Table of Contents

As filed with the Securities and Exchange Commission on May 15, 2006

Registration No. 333-124287

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 8

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

HEXION SPECIALTY CHEMICALS, INC.

(Exact name of registrant as specified in charter)

| New Jersey | 2821 | 13-0511250 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

180 East Broad Street

Columbus, Ohio 43215

(614) 225-4000

(Address, including zip code, and telephone number, including area code, of registrants’ principal executive offices)

Ellen German Berndt, Esq.

180 East Broad Street

Columbus, Ohio 43215

(614) 225-4000

(Name, address, including zip code, and telephone number, including area code, of agent for service of process)

With a copy to:

William B. Kuesel, Esq. O’Melveny & Myers LLP 7 Times Square New York, New York 10036 (212) 326-2000 | Kris F. Heinzelman, Esq. LizabethAnn R. Eisen, Esq. Cravath, Swaine & Moore LLP 825 Eighth Avenue New York, New York 10019 (212) 474-1000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

Title of each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price(1)(2) | Amount of Registration Fee(3) | ||

Common Stock, par value $0.01 per share (4) | $596,296,312 | $63,803.71 |

| (1) | Estimated solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457(o) under the Securities Act. |

| (2) | The proposed maximum offering price of each security will be determined by the registrant in connection with, and at the time of, the issuance of the securities. |

| (3) | Previously paid $94,160 by wire transfer on April 22, 2005. |

| (4) | Includes shares of common stock that the underwriters have the option to purchase to cover over-allotments, if any. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We and the selling shareholder may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 15, 2006

18,518,519 Shares

HEXION SPECIALTY CHEMICALS, INC.

Common Stock

Prior to this offering, there has been no public market for our common stock. The initial public offering price of our common stock is expected to be between $26.00 and $28.00. Our common stock has been approved for listing on the New York Stock Exchange under the symbol “HXN.”

We are selling 3,703,704 shares of common stock, and Hexion LLC, our parent (the “selling shareholder”), is selling 14,814,815 shares. We will not receive any of the proceeds from the sale of the shares being sold by the selling shareholder. We intend to use all of the net proceeds from the sale of common stock being sold by us together with available cash to repay certain indebtedness.

The underwriters have an option to purchase a maximum of 2,777,778 additional shares of common stock from the selling shareholder to cover over-allotments of shares of common stock.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 19.

| Price to Public | Underwriting Discounts and Commissions | Proceeds to Hexion Specialty | Proceeds to Selling Shareholder | |||||

Per Share | $ | $ | $ | $ | ||||

Total | $ | $ | $ | $ |

Delivery of the shares of common stock will be made on or about , 2006.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Credit Suisse | Goldman, Sachs & Co. | |||||

| JPMorgan | Lehman Brothers | |||||

Bear, Stearns & Co. Inc.

Citigroup

Deutsche Bank Securities

Morgan Stanley

UBS Investment Bank

William Blair & Company

KeyBanc Capital Markets

The date of this prospectus is , 2006.

Table of Contents

Table of Contents

| 1 | ||

| 19 | ||

| 36 | ||

| 38 | ||

| 39 | ||

| 40 | ||

| 41 | ||

| 43 | ||

| 53 | ||

MANAGEMENT’S DISCUSSIONAND ANALYSISOF FINANCIAL CONDITIONAND RESULTSOF OPERATIONS | 56 | |

| 89 |

| 111 | ||

| 127 | ||

| 130 | ||

| 140 | ||

| 149 | ||

| 154 | ||

| 156 | ||

| 159 | ||

| 166 | ||

| 166 | ||

| 167 | ||

| F-1 |

You should rely only on the information contained in this document or to which we have referred you. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

Dealer Prospectus Delivery Obligation

Until , 2006 (25 days after commencement of the offering), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligations to deliver a prospectus when acting as underwriters and with respect to unsold allotments or subscriptions.

i

Table of Contents

Market, Industry and Financial Data

This prospectus includes industry data that we obtained from periodic industry publications and internal company surveys. This prospectus includes market share and industry data that we prepared primarily based on management’s knowledge of the industry and industry data. Industry publications and surveys generally state that the information contained therein has been obtained from sources believed to be reliable.

Unless otherwise noted, statements as to our market share and market position relative to our competitors are approximated and based on management estimates using the above-mentioned latest-available third-party data and internal analysis and estimates. The global thermoset resins market is approximately $34 billion in annual sales. We based our market estimates on the $19 billion market for the product areas of the global thermoset resins market upon which we focus.

We determined our market share and market positions utilizing periodic industry publications. If we were unable to obtain relevant periodic industry publications, we based our estimates on our knowledge of the size of our markets, our sales in each of these markets and publicly available information regarding our competitors, as well as internal estimates of competitors’ sales based on discussion with our sales force and other industry participants.

Except as may otherwise be noted in this prospectus, all financial and other data for the year ended December 31, 2005 and the three months ended March 31, 2005 and 2006 presented herein give pro forma effect to the Hexion Formation, the Hexion Refinancings and the offering (each, as defined in “Prospectus Summary—Hexion Specialty Chemicals, Inc.—The Prior Transactions, the Hexion Formation and the Hexion Refinancings”), including the application of the net proceeds to the Company therefrom, as if they each had occurred on January 1, 2005, and all financial and other data as of March 31, 2006 presented herein give pro forma effect to the Hexion Refinancings and the offering, including the application of the net proceeds to the Company therefrom, as if they each had occurred on March 31, 2006 (with the financial and other data as of March 31, 2006 already reflecting the Hexion Formation, the Rhodia Acquisition, the Rohm and Haas Acquisition and the Brazilian Consumer Divestiture (each as defined in “Prospectus Summary—Recent Acquisitions and Divestiture”)). Except as may otherwise be noted in this prospectus, all financial and other data for the year ended December 31, 2005 and the three months ended March 31, 2005 does not give effect to the Akzo Acquisition, the Rhodia Acquisition, the Rohm and Haas Acquisition or the Brazilian Consumer Divestiture. Except as may otherwise be noted in this prospectus, all financial and other data for the three months ended and as of March 31, 2006 gives effect to the Rhodia Acquisition and the Rohm and Haas Acquisition from the respective dates of acquisition, but does not give effect to the Akzo Acquisition, which is expected to be completed during the second quarter.

ii

Table of Contents

This summary highlights information about Hexion Specialty Chemicals, Inc. and the offering contained elsewhere in this prospectus. It is not complete and may not contain all the information that may be important to you. You should carefully read the entire prospectus before making an investment decision, especially the information presented under the heading “Risk Factors.” In this prospectus, except as otherwise indicated herein, or as the context may otherwise require (i) all references to “Borden Chemical” refer to Borden Chemical, Inc. and its subsidiaries prior to the Hexion Formation (as defined in “—Hexion Specialty Chemicals, Inc.—The Prior Transactions, the Hexion Formation and the Hexion Refinancings”), (ii) all references to “Resolution Performance” refer to Resolution Performance Products Inc. and its subsidiaries prior to the Hexion Formation, provided that with respect to financial data, all references to “Resolution Performance” refer to Resolution Performance Products LLC, a former wholly-owned operating subsidiary of Resolution Performance Products Inc., and its subsidiaries, (iii) all references to “Resolution Specialty” refer to Resolution Specialty Materials Inc. and its subsidiaries prior to the Hexion Formation and (iv) all references to “Bakelite” refer to Bakelite Aktiengesellschaft and its subsidiaries prior to the Bakelite Transaction.

Hexion Specialty Chemicals, Inc.

Overview

We are the world’s largest producer of thermosetting resins, or thermosets. Thermosets are a critical ingredient for virtually all paints, coatings, glues and other adhesives produced for consumer or industrial uses. We are focused on providing a broad array of thermosets and associated technologies, with leading market positions in all key markets served. Our breadth of related products provides us with significant advantages across our operations, technologies and commercial organizations, while our scale provides us with significant efficiencies in our fixed and variable cost structure, allowing us to compete effectively throughout the value chain. In areas where it is advantageous, we are able to internally produce strategic raw materials, providing us with a lower cost operating structure and security of supply. Our value-added, technical service-oriented business model enables us to effectively participate in high-end specialty markets, while our scale enables us to extract value from higher volume applications.

Thermosets are developed to meet the performance characteristics required for each specific end use product. The type of thermoset used and how it is formulated, applied and cured determines the key attributes, such as durability, gloss, heat resistance, adhesion or strength of the final product. Hexion has the broadest range of thermoset resin technologies, with world class research, applications development and technical service capabilities. The total global thermoset resins market is approximately $34 billion in annual sales and includes products such as polyurethanes, urea-formaldehyde, phenol-formaldehyde, unsaturated polyesters, epoxies and melamine-formaldehyde. The key product areas of the global thermoset resins market upon which we focus and in which we have leading market positions is approximately $19 billion in annual sales, which excludes polyurethanes, unsaturated polyesters and furans/other.

Our products are used in thousands of applications and are sold into diverse markets, such as forest products, architectural and industrial paints, packaging, consumer products and automotive coatings, as well as higher growth markets, such as composites, UV cured coatings and electrical laminates. As of March 31, 2006, we had 94 production sites globally, and produce many of our key products locally in North America, Latin America, Europe and Asia. Through our worldwide network of strategically located production facilities, we serve more than 10,000 customers in over 100 countries. Our global customers include leading companies in their respective industries, such as 3M, Ainsworth, Ashland Inc., BASF, Bayer, DuPont, GE, Halliburton, Honeywell, Huntsman, Louisiana- Pacific, Owens Corning, PPG Industries, Sumitomo, Sun Chemical, Valspar and Weyerhaeuser.

Hexion was formed on May 31, 2005 through the combination of Borden Chemical (including Bakelite), Resolution Performance and Resolution Specialty. We believe the consolidation of these entities will provide us

1

Table of Contents

with significant opportunities for growth through global product line management, as well as considerable opportunities to increase operational efficiencies, reduce fixed costs, optimize manufacturing assets and improve the efficiency of capital spending. In 2005 and for the three months ended March 31, 2006, on a pro forma basis, we generated pro forma net sales of $4.7 billion and $1.2 billion, respectively. In 2005, 58% of our pro forma net sales were derived from sales to North America, 32% to Western Europe and 10% to Asia-Pacific, Latin America, Eastern Europe and other emerging markets. As of March 31, 2006, after giving pro forma effect to the Hexion Refinancings and the offering, we would have had $2.7 billion principal amount of outstanding indebtedness and $0.1 billion of cash and equivalents.

Our Business

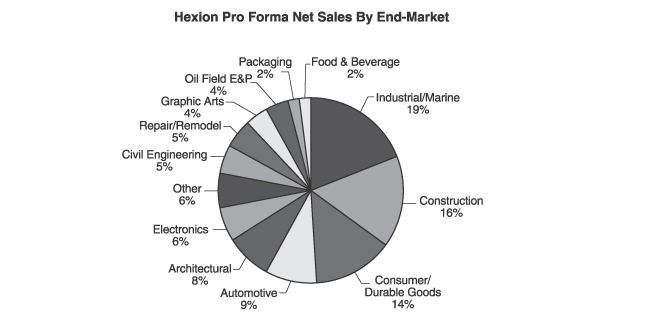

Our organizational structure is based on the products we offer and the markets we serve and at March 31, 2006 consisted of four operating divisions that are directly aligned with our reportable segments: Epoxy and Phenolic Resins, Formaldehyde and Forest Products Resins, Coatings and Inks, and Performance Products. The thermosets produced in each of our operating divisions and segments are used in two primary applications: adhesive & structural and coating. The table below illustrates our pro forma net sales to external customers for the year ended December 31, 2005 segregated by our two primary applications as well as the major product lines, major industry sectors, major end-use markets and key differentiating characteristics relative to each primary application.

Adhesive & Structural | Coating | |||

2005 Pro Forma Net Sales | $3.4 billion | $1.3 billion | ||

Major Products | • Formaldehyde based resins and intermediates • Epoxy resins and intermediates • Composite resins • Phenolic encapsulated substrates • Molding compounds | • Epoxy coating resins • Polyester resins • Alkyd resins • Acrylic resins • Ink resins and additives • Versatic acids and derivatives | ||

Major Industry Sectors Served | • Wood products and furniture • Transportation and industrial • Electrical equipment and appliances • Electronic products • Oil and gas field support • Marine and recreational (boats, RVs) • Chemical manufacturing | • Home building and maintenance • Transportation and industrial • Electrical equipment and appliances • Furniture • Printing • Chemical manufacturing | ||

Major End-Use Markets | • Plywood, particleboard, OSB, MDF • Carbon and glass fiber composites • Automotive friction materials • Furniture • Construction • Electrical laminates • Foundry • Oil and gas field proppants | • Decorative paints • Auto coatings • Marine and industrial coatings • Construction and maintenance coatings • Printing inks • Specialty coatings | ||

Key Characteristics of Resins | • Strength • Adhesion • Resistance (heat, water, electricity) | • Durability • Gloss and color retention • Resistance (water, UV, corrosion, temperature) • Strength | ||

2

Table of Contents

Adhesive & Structural Products and Market Applications

We are a leading global supplier of thermosets used in adhesive and structural applications. These products are used in a variety of end-markets including residential, commercial and industrial construction and repair/remodeling, furniture manufacture, automotive, oil and gas, chemicals and electronics. In 2005, sales of products used in adhesive & structural applications contributed approximately $3.4 billion to our total pro forma net sales. Our key products serving adhesive & structural applications include:

| • | Formaldehyde Based Resins and Intermediates. We are the leading producer of formaldehyde based resins for the forest products industry in North America with a 44% market share by volume and also hold significant positions in Europe, Latin America and Australia. Our products are used in a wide range of applications in the construction, automotive, electronics, oil drilling and steel industries. We are also the world’s largest producer of specialty phenolic resins and formaldehyde. We internally consume the majority of our formaldehyde production, giving us a significant competitive advantage. |

| • | Epoxy Resins and Intermediates. We are the world’s largest supplier of epoxy resins. Epoxy resins comprise the fundamental building blocks of many types of materials, such as formulated composite resins and structural adhesives and are often used in the auto, aerospace and electronics industries due to their unparalleled strength and durability. We also provide complementary products such as epoxy modifiers, curing agents, reactive diluents and specialty liquids. |

| • | Composite Resins. We are a leading producer of resins used in composites. Composites are a fast growing class of materials which are used in a wide variety of applications ranging from airframes and windmill blades to golf clubs. We supply epoxy resins to fabricators in the aerospace, sporting goods and pipe markets with a 50% market share in the United States and a 44% market share in Europe. In addition to epoxy, we manufacture resins from unsaturated polyester (UPR), which are generally combined with fiberglass for applications ranging from boat hulls to bathroom fixtures. |

| • | Phenolic Encapsulated Substrates. We are a leading producer of phenolic encapsulated sand and ceramic substrates used in oil field services and foundry applications. Our highly specialized compounds are designed to perform under extreme conditions, such as intense heat, high-stress and corrosive environments. In the oil field services industry we have a 45% global market share in resin encapsulated proppants, which are used to enhance oil and gas recovery rates and extend well life. We are also the leading producer by volume of foundry resins in North America with a 48% market share. Our foundry resin systems are used by major automotive and industrial companies for precision casting. |

| • | Molding Compounds. We are the leading producer of molding compounds in Europe, with an estimated market share of 64%. We formulate and produce a wide range of phenolic, polyester and epoxy compounds used to manufacture components requiring heat stability, electrical insulation, fire resistance and durability. |

Coating Products and Market Applications

We are also a leading global supplier of resins used in surface coating applications. Our coating products are used by customers in a variety of end-markets including architectural coatings, civil engineering, electronics, automotive and a wide variety of applications in the industrial and consumer markets. In 2005, sales of products used in coating applications contributed approximately $1.3 billion to our total pro forma net sales. Our key products serving coating applications include:

| • | Epoxy Coating Resins. In addition to the adhesive uses mentioned previously, epoxy resins are used for a variety of high-end coating applications which require the superior strength and durability of epoxy. Examples include protective coating for industrial and domestic flooring, pipe, marine and construction applications, powder coatings and automotive coatings. |

| • | Polyester Resins.We are a leading supplier of polyester coatings resins in North America with a market share of 10% and are also a major producer in Europe with a powder coatings market share of 10%. We |

3

Table of Contents

provide custom polyester resins, both liquid and powder, to customers for use in industrial coatings requiring specific properties such as gloss and color retention, resistance to corrosion and flexibility. Polyester coatings are typically used in transportation, automotive, machinery, appliances and metal office furniture. |

| • | Alkyd Resins.We share the leading position in alkyd resins in North America with a market share of 31% and are a major producer in Europe, specifically in Scandinavia and Italy. We provide alkyd resins to customers for use in the manufacture of professional grade paints and coatings. Our alkyd resins business shares an integrated production platform with our polyester resins business, which allows for flexible sourcing, plant balancing and economies of scale. |

| • | Acrylic Resins.We are a supplier of acrylic resins (solvent and water-based) in North America and Europe. Acrylic resins are used for interior trim paints and exterior applications where weathering protection, color and gloss retention are critical. In addition, we produce a wide range of specialty acrylic resins for marine and maintenance paints and automotive topcoats. We are also a low cost producer of acrylic monomer, the key raw material for our acrylic resins. This ability to produce key raw materials gives us a competitive cost advantage relative to our competitors and ensures adequacy of supply. |

| • | Ink Resins and Additives. We are the world’s largest producer of ink resins and associated products with a market share of 15%. Ink resins are used to apply ink to a variety of different substrates including paper, cardboard, metal foil and plastic. We are also a provider of formulated UV-cure coatings and inks. Our proprietary technology has enabled us to gain a leading position in the global fiber optic market. |

| • | Versatic Acids and Derivatives. We are the world’s largest producer of versatic acids and derivatives, with a market share of 76%. Versatic acids and derivatives are specialty monomers which provide significant performance advantages to finished coatings, including superior adhesion, flexibility, ease of application and other high performance characteristics. Applications for versatic acids and derivatives include decorative, automotive and protective coatings as well as other uses, such as pharmaceuticals and personal care products. |

Competitive Strengths

We are one of the leading specialty chemical companies in the world based on the following competitive strengths:

World’s Largest Thermoset Resins Producer. We are the world’s largest producer of thermoset resins with leading positions across various end-markets and geographies. Our global scale and breadth of product line provide us with significant advantages over many of our competitors. We are first or second in market position by volume in our key product areas, which collectively represent more than 75% of our pro forma 2005 net sales.

Unique Selling Proposition. The majority of our customers require solutions that are tailored to their individual production needs and require a high degree of technical service and customized product formulations. Our diverse thermoset product offering allows us to leverage related technologies across geographies, customers and end-markets in order to provide a broad range of product and technical service solutions. As a result, we have cultivated stable, longstanding customer relationships.

Global Infrastructure. We believe our global scope and our ability to internally produce key raw materials give us an advantage compared with many of our smaller competitors. We believe that we are well positioned in higher growth regions and will continue to grow internationally.

Low Cost Position. Our low cost manufacturing position is the result of our 94 production sites strategically located throughout the world and our selectively integrated supply position in critical intermediate materials. Our ability to internally produce key raw materials provides us a significant cost advantage over our competitors. Furthermore, our large market position and scale in each of our key product markets provides us with significant purchasing and manufacturing efficiencies.

4

Table of Contents

Well Positioned in Diverse End-Markets and Higher Growth Sectors. We have a diversified revenue and customer base in a variety of end-markets and geographies. Our products are used in a broad range of applications and are sold into stable markets, as well as higher growth markets.

Strong Free Cash Flow.We expect to generate strong free cash flow (cash flow from operating activities less anticipated capital expenditures) due to our size and position within the thermoset resins industry, and the industry leading cost structure we have in place. Additionally, we expect to realize significant synergies from the Hexion Formation which should further improve free cash flow.

Strong Management Team. We believe that we have a world-class management team led by Craig O. Morrison, our President and Chief Executive Officer, and William H. Carter, our Chief Financial Officer. Marvin O. Schlanger, former Chief Executive Officer of Arco Chemical and Resolution Performance, is our Vice Chairman. Our management team has demonstrated expertise in growing our businesses organically, integrating acquisitions and executing on significant cost cutting programs.

Strategy

We are focused on augmenting our growth, as well as increasing shareholder value, return on investment, cash flows and profitability. We believe we can achieve these related goals through the following strategies:

Utilize Our Integrated Platform Across Product Offerings.As the world’s largest producer of thermoset resins, we have an opportunity to provide our customers with a broad range of resins products on a global basis. We believe this provides us the opportunity to become a global, comprehensive solutions provider to our customers rather than simply offering a particular product, selling in a single geography or competing on price.

Develop and Market New Products. We will continue to expand our product offerings through internal innovation, joint research and development initiatives with our customers and research partnership formations. In 2005, on a pro forma basis, we incurred approximately $67 million in research and development expenses, which represented approximately 1.4% of our pro forma net sales during that period.

Expand Our Global Reach In Faster Growing Regions. We are focused on growing our business in the Asia-Pacific, Eastern Europe and Latin American markets, where the usage of our products is increasing. Furthermore, by combining sales and distribution infrastructures, we expect to accelerate the penetration of our high-end, value-added products into new markets.

Increase Margins Through Focus on Operational Excellence. We believe that through the combination of four stand-alone global resin companies, there will be opportunities to extract substantial cost savings in the near future. Management is currently targeting $250 million in synergies from the Hexion Formation, of which $125 million of net cost savings have been specifically identified. Management has developed detailed implementation plans to achieve the $125 million of cost savings. We achieved cost savings of $20 million in 2005 and $11 million in the first quarter of 2006. We expect that approximately 60% of the $125 million near term cost savings will be achieved by the end of 2006 with the remainder expected to be achieved in the following year. Through March 31, 2006, we have incurred one-time costs of approximately $13 million in connection with implementing these synergies and we expect to incur additional one-time costs of $62 million through 2007. Management has specifically identified a number of areas for savings and is actively pursuing key components of this strategy.

Pursue Targeted Add-On Acquisitions and Joint Ventures. The global thermoset resin industry is highly fragmented and is comprised of numerous small and mid-sized specialty companies focusing on niche markets, as well as small non-core divisions of large chemical conglomerates. As the largest company focused primarily on the thermoset resins space, we have a significant advantage in pursuing add-on acquisitions and joint ventures in areas that allow us to build upon our core strengths, expand our product, technology and geographic portfolio, and better serve our customers. We believe we can consummate a number of these acquisitions at relatively low valuations due to the scalability of our existing global operations.

5

Table of Contents

Risk Factors

Despite our competitive strengths discussed elsewhere in this prospectus, investing in our stock involves substantial risk. In addition, our ability to execute our strategy is subject to certain risks. The risks described under the heading “Risk Factors” immediately following this summary may cause us not to realize the full benefits of our strengths or may cause us to be unable to successfully execute all or part of our strategy. Before you invest in our stock, you should carefully consider all the information in this prospectus, including matters set forth under the heading “Risk Factors.”

The Prior Transactions, the Hexion Formation and the Hexion Refinancings

The Hexion Refinancings. In May 2006, we amended and restated our senior secured credit facilities. We refer to these senior secured credit facilities as the “new senior secured credit facilities” in this prospectus. Our new senior secured credit facilities are described under the heading “Description of Certain Indebtedness—First-Priority Lien Obligations—New Senior Secured Credit Facilities.” Upon entering into these new senior secured credit facilities, we repaid all amounts outstanding under our May 2005 term loan and synthetic letter of credit facilities. In addition, we made tender offers to repurchase all of our outstanding 8% Senior Secured Notes, 9½% Senior Second Secured Notes and 13½% Senior Subordinated Notes. On May 5, 2006, we accepted tenders from holders of 100% of the outstanding principal amount of the 8% Senior Secured Notes, 99.9% of the outstanding principal amount of the 9 1/2% Senior Second Secured Notes and 88.7% of the outstanding principal amount of the 13 1/2% Senior Subordinated Notes. In the event that not all of the 9 1/2% Senior Second Secured Notes or 13 1/2% Senior Subordinated Notes are repurchased pursuant to the tender offers, we expect to borrow under our new senior secured credit facilities to redeem any outstanding 9 1/2% Senior Second Secured Notes and 13 1/2% Senior Subordinated Notes shortly after the completion of the tender offers. We do not expect to incur any material additional costs in connection with any such redemptions. In connection with the tender offers, we received the required consents with respect to each series of notes to eliminate substantially all of the restrictive covenants and certain events of default included in the indentures under which such notes were issued. This prospectus is not an offer to purchase, a solicitation of an offer to purchase or a solicitation of consent with respect to our 8% Senior Notes, 9 1/2% Senior Second Secured Notes, and 13 1/2% Senior Subordinated Notes. The tender offers and consent solicitations have been made solely by the Offer to Purchase and Consent Solicitation Statement. On May 10, 2006, we entered into a $1 billion interest rate swap agreement. The swap is a three-year agreement designed to offset cash flow variability associated with interest rate fluctuations on our variable rate debt. The initial notional amount of the swap is $1 billion, which amortizes on a quarterly basis based on expected payments on our term loan in order to maintain a fixed to variable debt ratio of approximately 70% fixed to 30% variable. On May 12, 2006, we redeemed all of our outstanding Series A Preferred Stock with the proceeds of borrowings under our new senior secured credit facilities. We refer to the swap, the refinancing and the repurchases and redemptions of notes and preferred stock as the “Hexion Refinancings.”

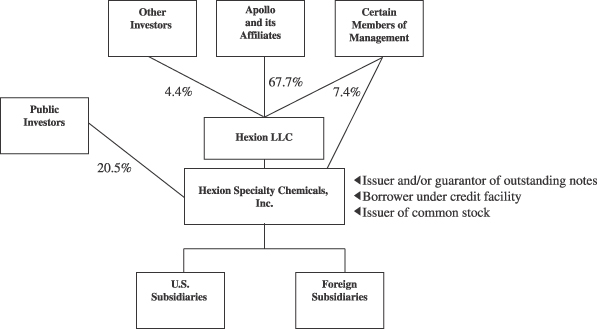

The Combinations. On May 31, 2005, Resolution Performance and Resolution Specialty were combined with and into Borden Chemical (the “Combinations”), all of which were controlled by Apollo Management, L.P. and its affiliates (“Apollo”). As of December 31, 2004, Apollo and its affiliated funds held approximately 98%, 72% and 95% of the then outstanding capital stock of Borden Chemical, Resolution Performance and Resolution Specialty, respectively. In connection with the Combinations, the minority interests in Resolution Performance and Resolution Specialty were eliminated. Upon the consummation of the Combinations, Borden Chemical changed its name to Hexion Specialty Chemicals, Inc. and BHI Acquisition LLC, Borden Chemical’s parent, changed its name to Hexion LLC. Immediately following completion of this offering, Apollo, through Hexion LLC, will hold approximately 70.9% of the outstanding common stock of Hexion.

The Borden Transaction. On August 12, 2004, an affiliate of Apollo acquired all of the outstanding capital stock of Borden Chemical (the “Borden Acquisition”). The Borden Acquisition, the related offering of second-priority senior secured floating rate notes (the “Original Floating Rate Notes”) and 9% second-priority senior secured notes (the “Fixed Rate Notes”) and the related transactions are collectively referred to in this prospectus as the “Borden Transaction.”

6

Table of Contents

The Resolution Performance Transaction. On November 14, 2000, an affiliate of Apollo acquired control of Resolution Performance in a recapitalization transaction (the “Resolution Performance Transaction”). Prior to the recapitalization, Resolution Performance was a wholly owned subsidiary of the Royal Dutch/Shell Group of Companies (“Shell”).

The Resolution Specialty Transaction. On August 2, 2004, Resolution Specialty, an affiliate of Apollo, acquired the resins, inks and monomers division (the “Resolution Specialty Acquisition”) of Eastman Chemical Company (“Eastman”). The Resolution Specialty Acquisition and the related transactions are collectively referred to in this prospectus as the “Resolution Specialty Transaction.”

The Bakelite Transaction.On April 29, 2005, a subsidiary of Borden Chemical acquired Bakelite (the “Bakelite Acquisition”). Upon the consummation of the Bakelite Acquisition, Bakelite became an indirect, wholly-owned subsidiary of Hexion Specialty Chemicals Canada, Inc. (“Hexion Canada”). The Bakelite Acquisition was financed through a combination of available cash and borrowings under a bridge loan facility, which was refinanced with the proceeds of our second-priority senior secured floating rate notes issued on May 20, 2005 (the “New Floating Rate Notes”) and borrowings under our May 2005 senior secured credit facilities (collectively, the “Bakelite Financing”). The Bakelite Acquisition, the repayment or assumption of certain of Bakelite’s debt in connection therewith and the Bakelite Financing are collectively referred to in this prospectus as the “Bakelite Transaction.”

We refer to the Borden Transaction, the Resolution Performance Transaction and the Resolution Specialty Transaction collectively as the “Prior Transactions.” We refer to the borrowings under our May 2005 senior secured credit facilities, the issuance of our Series A Preferred Stock and the application of the net proceeds therefrom to repay then-existing debt and pay a dividend on our common stock in May 2005 as described elsewhere in this prospectus, collectively, as the “Hexion Financings.” We refer to the Original Floating Rate Notes, the Fixed Rate Notes and the New Floating Rate Notes as the “Second-Priority Senior Secured Notes.” We refer to the offering of our common stock pursuant to this prospectus as “the offering.” We refer to the Combinations, the Hexion Financings and the Bakelite Transaction as the “Hexion Formation.” We refer to the Prior Transactions, the Hexion Formation, the Hexion Refinancings and the offering, including the application of the net proceeds to the Company therefrom, as the “Transactions.”

7

Table of Contents

Ownership Structure

The chart below illustrates our beneficial ownership structure after giving effect to the Transactions. Our ownership is presented on a fully-diluted basis.

We are a New Jersey corporation, with predecessors dating back to 1899. Our principal executive offices are located at 180 East Broad Street, Columbus, Ohio 43215. Our telephone number is (614) 225-4000. We maintain a website atwww.hexion.com where general information about our business is available.The information contained on our website is not a part of this prospectus.

8

Table of Contents

Recent Acquisitions and Divestiture

Acquisition of the Global Ink and Adhesive Resins Business of Akzo Nobel

On November 25, 2005, we agreed to acquire the global ink and adhesive resins business of Akzo Nobel (the “Akzo Acquisition”). The business produces resins used to manufacture inks for commercial printing and packaging, digital inks for laser and photocopying printing, and pressure sensitive adhesives used in tape and labeling applications. The business generated 2005 sales of approximately $215 million, and includes 10 manufacturing facilities in Europe, North America, Argentina, Asia and New Zealand. Closing should occur upon the successful completion of normal governmental reviews and consultations with employee workers’ councils, which we expect to occur during the second quarter of 2006. The acquisition will be funded through a combination of available cash and existing credit lines. We cannot assure you that the Akzo Acquisition will be completed on the timeframe anticipated or at all.

Acquisition of Decorative Coatings and Adhesives Business Unit of The Rhodia Group

On January 31, 2006, we acquired the decorative coatings and adhesives business unit of The Rhodia Group (the “Rhodia Acquisition”). The business generated 2005 sales of approximately $200 million, with 8 manufacturing facilities in Europe, Australia and Thailand. The acquisition was funded through a combination of available cash and existing credit lines.

Acquisition of Global Wax Compounds Business of Rohm and Haas

On March 1, 2006, we acquired the global wax compounds business of Rohm and Haas (the “Rohm and Haas Acquisition”). The business generated 2005 sales of approximately $10 million. The purchase included Rohm and Haas’ wax compounds technology and product lines, manufacturing equipment and other business assets. The acquisition was funded through available cash.

Divestiture of Alba Adesivos

On March 31, 2006, we sold Alba, Adesivos Industria e Comercio Ltda. (“Alba Adesivos”), a consumer adhesives company based in Boituva, Brazil, to the Henkel Group (the “Brazilian Consumer Divestiture”). Alba Adesivos is a producer of branded consumer and professional grade adhesives. The company generated 2005 sales of $38 million and has approximately 140 employees. The purchase price was paid in cash.

We expect the aggregate purchase price for these three acquisitions, net of proceeds from the divestiture, to be approximately $117 million.

9

Table of Contents

The Offering

Common stock offered by us | 3,703,704 shares |

Common stock offered by the selling shareholder | 14,814,815 shares |

Common stock to be outstanding after this offering | 86,260,551 shares(a) |

Use of Proceeds | We estimate that we will receive proceeds from our offering of our common stock, after deducting underwriting discounts and other expenses, of approximately $86 million, assuming the shares are offered at $27.00 per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus. We intend to use all of the net proceeds from the sale of the shares of our common stock being sold by us together with available cash to repay $100 million of our term loan under our new senior secured credit facilities. For sensitivity analysis as to the offering price and other information, see “Use of Proceeds” and “Dividend Policy.” |

We will not receive any proceeds from the sale of our common stock by the selling shareholder, including if the underwriters exercise their option to purchase additional shares. In the aggregate, the selling shareholder will receive approximately $380 million of the net proceeds of this offering, or approximately $451 million if the underwriters’ option to purchase additional shares is exercised in full, assuming the shares are offered at $27.00 per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus. See “Use of Proceeds” and “Underwriting.” |

Dividend Policy | We do not currently intend to pay any cash dividends on our common stock. See “Dividend Policy” and “Description of Capital Stock—Common Stock.” |

Listing | Our common stock has been approved for listing on the New York Stock Exchange under the symbol “HXN.” |

All information in this prospectus, unless otherwise indicated or the context otherwise requires:

| • | gives effect to a 0.853-for-1 reverse stock split of our common stock; and |

| • | does not give effect to the issuance of the following: |

(1) 4,105,148 shares of common stock issuable upon the exercise of options outstanding as of March 31, 2006, at a weighted average exercise price of approximately $6.39 per share (split adjusted and giving effect to the assumption of the applicable option plans from Hexion LLC by the Company prior to the consummation of the offering); or

(2) 14,000,000 shares of common stock which may be issued upon the exercise of options reserved for future grant.

| (a) | Includes 954,378 shares related to deferred compensation units. |

10

Table of Contents

Summary Historical and Pro Forma Financial and Other Data

The combination of Borden Chemical, Resolution Performance and Resolution Specialty has been treated, for accounting purposes, as a combination of entities under common control due to Apollo’s controlling interest in each of the companies. The audited consolidated financial statements presented herein reflect the results of operations of each company from the date such company was acquired by Apollo.

The following table summarizes certain historical and pro forma financial and other data for Hexion. The summary historical and pro forma financial and other data for Hexion as of December 31, 2004 and 2005, and for the years ended December 31, 2003, 2004 and 2005 have been derived from the audited consolidated financial statements of Hexion, included elsewhere in this prospectus. The summary historical and pro forma financial and other data for Hexion as of and for the three months ended March 31, 2005 and 2006 have been derived from the unaudited consolidated financial statements of Hexion, included elsewhere in this prospectus, and include all adjustments that management considers necessary for a fair presentation of our financial position and results of operations as of the date and for the period indicated. Results for the three months ended March 31, 2006 are not necessarily indicative of the results that may be expected for the entire year. The summary historical financial data of Hexion for the years ended December 31, 2003, 2004 and 2005 and the three months ended March 31, 2005 include:

| • | the results of operations of Resolution Performance for the years ended December 31, 2003, 2004 and 2005 and the three months ended March 31, 2005, which reflect purchase accounting adjustments from the date of acquisition of Resolution Performance by Apollo on November 14, 2000; |

| • | the results of operations of Borden Chemical for the period from August 12, 2004 to December 31, 2004, the year ended December 31, 2005 and the three months ended March 31, 2005, on a historical basis (because Borden Chemical is a public reporting registrant as a result of public debt that was outstanding prior to the Borden Transaction and which debt remains outstanding, Borden Chemical has elected to present its financial statements from the date of its acquisition by Apollo on the historical basis of accounting permitted under the SEC’s public debt exemptions); |

| • | the results of operations of Resolution Specialty for the period from August 2, 2004 to December 31, 2004, the year ended December 31, 2005 and the three months ended March 31, 2005, which reflect purchase accounting adjustments from the date of acquisition of Resolution Specialty by Apollo on August 2, 2004; and |

| • | the results of operations of Bakelite for the period from April 30, 2005 to December 31, 2005, which reflect purchase accounting adjustments from the date of the acquisition of Bakelite on April 29, 2005. |

The financial data for Hexion for the three months ended March 31, 2006 includes the results of the Rhodia Acquisition and Rohm and Haas Acquisition since January 31, 2006 and March 1, 2006, the respective dates of acquisition.

Accordingly, the results of operations of Hexion for periods prior to the Borden Acquisition, the Resolution Specialty Acquisition and the Bakelite Acquisition are not comparable to results for subsequent periods.

The summary unaudited pro forma financial data of Hexion gives effect, in the manner described under “Unaudited Pro Forma Financial Information,” to the Hexion Formation, the Hexion Refinancings and the offering, including the application of the net proceeds to the Company therefrom. Our unaudited pro forma balance sheet as of March 31, 2006, which already reflects the Prior Transactions, the Hexion Formation, the Rhodia Acquisition, the Rohm and Haas Acquisition and the Brazilian Consumer Divestiture, gives pro forma effect to the Hexion Refinancings and the offering, including the application of the net proceeds to the Company therefrom, as if they had occurred on such date but does not give effect to the Akzo Acquisition which is not considered significant under the provisions of Article 11-01(b) of Regulation S-X.Our unaudited pro forma statements of operations for the year ended December 31, 2005 and the three months ended March 31, 2005 give pro forma effect to the Hexion Formation, the Hexion Refinancings and the offering and our unaudited pro forma statement of operations for the

11

Table of Contents

three months ended March 31, 2006 gives pro forma effect to the Hexion Refinancings and the offering, including the application of the net proceeds to the Company therefrom, as if they had each occurred on January 1, 2005, as described under “Unaudited Pro Forma Financial Information”, but does not give effect to the Akzo Acquisition, the Rhodia Acquisition, the Rohm and Haas Acquisition and the Brazilian Consumer Divestiture which are not considered significant under the provisions of Article 11-01(b) of Regulation S-X. We have included pro forma data related to EBITDA and transaction costs, impairments and unusual items included in EBITDA for the last twelve months ended March 31, 2006 (the “LTM Period”) as we are required to measure compliance with the financial covenants in certain of our indentures based on Adjusted EBITDA for the most recent four quarter period.

The pro forma adjustments relating to the Bakelite Transaction and the minority interest acquisitions of Resolution Performance and Resolution Specialty as part of the Combinations are based on preliminary estimates of the fair value of the consideration provided, estimates of the fair values of assets acquired and liabilities assumed and available information and assumptions. The final determination of fair value could result in changes to the pro forma adjustments and the pro forma data included herein.

12

Table of Contents

The unaudited pro forma financial data for the year ended December 31, 2005, for the three months ended March 31, 2005 and 2006 and as of March 31, 2006 and for the LTM Period is presented for informational purposes only, and does not purport to represent what our results of operations would actually have been if the transactions had occurred on the dates indicated, nor does it purport to project our results of operations or financial condition that we may achieve in the future.

You should read this summary historical and pro forma financial and other data in conjunction with “Selected Historical Financial and Other Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Unaudited Pro Forma Financial Information,” together with all of the financial statements and related notes included elsewhere in this prospectus.

| Historical | Pro Forma | |||||||||||||||||||||||||||||||

Year Ended December 31, | Three Months Ended March 31, | Year Ended 2005 | Three Months March 31, | |||||||||||||||||||||||||||||

| 2003 | 2004 | 2005 | 2005 | 2006 | 2005 | 2006 | ||||||||||||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||||||||||||||

Statement of Operations | ||||||||||||||||||||||||||||||||

Net sales(1) | $ | 782 | $ | 2,019 | $ | 4,470 | $ | 1,012 | $ | 1,245 | $ | 4,717 | $ | 1,194 | $ | 1,245 | ||||||||||||||||

Cost of sales | 714 | 1,785 | 3,808 | 863 | 1,060 | 4,006 | 1,017 | 1,060 | ||||||||||||||||||||||||

Gross profit | 68 | 234 | 662 | 149 | 185 | 711 | 177 | 185 | ||||||||||||||||||||||||

Selling, general & administrative expense | 81 | 163 | 400 | 86 | 101 | 431 | 108 | 101 | ||||||||||||||||||||||||

Transaction costs | — | 56 | 44 | 7 | 4 | 44 | 7 | 4 | ||||||||||||||||||||||||

Other operating (income) expense(2) | 10 | 6 | 10 | (3 | ) | (30 | ) | 7 | (4 | ) | (31 | ) | ||||||||||||||||||||

Operating income (loss) | (23 | ) | 9 | 208 | 59 | 110 | 229 | 66 | 111 | |||||||||||||||||||||||

Interest expense, net | 77 | 117 | 204 | 45 | 54 | 219 | 55 | 55 | ||||||||||||||||||||||||

Write-off of deferred financing fees | — | — | 17 | — | — | — | — | — | ||||||||||||||||||||||||

Other non-operating expense, net | — | 5 | 16 | 9 | 1 | 16 | 9 | 1 | ||||||||||||||||||||||||

Income (loss) from continuing operations before income tax and minority interest | (100 | ) | (113 | ) | (29 | ) | 5 | 55 | (6 | ) | 2 | 55 | ||||||||||||||||||||

Income tax expense (benefit) | (37 | ) | — | 48 | 13 | 19 | 61 | 14 | 19 | |||||||||||||||||||||||

Income (loss) from continuing operations before minority interest | (63 | ) | (113 | ) | (77 | ) | (8 | ) | 36 | (67 | ) | (12 | ) | 36 | ||||||||||||||||||

Earnings for unconsolidated entities, net of taxes | — | — | 2 | — | 1 | 2 | — | 1 | ||||||||||||||||||||||||

Minority interest in net (income) loss of consolidated subsidiaries | 13 | 8 | (3 | ) | (2 | ) | (2 | ) | (4 | ) | (1 | ) | (2 | ) | ||||||||||||||||||

Income (loss) from continuing operations | (50 | ) | (105 | ) | (78 | ) | (10 | ) | 35 | (69 | ) | (13 | ) | 35 | ||||||||||||||||||

Loss from discontinued operations | — | — | 9 | — | — | — | — | — | ||||||||||||||||||||||||

Net income (loss) | (50 | ) | (105 | ) | (87 | ) | (10 | ) | 35 | (69 | ) | (13 | ) | 35 | ||||||||||||||||||

Redeemable preferred stock accretion | — | — | 30 | — | 13 | — | — | — | ||||||||||||||||||||||||

Net income (loss) available to common shareholders | $ | (50 | ) | $ | (105 | ) | $ | (117 | ) | $ | (10 | ) | $ | 22 | $ | (69 | ) | $ | (13 | ) | $ | 35 | ||||||||||

Cash Flow Data | ||||||||||||||||||||||||||||||||

Cash flows (used in) from operating activities | $ | (43 | ) | $ | (32 | ) | $ | 171 | $ | 24 | $ | 44 | — | — | — | |||||||||||||||||

Cash flows (used in) from investing activities | 7 | (20 | ) | (354 | ) | (20 | ) | (42 | ) | — | — | — | ||||||||||||||||||||

Cash flows from (used in) financing activities | 80 | 148 | 219 | 3 | (16 | ) | — | — | — | |||||||||||||||||||||||

Depreciation and amortization(3) | 58 | 86 | 148 | 36 | 38 | $ | 158 | $ | 42 | $ | 38 | |||||||||||||||||||||

Capital expenditures | 18 | 57 | 105 | 13 | 27 | 111 | 17 | 27 | ||||||||||||||||||||||||

13

Table of Contents

| Historical | Pro Forma | ||||||||||||||||||||||||||||||

Year Ended December 31, | Three Months Ended March 31, | Year Ended December 31, 2005 | Three Months Ended March 31, | LTM Period | |||||||||||||||||||||||||||

| 2003 | 2004 | 2005 | 2005 | 2006 | 2005 | 2006 | |||||||||||||||||||||||||

| (dollars in millions) | |||||||||||||||||||||||||||||||

Other Financial Data | |||||||||||||||||||||||||||||||

EBITDA (4) | — | — | — | — | — | $ | 369 | $ | 98 | $ | 147 | $ | 418 | ||||||||||||||||||

Transaction costs and non-cash charges included in EBITDA (5) | — | — | — | — | — | 76 | 7 | 10 | 79 | ||||||||||||||||||||||

Unusual items included in EBITDA (6) | — | — | — | — | — | 36 | 16 | (25 | ) | (5 | ) | ||||||||||||||||||||

Balance Sheet Data (at end of period) | |||||||||||||||||||||||||||||||

Cash and equivalents | $ | 49 | $ | 152 | $ | 183 | — | $ | 168 | — | — | $ | 141 | — | |||||||||||||||||

Working capital (7) | 177 | 433 | 427 | — | 423 | — | — | 379 | — | ||||||||||||||||||||||

Total assets | 1,191 | 2,696 | 3,209 | — | 3,307 | — | — | 3,263 | — | ||||||||||||||||||||||

Total debt | 683 | 1,850 | 2,354 | — | 2,340 | — | — | 2,690 | — | ||||||||||||||||||||||

Total liabilities and minority interest | 1,039 | 3,005 | 3,769 | — | 3,819 | — | — | 4,163 | — | ||||||||||||||||||||||

Redeemable preferred stock | — | — | 364 | — | 377 | — | — | — | — | ||||||||||||||||||||||

Total common stock and other shareholder’s equity (deficit) | 152 | (309 | ) | (924 | ) | — | (889 | ) | — | — | (900 | ) | — | ||||||||||||||||||

| (1) | Net sales included in the consolidated statement of operations for the year ended December 31, 2004 is comprised of: |

| Year Ended December 31, 2004 | ||||

| (dollars in millions) | ||||

Resolution Performance—For the year ended December 31, 2004 | $ | 996 | ||

Borden—For the period from August 12, 2004 to December 31, 2004 | 702 | |||

Resolution Specialty—For the period from August 2, 2004 to December 31, 2004 | 325 | |||

Eliminations | (4 | ) | ||

Total consolidated net sales for the year ended December 31, 2004 | $ | 2,019 | ||

| (2) | Other operating (income) expense for the three months ended March 31, 2006 (historical and pro forma) includes net gain of $37 recognized primarily on the Brazilian Consumer Divestiture. |

| (3) | Depreciation and amortization included in the pro forma statement of operations for the year ended December 31, 2005 and for the three months ended March 31, 2005 and 2006 is comprised of: |

| Year Ended December 31, 2005 | Three Months Ended March 31, | ||||||||||

| 2005 | 2006 | ||||||||||

| (dollars in millions) | |||||||||||

Hexion—For the year ended December 31, 2005 and for the three months ended March 31, 2005 and 2006 | $ | 148 | $ | 36 | $ | 38 | |||||

Bakelite—For the period from January 1, 2005 to April 29, 2005 and for the three months ended March 31, 2005 and 2006 | 11 | 7 | — | ||||||||

Total pro forma adjustment | (1 | ) | (1 | ) | — | ||||||

Total pro forma depreciation and amortization expense for the year ended December 31, 2005 and for the three months ended March 31, 2005 and 2006 | $ | 158 | $ | 42 | $ | 38 | |||||

| (4) | EBITDA is defined as net income (loss) before interest, taxes, depreciation and amortization and is used by management as a performance measure for certain performance-based cash bonus plans and measuring triggering events of certain performance-based stock options. We have presented EBITDA on a pro forma basis since management plans on using EBITDA as a benchmark for developing its ongoing performance measures for its cash bonus plans and certain performance-based stock option plans. We believe that pro forma EBITDA is more representative of our performance since it gives the full year effect to the Bakelite Acquisition which was completed in April 2005 whereas historical EBITDA gives effect to our acquisitions only as of the date we acquired such entity. We also believe that EBITDA is useful to investors because it is |

14

Table of Contents

frequently used by securities analysts, investors and other interested parties to evaluate companies in our industry. EBITDA is not a recognized term under GAAP, should not be viewed in isolation and does not purport to be an alternative to net income (loss) as an indicator of operating performance or cash flows from operating activities as a measure of liquidity. There are material limitations associated with making the adjustments to our earnings to calculate EBITDA and using this non-GAAP financial measure as compared to the most directly comparable U.S. GAAP financial measures. For instance, EBITDA does not include: |

| • | interest expense, and because we have borrowed money in order to finance our operations, interest expense is a necessary element of our costs and ability to generate revenue; |

| • | depreciation and amortization expense, and because we use capital assets, depreciation and amortization expense is a necessary element of our costs and ability to generate revenue; and |

| • | tax expense, and because the payment of taxes is part of our operations, tax expense is a necessary element of our costs and ability to operate. |

Additionally, EBITDA is not intended to be a measure of free cash flow for management’s discretionary use, as it does not consider certain cash requirements such as capital expenditures, contractual commitments, interest payments, tax payments and debt service requirements. Because not all companies use identical calculations, this presentation of EBITDA may not be comparable to other similarly titled measures for other companies. Also the amounts shown for EBITDA as presented herein differ from the amounts calculated under the definition of Adjusted EBITDA used in our debt instruments, which further adjust for certain cash and non-cash charges and is used to determine compliance with financial covenants and our ability to engage in certain activities such as incurring additional debt and making acquisitions.

The following table is a reconciliation of pro forma net income (loss) to pro forma EBITDA for Hexion:

| Pro Forma | |||||||||||||||

Year Ended December 31, 2005 | Three Months Ended March 31, | LTM | |||||||||||||

| 2005 | 2006 | ||||||||||||||

| (dollars in millions) | |||||||||||||||

Pro forma net income (loss) | $ | (69 | ) | $ | (13 | ) | $ | 35 | $ | (21 | ) | ||||

Pro forma interest expense, net(a) | 219 | 55 | 55 | 219 | |||||||||||

Pro forma income tax expense | 61 | 14 | 19 | 66 | |||||||||||

Pro forma depreciation and amortization | 158 | 42 | 38 | 154 | |||||||||||

Pro forma EBITDA | $ | 369 | $ | 98 | $ | 147 | $ | 418 | |||||||

| (a) | Includes $7 of amortization of deferred financing fees for the year ended December 31, 2005, and $2 for the three months ended March 31, 2005 and 2006. |

| (5) | Transaction costs and non-cash charges for Hexion are further detailed on the following table: |

| Pro Forma | ||||||||||||

Year Ended December 31, 2005 | Three Months Ended March 31, | LTM | ||||||||||

| 2005 | 2006 | |||||||||||

| (dollars in millions) | ||||||||||||

Transaction costs (a) | $ | 44 | $ | 7 | $ | 4 | $ | 41 | ||||

Non-cash charges (b) | 32 | — | 6 | 38 | ||||||||

| $ | 76 | $ | 7 | $ | 10 | $ | 79 | |||||

| (a) | Represents merger costs principally related to the Hexion Formation and expenses related to terminated acquisition activities. |

| (b) | Represents impairments of fixed assets of $9 and $4, non-cash stock based compensation of $13 and $2 and unrealized foreign currency exchange losses of $10 and $0 on debt instruments denominated in currencies other than the functional currency of the holder, for the year ended December 31, 2005 and the three months ended March 31, 2006, respectively. |

15

Table of Contents

| (6) | Unusual items that do not relate to the core operations of Hexion are further detailed on the following table: |

| Pro Forma | ||||||||||||||

Year Ended December 31, 2005 | Three Months Ended March 31, | LTM | ||||||||||||

| 2005 | 2006 | |||||||||||||

| (dollars in millions) | ||||||||||||||

Business realignment expenses (a) | $ | 9 | $ | 1 | $ | 3 | $ | 11 | ||||||

Other expenses (b) | 27 | 15 | (28 | ) | (16 | ) | ||||||||

Unusual items | $ | 36 | $ | 16 | $ | (25 | ) | $ | (5 | ) | ||||

| (a) | Business realignment expenses for the year ended December 31, 2005 included in EBITDA for Hexion relate to the excess of historical costs over current business staffing levels and comprises employee related costs of $4 including (i) historical salaries and benefits of employees terminated in 2005 at Resolution Specialty and Borden Chemical and (ii) the excess cost of employee benefit programs prior to the revision of such plans in 2005. Business realignment expenses include plant closure and non-recurring severance and other one time benefits paid to employees of $5, $1, $3 and $11 for the year ended December 31, 2005, the three months ended March 31, 2005 and 2006 and the LTM period, respectively. |

| (b) | Amounts include the following: |

Year Ended December 31, 2005 | Three Months Ended March 31, | LTM | |||||||||||||

| 2005 | 2006 | ||||||||||||||

Non-recurring litigation expenses | $ | 10 | $ | 2 | $ | 1 | $ | 9 | |||||||

Foreign currency loss on an exchange rate hedge relating to the Bakelite Acquisition | 11 | 11 | — | — | |||||||||||

Integration costs, transition fees and other non-recurring expenses | 6 | 4 | 8 | 10 | |||||||||||

Gain on divestitures of businesses | — | (2 | ) | (37 | ) | (35 | ) | ||||||||

| $ | 27 | $ | 15 | $ | (28 | ) | $ | (16 | ) | ||||||

| (7) | Working capital is defined as current assets less current liabilities. |

Senior Secured Credit Facilities

In May 2006, we amended and restated our senior secured credit facilities. Our new senior secured credit facilities consist of a seven-year $1,625 term loan facility, a seven-year $50 synthetic letter of credit facility and a five-year $225 revolving credit facility, each subject to an earlier maturity date, under certain circumstances. Upon entering into these new senior secured credit facilities, we repaid all amounts outstanding under our May 2005 term loan and synthetic letter of credit facilities. In addition, we made tender offers to repurchase all of our 8% Senior Secured Notes, 9 1/2% Senior Second Secured Notes and 13 1/2% Senior Subordinated Notes. On May 5, 2006, we accepted tenders from holders of 100% of the outstanding principal amount of the 8% Senior Secured Notes, 99.9% of the outstanding principal amount of the 9 1/2% Senior Second Secured Notes and 88.7% of the outstanding principal amount of the 13 1/2% Senior Subordinated Notes. On May 12, 2006, we redeemed all of our outstanding Series A Preferred Stock with the proceeds of borrowings under our new senior secured credit facilities. As of March 31, 2006, after giving pro forma effect to the Hexion Refinancings and the offering, we would have had $2,690 principal amount of outstanding indebtedness, including amounts outstanding under the new senior secured credit facilities and $141 of cash. See “Description of Certain Indebtedness—First-Priority Lien Obligations—New Senior Secured Credit Facilities.”

On May 10, 2006, we entered into a $1 billion interest rate swap agreement. The swap is a three-year agreement designed to offset cash flow variability associated with interest rate fluctuations on our variable rate debt. The initial notional amount of the swap is $1 billion, which amortizes on a quarterly basis based on expected payments on our term loan in order to maintain a fixed to variable debt ratio of approximately 70% fixed to 30% variable.

16

Table of Contents

Covenant Compliance

Certain covenants contained in the credit agreement governing our new senior secured credit facilities and the indentures governing the Second-Priority Senior Secured Notes (i) require the maintenance of a senior secured debt to Adjusted EBITDA ratio and (ii) restrict our ability to take certain actions such as incurring additional debt or making certain acquisitions if we are unable to meet defined Adjusted EBITDA to Fixed Charges, senior secured debt to Adjusted EBITDA and consolidated debt to Adjusted EBITDA ratios. Upon completion of the Hexion Refinancings, the most restrictive of these indenture covenants, the covenants to incur additional indebtedness and the ability to make future acquisitions, will require an Adjusted EBITDA to Fixed Charges ratio (measured on a trailing four-quarter basis) of 2.0 to 1.0. Failure to comply with these covenants can result in limiting our long-term growth prospects by hindering our ability to incur future indebtedness or grow through acquisitions.

Fixed Charges are defined as interest expense excluding the amortization or write-off of deferred financing costs. Adjusted EBITDA is defined as EBITDA further adjusted to exclude certain non-cash, non-recurring and realized or expected future cost savings directly related to prior acquisitions and the Combinations. We believe that the inclusion of the supplemental adjustments applied in calculating Adjusted EBITDA is appropriate to provide additional information to investors to demonstrate compliance with our financial covenants and assess our ability to incur additional indebtedness in the future. Adjusted EBITDA and Fixed Charges are not defined terms under GAAP. Adjusted EBITDA should not be considered an alternative to operating income or net income as a measure of operating results or an alternative to cash flows as a measure of liquidity. Fixed Charges should not be considered an alternative to interest expense.

See “Description of Certain Indebtedness” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources” for further information on our indebtedness and covenants.

17

Table of Contents

| Pro Forma | |||||||

Year Ended December 31, 2005 | LTM | ||||||

| (dollars in millions) | |||||||

Pro Forma EBITDA(1) | $ | 369 | $ | 418 | |||

Transaction costs and non-cash charges(1) | 76 | 79 | |||||

Unusual items(1) | 36 | (5 | ) | ||||

Effect of acquisitions, net of divestiture(2) | 11 | 11 | |||||

In process synergies(3) | 105 | 94 | |||||

Pro Forma Adjusted EBITDA(4) | $ | 597 | $ | 597 | |||

Pro Forma Fixed Charges | $ | 200 | $ | 208 | |||

Ratio of Pro Forma Adjusted EBITDA to Fixed Charges | 2.99 | 2.87 | |||||

| (1) | See footnotes (4) - (6) on pages 14-16 for more information on EBITDA, transaction costs and non-cash charges and unusual items. |

| (2) | Amount represents the incremental EBITDA impact for the Rhodia Acquisition, the Rohm and Haas Acquisition less the Brazilian Consumer Divestiture as if they had taken place at the beginning of the year. These acquisitions and the divestiture closed after December 31, 2005 and are included in our calculation of pro forma Adjusted EBITDA as permitted by our indenture covenants. |

| (3) | Represents $125 in estimated net cost savings specifically identified in connection with the Hexion Formation. We achieved cost savings of $20 in 2005 and $11 million in the first quarter of 2006. We expect that approximately 60% of the $125 near term cost savings will be achieved by the end of 2006 with the remainder expected to be achieved in the following year. Through March 31, 2006, we have incurred one-time costs of approximately $13 in connection with implementing these synergies and we expect to incur additional one-time costs of $62 through 2007. These estimated synergies include cost savings from rationalization of manufacturing facilities, removal of duplicative corporate and administrative functions, alignment of benefit plans and raw material purchasing initiatives. The estimated in process synergies by category are as follows: |

| Year Ended December 31, 2005 | LTM Period | |||||

Rationalization of manufacturing facilities | $ | 43 | $ | 41 | ||

Overhead synergies | 17 | 13 | ||||

Raw material savings | 45 | 40 | ||||

| $ | 105 | $ | 94 | |||

| (4) | We are required to have an Adjusted EBITDA to Fixed Charges ratio of greater than 2.0 to 1.0 to incur additional indebtedness under certain of our indentures. As of March 31, 2006, we are able to satisfy this covenant and incur additional indebtedness under our indentures. In addition, we expect to be able to satisfy our Fixed Charges ratio covenant upon the closing of the Akzo Acquisition, which we expect to occur in the second quarter of 2006. After giving effect to the Akzo Acquisition as if it had taken place at the beginning of 2005, our 2005 pro forma net loss would be $59, our 2005 pro forma Adjusted EBITDA would be $618, our Pro Forma Fixed Charges would be $213 and our ratio of Adjusted EBITDA to Fixed Charges would be 2.90. See “—Recent Acquisitions and Divestiture.” |

18

Table of Contents

An investment in our stock involves a high degree of risk. You should carefully consider the following information, together with other information in this prospectus, before buying shares of our stock. If any of the following risks or uncertainties occur, our business, financial condition and results of operations could be materially and adversely affected, the trading price of our stock could decline and you may lose all or a part of the money you paid to buy our stock.

Risks Relating to Our Business

Borden Chemical, Resolution Performance, Resolution Specialty and Bakelite have a limited history of working together as a single company. Should we fail to integrate the operations of Borden Chemical, Resolution Performance, Resolution Specialty and Bakelite and achieve cost savings and synergies, our results of operations and profitability would be negatively impacted.

We may not be successful integrating Borden Chemical, Resolution Performance, Resolution Specialty and Bakelite, and the combined company may not perform as we expect or achieve the net cost savings and synergies we anticipate. A significant element of our business strategy is the improvement of our operating efficiencies and a reduction of our operating costs. Management is currently targeting $250 million in synergies from the Hexion Formation, of which $125 million of net cost savings have been specifically identified. We achieved cost savings of $20 million in 2005 and $11 million in the first quarter of 2006. Through March 31, 2006, we have incurred one-time costs of approximately $13 in connection with implementing these synergies and we expect to incur additional one-time costs of $62 million through 2007. A variety of factors could cause us not to achieve the benefits of the cost savings plan, or could result in harm to our business. For example, certain of our European operations utilize IT systems with limited systems support. In the event we are not able to integrate these systems with our more advanced IT systems, our ability to efficiently operate in certain European countries could be diminished. In addition, the impact of Hurricanes Katrina and Rita on our business (negative cost impact of $27 million in the second half of 2005), along with future hurricanes and natural disasters, may affect our ability to achieve our cost savings plan in the near term. Additional factors include:

| • | delays in the anticipated timing of activities related to our cost savings plan; |

| • | higher than expected or unanticipated costs to implement the plan and to operate the business; |

| • | inadequate resources to implement the plan and to operate the business; |

| • | our inability to optimize manufacturing processes between the companies; |

| • | our inability to obtain lower raw material prices; |

| • | our inability to utilize new geographic distribution channels; |

| • | our inability to reduce corporate and administrative expenses; and |

| • | our inability to identify an additional $125 million of cost savings consistent with our synergy target. |

As a result, we may not achieve our expected cost savings in the time anticipated, or at all. In such case, our results of operations and profitability would be negatively impaired.

The Hexion Formation may prove disruptive and could result in the combined business failing to meet our expectations.

The continuing process of integrating the operations of Borden Chemical, Resolution Performance, Resolution Specialty and Bakelite may continue to require a disproportionate amount of resources and management attention. Our future operations and cash flows will depend largely upon our ability to operate Hexion efficiently, achieve the strategic operating objectives for our business and realize significant cost savings and synergies. Our management team may encounter unforeseen difficulties in managing the integration of our four businesses. In order to successfully combine and operate our businesses, our management team will need to

19

Table of Contents

continue to focus on realizing anticipated synergies and cost savings on a timely basis while maintaining the efficiency of our operations. Any substantial diversion of management attention or difficulties in operating the combined business could affect our sales and ability to achieve operational, financial and strategic objectives. For example, we expect to devote substantial management attention in order to implement financial reporting and other systems that will permit us to utilize a shared service business model (for certain processes) along with a single company wide management information and accounting system.

Our historical and pro forma financial information may not reflect what our actual results of operations and financial condition would have been had we been a combined company for the periods presented and thus these results may not be indicative of our future operating performance.

The historical financial information included in this prospectus is constructed from the separate financial statements of Resolution Performance, Borden Chemical and Resolution Specialty for periods prior to the consummation of the Hexion Formation. In addition, Bakelite has historically prepared its financial statements in accordance with German GAAP, which differs in certain respects from US GAAP. The Bakelite financial statement presentation included in this prospectus has been converted from the local GAAP of Bakelite and its subsidiaries to US GAAP. The pro forma financial information presented in this prospectus is based in part on certain assumptions regarding the Hexion Formation that we believe are reasonable. Our assumptions may prove to be inaccurate over time. Accordingly, the historical and pro forma financial information included in this prospectus may not reflect what our results of operations and financial condition would have been had we been a combined entity during the periods presented, or what our results of operations and financial condition will be in the future.

Our limited operating history and the challenge of integrating previously independent businesses make evaluating our business and our future financial prospects difficult. Our potential for future business success and operating profitability must be considered in light of the risks, uncertainties, expenses and difficulties typically encountered by recently organized or combined companies.