the consumer discretionary and financials sectors were areas of weakness. Winslow was able to add value over the benchmark in the materials and health care sectors. The Sands portion of the Fund underperformed the Index, hurt by stock selection in the consumer discretionary sector and a zero weight in the consumer staples sector. Good stock selection in the information technology sector was a positive contributor to Sand’s performance. Atlanta underperformed the benchmark and was hurt by information technology holding Acme Packet and a lack of exposure to the holding Visa, a strongly performing and large index weight holding. At March 31, 2013 the Fund no longer held Acme. Good stock selection in the materials and health care sectors was a positive contributor. Neuberger Berman underperformed the benchmark for the fiscal year. Overall, this more defensively positioned sub-advisor added value in sector weighting decisions, but was hurt by stock selection in the consumer sectors.

Risk Considerations

The Fund invests in growth stocks which may be particularly sensitive to market conditions. The Fund may experience high portfolio turnover which may result in higher costs and capital gains. The Fund’s volatility may be amplified by its ability to select sub-advisors to allocate assets.

2

Mercer Funds

March 31, 2013

Comparison of Change in Value of a $10,000 Investment in

Mercer US Large Cap Growth Equity Shares vs. the

Russell 1000® Growth Index

As of March 31, 2013

This graph shows the performance of the Mercer US Large Cap Growth Equity Fund1 Class Y-3 shares versus the Russell 1000® Growth Index from August 15, 2005, which is the inception date of the Fund, through March 31, 2013. The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-866-658-9896 for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

3

Mercer US Large Cap Value Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, which includes capital appreciation and income. The benchmark for the Fund is the Russell 1000® Value Index.

Investment Strategy

The Fund invests principally in equity securities issued by large capitalization U.S. companies that are considered undervalued based on the stocks’ intrinsic values relative to their current market prices.

Performance

For the fiscal year ended March 31, 2013, the Fund’s Y-3 share class performance was 16.71% compared to its benchmark return of 18.77%. Performance for the Fund is reported net of operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisors

As of March 31, 2013, the Fund employed four sub-advisors, Brandywine Global Investment Management, LLC (Brandywine), The Boston Company Asset Management, LLC (TBCAM), Robeco Investment Management, Inc. (Robeco), and O’Shaughnessy Asset Management, LLC (O’Shaughnessy). Brandywine seeks to build portfolios comprised of companies whose valuations are below the market but whose earnings growth prospects are equal or better than the market. The firm favors industry leaders with strong competitive positions and reasonable growth expectations given the team’s view of industry and overall economic conditions. TBCAM’s investment process is driven by bottom-up, fundamental security selection and uses a combination of traditional valuation measures and the identification of improving business momentum in their stock selection. Robeco’s process begins with a quantitative analysis that provides a statistical ranking of the investment universe based on valuation, momentum, and fundamental factors. The firm then applies fundamental analysis to those securities that includes validation of the quantitative analysis and fundamental research, including an in-depth review of the issuer’s financials. O’Shaughnessy uses quantitative models in seeking to find the most attractive companies on a shareholder yield basis. This is a combination of dividend yield and share buybacks.

Market Commentary and Fund Performance

For the Fund’s fiscal year, the market, as measured by the S&P 500 Index rose 14.0% continuing the rise which started in March 2009. The now four-year bull market has brought returns of 114% for the four-year period ending March 2013. For the prior fiscal year, it was split into distinct periods as economic news impacted investor’s views regarding which type of investments were most attractive. The fiscal year began with negative returns in the first fiscal quarter as the market digested a European debt crisis and the resulting global slowdown. Investors favored defensive type of equities and the perceived lower risk of U.S. treasuries. The fiscal year was marked by reassurance from the world’s central banks that they would do whatever was necessary to improve global economic growth, including an unprecedented conditional commitment from the U.S. Federal Reserve to maintain low interest rates until unemployment falls below 6.5% or the inflation rate exceeds 2.5%. These commitments coupled with an improving U.S. economic outlook initiated in the latter half of the fiscal year in the equity markets. While economic news was mixed over the fiscal year, there was continued and modest growth in nonfarm payrolls, a falling unemployment rate and an improved housing outlook. Growth expectations notched higher and this helped advance the U.S. equity market. Increased expectations were tempered by concerns over the ability of the two major political parties to settle issues regarding the federal budget — issues that must bridge deep philosophical differences. For the full fiscal year, large cap growth stocks, as measured by the Russell 1000® Growth Index provided the weakest returns among major indices rising 10.1%, while the Russell 1000® Value Index gained 18.8%. In addition defensive type stocks outperformed on the year and this is evident in sector performance as telecom, health care and consumer staples sectors outperformed. The Federal Reserve’s decision to keep interest rates lower for the foreseeable future has made riskier assets more attractive and despite some downturns during the period in reaction to poor economic news, the US equity markets have been trending upward.

Within the Russell 1000® Value Index, the best performing sectors for the fiscal year were consumer discretionary, consumer staples and telecommunication services, posting gains of 30.1%, 26.2%, and 24.3%, respectively. All ten sectors generated positive returns, with materials, energy and information technology lagging the other sectors for the year. These latter sectors posted returns of 4.9%, 8.2% and 10.6%, respectively.

4

Mercer US Large Cap Value Equity Fund

The Mercer Large Cap Value Equity Fund underperformed the Russell 1000® Value Index during the fiscal period. The primary driver of underperformance was stock selection in the telecommunication services, information technology and health care sectors. Within the telecommunication services sector, exposure to out-of-benchmark holdings Koninklijke, Vodafone and France Telecom was a significant detractor, costing the portfolio 79 basis points in relative results. Technology holdings Marvel, Qualcomm and Cisco were a drag on relative results over the period. The overweight to health care holdings Humana and Aetna while an underweight to the holding Bristol-Myers was a notable detractor in the health care sector. At March 31, 2013 the Fund no longer held Vodafone and Marvel. An overweight position in the consumer discretionary sector and good stock selection in the financials and energy sectors contributed positively to results.

Robeco’s underperformance relative to the index for the fiscal year and on a sector attribution basis, was due in large part to sector weighting decisions. The underweight positions to the telecommunication services and consumer staples sectors and an overweight position to the tech sector were all large detractors for the period. Good stock selection in the materials sectors was a modest positive contribution to the Fund’s performance for the fiscal year. O’Shaughnessy underperformed the Index for the fiscal year. Despite strong stock selection in the financials sector, which contributed positively to O’Shaughnessy’s performance, their broader investment mandate and stock selection in telecoms detracted from performance. Brandywine also underperformed for the fiscal year, and like Robeco, was primarily hurt by sector weighting decisions. Overall, stock selection added value. TBCAM outperformed the benchmark for the fiscal year. TBCAM’s outperformance was primarily driven by stock selection in the energy and consumer discretionary sectors. Stock selection in the tech sector was a detractor.

Risk Considerations

Value investing involves the risk that an investment made in undervalued securities may not appreciate in value as anticipated or remain undervalued for long periods of time. The Fund may experience high portfolio turnover which may result in higher costs and capital gains. The Fund’s volatility may be amplified by its ability to select sub-advisors to allocate assets.

5

Mercer Funds

March 31, 2013

Comparison of Change in Value of a $10,000 Investment in

Mercer US Large Cap Value Equity Shares vs. the

Russell 1000® Value Index

As of March 31, 2013

This graph shows the performance of the Mercer US Large Cap Value Equity Fund1 Class Y-3 shares versus the Russell 1000® Value Index from August 15, 2005, which is the inception date of the Fund, through March 31, 2013. The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-866-658-9896 for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased. Due to market conditions, the Fund has experienced unusually high performance which may not be sustainable or repeated in the future.

6

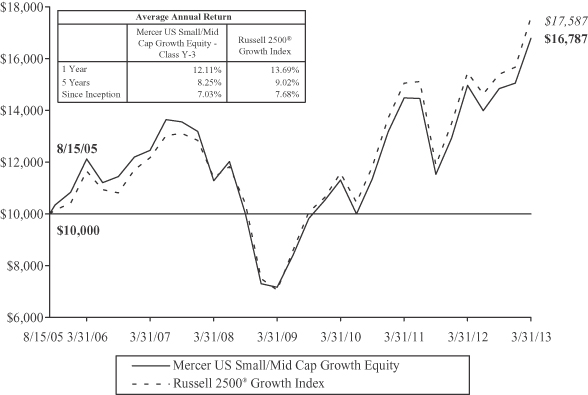

Mercer US Small/Mid Cap Growth Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, comprised primarily of capital appreciation. The benchmark for the Fund is the Russell 2500® Growth Index.

Investment Strategy

The Fund invests principally in equity securities issued by small-to-medium capitalization U.S. companies. The companies will generally have higher earnings and/or revenue growth histories or expectations relative to the Russell 2500® Growth Index.

Performance

For the fiscal year ended March 31, 2013, the Fund’s Y-3 share class performance was 12.11% compared to its benchmark return of 13.69%. Performance for the Fund is reported net of operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisors

As of March 31, 2013, the Fund employed four sub-advisors, Delaware Management Company (Delaware), Goldman Sachs Asset Management, L.P. (GSAM), Palisade Capital Management, L.L.C. (Palisade), and Westfield Capital Management Company, L.P. (Westfield). Delaware uses a bottom-up fundamental process in seeking to find companies with attractive business models that generate strong free cash flow. They also believe in a concentrated portfolio and will typically hold approximately 25 to 30 holdings. GSAM bases investment decisions on the identification of high-quality business franchises it believes that are strategically positioned for long-term growth. The firm seeks to invest in companies that meet its criteria for a high-quality growth investment, which include dominant market share, established brand name, pricing power, and recurring revenue streams. Palisade believes companies with strong or improving prospects for growth generate superior returns. Palisade believes that (1) fundamental research is the basis for identifying superior businesses, (2) long term investment success is the result of owning fundamentally strong and dynamic companies trading at a discount to their growth rates, (3) indentifying a dynamic of change before it appears in consensus estimates leads to superior returns, and (4) management plays a significant role in the success of a company. Westfield employs a fundamental, bottom-up approach which seeks to identify reasonably priced stocks with high earnings growth potential.

Market Commentary and Fund Performance

For the Fund’s fiscal year, the market, as measured by the S&P 500 Index, rose 14.0% continuing the rise which started in March 2009. The now four-year bull market has brought returns of 114% for the four-year period ending March 2013. For the prior fiscal year, it was split into distinct periods as economic news impacted investor’s views regarding which type of investments were most attractive. The fiscal year began with negative returns in the first fiscal quarter as the market digested a European debt crisis and the resulting global slowdown. Investors favored defensive type of equities and the perceived lower risk of U.S. treasuries. The fiscal year was marked by reassurance from the world’s central banks that they would do whatever was necessary to improve global economic growth, including an unprecedented conditional commitment from the U.S. Federal Reserve to maintain low interest rates until unemployment falls below 6.5% or the inflation rate exceeds 2.5%. These commitments coupled with an improving U.S. economic outlook initiated the latter half of the fiscal year in the equity markets. While economic news was mixed over the fiscal year, there was continued and modest growth in nonfarm payrolls, a falling unemployment rate and an improved housing outlook. Growth expectations notched higher and this helped advance the U.S. equity market. Increased expectations were tempered by concerns over the ability of the two major political parties to settle issues regarding the federal budget — issues that must bridge deep philosophical differences. For the full fiscal year, large cap growth stocks, as measured by the Russell 1000® Growth Index provided the weakest returns among major indices rising 10.1%, while the Russell 1000® Value Index gained 18.8%. In addition defensive type stocks outperformed on the year and this is evident in sector performance as telecom, health care and consumer staples sectors outperformed. The Federal Reserve’s decision to keep interest rates lower for the foreseeable future has made riskier assets more attractive and despite some downturns during the period in reaction to poor economic news, the US equity markets have been trending upward.

7

Mercer US Small/Mid Cap Growth Equity Fund

Within the Russell 2500® Growth Index, the best performing sectors for the fiscal year were industrials, financials and consumer staples posting gains of 22.1%, 20.9%, and 17.2%, respectively. Lagging sectors for the fiscal year were information technology, energy and consumer discretionary, posting returns of 1.8%, 8.1%, and 11.2%, respectively.

The Mercer US Small/Mid Cap Growth Equity Fund underperformed the Russell 2500® Growth Index for the period. The primary driver of underperformance was stock selection in the industrials sector. Notable detractors in this sector included Expeditors International, Ritchie Brothers, Kennametal and Ryder Systems, costing the portfolio 85 basis points in relative results. A lack of exposure to airline stocks was an additional and significant detractor for the period. Good stock selection in the energy and telecommunications sectors was a positive contributor for the fiscal year.

Delaware underperformed the index for the period. Because Delaware manages a concentrated and high tracking error portfolio with a long term investment horizon, performance can vary significantly from year to year, as was the case from prior fiscal year to the current fiscal year. The primary areas of underperformance were in the industrials, consumer discretionary and tech sectors. Good stock selection in the telecommunication services sector helped to offset some of the underperformance in other sectors. GSAM outperformed the index during the period. Strong stock selection in the tech, telecommunication services and consumer discretionary sectors boosted results for the period. In particular, stock selection among semiconductors, wireless telecommunications services and specialty retail stocks positively contributed to results. An underweight position and poor stock selection in the industrials sector detracted from results. Palisade underperformed for the period. Stock selection in the industrials and tech sectors was a significant detractor. In the tech sector, a significant overweight and stock selection among software industry stocks was a large detractor. A number of acquisitions in the portfolio boosted results. Westfield outperformed for the period. The primary driver of outperformance for the period was stock selection in the energy and consumer discretionary sectors. Stock selection in the health care and industrials sectors detracted from results.

Risk Considerations

The Fund invests in growth stocks which may be particularly sensitive to market conditions. Investments made in small and mid-capitalization companies may be more volatile and less liquid due to limited resources or product lines and more sensitive to economic factors. The Fund may experience high portfolio turnover which may result in higher costs and capital gains. The Fund’s volatility may be amplified by its ability to select sub advisors to allocate assets.

8

Mercer Funds

March 31, 2013

Comparison of Change in Value of a $10,000 Investment in

Mercer US Small/Mid Cap Growth Equity Shares vs. the

Russell 2500® Growth Index

As of March 31, 2013

This graph shows the performance of the Mercer US Small/Mid Cap Growth Equity Fund1 Class Y-3 shares versus the Russell 2500® Growth Index from August 15, 2005, which is the inception date of the Fund, through March 31, 2013. The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-866-658-9896 for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

9

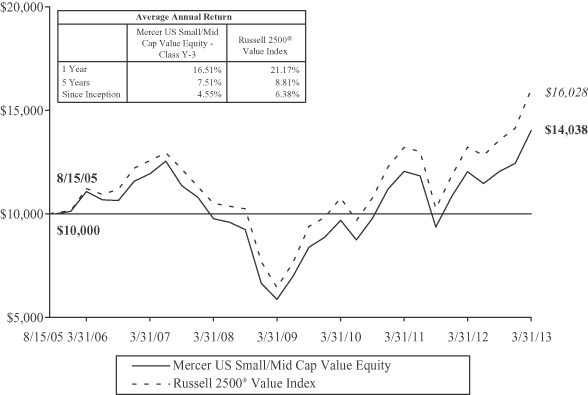

Mercer US Small/Mid Cap Value Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, comprised primarily of capital appreciation. The benchmark for the Fund is the Russell 2500® Value Index.

Investment Strategy

The Fund invests principally in equity securities issued by small-to-medium sized capitalization U.S. companies. Generally, the Fund invests in stocks that appear to be undervalued based on the stocks’ intrinsic values relative to their current market prices.

Performance

For the fiscal year ended March 31, 2013, the Fund’s Y-3 share class performance was 16.51% compared to its benchmark return of 21.17%. Performance for the Fund is reported net of operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisors

As of March 31, 2013, the Fund employed four sub-advisors, AQR Capital Management, LLC (AQR), NWQ Investment Management Company, LLC (NWQ), Systematic Financial Management, L.P. (Systematic), and River Road Asset Management, LLC (River Road). AQR’s investment philosophy combines concepts of value and momentum into a quantitative process blended with traditional factors as inputs and weightings partially determined through qualitative analysis. NWQ uses bottom-up fundamental analysis to identify undervalued companies where catalysts for improved valuation exist. The firm seeks stocks that are mispriced or neglected by Wall Street with attractive risk/reward characteristics. Systematic’s investment philosophy is predicated on its belief that stock prices are a reflection of consensus earnings estimates, and as revisions to those estimates rise or fall, stock prices will move accordingly. Systematic applies a strategic combination of qualitative and quantitative research seeking to identify high-quality, attractively valued small and medium-sized companies exhibiting a confirmed catalyst for stock price appreciation. River Road believes inefficiencies can be captured in smaller capitalization and out-of-favor companies and in those securities with little analyst coverage. Through bottom-up, fundamental research, the team seeks companies with attractive, sustainable returns that are financially strong and trade at compelling valuations.

Market Commentary and Fund Performance

For the Fund’s fiscal year, the market, as measured by the S&P 500 Index, rose 14.0% continuing the rise which started in March 2009. The now four-year bull market has brought returns of 114% for the four-year period ending March 2013. For the prior fiscal year, it was split into distinct periods as economic news impacted investor’s views regarding which type of investments were most attractive. The fiscal year began with negative returns in the first fiscal quarter as the market digested a European debt crisis and the resulting global slowdown. Investors favored defensive type of equities and the perceived lower risk of U.S. treasuries. The fiscal year was marked by reassurance from the world’s central banks that they would do whatever was necessary to improve global economic growth, including an unprecedented conditional commitment from the U.S. Federal Reserve to maintain low interest rates until unemployment falls below 6.5% or the inflation rate exceeds 2.5%. These commitments coupled with an improving U.S. economic outlook initiated the latter half of the fiscal year in the equity markets. While economic news was mixed over the fiscal year, there was continued and modest growth in nonfarm payrolls, a falling unemployment rate and an improved housing outlook. Growth expectations notched higher and this helped advance the U.S. equity market. Increased expectations were tempered by concerns over the ability of the two major political parties to settle issues regarding the federal budget — issues that must bridge deep philosophical differences. For the full fiscal year, large cap growth stocks, as measured by the Russell 1000® Growth Index provided the weakest returns among major indices rising 10.1%, while the Russell 1000® Value Index gained 18.8%. In addition defensive type stocks outperformed on the year and this is evident in sector performance as telecom, health care and consumer staples sectors outperformed. The Federal Reserve’s decision to keep interest rates lower for the foreseeable future has made riskier assets more attractive and despite some downturns during the period in reaction to poor economic news, the US equity markets have been trending upward.

10

Mercer US Small/Mid Cap Value Equity Fund

Within the Russell 2500® Value Index, the best performing sectors were consumer staples, consumer discretionary and health care with gains of 37.2%, 29.5%, and 26.5%, respectively. Lagging sectors included telecommunication services, and information technology, which posted returns of -3.1%, -3.5%, and -6.3%, respectively.

The Mercer Small/Mid Cap Value Equity Fund underperformed the Russell 2500® Value Index for the fiscal year. Stock selection in the consumer discretionary and health care sectors was the primary driver of underperformance for the period. In the consumer discretionary sector, notable detractors included the holdings Big Lots, Career Education, Ascena Retail and Express. At March 31, 2013 the Fund no longer held Express. In the health care sector, stock selection among health care providers cost the portfolio 84 basis points in relative results and was the leading industry detractor in that sector. Good stock selection in the financials and telecommunications sectors helped to offset underperformance in other sectors.

AQR, a manager with a quantitative strategy combining elements of valuation and momentum, underperformed the index. The strategy underperformed primarily due to implementation of a long/short model portfolio into a long only portfolio. AQR’s sector weighting decisions offset some of the underperformance on the year. NWQ underperformed the benchmark, with the strategy lagging in the tech and consumer discretionary sectors. In the tech sector, underperformance was largely due to significant overweights to underperforming semiconductor and electronic equipment industries. A lack of exposure to homebuilders in the consumer discretionary sector was an additional detractor. Stock selection in the financials sector helped relative results. River Road outperformed for the period, posting strong relative results in the financials and tech sectors. In tech, underweighting those same underperforming semiconductor and electronic equipment industries, was a boost to relative results. Stock selection in the consumer discretionary sector detracted from results. Systematic posted strong absolute returns but lagged the benchmark for the period. Stock selection in the consumer sectors was a significant detractor for the period. In the consumer discretionary sector, the holding Herbalife was a notable detractor, costing the portfolio 94 basis points in relative results. At March 31, 2013 the Fund no longer held Herbalife. Good stock selection in the materials sector was a positive contributor.

Risk Considerations

Value investing involves the risk that an investment made in undervalued securities may not appreciate in value as anticipated or remain undervalued for long periods of time. Investments made in small and mid-capitalization companies may be more volatile and less liquid due to limited resources or product lines and more sensitive to economic factors. The Fund may experience high portfolio turnover which may result in higher costs and capital gains. The Fund’s volatility may be amplified by its ability to select sub advisors to allocate assets.

11

Mercer Funds

March 31, 2013

Comparison of Change in Value of a $10,000 Investment in

Mercer US Small/Mid Cap Value Equity Shares vs. the

Russell 2500® Value Index

As of March 31, 2013

This graph shows the performance of the Mercer US Small/Mid Cap Value Equity Fund1 Class Y-3 shares versus the Russell 2500® Value Index from August 15, 2005, which is the inception date of the Fund, through March 31, 2013. The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-866-658-9896 for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

12

Mercer Non-US Core Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, which includes capital appreciation and income. The benchmark for the Fund is the MSCI EAFE Index.

Investment Strategy

The Fund invests principally in equity securities issued by non-U.S. companies of any capitalization, located in the world’s developed and emerging capital markets.

Performance

For the fiscal year ended March 31, 2013, the Fund’s Y-3 share class performance was 11.53% compared to its benchmark return of 11.25%. Performance for the Fund is reported net of operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisors

As of March 31, 2013, the Fund employed four sub-advisors, Arrowstreet Capital, Limited Partnership (Arrowstreet), Echo Point Investment Management, LLC (Echo Point), Lingohr & Partner North America, Inc. (Lingohr) and Massachusetts Financial Services Company (MFS). The Fund was reduced from six managers to four managers in September, 2012 when the dedicated emerging markets managers, Lazard Asset Management (Lazard) and William Blair & Company L.L.C. (William Blair) were removed from the Fund.

Arrowstreet employs a quantitative investment approach, focusing on developing and exploiting proprietary signals. Arrowstreet’s proprietary investment process measures the direct effects on stocks, as well as the indirect effects on countries, global sectors, country/sector interactions, and expanded linkages of inter-related companies. Arrowstreet constructs portfolios with an integrated alpha forecast, while simultaneously estimating risk and transaction costs, to create optimized portfolios. Echo Point manages a growth portfolio, which focuses on attractively valued stocks that are identified as being high quality and exhibiting strong growth characteristics. This strategy invests opportunistically in emerging markets. Lingohr manages a value portfolio, which consists of undervalued stocks identified through the firm’s disciplined, systematic, quantitative investment approach. Stock selection includes a fundamental qualitative overlay through the portfolio management team. This strategy invests opportunistically in emerging markets. MFS manages a value portfolio, which focuses on stocks whose long-term value they believe is not adequately reflected in the stock price. This strategy invests opportunistically in emerging markets.

Market Commentary and Fund Performance

International equity markets were influenced by the on-going sovereign debt crisis in Europe and uncertainty over China growth during the 12 month period ending March 31, 2013. The one year period was defined by two divergent markets. During the second quarter of 2012, concerns over the European crisis and the decelerating US economy resurfaced leading to the selloff of risky assets. News that the Eurozone had officially reentered a recession during the first quarter of 2012 fueled the market selloff. In addition, the French election, although the results were not a surprise, concerned investors due to the potential disruption of established austerity policies and increased tensions with Germany. In addition, the periphery countries remained in focus as Spain’s third largest bank, Bankia, was bailed out. Contributing to the global uncertainty was China’s government warning that their growth expectations for 2012 had fallen to 7.5% from the original 7.9% expectation.

However, over the subsequent 9-month period ending March 31, 2013, the markets stabilized as positive economic and fiscal news buoyed a market rally, posting a 19.8% return, after selling off -7.2% over the previous 3 months. During the third quarter of 2012, the world’s central bankers helped stem investors’ concerns about slowing economic growth and the potential of a Eurozone breakup with accommodative monetary policy. Europe rebounded during the third quarter spurred by the market’s positive reaction to the European Central Bank’s (“ECB”) bond-buying program which reduced the risk of sovereign default. Rounding out 2012, the market continued to rally into the fourth quarter supported by policy measures taken by the ECB and signs of China stabilization.

For 2013, the market forged ahead in January supported again by positive macro news. Positive news out of the U.S. sparked the market rally, particularly the news on the fiscal cliff resolution, an extension of the U.S. debt ceiling and positive earnings

13

Mercer Non-US Core Equity Fund

announcements. In addition, stabilization in Europe and signs that China growth may be recovering supported global equities. Over the rest of the quarter, however, uncertainty resurfaced again regarding stability in Europe particularly the Italian election results and the voter’s failure to endorse the fiscal austerity program. In addition, the banking crisis in Cyprus, fueled an increase in volatility during the second half of the quarter. The market proved resilient and held their gains and returned 5.2% for the first quarter of 2013. The MSCI EAFE Index posted a solid gain of 11.25% for the 12-month period ending March 31, 2013.

In this environment, the Mercer Non-US Core Equity Fund outperformed the MSCI EAFE Index by 0.28% for the 12-month period ending March 31, 2013. The Fund’s bias to quality in terms of investing in companies with sustainable levels of profitability and positive exposures to defensive sectors were the primary drivers of outperformance. In addition, favorable security selection in energy, information technology and materials contributed positively to performance. From a country perspective, positive selection in China, Japan, Germany, and the United Kingdom contributed positively to performance. Somewhat offsetting positive performance was negative country, sector and selection decisions. In particular, an underweight to Australia, an overweight to Italy and an overweight to emerging markets, such as Brazil and China detracted from performance. From a sector perspective, an underweight to the outperforming financials sector and an overweight to the underperforming information technology sector were detractors from performance. In addition, security selection was negative in consumer staples and consumer discretionary.

In aggregate, performance of the Fund’s sub-advisors was positive, with three of the four sub-advisors outperforming. MFS led all sub-advisors, by outperforming the index by 5.29%, as their style of focusing on undervalued, high quality businesses did well over the past year. Performance was driven by both sector and security selection decisions. Security selection was particularly strong in information technology, industrials and materials. Sector allocations were driven by underweighting industrials and materials in favor of overweighting consumer staples. From a regional perspective, selection in the Asia Pacific and Western Europe regions contributed positively to performance. Slightly offsetting the positive performance was the decision to overweight the poor performing telecommunication sector and negative security selection in the information technology sector. Another strong contributor for the year was Arrowstreet. Arrowstreet outperformed from a sector perspective as a result of positive contributors from sector allocations and selection. Sector allocations were positive as a result of overweighting health care and underweighting energy, materials and utilities. Selection was strong in consumer discretionary, energy, health care, industrials, and telecommunication services. From a regional perspective, most of the value-add was driven by positions in Western Europe (France, Germany, Spain, Sweden, and the United Kingdom). In addition, positions in Asia Pacific, led by Australia and Japan also added value. Slightly offsetting the positive performance was the decision to overweight the information technology sector and negative security selection within the sector. Echo Point also added value over the past year driven by positive selection in financials, information technology and telecommunication services. From a regional perspective, the majority of value-add was driven by selection in Europe, particularly in Germany and the United Kingdom. Slightly offsetting the positive performance was negative selection within the industrials sector. The primary detractor for the past year was Lingohr. Lingohr detracted from performance due to sector allocation and selection decisions. Sector allocations were hurt by underweighting consumer staples, financials and health care in favor of overweighting materials and consumer discretionary. Selection was particularly difficult in telecommunication services, consumer staples and industrials. From a regional perspective, most of the underperformance was due to the Emerging Market non-benchmark exposure. Slightly offsetting the negative performance was positive selection in the industrials sector.

Risk Considerations

The Fund invests in foreign and emerging market securities which involves certain risks such as currency volatility, political and social instability and reduced market liquidity. Emerging markets may be more volatile and less liquid than more developed markets and therefore may involve greater risks. Investments made in small and mid-capitalization companies may be more volatile and less liquid due to limited resources or product lines and more sensitive to economic factors. The Fund may experience high portfolio turnover which may result in higher costs and capital gains. The Fund’s volatility may be amplified by its ability to select sub-advisors to allocate assets.

14

Mercer Funds

March 31, 2013

Comparison of Change in Value of a $10,000 Investment in

Mercer Non-US Core Equity Shares vs. the

MSCI EAFE Index

As of March 31, 2013

This graph shows the performance of the Mercer Non-US Core Equity Fund1 Class Y-3 shares versus the MSCI EAFE Index from August 18, 2006, which is the inception date of the Fund, through March 31, 2013. The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-866-658-9896 for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

15

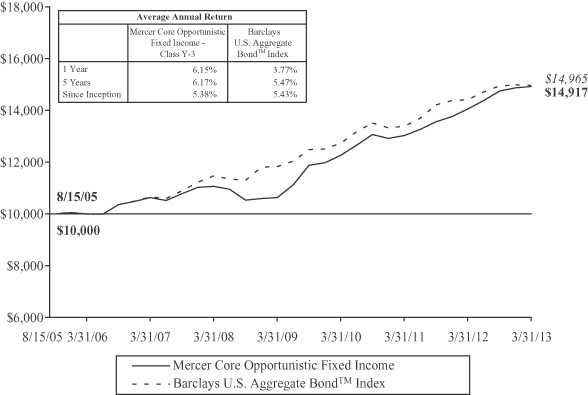

Mercer Core Opportunistic Fixed Income Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide total return, consisting of both current income and capital appreciation. The benchmark for the Fund is the Barclays U.S. Aggregate BondTM Index.

Investment Strategy

The Fund invests principally in investment grade fixed income securities, including government securities and corporate bonds. The Fund may also invest in non-investment grade bonds, non-U.S. dollar denominated bonds, bonds issued by issuers located in emerging capital markets, and certain derivative instruments.

Performance

For the fiscal year ended March 31, 2013, the Fund’s Y-3 share class performance was 6.15% compared to its benchmark return of 3.77%. Performance for the Fund is reported net of operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisors

As of March 31, 2013, the Fund employed four sub-advisors, Dodge & Cox, Western Asset Management Company (WAMCO), Pacific Investment Management Company LLC (PIMCO), and MacKay Shields LLC. Dodge & Cox manages its allocated portion of the Fund with an extended investment horizon supported by fundamental research and a strict valuation discipline. Their process emphasizes security-level research and individual security and sector selection to build a high-average-quality portfolio that seeks incremental yield versus the broad market. WAMCO manages its allocated portion of the Fund using a diversified, tightly controlled, value-oriented portfolio. The firm’s management style emphasizes the use of multiple strategies and active sector rotation and issue selection, while constraining overall interest rate risk relative to the benchmark. PIMCO manages its allocated portion of the Fund using a blend of long-range macro-economic forecasts with shorter-term, bottom-up security selection focused on valuation. The firm uses sector rotation and duration targeting as primary drivers of performance within a disciplined, risk-controlled approach. MacKay Shields manages its allocated portion of the Fund using a philosophy which is centered on the belief that the best risk-adjusted returns and, ultimately, the best absolute returns, are generated by a strategy of yield capture and error avoidance. This research process is focused on avoiding securities that have uncompensated risk.

Market Commentary and Fund Performance

Although there was frequent volatility and reversals of investor sentiment during the one-year period ending March 31, 2013, the general trend over the trailing twelve months was favorable for fixed income investors. U.S. Treasury rates fell moderately for the period, with the 10-year Treasury dropping 36 basis points (2.21% at March 31, 2012 versus 1.85% at March 31, 2013) and the 30-year Treasury dropping slightly less at 25 basis points (3.35% at March 31, 2012 versus 3.10% at March 31, 2013), but with sizable moves over short time periods and a wide trading range overall (nearly 100 basis points from high to low for the 10-year Treasury). The calendar pattern in recent years — strong starts followed by mid-year sell-offs and risk aversion, migrating back towards risk seeking in the closing months — continued to hold for 2012. After a big move upwards in risk assets to start the year, the second calendar quarter brought renewed market focus on challenges in the Euro-zone as well as deteriorating U.S. economic data, to the point where 10-year Treasury rates touched below 1.40% (a measure 60 basis points lower than the lowest level seen in the 2008 Global Financial Crisis). Later, despite mixed U.S. economic data and slowing global economic activity, market sentiment improved due largely to efforts by the European Central Bank and Federal Reserve to support economic growth and foster market confidence. Notable “interventions” and actions included extending Operation Twist, announcing Quantitative Easing III, and moving away from rate/date guidance towards inflation and employment targets. This improved sentiment, in addition to strong corporate fundamentals and improving news from Europe, drove a credit sector rally to end the year. Favorable market technicals were also present, with investor appetite for new issuance offering (any) yield relative to near-zero money markets and ultra-low Treasury yields. Not even the tightly contested U.S. presidential election, fiscal cliff/sequester discussions, and headline-making in Italy and Cyprus toward the end of the period could derail non-Treasury bond spreads from moving lower. Although market performance was positive, it was somewhat of a unsettled twelve-month period for investors given a slowly improving U.S. economy that appears to be balancing support for shorter-term risks with the need to prepare for longer-term prosperity.

16

Mercer Core Opportunistic Fixed Income Fund

Given a downward trend in both the U.S. Treasury curve (rates lower) and credit spreads (buyers pushing up prices for riskier assets) over the twelve months ending March 31, 2013, absolute returns in fixed income were relatively strong. Spread sectors (non-Treasury) provided healthy returns for the fiscal period in absolute terms and in relation to similar-duration Treasuries (excess returns), led by a double-digit return in the high yield sector. The Fund’s return was positive in both absolute terms and in relation to the Barclays U.S. Aggregate Bond Index for the period. The Fund benefited from its strategic overweight to spread sectors including an allocation to high yield that was the top performing sub-sector for the trailing twelve months. The Fund underweight to lower yielding US Treasuries in the form of a shorter duration stance or term structure bias (favoring certain maturities over others) relative to the index was detrimental to performance at times.

The risk posture of each sub-advisor correlated with their respective performance results. PIMCO’s relatively defensive top-down positioning was particularly helpful during periods of condensed risk-aversion but not detrimental during spread rallies. WAMCO’s more aggressive spread sector allocation provided returns well ahead of the Fund’s benchmark, while Dodge & Cox’s bias towards corporate credit and avoidance of government exposure most benefited the Fund after the June/July market shift. Although MacKay slightly trailed its sector benchmark, the high yield market itself greatly outperformed broad market fixed income, prompting MacKay to easily surpass the Fund’s benchmark. Strategic and/or tactical underweights to lower yielding US Treasuries in the form of a shorter duration stance or term structure bias (favoring certain maturities over others), relative to benchmarks was detrimental to sub-advisor performance at times.

Risk Considerations

The Fund is subject to the same risks as the underlying bonds in the portfolio such as credit, prepayment, call and interest rate risk. As interest rates rise the value of bond prices will decline. The Fund may invest in more aggressive investments such as foreign securities which may expose the Fund to currency and exchange rate fluctuations, derivatives (futures, options, swaps) and high yield debt (also known as junk bonds) all of which may cause greater volatility and less liquidity. Derivatives may be more sensitive to changes in market conditions and may amplify risks. The Fund may experience high portfolio turnover which may result in higher costs and capital gains. The Fund’s volatility may be amplified by its ability to select sub-advisors to allocate assets.

17

Mercer Funds

March 31, 2013

Comparison of Change in Value of a $10,000 Investment in

Mercer Core Opportunistic Fixed Income Shares vs. the

Barclays U.S. Aggregate Bond™ Index

As of March 31, 2013

This graph shows the performance of the Mercer Core Opportunistic Fixed Income Fund1 Class Y-3 shares versus the Barclays US Aggregate Bond™ Index from August 15, 2005, which is the inception date of the Fund, through March 31, 2013. The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-866-658-9896 for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

18

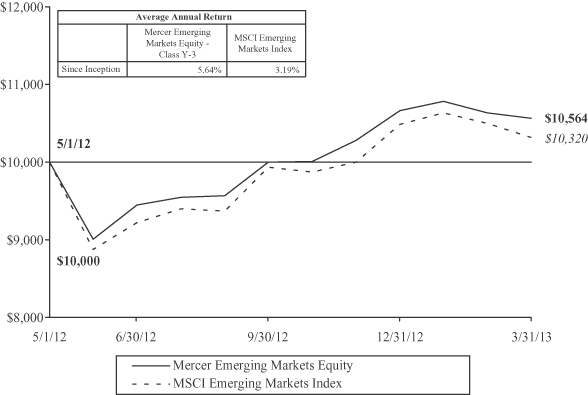

Mercer Emerging Markets Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, which includes capital appreciation and income. The benchmark for the Fund is the MSCI Emerging Markets Index.

Investment Strategy

The Fund invests principally in equity securities of large, medium and small capitalization companies, located in emerging markets, other investments that are tied economically to emerging markets, as well as in American, European and Global Depository receipts.

Performance*

Since inception of May 1, 2012, the Fund’s Y-3 share class performance was 5.64% compared to its benchmark return of 3.19%. Performance for the Fund is reported net of operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisors

As of March 31, 2013, the Fund employed three sub-advisors, AQR Capital Management, LLC (AQR), Kleinwort Benson Investors International Ltd. (KBI) and Vontobel Asset Management, Inc. (Vontobel). AQR employs a quantitative investment approach focused on sourcing alpha from currency, country and security selection models. AQR’s proprietary investment process uses systematic factors, such as value, momentum, quality factors within the alpha models. AQR constructs portfolios with an integrated alpha forecast, while simultaneously estimating risk and transaction costs, to create optimized portfolios. KBI manages a systematic process focusing on quality firms growing their dividend yield. The portfolio construction process uses sector and region constraints to minimize uncompensated risks to ensure the majority of risk is associated with the alpha model. Vontobel uses a fundamental process to identify high quality, sustainable growth companies in businesses with high barrier to entry. Vontobel’s risk management process focused on capital preservation and manages risk in absolute terms.

Market Commentary and Fund Performance

Emerging equity markets were influenced by the on-going sovereign debt crisis in Europe and uncertainty over China growth during the 11 month period ending March 31, 2013. The period was defined by two divergent markets. During the second quarter of 2012, concerns over the European crisis and the decelerating US economy resurfaced leading to the selloff of risky assets. News that the Eurozone had officially reentered a recession during the first quarter fueled the market sell-off. In addition, the French election, although the results were not a surprise, concerned investors due to the potential disruption of established austerity policies and increased tensions with Germany. In addition, the periphery countries remained in focus as Spain’s third largest bank, Bankia, was bailed out. Contributing to the global uncertainty was China’s government warning that their growth expectations for 2012 had fallen to 7.5% from the original 7.9% expectation.

However, over the subsequent 9-month period ending March 31, 2013, the markets stabilized as positive economic and fiscal news buoyed a market rally, posting a 12.3% return, after selling off -6.6% over the previous 2 months. During the third quarter of 2012, the world’s central bankers helped stem investors’ concerns about slowing economic growth and the potential of a Eurozone breakup with accommodative monetary policy. Europe rebounded during the third quarter spurred by the market’s positive reaction to the European Credit Bank’s (“ECB”) bond-buying program which reduced the risk of sovereign default. Rounding out 2012, the market continued to rally into the fourth quarter supported by policy measures taken by the ECB and signs of China stabilization.

For 2013, the market forged ahead in January supported again by positive macro news. Positive news out of the U.S. sparked the market rally, particularly the news on the fiscal cliff resolution, an extension of the U.S. debt ceiling and positive earnings announcements. In addition, stabilization in Europe and signs that China growth may be recovering supported global equities. Over the rest of the quarter, however, uncertainty resurfaced again regarding stability in Europe particularly the Italian election results and the voter’s failure to endorse the fiscal austerity program. In addition, the banking crisis in Cyprus and

| * | The Fund commenced operations on May 1, 2012. |

19

Mercer Emerging Markets Equity Fund

strict requirements for an EU bailout fueled an increase in volatility during the second half of the quarter. The market struggled to gain a footing and returned -1.62% for the first quarter of 2013. The MSCI Emerging Market Index posted a solid gain of 3.19% for the 11-month period ending March 31, 2013.

In this environment, the Mercer Emerging Markets Equity Fund outperformed the MSCI Emerging Markets Index by +2.45% for the 11-month period ending March 31, 2013. The Fund’s bias to quality in terms of investing in companies with sustainable levels of profitability and positive exposures to defensive sectors were the primary drivers of outperformance. The primary sector allocations adding value included overweighting consumer staples and underweighting energy, financials and materials. In addition, favorable security selection in consumer discretionary, consumer staples and industrials contributed positively to performance. From a country perspective, positive selection in Mexico, Malaysia and South Korea contributed positively to performance. Offsetting some of the positives for the Fund was negative security selection in financials and information technology.

In aggregate, performance of the Fund’s sub-advisors was positive, with all three sub-advisors outperforming. Vontobel was the strongest contributor, as their style of focusing on high quality, sustainable growth businesses did well over the past year. Performance was driven by both sector and selection decisions. Security selection was particularly strong in consumer staples and industrials. Sector allocations were driven by underweighting energy and materials in favor of overweighting consumer staples. From a regional perspective, selection in the Asia Pacific and Latin America regions contributed positively to performance. Slightly offsetting some of the positives for Vontobel was negative security selection in information technology and utilities. KBI added value primarily due to selection in consumer staples, energy, information technology, and telecommunication services. From a regional perspective, regional allocations drove performance, with an overweight to Asia Pacific (China and Taiwan) adding value. Detracting from KBI’s performance was negative security selection in the consumer staples and financial sectors. AQR also contributed positively, with a combination of currency, country and security selection adding value. Positive security selection contribution was driven by consumer staples, energy, financials, and industrials.

Risk Considerations

The Fund invests in emerging market securities which involves certain risks such as currency volatility, political and social instability and reduced market liquidity. Emerging markets may be more volatile and less liquid than more developed markets and therefore may involve greater risks. Investments made in small and mid-capitalization companies may be more volatile and less liquid due to limited resources or product lines and more sensitive to economic factors. The Fund may invest in more aggressive investments such as derivatives (futures, options, swaps) all of which may cause greater volatility and less liquidity. Derivatives are more sensitive to changes in market conditions and may amplify risks. The Fund may experience high portfolio turnover which may result in higher costs and capital gains. The Fund’s volatility may be amplified by its ability to select sub advisors to allocate assets.

20

Mercer Funds

March 31, 2013

Comparison of Change in Value of a $10,000 Investment in

Mercer Emerging Markets Equity Shares vs. the

MSCI Emerging Markets Index

As of March 31, 2013

This graph shows the performance of the Mercer Emerging Markets Equity Fund Class Y-3 shares versus the MSCI Emerging Markets Index from May 1, 2012, which is the inception date of the Fund, through March 31, 2013. The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-866-658-9896 for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

21

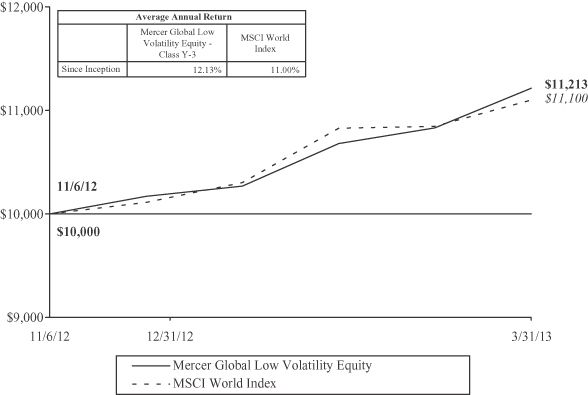

Mercer Global Low Volatility Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, which includes capital appreciation and income. The benchmark for the Fund is the MSCI World Index.

Investment Strategy

The Fund invests principally in equity securities of U.S. and foreign issuers, of large, medium and small capitalization companies.

Performance*

Since inception of November 6, 2012, the Fund’s Y-3 share class performance was up 12.13% compared to its benchmark return of 11.00%. Performance for the Fund is reported net of operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisors

As of March 31, 2013, the Fund employed three sub-advisors, Acadian Asset Management LLC (Acadian), MFG Asset Management (MFG) and First Eagle Investment Management, LLC (First Eagle). Acadian’s process uses both risk analysis and alpha forecasts to create the portfolio. The process uses a risk model to determine the systematic risk and the level of volatility of each stock in the investible universe. Once a stock’s risk is determined, the manager uses their alpha model as an overlay to determine the optimal mix of securities. The alpha model consists of five alpha categories including value, growth, risk, macroeconomic, and technical factors. MFG screens the universe of investible global stocks to identify companies which MFG believes have demonstrable and sustainable competitive advantages, which are then evaluated using MFG’s key quality criteria: economic moat; business risk; agency risk; and re-investment potential. The manager then incorporates “dual-lens” valuation using both long-term intrinsic value and three-year forecast total shareholder returns using MFG’s proprietary forecasts. Portfolio construction is determined by each stock’s ranking based on the qualitative assessment of the key criteria, the quantitative assessment driven by valuation, and detailed macroeconomic research within a robust risk management framework. From time to time, MFG may hold up to 20% in cash if warranted by their assessment of the macro environment. First Eagle can be broadly characterized as value in approach, looking to identify companies selling at a discount to intrinsic value with the goal being to avoid permanent impairment of capital (as opposed to temporary losses in share value relating to shifting investor sentiment or other normal share price volatility). The primary valuation measure is enterprise value to normalized earnings before interest and taxes, although other metrics can be applied depending on the company or industry. If stocks are deemed too expensive, based on their bottom up valuation analysis, cash or bonds will be held instead up to 20%. In addition, a gold exposure is maintained (both through gold backed exchange traded funds and the equities of gold mining companies), with the view that it is a potential portfolio hedge.

Market Commentary and Fund Performance

Global equity markets were influenced by the on-going sovereign debt crisis in Europe and uncertainty over China growth during the 5-month period ending March 31, 2013. The market rallied late in the 4th quarter, led by Europe and Asia, supported by policy measures taken by the ECB and signs of China stabilization.

For 2013, the market forged ahead in January supported again by positive macro news. Positive news out of the U.S. sparked the market rally, particularly the news on the fiscal cliff resolution, an extension of the U.S. Debt ceiling and positive earnings announcements. In addition, stabilization in Europe and signs that China growth may be recovering supported global equities. Over the rest of the quarter, however, uncertainty resurfaced again regarding stability in Europe particularly the Italian election results and the voter’s failure to endorse the fiscal austerity program. In addition, the banking crisis in Cyprus and strict requirements for an EU bailout fueled an increase in volatility during the second half of the quarter. The market proved resilient and held their gains and returned 5.1% for the first quarter of 2013. The MSCI World Index posted a solid gain of 11.00% for the 5-month period ending March 31, 2013.

| * | The Fund commenced operations on November 6, 2012. |

22

Mercer Global Low Volatility Equity Fund

In this environment, the Mercer Global Low Volatility Equity Fund outperformed the MSCI World Index by +1.13% for the 5-month period ending March 31, 2013. The Fund’s bias to lower market volatility with a high quality bias versus the broad index was rewarded over this time period. The majority of positive relative performance was during the first quarter of 2013, as more conservative positioning was rewarded. The defensive sector allocations such as overweight positions in consumer staples and utilities and underweighting the more cyclical areas of the market such as energy, financials, industrials, and materials added value. In addition, favorable security selection in consumer staples, financials and information technology contributed positively to performance. From a country perspective, positive selection in the United States, France and the United Kingdom contributed positively to performance. Offsetting some of the positives was a cash allocation that averaged approximately 9% in the Fund since inception.

In aggregate, performance of the Fund’s sub-advisors was positive, with two of the three sub-advisors outperforming. Acadian was a positive contributor as performance was driven by sector decisions. Sector allocations were driven by underweighting energy, information technology and materials and overweighting consumer staples. From a regional perspective, selection in the Asia Pacific region (ex-Japan), as well as North America and European regions, contributed positively to performance. Detracting from performance included the underweight to the outperforming consumer discretionary sector and negative security selection in the financials sector. MFG contributed positively to performance as performance was driven by both sector and security selection decisions. Security selection was strong in consumer discretionary and financials. Sector allocations were driven by overweighting consumer staples and underweighting materials. From a regional perspective, selection in North America and Western Europe contributed positively. First Eagle lagged since inception, with the majority of underperformance driven by a strategic allocation to gold and a tactical allocation to cash which both underperformed during the equity market rally over this time period. Offsetting some of the negative performance was positive security selection in financials and industrials.

Risk Considerations

The Fund invests in emerging market securities which involves certain risks such as currency volatility, political and social instability and reduced market liquidity. Emerging markets may be more volatile and less liquid than more developed markets and therefore may involve greater risks. Investments made in small and mid-capitalization companies may be more volatile and less liquid due to limited resources or product lines and more sensitive to economic factors. The Fund may invest in more aggressive investments such as derivatives (futures, options, swaps) all of which may cause greater volatility and less liquidity. Derivatives are more sensitive to changes in market conditions and may amplify risks. The Fund may experience high portfolio turnover which may result in higher costs and capital gains. The Fund’s volatility may be amplified by its ability to select sub-advisors to allocate assets.

23

Mercer Funds

March 31, 2013

Comparison of Change in Value of a $10,000 Investment in

Mercer Global Low Volatility Equity Shares vs. the

MSCI World Index

As of March 31, 2013

This graph shows the performance of the Mercer Global Low Volatility Equity Fund Class Y-3 shares versus the MSCI World Index from November 6, 2012, which is the inception date of the Fund, through March 31, 2013. The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-866-658-9896 for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

24

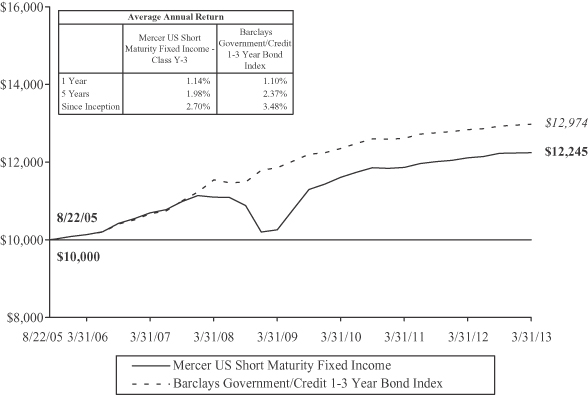

Mercer US Short Maturity Fixed Income Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide safety of principal and a moderate level of income. The benchmark for the Fund is the Barclays Government/Credit 1-3 Year Bond Index.

Investment Strategy

The Fund invests principally in investment grade fixed income securities of U.S. issuers, including government securities and corporate bonds. Generally, the Fund maintains an average dollar-weighted portfolio maturity of one to three years.

Performance

For the fiscal year ended March 31, 2013, the Fund’s Y-3 share class performance was 1.14% compared to its benchmark return of 1.10%. Performance for the Fund is reported net of operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisors

As of March 31, 2013, the Fund employed one sub-advisor, J.P. Morgan Investment Management Inc. (JP Morgan). JP Morgan manages the Fund using a bottom-up, relative value perspective, seeking to identify bonds that are high quality and offer inexpensive cash flows. The process is driven largely by security selection, seeking bonds that are undervalued.

Market Commentary and Fund Performance